Embed Size (px)

Citation preview

University of Nigeria Research Publications

UDOGU, Charles Eberecukwu

Aut

hor

PG/MBA/86/4181

Title

“Incidence of Informal Financial Organisations in some Selected Institutions

in Enugu – Anamabra State”

Facu

lty

Business Administration

Dep

artm

ent

Banking and Finance

Dat

e

October, 1987

Sign

atur

e

" I N C I D E N C E O F INFORPIAL F I N ~ L ~ T C I A L

ORGANISATIONS I N SOME S E L E C T E D I N S T -

I T U T I O N S I N ENUGU - ANAMABRA S T A T E "

UD OGU , CHARLES EBERECHJKWU

(PG - MBA - 86 - 4181)

I DEPfiRTMENT O F FINJLNCE

FACULTY OF B U S I N E S S ~ ~ D I Y I W I S T W L T I ON 1 U N I V E R S I T Y O F N I G E R I A

ENUGU CliMPUS, @J

0 i3

O C T O B m e 1987

I I I N C I D E N C E O F INFORMAL F I N A N C I A L

ORGANISAT1 ONS I N SOME S E L E C T E D I N S T I T U T I O N S

I N ENUGU - ANAMBRA S T A T E

B E I N G h T H E S I S REPORT PRESENTED

T O

T H E DEPARTMENT OF F I N A N C E

FACULTY OF B U S I N E S S I I D M I N I S T W L T I O N

U N I V E R S I T Y O F N I G E R I A b

ENUGU CAPPUS

BY

UDOGU , CHIARLES EBERECI-IUKWU

( P C - PlBA - 86 - 4181)

I N P A R T I A L FULFILMENT OF T H E REQUIREMENTS F O R T H E AWARD O F T H E DEGREELWLSTER O F B U S I N E S S PLDPIINISTRTITION (MBA) I N F I N ~ L N C E

S U P E R V I S O R :

DERN , FLCULTY O F B U S I N E S S L D M I N I S T R A T I ON

U N I V E R S I T Y O F N I G E R I A

ENUGU Cf3lPUS.

( i>

C E R T I F I C A T I O N

I CERTIFY THAT T H I S WORK CARRIED OUT

BY UDOGU , CHARLES EBERECHUKWU I N T H E DEPPLRTMENT ' OF b

F I N L N C E , UNIVERSITY OF N I G E R I A , ENUGU CAMPUS

UNDER NY GUIDANCE AND S U P E R V I S I O N *

FACULTY O F B U S I N E S S ADMINISTRRTION)

(ii)

D E D I C A T I O N - - - - - - - - - I - - - - - - - - =

T H I S WORK IS Df lDIChTED T O T H E GREEN

MENORY OF MY BELOVED F ~ L T H E R - W I T E MR. FRANC IS OGB ONNAYA UDOGU

WHO S L E P T I N T H E LORD SOME

TWFJ\JTY-THREE YERRS AGO

fipXpri, m y YGUR LOVING SOUL CONTIWE

T O R E S T I N P E R F E C T PEACE T I L L WE

MEET AGAIN T O Pl iRT NO MORE"

MY h ighes t apprec ia t ion goes t o the Almighty

~ o d and Father who no t only kept me a l i v e t o t h i s

day but also made the accomplishment of t h i s work,

once again, possible . ItMay a l l p ra i ses and a l l

thanksgiving be every moment HISll.

i ow ever, God, through t he ins t rumenta l i ty of

some ind iv idua l persons c a r r i e s o u t is marvelous

deeds. I n this p a r t i c u l a r case of mine, ~ o d has

used t he following ind iv idua l s , ( t o whom I own my

apprc ia t ions a l so ) t o acco~~ip l i sh t he work.

Foremost among these ind iv idua l persons i s my

p ro j ec t mentor (who is a l s o t h e Dean of t h e Faculty

of Business fldministration) professor Francis 0,

okafor. I n f a c t , without him, I doubt i f I would

have been ab le t o s e t t l e on a top ic t o wri te . I

hereby express my profound apprec ia t ion t o him no t only

f o r accepting t o supervise me, but a l s o squeezing out

time off h i s t i g h t programme t o o f f e r h i s c r i t i c i sms

during the course cf my study.

In l i k e manner, I wish t o show my apprec ia t ion t o

t h e co-ordinator of t h e pos t Graduate School, M r .

J.A. Ezeh who has worked r e l e n t l e s s l y very hard t o

s e e t o i t t h a t t he programme i s accomplished a s scheduled,

MY a p p r e c i a t i o n goes a l s o t o my u n c l e an s sponsor

Chief Pgthony A. o b i who took up t h e cha l l enge o f

s e e i n g me through a l l t h e s e y e a r s of academic

p u r s u i t s and t o him I s i n g f ~ o d Loves a c h e e r f u l Giver f

The l i s t w i l l b e incomple te i f 1 f a i l t o mention

a l l t h o s e who i n one way o r t h e o t h e r he lped me d u r i n g

my d a t a c o l l e c t i o n d r i v e s e s p e c i a l l y a l l t h o s e who

completed my q u e s t i o n n a i r e , and t h o s e who g r a n t e d me b

f r i e n d l y aud ience d u r i n g i n t e r v i e w s e s p e c i a l l y

Messrs ~ g w i n ( o f Eag le S t a r D a i l y S a v i n g s ) , o l i ( o f

M i n i s t r y of F inance and Economic p l a n n i n g ) , ~ b a (o f

M i n i s t r y of works and ~ o u s i n g ) , Sam (of Im), ~ b o (of

ogbe te ~ a r k e t ) , Ezeani ( o f A r i a Market) and MrS

Egwele (o f U,N.E.C.), To a l l t h e s e and o t h e r s

unmentioned, I show my g r a t i t u d u .

I a l s o thank a l l my f r i e n d s and c l a s sma te s ,

e s p e c i a l l y my roommate (pp-. Cha r l e s ~ g o l u m ) , Messrs

p e t e r fimah and ~ i v i n u s onuh f o r a l l t h e i r u s e f u l and

c o n s t r u c t i v e c r i t i c i s m s d u r i n g t h e course t h e s t u d y . F i n a l l y , my a p p r e c i a t i o n a l s o goes t o t h e Typ1.S

who saw t o it th3.t t h e work a s i t is produced is typed

w i th minimum of e r r o r s , and t h i s is no l e s s a pe r son

t h a n Mrs. B.U. wogbo .

However, t h e r e s p o n s i b i l i t y f o r t h e q u a l i t y of

t h e work i n terms of accuracy and in format ion con ten t

e n t i r e l y mine . t h e r e f o r e acknowledge a l l p r a i s e s

and c r i t i c i s m s t h a t fo l low t h e e n t i r e work as produced.

UDOGU , CHARLES EBERECHUKWU

UNIVERSITY OF N I G E R I A

ENUGU ChMF'US .

OCTOBER, 1987.

............................... C e r t i f i c a t i o n i

Dedication ......................OD........, ii

.................. L i s t of ~ a b l e s and Figures i x

CIUiPTER ONE: INTRODUCTION . . . . . . . . . . .~ . .~.~ 1 D

1 Basic I s sues ................. I Statement of Problem ............... 1.2. s tatement of objec t ives 2

............... 'l.4 s ign i f i c ance of s tudy 4

1.5 nef i n i t i o n of ~ e r m s ............... 5

1 . 6 imitations of t he s tudy .............. 7

2 p1txouuction ........................ 9

2.2. The Financia l ~ n f r a s t r u c t u r e - An overview^^

......... 2.3, he Informal ~ i n a n c i a l s e c t o r 17

2.4. ~ e a s o n s f o r continued co-existence ..... 21

2.5. Types of inform31 Financia l organisat ions 28

2.6, objec t ives and funct ions of These 35 organisa t ions ....d....O...............

2.7. organisa t ion and ~anagenen t : ........... 38

( v i i )

...... CW;PTER TIBEE: METIiOD O F RESURCH ; : ; 40

3.1. ~ e t e r m i n a t i o n of popu la t ion .......... 40

.......... 3.2. ne te rmina t ion of sample s i z e 40

...................... 3.3. Data c o l l e c t i o n 42

3.3.1 Sources of Data ....................... 42

. primary Data ..O.... .............O.. 42

. secondary Data ................O...... 43

3 - 4 . InFORP'IilL FINANCIAL ORGhNISBTIONS STUDIES 43 b . .................... 3 .5 i i na lys i s and Tes t s 43

3.5.2 T e s t s t a t i s t i c s ....................... 44

3.6 ~ e v e l o f s i g n i f i c a n c e ................. 46

3.7 Decis ion c r i t e r i o n 46

CH>LPTER FOUR: EXPL'iNATORY NOTES ON THE 47

OPER!LTI ONS OF THE INFC'RYU~L ORGliNISATI OIVS 47

STUDIES .................................... .................... 4.1. ~ a i l y c e n t r i b u t i o n 47

................. 4.2. chr i s tmas T h r i f t fund 55

4.3. I S U S U ................................ 63

CI-L'J'TER FIVE; PRESFA!TiLTI ObT ~ L L J iLNALYSIS OF 66

Dl'L'i'A: i:m TEST OF HYPOTHESES ........... 66

5.1 . p r e s e n t a t i o n and m a l y s i s of Data . . 66

.................... 5.2. T e s t of Hypotheses; 66

( v i i i )

PAGE

5.2.7. Tes t of Hypothesis 1 . . , . . . . . . . . . . . . . 5.2.2. Tes t of ~ y p o t h e s i s 2 ............,... 5.2.3. T e s t of ~ y p o t h e s i s 3 . . . . . . . . . . . . . . . .

CXLPTZR SIX: RZSE.RCH DEDUCTIONS,

6.1, ~ e s e a r c h Deductions ........,.....,... 6.2 necommendations .............. O . D . .

6.4, Areas f o r f u r t h e r nesearch . . . . . . . . . . . .

