Embed Size (px)

Citation preview

Unit 2– PFM domains and sequencing of reforms

Module 2.4: External control, legislative and regulatory framework and IT issues

External Control

Day 2: Sub-systems of PFM and prioritsing reforms

• Module 2.1. Expenditure Classification, budget Preparation and the MTEF

• Module 2.2. Expenditure and accounting cycle• Module 2.3. Program/Performance budget• Module 2.4. External control, legislative and

regulatory framework and IT (information technology)issues

22

Module 2.4

Two sub-modules:

• External Control(External Auditor, Parliament): Aims to put forward general principles and identify essential functions

• The information system: Aims to identify key questions to examine during the process of increasing computerisation

3

Module 2.4. Key Examined Points

• External control• External audit• Parliament

• Legislative and regulatory framework

• Information systems

4

External Audit

• Guaranteed by Supreme Audit Institution(SAI)• Court of Audit, Court of Finances, National Audit Office,

etc.

• The key point is the independence of the SAI• Which must be guaranteed by the constitution according

to INTOSAI (International Organization of Supreme Audit Institutions)

5

Basic Principles - INTOSAI(*)• A legislative and regulatory framework must be established

• Independence of SAI members

• Financial independence of SAI

• All the operations related to public finance must be under their supervision

• Unrestriced access to information

• Right and obligation to present reports

• Freedom to decide the content and scope of publication of audit reports

• Effective implementation of the recommendations

• Adequate resources (human and financial)

* International Organization of Supreme Audit Institutions 6

Different types of Audit• Compliance audit consists in assessing compliance with legal and

administrative rules, the integrity and suitability of administrative, financial and management control systems.

• Financial audit consists in reviewing the financial statements and the accounting systems on which they are based and report on them;

• Performance audits assesses management and operation performance of government programs as well as of some public departments and agencies i.e. to evaluate the effectiveness and efficiency with which the program or the organization uses various resources

7

End-of-year Accounts

• The end-of-year accounts are first submitted to the SAI, and then to the parliament• Often with significant delays

• La loi de règlement (French System)• Administrative account (Authorising Officer) and management

account (Accountant)• Report by Court of Audit/finance with certificate of compliance

(or not)• Major weaknesses

•Long delays;•Administrative and management accounts are often incomplete and difficult to compare

8

The Basics

General Principles• Functioning SAI, independent, covering all the financial

transactions and public money, qualified accountants and use of standards consistent with the code of conduct of INTOSAI

• Regularity Audit• End-of-the-year account Audit• Public reports of SAI• Respect of the recommendation by the executive• A parliamentary commission examines SAI reports

Procedure: PEFA indicators../…

9

PEFA-PI 25. Quality and timliness of annual financial statements - Basics

• (i) Spectrum of coverage of financial statement: Grade C o A consolidated government statement is prepared

annually….but the omission are not significant• (ii) Timliness of submission of financial statements: Grade A;

o The financial statement is submitted for external audit within 6 months of the end of the fiscal year.

o The key is to ensure that the total period for the submission of year-end accounts (PI-25 (ii) and PI-26 (ii)) is a maximum of 10 months

