Embed Size (px)

Citation preview

UnderstandingPrivate Sector Development

c/o PROFIT’s Approach

June 2007 EWB Canada S.Africa LTOV QMSiavonga, Zambia || Chad Hamre, Ka-Hay Law

Hello!

What do I mean to Dorothy?

Problems…

I’m sick, underweight

and I’m dying.

Solutions

• High Mortality - What are the typical solutions?

PROFIT’s solution is different:– Understand (Value Chain Framework) and

strengthen (Market Faciliation) Zambia’s beef industry’s value chain for the benefit of both Zambia’s economic growth and increased income/security for farmers.

• To be successful, you need unique field staff skills and organizational structures.

Expectations

1. Interested in PSD and value chains2. May be applicable to your work? (technical or

Org)3. You want to pick holes in the idea.

Caveats:– Trying to make resource for EWB

– First time, questions and feedback please!

– Content rich presentation

– Relate to Beef Industry for concrete examples

Specific Objectives

1. Introduce basic PSD concepts and history.

2. Share PROFIT’s Approach to PSD

3. Highlight PROFIT’s Organizational structure,

culture and challenges.

4. Relate to your experience and focus area

Overview

Introduction 5 min

Part 1: Introduction & BIG IDEA 20 min

Part 2: The PROFIT Approach 60 min

Part 3: What’s in it for me? 20 min

Summary/Conclusion 5 min

Part I: The BIG IDEA: PSD

• “PSD is a strategy for promoting economic growth and reducing poverty in developing countries by incorporating private industry and competitive markets into a country’s overall development framework.”

• PROFIT’s rendition: Increased industry growth while assuring meaningful poverty reduction at the household level.

• What is Private Sector Development?

Important Terms

• Value Chain

• SME

• Industry

• Upgrading

• Market Facilitation

• Competitiveness

• Competitive and Comparative Advantage

Demand Supply

SUPPORTING FUNCTIONS

RULESLaws

Info

rmal

rule

s

& no

rms

Standards

Regulations

Information

Infra

stru

ctur

eRelated

services

Business membership organisations

Government

Private sector

Not-for-profit sector

Informal networks

Enabling Environment Players

VALUE CHAINInputSuppliers

Producers Wholesale Retailers

Value Chain

Value Chain Framework

Financial (cross cutting)

Financial (cross cutting)

Sector-specific providers

Sector-specific providers

Cross-cutting providers

Cross-cutting providers

ProducersProducers

Input SuppliersInput Suppliers

WholesalersWholesalers

National RetailersNational Retailers

ExportersExporters

Global RetailersGlobal

Retailers

BuyersBuyers

Global Enabling Environment

Local / National Enabling Environment

Financial (cross cutting)

Financial (cross cutting)cutting)

Financial (cross cutting)

Sector-specific providers

Sector-specific providers

Sector-specific providers

Sector - specific providers

Cross-cutting providers

Cross-cutting providers

Cross-cutting providers

Cross-cutting providers

ProducersProducers

Input SuppliersInput Suppliers

WholesalersWholesalers

National RetailersNational Retailers

ExportersExporters

Global RetailersGlobal

Retailers

BuyersBuyers

• Firms

• Linkages

• Input Markets

• Support Markets

• End Markets

• Inter-firm Cooperation (horizontal and vertical)

• Enabling Environment

Important Terms

• Value Chain– Firms, Linkages ,Input Markets, Support Markets, End

Markets, Inter-firm Cooperation (horizontal and vertical), Enabling Environment

• SME• Industry• Upgrading• Market Facilitation• Competitiveness• Competitive and Comparative Advantage

PSD Today

• 60’s: Broad regional economic strategies and implemented policy

• 70’s: Comprehensive infrastructure projects.• 80’s Competitive advantage vs. comparative only• E90’s: Business development services (BDS) • M90’s: Market facilitation to affect the value chain

minus participating.• 90’s: Micro-enterprise development

Is PSD a new concept in development?

