Embed Size (px)

Citation preview

April 20, 2016

Update on the Privatisation Program

Privatisation Commission

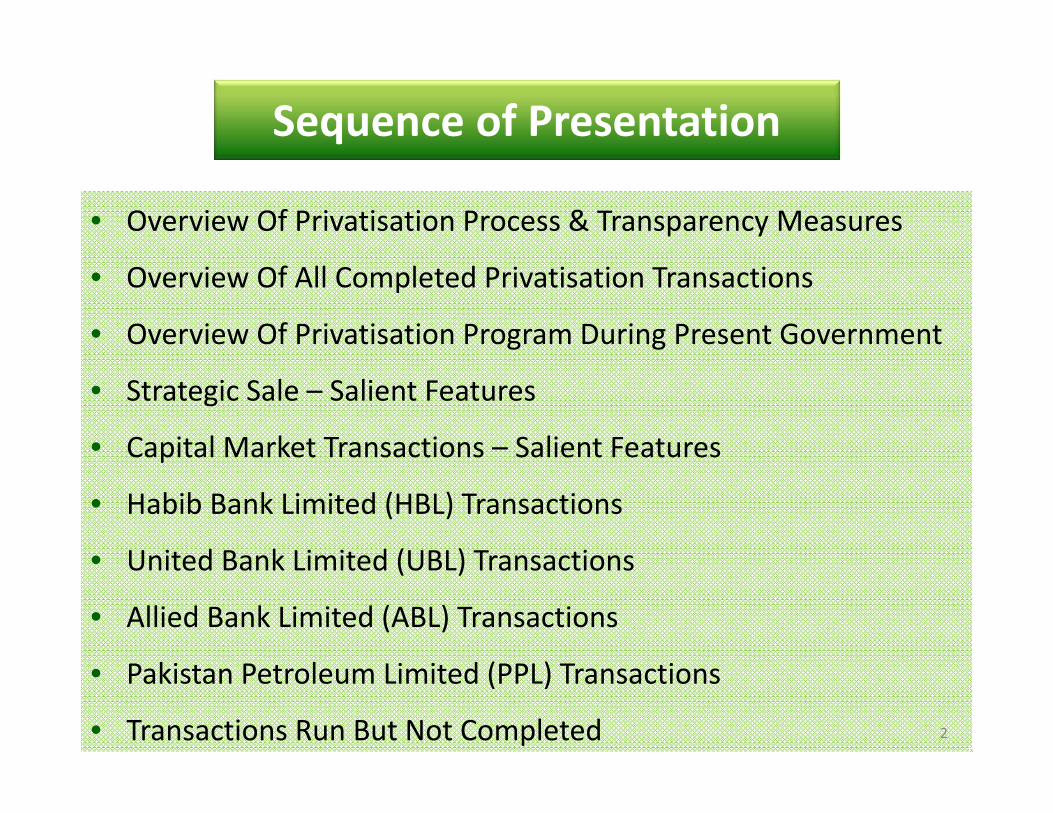

Sequence of Presentation

• Overview Of Privatisation Process & Transparency Measures

• Overview Of All Completed Privatisation Transactions

• Overview Of Privatisation Program During Present Government

• Strategic Sale – Salient Features

• Capital Market Transactions – Salient Features

• Habib Bank Limited (HBL) Transactions

• United Bank Limited (UBL) Transactions

• Allied Bank Limited (ABL) Transactions

• Pakistan Petroleum Limited (PPL) Transactions

• Transactions Run But Not Completed 2

3

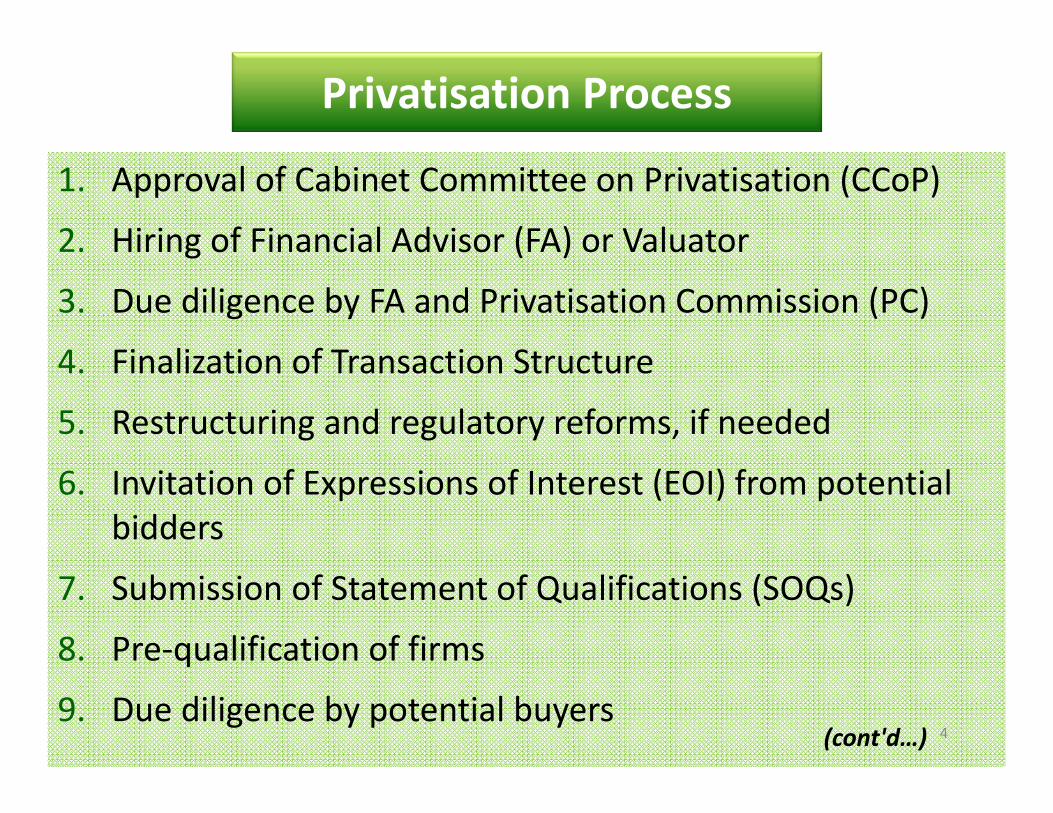

Overview Of Privatisation Process & Transparency Measures

1. Approval of Cabinet Committee on Privatisation (CCoP)

2. Hiring of Financial Advisor (FA) or Valuator

3. Due diligence by FA and Privatisation Commission (PC)

4. Finalization of Transaction Structure

5. Restructuring and regulatory reforms, if needed

6. Invitation of Expressions of Interest (EOI) from potential bidders

7. Submission of Statement of Qualifications (SOQs)

8. Pre‐qualification of firms

9. Due diligence by potential buyers(cont'd…) 4

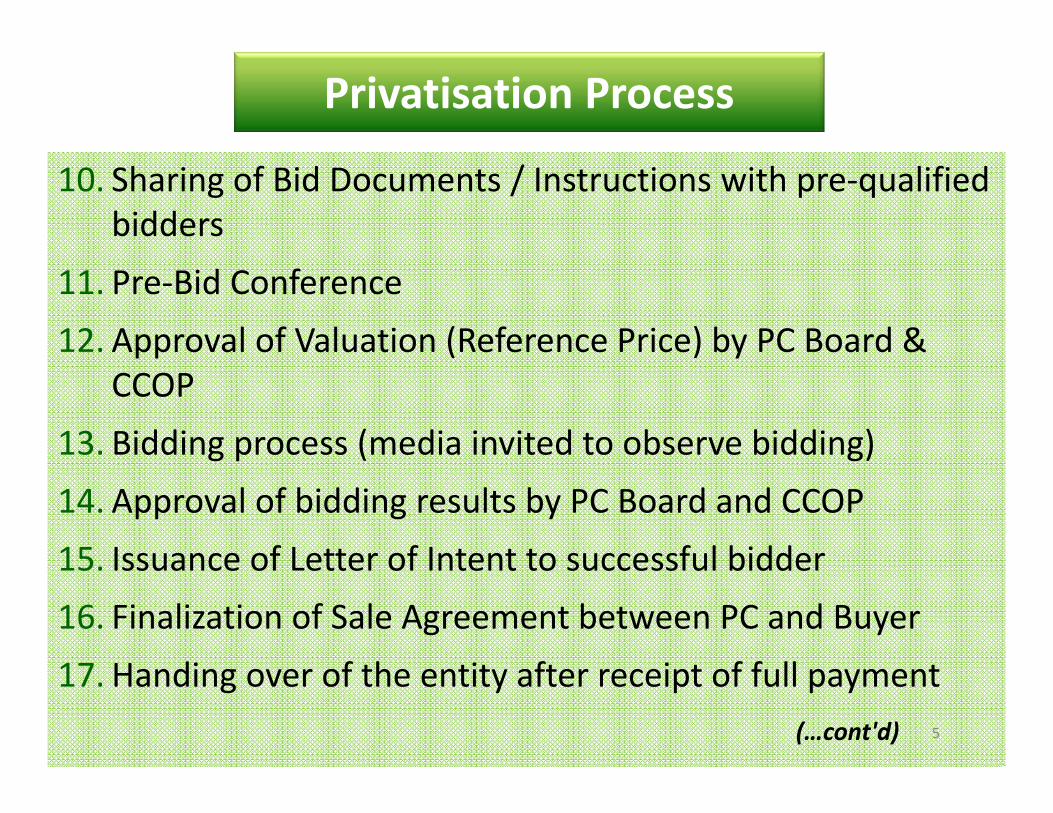

Privatisation Process

10. Sharing of Bid Documents / Instructions with pre‐qualified bidders

11. Pre‐Bid Conference12. Approval of Valuation (Reference Price) by PC Board &

CCOP13. Bidding process (media invited to observe bidding)14. Approval of bidding results by PC Board and CCOP15. Issuance of Letter of Intent to successful bidder16. Finalization of Sale Agreement between PC and Buyer17. Handing over of the entity after receipt of full payment

5(…cont'd)

Privatisation Process

• Process of check & balance is in place

