Embed Size (px)

Citation preview

1

UK CONSTRUCTIONMARKET VIEWSPRING 2018

MARKET VIEW | SPRING 2018

1

MARKET VIEW | SPRING 2018

REACHING A TURNING POINT

• Little has moved in the Brexit negotiations, but with just seven months until the negotiation deadline, we are close to entering a ‘no deal’ environment.

• A ‘no deal’ Brexit carries both tariff and non-tariff barriers that present cost and time risks to UK construction.

• Carillion’s failure has had a material impact on industry capacity and poses a contagion threat to the financial stability of thousands of suppliers.

• Further focus on payment practice and supply chain profitability will also affect cost levels and industry capacity.

• Recommendations from The Hackitt Review in Spring 2018, which is assessing the effectiveness of current building and fire safety regulations and related compliance and enforcement issues in multi occupancy high rise residential buildings, are expected to have a material impact on construction demand and cost.

REACHING A TURNING POINT

2

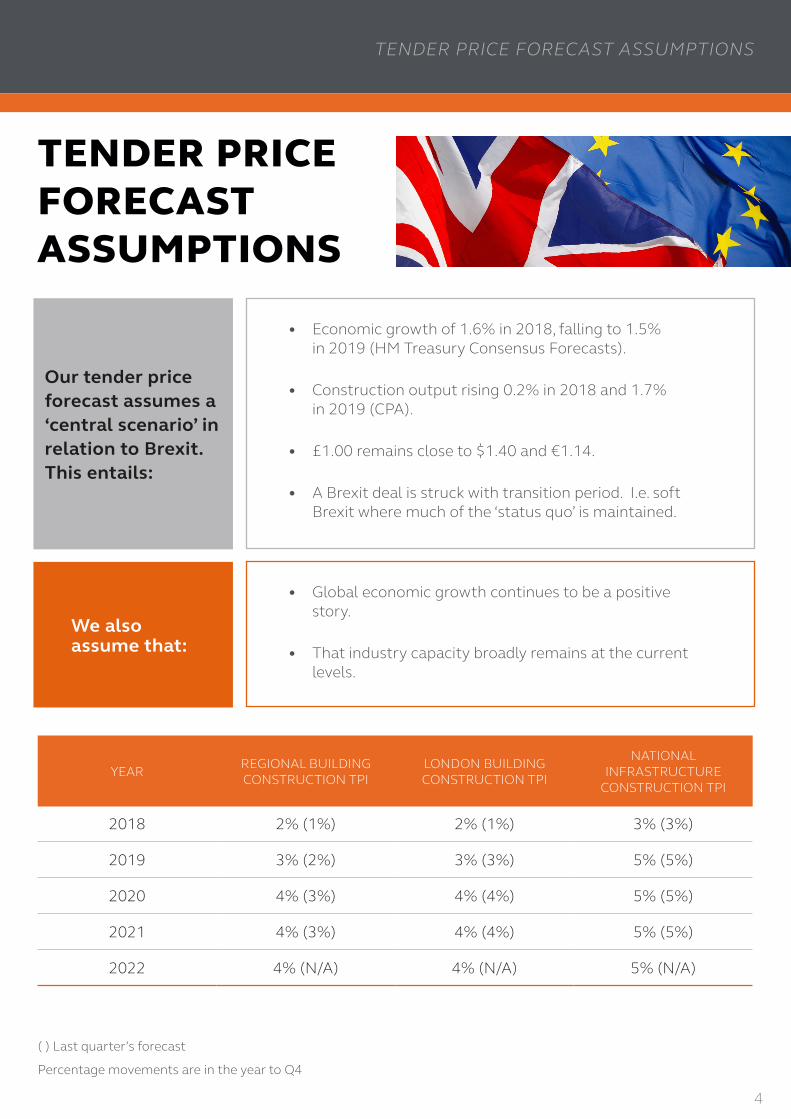

We have increased our tender price forecast for buildings markets, both regionally and for London. We have not made any changes to our infrastructure forecast. Our previous forecast is shown in brackets in the tender price forecast table below. The main factors considered in our revised forecast are as follows:

INFLATIONARY FACTORSMaterials costs. Though sterling has strengthened relatively against the dollar, it remains weak against the euro. Materials cost inflation continues to be aggressive with rates across all materials of 5-6% in the year holding up. Currency-linked packages where the whole subcontract is sourced from the EU see even higher levels of cost pressure.

