Embed Size (px)

DESCRIPTION

Bharti AXA strategy

Citation preview

STRATEGIC MANAGEMENT PROJECT

Submitted to-

Prof. Anshuman Tripathi

Submitted By-

Anurag Satpathy

Sec-B, U113074

Table of ContentsBusiness Model (4-22) Business Model of Bharti AXA 5

Business Model of Allianz (International Competitor)……………………………………………......11

Business Model of New India Assurance ( Government company) 16

Business Model of Bajaj Allianz (Domestic Competitor)………………………………………………19

Comparison between Bharti AXA and its competitors………………………………………………….21

Activity System Map (23-24)

Activity System map for Titan Insurance (Low Cost Organization) 23

Activity System map for Allianz (Diversified Organization) 24

VMO and Key Attributes of Success for Organizations………………………………………… (25-42)

INDIA- Low cost organization- Life Insurance Corporation……………………………………………25

-Diversified organization- Tata AIG…………………………………………………………………….27

ASIA- Low cost organization- Nippon Life Insurance…………………………………………………….28

- Diversified organization- Dongbu Insurance……………………………………………………….30

EUROPE- Low cost organization- AXA Insurance………………………………………………………….31

- Diversified organization- Generali Insurance…………………………………………………33

AFRICA- Low cost organization- Old Mutual Insurance………………………………………………..34

-Diversified organization- Pan Africa Insurance……………………………………………….35

NORTH AMERICA- Low cost organization- Prudential Insurance………………………………….37

-Diversified organization- Allstate Insurance…………………………………..38

SOUTH AMERICA- Low cost organization- Porto Seguro……………………………………………..40

-Diversified organization- SulAmerica……………………………………………..41

External Environment Analysis of the Industry……………………………………………………… (43-49)

PESTEL Analysis……………………………………………………………………………………………………………………..43

Industry Environment Analysis of Insurance Industry………………………………………… (50-54)

Porter’s 5 Force Model………………………………………………………………………………………………..50

SWOT Analysis………………………………………………………………………………………………………….53

Strategy of Closest Competitor (Bajaj Allianz)…………………………………………………..54

Complementary products/ services in insurance industry……………………………….. 58

History, Evolution, Growth, Profitability Rate & Future of the Industry….. (59-63)

Historical developments & evolution in the Insurance Industry……………………………………….59

Growth rate, Profitability trends & Future of the General Insurance Industry………………62

History, Evolution, Growth rate, Profitability trends & Future of Bharti AXA………………..63

Size of Insurance Industry across the world and in India…………………………………..64

Key success factors for Insurance Industry & Bharti AXA’s Performance………….67

1. Compare and Contrast the business model of your organization with:

An International Organization with a similar Business Model

A Domestic Organization with a similar Business Model

A Government Organization within the same industry

Business Model

A business model is a manager’s conception of how the set of strategies his company pursues

should mesh together into a congruent whole, enabling the company to gain a competitive

advantage and achieve superior profitability and how the various strategies and capital

investments made by a company should fit together to generate above- average profitability and

profit growth. A business model encompasses the totality of how a company will-

Select its customers

Define and differentiate its product offerings

Create value for its customers.

Acquire and keep customers.

Produce goods or services.

Lower costs

Deliver those goods and services to the market

Organize activities within the company

Configure its resources

Achieve and sustain a high level of profitability

Grow the business over time

We will look at Business model of Bharti AXA and its various competitors from the various

aspects mentioned above.

1. Business Model of Bharti AXA

Vision Statement

“To be the Preferred General Insurance Company for our Customers, Employees,

Shareholders, Business Partners & Society”

Bharti AXA GI lives by the simple truth; insurance plays an important role in protecting

organizations and individual aspirations. Through comprehensive and innovative insurance

solutions, the company seeks to redefine industry standards by offering unparalleled and

empathetic service to every Indian. This ropes in their collective vision “to be the preferred

General Insurance Company for our Customers, Employees, Shareholders, Business partners &

Society”.

Backed by its constant endeavor to find new and improved ways to add value to its customers

through its innovative product and service offerings, the company always seeks to make a

difference through its professional and pragmatic approach. Working as a team with utmost

integrity Bharti AXA strives to maintain best in class standards. It assures its customers to be by

their side in their hour of need.

Value Propositions

Innovation

Constantly striving to find new and improved ways to add value to all stake holders. Innovative

spirit has driven the company to launch revolutionary products.

Integrity

Always being responsible and doing the right thing. Settled over 4.6 lakhs + claims in five years,

a testimony to its focus on customer centricity.

Professionalism

Always seeking to make a difference. With sheer professionalism the company has managed to

surpass targets and increase its growth in leaps and bounds.

Pragmatism

Facing reality with courage and focusing on outcomes. The company’s pragmatic, realistic

approach to insurance has made it amongst the fastest growing insurers in India.

Team Work

Being one company, one diverse team. The company’s dedicated team of employees, agents,

partners and associates have enabled it to reach a milestone of 29 lakhs + policies in just five

years.

Product Offerings

Car Insurance: Bharti AXA car insurance offers protection to car, passengers, and helps stay

protected on the road. All plans enjoy servicing at 2,000+ cashless network garages across India,

24x7 claim assistance and easy claim settlement process, No Claims Bonus (NCB) up to 50% on

car insurance renewal from Bharti AXA or other insurer.

Two Wheeler Insurance: With Bharti AXA Two Wheeler Insurance enjoy servicing at

2,000+ cashless network garages across India, 24x7 claim assistance and easy claim settlement

process, No Claims Bonus (NCB) up to 50% on two wheeler insurance renewal from Bharti

AXA or other insurer.

Health Insurance: Bharti AXA offers health insurance with a range of benefits to take care of

the customer and his family's health care needs. Its Comprehensive Health Insurance is flexible

and affordable, available in 3 plans - Rs. 2 lakhs, Rs. 3 lakhs and Rs. 5 lakhs - to suit needs and

budget.

Critical Illness Insurance: Bharti AXA Critical Illness insurance covers in the event one is

diagnosed with any of the 20 critical illnesses covered. Upon diagnosis and a survival period of

30 days, it pays a lump sum compensation equivalent to the sum insured of the plan - Rs. 2 lakhs,

Rs. 3 lakhs or Rs. 5 lakhs.

Personal Accident Insurance: Personal Accident insurance is available in 3 plans - Rs. 10

lakhs, Rs. 20 lakhs and Rs. 30 lakhs - to protect one’s family with premium starting as low as Rs.

899.

Home Insurance: Bharti AXA Home Insurance protects house and valuable contents against

fire, burglary and other perils.

Organize activities within the company

The company commits itself to shaping a better tomorrow by choosing empathy over sympathy,

respect over pity, and contribution over payment; to meaningfully transform the society at large

as "we choose to care"

Global Challenge Walk: This is a part of the week long CR Week programme. The "Global

Challenge Walk" is an attempt to reduce carbon footprint as well as promote health and fitness.

Risk Education: Keeping in mind the increased need to spread awareness around gender

sensitivity and related issues, Bharti AXA GI dedicates one day of the CR Week this year as

"Risk Education Day".

Diversity and Inclusion: Bharti AXA GI is committed in promoting Diversity and Inclusion by

creating a work environment where all employees are treated with dignity and respect; and where

individual differences are valued. The D&I board is dedicated to cultivate a diverse and inclusive

environment where all employees feel fully engaged and included in our business and strategy to

become the "Preferred Company".

Communicating With the Stakeholders & Keeping Customers (Channels)

The company’s stakeholders are a diverse group of people and organizations – ranging from their

own employees to its customers. There are common threads: the requests for transparency,

honesty and respect. While they communicate with their stakeholders in many ways through

means customized to their needs, they believe that there is only one way to communicate – with

integrity.

Consumers: They provide information and receive feedback through products, website

interaction, customer satisfaction surveys, focus groups, help lines and call centers. They engage

with consumer product advocacy groups through direct communication and industry

associations.

Employees: Their employee surveys and regularly scheduled employee meetings give

employees the opportunity to express their views, and provide information at all levels across the

organization. They also regularly update their intranet portal, allowing for effective, on-demand

communication.

Shareholders: They provide information on strategies, policies and performance through their

Annual Report, Proxy Statement, Annual Shareholders Meeting, Reports and other public

statements including investor presentations.

Communities: They are in touch with the needs of local communities through philanthropic

efforts and provide support through programs, philanthropy and website interaction. They also

engage with local business and community leaders.

Sustaining high Level of Profitability

Sources of Funds: The sources of fund are from the premiums of the products mentioned above.

Net Premiums Earned

Profit/ Loss on sale/redemption of Investments

Interest, Dividend & Rent

Utilization of Funds: The funds are mainly used in settling the claims.

Net claims incurred

Commission

Operating expenses related to Insurance business

Premium Deficiency

Pool Expenses

Bharti AXA Life insurance

The insurance products by Bharti AXA Life Insurance Company Ltd include:

Wealth Confident

Future Confident

Future Confident II

Secure Confident

Save Confident

Invest Confident

Each life insurance or general insurance product of Bharti AXA Life is named confident as they

believe in making each customer 'Life Confident' giving them the assurance that the future of

their loved ones is financially secure even in their absence.

Some of its products are-

Individual Plans:

Bharti AXA Life Bright Stars: - A Unit Linked Child product. Bharti AXA Life Bright Stars

provides a launch pad for child’s bright future. They have Jumpstart benefit which is paid out at

maturity along with Policy Fund Value, which enables the child to explore more career options.

Bharti AXA Life Spot Suraksha: - Spot Suraksha helps it to create a pool of wealth to meet the

customer’s long-term needs, with an added advantage of simplified buying process.

Bharti AXA Dream Life Pension: - A Unit Linked Pension Product, Dream Life Pension,

Bharti AXA Life Insurance’s unique pension product ensures that the company’s retirement life

is the customer’s Dream Life.

Group Plans:

Bharti AXA Life – Swasthya Sanjeevani: - Swasthya Sanjeevani is a single premium group

critical illness product, providing comprehensive protection against 6 critical illnesses.

Bharti AXA Life – Sanjeevani: - Sanjeevani is a single premium group term life insurance

product, offering protection to the family.

Bharti AXA Life Mortgage Credit Shield: - Mortgage Credit Shield is a Group Product that

provides coverage to people who have availed of a Mortgage\ Home loan\ Home equity loan

from an Institution/Bank.

Bharti AXA Life Credit Shield: - Credit Shield is a Group Product that provides coverage to

people who have availed of a loan for 1 to 5 years from Group Policyholder.

Grow the Business Overtime

ISO Certification

Bharti AXA General Insurance is the first general insurance company in India to receive dual

certification of ISO 9001:2008 and ISO 27001:2005. ISO has helped in its ambition to become

the Preferred General Insurance Company in India. It proves efficiency of Bharti AXA General

Insurance in regard to core brand values like Available, Attentive & Reliable. It demonstrates

the value of strong attributes like trust of its Customers and partners.

Being ISO 27001:2005 certified means that the comply with best practices that ensure that its

customer's information is secure with it and is under explicit management control. The ISO

27001 certification provides it a top-down and consistent approach to address all compliance,

risk, and governance issues related to information security.

Customer service continues to be its focal point. The Company continues to move forward to

provide service delivery and processes, satisfying the customers and trade and establishing

standards that differentiates it from its competitors. Some of the achievements which are a

reflection of the company’s values are-

AXA has been placed as the numero uno insurer on Net Written Premiums for 2010 and ranks

second globally on assets by A.M. Best based on rating given by Best Link data.

Milestone of having sold over 29 lakh policies since inception.

Bharti AXA has consistently focused on improving service delivery mechanisms as a key

differentiator to enriching customer experience and as a testimony to this it have settled over 4.6

lakh claims, since inception. What differentiates the company is the focus it has on claims

consultancy at the beginning of the client relationship rather than at the occurrence of the loss.