Example and Insight.

Learning of mid nineties

+ Industry wide approach

So is PROFIT entirely innovative?

Value Chain

PROFIT APPROACH

Market Facilitation

+ =

*Innovation

Sustained Competitiveness

Part II: The PROFIT Approach

• Implementation Process• The Two Main Components

– Value Chain Framework– Market Facilitation

• Management Tools– Causal Models– Pathways

• Field Staff– Management Methodology

• Limitations

Implementation Process

Value Chain Potential and Constraints

Analysis

Intervention Targeting Analysis

Sub-sector Selection and Design Phase

Awareness Building and Commercial Relationship

Targeting

Agreements/ Contracts

Finalized and Signed

Relationship Building and Negotiation

Scale up and Exit Phase

Transactions Initiated and Monitored

Expansion and Exit

Dem

on

stra

tio

n/B

uyi

ng

D

ow

n R

isk

Ph

ase

Value Chain Framework

• Sub-sector Selection– Lead firm– High number of small holder

participation– Growth potential

• Identifying Competitive Advantage • Value Chain Analysis

– Enabling Environment– End Markets– Inter-firm Cooperation– Support Markets

• Sustaining Competitiveness

ProducersProducers

Input SuppliersInput Suppliers

Wholesalers

National RetailersNational Retailers

ExportersExporters

Global RetailersGlobal

Retailers

BuyersBuyers

ProducersProducers

Input SuppliersInput Suppliers

Wholesalers

National RetailersNational Retailers

ExportersExporters

Global RetailersGlobal

Retailers

BuyersBuyers

Speedy Analysis (BEEF)

• Sub-sector Selection– Lead firm – High number of small holder

participation– Growth potential

• Identifying Competitive Advantage

• Value Chain Analysis– Enabling Environment– End Markets– Inter-firm Cooperation– Support Markets

• Sustaining Competitiveness

Examples:

Vet Services

Outgrower model

Grades based pricing for abbattoirs

YESYES - ZAMBEEF

YESYES

Market Facilitation

• WHY: To build industry competitiveness with a strategy that:– Fosters industry and firm capacity to have effective

relationships, learn and innovate, and encourage rational flow of benefits

– Fosters a greater role for PS and more strategic role for others (gov, donors, etc.) who should not participate

• HOW:– Sequenced interventions ( ‘light touch’ buying

down risks)– Clearly defined exit strategy before entering

Market Facilitation

• Vet Service Functions– Market Research

– Identifying communities

– Linking Vet to Communities

– Business support to vet

– Shared promotional events

– Subsidized training of CLWs

– Vet networking meetings

Management/Planning Tools

• Causal Model – broad planning and donor pleasing.

• Pathway – flexible management tool to guide decision making.

The Causal Model

A causal model provides a vision of a competitive industry and the expected benchmarks along the path to competitiveness.

Impacts Outcomes Outputs Program Activities

Vision of industry competitiveness

Benchmarks

SO5: Increased Private Sector Competitiveness in Agriculture and Natural Resources

IR 1: To increase access of Small and Medium Scale entrepreneurs (SME) to markets, financial and business development services

IR 2: To enhance value added production and service technologies

PR

OF

IT P

RO

GR

AM

C

AU

SA

L M

OD

EL

Objective 1

To Improve Interfirm Cooperation in Selected Industries that Leads to

Improved Productivity and Value Addition

Objective 2

To Improve the Functioning and Responsiveness of Support Markets, that Leads to Greater Innovation and

Increased Industry Capacity to Respond to Market Dynamics

Objective 3

To Improve the Non-Policy Enabling Environment that Leads to Increased Confidence of and Credibility in Market

Mechanisms

•Increased productivity at the SH production level•Increased quality of SH production•Increased value and volume of SH production sold into selected industries•% of SHs entering structured markets•Increased overall productivity for each of the selected industries•% increased employment•Increased value of investment in selected industries