I Advert isement bLid

2 a Conversion of Daily Income t o 1Jlnual Incomes

3. Conversion of income rcmges t o Absolute va lues

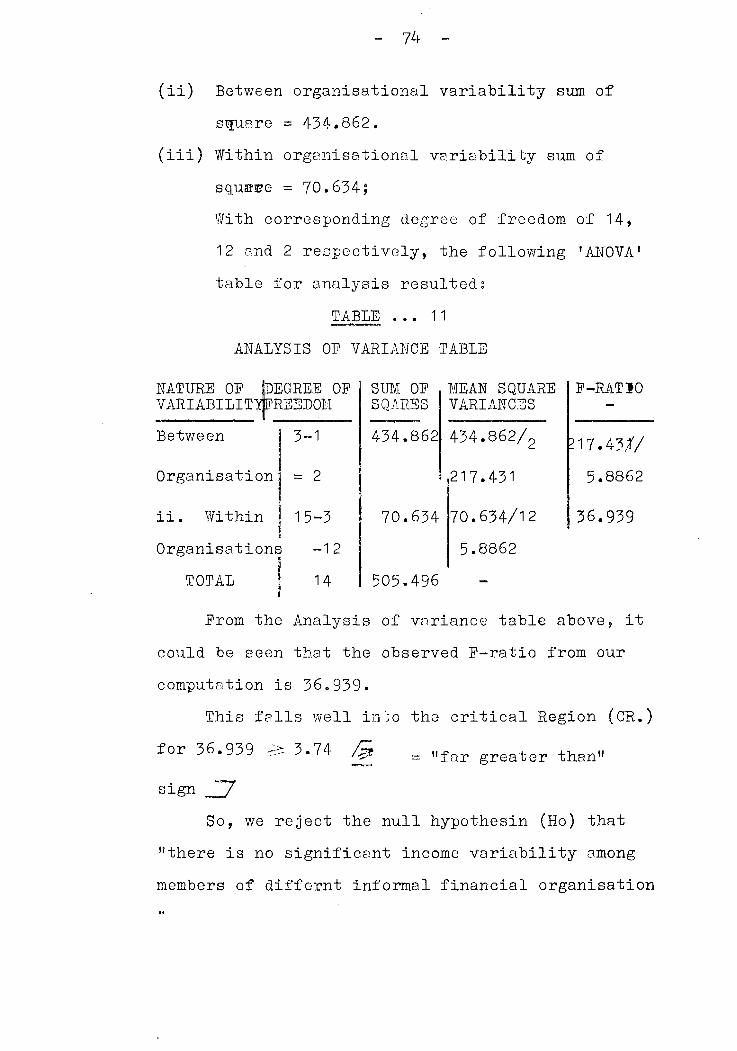

4. computat ion of p r a t i o sum of squa re s

5. computat ion of Regress ion parameters I

7. Regress ing Rate of Returns 011 :?mo~:nts

c o n t r i b u t e d i n Christmas m n d T h r i f t

8. Q u e s t i o n n a i r e

9. Bib l iography

v i t a

( i x >

LIST OF TliBLES AND FIGURES

1 . Da i ly c o n t r i b u t i o n

2. A c t i v i t y F igures

3 . ~ s u s u D i s t r i b u t i o n

4. Ques t ionna i re l ~ c c o u n t i n g

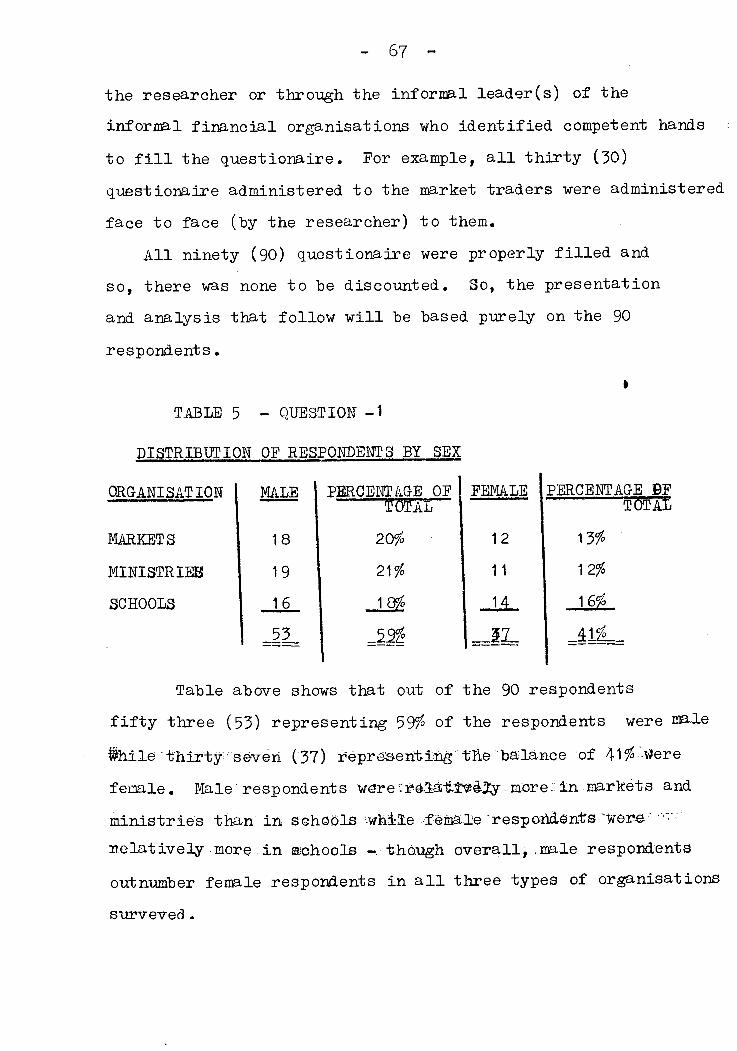

5 . D i s t r i b u t i o n of Respondents by Sex

6. D i s t r i b u t i o n of ~ e s p o n d e n t s by Marital s t a t u s

7. Tflcome D i s t r i b u t i o n of ~ e s p o n d e n t s

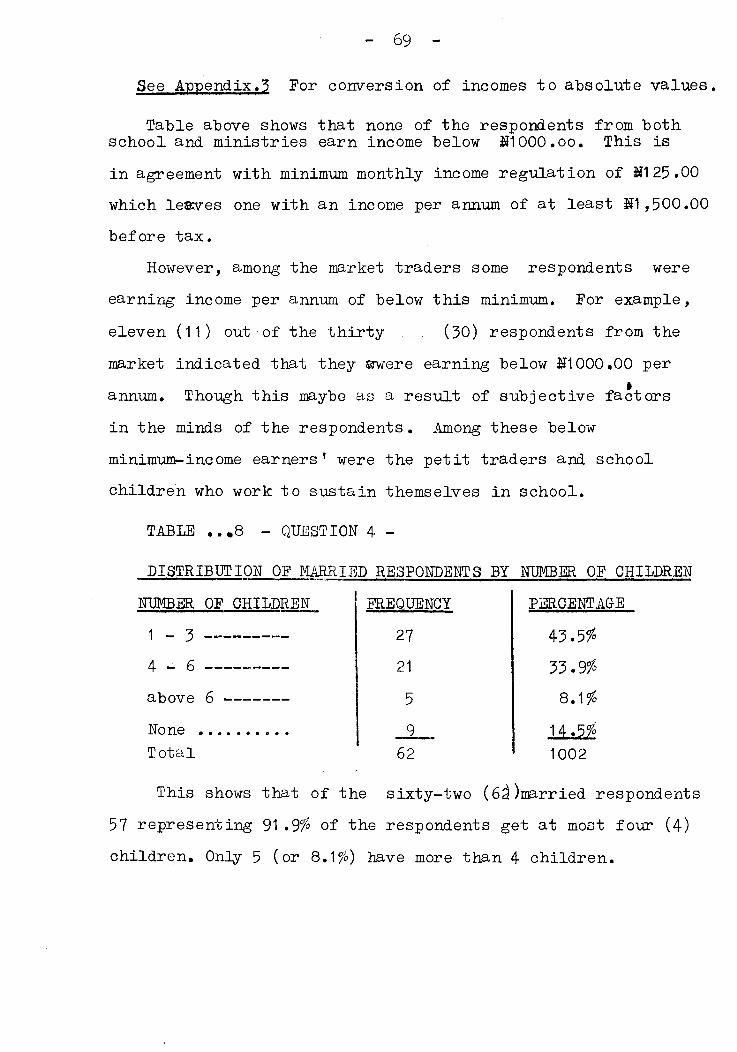

8. D i s t r i b u t i o n of Married Respondents by

pqember of Chi ldren

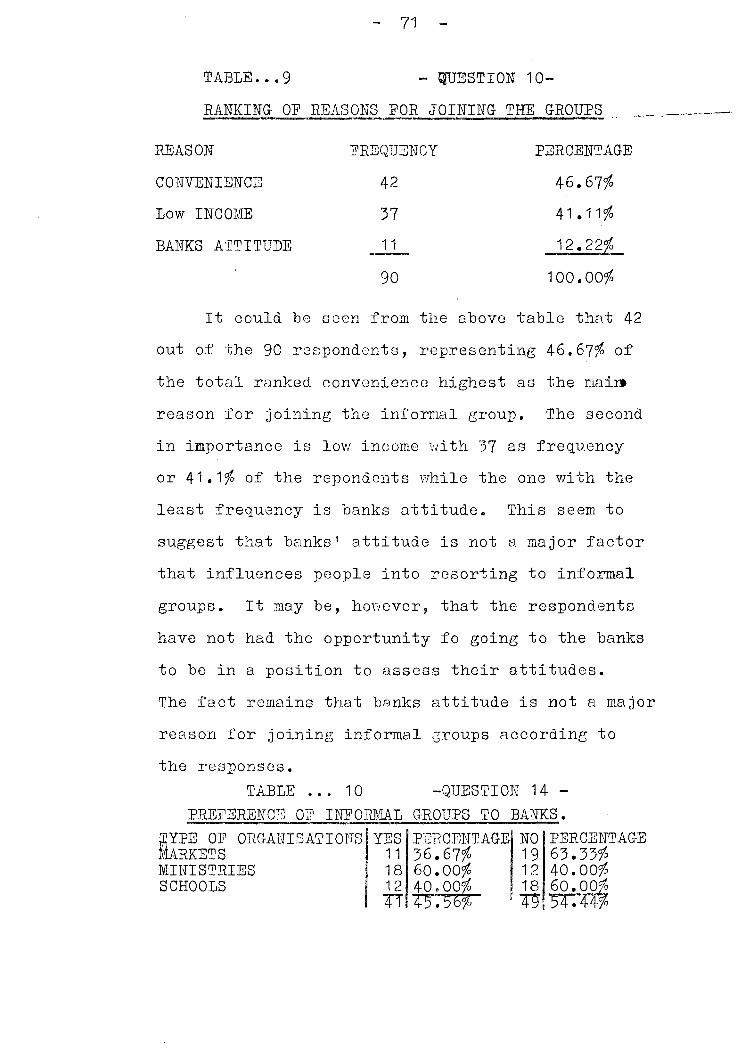

9. Ranking of reasons f o r j o i n i n g t h e Groups

10. p re fe rence of In formal Groups t o ERnks

11. Analysis of va r i ance Table

F I GI JRES :

1. Funds Trans fe r Function

3. Formal of Emergency Withdrawal ca rd .

4. c r i t i c a l Region f o r hypothes i s 1

5. c r i t i c a l Region f o r hypothes i s 2

6 c r i t i c a l Region f o r hypothes i s 3

7, c r i t i c a l Region f o r hypothes i s 4

~ g s z n ~ c z

The t r a d i t i o n a l f i n a n c i a l i n s t i t i o n s , otherwise

ca l l ed t h e informal f i n a n c i a l organisa t ions , which

form the theme of t h i s work, have been found t o be

p laying a major r o l e i n t he savings mobil izat ion e f f o r t s

~f v a r i ~ u s economic u n i t s , i n s p i t e of t h e exis tence

of t h e m ~ d e r n sophis t ica ted f i n a n c i a l i n s t i t u t i o n s

l i k e banks.

~t i s su rp r i s i ng t o f i nd t h a t even i n t h e b

urban cen t res , where such informal f i n a n c i a l

arrangements should normally be looked down upon as

being crude and p r imi t ive , these i n s t i t u t i o n s s t i l l

survive.

Three groups of i n s t i t u t i o n s were se lec ted i n

JgIUgU t o prove the exis tence o r otherwise of these

organisa t ions and a l s o t o f i n d out, where they e x i s t ,

t h e forms of t h e i r presence and t h e i r modes of

organisa t ion and ope ra t im .

prel iminary inves t iga t ions through an i n i t i a l

extensive interview with indiv iduals fr3m among t he

th ree groups of i n s t i t u t i o n s se lec ted

Viz: Markets, Min i s t r i e s and schools - revealed

t h a t these informal organisat ions ac tua l l y ex i s t .

fL c lo se r study cf t he i n s t i t u t i o n s revealed t h a t

these informal f i n a n c i a l groups e x i s t along organisa-

t i o n a l l i n e s . I n t h e markets, which a r e dominated by market t r a d e r s whose income s t reams come on d a i l y

b a s i s , informal f i n a n c i a l o rgan i sa t ions t h a t r e l y on

d a i l y c o n t r i b u t i o n e x i s t . I n t h e M i n i s t r i e s and

Higher ~ n s t i t u t i o n s , workers tend t o o rgan i se t h e i r

own groups on monthly payment b a s i s n a i n l y because

t h e i r remunerations a r e pa id by t h e month.

o u t of t h e 90 respondents t o t h e q u e s t i o n n a i r e ,

i t was found t h a t 53(59%) were men and 37(41%)

were women. This seems t o sugges t t h a t men involve 8

themselves more i n sav ings t h a n women. Again, ou t of

t h e 90 respondents , 62(69%) were married men and

women. This f a c t and t h e f a c t t h a t men a r e more may

combine t o sugges t t h a t t h e need t o save has a

p o s i t i v e r e l a t i o n s h i p wi th f ami ly r e s p o n s i b i l i t i e s .

