Embed Size (px)

Citation preview

Updates on the U.S. Economy, Investment Markets, and Financing StrategiesPrepared for:

March 6, 2014

Bill KielczewskiSVP - Managing DirectorInstitutional InvestmentsHuntington Capital [email protected]

Dan VandenBoschVP - DirectorPublic FinanceHuntington Capital [email protected]

Introduction and Overview

Global Economic Growth – slow recovery continues

3

The IMF projects World Output to grow at 3.7% for 2014, up from 3.0% in 2013.

“The basic reason behind the stronger recovery is that the brakes to the recovery are progressively being loosened,” said Olivier Blanchard, the IMF’s chief economist and director of its Research Department. “The drag from fiscal consolidation is diminishing. The financial system is slowly healing”.

World Output 2012 2013 2014 2015

Advanced Economies 1.4% 1.3% 2.2% 2.3%

• United States 2.8% 1.9% 2.8% 3.0%• Euro Zone -0.7% -0.4% 1.0% 1.4%• Japan 1.4% 1.7% 1.7% 1.0%• United Kingdom 0.3% 1.7% 2.4% 2.2%

Emerging and Developing Countries 4.9% 4.7% 5.1% 5.4%

• China 7.7% 7.7% 7.5% 7.3%• India 3.2% 4.4% 5.4% 6.4%• Latin America and Caribbean 3.0% 2.6% 3.0% 3.3%• Middle East and North Africa 4.1% 2.4% 3.3% 4.8%

Source: IMF website

4

All 4 of the worlds major central banks have implemented some form of quantitative easing in an attempt to increase their domestic growth rate.

Globally, interest rates have increased year over year. With growth projected at 3.7% and inflation rates near or below growth rates, how much higher can they go?

Global Economic Growth – Interest rates, FX, and global Q.E.

Country Credit Ratings

Debt % GDP

10 Year IR

10 Year IR change YoY

CPI YoY Unemployment Rate

Currency % change YoY (USD)

United States AA Aaa 70% 2.68% 0.73% 1.50% 6.60% 0.00%

United Kingdom AAA Aa1 89% 2.71% 0.62% 2.00% 7.10% 4.79%

Germany AAA Aaa 81% 1.66% 0.05% 1.30% 6.80% 1.59%

Italy BBB Baa2 127% 3.68% -0.86% 0.70% 12.70% 1.59%

Japan AA- Aa 219% 0.61% -0.15% 1.60% 3.70% 8.64%

Australia AAA Aaa 32% 4.14% 0.67% 2.70% 5.80% -12.78%

China AA- Aa3 32% 5.50% 0.88% 2.50% - -2.77%

India BBB- Baa 52% 7.50% 0.89% 9.13% - 15.00%

Brazil BBB Baa2 59% 4.75% 1.91% 5.59% - 20.90%

Source: IMF website

U.S. Economy – can we reach our projected 3.0% GDP growth

5

The Federal Reserve projects U.S. GDP growth of 3.0% for 2014. Federal Reserve Bank of Philadelphia President Charles Plosser, who votes on policy this year, said he

expects the economy to expand 3 percent in 2014 as the jobless rate falls to 6.2 percent by year-end, warranting a quicker tapering to bond purchases by the central bank.

Policy makers made the first two cuts to asset purchases in December and January, slowing to $65 billion a month from $85 billion.

“My preference is to scale back our purchase program at a faster pace to reflect the strengthening economy,” he said in a speech in Rochester, New York. “We must begin to back away from increasing the degree of policy accommodation in a manner commensurate with an improving economy,”

Source: Bloomberg

U.S. Economy – Is this the best we can do

6

Leading Economic Indicators in February was 0.3% versus survey expectations of 0.3%. The 40 year average for the U.S. is 0.1%. 1974-2014

Source: Bloomberg

U.S. Economy – Is this the best we can do

7

LEI Leading Credit Indicators Index shows credit expansion slowing. Average rate of the LCI index over past 25 years is 0.1%. The current reading is -1.90%. 1990-2014

