Embed Size (px)

DESCRIPTION

A Research coonducted on UBL credit policies BY GCUF students.."The Regents & Stallwart's"

Citation preview

1 | P a g e

DEDICATION Words are looking to express obligations to our affectionate parents and teachers for

their love, good, wishes, inspirations, motivation, has enabled us to reach this stage.

We remember their unceasing prayers without which the present destination would

have been mere a dream.

2 | P a g e

Table of Contents

DEDICATION ........................................................................................................................................ 1

ACKNOWLEDGEMENT ....................................................................................................................... 4

Executive Summary .............................................................................................................................. 6

CHAPTER NO.1 ................................................................................................................................... 7

1.1 Overview of Credit Analysis and Investment Banking:- .......................................................... 7

Introduction ........................................................................................................................................ 7

Definition ............................................................................................................................................ 7

Why Credit Score Analysis is Important? ....................................................................................... 8

1.2 Importance of Credit Analysis of Individual Borrowers............................................................ 9

1.4 Investment banking ................................................................................................................. 9

CHAPTER NO.2 ................................................................................................................................. 12

2.1 Banking History:- ...................................................................................................................... 12

2.2 United Bank Limited: .................................................................................................................... 12

2.2.3 Functions of UBL: .................................................................................................................. 14

2.2.4 Role of UBL in Banking Sector:............................................................................................ 15

2.2.5 Computerization of UBL:....................................................................................................... 15

2.2.6 Credit Department of UBL: ................................................................................................... 16

CHAPTER NO.3 ................................................................................................................................. 18

“NIMRA TEXTILE LIMITED” .............................................................................................................. 18

3.1 Financial analysis:- ................................................................................................................... 20

“CREDIT POLICY AND ITS IMPLEMENTATION” ....................................................................... 30

Credit Policy: ............................................................................................................................... 30

Procedure for Financing from UBL ............................................................................................ 30

3.3.2.1 Purpose: .......................................................................................................................... 30

3.3.2.2 Business .......................................................................................................................... 30

3.3.2.3 Security: .......................................................................................................................... 30

CHAPTER NO.5 ................................................................................................................................. 33

3 | P a g e

“CREDIT PRINCIPLES AND OTHER REQUIREMENTS” .......................................................... 33

5.1 The 5 C’s of Credit.................................................................................................................... 35

5.2 SWOT Analysis:- ...................................................................................................................... 38

5.2.1 A strength could be: .......................................................................................................... 38

5.2.2 A weakness could be: ....................................................................................................... 39

5.2.3 An opportunity could be: ................................................................................................... 39

5.2.4 A threat could be: .............................................................................................................. 39

5.3 PEST Analysis: ......................................................................................................................... 40

5.3.1 Political Factors ..................................................................................................................... 40

5.3.2 Economic Factors .................................................................................................................. 41

5.3.3 Sociocultural Factors ............................................................................................................ 41

5.3.4 Technological Factors ........................................................................................................... 41

5.4 Porter’s Five Force Analysis: ............................................................................................... 43

5.4.1 The threat of entry. ................................................................................................................ 43

5.4.2 The power of suppliers. ........................................................................................................ 44

5.4.3 The threat of substitutes ....................................................................................................... 44

5.4.4 Competitive Rivalry ............................................................................................................... 45

5.5 Macro-economic risk areas ..................................................................................................... 45

5.6 Micro-economic risk areas: ...................................................................................................... 46

5.7 Rules followed by the bank for Credit Risk Management: .................................................... 46

CHAPTER NO.6 ................................................................................................................................. 49

Differences and Similarities in theoretical and practical approach ............................................. 49

CHAPTER NO.7 ................................................................................................................................. 52

“Conclusion and Recommendation” .............................................................................................. 52

4 | P a g e

ACKNOWLEDGEMENT All praise to Almighty Allah, the most Gracious and compassionate. Who created the

universe and bestowed mankind with the knowledge and blessings of Allah be upon the

Holy Prophet Muhammad (S.A.W.) who guided mankind with the Holy Quran and

Sunnah, the everlasting source of guidance and knowledge for humanity.

It is an utmost pleasure to be able to express to heartiest gratitude and deep sense of

devotion to our reverend and worthy supervisor respected SIR Syed Ahmed Gillani; who guide us to achieve this goal. We also like to thank Engr. Saqib Hassan Minhas

(Regional Head of Credit Admin Deptt), Mohammad Shahzaib (processing manager),

Asad Rasool (Credit Admin Officer) of UBL who gave us their precious time and

provide us data and information.

Place: Faisalabad

5 | P a g e

Signatures of Participants of Project

Group Leader

Farman Ali 454

Group Members

Javaria Iqbal (302)

Muhammad Usman Virk (327)

Mian Mubeen Ahmed (339)

M.Taimoor Saeed (343)

M.Rashid Latief (344)

M.Shahid Rasheed (351)

Rehana Hayat (354)

Shymmal Khan (362)

6 | P a g e

Executive Summary

UBL is the second largest bank of Pakistan with assets over Rs. 550 billion and a solid track record of 46 years in addition to the convenience of over 1400 branches serving its customers throughout the country and also at several overseas locations.

In our project we first give an overview of credit analysis and investment policy and why credit analysis is important for evaluating the borrower .It highlights the factors that are important for credit analysis. The first chapter also provides an overview of the functions of investment banking.

In chapter 2 a brief banking history is first provided And then banking in Pakistan. An overview of UBL is provided with Introduction of its departments and subsidiaries. By elaborating UBL role in economy our project specify how UBL help in the economic growth of the country. UBL has taken leading start in the introduction of computers in (1966- 1968) in important cities. By introducing UBL online system, money gram facility, and hajj services UBL is maintaining its leadership in the industry. Credit extension is the principal function of a bank, through which pace of activity is accelerated in the various sectors of economy.

Chapter 3 majorly comprises financial analysis of an important client of UBL Name Nimra textiles. In which we Use different ratios to analyze the financial condition of Nimra textiles.

Chapter 4 majorly comprises the credit policy and implications of UBL.A brief summary of procedures followed by UBL in financing is shown in this area. An attempt has been made by us to elaborate the security requirements for loan disbursement by UBL.

Credit principles and other requirements are mentioned under chapter number four. The 5 c’s of credit are also covered under this chapter. An attempt has been made to cover the stated prudential requirements of state bank of Pakistan for loan disbursement.

Chapter 6 provides insight into difference between the practical and theoretical approach of UBL credit policies. It also provides an insight into loan covering process followed by UBL.

At the end of this project,on the basis of our observations suggestions are recommended as per learning from analysis.This project also will provide a better and brief learning about United Bank Limited.

7 | P a g e

CHAPTER NO.1 INTRODUCTION TO SUBJECT

“CREDIT ANALYSIS AND INVESTMENT BANKING”

1.1 Overview of Credit Analysis and Investment Banking:-

The process of credit analysis may be explained as a procedure, which is carried out in

order to find out the capacity of an issuer to provide some credit to the debtor. This

process is applicable to individual borrowers as well as the issuers of securities.

Introduction Credit analysis focuses at determining credit risk for various financial and nonfinancial

instruments as well as projects. Credit risk analysis can be separated into two steps.

