Embed Size (px)

Citation preview

Unemployment, the Business Cycle and

Monetary Policy

Augmenting a Medium Sized New Keynesian DSGE Model

with Labor Market Dynamics

Master’s Thesis

to confer the academic degree of

Master of Science

in the Master’s Program

Economics

Author:

Alexander Koll

Submission:

Department of Economics

Thesis Supervisor:

Prof. Dr. Michael Landesmann

Assistant Thesis Supervisor:

Dr. Jochen Güntner

June 2015

1

Sworn Declaration

“I hereby declare under oath that the submitted Master's degree thesis has been written solely

by me without any third-party assistance, information other than provided sources or aids have

not been used and those used have been fully documented. Sources for literal, paraphrased and

cited quotes have been accurately credited.

The submitted document here present is identical to the electronically submitted text document”

2

Table of Contents 1. Abstract .......................................................................................................................................................... 3

2. Introduction .................................................................................................................................................... 3

3. The Christiano Eichenbaum Evans Model ..................................................................................................... 4

3.1. Empirical Estimation of a Monetary Policy Shock ........................................................................................ 4

3.2. The New Keynesian Model ............................................................................................................................ 6

3.3. Overview of the Model ................................................................................................................................... 7

3.4. Final Goods Firm ........................................................................................................................................... 8

3.5. Intermediate Goods Firms .............................................................................................................................. 8

3.6. Households ................................................................................................................................................... 11

3.7. The Wage Decision ...................................................................................................................................... 16

3.8. Monetary and Fiscal Policy .......................................................................................................................... 18

3.9. Market Clearing and Equilibrium ................................................................................................................. 18

4. The Search and Matching Model ................................................................................................................. 18

4.1. Workers ........................................................................................................................................................ 22

4.2. Firms ............................................................................................................................................................ 23

4.3. Wage determination ..................................................................................................................................... 23

5. Augmenting the CEE Model with the Search and Matching Model ............................................................ 24

5.1. The Discount Factor of Firms....................................................................................................................... 24

5.2. Firms in the DMP Framework ...................................................................................................................... 25

5.3. Wage Bargaining .......................................................................................................................................... 27

5.4. The Labor Market ......................................................................................................................................... 27

5.4.1. Intensive versus Extensive Margin ...................................................................................................... 28

5.4.2. Intermediate Goods Firms and Labor Input ......................................................................................... 28

5.5. Resource Constraint ..................................................................................................................................... 29

6. Model Simulation ......................................................................................................................................... 30

6.1. Parameter Values used for Calibration ......................................................................................................... 31

6.2. Monetary and Fiscal Policy in the NKSM Model ........................................................................................ 32

6.3. Impulse Response Functions to a Monetary Policy Shock ........................................................................... 34

6.4. Impact of Various Parameter Values on the Models Performance ............................................................... 40

6.5. Impulse Response Functions to a Technology Shock .................................................................................. 42

6.6. Further Research proposals .......................................................................................................................... 47

7. Conclusion .................................................................................................................................................... 48

A. Appendix ...................................................................................................................................................... 50

A.1. Real Marginal Cost of a Cobb-Douglas Production Technology ................................................................. 50

A.2. Log-Linearization ......................................................................................................................................... 52

A.3. The Log-Linearized System of the CEE Model ........................................................................................... 54

A.4. The Log-Linearized System of the DMP Model .......................................................................................... 60

A.5. Dynare and MATLAB Code ........................................................................................................................ 68

B. List of Figures .............................................................................................................................................. 81

C. References .................................................................................................................................................... 82

3

1. Abstract

I develop and simulate a medium sized New Keynesian DSGE model that incorporates a variant

of the Diamond Mortensen Pissarides Search and Matching model of the labor market.

Conventional New Keynesian models struggle to account for involuntary unemployment. In

contrast, the model presented here is able to capture the reaction of unemployment to a

monetary policy shock. The framework also accounts for the observed inertia and persistence

in several aggregate quantities. More work is required to improve the response of inflation in

the model.

2. Introduction

The primary motivation for this thesis is twofold. Firstly, in conventional New Keynesian

frameworks, nominal wage rigidity is the key feature to replicate the empirically observed

inertial, persistent and hump-shaped response of inflation and aggregate variables to a monetary

policy shock. I want to ascertain if staggered wage contracts are still an important friction that

is essential for the augmented model’s performance.

Secondly, fluctuations in involuntary unemployment are an integral part of the business cycle

and an unpleasant fact of everyday life. However, many macroeconomic models struggle to

account for this component. As a result, this thesis extends the now conventional New

Keynesian model developed by Christiano et al. (2005) to a more realistic framework that

incorporates involuntary equilibrium unemployment and delivers predictions for labor market

flows.

Chapter 3 and 4 describe the two models in detail. Chapter 5 explains the way the frameworks

are linked together. The only significant modification to the Christiano et al. (2005) model is

the different treatment of the labor market, which integrates the DMP model. This thesis

discusses the issues and considerations that arise in New Keynesian modelling in general, and

specifically in the combination of the two frameworks. The model presented here seeks to

combine the most plausible considerations of various papers to reach a credible solution.

Chapter 6 simulates the augmented model with respect to an expansionary monetary policy

shock, as well as a positive technology shock. 1 For this purpose, the model is calibrated using

parameter values from the existing literature. Specifically, the parameterizations provided by

Christiano et al. (2013) as well as Gertler et al. (2008) are utilized. Furthermore, the importance

of several parameters and their implications for the performance of the model are explained.

Before proceeding to the conclusion in chapter 7, a short discussion about potential future

research is provided. The appendix includes the derivations for all the important equations as

well as the respective log-linearizations. The working paper of Christiano et al. (2001) contains

any aspect of the New Keynesian model that is not described in this thesis. Moreover, the

appendix includes the complete Dynare (Adjemian, et al., 2011) and MATLAB codes needed

to replicate the simulations and the corresponding graphs used throughout this thesis.

1 Note that Christiano et al. (2005) do not discuss a technology shock.

4

3. The Christiano Eichenbaum Evans Model

This chapter explains the model and summarizes the key parts and findings of the paper written

by Christiano et al. (2005). The authors, CEE henceforth, develop and simulate a New

Keynesian model that is used to examine the combination of real and nominal rigidities that

help to replicate the empirically observed inertia and persistence in real variables in response

to a monetary policy shock

3.1. Empirical Estimation of a Monetary Policy Shock

Prior to building a model one needs to determine how macroeconomic variables actually

respond in reality. CEE describe monetary policy as

𝑅𝑡 = 𝑓(𝛀𝑡) + 𝜖𝑡, 3.1-1

where 𝑅𝑡 is the federal funds rate, 𝑓 is a linear function of the time 𝑡 information set 𝛀𝑡 and 𝜖𝑡 is the monetary policy shock. The Federal Reserve Bank is assumed to allow money growth to

be whatever is required to ensure that equation 3.1-1 holds. The maintained assumption for

identification states that 𝜖𝑡 is orthogonal to the entries in 𝛀𝑡.

The authors use an identified nine-variable vector autoregressive (VAR) model for estimating

the impulse response functions of eight major macroeconomic variables. The VAR has the

following structure:

𝒀𝑡 =𝑌1𝑡𝑅𝑡𝑌2𝑡

, 𝒀1𝑡 =

[ 𝑅𝑒𝑎𝑙 𝐺𝐷𝑃

𝑅𝑒𝑎𝑙 𝐶𝑜𝑛𝑠𝑢𝑚𝑝𝑡𝑖𝑜𝑛

𝐺𝐷𝑃 𝐷𝑒𝑓𝑙𝑎𝑡𝑜𝑟

𝑅𝑒𝑎𝑙 𝐼𝑛𝑣𝑒𝑠𝑡𝑚𝑒𝑛𝑡

𝑅𝑒𝑎𝑙 𝑊𝑎𝑔𝑒

𝐿𝑎𝑏𝑜𝑟 𝑃𝑟𝑜𝑑𝑢𝑐𝑡𝑖𝑣𝑖𝑡𝑦]

, 𝒀2𝑡 = [𝑅𝑒𝑎𝑙 𝑃𝑟𝑜𝑓𝑖𝑡𝑠

𝐺𝑟𝑜𝑤𝑡ℎ 𝑅𝑎𝑡𝑒 𝑜𝑓 𝑀2] 3.1-2

The ordering of the variables entails two key identification assumptions. Firstly, the vector 𝒀1𝑡 consists of those variables that are assumed to respond slowly to a monetary policy shock.

Therefore, they are contained in the time 𝑡 information set. Secondly, 𝒀2𝑡 contains variables

that are allowed to respond contemporaneously with a monetary policy shock and are thus not

contained in 𝛀𝑡. For this reason, only past values of 𝒀2𝑡 are included in the time 𝑡 information

set.

The choice of variables in each vector is consistent with the timing assumptions made in the

model described below. All variables, except money growth, have been transformed using the

natural logarithm but were kept in levels. Since several variables are growing over time, this

could theoretically affect the estimation results. However, CEE argue that alternative

specifications, that account for potential cointegration relationships, have been tested and that

the results are unaffected.

5

The sample period in the paper spans from the third quarter 1965 to the third quarter 1995.2

Ignoring the constant term, the VAR(4) model, as estimated by CEE, has the following form

𝒀𝑡 = 𝑨1𝒀𝑡−1 +⋯+ 𝑨4𝒀𝑡−4 + 𝑪𝜼𝑡 . 3.1-3

The vector 𝜼𝑡 is a nine dimensional zero-mean, serially uncorrelated shock with a diagonal

variance-covariance matrix. 𝑪 is a 9x9 lower triangular matrix with diagonal terms equal to

unity. The seventh element of the vector 𝜼𝑡 is the monetary policy shock denoted by 𝜖𝑡. This

results from the fact that there are six variables in 𝒀1𝑡.

Note that a contractionary monetary policy shock corresponds to a positive shock to 𝜖𝑡. The

dynamic behavior of 𝒀𝑡, after a one standard deviation shock to 𝜖𝑡, is computed by ordinary

last squares. The resulting path gives the coefficients in the impulse response functions that

CEE are interested in. The authors argue that the ordering of the variables within 𝒀𝑖𝑡 does not

alter the results.

Figure 3.1-1, taken from CEE, shows the impulse response functions of all variables

in 𝒀𝑡 following an expansionary one-standard-deviation shock in monetary policy. Lines

marked with plus signs correspond to the VAR based point estimates. Grey areas are the 95

percent confidence intervals from the VAR.3 Solid lines are the DGE model’s impulse

responses. The asterisk specifies the period in which the policy shock occurs.

Units on the horizontal axes are quarters, whereas units on the vertical axes denote percentage

deviations from the unshocked path, except for inflation, the interest rate as well as the growth

rate of money which are denoted in annualized percentage point deviations (APR) from their

unshocked path.

Based on the VAR results, CEE point out several interesting responses to an expansionary

monetary policy shock.

Output, consumption as well as investment respond in a hump-shaped manner, reaching

their peak after around one and a half years. All three variables return to pre-shock levels

roughly three years later.