Source: Bloomberg

U.S. Economy – Is this the best we can do

8

Durable Goods Orders are negative for both readings thus far in 2014. The current reading is -1.0%; last months number was revised down to -5.30%. Both are well below our 0.8% historical average. 1994-2014

Source: Bloomberg

U.S. Economy – Is this the best we can do

9

Construction Spending shows signs of stabilization. The bottom looks to have been formed in 2009 and we are trending back to our historical average. The current reading is 0.1% vs. historical average of 0.5%. 1993-2014

Source: Bloomberg

U.S. Economy – Home Prices Rebound

10

Home Prices in the U.S. have bounced back from their 15 year lows during the credit crisis. Will this trend continue without the Fed’s Q.E. support?S&P/Case-Shiller Home Price Index 1994-2014

Source: Bloomberg

U.S. Economy – How are Homes Sales

11

Home sales in the U.S. have slowed to -9.10%. Is there a correlation between buying a home and Government intervention in the market place? See below: Stimulus Package 1st Time Home Buyer Tax Credit / QE’s 1-3 / Fed TaperingU.S. Pending Home Sales Index YoY. 2002-2014

QE 1 starts in 11/08

1st Time Home Buyer Tax Credit added to Stimulus Package. 2/09

QE2QE 2 11/10

QE 3 9/12

QE2Fed announced “Tapering”

Source: Bloomberg

U.S. Economy – Is Corporate America hiring

12

U.S. job openings are picking up after the “great recession” and we have made our way back to 2004-2008 hiring levels. Are there enough “qualified” employees in our underemployment bucket to fill these new positions? 2000-2014

Source: Bloomberg

U.S. Economy – Unemployment Rate at 6.60%

13

We are very close to the Federal Reserves 6.50% desired rate which they state will allow them to slow their accommodative policy. Will they follow through with an end to QE and look to raise the overnight rate anytime soon, or, change their playbook with the recent weakening economic data?

Source: Bloomberg

U.S. Economy – Underemployment rate at 12.70%.

14

Do we have a “structural” employment problem within the U.S.?

We are well off the high rate of 17.20%, but, we are also 5 years out from the start of the “great recession”. Why can’t these folks in the underemployment index match up with all the new hiring opportunities presented in the JOLT Index?

38% of business owners surveyed in the January 2014 NFIB say they can not find “qualified workers” in the U.S. work force. 1994-2014

Source: Bloomberg

Investment Strategies

Investing in the Current Market

16

Quantitative Easing and Federal Funds Rate Discussion

The Federal Reserve has held the U.S. overnight rate near zero for the last 4.5 years. In their most recent meetings they started to “taper” Government Bond purchases by $10 Billion dollars. Most economists expect the Fed to continue with tapering and end their bond purchasing program (Q.E.) by the end of 2014.

The Federal Reserve has also said that they will hold the target interest rate for Federal Funds Rate at 0 to 0.25 at least as long as unemployment remains above 6.5% and inflation remains below their accepted level of 2.0 – 2.50%.

The Unemployment rate fell to 6.6%, but, the participation rate within that survey fell to 63%, near the lowest level since 1978. Inflation data for the U.S. in March showed the Fed’s favorite gauge, PCE core YOY, was at 1.10%.

The market has started to adjusted to “tapering”, economic data, and the Federal Reserves forward guidance on rates by extending the dates at which it anticipates the overnight rate to increase. Please see the Chicago Board of Trades Fed Funds Futures Contracts on the next slide for expected date and rate changes.

Investing in the Current MarketFed Funds Futures Contracts

17Source: Bloomberg

18

Bond Strategies; Portfolio Ladders and Barbells

Ladder Strategy / Asset-Liability MatchStaggers maturities of bonds in a portfolio and sets a schedule for reinvestment of proceeds

Tota

l Por

tfol

io

Benefits:• Periodic maturities allow you to control liquidity based

upon anticipated needs• Interest rate volatility is reduced as portfolio is spread

across different maturities and coupons• Proceeds from the maturing investment can be used

for the scheduled draw, or reinvested in another investment if it is not needed.