The first part consists of analyzing the credit risk of a particular asset. The second part

analyses the risk of the whole portfolio which comprises the individual credit sensitive

entities. And it is true that the measurement and management of Credit risk has become

a key risk-management issue for both financial and non-financial institutions. With the

improved liquidity in credit derivative market and advances in modeling, the accurate

measurement and management of credit risk to achieve the desired exposure is not as

difficult as before.

Definition

• The process of evaluating an applicant's loan request or a corporation's debt

issue in order to determine the likelihood that the borrower will live up to his/her

obligations.

• Credit analysis is the method by which one calculates the credit worthiness of a

business or organization. The audited financial statements of a large company

might be analyzed when it issues or has issued bond or a bank may analyze the

8 | P a g e

financial statements of a small business before advancing or renewing a

commercial loan.

Credit analysis involves a wide variety of financial analysis techniques, including

ratio and trend analysis as well as the creation of projections and a detailed analysis of

cash flows. Credit analysis also includes an examination of collateral and other sources

of repayment as well as credit history and management ability.

Before approving a commercial loan, a bank will look at all of these factors with the

primary emphasis being the cash flow of the borrower. A typical measurement of

repayment ability is the debt service coverage ratio. A credit analyst at a bank will

measure the cash generated by a business (before interest expense and excluding

depreciation and any other non-cash or extraordinary expenses).

.What Does Credit Analysis Mean?

A type of analysis an investor or bond portfolio manager performs on companies or

other debt issuing entities about the entity's ability to meet its debt obligations. The

credit analysis seeks to identify the suitable level of default risk associated with

investing in that particular entity.

Why Credit Score Analysis is Important?

Credit score is the basis of sanction of loan by a lender and therefore credit

scores analysis is very important for the borrower to know where exactly he or she

stands. Credit score basically is the formula that the lenders use to calculate the risk

factor while sanctioning loans for the prospective borrower. That objective is

accomplished by lenders through credit score analysis relating to the prospective

borrower. At the same time such credit score analysis is important for the prospective

borrower to know exactly where he or she stands in the expectancy for the sanction of

loan.

Factors in Credit Score Analysis

Major factors that are taken into account in the credit score analysis are –

§ Payment history of the prospective borrower.

§ Current outstanding debt of the client.

§ Length of the credit history.

9 | P a g e

§ Sources for regular flow of income.

1.2 Importance of Credit Analysis of Individual Borrowers

In case of the individual borrowers the system of credit analysis is used in order to

measure the economic capability. This is done in the context of repayment of debt. The

system tries to find out if the borrower would be able to pay his debts at the proper time.

With the help of credit analysis the lenders can also find out if the debtor would at all be

able to pay back the debt.

1.3 Use of Credit Analysis of Corporate Entities

The system of credit analysis is also applicable for reviewing the financial capacities of

a certain issuer who is dealing in debt instruments. This process is thus extremely

crucial for those who put their money in these debt instruments.

In Credit Analysis we discussed deeply about the Balance Sheet. Because on that

bases bank decide that firm have long term debt paying ability or not. There are few

mainly items are mentioned below;

• Fixed assets

• Current assets

• Stock

• Current ratio

• Long term liability

• Called up share / Treasury Stock

• Share Premium

• Revaluation Reserve

• P / L figure C – P/L

• Share holder Equity

1.4 Investment banking

Investment banking is a field of banking that aids companies in acquiring funds.

Investment banks create securities, including stocks and bonds, for themselves and

10 | P a g e

other companies, and facilitate the trade in them. They also help companies manage

mergers and acquisitions.

Through investment banking, an institution generates funds in two different ways. They

may draw on public funds through the capital market by selling stock in their company,

and they may also seek out venture capital or private equity in exchange for a stake in

their company.

Functions of Investment Bank:

Unlike commercial banks and savings and loans, investment banks do not seek cash

deposits from customers in the form of checking and savings accounts, and they do not

make traditional interest-bearing loans to individual customers. Investment banks

instead make their money primarily

• By advising corporate clients on the creation of stocks, bonds and other

securities

• By underwriting securities

• By facilitating mergers and acquisitions, along with any due diligence and

securities exchanges that may go along with them.

• And by brokering (or selling) securities to investors.

Investment bankers have also created a broad array of investment options to go along

with traditional stocks and bonds, including securities derivatives such as call and put

options, which allow investors to lock in a buy or sell price on an investment at a future

date, and credit default swaps, which insure bond buyers against the risk that a bond

seller will renege on the debt. Investment banks also lend stocks to facilitate short

trades, in which speculators borrow stock and sell it in hopes that its price will decline

before they buy it and return it to the lender.

An investment banking firm also does a large amount of consulting. Investment bankers

give companies advice on mergers and acquisitions, for example. They also track the

market in order to give advice on when to make public offerings and how best to

manage the business' public assets. Some of the consultative activities investment

11 | P a g e

banking firms engage in overlap with those of a private brokerage, as they will often

give buy-and-sell advice to the companies they represent.

Investment banks provide a numerous finance-related services, including underwriting,

raising capital for companies by issuing equity or debt securities

and facilitating mergers. When raising capital for a firm, an investment bank is acting as

an intermediary between investors and the issuer. Capital raised can come from private

investors (who often have a high net worth), or from pools of capital obtained within the

public markets. Capital obtained from public markets is normally through an initial public

offering (IPO); however, special purpose acquisition companies (SPACs) are another

alternative.

Role of Investment Banks in Economy:

The primary role of investment banking in the economy has traditionally been to help

businesses raise capital for their operations by selling investment securities to the

general public.

Through innovations of financial instruments and advisory to clients like corporate firms

and government, which are main vehicles in growth of an economy, investment banks

assist these clients to raise funds.

One of the main functions of the money and capital markets is to allocate efficiently the

flow of funds from savings surplus economic units to savings deficit units. The efficiency

of capital market is instrumental in the channeling of savings to investment opportunities

and in the growth and development of a viable economy. Substantial amounts of funds

are raised by business firms and the Government through the issue of new securities.

The major institutions acting as intermediaries between firm seeking external funds in

capital markets and the investment public are investment houses. The investment

banker assists the issuing firm in designing and timing securities offerings, formulates

plans for raising funds through the capital markets and provide the distributing

organization. One of the fundamental economic functions of the investment banker is to

underwrite the risk of fluctuations in the market price of the securities being issued,

during the time of offering.

12 | P a g e

CHAPTER NO.2

“INTRODUCTION TO THE BANK”

2.1 Banking History:- Consensus on the origination of word “Bank” is not yet reached at. Some authors

opinion is that this word is derived from the words “Bancus” or “Banque”, which mean a

bench and they further relate banking business inception to Jews in Lombardy. Other

authorities state that the word “Bank” is derived form the German word “Back” which

means “Joint Stock fund” and later on due to German occupation of Italy, this word was

italianated into “Bank. Authors quote

Babylonians (few quotes Chinese) who developed banking system as early as 2000.

B.C1

Banking in Pakistan Banking started in Pakistan after the bold and emergent decision of formulation of SBP

on July 30, 1948. Thereafter this sector has witnessed enormous growth. In 1974 banks

were nationalized, in the hope that new era of growth could be achieved through it.

