Embed Size (px)

Citation preview

Understanding the Understanding the Real Property TaxReal Property Tax

and the Assessment and the Assessment ProcessProcess

February 2, 2010 – Town of February 2, 2010 – Town of KendallKendall

TONIGHT’S TOPICSTONIGHT’S TOPICS

-Overview of the Real Property Tax

-Local Equalization & the Job of the Assessor

-Reassessment & the Benefits of Equity

-Appeals Process

Property Tax in NYSProperty Tax in NYS Finances local Finances local

govt. and schoolsgovt. and schools

4250 taxing 4250 taxing jurisdictionsjurisdictions

Largest single revenue source

Schools 55%Towns 33%

WHERE THE REAL PROPERTY TAX GOESWHERE THE REAL PROPERTY TAX GOES

Total Outside NYC = $28.85 Billion

School Purposes$17.99 Billion

62.4%County Purposes$4.89 Billion

16.9%

Town Purposes$2.11 Billion

7.3%

Special District Purposes$1.87 Billion

6.5%

City Purposes$ .92 Billion

3.2%

Source: Based on data from the Office of the State Comptroller.

(Real Property Tax Levies by Purpose; Local Fiscal Years Ending in 2008)

Village Purposes$1.07 Billion

3.7%

Taxing JurisdictionsTaxing Jurisdictions

TownTown – Budget and Tax Levy set by – Budget and Tax Levy set by Town Board. Tax levy is distributed Town Board. Tax levy is distributed to all property inside the town to all property inside the town boundaryboundary

VillageVillage – Budget and Tax Levy set by – Budget and Tax Levy set by Village Board – Tax Levy distributed Village Board – Tax Levy distributed to all property inside the village to all property inside the village boundaryboundary

Taxing JurisdictionsTaxing Jurisdictions

CountyCounty – Budget and Tax Levy set by – Budget and Tax Levy set by County Legislature – Tax Levy County Legislature – Tax Levy distributed to all property inside the distributed to all property inside the county boundarycounty boundary

SchoolSchool – Budget and Tax Levy set by – Budget and Tax Levy set by School Board – Tax Levy Distributed School Board – Tax Levy Distributed to all property inside the school to all property inside the school district boundarydistrict boundary

Understanding the Understanding the Property TaxProperty Tax

The Real Property Tax is The Real Property Tax is anan

Ad ValoremAd Valorem taxtax

Understanding the Understanding the Property TaxProperty Tax

...the amount of tax paid ...the amount of tax paid depends on the value depends on the value

of real property owned of real property owned

Understanding the Understanding the Property TaxProperty Tax

Calculation of Property Taxes:Calculation of Property Taxes:Amount of Tax Levy (Budget Amount of Tax Levy (Budget

minus Revenues)minus Revenues)Divided by Taxable Assessed Divided by Taxable Assessed

Value (Assessed Value minus Value (Assessed Value minus Exemptions)Exemptions)

Equals Tax Rate (x 1000)Equals Tax Rate (x 1000)

Understanding the Understanding the Property TaxProperty Tax

Example: Example: Calculation of Property TaxesCalculation of Property Taxes Amount of Amount of Town Town Tax Levy Tax Levy

$540,000$540,000 Divided by TaxableDivided by Taxable

Assessed Value Assessed Value $120,000,000$120,000,000

Equals Tax Rate Equals Tax Rate $4.50 per $4.50 per $1000$1000

Understanding the Understanding the Property TaxProperty Tax

Sample Tax Bill: Sample Tax Bill:

Assessed Value of home Assessed Value of home $80,000$80,000Tax Rate Tax Rate $4.50 per $4.50 per

$1000$1000CalculationCalculation $80,000 * $4.50$80,000 * $4.50 = =

$360$360

10001000

Understanding the Understanding the Property TProperty Taxax

Although Although assessmentsassessments play an play an integral part of the tax integral part of the tax calculation, the amount of the calculation, the amount of the tax levytax levy is the controlling factor is the controlling factor in the amount of taxes we all payin the amount of taxes we all pay

Understanding the Understanding the Property TaxProperty Tax

Example: Example: Calculation of Property TaxesCalculation of Property TaxesAmount of Amount of Town Town Tax Levy Tax Levy $540,000$540,000Divided by TaxableDivided by Taxable

Assessed Value Assessed Value $60,000,000$60,000,000

Equals Tax Rate Equals Tax Rate $9.00 per $9.00 per $1000$1000

Understanding the Understanding the Property TaxProperty Tax

Sample Tax Bill: Sample Tax Bill:

Assessed Value of home Assessed Value of home $40,000$40,000Tax Rate Tax Rate $9.00 per $9.00 per

$1000$1000CalculationCalculation $40,000 * $9.00$40,000 * $9.00 = =

$360$360

10001000

Understanding the Understanding the Property TaxProperty Tax

Assessments affect the Assessments affect the distributiondistribution of the Real of the Real Property TaxProperty Tax