Barbell StrategyUtilizes only short-term investments and longer term bonds

Tota

l Por

tfol

ioBenefits:• Longer-term bonds provide higher interest rates, while shorter-

term bonds provide liquidity• Can help to mitigate risk of owning longer-term bonds in a rising

(or anticipated to rise) interest rate environment by allocating just a portion of investments to longer-dated securities

• Maturities of shorter-term bonds can be reinvested in different types of bonds or other securities should market conditions change

Po

rtfolio

Matu

rity

Po

rtfolio

Matu

rity

Investing in the Current Market – “Roll down” the yield curve and use it’s “steepness” to your advantage.

Changes in the U.S. Yield Curve 2010 / 2012 / 2014

19Source: Bloomberg

Fixed Income Options for MI Government Entities: Overview

20

Time Horizon

Short-Term(12 months and < )

Intermediate / Long Term(> 12 months)

Relativ

e Risk

Risk-Free• Treasury Bills

• Agency Discount Notes• Government MMKT

• Treasury Notes/Bonds• Agency Notes/Bonds

Low• Bank Deposit / MMKT Accounts

• Bank Certificates of Deposit• Commercial Paper (IG A1/P1)

• Agency MBS• Callable Agency Bonds

• MI Municipal Notes/Bonds

Moderate

Financing Outlook and Strategies

Municipal Yields (Last 5 Years)

22

The MMD "AAA" curve is written daily to represent a fair value offer-side of the highest-grade AAA rated state GO's, as determined by the MMD analyst team.

Source: Thomson Reuters. As of March 3, 2014.

5 Years Ago

Today1 Month Ago

3 Months Ago

1 Year Ago(%)

(Years)

CurrentOne

Month AgoThree

Months AgoOne Year

AgoFive Years

Ago1 0.15 0.17 0.18 0.20 0.482 0.25 0.34 0.35 0.33 1.223 0.41 0.49 0.62 0.46 1.324 0.66 0.80 0.93 0.59 1.535 0.96 1.14 1.31 0.74 1.756 1.37 1.57 1.65 0.88 1.977 1.71 1.94 1.97 1.09 2.168 2.01 2.24 2.26 1.30 2.379 2.22 2.46 2.45 1.50 2.59

10 2.35 2.62 2.62 1.68 2.8211 2.49 2.76 2.79 1.78 3.1012 2.62 2.89 2.95 1.86 3.3713 2.75 3.03 3.11 1.94 3.5514 2.86 3.15 3.26 2.01 3.7215 2.97 3.25 3.39 2.08 3.8916 3.07 3.35 3.52 2.14 4.0117 3.16 3.44 3.64 2.20 4.1218 3.24 3.53 3.72 2.26 4.2319 3.31 3.60 3.80 2.32 4.3420 3.36 3.66 3.86 2.38 4.4221 3.41 3.72 3.93 2.44 4.5122 3.46 3.77 3.99 2.50 4.5623 3.5 3.82 4.05 2.56 4.6124 3.54 3.85 4.10 2.62 4.6625 3.58 3.88 4.14 2.66 4.6926 3.61 3.91 4.17 2.68 4.7027 3.63 3.94 4.19 2.69 4.7128 3.65 3.96 4.21 2.70 4.7229 3.66 3.97 4.22 2.71 4.7330 3.67 3.98 4.23 2.72 4.74

1 3 5 7 9 11 13 15 17 19 21 23 25 27 290

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

• 10 year Michigan Municipal Bonds are currently trading at a 0.65% spread to “AAA” MMD 10 year Bonds. (Illinois Muni Bonds are trading at a 1.20% spread)

Municipal Bond Funds Suffered in 2013 but Investors are Starting to Come Back

23

MUNICIPAL BOND FUND FLOWS – 2009 - PRESENT

Source: ICI Institute..

