Embed Size (px)

Citation preview

Todd D. Keator, Thompson & Knight LLP, Dallas, TX

Understanding the New Partnership Audit Rules

State Bar of Texas Tax Section Annual Meeting June 17, 2016

• Summary of New Partnership Audit Rules

• Open Issues

• Drafting Considerations in Partnership Agreements and Other Agreements

Overview

2

- Congress repealed and replaced the 1982 Tax Equity and Fiscal Responsibility Act (TEFRA) and electing large partnership (ELP) rules with a new regime for partnership adjustments and audits that is focused on partnership-level assessments and collections.

- Game changer that is going to force most partnerships to amend partnership agreements to take into account the potential partnership entity level assessments.

- IRS requested comments in Notice 2016-23. State Bar of Texas Tax Section provided comments on April 26, 2016.

Bipartisan Budget Act of 2015 – “BBA”

3

• Effective Date: Applies to returns filed for partnership taxable years beginning after December 31, 2017;

• TEFRA and ELP rules repealed (and partners no longer have rights to participate in tax audits or litigation – i.e., no more “notice partners” concept);

• New rules apply to all partnerships unless the partnership elects out;

• Tax on “imputed underpayments” is assessed and collected at the partnership level (unless the partnership makes an election to push out the tax liability to its partners);

• “Tax Matters Partner” is replaced with new “Partnership Representative” (who need not be a partner).

Highlights of BBA

4

• TEFRA – Key elements: - Audit process determined at partnership level (instead of

multiple audits at individual partner level); - IRS interacts with “tax matters partner” (who must be a

partner); - Resulting deficiencies flow through to partners; - Collection efforts at partner level, which proved

administratively burdensome with large partnerships with tens of thousands of partners (such as MLPs), especially where IRS attempted to collect very small amounts from thousands of partners (cost outweighed collections).

• IRS did not have the resources or capability to audit large partnerships and multi-tiered partnerships due to complexity of allocating adjustments to ultimate partners and assessing tax.

• Result was that IRS audited less than 1% of large partnerships and collected very little tax from these audits.

Purpose of BBA – Replace TEFRA

5

• Benefits of BBA over TEFRA:

- Easier for IRS to audit partnerships and collect tax;

- No right to notice/participation in audits by individual partners;

- Statutory default is to collect tax at partnership level; thus, burden of passing adjustment through to the partners shifts from the IRS to the partnership.

• Congress estimates partnership audits under the new rules will generate approximately $10 billion in tax revenue.

BBA – Key Benefits

6

• Effective for partnership tax years beginning after December 31, 2017

• Partnerships may elect to have the rules apply earlier (for tax years beginning after November 2, 2015).

- Query whether partnerships should elect in early?

• “The delayed effective date does not mean that partnership tax advisors can take a siesta until the end of 2017. The changes have profound implications for partnership agreements drafted today and afterward – and also for partnership agreements drafted yesterday and before.” – Terry Cuff.

Effective Date of New Partnership Audit Procedures

7

• Who do you represent?

• Address in new partnership and LLC agreements prospectively.

• Amend prior agreements? Will partners agree?

• Other relevant agreements:

- Purchase and Sale Agreements;

- Contribution Agreements;

- Redemption and Dissolution Agreements;

- Merger Agreements;

- Disclosure documents;

- Loan Agreements;

- Side letters.

DRAFTING POINTS

8

• Audits (and any litigation) conducted at the partnership level.

• Default rule is that partnership is assessed tax liability on the “Imputed Underpayment Amount”

- Partnership is generally assessed tax at the highest rate under Sec. 1 or Sec. 11 (i.e., 39.6%), unless it can demonstrate that the tax should be lower (corporate partners or individual partners subject to lower capital gains or dividend rate)

- “Imputed Underpayment Amount” is reduced to the extent partners “for the reviewed year” file amended returns and pay the tax

- Partnership can elect to file adjusted partner statements (quasi amended K-1s) for each partner for the “reviewed year”

- Special rule for reallocation of distributive share

- Negative adjustments reduce income in adjustment year

Highlights of New Partnership Audit Procedures

9

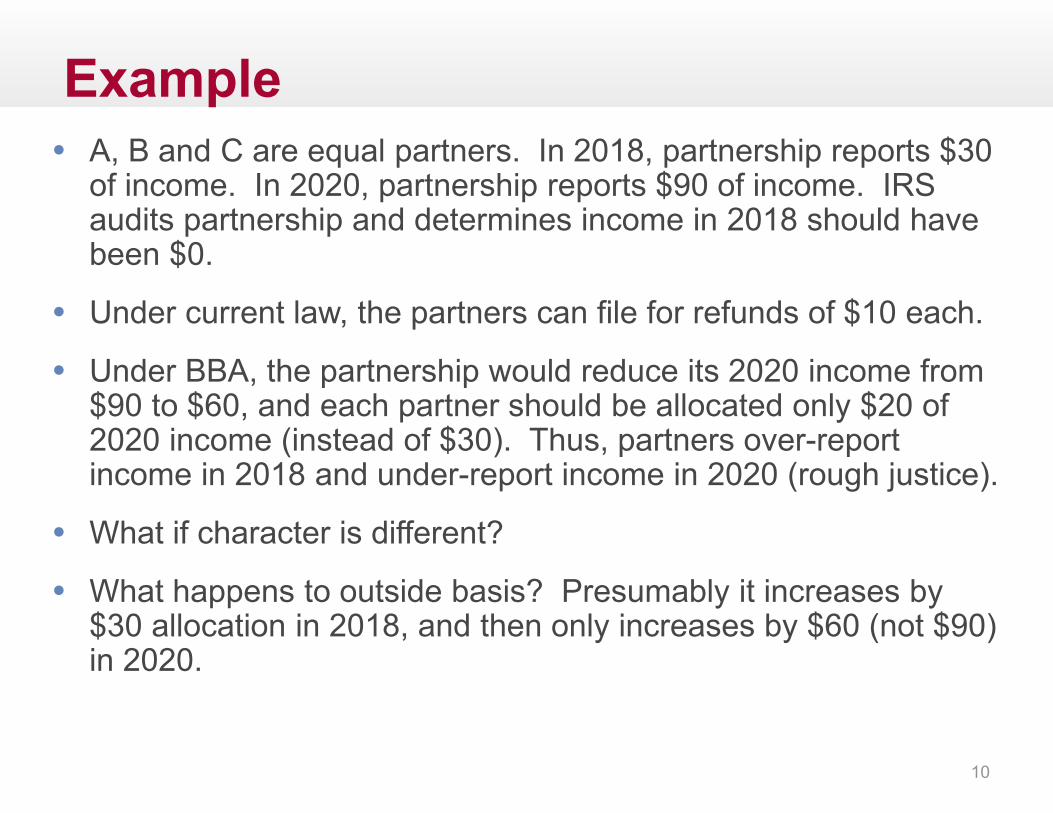

• A, B and C are equal partners. In 2018, partnership reports $30 of income. In 2020, partnership reports $90 of income. IRS audits partnership and determines income in 2018 should have been $0.

• Under current law, the partners can file for refunds of $10 each.

• Under BBA, the partnership would reduce its 2020 income from $90 to $60, and each partner should be allocated only $20 of 2020 income (instead of $30). Thus, partners over-report income in 2018 and under-report income in 2020 (rough justice).

• What if character is different?

• What happens to outside basis? Presumably it increases by $30 allocation in 2018, and then only increases by $60 (not $90) in 2020.

