Embed Size (px)

Citation preview

Update on the MPF System in Hong Kong - Retirement Planning

and Challenges

Alice LawChief Operating Officer and Executive Director,Mandatory Provident Fund Schemes Authority

11 January 2018

Hong Kong’s

Demographic

Developments

3

Ageing Population in Hong Kong (1)

Percentage of the population aged 65 and over(excluding foreign domestic helpers)

Year 2016 Year 2066

37%

17%

4

Year 2016 Year 2066

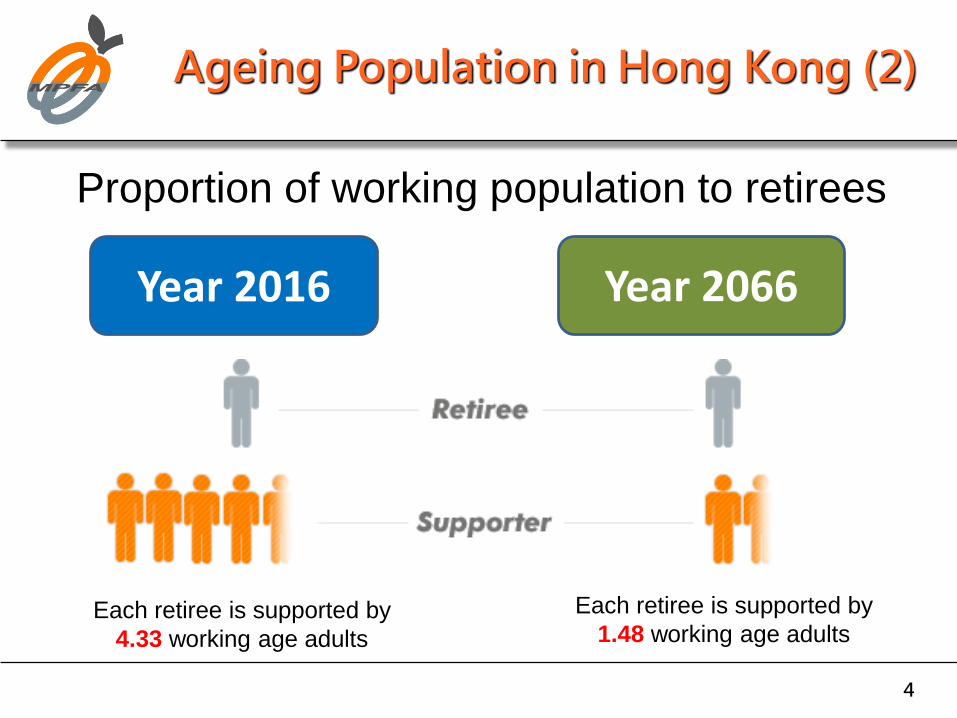

Proportion of working population to retirees

Each retiree is supported by

4.33 working age adults

Each retiree is supported by

1.48 working age adults

Ageing Population in Hong Kong (2)

5

Year 2016 Year 2066

Life expectancy of Hong Kong people

Women

Age 87

Men

Age 81

Women

Age 93

Men

Age 87

Ageing Population in Hong Kong (3)

Overview of

MPF System

7

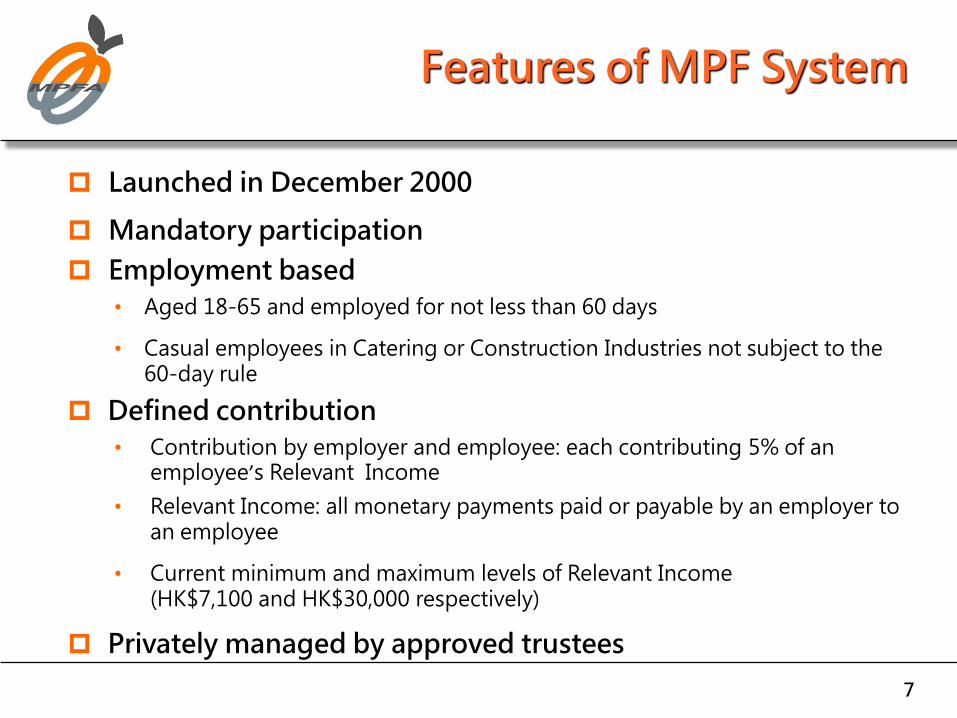

Features of MPF System

Launched in December 2000

Mandatory participation

Employment based

• Aged 18-65 and employed for not less than 60 days

• Casual employees in Catering or Construction Industries not subject to the 60-day rule