• Increased #’s of service providers being certified/trained •Increased % of SHs sales from certified/trained service providers•Increased # of SH accessing alternative disputes mechanisms•Increased # of SH accessing broad-based market information systems

•Increased value of input and output support market products and services sold to SHs and lead firms•Increased rate of adoption among SHs using improved technologies•Increased value of financial services accessed by SHs•Increased # of SHs accessing market and production information

US

AID

R

ES

UL

TS

F

RA

ME

WO

RK

PROFIT Strategic Goal: To improve the capacity of selected industries in which large numbers of micro and small enterprises (MSE) contribute and benefit to effectively compete over the near,

medium and long term.

Industry Vision

•# SH under formal contract with buyers•# abattoirs with grading/pricing system in place

•# CLW trained•# of SH receiving broadbasedmarket information•# SH accessing alternative dispute mechanisms •# transporters being certified by ZNFU

•# of CLW linked to vets•# of private vets providing services•# SH under vet contract•# of animals on vet contract•Value of Vet services sold to SH•# of Vets. promoting and informing SH via SMS•# of SH accessing auction services•# of SH accessing feedlot services•Value of auction services purchased by SHs•Value of feedlot services purchased by SHs•# of SHs animals going through feedlot services•Value of Animals sold through auction•Value of sales of animals from feedlot facilities (ZMK)•# SH accessing finance (commercial)•# SH accessing finance (value chain)•Value of financial services accessed by SH (commercial)•Value of financial services accessed by SH (value chain)•# of SH accessing non-credit financial services (insurance, savings)•Value of SH accessing non-credit financial services (insurance, savings)

OU

TP

UT

S

•# SH under formal contract with buyers•# abattoirs with grading/pricing system in place

•# SH under formal contract with buyers•# abattoirs with grading/pricing system in place

•# CLW trained•# of SH receiving broadbasedmarket information•# SH accessing alternative dispute mechanisms •# transporters being certified by ZNFU

•# CLW trained•# of SH receiving broadbasedmarket information•# SH accessing alternative dispute mechanisms •# transporters being certified by ZNFU

•# of CLW linked to vets•# of private vets providing services•# SH under vet contract•# of animals on vet contract•Value of Vet services sold to SH•# of Vets. promoting and informing SH via SMS•# of SH accessing auction services•# of SH accessing feedlot services•Value of auction services purchased by SHs•Value of feedlot services purchased by SHs•# of SHs animals going through feedlot services•Value of Animals sold through auction•Value of sales of animals from feedlot facilities (ZMK)•# SH accessing finance (commercial)•# SH accessing finance (value chain)•Value of financial services accessed by SH (commercial)•Value of financial services accessed by SH (value chain)•# of SH accessing non-credit financial services (insurance, savings)•Value of SH accessing non-credit financial services (insurance, savings)

•# of CLW linked to vets•# of private vets providing services•# SH under vet contract•# of animals on vet contract•Value of Vet services sold to SH•# of Vets. promoting and informing SH via SMS•# of SH accessing auction services•# of SH accessing feedlot services•Value of auction services purchased by SHs•Value of feedlot services purchased by SHs•# of SHs animals going through feedlot services•Value of Animals sold through auction•Value of sales of animals from feedlot facilities (ZMK)•# SH accessing finance (commercial)•# SH accessing finance (value chain)•Value of financial services accessed by SH (commercial)•Value of financial services accessed by SH (value chain)•# of SH accessing non-credit financial services (insurance, savings)•Value of SH accessing non-credit financial services (insurance, savings)

OU

TP

UT

S•Industry productivity (Overall industry sales overtime)•Employment created in beef industry•SH gross margin•Value of animals sold by SHs into commercial channels (feedlots, auctions, commercial abattoirs)•% of beef sold as choice by SHsunder vet contract •Value of investment in the beef industry (ZMK)•Vet income from SH contracts•SH yield per animal