Labour costs. The market remains very busy and capacity severely constrained. There is now a growing body of evidence to suggest that the number of EU workers in UK construction is falling. The skills shortage is not improving, which is leading to continued labour cost inflation of at least 3% per annum.

Capacity. Capacity to deliver in the market remains constrained. This is particularly pertinent in hot regional markets, such as Manchester, or on projects where complexity and scale leads to a smaller available pool of expertise.

Supply chain profitability. Tempered tender price growth and high input cost growth has squeezed supplier margins. This has negatively impacted profitability in the supply chain, which was only just recovering from the great recession of 2008. Last year, the average margin for the top ten main contractors was

-0.5%. Even across the top 100 main 2-3% of contractors, the average margin was around 2%. As a result, the ability for the supply chain to reduce or hold pricing is very constrained.

Supply chain fragility. Supplier fragility has also further contributed to existing capacity constraints. The failure of suppliers and loss of ‘organised capacity’ will have a tangible impact on competitive tension and therefore pricing. This issue is not limited to Carillion however, with some other suppliers in special measures, such as Interserve. The Carillion liquidation is explored in more detail later in this paper.

Risk. Events surrounding Carillion are likely to impact levels of trust and transparency in the whole sector. As a result, we anticipate that the attitude to risk will generally harden. For much of the supply chain it is likely this will manifest itself as higher prices. Additionally, the timetable of Brexit now means that the supply chain are pricing projects that will commence on site after the Brexit deal has been made. However, because they are pricing them with no visibility of what the Brexit deal will be and therefore what the operating environment will be, they are likely to factor this into the price as a risk allowance.

Hackitt Review. The independent Hackitt review was commissioned last July following the Grenfell tragedy. It is widely anticipated that recommendations from the review will

TENDER PRICE FORECAST

REACHING A TURNING POINT

MARKET VIEW | SPRING 2018

3

focus on design and performance risks of complex buildings – particularly residential high rise. It is likely that key areas for attention will include sprinkler systems, means of escape and cladding together with building regulations approval and assurance processes. In our view, in addition to the additional costs that arise from essential changes introduced by the report, the review will have a wider inflationary effect partly as a result of an increased volume of work and also as a reflection of the greater risk associated with complex buildings.

DEFLATIONARY FACTORSEconomic performance. The deep uncertainty associated with Brexit has undoubtedly had an adverse impact on the pace of economic growth in the UK. The UK economy grew 1.8% in 2017, the slowest growth rate since 2012. The potential for global growth taking off presents upside for British exporters. That

said, the Office of Budget Responsibility forecast growth of 1.5% or under per annum to 2022. Historically, construction demand has been less buoyant with weaker economic growth.

Uncertainty impacting demand levels. Significant downside risks to future demand levels remain. The private commercial sector saw a gradual decline in output across the quarters of 2017, as did the public sector. Uncertainty is hampering investment decisions in a number of key commercial sectors, such as offices. Additionally, the government budget deficit targets continue to constrain any potential for expansion of public spending. The potential for faster and higher interest rate rises may also threaten continued growth in the private residential market. The nature of the Brexit deal will continue to be a pivotal factor in the future outlook for all construction sectors, but particularly those relying on private, and speculative, investment.

0

5,000

10,000

15,000

20,000

25,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4Q1 Q2 Q3 Q4Q1 Q2 Q3 Q4Q1 Q2 Q3 Q4Q1 Q2 Q3 Q4

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Volu

me

(£m

) Sea

sona

lly

Adju

sted

PRIVATE COMMERCIAL PRIVATE INDUSTRIAL PUBLIC SECTOR

INFRASTRUCTURE PRIVATE RESIDENTIAL PUBLIC RESIDENTIAL

UK CONSTRUCTION OUTPUT (ONS)

TENDER PRICE FORECAST ASSUMPTIONS

4

• Economic growth of 1.6% in 2018, falling to 1.5% in 2019 (HM Treasury Consensus Forecasts).