Example

10

• “Reviewed Year” – Partnership tax year or return under audit

• “Adjustment Year” – Generally the year in which the adjustment for the “reviewed year” becomes final (i.e., under court decision or notice of final partnership adjustment)

• “Imputed Underpayment Amount” – Net non-favorable adjustments to the partnership tax year multiplied by the applicable tax rate(s)

• “Partnership Representative” – Party selected to represent the partnership before the IRS and to make tax decisions on behalf of the partnership

Key Definitions

11

• Each partnership must designate a “Partnership Representative” (PR) who has the sole authority to act on behalf of the partnership

• PR must be a “person” with a substantial U.S. presence - Under 7701(a)(1), the term “person” includes, an individual, trust,

estate, partnership, association, company, or corporation - Guidance is needed as to who can act on behalf of an entity that

is designated as the PR - Substantial U.S. presence is not defined. But See Treas. Reg. §

301.7701(b)-1 for guidance on “substantial U.S. presence” - PR is not required to be a partner in the partnership (i.e., now the

CFO can serve in this role) • IRS will appoint a PR if the partnership does not designate one. How

will this be determined? Must there be a connection? Texas Tax Section letter recommends default be to designate the GP or partner with largest profits interest, and that appointed PR must consent.

• How do we identify the PR to the IRS? On form 1065?

Partnership Representative

12

• IRS asserts imputed underpayment against Partnership in the amount of $1,000. PR decides not to notify the Partners of the IRS audit, and PR (on behalf of Partnership) chooses to accept the underpayment and not seek administrative or judicial review (without informing any of its partners). PR further elects to push out the tax on the partners. Partner A has a 10% share and receives an adjusted K-1 showing $100 of additional income, the tax on which is $39.60. If Partner A disagrees with the imputed underpayment, what can Partner A do?

• Partner A has no right to challenge the initial audit and assessment. Partner A must pay the tax or face IRS collections.

Example

13

• Agreements should address standards for selecting, terminating and replacing the Partnership Representative.

• Current practice has been to include a “Partnership Representative” provision in the TMP section.

• Scope of Partnership Representative provision depends on who you represent (i.e., total authority vs. board consent vs. partner consent at some level).

• Key issues include: notice to partners (of proposed and final adjustments, etc.); duty to inform; extending the SOL; settling an audit; filing a petition for readjustment; other material concessions. Should these rights extend to both current and former partners?

• Decisions to pay tax or make push out election? Must partners approve? Which partners? What threshold? De minimis payments? Other considerations?

• Indemnification of Partnership Representative?

DRAFTING POINTS

14

• Partnership Representative Provision (Simple):

With respect to tax years beginning after December 31, 2017, the partnership representative of the Partnership pursuant to Code Section 6223(a) shall be , or any Partner or other person with a substantial presence in the United States designated by the General Partner in the manner prescribed by the Internal Revenue Service.

DRAFTING POINTS

15

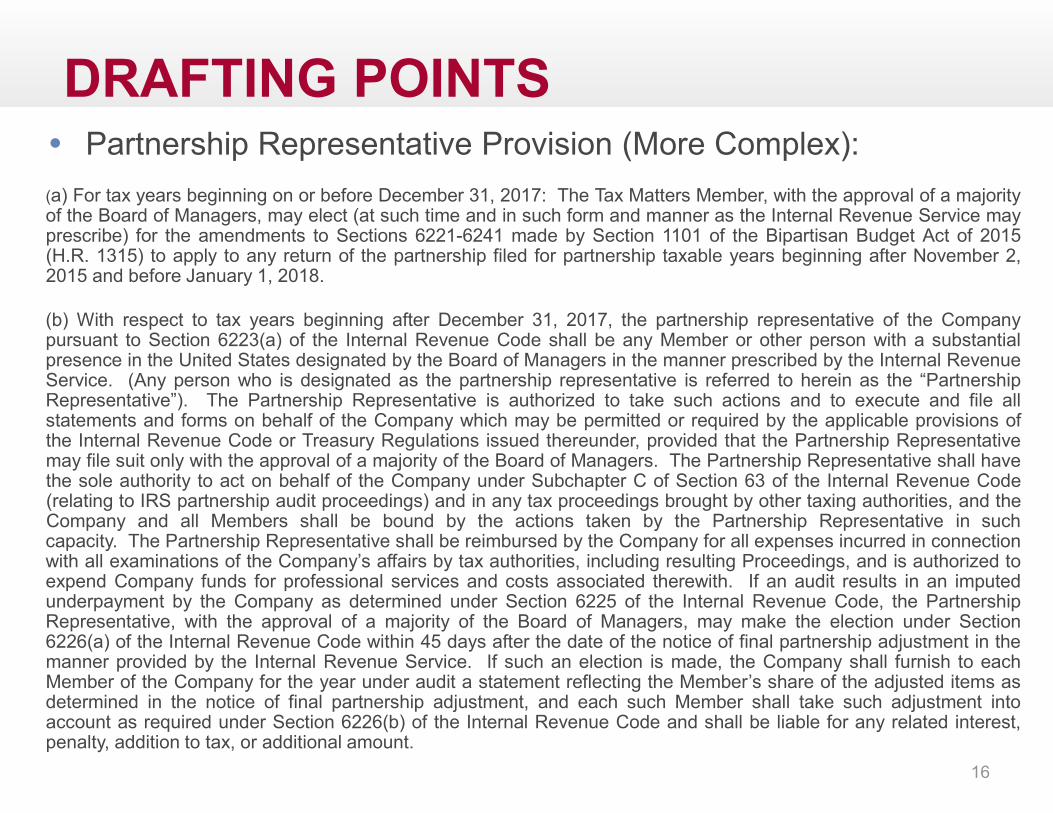

• Partnership Representative Provision (More Complex): (a) For tax years beginning on or before December 31, 2017: The Tax Matters Member, with the approval of a majority of the Board of Managers, may elect (at such time and in such form and manner as the Internal Revenue Service may prescribe) for the amendments to Sections 6221-6241 made by Section 1101 of the Bipartisan Budget Act of 2015 (H.R. 1315) to apply to any return of the partnership filed for partnership taxable years beginning after November 2, 2015 and before January 1, 2018.

(b) With respect to tax years beginning after December 31, 2017, the partnership representative of the Company pursuant to Section 6223(a) of the Internal Revenue Code shall be any Member or other person with a substantial presence in the United States designated by the Board of Managers in the manner prescribed by the Internal Revenue Service. (Any person who is designated as the partnership representative is referred to herein as the “Partnership Representative”). The Partnership Representative is authorized to take such actions and to execute and file all statements and forms on behalf of the Company which may be permitted or required by the applicable provisions of the Internal Revenue Code or Treasury Regulations issued thereunder, provided that the Partnership Representative may file suit only with the approval of a majority of the Board of Managers. The Partnership Representative shall have the sole authority to act on behalf of the Company under Subchapter C of Section 63 of the Internal Revenue Code (relating to IRS partnership audit proceedings) and in any tax proceedings brought by other taxing authorities, and the Company and all Members shall be bound by the actions taken by the Partnership Representative in such capacity. The Partnership Representative shall be reimbursed by the Company for all expenses incurred in connection with all examinations of the Company’s affairs by tax authorities, including resulting Proceedings, and is authorized to expend Company funds for professional services and costs associated therewith. If an audit results in an imputed underpayment by the Company as determined under Section 6225 of the Internal Revenue Code, the Partnership Representative, with the approval of a majority of the Board of Managers, may make the election under Section 6226(a) of the Internal Revenue Code within 45 days after the date of the notice of final partnership adjustment in the manner provided by the Internal Revenue Service. If such an election is made, the Company shall furnish to each Member of the Company for the year under audit a statement reflecting the Member’s share of the adjusted items as determined in the notice of final partnership adjustment, and each such Member shall take such adjustment into account as required under Section 6226(b) of the Internal Revenue Code and shall be liable for any related interest, penalty, addition to tax, or additional amount.

DRAFTING POINTS

16

• Partnership Representative – Combined Provision (Board Managed):

Add to Defined Terms: “Partnership Representative” means (i) for taxable years (or any portion thereof) prior to the effective date of the BBA, the Partner designated by the Board to serve as the “tax matters partner” (as defined in Section 6231(a)(7) of the Code (as in effect before amendment of the BBA)), and (ii) for taxable years (or any portion thereof) for which the provisions of the BBA are effective, the Person designated by the Board to serve as the “partnership representative” (as defined in Section 6223(a) of the Code, as amended by the BBA).