Feb-09 Aug-09 Feb-10 Aug-10 Feb-11 Aug-11 Feb-12 Aug-12 Feb-13 Aug-13 Feb-14-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

15,000Municipal Bond Fund Flows ($Bil)

Emergence of the Taxable Market

Taxable municipal issuance increased 17% in 2013 Approximately 40% of taxable proceeds were

used for the refunding of outstanding indebtedness

The receptiveness from “cross-over” buyers in municipal offerings shows the trend of an emerging market that started out of the Build America Bond ProgramThe added buyer universe continues to add depth and liquidity to the municipal market

24Source: Bond Buyer, Offering Documents

Source: Bond Buyer

TAXABLE ISSUANCE VOLUME

$32,832

$38,364

2012 2013 -

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Refunding New Money Combined

($ mil)

With a Sharp Decline in Refunding's, New Bond Issues Fell 12.5% in 2013

25

MUNICIPAL MARKET ISSUANCE - 2004 – 2013

Source: Bond Buyer

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$359,748

$408,283

$388,838

$429,894

$389,632

$409,689

$433,269

$287,718

$379,519

$329,807

$000

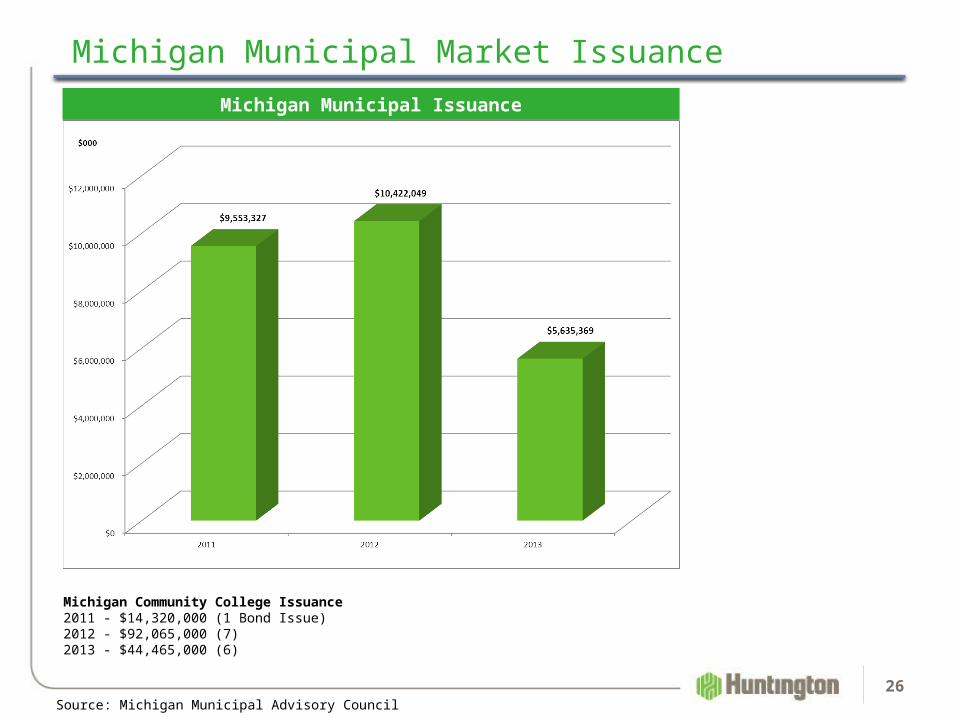

Michigan Municipal Market Issuance

26

Michigan Municipal Issuance

Source: Michigan Municipal Advisory Council

Michigan Community College Issuance 2011 - $14,320,000 (1 Bond Issue)2012 - $92,065,000 (7)2013 - $44,465,000 (6)

0

50,000

100,000

150,000

200,000

250,000

300,000

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

82,41377,62476,25976,81978,996

89,46790,60194,897

99,160106,457

114,029115,859126,178

138,877145,013

147,443158,726

175,939

213,190

263,196

274,336

$ mil

But How Much Are We Missing As Borrowers Utilize Direct Bank Placements?

