Embed Size (px)

Citation preview

Update on the McCarran-Ferguson ActUpdate on the McCarran-Ferguson ActWilliam M. Katz, Jr.William M. Katz, Jr.

Thompson & Knight LLPThompson & Knight LLP

ABA Section of Antitrust LawABA Section of Antitrust LawInsurance Industry Committee Regional ProgramInsurance Industry Committee Regional Program

New York, NYNew York, NYMay 17, 2006May 17, 2006

ALGIERS AUSTIN DALLAS FORT WORTH HOUSTON LONDON MEXICO CITY MONTERREY NEW YORK PARIS RIO DE JANEIRO VITORIA

2

History of McCarran-Ferguson

• Paul v. Virginia, 75 U.S. (8 Wall.) 168 (1868) – Supreme Court held that Commerce Clause did not preclude state regulation of insurers

• U.S. v. South-Eastern Underwriters Ass’n, 322 U.S. 533 (1944) – Supreme Court held that insurance was interstate commerce and could be regulated under the Commerce Clause

• McCarran-Ferguson Act (1945) – Congress responded to South-Eastern Underwriters and passed a statute giving states the right to continue regulating the insurance industry

3

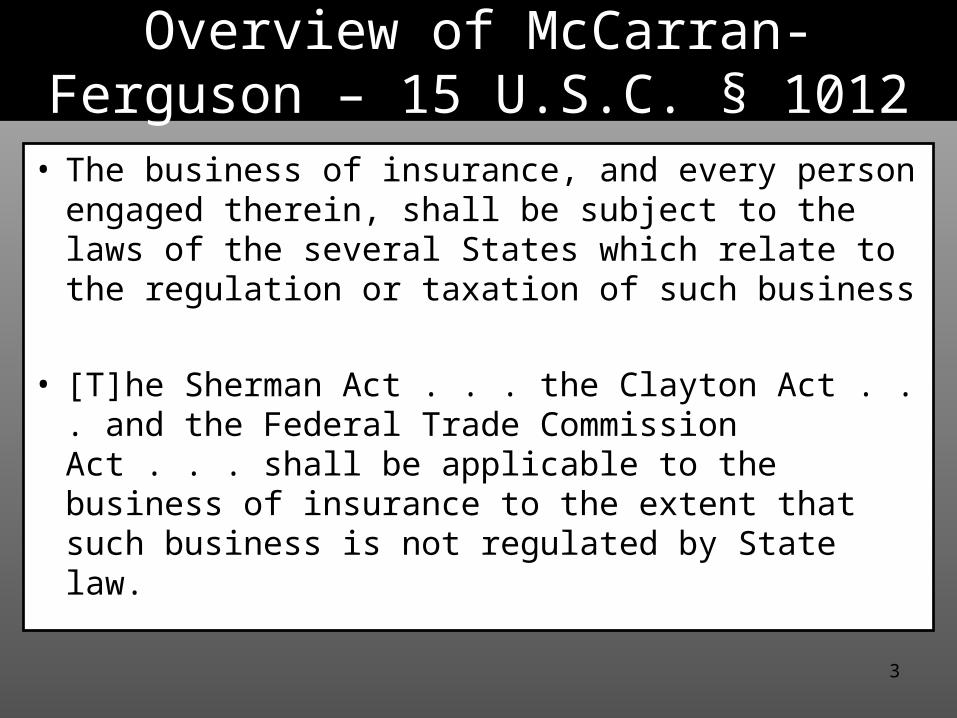

Overview of McCarran-Ferguson – 15 U.S.C. § 1012

• The business of insurance, and every person engaged therein, shall be subject to the laws of the several States which relate to the regulation or taxation of such business

• [T]he Sherman Act . . . the Clayton Act . . . and the Federal Trade Commission Act . . . shall be applicable to the business of insurance to the extent that such business is not regulated by State law.