Replace normal TMP section: For taxable years before the effective date of the BBA, the Partnership Representative shall have all of the rights, duties, powers and obligations provided for in Sections 6221 through 6232 of the Code (as in effect before amendment by the BBA) with respect to the Partnership, subject, in all cases, to the consent of the Board. For taxable years for which the provisions of the BBA are in effect, all decisions regarding elections under Section 6221(b) or Section 6226 of the Code, as amended by the BBA, shall be made by the Partnership Representative subject, in all cases, to the consent of the Board.

Drafting Points

17

• Comprehensive PR Provision: (a) The Managers shall elect one among them who is eligible to serve as the Company’s “tax matters partner” as defined in Code Section 6231(a)(7) and any comparable provision of state or local tax law, as in effect for taxable years beginning before December 31, 2017, and as the “partnership representative” (as defined in Code Section 6223(a), as in effect for taxable years beginning after December 31, 2017, and the Treasury Regulations thereunder) (such Member serving as the “tax matters partner” or “partnership representative, as applicable, the “Company Representative”) and the Company Representative shall take such actions as are required to be designated the tax matters partner or partnership representative, as applicable, under applicable Treasury Regulations. The Company Representative shall represent the Company in connection with all examinations of the Company’s tax returns by tax authorities, including administrative and judicial proceedings to contest any proposed adjustments. Furthermore, the Company Representative shall have the rights, power and authority, and shall be subject to all of the obligations, for the making of any elections and the conduct of, and the decision to initiate (where applicable), any administrative and judicial proceedings involving the Company under the partnership audit provisions of Subchapter C of Chapter 63 of the Code as amended by the Bipartisan Budget Act of 2015 (the “Budget Act”) and in effect for any relevant Company taxable year (such provisions, together with applicable Treasury Regulations and other Internal Revenue Service (“IRS”) guidance, are referred to herein as the “New Audit Rules”), including (i) an IRS examination of the Company, (ii) a request for administrative adjustment filed by the Company, (iii) the filing of a petition for readjustment (including choice of judicial forum) with respect to a final notice of partnership adjustment, (iv) the appeal of an adverse judicial decision, (v) the compromise, settlement or dismissal of any such proceedings on such terms as the Company Representative, in consultation with the Company’s tax advisors, deems appropriate, taking into account the collective interests of the Member and former Members affected thereby, (vi) if the Company is eligible, electing out of the New Audit Rules under Code Section 6221(b), and (vii) the making of an election under Code Section 6226(a). Each Member agrees to be bound by the decisions and elections made by the Company Representative under the New Audit Rules. Subject to Section 8.5(c), the Company Representative has the exclusive right to conduct Proceedings relating to Company taxes, including under the New Audit Rules, and to determine whether the Company (either on its own behalf or on behalf of the Members) will contest or continue to contest any tax deficiencies assessed or proposed to be assessed by any taxing authority. The Company Representative shall keep the Members informed on a timely basis of all material developments with respect to any such Proceeding and consistent with the requirements of the New Audit Rules, the Company Representative shall take commercially reasonable measures to inform the Members of any material decision or actions it takes in its capacity as Company Representative.

Drafting Points

18

• Comprehensive PR Provision, Continued (b) Each Member shall cooperate with the Company Representative and do or refrain from doing all things reasonably requested by the Company Representative with respect to the conduct of any Company tax Proceeding. Each Member (other than the Company Representative) waives any right that such Member has to participate in administrative or judicial proceedings relating to the determination of partnership items at the partnership level under I.R.C. Section 6224 or similar provisions in other tax jurisdictions where such proceedings are being prosecuted by the Company Representative. Each Member that is a pass-thru partner (as defined in I.R.C. Section 6231(a)(9)) shall cause such waiver to be binding on all persons owning an interest in the Company through such Member. The Company Representative may exercise the power of attorney granted in Section [ ] to execute and file any statements or forms with the Internal Revenue Service or other tax authorities to effect such waiver.

(c) The Company Representative may not bind any other Member to a settlement agreement relating to taxes without obtaining the written concurrence of such Member.

(d) Any deficiency for taxes imposed on a Member (including penalties, additions to tax or interest imposed with respect to such taxes) shall be paid by such Member and, if paid or required to be paid by the Company, is recoverable from such Member pursuant to Section [ ] or by other legal means.

(e) The Members hereby consent in advance to any amendments to this Section [ ] that the Company Representative, in consultation with the Company’s tax advisors, determine are reasonably necessary and appropriate to address additional guidance provided in IRS guidance relating to the New Audit Rules, or to take into account subsequently enacted amendments to the New Audit Rules, or that the Company Representative otherwise determines are in the best interest of the Company and the Members in complying with the New Audit Rules.

Drafting Points

19

• All partners are bound by a final resolution in the partnership proceeding

• Unlike under TEFRA, partners do not have the right to participate in the proceeding or receive notice of the proceedings from the IRS

• Penalties determined at the partnership level; no partner level defenses to penalties

• Only partnership-level statute of limitations relevant – a partner’s statute of limitations is no longer taken into account, unless the partnership elects out of the new rules

Partnership Level Determination

20

• Sample Agreement to be Bound by BBA decisions:

Except as otherwise required by applicable law or regulatory requirements or determined by the Board, each Partner and Former Partner agrees (i) to treat, on such Partner or Former Partner’s individual income tax returns, all tax-related items (including the amount of any contributions and distributions, as well as any item of income, gain, loss, deduction or credit) relating to such Partner or Former Partner’s interest in the Partnership in a manner consistent with the treatment of such item by the Partnership as reflected on the Schedule K-1 or other information statement furnished by the Partnership to such Partner for use in preparing such Partner or Former Partner’s income tax returns, (ii) to amend Partner or Former Partner’s tax returns and pay any resulting taxes, interest and penalties in connection with the Partnership’s electing under Section 6225(a) of the Code, as amended by the BBA, and (iii) to take into account any adjustments and pay any taxes, interest and penalties that result from the Partnership’s electing under Section 6226 of the Code, as amended by the BBA. No Partner or Former Partner shall have the right to participate in the audit of any Partnership tax return or any administrative or judicial proceedings conducted by the Partnership or the Partnership Representative arising out of or in connection with any such audit.

Drafting Points

21

• Computation of Imputed Underpayment Amount

- All adjustments to income, gain, deduction, and loss are netted and multiplied by the highest rate in Code Section 1 (39.6%) or Code Section 11 (35%) (which currently would be 39.6%) [Note: The highest rate aspect will encourage “push out” elections]

- Any increase or decrease in loss is treated as a decrease or increase in income

- After the Imputed Underpayment Amount is calculated, changes in credits are taken into account as a increase or decrease in the Imputed Underpayment Amount, as appropriate under the circumstances

- Tax assessment is made for the Adjustment Year; not the Reviewed Year

• What effect on outside basis and capital accounts?

Partnership Tax Assessment – “Imputed Underpayment Amount”

22

• Computation of Imputed Underpayment Amount - Partnership can submit evidence to reduce the imputed

underpayment by the portion that would be allocable to tax exempt entities [query how this works with tiered entities]

- Partnership can submit evidence to modify the “Applicable Highest Tax Rate” as follows: • Partner receiving allocation is a corporation subject to 35%

maximum tax rate [query what happens if maximum individual rate drops below highest corporate rate]

• Partner receiving allocation of capital gains and dividends is an individual subject to reduced tax rates

• Partner is a partner in an MLP and has suspended passive activity losses related to the MLP (see 469(k))

• Applicable rate is always the highest rate with respect to the income (query which rate applies to capital gain)

• Secretary is authorized to issue regulations or other guidance for additional modifications to the Imputed Underpayment Amount

Partnership Tax Assessment – “Imputed Underpayment Amount”

23

• Partnership has ($100) capital loss and $100 of ordinary income in the reviewed year. What is the imputed underpayment for such year? - Answer: Zero?

Example

24

• Partnership has 3 equal partners – A, B and C. A is itself a partnership with 2 equal partners, both are tax exempt entities. B is a corporation taxed at 35%. C is an individual. An audit results in a $90 increase in Partnership’s long term capital gain for the audit year.

