Embed Size (px)

Citation preview

University of Nigeria Research Publications

TAKON ,Samuel Manyo

Aut

hor

PG/M.SC/03/37078

Title

Testing the Effectiveness of Camel Rating Model in Predicting Bank Distress in

Nigeria

Facu

lty

Business Administration

D

epar

tmen

t

Banking and Finance

Dat

e

November, 2006

Sign

atur

e

TESTING THE EFFECTIVENESS OF CAMEL RATING MODEL IN PREDICTING BANK DISTRESS IN NIGERIA

TAKON SAMUEL MANYO Reg. No. PGIM. SC103137078

DEPARTMENT OF BANKING AND FINANCE UNIVERSITY OF NIGERIA

ENUGU CAMPUS

NOVEMBER, 2006.

TITLE PAGE

TESTING THE EFFECTIVENESS OF CAMEL RATING MODEL IN PREDICTING BANK DISTRESS IN NIGERIA

TAKON SAMUEL MANY0 PGIM. SCl03137078

AN M.SC DISSERTATION SUBMITTED IN PARTIAL FULFILMENT OF THE REQUIREMENTS FOR THE AWARD OF THE DEGREE OF MASTER OF

SCIENCE (M.SC) IN BANKING AND FINANCE

DEPARTMENT OF BANKING AND FINANCE UNIVERSITY OF NIGERIA

ENUGU CAMPUS

NOVEMBER, 2006.

CERTIFICATION

This is to certify that this M.Sc Dissertation by Takon, Samuel Manyo

(PGIM SCl03137078) presented to the Department of Banking and Finance,

University of Nigeria, Enugu Campus is original and has not been submitted for

award of any degree or diploma either in this or any other tertiary institution.

This is to certify that this M.Sc Dissertation by Takon, Samuel Manyo

(PGlM.SCl03l37078) presented to the Department of Banking and Finance,

University of Nigeria, Enugu Campus, meets the departments requirement and

has been submitted in partial fulfillment of the requirements for the award of M.Sc

Degree in Banking and Finance.

m4.* DR. B.E CHIKELEZE (Supervisor)

(+&- RS N J MODEBE Date 1

( ~ e d d L of Department)

i i i

DEDICATION

This work is dedicated to my family members, especially my wife Helen and

children Jamima and Enun Takon and all men of goodwill.

ACKNOLEDGEMEMTS

What can one do without first recourse to the MAKER. Life, knowledge, good

health, vision, blessings, protection and all come from Him. What He wills come to

pass. My deepest and profound appreciation goes to GOD ALMIGHTY for His

mercies and kindness towards me all the time.

My profound gratitude goes to my research supervisors, Dr. A.M.O. Anyafo

and Dr. B.E. Chikeleze for all the pains taken to read every bit of the work as well

as their frank criticisms

I am equally grateful to the entire members of the Department of Banking

and Finance, U.N.E.C. for their friendliness, encouragements, co-operation and

transparency in handling every case 1 presented before them. Special thanks to

my Head of Department, Banking and Finance, Mrs. N.J. Modebe, Prof. F.O.

Okafor, Prof. C.U Uche, Dr. (Mrs.) Ogamba and Mr. Egbenta of the Department of

Estate Management, U.N.E.C for their precious counsels.

Special thanks to my wife Helen, for her prayers, financial and material

support, and all inconveniencies she patiently endured throughout this

programme. I lack words to express my deep appreciation to one of my mates and

friend, Fidelis Atseye, for his wonderful contributions to the success of this

research work.

I remain immensely grateful to my brothers and in-laws, pastor

Roland Takon, William Takon, Mr. E.A. Ogbe and family Bassey Obaji for their

financial and moral support.

Others solidly behind me were Victor Egba of the NDIC, Mr. Ebuta, Senior

Manager UBA, Mr. Victor Agunwah, Mr. Sylvester Anyanor of the First Bank and

Mr. Sunday Nwite for their financial and material support. My sister Mbamba

Takon and my children, who were always rallying round me in order to encourage

me, are not left out. I equally thank Miss Precious lkpo of Helitze Consult and Miss

Modesty Udeaku of God Makes The Difference Biz Center for the nice typing work

done to this study.

Finally, I thank those who must have contributed in one way or the other to

the successful completion of this study. I say may the Almighty God reward them

abundantly.

TAKON,S.M.

DECEMBER, 2005

ABSTRACT

Distress in the Nigerian banking sector has a long history. Between 1950

and 1954 as a result of poor capitalization, incompetent management, poor

accounting records, weak deposits, amongst others, the banking industry

witnessed financial crises that led to the failure of 21 indigenous banks, The

enactment of 1952 and 1958 ordinances did not solve the problem.

After the deregulation of the banking industry in the early 1990's the

banking crises re-surfaced which led to the liquidation of 26 distressed banks by

the CBN in 1998. This created widespread financial panic arid loss of public

confidence.

Considering the fact that bank distress has a multiplier effect on the

economy, there is need for a robust predicting model that will serve as an early

warning signal as to reduce the occurrence of distress. This study attempted a

test of the effectiveness of the CAMEL model in predicting bank distress in

Nigeria.

Data for this study were collected from published annual reports and

accounts of 12 banks between

distressed and non-distresses

technique was utilized.

the period 200

groups of six

i - 2004. The banks were under the

banks each. A random sampling

, In order to achieve objectives of the study, two statistical tools were

employed in the analysis of data: 'Multiple Discriminant Analysis (MDA) and

Multiple Regression Analysis using the SPSS.

MDA Model was initially used by Altman in 1968 to predict corporate

bankruptcy. This theoretical framework has come to be known as Altman 2-score.

In the second analysis, the CAMEL was regressed against the Z-score in order to

determine their impact on the prediction of distress

vii

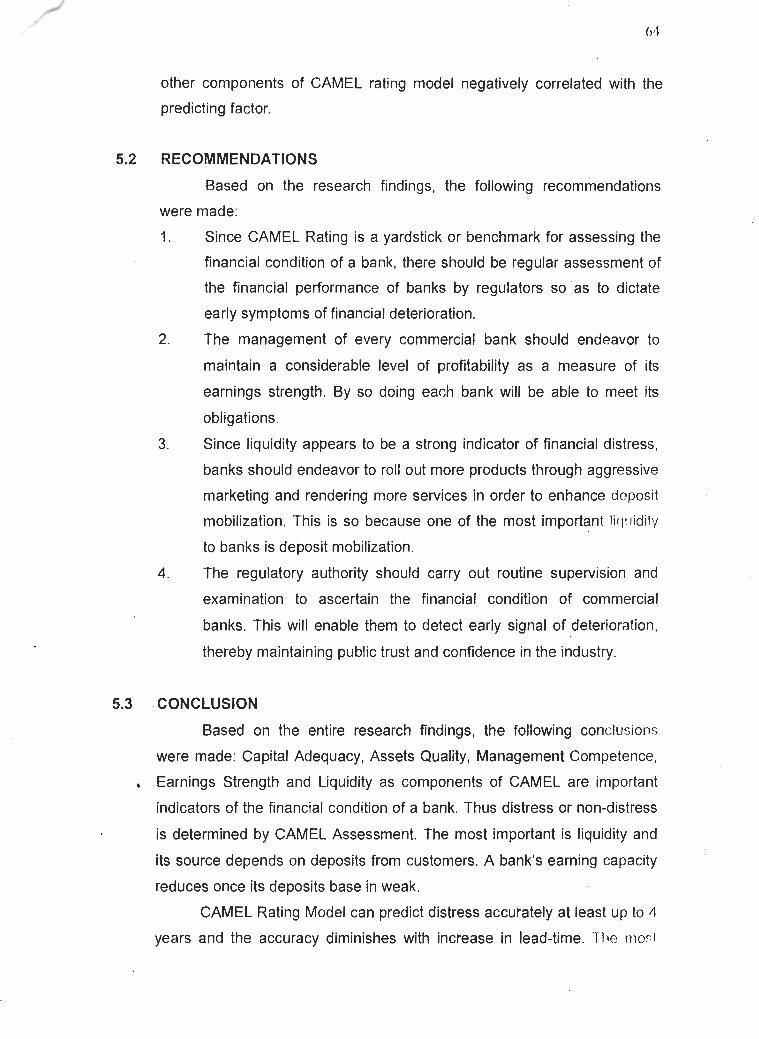

The results show that all of the observed CAMEL ratios exhibit a

deteriorating trend as distress approaches. The regressed estimates show that all

components of the CAMEL Rating have a significant relationship with the variable

(Z-score). Apart from earnings strength, all the other components of CAMEL rating

model negatively correlated with the predicting variable.

