Embed Size (px)

Citation preview

UNIT-IIIUNIT-III

THEORY OF THEORY OF PRODUCTIONPRODUCTION & & COSTCOST ANALYSISANALYSIS

Concept of ProductionConcept of Production

It a manufacturing processIt a manufacturing process It’s a process of different commoditiesIt’s a process of different commodities Its includes Raw material, Work in Its includes Raw material, Work in

progress & finished goods.progress & finished goods.

Concept of ProductionConcept of Production

Basically 3 components in the production Basically 3 components in the production processprocess

ProductProduct ProductivityProductivity productionproduction

Concept of ProductionConcept of Production

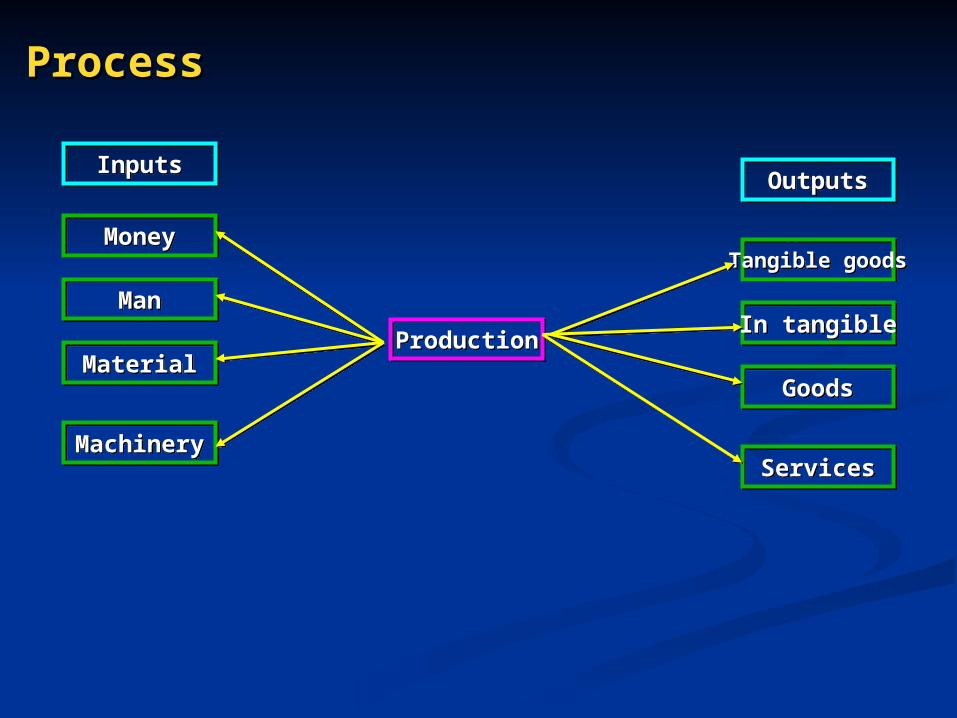

Production is an activity of Production is an activity of transforming the inputs in to outputtransforming the inputs in to output

Production involves step-by-step Production involves step-by-step conversion of one form material in to conversion of one form material in to another form through mechanical another form through mechanical processprocess

Meaning & DefinitionMeaning & Definition

According to ES BuffaAccording to ES Buffa “Production is a “Production is a process by which goods and services are process by which goods and services are created.”created.”

In economicsIn economics “the term production means a “the term production means a process in which the resources are transferred or process in which the resources are transferred or converted in to a different and more usually converted in to a different and more usually commodities.”commodities.”

In general production meansIn general production means “Transforming “Transforming inputs in to an output. Its however limited to inputs in to an output. Its however limited to manufacturing organization.”manufacturing organization.”

ProcessProcess

InputsInputsOutputsOutputs

MoneyMoney

ManMan

MaterialMaterial

MachineryMachinery

Tangible goodsTangible goods

In tangibleIn tangible

GoodsGoods

ServicesServices

ProductionProduction

Types of production functionsTypes of production functions

Basically 2 types of functionsBasically 2 types of functions

1.Short run production function1.Short run production function

2.Long run production function2.Long run production function

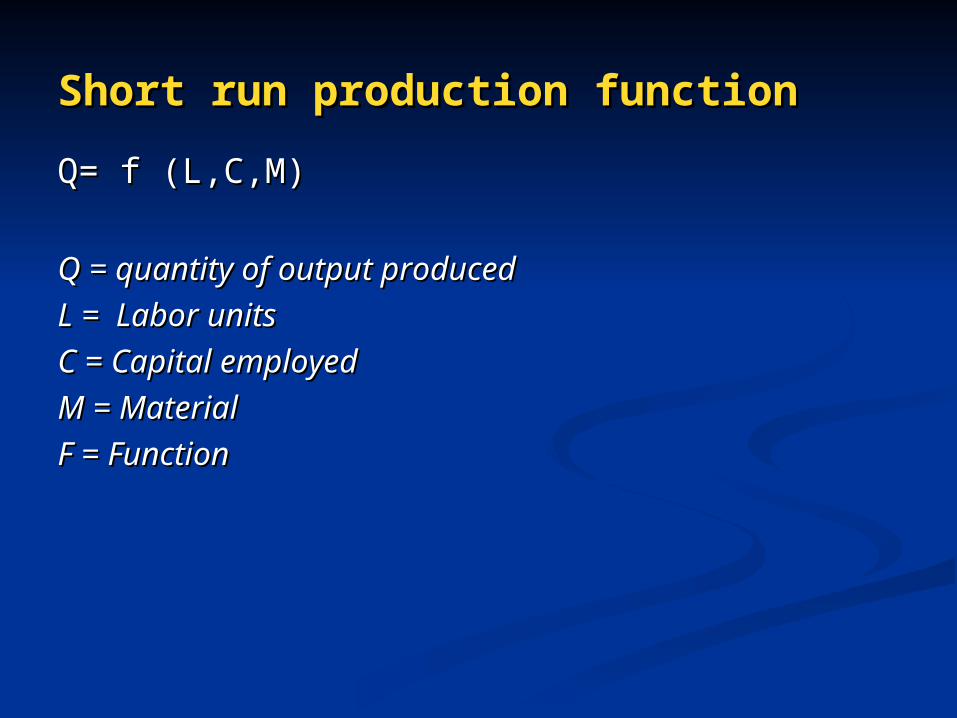

Short run production functionShort run production function

Q= f (L,C,M)Q= f (L,C,M)

Q = quantity of output producedQ = quantity of output produced

L = Labor unitsL = Labor units

C = Capital employedC = Capital employed

M = MaterialM = Material

F = FunctionF = Function

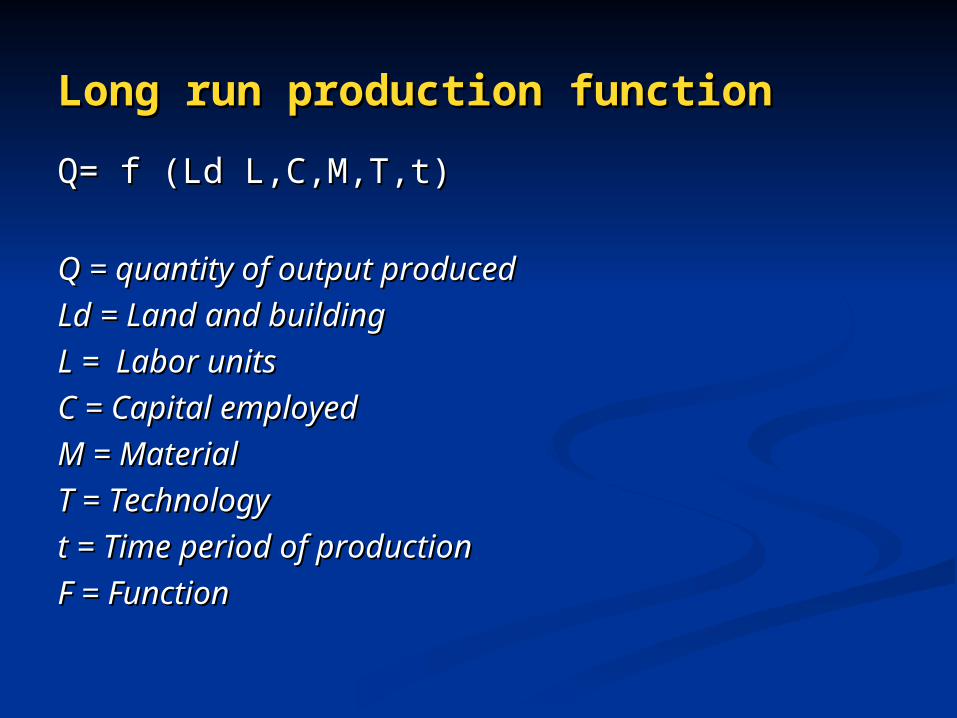

Long run production functionLong run production function

Q= f (Ld L,C,M,T,t)Q= f (Ld L,C,M,T,t)

Q = quantity of output producedQ = quantity of output produced

Ld = Land and buildingLd = Land and building

L = Labor unitsL = Labor units

C = Capital employedC = Capital employed

M = MaterialM = Material

T = TechnologyT = Technology

t = Time period of productiont = Time period of production

F = FunctionF = Function

Isoquant curveIsoquant curve

It is curve based on production or sales or It is curve based on production or sales or purchasespurchases

It is profit curve alsoIt is profit curve also

The term Isoquant has its origin from two The term Isoquant has its origin from two words words iSo iSo and and qUantus.qUantus.

iSo iSo is a greek word meaning is a greek word meaning equalequal and and quantus is Latin word meaning quantus is Latin word meaning quantity.quantity.

An isoquant curve is therefore called iso-An isoquant curve is therefore called iso-product curve or production in difference product curve or production in difference curve.curve.

Meaning & DefinitionMeaning & Definition

Iso quants are used to present a production Iso quants are used to present a production function with two variable inputs.function with two variable inputs.

Eg. Let us consider a production function with Eg. Let us consider a production function with the quantities of out put produced by using the quantities of out put produced by using different combinations of two inputs such as different combinations of two inputs such as laborlabor and and capital capital

Meaning & DefinitionMeaning & Definition

In other words an iso quant is a line joining In other words an iso quant is a line joining different combinations of labor and capital that different combinations of labor and capital that yield the same level of production.yield the same level of production.