• If Partnership pays the tax due under the default rule, the tax is $35.64 ($90 x 39.6%).

• Partnership can submit evidence to reduce the imputed underpayment as follows:

- B’s share = $30 x 35% = $10.50

- C’s share = $30 x 20% = $6

- A’s share = $0?

• If successful, the tax burden has been reduced to $16.50. [query how the resulting tax burden is now allocated among the partners]

Example

25

• In 2018, A and B own Partnership 50/50, and Partnership reports $1M deduction (allocated 50/50). In 2019, A sells her interest to C for a gain. C succeeds to A’s capital account. In 2020, IRS disallows the 2018 deduction, resulting in 2020 underpayment of $396,000 ($1M x 39.6%). Partnership is liable for the underpayment, which, with interest and penalties, comes out to $500,000. B and C indirectly bear this burden. What are the basis and capital account adjustments? Texas Tax Section comments recommend:

- Allocate $1M 2020 income to B and C 50/50. This increases outside basis and capital accounts by $500,000 each.

- Allocate $500k payment (nondeductible) to B and C 50/50. This decreases outside basis and capital accounts by $250,000 each.

Example (from Texas Tax Section)

26

• Partnership Agreements should address:

- Obligation of Partnership Representative to seek to lower partnership rate of tax.

- Authority in Partnership Agreement to request partner-specific information, and obligation to provide information. May include confidential information (e.g. tax returns).

- Ability to pay tax from partnership accounts, or to call capital or loans to pay the tax (and penalties for failure to contribute).

- Ability to treat tax payments as advanced distributions (similar to withholding tax payments).

- Allocation of the tax burden among the partners.

- Indemnification and clawback from prior partners.

• Tax exempt entities are asking for side letters.

DRAFTING POINTS

27

• Simple indemnification provision:

Each Partner and Former Partner hereby agrees to be liable for its proportionate share (as determined by the General Partner) of any tax imposed on the Partnership attributable to any taxable year (or portion thereof) of the Partnership for which such person was a Partner.

Drafting Points

28

• Agreement to Bear Tax Liability

If the Partnership becomes liable for any taxes, interest or penalties under Section 6225 of the Code, as amended by the BBA (following a final determination of such liability by the relevant governmental authority, or as determined by the Board), each Person that was a Partner of the Partnership for the taxable year to which such liability relates shall indemnify and hold harmless the Partnership for such Person’s allocable share of the amount of such tax liability, including any interest and penalties associated therewith, as reasonably determined by the Board. The Partnership shall have a right of setoff against distributions to a Partner or Former Partner in the amount of such withholding tax or other liability or obligation. Any amount withheld pursuant to this Section [ ] shall be treated as an amount distributed to such Partner or Former Partner for all purposes under this Agreement.

Drafting Points

29

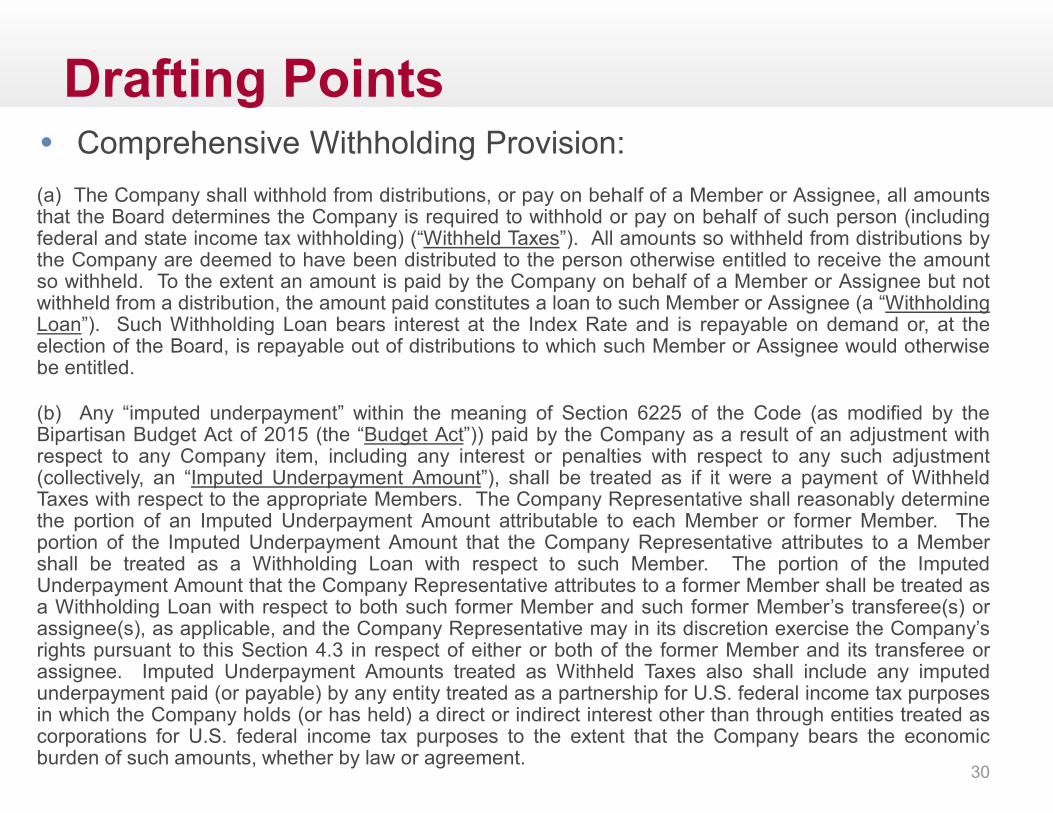

• Comprehensive Withholding Provision: (a) The Company shall withhold from distributions, or pay on behalf of a Member or Assignee, all amounts that the Board determines the Company is required to withhold or pay on behalf of such person (including federal and state income tax withholding) (“Withheld Taxes”). All amounts so withheld from distributions by the Company are deemed to have been distributed to the person otherwise entitled to receive the amount so withheld. To the extent an amount is paid by the Company on behalf of a Member or Assignee but not withheld from a distribution, the amount paid constitutes a loan to such Member or Assignee (a “Withholding Loan”). Such Withholding Loan bears interest at the Index Rate and is repayable on demand or, at the election of the Board, is repayable out of distributions to which such Member or Assignee would otherwise be entitled.

(b) Any “imputed underpayment” within the meaning of Section 6225 of the Code (as modified by the Bipartisan Budget Act of 2015 (the “Budget Act”)) paid by the Company as a result of an adjustment with respect to any Company item, including any interest or penalties with respect to any such adjustment (collectively, an “Imputed Underpayment Amount”), shall be treated as if it were a payment of Withheld Taxes with respect to the appropriate Members. The Company Representative shall reasonably determine the portion of an Imputed Underpayment Amount attributable to each Member or former Member. The portion of the Imputed Underpayment Amount that the Company Representative attributes to a Member shall be treated as a Withholding Loan with respect to such Member. The portion of the Imputed Underpayment Amount that the Company Representative attributes to a former Member shall be treated as a Withholding Loan with respect to both such former Member and such former Member’s transferee(s) or assignee(s), as applicable, and the Company Representative may in its discretion exercise the Company’s rights pursuant to this Section 4.3 in respect of either or both of the former Member and its transferee or assignee. Imputed Underpayment Amounts treated as Withheld Taxes also shall include any imputed underpayment paid (or payable) by any entity treated as a partnership for U.S. federal income tax purposes in which the Company holds (or has held) a direct or indirect interest other than through entities treated as corporations for U.S. federal income tax purposes to the extent that the Company bears the economic burden of such amounts, whether by law or agreement.

