Embed Size (px)

Citation preview

UK UPDATE AND THE IMPACT OF BREXIT

H L B N O R T H A M E R I C A N TA X C O N F E R E N C E

DECEMBER 2016

INTRODUCTION UK update and the impact of Brexit

The UK in 2016

Impact of

Brexit

UK tax round

up

THE UK IN 2016 A slice of British culture….

The y

ear

in p

ictu

res

JANUARY Part of the British rock aristocracy…

David Bowie died 10 January 2016

FEBRUARY Briton’s drinking twice as much coffee as tea

The nation’s favourite drink is under threat

Oxford and Cambridge boat race 27 March 2016

MARCH Bad weather almost sink boat race…we like talking about the weather!

APRIL Foreign Office gets a new Chief mouser

Palmerston joins Foreign Office on 13 April 2016

MAY Biggest upset in Premiership sporting history

Leicester city won the Premiership title

JUNE UK votes to leave the EU

EU referendum on 23 June 2016

JULY The second of the Queen’s two birthday parties

The Queen had official 90th birthday

AUGUST Harry Potter grows up…

New Harry Potter book is released

SEPTEMBER New five pound note is impossible to tear and can survive the wash

First polymer bank note enters circulation

OCTOBER Britain goes mad for cake

The Great British Bake Off final

NOVEMBER The UK gets Trumped…

The agenda changes on the 8 November

BREXIT Hard or soft it’s going to be painful

Planning to formally leave the EU in 2019

BREXIT IMPLICATIONS Moving forward

L

ea

vin

g th

e E

U

• Referendum on 23 June 2016

• Uncertainty persists

• Plan to trigger Article 50 in March 2017

• Leave the EU by April 2019

• Many questions and hurdles

• Tax implications

• Some good, some bad and some ugly…

SIZE OF THE UK MARKET Total market value of all final goods and services produced in a year (GDP)

Country GDP Ranking 2016 Size ($ bn)