This i s moreso, when we look a t t h e uses i n t o which

t h e s e sav ings a r e put . Some of t h e uses are:-

paying of f i x e d o b l i g a t i o n s l i k e s choo l f e e s , house

r e n t s and o t h e r b i l l s , and t h e purchase of f i xed

a s s e t s l i k e home fu rn i sh ings .

Convenience and low income were t h e two f a c t o r s

ranked h i g h e s t as major exp lana t ions f o r involvement

i n i n fo rma l f i n a n c i a l o rgan i sa t ions . The a t t i t u d e of

banks was minimally mentioned - may be because t h e

respondents never had access t o banks o r t h a t they s t i l l

recognize t h e unique r o l e s t h a t banks can play.

( x i i )

There were s i g n i f i c a n t income v a r i a b i l i t y among

members of v a r i o u s in formal f i n a n c i a l groups. The .

d a i l y c o n t r i b u t o r s i n t h e market p l a c e s were mai ly

people of ve ry low income. 8003 of t h e market respondents

were below pq2000.00 p e r annum income, whi le over 60%

of t h e m i n i s t r y and schoo l workers i n ~ s u s u and

ch r i s tmas t h r i f t funds were i n incomes p e r annum

of over p42000.00

Though t h e s e respondents belong t o one form of

i n fo rma l group o r t h e o t h e r , m a j o r i t y o f them s t i h l

do no t p r e f e r i n fo rma l groups t o ~anks.

in ally, t h e s e i n fo rma l groups have t h e i r own

p e c u l i a r i t i e s , n o t on ly among groups of i n s t i t u t i o n s

b u t a l s o w i t h i n each group of i n s t i t u i o n s , i n t h e

ways t hey a r e organised.

CHAPTER ONE .-

INTRODUCTION

BASIC ISSUES

one i n s t i t u t i o n t h a t plays a v i t a l r o l e i n t he

savings mobil izat ion e f f o r t s among t h e various economic

u n i t s i n our soc i e ty , but which has of ten been neglected

is t h e informal f i n a n c i a l i n s t i t u t i o n , a l s o ca l l ed t h e

t r a d i t i o n a l f i n a n c i a l i n s t i t u t i o n o r t he informal

c a p i t a l market,

~mphas i s , among t he f i n a n c i a l w r i t e r s , analys ts

and commentators, has been on t h e formal and institutions- b

l i s e d f i n a n c i a l i n s t i t u t i o n s and co-operative associa t ions

o r unions, with t he r e s u l t t h a t l i t t l e or nothing i s

ever s a i d about the informal s ec to r ,

pqentions ever made of these i n s t i t u t i o n s ( t h a t i s

t h e informal i n s t i t u t i o n s ) have remained s p a t i a l i-n a

few f inance l i t e r a t u r e t h a t ca re t o recognize t h e i r

presence.

~ h o u g h t h e t rend seems t o be changing, with some

s tud ies now being ca r r i ed out on informal f i n a n c i a l

organisa t ions , t h e amount of work done remains l i t t l e

when compared with work a l ready done i n t h e formalised

s e c t i o r , pgoreso, these s t ud i e s a r e never de t a i l ed and

often. come up a s newspaper a r t i c l e s or commentaries,

one reason f o r t h i s neglec t may be due t o t h e

informal na ture of t h e a c t i v i t i e s ca r r i ed out by these

ins - t i tu t ions . Sometimes, such associa t ions do not even

have names under which they operate , They a r e

usua l ly f o rmd among f r i ends , co-workers, age grades,

t r a d e r s , r e l a t i o n s and other i d e n t i f i a b l e groups who

can e a s i l y come together t o make r egu la r con-tributions,

Evidences abound t o show t h a t these informal

f i n a n c i a l organiaat ions have contrinued t o co-exist

with t he modern f i n a n c i a l i n s t i t u i o n due mainly t o

the inadequacy of f a c i l i t i e s of fered by t h i s formal

s ec to r , and a l s o due t o the f l e x i b i l i t y t h a t t h e

informal s ec to r provides.

STATST ZNT Oil' PKOI31ZM: - = - --.------- - . .. , - Given t he above p rob l em, t h e major poin t of

concern w i l l be t o f ind out why these informal f i nznc i a l

organisat ions have continued t o co-exist w i t h t he

formalised o r i n s t i t u t i o n a l i s e d f i n a n c i a l organisat ions

i n oar cor:liiiunities p a r t i c u l a r l y i n the ~ l r b a n cent res

where we have a networl; of fo rna l i sed i n s t i t u t i o n s .

Their modes of operat ion i n terms of a c t i v i t i e s ,

organisa t ion and performance as wel l as the problems

t h a t confront them a r e ye t other i s sues t h a t t he s tudy

w i l l address i t s e l f t o .

STATEL LIQTT OF OBJECTIVES : .=- -.- -s --- "--A&.

The i n fo r~xa l f i n a n c i a l i n s t i t u t i o n s have been found

-to be co-exist ing with the f ormalised o r i n s t i t u t i o n a l i s e d

f i n a n c l a l i n s t i t u t i o n s l i k e t h e commercial banks and

co-operat ive s o c i e t i e s and a l s o p l a y t h e v i t a l r o l e of

sav ings mob i l i za t ion from t h e ' n e t s a v e r s t t o t h e ' n e t

consumers o r u s e r s ' of funds f o r va r ious investment

purposes. The c u r r e n t s tudy then aims a t t h e fo l lowing

ob jec t ives : - ,

To determine t h e i n c i d e n t s o r o therwise and

reasons f o r co-exis tence of t h e s e i n fo rma l

i n s t i t u t i o n s wi th t h e formal i sed i n s t i t u t i o n s . b To examine t h e ope ra t ions ( i n terms of s e r v i c e s

r ende red ) , o r g a n i s a t i o n and performance of

t h e s e i n s t i t u t i o n s .

To f i n d ou t t h e prcblems con f ron t ing t h e

smooth f u n c t i o n i n g of t h e s e i n s t i t u t i o n s

To mike recommendations on how t o improve on

t h e a c t i v i t i e s of t h e s e i n s t i t u t i o n s . I n o ther -

words, t o recommend ways f o r overcoming t h e

problems con f ron t ing t h e i n s t i t u t i o n s .

STATEMENT OF HYPOTHESES :

l e Hol There i s no s i g n i f i c a n t income v a r i a b i l i t y

among members of d i f f e r e n t in formal

f i n a n c i a l o rgan i sa t ions ,

2. Ho2 Dai ly income has no s i g n i f i c a n t i n f l u e n c e

on t h e amount con t r ibu t ed by t h e d a i l y

cor i t r ibu tors ,

3- Ho3 I?ieri!bers of i n f o r ~ a l - f i n a n c i a l o rgan i sa t ions

do n o t p r e f e r in formal f i n a n c i a l groups t o

bank.

4. Eo4 Rate of r e t u r n s on t h e c o n t r i b u t i o n s of t h e

menlbers of Chr i s t j - z t s fund does no-t depent B

signif i c a ~ l l t l y on amounts con t r ibu t ed over

t h e per iod .

been done i n t h i s a r e a of in formal f i n a n c i a l organi.sat ions

The c u r r e n t s t u d y i s t h e r e f o r e , almost l i k e

furming i n a f a l l o w land o r f i s h i n g i n a mighty ocean.

Secause of t h i s , t h e s tudy wi :Ll be s i b n i f i c a n t t o t h e

f ollowin;3: - * The r e s e a r c h e r , who ,!lay be i n t ~ r e s t e d i n i n q u i r i n g

more i n t o t h e ~ c t i v i t i e s of t h e s e groups

* The une;nployed, who lay d i scove r o p p o r t u n i t i e s i n

going i n t o t h e unuiscovercd t r e a s u r y as a c a r e e r

by s t a r t i n g such o rgan i sa t ions a s d a i l y con t r ibu t ion ,

* The workers, who may no t have known of t h e e x i s t e n c e

of such savings arrangement among co-workers . The p o l i c y makers, who should s e e t h e s e o rgan i sa t ions

as having p o t e n t i a l s f o r he lp ing i n sav ings

mob i l i za t ion , and s o he lp modernize them.

F i n a l l y , t h e s tudy w i l l a l s o be s i g n i f i c a n t t o t h e

formal l zed f i n a n c i a l i n s t i t u t i o n s who should begin

t o recognize them a s having p o t e n t i a l s f o r he lp ing

i n sav ings mob i l i za t ion , and then channel t h e i r ,

marketing e f f o r t s towards encouraging them, r a t h e r

t han s e e them as r i v a l s .

DEFIRITION OF TERMS : ----- -A-- .- - I n t h i s s tudy , t h e fo l lowing terms were

employed t o mean t h e fol lowing:

1. Incidence: jqeaning ways i n which t h e in formal - -- ---- - -- f i n a n c i a l o rgan i sa t ions e x i s t and a f f e c t t h e s e l e c t e d

i n s t i t ~ t i o n s . I n otherwords, inc idence has been

employed h e r e t o mean !presence! o r !ex is tence!

v o l u n t a r i l y formed groups o r i n d i v i d u a l s , who

formed f o r t h e purpose of engaging i n some kind of

mutual-aid scheme through sav ings mobi l iza t ion .

This impl ies absence of coerc ion o r compulsion;

gene ra l lack of anykind of s o p h i s t i c a t e d o rgan i sa t iona l

s t r u c t u r e ; and u s e of f r e e - w i l l and s e l f de t e rmina t ion

i n one ts d e c i s i o n t o a s s o c i a t e f o r t h e purpose of

sav ings and/or lending.

3 . T h r i f t : Th i s , according t o s t r i c k l a n d means t h e

evoidance of extravagance and t h e p r a c t i c e of wise

spending ( s t r i c k l a n d 1934 p.13). I n t h i s s t u d y ,

t h r i f t a l s o means t h e a r t of r e f r a i n i n g from c u r r e n t

consumption now, i n o rde r t o have more t o spend i n

f u t u r e . ~t does n o t mean be ing s t i n g y .

4. I s a s u : This means t h e r evo lv ing type of i n f o r m a l b

f i n a n c i a l arrangement whereby a few i n d i v i d u a l s o u t

of mutual unders tanding and f r e e - w i l l dec ide t o

c o n t r i b u t e a sum c e r t a i n i n amount on monthly b a s i s ,

t o g ive o u t loans t o members i n r o t a t i o n . A s much

as p o s s i b l e , t h e amounts con t r ibu t ed a r e uniform f o r

ea se of account ing and c r g a n i s a t i o n . Number of

persons i n a group i s u s u a l l y small,. r e l a t i v e l y .

5 Fund: This means a sum of mcney made a v a i l a b l e - ( o r s e t a s i d e ) f o r a de f ined p r p o s e . I n otherwords,

it i s a pool of money s p e c i f i c a l l y made a v a i l a b l e f o r

a known o b j e c t i v e .

6 Rate of Return: This i s employed t o mean, t h e

percen tage of r e t u r n ( o r i n t e r e s t earned? p e r HI .00

of c o n t r i b u t i o n i n a pool of fund when t h e c o n t r i b u t i o n s

a r e given back o r shared ou t t o t h e i n i t i a l

c o n t r i b u t o r s t o t h e fund.

7. u.N.E.C. Th is is an a b b r e v i a t i o n f o r ! u n i v e r s i t y d

of ~ g g e r i a , Enugu Campus.