• Process of controls is also in place

• Decisions are broad‐based as every transaction is scrutinized / goes throughvarious independent forums such as:

Evaluation Committee for hiring of Financial Advisor

Transaction Committee

Board of the Privatisation Commission

Cabinet Committee on Privatisation (CCOP)

• Chairman and Secretary, PC, have no independent powers to direct orinfluence any transaction

6

How Transparency is Ensured

• Evaluation Committee is constituted by the Chairman, PC

• Purpose: Evaluating the technical and financial proposals submitted by theinterested parties for Financial Advisory Services for privatisation transactions

• The Committee comprises of the following:

1. 1‐2 members of the PC Board

2. Representative of Administrative Ministry

3. Representative of Finance Division

4. Transaction Manager & Director General of PC

5. Representative of relevant Regulatory Authority (Optional)7

Composition of Evaluation Committee for Hiring of Financial Advisors

• Transaction Committee for each transaction is approved by Chairman, PC,under delegation by the PC Board

• Purpose: To consider Financial Advisor’s recommendations on requisitetransaction‐related decisions, and provide recommendations to PC Board

• Transaction Committee consists of the following members:

1. 1‐2 members of the PC Board

2. Representative of Administrative Ministry

3. Representative of Finance Division

4. Management of SOE being privatised

5. Transaction Manager & Director General of PC

6. Representative of relevant Regulatory Authority (Optional)8

Transaction Committee Members

9

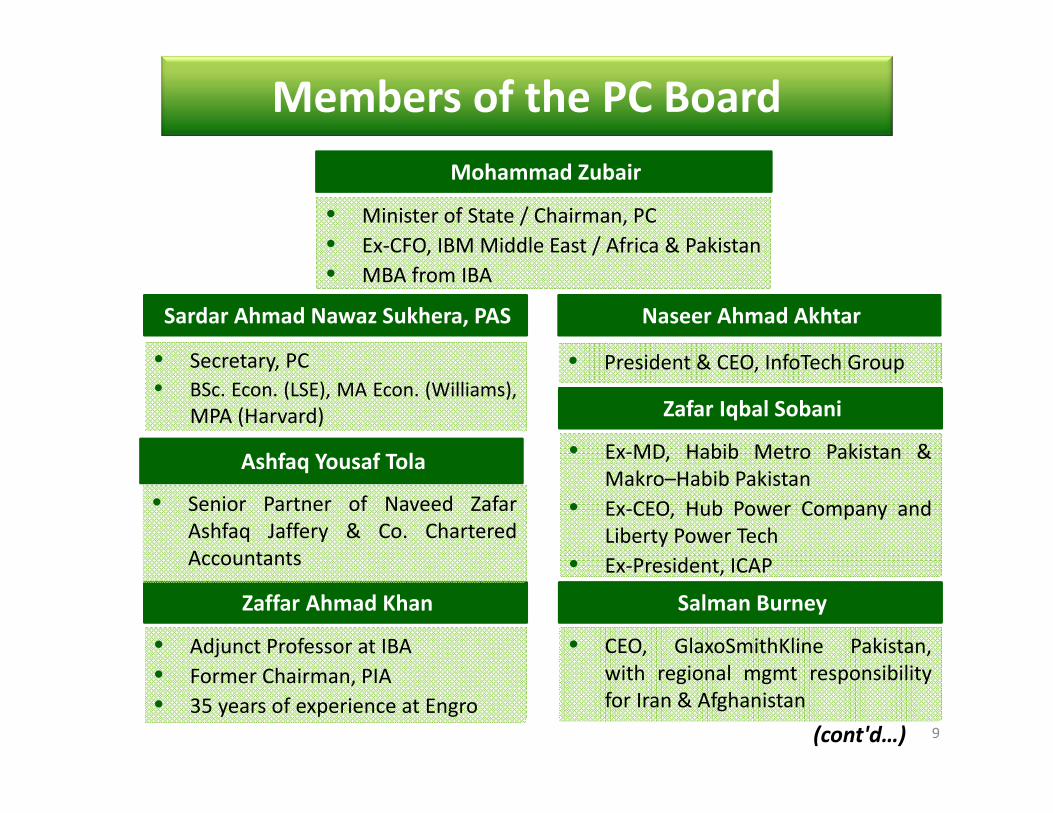

Members of the PC Board

• Minister of State / Chairman, PC• Ex‐CFO, IBM Middle East / Africa & Pakistan• MBA from IBA