Assessors are charged by Assessors are charged by law with the duty of law with the duty of assessing real propertyassessing real property

The Job of the AssessorThe Job of the Assessor Provide fair assessments by determining the Provide fair assessments by determining the

market valuemarket value of each property of each property

Process Process exemptionsexemptions, such as STAR, Senior , such as STAR, Senior Citizens, and VeteransCitizens, and Veterans

Prepare and publish the assessment rollPrepare and publish the assessment roll

Help taxpayers understand assessmentsHelp taxpayers understand assessments

Defend assessments at administrative and Defend assessments at administrative and judicial appealsjudicial appeals

Duties of the AssessorDuties of the Assessor Process all transfers of property ownership Process all transfers of property ownership

(sales)(sales)• Change names, record sales informationChange names, record sales information

Collect and record all property informationCollect and record all property information• Review permits and demolition reportsReview permits and demolition reports• Measure and record all informationMeasure and record all information

Gather and analyze valuation dataGather and analyze valuation data• Verify sales and correct as neededVerify sales and correct as needed• Identify areas of similar market influence in townIdentify areas of similar market influence in town• Compile and apply valuation tables Compile and apply valuation tables

Duties of the AssessorDuties of the Assessor Prepare assessment rollPrepare assessment roll

• Enter all value changesEnter all value changes• Record all exemptionsRecord all exemptions• Determine Level of AssessmentDetermine Level of Assessment• Publish legal noticesPublish legal notices• Send Change of Assessment noticesSend Change of Assessment notices• Sit with assessment roll for 3 daysSit with assessment roll for 3 days

Defend assessmentsDefend assessments• Grievance DayGrievance Day• Small Claims Assessment ReviewSmall Claims Assessment Review

Manage officeManage office• Establish office hours Establish office hours • Attain certification and obtain mandatory training Attain certification and obtain mandatory training • Public relationsPublic relations

Additional Duties during Additional Duties during UpdateUpdate

Develop valuation tables and schedules Develop valuation tables and schedules Generate computer-assisted value for Generate computer-assisted value for

each propertyeach property Field review each valueField review each value Notify taxpayers of new assessmentsNotify taxpayers of new assessments Hold informal hearingsHold informal hearings Inform taxpayers of hearing resultsInform taxpayers of hearing results

ASSESSMENT ASSESSMENT CALENDARCALENDAR

July 1July 1st of the prior yearst of the prior year …..….....Valuation Date …..….....Valuation Date

March 1March 1stst ………....... Taxable Status Date ………....... Taxable Status Date Deadline for all exemption Deadline for all exemption

applicationsapplications

May 1May 1stst …...…. Tentative Assessment Roll …...…. Tentative Assessment Roll

4th Tues. in May................ Grievance Day4th Tues. in May................ Grievance Day

July 1July 1stst …………… Final Assessment Roll …………… Final Assessment Roll

TAX CYCLETAX CYCLE

Sept 1Sept 1st st …..…...........................School Tax…..…...........................School Tax

Jan 1Jan 1stst ………......... Town and County Tax ………......... Town and County Tax

June 1June 1stst .…...…....................... Village Tax .…...…....................... Village Tax

REAL PROPERTY TAX REAL PROPERTY TAX LAWLAW

§305 RPTL - Assessment Standard

All real property in each assessing unit shall be assessed at a uniform percentage of value.

EQUITY is the GOALEQUITY is the GOAL

All real property in each assessing unit shall be assessed at a uniform percentage of value

ValueValue is defined as is defined as "market value""market value" - the most - the most probable sale price, in a competitive and open probable sale price, in a competitive and open market, freely arrived at by normal negotiations market, freely arrived at by normal negotiations without undue pressure on either the buyer or the without undue pressure on either the buyer or the seller.seller.

tax bills must display the municipality's uniform tax bills must display the municipality's uniform percentage and the parcel's market valuepercentage and the parcel's market value

ASSESSMENT EQUITY ASSESSMENT EQUITY

Equity with respect to assessments and real property taxes means:

Properties are assessed at a uniform Properties are assessed at a uniform percentage of valuepercentage of value

Properties with similar values pay similar Properties with similar values pay similar taxestaxes

Taxpayers pay their fair shareTaxpayers pay their fair share

How Is Market Value How Is Market Value Determined?Determined?

The Assessor does NOT set market The Assessor does NOT set market valuevalue

Market Value is determined by Market Value is determined by analyzing valid real estate salesanalyzing valid real estate sales

Trends and values observed from Trends and values observed from the sales are applied to unsold the sales are applied to unsold propertiesproperties

What Drives Market Value?What Drives Market Value? Location, Location, LocationLocation, Location, Location

Some locations are more desirable Some locations are more desirable than others. To some lakefront and than others. To some lakefront and lake view property is highly desirablelake view property is highly desirable

Style, size, condition of homes affect Style, size, condition of homes affect valuevalue

What Drives Market Value?What Drives Market Value?