8. I.PI.T, Th is i s an a b b r e v i a t i o n f o r ? I n s t i t u t e of --* - Management and Technology, F f l u ~ .

9. A,S,U. TECH: This is an a b b r e v i a t i o n f o r fnnambra ----- S t a t e u n i v e r s i t y of ~ e c h n o l o g y ( m u g ~ campus)rl

LIMITATIONS OF THE STUDY -- ----- The r e sea rch work, as anyother endeavour of man,

w a s n o t wi thout i t s c o n s t r a i n t s i n terms of l i m i t i ~ g

f a c t o r s . Some of t h e s e c o n s t r a i n t s ( t h e l i s t n o t

be ing exhaus t ive) inc lude : -

Finance: This i s a ve ry l i m i t i n g f a c t o r i n whatever

a c t i v i t y one f i n d s h imse l f . I n t h i s case of t h e

s tudy , t h e r e s e a r c h e r be ing a s t u d e n t was q u i t e

cons t r a ined by l ack of funds , Frequent c a l l s made on

t h e s e l e c t e d i n s t i t u t i o n s meant a l o t of money on

t r a n s p o r t s and sometimes c i r c u m s t a n t i a l pat ronages

p a r t i c u l a r l y i n t h e market p l aces . Because t h e meagre

purse of t h e student-researcher1 was n o t r i c h

enough t o engage i n an ex t ens ive r e sea rch , t h e scope

of t h e s t u d y was h igh ly r e s t r i c t e d .

2. Time: cons ide r in2 t h e f a c t t h a t t h i s r e sea rch work -- had t o be combined wi th classroom l e c t u r e s and inview

of t h e f a c t t h a t t h e whole s tudy s t a r t e d on ly i n t h e

second semester of t h e s e s s i o n run r ing , t h e r e was n o t

enough t ime a v a i l a b l e f o r t h e s tudy . The r e s e a r c h e r

had t o f o r f e i t h i s l e c t u r e s and r e s t s sometimes i n

o rde r t o meet up wi th appointments. m e n a t t h a t ,

t h e p r e s s u r e of t ime was s t i l l much.

3. Lack of Co-operation: This i s ye t ano ther of such -.- - a- ----- -.-

cons - t r a in t s encountered. 111 t h e f i e l d of s tudy one

had t o meet with ve ry unco-operat ive elements. Some-

t imes , you i d e n t i f y somebody who i n d i c a t e d be ing i n b

t h e in formal group b u t w i l l d e c l i n e o u t r i g h t t o f i l l

your q u e s t i o n n a i r e o r g ive you any audience f o r

i n t e rv i ew. Also, some c o l l e c t e d your ques t ionna i r e s

and k e p t t hen only t o g ive it back t o you a f t e r many

p o i n t s of c a l l ; when t h e s e a r c h f c r ano ther p o t e n t i a l

respondent begins once more.

4. p a c i t y of L i t e r a t u r e : The t o p i c of r e sea rch i s U_L LI_----------

p a r t i c u l a r l y a f f e c t e d by t h i s problem. ~ o t much has

been w r i t t e n on t h e s u b j e c t . A s a r e s u l t t h e r e were

n o t much l i t e r a t u r e t o re-riew i n t h e l i t e r a t u r e rev iew

s e c t i o n of t h e r e p o r t .

5. Bias : c l o s e l y r e l a t e d t o t h e problem of l ack of - co-operat ion i s b i a s . 'The respondents sonetimcs tended

t o answer t h e way they f e e l you want them t o answer t h e

ques t ions . Also, t h e r e may have been some ambiguity

i n the ques t ions t h e way they were framed t h a t may have a f f e c t e d t h e answers.

St r i ck land , C,F. Report on t h e In t roduct ion of

Co-operative Soc i e t i e s i n t o b

Nigeria, ( ~ a g o s Government P r i n t e r

CHAPTER TWO

Savings h a b i t among t h e peoples of t h e

developing count r ies of t h e world have been found t o

be very low. Though low per c a p i t a income may be

c i t e d as one of t h e major causes of t h i s low ebb i n

t h e savings p o t e n t i a l s , t h i s does not t e l l t h e whold

s t o r y . Lack of savings i n s t i t u t i o n s has a l s o been

found t o be a con t r ibu to r t o t h e poor savings h a b i t .

o the r f a c t o r s o f t en adduced include:-

Imperfect maintenance of law and order , p o l i t i c a l

i n s t a b i l i t y , u n s e t t l e d monetary condi t ions , lack of

con t inu i ty i n economic l i f e , t he extended family

system with i t s d r a i n on resources and i t s s t i f f l i n g

of personal i n i t i a t i v e , and c e r t a i n systems of land

tenure which i n h i b i t savings ( ~ r i v i n e 1967 p .23O).

Given a l l t h e s e impediments t o saving and a l s o

given t h a t economic development r equ i res a r i s e i n t h e

r a t e of savings and investment s o a s t o break the

v ic ious c i r c l e of poverty, the c e n t r a l i s s u e cf

economic develop~~lcnt then becomes - t h e problem of

mobilizing and a l l o c a t i n g resources f o r t h e growth i n

such a manner t h a t growth becomes s e l f - s u s t a i n i n g

( ~ r i v i n e p . 229)

Resources mob i l i za t ion and a l l o c a t i o n imply t h e

accumulation of sav ings and channel ing them from t h e

n e t s a v e r s t o t h e n e t consumers f o r op t imal

investment. There i s c e r t a i n l y an u rgen t need f o r t h e

sys t ema t i c aggrega t ion and o r g a n i s a t i o n of savings

(powell 1966 p.273) i f any meaningful econcmic

development could be achieved, a s sav ings form t h e

bedrock of investment.

This onerous t a sk of sav ings mob i l i za t ion a n 8

o r g a n i s a t i o n i s mostly performed by t h e va r ious

f i n a n c i a l i n t e r m e d i a r i e s i n t h e economy. They employ

a l l s o r t s of f i n a n c i a l arrangements a t t h e i r d i s p o s a l

t o f a c i l i t a t e t h i s t a sk .

Apart from banks and o f f i c i a l ( fo rmal ) c r e d i t

f unds , some f i n a n c i a l suppor t i s a v a i l a b l e t o t h e

smal l -holders from secondary sources of development

funds . Loans of t h i s k ind a r e a v a i l a b l e , a l though

t o a l i m i t e d e x t e n t , from co-opera t ive s o c i e t i e s ,

unions and l o c a l government a u t h o r i t i e s which

f inance loan programmes from t h e i r own resourc2s .

Some shor t - te rm c r e d i t can be obta ined from t r a d i n g

o rgan i sa t ions as w e l l a s from t r a d e r s (and o t h e r

in formal groups). There i s a l s o a c e r t a i n amount of

p r i v a t e l end ing , which i s arranged between i n d i v i d u a l

fa rmers , o r between farmers and non-f armers e s p e c i a l l y between r e l a t i v e s (Marl in 1970 p.287). These l a t e r

sou rces of c r e d i t s f o r investment purposes a r e a l l

i n fo rma l t r a d i t i o n a l sources of funds , t h i n g

then becomes c l e a r -- t h e i n fo rma l s e c t o r a l s o p l ays

a b i g r o l e i n sav ings mob i l i za t ion e f f o r t s ,

u n f o r t u n a t e l y , t h e s e r o l e s played by t h e

in formal s e c t o r and t h e p o t e n t i a l s it has f o r p l ay ing

more, i n sav ings mob i l i za t ion e f f o r t s have been

g r o s s l y neg lec ted p a r t i c u l a r l y i n t h e . .-: economic

l i t e r a t u r e , ~ r e a t m e n t s given t o t h e s e c t o r lmd b

remained s p a t i a l ,

THE FITJANCIAL INFRGTRUCTURE AN 0VERVIF.N

The f i n a n c i a l i n s t i t u t i o n s g e n e r a l l y , perform

two f u n c t i o n s v i z : t h e economic and f i n a n c i a l

f u n c t i o n s ( ~ u r d a 1975 p.5)

Economic Function: They f a c i l i t a t e t r a n s f e r of r e a l -II

economic resources from l e n d e r t o borrower,

~ i n a n c i a l Function: They provide borrowers wi th funds p- --- ( o r purchas ing power) t h a t they want o r need t o have

now, t o ca r ryou t t h e i r p l ans

k d i s t i n c t i o n made between t h e two f u n c t i o n s is

t h a t when r e a l r e sou rces a r e a f f e c t e d ( i n t h e

t r a n s a c t i o n ) , we r e f e r t o t h e economic f u n c t i o n s , b u t

when such t r a n s f e r s have l i t t l e o r no e f f e c t upon

r e a l resources a l l o c a t i o n , economists r e f e r t o i t

as f i n a n c i a l func t ions . However, it must be noted

t h a t many f i n a n c i a l t r a n s f e r s have on ly a s l i g h t

e f f e c t upon r e a l resources a l l o c a t i o n ( i b i d ) . So, t h e

major f u n c t i o n of t h e f i n a n c i a l i n s t i t u t i o n s

g e n e r a l l y i s f i n a n c i a l i n n a t u r e , through t h e

t r a n s f e r of funds from n e t s a v e r s t o n e t consumers.

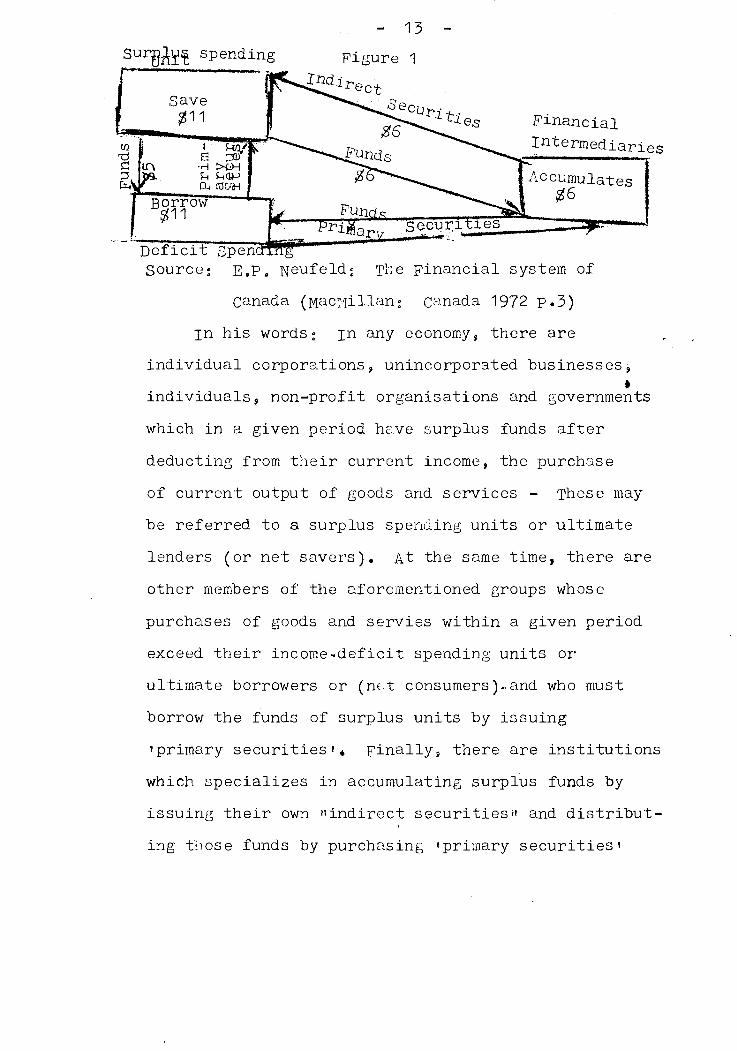

A good p i c t o r a l i l l u s t r a t i o n s of t h i s funds

t r a n s f e r f u n c t i o n of t h e f i n a n c i a l i n s t i t u t i o n s w a s b

given by ~ e u f e l d i n h i s work e n t i t l e d t h e f i n a n c i a l

system of Canadaft ( ~ e u f e l d 1972 p.3). ~ e u f e l d saw

f i n a n c i a l system as composing of i n s t i t u t i o n s and

i n d i v i d u a l s engaged i n t r a n s f e r i n g funds from t h o s e

i n s u r p l u s t o t hose i n d e f i c i t and i n f a c i l i t a t i n g

changes i n ownership of f i n a n c i a l claims t h a t t h e

process i n e v i t a b i y c r e a t e s . The f i r s t p a r t of t h e

d e f i n i t i o n ( t h a t i s - t r a n s f e r i n g funds from t h o s e

i n s u r p l u s t o t h o s e i n d e f i c i t he r e f e r r e d t o as t h e

f i n a n c i a l in te rmedia t ion . Below i s t h e p i c t o r a l

i l l u s t r a t i o n of t h e f i n a n c i a l func t ions as given

- 13 - sur&r% spending F igu re 1

Source: z,p, ~ e u f e l d : The F i n a n c i a l system of

Canada ( ~ a c r q i l l a n : canada 1972 p .3)