Drafting Points

30

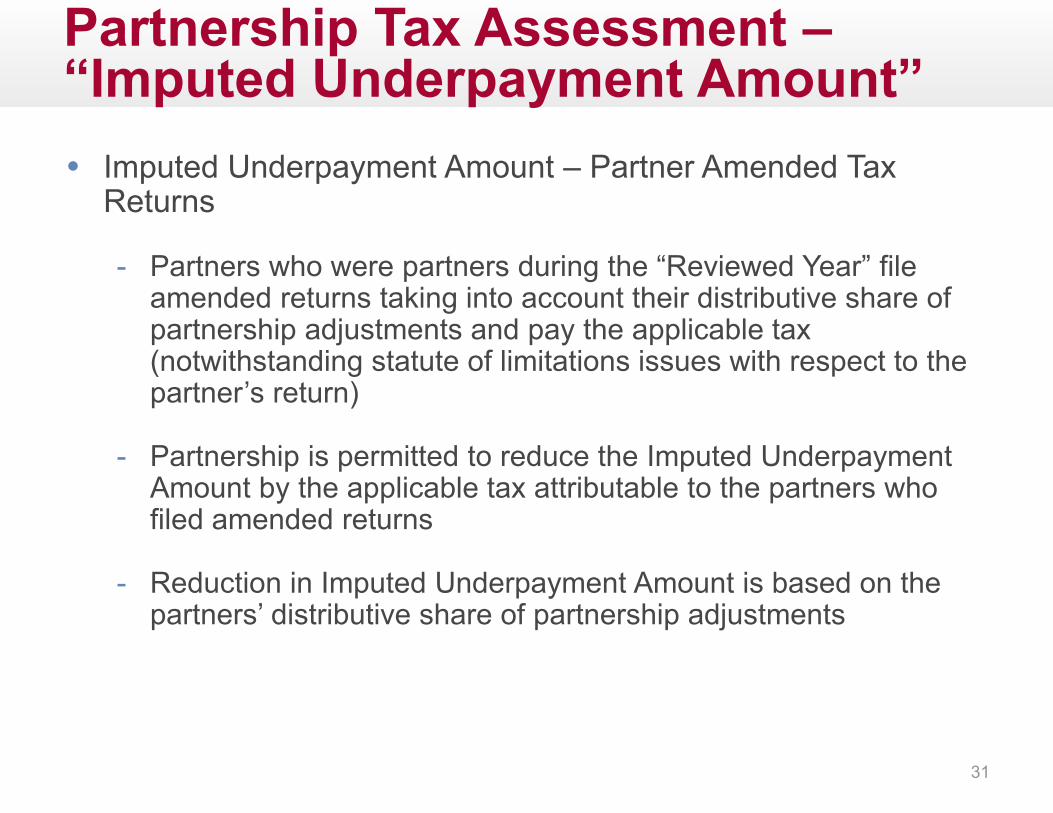

• Imputed Underpayment Amount – Partner Amended Tax Returns

- Partners who were partners during the “Reviewed Year” file amended returns taking into account their distributive share of partnership adjustments and pay the applicable tax (notwithstanding statute of limitations issues with respect to the partner’s return)

- Partnership is permitted to reduce the Imputed Underpayment Amount by the applicable tax attributable to the partners who filed amended returns

- Reduction in Imputed Underpayment Amount is based on the partners’ distributive share of partnership adjustments

Partnership Tax Assessment – “Imputed Underpayment Amount”

31

• Imputed Underpayment Amount – Time for Submission of Documents and Evidence

- Partnership has 270 days from the date when the Notice of Proposed Adjustment is mailed to the partnership (pursuant to Code Section 6231) to file any documents or evidence to have the Imputed Underpayment Reduced

- IRS must approve any modification of the imputed underpayment amount

- Documents must be drafted in a manner to comply with this timeline

Partnership Tax Assessment – “Imputed Underpayment Amount”

32

• In 2018, A and B own Partnership 50/50, and Partnership reports $1M deduction (allocated 50/50). In 2020, IRS disallows the 2018 deduction, resulting in 2020 underpayment of $396,000 ($1M x 39.6%). A files an amended return for 2018 reporting her 50% share of the partnership adjustment ($500,000) and paying total tax, interest and penalty of $250,000. As a result, Partnership’s imputed underpayment is reduced to $500,000, and Partnership pays total tax, interest and penalty of $250,000. How is this amount allocated between A and B? Texas Tax Section comments conclude:

- Default is to allocate $500,000 income and $250,000 payment 50/50. Is this fair to A?

- Comments recommend instead that the $250,000 payment (non-deductible) be allocated only to B. How would this be handled? Reduce B’s capital account or treat as a withholding tax payment?

Example

33

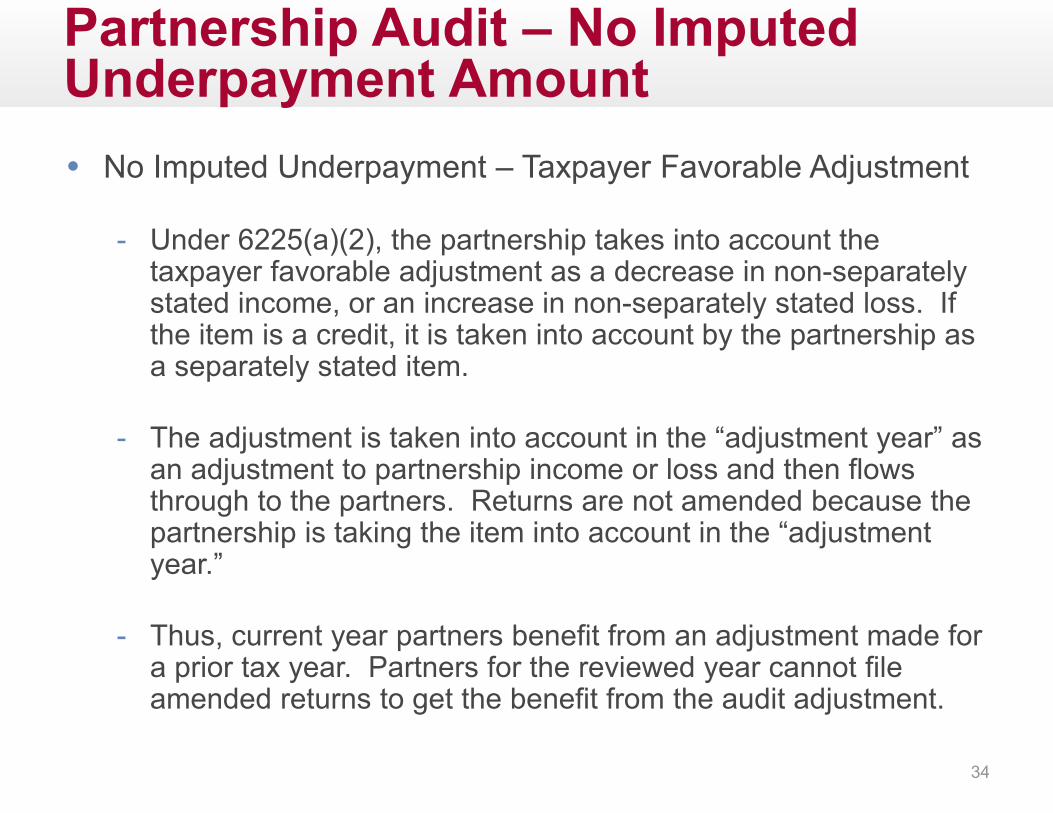

• No Imputed Underpayment – Taxpayer Favorable Adjustment

- Under 6225(a)(2), the partnership takes into account the taxpayer favorable adjustment as a decrease in non-separately stated income, or an increase in non-separately stated loss. If the item is a credit, it is taken into account by the partnership as a separately stated item.

- The adjustment is taken into account in the “adjustment year” as an adjustment to partnership income or loss and then flows through to the partners. Returns are not amended because the partnership is taking the item into account in the “adjustment year.”

- Thus, current year partners benefit from an adjustment made for a prior tax year. Partners for the reviewed year cannot file amended returns to get the benefit from the audit adjustment.

Partnership Audit – No Imputed Underpayment Amount

34

• Partnership AB reports $0 income in year 1 and $20,000 of income in year 2. A year 4 audit shows $10,000 should have been reported in each of years 1 and 2. Thus, there is an imputed underpayment in year 1 of $3,960. The partnership pays this amount, plus interest, at the end of year 4. What happens to the year 2 amount?