Economic influencesEconomic influences Interest ratesInterest rates Availability of amenities and jobsAvailability of amenities and jobs Commuting distance to employment Commuting distance to employment

centerscenters Farming opportunitiesFarming opportunities These among other factors may influence These among other factors may influence

property valuesproperty values

The real estate market has seen some The real estate market has seen some dramatic activity, not only in the number of dramatic activity, not only in the number of sales, but the price of real estate.sales, but the price of real estate.

One thing is certain, different types of One thing is certain, different types of properties in different locations will properties in different locations will increase in value at a different pace!increase in value at a different pace!

After a period of time without systematic After a period of time without systematic analysis of property values and analysis of property values and reassessmentreassessment, equity is no longer there., equity is no longer there.

ReassessmentReassessment

A systematic analysis of all locally A systematic analysis of all locally assessed parcels to assure that all assessed parcels to assure that all assessments are at a stated uniform assessments are at a stated uniform percentage of value as of the percentage of value as of the valuation date of the assessment roll valuation date of the assessment roll upon which the assessments upon which the assessments appear. (RPTLappear. (RPTL§§ 102) 102)

ReassessmentReassessment

The terms The terms reassessment, reassessment, revaluationrevaluation and and updateupdate are are synonymous.synonymous.

Reassessment – What It Does

Produces equity by eliminating unfair assessments.

Distributes tax burden fairly within the municipality.

Provides defensible data and assessments.

Increases taxpayer confidence and understanding.

Reassessment –What It Does Not Do

Generate additional revenue

Correct external inequalities

Prevent tax shifts

Compensate taxpayers for prior inequities

Steps in a ReassessmentSteps in a Reassessment Assessment Equity AnalysisAssessment Equity Analysis Reassessment DecisionReassessment Decision Analysis of SalesAnalysis of Sales Edit DataEdit Data Production and Review of ValuesProduction and Review of Values Notification of Preliminary ValuesNotification of Preliminary Values Informal HearingsInformal Hearings File Tentative Assessment RollFile Tentative Assessment Roll Grievance DayGrievance Day

Town of KendallTown of Kendall

Property Use # of Parcels

Residential 1052

Commercial 18

Farm 229

Vacant land 389

Utility & special franchise 16

Wholly exempt 39

Total Parcels 1743

Town of KendallTown of Kendall

Assessed ValuesAssessed ValuesResidential parcelsResidential parcels Average assessment $ 110,832 Average assessment $ 110,832

Sale PricesSale Prices Residential Residential Average residential sale price $ 132,876Average residential sale price $ 132,876

Town of Kendall – Residential ValuesTown of Kendall – Residential Values

NbhdNbhd Avg. Avg. AssessmeAssessme

nt in nt in 20092009

Avg. Avg. Selling Selling PricePrice

RatioRatio

RuralRural 90,27090,270 98,70998,709 .91.91

LakefroLakefrontnt

153,729153,729 193,812193,812 .79.79

LakevieLakevieww

99,40099,400 118,700118,700 .84.84

Do You Know Your Market Do You Know Your Market Value?Value?

Get a reasonable estimate of the Get a reasonable estimate of the market value of your propertymarket value of your property

Lists of recent sales and photographs Lists of recent sales and photographs are available at the Assessor’s Officeare available at the Assessor’s Office

Look at the homes insert in the Look at the homes insert in the newspaper, real estate ads, and web-newspaper, real estate ads, and web-sitessites

Notification of Preliminary Notification of Preliminary AssessmentsAssessments

Change of Assessment NoticesChange of Assessment Notices Assessment DisclosureAssessment Disclosure NoticeNotice

Assessment Disclosure Assessment Disclosure AnalysisAnalysis

§511 RPTL§511 RPTL Show change in Tax liabilityShow change in Tax liability Sometimes called “Impact Notices”Sometimes called “Impact Notices” 60 days prior to Tentative Roll (March 1)60 days prior to Tentative Roll (March 1)

Assessment Disclosure Assessment Disclosure AnalysisAnalysis

To illustrate the possible effect of the To illustrate the possible effect of the reassessment on your taxes, we use reassessment on your taxes, we use the new full value assessments and the new full value assessments and last year’slast year’s budgets budgets

Assessment Disclosure AnalysisAssessment Disclosure Analysis

Example:Example:Amount of Amount of TownTown Tax Levy Tax Levy $540,000$540,000

Divided by Taxable Assessed Value Divided by Taxable Assessed Value

’’0909 $120,000,000 $120,000,000 vs.vs. ’10 ’10 $138,000,000$138,000,000

Equals Tax Rate Equals Tax Rate

‘‘0909 $4.50 per $1000$4.50 per $1000 vs. ’10 vs. ’10 $3.91 $3.91 per $1000per $1000