2. Business Model of Allianz (International Competitor)

Mission Statement

To be the outstanding competitor in our chosen markets by delivering:

• Products and services that our clients recommend

• A great company to work for

• The best combination of profit and growth.

It is important that the company is aware of its Mission and Values to inform its choice of

actions guide the behavior and define the company and what it stands for.

The Mission of the company is best remembered by thinking about it in terms of the three

stakeholder groups whose needs the company must meet simultaneously:

• Customers – both intermediaries and policyholders – They want the company to provide them

with the products and services that meet their needs, and the ambition is to do this so well that

the customers are happy to recommend them to others.

• Ourselves – All want a great place to work; and

• Shareholder – Must use all its skills to deliver attractive returns to its shareholder, Allianz SE,

with the goal being to achieve the best combination of profit and growth amongst the peer

competitors in the UK.

The company wants to achieve its Mission:

• Through outstanding technical, sales and leadership skills

• By being professional, dynamic, innovative, focused and socially responsible

• With teamwork, passion and style!

The core values which the company delivers to its customers are-

1. Outstanding Technical, Sales and Leadership Skills

Building an organization whose people have outstanding technical, sales and leadership skills is

central to delivering for customers and thereby achieving Mission. This provides the key source

of competitive differentiation for it. It are committed to investing to develop the people and

ensuring that its skill base rises year on year.

2. Professional

To be successful it must demonstrate its professionalism by being accurate in the work, efficient,

personable and fair in all its dealings and with a continued commitment to high quality. It

supports this by helping the people work towards achieving appropriate professional

qualifications and accreditations.

3. Dynamic

Insurance is a fast moving industry, change is the norm and it needs to embrace change to be

successful. It achieves this by being proactive and moving quickly, displaying ‘hunger’ in all our

actions and in support of its customers.

4. Innovative

New ideas are essential to improve the company and it must continually innovate to make the

company better. It needs to be creative, commercially oriented and to seek entrepreneurial

solutions for the benefit of all its customers.

5. Focused

It will be clear about its objectives and what the targets are. It is then committed to the

achievement of its objectives and delivering against the promises.

6. Socially Responsible

It is mindful of the communities around it and its obligation and ability to make a positive

contribution to society and the environment. It is proactive in finding opportunities to provide

targeted support – big and small – and working to create a sustainable future.

7. Teamwork

It can only achieve the mission by working collaboratively across teams, departments and

divisions. It must also leverage the opportunities of cooperating across the wider Allianz Group,

and working with both the suppliers and customers to create and deliver outstanding solutions.

8. Passion

Having energy, enthusiasm and personal engagement, putting in the extra effort to make the

company successful through constant focus on its customers and their satisfaction.

9. Style

Ensuring the company always represents itself to a high standard and with a confidence which

distinguishes it from its competitors. Its style creates a company customers want to do business

with and talented people want to work for.

Innovative New Business Model

Allianz launched its integrated full-cycle business model based on a

new QuoteSME platform. It provides full integration between quote platforms and telephony

capability, and allows brokers to trade completely online.

Developed using the latest technology, QuoteSME will provide a wide underwriting footprint,

instant online quotations and immediate delivery of electronic documentation, all backed by the

expertise of a specialist SME underwriting team.

Fully-integrated SME business model now provides multiple routes to market, offering brokers

the flexibility required to trade successfully in a competitive market.”

Key Benefits of the new platform are-

The ability to compete new business, mid-term adjustments and renewals online.

Instant electronic documentation delivery at point of sale.

A customer centric website with easy navigation and detailed product information

Dedicated support from qualified underwriters

Ability to flex premium and/ or commission earnings

Product Offerings

Private insurance-

Family, Health

Car & motorbike

House & Home

Retirement planning

Business Insurance

Large Corporations

Small and medium-sized companies

Credit insurance

Global Lines of Business The global lines of business for Allianz are-

Reinsurance

Employee benefits

Company health insurance

Direct Insurance

Life insurance

Real estate

Internal shared services

Some of the sustainable solutions provided by Allianz are-

Microinsurance

Insurance & services

Investment & other products

Strategy

There are 5 goals of the group strategy. They are-

1. Profitable and sustainable growth

Seek profitable and sustainable growth in three business segments: Property-Casualty insurance,

Life/ Health insurance, and Asset Management.

2. Well-balanced and synergetic business portfolio

The company’s segments and operating entities complement and enrich each other, primarily by

serving the diverse needs of its customers. It exploits the group-wide synergies that stem from its

strong brand, its capital allocation, functional and industry best practices, as well as from shared

operations and joint investments in technology.

3. Strong capitalization

Strive to protect the capital of its investors and to support its businesses with sufficient capital to

withstand shocks and to protect the wellbeing of the customers.

4. World-class investment management

Qualitative growth and solid capitalization depend on a sound and sustainable investment

strategy that can generate stable returns and compensate, if necessary, for low interest rates or

looming inflation.

5. State-of-the-art risk framework

Through the risk policies, guidelines and systems the company ensures that its investment,

underwriting and operational decisions are made within the limits of its carefully defined

appetite and tolerance for foreseeable risks.

3. Business Model of New India Assurance (Government Organization)

Vision

To be the most respected, trusted and preferred Non-life Insurer in the Global markets we

operate.

Mission

To develop General Insurance Business in the best interest of the community.

To provide Financial Security to Individuals, Trade, Commerce & all other segments of the

Society by offering Insurance products & Services of High Quality at affordable Cost.

Values delivered to the Customers

The values delivered by New India Assurance Co. Ltd. Are-

Highest priority to Customers needs

High standards of Public Conduct

Transparency in operations

Culture of the Organization

The company provides for a very friendly culture to its employees. They are-

Courtesy and Caring

Initiatives and Innovation

Integrity, Trustworthiness and Reliability

Commitments

The company is highly committed to its customers and is customer centric. It promises to-

Act courteously, fairly and reasonably in all its dealings with the customers.

Make sure all the policy documents and claim procedures are clear and complete

information is given about the products and services.

Deal quickly and sympathetically with the grievances of the customer and resolve efficiently

through nominated customer service officers in all operating offices.

Educate the client about grievance redressal mechanism including the system of grievance

redressal through Ombudsman.

Respond to all commercially viable General Insurance requirements of all categories

including products for weaker section of the society at affordable price within 3 months

from the date of such requirement.

Continue to develop a dedicated, sensitized and professional workforce for efficient

execution of roles assigned to them.

Have a regular monitoring and consultative process with all the service providers and set up

monitoring mechanism for delivery of promised services to its customers.

Standards for Access to Citizens

The company commits to-

Host on its website http://newindia.co.in for all relevant information relating to working

hours, contact nos., documents required for issuance of policies and claim settlement.

Make available information on products and services through display in office, information

kiosks, Brochures relating to the Products and Services in Regional Languages and in easy

to understand 'style'.

Reach out through electronic and print media, intermediaries and other active

communication channels available.

Enhance the access of citizens through helpline, call centre, portal and personalized

interactions through Retail customers Meets.

Standards for Servicing

The company gives utmost importance to service. In this regard it commits to-

Strive to achieve and excel the time lines/bench mark set forth by the regulator in respect of

policyholders servicing.

Be clear and transparent in seeking fulfillment of requirements for settling a claim or any

other services to the customer.

Standards and Fairness and Openness

The company is very fair and open as far as any disclosure is concerned. It commits to-

Enable the customers with opportunities to provide the organization with feedback on

services availed by them and suggest improvement through customer meets surveys, web

and interactive voice response system (IVRS). It has established call centre and also direct

customer on line, dedicated e-mail facility at suggestions (at) newindia.co.in through which

customers can provide their suggestion for betterment of service.

Enhance customer satisfaction through adoption of latest technologies in the area of

servicing processing and review of systems and methods.

Strengths

Largest number of Offices - In India and Abroad Trained and technically qualified staff 1085 fully

computerized offices across India. "A-" (Excellent) rating by A.M.Best & Co (Europe) First domestic

company to be rated by an International Rating Agency Rating based upon following factors:

Superior capital position, Strong operating performance, and strong market position. Only company

to develop significant International operations, long record of successful trading outside India.

Products Offered By New India Assurance

a. Personal Insurance

New India Floater Mediclaim policy

Personal Accident Policy

Motor Policy

Group Mediclaim Policy

b. Commercial Insurance

Shopkeeper’s policy

Aviation Insurance

Marine cargo policy

Jewelers block policy

c. Industrial Insurance

d. Liability Insurance

e. Social Insurance

4. Business Model of Bajaj Allianz (Domestic Competitor)

Vision

To be the first choice insurer for customers

To be the preferred employer for staff in the insurance industry

To be the number one insurer for creating shareholder value

Mission

As a responsible, customer focused market leader, we will strive to understand the insurance needs of

the consumers and translate it into affordable products that deliver value for money.

Partnership Based on Synergy

Bajaj Allianz General Insurance offers technical excellence in all areas of General and Health

Insurance as well as Risk Management. This partnership successfully combines Bajaj Finserv's in

depth understanding of the local market and extensive distribution network with the global experience

and technical expertise of the Allianz Group. As a registered Indian Insurance Company and a capital

base of Rs. 110 crores, the company is fully licensed to underwrite all lines of general insurance

business including health insurance.

Values Delivered to Customers

Customer First, Always

Treat all customers with warmth and respect

Understand and manage customer expectations

Listen and are empathetic to the customer

Engage with the customer in the long term

Spirit of Adventure

Lead change

Look for opportunities to innovate at every level

Empower others to take responsible decisions

Show tolerance for failure

Trust

Are accessible to all

Are fair and transparent

Are open to feedback

Keep commitments

Trust each other to do a good job and give due credit

Own up to mistakes

Shared Ownership

Take collective ownership for success and failure

Respect divergent views and own the decisions taken

Put organizational interest above team & individual interests

Consciously include and respect people from different backgrounds

High Standards

Set new benchmarks of excellence

Are open to new ideas for raising the bar

Take pride in our work and excel in what we do

Products offered by Bajaj Allianz

Life insurance

Health insurance

Motor insurance

Travel insurance

Home insurance

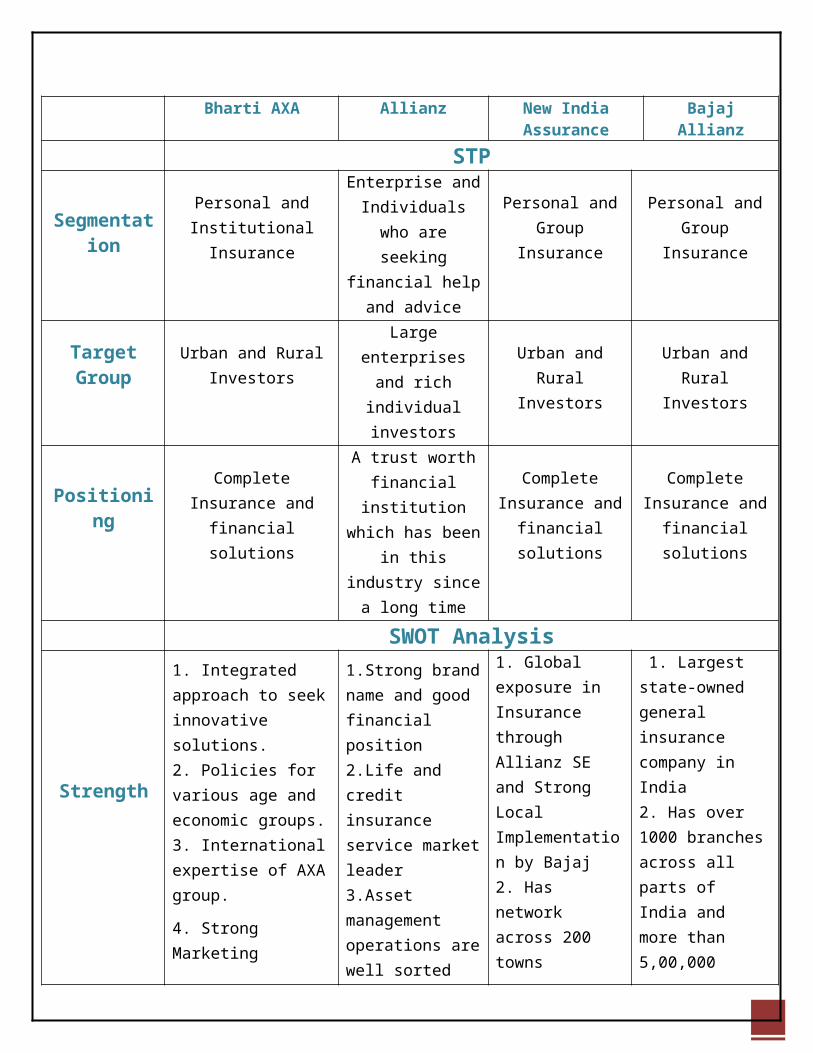

Comparision between Bharti AXA and its Competitors

Bharti AXA Allianz New India Assurance

Bajaj Allianz

STPEnterprise and

SegmentationPersonal and

Institutional InsuranceIndividuals who are

seeking financial help and advice

Personal and Group Insurance

Personal and Group Insurance

Target Group

Urban and Rural Investors

Large enterprises and rich individual

investorsUrban and Rural

InvestorsUrban and Rural

Investors

PositioningComplete Insurance and

financial solutions

A trust worth financial institution which has been in

this industry since a long time

Complete Insurance and financial

solutions

Complete Insurance and financial

solutions

SWOT Analysis

Strength

1. Integrated approach to seek innovative solutions.2. Policies for various age and economic groups.3. International expertise of AXA group.