• Construction output rising 0.2% in 2018 and 1.7% in 2019 (CPA).

• £1.00 remains close to $1.40 and €1.14.

• A Brexit deal is struck with transition period. I.e. soft Brexit where much of the ‘status quo’ is maintained.

• Global economic growth continues to be a positive story.

• That industry capacity broadly remains at the current levels.

TENDER PRICE FORECAST ASSUMPTIONS

YEAR REGIONAL BUILDING CONSTRUCTION TPI

LONDON BUILDING CONSTRUCTION TPI

NATIONAL INFRASTRUCTURE

CONSTRUCTION TPI

2018 2% (1%) 2% (1%) 3% (3%)

2019 3% (2%) 3% (3%) 5% (5%)

2020 4% (3%) 4% (4%) 5% (5%)

2021 4% (3%) 4% (4%) 5% (5%)

2022 4% (N/A) 4% (N/A) 5% (N/A)

Our tender price forecast assumes a ‘central scenario’ in relation to Brexit. This entails:

We also assume that:

( ) Last quarter’s forecast

Percentage movements are in the year to Q4

MARKET VIEW | SPRING 2018

5

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

150

200

250

300

350

Carillion were the second largest Tier 1 contractor in the UK directly employing 20,000 people in the UK.

Their 2016 construction turnover was £1.5bn and in 2016 they reported a construction order book of £2.5bn with further pipeline of construction contract opportunities of £12.5bn.

The company experienced financial difficulties in 2017, and went into compulsory liquidation on 15 January 2018, the most drastic procedure in UK insolvency law. The insolvency has caused project shutdowns, job losses - 989 UK redundancies up to 12 February 2018 - and potential financial losses to Carillion’s 30,000 suppliers and 28,500 pensioners.

It has also led to questions and parliamentary enquiries about the conduct of the firm’s directors and auditors, and about the UK Government’s relationships with major suppliers working on Private Finance Initiative (PFI) schemes and other privatised provision of public services.

In our view, Carillion’s failure is an inflection point in the industry and will materially change commercial dynamics, including pricing behaviours, for the foreseeable future.

CARILLION

ARCADIS TENDER PRICE INDICES MARCH 2018 INDEX BASE 1985=100

REGIONAL BUILDING CONSTRUCTION TPI LONDON BUILDING CONSTRUCTION TPI NATIONAL INFRASTRUCTURE CONSTRUCTION TPI

FORECAST

CARILLION

6

INDUSTRY CAPACITY

Carillion’s liquidation will impact levels of competitive tension as there will be less ‘organised capacity’ to respond to market opportunities. There will be a large amount of retendering opportunities coming back to the market as a result of Carillion’s £2.5bn order book combined with the need to complete projects where Carillion’s involvement has been terminated.

SHORT TERM

INDUSTRY SOLVENCY

It is reported that Carillion owe £1bn to their supply chain, either as retentions or payments. Subcontractors owed money by Carillion will be treated as ‘unsecured creditors’, a term used to describe those with no assets secured against their debt. The status of unsecured creditor places these companies at the bottom of the pecking order when it comes to receiving repayment as part of the liquidation process. Failure to recover monies owed is likely to spread the contagion of insolvency. Small firms are owed an average of £141,000, with one firm reporting that Carillion owes it £800,000. Medium-sized businesses are owed an average of £236,000, with the largest debt in this category totalling £1.4m.

SHORT TERM

WHAT ARE THE IMPACTS OF THE FAILURE OF CARILLION?

MARKET VIEW | SPRING 2018

7

WHAT ARE THE IMPACTS OF THE FAILURE OF CARILLION? (CONTINUED)

RISK ALLOCATION & COMMERCIAL BEHAVIOURS

The failure of Carillion will accelerate the adoption of more prudent commercial behaviours and a hardening of attitudes towards risk. This is likely to be an inflationary force on prices. Governance models on projects and within contracting organisations will also come under a greater level of focus and the reliability of financial indicators that have historically been relied upon may be called into question.