• Year 2 now has a $10,000 overpayment (because $10,000 was reallocated to year 1 in the audit). This is reported as a taxable loss in year 4, and A and B each get a year 4 K-1 showing a $5,000 loss.

- If A also has $5,000 of income in year 4, A can offset this income with the $5,000 loss.

- If B has no income in year 4, B must carry the loss forward and hope to be able to use it.

- Note that A and B get no interest benefit on the loss moved from year 2 to year 4.

Example

35

• Opt-Out for “Small” Partnerships

- Partnerships with 100 partners or less can opt out of the entity-level partnership determination

• Year by year election

• The election must include a disclosure of the name and TIN of the each partner

• How are community property spouses treated? 1 or 2 partners? Texas Tax Section comments advise counting as 1 (see also Rev. Proc. 2002-22). What about persons receiving via inheritance?

- Partners must be individuals, C corporations (including any foreign entity that would be treated as a C corporation if domestic), S Corporations or estates of deceased partners (no upper-tier partnerships)

• S corporation shareholders must be counted for purposes of the 100 partner test and disclosed to the IRS

Alternatives to Partnership-Level Assessment: Election Out for Small Partnerships

36

• Opt-Out for “Small” Partnerships

- The partnership must notify each partner of the election out.

- If election is made, IRS must make determinations at the partner level (similar to the TEFRA small partnership rules)

- Query whether 100 partners is still too large and will still impose an administrative burden on the IRS

• Should partnerships eligible to elect out do so? If they do, the partnership audit is back to “prehistoric era” where if you have 99 partners you can have 99 separate audits and 99 different results. General consensus among practitioners so far seems to be to recommend electing out if possible.

- For this reason, IRS public comments have expressed reluctance to expand election out.

Alternatives to Partnership-Level Assessment: Election Out for Small Partnerships

37

• Fund has 99 partners, 98 of whom are individuals and one of which is a single member LLC (a disregarded entity) owned by an individual. Can Fund elect out? Bluebook indicates that Fund should look through to the owner, so election out should be available. Texas Tax Section comments agree.

• Same, but now Fund has 97 individual partners and 2 DRE partners owned by individuals. Are there 101 partners here? Bluebook says count both DRE and owner, so 101. Texas Tax Section comments say 99.

• Fund has 98 partners, 97 of whom are individuals and one of which is a general partnership consisting of two individuals. Due to the general partnership partner, Fund is ineligible to elect out (unless IRS issues regulations saying otherwise). Texas Tax Section provided 3 criteria for election out here:

- LTP must provide IRS with name and TIN of each direct and indirect partner.

- Total number of K-1s throughout the chain is 100 or less.

- Only 2 tiers of partnerships allowed. Why limit to 2 tiers?

Example

38

• Partnership Agreement should address election out, and criteria for electing same.

• Should Partnership Representative have the authority? Should partners have approval rights? What threshold?

• If election out is desired, agreement should provide transfer restrictions to avoid transfers that would negate the ability to elect out.

• Partners should be obligated to provide requisite information to the Partnership Representative supporting the election out.

• Covenant in partnership agreement to remain under 100 partners?

DRAFTING POINTS

39

• Sample Election Out: The Partners agree to make the election provided in Code Section 6221(b)(1) for each taxable year of the Partnership for which the Partnership is eligible to make such election. The General Partner is authorized to make the disclosure required under Code Section 6221(b)(D)(ii) and the Partners hereby agree to provide their names and taxpayer identification numbers to the General Partner for this purposes.

• Additional S-Corporation Language: In the case of any Partner that is taxable as an “S corporation” (as defined in Code Section 1361(a)(1)), such Partner also agrees to provide the General Partner with the name and taxpayer identification number of each person with respect to whom such Partner is required to furnish a statement under Code Section 6037(b) for the taxable year of such Partner ending with or within the Partnership’s taxable year for which the election out under Code Section 6221(b)(1) is made.

DRAFTING POINTS

40

• Partnership Election to Issue Adjusted Partner Statements under Section 6226 (“Push Out” election)

- Any partnership may elect to issue adjusted “statements” (essentially amended K-1s) to the partners who were partners during the reviewed year

- Election must be made within 45 days of receiving the notice of final partnership adjustment

- Partnership must then furnish statements to each partner for the reviewed year and to the IRS [Query: When are these due?]

- The partners receiving the statements are subject to tax in the year of the statement, but the tax due equals the amount of tax that would have been owed in the reviewed year and intervening years to the extent of a tax increase due to the adjustment to tax attributes

- Tax attributes in the adjustment year are also adjusted

Alternatives to Partnership-Level Assessment: “Push Out” Election

41

• Partnership Election to Issue Amended “Statements”

- Reviewed year partners are liable for interest and penalties

- Interest is charged at higher rate (2 percentage points higher than rate in Section 6621(c) (interest charged from due date of partnership return for the reviewed year)

- Reviewed year partners have no right to an administrative or judicial review

• Not required by statute to consent to issuance of statements

• Bound by partnership-level determination

- No joint and several liability

• Will the “push out” election become the de facto default rule?

• What result if partner receiving adjusted K-1 fails to pay the tax? Must the partnership now pay?

Alternatives to Partnership-Level Assessment: Amended Statements

42

• In 2018, A and B own Partnership 50/50. B is itself a 50/50 partnership between D and E. Partnership reports $1M deduction (allocated 50/50 to A and B). In 2020, IRS disallows the 2018 deduction, resulting in 2020 underpayment of $396,000 ($1M x 39.6%). Partnership is liable for the underpayment, which, with interest and penalties, comes out to $500,000, but chooses to make the push out election to A and B. What is the consequence to B? Possibilities:

- B, as a flow through entity, is ineligible to make a subsequent push out election and so must pay the tax ($198,000 @ 39.6%).

- Alternatively, the Texas Tax Section recommends that B also be able to make a push out election to D and E.

- [Note: As a further alternative B, as a flow through entity, is not a taxpayer and so even if not eligible to make a push out election, may be permitted (or required) to pass through the $500,000 item to D and E on regular K-1s.]

Example (from Texas Tax Section)

43

• Partnership has 3 equal partners – A, B and C. A is itself a partnership with 2 equal partners, both are tax exempt entities. B is a corporation taxed at 35%. C is an individual. An audit results in a $90 increase in Partnership’s long term capital gain for the audit year. Partnership makes the push out election and provides A, B and C each with an adjusted statement showing a $30 increase in long term capital gain. Results:

- B pays tax of $10.50;

- C pays tax of $6.00;

- Does A pay tax of $11.88 ($30 x 39.6%)? Or can A make its own push out election and send statements to its two tax exempt partners, who pay $0 tax? Bluebook implies that A must pay the tax here. If so, can A follow the procedures in 6225(c) to reduce the tax to $0 based on having tax exempt partners?

Example

44

• Should the “push out” election be mandatory or optional? If optional, what are the standards for deciding? Some factors include fairness to current vs. prior partners, accuracy of adjustments, additional 2% interest, SECA/NII tax, additional partner level expense, and de minimis situations.

• Covenants that partners, whether current or former, will comply with the push out election and pay the resulting tax.

• Is 45 day window is realistic under the partnership agreement?

• Authority of PR to make push out election following liquidation?

• Lender preference?

• Covenants in Purchase Agreements?

• Can a partnership make the election and seek judicial review? Some comments recommend protective push out election, with ability to (i) defer sending adjusted K-1s and (ii) revoke push out election pending outcome of judicial review.