4. Strong Marketing Campaign.5. 74% stake from Bharti and 26% stake from AXA Asia Pacific Holdings Ltd.

1.Strong brand name and good financial position2.Life and credit insurance service market leader3.Asset management operations are well sorted out4.Has over 150,000 employees

1. Global exposure in Insurance through Allianz SE and Strong Local Implementation by Bajaj2. Has network across 200 towns3. Fundamentally Strong with good paying Capabilities4. Allianz AG is an insurance conglomerate globally and one of the largest asset managers in the world.

1. Largest state-owned general insurance company in India2. Has over 1000 branches across all parts of India and more than 5,00,000 agents.

3. Has over 40,000 employees across India

Weakness

1. Less penetration in rural India.

2. Small agent base.3. Insurance companies have a poor image when it comes to payment of dues.

1. Heavily dependent on automobile market

2.Stiff competition with other major players

3.Controversies during the world war II

1. Lack of penetration in rural areas.

2. Smaller Infrastructure as compared to established players

1. It has an image of a Government agency and hence lacks innovation.2. Being a Government agency, red tape and bureaucracy causes problems3. Managing a huge workforce during economic crisis meant overburdened

due to salaries

Opportunity

1. Growing rural market2. Earning Urban Youth

3. Cross selling through financial services such as banking

1.Expansion in other countries2.Diversifying portfolios for customers3.Retirement benefits on the boom4.Innovative schemes

1. Growing rural market potential

2. Urban Youth with growing income

1. Use of Technology to provide effective services to cater to urban population.

2. Government Schemes implementation

Threat

1. Stringent Economic measures by Government and RBI2. Entry of new NBFCs in the sector

1.Changing govt regulations and financial crisis like recessions2.Natural disasters3.Increase in fraud cases

1. Economic crisis and economic instability

2. Entry of new NBFCs in the sector

3. Increasing awareness amongst people about securing their future

1. Economic crisis.

2. Entry of new NBFCs in the sector.

3. Varying Govt policies

2. Prepare an Activity System Map for both a Low Cost Organization as well

a Diversified Organization operating in the Industry/ Sector selected.

Activity System Map

Managers often find it difficult to identify with any clarity the strategic capability of their

organization. Too often they highlight capabilities not valued by customers but seen as important

within the organization, perhaps because they were valuable in the past. Or they highlight what

are, in fact, critical success factors (product features particularly valued by customers) like ‘good

service’ or ‘reliable delivery’, whereas strategic capability is about the resources, processes and

activities that underpin the ability to meet such critical success factors. Or they identify

capabilities at too generic a level. This is not surprising given that strategic capability may well

be embedded in a complex set of linked activities. But if they are to be managed proactively,

finding a way of identifying and understanding capabilities and the linkages that are likely to

characterize competences is important. One way of undertaking such diagnosis is by means of

an activity system map that tries to show how the different activities of an organization are

linked together.

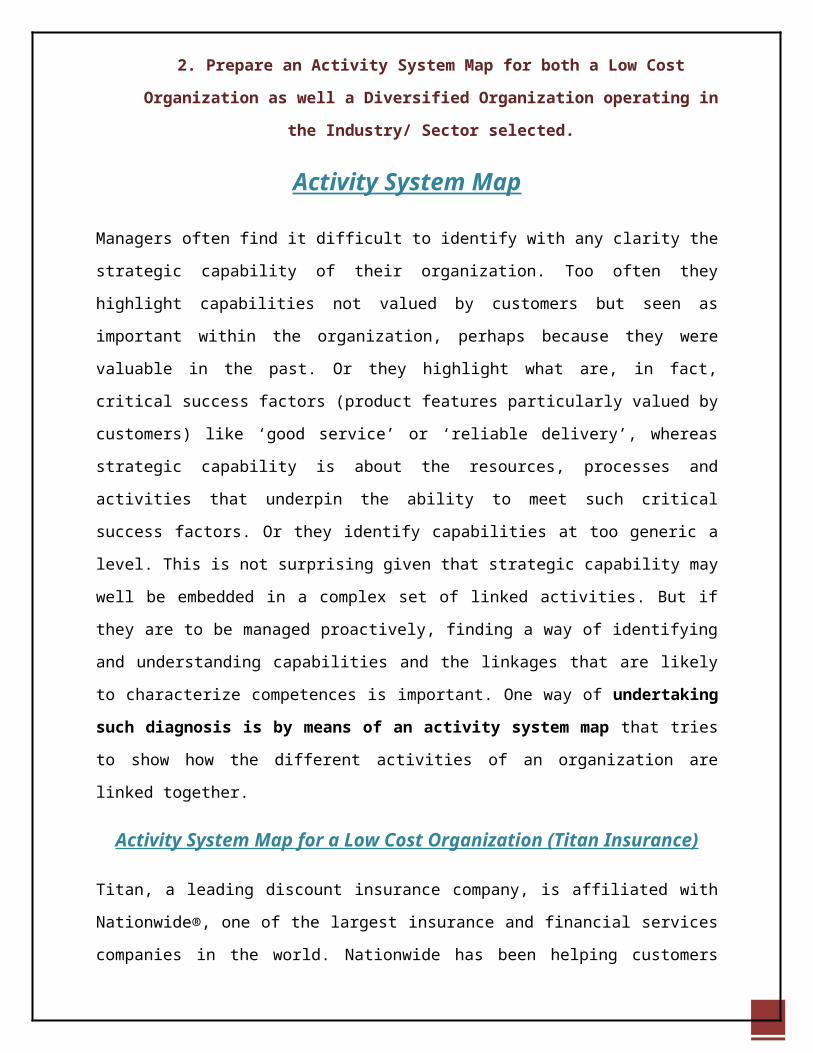

Activity System Map for a Low Cost Organization (Titan Insurance)

Titan, a leading discount insurance company, is affiliated with Nationwide®, one of the largest

insurance and financial services companies in the world. Nationwide has been helping customers

protect what's most important to them and providing outstanding customer service .

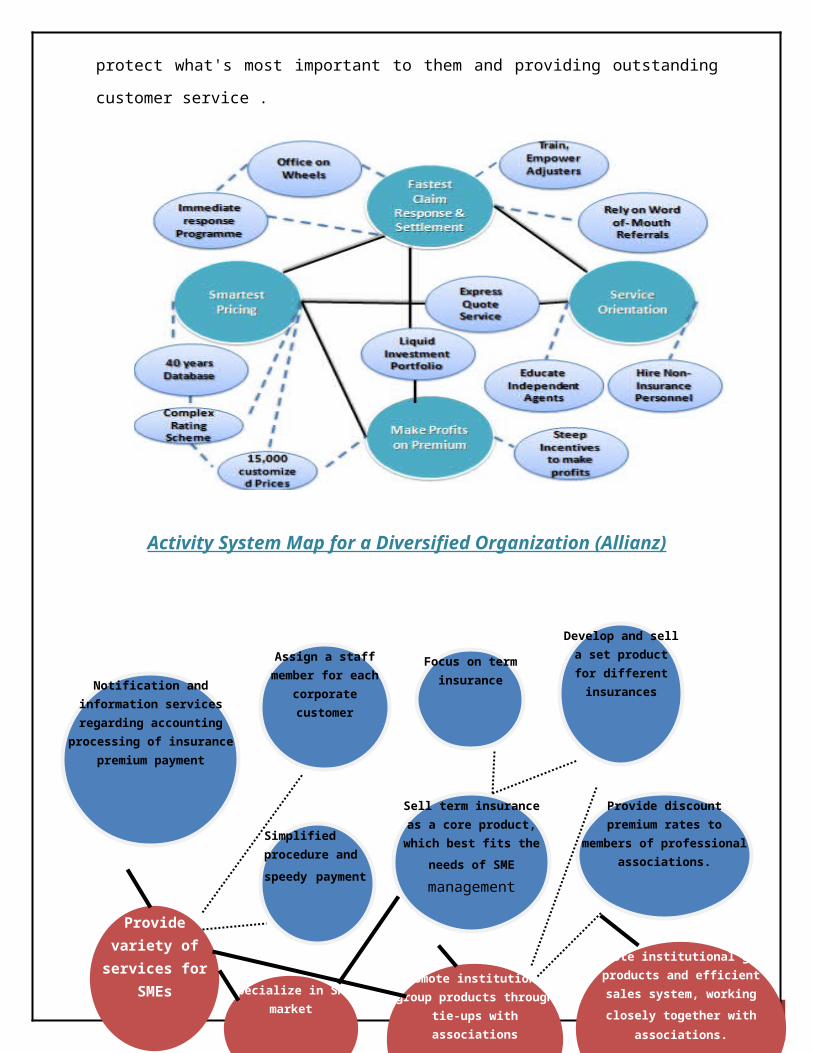

Activity System Map for a Diversified Organization (Allianz)

n

Notification and information services regarding accounting

processing of insurance premium payment

Sell term insurance as a core product, which best fits the

needs of SME

management

Simplified procedure

and speedy payment

Assign a staff member for each corporate

customer

Provide discount premium rates to members of professional

associations.