SHORT TERM

INDUSTRY REPUTATION

The high-profile nature of Carillion’s failure has highlighted deeply-rooted problems in the industry. The news of mass job losses and negative assessments of the construction industry will likely put off potential recruits, disappoint the public and reinforce some traditional negative stereotypes and lead to review of how the government does business with the UK construction industry.

LONG TERM

INDUSTRY CHANGE

The scale of Carillion’s failure has reinvigorated already well-developed debates about the need for industry change. Many of the issues that negatively affected Carillion are impacting the wider supply chain, and it is clear that industry business models are not fit for a sustainable future. The failure of Carillion is likely to act as a catalyst for further change in how the industry does business and manages risk. This is likely to include increased focus on payment practices and whether contractors can trade on project cashflows alone.

LONG TERM

CARILLION

8

QUANTIFY SUPPLY CHAIN EXPOSURE

It may be prudent for clients to undertake a review of their supply chain to understand how exposed to Carillion any key suppliers are. There may be actions clients can take to support affected suppliers and mitigate any elevated risk of supplier failure.

SHORT TERM

REVIEW DUE DILIGENCE PROCESSES

Processes aimed at providing assurance around financial risk and governance may need to be reviewed to ensure they are as robust as possible, and importantly, being followed.

SHORT TERM

SUPPORT ELIMINATION OF AVOIDABLE RISK & RISK

TRANSFER

Clients may review what risk is transferred to the supply chain and how. There may be a greater focus on transparency of risk management and increased push earlier on in projects around eliminating avoidable risks. Furthermore, clients have a role in mitigating risk through the provision of good quality design solutions and avoidance of change.

LONG TERM

REVIEW PAYMENT PRACTICES

Clients may review their payment processes to ensure that they are not unduly exposed to work in progress and title on materials. However, the importance of fair and prompt pay practices has been highlighted again and clients may review wider project payment processes to ensure that they are aligned to progress on site and support the supply chain’s financial health, enabling cash to reach lower tiers of the supply chain within a reasonable timescale.

LONG TERM

WHAT ACTIONS MIGHT CLIENTS CONSIDER TAKING IN RESPONSE?

CONTACTWILL WALLERMARKET INTELLIGENCE LEAD

SIMON RAWLINSONHEAD OF STRATEGIC RESEARCH & INSIGHT

SIMON LIGHTUK CLIENT DEVELOPMENT DIRECTOR

WWW.ARCADIS.COM

@ArcadisUK

Arcadis United Kingdom

Arcadis

Our world is under threat - from climate change and rising sea levels to

rapid urbanisation and pressure on natural resource. We’re here to answer

these challenges at Arcadis, whether it’s clean water in Sao Paolo or

flood defences in New York; rail systems in Doha or community homes

in Nepal. We’re a team of 27,000 and each of us is playing a part.

Arcadis. Improving quality of life.

Disclaimer

This report is based on market perceptions and research carried out by

Arcadis, as a design and consultancy firm for natural and built assets. It is for

information and illustrative purposes only and nothing in this report should be

relied upon or construed as investment or financial advice (whether regulated

by the Financial Conduct Authority or otherwise) or information upon which

key commercial or corporate decisions should be taken. While every effort

has been made to ensure the accuracy of the material in this document,

neither the Centre for Economics and Business Research Ltd nor Arcadis will

be liable for any loss or damages incurred through the use of this report.

© 2017 Arcadis

![# Content Form Name 1 Assets B10A - Assets...B10E - Liabilities (Branch) 1. Balance Sheet Statement [Statement of Financial Position] 1.2 Liabilities Line Item Amount Financial liabilities](https://img.dokumen.tips/doc/110x75/60ae59b6f0c1ae5d2b3584b4/-content-form-name-1-assets-b10a-assets-b10e-liabilities-branch-1-balance.jpg)