Inflation also responds in a sluggish way, while reaching its peak after about two years.

The interest rate decreases for about a year.

Real profits, real wages and labor productivity rise.

The growth rate of money increases instantaneously.

2 The sample period is identical to Christiano et al. (1999). 3 Confidence intervals are calculated by the method described in Sims and Zha (1999).

6

Figure 3.1-1 Model and VAR based Impulse Responses (CEE 2005)

Table 3.1-1 Percentage Variance due to Monetary Policy Shocks (CEE 2005)

The authors remark that their estimation strategy focuses solely on the share caused by a

monetary policy shock. Table 3.1-1 seeks to explain how large that factor is in relation to the

aggregate variation in the data. With the exemption of inflation and the real wage, monetary

policy shocks appear to explain a nontrivial fraction of the variation in the variables. However,

the sizeable confidence intervals reveal that these point estimates should be interpreted with

caution. Moreover, unlike the impulse response functions discussed above, variance

decompositions are generally not insensitive to alternative specifications. This thesis abstracts

from issues that arise from potential misspecifications.

3.2. The New Keynesian Model

CEE estimate a dynamic general equilibrium model (DGE) with a mixture of five different real

and nominal rigidities. Calvo-style nominal price and wage contracts are implemented as

nominal rigidities, whereas habit formation in the utility function, convex investment

adjustment costs, variable capital utilization as well as working capital loans are considered as

The variance decompositions show how

much of the k-step ahead forecast error

variance of each of the variables in 𝒀𝑡 can be explained by the exogenous

monetary policy shock, for 𝑘 = 4, 8

and 20 quarters.

The boundaries of the associated 95%

confidence intervals are shown in

parenthesis and are calculated from the

estimated VAR via bootstrapping.

7

real rigidities. The upcoming sections explain the model economy as developed by CEE.4 Some

additional comments not provided by CEE are added whenever it facilitates the understanding

of the model.

3.3. Overview of the Model

Before explaining the parts of the model in detail, it helps to provide a crude overview of the

core elements. To facilitate the understanding of the basic structure of the model, Figure 3.3-1

sketches out how the various agents are interconnected. The following sections systematically

formulate the problems firms and households face in detail.

A representative, perfectly competitive firm produces a final consumption good that consists of

a continuum of intermediate goods, which in turn are produced by monopolists that employ

homogenous labor and capital services rented in perfectly competitive factor markets. At the

end of each period, profits generated by intermediate goods firms are distributed to a continuum

of households, who face several decisions during each period. They choose how much to

consume, how many units of capital services they accumulate and supply, how to divide their

financial assets into deposits, cash holdings, and so forth.

Figure 3.3-1 The Model Economy

4 To provide a more comprehensive picture, the description of the model combines parts from the published paper

as well as the working paper (Christiano et al., 2001).

8

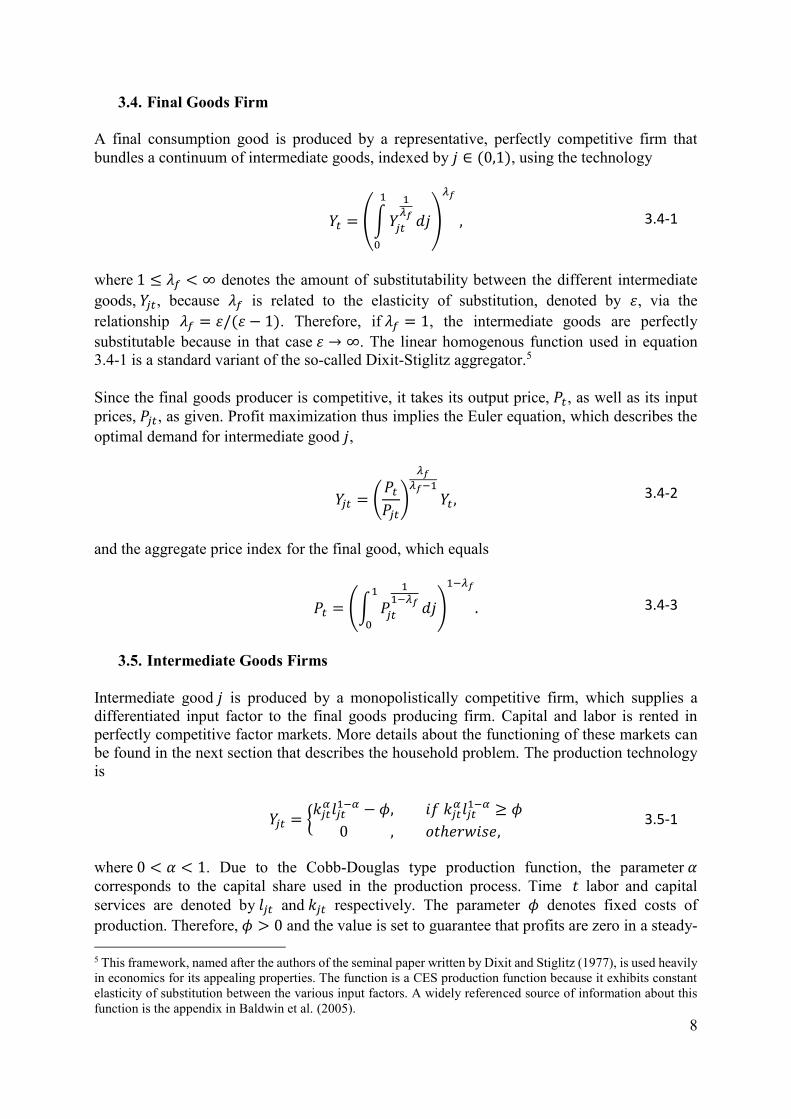

3.4. Final Goods Firm

A final consumption good is produced by a representative, perfectly competitive firm that

bundles a continuum of intermediate goods, indexed by 𝑗 ∈ (0,1), using the technology

𝑌𝑡 = (∫𝑌𝑗𝑡

1𝜆𝑓

1

0

𝑑𝑗)

𝜆𝑓

, 3.4-1

where 1 ≤ 𝜆𝑓 < ∞ denotes the amount of substitutability between the different intermediate

goods, 𝑌𝑗𝑡, because 𝜆𝑓 is related to the elasticity of substitution, denoted by 휀, via the

relationship 𝜆𝑓 = 휀/(휀 − 1). Therefore, if 𝜆𝑓 = 1, the intermediate goods are perfectly

substitutable because in that case 휀 → ∞. The linear homogenous function used in equation

3.4-1 is a standard variant of the so-called Dixit-Stiglitz aggregator.5

Since the final goods producer is competitive, it takes its output price, 𝑃𝑡, as well as its input

prices, 𝑃𝑗𝑡, as given. Profit maximization thus implies the Euler equation, which describes the

optimal demand for intermediate good 𝑗,

𝑌𝑗𝑡 = (𝑃𝑡𝑃𝑗𝑡)

𝜆𝑓𝜆𝑓−1

𝑌𝑡 , 3.4-2

and the aggregate price index for the final good, which equals

𝑃𝑡 = (∫ 𝑃𝑗𝑡

11−𝜆𝑓

1

0

𝑑𝑗)

1−𝜆𝑓

. 3.4-3

3.5. Intermediate Goods Firms

Intermediate good 𝑗 is produced by a monopolistically competitive firm, which supplies a

differentiated input factor to the final goods producing firm. Capital and labor is rented in

perfectly competitive factor markets. More details about the functioning of these markets can

be found in the next section that describes the household problem. The production technology

is

𝑌𝑗𝑡 = {

𝑘𝑗𝑡𝛼 𝑙𝑗𝑡

1−𝛼 − 𝜙, 𝑖𝑓 𝑘𝑗𝑡𝛼 𝑙𝑗𝑡

1−𝛼 ≥ 𝜙

0 , 𝑜𝑡ℎ𝑒𝑟𝑤𝑖𝑠𝑒, 3.5-1

where 0 < 𝛼 < 1. Due to the Cobb-Douglas type production function, the parameter 𝛼

corresponds to the capital share used in the production process. Time 𝑡 labor and capital

services are denoted by 𝑙𝑗𝑡 and 𝑘𝑗𝑡 respectively. The parameter 𝜙 denotes fixed costs of

production. Therefore, 𝜙 > 0 and the value is set to guarantee that profits are zero in a steady-

5 This framework, named after the authors of the seminal paper written by Dixit and Stiglitz (1977), is used heavily

in economics for its appealing properties. The function is a CES production function because it exhibits constant

elasticity of substitution between the various input factors. A widely referenced source of information about this

function is the appendix in Baldwin et al. (2005).

9

state. Profits are distributed to households at the end of each period. Naturally, production only

takes place whenever fixed costs are covered, as represented by 𝑘𝑗𝑡𝛼 𝑙𝑗𝑡

1−𝛼 ≥ 𝜙.

Entry and exit is ruled out to keep the analysis technically feasible. Since profits are stochastic

and zero on average, they must be negative at times. If firms were allowed to exit, companies

must also be able to enter, otherwise the economy would end up with no firms, and thus no

production. However, once the model allows for entry, the firms cannot remain monopolists

because the apparent profit opportunities would result in firms wanting to enter the market and

exploit the profitable intermediate goods sectors. Consequently, monopoly power would vanish

and a more complicated analysis that endogenously determines entry and exit dynamics would

be necessary.

The nominal wage, 𝑊𝑡, does not have a firm specific subscript because it is chosen to be the

same across households that can reoptimize.6 Moreover, the nominal wage bill, 𝑊𝑡𝑙𝑗𝑡, must be

paid at the beginning of each period. As a result, the firms must borrow from financial

intermediaries. Repayment, denoted by 𝑊𝑡𝑙𝑗𝑡𝑅𝑡, occurs at the end of each period, where 𝑅𝑡

denotes the gross interest rate. The authors refer to this setup as working capital loans. They are

important because these loans generate a reduction in the firms’ marginal cost whenever the

interest rate drops due to an expansionary monetary policy. This in turn leads to a decline in

inflation.

Let 𝑅𝑡𝑘 be the nominal rental rate on capital. Therefore, total period 𝑡 costs for an intermediate

goods firm are 𝑆𝑡(𝑌𝑡, 𝑅𝑡𝑘,𝑊𝑡𝑅𝑡) = 𝑅𝑡

𝑘𝑘 +𝑊𝑡𝑙𝑗𝑡𝑅𝑡. Given Cobb-Douglas technology, cost

minimization implies that real marginal costs have the form

𝑠𝑡 = (

1

1 − α)1−𝛼

(1

𝛼)𝛼

(𝑟𝑡𝑘)

𝛼(𝑤𝑡𝑅𝑡)

1−𝛼, 3.5-2

where 𝑟𝑡𝑘 = 𝑅𝑡

𝑘/𝑃𝑡 and 𝑤𝑡 = 𝑊𝑡/𝑃𝑡 denote the real rental rate on capital services and the real

wage rate. As usual, capital letters correspond to nominal variables, whereas lower case letters

correspond to the respective real terms. The firms’ profits, putting aside fixed costs, are given

by the relation [𝑃𝑗𝑡/𝑃𝑡 − 𝑠𝑡 ]𝑃𝑡𝑌𝑗𝑡, where 𝑃𝑗𝑡 denotes firm 𝑗’s price.