• (iii) The accounting standards used: Score C

10

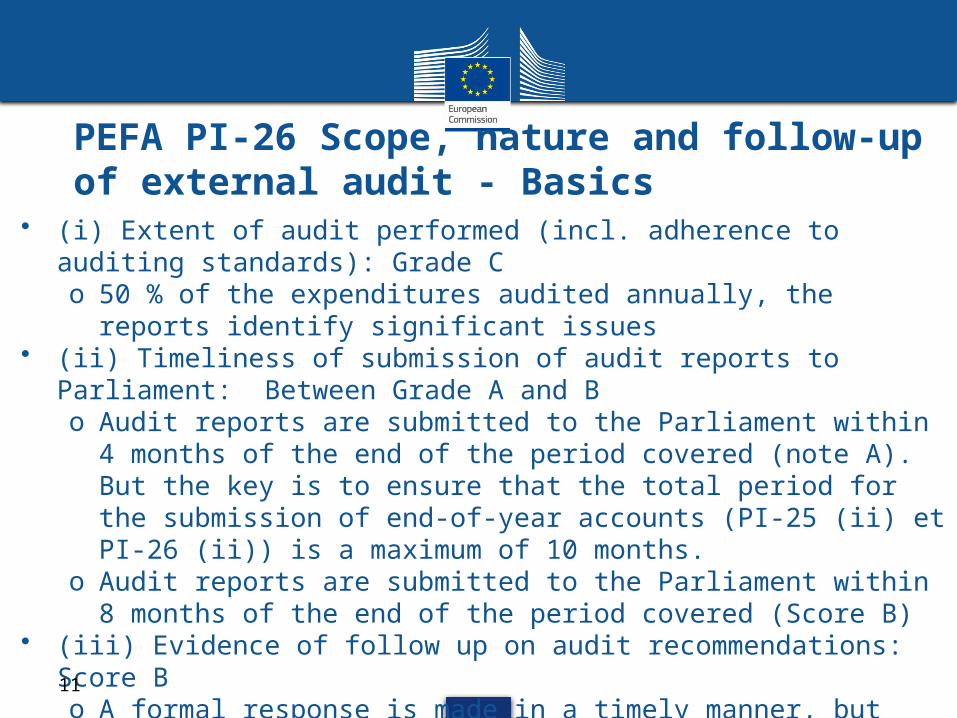

PEFA PI-26 Scope, nature and follow-up of external audit - Basics

• (i) Extent of audit performed (incl. adherence to auditing standards): Grade C o 50 % of the expenditures audited annually, the reports identify

significant issues• (ii) Timeliness of submission of audit reports to Parliament:

Between Grade A and Bo Audit reports are submitted to the Parliament within 4 months

of the end of the period covered (note A). But the key is to ensure that the total period for the submission of end-of-year accounts (PI-25 (ii) et PI-26 (ii)) is a maximum of 10 months.

o Audit reports are submitted to the Parliament within 8 months of the end of the period covered (Score B)

• (iii) Evidence of follow up on audit recommendations: Score Bo A formal response is made in a timely manner, but there is

little evidence of systematic follow up. 11

PEFA PI- 28. Legislative scrutiny of external audit reports - Basics

• (i) Timeliness of examination of audit reports : Grade Co Scrutiny of audit reports is usually completed by the

legislature within 12 months from receipt of the reports.• (ii) Extent of hearings : Grade C

o In-depth hearings on key findings take place with responsible officers from the audited entities as a routine, but may cover only some of the entities... (Score C because priority is given to measures depending on the Executive)

• (iii) Issuance of recommended actions by the legislature and implementation by the executive: Grade B

o Actions are recommended, and proof has been drawn that they were acted upon by the executive.

12

The Parliament

Basics• Allow sufficient time for the Parliament to discuss the

Finance Act• Submission of the audited accounts within 10 months

of the end of fiscal year (cf. PEFA PI-25 (ii) et PI-28 (ii)) Gradually reinforce the capacity of the parliament

• Importance of parliamentary commission

13

PI-27 Legislative scrutiny of the annual budget law. The basics

• i) Scope of the legislature’s scrutiny : Grade B . o The Parliamentary control covers fiscal policies and

aggregates for the coming year as well as detailed estimates of expenditure and revenue.

• ii) Extent to which the legislature’s procedures are well-established and respected : Grade B. o Simple procedures exist for the Parliament’s budget review and

are respected.

• iii) Adequacy of the time devoted to providing a response to budget proposal

• iv) Rules for in-year amendments to the budget without ex-ante approval by the Parliament.

• 14

PEFA PI-27 Legislative scrutiny of the annual budget law. The Basics

• iii) Adequacy of time for the legislature to provide a response to budget proposals. Grade B.o The legislature has at least one month to review the budget

proposals. • iv) Rules for in-year amendments to the budget without ex-

ante approval by the legislature. o Clear rules exist for in-year budget amendments by the

executive, and are usually respected, but they allow extensive administrative reallocations.