Focus on term insurance

Develop and sell a set product for different

insurances

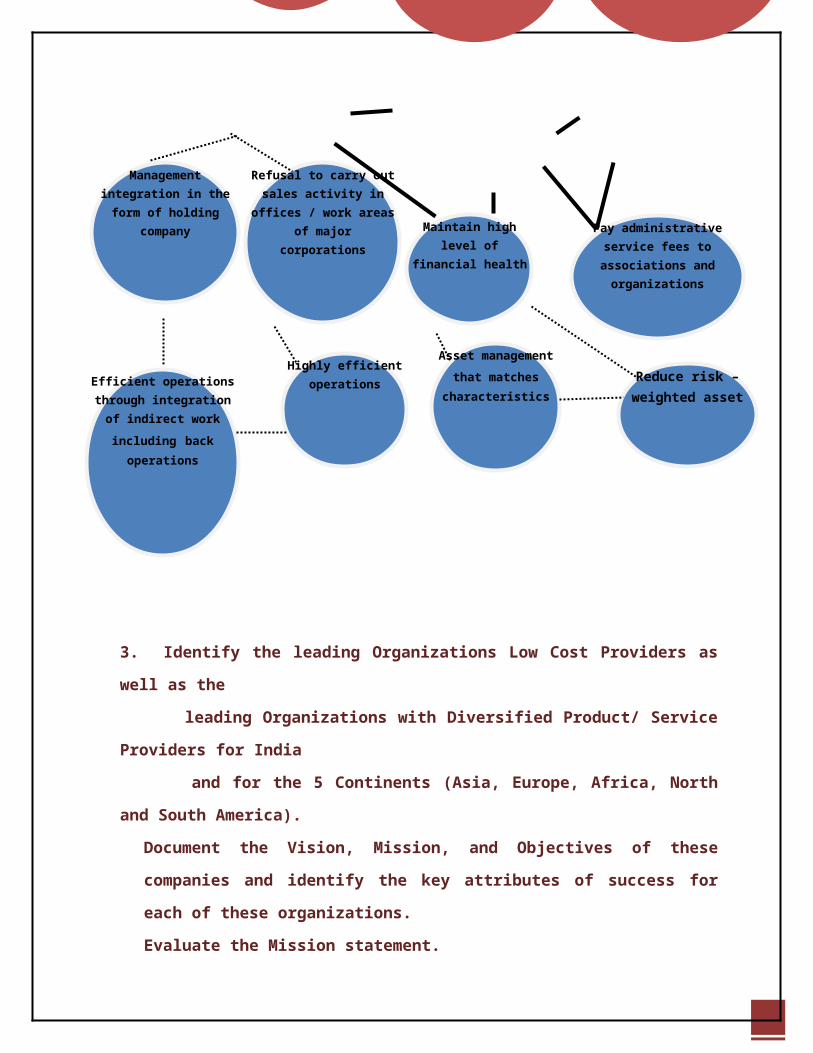

3. Identify the leading Organizations Low Cost Providers as well as the

leading Organizations with Diversified Product/ Service Providers for India

and for the 5 Continents (Asia, Europe, Africa, North and South America).

Document the Vision, Mission, and Objectives of these companies and

identify the key attributes of success for each of these organizations.

Evaluate the Mission statement.

Prepare the Strategy Statements and identify the Value Proposition and

Strategy Sweet Spots.

1. INDIA

Sell term insurance as a core product, which best fits the

needs of SME

management

Simplified procedure

and speedy payment

Provide variety of services for SMEs

Specialize in SME market

Reduce risk –weighted asset

Promote institutional group products through tie-ups with

associations

Maintain high level of financial health

Refusal to carry out sales activity in offices / work

areas of major corporations

Management integration in the form of holding

companyPay administrative service fees

to associations and organizations

Asset management that

matches characteristicsHighly efficient

operationsEfficient operations through integration of indirect work

including back operations

Promote institutional group products and efficient sales system, working

closely together with associations.

Provide discount premium rates to members of professional

associations.

a. Low Cost Service Provider in India (Life Insurance Corporation)

Vision

"A trans-nationally competitive financial conglomerate of significance to societies and Pride of

India.

Mission

"Explore and enhance the quality of life of people through financial security by providing

products and services of aspired attributes with competitive returns, and by rendering resources

for economic development."

Objectives

Spread Life Insurance widely and in particular to the rural areas and to the socially and

economically backward classes with a view to reaching all insurable persons in the country

and providing them adequate financial cover against death at a reasonable cost.

Maximize mobilization of people's savings by making insurance-linked savings adequately

attractive.

Bear in mind, in the investment of funds, the primary obligation to its policyholders, whose

money it holds in trust, without losing sight of the interest of the community as a whole; the

funds to be deployed to the best advantage of the investors as well as the community as a

whole, keeping in view national priorities and obligations of attractive return.

Conduct business with utmost economy and with the full realization that the moneys belong

to the policyholders.

Act as trustees of the insured public in their individual and collective capacities.

Meet the various life insurance needs of the community that would arise in the changing

social and economic environment.

Involve all people working in the Corporation to the best of their capability in furthering

the interests of the insured public by providing efficient service with courtesy.

Promote amongst all agents and employees of the Corporation a sense of participation,

pride and job satisfaction through discharge of their duties with dedication towards

achievement of Corporate Objective

Key Success Factors

Claims settlement is the major factor for the success of LIC as its claims settlement operations

are transparent and fair. The corporation looks for reasons to settle claims rather than avoid

making payments on claims. In short, LIC's ability to withstand competitive pressure in the

market can largely be attributed to its positive and proactive claims settlement operations.

Prompt and timely settlement of claims help in enhancing the confidence of policyholders in

insurance company; thereby, the business of the latter will increase manifold.

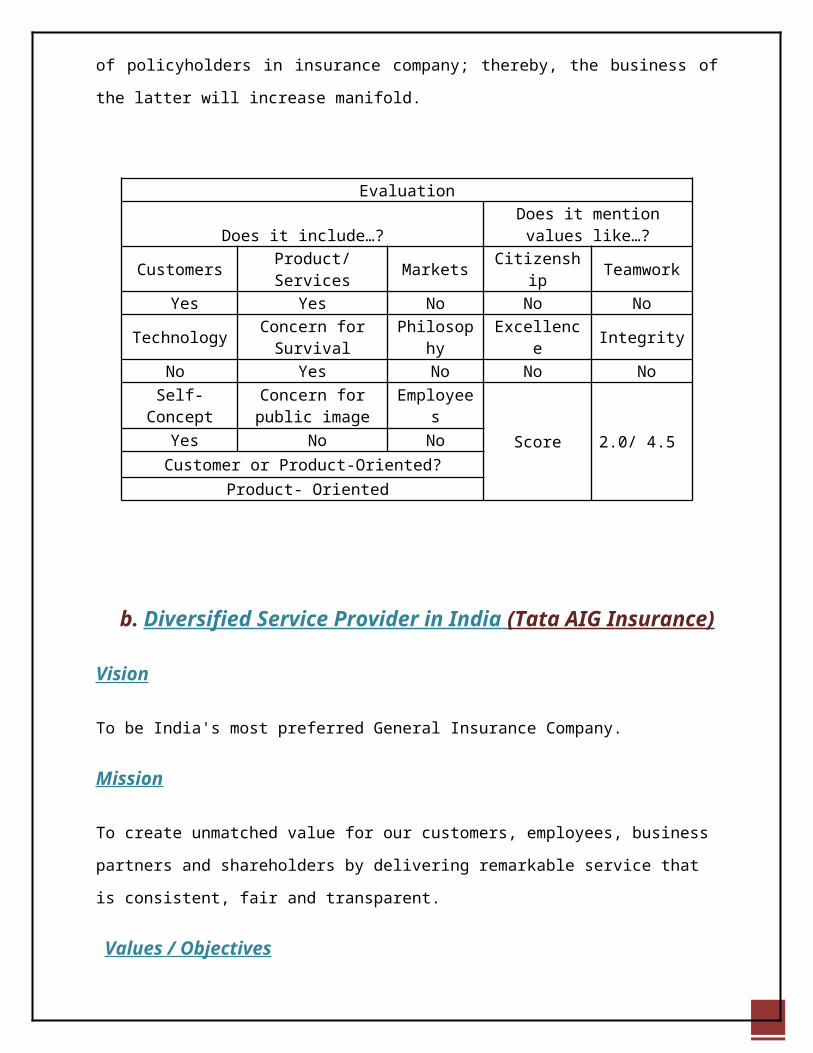

Evaluation

Does it include…?Does it mention values

like…?

CustomersProduct/Services

Markets Citizenship Teamwork

Yes Yes No No No

TechnologyConcern for

SurvivalPhilosoph

yExcellence Integrity

No Yes No No No

Self- Concept

Concern for public image

Employees

Score 2.0/ 4.5 Yes No No

Customer or Product-Oriented?

Product- Oriented

b. Diversified Service Provider in India (Tata AIG Insurance)

Vision

To be India's most preferred General Insurance Company.

Mission

To create unmatched value for our customers, employees, business partners and shareholders by

delivering remarkable service that is consistent, fair and transparent.

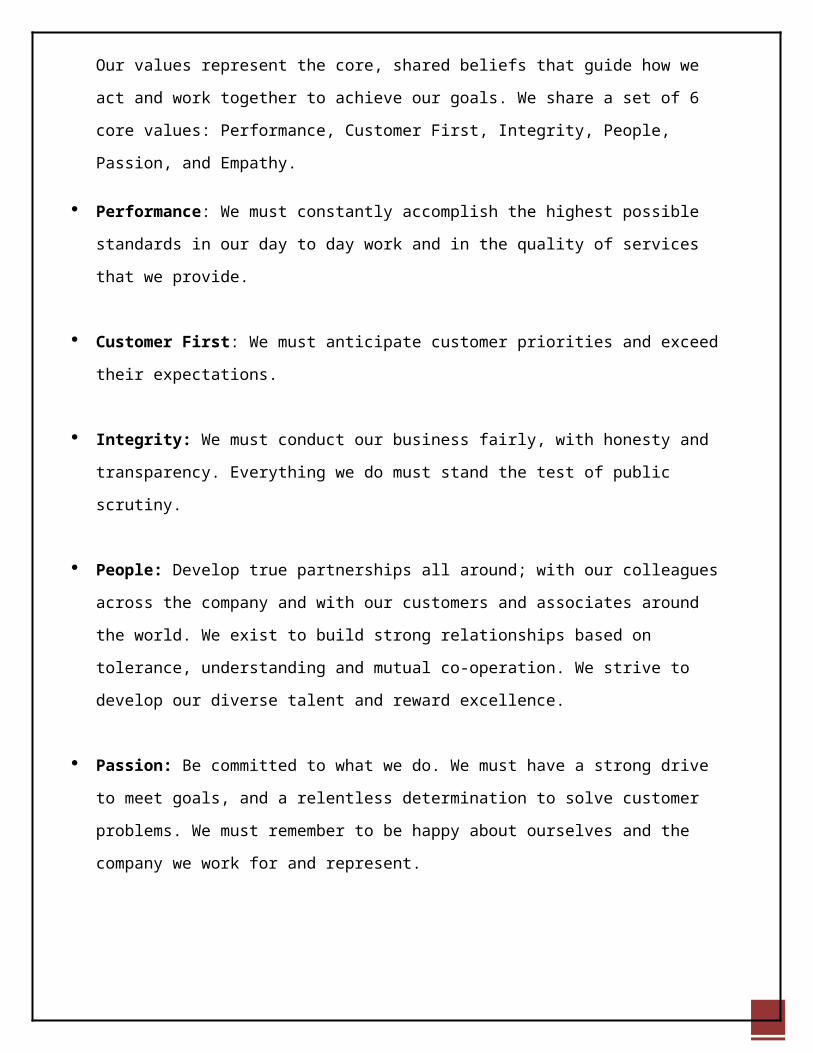

Values / Objectives

Our values represent the core, shared beliefs that guide how we act and work together to achieve

our goals. We share a set of 6 core values: Performance, Customer First, Integrity, People,

Passion, and Empathy.

Performance: We must constantly accomplish the highest possible standards in our day to day

work and in the quality of services that we provide.

Customer First: We must anticipate customer priorities and exceed their expectations.

Integrity: We must conduct our business fairly, with honesty and transparency. Everything we

do must stand the test of public scrutiny.

People: Develop true partnerships all around; with our colleagues across the company and with

our customers and associates around the world. We exist to build strong relationships based on

tolerance, understanding and mutual co-operation. We strive to develop our diverse talent and

reward excellence.

Passion: Be committed to what we do. We must have a strong drive to meet goals, and a

relentless determination to solve customer problems. We must remember to be happy about

ourselves and the company we work for and represent.