viii

TABLE OF CONTENTS

Title Page

Certification

Dedication

Acknowledgements -

Abstract - -

Table of Content - -

List of Tables- -

List of Appendixes -

CHAPTER ONE: INTRODUCTION

Background of the Problem

Statement of the Problem -

Research Objectives

Research Questions -

Research Hypotheses -

Scope of the Study - -

Significance of the Study -

Definition of Terms - -

References

CHAPTER TWO: REVIEW OF RELATED LITERATURE

2.1 Prediction of Bank Distress: Theoretical Framework -

iv

- vi

viii

xi

xii

Symptoms and Causes of Bank Distress- -

Symptoms of Bank Distress - - -

Causes of Bank Distress - - - -

Failure Resolution Measure Adopted In Nigeria -

Camel Assessment in Relation to Bank Distress

Capital Adequacy - - - - -

Measurement of Capital Adequacy - -

Fixed Minimum Capital Requirement - - Limitation of Lending Limits - - -

Weighted RiskIAsset Ratio- - - -

Implication of Bank Distress - - -

Studies and Models in Predicting Bank Distress

The Early Warning Models - - - -

Critical Variables Considered in Previous Studies

References

CHAPTER THREE: RESEARCH METHODOLOGY

Research Design - - - - - - - 3 9

Sources of Primary and Secondary Data- - - - 3 9

Methods of Data Collection - - - - - 3 9

$opulation and Sample Selection - - - - - 40

Theoretical Model and Data Analysis - - - - 40

Rationale for Using Multiple Discrminnant Analysis (MDA)

in this study - - - - - - - - 4 1

X

Model Specification - - - - - - - 42

Variable Definition - - - - - - - 43

Techniques of Data Analysis - - - - - 44

Statement of Null and Alternate Hypotheses - - - 44

Hypotheses Test Statistics - - - - - - 45

References

CHAPTER FOUR: DATA PRESENTATION AND ANALYSIS

Introduction - - - - - - - -

Presentation of Data - - - - - - -

Data Analysis and Presentation - - - - -

Computing "Critical Value" To Determine Distress and

Non-Distress Group - - - - - - -

Presentation of Regression Results - - - -

Discussion of Findings - - - - - - -

Test of Hypotheses - - - - - -

Summary of Findings - - - - - -

CHAPTER FIVE: SUMMARY, CONCLUSION AND RECOMMENDATION

5.1 Summary - - - - - - - 63

5.2 Recommendations - - - - - - 64 a

5.3 Conclusion - - - - - - 64

5.4 Suggested Area for further Study - - - - - 65

BIBLOGRAPHY

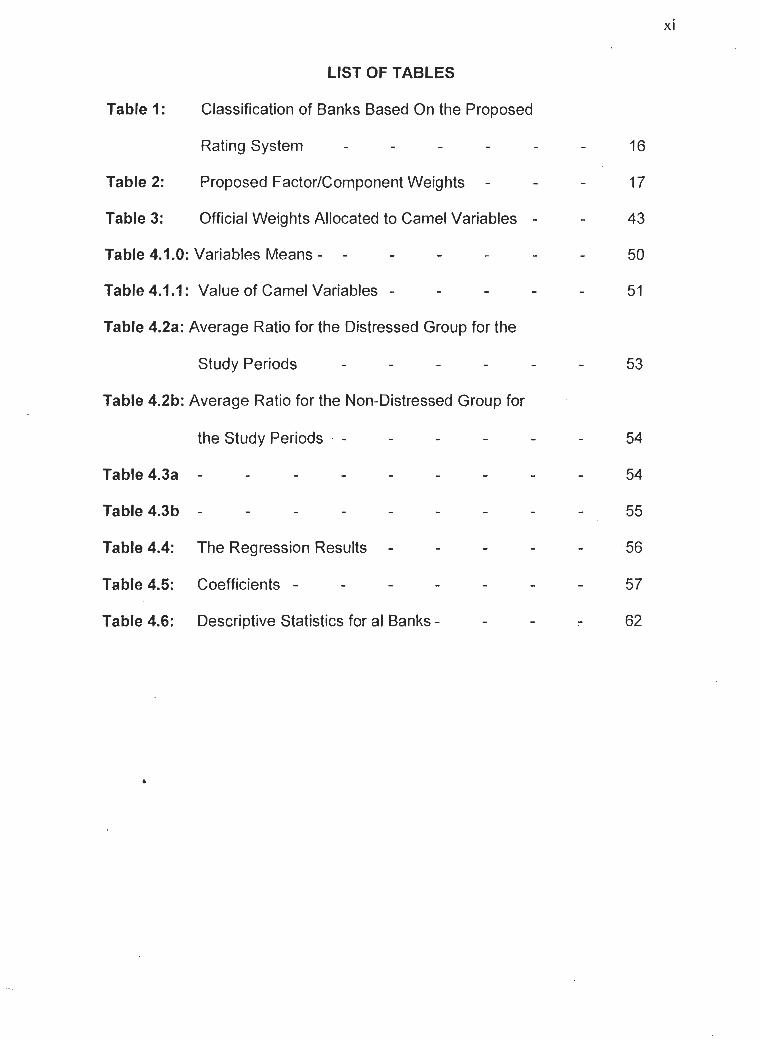

LIST OF TABLES

Table 1: Classification of Banks Based On the Proposed

Rating System - - - - -

Table 2: Proposed Factor/Component Weights - -

Table 3: Official Weights Allocated to Camel Variables -

Table 4.1 .O: Variables Means - - - - - -

Table 4.1 .I : Value of Camel Variables - - - -

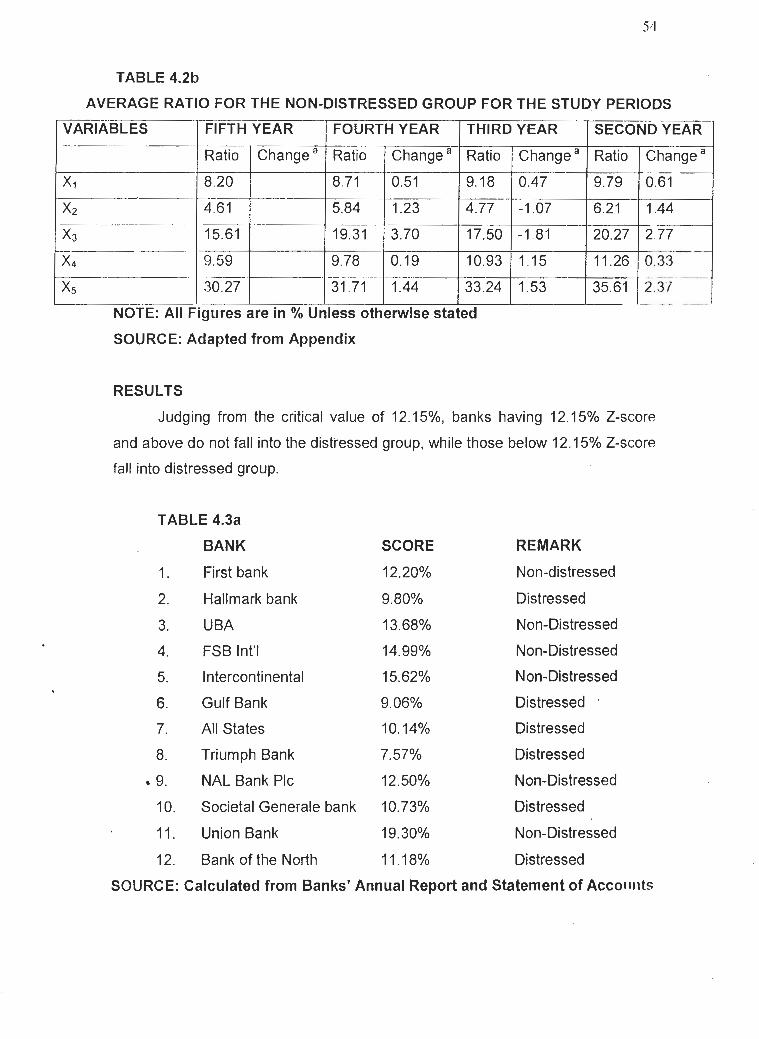

Table 4.2a: Average Ratio for the Distressed Group for the

Study Periods - - - - -

Table 4.2b: Average Ratio for the Non-Distressed Group for

the Study Periods . - - - - -

Table 4.3a - - - - - - - -

Table 4.3b - - - - - - - -

Table 4.4: The Regression Results - - - -

Table 4.5: Coefficients - - - - - -

Table 4.6: Descriptive Statistics for al Banks - - -

xii

~ppendix 1 - - Appendix 2 - - Appendix 3 - - Appendix 4 - -

LIST OF APPENDICES

CHAPTER ONE

INTRODUCTION

1.1 BACKGROUND OF THE PROBLEM

Modern Banking operations started in Nigeria in 1892 when the

British Colonial authorities established the African Banking Corporation

(ABC) for the purpose of distributing currency notes of the Bank of England

(NDIC, 1997).

The problem of distress in the banking sector in particular and the

financial system in general also has a long history. It dates back to the

establishment of the Central Bank of Nigeria in 1959.

During the colonial days, expatriate banks then served the interest of

the foreigners only. To redress this, Nigerian entrepreneurs went into

banking between 1920 and 1950 as to meet the financial needs of

Nigerians. See for example, Uche (1996) and (2000).

Due to the problem of inadequate capital and unfair competition from

foreign banks, 21 out of 25 banks established up to 1954 became

distressed and failed. However, the intensity, scope and dept of the current

distress condition since 1989, has been more serious in many ways

unprecedented. Within the late 1990s a large number of operators in the

country's banking system were in severe distress, a situation that has

caused regulatory authorities to put several measures in place as to arrest

the deteriorating trend.

Doguwa (1996) observed that the increased risks assumed by the

commercial and merchant banks, poor quality of loans and a'dvances.

mismanagement, fraud and local national economic trends, amongst other

things, were responsible for the increase in the number of problem banks in

, Nigeria. Between 1989 and 1997, the operating environment for

commercial and merchant banks became generally unstable due to civil

disturbances, industrial unrest, high inflation, negative real interest rates

and low public confidence, mainly as a result of distress in banks. In 1998,

the CBN liquidated 26 distressed banks made up of 13 commercial and 13

merchant banks after realizing that these banks were irredeemable and

terminally distressed. Before then, five other banks had been liquidated in

1994 and 1995. The distressed episode eroded public confidence in the

Nigerian Banking system, thereby encouraging a lot more people to

patronize the informal sector.