Eg. Quantity of out put produced.Eg. Quantity of out put produced.

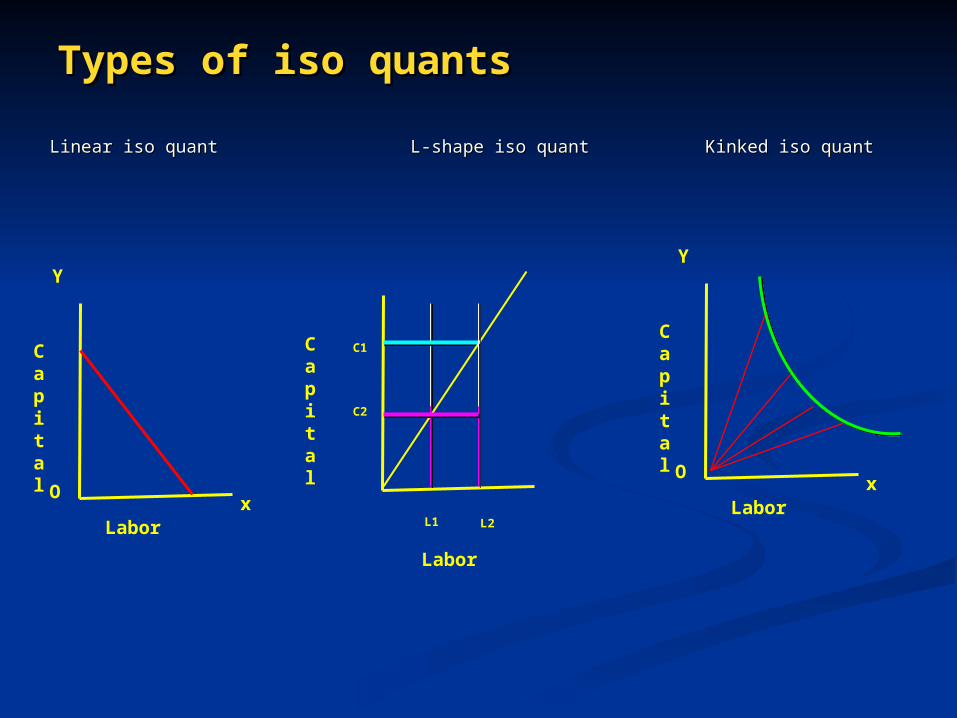

Types of iso quantsTypes of iso quants

Y

OX

M1

P

P1

price

Demand

M

Basically 3 typesBasically 3 types

Linear iso quantLinear iso quant L-shape iso quantL-shape iso quant Kinked iso quantKinked iso quant

Types of iso quantsTypes of iso quants

Linear iso quant Linear iso quant L-shape iso quant L-shape iso quant Kinked iso quantKinked iso quant

Y

O

Capital

Laborx

L1 L2

C1

C2

Capital

Labor

Y

O

Capital

Laborx

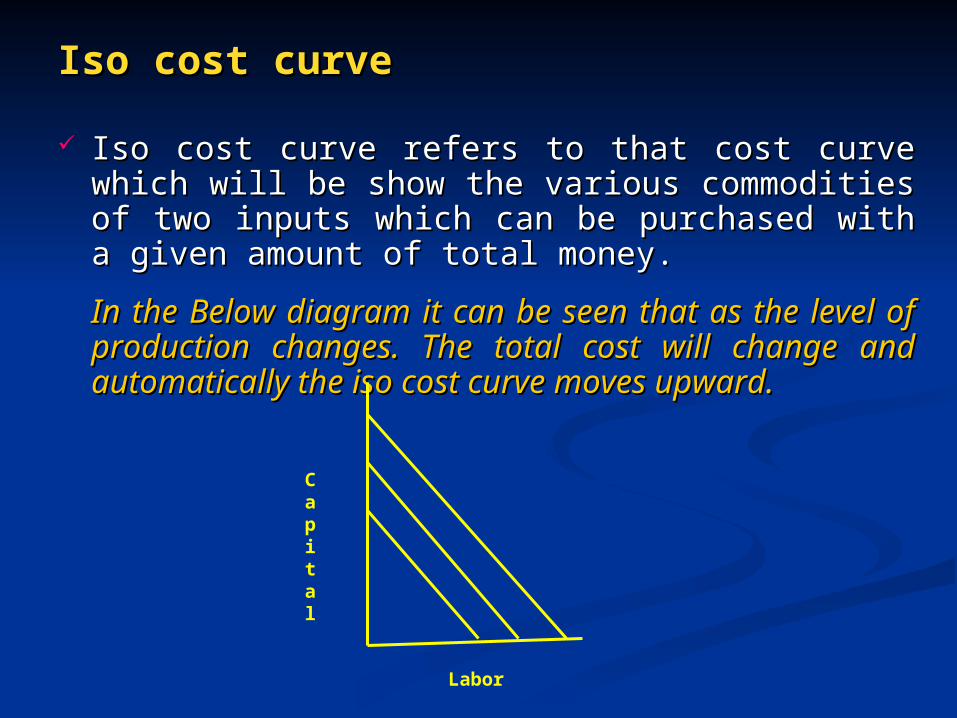

Iso cost curveIso cost curve

Iso cost curve refers to that cost curve which will Iso cost curve refers to that cost curve which will be show the various commodities of two inputs be show the various commodities of two inputs which can be purchased with a given amount of which can be purchased with a given amount of total money.total money.

In the Below diagram it can be seen that as the In the Below diagram it can be seen that as the level of production changes. The total cost will level of production changes. The total cost will change and automatically the iso cost curve change and automatically the iso cost curve moves upward.moves upward.

Capital

Labor

Types of Iso cost curvesTypes of Iso cost curves

Capital

Labor

Capital

Labor

Super imposition of iso cost curveSuper imposition of iso cost curve Iso quant showing line of price level Iso quant showing line of price level

Assumptions of Isoquant curvesAssumptions of Isoquant curves

An isoquant curve has two inputs say labor and An isoquant curve has two inputs say labor and capital to produce an out put.capital to produce an out put.

The two inputs are perfectly substitutable to each The two inputs are perfectly substitutable to each other but at a diminishing rate.other but at a diminishing rate.

The technology applied in the production process in The technology applied in the production process in given or constant.given or constant.

The substitution of one input for the other levels the The substitution of one input for the other levels the output unaffected. output unaffected.

MRTSMRTS of Isoquant of Isoquant ((MMarginal arginal RRate of ate of TTechnical echnical SSubstitutions)ubstitutions)

If we assumed tow factors of production say If we assumed tow factors of production say labor and capital. Then the marginal rate of labor and capital. Then the marginal rate of technical substitution of capital for labor is technical substitution of capital for labor is the number of units of labor which can be the number of units of labor which can be replaced by one unit of capital, which the replaced by one unit of capital, which the quantity of output remaining the same.quantity of output remaining the same.

Least cost combination of inputsLeast cost combination of inputs

When a consumer I faced with the problem of When a consumer I faced with the problem of making choice b/w two or more goods with given making choice b/w two or more goods with given resources.resources.

The producer may be reach an optimum point by The producer may be reach an optimum point by choosing the least-cost combination of inputschoosing the least-cost combination of inputs

The producer will choose that combination of inputs The producer will choose that combination of inputs with produces maximum out puts at lowest cost.with produces maximum out puts at lowest cost.

FormulaeFormulae

1.1. Managerial product of input Managerial product of input XX

Price of input of Price of input of XX

1.1. Managerial product of input Managerial product of input Y Y

Price of input of Price of input of YY

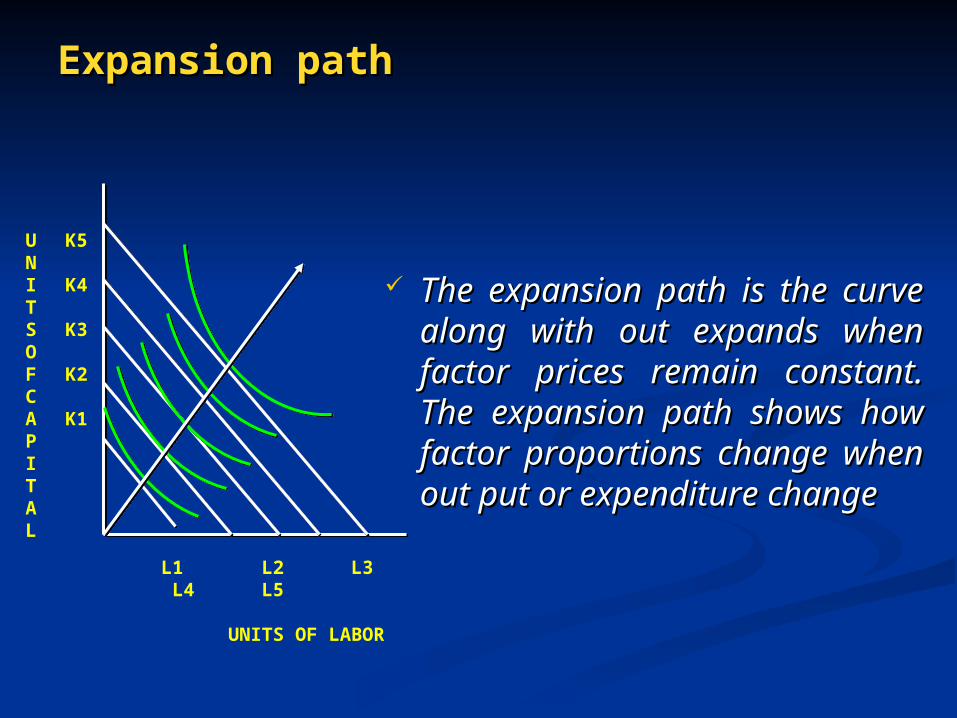

Expansion pathExpansion path

K5

K4

K3

K2

K1

L1 L2 L3 L4 L5

UNITS OF LABOR

UNITSOFCAPITAL

The expansion path is the curve The expansion path is the curve along with out expands when along with out expands when factor prices remain constant. factor prices remain constant. The expansion path shows how The expansion path shows how factor proportions change when factor proportions change when out put or expenditure changeout put or expenditure change

Cobb Douglas production functionsCobb Douglas production functions

It was introduced by It was introduced by Charles W. cobb and Charles W. cobb and Paul H. douglas Paul H. douglas in the 1920s. They suggested a in the 1920s. They suggested a production function of the form..production function of the form..