However the process is reverse since 1991, up till now MCB, ABL, and UBL have been

privatized and HBL is in the process of its privatization.

2.2 United Bank Limited: On November 9, 1959, UBL was notified and included as a private schedule bank with

authorized capital of Rs. 20 million; issued and paid up capital of Rs. 10 million divided

into 1 million shares of Rs. 10/ each. Currently BOD and president/ CEO Mr. Amar Zafar

Khan being a member of this newly formed set up manage UBL. Chairman His

Highness Shaikh Nahayan Mabarak Al Nahayan and Deputy Chairman Sir Mohammed

Anwar Pervez are the two supreme controllers of the bank’s affairs. Another

development is the appointment of director operation, Nauman Hussain by the newly

13 | P a g e

privatized bank. Senior management of the bank is shown in the chart given at the end

of chapter.

2.2.1 Number of Branches: UBL has a large network of branches, which extends to the remotest areas of the

country. In December 1983, there were 1623 branches whereas in 1974 it had only

1238 branches and in October 2003 these figures show total number of 1007

branches3.

UBL has been very active in increasing its overseas branches network. The first foreign

branches were established in London in 1963. Now UBL has branches in Bahrain,

Qatar, Saudi Arabia, United Arab Emirates, Yemen Arab Republic, UK Switzerland,

Egypt, Oman and The United States. These branches are playing a significant role in

channeling home remittances and foreign trade of Pakistan.

Subsidiaries: UBL has four subsidiaries, namely:

• United National Bank Limited (UNB), UK

• United Bank AG (Zurich), Switzerland

• United Executers and trustees Company Limited

• United Bank Financial Services (Private) Limited

2.2.2 Departments: • Account department

• Deposit department

• Credit department

• Remittances department

• Clearing department

• Human resource department

• Bill department

• Lockers department

14 | P a g e

• Control and compliance department (CCD)

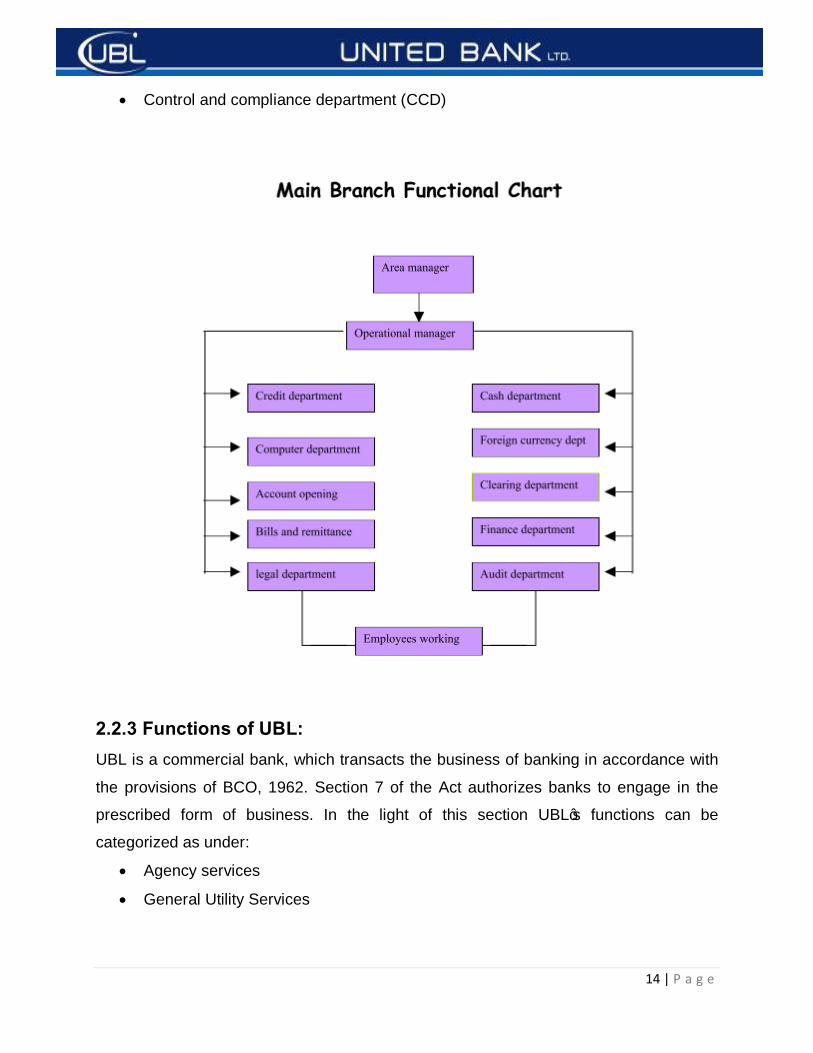

2.2.3 Functions of UBL: UBL is a commercial bank, which transacts the business of banking in accordance with

the provisions of BCO, 1962. Section 7 of the Act authorizes banks to engage in the

prescribed form of business. In the light of this section UBL’s functions can be

categorized as under:

• Agency services

• General Utility Services

15 | P a g e

• Underwriting of loans raised by the Government or public bodies and trading by

corporations etc.

• Providing specialized services to customers, and

• Hajj-related services.

2.2.4 Role of UBL in Banking Sector: The impressive growth and development, which UBL achieve, present it undoubtedly

the most dynamic and progressive. In a very shorter period of time it became one of the

leading banks overtaking several other older and its competitorbanks4. The major

contributions5 the bank ahs made are enlisted below:

• Record setting performance and commitment to serve the customers

• Personalized service and dynamic approach

• Catalyst of changes

• Professional management

• Modern banking policy

• Human resource development

• Small loans (or) micro credits

• Pacesetter in economic research established in 1967, department for economic

research.

• Utility bills collection

• Credit cards (unicard-1970)

• Travelers Cheques (Humarah-1971)

• Diaries and calendars – received prizes too.

2.2.5 Computerization of UBL: UBL has taken leading start in the introduction of computers in (1966- 1968)6 in

important cities. Its three computers centers Rawalpindi, Lahore and Karachi are

equipped with the modern mainframe computers of various Capacities. Every branch

has been decorated with microcomputers. The use of computers has enabled the bank

to save time and efforts raise efficiency and deliver the goods speedily to its customers.

This has also allowed the bank to maintain its leadership within the industry.

16 | P a g e

i. UBL - On line System7: Themes of this service is “Access anytime, anywhere, any device” which Symbolizes

comfort, convince and connectivity. UB-Online a web based service that can b

accessed through multiple media link like, (i) PC via internet (00) Mobile phone with

WAP or free SMS) (iii) Personal Digital (iv) assistants and (v) Plain telephone; following

are some of the exciting features:

o Accounts statement & electronic data interchange

o Graphical analysis

o Alerts service /facility, search facility and activity long

o The banks as another computer-based system known as “UIBANK”8, which is a well-

develop on-line branch-banking package. The system automatically prepares various

report, central bank returns, and statement of accounts for customers.

ii. Money Gram facility: The bank has recently employed money gram service system, which can affect money

transfers within minutes. Similarly the system used for local transfer of money

transactions is called uni-remote.

iii. Hajj service: Keeping to its tradition is august 1982 provided electronic facility at its Hajj booth and

has installed now modern computers at designated branches (Hajis) and increasing

efficiency. This facility has reduced the service time to less than six minutes per Haji

compare to about half-an-hour to 45 minutes per Haji earlier.