Despite the effort by the regulatory authorities to arrest this ugly

situation, the outcome has not been completely satisfactory as the problem

still persisted.

Bank distress therefore serves as a signal, hence an early warning

to the regulatory authorities and the general public.

According to Doguwa (1996), a number of factors make an effective

statistical early warning system desirable, especially in aiding regulatory

authorities respond efficiently to initial signs of distress. First, significant

changes in a bank management policies and financial condition can occur

between examinations. Second, an on-site examination is a lengthy and

expensive process and not always the most cost effective method of

tracking small, but important changes in bank's financial condition. Third,

although examiners generally are sensitive to the developing trends that

indicate potential future management or financial problems and normally

comment on such problems or matters in their reports, they must

necessarily emphasize their findings concerning the actual condition of the

bank rather than the estimated impact of potential problem. ~ourth, an

examiner's findings are part of the official record and could provide the

basis for the enforcement or other supervisory actions. In practice,

statistical early warning measure can be informal; affording the opportunity

for experiments with techniques to uncover financial weakness at its

earliest stages. Moreover, an efficient early warning system can be a useful

tool of analysis in the appraisal of a bank's financial condition.

1.2 STATEMENT OF THE PROBLEM

Conceptually, two major forms of problems could confront a bank

like many other profit-seeking organizations, the world over. These are

problems of illiquidity and insolvency. Both are sources of worry for owners

and management of banks as well as monetary authorities.

The increasing problem of bank distress in Nigeria especially in the

1990's has refocused attention on efforts to identify problem banks and to

predict distress/failures with sufficient lead time of regulators and

management as to institute remedial action to prevent them from going into

insolvency. Apart from the regulators and management, those who share

the concern in this issue include the depositors, bankers, shareholders and

the general public. The recent increase in the capitalization requirement for

commercial banks by the Central Bank of Nigeria is a pointer to the

aforesaid.

Accordingly, Nigerian Banks are required to have a minimum capital

of N25 billion (Twenty five billion naira) with effect from January 2006.

However, capital adequacy is not the only index for assessing the strength

or weakness of commercial banks. Other indices (variables) used in

identifying distressed banks are captured by the "CAMEL Assessment".

What constitutes a problem in this research report is the

effectiveness of CAMEL rating model in predicting bank distress in Nigeria.

RESEARCH OBJECTIVES.

In the light of the above problems identified in the preceding section,

the major objectives of the research was to determine the effectiveness of

CAMEL Rating Model in predicting bank distress in Nigeria.

Specifically, the research was designed to achieve the following

objectives:

To determine the impact of capital adequacy in predicting bank distress in

Nigeria.

To determine the impact of asset quality in predicting distress in the

Nigerian banking industry.

To determine the impact of Management competency in predicting bank

distress in Nigeria.

4. ,To determine Earnings Strength in predicting bank distress in Nigeria.

5. To determine the impact of Liquidity in predicting bank distress in Nigeria.

1.4 RESEARCH QUESTIONS

1. What is the impact of Capital Adequacy in predicting bank distress?

2. What is the impact of Asset quality in predicting bank distress?

3. What is the impact of management competency in predicting bank

distress?

4. What is the impact of Earnings strength in predicting bank distress?

5. What is the impact of liquidity strength in predicting bank distress.

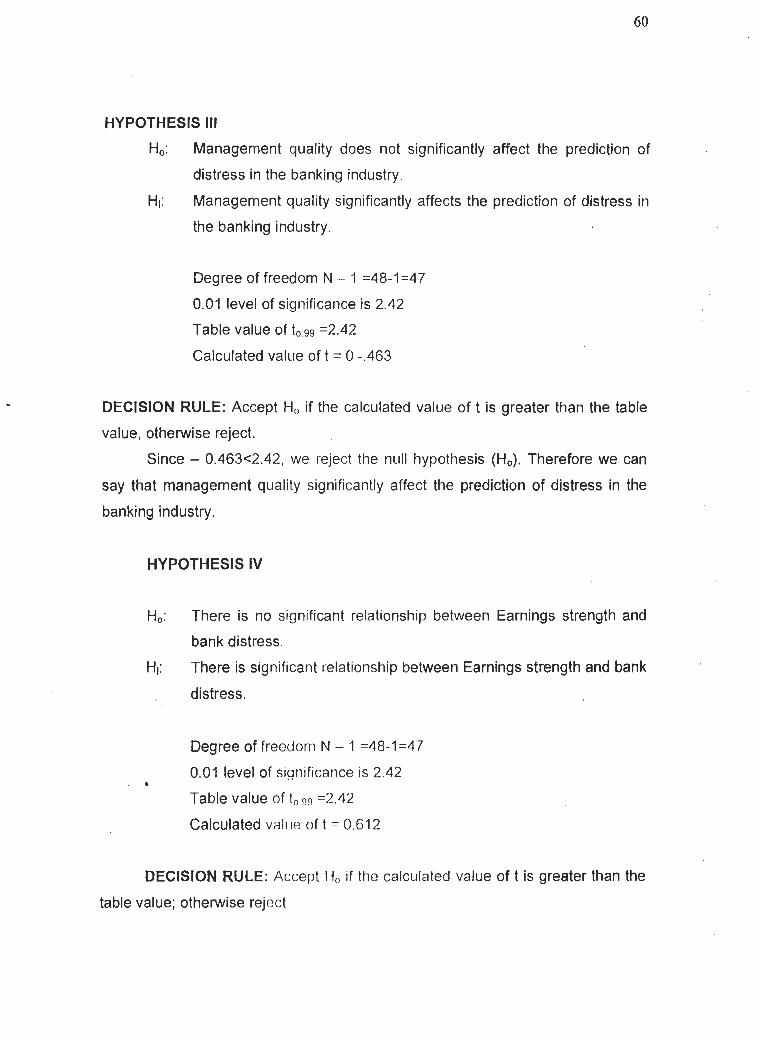

RESEARCHHYPOTHESES

There is no significant relationship between Capital Adequacy and the

prediction of bank distress.

There is no significant relationship between Asset Quality and the

prediction of bank distress.

There is no significant relationship between Management Competency and

predicting of bank distress.

There is no significant relationship between Earnings Strength and

predicting of bank distress.

SCOPE OF THE STUDY

This study is restricted to commercial banks in Nigeria.

Currently there are 89 commercial banks in the Nigerian banking industry.

As a result of the researcher's inability to lay hands on their Annual reports

and Accounts, some banks that have already been identified with distress

symptoms are excluded. They include Fortune Bank Plc, Savannah Bank

Plc, etc. Therefore, 83 commercial banks wme targeted for the study.

The study period spanned 2001 - 2004. This period is significant

because it marks the beginning of a new decade. Moreso, previous studies

were carried out prior to this period.

SIGNIFICANCE OF THE STUDY

The significance of this study is borne out of the vantage position the b

banking sector occupies in an economy in terms of financial leverage,

capital formation, provision of an efficient payment system and facilitating

the implementation of monetary policies. Banks are catalysts in the

economic system and virtually all economic activities revolve round the

bank, therefore, its collapse would be so contagious to the extent that other

sectors of the economy may be paralyzed.

In the light of the above, any case of mass bank failureldistress

especially in a developing economy like ours could be seen as a macro-

economic issue which should be properly handled to sustain public

confidence. As at December, 1995, the market share of 60 distressed

banks in deposit mobilization was N70 billion, constituting 33.5 per cent of

total industry deposit of N211 billion, and loans and advances of N66.5

billion constituting 38 per cent of the industry's total loans and advances of

N175.9 billion. These facts and figures therefore lend confidence to the

significance of the study in order to avert a collapse of the financial system

and ensure that the banking industry remains safe and sound. Beside their

uses by supervisory authorities, problem banks identification models could

be of great value to the management of any bank. For instance,

identification models that provide quantitative estimates of weights of key

financial variables in the determination of the probability of distresslfailure

could be used by them to determine its probability of failure or distress.

Lastly, for fact that the issue of bank distress is no respecter of the

level of economic development, developed or developing, failureldistress

resolution options in the industry should be taken with all seriousness by

the regulatory authorities. Without doubt, this study should be able to make

some useful recommendations of how distress syndromes in the Nigerian

banking system could be resolved amicably.

1.8 DEFINITION OF TERMS

Some of the terms used in the study are explained hereunder so that

the study could be easily comprehended by any non-professional. .

1. DISTRESS

A bank is said to be distressed when it is unable to meet its , b

obligations to the customers, as well as the owners and the economy. Such

inability, often results from weakness in its financial, operational and

managerial conditions which would have rendered it either illiquid andlor

insolvent (CBNINDIC 1995).

2, INFORMAL FINANCIAL SECTOR

This describes entities and other financial transactions not directly

open to control by fundamental monetary and financial policy instruments

that are not regulated. It consists of borrowing and lending amongst

individuals and firms that are not registered with government as financial

intermediaries and are not subject to government supervision.