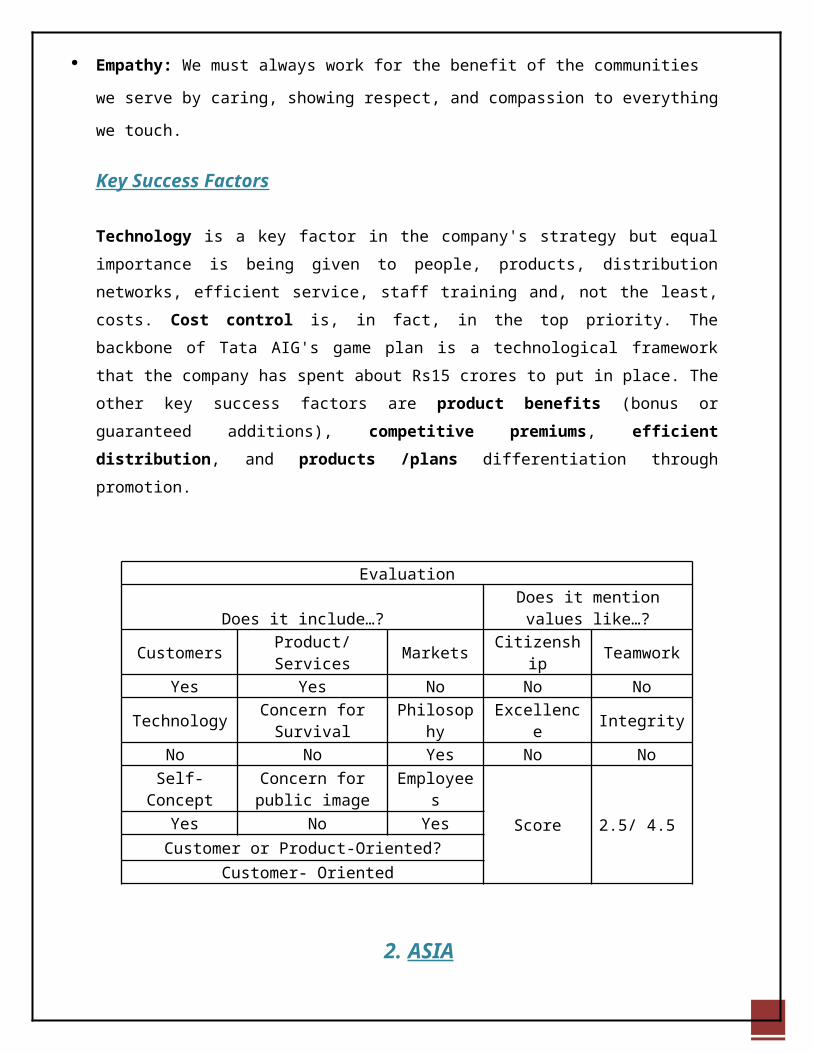

Empathy: We must always work for the benefit of the communities we serve by caring, showing

respect, and compassion to everything we touch.

Key Success Factors

Technology is a key factor in the company's strategy but equal importance is being given to

people, products, distribution networks, efficient service, staff training and, not the least, costs.

Cost control is, in fact, in the top priority. The backbone of Tata AIG's game plan is a

technological framework that the company has spent about Rs15 crores to put in place. The other

key success factors are product benefits (bonus or guaranteed additions), competitive

premiums, efficient distribution, and products /plans differentiation through promotion.

Evaluation

Does it include…?Does it mention values

like…?

CustomersProduct/Services

Markets Citizenship Teamwork

Yes Yes No No No

TechnologyConcern for

SurvivalPhilosoph

yExcellence Integrity

No No Yes No No

Self- Concept

Concern for public image

Employees

Score 2.5/ 4.5 Yes No Yes

Customer or Product-Oriented?

Customer- Oriented

2. ASIA

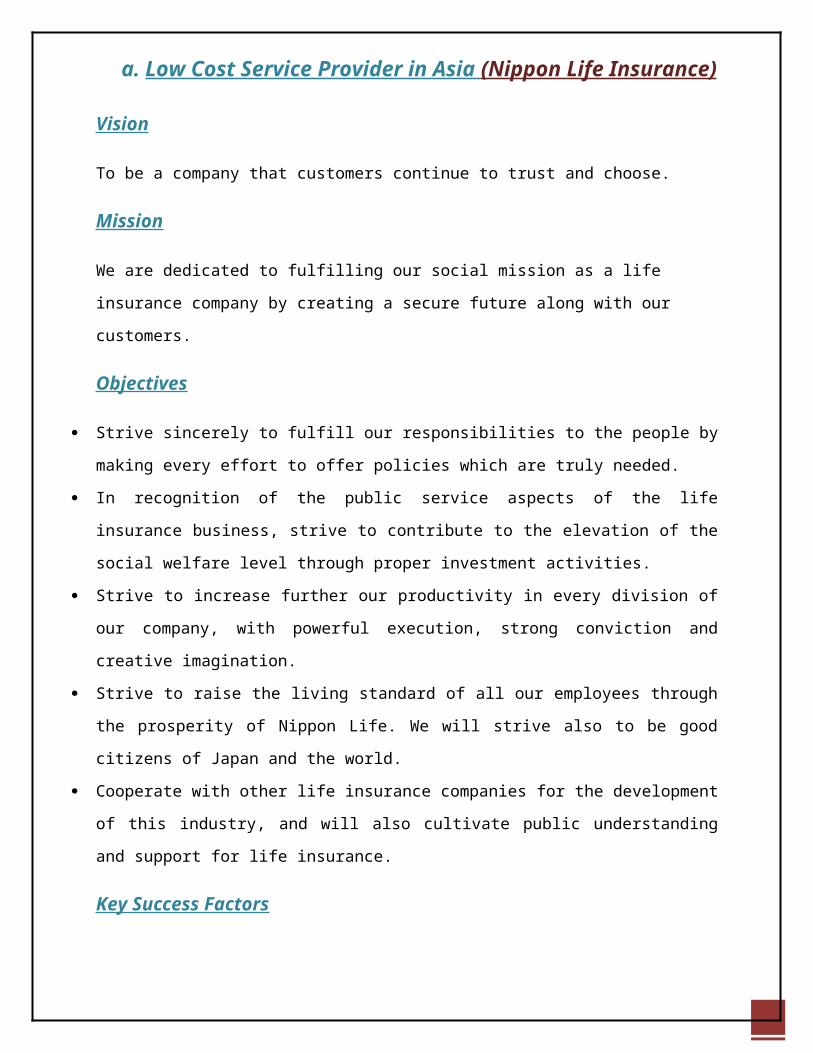

a. Low Cost Service Provider in Asia (Nippon Life Insurance)

Vision

To be a company that customers continue to trust and choose.

Mission

We are dedicated to fulfilling our social mission as a life insurance company by creating a secure

future along with our customers.

Objectives

Strive sincerely to fulfill our responsibilities to the people by making every effort to offer

policies which are truly needed.

In recognition of the public service aspects of the life insurance business, strive to contribute to

the elevation of the social welfare level through proper investment activities.

Strive to increase further our productivity in every division of our company, with powerful

execution, strong conviction and creative imagination.

Strive to raise the living standard of all our employees through the prosperity of Nippon Life. We

will strive also to be good citizens of Japan and the world.

Cooperate with other life insurance companies for the development of this industry, and will also

cultivate public understanding and support for life insurance.

Key Success Factors

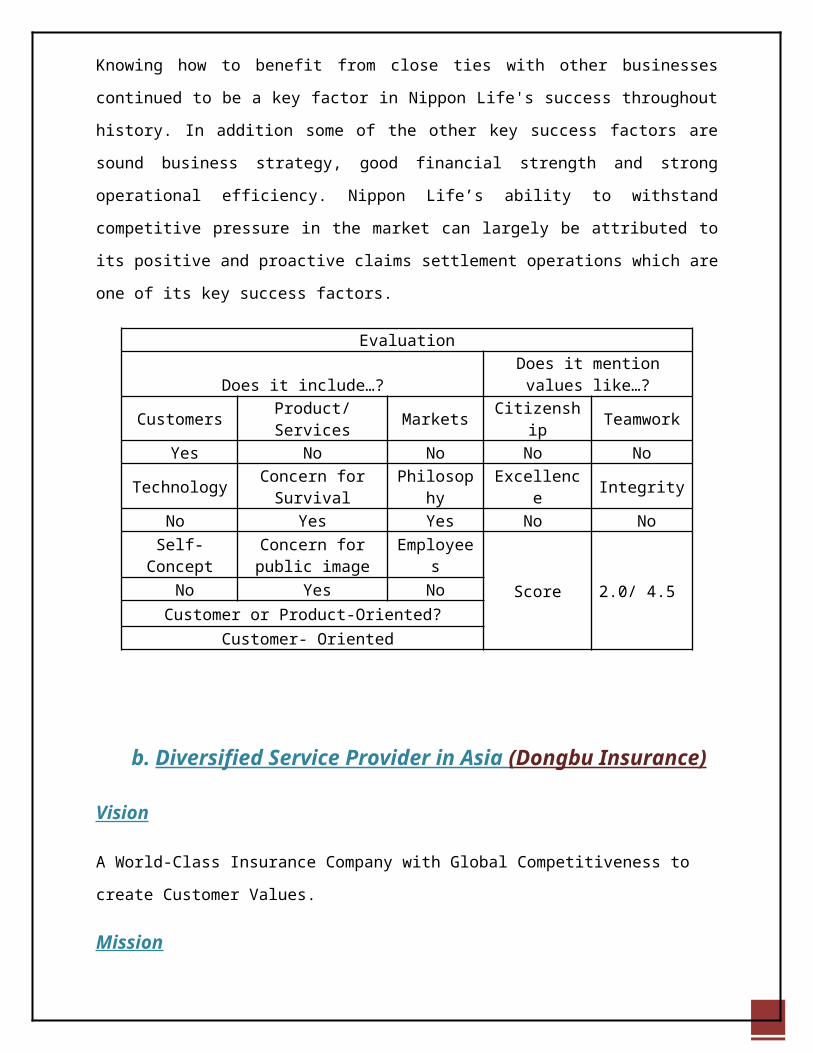

Knowing how to benefit from close ties with other businesses continued to be a key factor in

Nippon Life's success throughout history. In addition some of the other key success factors are

sound business strategy, good financial strength and strong operational efficiency. Nippon Life’s

ability to withstand competitive pressure in the market can largely be attributed to its positive

and proactive claims settlement operations which are one of its key success factors.

Evaluation

Does it include…?Does it mention values

like…?

CustomersProduct/Services

Markets Citizenship Teamwork

Yes No No No No

TechnologyConcern for

SurvivalPhilosoph

yExcellence Integrity

No Yes Yes No No

Self- Concept

Concern for public image

Employees

Score 2.0/ 4.5 No Yes No

Customer or Product-Oriented?

Customer- Oriented

b. Diversified Service Provider in Asia (Dongbu Insurance)

Vision

A World-Class Insurance Company with Global Competitiveness to create Customer Values.

Mission

A top-notch company with sustainable growth driven by customer satisfaction and maximize

customer values by-

Completion of customer protection structure.

Customer service that exceeds their expectation

Boost brand image.

Objectives

Establish world class asset management competence

Expand overseas

Construct global- standard business infrastructure.

Secure unrivaled business efficiency.

Identify new business models in line with the core business.

Hire and nurture specialists.

Expand blue-chip customer base.

Enhance channel productivity.

Key Success Factors

Sound business strategy, good financial strength and strong operational efficiency continue to

be key factors in Dongbu Insurance success. Ability to withstand competitive pressure in the

market is one of its key success factors. People, products, distribution networks, efficient

service, staff training are other key factors.