Q = A, LQ = A, Lbb K K 1-b1-b

Q=Q= quantity of the out put producedquantity of the out put producedA= constant A= constant L= Labor unitsL= Labor unitsK= Capital unitsK= Capital unitsb = Parametersb = Parameters

Properties Properties

for output (Q) to exist both labor and capital should be positive for output (Q) to exist both labor and capital should be positive and not equal to zero.and not equal to zero.

Q = A LQ = A Laa KK1-b ,1-b , L>0,K<0L>0,K<0 The addition of parameters is equal to oneThe addition of parameters is equal to one

b+1-b = 1b+1-b = 1 The later version of production functionThe later version of production function ParametersParameters It helps to find out the short run relationship between Input and It helps to find out the short run relationship between Input and

Out putOut put

1.Martinal product of labor (MPL)1.Martinal product of labor (MPL)

2.Marginal product of capital (MPC)2.Marginal product of capital (MPC)

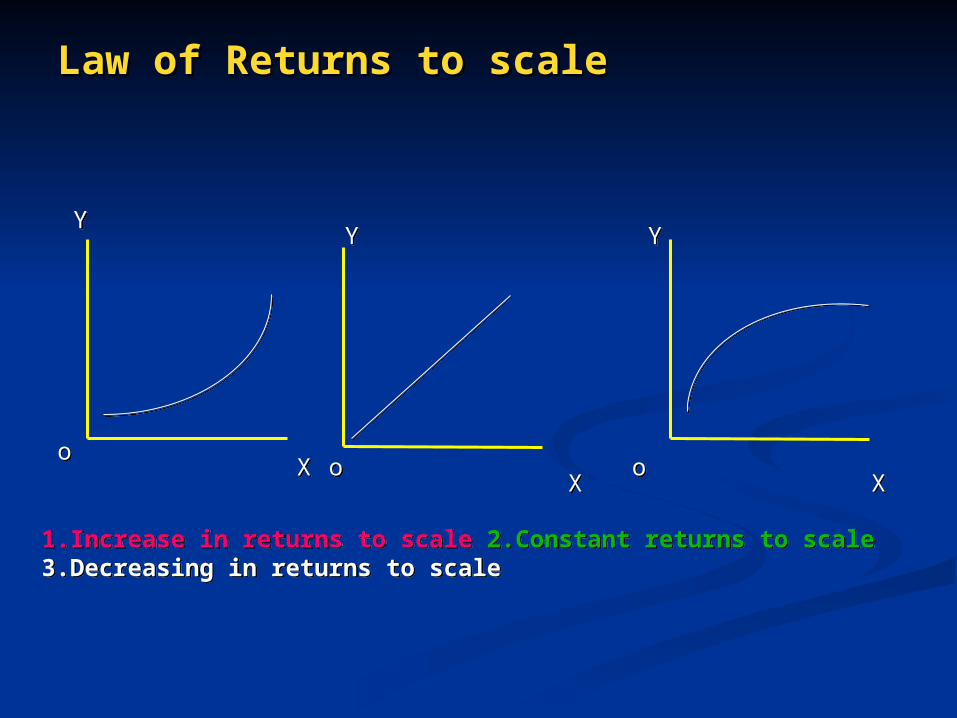

Law of Returns to scaleLaw of Returns to scale

The behavior of output when the varying quantity of one input is The behavior of output when the varying quantity of one input is combined with a fixed quantity of the other can be categorized in to 3 combined with a fixed quantity of the other can be categorized in to 3 stages stages

The law of returns to scale can be designed as the percentage of The law of returns to scale can be designed as the percentage of increase in the output where all the inputs vary in the same proportion increase in the output where all the inputs vary in the same proportion

The law of return to scale refers to the relationship between inputs The law of return to scale refers to the relationship between inputs and outputs in the long run when all the inputs (both fixed & variable) and outputs in the long run when all the inputs (both fixed & variable) are varied same proportion are varied same proportion

Law of Returns to scaleLaw of Returns to scale

AA

BB CC

DD

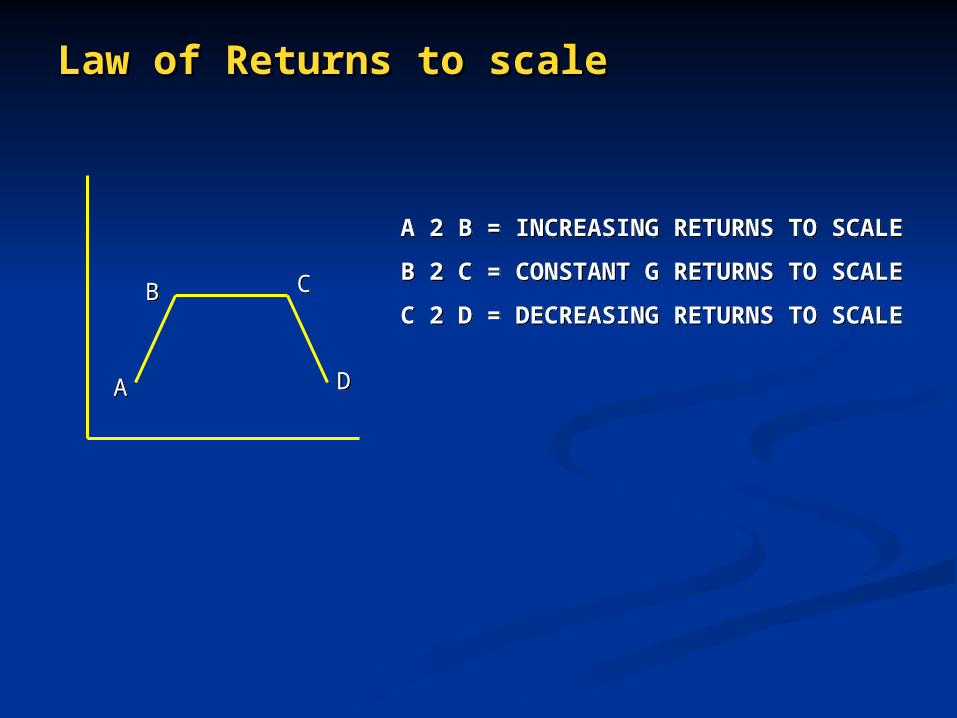

A 2 B = INCREASING RETURNS TO SCALE

B 2 C = CONSTANT G RETURNS TO SCALE

C 2 D = DECREASING RETURNS TO SCALE

A 2 B = INCREASING RETURNS TO SCALE

B 2 C = CONSTANT G RETURNS TO SCALE

C 2 D = DECREASING RETURNS TO SCALE

Law of Returns to scaleLaw of Returns to scale

Increasing returns to scaleIncreasing returns to scale occurs when a percentage increase in occurs when a percentage increase in inputs lead to a greater percentage increase in the output.inputs lead to a greater percentage increase in the output.

eg. If a 5% increase in inputs results in 10% increase in the output, an eg. If a 5% increase in inputs results in 10% increase in the output, an organization is to attain increase returns organization is to attain increase returns

Constant returns to scaleConstant returns to scale if occur an when the percentage in the if occur an when the percentage in the output is equal to the percentage of increase in inputs.output is equal to the percentage of increase in inputs.

eg. If the inputs are increase at 10% and if the result output also increase eg. If the inputs are increase at 10% and if the result output also increase at 10%at 10% Decreasing returns to scaleDecreasing returns to scale If the proportionate increase is less If the proportionate increase is less

then proportionate increase in the out put then a situation is called decreasing then proportionate increase in the out put then a situation is called decreasing returns.returns.

eg. If the inputs are increase at 10% and if the result output also increase eg. If the inputs are increase at 10% and if the result output also increase at 5%at 5%

Law of Returns to scaleLaw of Returns to scale

ooXX

YY

ooXX

YY

ooXX

YY

1.Increase in returns to scale 2.Constant returns to scale 3.Decreasing in returns to scale 1.Increase in returns to scale 2.Constant returns to scale 3.Decreasing in returns to scale

Economies of scaleEconomies of scale

Basically 3 types of Economies

1. Small scale

2. Medium scale

3. Large scale

Law of returns also confined in accordance with the scale of proportion of the firm.

1.Increasing Returns

2. Constant Returns

3. Decreasing Returns

Basically 3 types of Economies

1. Small scale

2. Medium scale

3. Large scale

Law of returns also confined in accordance with the scale of proportion of the firm.

1.Increasing Returns

2. Constant Returns

3. Decreasing Returns

Types of EconomiesTypes of Economies

Basically 2 types of Economies

1. Economies of scale

2. Diseconomies of scale

Basically 2 types of Economies

1. Economies of scale

2. Diseconomies of scale

Economies of scaleEconomies of scale

Internal or Real Economies

1. Economies in production

2. Economies in Marketing

3. Managerial Economies

4. Economies in Transport & Storage

Internal or Real Economies

1. Economies in production

2. Economies in Marketing

3. Managerial Economies

4. Economies in Transport & Storage

Economies of scale (contd..)Economies of scale (contd..)

External or Pecuniary Economies

1. Large scale of purchase of Raw material

2. Large scale equation of external finance

3. Massive Advt.

4. Establishment of transport & warehouse

External or Pecuniary Economies

1. Large scale of purchase of Raw material

2. Large scale equation of external finance

3. Massive Advt.

4. Establishment of transport & warehouse

Diseconomies of scaleDiseconomies of scale

1. Internal Diseconomies

2. External Diseconomies

1. Internal Diseconomies

2. External Diseconomies

Introduction to Cost analysisIntroduction to Cost analysis

It means a piece of work

It is process of Raw material and work in progress

It is a unit price of commodity

It means a piece of work

It is process of Raw material and work in progress

It is a unit price of commodity

Types of Cost analysisTypes of Cost analysis

Actual cost

Opportunity cost

Sunk cost

Incremental cost

Explicit cost

Implicit cost or imputed cost

Book cost

Out of pocket cost

Accounting cost

Economic cost

Actual cost

Opportunity cost

Sunk cost

Incremental cost

Explicit cost

Implicit cost or imputed cost

Book cost

Out of pocket cost

Accounting cost

Economic cost

Types of Cost analysis (contd..)Types of Cost analysis (contd..)