~n h i s words: ~n any economy, t h e r e a r e . .

i n d i v i d u a l co rpo ra t ions , unincorporated bus ines ses , b

i n d i v i d u a l s , non-prof i t o r g a n i s a t i o n s and governments

which i n a given per iod have s u r p l u s funds a f t e r

deduc t ing from t h e i r c u r r e n t income, t h e purchase

of c u r r e n t ou tpu t of goods and s e r v i c e s - These may

be r e f e r r e d t o s s u r p l u s spending u n i t s o r u l t i m a t e

l ende r s ( o r n e t s a v e r s ) . A t t h e same t ime, t h e r e a r e

o t h e r members of t h e aforementioned groups whose

purchases of goods and s e r v i e s w i t h i n a given per iod

exceed t h e i r i n ~ o m e ~ d e f i c i t spending u n i t s o r

u l t i m a t e borrowers o r (nc t consumers)- and who must

borrow t h e funds of s u r p l u s u n i t s by i s s u i n g

tprimary s e c u r i t i e s l r F i n a l l y , t h e r e a r e i n s t i t u t i o n s

which s p e c i a l i z e s i n accumulating s u r p l u s funds by

i s s u i n g t h e i r own i f i n d i r e c t s e c u r i t i e s i t and d i s t r i b u t -

i n g t i lose funds by purchasing primary s e c u r i t i e s

o r even o the r t i n d i r e c t s e c u r i t i e s ? That i s , t h e i r

l i a b i l i t y instruments i n t h e form of i n d i r e c t

s e c u r i t i e s a r e t h e i r source of funds, and t h e i r a s s e t s

i n t h e form of i n d i r e c t and primary s e c u r i t i e s

i n d i c a t e how they have uscd t h e i r funds, Those

i n s t i t u t i o n s a r e r e f erred t o as f i n a n c i a l in t e rmedia r i e s ,

I n t h i s i n s t i t u t i o n a l environment t h e r e f o r e , su rp lus

spending u n i t s can i n v e s t t h e i r funds i n t h e primary

s e c u r i t i e s of d e f i c i t spending u n i t s o r i n the B

i n d i r e c t s e c u r i t i e s of f i n a n c i a l in termediar ies ,

D e f i c i t spending u n i t s can s e l l t h e i r primary

s e c u r i t i e s t o su rp lus spending u n i t s , o r t o f i n a n c i a l

in termediar ies ( i b i d p,4)

From t h i s simple model of f i n a n c i a l a c t i v i t i e s

of t h e f i n a n c i a l market a s given by ~ e u f e l d , the

following deductions emerge: - t h e r e is one

p r i n c i p a l func t ion of the f i n a n c i a l market, namely:

t h e func t ion of t r a n s f e r r i n g funds t h a t surp lus

spending u n i t s have a v a i l a b l e , t o d e f i c i t spending u n i t s ,

- Three bas ic economic u n i t s a r e d i sce rn ib le : - t h e

t h e n e t save r , t h e n e t consumer, t h e

intermediary.

- Two types of t r a n s f e r s a r e poss ib le :

( a ) Face t o face t r a n s f e r between saver cmd - borrower, I n which case , the intermediary i s

no t Very important. He may only serve as a

broker, However, t h i s kind of resource t r a n s f e r i

f raugh t with numerous problems, such as problem

of imperfections i n t he market, problem of I double coincidence of wants a s i n b a r t e r

economy ( f o r example somebody who has savings

may not e a s i l y f i nd an o u t l e t or one,who wants

t o borrow. on the otherhand, those who have no b

savings and want t o borrow may no t e a s i l y f ind

t he saver t o borrow from). Furthermore, the

d i f f i c u l t y a t times, of t h e small savers i n

1 gaining access to. markets where primary

1 s e c u r i t i e s a r e bought and sold , and t he

r e l a t i v e l y high costs- of e f f ec t i ng small I

t r ansac t ions , combined with t h e l a rge

I denominations i n which they usua l ly t ake p lace , I has resu l t ed again i n a preference by t h e

publ ic f o r t lose f i n a n c i a l intermediar ies

I f e a tu r i ng claims aga ins t themselves which I I emphasize t h e a t t r i b u t e s of l i q u i d i t y and safety.

( b ) Intermediation: under t h i s arrangement, f i n a n c i a l .-. intermediar ies accumulate savings from surplus

economic u n i t s and then mc&e them ava i l ab l e t o

those who need them.

~ y t h i s a c t i on of the f i n a n c i a l in termediar ies

i n mobilizing savings from ne t savers t o ne t

consumers, c r e d i t , which i s a combination of

p o t e n t i a l i t y and a c t u a l i t y - obtaining cash,

goods and se rv ices ( a c t u a l i t y ) by given a promise

t o pay money ( p o t e n t i a l i t y ) is created. ( see

Abe 1981 p. 115) The i n t e r a c t i o n among t h e t h r ee

i d e n t i f i ~ b h un i t s gives r i s e t o t he f i n a n c i a l

funct ions of the f i n a n c i a l s ec to r ,

Among the i d e n t i f i c ab l e f i n a n c i a l

i n s t i t u t i o n s t h a t perform f i n a n c i a l funct ions

d i s t i n c t i o n i s o f t en made as per t h e i r modus

operandi, hence we begin t o t a l k of formal i ty

versus informal i ty of thc i n s t i t u t i o n s ; banking

versus non-banking i n s t i t u t i o n s , and s o on,

Though these i n s t i t u t i o n s d i f f e r i n modes

and nomenclature they s t i l l perform the same

funct ion- Savings mobilization.

Generally, the f i n a n c i a l in termediar ies

include: t he commercial banks, merchant banks,

development f inance i n s t i t u t i o n s , insurance

companies, c r e d i t and savings i n s t i t u t i o n s ,

investment t r u s t s and mortgage i n s t i t u t i o n s

be regrouped i n t o banking and ~non-banking

i n s t i t u t i o n s . The non-banking i n s t i t u t i o n s can

be s a i d t o be of f o u r types (od le 1972 p.10)

1. Savings (and c r e d i t ) i n s t i t u t i o n s - p o s t a l savings ,

Building s o c i e t i e s and c r e d i t unions and

co-operatives . 2. Insurance ~ n s t i t u i o n s - Li fe and on-life s e c u r i t y

funds.

3 . unorganised money market opera tors - woney lenders

pawn brokers e t c .

4. publ ic f inance corporat ions - I n d u s t r i a l and

; ,g r i cu l tu ra l c r e d i t coroporations . b

Every o the r f i n a n c i a l i n s t i t u i o n s a p a r t from t h e

f o u r given above, come under t h e banking s e c t o r . These

in termediar ies including the f i n a n c i a l instruments ,

r u l e s conventions and norms which f a c i l i t a t e and

r e g u l a t e t h e flow of funds through t h e macro-

economy c o n s t i t u t e t h e f i n a n c i a l system; and t h i s

system i s con t ro l l ed by t h e government through t h e

agency of t h e Cent ra l ~ank (okafor p67)

F inanc ia l s e c t o r s t u d i e s have tended t o concentrate

on formal f i n a n c i a l in termediar ies : the c a n t r a l Banking

and monetary macro-relations here looks a t t h e g loba l

p i c t u r e of a l l t h e formalised f i n a n c i a l i n s t i t u t i o n s

wi th in an economy, inc ludicg a l l t h e banking and non-

banking i n s t i t u t i o n s - whose a c t i v i t i e s , i n one way o r

t h e o the r , a f f e c t t h e movement and a p p l i c a t i o n of money

such a s t h e commercial banks, t h e mortgage banks, t h e insurance companies, pension funds e t c .

Emphasis on these f or'malised f i n a n c i a l in termediar ie . i n t h e p a s t has not been without u t t e r neglec t of the informal f i n n n c i a l i n s t i t u t i o n s i s a l s o c a l l e d t r a d i t i o n a l f i n a n c i a l i n s t i t u t i o n s ( o r system).

However, evidences have show;? t h a t t h e s e forma-

l i s e d f i n a n c i a l i n s t i t u t i o n s , i n s p i t e of a l l emphasis,

a r e g r o s s l y inadequate t o meet t h e f i n a n c i a l needs

of t h e g e n e r a l i t y of t h e peoples i n t h e var ious

world economics, p a r t i c u l a r l y i n t h e developing

c o u n t r i e s , where t h e s e r v i c e s a r e n o t only i n a c c e s s i b l e

b u t a l s o a r e no t s u f f i c i e n t l y a v a i l a b l e even t o those

who have access t o them. A g r e a t ma jo r i ty of t h e .. C

r u r a l dwe l l e r s , t h e i l l i t e r a t e s , t h e low incornc

e a r n e r s , who c o n s t i t u t e 60 - 80% of t h e populat ion

of t h e s e developing coun t r i e s have v i r t u a l l y no b

access t o t h e s e r v i c e s rendered by t h e formal i sed

f i n a n c i a l i n s t i t u t i o n s . ~t then fol lows t h a t s

szenar io whereby e f S o r t s a r e concentra ted on

s t u d i e s of t h e f ormalised i n s t i t u t i o n s t h a t c a t e r

only f o r 20 - 40% of t h e popula t ion a t -the expense

of t h e informal i n s t i t u t i o n s i s not s a t i s f a c t o r y .

Ever be fo re t h e advent of t h e modern f i n a n c i a l

i n s t i t u t i o n s ( t h a t i s , t h e formal ised i n s t i t u t i o n s ) ,

t h e r e e x i s t e d , one kind of informal f i n a n c i a l cO-

ope ra t ion o r another zmong t h e var ious economic

u n i t s through which they mobil ized savings . Co-

ope ra t ion according t o Bedi (1962), i s t h e a c t of

persons v o l u n t a r i l y u n i t i n g f o r u t i l i z i n g , r e c i p r o c a l 1 , t h e i r own f o r c e s , resources o r bo th , under t h e i r

mutual arrangement t o t h e i r economic p r o f i t s o r l o s e s ,

pu t i n another way, t h i s kind of co-operation is

form of organisa t ion wherein persons v o l u n t a r i l y

a s soc ia te together as human beings on the b a s i s of

equi ty f o r t h e promotion of t h e economic i n t e r e s t s

of thzmselves ( c a l v e r t 1959 p.1) professor okafor

i d e n f i f i e d o the r f e a t u r e s of t h i s kind of arrangement

a s s e l f -imposed bu t group - inf luenced, mandatory

savifigs, Ije f u r t h e r explained t h a t t h e arrangement

i s vouluntary, because each member determines t h e

a c t u a l amount of r egu la r savings t o make, b u t group- b

influenced because t h e s o c i e t y determines t h e

minimum per iod ic con t r ibu t ion acceptable (okaf o r p.1 I )

This form of informal co-operation have bzen

shown t o have ex i s t ed long before t h e coming of t h e

modern and formalised f i n a n c i a l arrangements.