Price-setting is assumed to follow a variation of the mechanism suggested in Calvo (1983). The

Calvo model of staggered price adjustment is probably the most popular price-setting

framework in modern macroeconomics. Only a constant, exogenously determined fraction of

firms is allowed to reoptimize its nominal price. Thus, reoptimization is independent across

firms and time and each firm faces a constant probability, 1 − 𝜉𝑝, of being able to optimize

prices. CEE assume that firms that can reoptimize its price do this before the realization of the

time 𝑡 growth rate of money.

The evident shortcoming of this theory is that firms cannot influence the timing of price

adjustments. Nonetheless, empirical evidence suggests that prices are not fully flexible. A more

realistic framework results in an inflation equation that becomes complex and hard to solve

analytically. For this reason, the Calvo model is a convenient way of generating empirically

plausible results within an operational framework. Moreover, CEE explain that one objection

to the Calvo style staggered price setting is that the standard formulation implies that inflation

6 Note that this is not an assumption but a result of the model setup as shown for example in Woodford (1996).

10

leads output, which is empirically counterfactual, as highlighted by Fuhrer and Moore (1995).

However, Gali and Gertler (2000) point out that this criticism does not apply to frameworks in

which 𝑠𝑡 represents real marginal costs rather than the output gap. Therefore, according to CEE,

this criticism of the Calvo pricing scheme does not apply to their model.

CEE interpret the Calvo price setting as capturing various costs of changing prices, such as

costs that arise from collecting data, from negotiating and communicating new prices or from

decision making itself. However, they do not allow for so-called menu cost interpretations

because they would apply to all price changes, including the ones associated with the simple

lagged inflation indexation scheme explained above. The authors reference microeconomic

evidence provided by Zbaracki et al. (2000) that suggests that expenses associated with

reoptimization are significantly more important than menu costs.

Firms that cannot reoptimize prices engage in lagged inflation indexation:

𝑃𝑗𝑡 = 𝜋𝑡−1𝑃𝑡−1 3.5-3

In other words, these firms change prices to match the past inflation rate. Therefore, the current

inflation rate is characterized by 𝜋𝑡 = 𝑃𝑡+1/𝑃𝑡. Lagged inflation indexation implies that

inflation itself becomes sticky. Given a proper choice of parameters, the model is able to

account for the empirically observed degree of serial correlation in inflation. Moreover, let ��𝑡 denote the value of 𝑃𝑗𝑡 chosen by firms that can reoptimize prices at time 𝑡. Just as in the case

of wages mentioned above, the nominal reoptimized price does not have a firm specific

subscript because it is identical across firms. The firm chooses ��𝑡 to maximize

Ε𝑡−1∑(𝛽𝜉𝑝)

𝑙𝑣𝑡+𝑙(��𝑡𝑋𝑡𝑙 − 𝑠𝑡+𝑙𝑃𝑡+𝑙)𝑌𝑗,𝑡+𝑙,

∞

𝑙=0

3.5-4

with 𝑣𝑡 being the marginal value of a dollar to the household, which is due to the assumption

of state contingent securities identical across households. Naturally, 𝑣𝑡 is outside the firms’

control and thus taken as exogenous. The lagged expectations operator, Ε𝑡−1, is conditional on

lagged growth rates of money, denoted by 𝜇𝑡−𝑙, with 𝑙 ≥ 1. This specification is used because

of the assumption that firms set ��𝑡 prior to the time 𝑡 growth rate of money.

The optimization problem maximizes 3.5-4, subject to 3.5-2 and 3.4-2 as well as

𝑋𝑡𝑙 = {

𝜋𝑡 × 𝜋𝑡+1 ×⋯𝜋𝑡+𝑙+1 𝑓𝑜𝑟 𝑙 ≥ 11 𝑓𝑜𝑟 𝑙 = 0

. 3.5-5

The reoptimized price ��𝑡 changes firm 𝑗’s profit only as long as it cannot optimize prices itself,

in which case 𝑃𝑗,𝑡+𝑙 = ��𝑡𝑋𝑡𝑙. The probability that a firm is forced to engage in lagged inflation

indexation is denoted by (𝜉𝑝 )𝑙.

The first order condition of the optimization problem reads

Ε𝑡−1∑(𝛽𝜉𝑝)

𝑙𝑣𝑡+𝑙𝑌𝑗,𝑡+𝑙(��𝑡𝑋𝑡𝑙 − 𝜆𝑓𝑠𝑡+𝑙𝑃𝑡+𝑙)

∞

𝑙=0

= 0. 3.5-6

11

In the absence of Calvo style staggered price setting, all firms can optimize prices and 𝜉𝑝 = 0.

Consequently, 3.5-6 reduces to the standard condition that firms set prices as a constant markup,

denoted by 𝜆𝑓, over marginal costs. As already shown in Calvo (1983), equation 3.4-3 can be

rewritten as

𝑃𝑡 = [(1 − 𝜉𝑝)��𝑡

11−𝜆𝑓 + 𝜉𝑝(𝜋𝑡−1𝑃𝑡−1)

11−𝜆𝑓]

1−𝜆𝑓

. 3.5-7

Log-linearization of equation 3.5-7 in real terms and slightly rearranging yields7

��𝑡 =

𝜉𝑝

1 − 𝜉𝑝(��𝑡 − ��𝑡−1). 3.5-8

Given these definitions, log-linearization of equation 3.5-6 results in

��𝑡 = Ε𝑡−1 [��𝑡 +∑(𝛽𝜉𝑝)

𝑙[(��𝑡+𝑙 − ��𝑡−𝑙−1) + (��𝑡+𝑙 − ��𝑡+𝑙−1)]

∞

𝑙=1

], 3.5-9

Equation 3.5-9 together with 3.5-8 can be combined to the inflation Phillips Curve8

��𝑡 =

1

1 + 𝛽��𝑡−1 +

𝛽

1 + 𝛽𝐸𝑡−1��𝑡+1 +

(1 − 𝛽𝜉𝑝)(1 − 𝜉𝑝)

𝜉𝑝𝐸𝑡−1��𝑡. 3.5-10

As outlined in section 3.1, one of the key identification assumptions of the VAR model is that

the price level does not respond contemporaneously with a monetary policy shock and is thus

not contained in time 𝑡 information set Ω𝑡. Under this Phillips curve specification, the time 𝑡 inflation rate does not respond to a time 𝑡 monetary policy shock either.

3.6. Households

A continuum of households face a number of decisions during each period. Unlike CEE, this

thesis uses 𝑖 ∈ (0,1) instead of 𝑗 ∈ (0,1) to avoid confusion.9 Each household decides upon

consumption versus capital accumulation and how many units of capital services to supply.

Furthermore, it acquires state contingent securities, which are conditional on whether it can

reoptimize its wage decision. These securities guarantee that households are homogenous with

respect to consumption and asset holdings. However, they are heterogeneous with respect to

the wage rate and the hours they work, as is reflected in the notation, an issue already mentioned

in section 3.5.

Households that can reoptimize wages set them according to a Calvo framework that is similar

to the one used for price setting. Households are also assumed to receive a lump sum transfer

7 Section A.2 of the appendix explains the method of log-linearization and the notation. The following derivation

is already provided here to facilitate a coherent characterization of the intermediate goods sector problem. 8 Named after the economist Alban W. Phillips, who was the first to observe and describe the short run inverse

relationship between unemployment and inflation. 9 This is done because the subscript 𝑗 already denotes firms.

12

from the monetary authority. Furthermore, they decide upon the amount of financial assets they

hold in the form of deposits with a financial intermediary or in the form of cash.

The utility function for the 𝑖𝑡ℎ household has the form10

𝛦𝑡−1𝑖 ∑𝛽𝑙 [𝑙𝑜𝑔(𝑐𝑡+𝑙 − 𝑏𝑐𝑡+𝑙−1) − 𝜓0(𝑛𝑖,𝑡+𝑙)

2+ 𝜓𝑞

𝑞𝑡+𝑙1−𝜎𝑞

1 − 𝜎𝑞]

∞

𝑙=0

, 3.6-1

where 𝑐𝑡 denotes time 𝑡 real consumption and 𝑛𝑖,𝑡 symbolizes time 𝑡 hours worked, which CEE

denote as ℎ𝑖𝑡. Since this quantity denotes labor as measured in the data, the standard notation

for employment used in the literature, 𝑛𝑡, seems more functionally adequate than ℎ𝑡.11 The

functional form implies a standard disutility of work term with 𝜓0 set to ensure a steady-state

value of labor equal to unity, thus full employment. Furthermore, 𝑞𝑡 = 𝑄𝑡/𝑃𝑡 denotes real cash

balances and 𝑄𝑡 represents nominal cash balances.12

The value for parameter 𝜓𝑞 is set to guarantee that 𝑄/𝑀 = 0.44 in steady-state, which is the

ratio of the money aggregates M1 over M2 at the beginning of the data set. 𝑀 denotes the

steady-state stock of money in the model. According to CEE, different values of 𝜓𝑞 only change

the estimate of the elasticity of money demand, 𝜎𝑝. The lagged expectation operator has the

same purpose as described in section 3.5.

The parameter 𝑏 introduces non-separability of preferences over time. In other words, an

increase in time 𝑡 consumption lowers marginal utility of current consumption and increases

marginal utility of next period’s consumption. Intuitively, old habits are hard to break and new

habits are difficult to form. This feature is called habit formation in the literature and is

essentially a statement about the behavioural pattern of individuals.

Figure 3.6-1 Habit Formation in the Utility Function

10 The representation of the utility function is different from CEE because the authors describe the functional form

of the terms separately. This thesis combines the equations to facilitate notation. 11 The Search and Matching model discussed in chapter 4 also uses 𝑛𝑖𝑡. 12 Including money in the utility function (MIU) is a frequently used framework in macroeconomics that was

initially developed by Sidrauski (1967). This setup models the opportunity costs of holding money with respect to

foregone interest payments. Therefore, the MIU term encourages households to optimize money holdings.

13

Figure 3.6-1 shows how consumption evolves over time in response to a positive monetary

policy shock. Habit formation is important for replicating the observed hump-shaped rise in

consumption. Standard utility functions conventionally used in economic models cannot

generate this pattern.

The households’ budget constraint in nominal terms has the form

𝑀𝑡+1 = 𝑅𝑡[𝑀𝑡 − 𝑄𝑡 + (𝜇𝑡 − 1)𝑀𝑡𝛼] + 𝐴𝑖,𝑡 + 𝑄𝑡 +𝑊𝑖,𝑡𝑛𝑖,𝑡 + 𝑅𝑡

𝑘𝑢𝑡��𝑡+ 𝐷𝑡 − 𝑃𝑡[𝑖𝑡 + 𝑐𝑡 + 𝑎(𝑢𝑡)��𝑡].