Direct cost

Controllable cost

Non-controllable cost

Historical cost or Replacement cost

Shut down cost

Abandonment cost

Urgent cost and postponement cost

Business cost and full cost

Fixed cost

Variable cost

Direct cost

Controllable cost

Non-controllable cost

Historical cost or Replacement cost

Shut down cost

Abandonment cost

Urgent cost and postponement cost

Business cost and full cost

Fixed cost

Variable cost

Types of Cost analysis (contd..)Types of Cost analysis (contd..)

Total cost

Average cost

Marginal cost

Short-run cost

Long run cost

AVC, AFC, ATC

Total cost

Average cost

Marginal cost

Short-run cost

Long run cost

AVC, AFC, ATC

AnalysisAnalysis

Actual cost

Actual cost is defined as the cost or expenditure which a firm incurs for producing or acquiring a good or service. The actual costs or expenditures are recorded in the books of accounts of a business unit. Actual costs are called as “Out lay Costs” or “Absolute Costs”

Eg. Cost of Raw material, wages, salaries (production)

Actual cost

Actual cost is defined as the cost or expenditure which a firm incurs for producing or acquiring a good or service. The actual costs or expenditures are recorded in the books of accounts of a business unit. Actual costs are called as “Out lay Costs” or “Absolute Costs”

Eg. Cost of Raw material, wages, salaries (production)

Analysis (contd..)Analysis (contd..)

Opportunity cost

opportunity cost is concerned with the cost of forgone opportunities/alternatives. In other words, it is the return from the second best use of the firms resources which the firm forgoes in order to avail of the return from the best use of the resources.

Eg. Own land and building of the company or firm

Opportunity cost

opportunity cost is concerned with the cost of forgone opportunities/alternatives. In other words, it is the return from the second best use of the firms resources which the firm forgoes in order to avail of the return from the best use of the resources.

Eg. Own land and building of the company or firm

Analysis (contd..)Analysis (contd..)

Sunk cost

Sunk costs are those do not alter by varying the nature or level of business activity. Sunk costs are generally not taken into consideration in decision making as they do not vary with the changes in the future. Sunk costs are a part of the outlay/actual costs. sunk costs areas “non-avoidable costs”. Or “non-escapable costs”.

Eg. All the past costs are considered as sunk costs. The best example is amortization of past expenses, like depreciation

Sunk cost

Sunk costs are those do not alter by varying the nature or level of business activity. Sunk costs are generally not taken into consideration in decision making as they do not vary with the changes in the future. Sunk costs are a part of the outlay/actual costs. sunk costs areas “non-avoidable costs”. Or “non-escapable costs”.

Eg. All the past costs are considered as sunk costs. The best example is amortization of past expenses, like depreciation

Analysis (contd..)Analysis (contd..)

Incremental cost

Incremental costs are additions to costs resulting from a change in the nature or level of a business activity. As these costs can be avoided by not bringing any variation in the activity, they are also called as “avoidable costs”. Or “Escapable costs”.

Eg. Change in distribution channel adding or deleting a product in the product line, replacing a machinary.

Incremental cost

Incremental costs are additions to costs resulting from a change in the nature or level of a business activity. As these costs can be avoided by not bringing any variation in the activity, they are also called as “avoidable costs”. Or “Escapable costs”.

Eg. Change in distribution channel adding or deleting a product in the product line, replacing a machinary.

Analysis (contd..)Analysis (contd..)

Explicit cost

Explicit costs are those expenditures that are actually paid by the by the firm. Those costs are recorded in the books of accounts. Explicit costs are important for calculating the profit and loss accounts and guide in economic decision making. Its are also called paid up costs.

Eg. Interest payment on borrowed funds, rent payment, wages paid

Explicit cost

Explicit costs are those expenditures that are actually paid by the by the firm. Those costs are recorded in the books of accounts. Explicit costs are important for calculating the profit and loss accounts and guide in economic decision making. Its are also called paid up costs.

Eg. Interest payment on borrowed funds, rent payment, wages paid

Analysis (contd..)Analysis (contd..)

Implicit or Imputed cost

These cots are a part of opportunity cost. they are the theoretical costs. i.e. they are not recognized by accounting system and are not recorded in the books of accounts. But are very important in certain decisions. They are also called as imputed costs.

Eg. Rent on idle time, depreciation on fully depreciated property still in use, interest on equity capital.

Implicit or Imputed cost

These cots are a part of opportunity cost. they are the theoretical costs. i.e. they are not recognized by accounting system and are not recorded in the books of accounts. But are very important in certain decisions. They are also called as imputed costs.

Eg. Rent on idle time, depreciation on fully depreciated property still in use, interest on equity capital.

Analysis (contd..)Analysis (contd..)

Book costs

Book costs are those costs which don’t involve any cash payments but a provision is made in the books of accounts in order to include them in the profit and loss account and take tax advantages, like provision for depreciation and unpaid amount of Interest on the owners capital

Book costs

Book costs are those costs which don’t involve any cash payments but a provision is made in the books of accounts in order to include them in the profit and loss account and take tax advantages, like provision for depreciation and unpaid amount of Interest on the owners capital

Analysis (contd..)Analysis (contd..)

Out of pocket cost

Out of pocket costs are those costs or expenses which are current payments to the outsiders of the firm. All the explicit costs fall into the category of out of pocket costs.

Eg. Rent paid, wages, Transport charges and salaries

Out of pocket cost

Out of pocket costs are those costs or expenses which are current payments to the outsiders of the firm. All the explicit costs fall into the category of out of pocket costs.

Eg. Rent paid, wages, Transport charges and salaries

Analysis (contd..)Analysis (contd..)

Accounting costs

Accounting costs are the actual or out lay costs that point out the amount of expenditure that has already been incurred on a particular process or on production as such accounting costs facilitate for managing the taxation needs and profitability of the firm

Eg. All sunk costs are accounting costs.

Accounting costs

Accounting costs are the actual or out lay costs that point out the amount of expenditure that has already been incurred on a particular process or on production as such accounting costs facilitate for managing the taxation needs and profitability of the firm

Eg. All sunk costs are accounting costs.

Analysis (contd..)Analysis (contd..)

Economic costs

Economic costs are related to future. They play a vital role in business decisions as the costs considered in decision making are usually future costs. they have the nature similar to that incremental imputed, explicit and opportunity costs.

Economic costs

Economic costs are related to future. They play a vital role in business decisions as the costs considered in decision making are usually future costs. they have the nature similar to that incremental imputed, explicit and opportunity costs.

Analysis (contd..)Analysis (contd..)

Direct costs

Direct costs are those which have direct relationship with a unit of operation like manufacturing a product, organization a process of an activity et. In other words, direct costs are those which are directly and definitely identifiable.

Eg. In operating railway services, the costs of wagons, coaches and engines are direct costs.

Direct costs

Direct costs are those which have direct relationship with a unit of operation like manufacturing a product, organization a process of an activity et. In other words, direct costs are those which are directly and definitely identifiable.

Eg. In operating railway services, the costs of wagons, coaches and engines are direct costs.

Analysis (contd..)Analysis (contd..)

In direct costs

Indirect costs are those which cannot be easily and definitely identifiable in relation to a plant, a product, a process or a department. Like the direct costs indirect costs, do not vary means they may or may not be variable in nature.

Eg. Factory building, The track of railway system

In direct costs

Indirect costs are those which cannot be easily and definitely identifiable in relation to a plant, a product, a process or a department. Like the direct costs indirect costs, do not vary means they may or may not be variable in nature.

Eg. Factory building, The track of railway system

Analysis (contd..)Analysis (contd..)

Controllable costs

Controllable costs are those which can be controlled or regulated through observation by an executive and therefore they can be used for assessing the efficiency of the executive. Most of the costs are controllable.

Eg. Inventory costs can be controlled at the shop level

Controllable costs

Controllable costs are those which can be controlled or regulated through observation by an executive and therefore they can be used for assessing the efficiency of the executive. Most of the costs are controllable.

Eg. Inventory costs can be controlled at the shop level

Analysis (contd..)Analysis (contd..)

Non Controllable costs

Non Controllable costs are those which can not be subjected to administrative control and supervision are called non controllable costs.

Eg. Costs due obsolesce and depreciation, capital costs.

Non Controllable costs

Non Controllable costs are those which can not be subjected to administrative control and supervision are called non controllable costs.

Eg. Costs due obsolesce and depreciation, capital costs.

Analysis (contd..)Analysis (contd..)

Historical cost & Replacement cost

Historical cost (Original cost) of an asset refers to the original price paid by the management to purchase it in the past. Whereas the Replacement cost refers to the cost that a firm incurs to replace or acquire the same asset now.

The distinction between the historical cost and the replacement cost result from the changes of prices over time.

Eg. If a firm acquires a machine for rs.20,000 in the year 1990 and the same machine cost of rs.40,000 now. The amount of rs.20,000 is the historical cost and the amount of rs.40,000 is the replacement cost.

Historical cost & Replacement cost

Historical cost (Original cost) of an asset refers to the original price paid by the management to purchase it in the past. Whereas the Replacement cost refers to the cost that a firm incurs to replace or acquire the same asset now.

The distinction between the historical cost and the replacement cost result from the changes of prices over time.

Eg. If a firm acquires a machine for rs.20,000 in the year 1990 and the same machine cost of rs.40,000 now. The amount of rs.20,000 is the historical cost and the amount of rs.40,000 is the replacement cost.

Analysis (contd..)Analysis (contd..)

Shut down costs

The costs which a firm incurs when it temporarily stops its operations are called “shutdown costs”. These costs can be saved when the firm again starts its operations. Shutdown costs include fixed costs, maintenance cost, lay-off expenses etc..