United States 1 18.5

China 2 11.4

Japan 3 4.7

Germany 4 3.5

UK 5 2.7

France 6 2.5

India 7 2.3

Italy 8 1.9

Brazil 9 1.8

Canada 10 1.5

1. DIRECT TAXES The good…

Direct tax rules must

comply with EU treaty freedoms

No restrictions on UK rates

or rules

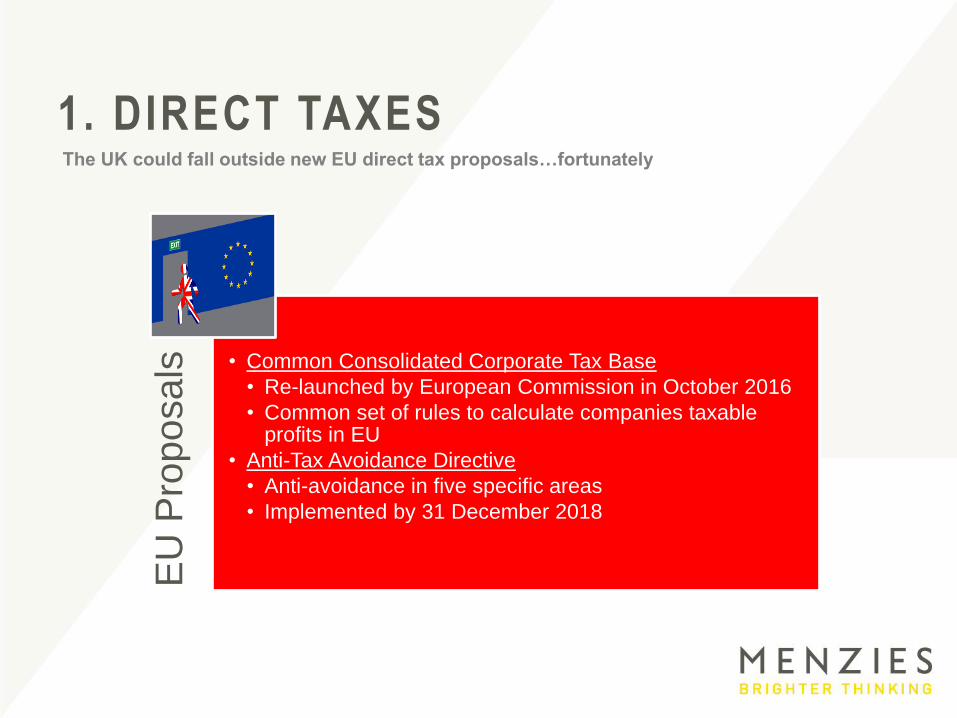

1. DIRECT TAXES The UK could fall outside new EU direct tax proposals…fortunately

E

U P

rop

osa

ls

• Common Consolidated Corporate Tax Base

• Re-launched by European Commission in October 2016

• Common set of rules to calculate companies taxable profits in EU

• Anti-Tax Avoidance Directive

• Anti-avoidance in five specific areas

• Implemented by 31 December 2018

2. STATE AID The good…

State aid restrictions

UK can provide

targeted tax incentives

2. STATE AID The good…

Research and Development Patent Box Investment Share ownership Growth

3. EU DIRECTIVES The bad…

Access to EU

Directives

Reliant on tax treaties

3. HOLDING COMPANY STRUCTURES The bad…

US

UK

Germany

Ireland

France

Dividends

Interest

Royalties

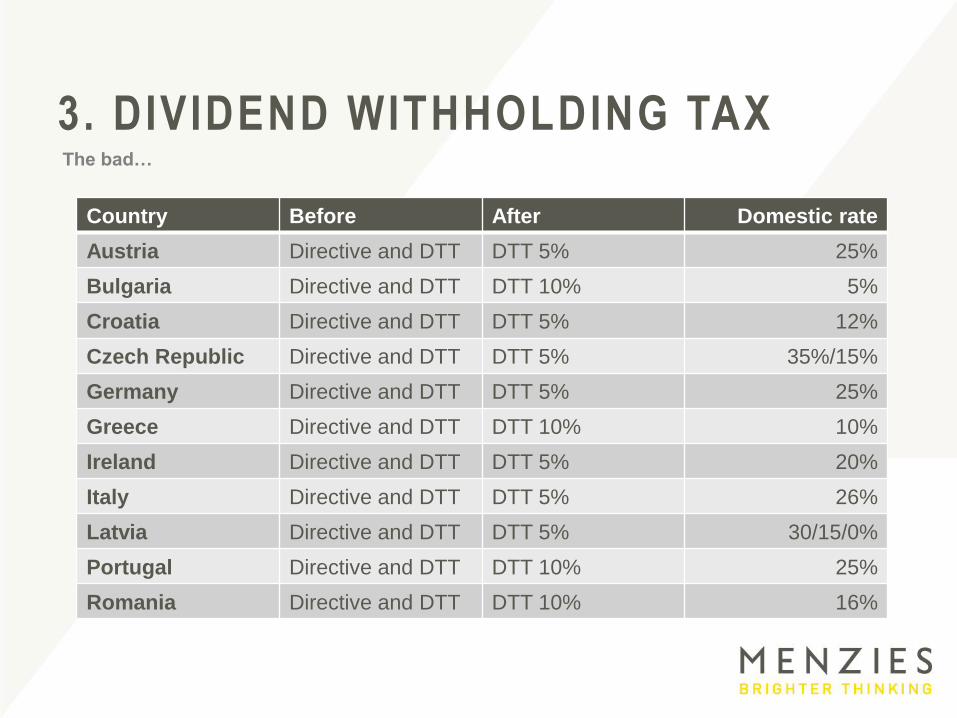

3. DIVIDEND WITHHOLDING TAX The bad…

Country Before After Domestic rate

Austria Directive and DTT DTT 5% 25%