3.6-2

The period 𝑡 + 1 money stock of households, denoted by 𝑀𝑡+1, has to equal the sum of the

expressions on the right-hand side. Deposits held at financial intermediaries are defined as

[𝑀𝑡 − 𝑄𝑡 + (𝜇𝑡 − 1)𝑀𝑡𝛼]. These deposits earn the gross nominal interest rate 𝑅𝑡. Moreover,

𝐴𝑖,𝑡 denotes net cash flows from state contingent securities, and 𝑄𝑡 stands for nominal cash

balances. Labor income is given by 𝑊𝑖,𝑡𝑛𝑖,𝑡, whereas earnings from supplying capital services

are denoted by 𝑅𝑡𝑘𝑢𝑡��𝑡. Firm profits are represented by 𝐷𝑡, and nominal consumption is

specified as 𝑃𝑡𝑐𝑡. Lastly, 𝑃𝑡[𝑖𝑡 + 𝑎(𝑢𝑡)��𝑡] denotes the stock of installed capital, which is owned

by households and evolves according to

��𝑡+1 = (1 − 𝛿)��𝑡 + [1 − 𝜙𝑖 (

𝑖𝑡𝑖𝑡−1

− 1)2

] 𝑖𝑡. 3.6-3

In other words, next period’s physical capital stock equals the sum of current period’s capital

stock adjusted for capital depreciation, denoted by 𝛿, and current and past investment that is

transformed via a technology that adds to next period’s installed capital. CEE only discuss the

properties of this function without stating the exact functional form, as can be seen in equation

3.6-15. Thanks to my supervisor Dr. Güntner, I was able to write down an operational function

that fulfils the properties stated in CEE.

Moreover, the physical capital stock, ��𝑡, is associated with capital services via the

relationship 𝑘𝑡 = 𝑢𝑡��𝑡, with 𝑢𝑡 symbolizing the utilization rate of capital, which is effectively

a control variable of the households. Finally, (𝜇𝑡 − 1)𝑀𝑡𝛼 is a lump sum payment that the

monetary authority is assumed to pay to households. The variable 𝜇𝑡 denotes the gross growth

rate of the economy-wide per capita stock of money, 𝑀𝑡𝛼.

The budget constraint in real terms can be expressed as

𝜋𝑡+1𝑚𝑡+1 = 𝑅𝑡(𝑚𝑡 − 𝑞𝑡) +

(𝜇𝑡 − 1)𝑀𝑡𝛼

𝑃𝑡+ 𝑎𝑖𝑡 + 𝑞𝑡+𝑤𝑖𝑡𝑛𝑖𝑡 + 𝑟𝑡

𝑘𝑢𝑡��𝑡

+ 𝑑𝑡 − 𝑖𝑡 − 𝑐𝑡 + 𝑎(𝑢𝑡)��𝑡,

3.6-4

where 𝜋𝑡 = 𝑃𝑡/𝑃𝑡−1 denotes the gross inflation rate of the general price level.

Household 𝑖 is assumed to

max 𝑐𝑡, 𝑞𝑡, 𝑚𝑡+1, 𝑢𝑡, 𝑖𝑡, ��𝑡+1

utility function 3.6-1

subject to 3.6-4 3.6-5

14

Therefore, the Lagrangean has the form

ℒ = 𝛦𝑡−1

𝑖 ∑𝛽𝑙−𝑡∞

𝑙=0

{[𝑙𝑜𝑔(𝑐𝑡+𝑙 − 𝑏𝑐𝑡+𝑙−1) − 𝜓0(𝑛𝑖,𝑡+𝑙)2+ 𝜓𝑞

𝑞𝑡+𝑙1−𝜎𝑞

1 − 𝜎𝑞]

+ 𝜓𝑐,𝑡+𝑙 [𝑅𝑡+𝑙(𝑚𝑡+𝑙 − 𝑞𝑡+𝑙) +(𝜇𝑡+𝑙 − 1)𝑀𝑡+𝑙

𝛼

𝑃𝑡+𝑙+ 𝑎𝑖𝑡+𝑙+𝑞𝑡+𝑙 + 𝑤𝑖𝑡+𝑙𝑛𝑖𝑡+𝑙 + 𝑟𝑡+𝑙

𝑘 𝑢𝑡+𝑙��𝑡+𝑙 + 𝑑𝑡+𝑙 − 𝑖𝑡+𝑙

− 𝑐𝑡+𝑙 + 𝑎(𝑢𝑡+𝑙)��𝑡+𝑙 − 𝜋𝑡+𝑙+1𝑚𝑡+𝑙+1]},

3.6-6

where 𝜓𝑐,𝑡 = 𝑣𝑡𝑃𝑡 and 𝑣𝑡 denotes the marginal value of a dollar to the household, which is due

to the assumption of state contingent securities identical across households. As a result, the

Lagrange multiplier 𝜓𝑐,𝑡 denotes the marginal utility of 𝑃𝑡 units of currency.

The corresponding FOCs are given by:

𝜕ℒ

𝜕𝑐𝑡:

1

𝑐𝑡 − 𝑏𝑐𝑡−1−

𝛽𝑏

𝑐𝑡+1 − 𝑏𝑐𝑡− 𝜓𝑐,𝑡 = 0. 3.6-7

In CEEs timing convention, the equation has the form

Ε𝑡−1𝑢𝑐,𝑡 = Ε𝑡−1𝜓𝑐,𝑡, 3.6-8

where 𝑢𝑐,𝑡 denotes the marginal utility of consumption at time 𝑡. Moreover, 𝜓𝑐,𝑡 corresponds

to the value of a dollar in the current period.

Equation 3.6-9 describes the household’s FOC for nominal cash balances,

𝜕ℒ

𝜕𝑞𝑡: 𝜓𝑞𝑞𝑡

−𝛿𝑞 − 𝜓𝑐,𝑡(𝑅𝑡 − 1) = 0, 3.6-9

which holds irrespective of the realization of the contemporary money growth rate because the

cash balance decision is carried out afterwards. Hence, the marginal utility of dollar assigned

to cash balances must correspond to the marginal utility of a dollar allocated to the financial

intermediary.

𝜕ℒ

𝜕𝑚𝑡+1: Ε𝑡𝛽𝜓𝑐,𝑡+1𝑅𝑡+1 − Ε𝑡𝜓𝑐,𝑡𝜋𝑡+1 = 0. 3.6-10

Rewriting this equation results in

Ε𝑡𝛽𝜓𝑐,𝑡+1

𝑅𝑡+1𝜋𝑡+1

= Ε𝑡𝜓𝑐,𝑡,

which shows that the expected present discounted value of the cash acquired by depositing a

dollar in next period’s financial market matches the value of a dollar in the current period.

15

𝜕ℒ

𝜕𝑢𝑡: Ε𝑡−1𝜓𝑐,𝑡[𝑟𝑡

𝑘 − 𝑎′(𝑢𝑡) ] = 0. 3.6-11

Equation 3.6-11 is the Euler equation that characterizes the household’s capital utilization

decision. Accordingly, the expected marginal cost of raising the capital utilization rate must

equal the corresponding marginal benefit.

A few further remarks are necessary to determine the FOC with respect to time 𝑡 investment as

well as time 𝑡 + 1 physical capital. As already remarked in section 3.3, intermediate goods

firms employ homogenous labor and capital services rented in perfectly competitive factor

markets. The following considerations are based on lecture notes from the PHD course

“Advanced Economics” of my supervisor Dr. Güntner.

Assume that intra-temporal investment is implemented by a competitive capital goods producer

that purchases (1 − 𝛿)𝑘𝑡 at the market price, 𝑃𝑘′𝑡, obtains 𝑖𝑡 investment goods, and sells 𝑘𝑡+1

at the same market price, taking equation 3.6-3 into consideration. Since firms are also owned

by households, the same discount factor can be used and the competitive capital goods producer

maximizes

Ε𝑡−1∑𝛽𝑙

∞

𝑙=0

[𝑃𝑘′,𝑡+𝑙𝑘𝑡+𝑙+1 − 𝑃𝑘′,𝑡+𝑙(1 − 𝛿)𝑘𝑡+𝑙 − 𝑖𝑡+𝑠]

= Ε𝑡−1∑𝛽𝑙∞

𝑙=0

[𝑃𝑘′,𝑡+𝑙 (1 − 𝜙𝑖 (𝑖𝑡+𝑙𝑖𝑡+𝑙−1

− 1)2

) 𝑖𝑡 − 𝑖𝑡+𝑙].

3.6-12

Consequently, the FOC with respect to time 𝑡 investment is

𝜕ℒ

𝜕𝑖𝑡: 𝜓𝑐,𝑡 {1 + 𝜙𝑖𝑃𝑘′𝑡 [(

𝑖𝑡𝑖𝑡−1

)2

−𝑖𝑡𝑖𝑡−1

] + 𝑃𝑘′𝑡𝜙𝑖

2(𝑖𝑡𝑖𝑡−1

− 1)2

}

− 𝛽Ε𝑡−1𝑃𝑘′,𝑡+1𝜓𝑐,𝑡+1𝜙𝑖 [(𝑖𝑡+1𝑖𝑡

)3

− (𝑖𝑡+1𝑖𝑡

)2

] − 𝜓𝑐,𝑡𝑃𝑘′𝑡 = 0.

3.6-13

CEE do not explicitly state the functional form 𝐹(𝑖𝑡, 𝑖𝑡−1) that describes how the capital stock

evolves, but rather use the expression provided in equation 3.6-15. Therefore, the FOC in their

paper has the shortened, yet equivalent form

Ε𝑡−1𝜓𝑐,𝑡 = Ε𝑡−1[𝜓𝑐,𝑡𝑃𝑘′𝑡𝐹1,𝑡 + 𝛽𝜓𝑐,𝑡+1𝑃𝑘′𝑡+1𝐹2,𝑡+1], 3.6-14

where 𝐹𝑗,𝑡 is the partial derivative of 𝐹(𝑖𝑡, 𝑖𝑡−1) with 𝑗 = 1,2. This function characterizes how

current and past investment can be converted into installed capital in the following period and

is specified by

𝐹(𝑖𝑡, 𝑖𝑡−1) = [1 − 𝑆 (𝑖𝑡

𝑖𝑡−1)] 𝑖𝑡. 3.6-15

CEE only restrict the function to the following properties: 𝑆(1) = 𝑆′(1) = 0 and the

investment adjustment cost parameter 𝜂𝑘 ≡ 𝑆′′(1) > 0. The right-hand side of equation 3.6-14

states that 𝐹1,𝑡 additional units of next period’s physical capital stock ��𝑡+1 can be produced with

16

an extra unit of the investment goods, whose value is denoted by 𝑃𝑘′𝑡𝐹1,𝑡Ε𝑡−1𝜓𝑐,𝑡. Moreover,

increasing period 𝑡 investment affects next period’s quantity of installed capital by 𝐹2,𝑡+1. The

respective discounted value is given by 𝛽𝜓𝑐,𝑡+1𝑃𝑘′𝑡+1𝐹2,𝑡+1. Note that the price of investment

goods in terms of consumption is equal to unity. Hence, equation 3.6-14 states that the marginal

cost of one unit of investment corresponds to the sum of these values.