Defined contribution

• Contribution by employer and employee: each contributing 5% of an employee’s Relevant Income

• Relevant Income: all monetary payments paid or payable by an employer to an employee

• Current minimum and maximum levels of Relevant Income(HK$7,100 and HK$30,000 respectively)

Privately managed by approved trustees

8

World Bank Old Age Protection Framework

Five Pillars Framework

2. Employment based, mandatory, contributory and privately managed (e.g. MPF)

3. Voluntary savings(e.g. personal savings and insurance)

4. Informal support (e.g. family support)

Other formal social programmes (e.g. health care and housing)

Other individual assets (e.g. home ownership)

1. Mandatory, contributory and publicly managed

0. Non-contributory, publicly financed and managed (e.g. Comprehensive Social Security Assistance Scheme in Hong Kong)

9

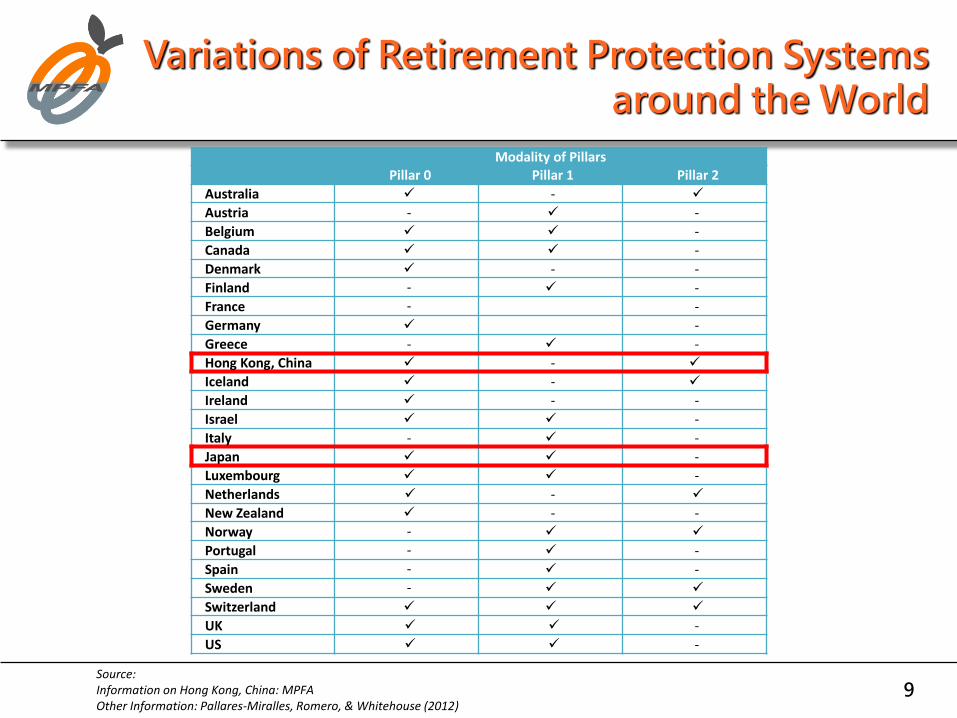

Variations of Retirement Protection Systems around the World

Modality of PillarsPillar 0 Pillar 1 Pillar 2

Australia -

Austria - -

Belgium -

Canada -

Denmark - -

Finland - -

France - -

Germany -

Greece - -

Hong Kong, China -

Iceland -

Ireland - -

Israel -

Italy - -

Japan -

Luxembourg -

Netherlands -

New Zealand - -

Norway -

Portugal - -

Spain - -

Sweden -

Switzerland

UK -

US -

Source: Information on Hong Kong, China: MPFAOther Information: Pallares-Miralles, Romero, & Whitehouse (2012)

10

As at 31 Dec 2017

With

Retirement

Protection Without

Retirement

Protection

Before Implementation of MPF System

2

3

1

3

Joined MPF schemes

73%Joined other retirement schemes(e.g. Civil Servants, ORSO)

12%

Not required to join any local retirement schemes(e.g. Domestic Helpers)