2.2.6 Credit Department of UBL: Credit extension is the principal function of a bank, through which pace of activity is

accelerated in the various sectors of economy. Also the indicators, which mainly reflect

the high quality of bank’s management, are its prudent financing decisions, proper

control of finance and prompt recovery. In this regard the credit policy of a bank play a

very important role as it provides the overall framework, responsibilities, authorities and

facilitate decision-making. Credit department performance is subject to a defined policy

on credit control exercised by the SBP. SBP affect credit decisions through the

weapons of bank rate, open market operations, variable reserve requirements, selective

credit restrictions and prudential regulations.

17 | P a g e

Importance In the past decade, regulators have been gaining familiarity and experiences in the

monitoring of banks and other financial institution in terms of solvency and capital

adequacy. Some of the perverse effects of the Basle accord have been widely

documented. With the arrival of the new Basle II accord around 2005 and other

improvement in accounting, it is important for financial institutions to develop internal

models to demonstrate the capability of risk management, including demonstrating the

effectiveness of hedging which can result in freeing up of regulatory capital. Given the

improvement in the regulatory regime, sound credit analysis, rather optimization

according to arcane rules, are more relevant for the future. During 2001 and 2002, there

have been very high profile cases of default, such as Enron and WorldCom with very

large amount of outstanding debt. Some financial institutions have been caught

unguarded with large amount of exposure. During the late 90’s, banks have been

pressured to lend money to gain business in other areas such as merger and

acquisitions, resulting in large exposure of idiosyncratic credit risk to particular

companies. The current prevalent practice of marking loans at par value regardless of

the counter party’s credit risk poses significant problems in proper risk management.

Therefore the correct credit analysis and accurate measurement of the amount of credit

risk involved is very important in determining whether the extra benefit from other

business can compensate. With the increasing usage of largely unfunded derivative

transactions, such as swaps, it is increasing important to assess the counter party risk,

as well as the correlation between market risk and credit risk, as the collapse of the

trading company Enron readily demonstrated

18 | P a g e

CHAPTER NO.3

“INTRODUTION OF CLIENT OF THE BANK”

In Faisalabad region UBL has got much customer base and most of industries are

customers of bank .Some of the major customers who take loan facility from UBL are as

under

• A.A Spinning Mills Limited

• Arshad Corporation Private Limited

• Crescent Textiles Mills Limited

• Huda Sugar Mills

• Interloop Private Limited

• Ittehad Fabrics

• Punjab Beverages

• Sitara Spinning Mills Limited

• United industries

• Zahid Jee Textiles Mills Limited

• Nimra Textile limited

“NIMRA TEXTILE LIMITED” Nimra textile is remarkable bold figure among Top manufacturers & suppliers of Textile

Woven Products (Home Textile) in Pakistan and it does not require any formal

introduction.

Business Type: Manufacturer, Trading Company

Products/Services:

Garments,Curtains,Fabrications,Flat/ Fitted , Sheets, Duvet

Covers,Matress Covers, Bed in a bag, Bed Spreads , Quilt

19 | P a g e

Covers accessories, Bed Linen,Kitchen

Production site: Bleaching, Dyeing, Rotary and flat bed

Number of employees: above 1000 people

Exports Per Annum: more than US $70

Production facilities:

• 260 Sulzer Projectile / Air Jet looms,

• 400 Auto / Dobbies / Jacquad looms,

• CAD & Engraving

• Rotary Printing Stork / State of the Art Zimmer 5

machines,

• Reggiani Flat Bed Printing Machine,

• Thermosole Dyeing Babcock / Manforts 3 machines

Quality control:

• 18 Quilting machines

• 600 Stitching machines

Year Established: 2001

Trade & Markets: North America

Eastern Europe

Western Europe

Total Annual Sales Volume:

US$50 Million - US$100 Million

20 | P a g e

3.1 Financial analysis:- These section efforts have been made to cover all relevant aspects of the financial

performance of Nimra textiles limited. Overtime comparison and ratio analysis are

carried out with the view to extract concrete conclusion to describe financial standing

and performance of the company.

Liquidity Ratios:

3.1.1 Current Ratio

Current Ratio= total current assets/total current liabilities

2009 2010

1.012245127 1.042310714

The current ratio shows the total current assets that are available to fulfill total current

liabilities. They shows the liquidity position of the company. It shows the short term debt

paying ability of the company. If compare this liquidity ratio for Nimera textiles for the

years 2009 and 2010 then it shows that the liquidity position of the company has

improved by 0.02%.IIt creates a feasible situation for UBL to grant loan to Nimera

textiles.

0.99

1

1.01

1.02

1.03

1.04

1.05

Current Ratio

2009

2010

21 | P a g e

3.1.2 Quick Ratio

Quick ratio=Total current assets-inventories/total current liabilities

2009 2010

0.40400925 0.547899289

Quick ratio also refers to liquidity ratio and it depicts the liquidity position of the

companies that depend upon their inventory that is seasonal functioning. So the current

figures of quick ratio for Nimra textiles shows that that this company is very feasible for

seasonal loaning as this ratio is improved by 0.1% in 2010.

0

0.1

0.2

0.3

0.4

0.5

0.6

Quick Ratio

2009

2010

3.1.3 Cash Ratio

Cash ratio=Cash+Bank+Marketable securities/Total current liabilities

2009 2010

0.008149897 0.041725586

It extreme level of checking the liquidity position of the company as compare to current

and quick ratio as it excludes all least liquid assets. If we look at above figures of cash

ratio then we find that the ratio has increased by 0.032% it means that the company

increasing its liquid assets.