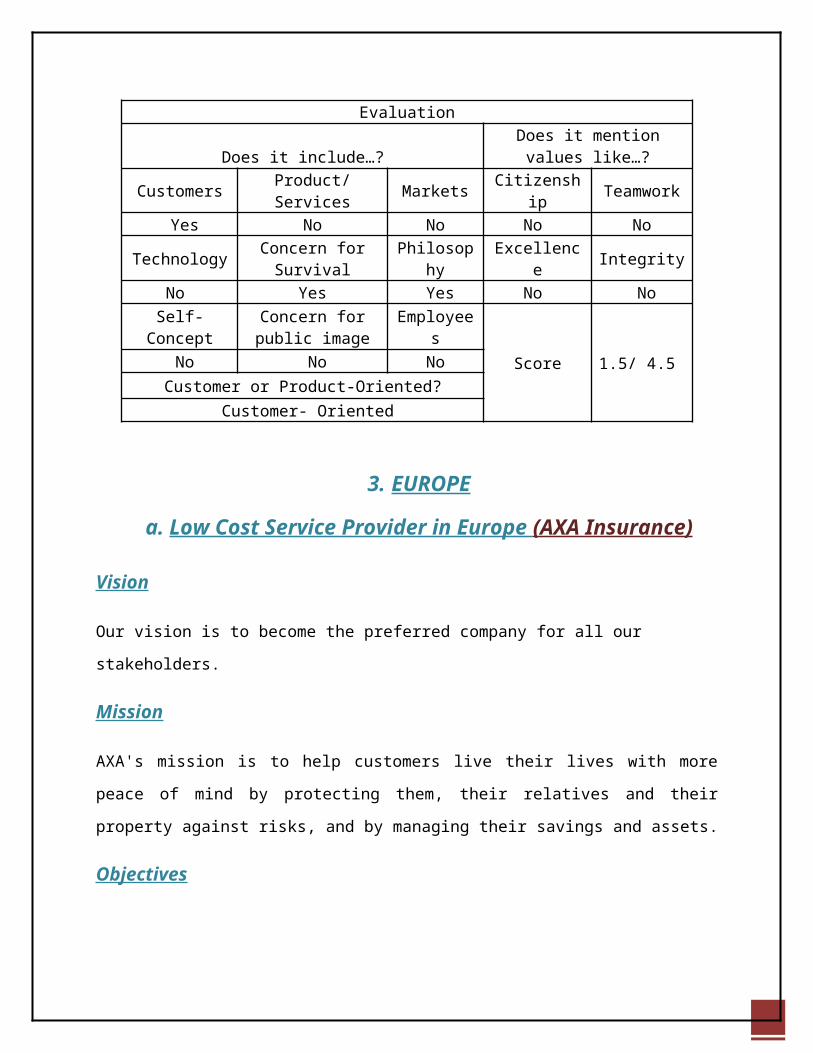

Evaluation

Does it include…?Does it mention values

like…?

CustomersProduct/Services

Markets Citizenship Teamwork

Yes No No No No

TechnologyConcern for

SurvivalPhilosoph

yExcellence Integrity

No Yes Yes No No

Self- Concept

Concern for public image

Employees

Score 1.5/ 4.5 No No No

Customer or Product-Oriented?

Customer- Oriented

3. EUROPE

a. Low Cost Service Provider in Europe (AXA Insurance)

Vision

Our vision is to become the preferred company for all our stakeholders.

Mission

AXA's mission is to help customers live their lives with more peace of mind by protecting them,

their relatives and their property against risks, and by managing their savings and assets.

Objectives

Continue the in-depth work on strengthening focus on the customer and fostering employee

involvement through building a culture of trust and achievement.

Responsibility to leverage skills, resources and risk expertise to build a stronger and safer

society.

Focus on core business - insurance and asset management - and aim to become the preferred

company of our key stakeholders.

Reinforce customer centricity and promote the engagement of our employees by rethinking our

corporate culture.

Committed to redefining the standards of business so as to truly differentiate ourselves and earn

the trust of our key stakeholders.

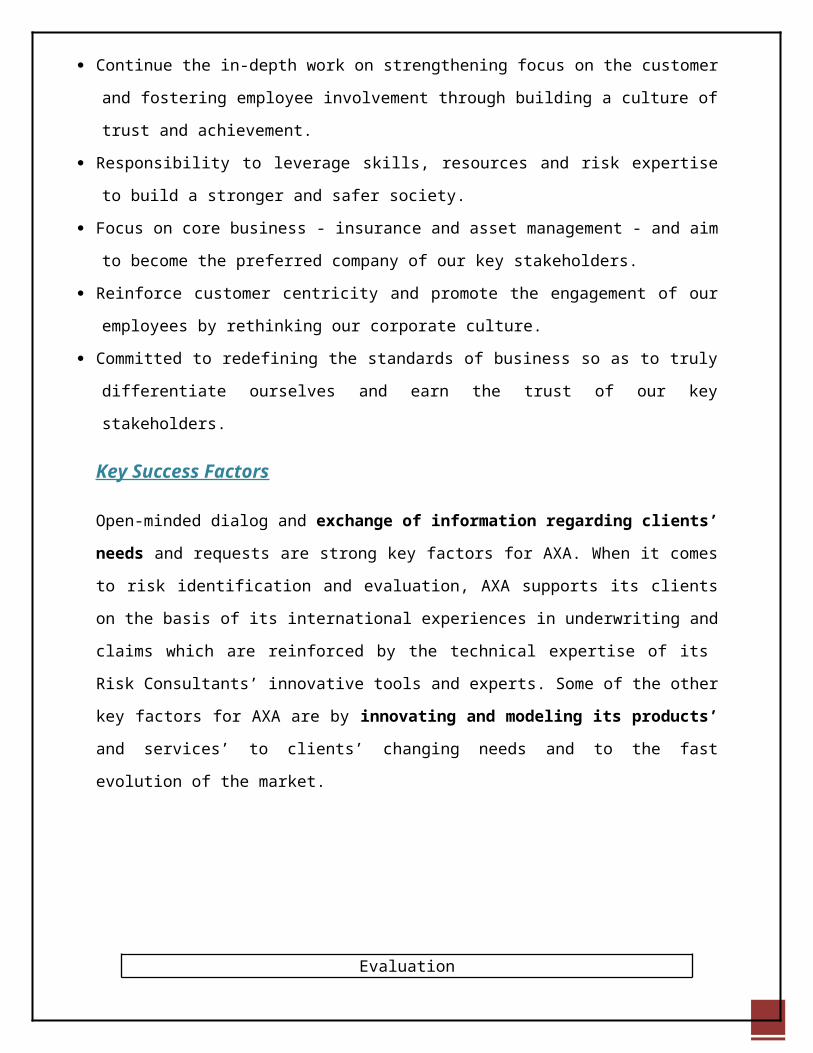

Key Success Factors

Open-minded dialog and exchange of information regarding clients’ needs and requests are

strong key factors for AXA. When it comes to risk identification and evaluation, AXA supports

its clients on the basis of its international experiences in underwriting and claims which are

reinforced by the technical expertise of its Risk Consultants’ innovative tools and experts. Some

of the other key factors for AXA are by innovating and modeling its products’ and services’ to

clients’ changing needs and to the fast evolution of the market.

Evaluation

Does it include…?Does it mention values

like…?

CustomersProduct/Services

Markets Citizenship Teamwork

Yes No No No No

TechnologyConcern for

SurvivalPhilosoph

yExcellence Integrity

No No Yes No No

Self- Concept

Concern for public image

Employees

Score 1.0/ 4.5 No No No

Customer or Product-Oriented?

Customer- Oriented

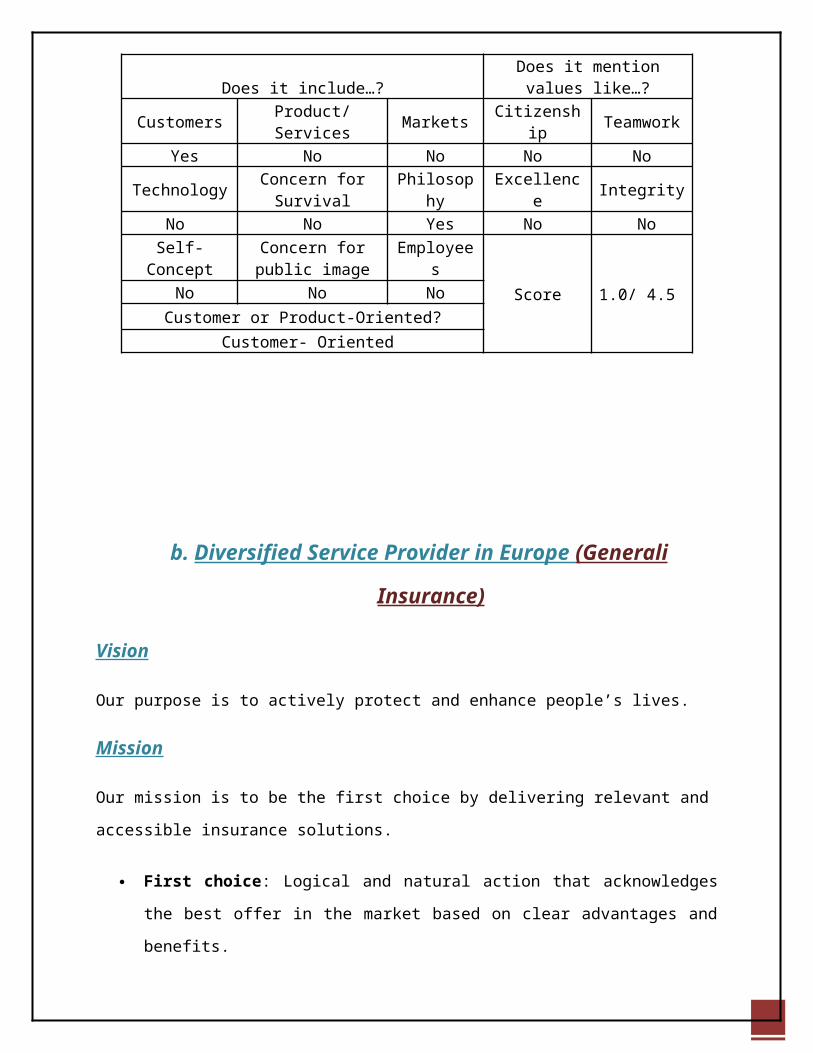

b. Diversified Service Provider in Europe (Generali Insurance)

Vision

Our purpose is to actively protect and enhance people’s lives.

Mission

Our mission is to be the first choice by delivering relevant and accessible insurance solutions.

First choice: Logical and natural action that acknowledges the best offer in the market

based on clear advantages and benefits.

Delivering: We ensure achievement striving for the highest performance.

Relevant: Anticipating or fulfilling a real life need or opportunity, tailored to local and

personal needs and habits, perceived as valuable.

Accessible: Simple, first of all, and easy to find, to understand and to use; always

available, at a competitive value for money.

Insurance solutions: We aim at offering and tailoring a bright combination of protection,

advice and service.

Objectives

Strategic Objective -To pursue the Group's growth objectives by creating, together with

economic value, social and environmental value for all stakeholders

Operational Objective - To provide access to insurance for those excluded from the traditional

market due to their income status.

Group Commitment- Greater distribution of micro insurance products that meet the specific

needs of the working poor in the countries where the Group operates.

Deliver on the promise-

Tie a long-term contract of mutual trust with our people, clients and stakeholders; all of

our work is about improving the lives of our clients.

To commit with discipline and integrity to bringing this promise to life and making an

impact within a long lasting relationship.