Mohammad Zubair

• Secretary, PC• BSc. Econ. (LSE), MA Econ. (Williams),

MPA (Harvard)

Sardar Ahmad Nawaz Sukhera, PAS

• President & CEO, InfoTech Group

Naseer Ahmad Akhtar

• Ex‐MD, Habib Metro Pakistan &Makro–Habib Pakistan

• Ex‐CEO, Hub Power Company andLiberty Power Tech

• Ex‐President, ICAP

Zafar Iqbal Sobani

(cont'd…)

• Adjunct Professor at IBA• Former Chairman, PIA• 35 years of experience at Engro

Zaffar Ahmad Khan

• CEO, GlaxoSmithKline Pakistan,with regional mgmt responsibilityfor Iran & Afghanistan

Salman Burney

Ashfaq Yousaf Tola

• Senior Partner of Naveed ZafarAshfaq Jaffery & Co. CharteredAccountants

10

Members of the PC Board

• Advocate and legal consultant atNishtar & Zafar

• LLM Harvard

Aziz Nishtar

• Industrialist & MBA in marketing

Arsallah Khan Hoti

• Ex‐CEO of Trading Company• Ex‐Country Rep, Exxon Mobil

Shahid Shafiq

• Ex‐Chairman, Lahore Chambers ofCommerce

• Director of Lahore TransportCompany, OGDCL, and BISP

Yawar Irfan Khan

• Capital Markets specialist

Khurram Schehzad

• CEO, Qaim Automotive Mfg Pvt Ltd

Engr. M. A. Jabbar

• Senior partner of a firm ofChartered Accountants

Zafar Iqbal

• Ex‐CEO, Nat’l Asset Mgmt Co.• Ex‐Commissioner, SECP

Etrat Hussain Rizvi

1. Minister for Finance, Economic Affairs, Revenue, Statistics

and Privatisation (Chairman, CCOP)

2. Various economy‐related Federal Ministers & Secretaries

3. Governor, State Bank of Pakistan

4. Chairman, Securities & Exchange Commission of Pakistan

5. Chairman, Board of Investment

6. Chairman, Privatisation Commission11

Members of the CCOP

Other forums taken on board at various stages, including

submission of documents:

• National Accountability Bureau (NAB)

• Public Procurement Regulatory Authority (PPRA)

• Competition Commission of Pakistan (CCP)

• Securities and Exchange Commission of Pakistan (SECP)

12

Additional Forums taken on board

• Financial Advisors (FAs) are appointed by PC to advise on each transaction

• FAs are also not single organisations but a consortium of leading and credible:

i. Investment Banks – Credit Suisse, Citibank, Deutsche Bank, Bank of AmericaMerrill Lynch

ii. Chartered Accountant firms – PwC, KPMG, Deloitte, Ernst & Young, Fergusons

iii. Legal firms – Allen & Overy, Latham & Watkins, Cleary Gottlieb Steen &Hamilton, Freshfields, Haidermota BNR, Mohsin Tayebaly

iv. Technical Advisors – IATA (Aviation), Lahmeyer (Power)

v. HR consultant groups – Excelerate, Abacus Consulting

• During the deliberations by the PC Board and CCOP, the recommendations andjustifications are presented by the FA

13

Financial Advisors appointed by PC for Privatisation Transactions

14

Overview Of All Completed Privatisation Transactions

Period Governing Party / Institution

No. of Transactions Completed

Total Privatisation Proceeds raised

Jan 1991 – July 1993 PML‐N 64 Rs. 12.0 bn

Oct 1993 – Nov 1996 PPP 28 Rs. 44.9 bn

Feb 1997 – Oct 1999 PML‐N 9 Rs. 2.0 bn

Oct 1999 – Nov 2002 Military Rule 27 Rs. 38.7 bn

Nov 2002 – Nov 2007 PML‐Q 38 Rs. 377.2 bn

Mar 2008 – Mar 2013 PPP 1 Rs. 1.3 bn

Jun 2013 to date PML‐N 5 Rs. 172.5 bn

TOTAL 172 Rs. 648.6 bn

15

Completed Privatisation Transactions

16

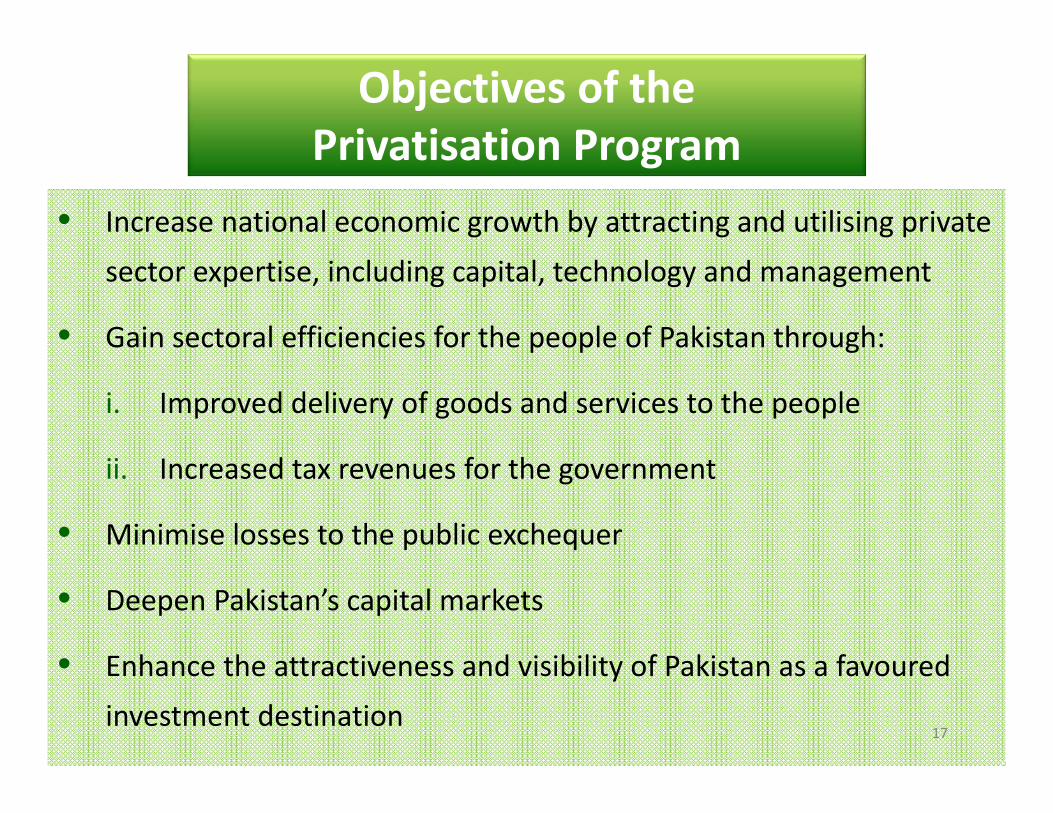

Overview Of Privatisation Program During Present Government

• Increase national economic growth by attracting and utilising private sector expertise, including capital, technology and management