Shut down costs

The costs which a firm incurs when it temporarily stops its operations are called “shutdown costs”. These costs can be saved when the firm again starts its operations. Shutdown costs include fixed costs, maintenance cost, lay-off expenses etc..

Analysis (contd..)Analysis (contd..)

Abandonment costs

Abandonment costs are those costs which are incurred for the complete removal of the fixed assts from use. These may occur due to obsolesce or due to improvisation of the firm. Abandonment costs thus involve problem of disposal of the assts

Abandonment costs

Abandonment costs are those costs which are incurred for the complete removal of the fixed assts from use. These may occur due to obsolesce or due to improvisation of the firm. Abandonment costs thus involve problem of disposal of the assts

Analysis (contd..)Analysis (contd..)

Urgent cost and Post ponable cost

Urgent costs are those costs which have to be incurred compulsorily by the management in order to continue its operations.

Eg. Costs of material, labor, fuel

Post ponable costs are those which if not incurred in time do ot effect the operational efficiency of the firm

Eg. Maintenance of costs

Urgent cost and Post ponable cost

Urgent costs are those costs which have to be incurred compulsorily by the management in order to continue its operations.

Eg. Costs of material, labor, fuel

Post ponable costs are those which if not incurred in time do ot effect the operational efficiency of the firm

Eg. Maintenance of costs

Analysis (contd..)Analysis (contd..)

Business costs & Full costs

Business costs include all the expenses incurred by the firm to carry out business activities. According to Watson and Donald “Business costs include all the payments and contractual obligations made by the firm

Eg. Income tax, profit & loss

Full costs include business costs, opportunity costs and normal profit. Opportunity cost is the expected return /earnings form the next best use of the firm.

Business costs & Full costs

Business costs include all the expenses incurred by the firm to carry out business activities. According to Watson and Donald “Business costs include all the payments and contractual obligations made by the firm

Eg. Income tax, profit & loss

Full costs include business costs, opportunity costs and normal profit. Opportunity cost is the expected return /earnings form the next best use of the firm.

Analysis (contd..)Analysis (contd..)

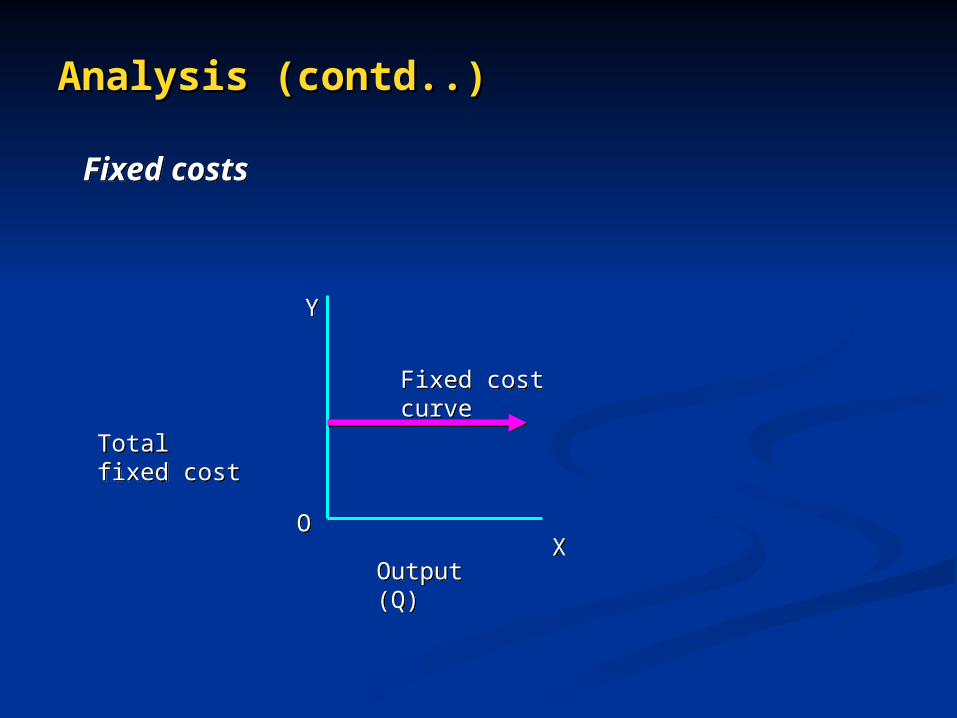

Fixed costs

Fixed costs are the costs that do not vary with the changes in output. In other words, fixed costs are those which are fixed in volume though there are variations in the output level.

Eg. Expenditures on depreciation costs of administrative or managerial staff, rent on land and building and property tax etc.

Fixed costs

Fixed costs are the costs that do not vary with the changes in output. In other words, fixed costs are those which are fixed in volume though there are variations in the output level.

Eg. Expenditures on depreciation costs of administrative or managerial staff, rent on land and building and property tax etc.

Analysis (contd..)Analysis (contd..)

Fixed costs Fixed costs

Output (Q)Output (Q)

Total fixed costTotal fixed cost

YY

OOXX

Fixed cost curveFixed cost curve

Analysis (contd..)Analysis (contd..)

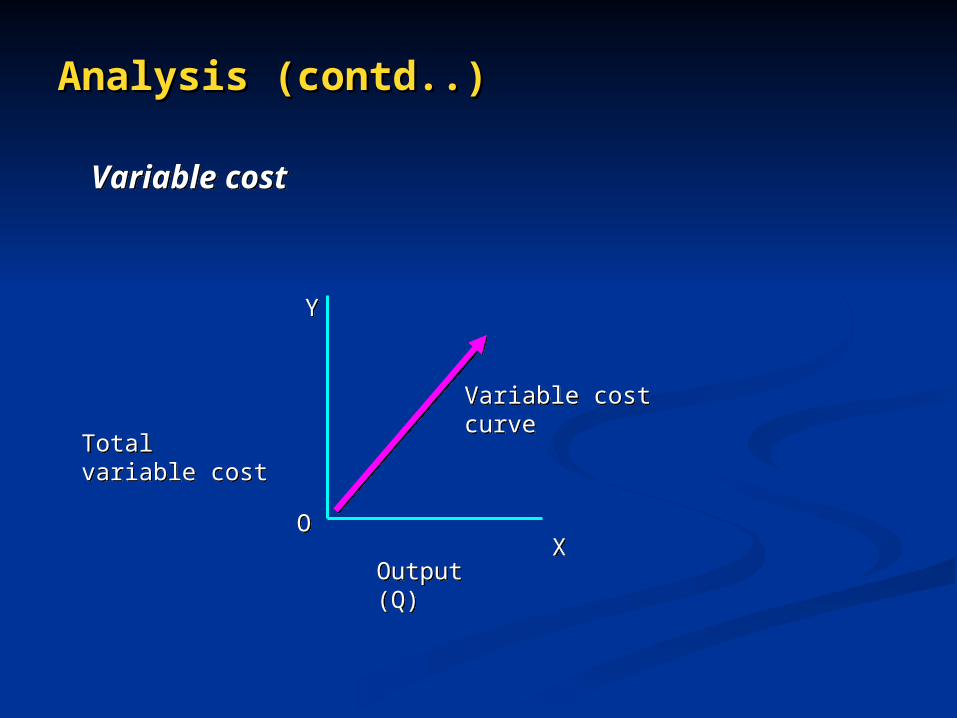

Variable cost

Variable costs ae those that are directly dependent on the output i.e. they vary with the variation in the volume / level of output. Variable costs increase with an increase in output level but not necessarily in the same proportion.

Eg. Cost of raw material, expenditures on labor, running cost or maintenance costs of fixed assets.

Variable cost

Variable costs ae those that are directly dependent on the output i.e. they vary with the variation in the volume / level of output. Variable costs increase with an increase in output level but not necessarily in the same proportion.

Eg. Cost of raw material, expenditures on labor, running cost or maintenance costs of fixed assets.

Analysis (contd..)Analysis (contd..)

Variable cost Variable cost

Output (Q)Output (Q)

Total variable costTotal variable cost

YY

OOXX

Variable cost curveVariable cost curve

Analysis (contd..)Analysis (contd..)

Total cost

Total cost refers to the money value of the total resources required for the production of goods and services by the firm. In other words, it refers to the total outlays of money expenditure, both explicit and implicit.

TC = VC+FC

TC = Total cost

VC = Variable cost

FC = Fixed cost

Total cost

Total cost refers to the money value of the total resources required for the production of goods and services by the firm. In other words, it refers to the total outlays of money expenditure, both explicit and implicit.

TC = VC+FC

TC = Total cost

VC = Variable cost

FC = Fixed cost

Analysis (contd..)Analysis (contd..)

Total cost curve Total cost curve

Output (Q)Output (Q)

Total costTotal cost

YY

OOXX

Total costTotal cost

Analysis (contd..)Analysis (contd..)

Average cost

It refers to the cost per unit of output assuming that production of each unit of output incurs the same cost. It is statistical in nature and is not an actual cost. It is obtained by dividing Total cost.

TC

AC =

Q

TC = Total cost incurred in production process.

Q = Output cost

Average cost

It refers to the cost per unit of output assuming that production of each unit of output incurs the same cost. It is statistical in nature and is not an actual cost. It is obtained by dividing Total cost.

TC

AC =

Q

TC = Total cost incurred in production process.

Q = Output cost

Analysis (contd..)Analysis (contd..)

Marginal cost

MC refers to the incremental or additional costs that are incurred when there is an addition to the existing output level of goods and services, in other words it is the addition to the total cost on account of producing addition units of the output

MC = TC (n+1)

MC = Marginal cost

TCn = Total cost before addition of units

TC(n+1) = Total cost after addition

n = Number of units of output

Marginal cost

MC refers to the incremental or additional costs that are incurred when there is an addition to the existing output level of goods and services, in other words it is the addition to the total cost on account of producing addition units of the output

MC = TC (n+1)

MC = Marginal cost

TCn = Total cost before addition of units

TC(n+1) = Total cost after addition

n = Number of units of output

Analysis (contd..)Analysis (contd..)

Marginal cost curve Marginal cost curve

Output (Q)Output (Q)

YY

OOXX

Marginal costMarginal cost

Marginal costMarginal cost

Analysis (contd..)Analysis (contd..)