22 | P a g e

0.99

1

1.01

1.02

1.03

1.04

1.05

CASH RATIO

2009

2010

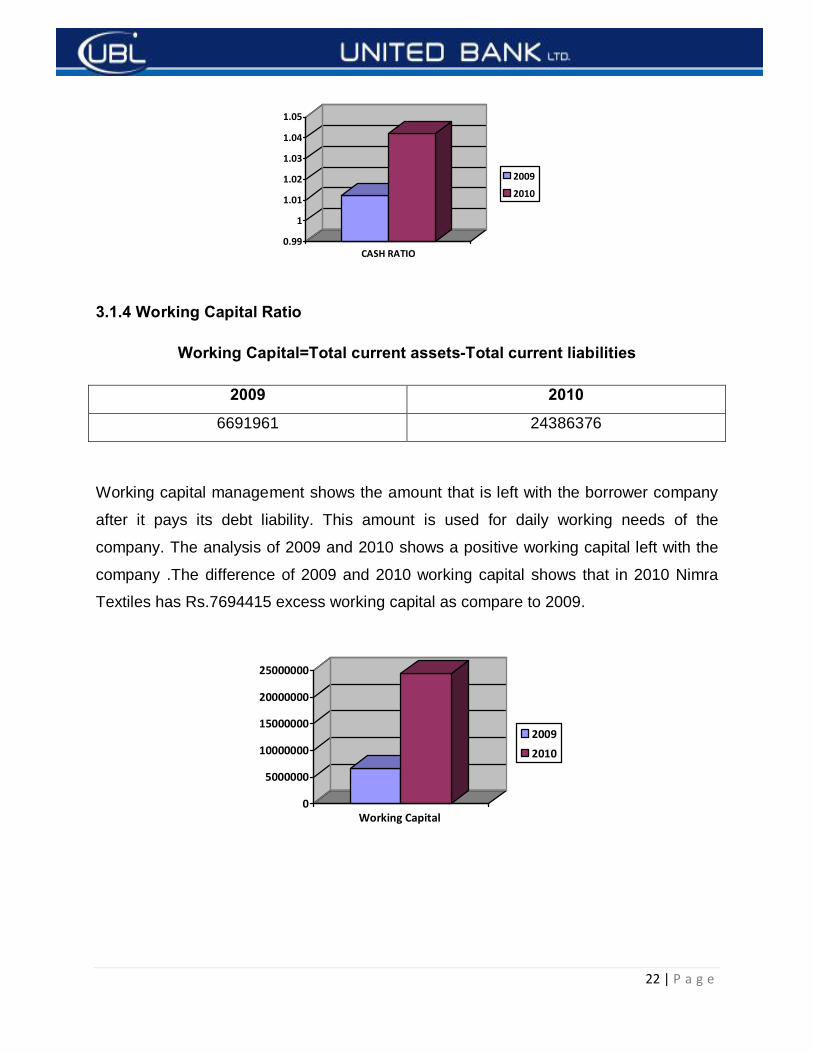

3.1.4 Working Capital Ratio

Working Capital=Total current assets-Total current liabilities

2009 2010

6691961 24386376

Working capital management shows the amount that is left with the borrower company

after it pays its debt liability. This amount is used for daily working needs of the

company. The analysis of 2009 and 2010 shows a positive working capital left with the

company .The difference of 2009 and 2010 working capital shows that in 2010 Nimra

Textiles has Rs.7694415 excess working capital as compare to 2009.

0

5000000

10000000

15000000

20000000

25000000

Working Capital

20092010

23 | P a g e

3.1.5 Profitability ratios:

Profitability= (Gross income/sales)*100

2009 2010

13.4638 11.5345

Gross profit is critical because it represents the amount of money remaining to pay

operating expenses,financing cost and taxes.The gross income over sales ratio

decreases by 2% in 2010 which shows the negative sign of profitability for Nimra

textiles.

10.5

11

11.5

12

12.5

13

13.5

Profitablility Ratio

2009

2010

3.1.6 Operating income over sales ratio:

(Operating income/sales)*100

2009 2010

6.31586 4.9712

Operating income over sales ratio shows that in 2010 the profitability of the firm has

decreased by 2 % which goes against the Nimra textiles.

24 | P a g e

0

1

2

3

4

5

6

7

Operating income over sale Ratio

20092010

3.1.7 Earnings before Interest and tax ratio:

(EBIT/sales)*100

2009 2010

2.44486 2.53265

Earnings before interest and taxes over sales ratio almost remained constant in both

years. There is no significant change over the year It shows that company remained

comparatively stable.

2.4

2.42

2.44

2.46

2.48

2.5

2.52

2.54

Earning before interest & tax ratio

20092010

25 | P a g e

3.1.8 Earnings after Tax Ratio

(EAT/sales)*100

2009 2010

1.50125 1.60368

This ratio shows the profit that is available form each rupee of the sale.Earnings after

tax and gross spread ratio have increased by 0.1% in 2010 that is the positive sign of

Nimra textiles. This can be because of new investment and business expansions.

1.441.461.48

1.51.521.541.561.58

1.61.62

Current Ratio

20092010

Activity Ratios:

3.1.9 Stock Turnover Ratio

Stock turnover = Stock/COGS*365

2009 2010

89.9139 61.0364

The stock turnover ratio shows that how many days inventory takes place to convert

into finished goods if compare this ratio for 2009 and respectively for 2010 then it shows

the positive condition of Nimra textiles as the days have decreased by 28 in 2010.

26 | P a g e

0

20

40

60

80

100

stock turnover Ratio

20092010

3.1.10 Debtors to Sales Ratio

Debtors to sales= trade debtors/sales*365

2009 2010

23.8985 37.082539

Debtors to sales ratio also shows that how many days the company recovers its

receivables.if look at this ratio for 2009 and 2010 then it shows that company

receivables turnover ratio is increased by 14 days. It shows a negative trend in a

company.

0

5

10

15

20

25

30

35

40

Debtors to sales ratio

20092010

27 | P a g e

3.1.11 Payable Turnover Ratio

Payables turnover ratio= Accounts payables/COGS*365

2009 2010

30.39299 17.908361

Payable turnover ratio decreased by 50% in 2010 which shows a very positive sign for

further lending to the company it means that Nimra textile is paying Back its payables

13 days early in 2010 than in 2009.

0

5

10

15

20

25

30

35

Payable turnover Ratio

20092010

3.1.12 Cash Conversion Cycle

Cash conversion cycle= Stock turnover+ACP-APP

2009 2010

83.41948 80.21064

Cash conversion cycle shows days the company takes to convert its raw material into

cash. In 2010 Nimra textile shows a short cash conversion cycle as compare to 2009 by

3 days.

28 | P a g e

0

20

40

60

80

100

stock turnover Ratio

20092010

3.1.13 Interest Coverage

Interest coverage= Profit before taxes/interest charges

2009 2010

0.65089 1.105823

Ratio used to determine how easily a company can pay interest on outstanding debt.

The higher the ratio, the lesser the company is burdened by debt expense. so it shows

the positive sign for the company as it increased by 0.5% in 2010 as compare to 2009.

0

0.2

0.4

0.6

0.8

1

1.2

Interest coverage

20092010

29 | P a g e

3.1.14 Leverage Ratio

Leverage ratio= Total liabilities/Equity

2009 2010

1.99989 1.89496

Any ratio used to calculate the financial leverage of a company to get an idea of the

company's methods of financing or to measure its ability to meet financial obligations. It

remains almost steady in both years and there is no significant change.

1.84

1.86

1.88

1.91.92

1.94

1.961.98

2

Leverage Ratio

20092010

30 | P a g e

CHAPTER NO.4

“CREDIT POLICY AND ITS IMPLEMENTATION” Credit Policy: Credits operations are undertaken in accordance to bank’s credit policy. The policy

strictly prohibits violation of SBP/Local central bank’s rules and suggests financing of

self liquidating, cash flow supported and well collateralized transactions, which equate

the principle of lending (safety, liquidity, dispersal, remunerations and suitability).

Procedure for Financing from UBL When a party comes for financing, banker will ask the following questions.

3.3.2.1 Purpose: In this the party mentions the purpose; they want to apply for the finances. No lending is done

without purpose.

3.3.2.2 Business The party must have some specific running business i.e. general merchandise,

construction business etc.

The second question arises of the cash flow that how much flow is generated by the

party from the current business.