• Gain sectoral efficiencies for the people of Pakistan through:

i. Improved delivery of goods and services to the people

ii. Increased tax revenues for the government

• Minimise losses to the public exchequer

• Deepen Pakistan’s capital markets

• Enhance the attractiveness and visibility of Pakistan as a favoured investment destination

17

Objectives of the Privatisation Program

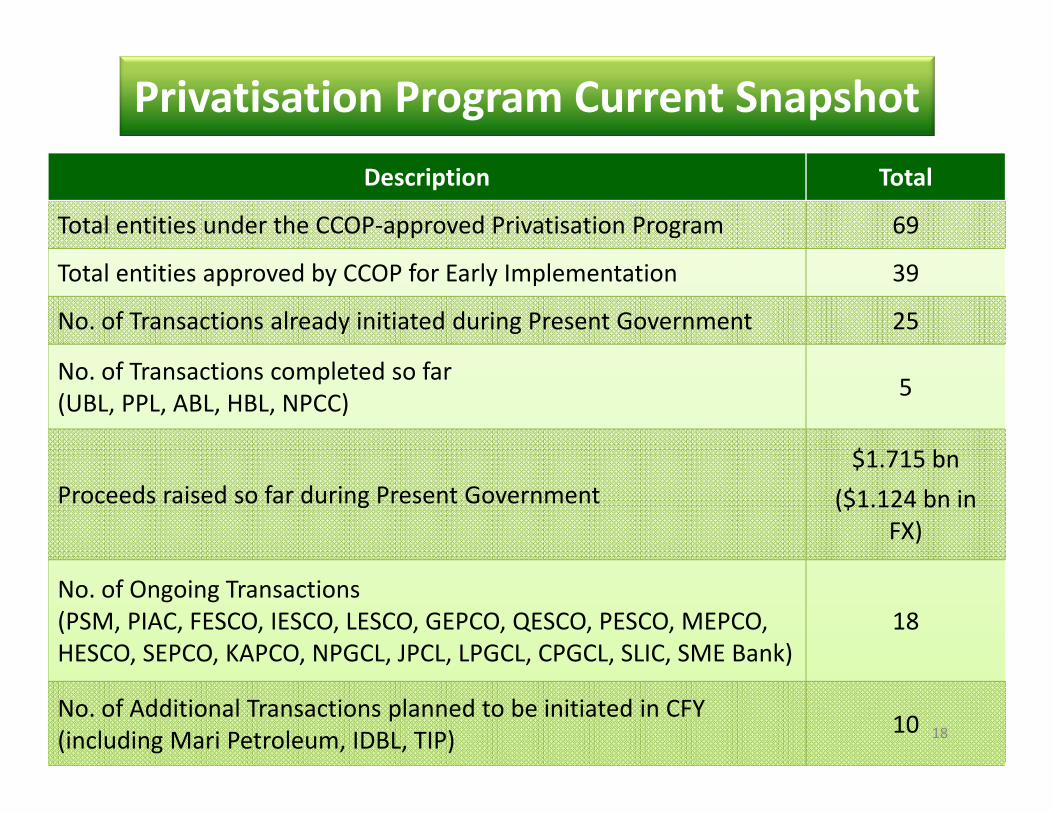

Description Total

Total entities under the CCOP‐approved Privatisation Program 69

Total entities approved by CCOP for Early Implementation 39

No. of Transactions already initiated during Present Government 25

No. of Transactions completed so far(UBL, PPL, ABL, HBL, NPCC) 5

Proceeds raised so far during Present Government$1.715 bn

($1.124 bn in FX)

No. of Ongoing Transactions (PSM, PIAC, FESCO, IESCO, LESCO, GEPCO, QESCO, PESCO, MEPCO, HESCO, SEPCO, KAPCO, NPGCL, JPCL, LPGCL, CPGCL, SLIC, SME Bank)

18

No. of Additional Transactions planned to be initiated in CFY(including Mari Petroleum, IDBL, TIP) 10 18

Privatisation Program Current Snapshot

Raised gross proceeds of Rs. 172.9 billion so far, including over $1.1 billion in FX, from 5 completed transactions:

• UBL Offering (June 2014) – Rs. 38.2 billion, including $315 million in FX First transaction after gap of 7 years. Only 7% discount, lower than

average in comparable markets in the Asia‐Pacific region (~12%)• PPL Offering (June 2014) – Rs. 15.4 billion

First ever transaction to fetch a premium on sale of any Pakistani scrip• ABL Offering (December 2014) – Rs. 14.4 billion, including $20 million in FX Only 2.5% discount, beating Asia Region precedent benchmarks

• HBL Offering (April 2015) – Rs. 102.4 billion, including $764 million in FX Largest ever equity offering in Pakistan and any Asian Frontier Market

• NPCC Strategic Sale (August 2015) – Rs. 2.5 billion, all in FX of $25 million

Sold after 4 unsuccessful attempts in previous governments. First strategic sale since 2008 19

Transactions Completed So Far

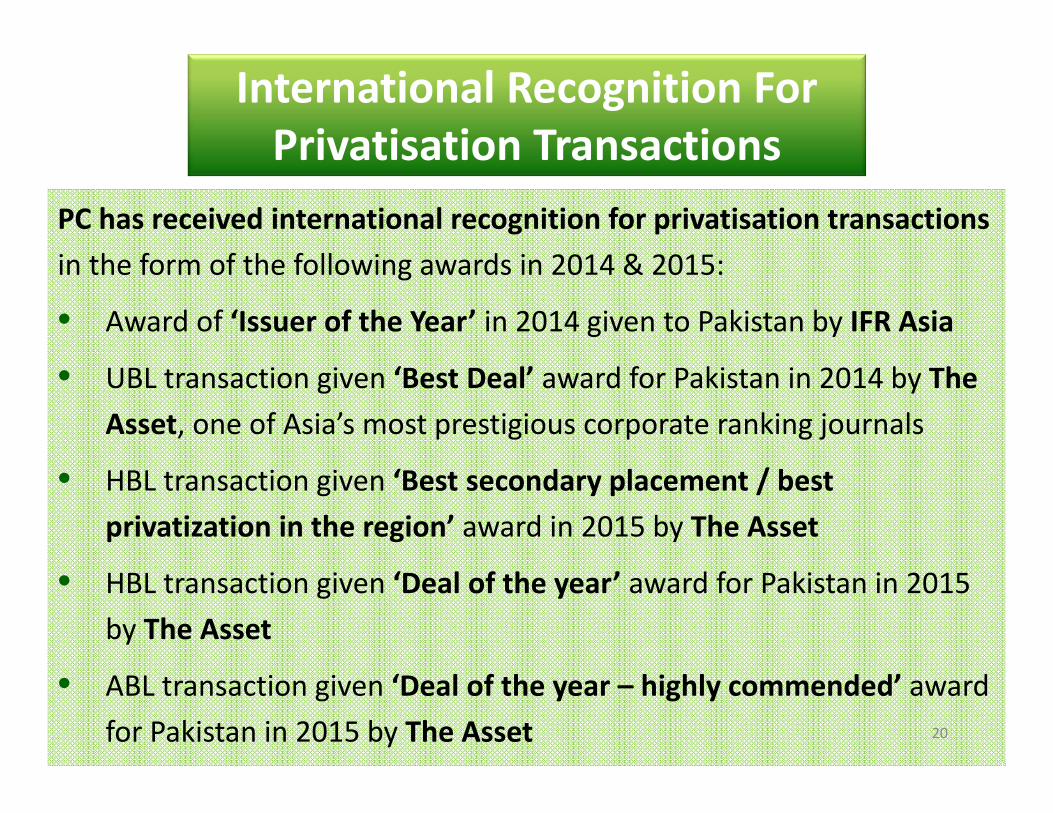

PC has received international recognition for privatisation transactions in the form of the following awards in 2014 & 2015:

• Award of ‘Issuer of the Year’ in 2014 given to Pakistan by IFR Asia

• UBL transaction given ‘Best Deal’ award for Pakistan in 2014 by The Asset, one of Asia’s most prestigious corporate ranking journals

• HBL transaction given ‘Best secondary placement / best privatization in the region’ award in 2015 by The Asset

• HBL transaction given ‘Deal of the year’ award for Pakistan in 2015 by The Asset

• ABL transaction given ‘Deal of the year – highly commended’ award for Pakistan in 2015 by The Asset 20

International Recognition For Privatisation Transactions

• On PC’s initiative, top‐ranked interested parties for Financial Advisory Services for privatisation transactions were encouraged to match the lowest financial bid or reduce their bid offer already approved by PC Board

PC has generated savings of $6.79 million (equivalent to Rs. 690 million) in Financial Advisory Services contracts so far. This is, arguably, unprecedented in the public sector!

21

Savings Generated In Financial Advisory Services Contracts

• There are currently 18 ongoing transactions at PC including PIA, Power

Sector entities, PSM, SLIC and SME Bank

• After the last major sectoral privatisation of the Banking and

Telecommunication sectors, this is the first time that efforts are being

undertaken to shift the entire Power and Aviation sectors from the public

domain to the private sector

• The privatisation process for some of these entities, such as PIA (approved

by CCI for P‐list in 1997), PSM (approved by CCI for P‐list in 1997, and

decision reaffirmed by CCI in 2006) and FESCO (approved by CCI for P‐list in

2011), has reached an advanced stage for the first time ever 22

Overview of Ongoing Transactions

• FA for restructuring of PIAC leading to private sector participation in core

operations was appointed in October 2014

• In February 2015, PC recommended the conversion of PIAC, a statutory

corporation, into a public limited company, through legislation, as an

essential pre‐requisite for the transaction

• Due diligence by the FA was completed in August 2015

• PIAC (Conversion) Ordinance 2015 was promulgated on December 04, 2015.

However, the Senate disapproved the Ordinance on December 31, 2015

• PIAC (Conversion) Bill 2015 was approved by the National Assembly on

January 21, 201623

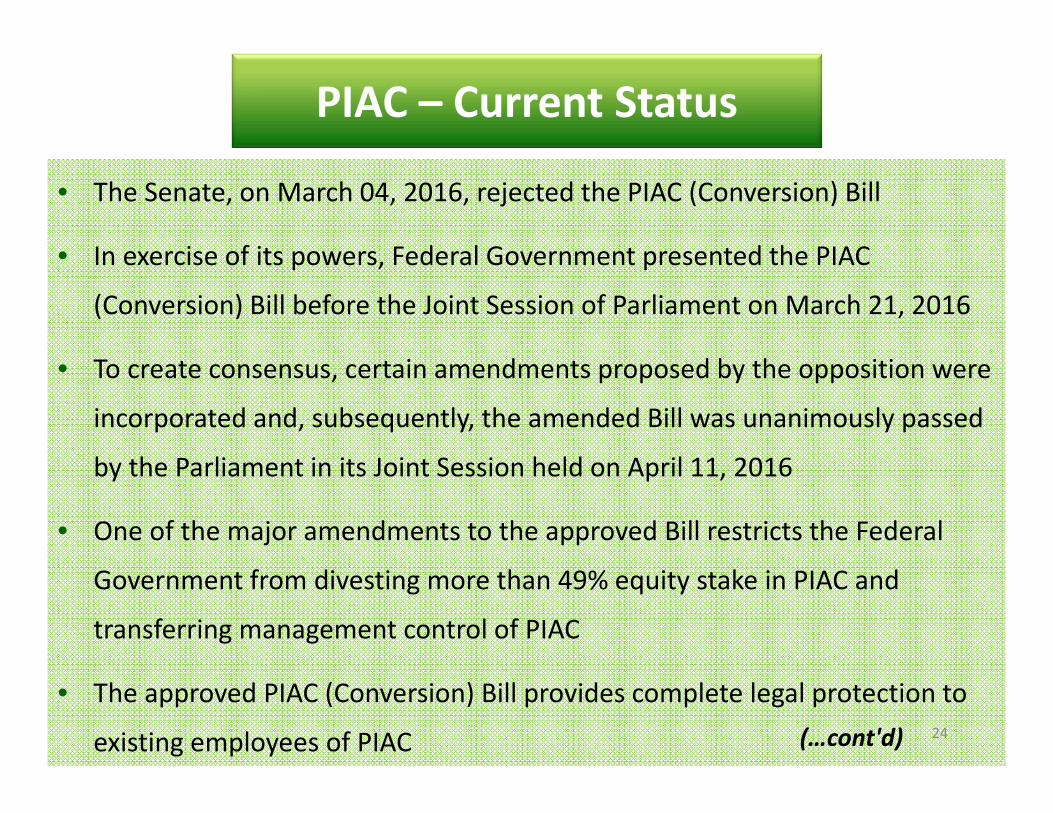

PIAC – Current Status

(cont'd…)

• The Senate, on March 04, 2016, rejected the PIAC (Conversion) Bill

• In exercise of its powers, Federal Government presented the PIAC

(Conversion) Bill before the Joint Session of Parliament on March 21, 2016

• To create consensus, certain amendments proposed by the opposition were

incorporated and, subsequently, the amended Bill was unanimously passed

by the Parliament in its Joint Session held on April 11, 2016

• One of the major amendments to the approved Bill restricts the Federal

Government from divesting more than 49% equity stake in PIAC and

transferring management control of PIAC

• The approved PIAC (Conversion) Bill provides complete legal protection to

existing employees of PIAC 24

PIAC – Current Status

(…cont'd)

• EOIs from investors for FESCO were invited on November 02, 2015 with deadline for submission by December 31, 2015

• 7 Interested Parties (IPs) submitted EOIs by the deadline. Some of these IPs, as well as additional IPs, requested an extension to the deadline in order to submit the requisite EOIs / SOQs

• PC suggested the publication of an advertisement extending the deadline, which would both enable maximum investor participation and fulfil requirements of PC Ordinance

• However, as the government is revisiting its strategy with respect to DISCOs, the necessary clearance has not been received by PC

• Once the government has confirmed a strategy for DISCOs, a decision on the fate of the FESCO transaction, as well as the privatisation of other DISCOs, shall be made 25

FESCO – Current Status

• FA for privatisation of PSM was appointed in April 2015. Due Diligence by the FA was completed in August 2015

• The transaction structure was proposed and approved by the PC Board. However, on October 02, 2015, the CCOP decided that as the Government of Sindh (GoS) had expressed interest in acquiring PSM, they should be offered to acquire PSM with all its assets and liabilities