4

Effect of McCarran-Ferguson

• Immunizes from Sherman Act challenge conduct that is: • part of the “business of insurance”; • regulated by state law; and • not a boycott of unrelated transactions

5

Business of Insurance

• Whether the practice has an effect of transferring or spreading a policyholder’s risk

• Whether the practice is an integral part of the policy relationship between insurer and insured

• Whether the practice is limited to entities within the insurance industry

Source: Union Labor Life Ins. Co. v. Pireno, 458 U.S. 119 (1982)

6

Regulated by State Law

Conduct is regulated by state law if the insurer is subject to general regulatory standards, regardless of the quality of the regulatory scheme or enforcement

7

Boycott Exception – 15 U.S.C. § 1013(b)

Nothing contained in this chapter shall render the said Sherman Act inapplicable to any agreement to boycott, coerce, or intimidate, or act of boycott, coercion, or intimidation

8

Scope of McCarran-Ferguson

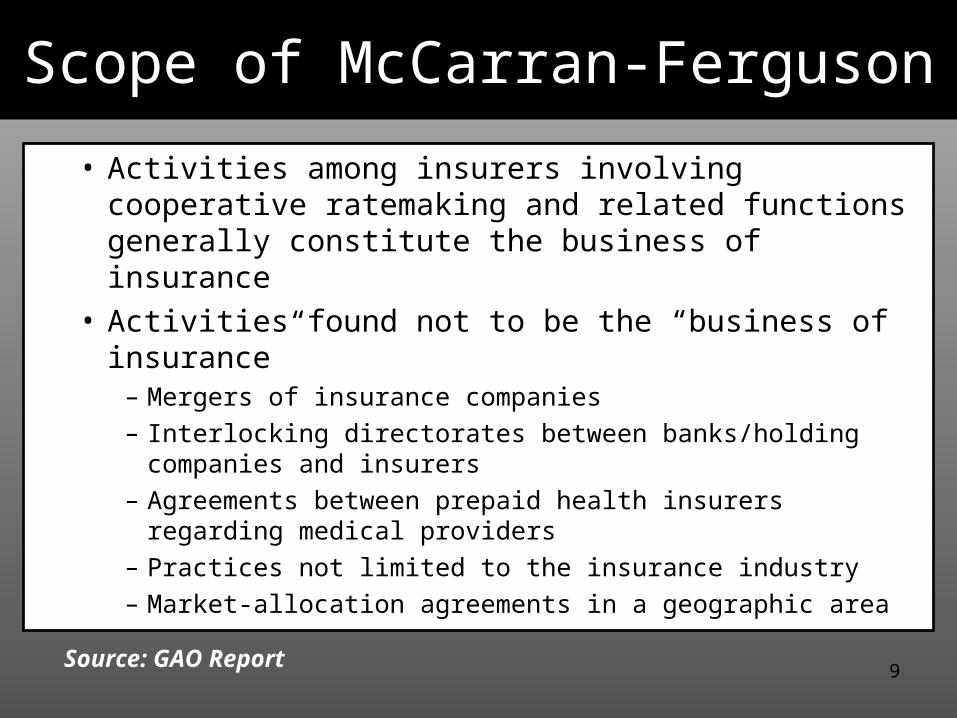

• Activities among insurers involving cooperative ratemaking and related functions generally constitute the business of insurance

• Activities found to be the “business of insurance”– Jointly setting agent commission rates

– Fixing rates pursuant to joint agreements and ratings boards

– Classifying and re-classifying risks

– Agreeing to pay damage claims based on agreed-upon labor rates

– Limiting or refusing to offer certain types of coverage

– Jointly undertaking activities to limit risks – including by revising policy language

Source: GAO Report

9

• Activities among insurers involving cooperative ratemaking and related functions generally constitute the business of insurance

• Activities found not to be the “business of insurance”– Mergers of insurance companies– Interlocking directorates between banks/holding companies and

insurers– Agreements between prepaid health insurers regarding medical

providers– Practices not limited to the insurance industry– Market-allocation agreements in a geographic area