Bulgaria Directive and DTT DTT 10% 5%

Croatia Directive and DTT DTT 5% 12%

Czech Republic Directive and DTT DTT 5% 35%/15%

Germany Directive and DTT DTT 5% 25%

Greece Directive and DTT DTT 10% 10%

Ireland Directive and DTT DTT 5% 20%

Italy Directive and DTT DTT 5% 26%

Latvia Directive and DTT DTT 5% 30/15/0%

Portugal Directive and DTT DTT 10% 25%

Romania Directive and DTT DTT 10% 16%

4. EMPLOYEE MOBILITY The ugly…

EU social security

contributions system

Potential for multiple social

security contributions

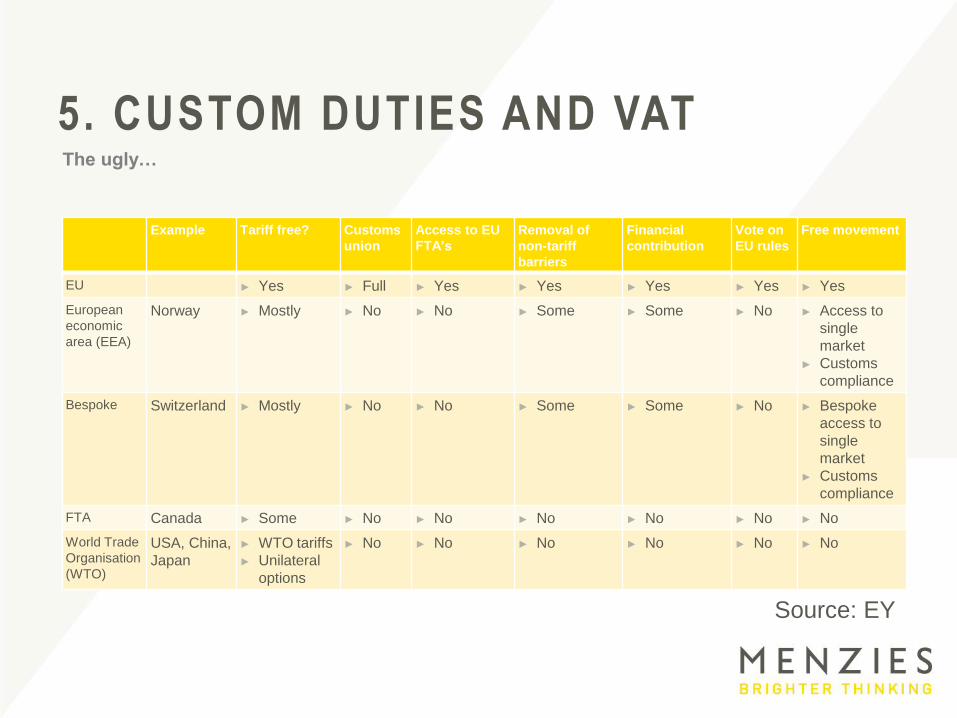

5. CUSTOM DUTIES AND VAT The ugly…

Free trade system

Potential for trade

tariffs and restrictions

5. CUSTOM DUTIES AND VAT The ugly…

Example Tariff free? Customs

union

Access to EU

FTA’s

Removal of

non-tariff

barriers

Financial

contribution

Vote on

EU rules

Free movement

EU ► Yes ► Full ► Yes ► Yes ► Yes ► Yes ► Yes

European

economic

area (EEA)

Norway ► Mostly ► No ► No ► Some ► Some ► No ► Access to

single

market

► Customs

compliance

Bespoke Switzerland ► Mostly ► No ► No ► Some ► Some ► No ► Bespoke

access to

single

market

► Customs

compliance

FTA Canada ► Some ► No ► No ► No ► No ► No ► No

World Trade

Organisation

(WTO)