•% cost coverage from fees and membership dues for ZNFU SMS service.•%CLW meetings skill standards audit•# of private vets organized into network

•Value of SH investment (crawls, dip tanks)•# Cattle loss among SH cattle in scheme •Calving rates among SH cattle in scheme•# New entrants providing feedlot and auction services to SHs•# New entrants providing financial services to SHs•Improved repayment rateO

UT

CO

ME

S•Industry productivity (Overall industry sales overtime)•Employment created in beef industry•SH gross margin•Value of animals sold by SHs into commercial channels (feedlots, auctions, commercial abattoirs)•% of beef sold as choice by SHsunder vet contract •Value of investment in the beef industry (ZMK)•Vet income from SH contracts•SH yield per animal

•% cost coverage from fees and membership dues for ZNFU SMS service.•%CLW meetings skill standards audit•# of private vets organized into network

•Value of SH investment (crawls, dip tanks)•# Cattle loss among SH cattle in scheme •Calving rates among SH cattle in scheme•# New entrants providing feedlot and auction services to SHs•# New entrants providing financial services to SHs•Improved repayment rateO

UT

CO

ME

S

Benchmarks

Management Tools

• Causal Models nice… but not flexible and hard to understand and guide.

• PROFIT’s Solution, the Pathway is a flexible management tool.

The Pathway

Industry Not Competitive

Competitive Industry

Demonstrate benefits of integrating smallholders into commercial channels ….

Indicator B

Indicator C

Indicator A

Indicator D

Competitiveness Indicators

Demonstration/Buying Down Risk Phase (Intervention)

Scale and Exit Phase (observation)

Intervention B

Intervention D

Intervention C

Intervention A

Actions

Actions

Actions

Actions

Actions

Pathway actions for scale, sustainability

and exit

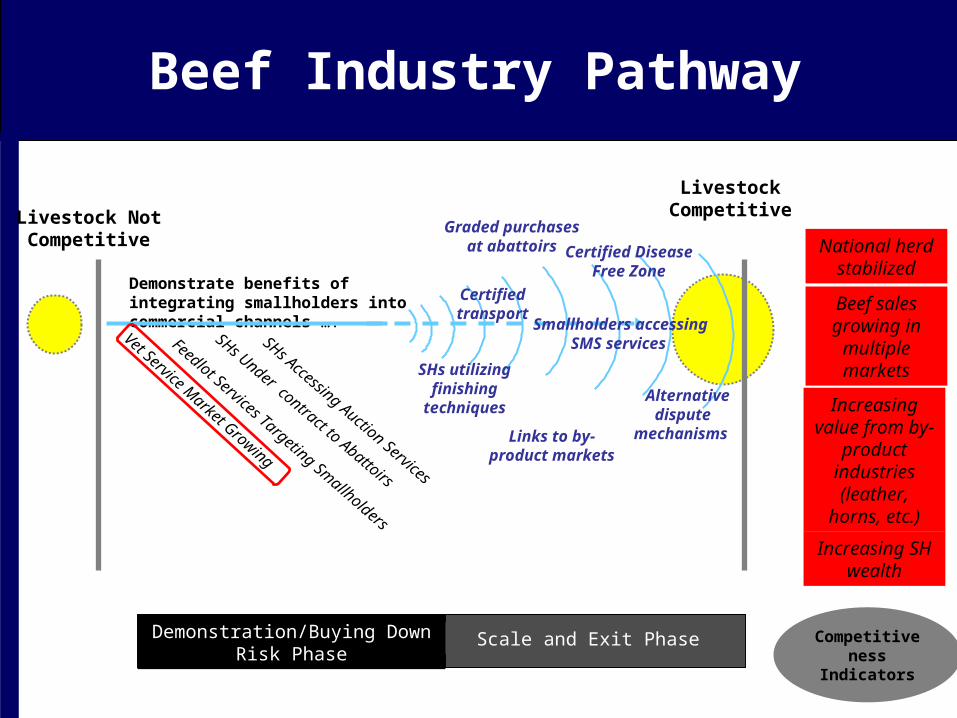

Beef Industry Pathway

Livestock Not Competitive

Livestock Competitive

Demonstrate benefits of integrating smallholders into commercial channels ….