Key Success Factors

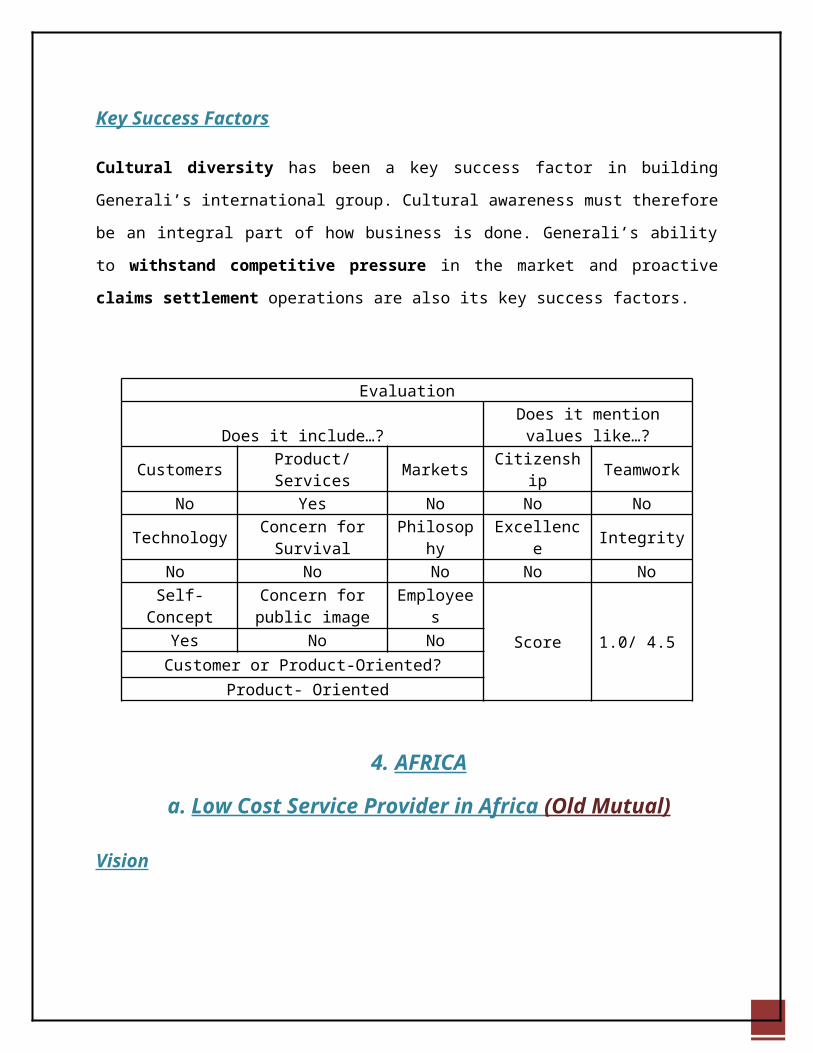

Cultural diversity has been a key success factor in building Generali’s international group.

Cultural awareness must therefore be an integral part of how business is done. Generali’s ability

to withstand competitive pressure in the market and proactive claims settlement operations

are also its key success factors.

Evaluation

Does it include…?Does it mention values

like…?

CustomersProduct/Services

Markets Citizenship Teamwork

No Yes No No No

TechnologyConcern for

SurvivalPhilosoph

yExcellence Integrity

No No No No No

Self- Concept

Concern for public image

Employees

Score 1.0/ 4.5 Yes No No

Customer or Product-Oriented?

Product- Oriented

4. AFRICA

a. Low Cost Service Provider in Africa (Old Mutual)

Vision

Our vision is to be our customers' most trusted partner - passionate about helping them achieve

their lifetime financial goals.

Mission

Our mission is to drive strategic growth, through leveraging the strength of our people and

through accelerating collaboration between our businesses. Our focus is to expand in South

Africa, Africa and other selected emerging markets; and to improve and grow Old Mutual

Wealth and US Asset Management.

Objectives

Deliver on customer promise

Drive profitable growth in core

Accelerate collaboration across the Group

Build a culture of excellence

Key Success Factors

Innovating and modeling its products’ and services’ to clients’ changing needs and to the fast

evolution of the market are critical success factors for Old Mutual. People, products,

distribution networks, efficient service are other key factors.

Evaluation

Does it include…?Does it mention values like…?

CustomersProduct/Services

MarketsCitizenshi

pTeamwor

k Yes No Yes No No

Technology

Concern for Survival

Philosophy

Excellence

Integrity

No Yes No No NoSelf-

ConceptConcern for public image

Employees

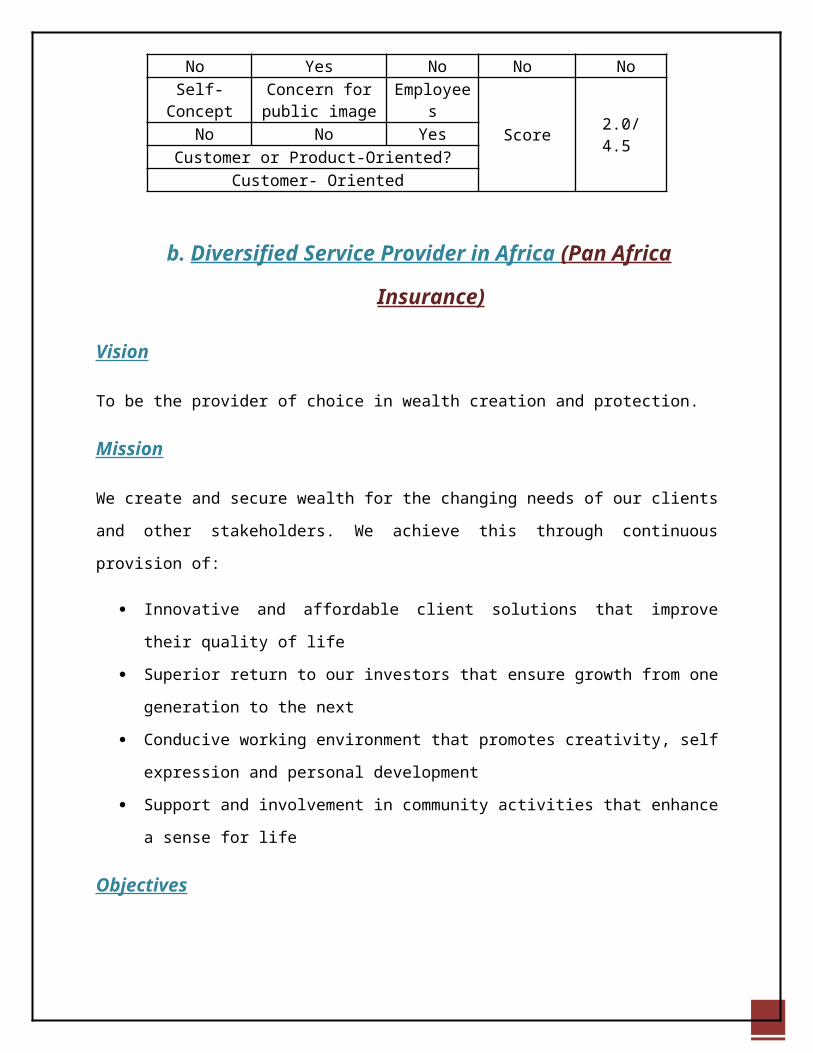

Score 2.0/ 4.5 No No YesCustomer or Product-Oriented?

Customer- Oriented

b. Diversified Service Provider in Africa (Pan Africa Insurance)

Vision

To be the provider of choice in wealth creation and protection.

Mission

We create and secure wealth for the changing needs of our clients and other stakeholders. We

achieve this through continuous provision of:

Innovative and affordable client solutions that improve their quality of life

Superior return to our investors that ensure growth from one generation to the next

Conducive working environment that promotes creativity, self expression and personal

development

Support and involvement in community activities that enhance a sense for life

Objectives

Client Focus- Listen to our clients and understand their needs; approach situations and

challenges from the client's point of view.

Accountability- Take full responsibility for our actions and results as well as honour our

commitments and take pride in good corporate citizenship.

Professionalism- Our internal and external relationships are conducted with respect and

discretion.

Integrity- Take pride in treating all stakeholders in an honest and fair manner, while maintaining

dignified and ethical conduct at all levels of our interactions.

Nurturing- Recognize both individual and team potential in an effort to draw synergies that help

achieve our goals.

Key Success Factors

Pan Africa’s ability to withstand competitive pressure in the market can largely be attributed to

its positive and proactive claims settlement operations. Prompt and timely settlement of claims

help in enhancing the confidence of policyholders in the insurance company.

Evaluation

Does it include…?Does it mention values like…?

CustomersProduct/Services

MarketsCitizensh

ipTeamwo

rk Yes Yes No No No

Technology

Concern for Survival

Philosophy

Excellence

Integrity

No Yes No No NoSelf-

ConceptConcern for public image

Employees

Score 2.5/ 4.5 Yes Yes NoCustomer or Product-Oriented?

Customer- Oriented

5. NORTH AMERICA

a. Low Cost Service Provider in North America (Prudential Insurance)

Vision

To distinguish Prudential as an admired multinational financial services leader, trusted partner,

and provider of innovative solutions for growing and protecting wealth.

Mission

To help our customers achieve financial prosperity and peace of mind.

Objectives

How we conduct our business is just as important as what we do. Our objectives are the

principles that guide us daily in helping our customers achieve financial prosperity and peace of

mind. At all times, we strive to distinguish Prudential Insurance as an admired multinational

insurance services leader and trusted brand that is differentiated by top talent and innovative

solutions for all stages of life.

Worthy of Trust: We keep our promises and are committed to doing business the right way.

Customer Focused: We provide quality products and services that meet our customers' needs.

Respect for Each Other: We are inclusive and collaborative, and individuals with diverse

backgrounds and talents can contribute and grow.

Winning: We are passionate about becoming the unrivaled industry leader by achieving superior

results for our customers, shareholders, and communities.

Key Success Factors

One key success factor differentiating the company from its competitors is its leadership

capacity at all levels of the organization. Some of the other success factors are solid brand,

global career development opportunities and culture. Size and reputation is also a key success

factor.

Evaluation

Does it include…?Does it mention values

like…?

CustomersProduct/Services

Markets Citizenship Teamwork

Yes No No No No

TechnologyConcern for

SurvivalPhilosoph

yExcellence Integrity

No No No No No

Self- Concept

Concern for public image

Employees

Score 1.0/ 4.5 Yes No No

Customer or Product-Oriented?

Customer- Oriented

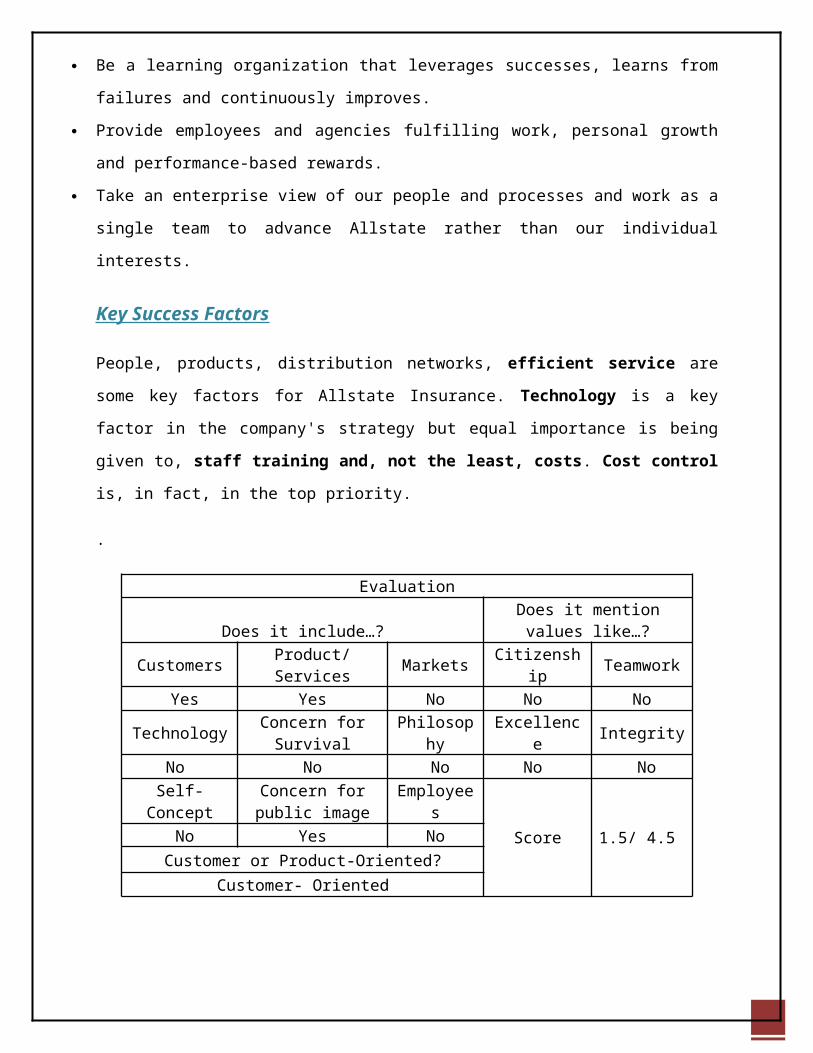

b. Diversified Service Provider in N. America (Allstate Insurance )

Vision

Deliver substantially more value than the competition by reinventing protection and retirement to

improve customers' lives.