13%

Not yet joined any MPF schemes

2%

Coverage of the Employed Population by Retirement Protection in Hong Kong

11

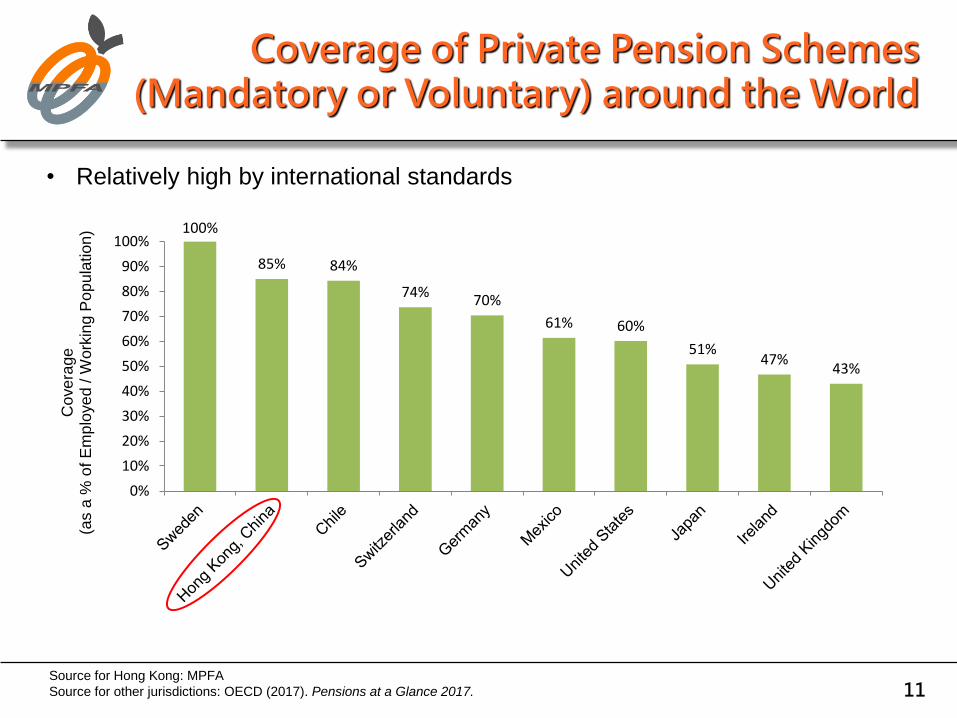

Coverage of Private Pension Schemes (Mandatory or Voluntary) around the World

100%

85% 84%

74%70%

61% 60%

51%47%

43%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cove

rage

(a

s a

% o

f E

mp

loye

d / W

ork

ing P

op

ula

tion

)

Source for Hong Kong: MPFA

Source for other jurisdictions: OECD (2017). Pensions at a Glance 2017.

• Relatively high by international standards

MPF Market

13

Framework of MPF Investments

MPF schemes (32 as of 31/12/2017) comprise a number of constituent funds (CF) (469 as of 31/12/2017)

On average each scheme has 15 CF (as of 31/12/2017)

Employers choose schemes, employees choose CF

Mandatory Provident Fund Schemes (General) Regulation sets out some rules about CF and also what CF can invest into

14

Regulation of MPF Funds (1)

Permissible investments

• High quality debt securities (e.g. BBB- by S&P, Baa3 by Moody)

• Fully-paid up shares listed on approved exchanges (e.g. HK & overseas markets like US, Japan, EU and Australia, etc.)

• Index Tracking Collective Investment Schemes

• Bank deposits

• Convertible debt securities

• Warrants (not exceeding 5% of fund assets, and not contain a put warrant except for hedging purposes)

15

Regulation of MPF Funds (2)

Permissible investments

• Futures and options (for hedging purposes; or for other purposes only if not exceed 10% of the fund asset and not result in the fund becoming leveraged)

• Currency forward contracts (for hedging and settlement purposes only)

• Other securities

fully-paid up shares listed on non-approved stock exchanges (not exceed 10% of the fund assets)

16

Regulation of MPF Funds (3)

General restrictions

• diversification of investments

• borrowing of money

• borrowing and lending of securities

• currency exposure (minimum 30% HKD)

17

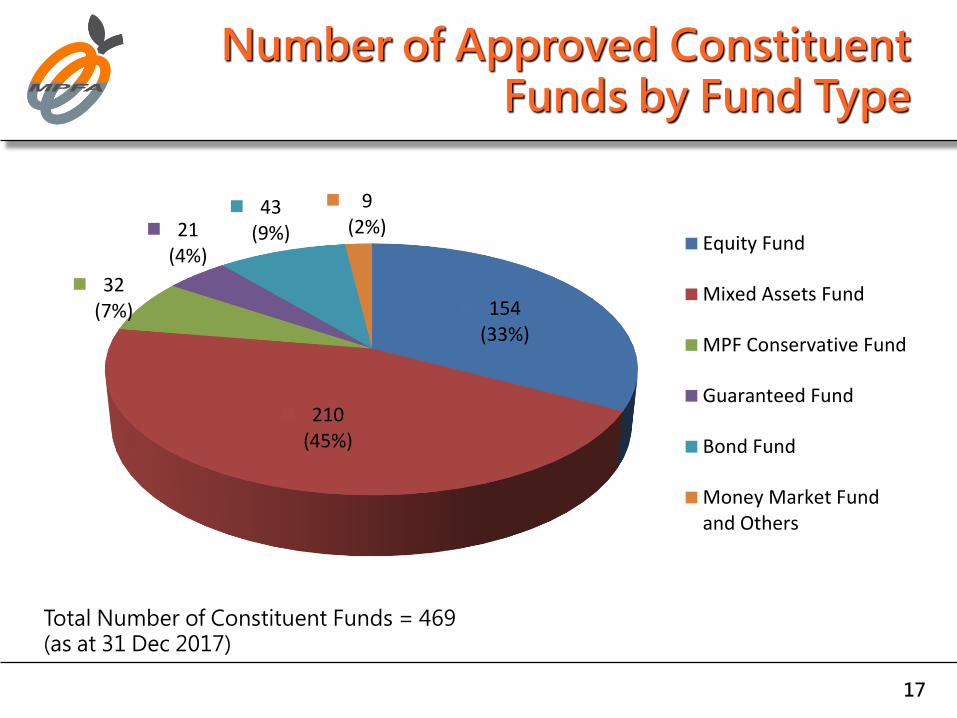

Number of Approved Constituent Funds by Fund Type

154(33%)