Vet Service Market Growing

Feedlot Services Targeting Smallholders

SHs Accessing Auction Services

SHs Under contract to Abattoirs

Beef sales growing in

multiple markets

Increasing value from by-

product industries (leather,

horns, etc.)

National herd stabilized

Increasing SH wealth

Competitiveness Indicators

Demonstration/Buying Down Risk Phase

Scale and Exit Phase

Graded purchases at

abattoirs

Certified transport

Smallholders accessing SMS

services SHs utilizing finishing

techniques

Certified Disease Free Zone

Links to by-product markets

Alternative dispute

mechanisms

Vet Services Pathway

Vet Services not Competitive

Vet Services Competitive

Vets identified & HHP developed

Comm

unity identified & awareness

Services and payment delivered

Contract negotiated and signed

Demonstrate benefits of targeting smallholder market….

Diagnostic services

New AI and feed supplement services

in HHP

Financial Services

CLW Standards

Improved networking of

vets

Improved infrastructure

Better managed Vet businesses

New communities

under contract

More Animals Under Contract

New vets enter market

Increasing smallholder productivity

More Services and Providers

Competitiveness Indicators

Demonstration/Buying Down Risk Phase

Scale and Exit Phase

Field Staff

• What do field staff actually do in practice?– Market Research

– Community Organization

– Business Support

– Transaction/Relationship Facilitation

– Learning & Communicating

• Summary:(1) Coach (2) Mediator (3) Investigative Reporter

Special Field Staff Demands

1. Understand the Approach

2. Have Industry Vision

3. Organizational Culture

4. Market Facilitation Abilities

5. Learning Capture

Management Methodology

• Lean, highly skilled team

• Team Based (hierarchy alternative)

• Effective Knowledge Capture

• Continuous Staff Upgrading

The Response

Value Chain Potential and Constraints

Analysis

Intervention Targeting Analysis

Sub-sector Selection and Design Phase

Awareness Building and Commercial Relationship

Targeting

Agreements/ Contracts

Finalized and Signed

Relationship Building and Negotiation

Scale up and Exit Phase

Transactions Initiated and Monitored

Expansion and Exit

Tacit Learning Captured1. PROFIT operating culture2. Activity discussion3. Staff to staff exchanges4. Learning workshops5. Annual facilitated staff retreat

Explicit Learning Captured

1. Monthly field reports

2. Quarterly reports

3. Formal external and internal assessments

Dem

on

stra

tio

n/B

uyi

ng

D

ow

n R

isk

Ph

ase

Limitations / Challenges

• Question: What limitations do you see to this approach?

Limitations

• High road principles make for slow progress

• Limits in which sectors you can work in

• Can’t define final results

• Tempting to participate in value chain

• Vulnerable to other Donor programs

• Philosophical disagreement towards market systems and their endpoints.

PART 3: What’s in it for me?

Questions:1. What elements of PROFIT’s approach might

apply to your partner/project?• 10 min – THINK (alone or in pairs)• 15 min – SHARE (2 min each)

A few general lessons

1. Learning Learning Learning

2. Big Things, Small People

3. Failures Rock!

4. Reading and Reacting

5. Incentives

6. System Based Approach

7. Distortions

Summary

• PSD is…

• Value Chains are important because…

• Market facilitation is…and is important for PROFIT because….

• Requires excellent field staff…

• This requiring a creative management methodology…

• Maybe general lessons applicable for you…

THANKS!

Thanks.

The Value Chain, Good for

me and you!