Likewise, for the FOC with respect to time 𝑡 + 1 physical capital, the household is assumed to

purchase 𝑘𝑡 in period 𝑡 − 1 at the competitive market price 𝑃𝑘′,𝑡−1. In period 𝑡, the household

rents out the capital stock at the real capital rental rate, 𝑟𝑡𝑘, and sells the depreciated capital

stock at the end of the period at the current market price 𝑃𝑘′𝑡. As a result, the respective terms

in the budget constraint read

Ε𝑡−1∑𝛽𝑙

∞

𝑙=0

𝜓𝑐,𝑡+𝑙[𝑟𝑡+𝑙𝑘 𝑢𝑡+𝑙��𝑡+𝑙 + 𝑃𝑘′,𝑡+𝑙(1 − 𝛿)��𝑡+𝑙

− 𝑃𝑘′,𝑡+𝑙−1𝑎(𝑢𝑡+𝑙)��𝑡+𝑙],

3.6-16

and hence the Euler equation for next period’s physical capital stock ��𝑡+1 has the form

𝜕ℒ

𝜕��𝑡+1: 𝛽Ε𝑡−1𝜓𝑐,𝑡+1[𝑢𝑡+1𝑟𝑡+1

𝑘 + 𝑃𝑘′,𝑡+1(1 − 𝛿) − 𝑃𝑘′,𝑡𝑎(𝑢𝑡+1)]

− Ε𝑡−1𝜓𝑐,𝑡𝑃𝑘′,𝑡 = 0. 3.6-17

To obtain the expression found in CEE, equation 3.6-17 needs to be divided by 𝑃𝑘′,𝑡. Note that

there is a typo in the equation provided in the working paper of the authors,

because 𝑃𝑘′,𝑡𝑎(𝑢𝑡+1) misses 𝑃𝑘′,𝑡. As will be shown in the appendix, this typo is irrelevant in

the log-linearization of the equation, since the term cancels out either way.

3.7. The Wage Decision

Based on Erceg et al. (2000), CEE adopt a wage setting decision that takes place between

households and a representative, competitive firm that converts labor into an aggregate labor

input, 𝑙𝑡, which is used in the intermediate goods sector, as described in section 3.5.

The following technology converts labor into the aggregated labor input

𝑙𝑡 = (∫𝑛𝑖𝑡

1𝜆𝑤

1

0

𝑑𝑖)

𝜆𝑤

, 3.7-1

where 𝑛𝑖𝑡 denotes a differentiated labor service that is supplied by household 𝑖. The CES

production function is technically identical to the one used in the final goods production, as

described in section 3.4. Therefore, the optimal demand for labor supplied by household 𝑖 equals

𝑛𝑖𝑡 = (𝑊𝑡

𝑊𝑖𝑡)

𝜆𝑤𝜆𝑤−1

𝑙𝑡, 3.7-2

17

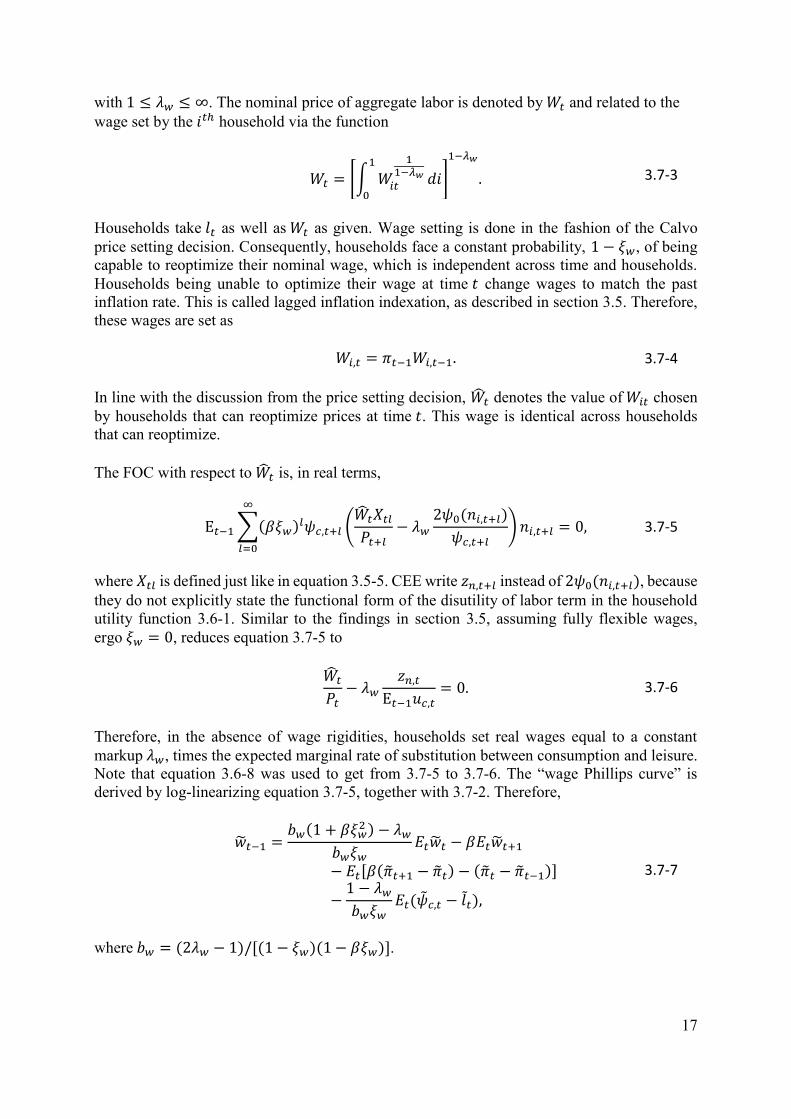

with 1 ≤ 𝜆𝑤 ≤ ∞. The nominal price of aggregate labor is denoted by 𝑊𝑡 and related to the

wage set by the 𝑖𝑡ℎ household via the function

𝑊𝑡 = [∫ 𝑊

𝑖𝑡

11−𝜆𝑤

1

0

𝑑𝑖]

1−𝜆𝑤

. 3.7-3

Households take 𝑙𝑡 as well as 𝑊𝑡 as given. Wage setting is done in the fashion of the Calvo

price setting decision. Consequently, households face a constant probability, 1 − 𝜉𝑤, of being

capable to reoptimize their nominal wage, which is independent across time and households.

Households being unable to optimize their wage at time 𝑡 change wages to match the past

inflation rate. This is called lagged inflation indexation, as described in section 3.5. Therefore,

these wages are set as

𝑊𝑖,𝑡 = 𝜋𝑡−1𝑊𝑖,𝑡−1. 3.7-4

In line with the discussion from the price setting decision, ��𝑡 denotes the value of 𝑊𝑖𝑡 chosen

by households that can reoptimize prices at time 𝑡. This wage is identical across households

that can reoptimize.

The FOC with respect to ��𝑡 is, in real terms,

Ε𝑡−1∑(𝛽𝜉𝑤)

𝑙𝜓𝑐,𝑡+𝑙 (��𝑡𝑋𝑡𝑙𝑃𝑡+𝑙

− 𝜆𝑤2𝜓0(𝑛𝑖,𝑡+𝑙)

𝜓𝑐,𝑡+𝑙)𝑛𝑖,𝑡+𝑙 = 0,

∞

𝑙=0

3.7-5

where 𝑋𝑡𝑙 is defined just like in equation 3.5-5. CEE write 𝑧𝑛,𝑡+𝑙 instead of 2𝜓0(𝑛𝑖,𝑡+𝑙), because

they do not explicitly state the functional form of the disutility of labor term in the household

utility function 3.6-1. Similar to the findings in section 3.5, assuming fully flexible wages,

ergo 𝜉𝑤 = 0, reduces equation 3.7-5 to

��𝑡

𝑃𝑡− 𝜆𝑤

𝑧𝑛,𝑡Ε𝑡−1𝑢𝑐,𝑡

= 0. 3.7-6

Therefore, in the absence of wage rigidities, households set real wages equal to a constant

markup 𝜆𝑤, times the expected marginal rate of substitution between consumption and leisure.

Note that equation 3.6-8 was used to get from 3.7-5 to 3.7-6. The “wage Phillips curve” is

derived by log-linearizing equation 3.7-5, together with 3.7-2. Therefore,

��𝑡−1 =

𝑏𝑤(1 + 𝛽𝜉𝑤2 ) − 𝜆𝑤

𝑏𝑤𝜉𝑤𝐸𝑡��𝑡 − 𝛽𝐸𝑡��𝑡+1

− 𝐸𝑡[𝛽(��𝑡+1 − ��𝑡) − (��𝑡 − ��𝑡−1)]

−1 − 𝜆𝑤𝑏𝑤𝜉𝑤

𝐸𝑡(��𝑐,𝑡 − 𝑙𝑡),

3.7-7

where 𝑏𝑤 = (2𝜆𝑤 − 1)/[(1 − 𝜉𝑤)(1 − 𝛽𝜉𝑤)].

18

3.8. Monetary and Fiscal Policy

Unlike the standard monetary policy representation used in CEE, this thesis uses a Taylor rule

of the form

𝑅𝑡𝑅= (

𝑅𝑡−1𝑅

)𝜌𝑟

[(Ε𝑡𝜋𝑡+1𝜋

)𝜌𝜋

(𝑌𝑡𝑌)𝜌𝑌

]

1−𝜌𝑟

𝑒𝜖𝑡 , 3.8-1

where 0 ≤ 𝜌𝑟 ≤ 1 determines the central bank’s pursuit to smooth interest rates over time.13 A

value different from zero reflects interest rate inertia in the Taylor rule. Moreover, 𝜌𝜋 gauges

the central bank’s reaction to deviations of inflation from gross steady-state inflation, which is

defined by 𝜋 = 𝑃/𝑃 = 1. The parameter 𝜌𝑌 regulates the central bank’s response to deviations

of output of the final goods from steady-state output. The mean zero, identically and

independently distributed (i.i.d) random error term 휀𝑡 accounts for the monetary policy shock

described in equation 3.1-1. Please refer to section 6.2 for more details about the Taylor rule.

The government is assumed to impose non distortionary lump sum taxes. Furthermore, it

follows a Ricardian fiscal policy. Consequently, fiscal policy need not be specified and inflation

is unaffected by government actions, as CEE explain.

3.9. Market Clearing and Equilibrium

According to the authors, financial intermediaries obtain 𝑀𝑡 − 𝑄𝑡 from households and a

transfer (𝜇𝑡 − 1)𝑀𝑡 from the monetary authority. In equilibrium, 𝑀𝑡 = 𝑀𝑡𝑎, where 𝑀𝑡

𝑎 defines

the economy-wide per capita stock of money. Likewise, the variable 𝜇𝑡 denotes the gross

growth rate of 𝑀𝑡𝛼. Therefore, the total amount of money that financial intermediaries receive

is 𝜇𝑡𝑀𝑡 −𝑄𝑡.