210(45%)

32(7%)

21(4%)

43(9%)

9(2%)

Equity Fund

Mixed Assets Fund

MPF Conservative Fund

Guaranteed Fund

Bond Fund

Money Market Fundand Others

Total Number of Constituent Funds = 469(as at 31 Dec 2017)

18

Net Asset Values of Approved Constituent Funds by Fund Type

353.9

(43%)

306.2

(37%)

76.6

(9%)

61.4

(7%)

25.3

(3%)

3.1

(<0.5%) Equity Fund

Mixed Assets Fund

MPF Conservative Fund

Guaranteed Fund

Bond Fund

Money Market Fundand Others

Total NAV = HK$826.6 billion(as at 30 Nov 2017)

($ billion)

19

Asset Allocation of Approved Constituent Funds by Asset Class

69%

18%

13%Equities

Debt Securites

Deposits & Cash

(as at 30 Sep 2017)

20

Asset Allocation of Approved Constituent Funds by Geographical Region

59%

4%

10%

15%

13% Hong Kong

Japan

Asia*

North America

Europe

(as at 30 Sep 2017)

* excluding Hong Kong and Japan

Retirement

Savings

Generated by

the MPF System

22

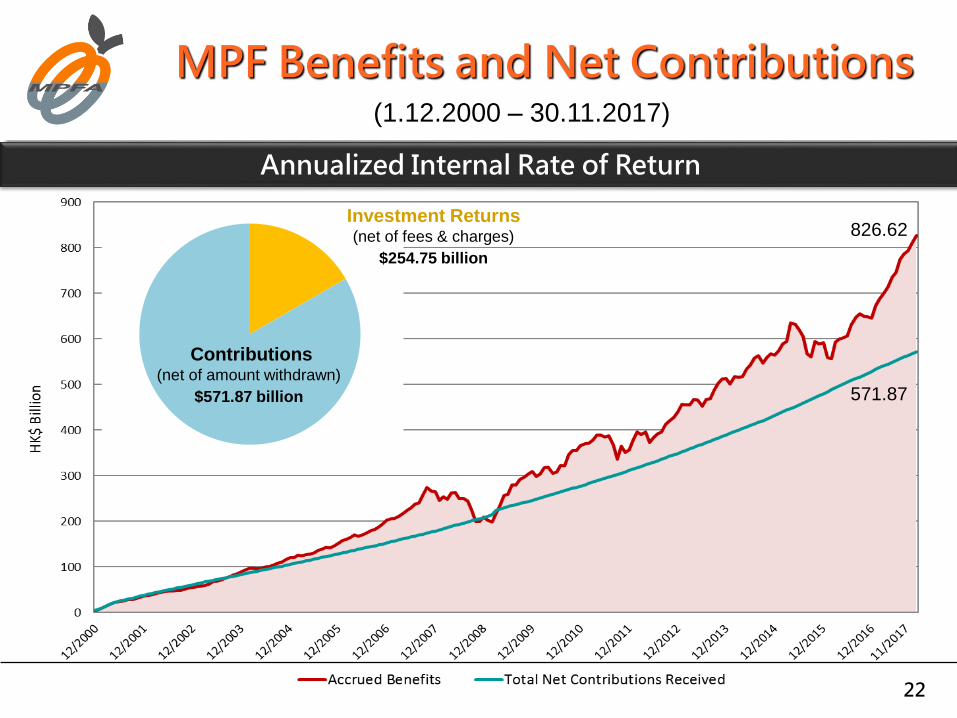

MPF Benefits and Net Contributions

Annualized Internal Rate of Return

(1.12.2000 – 30.11.2017)

Contributions(net of amount withdrawn)

$571.87 billion

Investment Returns(net of fees & charges)