27

UNITED STATES FINANCIAL INSTITUTIONS – MUNICIPAL HOLDINGS

86% Increase

since 2008

Source: Bond Buyer

Rating Changes

Rating Changes

On 1/15/14 Moody’s Investor Services released a new rating methodology

29

Pension Adjustment Steps

• Allocates cost-sharing plan liabilities

• Discounts accrued liabilities using a market discount rate

• Determines the value of plan assets

• Calculates adjusted net pension liability

• Amortizes adjusted net pension liability

• Applies to calculation versus full value and to revenue

30

Refunding Opportunities

Refunding

What is a Refunding?

• Issuance of new debt at lower interest rates to replace debt which is currently outstanding at higher rates

• A refunding of debt can also entail the issuance of new debt at either lower or higher interest rates to restructure the payments on existing debt.

• Budget relief• Creates debt service capacity for new money

• Factors that make a refunding work:• Lower Interest Rates• Time

• Savings Target: 3% in minimum present value savings

32

Refunding - Continued

• Current – refunding completed within 90 days of the call date on the bonds being refunded

Bond holders are notified and bonds are paid off

• Advance – refunding completed more than 90 days before the call date on the bonds being refunded

• Long Escrow period – escrow reinvestment rate is critical• Only one advance refunding of a new money bond issue is permitted by the

IRS• Proceeds are “Escrowed” until call date then bond holders are paid off

33

Refunding - Continued

• Typically, 10 Years after the original borrowing, a 20 year bond interest rate can be replaced with a 10 year bond interest rate

• Today’s market allows issuers to capture:

1) Rolling down the Yield Curve

2) Historically Low Rates

3) Steep Yield Curve

34

Example – Tax Exempt Refunding

35

Dated Date 5/1/2014Arbitrage yield 2.08625%Escrow yield 0.10028%Value of Negative Arbitrage $55,835

Bond Par Amount $4,890,000True Interest Cost 2.17280%Net Interest Cost 2.22529%Average Coupon 2.65407%Average Life 6.1232106

Par amount of refunded bonds $4,750,000Average coupon of refunded bonds 4.86854%Average life of refunded bonds 6.4549123

PV of prior debt to 05/01/2014 @ 2.086251% $5,624,848Net PV Savings $582,614Percentage savings of refunded bonds 12.26555%Percentage savings of refunding bonds 11.91439%

SourcesBond Proceeds Par Amount $4,890,000

Premium $152,836$5,042,836

UsesRefunding Escrow Deposits Cash Deposit $0.92

SLGS Purchases $4,968,883

Delivery Date Expenses Cost of Issuance $73,350

Other Uses of Funds Additional Proceeds $602$5,042,836

Example – Tax Exempt Refunding

36

DatePrior Debt

ServiceRefunding Debt

Service SavingsPresent Value

Savings12/1/2014 $221,735 $185,844 $35,891 $36,60212/1/2015 $611,735 $551,675 $60,060 $58,67412/1/2016 $612,695 $552,275 $60,420 $57,76212/1/2017 $612,710 $550,600 $62,110 $58,10412/1/2018 $611,750 $548,850 $62,900 $57,58612/1/2019 $610,000 $549,750 $60,250 $53,98412/1/2020 $612,250 $550,450 $61,800 $54,16612/1/2021 $608,250 $546,200 $62,050 $53,22312/1/2022 $613,250 $551,650 $61,600 $51,70812/1/2023 $611,750 $551,500 $60,250 $49,49112/1/2024 $609,000 $545,900 $63,100 $50,711

Total $6,335,125 $5,684,694 $650,431 $582,012

Savings Summary

Taxable Refunding

37

• Advance refunding rules only apply to tax-exempt debt

• Issuers are permitted to refund an issue more than 90 days prior to the call date even if the issue has been advance refunded once if it uses taxable debt

• For the first half of 2013 spreads between taxable and tax-exempt rates were very narrow making it a very good tool to use

• Spreads have widened out and with the expectation that rates will remain low through 2014 it may make sense to wait to be able to use tax-exempt rates if an issue is callable 11/1/14 and becomes an current refunding as of 8/1/14

Build America Bonds

Build America Bond’s

• Build America Bonds are a taxable municipal bond program enacted by congress in 2009 and extended through December 31, 2010.

• The taxable bonds receive an interest subsidy(originally 35%) and at the time a comparable if not a lower cost option to tax-exempt bonds.