For ExampleFor Example#1 Sample Disclosure Notice: #1 Sample Disclosure Notice: 2009 Assessed Value 2009 Assessed Value $80,000$80,000

Tax Rate Tax Rate $4.50 per $1000$4.50 per $1000CalculationCalculation $80,000 * $4.50$80,000 * $4.50 = =

$360$360 10001000

2010 Assessed Value 2010 Assessed Value $90,000$90,000Tax Rate Tax Rate $3.91 per $1000$3.91 per $1000CalculationCalculation $90,000 * $3.91$90,000 * $3.91 = =

$351.90$351.90 10001000 $351.90 - $360.00 = $8.10 decrease$351.90 - $360.00 = $8.10 decrease

For ExampleFor Example#2 Sample Disclosure Notice: #2 Sample Disclosure Notice: 2009 Assessed Value 2009 Assessed Value $80,000$80,000

Tax Rate Tax Rate $4.50 per $1000$4.50 per $1000CalculationCalculation $80,000 * $4.50$80,000 * $4.50 = =

$360.00$360.00 10001000

2010 Assessed Value 2010 Assessed Value $96,000$96,000Tax Rate Tax Rate $3.91 per $1000$3.91 per $1000CalculationCalculation $96,000 * $3.91$96,000 * $3.91 = =

$375.36$375.36 10001000 $375.36 - $360.00 = $15.36 increase$375.36 - $360.00 = $15.36 increase

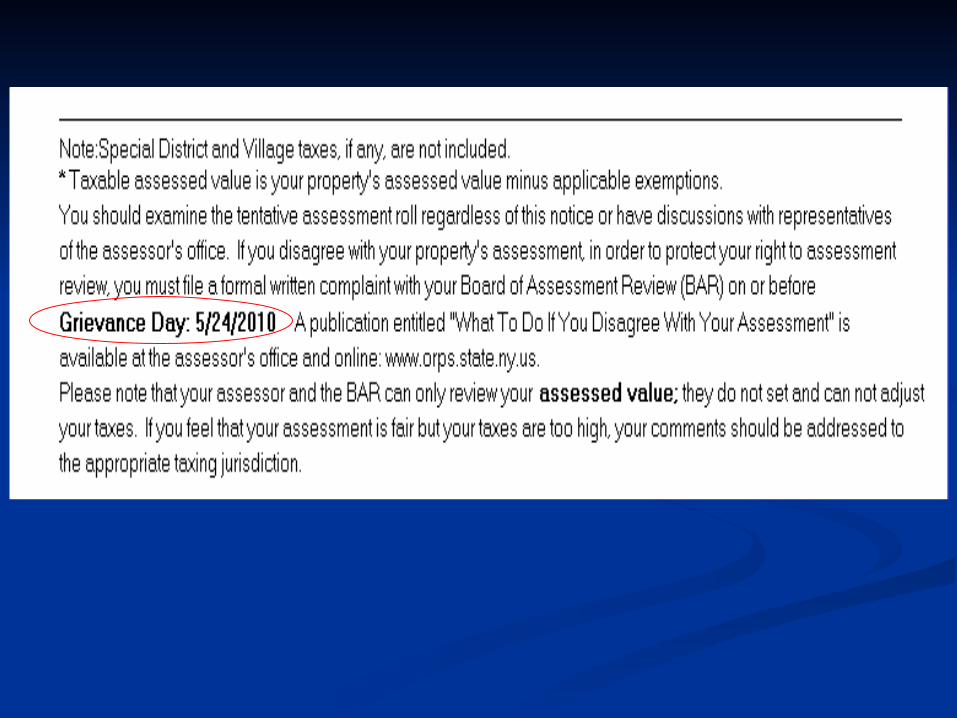

Appeal ProcessAppeal Process

Informal MeetingInformal Meeting

BAR Board of Assessment ReviewBAR Board of Assessment Review

SCAR Small Claims Assessment ReviewSCAR Small Claims Assessment Review

Article 7 NY Supreme CourtArticle 7 NY Supreme Court

Appeal Process – Sources Appeal Process – Sources of Taxpayer Informationof Taxpayer Information

Assessor’s OfficeAssessor’s Office County websiteCounty website

Real estate websites, e.g.,Real estate websites, e.g., http://homesteadnet.com

"A Taxpayer's Guide: How to "A Taxpayer's Guide: How to File for A Review of Your File for A Review of Your Assessment” available on line at Assessment” available on line at www.orps. ststate..ny.us

Want More Want More Information?Information?

Visit the New York State Visit the New York State Office of Real Property Office of Real Property Services Website at:Services Website at:

www.orps.state.ny.uswww.orps.state.ny.us