$254.75 billion

826.62

571.87

23

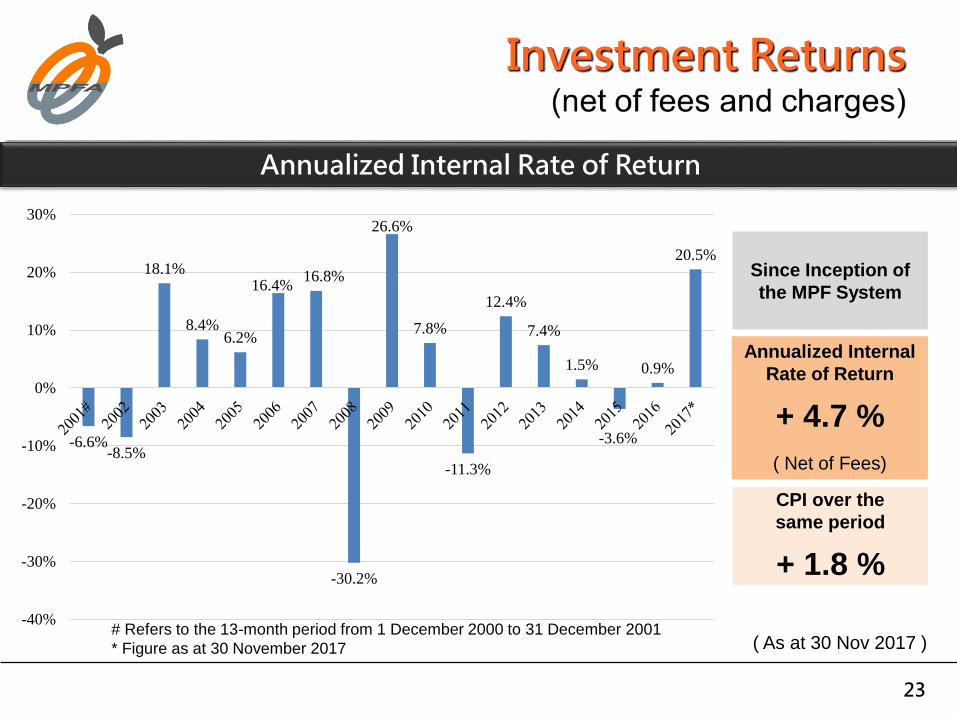

Investment Returns

Annualized Internal Rate of Return

Annualized Internal

Rate of Return

+ 4.7 %

( Net of Fees)

Since Inception of

the MPF System

CPI over the

same period

+ 1.8 %

( As at 30 Nov 2017 )

-6.6%-8.5%

18.1%

8.4%6.2%

16.4%16.8%

-30.2%

26.6%

7.8%

-11.3%

12.4%

7.4%

1.5%

-3.6%

0.9%

20.5%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

# Refers to the 13-month period from 1 December 2000 to 31 December 2001

* Figure as at 30 November 2017

24

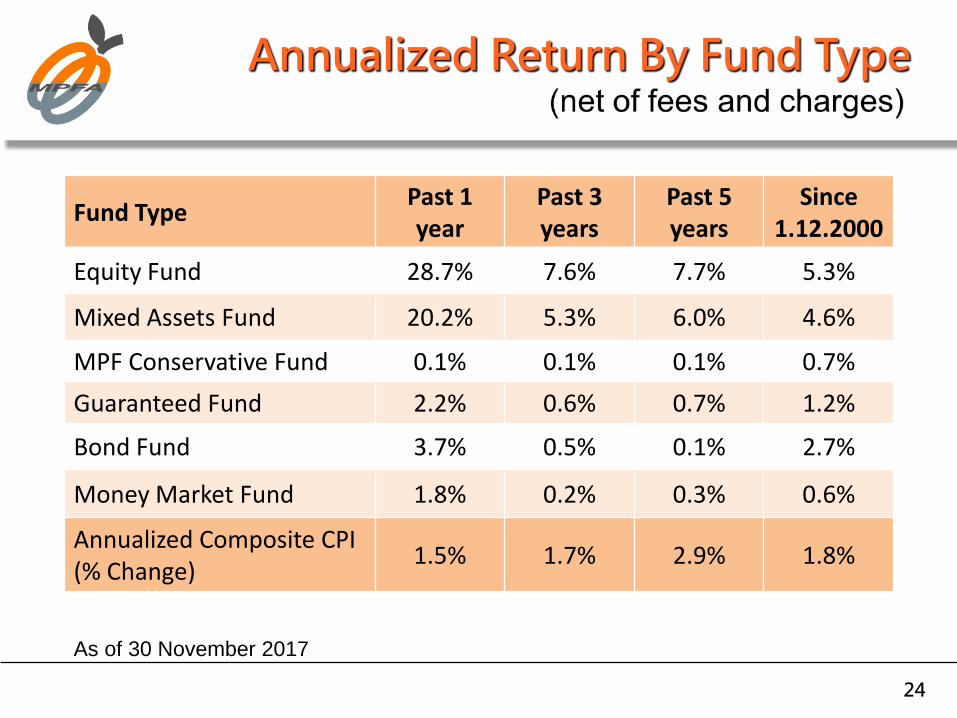

Annualized Return By Fund Type

Fund TypePast 1 year

Past 3 years

Past 5 years

Since 1.12.2000

Equity Fund 28.7% 7.6% 7.7% 5.3%

Mixed Assets Fund 20.2% 5.3% 6.0% 4.6%

MPF Conservative Fund 0.1% 0.1% 0.1% 0.7%

Guaranteed Fund 2.2% 0.6% 0.7% 1.2%

Bond Fund 3.7% 0.5% 0.1% 2.7%

Money Market Fund 1.8% 0.2% 0.3% 0.6%

Annualized Composite CPI (% Change)