Short run cost and Long run cost

Both short run and long run costs are related foxed and variable costs and are often used in economic analysis.

Short run costs: these costs are which vary with the variations in the output with size of the firm as same. Short run costs are same as variable costs.

Long run costs: these costs are which incurred on the fixed assets like land and building, plant and machinery etc. long run costs are same as fixed costs.

Short run cost and Long run cost

Both short run and long run costs are related foxed and variable costs and are often used in economic analysis.

Short run costs: these costs are which vary with the variations in the output with size of the firm as same. Short run costs are same as variable costs.

Long run costs: these costs are which incurred on the fixed assets like land and building, plant and machinery etc. long run costs are same as fixed costs.

Analysis (contd..)Analysis (contd..)

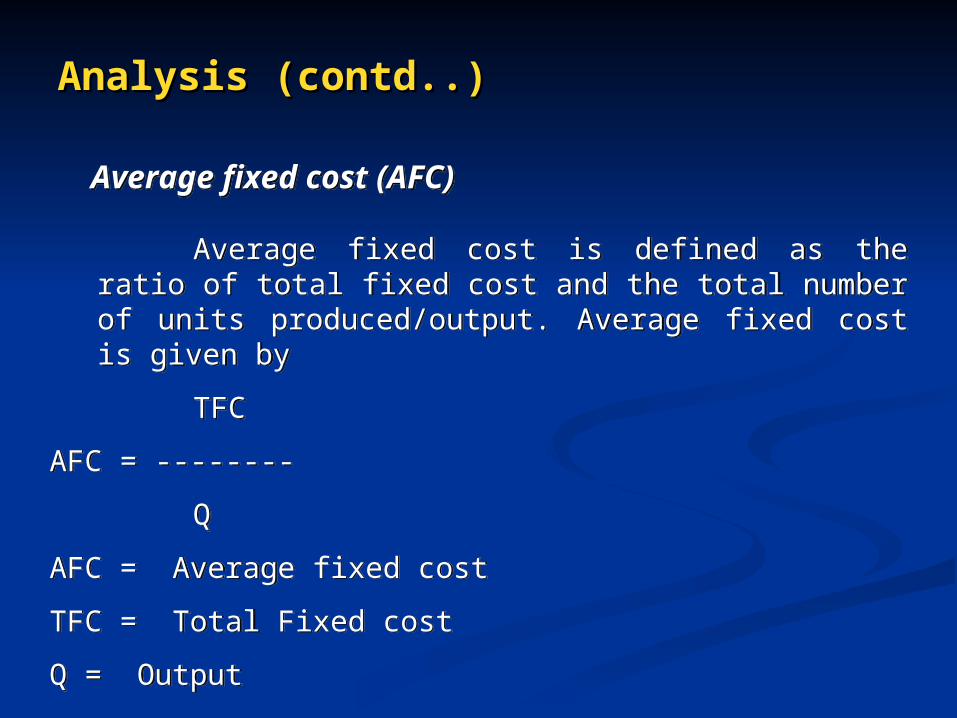

Average fixed cost (AFC)

Average fixed cost is defined as the ratio of total fixed cost and the total number of units produced/output. Average fixed cost is given by

TFC

AFC = --------

Q

AFC = Average fixed cost

TFC = Total Fixed cost

Q = Output

Average fixed cost (AFC)

Average fixed cost is defined as the ratio of total fixed cost and the total number of units produced/output. Average fixed cost is given by

TFC

AFC = --------

Q

AFC = Average fixed cost

TFC = Total Fixed cost

Q = Output

Analysis (contd..)Analysis (contd..)

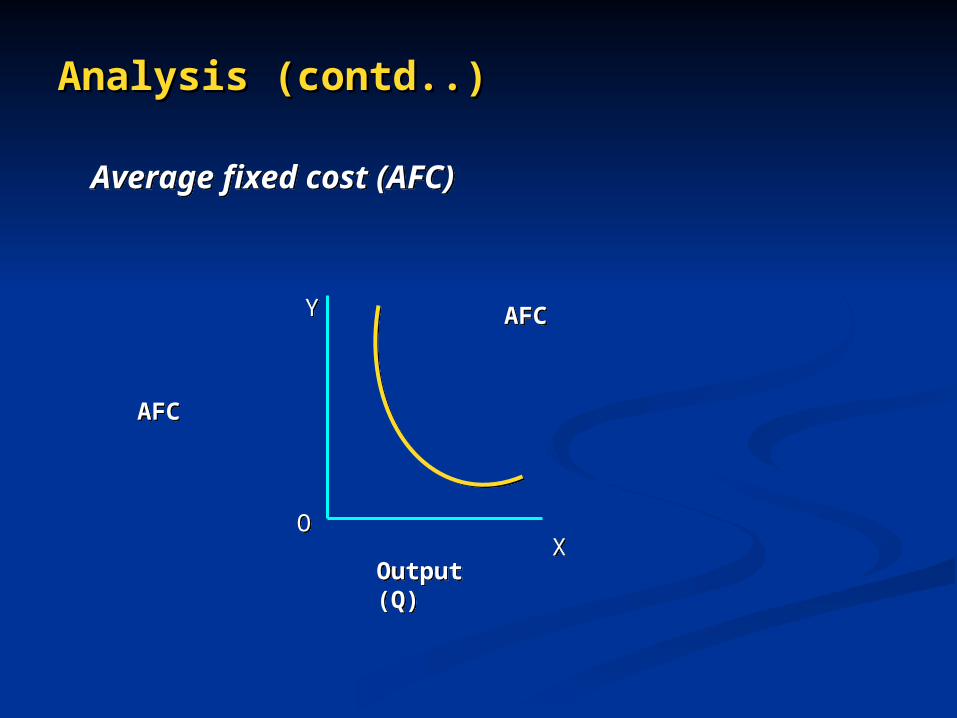

Average fixed cost (AFC) Average fixed cost (AFC)

Output (Q)Output (Q)

YY

OOXX

AFCAFC

AFCAFC

Analysis (contd..)Analysis (contd..)

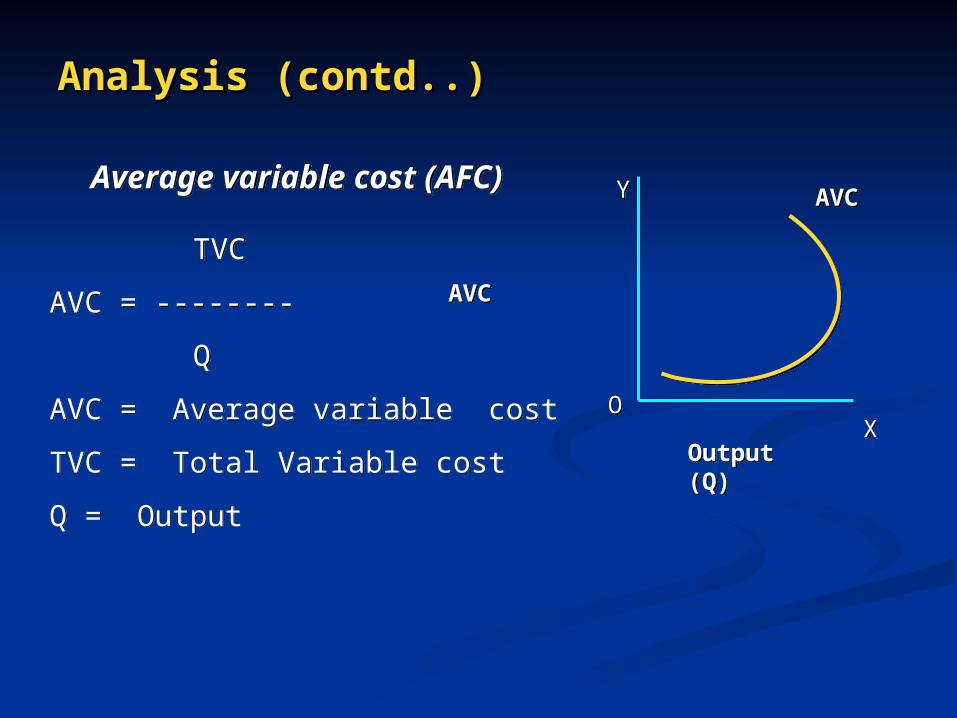

Average variable cost (AFC)

TVC

AVC = --------

Q

AVC = Average variable cost

TVC = Total Variable cost

Q = Output

Average variable cost (AFC)

TVC

AVC = --------

Q

AVC = Average variable cost

TVC = Total Variable cost

Q = Output

Output (Q)Output (Q)

YY

OOXX

AVCAVC

AVCAVC

Analysis (contd..)Analysis (contd..)

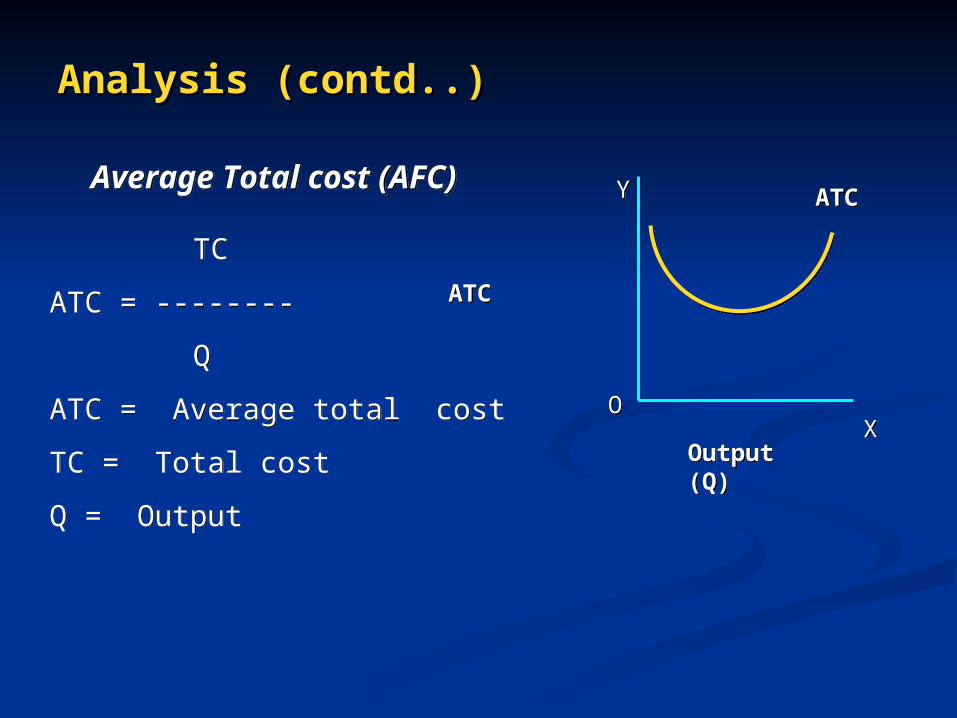

Average Total cost (AFC)

TC

ATC = --------

Q

ATC = Average total cost

TC = Total cost

Q = Output

Average Total cost (AFC)

TC

ATC = --------

Q

ATC = Average total cost

TC = Total cost

Q = Output

Output (Q)Output (Q)

YY

OOXX

ATCATC

ATCATC

Analysis (contd..)Analysis (contd..)