3.3.2.3 Security: The bank will secure itself against the lending. There can be two type of security.

Ø Commercial

Ø Residential

The bank prefers commercial security. Relationship Manager (RM) is mainly

responsible for the relationship between the bank and party. He acts like a bridge

between the two.

In the first instance the party would prepare the following property documents.

Ø AKS Shajarah

Ø Naqsha Tasveeri

Ø Approved Building Plan

Ø Tresh fard

31 | P a g e

Ø Intaqal Naqal

The party is asked to contact any valuator on the panel of UBL. ICM&L and Tajak Builder are on

the panel of UBL. The valuator will visit the site and set market value and FSV of the said

property. He prepares report of at least three pages. These documents sent for one page legal

opinion to any layer on the panel of UBL. Having clear legal opinion RM start preparing credit

Approval (CA). The documents are signed by the RM & AM and then forwarded to UBL RHQ in

Peshawar. Here SRM examines the CA if he found some exception he will send it back to the

respective Rm.

RM rectifies the acceptation and sends it back to SRM. SRM studied and pass it to credit officer.

He has three hours of time to study the CA and if found correct then he pass it to another credit

officer. After his examination the CA is passed on to the credit risk manager. He checks the CA

and after signing it sent to CAD. He forwards the CA to SCO. Whose office is at UBL RUCO at

Lahore, after his signature the C.A is sent back to RCAD.

RCAD make a check less list and asked the RM to contact the party to complete the said

documents they are.

Ø Letter of continuity

Ø Personal Guarantee

Ø Letter of hypothecation of stock

Ø D.P Note

Ø Mortgage Deed

Ø NIC of executants and witness

Ø Stock report

Ø Insurance policy

Ø Party profile

After completion of charge document RM send it to RCAD when they found it correct, they

issues DAC. A copy of DAC is sent to RM and NICF account is opened and debit transaction

starts.

32 | P a g e

Process Flow Diagram of Loan Disbursement

33 | P a g e

CHAPTER NO.5

“CREDIT PRINCIPLES AND OTHER REQUIREMENTS” This section outlines the basic principles that UBL will pursue for extending credit

facilities. These principles will serve as useful guidelines and precautionary measures

for prudent lending.

a) UBL will not extend any such credit facilities, which violate the rules and

regulations prescribed by the State Bank of Pakistan and/or local Central Banks

from time to time.

b) UBL will consider financing of self-liquidating, cash flow supported and well

collateralized transactions within a Business Group’s target market and risk

acceptance criteria.

c) UBL will participate in syndicated facilities if the transaction fulfils the parameters

established by the Bank.

d) UBL will, prior to allowing the facilities, satisfy itself that these are adequately

secured with relevant and legally enforceable documents.

e) UBL will ensure that facilities allowed are well aligned to customers' business

structure and specific needs.

f) UBL will assess the customer’s character for integrity and willingness to repay by

studying the background and credit history of the customer to establish

commitment to repay.

g) Facilities provided by UBL will be well diversified into such industrial/trading

sectors where UBL has the necessary skills and resources to achieve a strong

market position and adequate return on capital.

h) UBL shall only lend up to the amount that the customer has capacity and ability

to repay. Customer's liquidity and repayment capacity will be determined by

34 | P a g e

careful analysis of financial statements and future projections to ensure that

customer’s financial condition remains satisfactorily liquid to repay the bank.

i) It is against UBL’s policy to provide financing for speculative purposes and/or

undesirable activities. For Islamic Banking business, Shariah compliant business

activities shall be financed based on evaluation on Islamic Financial Accounting

Standards.

j) UBL shall not allow any credit facility to clients, who have been allowed

waivers/write offs in UBL. Any exception to this will need approval of the highest

level of Credit Committee including the Group Executive Risk & Credit Policy.

k) UBL shall maintain adequate margin against credit facilities, in accordance with

State Bank of Pakistan’s Prudential Regulations and/or local Central Banks’

instructions. If deemed necessary, the appropriate business unit / credit authority

may specify a higher margin.

l) UBL shall continue to invest in development of officers dealing with credit related

matters, to ensure maximum output and utmost participation of individuals

involved with credit risk management and the credit process.

m) Documents included as annexures of this manual will require regular updates

and modification as per the requirements and needs of the businesses and

changing market dynamics. The Group Executive Risk & Credit Policy will

approve any and all updates and modifications in such documents. Any major

structural changes and/or modifications will require ratification by the Board

Credit Committee / Board of Directors as well as clearance by the State Bank of

Pakistan.

n) Any addition/amendment/deletion/deviation in this manual to meet changing

conditions and/or regulatory/legal requirements of any domestic or overseas

location will be approved by the Group Executive Risk & Credit Policy. However,

if any such change weakens any provision in this manual, the same shall require

35 | P a g e

ratification by the Board Credit Committee / Board of Directors as well as

clearance by the State Bank of Pakistan.

o) This Manual represents policies and procedures introduced to streamline and

consolidate all rules applicable to credit process globally. However, management

reserves the right to formulate auxiliary Credit Policies for any domestic or

overseas location within parameters laid down in this Manual.

5.1 The 5 C’s of Credit It's one of the most common questions among small business owners

seeking financing: "What will the bank be looking for from me and my business?" While

each lending situation is unique, many banks utilize some variation of evaluating the five

C's of credit when making credit decisions: character, capacity, capital, conditions and

collateral. We'll take a look at each of these ingredients and how they may impact your

funding request. Review each category and see how you stack up.

5.1.1 Character

What is the character of the management of the company? What is

management's reputation in the industry and the community? Investors want to put their

money with those who have impeccable credentials and references. The way you treat

your employees and customers, the way you take responsibility, your timeliness in

fulfilling your obligations — these are all part of the character question.

This is really about you and your personal leadership. How you lead yourself and

conduct both your business and personal life gives the lender a clue about how you

are likely to handle leadership as a CEO. It's a banker's responsibility to look at the

downside of making a loan. Your character immediately comes into play if there is a

business crisis, for example. As small business owners, we place our personal stamp

on everything that affects our companies. Often, banks do not even differentiate

between us and our businesses. This is one of the reasons why the credit scoring

process evolved, with a large component being our personal credit history.

5.1.2 Capacity

36 | P a g e

What is your company's borrowing history and track record of repayment?

How much debt can your company handle? Will you be able to honor the obligation and

repay the debt? There are numerous financial benchmarks, such as debt and liquidity

ratios, that investors evaluate before advancing funds. Become familiar with the

expected pattern in your industry. Some industries can take a higher debt load; others

may operate with less liquidity.

5.1.3 Capital

How well-capitalized is your company? How much money have you invested

in the business? Investors often want to see that you have a financial commitment and

that you have put yourself at risk in the company. Both your company's financial

statements and your personal credit are keys to the capital question. If the company is

operating with a negative net worth, for example, will you be prepared to add more of

your own money? How far will your personal resources support both you and the

business as it is growing? If the company has not yet made profits, this may be offset by

an excellent customer list and payment history. All of these issues intertwine, and you

want to ensure that the bank perceives the business as solid.