3. REGULATION

This means a body of specific rules of agreed behaviour, either

imposed by some government or other external agency or self-imposed by

explicit or implicit agreement within the industry that limits the activities and

business operation or financial institutions (NDIC, 1997).

4. REGULATORY AUTHORITIES

Within the context of this study, the Central Bank of Nigeria (CBN)

and the Nigerian Deposit Insurance Corporation (NDIC) constitute the

nation's regulatory and supervisory authorities for the nation's banking '

sector. They therefore act as the representative of the federal government.

5. INSOLVENCY AND ILLIQUIDITY

According to Uche (1996), Insolvency refers to a condition in which

the sum of assets of a firm is less than the sum of its liabilities (Jimoh,

1993).

6. BANK FAILURE

For the purpose of this study, bank failure is the inability of a bank to

meet its obligation to its customers, owners and to the economy

, occasioned by a fault of weakness in its operation, which had rendered it

either illiquid or insolvent.

7. PROBLEM BANK

For the purpose of this study, problem bank is used for the likely

distressed bank. They are therefore used interchangeably.

According to Sinkey (1975) a problem bank is one that, in the eyes of the

Federal banking agencies, has violated a law or regulation or engaged in

an "unsafe or unsound" banking practice to such an extent that the present

or future solvency of the bank is in question.

8. CAMEL

Camel is a measure applied to assess the quality of bank

management and interpreted as follows:

C = Capital Adequacy,

A = Asset quality,

M = Management Quality,

E = Earnings strength and

L = Liquidity.

It is a measure for judging .how well managed a bank is or the degree of the

bank's mismanagement (moral hazard behaviour) and establishes the level of

capital adequacy of a bank. (ONOH 2002)

REFERENCES

CBN INDIC (1 995), "A study of Distress in the Nigerian financial Services

Industry".

Doguwa, S.1 (1996), "Early Warning Models for the ldentification of Problem

Banks in Nigeria1', CBN Economic and financial Review, Vol. 34 (NO.l),

462- 487

Jimoh, A. (1993), "The Role of Early Warning Models in the ldentification of

Problem Banks; Evidence from Nigeria", Nigeria Financial Review, Vo1.6

(NO. 1),29-40

NDlC (1997), "Safe and Sound Banking Practices in Nigeria, Selected Essays; by

John U. Ebhodahe",

Onoh, J.K. (2002), "Dynamics of Money, Banking and Finance in Nigeria -An

Emerging Market" P 220.

Sinkey, J.F (1975), "A Multivariate Statistical Analysis of The Characteristics of

Problem banks", The journal of Finance NO.l, 21-36.

The Research Department, Nigerian Deposit Insurance Corporation (NDIC, 1997),

"A Study of Distress in the Nigeria Financial Services Industry" by Peter

Umoh (Ed.) F S R C L NDlC Publication.

Uche, C.U (1996) , "The Nigerian failed Bank Dec~ee; A Critique, "Journal of

Inten~ational Banking Law", Vol. 11 (issue 10). 436-441.

6

Uche , C.U (2000), "Banking regulation in an era of structural Adjustment. The

case

of Nigeria", Journal of Financial Regulation and compliance Vol. 8-(NO .2)

157-165.

CHAPTER TWO

REVIEW OF RELATED LITERATURE

PREDICTION OF BANK DISTRESS: THEORETICAL FRAMEWORK

Literally, the term "Distress" is used to describe a bank or a financial

institution that is facing financial difficulties. It is a state of "inability" or

"weakness" which prevents the achievement of set goals and operations.

Bentson (1986), associates distress with a cessation of independent

operations or continuance only by virtue of financial assistance from the

banking system's safety net such as the supervisory/regulatory agency or a

deposit insurer. Ologun (1994) describes a financial institution as unhealthy

if it exhibits several financial operational and managerial weaknesses.

Predicting corporate failure or bankruptcy may be credited to two

distinguished scholars for their pioneering works: Secrit (1938) and Altman

(1968), Secrit's theoretical model was designed to identify symptoms of

failure and non-failure of banks. In his Autopsy and Diagnosis, he examined

seven hundred and forty one (741) national banks that failed between 1920

and 1930 and one hundred and eleven (1 11) that did not fail prior to 1933 as

to "source indication of likely survival or of deathV.This

comparative analysis utilized discriminatory theoretical framework.

Altman (1 968) in his work on financial ratios and discriminant analysis

employed the Multiple Discriminant Analysis (MDA) framework to predict

corporate bankruptcy.

Another modeling approach that classified banks into problem and

non-problem group is the Logit Model. This has been the conceptual

framework adopted by Jimoh (1993), Ako (1999), Doguwa (1996), West

(1985) and Sinkey (1975).

From the foregoing, early warning models are anchored on the above

theoretical frameworks-Multiple Discriminant Analysis and Logit Models. See

also Nyong (1994) and Martin (1977).

SYMPTOMS AND CAUSES OF BANK DISTRESS

SYMPTOMS

The symptoms of bank distress are varied in nature but the most

common observable ones as indicated by Oguneleye (1993), include the

following:

late submission of returns to the regulatory authorities;

falsification of returns;

rapid staff turnover;

frequent top management changes;

inability to meet obligation as at when due;

use of political influence;

petition/anonymous letters;

persistent adverse clearing position;

borrowing at desperate rates;

persistent contravention of laid down rules;

weak deposit base;

inadequate capitalization; and

persistent overdrawn current account position at the CBN.

CAUSES OF BANK DISTRESS

The broad causes of bank distress particularly in Nigeria include, but

are not limited, to the following:

Policy and Regulatory Environment:

Prior to the adoption of comprehensive economic reform programme

under the Structural Adjustment Programme (SAP), the Nigerian banking

system could simply be described as highly regulated. Some of these

regulations had sometimes been counter-productive and had contribuled to

the strains in our banking system. Banks were subjected to some restrictions

thereby limiting their ability to adapt to changing market conditions. The

government had generally in the past made the control over banks an

important tool of the country's economic development strategies. Some of

the policies manifested in the form of direct control and the establishment of

interest rate ceiling as well as the restrictions on entry into the banking

industry. The adoption of such measures, though sometimes imperative,

exposed many weak banks and threatened them with illiquidity and

insolvency.

(b) Capital Inadequacy:

A function of capital in a bank is to serve as a means by which losses

can be absolved. It provides a cushion to withstand abnormal losses not

covered by current earnings, enabling banks to regain equilibrium and to re-

establish a normal earnings pattern. The problem of inadequate capital has

been further accentuated by the huge amount of non-performing loans which

has eroded some banks' capital base.

(c) Economic Downturn:

The adverse economic condition in Nigeria since mid 1981 had been

characterized by high inflation, depreciating value of the Naira, large fiscal

deficits, heavy external and internal debt, overhang and slow growth. Arising

from this stress in the economy, many borrowers were unable to service

their loans thereby making many banks to come to severe crises.

(d) ' Borrowing and Lending Culture:

This problem of economic downturn has been exacerbated by the

altitude of some borrowers who are unwilling to repay even when they are

known to have the means to service their debts. There are also some

"professional" borrowers who through connivance with some banks staff take

bank loans with no intention to repay them, These problems greatly impaired

the quality of the banks' assets as non-performing loans and advances

become unbearable and turn out to be a high burden on many of them. b

(e) Asymmetric information:

This is described as a situation whereby a borrower taking,out a loan

has superior information about the potential returns and the risk associated

with the investment project than the bank lending the money. This problem

of asymmetric information is often rampant in an unstable economy as loans

are likely to extend for risky projects and borrowers may have incentives to

misallocate funds for personal use or invest them in unprofitable projects.

Some loans are being diverted for personal use and for projects not meant

for such loans.

(f) Poor Corporate GovernmentIManagement:

It has become a worldwide dictum that the quality of corporate

governance or management makes an important difference between sound

and unsound banks. Just as it is in other parts of the world, so it is

established in Nigeria that mismanagement is the main culprit causing

banking crises. A very significant characteristic of mismanagement is in the

negative attitude and behavior of bank managers which is difficult to reverse

by the application of external policies and measures.

The common types of mismanagement which include technical

mismanagement, cosmetic mismanagement, desperate mismanagement

and fraud are often identified to be common in banks, and are prominent in

banking industry and they often undermine the health of our banks.

(g) Aftermath of Competition:

The deregulation of the economy has brought about, increased

competition and innovation in the market place. The increasing competitive

environment, allocative and operational efficiency require that inefficient and

marginal firms be crowded out and allowed to go under. In a way, it is a

paradox that while competition enhanced the menu of bank products

available to customers such competition has indirectly caused the insolvency

and failure of some banks in Nigeria through increased cost schedules.

(Adeyemi, 1993).

2.3 FALIURE RESOLUTION MEASURE ADOPTED IN NIGERIA

Depending on the severity and peculiarity of the situation, the

Regulatory Authorities in Nigeria have over the years, successfully adopted

the following measures among others to address bank distress.

(i) Accommodation facilities were granted to ten (10) banks which had liquidity

crises to the tune of N2.3 billion in 1989 following withdrawal'of pirblic

sector funds from commercial and merchant banks and the transfer of

same to CBN during that year.

(ii) Take-over of management and control of twenty-four (24) distressed banks

by the Regulatory Authorities to safeguard their assets.

(iii) Acquisition, restructuring and sale of seven (7) distressed banks to new

investors.