Break even analysis

The Break – Even point can be defined as that level of sales at which total revenue equals total costs and the net income is equal to zero. This is also known as no-profit and no-loss point.

Break even analysis

The Break – Even point can be defined as that level of sales at which total revenue equals total costs and the net income is equal to zero. This is also known as no-profit and no-loss point.

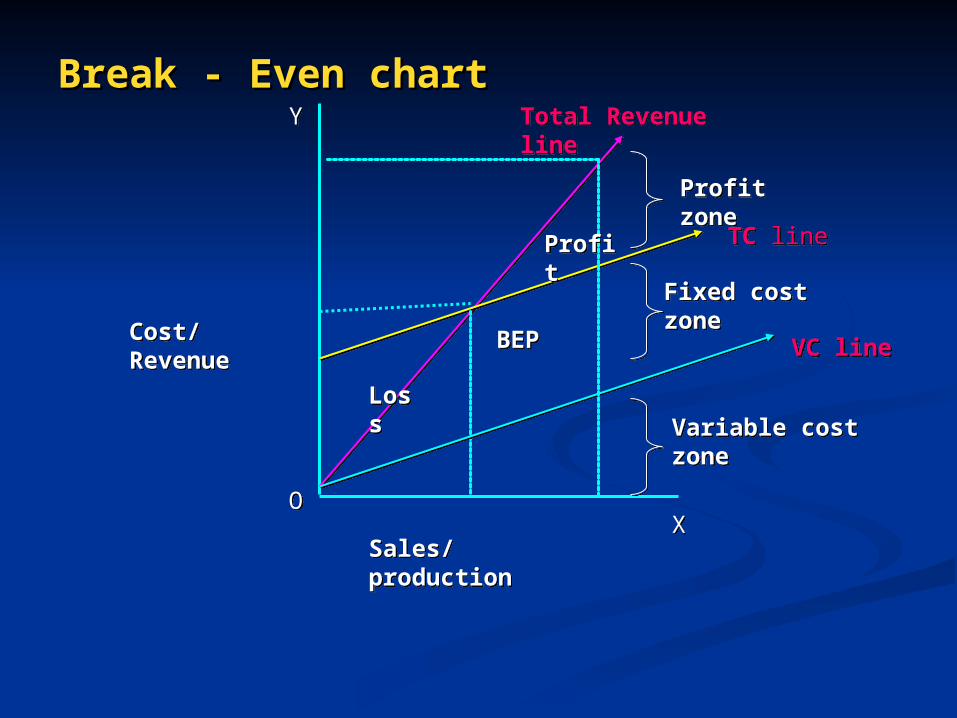

Break - Even chartBreak - Even chart

Sales/productionSales/production

YY

OOXX

Cost/RevenueCost/Revenue BEPBEP

Profit zoneProfit zone

Fixed cost zoneFixed cost zone

Variable cost zoneVariable cost zone

TC lineTC line

VC lineVC line

Total Revenue lineTotal Revenue line

LossLoss

ProfitProfit

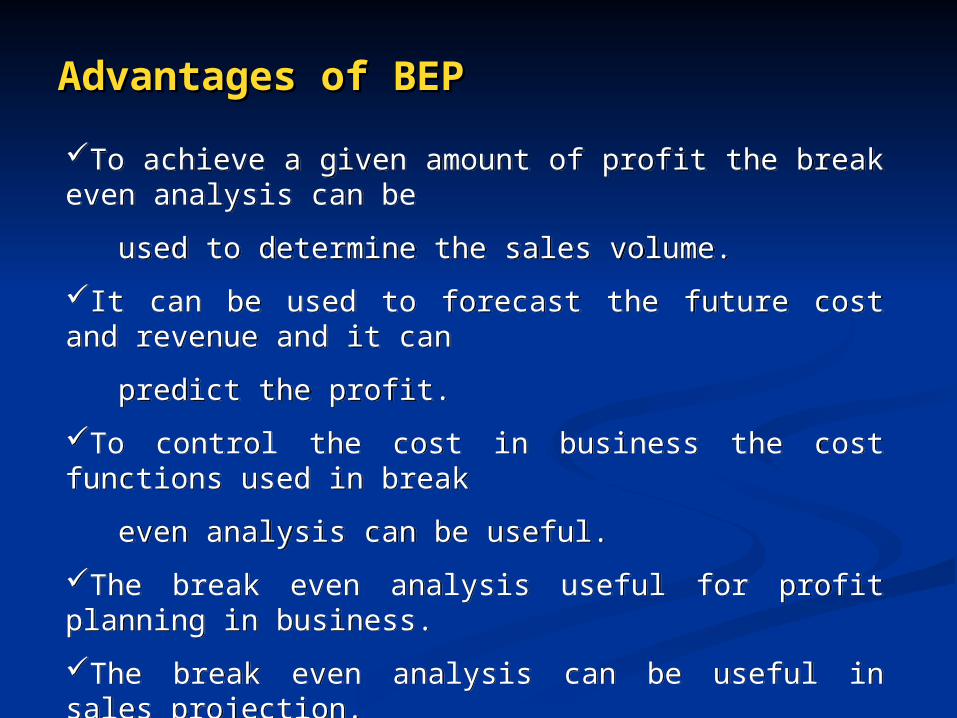

Advantages of BEPAdvantages of BEP

To achieve a given amount of profit the break even analysis can be

used to determine the sales volume.

It can be used to forecast the future cost and revenue and it can

predict the profit.

To control the cost in business the cost functions used in break

even analysis can be useful.

The break even analysis useful for profit planning in business.

The break even analysis can be useful in sales projection.

To achieve a given amount of profit the break even analysis can be

used to determine the sales volume.

It can be used to forecast the future cost and revenue and it can

predict the profit.

To control the cost in business the cost functions used in break

even analysis can be useful.

The break even analysis useful for profit planning in business.

The break even analysis can be useful in sales projection.