• PC approached GoS in this regard vide its letters dated October 14, 2015, November 04, 2015 and December 03, 2015. Furthermore, in its letter dated December 15, 2015, PC requested GoS to respond by December 31, 2015

• GoS responded vide its letter dated January 04, 2016, requesting certain documents in order to make a decision on the matter. The same were provided by PC, vide a letter dated January 07, 2016, in which GoS was requested to convey its final decision by January 21, 2016

26

PSM – Current Status

(cont'd…)

• GoS, vide its letter dated January 08, 2016, informed PC that it is not in a position to convey its response by January 21, 2016, as it will take a longer period of time to carry out the due diligence process

• PC wrote to GoS, vide its letter dated February 10, 2016, allowing the GoS an additional 2‐3 weeks to revert back with its decision

• In the meantime, GoS wrote to PC, vide its letter dated February 09, 2016, stating that it cannot make a decision till the following actions are taken by GOP, to facilitate GoS in making the final decision:

i. Share PC’s Financial Advisor’s technical and financial due diligence reports

ii. Restore gas supply to PSM immediately to avoid permanent damage to PSM

iii. Share an appropriate ‘Incentive Package’ for the revival of PSM

27(…cont'd…)

PSM – Current Status

• PC, vide its letter dated March 17, 2016, responded to the letter from GoS, stating:

i. In case GoS considers setting up an industrial zone on PSM’s non‐core land, post‐acquisition, the Federal Government may consider providing incentive packages similar to those provided to other industrial zones

ii. Once GoS takes over PSM and clears its current liability towards Sui Southern Gas Company Limited (SSGCL), the gas supply shall be immediately restored

iii. Requesting that the FINAL OFFER of GoS on acquisition of PSM, based on the offer of the Federal Government, i.e. on an “as is where is”, may kindly be conveyed within 2‐3 weeks

• Despite having been provided complete access to PSM’s site and management, GoShas not been able to provide a definitive response to the offer in over 6 months.For normal transactions, PC allows max. 3‐4 weeks to each interested party to complete its buy‐side Due Diligence

• Once the matter with GoS is closed, the transaction shall be finalised within 4‐5 months thereafter

28(…cont'd)

PSM – Current Status

29

Strategic Sale – Salient Features

• Strategic sale of GoP’s 88% stake in NPCC has been successfully completed in August 2015, after 4 unsuccessful attempts during previous governments

• First strategic sale by GoP in over 8 years

• GoP’s stake has been sold for Rs. 2.5 billion to a Saudi business group, M/s Mansour Al Mosaid

• The price obtained was:

i. 27% above the CCoP‐approved reserve price of Rs. 1.97 billion; and

ii. 49% higher than the break‐up value of Rs. 951 per share

• All proceeds from the transaction have been generated in the form of Foreign Exchange (FX) worth $25 million

• All payments relating to Golden Handshakes (GHS) / Voluntary Separation Scheme (VSS), amounting to Rs. 64 million, have been made by the buyer

• Under the Share Purchase Agreement (SPA) executed between GOP and the buyer, all existing employees, including those who have reached superannuation, are to be retained for at least 1 year 30

Strategic Sale Of NPCC – Salient Features

31

Capital Market Transactions –Salient Features

32

Capital Market Transactions: Share Price Comparison

SrNo Transaction

Transaction Completion

Date

Revenues Raised

PC SalePrice

Lowest Share Price Since PC Sale (w/ date)

Current Share Price

(Apr 19, 2016)

1. UBL Jun 12, 2014 Rs. 38.2 bn Rs. 158 Rs. 143.69(Jan 27, 2016) Rs. 156.00

2. PPL Jun 28, 2014 Rs. 15.4 bn Rs. 219 Rs. 101.08(Jan 18, 2016) Rs. 127.68

3. ABL Dec 12, 2014 Rs. 14.4 bn Rs. 110 Rs. 83.25(Mar 02, 2016) Rs. 92.20

4. HBL Apr 11, 2015 Rs. 102.4 bn Rs. 168 Rs. 170.79(Mar 30, 2016) Rs. 173.36

Share price movements of stocks are based on domestic and international market conditions and dynamics, and can not be predicted

33

Habib Bank Limited (HBL) Transactions

34

HBL – All Completed Transactions

SrNo Transaction Completion

DateStake Sold Sale Price Price per

1% stake Buyer

1. Strategic Sale December 2003 51% Rs. 22,409m Rs. 439mAgha Khan Fund for

Economic Development

2. Initial Public Offering October 2007 7.5% Rs. 12,161m Rs. 1,621m General Public Thru

Stock Exchange

3. Secondary Public Offering April 2015 41.5% Rs. 102,000m Rs. 2,458m

Institutional & HNWI Offer Thru Stock

Exchange

The strategic sale of 51% stake in HBL in 2003:

i. led to improvement in the company’s operational and financial performance

ii. increased the tax and dividend collections for the GOP from HBL

iii. increased the value of HBL’s shares significantly

iv. enabled the GOP to fetch far higher prices in subsequent sales

35

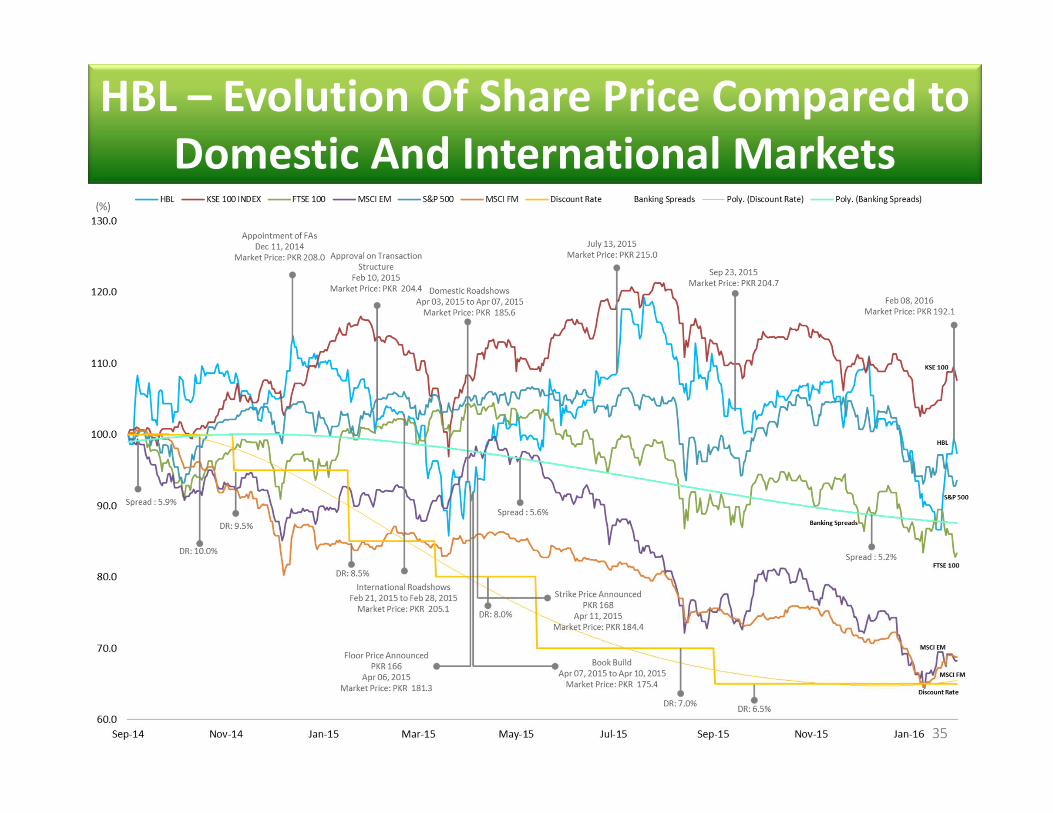

HBL – Evolution Of Share Price Compared to Domestic And International Markets

36

United Bank Limited (UBL) Transactions

37

SrNo Transaction Completion

DateStake Sold Sale Price Price per

1% stake Buyer

1. Strategic Sale October 2002 51% Rs. 12,350m Rs. 242mConsortium of Bestway & Abu Dhabi Group

2. Initial Public Offering August 2005 4.2% Rs. 1,087m Rs. 259m General Public Thru

Stock Exchange

3. Secondary PublicOffering (GDR) June 2007 25% Rs. 39,450m Rs. 1,578m

GDR offering to institutionalinvestors

4. Secondary PublicOffering June 2014 19.6% Rs. 38,224m Rs. 1,950m

Institutional & HNWI Offer Thru Stock Exchange

The strategic sale of 51% stake in UBL in 2002:

i. led to improvement in the company’s operational and financial performance

ii. increased the tax and dividend collections for the GOP from UBL

iii. increased the value of UBL’s shares significantly

iv. enabled the GOP to fetch significantly higher prices in subsequent sales

UBL – All Completed Transactions

38

UBL – Evolution Of Share Price Compared to Domestic And International Markets

39

Allied Bank Limited (ABL) Transactions

40

SrNo Transaction Completion

DateStake Sold Sale Price Price per

1% stake Buyer

1. Strategic Sale February 1991 51% Rs. 972m Rs. 19m EMG

2. Secondary Public Offering December 2014 11.5% Rs. 14,440m Rs. 1,256m

Institutional & HNWI Offer Thru Stock Exchange

The strategic sale of 51% stake in ABL in 1991:

i. led to improvement in the company’s operational and financial performance

ii. increased the tax and dividend collections for the GOP from ABL

iii. increased the value of ABL’s shares significantly

iv. enabled the GOP to fetch a significantly higher price in the subsequent sale

ABL – All Completed Transactions

41

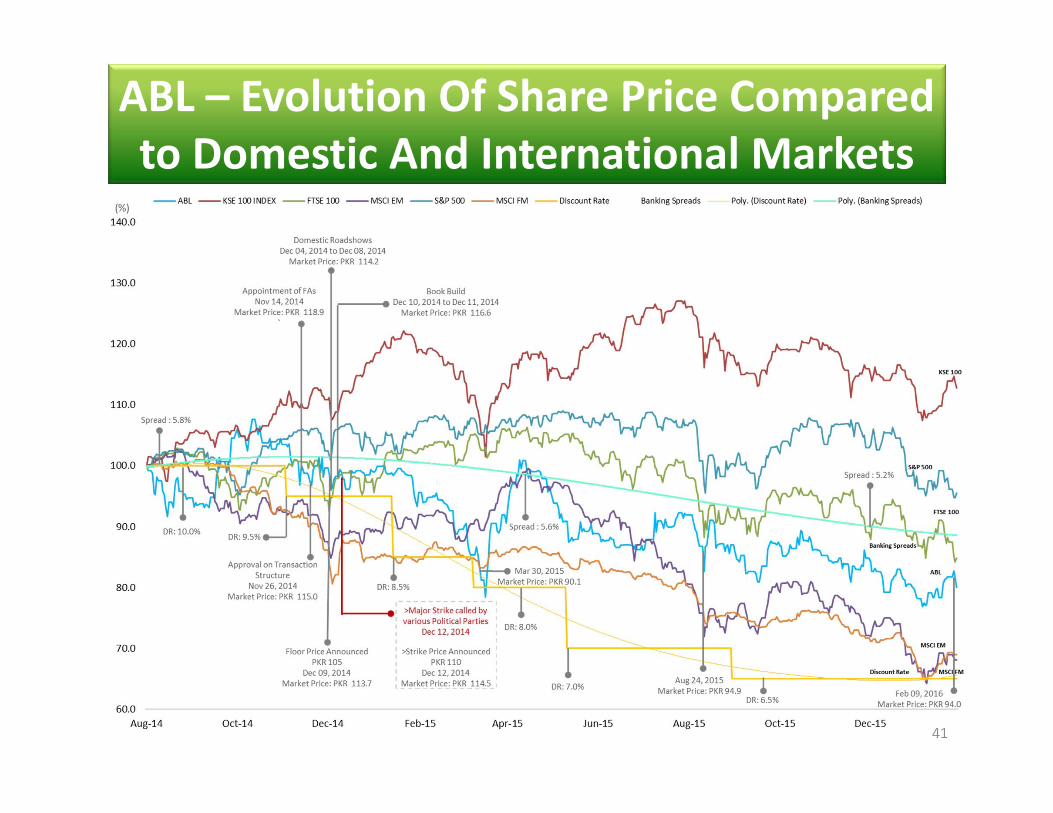

ABL – Evolution Of Share Price Compared to Domestic And International Markets

42

Pakistan Petroleum Limited (PPL) Transactions

43

SrNo Transaction Completion

Date Stake Sold Sale Price Price per 1% stake Buyer

1. Initial Public Offering July 2004 15% Rs. 5,633m Rs. 376m

General Public Thru Stock Exchange

2. Secondary Public Offering June 2014 3.6% Rs. 15,342m Rs. 4,322m

Institutional & HNWI Offer Thru Stock Exchange

The Initial Public Offering of 15% stake in PPL in 2004:

i. enabled ownership of PPL shares by the general public

ii. led to price discovery of PPL shares

iii. allowed members of general public to benefit from dividends and increases in share price of PPL

iv. enabled the GOP to fetch a significantly higher price in the subsequent sale

PPL – All Completed Transactions

44

PPL – Evolution Of Share Price Compared to Domestic And International Markets

45

Transactions Run But Not Completed

1 OGDCL transaction was postponed due to: (i) significant drop in global oil prices (ii) KPK Govtcase in PHC (iii) PTI Dharna2 Strategic sale of HEC could not be completed as the buyer did not pay up the balance amountof Rs. 225 million. Earnest money worth Rs. 25 million has been forfeited. The buyer went to theIslamabad High Court (IHC) seeking the transaction. PC got the stay vacated & has also got acriminal case lodged against the Buyer for the dishonoured cheque. Case still pending in IHC. 46

Transactions Run But Not Completed

SrNo Transaction

Process Completion Date

Expected RevenueExpected FX

(USD)PKR USD

Equivalent

1. OGDCL1 November 2014 Rs. 80 bn $800m $600m

2. HEC2 June 2015 Rs. 0.25 bn $2.5m $2.5m

GRAND TOTAL Rs. 80.25 bn $802.5m $602.5m

• FA appointed in April 2014 for divestment of up to 10% stake in OGDCL through international and domestic capital markets