(iv) Closure of 26 terminally distressed banks that failed to respond to various

regulatory / supervisory initiatives. While the liquidation of Savannah Bank

of Nigeria and Peak Merchant Bank were suspended due to court action, it

is noteworthy that all the banks were closed with minimal disruption to the

banking system.

(v) . The promulgation and implementation of the failed Banks (Recovery of

Debts) and financial Malpractices Decree No.18 of the 1994 was to ensure

speedy dispensation of justice. The main thrust of the Decree was to assist

the recovery of debts owed to failed banks and to punish individuals

involved in the monumental incidence of financial malpractices in the

distressed banks. The initiative was indeed a complimentary measure.

The highly acclaimed implementation of the Failed Bank' Decree

which was facilitated by the Regulatory Authorities was indeed a major

plank in the resolution to contain distress and promote the soundness of

the Nigerian banking system. Following the implementation of the Decree a

reasonable amount of recoveries had been made.

As part of failure resolution measures the Nigeria Deposit Insurance

(NDIC) continues to serve as the liquidator to 34 closed banks. The

-corporation's activities in this regard include the following:

(a) Payment of Liquidation Dividend to Depositors:

In addition to the payment of insured depositors of the closed banks,

depositors with credit balances in excess of the insured limit were paid

liquidation dividends based on the volume of proceeds of the closed banks

assets realized by the corporation.

Payment of Liquidation Dividend to General Creditors:

Liquidation dividend has also been paid to some general creditors of

some of the banks.

The combined effect of these measures was a significant'reduction

in the level of distress in the banking system as well as enhancement of the

public confidence in the system.

CAMEL ASSESSMENT IN RELATION TO BANK DISTRESS.

The majority of prior research for prediction of bank distress focused

on capturing information representative of capital adequacy (c) Asset

quality (A),management quality (M), Earnings (E), and Liquidity (L) which

are designated as CAMEL rating or Model. The choice of these factors

occurs based on the theory that each is representative of a majorcelement

in a bank's financial statement. Earlier studies such as Sinkey (1975),

Altman (1977), Martin (197'7), Hanweck (1984) and Barth et al (1985)

analysed the financial characteristics of banks and of saving and

associations.

Accordingly, these studies adopt more or less the same variables,

based on the five categories of CAMEL. A weakness in any of these

variables may present a threat to the bank's continuing existence. One of

these threats represented in CAMEL exists in covering loan repayment

defaults and off-set the threat of losses or large withdrawals that might

occur. A measure of capital adequacy (C) represents past income

with its cushion to absorb future losses and that of Earnings (E) describes

present income. Both can assist in covering threats of losses. The

management (M) factor opens or closes t k door to risk, as management

takes action with assets and makes decisions related to capital and

earnings.

CAMEL was originally developed by the FDIC for the purpose of

determining when to schedule an on-site examination of a bank (Thomson,

1991). This related to the likelihood that bank distress may result when any

of the five factors is inadequate. Although researchers have a common

adherence to the broad guide-lines available in the CAMEL criteria,

previous studies for prediction of bank distresslfailure contained no

consistent set of CAMEL measures.

In Nigeria, an institution that has not met the minimum capital

adequacy and liquidity ratios may have manifested some symptoms of

distress without providing a good measure of the extent of distress.

In order to derive an efficient measure of distress through the

establishment of thresholds, attempts have been made at developing a

composite measure based on these CAMEL parameters for supervisors to

determine on a uniform platform, the extent of distress in each of the banks

as and by extension in the financial system as a whole. Such measure can

then be calibrated into a rating category like sound, weak, distressed,

terminally distressed, etc (NDIC, 1995). The usefulness of the CAMEL

criteria for prediction of distress exists in establishment of a foundation for

understanding a bank's health. As the FDIC does not divulge the details of

the representative measures for CAMEL, the ensuring complication for

researchers arises in determining which measures best correspond to the

five CAMEL factors. Typically, in the past, researchers collected a variety of

measures relating to each of the factors with variable selection often

occurring as a function of a statistical method, such as step wise regression

or factor analysis.

Lane et al (1986), included 21 ratios representative of factors in

CAMEL, Martin's (1977) and Tam and Kiang (1992), employed 19 variables

covering 4 CAMEL categories, Looney et al (1989) and Lane et al (1986)

used a step-wise approach to narrow their set of variables from 21 to 4.

Majority of the studies examined only four of the CAMEL factors and

excluded representative measure for management, as it proves to be the

most difficult to capture.

A composite measure could equally be used. This simply is a

weighted average of the CAMEL parameters summed up to unity (100%).

The monetary authorities in Nigeria recently embarked on the

development of a rating system for banks. This was initiated jointly by the

CBN and NDIC and the drafting rating system provides for classifying

banks as shown below, given their composite scores.

TABLE l

CLASSIFICATION OF BANKS BASED ON THE PROPOSED RATING SYSTEM

CLASS COMPOSITE SCOPE (%)

86 - 100

71 - 85

56 - 70

41 - 55

0 - 4 0

Source: NDiC Quarterly Voi. 7 SeptIDec. 1997

RATING -1 Very sound 1 Sound

Satisfactory

Marginal

Unsound

Details of weights and financial ratios used for assessing each CAMEL

factors are also shown in Table 11.

TABLE ll

PROPOSED FACTORICOMPONENT WEIGHTS

-

FACTOR

CAPITAL

-- - - - - . - ASSET QUALITY

MANAGEMENT

LIQUIDITY

COMPONENT

a. Capital to Risk Assets Ratio.

b. Adjusted Capital Ratio

c. Capital Growth rate

a. Non-performing Risk Asset to total Risk Assets

b. Reserve for losses to non-performing Risk Assets

c. Non-performing Risk Assets to Capital and Reserve

a. CAELl85 b. Compliance with

Laws & Regulation a. Profit before Tax to

Total Assets. b. Total Expenses to

Total Income c. Net lnterest lncome

to total Earning Assets

d. lnterest Expenses to Total Earnings Assets

a. Liquidity Ratio b. Net loan and

Advances to Total Deposits.

TOTAL

Source,: NDIC QUARTERLY Vo1.6 (Nos 3 x 4)

SeptlDec. 1996.

2.5 CAPITAL ADEQUACY

COMPONENT WEIGHT (%)

15

The capital of a firm can be defined as the money that has to be

raised as to purchase real assets. Hence, it can be taken to be the net

worth (assets less liabilities) of a firm. What then constitutes an adequate

measure of capital in any organization? For incisive and thoughtful

explanations, we shall limit adequacy of capital concept to commercial

banks' fund. What constitutes a commercial banks' fund or capital is its own

fund consisting mainly of: share holders' funds, long term debt, deposit and

other short term liabilities.

The share holders' funds normally is a composition of paid-up

capital, share premium, statutory reserves, profits for distribution and other

reserves. For some regulatory reasons, the monetary authorities recognize

only paid-up capital and statutory reserves as constituents of banks fund in

the measurement of capital adequacy. Some questions that may be asked

at this point are: why do banks require adequate capital? Is it not possible

that a bank without adequate capital can yet function properly and

efficiently? In the context of bank capital and its adequacy, the above

questions are very important because they tend to address the critical

issues upon which adequate capital is recommended for banks.

In an attempt to answer the first question, we can say that banks

require adequate capital to serve as a fall-back and of course, shock

absorber in the event of losses resulting from fund placement by banks. It

is necessary to measure capital to determine whether a bank's capital is

adequate to cushion possible losses resulting from loan losses and

disappointing interest margins. Such funds, should therefore, not be

subjected to fixed interest or fixed redemptions as these impose their own

limitations on usage of the funds.

In answer to the second question as to whether it is not possible that

a bank with adequate capital can function promptly and efficiently. There is

no bank that can function either promptly or efficiently without adequate ,

capital. The capital fund is an amalgam of equity funds and long-term debt

without which no business organization can function, how much less a b

bank. That is the more reason which capital adequacy becomes one of the

five key elements (basket of elements) considered in the assessment of

whether a bank is in distress or otherwise.

These five elements usually considered are: capital adequacy, asset

liquidity, managetilerit efficiency, earning performance and liquidity

position. These elements, which serve as index for assessment, are called

uniform inter- agency bank rating system represented with the acronym "

CAMEL". It therefore follows that for a bank to perform efficiently and

considered healthy, the provision of adequate capital cover must be

ensured.

Apart from the above, ensuring capital adequacy is an act of fund

management, which is a pre- requisite for any organization's survival.

Capital management includes the capital of a bank. It should be noted that

sound capital management in banking requires the maintenance of

adequate base of capital funds supplemented by long term debt.

However, it is the policy of banks generally to maintain sound capital

growth by balancing earnings allocation between dividend pay out and

profit retention in order to enhance future assets and earnings and by

issuing this point, we have been able to state the need to maintain

adequate capital in an organization especially bank and more impartially,

the management of such capital.

2.5.1 MEASUREMENT OF CAPITAL ADEQUACY

Somehow one may be tempted to think that the measurement of

adequate capital is not only a relative concept, a question of fact, but also a

subjective index whose common denominator is "what constitutes a safe

heaven for stock holders" interest. Hence the questions-how can capital

adequacy be determined? Whose duty is it to measure capital adequacy

and under what circumstances? The concept of capital adequacy has no

straight forward approach or definition. This is because banks vary in

sizes, location, magnitude of activities and level of risks arising from their

operations (Onyia, 1998).