15

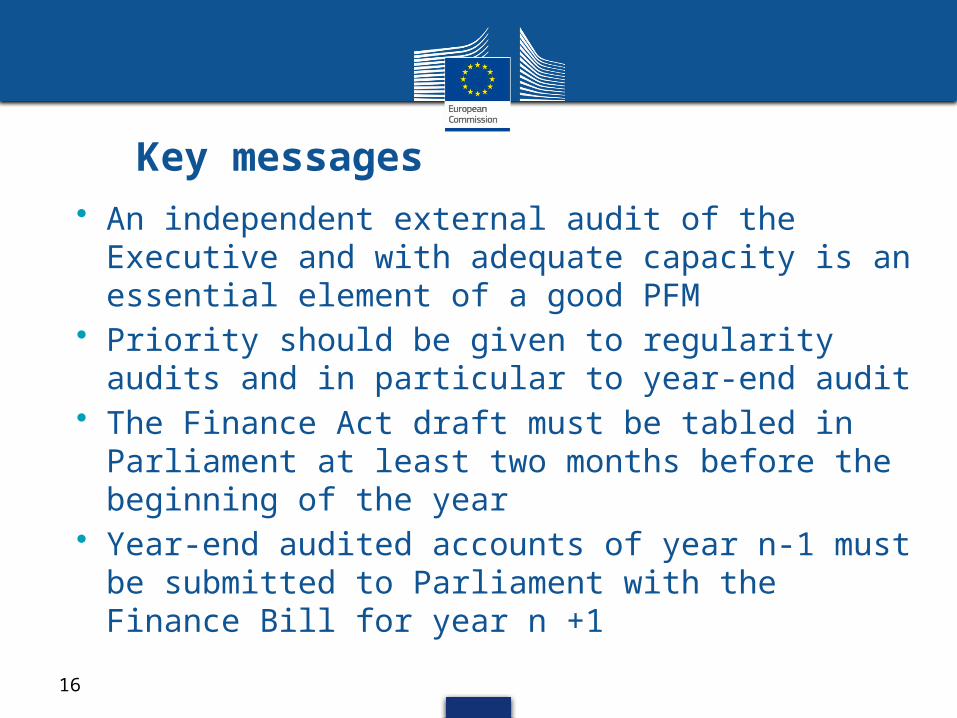

Key messages• An independent external audit of the Executive

and with adequate capacity is an essential element of a good PFM

• Priority should be given to regularity audits and in particular to year-end audit

• The Finance Act draft must be tabled in Parliament at least two months before the beginning of the year

• Year-end audited accounts of year n-1 must be submitted to Parliament with the Finance Bill for year n +1

16

Module 2.4. Key Examined Point

• External Control• External Audit• Parliament

• Legislative and regulatory framework

• Information systems

17

Legislative and Regulatory framework

• Constitution• [Organic] Budget Act (or Public Finance

Management Act, Budget Framework Law, etc.)

• Other laws and regulationsAudit ActFiscal responsibility lawTerritorial Authorities Financial Act (French system)Decree on Public AccountingFinancial regulations

18

Key points of the legislative framework

• Provide a framework for the parliamentary authority

• Establish responsibilitiesCountries in transition: strengthen the powers

of the Minister of Finance

• Define the principles of sound fiscal management

• Define the reporting obligation

19

Organic laws governing financial laws: Key Elements• General principles

Unity, Universality, transparency

• Concepts and definition• Scope of the Budget• General principles for accounting and budget

classification• The budget authorisation• The budget calendar• Execution and revision of the budget• Debt and liabilities• Roles and responsibilities • Relations with local communities• External Audit• Sanctions 20