Loan market clearing implies

𝜇𝑡𝑀𝑡 − 𝑄𝑡 = 𝑊𝑡𝑙𝑡, 3.9-1

where 𝑊𝑡𝑙𝑡 denotes the nominal wage bill, which intermediate goods producers must pay at the

beginning of each period. Consequently, these firms must borrow from financial intermediaries.

Finally, the aggregate resource constraint reads

𝑐𝑡 + 𝑖𝑡 + 𝑎(𝑢𝑡) ≤ 𝑌𝑡 . 3.9-2

4. The Search and Matching Model

As mentioned in the introduction, the frictional equilibrium unemployment model presented

here is based on papers written by Diamond (1982) as well as Mortensen and Pissarides (1994).

The underlying idea is that firms and workers are simultaneously searching for matching

counterparts in the labor market. Therefore, the literature generally refers to the model as the

Diamond-Mortensen-Pissarides Search and Matching model of unemployment (the DMP

13 Christiano et al. (2005) use this specification in their robustness tests.

19

model, hereafter). This chapter develops a standard DMP model. Any considerations regarding

the integration of the DMP model into the CEE framework are left for chapter 5.

The model seeks to explain the existence of involuntary unemployment via frictional search

unemployment. In other words, there are workers that are willing to work at the current wage

but cannot find jobs. Search efforts by workers and firms are coordinated via a so-called

matching function that determines flows from unemployment to employment. On the other

hand, current matches are destroyed with an exogenous separation probability that can be

interpreted as firing or turnover dynamics which generate flows from employment to

unemployment.

The core assumptions of the basic model are as follows:

‒ Workers and firms are heterogeneous with respect to their skills, skill requirements as

well as their location.

‒ Workers and firms are risk neutral and all have imperfect information regarding their

potential counterparts.

‒ Constant returns to scale (CRS) in production and the matching function: no need to

distinguish between firms and jobs.

‒ Free entry of firms ensures that the value of posting a vacancy is zero in equilibrium.

‒ Search is costly but each match generates a surplus that is shared between workers and

firms via generalized Nash bargaining.

‒ Workers always participate in the job market and their reservation wage is lower than

the productivity of any offered job. Thus, workers always accept the offer.

To find new workers and to hire 𝑛𝑗𝑡 employees, each firm post vacancies, denoted by 𝑣𝑗𝑡. The

total number of vacancies is calculated as 𝑣𝑡 = ∫ 𝑣𝑗𝑡𝑑𝑗1

0 and the total number of employed

workers is 𝑛𝑡 = ∫ 𝑛𝑗𝑡𝑑𝑗1

0 respectively.14 It is assumed that all unemployed workers search for a

job. Moreover, the total work force is normalized to unity. Therefore, the pool of unemployed

workers coincides with the unemployment rate, which is calculated as the difference between

unity and employment.

𝑢𝑡 = 1 − 𝑛𝑡 . 4-1

Two different timing assumptions are used in the literature. Firstly, newly employed workers

have to wait until next period before they start working. This setup is in line with the baseline

DMP model and for example used by Krause and Lubik (2007). Secondly, newly hired workers

are expected to meet with firms, to bargain and to start to work immediately in the same period.

This framework is for instance used by Gertler et al. (2008) as well as Christiano et al. (2013).

As mentioned in section 3.1, CEE’s sample period for their VAR estimations is 1965Q3-

1995Q3. The U.S. labor market has a median duration of unemployment of roughly 7 weeks in

the model’s time period (Fred Database, 2015). Christiano et al. (2013) reason that using

quarterly data is comparatively long with respect to the US unemployment duration. Therefore,

the authors argue that it seems more plausible to use their employed timing assumption.

14 This setup is identical to Krause and Lubik (2007). Moreover, equation 5.5-1 uses the same definition.

20

Figure 4-1 Dice-DFH Mean Vacancy Duration Measure

On the other hand, not all workers apply for jobs and bargain only at the beginning of each

period. It seems more realistic that potential employees and firms continuously try to find

suitable matches. This in turn implies that the workforce would also fluctuate intra-temporally.

Moreover, using more up-to-date data reveals that employers are recently waiting longer to fill

vacant positions. According to the Fred database, the median duration of unemployment is

slightly above twelve weeks since the turn of the millennium.

Furthermore, the Dice-DFH Vacancy Duration Measure, as developed by Davis et al. (2010),

quantifies the average number of working days taken to fill vacant job positions. As can be seen

in Figure 4-1, the index ranges approximately between 15 and 26 working days over the last 14

years (Dice Holding, 2015). Consequently, this thesis assumes that newly hired workers have

to wait until next period before they begin working. As a result, it is assumed that newly hired

workers remain in the work force for at least one period, which is in line with Christiano et al.

(2013) as well as Gertler et al. (2008).15

The matching function 𝑚𝑡, which determines the number of newly hired workers, is given by

𝑚𝑡 = 𝛾𝑢𝑡𝜉𝑣𝑡1−𝜉

, 4-2

with 0 < 𝜉 < 1.16 This Cobb-Douglas type function describes the result of the matching process

which depends on the constant efficiency parameter 𝛾, the time 𝑡 unemployment rate 𝑢𝑡, as well

as the available job vacancy rate 𝑣𝑡, which is computed as the quantity of unfilled jobs

expressed as a proportion of the labor force. Furthermore, the matching function’s diminishing

marginal return implies a congestion externality because each worker searching for a job

decreases the likelihood of others finding a job.

15 Other authors like Krause and Lubik (2007) assume that new employees are immediately subject to job

separation. 16 The name matching function originates from newly hired workers being termed matches.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Jan

-01

Au

g-0

1

Mar

-02

Oct

-02

May

-03

Dec

-03

Jul-

04

Feb

-05

Sep

-05

Ap

r-0

6

No

v-0

6

Jun

-07

Jan

-08

Au

g-0

8

Mar

-09

Oct

-09

May

-10

Dec

-10

Jul-

11

Feb

-12

Sep

-12

Ap

r-1

3

No

v-1

3

Jun

-14

Jan

-15

Wo

rkin

g D

ays

Source: Dice Hiring Indicators

Dice-DFH Mean Vacancy Duration Measure

21

Labor market tightness 𝜃, from the worker’s perspective, is defined as vacancies over

unemployment

𝜃𝑡 ≡𝑣𝑡𝑢𝑡. 4-3

The job filling rate of firms is denoted by17

𝑞𝑡 = 𝑞(𝜃𝑡) =𝑚𝑡

𝑣𝑡. 4-4

Using the matching function this can be shown to be decreasing in labor market tightness

𝑞(𝜃𝑡) = 𝑚𝜃𝑡−𝜉 , 4-5

with – 𝜉 being the elasticity of the job filling rate with respect to the labor market tightness,

defined as 𝜕𝑞𝑡

𝜕𝜃𝑡

𝜃𝑡

𝑞𝑡.

On the other hand, the job finding rate of workers is increasing in labor market tightness

𝑓𝑡 = 𝜃𝑡𝑞(𝜃𝑡) =𝑚𝑡

𝑢𝑡= 𝑚𝜃𝑡

1−𝜉 . 4-6

Both the job finding and the job filling rate depend on aggregate variables and are thus taken

as given by individual firms and workers and can be interpreted as probabilities.

The law of motion for employment is described by the function

𝑛𝑡 = (1 − 𝜌)𝑛𝑡−1 + 𝑥𝑡−1𝑛𝑡−1, 4-7

where 𝑛𝑡 denotes employment and 𝜌 the exogenous job separation rate. The presumed stability

of job separations is based on findings by Hall (2005) and Shimer (2005), who argue that the

job separation rate is relatively acyclical, or weakly countercyclical. Hall explains that it is a

common, yet erroneous belief that the sharp rise of unemployment during recessions were the

consequence of increased job separation rates. In fact, unemployment increases mainly because

of reduced hiring rates during downturns and changes in the job separation rate are miniscule

relative to the observed movements in employment.

Moreover, Shimer (2005) deduces that a time varying job separation cannot be important

because it would imply a positively sloped Beveridge curve, which plots the relationship

between the unemployment and the vacancy rate.18 The latter is typically depicted on the

vertical axes. Empirically, the Beveridge curve is negatively sloped, which suggests that high

unemployment rates are generally accompanied by a low vacancy rate, and vice versa.

As a result of the stable job separation rate, fluctuations in unemployment are due to cyclical

variation in hiring in this model. Moreover, workers who lose their job are not allowed to search

17 The job filling rate is also called the job matching rate in the literature. 18 The curve is named after the economist William H. Beveridge.

22

for a new occupation until the next period. The hiring rate is defined as the ratio of new hires

to the existing workforce

𝑥𝑖𝑡 =𝑞𝑡𝑣𝑖𝑡 𝑛𝑖𝑡

. 4-8

Given this setup, the hiring rate is effectively a firm’s control variable since the likelihood that

each posted vacancy will be filled is known to be the job filling rate 𝑞𝑡. Note that the firm’s

problem is equivalent to choosing how many vacancies to post, since one implies the other.

Moreover, using the definition of the hiring rate together with the job matching rate, equation

4-7 can be rewritten as

𝑛𝑡 = (1 − 𝜌)𝑛𝑡−1 +𝑚𝑡−1. 4-9 4.1. Workers

The worker’s choices depend on the value of employment in period 𝑡 which equals19

𝐻𝑡 = 𝑤𝑡 + Ε𝑡𝛽[(1 − 𝜌)𝐻𝑡+1 + 𝜌𝐼𝑡+1]. 4.1-1

The real wage, denoted by 𝑤𝑡, is the result of the Nash Bargaining process described below.

The term in parenthesis describes the expected discounted value of being employed or

unemployed in period 𝑡 + 1, weighted by the relevant probabilities.

The value of being unemployed is given by20

𝐼𝑡 = 𝑜 + Ε𝑡𝛽[𝑓𝑡𝐻𝑡+1 + (1 − 𝑓𝑡)𝐼𝑡+1], 4.1-2

with 𝜊 being the worker’s outside option which can be interpreted as an umbrella term for all

sorts of different non-market activities and options considered in the literature.21 Since the

outside option is constant in this thesis, no exact interpretation is provided. Otherwise, all

possible explanations would always have to exactly offset each other. As explained in section

3.8, the government is assumed to impose non distortionary lump-sum taxes. Insofar, fiscal

policy need not be specified, as CEE explain.

Section 6.4 explains the importance of the outside option for the model’s performance. A more

detailed discussion of the labor market in general can be found in section 5.4. As before, the

expression in parenthesis of equation 4.1-2 describes the expected discounted value of being

employed or unemployed in period 𝑡 + 1. This time, weighted by the job finding rate and its

complement, respectively.