At any rate, we can say that capital adequacy can be measured in

,many organizations especially banks, ratio analysis is used as a set

standard to measure the adequacy of capital funds even though that some

scholars warn that in accepting this criteriori, it should not be taken as an

end itself. The reason they argue is that the emphasis of ratio analysis of

common ratios and therefore sheds no light neither on the particular bank's

operations nor methods that are available for regulatory of bank capital. In

Nigeria, the monetary authorities have over the years used the 'following

methods;

I. Fixed minimum capital requirement,

ii. Limitations of lending limit, and

iii. Weighted risklasset ratio

2.5.2 FIXED MINIMUM CAPITAL REQUIREMENT

The end of the free banking era (1952) brought with it an end to

unregulated practice in the provision of commencement capital for banking

business in Nigeria. The fixed minimum capital requirement as a measure

of capital adequacy dictates that a bank should legally maintain at least a

fixed minimum paid-up capital to the tune of certain amount of money.

In Nigeria, the application of this method in measuring capital

adequacy became effective with the enactment of first ever banking Act in

1952. The act stipulated.for the first time, the minimum paid-up capital

requirement for commencement of banking business in Nigeria. The

banking act of 1969 as amended in 1979 stipulated that the paid-up capital

of indigenous banks should be a minimum of Pd600,000, while 811,500,000

was fixed for foreign banks. The same act required merchant banks to

maintain Pd2m.

It is noteworthy to observe that government of Nigeria has continued

to make changes on paid-up capital through other policy adjustments. In

1997, the stipulated minimum paid-up capital for banks .was put at

81500million with 31" December 1998 as the expiry date for full compliance

.by affected banks. This is against N50m and N40m paid up capital fixed for

commercial and merchant banks in 1990 respectively; but by operation

discovered to be inadequate. The essence of this requirement is to ensure

that banks are not under-capitalized thereby putting at risk stockholders

interest and exposing the bank to avoidable risk. This therefore, becomes

sure way to measure capital adequacy of banks. The current minimum

capital requirements stands at N25billion with effect from lS' January 2006.

LIMITATION OF LENDING LIMITS

This aspect of measurement of capital adequacy is clearly an

attempt by monetary authorities to save the banks from risking depositors'

and owners' funds. It is an arrangement whereby the capital of a bank to

lend (large loans) is limited to a certain percentage of the bank funds. The

implementation of the arrangement is that the amount of financial

accornrnodation which a particular commercial bank can offer a

custonier/depositor does not only depend on the stipulated lending limit but

also on the magnitude of paid up capital and reserves.

Before 30Ih June 1991, the maximum loan that any Nigerian bank

could grant to a single customer was 33 X% of the sum of the paid up

capital and statutory reserves of the bank. But since the promulgation of

Banks and Other Financial Institutions Decree (BOFID) of 1991, the limit

has been changed to 20% and 50% for Commercial and merchant banks

respectively. However, there are exceptions, which in most cases require

the approval of the Central Bank of Nigeria (CBN).

2.5.4 WEIGHTED RlSKlASSET RATIO

The risklasset as an index of measurement of capital adequacy

establishes the relationship between risk assets of particular bank and its

capital funds. The implication is that the level of capital cover required by

any asset in the bank's portfolio is directly dependent on the magnitude and

level of risk prevalent in that asset.

It therefore follows that gilt-edged securities as federal governrlient

of Nigeria development loan stock would require less bank cover than

securities issued by an individual firm. At any rate, weighted risklasset ratio

is a complete exposition of whatever class of asset and its risk.

Some authors vary in their approach to classification of the assets

and their various risk levels. Banking literature recognize all of them

probably because they fall within the portfolio of assets of banks. It stiould

be noted that the more risk free an asset the less need for capital cover.

That is why assets classified as liquid like cash, and most money market

instruments whose convertibility into cash is easy require little or no capital

cover. Other assets like normal assets do not require capital cover. Assets

classified as sub-standard require lo%, doubtful debts 50%, bad debts

100% and fixed assets 100% respectively.

2.6 IMPLICATION OF BANK DISTRESS

The adverse effect of bank distress on the economy of any country

is not a respecter of the level of development (Ebhodaghe 1995). Whether

a country is industrialized, developed and big or poor, under-developed and

small, bank failures, if not well managed, portend doom and collapse for

the economy. The devastating effects of bank failures on the only super

power in the world today- the United States of America (USA)- and the

threat it posed to the economy of the first industrial country-Britain- are well

documented in the literature (see Ebhodaghe, 1995).

The government's regulators, members of the public and bank

operators have always resented bank failures due to various reasons.

Governments are particularly concerned in view of the social, political and

economic implications of bank distress. The externalities associated with

bank distress make it distasteful and of serious macro economic

implications unlike what obtains when a non-bank institution fails. For

example, if a brewery company should become insolvent, its demise would

not adversely affect other brewery companies and as a matter of fact they

should benefit by having more customers. However when a bank fails or

becomes distressed, apart from the economy, there may be a spill over of

the problems to the other banks.

Of course, the real or perceived threat of contagion across banks

and the potential for high macroeconomic costs resulting from bank

distress have often led government to adopt a safety net to prevent these

outcomes (Glaessner and Mas, 1995). Some of these adverse effects of

bank distress are reviewed below.

A. EROSION OF PUBLIC CONFIDENCE

About the greatest havoc of bank distress is the erosion of public

confidence in the system especially if the distress is not well managed.

Banking is built on trust and confidence. Once the trust and confidence are

misplaced, banks would no longer be efficient in playing their role of

financial intermediation. The loss of public confidence would no longer be

automatically having many adverse effects. It can easily cause panic and

bank runs, which would threaten the survival of other healthy banks

through systematic risk particularly in the absence of a deposit insurance

scheme or other forms of safety net.

A situation where there is loss of public confidence and bank runs,

demonetisation would be a logical problem. There would be massive

portfolio shift to safer assets such as foreign currencies, government

securities and non- monetary assets as well as capital flight. The

prepondence of the banking public that would not be able to participate in

portfolio shift would not have a safe place to invest part of their wealth.

As this is supposed to be government's responsibility, there will be political

pressure for government to abate the crisis. Equally related to

demonstration is the negative implication for banking culture. Already the

banking culture in Nigeria is poor and low and bank distress would only

exacerbate the situation. As an evidence of this ugly development in

Nigeria, currency outside banks as a proportion of narrow money supply

rose sharply from 42.3% in 1987 before government started to officially

identify the number of distressed banks to 57.4% in 1995(a year when 60

out of the 115 banks were distressed by the authorities) before it declirlecl

to about 50% in1997 (NDIC,1997)

Hitherto, investment in the banking sector had been considered

lucrative. Bank distress would make investors lose their investments in the

banking industry, rather there would be compounded by low profitability for

the remaining banks as loss of public confidence in them would jeopardize

their patronage and earnings.

B. ECONOMIC EFFECTS. ~p4QWt Banks are central to an effective and efficient payments systems in

any country. With bank distress, the payments systems would be perilous b

and at great risk as the link between the real sector and the financial scctor

including international settlement would be greatly impaired. This would

inhibit the intermediation role of banks.

In circumstances where the capacity of banks to perform their main

role of financial intermediation is "impaired" the real sector of the economy

would be adversely affected. Banks are the main means by which

monetary policy is implemented in an economy. With bank failures this

would be hampered and development would be elusive.

Failed banks would be incapacitated from extending new credit. The

healthy banks would equally be constrained from granting credit for fear of

such facilities becoming delinquent. If credits are extended at all, they are

likely to be for short term and mainly to finance commerce and purchase of

foreign exchange. A country where banks become highly speculative and

reckless such as depicted here is dubbed as a "casino" economy. The

effect of these would be to further crowd out of the productive sectors of

manufacturing and agriculture from the credit market. Yet the productive

sector must be galvanized for macroeconomic stability to materialize.

The failure of a large bank or many banks can lead to a sudden

contraction of the money supply as well. This would have very serious

adverse implication for macroeconomic stability as economists, whether

, monetarist or fiscalists, are in accord that the level of money supply has a

positive correlation with the volume of activities in the economy.

Bank failures can hinder effective competition and an efficient

financial intermediation. Competitive banking system will force banks to

operate efficiently if they are to make profits, keep their customers and

remain in business. For this to obtain will depend on, among others, the

number of banks operating in a market, and whether the existing banks are

of an appropriate size and strength for the needs of their customers. Bank

failures can lead to undue concentration. And inefficiency of delivery of

banking services as failed banks are charged and new banks are not given

..free entry.

C. GLOBAL EFFECT.

The primary counterparts of foreign creditors are the banks as they

. are the financial gateway to a country. With bank distress, the international

perception of the banking system would be that of suspicion as it would be

feared that their funds could be locked up and / or lost in the banking

system. In most cases, the international community, except those involved

in criminal practices such as advanced fee frauds popularly known as '419"

in Nigeria and other types of frauds would not extend credit to a country in

which it's banking system is distressed. This would undoubtedly

compromise foreign investment and lead to escalation of capital flight out of

the coimtry.

STUDIES AND MODELS IN PREDICTING BANKS DISTRESS.

Many studies and models have predicted with some degree of

accuracy, the likelihood of success or failure of banks in particular and firms

in general. This review of past studies begins with Altman Multiple

Discriminant Analysis (MDA) Model which is similar to Secret's.