• On November 05, 2014, PC Board and CCOP approved a strike price of Rs. 216 per share, i.e. discount of ~5.9% to closing price of the same day, i.e. Rs. 229.62 per share

• Book Building was initiated on November 05, 2014, and closed on November 07, 2014

• Total orders of ~$342 million (~162.76 million shares) were received, i.e. 0.52x coverage of the offer size (~311 million shares) at the Floor Price

• On November 08, 2014, PC Board approved the strike price at Rs. 216 per share. OGDCL share price was Rs. 225.02, as of close on November 07, 2014

• PC Board’s recommended strike price was submitted to CCOP on November 08, 2014, for approval. However, CCOP decided to postpone the OGDCL transaction due to significant drop in global oil prices

• Since November 26, 2014, the OGDCL share price has never reached the same levels again due to the global oil market and capital market conditions

• OGDCL share price was Rs. 116.57 per share, as of close on April 19, 2016 47

OGDCL Transaction

• 3 unsuccessful attempts were made in 2006, 2011 and 2013, to privatise HEC. Not even a single bidder deposited the earnest money in any of the 3 instances

• HEC transaction was reinitiated in December 2014. 3 Interested Parties submitted EOI for bidding, and conducted buy‐side due diligence. However, only one bidder remained in the process thereafter, i.e. M/s Cargill Holding Ltd, and deposited earnest money worth Rs. 25 million with PC

• Sole bidder accepted the CCOP‐stipulated terms and conditions for sale, and the CCOP approved the sale on this basis on March 26, 2015. The terms and conditions stipulated that the buyer shall:i. Make a cash payment of Rs. 250 millionii. Assume all current and future liabilities of the HEC, including running finance liability worth Rs.

435 millioniii. Take up liabilities pertaining to the Gratuity and Provident und of the employees, including

gratuity worth Rs. 30 millioniv. Not benefit from any previous losses and potential tax adjustments in the future, worth Rs. 190

millionv. Surrender all potential claims to any Sales Tax refund with the FBR, worth Rs. 191 million

• In total, the buyer agreed to a Total Sale Consideration worth Rs. 1,095 million. However, the cheque deposited by the buyer for the balance amount worth Rs. 225 million bounced. Therefore, the Letter of Acceptance (LOA), which had been issued to the buyer, was revoked, and the Earnest Money worth Rs. 25 million was forfeited by PC and the entity was retained by GOP

• Buyer went to the Islamabad High Court (IHC) to seek the transaction. PC got the stay vacated and has also got a criminal case lodged against the buyer for the dishonoured cheque. Case is still pending before the IHC

48

HEC Transaction

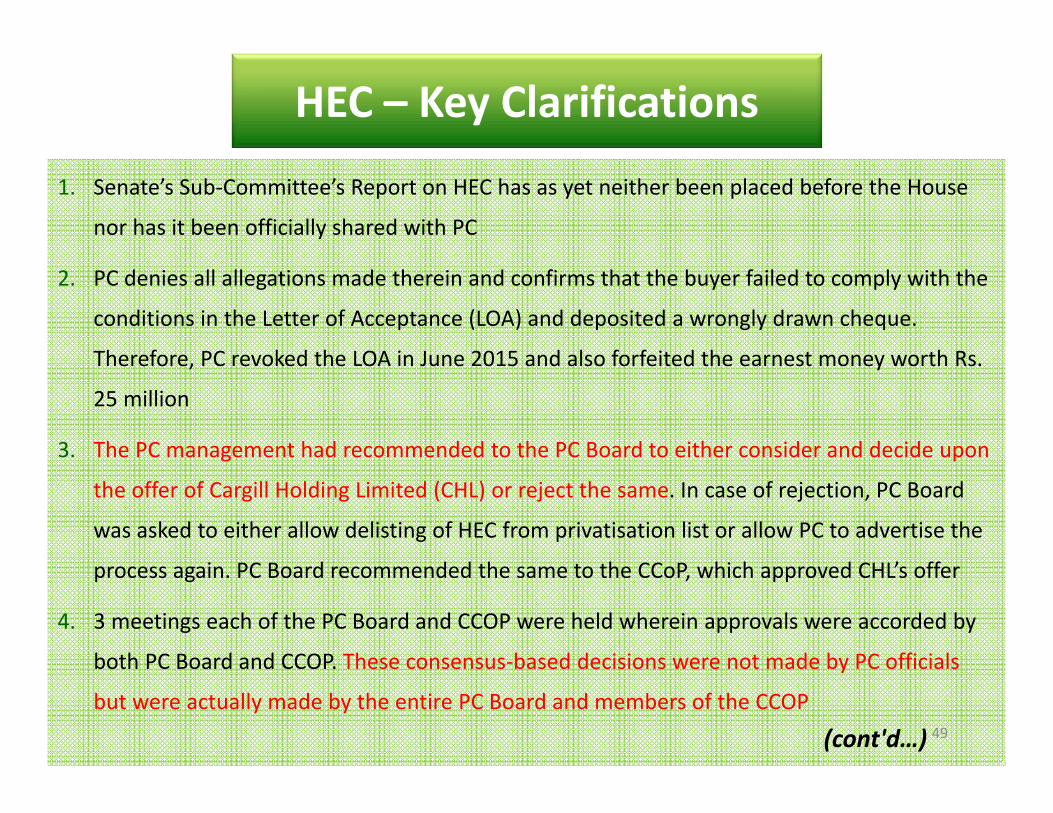

1. Senate’s Sub‐Committee’s Report on HEC has as yet neither been placed before the House

nor has it been officially shared with PC

2. PC denies all allegations made therein and confirms that the buyer failed to comply with the

conditions in the Letter of Acceptance (LOA) and deposited a wrongly drawn cheque.

Therefore, PC revoked the LOA in June 2015 and also forfeited the earnest money worth Rs.

25 million

3. The PC management had recommended to the PC Board to either consider and decide upon

the offer of Cargill Holding Limited (CHL) or reject the same. In case of rejection, PC Board

was asked to either allow delisting of HEC from privatisation list or allow PC to advertise the

process again. PC Board recommended the same to the CCoP, which approved CHL’s offer

4. 3 meetings each of the PC Board and CCOP were held wherein approvals were accorded by

both PC Board and CCOP. These consensus‐based decisions were not made by PC officials

but were actually made by the entire PC Board and members of the CCOP49

HEC – Key Clarifications

(cont'd…)

5. As far as PC is concerned, the HEC transaction stands terminated since the LOA was revoked

in June 2015. The transaction underwent all legal processes. No financial loss has been

caused to GoP. Instead, GoP has retained Earnest Money of Rs. 25 million and also the SOE

6. PC has registered an FIR against CHL’s representative for depositing a wrongly drawn cheque

7. PC is fully committed to ensure the highest standards of integrity and transparency in

conducting all its transactions. If PC was assisting CHL in the whole process, it would not

have revoked the LOA but instead would have facilitated the buyer to takeover HEC

8. PC itself shares all the transaction documents with the NAB at the end of each transaction.

This is a mandatory process, which the PC has implemented already. Furthermore, the

Auditor General of Pakistan has also been requested to complete the transactional audit of

all completed transactions

50

HEC – Key Clarifications

(…cont'd)

Thank You

51