Scope of McCarran-Ferguson

Source: GAO Report

10

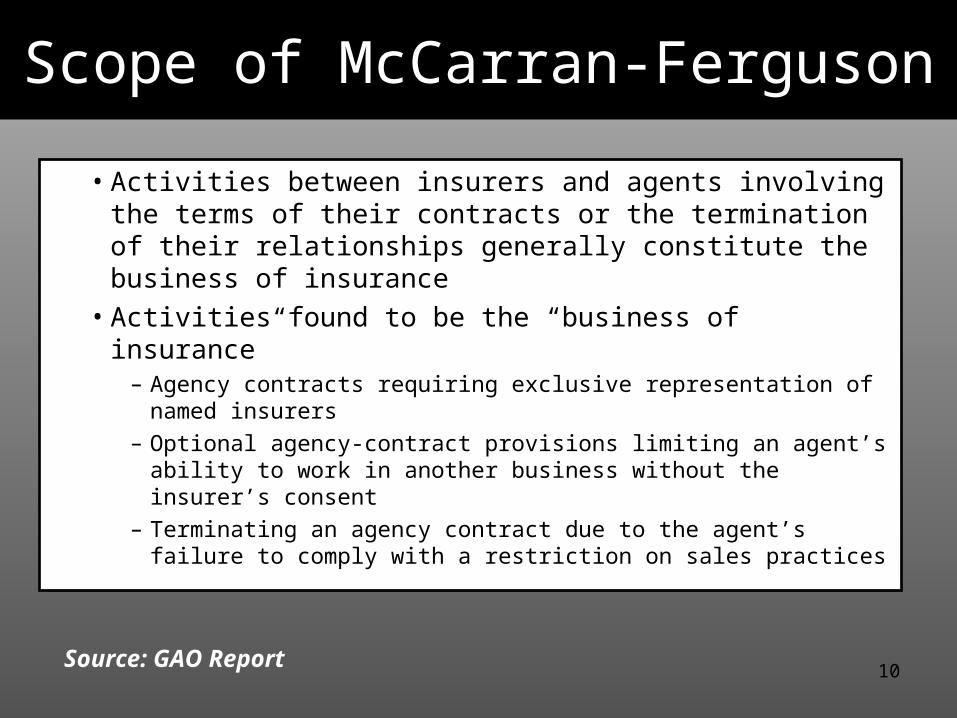

• Activities between insurers and agents involving the terms of their contracts or the termination of their relationships generally constitute the business of insurance

• Activities found to be the “business of insurance”– Agency contracts requiring exclusive representation of

named insurers– Optional agency-contract provisions limiting an agent’s ability

to work in another business without the insurer’s consent– Terminating an agency contract due to the agent’s failure to

comply with a restriction on sales practices

Scope of McCarran-Ferguson

Source: GAO Report

11

• Activities between insurers and agents involving the terms of their contracts or the termination of their relationships generally constitute the business of insurance

• Activities found not to be the “business of insurance”– Terminating an agent who handled insurance contracts and

securities because the limitation on securities wasn’t the business of insurance

– Inducing agents not to sell another insurer’s products– Inducing agents to use or misappropriate another insurer’s trade

secrets– Pirating a general agent’s subagents

Scope of McCarran-Ferguson

Source: GAO Report

12

• Activities involving the relationship between insurer and insured constitute the business of insurance, especially when the activity involves risk-spreading and primarily impacts competition in the insurance industry

• Activities found to be the “business of insurance”– Certain types of tying – like an auto insurer’s requirement that

insured join a certain auto club– Refusing to offer a health insurance policy that did not include a

spouse– Agreeing to offer medical malpractice coverage only to members

of a county medical association– Setting terms and conditions of the insurance policy

Scope of McCarran-Ferguson

Source: GAO Report

13

• Activities involving the relationship between insurer and insured constitute the business of insurance, especially when the activity involves risk-spreading and primarily impacts competition in the insurance industry

• Activities found not to be the “business of insurance”– Refusing to pay for services rendered by psychologists unless

billed through a physician – the decision on who to pay isn’t the business of insurance

– Conspiracy between physician and malpractice insurer to cancel a competing physician’s coverage