According t o Onyemachi ( ~ u s i n e s s Times lyay 18 1987 - -

~ 0 1 4 ) 9

1lBef ore t h e advent of mod-ern co-operative l h r i f t

and c r e d i t s o c i e t i e s , t h e r e ex i s t ed s i m i l a r organisa t ions

which operated almost l i k e co-operative c r e d i t s o c i e t i e s ,

These co-operative l i k e organisa t ions exis ted and

s t i l l e x i s t i n many p a r t s of t h e world today,

e s p e c i a l l y i n Southern Asia, ~ { e s t ~ f r i c a and t h e West

Indies . They a r e a s soc ia t ions formed upon a core of

- 20 - p a r t i c i p a n t s who agree t o make r e g u l a r c o n t r i b u t i o n s

t o a fund which i s given, i n a whole o r i n p a r t , t o

each c o n t r i b u t o r i n rotat ionsl ,

Another evidence of t h e ex i s t ence of such

arrangements i n t h e e a r l y days w a s given by ~ o n a l d s o n

e t a l i n t h e fol lowing l i n e s , !!The aggrega t ion of

money, even t h e r~loney of t h e i n d u s t r i a l workers, i n t o

p o t e n t i a l l y p roduc t ive masses had a l r e a d y made some

p rog res s when t h e modern money market came i n t o being.. .

When i n s t i n c t g ives p h c e t o reason , under t h e

s t imu lus of a b e t t e r s o c i a l &nvironment, money is b

t ransformed from a ba r r en s t o r e of v a l u e i n t o a

phalanx of f ecund i ty , because hoa rd ing is superseded

by t h e d e p o s i t account. The change, a t t h e lower

ex t r emi ty of t h e s o c i a l s c a l e , i s c l e a r l y d i s c e r n i b l e

b e f o r e t h e end of t h e 18 th cen t ru ry . . . . The process

of t r ans fo rma t ion from hca rd t o d e p o s i t - no t always

on i n t e r e s t - b e a r i n g d e p o s i t went on!! (Donaldson e t a l

1977 ~ ~ 2 6 9 ) ~

1t should be noted t h a t t h e s a f e t y of t h e money

t h e n , (and even now) was o f t e n considered an ample

r e t u r n t o t h e d e p o s i t o r . I n sach hands, it i s

secured n g a i m t p i l f e r e r s , t h i e v e s and robe r s which

i t cannot be i n t h e d e p o s i t o r l s h a b i t a t i o n ,

These anc ien t arrangements a r e what we r e f e r

t o a s t h e t r a d i t i o n a l f i n a n c i a l i n s t i t u t i o n s which

have continued t o su rv ive up t o now,

un fo r tuna te ly , t he presence of t h e modern

f i n a n c i a l i n s t i t u t i o n s has tended t o dwarf t h e

p o p u l a r i t y of t h i s . t r a d i t i o n a l f i n a n c i a l

i n s t i t u t i o n among a g r e a t major i ty of t h e people,

However, due t o t h e ind ispensable r o l e s and

o t h e r p e r c u l i a r i t i e s of t h i s t r a d i t i o n a l

i n s t i t u t i o n , i t has no t been completely debased,

The i n s t i t u t i o n has continued t o s tand t h e t e s t 0%

time arid has contiriued t o co-exis t wi th t h e modern

f i n a n c i a l i n s t i t u t i o n s ,

REASONS FOR THIS CGNTITJUZD CO-FXISTENCE

me would expect t h a t t h e emergence of t h e modern

f i n a n c i a l i n s t i t u t i o n s a s we f i n d them today would

have s p e l t t h e t o t a l c o l l a p s e of t h e crude

t r a d i t i o n a l f i n a n c i a l i n s t i t u t i o n s , s u r p r i s i n g l y ,

t h e s e i n s t i t u t i o n s have been found t o cont inue

co-exis t ing with t h e b e t t e r organised, formal i sed

f i n a n c i a l o rgan i sa t ions , Many reasons hzve been

adduced f o r t h i s continued co-exis tence of t h e two

seemingly incompat ible systems,

- SRVZRS ' AND BOIIROWBS ' PREFERENCE AND NED : -.

The funct ion of a sound f i n a n c i a l s t r u c t u r e

i s t o move f i n a n c i a l resources e f f i c i e n t l y from

surplus t o d e f i c i t non-f inancial u n i t s and from

a c t i v i t i e s y ie ld ing low s o c i a l r e tu rns t o those high

y ie ld ing , s o c i a l r e tu rns . . This movement of

funds requ i res , among o the r t h i n g s , f i n a n c i a l

instruments t h a t a r e cons i s t en t with savers t

and borf owers f p r e f erenceand needs, These a t t r i b u t e s --- have faund s u f f i c i e n t expression i n t h e t r a d i t i o n a l

f i n a n c i a l i n s t i t u t i o n s . The t r a d i t i o n a l f i n a n c i a l

i n s t i t u t i o n s have been found t o be very compatible , - . with t h e preferences and needs of v a s t majori ty

of t h e masses who seek and make use of the

f a c i l i t i e s offered t h e i n s t i t u t i o n s .

of t h i s , t h e informal c r e d i t markets ( a s t h e

t r a d i t i o n a l i n s t i t u t i o n s a r e a l s o c a l l e d ) se rve a

very u s e f u l purpose and t h e r e should be no l e g a l

o r customary obs tac les t o t h e i r development.

Ififorma1 market dea le r s a r e o f t e r n much b e t t e r

placed than banks t o i d e n t i f y new oppor tuni t ies f o r

f i n a n c i a l t r ansac t ions - new markets r equ i r ing

new products and processes. (Bhat t 1986 p.21).

Because of t h i s high f l e x i b i l i t y of fered by t h e

i n s t i t u t i o n . ( t r a d i t i o n g i t has continued t o

e x i s t along with t h e modern i n s t i t u i o n s ,

- unique Services provided: -- The unique s e r v i c e s rendered by these informal

i n s t i t u t i o n s have been found as a s t rong reason why

they have survived t h e competit ion of modern

f inancing opt ions, According t o professor okafor

(lg83), t hese i n s t i t u t i o n s have survived t h e competition

of modern f inancing options because of some unique

s e r v i c e s which they provide, inc luding , among others:-

provis ion of l i b e r a l c r e d i t f a c i l i t i e s f o r b

members, pqost s o c i e t i e s g ran t f i n a n ~ i a l

a s s i s t a n c e without i n s i s t i n g on s e c u r i t i e s

o the r than t h e s o c i a l sanc t ion of t h e group o r

t h e community which o f t e n d e t e r s d e f a u l t ,

Reduction of u n c e r t a i n t i e s i n investment

planning. planning i s f a c i l i t a t e d by t h e

exis tence of def ined schedules f o r c o l l e c t i n g

group cont r ibut ions (okaf o r p .7l) ,

These se rv iees which a r e r a r e t o f i n d among

t h e modern f i n a n c i a l i n s t i t u t i o n s mark t h e

i n f o rna l s e c t o r out a s a hope f o r t h e masses.

Because of t h i s , they have continued t o e x i s t

s i d c by s i d c with t h e so-cal led soph i s t i ca ted

modern i n s t i t u t i o n s even i n t h e urban areas ,

p ro fesso r onoh surnrnarised h i s own reasons

f o r t h i s co-existence under two broad ca tegor ies

namely; ignorance and banking v i g i d i t i e s (onoh 1980

pp 27 - 28)

- Ignorance: --.--. This has been i d e n t i f i e d a s a major c o n t r i b u t o r

t o poor banking h a b i t s among a v a s t major i ty of our

people. I n most developing c o u n t r i e s , t h e i l l i t e r a c y

r a t e i s y e t very h igh ( i n some p l a c e s , it i s s t i l l

as high as 70%). A s a r e s u l t of i l l i t e r a c y , t hey do

n o t understand what t h e rudiments of banking

bus iness a r e and do n o t a p p r e c i a t e t h e s e r v i c e s t h a t

banks render. b

Also, duc t o bad exper iences with banking

bus iness r i g h t from t h e incep t ion of banking

bus iness i n ~ i g e r i e , p a r t i c u l a r l y du r ing t h e c ra sh

of t h e mushroom banks i n t h c f i f t i e s whlch l c d t o

f i n a n c i a l r u i n s f o r many deposkors and a l s o , t h e

exper iences of depos i to r s du r ing the ~ i g e r i a n c i v i l

\far of 1967 - 1970 i n t h e w a r zones (onoh p.27)

t h e r e has remained t h i s f e a r among t h e i l l i t e r a t e s

about t h e s a f e t y of a d e p o s i t o r f s money wi th t h e

banks as t h e memory of t h e s e awful exper iences is

s t i l l green with those d i r e c t l y o r i n d i r e c t l y

a f f e c t e d . AS a r e s u l t of t h i s l ack of confidence

among t h e i l l i t e r a t e s of t h e developing c o u n t r i e s , of

which ~ ~ g e r i a i s one, they had continued t o s e e t h e

- 25 -

t r a d i t i o n a l f i n z n c i a l institutions as t h e b e s t b e t and

avenues f o r ensur ing s a f e t y f o r t h e i r savings.

- BANKING REGIDITIES : ----- -

The banking i n s t i t u t i o n s which i s t h e k ing of

t h e modern and formal ised f i n a n c i a l o rgan i sa t ions i s

f r a u g h t wi th n o t o r i e t y of r i g i d i t i e s . I n o rde r t o

maintain a high s tandard 01 banking p r a c t i c e , U g i s l a -

t i o n i s passed t o r e g u l a t e t h e ope ra t ions of f i n a n c i a l

i n s t i t u t i o n s t h a t ca r ryou t t h e func t ions of modern

banks. The Niger ian Banking Decree (Decree NO. I 1969) B

as amended i s one such l a w which has r a i s e d some d u s t s .

The p rov i s ions of t h i s dec ree , f o r one t h i n g ,

succeeded i n l i m i t i n g t h e number of banks being

e s t a b l i s h e d with t h e r e s u l t t h a t banking f a c i l i t i e s

a r e t n s u f f i c i e n t l y a v a i l a b l e , p a r t i c u l a r l y i n t h e

r u r a l a r eas .

Even where t h e banking f a c i l i t i e s a r e a v a i l a b l e ,

a number of problems a r e encountered by p o t e n t i a l

depos i to r s . The f i r s t of such problems is t h e long

p rocesses t o be undergone be fo re a chequeable account

i s opened - t h e demand f o r r e f e r e e s , a l l t h e forms

t o be f i l l e d (even where one i s n o t l e t t e r e d and t h e

h igh l e v e l of i n i t i a l d e p o s i t s , when t h e account i s

f i n a l l y oened,) The problems encountered when ope ra t ing

it i s even worse. A l o t of t ime i s wasted whi le t r y i n g

t o cash a s i n g l e cheque. I n some cases , it takes a

whole day t r y i n g $0 cash a cheque. I n t e r c i t y

t r a n s a c t i o n takes weeks o r even a month before it

is c leared , k l s o , t h e a t t i t u d e of t h e o f f i c i a l s of

t h e banks t o customers is another de te ran t .

Discr iminat ion aga ins t customers abounds. Somelbigl

customers a r e given p r e f e r e n t i a l treatment with a l l

t h e courtesy denied the !ordinary! customers . The

condi t ion f o r loans may be d i f f i c u l t t o comply with

by a smal l saver intending t o borrow from a bank.

~ 1 1 these r i g i d i t i e s very common among banks and ' o the r formalised f i n a n c i a l i n s t i t u t i o n s compound t o

make t h e i r se rv ices inaccess ib le t o the majori ty

of t h e people, such t h a t they f i n d consolat ion i n t h e

t r a d i t i o n a l f i n a n c i a l i n s t i t u t i o n s .