19 The capital letter 𝐻 was chosen because 𝑁 already denotes employment and 𝐿 denotes the aggregate labor input

as used in the intermediate goods production process. Therefore, the value of employment is denoted as 𝐻 to avoid

confusion. It helps to think of 𝐻 as standing for “hired”, thus denoting the value of being hired. 20 The capital letter 𝐼 was used because 𝑈 already denotes unemployment. 𝐼 can be interpreted as idleness. 21 For instance, the outside option can be understood as the disutility of working (Lubik, 2009), the value of home

production (Walsh & Ravenna, 2007), the value of being unemployed (Christiano et al., 2013) or the value of

leisure (Shimer, 2005).

23

4.2. Firms

Firms can post vacancies (or job openings, positions) at a constant cost 𝜅 per period and

vacancy. The value of a vacancy is therefore given by

𝑃𝑡 = −𝜅 + Ε𝑡𝛽[𝑞(𝜃𝑡)𝐽𝑡+1 + (1 − 𝑞(𝜃𝑡))𝑃𝑡+1], 4.2-1

with the weight 𝑞(𝜃𝑡) being the aforementioned job matching rate, or the probability of filling

a job. The value of job 𝐽 is described via the relationship

𝐽𝑡 = 𝐴𝑡 − 𝑤𝑡 + Ε𝑡𝛽[(1 − 𝜌)𝐽𝑡+1 + 𝜌𝑃𝑡+1], 4.2-2

where 𝐴𝑡 is the productivity of firms. Constant returns to scale in the production function as

well as the matching function imply that this relationship can also be interpreted as the value of

a firm. The value of next period’s job 𝐽𝑡+1 is weighted by the probability of still having a job in

that period, denoted by 1 − 𝜌. Likewise, the value of posting a vacancy in period 𝑡 + 1 is

weighted by the probability of being laid-off (the job separation rate). This accounts for the fact

that unemployed people increase the value of a vacancy for firms.

Free entry of firms ensures that, in equilibrium, no producer can generate excess returns. Hence,

the value of posting a vacancy must be zero (𝑃𝑡 = 0) and 4.2-1 can be rewritten as

𝜅

𝑞(𝜃𝑡)= Ε𝑡𝛽𝐽𝑡+1, 4.2-3

where 1/𝑞(𝜃𝑡) = 𝑣𝑡/𝑚𝑡 can be interpreted as the expected duration of a posted vacancy.

Combining this with 4.2-2, again using 𝑃𝑡 = 0, yields the job creation condition

𝜅

𝑞(𝜃𝑡)= Ε𝑡𝛽 [𝐴𝑡+1 − 𝑤𝑡+1 + (1 − 𝜌)

𝜅

𝑞(𝜃𝑡+1)]. 4.2-4

The equality in 4.2-4 states that 𝜅/𝑞(𝜃𝑡) , the expected cost of posting a vacancy, equals the

expected benefit from a filled vacancy. Further considerations are left unexplained in this

section. Refer to section 5.2 for a complete treatment of the firms in the DMP model within the

CEE framework.

4.3. Wage determination

The equilibrium real wage 𝑤𝑡 is the outcome of an axiomatic Nash Bargaining process that

maximizes the generalized Nash product denoted by

max𝑤𝑡

(𝐽𝑡 − 𝑃𝑡)1−𝜂(𝐻𝑡 − 𝐼𝑡)

𝜂 , 4.3-1

with 𝜂 being the workers bargaining power, or the share of the joint surplus that goes to the

workers.22 The final solution to this bargaining process is

𝑤𝑡 = 𝜂(𝐴𝑡 + 𝜅𝜃𝑡) + (1 − 𝜂)𝑜. 4.3-2

22 The solution method is named after the mathematician John Forbes Nash, Jr.

24

As a result, the real wage is the weighted average of productivity, labor market tightness and

the outside option of workers. Moreover, by the definition of the labor market tightness, the

more firms look for workers (the higher 𝑃𝑡, given 𝐼𝑡) or the fewer workers look for jobs (the

lower 𝐼𝑡, given 𝑃𝑡), the higher the wage the worker can get.

5. Augmenting the CEE Model with the Search and Matching Model

There are five points of contact that link the two models together. The first point is the redefined

discount factor of firms in the DMP model. The second point regards the way the firm problem

is formulated in the DMP model in order to introduce output, which is neglected in traditional

Search and Matching frameworks. This also slightly changes the wage bargaining process,

which is the third point of contact. The fourth point regards the DMP firms producing the

aggregate labor input that is used in the intermediate goods production process. The final point

of contact concerns the resource constraint.

The augmented model is known as the New Keynesian Search and Matching model in the

literature, or NKSM model for short. This chapter discusses the issues and considerations that

arise in New Keynesian modelling in general, and specifically in the combination of the two

models. Overall, several related, yet competing frameworks exist and more research is needed

to determine the preferable model. The model presented here seeks to combine the most

plausible considerations of various papers to reach a credible solution.

The first papers incorporating DMP frameworks into DSGE models date back to Merz (1995)

and Andolfatto (1996). However, both papers used Real Business cycle models instead of New

Keynesian DSGE models. Seminal papers that combine contemporary New Keynesian models

with Search and Matching frameworks are Walsh (2003), Krause and Lubik (2007), Gertler et

al. (2008) and Christoffel et al. (2009). Furthermore, Christiano et al. (2013) build a model that

uses a setup of the labor market that is close to the one considered in this thesis.

Contrary to CEE, Gertler et al. (2008) assume that final goods producers are monopolistically

competitive, whereas intermediate goods producers (wholesalers in Gertler et al.) are assumed

to be competitive. This circumvents bargaining spillovers amid employees, which is needed

because Gertler et al. (2008) incorporate the labor market directly into the intermediate goods

producers’ problem. More details can be found in the authors’ paper. Due to the separated labor

market in CEE, there is no need to worry about bargaining spillovers in this framework, despite

monopoly power of intermediate goods producers.

The question of which of the two variants is more realistic remains unanswered in this thesis,

which attempts to change as little as possible from the CEE model. As a result, it assumes that

the labor market is separated from the intermediate goods sector.

5.1. The Discount Factor of Firms

The first point of contact arises via a redefined discount factor of the firms operating in the

DMP model, which is now given by

Ε𝑡𝛽 (

𝑈𝑐,𝑡+1𝑈𝑐,𝑡

) = Ε𝑡𝛽 (𝜓𝑐,𝑡+1

𝜓𝑐,𝑡), 5.1-1

25

where 𝑈𝑐,𝑡 denotes the marginal utility of consumption from the CEE model. This construction

of a stochastic pricing Kernel is consistent with other general equilibrium models that account

for labor market variables.23

The original DMP framework does not model production because the main interest lies in

employment dynamics. In this thesis, companies operating in the DMP part of the model

economy bundle the workforce to a homogenous aggregate labor input using the following

production function24

𝑙𝑗𝑡 = 𝐴𝑡𝑛𝑗𝑡 . 5.1-2

Therefore, technology is linear in labor input and driven by an aggregate labor augmenting

technology shock that is identical to all firms. This shock follows the stationary law of motion

𝐴𝑡 = 𝐴𝑡−1𝜌

𝐴1−𝜌eϵt , 5.1-3

with 𝜖𝑡 ∼ 𝑁(0, 𝜎𝜖2) and 𝜌 < 1 being the degree of autocorrelation. A more detailed discussion

of technology shocks can be found in section 6.5.

Given the linear production function, firms are indifferent to the quantity of labor hired at a

given wage rate. Due to the separation of the labor market and the intermediate goods producers

in the CEE model, there is only a small change to the Nash bargaining setup used in the standard

DMP model, which is due to a modification in the marginal product of a worker.

5.2. Firms in the DMP Framework

Recall from section 3.5 that intermediate goods firms rent labor and capital in perfectly

competitive factor markets. Consequently, each labor market firm faces a perfectly elastic

demand curve and the market price for the aggregate labor input used in the intermediate goods

production process, denoted by 𝑃𝑡𝑤, is taken as given by individuals.

The equilibrium capacity of the labor output of a single labor market firm will be entirely

determined by the quantity of output the firm decides to supply. Therefore, equation 5.1-2

represents the output constraint, which can be written as

𝐴𝑡𝑛𝑗𝑡 ≥ 𝑙𝑗𝑡 , 5.2-1

where the left-hand side characterizes the potential maximum output of the homogenous

aggregate labor input, because 𝑛𝑗𝑡 corresponds to the labor force as measured in the data. As

usual, profits are calculated as revenues (𝑃𝑡𝑤/𝑃𝑡 )𝑙𝑗𝑡 minus costs, which consist of the real wage

bill 𝑤𝑗𝑡𝑛𝑗𝑡 and vacancy posting costs 𝑘𝑣𝑗𝑡.

23 Examples of papers that employ this setup are Christiano et al. (2013), Lubik (2009) or Gertler et al. (2008).

More details about the usefulness of a stochastic discount factor can be found in Hansen and Renault (2010). 24 Eventually, all 𝑗 subscripts can be erased due to the fact that constant returns to scale in the DMP firms

production and matching functions imply that there is no need to distinguish between firms. Recall that subscript 𝑗 is used to denote firms, whereas subscript 𝑖 characterizes households. Thus, 𝑛𝑗𝑡 = 𝑛𝑖𝑡 must hold in equilibrium.

26

As a result, the intertemporal profit maximization problem of labor market firms has the

following form:

max

𝑙𝑖𝑡, 𝑛𝑡, 𝑣𝑖𝑡𝐸0∑𝛽𝑡

𝜓𝑐,𝑡

𝜓𝑐,0

∞

𝑡=0

[(𝑃𝑡𝑤

𝑃𝑡) 𝑙𝑗𝑡 − 𝑤𝑗𝑡𝑛𝑗𝑡 − 𝑘𝑣𝑗𝑡]. 5.2-2

Consequently, the Lagrangean becomes

ℒ = 𝐸0∑𝛽𝑡

𝜓𝑐,𝑡

𝜓𝑐,0

∞

𝑡=0

[(𝑃𝑗𝑡𝑤

𝑃𝑡) 𝑙𝑗𝑡 − 𝑤𝑗𝑡𝑛𝑗𝑡 − 𝑘𝑣𝑗𝑡]

+ 𝐸0∑𝛽𝑡𝜓𝑐,𝑡

𝜓𝑐,0

∞

𝑡=0

𝑚𝑐𝑗𝑡𝑤[𝐴𝑡𝑛𝑗𝑡 − 𝑙𝑗𝑡]

+ 𝐸0∑𝛽𝑡𝜓𝑐,𝑡

𝜓𝑐,0

∞

𝑡=0

𝜇𝑗𝑡[(1 − 𝜌)𝑛𝑗𝑡−1 + 𝑞(𝜃𝑡−1)𝑣𝑗𝑡−1 − 𝑛𝑗𝑡],

5.2-3

where the Lagrange multiplier 𝜇𝑗𝑡 denotes the value of a job, as will be explained below. For

the second constraint, equation 4-4 was used to rewrite the employment accumulation equation,

denoted by equation 4-9. Note that marginal costs act as a Lagrange multiplier in this setup.25

This is feasible because the contribution of an additional unit of output to the firm’s revenue

equals marginal costs.