USA, China,

Japan

► WTO tariffs

► Unilateral

options

► No ► No ► No ► No ► No ► No

Source: EY

HOW TO PREPARE FOR BREXIT Evaluating your existing structures and operations

Key questions that need to be addressed

BREXIT RISKS AND OPPORTUNITIES Preparing the groundwork for change

UK entity

Trade

Employment

Finance Taxation

Operational

TRADING RELATIONSHIP Supply of goods or services to and from the EU

UK businesses that buy or sell goods within the EU are likely to suffer increased costs and administration if the UK leaves the Single Market (i.e. so called ‘hard Brexit’). This is because goods moving between the UK and EU would become subject to Customs procedures and the simplified VAT rules for intra-community trade would be lost. Those that supply services will also need to consider the new regime and any access restrictions or new regulations that may apply.

• What trade relationships do you have with customers or suppliers in the EU (or other countries with which the EU has trade agreements)?

• How dependent is your business and supply chain on the movement of goods between the UK and EU or other countries with which the EU has trade agreements?

• What impact would a hard Brexit have on your business and how could you minimise the impact?

• Is your business dependent on a particular regime e.g. passporting, to access the EU services markets (or markets of other countries with which the EU has trade agreements)?

• What will be the most efficient model for your business post Brexit and should you consider setting up operations somewhere within the EU?

• What other markets outside of the EU might be fruitful ones with attractive existing trade agreements?

EMPLOYMENT The free movement of workers is a founding principle of the EU

The free movement of workers has been a significant factor in the UK’s decision to leave the EU. As a result it can certainly be anticipated that there will be a people impact arising from Brexit.

• How reliant is your business on the free movement of EU workers across EU borders?

• What individuals do you have working in critical roles outside their home country?

• Will your ability to recruit staff be affected and do you need to reassess your recruitment and/or training policies?

• Is Hard Brexit likely to lead to a skills shortage in your industry and so drive up costs?

• What employee communication and engagement is appropriate?

FINANCE AND ACCOUNTING Cashflow, business plans and remodelling considerations

As with all change, it can be expected that there will be some winners and losers post Brexit. For some there may be cash flow impacts, perhaps arising from reduced consumer spending and higher costs, and therefore it is important to review your existing business plan and consider remodelling it for possible Brexit scenarios.

• How robust is your cash flow and have you stress tested liquidity by reviewing your working capital needs?

• What impact does forex movement have on your business and is it possible to mitigate on-going currency volatility?

• How do you determine your export pricing and commitments while sterling is weak knowing it might get stronger in the future?

• What is the timing of future capital expenditure and what are the costs and benefits of this investment?

• What are the terms of your existing bank facility, and could these need to be amended or renegotiated?

• With tighter lending criteria, what alternative sources of funding may be available to the business?

• Do you have grants or other funding sources from the EU?

• How are asset valuations likely to be affected in the year end financial statements?

TAXATION Direct taxes have always been the responsibility of individual member states

Direct taxes (corporation tax and income tax) have been left a bit in the shadows of indirect taxes, but companies may still be affected by changes in this area.

• How reliant is your business on the EU Tax Directives and how do these reduce your cost of doing business?

• What relief will be available in the future under bilateral double tax treaties?

• Should you repatriate profits from EU subsidiaries pre Brexit?

• What is your tax operating model and will you need to review your transfer pricing policy?

• What benefits could arise from a restructuring or remodelling of the group?

• How do EU rules currently affect workers social security contributions?

OPERATIONAL At the heart of all businesses are the relationships with customers and suppliers

Although there is still much uncertainty over the impact of Brexit, it is important to take time to assess the economic viability of the commercial relationships as they are the life blood for the business

• What is your contractual position with critical customers and suppliers?

• How are your customers and suppliers likely to be affected by Brexit, and what impact could this have on your business?

• Do you need to consider diversification of the supply chain and customer base and reassess supplier dependency?