• On March 1, 2013, approximately $85 billion of federal budget cuts went into effect, meaning all subsidy payments for direct-pay municipal bonds, including BABs, to be paid between that date and Sept. 30 would be reduced by 8.7% through 9/30/13 and 7.2% from 10/1/13 to 9/30/14.

• With the subsidy cut, issuers started to look to redeem Build America Bonds at par plus accrued interest because they believe the cuts in their federal subsidy payments under sequestration has triggered the extraordinary redemption provisions in their bond documents.

• The bond documents said an “extraordinary event” would occur and trigger a call if there was a change to the federal tax code, pursuant to which the federal subsidy payment is reduced or eliminated.”

39

Build America Bond Structure

40

Period

Ending

Total Debt

Service SubsidyNet Debt

Service

12/1/2013 1,654,412.50 -527,729.52 1,126,682.98

12/1/2014 1,684,142.50 -527,643.14 1,156,499.36

12/1/2015 1,757,252.50 -527,038.44 1,230,214.06

12/1/2016 1,646,312.50 -525,137.94 1,121,174.56

12/1/2017 1,646,042.50 -525,051.54 1,120,990.96

12/1/2018 1,690,772.50 -524,965.16 1,165,807.34

12/1/2019 1,903,072.50 -524,101.30 1,378,971.20

12/1/2020 1,888,762.50 -519,522.82 1,369,239.68

12/1/2021 1,971,868.76 -514,117.66 1,457,751.10

12/1/2022 1,973,600.00 -506,672.82 1,466,927.18

12/1/2023 1,923,737.50 -498,718.06 1,425,019.44

12/1/2024 1,995,468.76 -491,273.22 1,504,195.54

12/1/2025 2,361,143.76 -481,890.70 1,879,253.06

12/1/2026 2,292,362.50 -463,083.64 1,829,278.86

12/1/2027 2,474,268.76 -444,496.54 2,029,772.22

12/1/2028 2,474,675.00 -420,630.26 2,054,044.74

12/1/2029 2,474,925.00 -395,114.26 2,079,810.74