The FOCs have the following form:

𝜕ℒ

𝜕𝑙𝑖𝑡: 𝑃𝑗𝑡𝑤

𝑃𝑡= 𝑚𝑐𝑗𝑡

𝑤 5.2-4

𝜕ℒ

𝜕𝑛𝑖𝑡: 𝑤𝑡 = 𝑚𝑐𝑗𝑡

𝑤𝐴𝑡 − 𝜇𝑗𝑡 + (1 − 𝜌)𝐸𝑡𝛽𝜓𝑐,𝑡+1

𝜓𝑐,𝑡𝜇𝑗𝑡+1 5.2-5

𝜕ℒ

𝜕𝑣𝑖𝑡: 𝜅 = 𝐸𝑡𝛽

𝜓𝑐,𝑡+1

𝜓𝑐,𝑡𝜇𝑗𝑡+1𝑞(𝜃𝑡) 5.2-6

The third FOC can be rewritten as

𝜅

𝑞(𝜃𝑡)= 𝐸𝑡𝛽

𝜓𝑐,𝑡+1

𝜓𝑐,𝑡𝜇𝑗𝑡+1.

Moreover, following the discussion of footnote 24, all 𝑗 subscripts can be erased. Therefore,

∫ 𝜇𝑗𝑡𝑑𝑗 = 𝐽𝑡1

0, denotes, just like in the standard DMP model, the value of all firms.

25 The notation 𝑚𝑐𝑖𝑡

𝑤 was chosen to distinguish these marginal costs from the ones in the New Keynesian baseline

model.

27

Given this consideration, the third FOC can be rewritten as

𝜅

𝑞(𝜃𝑡)= 𝐸𝑡𝛽

𝜓𝑐,𝑡+1

𝜓𝑐,𝑡𝐽𝑡+1, 5.2-7

which equals equation 4.2-3, except for the marginal cost term and the stochastic discount

factor, which links the NK model to the DMP model, as described above.

The second FOC can be rewritten as

𝐽𝑡 = 𝑚𝑐𝑡

𝑤𝐴𝑡 − 𝑤𝑡 + (1 − 𝜌)𝐸𝑡𝛽𝜓𝑐,𝑡+1

𝜓𝑐,𝑡𝐽𝑡+1. 5.2-8

Apart from the aforementioned linkages between the models, this equation is identical to the

value of a job as described by equation 4.2-2.

The first FOC simply states that marginal costs equal marginal revenue, which due to perfect

competition equals the (real) price 𝑃𝑡𝑤/𝑃𝑡 that firms can charge for the labor input sold to

intermediate goods producers. As a result,

𝑝𝑡𝑤 = 𝑚𝑐𝑡

𝑤, 5.2-9

where 𝑚𝑐𝑡𝑤 is given by equation 5.2-8. Forwarding 5.2-8 by one period and inserting it into the

second FOC yields the following job creation condition which resembles equation 4.2-4:

𝜅

𝑞(𝜃𝑡)= 𝐸𝑡𝛽

𝜓𝑐,𝑡+1

𝜓𝑐,𝑡[𝑚𝑐𝑡+1

𝑤 𝐴𝑡+1 − 𝑤𝑡+1 + (1 − 𝜌)𝜅

𝑞(𝜃𝑡+1)]. 5.2-10

5.3. Wage Bargaining

Wage bargaining is done according to the standard Nash bargaining framework described in

section 4.3. There is only one difference to the canonical Search and Matching model, namely

that equation 5.2-8, includes the marginal cost term, which in turn influences the marginal

product of a worker. Therefore, the wage rate is determined by the following relation

𝑤𝑡 = 𝜂𝑚𝑐𝑡𝑤𝐴𝑡 + 𝜂𝜅𝜃𝑡 + (1 − 𝜂)𝑜. 5.3-1

All other considerations are identical to section 4.3. The derivation can be found in subsection

A.4.9 of the appendix.

5.4. The Labor Market

The fourth point of contact is in the perfectly competitive labor market where intermediate

goods firms rent labor just like in the CEE setup. Overall, the household problem in the

combined model is almost identical to the one discussed in the CEE model, except that

employment is no longer a choice variable. The following subsection discusses several

considerations that are worth noting.

28

5.4.1. Intensive versus Extensive Margin

In the CEE setup, the household utility function includes a disutility of labor term. As a result,

the model does not generate movements in unemployment but voluntary movements in hours

worked. This optimization process is a common approach in standard DSGE models and is

called adjustment on the intensive margin in the literature. However, Barro’s critique (1977)

states that deviations on the intensive margin take place in long lasting relationships between

workers and firms. In theory, such interactions provide many ways of undoing the effects of

staggered nominal wage contracting. Further discussions of this issue can be found in Christiano

et al. (2008) as well as Shimer (2008).

On the other extreme, employment adjusts solely with regard to the extensive margin. This can

be modelled via the standard DMP model, since households simply accept the outcome of the

bargaining and matching process. As a result, the utility function does not include disutility of

labor anymore. Other authors like Lubik (2009) allow for a mixture of the two extreme cases.

In Lubik’s variation, the hiring decision is still subject to rigidity due to the Search and

Matching framework. Yet, the decision on how many hours to supply is fully flexible. In this

setup, the utility function still contains a disutility of labor term. However, the resulting

optimization problem is only between the present workforce and the firm.

Allowing for both variations intuitively seems to be the most plausible structure. However,

Gertler et al. (2008) suggest that most of the cyclical variation in hours is on the extensive

margin and that the intensive margin seems to play an insignificant role over the business cycle.

Likewise, empirical studies found a low overall elasticity of labor supply with respect to the net

wage rate.26 Therefore, it seems reasonable to follow Gertler et al. (2008) by assuming that only

the extensive margin matters.

5.4.2. Intermediate Goods Firms and Labor Input

Just like in CEE, the nominal wage bill for firm 𝑗, this time denoted by 𝑃𝑗𝑡𝑤𝑙𝑗𝑡, has to be paid in

advance. Consequently, the firm must borrow the amount at the current interest rate. The loan

is repaid after the firms collect their sales revenues at the end of each period. Refer to section

3.5 for a detailed explanation of the advantage of this setup in the context of the standard CEE

model.

A monopolist manufactures the intermediate good 𝑗 according to a Cobb-Douglas production

function of the form

𝑌𝑗𝑡 = {

𝑘𝑗𝑡𝛼 𝑙𝑗𝑡

1−𝛼 − 𝜙, 𝑖𝑓 𝑘𝑗𝑡𝛼 𝑙𝑗𝑡

1−𝛼 ≥ 𝜙

0 , 𝑜𝑡ℎ𝑒𝑟𝑤𝑖𝑠𝑒. 5.4.2-1

26 Blundell (1992) provides an excellent survey of papers in that subfield of economics. In general, the empirical

studies found a low overall elasticity (total effect) of labor supply with respect to the net wage rate, which suggest

that the compensated wage elasticity (the substitution effect) and the income elasticity (income effect)

approximately offset each other.

29

However, this time 𝑙𝑗𝑡 denotes the time 𝑡 aggregate labor service purchased at the competitive

price from the DMP firms.27 The competitive price 𝑃𝑗𝑡𝑤 equals the marginal costs of the DMP

firms.

The aggregate amount of the homogeneous labor input, denoted by 𝑙𝑡, is calculated according

to

𝑙𝑡 = ∫ 𝑙𝑗𝑡𝑑𝑗

1

0

. 5.4.2-2

Note that this does not denote the total labor force as measured in the data. This problem is

identical to CEE. Refer to section 5.5 for more details. Furthermore, this relationship also

represents the market clearing condition for the DMP sector.

5.5. Resource Constraint

The fifth and final point is regarding the resource constraint that specifies the division of the

homogenous final goods in the economy. In addition to the standard resource constraint used

in CEE, vacancy posting costs need to be taken into account. These cannot already be

considered on the DMP labor market level because no consumption takes place in this stage of

production. Moreover, the Search and Matching framework now determines the aggregate

amount of the homogeneous labor input used in the intermediate goods production process. Just

like in CEE, total output needs to be related to total labor as measured in the data, calculated as

𝑛𝑡 = ∫ 𝑛𝑖𝑡𝑑𝑖.

1

0

5.5-1

Using this with equations 5.1-2 and 5.4.2-2 yields the modified resource constraint given by

𝑐 + 𝑖 + 𝑎(𝑢)�� + 𝜅𝑣 ≤ (𝑃∗

𝑃)

𝜆𝑓𝜆𝑓−1

𝑘𝛼(𝐴𝑛)1−𝛼. 5.5-2

The log-linearized resource constraint has the form

[1

𝛽− (1 − 𝛿)]

𝑠𝑘𝑠𝑐��𝑡 + ��𝑡 +

𝛿𝑠𝑘𝑠𝑐

𝑖𝑡 +𝑠𝜅𝑣𝑠𝑐

��𝑡 =𝛼

𝑠𝑐��𝑡 +

1 − 𝛼

𝑠𝑐(��𝑡 + ��𝑡), 5.5-3

where all variables are defined as in CEE and the additional term 𝑠𝜅𝑣 = 𝜅𝑣/𝑌. The exact steps

in the log-linearization of the resource constraint are provided in the appendix.

27 In this case, the parameter 𝛼 corresponds to the capital share used in the production process, whereas the

parameter 1 − 𝛼 is not the labor share, which partially depends on the outcome of the bargaining process described

in section 4.3.

30

6. Model Simulation

CEE distinguish between three groups of parameters in their paper. The first group of

parameters is calibrated in a way that guarantees plausible steady-state values for the affected

variables. The second group of parameters characterizes monetary policy, whereas the third

group is assessed by minimizing a measure of the gap between the model and the empirical

impulse response functions.28

Other authors like Christiano et al. (2013) use a Bayesian estimation strategy with a

considerable larger data set that covers the period 1951Q1 to 2008Q4. The authors estimate

various model specifications, including one that uses a Nash Bargaining search setup that is

similar to the one described in this thesis. Furthermore, Gertler et al. (2008) also use the same

quarterly series in combination with a Bayesian estimation strategy. Their sample period in the

paper goes from 1960Q1 to the 2005Q1. Among other setups, they also estimate a model that

uses a Nash Bargaining framework that is comparable to the one applied here.

Replicating any of the procedures described above goes beyond the scope of this thesis.

Therefore, the estimated parameter values from the aforementioned papers are used for

calibrating the model presented here. Needless to say, this approach is inferior to estimating the

parameters for this specific model. However, this task would significantly extend the workload.

Therefore, this tactic is used for the sake of brevity.

Five different models are simulated and compared in this chapter. Initially, the standard CEE

model, which serves as the benchmark model, is considered. Moreover, the benchmark model

with fully flexible wages is simulated as well. This is done to obtain impulse response functions

that highlight the importance of the staggered wage setting framework for the benchmark