• Would a strategic acquisition address structural changes or opportunities in the market?

• What are your terms of trade and should you revise aspects such as credit terms, cash collection and invoice settlement policies?

• Do you transfer customer (or employee) data between the UK and EU?

• Should you establish a Brexit response committee to monitor the on-going risks and opportunities for the business?

UK TAX ROUND UP Up date for US tax advisers

L

ea

vin

g th

e E

U

• BEPS

• People of Significant Control

• Residential property taxes

• Corporation tax

BEPS The UK has been a strong supporter of BEPS

UK is an early adopter of BEPS measures

2

BEPS Action OECD Recommendation UK implementation Corporate response

1: Digital Economy Countries may choose to adopt a range of

unilateral measures.

UK introduced Diverted Profit Tax (DPT) but

wider than just digital sector.

Large multinational groups should

review DPT rules.

2: Hybrid Mismatches Adopt rules to deny tax advantages arising

from hybrid instruments and entities.

New hybrid mismatch legislation will apply

automatically from 1 January 2017.

Review mismatch transactions

between UK and other jurisdictions.

3: Controlled Foreign

Companies

Introduce / strengthen CFC rules. Existing CFC rules expected to remain,

exemptions may come under scrutiny.

Continue to apply existing rules.

4: Interest and other

financial payments

Restriction on deductibility of interest

expense and similar payments.

Tax deductibility of corporate interest to be

set at 30% of EBITDA from 1 April 2017.

Consider if net UK interest expense

exceeds de minimis threshold of £2m.

5: Harmful tax

practices

Preferential tax regimes, particularly

Intellectual Property (IP) regimes, to be

amended.

Patent Box has been revised from 1 July

2016 to include an R&D nexus approach.

Review IP assets and R&D

expenditure carried out by company.

6: Tax treaty abuse Amend tax treaties to prevent treaty shopping

and abuse.

Treaty changes may arise. Extended

withholding tax regime for royalties from July

2016.

Review cross-border royalty payments

and impact of new rules.

7: Permanent

Establishments (PE)

PE rules to be tightened resulting in lowering

of threshold to create tax presence.

UK likely to adopt lower threshold and

already introduced Diverted Profit Tax.

Assess any changes to PE risk for

overseas activities.

8 to 10: Transfer

pricing

Extensive changes focused on value creation

and aligning substance with profits.

New guidelines will be enacted into UK law

when finalised.

Review existing transfer pricing

arrangements against new guidelines.

11: Economic analysis

of BEPS

Measuring and monitoring of BEPS to show

impact of proposals.

HMRC to collect data to assess impact of

BEPS.

No response necessary.

12: Mandatory

disclosure regimes

Disclosure of abusive transactions,

arrangements and structures.

UK already has suitable disclosure rules. No change to existing rules.

13: Transfer pricing

(documentation)

Master file, local files and Country-by-

country-reporting (CBCR) obligations.

UK an early adopter of CBCR for periods

commencing from 1 January 2016.

UK CBCR required where worldwide

group turnover exceeds €750m.

14: Tax dispute

resolution

Minimum standards to improve tax dispute

resolution under Mutual Agreement

Procedures.

UK committed to mandatory binding

arbitration.

No response necessary.

15: Multilateral

instrument

Adopt multinational instrument to implement

treaty based BEPS outcomes.

No action until multinational instrument ready

for signing by end of 2016.

No response necessary.

PEOPLE OF SIGNIFICANT CONTROL Movement towards increased transparency…

Public disclosure of ownership of UK businesses

RESIDENTIAL PROPERTY Plenty of changes to get to grips with…

Taxes are starting to affect the UK property market

ENVELOPED DWELLINGS Significant tax costs to putting a wrapper around residential property

Enveloped Dwellings

15% SDLT on

properties > £500,000

28% CGT

Annual Charge

ANNUAL TAX ON ENVELOPED DWELLING ATED is not cuddly…

Property value 2016/17

£500,000 - £1m £3,500

£1m - £2m £7,000

£2m - £5m £23,350

£5m - £10m £54,450

£10m - £20m £109,050

£20m+ £218,200

Various reliefs apply from annual charge. Must claim on ATED return.