1.5% 1.7% 2.9% 1.8%

As of 30 November 2017

25

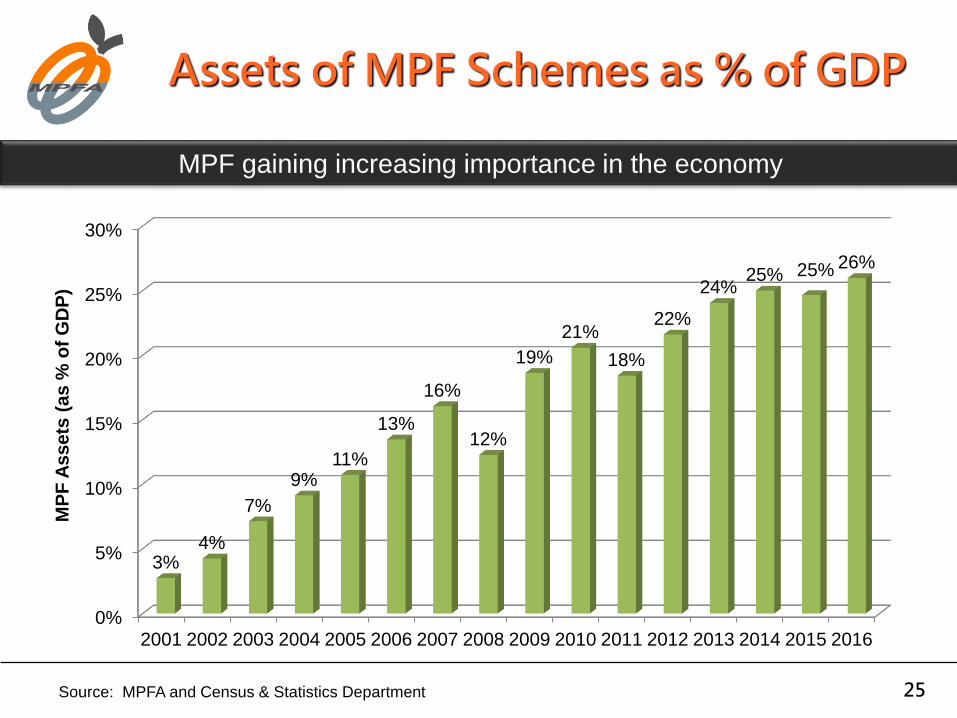

Assets of MPF Schemes as % of GDP

MPF gaining increasing importance in the economy

0%

5%

10%

15%

20%

25%

30%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

3%4%

7%

9%11%

13%

16%

12%

19%

21%

18%

22%

24%25% 25% 26%

MP

F A

ss

ets

(a

s %

of

GD

P)

Source: MPFA and Census & Statistics Department

26

Pension Fund Assets as % of GDP

Room for growth compared to OECD jurisdictions

0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

Denmark OECD Average Japan Hong Kong,China

209.0%

49.5%29.4% 26.0%

Pe

ns

ion

Fu

nd

As

se

ts(%

of

GD

P)

as

at

31

De

c 2

01

6

Source: OECD. (2017). Pension Markets in Focus <figures for jurisdictions other than Hong Kong>

MPFA and Census & Statistics Department <figure for Hong Kong>

Note: Pension fund assets of Hong Kong refer to assets of MPF schemes only; assets in other retirement

schemes are not included

27

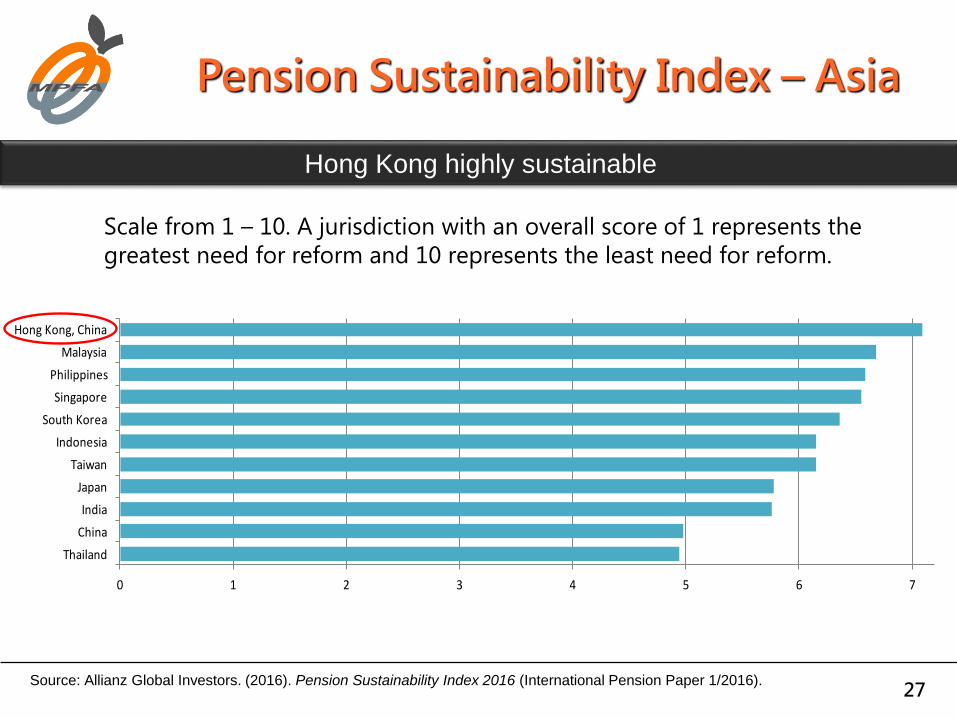

Pension Sustainability Index – Asia

Hong Kong highly sustainable

0 1 2 3 4 5 6 7

Thailand

China

India

Japan

Taiwan

Indonesia

South Korea

Singapore

Philippines

Malaysia

Hong Kong, China

Scale from 1 – 10. A jurisdiction with an overall score of 1 represents the

greatest need for reform and 10 represents the least need for reform.