The technique of Multiple Discriminant Analysis (MDA) helps to

combine different ratios into a single measure of the probability of failure

(bankruptcy). MDA can be used to classify companies (banks inclusive), on

the basis of their characteristics as measured by financial ratios, into two

groups: distress or non-distress, failure or non-failure, etc. The empirical

studies of Beaver (1966) and Gupta (1979) identified ratios which have

discriminating power. What .is, however, required from the practical point of

view is the understanding of seriousness posed by low performing ratios

and the combined effect of use of MDA helps to consolidate the effects of

all ratios. MDA constructs a boundary line (a discriminant function), using

historical data of the bankrupt (distressed) and non-bankrupt (non-

distressed) firms. Altman was the first person to apply analysis in finance

for studying bankruptcy (Pardey, 2000).

Altman (1968) after reviewing past studies, discovered that the

works established certain important generalization regarding the

performance and trends of particular measurement, the adaptation of firms,

bgth theoretically and practically, is questionable. He also observed that

ratio analysis presented in this fashion is susceptible to faulty interpretation

and potentially confusing. He therefore chose a Multiple Discriminant

Analysis (MDA) as the appropriate technique as to bridge the gap. In b

classifying firms into bankrupt and non-bankrupt groups, the term

"bankruptcy" was used to describe business failure.

The Altman MDA (also called Z-score) is defined by the' following

discriminant function:

Z = V, XI + V2X2+ . . . . . . + V"X,,

which transforms individual variable values to a single discriminant score of

Z value which is then used to classify the firm,

where V, V2 . . . . . . . . Vn = Discriminant coefficients

XI X2 ........ Xn = Independent Variables

The MDA computes the discriminant coefficients Vj, while the

independent variables XI, are the actual values where j = 1, 2 . . . . . . n

The study showed that if ratios are analysed within a multivariate

framework, it will take on greater statistical significance than the common

technique of sequential ratio comparisons and results were encouraging.

Ako (1999) employed six models (MDA inclusive) to analjlse capital

markets and equity failure in Nigeria. These models are: The Univariate

Analysis Model; The Multiple Discriminant Analysis Model; The Linear

Probability Model; Logit Analysis Model; Probit Analysis Model and Non

parametric Analysis Model. In her procedure, MDA formed linear

combinations of the independent variables (predictor) which served as the

basis for classifying firms into failure and non-failure groups: Thus the

information contained in the actual values or the predictor variables is

summarized in a single index called Z-value or Z-score. She explained

further that to distinguish between the groups, the computed Z-Jalues for

the groups must differ. Therefore each group must have its own equation.

In the light of the above, she specified five (5) discriminantfunctions

(equation). They are as follows;

Z = wo + w, L, + w2R + w3E +W4D +W50P + W6 I S + W7Y

+wsZ + wgT + wlOL + w11 PER + wlzw + w13RR ...... 1

Equation 1 serves as the full discriminant models while Equation 2 is

a semi-full models. Equations 3, 4 and 5 provide further discrirnir~ant

analysis. WO ... .. . W13 are discriminant coefficients upon which the

variables (predictors) such as L, E, OP, PER, Y etc are weighted.

It is important to note that more variables (ratios) were considered

unlike Altman that used few ratios.

The results indicated that issues (Equity) which fail are from

companies with lower profitability, returns, dividend, retention rate and

working capital ratio. Also indicated was that the offer price, earnings,

dividend and income are the variables whose means are most ranked

higher in terms of relative importance (i.e. contribution to overall

discriminant function) The overall discriminant function also fitted the data

reasonably well. Furthermore, the predictive power of the model and its

variants were found to be generally quite high, also suggesting that there

are significant differences in the weights investors attach to factors

influencing their investment decisions.

Using the same MDA, Sinkey (1975) found evidence that support

that the measure of banking factors such as asset composition, loan

characteristics, capital adequacy, sources and uses of revenue, efficiency,

and profitability are good discriminators between the group (i.e. group

mean differences exist). He presented a multivariate statistical analysis of

the balance sheet and income statement characteristic of problem banks in

the years 1969-1972. Newly identified problem banks were matched with

non-problem banks and Multiple Discriminant Analysis was used to test for

group mean as to describe the overlap between groups, and to construct

rules to classify observations (banks) into problem and non-problem

groups.

He used a ten-variable set, the determinant tests which showed that +

both the group mean vectors and group dispersion matrices which were

significantly different in all four years. The chi-square measures of group

overlap indicated that the distribution of the individual vectors of the two

groups overlapped substantially in all four years. The classification results,

which measured the intersection (or overlap) of the two groups, described

groups that are relatively separate even in 1969 and that overlapped less

and less over the next three years. These classification results were quite

encouraging.

Doguwa (1996) explained that Altman et al (1991) identified short

comings associated with the use of MDA model in the prediction of financial

distress in firms. The short comings are;

(i) Predicted values cannot be interpreted as probabilities, since they

are

not constrained to fall between 0 and 1.

(ii) Linear discriminant analysis does allow direct prediction of group

membership, but assumption of multivariate normality of the

independent variables as equal variance-covariance matrices in the

two groups, are required for the prediction rule to be optimal.

As a result of the above short-comings, Doguwa (1996) adopted the

logit model to determine the conditional probability PI, that the ith bank will

fail, given a set of k derived balance sheet ratios: XI1, XI2... . . . Xik for that

bank. The model could be expressed thus: let Yf, Y2....., Yn be independent

binary response variables whose probability functions PI, P2,. ... Pn satisfy

the equation.

P 1 Log - = a, + aj Xij ...... 1

K

1-pi * 1 where I = 1, 2... ... n and pi is given by

Pi = 1

............ .2 1-+ exp (-Bi)

with Bi defined as:

The coefficient a, (j = 1, 2 . . . n) measures the effects on the odds of

failure of a unit change in the corresponding independent variables. The

parameters of equation (2) are estimated by maximizing over the aj's the

log likelihood function:

n n ...... L= Yi log (Pi) + 1 (i-Yi) log (I-pj) . .4

i - I i-1

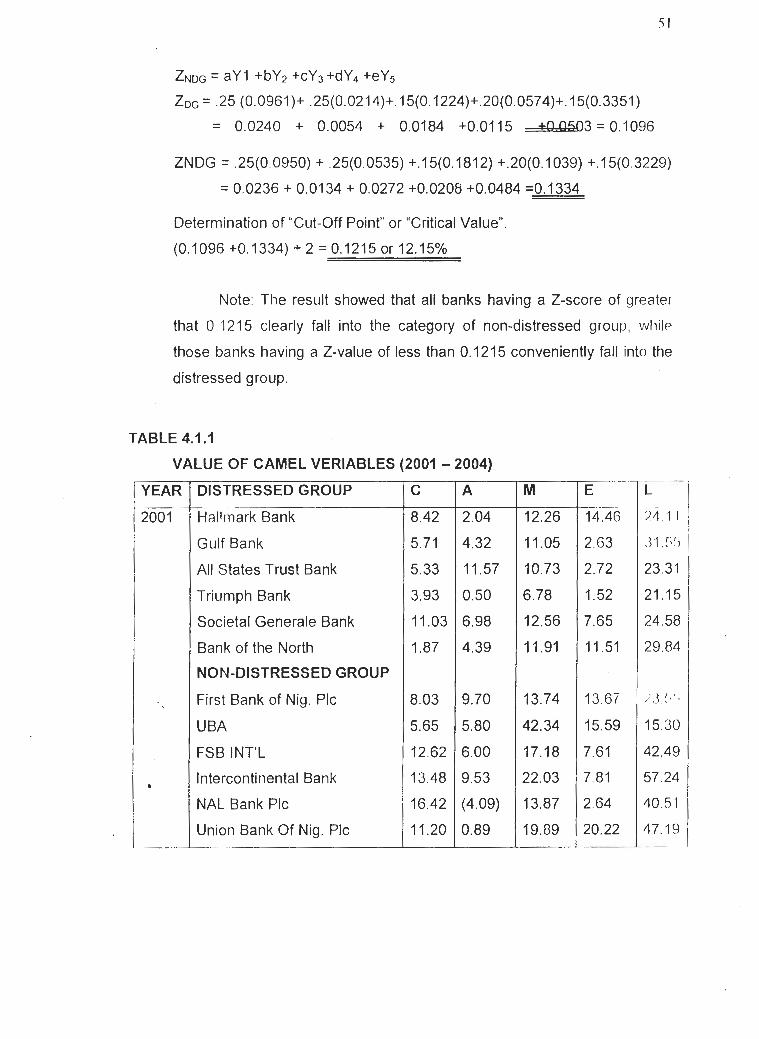

The result of Doguwa's analysis showed that five discriminatory

variables are important in distinguishing weak from non-problem

commercial banks. These variables are capital adequacy, asset quality,

liquidity, loan category and profitability.

2.8 THE EARLY WARNING MODELS

An early warning model is an established procedure (usually

statistical) for classifying banks into groups (usually failure and non-failure,

distressed or non-distressed). This is usually done using only financial

characteristics of candidate institution. The goal of an early warning model

is to identify an institution's financial weakness at the initial stage in its

process of determination so as to warn interested parties of its potential

failure or distress.

A survey of literature reveals that six (6) statistical models are

employed as early warning models in the prediction of financial distress,

failure or weakness.

The models are as follows:

The univariate Analysis Model:

The Multiple Discriminant analysis Model.

The Linear Probability Model

Logit Analysis Model

Probit Analysis Model

Nonparametric Analysis Model.