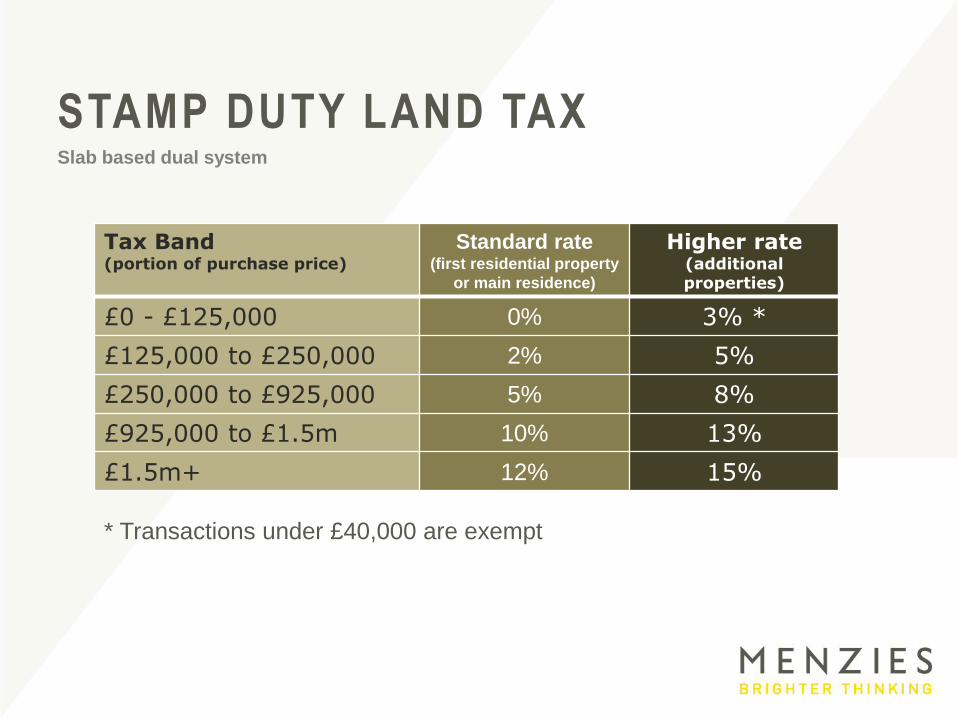

STAMP DUTY LAND TAX Slab based dual system

Tax Band (portion of purchase price)

Standard rate (first residential property

or main residence)

Higher rate (additional properties)

£0 - £125,000 0% 3% *

£125,000 to £250,000 2% 5%

£250,000 to £925,000 5% 8%

£925,000 to £1.5m 10% 13%

£1.5m+ 12% 15%

* Transactions under £40,000 are exempt

CORPORATION TAX How low can it go…

17% in 2020

CONCLUSION Uncertain times but must try to…

Menzies confidentiality statement This proposal is commercial in confidence. Its contents are the property of Menzies LLP and may not be circulated without our permission. The content of this

proposal is intended to provide general guidance and information about the services provided by Menzies LLP. The information does not constitute

professional advice and should not be relied upon as such. Menzies LLP accepts no responsibility for the consequences of any action taken or not taken in

reliance on the information contained in this proposal.

Whilst we make every effort to ensure that the content of this proposal is accurate and up to date, legislation is subject to change and Menzies LLP makes no

representation or warranty regarding the accuracy or reliability of the information in this proposal, after the date of submission.

For a full selection of legal notices, including registration numbers and registered office locations, professional indemnity insurance and The Bribery Act,

please see our website www.menzies.co.uk/en/legal-notice