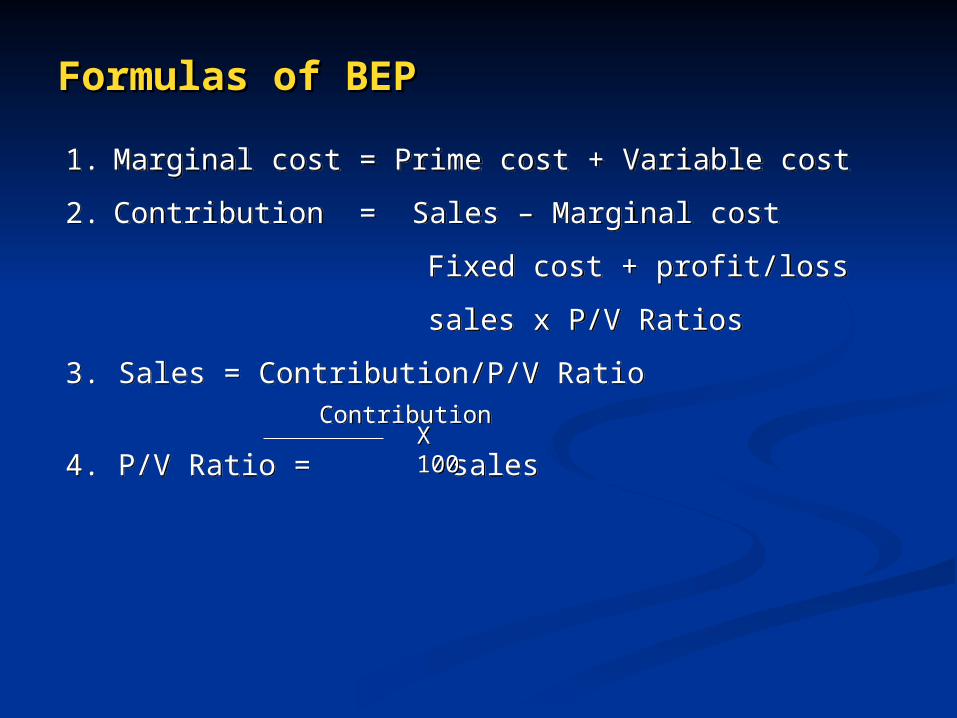

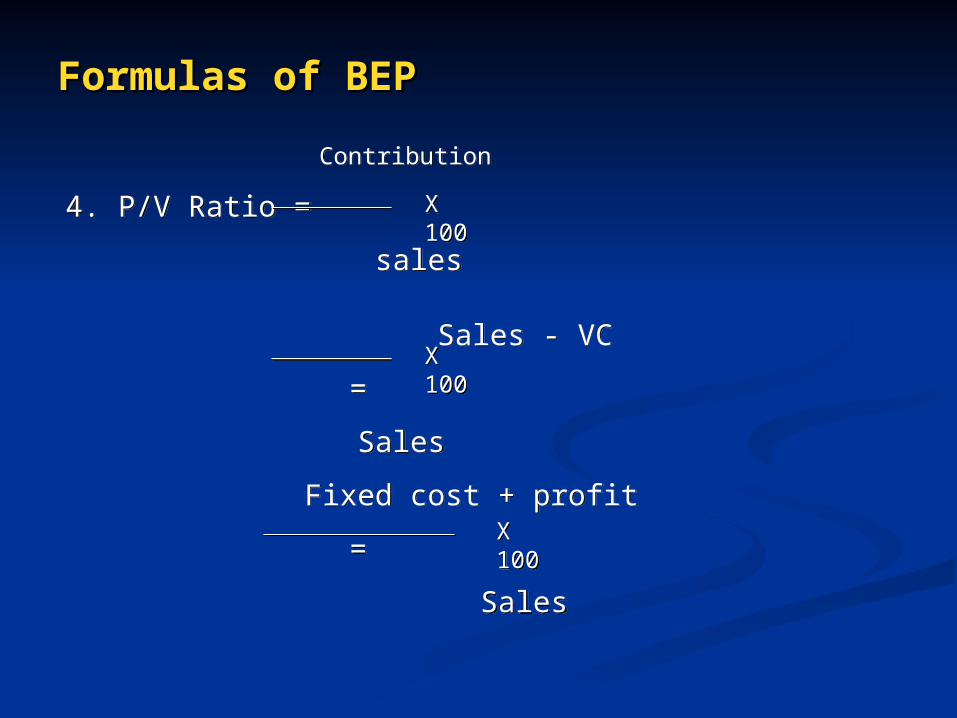

Formulas of BEPFormulas of BEP

1. Marginal cost = Prime cost + Variable cost

2. Contribution = Sales – Marginal cost

Fixed cost + profit/loss

sales x P/V Ratios

3. Sales = Contribution/P/V Ratio Contribution

4. P/V Ratio = sales

1. Marginal cost = Prime cost + Variable cost

2. Contribution = Sales – Marginal cost

Fixed cost + profit/loss

sales x P/V Ratios

3. Sales = Contribution/P/V Ratio Contribution

4. P/V Ratio = salesX 100X 100

Formulas of BEPFormulas of BEP

Contribution

4. P/V Ratio =

sales

Sales - VC

=

Sales

Fixed cost + profit

=

Sales

Contribution

4. P/V Ratio =

sales

Sales - VC

=

Sales

Fixed cost + profit

=

Sales

X 100X 100

X 100X 100

X 100X 100

Formulas of BEPFormulas of BEP

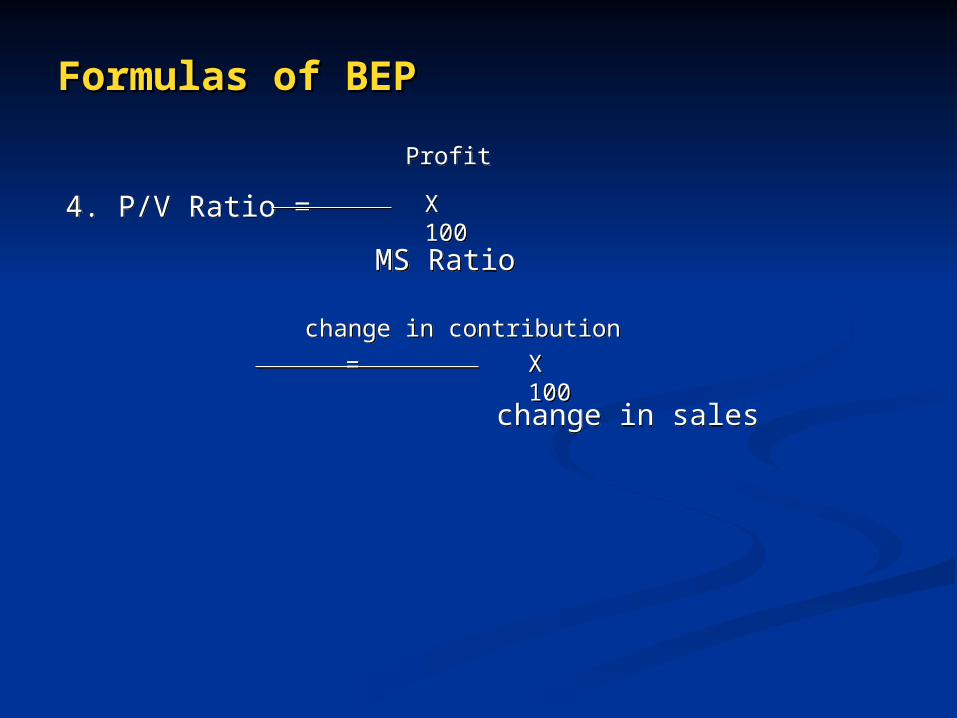

Profit

4. P/V Ratio =

MS Ratio

change in contribution

=

change in sales

Profit

4. P/V Ratio =

MS Ratio

change in contribution

=

change in sales

X 100X 100

X 100X 100

Formulas of BEPFormulas of BEP

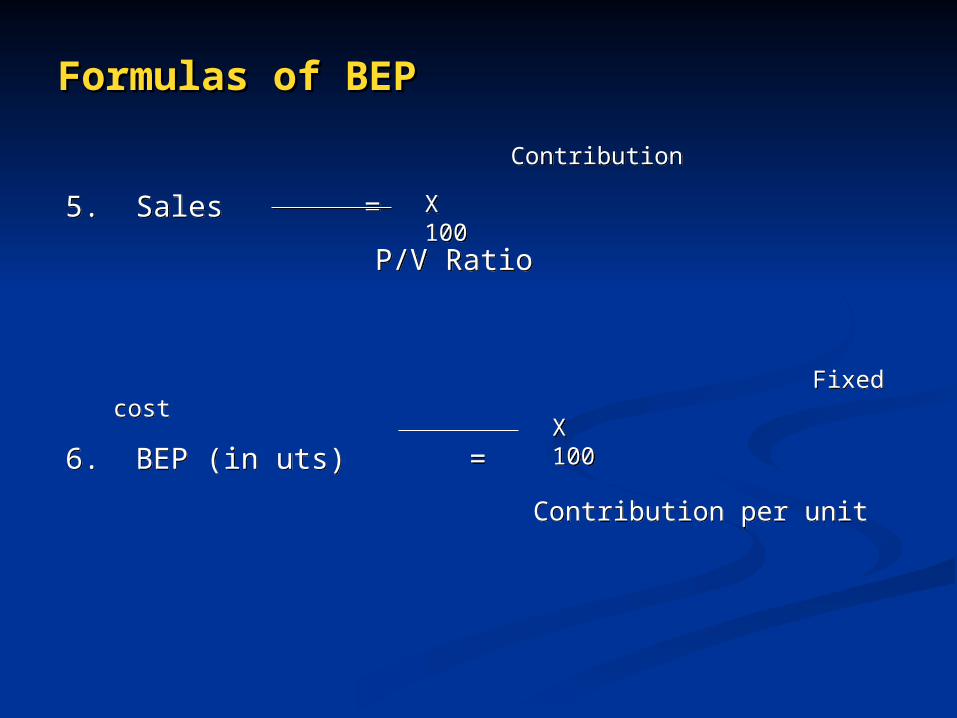

Contribution

5. Sales =

P/V Ratio

Contribution

5. Sales =

P/V Ratio

X 100X 100

Fixed cost

6. BEP (in uts) =

Contribution per unit

Fixed cost

6. BEP (in uts) =

Contribution per unit

X 100X 100

Formulas of BEPFormulas of BEP

FC X S

6. BEP (in Rs.) =

S – V

7. Margin of safety = Total sales – BEP Sales

Total sales - BEP Sales =

Total Sales

FC X S

6. BEP (in Rs.) =

S – V

7. Margin of safety = Total sales – BEP Sales

Total sales - BEP Sales =

Total Sales

Formulas of BEPFormulas of BEP

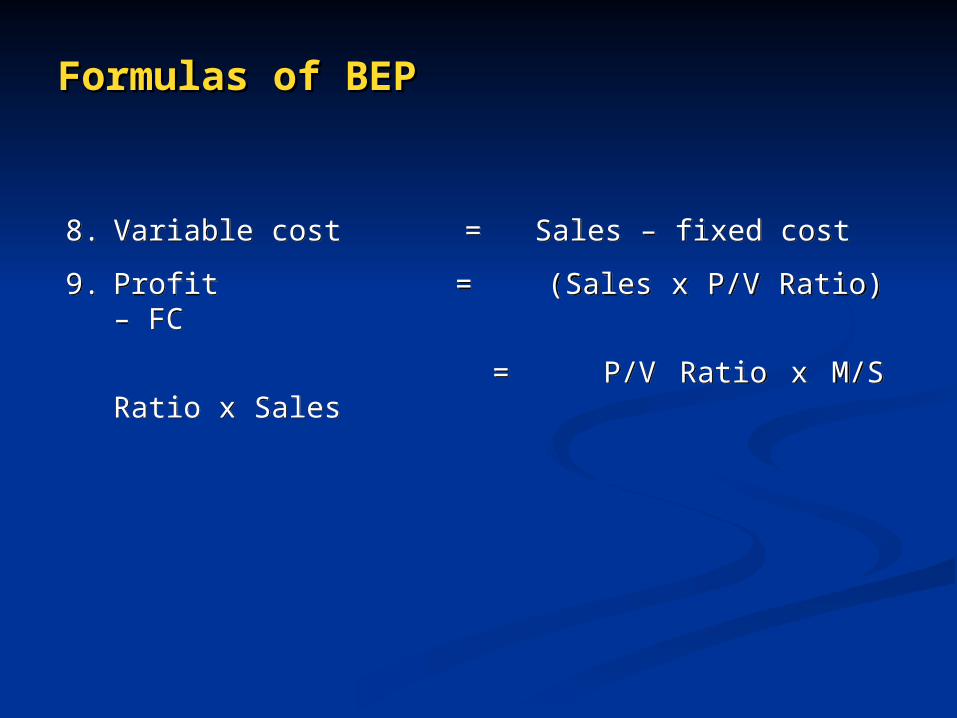

8. Variable cost = Sales – fixed cost

9. Profit = (Sales x P/V Ratio) – FC

= P/V Ratio x M/S Ratio x Sales

8. Variable cost = Sales – fixed cost

9. Profit = (Sales x P/V Ratio) – FC

= P/V Ratio x M/S Ratio x Sales