5.1.4 Conditions

What are the current economic conditions and how does your company fit

in? If your business is sensitive to economic downturns, for example, the bank wants a

comfort level that you're managing productivity and expenses. What are the trends for

your industry, and how does your company fit within them? Are there any economic or

political hot potatoes that could negatively impact the growth of your business?

5.1.5 Collateral

While cash flow will nearly always be the primary source of repayment of a

loan, bankers look at what they call the secondary source of repayment. Collateral

represents assets that the company pledges as an alternate repayment source for the

loan. Most collateral is in the form of hard assets, such as real estate and office or

37 | P a g e

manufacturing equipment. Alternatively, your accounts receivable and inventory can be

pledged as collateral.

The collateral issue is a bigger challenge for service businesses, as they have fewer

hard assets to pledge. Until your business is proven, you're nearly always going to

pledge collateral. If it doesn't come from your business, the bank will look to your

personal assets. This clearly has its risks — you don't want to be in a situation where

you can lose your house because a business loan has turned sour. If you want to be

borrowing from banks or other lenders, you need to think long and hard about how you'll

handle this collateral question.

Keep in mind that in evaluating the five C's of credit, investors don't give equal weight to

each area. Lenders are cautious, and one weak area could offset all the other strengths

you show. For example, if your industry is sensitive to economic swings, your company

may have difficulty getting a loan during an economic downturn — even if all other

factors are strong. And if you're not perceived as a person of character and integrity,

there's little likelihood you'll receive a loan, no matter how good your financial

statements may be. As you can see, lenders evaluate your company as a total package,

which is often more than the sum of the parts. The biggest element, however, will

always be you.

38 | P a g e

5.2 SWOT Analysis:-

5.2.1 A strength could be:

• Your specialist marketing expertise.

• A new, innovative product or service.

• Location of your business.

• Quality processes and procedures.

• Any other aspect of your business that adds value to your product or service.

39 | P a g e

5.2.2 A weakness could be:

• Lack of marketing expertise.

• Undifferentiated products or services (i.e. in relation to your competitors).

• Location of your business.

• Poor quality goods or services.

• Damaged reputation.

5.2.3 An opportunity could be:

• A developing market such as the Internet.

• Mergers, joint ventures or strategic alliances.

• Moving into new market segments that offer improved profits.

• A new international market.

• A market vacated by an ineffective competitor

5.2.4 A threat could be:

• A new competitor in your home market.

• Price wars with competitors.

• A competitor has a new, innovative product or service.

• Competitors have superior access to channels of distribution.

• Taxation is introduced on your product or service.

40 | P a g e

5.3 PEST Analysis:

5.3.1 Political Factors

The political arena has a huge influence upon the regulation of businesses, and the

spending power of consumers and other businesses. You must consider issues such

as:

1. How stable is the political environment?

2. Will government policy influence laws that regulate or tax your business?

3. What is the government's position on marketing ethics?

4. What is the government's policy on the economy?

5. Does the government have a view on culture and religion?

6. Is the government involved in trading agreements such as EU, NAFTA, ASEAN, or

others?

41 | P a g e

5.3.2 Economic Factors

Marketers need to consider the state of a trading economy in the short and long-terms.

This is especially true when planning for international marketing. You need to look at:

1. Interest rates.

2. The level of inflation Employment level per capita.

3. Long-term prospects for the economy Gross Domestic Product (GDP) per capita, and

so on.

5.3.3 Sociocultural Factors

The social and cultural influences on business vary from country to country. It is very

important that such factors are considered. Factors include:

1. What is the dominant religion?

2. What are attitudes to foreign products and services?

3. Does language impact upon the diffusion of products onto markets?

4. How much time do consumers have for leisure?

5. What are the roles of men and women within society?

6. How long are the population living? Are the older generations wealthy?

7. Do the population have a strong/weak opinion on green issues?

5.3.4 Technological Factors

Technology is vital for competitive advantage, and is a major driver of globalization.

Consider the following points:

42 | P a g e

1. Does technology allow for products and services to be made more cheaply and to a

better standard of quality?

2. Do the technologies offer consumers and businesses more innovative products and

services such as Internet banking, new generation mobile telephones, etc?

3. How is distribution changed by new technologies e.g. books via the Internet, flight

tickets, auctions, etc?

4. Does technology offer companies a new way to communicate with consumers e.g.

banners, Customer Relationship Management (CRM), etc?

43 | P a g e

5.4 Porter’s Five Force Analysis:

Five force analysis helps the marketer to contrast a competitive environment.It has similarities with other tools for environmental audit,Such as PEST analysis,but tends to focus on the single,stand alone,business or SBU (Strategic Business Unit) rather than a single product or range of products.For example,DELL would analyse the market for business computers i.e one of its SBUs.

Five forces analysis looks at five key areas namely the threat of entry, the power of

buyers, the power of suppliers, the threat of substitutes, and competitive rivalry.

5.4.1 The threat of entry.

• Economies of scale e.g. the benefits associated with bulk purchasing.

• The high or low costs of entry e.g. how much will it cost for the latest technology?

• Ease of access to distribution channels e.g. Do our competitors have the

distribution channels sewn up?

44 | P a g e

• Cost advantages not related to the size of the company e.g. personal contacts or

knowledge that larger companies do not own or learning curve effects.

• Will competitors retaliate?

• Government action e.g. will new laws be introduced that will weaken our

competitive position?

• How important is differentiation? e.g. The Champagne brand cannot be copied.

This desensitizes the influence of the environment.

• This is high where there a few, large players in a market e.g. the large grocery

chains.

• If there are a large number of undifferentiated, small suppliers e.g. small farming

businesses supplying the large grocery chains.

• The cost of switching between suppliers is low e.g. from one fleet supplier of

trucks to another.

5.4.2 The power of suppliers.

The power of suppliers tends to be a reversal of the power of buyers.

• Where the switching costs are high e.g. Switching from one software supplier to

another.

• Power is high where the brand is powerful e.g. Cadillac, Pizza Hut, Microsoft.

• There is a possibility of the supplier integrating forward e.g. Brewers buying bars.

• Customers are fragmented (not in clusters) so that they have little bargaining

power e.g. Gas/Petrol stations in remote places.

5.4.3 The threat of substitutes

• Where there is product-for-product substitution e.g. email for fax Where there is

substitution of need e.g. better toothpaste reduces the need for dentists.

• Where there is generic substitution (competing for the currency in your pocket)

e.g. Video suppliers compete with travel companies.

• We could always do without e.g. cigarettes.

45 | P a g e

5.4.4 Competitive Rivalry

• This is most likely to be high where entry is likely; there is the threat of substitute

products, and suppliers and buyers in the market attempt to control. This is why it

is always seen in the center of the diagram.

5.5 Macro-economic risk areas In considering a structured approach to credit, the process requires a categorization of

each risk element. It should be noted that there exists considerable overlap and

interrelationship between these elements. The aspects considered in this section have

substantial interconnections and interrelationships with each having an effect upon

another

46 | P a g e

5.6 Micro-economic risk areas:

One of the most fundamental non-financial aspects crucial for the long term success of

a business is its strategy and plans. Corporate strategy is developed by management

and will reflect their judgment using their skills, expertise, experience and

entrepreneurial flair. At the strategic level they will establish the fundamentals of the

business and the basic direction for the future. At the business plan level they will

address the practical implementation of the strategic decisions.