MDA and Logit Models have been discussed exhaustively in 2.3

above

At this juncture, it is important to note that Jagtiani et al (2000)

observed that despite the widespread popularity of a logit model as an

effective Early Warning System (EWS) approach, it does have some draw-

back in term of the information that it produces, for example, it is not

possible to determine from the parameter estimates generated by logit

hodels which variables are most ~ ~ s e f u l in predicting capital-inadequate

banks (or alternatively capital-adequate banks). The results only 'indicate

the effectiveness of each variable's ability to discriminate between the two

groups of banks. While the logit model seeks to minimize classification

errors, they do not provide any information about how each-variables

affects Type 1 and 11 errors per se. In addition, logit models are not well

suited to examining interactions between variables.

Beaver (1966) utilized Univariate Analysis model to predict failure.

His work compared a list of ratios individually for failed firms and.a matched

sample of non-failed firms. Observed evidence for five (5) years prior to

failure was cited as conclusive that ratio analysis can be useful in failure

prediction. Ako (1999) quoting Booth (1983) as having employed univariate

analys~s to test four decomposition measures to ascertain the ability of the

attributes, size and stability to discriminate between failed and non-failed

companies. His results concluded that the attributes of most of the

decomposition measures discriminate between failed and non-failed.

However, other researchers have identified its lack of multivariate analysis

as a major short-coming of such studies, i.e, they only consider the

measurements used for group assignments one at a time.

Another model mentioned above is the Probit Analysis Model. This

method, unlike the logit method, avoids the problem of non-normality of the

error term. The intuition behind the probit models is similar to that behind

the logit model. However, for probit, it is argued that if failure is the result of

many independent individually inconsequential additive factors, it is

reasonable to assume the threshold level to be normally distributed (Ako,

1999). This implies that probability is measured by the area under the

standard normal curve which has means = 0 and variance = 1.

Ako (1999) stated that researchers who used this model include

Grablowsky and Tally who used the technique to classify credit application

. of 200 companies using 11 explanatory variables. Their study employed

both Probit and MDA analysis and concluded that Probit analysis was a

variable alternative to MDA as a classification model. Furthermore, Probit

analysis was found to outperform MDA in efficiency principally, because

like the Logit model, Probit model does not require the normality

assumption. Empirical evidence also suggest that Probit Analysis Model

and the Logit Model have similar distribution; both logistic distribution has

slightly thicker tails. However a major problem of using both the Logit and

probit methods is the lack of readily available procedures in many of the

existing statistical packages. Moreover specifications for Probit analysis are

rather complex computationally.

Another model is the Non-Parametric Analysis Model (NM). These

are relatively new approach to classification problem. Their approach

appears to overcome some of the short comings and problems of traditional

MDA and LP models. The Non-parametric models is a modification of MDA

which uses inequalities (instead of equalities) in its maximization

procedures. Moreover, the misclassification errors identified and the

expected cost of misclassification are often smaller than those obtained

with MDA, Logit or Probit Analyses. This latter property and the fact that

different coefficients are obtained for the same variables shed light on the

relative significance and magnitude of the individual variables, as well as on

the interpretation given to results. The NM usually uses forward stepwise

analysis to obtain coefficients for selected variables.

Amongst the notable researchers who used NM include Frydman,

Altman and Kao (FAK, 1985), Marais et al (1984). Both employed NM

namely a recursive partitioning algorithm for classification of bankruptcy

and commercial loans respectively. Their technique was found to

outperform MDA for most empirical results. However, a major short coming

of the recursive partitioning method is that it cannot be used for scoring

observations within the same group as it does not employ a ration scale

unlike the MDA which assigns a score to each observation on a continuous

scale.

2.9 . CRiTlCAL VARIABLES CONSIDERED IN PREVIOUS STUDIES.

Earlier studies such as Sinkey (1 9754, Altman (1 977), Martin (I 977),

Avery and Hanweck (1 984), and Barth et al (1 985), Barr and Siems (1 996)

and Doguwa (1996) analysed the financial characteristics of banks and of

savings and loans associations. Accordingly these studies adopted more or

less the same variables, based on five (5) categories of capital adequacy,

asset quality, management quality, earnings and liquidity (CAMEL) that are

used by the regulators for evaluation process.

Sinkey (1975), finds the loan revenue variable, which is an indicator

of asset quality is the best discriminator. Although the differences in the

means of the management quality, honesty and loan to-capital variables

are also statistically different, the classification accuracy of the model is low

because of the overlap between the problem and non-problem banks

Other variables considered include profitability ratios, capital adequacy and

sources and uses of revenue. Sinkey was the first to apply linear ~nultiple

discriminant analysis to classify banks into either the problem or nor)-

problem groups He reported the following rates of misclassifying a problem

as a non-problem bank for the years: 1969-72; 27%, 28%, 24% and 18%.

The group mean vectors and group dispersion matrices are significantly

different in all the four years, and the differentials increase over time. The

findings suggest that problem banks appear to be different from non-

problem banks, and the difference is increase over time. However, chi-

square measures of group overlap indicate that the distributiohs of the

individual bznks' characteristics overlap substantially and accordingly

Sinkey commented that the "descriptive" classification results were "better"

than might expected.

Ako (1999) listed the following financial ratios as good discriminators

between failed and non-fail firms in her analysis of capital market and

equity failure in Nigeria:-

Liquidity Ratios

Profitability Ratios

Leverage Ratios

Activity Ratios

Returns and Market Ratios.

Altman (1977), concluded that operating income and its trend are the

most important discriminators. He also foulid that net worth and real estate-

owned variables to be important. The reason was that these variables

reflect the capital, profitability and asset quality of a financial institution

Martin (1977), found that the variables representing earnings, loall

quality and capital were useful in distinguishing problem banks from non-

problem banks. In using the logit analysis, he used the following variables.

Net Income to Total Assets; Gross charge offs to Net operating income;

commercial and industrial loans to Total loans; and Gross capital Risk

Assets. Furthermore he found that misclassification rates depend on the

observation period and the combination of variables included into the

model. He selected combinations of variables in 1970 and 1974 and

reported the following ranges of misclassification errors: 1975-1 976, 1971 -

72 for failed banks: 4.0% - 13.0%, 42.0%-50.0% while survived banks had

9.0%-11.0%. 15%-33.0%: The implications of his results are that, first,

earnings and capital adequacy are of relevance only when the level of loan

losses is high, and, secondly, statistical early warning models are of most

interest in periods of moderate adversity, rather than in times that are

better or substantially worse. In terms of performance, the classification

accuracies are similar between discriminant and logit models.

Avery and Hanweck (1984), interpret that bank size is critical in a

bank's survival as it indicates its ability to raise capital and reflects the

reluctance of regulators to close a failing but large bank. They also

concluded that local banking variables are not important in explaining bank

closures because of the unexpected signs of the coefficients.

Barth et al (1985), found that the variables representing capital

adequacy, asset quality, earnings and liquidity are the only Statistically

significant variables. However, they interpret size as an indicator of greater

liquidity as they believe that a larger financial institution has a greater ability

to borrow as to alleviate liquidity problems.

Bar and Siems (1996) applied six variables selected for failure

prediction models. These variables were:

- Equity capital to Total loans for capital adequacy;

- Non performing loans to Total Assets for Asset Quality;

- . DEA efficiency score for Management Quality;

- Net income to Total Assets for Earnings Ability;

- Large Dollar Deposits to Total Assets for liquidity;

- . Percentage change in Residential construction for Local Economic

Conditions.

Their research revealed that a coriiparison of the One-Year-Ahead

and Two-Year-Ahead mean values gave insight into differences between.

The surviving and failing populations. Except for liquidity measure, the gap

between the mean values for survivors and failures widens as failures

approaches. Also there is a difference in mean values for the survivors, but

a noticeable deterioration for failures (except for the liquidity variables).

They concluded that one might expect the IYA model to predict failure with

greater accuracy than the 2YA model. The standard probit methodology

was used to develop models that would classify banks as either survivors

or failures.

Doguwa (1996), in his Logit Regression Approach, used a set of

variables expressed in ratio form (percentages) in identifying problems

banks in Nigeria. These include variables CAR and CLR to measure capital

adequacy; LRWA, LQR, LCR, LTA and BDL for quality and risk of a bank's

portfolio; LAS LR and LDR reflect in various ways the liquidity position of

the bank and its ability to respond to liquidity pressures. Others included

variables SFR and TKA for source of funds; LSL for loan category and

lastly ROA and ROC, for retained profit (loss) for earnings. The resulis

showed that five variables are important i r ~ distinguishing weak from sound

commercial banks. These variables are Capital Over Risk Weighted Assets

(CAR), Risk Weighted Assets to Total assets (LRWA), Treasury Bills and

Certificates to Total current liabilities (LAS), Loans and Advances to states

and local governments to Total Loans (LSL) and Retained. Profit (or loss)

to Total Assets (ROA). One interesting result was that four explanatory

variables (discriminatory factors) in the analysis bear close resemblances

to the CAMEL components, while the loan category factor indicates that

increased loans to states and local governments have contributed to the

distress condition of commercial banks.

Cole and Gunther (1995), applying a split-population survival time

. model, separated the determinants of bank failure from factors that

influence the survival time of failed banks.

They found that the basic indicators of a bank's condition, such as

capital, troubled assets and net income, are significant in explaining the

timing of a bank failure. However, many other variables typically included in

bank failure models, such as measures of bank liquidity, are not associated

with failure time.

REFERENCES