Reasons f o r t h e continued co-existence of t h e

informal s e c t o r with the modern i p s t i t u t i o n s a l s o

abound among farmers. Some of these reasons among

o thers include: - - They a r e major sources of c r e d i t t o farmers.

According t o ~ i l l e r (7 977) the non- ins t i tu t iona l

sources ( t h e informal lenders) provide most of

the c r e d i t s used by smal l farmers , (while t h e

commercial banks and o the r f ormalised i n s t i t u t i o n s

c a t e r f o r the f i n a n c i a l needs of t h e meciiut;l and

l a r g e s i z e d fa rmers ) . Be t h a t as i t may, t h e --

in formal o r n o n - i n s t i t u t i o n a l sources cont inue t o e x i s t

as long a s t h e s m a l l farmers cont inue t o e x i s t .

- u n a t t r a c t i v e n e s s of A g r i c u l t u r a l loans t o s m a l l

farmers: This i s another reason advanced by t h e ~ o o d

and A g r i c u l t u r a l o rgan i sa t ion (F ,A. 0) f o r t h e

continued co-exis tence of t h e in formal i n s t i t u t i o n s

with t h e modern ones. small farmers a r e t o o numerous

afid a r e n o t i n d i v i d u a l l y known t o banks. I n t h e words

of ~ ~ f l ~ ~ ~ " t h e e x t r a expense of adminis te r ing a b

m u l t i p l i c i t y of s m a l l loans t o fa rmers , who a r e

g e n e r a l l y i l l i t e r a t e s and of low p r o d u c t i v i t y , and

t h c high r i s k s involved tend t o discourage t h e

ord inary bank from e n t e r i n g t h e f ie ld11 . (F.A.o.

1965 p.V). Because of t h i s , t h e small farmer has

no o t h e r f i nanc ing opt ion than t o r e s o r t t o t h e crude

f r a d i t i o n a l methods of f i nanc ing t o n a i s e t h e needed

funds.

o t h e r reasons f o r t h e s u r v i v a l of t h e in formal

s e c t o r a r e : - - ~overnmen t s apparen t i n d i f f e r e n c e i n encouraging

r u r a l banking. This has tended t o enhance t h e

p r o l i f e r a t i o n of t h e t r a d i t i o n a l f i n a n c i a l

i n t e r m e d i a r i e s (onoh p.29).

- Convenience and l i q u i d i t y which a r e among t h e

f a c t o r s i d e n t i f i e d by ~ u r d a (1975 p.197) a s

c r i t e r i a f o r s e l e c t i n g i n s t i t u t i o n s f o r saving,

have a l s o helped t o account f o r t h e continued

co-existence of t h e i n f o r n a l f i n a n c i a l organisa t ions ,

TYPES OF INFORMAL FINANCIAL ORGANISATIONS

~t i s not easy t o completely i d e n t i f y a l l t h e

var ious types of t h e informal f i n a n c i a l organisa t ions ,

For one th ing , a s the name implies , these organisa t ions

a r e informal i n na tu re and t h e r e a r e no laws laid,down

t o guide t h e i r $orri~cition and operat ion, A s a r e s u l t , . . . ,

when once two o r more people a r e capable of coming

toge the r f o r t h e common purpose of mutually a id ing

each o ther i n f i n a n c i a l terms o r f o r t h e purpose of

extendillg c r e d i t s t o o u t s i d e r s , through some pe r iod ic

con t r idu t ions , an informal f i n a n c i a l organisa t ion

emerges,

However, some f inance scho la r s have been able

t o i d e n t i f y some common forms o r systems

of these t r a d i t i o n a l f i n a n c i a l organisat ions.

For example, p ro fesso r Onoh i d e n t i f i e d twelve of

$i.uch systems i n h i s work as following: - 1 , ~ s u s u ( ~ s u s u , osusu, susu) group,

2. Fillarlce through s l ave ry , human labour and ch i ld

marriage (This i s no i n vogue)

3 . 4.

5.

6.

7.

8.

9.

10.

11

12.

and

- 2 9

Age grade assoc ia t ion

v i l l a g e adminis t ra t ion cont r ibut ions

v i l l a g e r u r a l developm~nt schemes

Men s revolving loan associa t ions

Married womenfs assoc ia t ions

~ a i n i l y fund pools

Fgtended falriily co-operative fund

Town u ~ i o n s

Local money lenders and

Soc i a l clubs (onoh p.13) 8

Each of these groupings has i t s va r i a t i ons

the number of such va r i a t i ons vary from

l o c a l i t y t o l o c a l i t y . For example, tak ing up

v i l l agee r u r a l development schemes ; while i n some

places they may be organised j u s t f o r one scheme (

say e l e c t r i f i c a t i o n scheme$, some may have such a

r u r a l development scheme as a s tanding or permanent

f ea tu res . 1r1 other words, while some of t h e schemes

a r e adhoc i n na tu re , some a r e standii3g. a l s o , while

some a r e f o r s p e c i f i c p r o j e c t s , o thers a r e formed

f o r development general ly.

of these twelve types given above, t he most

popular and most widespread of t r a d i t i o n a l i n s t i t u t i o n

prevalent i n almost a l l t h e nooks and corners of

the world p a r t i c u l a r l y i n t he developing countr ies

a r e those engaged i n snvings, loan and mutual schemes.

I n t h e words o f professor onoh: these schemes a r e

in teg ra ted i n a system r e f e r r e d t o i n l o c a l par lance

as i susu i n ~ g b o land. A s a r e s u l t of t h i s popu ia r i ty

which i susu system enjoys, i t w i l l now be given some

deeper treatement.

The I s u s c system:

According t o professor okafor , the ~ s u s u - t y p e

s o c i e t y is based on t h e p r i n c i p l e of self-imposed

bu t group-ii:f luenced mandatory savings. ~t is

voluntary9 becausc each member determines t h e

a c t u a l amount of r egu la r savings t o make, but b

group-influenced because the s o c i e t y de-termines t h e

minimum p e r i o d i c contribu-tion acceptable ( okaf o r

p. 71) . con t r ibu t ions r a i s c d through t h i s system

a r e appl ied i n t h e ways agreed upon by t h e menbers

i n a l l e i v a t i n g the f i n a n c i a l problems of members.

This kind of f i n a n c i a l arrangement which i s co-

opera t ive l i k e has been found t o e x i s t i n many .

p a r t s of t h e world, e s p e c i a l l y i n Southern Asia,

Afr ica and the y e s t Ind ies . ~t i s given

d i f f e r e n t rlanies i n t h e varicjus places it i s found

f o r example i n N~ g c r i a it i s known by t h e

fol lowing names:-

~ s u s u , aha, Adashi, Ajo, ~ s u s u ain,d/or as hi, among

t h e d i f f e r e n t e thn ic groups t h a t cu t across t h e

country (onyemachi 1987), I n 2bo land i t i s c a l l e d

i s u s u , yorubas c a l l i t esusu whi le t h e Hausas c a l l

i t adash i . A t t h e i n t e r n a t i o n a l level : I nd i ans

r e l e r t o it as Kameti; o t h e r c o u n t r i e s wi th t h e i r

d i f f e r e n t names f o r t h e financial arrangement a re : -

S i e r r a Leone - zlsusus; Cameron - d jangg i ; Indonesia-

a r i s a n ; japarl- K O ; Victnam - ho; China - h u i ;

Malaya - t o u t i ; a e n i n Republic - ndjariu; Congo - k i limo.

~ h o u g h t h e system may d i f f e r i n nomenclature

among c o u n t r i e s and e t h n i c groups, t h e system b

remains same - a c o n t r i b u t i o n c lub whereby a

l a r ~ e group of people meet a t r e g u l a r i n t e r v a l s

t o pay a f i x e d s u b s c r i p t i o n i n t o a fund which

i s given t o each member i n t u r n (Ardener 1953

PP 217 - 219).

The i s u s u system has been found t o have

e x i s t e d f o r a very longtime i n h i s t o r y , According

t o Reverend o ~ k e e f f e ( s e e onyemachi 1987).....

c e r t a i n l y t h e esusu e x i s t e d i n 1843, f o r

according t o him rlcrowthePs 1 yoruba vocabula r ly

of t h a t d a t e gave d e t a i l s of s m a l l r o t a t i n g c r d d i k

a s s o c i a t i o n s ammg t h e ~ g b n and noted t h a t t h e term

1 ~ s u f was used f o r c m t r i bution:!. u n f o r t u n a t e l y ,

one caniiot t e l l wi th any degree of e x a c t i t u d e when

t h e i susu system a c t u a l l y s t a r t e d - though t h a t

i s not very important,

onyemachi i d e n t i f i e d fou r c l a s s i f i c a t i c n s 1 .

of t h i s system based on the method of operat ions,

1. TYPE A: This i s organised i n such a way --- t h a t each member pays i n some s p e c i f i c amount

money i n t o a fund. The to - t a l amount

cb l l ec ted is thcn handed over t o one member

f o r h i s use . This process i s repeated

s eve ra l times from one member t o another,

?;fi?en ever/body has gc t h i s /he r own tu rn , the

assoc ia t ion may e i t h e r come t o an end o r &other

round of cont r ibut ion m y be s t a r t e d , Here,

who ge t s f i r s t o r second o r l a s t , a s the case

may be, is determined through ba l l o t i ng ,

2, TYPE B: I n t h i s types cont r ibut ions a r e a l s o -- made as i n type A above, but i n t h i s case, no

payment i s made i n cash t o anybody. Ins tead ,

the t o t a l co l l e c t i on i s usua l ly invested on

something concrete a t the end of t he year f o r

one member (probably t o check t he tendecny

among members of c'iverting the funds t o non-

productive uses) . The process is a l s o

repeated u n t i l everybody i s served. This form

of arrangen;t.nt is comnion among tht? M.ano/~andigo

people of ~ i b c r i a ,

3. TYPE C . This type i s organised i n such a way

t h a t a respected and t r u s t worthy member c o l l e c t s

contribution:: from a l l members a t r egu la r

i n t e r v a l s . r\jo p a r t o r t o t a l cont r ibut ions

co l l ec ted is paid out t o members, n e i t h e r

a r e they given c r e d i t s a t such regu la r i n t e r v a l s .

A 1 1 t h e money co l l ec ted i s l e f t i n t h e custody

of t h e chosen honest member u n t i l the year ends

o r another pre-arranged t ime, when t o t a l

a m ~ u n t s contr ibuted by each member i s given

back t o him o r he r . This arrangement is

popular among t h e Vai people of L ibe r i a and

t h e former rJostern region of Nigeria.

4. TYPE Do This i s thc t y p i c a l savings and c r e d i t -- assoc ia t ion organised i n such a way t h a t i t s

l i f e s p a n o r dura t ion i s t i e d t o t h e a c q u i s i t i o n

of d e f i n i t e ma te r i a l a s s e t s by a l l members.

xverymember must have benef i ted from t h e

a s s o c i a t i o n - mate r i a l -asset-wise before i t s

l i f e s p a n is conplcted. I n o the r words, i n t h i s

kind of arrangement, no sooner t h e a s s o c i a t i o n

has achieved t h e major ob jec t ive of hers than

it i s disbanded by members themselves.

Apart from t h e s e four types descr ibed ,

there i s yet another type whereby the u s u a l

c o l l e c t i o n i s got from mzmbers bu t c r e d i t s

can be given t o both members and non-members. A

non-member, provided he can g e t a member of the

a s soc ia t ion a s a guarantor , can request f o r c r e d i t

from the associa t ions I n t e r e s t i s chargeable on t h e

loan. NO d i s t r i b u t i o n i s made t o members d i r e c t l y

a f t e r t h e rebwlar co l l ec t ion .