12/1/2030 2,559,675.00 -367,838.52 2,191,836.48

12/1/2031 2,524,500.00 -337,387.28 2,187,112.72

12/1/2032 2,514,250.00 -302,112.78 2,212,137.22

12/1/2033 2,796,500.00 -264,438.68 2,532,061.32

12/1/2034 2,898,750.00 -217,166.06 2,681,583.94

12/1/2035 2,867,250.00 -163,894.38 2,703,355.62

12/1/2036 2,675,625.00 -107,383.22 2,568,241.78

12/1/2037 2,295,125.00 -51,232.00 2,243,893.00

54,944,495.04 -10,228,639.94 44,715,855.10

Subsidy shown is original 35%

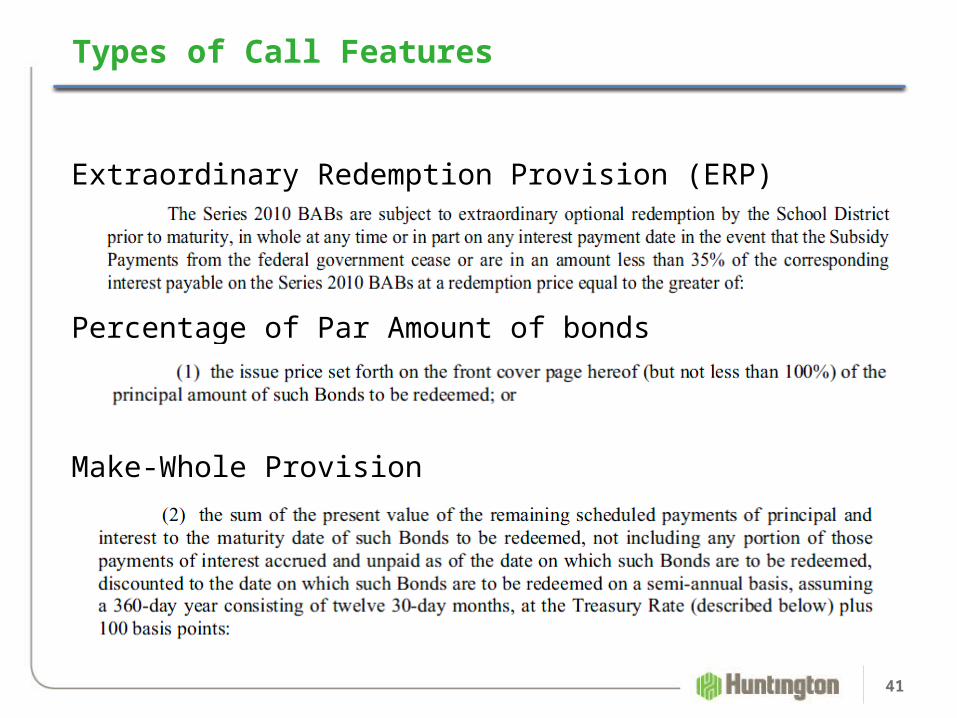

Types of Call Features

Extraordinary Redemption Provision (ERP)

Percentage of Par Amount of bonds

Make-Whole Provision

41

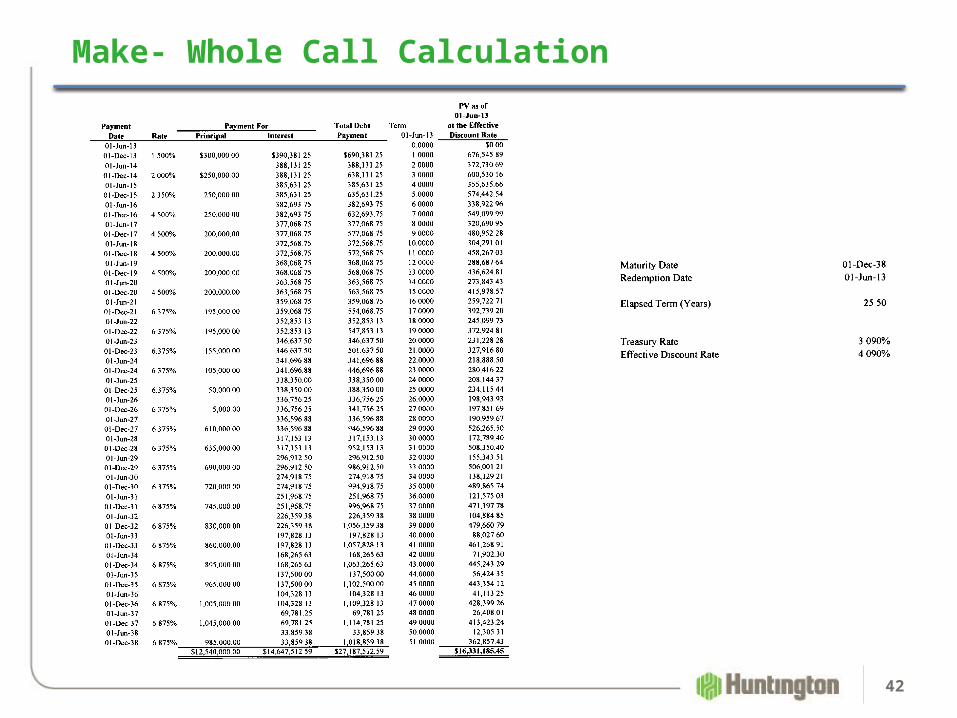

Make- Whole Call Calculation

42

Build America Bond Refunding

43

Bank Qualified Issues

Bank Qualified

• Banks are large buyers of municipal bonds.

• However, Banks may not deduct the carrying cost (the interest expense incurred to purchase or carry an inventory of securities) of tax-exempt municipal bonds. For banks, this provision has the effect of eliminating the tax-exempt benefit of municipal bonds. An exception is included in the Code that allows banks to deduct 80% of the carrying cost of a "qualified tax-exempt obligation." In order for bonds to be qualified tax-exempt obligations the bonds must be (i) issued by a "qualified small issuer," (ii) issued for public purposes, and (iii) designated as qualified tax-exempt obligations. A "qualified small issuer" is (with respect to bonds issued during any calendar year) an issuer that issues no more than $10 million of tax-exempt bonds during the calendar year. Qualified tax-exempt obligations are commonly referred to as "bank qualified bonds."