5.7 Rules followed by the bank for Credit Risk Management: 5.7.1 PRs. For SMES

Regulation R-1 Sources and capacity of repayment and cash flow backed lending.

Regulation R-2 Personal guarantees.

Regulation R-3 Limit on clean facilities.

Regulation R-4 Securities.

Regulation R-5 Margin requirements.

Regulation R-6 Per party exposure limit.

Regulation R-7 Aggregate exposure of a bank/DFI on SME sector.

Regulation R-8 Minimum conditions for taking exposure.

Regulation R-9 Proper utilization of loan.

Regulation R-10 Restriction on facilities to related parties.

Regulation R-11 Classification and provisioning for assets.

5.7.2 PRs for Corporate Commercial

RISK MANAGEMENT (R)

Regulation R-1 Limit on exposure to a single person.

47 | P a g e

Regulation R-2 Limit on exposure against contingent liabilities.

Regulation R-3 Minimum conditions for taking exposure.

Regulation R-4 Limit on exposure against unsecured financing facilities.

Regulation R-5 Linkage between financial indicators of the borrower and total exposure

from financial institutions.

Regulation R-6 Exposure against shares/TFCs and acquisition of shares.

Regulation R-7 Guarantees

Regulation R-8 Classification and provisioning for assets.

Regulation R-9 Assuming obligations on behalf of NBFCs.

Regulation R-10 Facilities to private limited company.

Regulation R-11 Payment of dividend.

Regulation R-12 Monitoring.

Regulation R-13 Margin requirements.

5.7.3 PRs for Consumer Loaning

Regulation R-1 Facilities to related persons & utilization of clean loans for Initial Public

Offerings (IPOs)

Regulation R-2 Limit on exposure against total consumer financing.

Regulation R-3 Total financing facilities to be commensurate with the income.

Regulation R-4 General reserve against consumer finance.

Regulation R-5 Bar on transfer of facilities from one category to another to avoid

classification.

Regulation R-6 Margin requirements.

48 | P a g e

5.7.4 PRs for Credit Cards

Regulation O-1 Receipt of credit cards.

Regulation O-2 Statement of accounts.

Regulation O-3 Unauthorized/wrong transactions.

Regulation O-4 Partial payment by cardholder.

Regulation O-5 Due date for payment.

Regulation R-7 Maximum card limit.

Regulation R-8 Classification and provisioning.

49 | P a g e

CHAPTER NO.6

Differences and Similarities in theoretical and practical approach We visited United Bank Limited (UBL) and conducted meeting with CAD Manager and

other concerned persons and found following that UBL follow most of the credit principal

that we have studied during our course. The difference and similarities are as under

(1) The Prudential regulations (PRs) of state bank of Pakistan are strictly

followed and in case of any violation of these regulation SBP impose the

penalties or issue different warning to banks

(2) The documents needed for advancing loan must be duly approved by

concerned authorities.

(3) The character of the borrower is evaluated by different out sourcing firm

and Electronic Credit Information Bureau (ECIB) report.

(4) The usual principal of lending like 5 C,S of credit, financial analysis of the

borrower is done by the bank RM department of UBL

(5) The SWOT analysis of the borrower is done by the borrower himself and

some outsource agencies employed by the bank also conduct SWOT

analysis for the banks.UBL has contract with the risk consulting firm ICIL.

This firm provides UBL all the information about the character, SWOT

analysis etc. of the borrower. The bank gives due weight age to this

analysis report.

(6) The pest analysis is also taken into consideration when it is applicable.

(7) The loan collection procedure as we have studied is followed almost in the

same order i.e.

• Recovery letter

• Telephone call

• Personal visit

50 | P a g e

• The collection agencies (in case of car financing only)

• Legal action

UBL try to solve the problems up to first three steps because last two steps involve legal

actions which prolong to some period and also hurt the reputation of the banks.

(8) For rescheduling of loan 90 days as grace period allowed to borrower.

(9) For restructuring bank decrease the mark up rate and also increase the

installment period.

(10) When we ask about the borrower risk assessment the manager

have not enough knowledge about Michael porters risk assessment model

and Porter five competitive forces. They use traditional method to assess

the borrower risk.

(11) The financial statements are accepted as it is provided by the

borrower. The only thing important is the statements should be audited by

some approved charted accountant firms. Because audited financial

statement of the borrower is only requirement by SBP. The bank loan

processing officers has no concern with window dressing or any other fake

information showed in the financial statement.

(12) As for securities against loan is concern the security is critical

analyze it should have sufficient market value, liquidity, and not perishable

in nature.

(13) The security against the loan is valued according to the Forced

Sale Value (FSV). the Forced Sale Value(FSV) of the securities depend

on the type of security and its value. the UBL usually value security on

following ways

• Land =15%

• Building =20%

51 | P a g e

• Machinery=25%

(14) The industry condition of the borrower also given due

consideration.

(15) The economic condition of the country has also impact on credit

policies of banks; unfavorable economic condition leads to strict credit

policy and vice versa.

52 | P a g e

CHAPTER NO.7

“Conclusion and Recommendation” 7.1 Conclusion The study is mainly focused on the credit policies and the tools used for credit risk

analysis. Present study is done on one of the leading bank of Pakistan UBL. We

critically examined and analyze documents procedures, rules and regulations regarding

financing decision of banks. We elaborate different tools and techniques used by UBL

management and to assess borrower risk. We also elaborate different aspect of UBL

credit policy. UBL human resources are highly qualified and have update knowledge

about present developments in the areas of credit risk analysis. Still there are some

minute difference in practical approaches and techniques used by the bank for risk

assessment. The reason is behind these differences are traditional method of risk

assessment, unqualified borrower, and unavailability of sufficient documents and less

use of credit rated agencies.

The present study also enables us to get familiar with financing decision process and

evaluation of borrower risk.

7.2 Recommendations

Although UBL have wonderful credit policies but still there is room for a lot of

improvement and innovations.

Following are some of the suggestions and recommendations that I want to make:

Ø A regular contact with the customers should be maintained in personally.

Because there is an era of retaining the customers. So I recommend that there

should be CRM to get feedback from customers.

53 | P a g e

Ø A proper timeline in cas disbursement should be defined which is usually

comprised due to lengthy processing and documentation requirements.

Ø Relationship managers should be fully trained and need to be fully equipped with

requisite knowledge and skills.

Ø A proper infrastructure should be defined for carrying out computerized financial

analysis of borrower’s business.

Ø Heavy collaterals requirements should be avoided to serve large pool of

borrowers. Heavy collaterals requirements restrict credit business of the bank.

Ø The credit proposal and other documents at times should be properly and

sufficiently prepared before taking approval.

Ø Filing and record maintenance of credit related documents should be done

efficiently.

Ø There is no facility for students to get mark free loan in this bank. So, this bank

should provide free of mark up or easy terms and conditions loan to students and

deserving persons on merit. I hope this scheme will be successful in producing

intelligent, intellectual and brilliant students.

54 | P a g e