DRAFTING POINTS

45

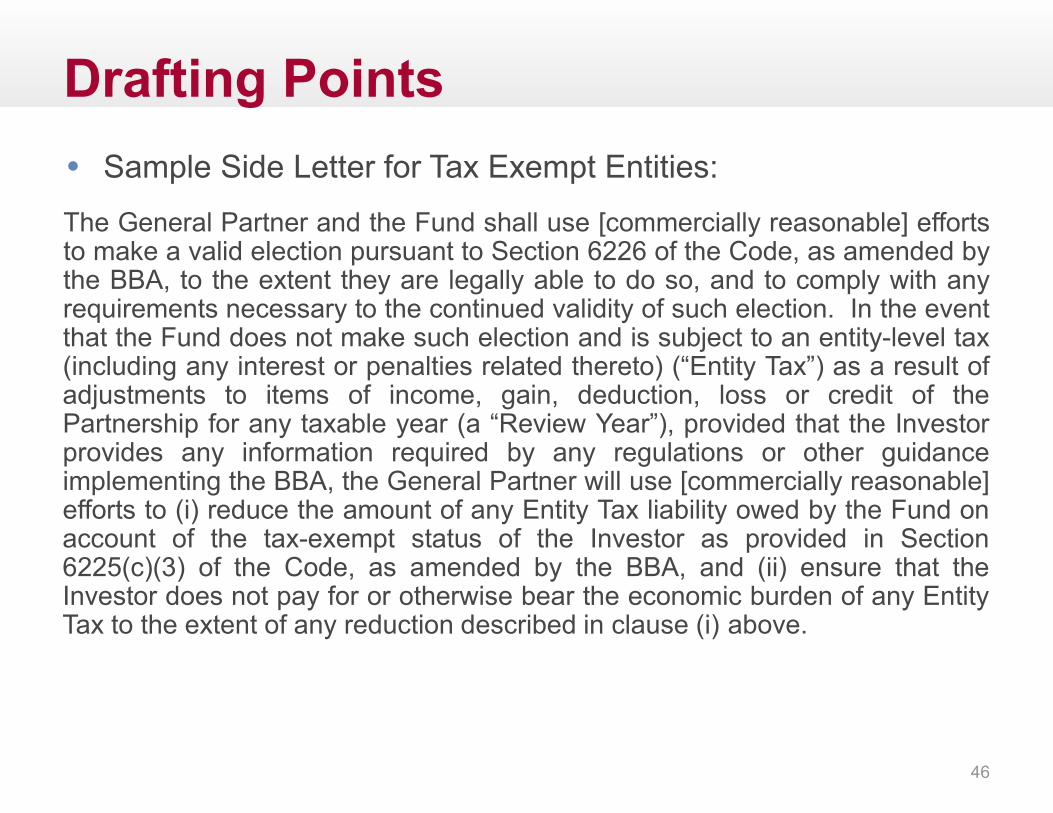

• Sample Side Letter for Tax Exempt Entities:

The General Partner and the Fund shall use [commercially reasonable] efforts to make a valid election pursuant to Section 6226 of the Code, as amended by the BBA, to the extent they are legally able to do so, and to comply with any requirements necessary to the continued validity of such election. In the event that the Fund does not make such election and is subject to an entity-level tax (including any interest or penalties related thereto) (“Entity Tax”) as a result of adjustments to items of income, gain, deduction, loss or credit of the Partnership for any taxable year (a “Review Year”), provided that the Investor provides any information required by any regulations or other guidance implementing the BBA, the General Partner will use [commercially reasonable] efforts to (i) reduce the amount of any Entity Tax liability owed by the Fund on account of the tax-exempt status of the Investor as provided in Section 6225(c)(3) of the Code, as amended by the BBA, and (ii) ensure that the Investor does not pay for or otherwise bear the economic burden of any Entity Tax to the extent of any reduction described in clause (i) above.

Drafting Points

46

• How are oil & gas tax partnerships treated under the default rule (i.e., partnership pays the tax)?

• Who is liable if there is no juridical entity to collect a tax deficiency from?

• Texas Tax Section comments recommend that oil & gas tax partnerships be forced to apply the push out election in all instances, because there is no juridical entity to collect from.

• What if a tax partnership has elected out of Subchapter K? Now, Texas Tax Section comments recommend that the partnership audit rules would no longer apply because the tax partnership is no longer required to file a return under 6031(a).

• Should tax partnership agreements contain an affirmative covenant to either elect our or make the push out election?

Tax Partnerships

47

• Procedure to elect to have the new partnership audit rules apply now

- In what circumstances would a partnership want to have the new partnership audit rules apply now?

- Examples:

• Administrative convenience;

• Small adjustments;

• Avoid extra 2% interest charge;

• Avoid SE and NII tax;

• Netting;

• Ensure consistent partner reporting by dominant partner;

• Shield partners from personal liability?

Open Issues: Election to Apply New Partnership Audit Rules Now

48

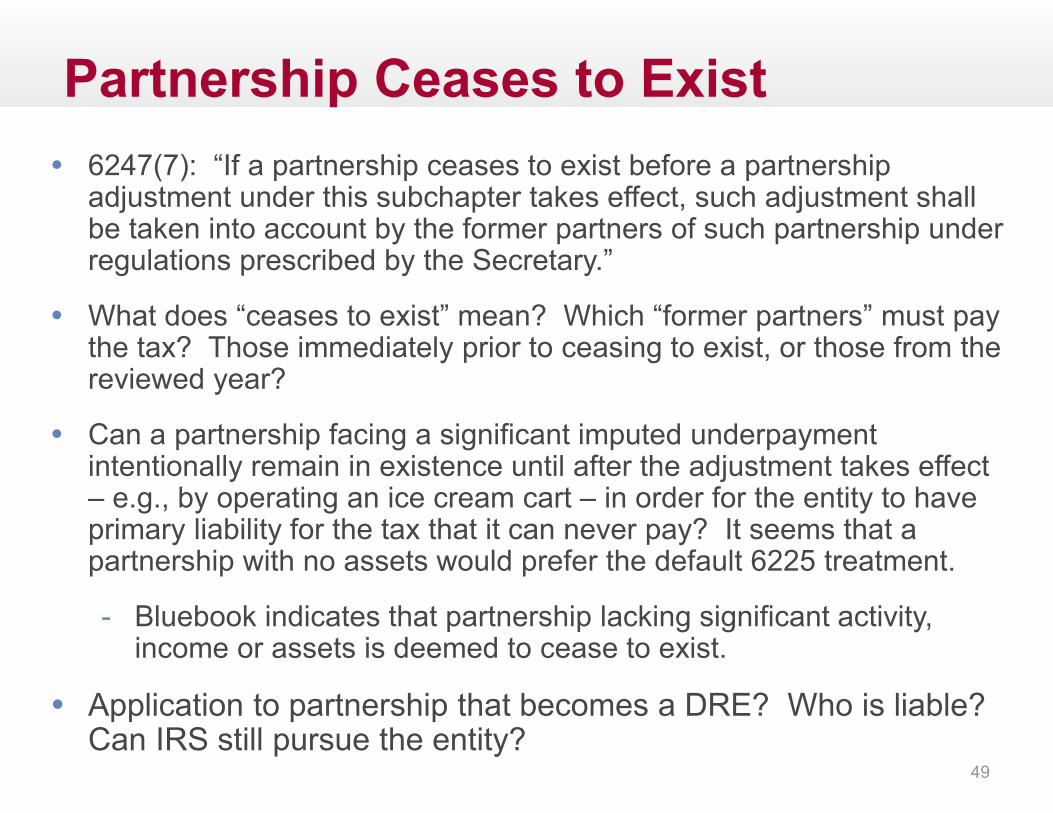

• 6247(7): “If a partnership ceases to exist before a partnership adjustment under this subchapter takes effect, such adjustment shall be taken into account by the former partners of such partnership under regulations prescribed by the Secretary.”

• What does “ceases to exist” mean? Which “former partners” must pay the tax? Those immediately prior to ceasing to exist, or those from the reviewed year?

• Can a partnership facing a significant imputed underpayment intentionally remain in existence until after the adjustment takes effect – e.g., by operating an ice cream cart – in order for the entity to have primary liability for the tax that it can never pay? It seems that a partnership with no assets would prefer the default 6225 treatment.

- Bluebook indicates that partnership lacking significant activity, income or assets is deemed to cease to exist.

• Application to partnership that becomes a DRE? Who is liable? Can IRS still pursue the entity?