• Effectively two types of municipal bonds were created under the Act; bank qualified (sometimes referred to as "BQ") and non-bank qualified. Although banks may purchase non-bank qualified bonds they seldom do so. The rate they would require in order for the investment to be profitable would approach the rate of taxable bonds. As a result, issuers obtain lower rates by selling bonds to investors that realize the tax-exempt benefit. In contrast, banks have a strong appetite for bank qualified bonds that are in limited supply. As a result, bank qualified bonds carry a lower rate than non-bank qualified bonds

45

Bank Qualified - Continued

Any issuer that is planning to issue less than $10 million of tax-exempt securities in a calendar year should consider designating the issue as bank qualified in order to obtain the associated interest cost savings. Issuers requiring more than $10,000,000 may be able to take advantage of bank qualification by issuing two series of bonds. For example, for a $20,000,000 financing, a $10,000,000 issue could be sold this year and one could be sold next year to obtain 2 bank qualified issues. Similarly, for a $25,000,000 financing, $10,000,000 could be sold as bank qualified bonds this year and a non-bank qualified $15,000,000 issue could be sold next year.

46

Bank Qualified Spreads

47

Year BQ NON-BQ1 0.45 0.502 0.54 0.653 0.71 0.834 0.92 1.085 1.32 1.496 1.65 1.877 2.06 2.318 2.35 2.659 2.59 2.93

10 2.76 3.1411 2.88 3.3212 3.00 3.4913 3.12 3.6514 3.25 3.8115 3.34 3.9416 3.44 4.0917 3.54 4.2218 3.64 4.3219 3.74 4.4220 3.84 4.52

Appendix C:Disclaimer and Additional Considerations

49

DisclaimerThis report has been prepared for informational purposes only, and does not constitute an offer, recommendation or solicitation to buy or sell any securities. The content of this report is based upon information generally available to the public from sources believed to be reliable. No representation is made that the information is accurate or complete or that any returns indicated will be achieved. Past performance is not indicative of future results. Price and availability are subject to change without notice. The Huntington Investment Company (HIC), or persons involved in the preparation or issuance of this material, may from time to time, have long or short positions in, and buy or sell, the securities, futures or options identical with those mentioned herein. HIC is a wholly owned subsidiary of Huntington Bancshares Incorporated (HBI) and is registered as a Broker Dealer with the NASD, and a member of SIPC. Investments are Not FDIC Insured, May Lose Value, and are Not Bank Guaranteed.

50

Additional Considerations Huntington does not offer or provide accounting, tax or legal advice to its clients. Each client should seek his or her own, and

Huntington advises you to seek your own, advisors for tax, accounting and legal issues in light of your own circumstances.

Although the statements of fact in this presentation have been obtained from and are based upon sources that Huntington

believes are reliable, we do not guarantee their accuracy, and any such information may be incomplete or condensed. All

opinions, estimates and examples constitute Huntington’s judgment as of the date of this presentation and are subject to

change without notice.

This presentation is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or

sale of any security or derivative product or a recommendation for you to utilize any product. This presentation also does not

attempt to forecast future movements of market prices.

The information in this presentation provides a general overview of each of the topics addressed, and may include general

information regarding certain of the U.S. legal, tax and accounting considerations that may affect the transactions described

herein. The descriptions of such matters are necessarily general, do not address the situation of a particular client and do not

purport to be complete.

The statements contained in this presentation to you are intended for your sole use. It may not and should not be relied upon

or utilized by any other party without the express prior written consent of Huntington.

This presentation does not constitute an assessment of the creditworthiness or financial strength or weakness of the client or

any dealer.

® and Huntington® are federally registered service marks of Huntington Bancshares Incorporated.

© 2012 Huntington National Bank.