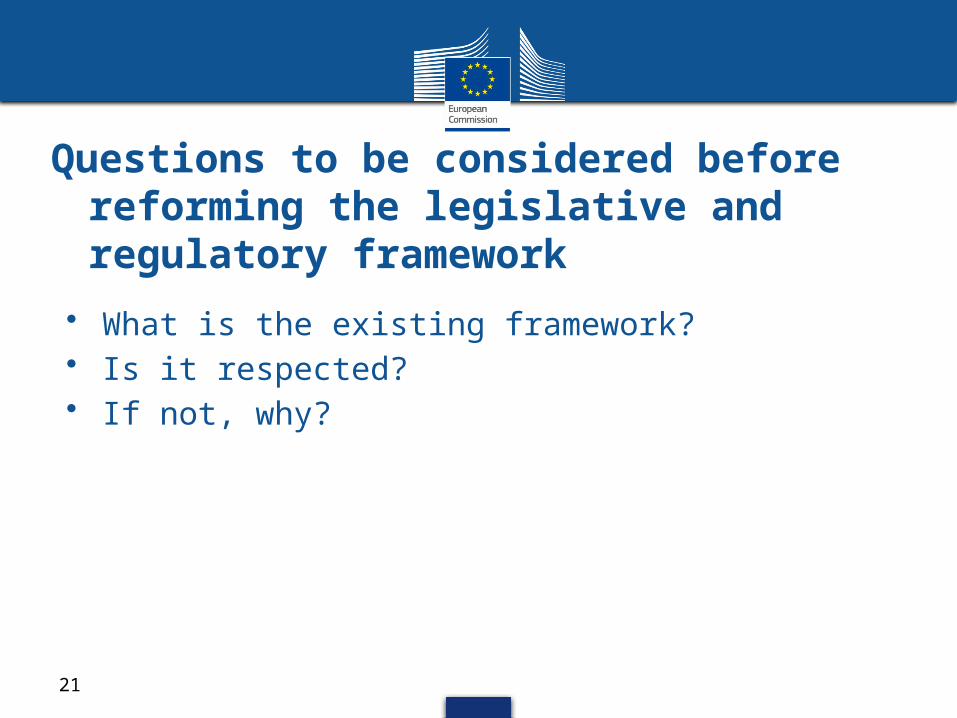

Questions to be considered before reforming the legislative and regulatory framework

• What is the existing framework?• Is it respected?• If not, why?

21

Key Messages

• The legislative and regulatory framework must follow the basics discussed

• The first step is an organic law establishing principles for budget management and distribution of responsibilities

• It should be checked whether the existing legislative and regulatory framework is implemented

22

Module 2.4. Key Points examined

• External control• External Audit• Parliament

• Legislative and regulatory framework

• Information Systems

23

Information Management Systems

• Management information is necessary• For scheduling, implementation and surveillance;• For the Minister of finance and sectoral ministries

• It is not a mere collection of statistical data• Financial and Physical Information• Dashboard• Must be available quickly in order to enable to take decisions

• It is not only IT, but It may be useful to classify, sort and publish the data in various formats.

24

Integrated Financial Management System• “Heart” of the accounting system (General

Accounting)• Setting standard exchanges between systems• Covers all financial transactions

• Other Systems:• Budgetary module:

Accounting and budgetary control• Preparation of budget• Treasury management• Debt management• Revenue• Management modules for managers

25

26

General Accouting

Debt Management

Accounts Payable

Revenue management

systems

- Tax- Customs

- ..

Client Accounts

Budget &movement of

credit

Budget commitment

Validation-Authorisation

Payment

Budgetary System

staff management

payroll management

Treasury management

Macroeconomic foreacasts.