Scope of McCarran-Ferguson

Source: GAO Report

14

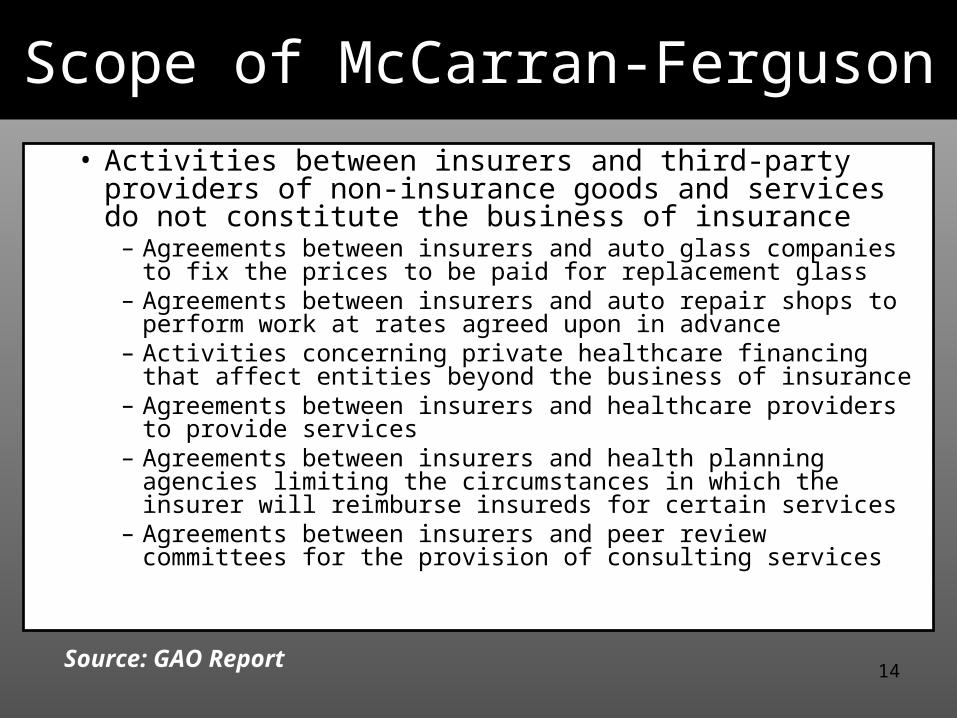

• Activities between insurers and third-party providers of non-insurance goods and services do not constitute the business of insurance

– Agreements between insurers and auto glass companies to fix the prices to be paid for replacement glass

– Agreements between insurers and auto repair shops to perform work at rates agreed upon in advance

– Activities concerning private healthcare financing that affect entities beyond the business of insurance

– Agreements between insurers and healthcare providers to provide services

– Agreements between insurers and health planning agencies limiting the circumstances in which the insurer will reimburse insureds for certain services

– Agreements between insurers and peer review committees for the provision of consulting services

Scope of McCarran-Ferguson

Source: GAO Report

15

Update in the Courts

16

Gilchrist v. State Farm,390 F.2d 1327 (11th Cir. 2004)

• Filed in the Northern District of Florida and appealed to the Eleventh Circuit under Rule 23(f)

• Plaintiffs alleged that Defendants conspired to limit insurance coverage by using non-OEM parts – didn’t allege direct conspiracy to fix rates or premiums, but instead alleged impact on rates due to non-price conspiracy for non-OEM parts

• District Court denied Defendants’ motion to dismiss based on McCarran-Ferguson – certified under 28 U.S.C. § 1292(b), but Eleventh Circuit declined appeal

• District Court then certified a nationwide class of approximately 70 million policyholders

17

Gilchrist v. State Farm,390 F.2d 1327 (11th Cir. 2004) (cont’d)• Eleventh Circuit granted Defendants petition under

Rule 23(f), and after oral argument, solicited additional briefing on McCarran-Ferguson

• Eleventh Circuit dismissed the case, finding that the federal courts lacked subject-matter jurisdiction based on McCarran-Ferguson– Business of insurance was met because Plaintiffs’ claims

attacked rate-making and the terms of the insurance contract

– No boycott because the alleged refusal to deal was in the underlying transaction (refusing to buy or provide OEM parts), rather than in a collateral transaction

18

Perez v. State Farm

• Filed on March 14, 2006, in the Northern District of California by one of the same law firms as Gilchrist

• Similar to Gilchrist because it challenges the use of non-OEM parts by insurers

• Claims asserted are under California’s Unfair Competition Law and the Cartwright Act, California’s antitrust statute

19

In re Insurance BrokerageAntitrust Litigation

• Grew out of investigation by New York Attorney General

• Several private cases consolidated in the District of New Jersey in February 2005

• Complaint alleges that 78 commercial insurers and 37 brokers colluded to: – rig bids; – submit false quotes; – allocate customers and markets; – adopt secret contingent commissions deals

20

In re Insurance BrokerageAntitrust Litigation (cont’d)

• Does McCarran-Ferguson apply?– Business of Insurance

• Defendants – Plaintiffs’ allegations concern the business of insurance

– Steering business to insurers in exchange for fees– Manipulating bids on insurance contracts– Allocating customers among insurers