In more s p e c i f i c t e r n s , t h e r e i s a v a r i a t i o n of

t h c schenles c a l l e d ~ b h i s h i l i n Ind ia , which is

common among a l l c l a s s e s of soc ie ty , e s p e c i a l l y

t r a d e r s and labourers i n t h e ~ ( o l h a p u r D i s t r i c t of t h e

Bombay s t a t e . b his his advance loans up t o a c e r t g i n

extent and f o r c e r t a i n purposes. Before s t a r t i n g a

Bhishi , i t s dura t ion (usau l ly between one and t h r e e

years ) and t h e r a t e of savings expected of the

members a r e decided upon. The cont r ibut ions made by

membcrs, togethcr with i n t e r e s t , a r e repaid them on

t h e terminat ion of t h e hish hi i n proport ion t o t h e i r

sha re i n savings. This kind of arrangement resembles

what we have i n some m i n i s t r i e s i n ~ . g e r i a some times 3.

c a l l e d clwistmas t h r i f t fund. ~ n i s h i s , it must be

noted, can be terminated even before t h e pcr iod

normally f ixed f o r them (committee of ~ i r e c t i o n

1954 p.28).

one th ing t o be noted about these typologies

of mutual cont r ibut ions and c r e d i t ex tent ion is t h a t

t h e r e i s no c lea r -cu t l i n e of demarcation among them.

~ l l involve one kind of f i n a n c i a l con t r ibu t ion o r

t h e o ther , AS a r e s u l t , op i r~ions have continued t o

vary among va r iours a u t h o r i t i e s on t h e b e s t way t o

c l a s s i f y t h e infgrmal f i n a n c i a l i n s t i t u t i o n s . For

example while the F.A,@. (1959) took a pure ly

t r a d i t i o n a l view po in t i n identifying b a s i c a l l y two

types of c r e d i t societies namely: strural t h r i f t

and c r e d i t societyit and {turban t h r i f t and c r e d i t soc ie ty :

(F .A,rJ. Agr icu l tu ra l ~evc lopr r ,mt paper 1959 pp .19-27)

Adeyeye (1978) adopted e n t i r e l y d i f f e r e n t approach

by lumping, genera l ly , c r e d i t s and t h r i f t s s e p a r t e l y

and c a l l i n g them - rfco-credits!! and vtco-thrifts!!,

~ r r e s p e c t i v e of the approach adopted i n

c l a s s i f y i n g then!, t h e f a c t remains t h a t the re e x i s t s

d i f f e r e n t types of t h r i f t s and c r e d i t a s soc ia t ions

i n t h e t r a d i t i o n a l s o c i e t i e s who organise one kind of

f i n a n c i a l nutua l a id scheme o r the o the r t o mobilize

savings,

0BJECTIVES AND FUNCTIONS OF THESE INSTITUTIONS %

T h r i f t , which i s tllc avoidance of extravngance

and t h e p r a c t i c e of wise spending are t h e lessons

which t h e Afr ican has t o learn. What i s needed i s

t h r i f t under supervis ion; organised and cc~n t ro l l ed

t h r i f t , f r e e from specu la t ion ( s o f a r as humanly

p o s s i b l e ) , f r e e from t h e r i s k of embezzlemant. T h r i f t

must be v o l u n t a r y , i f t h e s a v e r i s ever t o become a

r e s p o n s i b l e c i t i z e n , it ixust be coii t inuous, i f an

econornic r e s u l t i s t o be a t t a i n e d , and it mst be

p r a c t i s e d by organised and s e l f governing groups i f

t h e l abour of s u p e r v i s i o n and c o s t of management a r e

n o t t o tc excess ive ( s t r i c k - l a n d 1934) p.13) From

t h e above s t a t emen t s , one o b j e c t i v e of t h r i f t

o rgan i sa t ions becofiic t h a t of cnccurngirig t h e h a b i t

of s u s t a i n e d and organised sav ings , b

Okonjo notcd t h a t t h e main aim of t h e a s s o . i a t i o n

i s t o assist i t s members i n sma l l s c a l e c a p i t a l

format ion by making them pay compulsor i ly a t s h o r t

r e g u l a r i n t e r v a l s l i k e on a f o u r day n a t i v e weeks,

weekly, f o r t h n i g h t l y o r monthly b a s i s , a f i x e d sum

of money which i s t h e n pooled t o g e t h e r and given t o

members a t a time on 2 r o t a t o r y b a s i s (Ckcnjo,

unpublished work), This aim o r 1 ob jec t ive1 of

a s s i s t i n g members i n s x a l l - s c e l c c a p i t a l format ion

conforms with t h e savi.ngs encwragement o b j e c t i v e

of a s s i s t i n g members i n sma l l - s ca l e c a p i t a l f o r n a t i o n

conforms wi th t h e sav ings ericouragement o b j e c t i v e

e a r l i e r nu t ed,

Apar t from encouraging c a p i t a l fo rmat ion , through ,% '

s a v i n g s , the va r ious i n f o r tml f i n a n c i a l o rgan i sa t ions

a l so aim a t and perform c r e d i t funct ions by t . extending c r e d i t s t o deserving inves tors out of the

accumulated savings made from the per iodic contr ibut ions.

In the words of professor onoh: ' A good number of t he

t r a d i t i o n f i n a n c i a l ins t i - tu t ions perform c r e d i t

func t ions , prmviding c r e d i t t o t h e i r members, on

which i n t e r e s t i s charged by some assoc ia t ions , while

o the r s provide i n t e r e s t , f r e e c r e d i t . Some demand

some form of c o l l a t e r a l s e c u r i t y while o thers r e l y

on t he i n t e g r i t y of members, ( Onoh p .21)

Ljhile savings and c r e d i t funct ions remain t h k

dominant funct ions of these i n s t i t u t i o n s , other

func t ions a r e d i sce rn ib le among t h e various forms

of such organisat ions t h a t e x i s t , For example, t he

age grade assoc ia t ions perform c e r t a i n cicveloprnental

p ro j ec t s i n t h e v i l l a g e s e i t h e r vo lun ta r i ly o r

mandatorily, The various v i l l a g e funds a r e no t r a i sed

f o r credi t -extension as such but f o r developmental

p ro j ec t s ,

These various organisat ions a l s o form avenues

where people come together t o provide a l l s o r t s of

mutual a id t o each o ther , Those i n some kind of

f i n a n c i a l predicaments may he ba i l ed out of t h e i r

precarious s t a t e s through obt ianing some discount

se rv ices even where t h e i r tu rns f o r the r o t a t i n g funds

have no t matured,

A g r e a t ma jo r i t y of t h e s e a s s o c i a t i o n s a l s o

perform some s o c i a l f u n c t i o n s , f o r example a t

b u r i a l ceremonies 2nd o t h e r f e s t i v a l s .

ow ever, t h r i l t and c r e d i t f u n c t i o n s remain

t h e key f u n c t i o n s performed by ma jo r i t y of t h e

i n s t i t u t i o n s t h a t a r e i d e n t i I i a b l e .

ORGANISATI ON AND WLNkGEI'DINT : - Due t o t h e n a t u r e of t h e o r g a n i s a t i o n s , ( t h a t

i s t h e in formal n a t u r e of t h e i n s t i t u t i o n s ) t h e r e i s

no s o p h i s t i c a t e d o r g a n i s a t i o n o r management

s t r u c t u r e , f o r them. There may o r may no t be perhanent

l e a d e r s (onoh p .I 7) t h e r e o r g a n i s a t i o n s a r e u s u a l l y

very s i m p l i f i e d somctimcs r e q u i r i n g j u s t coming t o g e t h e r

of a few people t o mnkc t h e u s u a l c o n t i r i b u t i o n .

I n some arrangements, t h e r e a r e no formal meetings,

A de s igna t ed c o l l e c t o r merely goes round a t t h e

appointed t ime, and a p p l i e s t h e proceeds as mutual ly

agreed upon by members. where meetings a r e t o be

h e l d , such meetin@ a re u s u a l l y r o t a t e d among members

and t h e member who h o s t s a meeting au toma t i ca l ly

becomes t h e chairman of t h e day

There a r e no w r i t t e n laws, r u l e s o r r e g u i a t i o n s

t o gu ide t h e ope ra t ion of t h e o l d e r f i n a n c i a l u n i t s .

The convent ions , a r e however, known by members who

keep t o them and r e s p e c t then l i k e any w r i t t e n laws.

The f requency of meeting, t h e day, t ime and

p lace a s we l l a s t h e amount t c be pa id by each

member a r e usua l ly determind by genera l consensus o r

by t h e inner l eader s , where thcy e x i s t (onoh p.18)

The more rccen t organisa t ions of the t r a d i t i o n a l

o rgan i sa t ions , however, now 'n;lvc w r i t t e n guiding

c o n s t i t u t i o n s , a complete s e t of p r i n c i p a l o f f i c e r s

and even maintain bank accounts , f o r example t h e

s o c i a l c lubs , t h e f ~ j o or' , d a i l y con t r ibu t ion which

i s a v s r i a n t of t h e i susu , and i n f a c t almost a l l

o thers . This may be due t o t h e improving standard,

of educat ion and the r i s e i n l i t e r a c y r a t e ,

The na tu re of thzse organisa t ions a r e such t h a t

r equ i res l i t t l e f i n a n c i a l management, even a t t h i s

t h e i r new re-or ienta t ion .

Conformity t o t h e l a i d down r u l e s and

regu la t ions as w e l l a s the genera l conventions i s

ensured through the use of sanct ions. Any member

f o r example who d e f a u l t s i n r egu la r cont r ibut ions i s

s w c t i o n e d , and such a person r e a l l y f i n d s it

d i f f i c u l t t o gain accept*:nce i n t o any such informal

group,

-- --* REFERENCES

*- . Abe, S , I . . IfNigerian Jarmers and Their Finance

" Adeyeye, S.0, The Co-operative ~dvement i n Nigeria- Yesterda Today and Tgmorrow: (Cotting;;: Vandenhoen and Ruprecht 1978):

Ardener, S ,

I

Bedi, R.D. . Theory, History and P rac t i c e of Co- I operat ion 3rd ed,( lndia: Prabhat Press , Meernt 1962).

I I I . Bhatt , V.V. Devehpment Perspect ives Problems, I I

St r a t egy and Po, l lc les (Oxford: I Pergamon Press 1980).

I! I

. Bourne, Comptom: I1Structure and Performance of Jamalcan I Rural F inanc ia l Markets" Soc i a l and Economic Studies Volume 32 Number 1

i 1

March 'l983, .I Burda, Edward I, Consumer Fi.nance (Newyork: Harcourt

brace Joranovich Inc. 1975).

Calver t , H,G, The Law and P r inc ip l e s of Co-Operations (unpublished Work - London 1959). I

Quoted i n Enugu Consultants Report NO 6 1961,

Donaldson, Elvin Personal Finance 6 th ed, (Newyork : ) e t a 1 Ronald Press Company 1977).

MAgr icu l tu ra l Credi t Through Co-operatives a n d other institution^^^ F.A.o. Agr icu l tu ra l ' Studies No 68 1965

"Co-operative T h r i f t Credi t and Marketing I i i n Economicall~v Underdeveloped Countriesl1 I

Agr icu l tu ra l ~ e v e l o ~ m e n t paper No 34 U , N Rome '1959.

India , Committee of Direct ion; Report of " A l l Ind ia Rura l Credi t Survey Volume 111 Hombay 1934

.. Krivine, D ed, I1Fiscal and Monetary Problems i n Developing S t a t e s (New York : 1967).

METHOD OF R E S W C H 4.

3.1. DETERMINATION OF P0IDUT;ATION:

The nature of the current study i s such tha t t h e

population i s not well defined', This i s due to the Tollotrlng

reasons( s)': - Informa.1 f inanc ia l o r g m i sa t ions , as: the name implies,

i s informal i n nature, There i s no record of the number ,md