Source: Allianz Global Investors. (2016). Pension Sustainability Index 2016 (International Pension Paper 1/2016).

Challenges &

Latest Reforms

of MPF System

29

Role of MPF in a multi pillar system – provision of basic retirement protection

Employment based

Mandatory contribution of 10% of employees’ relevant income (employers and employees each contribute 5%), subject to a cap (HK$30,000)

(employees earning less than HK$7,100 do not need to contribute themselves)

Relatively short contribution period (launched for only 17 years)

Coverage and Adequacy

30

Fees & Expenses – Privately managed

• FER, an indicator to measure fees, has indeed droppedfrom 2.1% (2007) to 1.56%

- As a result of MPFA urging trustees to respond to public calls,simplification of administration procedures, etc

Returns – Subject to market volatility and higher fee structures

• High equity exposure of members’ investment (69% oftotal assets as at Sep 2017)

Fees and Returns (1)

31

Fees and Returns (2)

Savings from 0.54% Reduction in Fees Over 40 Years

1,544,000

1,357,000

0

500,000

1,000,000

1,500,000

2,000,000

1 2 3 4 5 6 7 8 9 10111213141516171819202122232425262728293031323334353637383940

$

Investment Horizon / Year

FER at 1.56%

FER at 2.10%

Key Assumptions

• Gross investment return (before fees and expenses) is 5% per year.

• Each FER level remains constant throughout the 40-year investment horizon.

• Monthly salary is $15,000, which was the median salary of Hong Kong’s employed persons as at Q1 2017.

• No salary growth.

Increase in Final

Accrued Benefits:

$188,000(13.8%)

32

Latest Reforms

Default Investment Strategy (DIS)

Standardizing, Streamlining & Automating (SSA) Administration Processes

33

Default Investment Strategy (DIS) (1)

A ready-made, low fee default investment solution

Launched on 1 April 2017

34

DIS (2)

Why develop this reform measure?

Investment decision-making is difficult

Too many funds, hard to choose

Defaults different scheme to scheme

International best practices

Need for a low cost default solution

35

DIS (3)

DIS “One, Two, Three”

One ready-made, low fee investment solution

Comprised of Two constituent funds

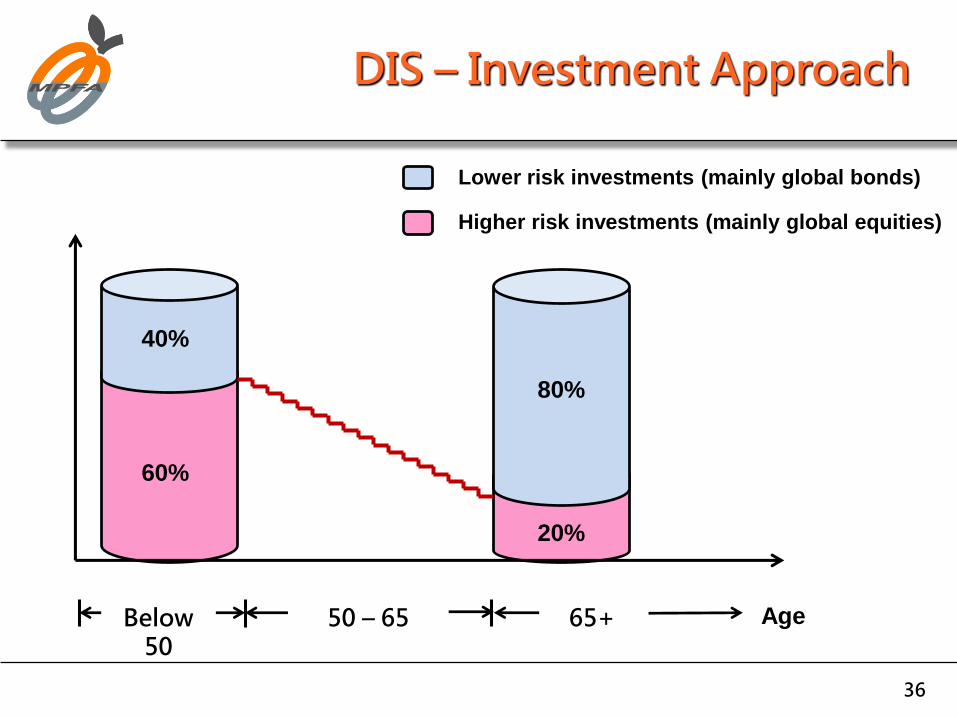

• Core Accumulation Fund (CAF) - 60% higher risk

• Age 65 Plus Fund (A65F) - 20% higher risk

Three main features

• Fee controls

Management fee : 0.75% of total asset value of fund

Recurrent out-of-pocket expenses : 0.20% of total asset value of fund

• Automatically de-risk as members approach retirement age

• Diversified investment in global market

36

DIS – Investment Approach

Lower risk investments (mainly global bonds)

Higher risk investments (mainly global equities)