Budget Preparation

In practice (1) A large majority of the integrated systems are only

partially implemented Yet, the implementation process is time consuming

Dener. World Bank 2011

27

In practice (2) The average cost of the World Bank projects

is US$ 7.7 million

Dener. World Bank 2011

28

29

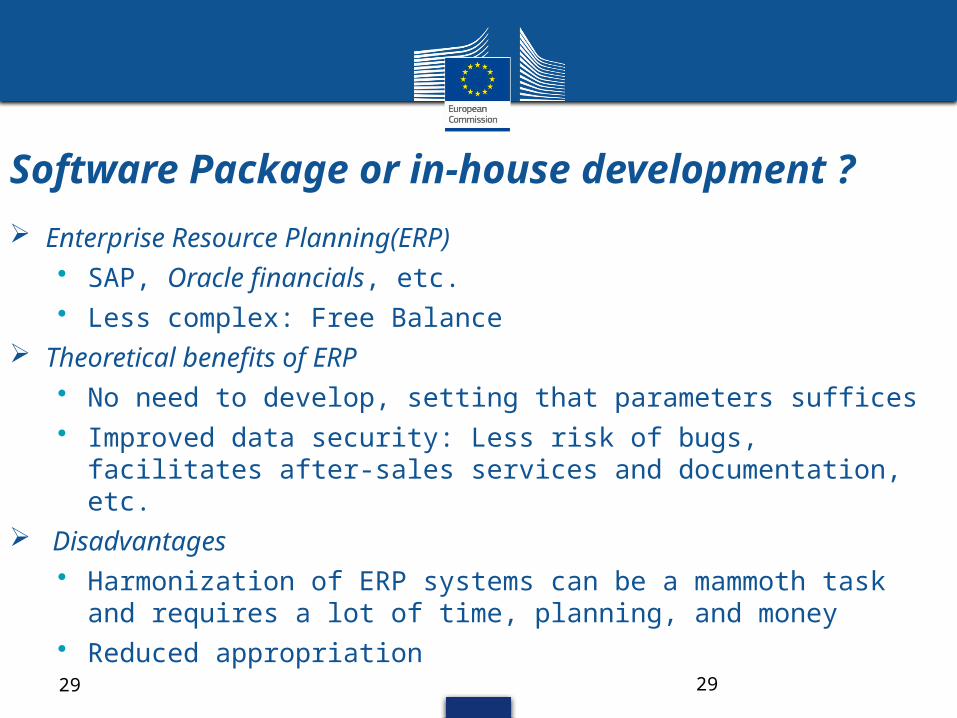

Software Package or in-house development ?

Enterprise Resource Planning(ERP) • SAP, Oracle financials, etc.• Less complex: Free Balance

Theoretical benefits of ERP • No need to develop, setting that parameters suffices • Improved data security: Less risk of bugs, facilitates after-sales

services and documentation, etc. Disadvantages

• Harmonization of ERP systems can be a mammoth task and requires a lot of time, planning, and money

• Reduced appropriation

29

Chorus : The Court of Auditors points a drop of 500 million euros ….While the Estimated cost of the Chorus project was Estimated in 2006 to be 1.01 billion Euros for the 2006-2015 period, the Agency for State Financial Data (ASFD) has updated its forecast because “adaptation cost of the departmental systems has been estimated to be € 220 million and that of the environment , which Chorus estimated to be € 280 million, bringing the total project cost of € 1.5 billion. "

An integrated system : CHORUS- France

30

According to an IMF study the computerized budget management system in Tanzania is one of the systems that give satisfactory results

This system has led to ad hoc development in Tanzania

It is not fully integrated. The following entities and systems are not integrated into the central system: (i) payroll and human resource management system, (ii) budget preparation system, (iii) computerized tax administration systems (iv) 21 sub-treasuries and regional ministries

Tanzania – A partially-integrated but functional system

3131

32

Should an ERP dictate procedure ?

Proponents of ERP suggest to review budgetary procedures to adapt to a ERP

• This is a mechanism that enables to reduce the costs of setting the parameters

This approach should be avoided

• Questionable procedures should not be computerised

• BUT computerization must take into account the existing, ongoing reforms and administrative culture

32

Computerisation should not substitute for establishment of proper procedures to create a robust system

Computerisation does not ensure integrity and regularity

GIGO

33

Preparing a computerization project Define the scope of the project Prior review of the procedures (ex. Budgetary

Classification) Examine capacity constraints, ensuring political

engagement Choose the options (ERP, development) Modalities of progressive extension to national

territory and ministries Project management apparatus Budget & Funding Change management

34

Sequencing (1)• Basics: A manual system, a precise budget classification,

charts of accounts, well defined procedures.• Subsequently, choosing the implementation approach based

on the existing system, planned reforms, etc• Scope of ERP

– In general, at least accounting and expenditure– But, starting with an auxiliary system such as payroll

can provide with a better cost-benefit ratio• Territorial coverage: An exhaustive territorial coverage can

take time– The procedure MUST be functional with or without

computerisation

35

Sequencing (2)

• Choosing the implementation process….• Technical aspects

– ERP or application development?

» Choice of ERP if ERP varies

– National network or separate database?

• Change management• Organisation and management of the project

• Training

• Other aspects of human resource management.

36

• Computerisation provides important support to management

• But it carries risks, which increase when:o The project is more complexo The ability of local officials to critically evaluate all

the aspects of the project is limitedo The project is led or strongly influenced by external

consultantso Political support is insufficient

• Integrated systems based on ERP can be very expensive and risky

Key Message

3737