• Plaintiffs disagree that McCarran-Ferguson applies– Allocating customers and rigging bids doesn’t involve spreading

policyholder risk– Anticompetitive agreements between insurers and brokers do not

directly relate to the insurer-insured relationship– Anticompetitive conduct having an effect on premium levels is not

the same as cooperative ratemaking, which is covered by McCarran-Ferguson

21

In re Insurance BrokerageAntitrust Litigation (cont’d)

– Regulated by State Law• Defendants

– All 50 states and DC regulate the business of insurance and unfair trade practices

– Many states have investigated and sued over the conduct at issue

• Plaintiffs– State regulation is ineffective– States don’t regulate contingent commissions, bid rigging,

and market allocations

22

In re Insurance BrokerageAntitrust Litigation (cont’d)

– Boycott Exception• Defendants

– Conspiracy to charge higher price isn’t a boycott– No refusal to deal on collateral transaction– In any event, the alleged refusal to deal was part of a bid-

rigging conspiracy

• Plaintiffs– Brokers refused to deal with insurers unless insurers entered

into broader agreements related to entire lines of business– Brokers threatened to cut off all business to insurers to

induce them into entering into the contingent-commission agreement

23

State of Florida v. Marsh

• Filed on March 14, 2006, by Florida’s AG and Department of Financial Services in Florida state court

• Florida is suing Marsh and its affiliates under Florida’s antitrust and RICO statutes on behalf of the State of Florida and Florida insureds

• Marsh claims that the claims asserted were – “cut and pasted” from a 2004 lawsuit filed by New York,

and – released as part of its earlier $850,000,000 settlement to

eligible policyholders, including those in Florida

24

Update in Congress

• Carter McDowell – Spring Meeting– No legislation in 2006 – Congress generally legislates in

odd-numbered years and oversees in even-numbered years due to election cycle – Look for legislation in 2007

– Oxley is retiring – insurance legislation is a potential issue for the next chair of the House Financial Services Committee

– Insurance is one of three legs of U.S. financial services – banking and securities are the others – and insurance is where the U.S. is least competitive on a global basis

– Need to have a federal regulator – raises political issues about the size of government and bureaucracy

– Needs to be off-budget and self-funded

25

Update in Congress (cont’d)

• National Insurance Act of 2006– Introduced by Senators Sununu and Johnson in

early April 2006– Optional federal chartering – would repeal

McCarran for those companies seeking a federal charter

– Regulator would be within Treasury Department– Hearing was scheduled for April 25, 2006– Rescheduled for?

26

Update-Antitrust Modernization Commission

• AMC conducted a hearing on December 1, 2005, on statutory immunities and exemptions– Very little discussion of McCarran-Ferguson– Mentioned only a few times and no real

substantive discussion

• AMC’s recommendation to Congress is due in April 2007

27

Update-Antitrust Modernization Commission (cont’d)

• Comments submitted to AMC– Three favored continuation of McCarran-Ferguson

• Property Casualty Insurers Association of America• NCCI Holdings and National Council on Compensation, Inc.• American Insurance Association

– Three favored repeal of McCarran-Ferguson• New York Attorney General’s Office• Vehicle Information Services, Inc.• Professor Peter Carstensen

– ABA Section of Antitrust Law• Comment discusses the 1989 ABA Policy regarding McCarran-

Ferguson, which favors repeal and replacement with certain limited safe-harbors for demonstrably procompetitive conduct

• Comments analyzes some of the literature addressing the pros and cons of repeal

Update on the McCarran-Ferguson ActWilliam M. Katz, Jr.

Thompson & Knight LLP

ABA Section of Antitrust LawInsurance Industry Committee Regional Program

New York, NYMay 17, 2006

ALGIERS AUSTIN DALLAS FORT WORTH HOUSTON LONDON MEXICO CITY MONTERREY NEW YORK PARIS RIO DE JANEIRO VITORIA

![Ariel Katz Associate Professor University of Toronto, Faculty ......[P]atent and antitrust policies are both relevant in determining the "scope of the patent monopoly" — and consequently](https://img.dokumen.tips/doc/110x75/61330b39dfd10f4dd73ad5a9/ariel-katz-associate-professor-university-of-toronto-faculty-patent-and.jpg)