Partnership Ceases to Exist

49

• Procedure to elect out of the new partnership audit rules

- If a partner is a disregarded entity and its owner is an individual, C corporation, or S corporation, or estate, can the partnership elect out?

- If a partner is a grantor trust, can the partnership elect out?

- What about S corporation partners with trusts as shareholders?

- Should every partnership with 100 or less qualifying partners elect out?

- In what circumstances would a partnership not want to elect out?

- Does the IRS have the authority to extend the election out rules to tiered partnerships?

- Can partnership with over 100 partners divide into two partnerships to qualify for election out?

Open Issues: Election to Opt-Out

50

• What are the procedures for designating a PR (on the return)?

• How frequently can a partnership change its PR designation?

• If the partnership does not designate a PR, what rules or guidelines will govern the IRS’s PR designation?

• What happens if PR requires partner consent for actions but does not receive it?

• Can partnership agreement preclude appointment of PR without partner consent? Would anyone agree to serve without partner consent and indemnification? Consider providing for no indemnification for PR unless partners consent to PR’s appointment.

• Appoint PR in Liquidation/Termination Agreement with authority to make push out election?

Open Issues: Partnership Representative

51

• What procedures will apply to reduce the Imputed Underpayment Amount by taxes paid by the partners on amended returns?

• The Imputed Underpayment Amount can be reduced if “allocable” to a tax-exempt partner, corporate partner or—in the case of a qualified dividend or capital gain—an individual. Does this refer to the partners in the Reviewed Year or the Adjustment Year?

- Note: Section 6225(c)(4)(B) refers to the partner’s distributive share in the reviewed year

• Does the Imputed Underpayment Amount take into account adjustments that result from changes to tax attributes in the years following the reviewed year? If not, how are such adjustments taken into account?

Open Issues: Imputed Underpayment Amount

52

• How will the Election to Issue Amended Statements work in a tiered setting?

- Will the election apply to a partnership tier such that the partnership is required to issue amended statements or can it pay the entity-level assessment? Will the IRS require that the first tier pay the entity-level assessment? Can an UTP even be liable for the tax? [Note that Bluebook requires UTP to pay tax.]

- What if one of the tiers from the Reviewed Year has terminated before the Adjustment Year?

- What if one of the tiers is an S corporation? Can it also make a push out election?

• How is the tax computed if the tax would decrease in the intervening years due to an adjustment to tax attributes?

• What happens if all of the reviewed year partners don’t pay?

• What if the partnership cannot locate a former partner? Retaining partner addresses, and covenants to supplement addresses, now more important.

Open Issues: Election to Issue Amended Statements

53

1. Provisions for selecting Partnership Representative and restrictions on actions taken by PR

a. Statute extensions

b. Settlements

c. Election out

d. Amended statements

e. Duty to forward notices

2. Provisions allowing or requiring an election out or a push out election

3. Escrow and indemnification provisions when partners sell their interests

4. Provisions requiring upper-tier flow-through entities to share identifying information about their owners

Impact on Partnership Governance and Partnership Agreements

54

5. Provisions regarding adjusted partner statements

a. Notice?

b. Consent of partners for reviewed year?

6. Information-sharing provisions to allow partnership to determine if ultimate owners are:

a. Corporations

b. Individuals entitled to lower capital gain and dividend rates

c. Tax exempt entities

7. Provisions specially allocating tax payments among partners

Impact on Partnership Governance and Partnership Agreements

55

• Loan Documents. Lenders likely will desire covenant to make election out or to make push out election.

• Purchase Agreements. - More due diligence? - Additional representations about partnership level taxes? - Covenants/indemnfication addressing pre-closing tax liability

imposed on the Partnership or Buyer? - Covenants to make push out election or, alternatively, that Seller

will indemnify Buyer for partnership level taxes attributable to Seller’s interest? ?

• Redemption and Dissolution Agreements – same issues. - If partnership liquidates, consider provision appointing PR for

audits occurring post-termination and procedures for push out election.

• Disclosure Documents and PPMs

Impact on Other Agreements

56

• Disclosure documents (from Shell Midstream Partners): • Risk Factor: If the IRS makes audit adjustments to our income tax returns for tax years beginning

after 2017, it may collect any resulting taxes (including any applicable penalties and interest) directly from us, in which case our cash available for distribution to our unitholders might be substantially reduced. Pursuant to the Bipartisan Budget Act of 2015, if the IRS makes audit adjustments to our income tax returns for tax years beginning after 2017, it may collect any resulting taxes (including any applicable penalties and interest) directly from us. We will generally have the ability to shift any such tax liability to our general partner and our unitholders in accordance with their interests in us during the year under audit, but there can be no assurance that we will be able to do so under all circumstances. If we are required to make payments of taxes, penalties and interest resulting from audit adjustments, our cash available for distribution to our unitholders might be substantially reduced.

• Tax Disclosure: Entity-level Audits and Adjustments. Pursuant to the Bipartisan Budget Act of 2015, if the IRS makes audit adjustments to our income tax returns for tax years beginning after 2017, it may collect any resulting taxes (including any applicable penalties and interest) directly from us. We will generally have the ability to shift any such tax liability to our general partner and our unitholders in accordance with their interests in us during the year under audit, but there can be no assurance that we will be able to do so under all circumstances. If we are required to make payments of taxes, penalties and interest resulting from audit adjustments, our cash available for distribution to our unitholders might be substantially reduced. Pursuant to this new legislation, we will designate a person (our general partner) to act as the partnership representative who shall have the sole authority to act on behalf of the partnership with respect to dealings with the IRS under these new audit procedures.

Impact on Other Agreements

57

4.02(f). Bipartisan Budget Act of 2015. For taxable years beginning after December 31, 2017 (or any earlier year, if the General Partner so elects) (i) the General Partner will be designated, and will be specifically authorized to act as, the Partnership Representative, and (ii) the Partnership Representative will apply the provisions of subchapter C of Chapter 63 of the Code, as amended by the 2015 Act (or any successor rules thereto) with respect to any audit, imputed underpayment, other adjustment, or any such decision or action by the Internal Revenue Service with respect to the Partnership or the Partners for such taxable years, in the manner determined by the Partnership Representative. For the avoidance of doubt, the Partnership Representative may (A) elect to apply the rules in subchapter C of Chapter 63 of the Code, as amended by the 2015 Act, for taxable years prior to January 1, 2018, or (B) elect to apply Section 6221(b) (if applicable) or Section 6226 of the Code or elect to file an administrative adjustment pursuant to Section 6227 of the Code, in each case as amended by the 2015 Act and in the manner determined by the Partnership Representative. Each Partner does hereby agree to indemnify and hold harmless the Partnership from and against any liability with respect to its share of any tax deficiency paid or payable by the Partnership that is allocable to the Partner (as reasonably determined by the General Partner) with respect to an audited or reviewed taxable year for which such Partner was a Partner in the Partnership (for the avoidance of doubt, including any applicable interest and penalties). The obligations set forth in this Section 4.02(f) will survive such Partner’s ceasing to be a Partner in the Partnership and/or the termination, dissolution, liquidation and winding up of the Partnership.

4.02(g) Cooperation. Each Partner will provide such cooperation and assistance, including executing and filing forms or other statements and providing information about the Partner, as is reasonably requested by the Tax Matters Partner or Partnership Representative, as applicable, to enable the Partnership to satisfy any applicable tax reporting or compliance requirements, to make any tax election or to qualify for an exception from or reduced rate of tax or other tax benefit or be relieved of liability for any tax regardless of whether such requirement, tax benefit or tax liability existed on the date such Partner was admitted to the Partnership. If a Partner fails to provide any such forms, statements, or other information requested by the Tax Matters Partner or Partnership Representative, as applicable, such Partner will be required to indemnify the Partnership for the share of any tax deficiency paid or payable by the Partnership that is due to such failure (as reasonably determined by the General Partner). The obligations set forth in this Section 4.02(g) will survive such Partner’s ceasing to be a Partner in the Partnership and/or the termination, dissolution, liquidation and winding up of the Partnership.

Atlas Growth Partners, LP

58