≥65

40%

60%

80%

20%

Age50 – 65Below 50

65+

37

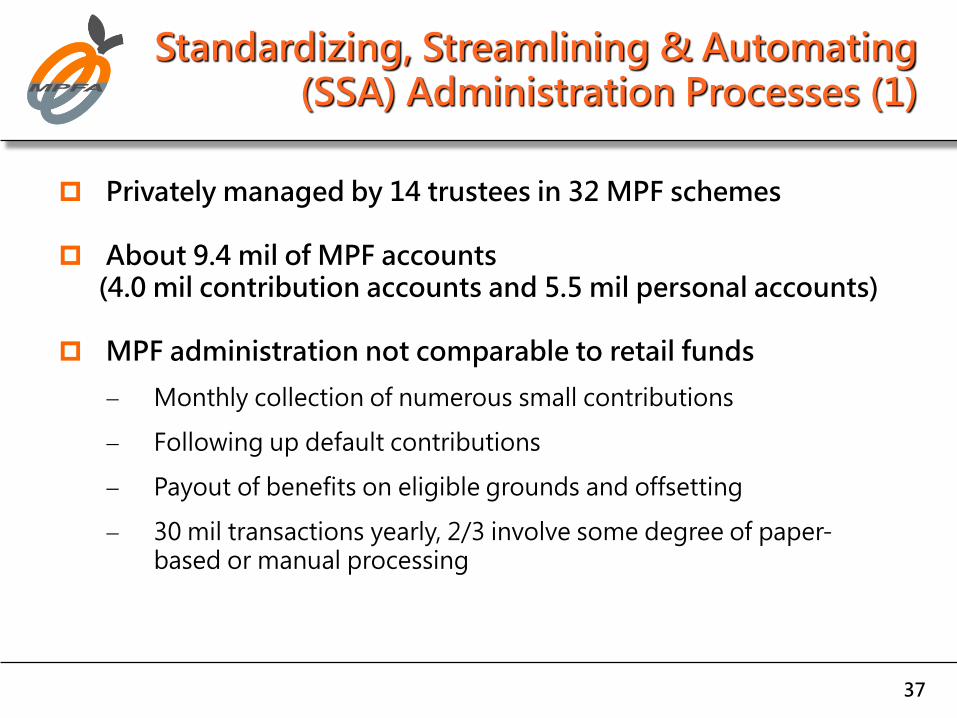

Standardizing, Streamlining & Automating (SSA) Administration Processes (1)

Privately managed by 14 trustees in 32 MPF schemes

About 9.4 mil of MPF accounts(4.0 mil contribution accounts and 5.5 mil personal accounts)

MPF administration not comparable to retail funds

Monthly collection of numerous small contributions

Following up default contributions

Payout of benefits on eligible grounds and offsetting

30 mil transactions yearly, 2/3 involve some degree of paper-based or manual processing

38

Standardizing, Streamlining & Automating (SSA) Administration Processes (2)

Objectives

1Improve

accuracy, reliability and

efficiency

2

43

Lower costs and

fees

Enhance user experience

Enable future reform

39

Key Features

Registration and unique user ID

Central database

Electronic one-stop access

Streamlined electronic processing

Standardized procedures, forms and formats

Service centres to assist less computer-literate duringtransition

Conceptual Model of eMPF

40

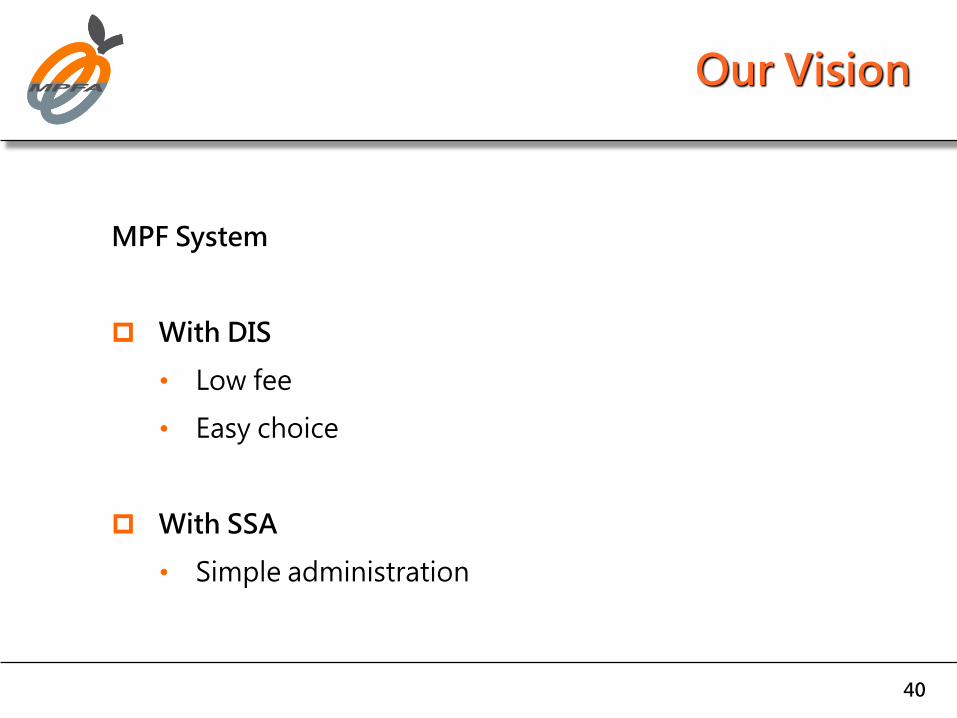

MPF System

With DIS

• Low fee

• Easy choice

With SSA

• Simple administration

Our Vision