Mission

Help customers realize their hopes and dreams by providing the best products and services to

protect them from life's uncertainties and prepare them for the future.

Objectives

Put the customer at the center of all our actions.

Utilize consumer insights, data and technology to serve customers and generate growth and

attractive economic returns.

Execute well considered decisions with precision and speed.

Focus relentlessly on those few things that provide the greatest impact.

Be a learning organization that leverages successes, learns from failures and continuously

improves.

Provide employees and agencies fulfilling work, personal growth and performance-based

rewards.

Take an enterprise view of our people and processes and work as a single team to advance

Allstate rather than our individual interests.

Key Success Factors

People, products, distribution networks, efficient service are some key factors for Allstate

Insurance. Technology is a key factor in the company's strategy but equal importance is being

given to, staff training and, not the least, costs. Cost control is, in fact, in the top priority.

.

EvaluationDoes it include…? Does it mention values

like…?

CustomersProduct/Services

Markets Citizenship Teamwork

Yes Yes No No No

TechnologyConcern for

SurvivalPhilosoph

yExcellence Integrity

No No No No No

Self- Concept

Concern for public image

Employees

Score 1.5/ 4.5 No Yes No

Customer or Product-Oriented?

Customer- Oriented

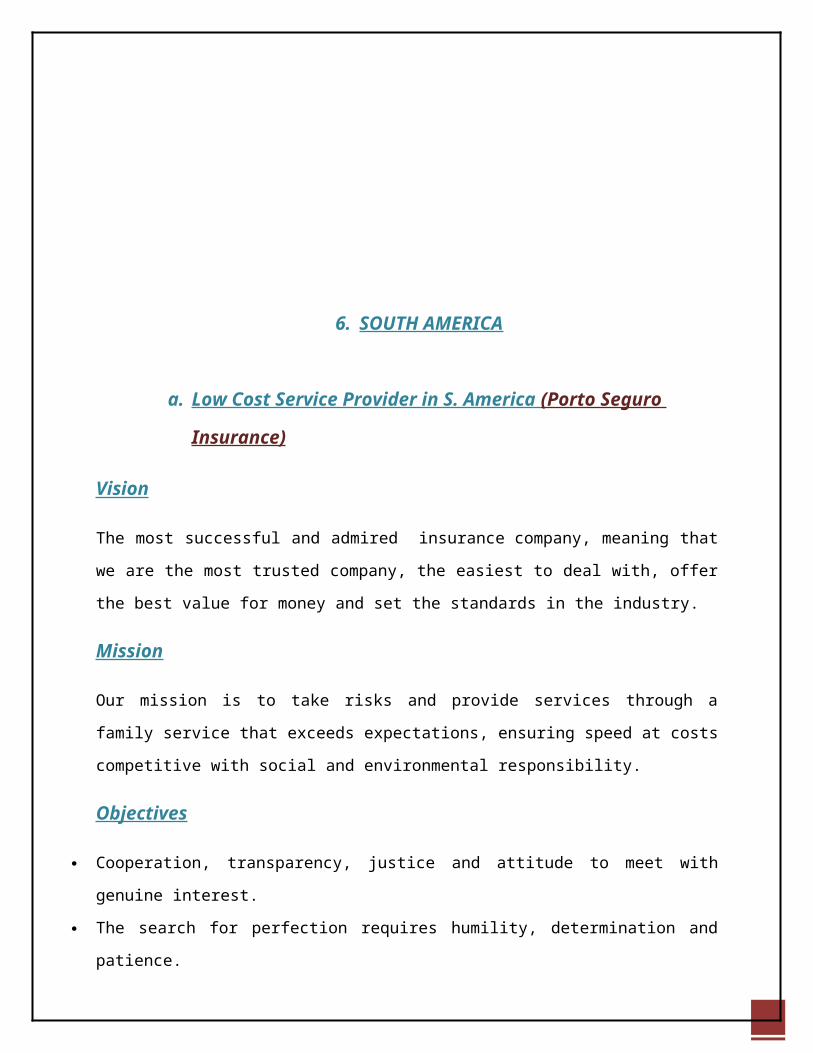

6. SOUTH AMERICA

a. Low Cost Service Provider in S. America (Porto Seguro Insurance)

Vision

The most successful and admired insurance company, meaning that we are the most trusted

company, the easiest to deal with, offer the best value for money and set the standards in the

industry.

Mission

Our mission is to take risks and provide services through a family service that exceeds

expectations, ensuring speed at costs competitive with social and environmental responsibility.

Objectives

Cooperation, transparency, justice and attitude to meet with genuine interest.

The search for perfection requires humility, determination and patience.

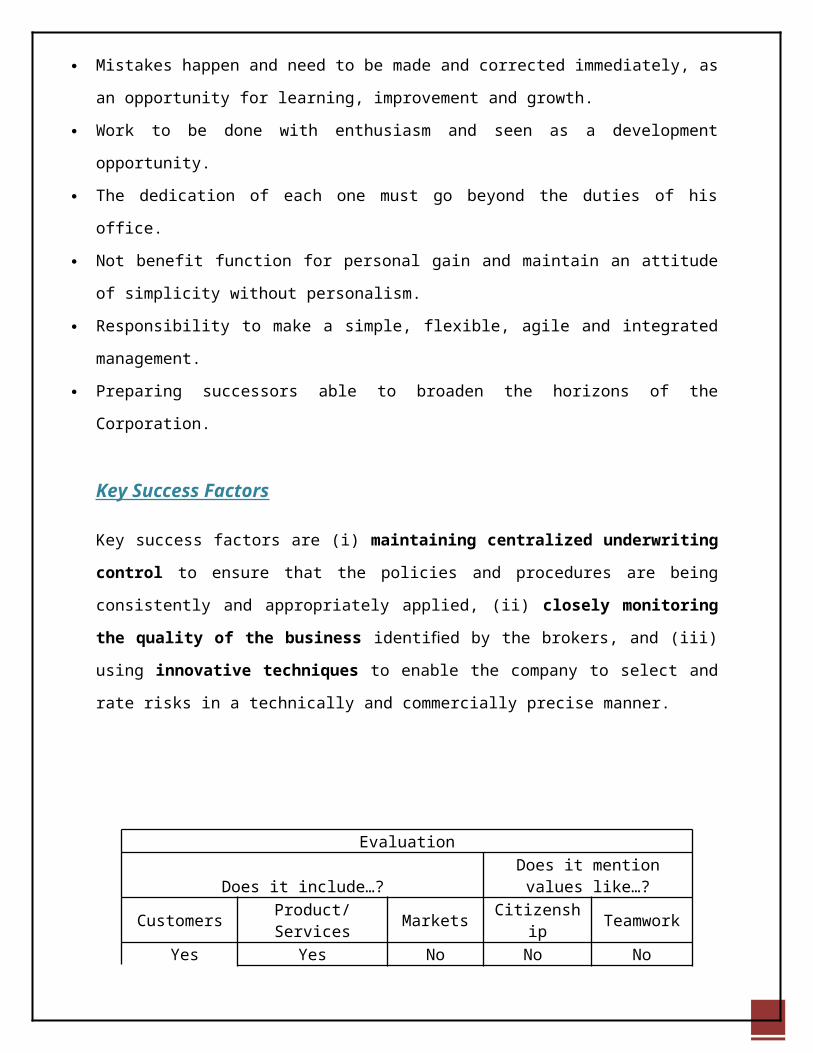

Mistakes happen and need to be made and corrected immediately, as an opportunity for learning,

improvement and growth.

Work to be done with enthusiasm and seen as a development opportunity.

The dedication of each one must go beyond the duties of his office.

Not benefit function for personal gain and maintain an attitude of simplicity without personalism.

Responsibility to make a simple, flexible, agile and integrated management.

Preparing successors able to broaden the horizons of the Corporation.

Key Success Factors

Key success factors are (i) maintaining centralized underwriting control to ensure that the

policies and procedures are being consistently and appropriately applied, (ii) closely monitoring

the quality of the business identified by the brokers, and (iii) using innovative techniques to

enable the company to select and rate risks in a technically and commercially precise manner.

Evaluation

Does it include…?Does it mention values

like…?

CustomersProduct/Services

Markets Citizenship Teamwork

Yes Yes No No No

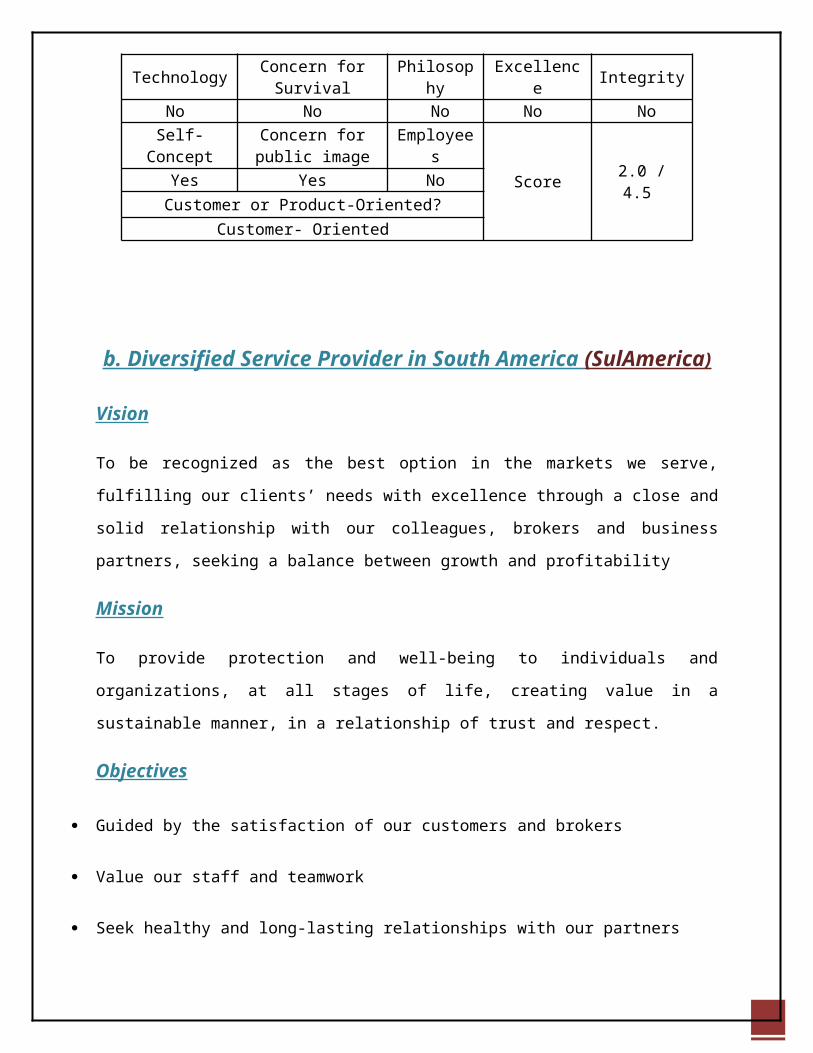

TechnologyConcern for

SurvivalPhilosoph

yExcellence Integrity

No No No No No

Self- Concept

Concern for public image

Employees

Score 2.0 / 4.5 Yes Yes No

Customer or Product-Oriented?

Customer- Oriented

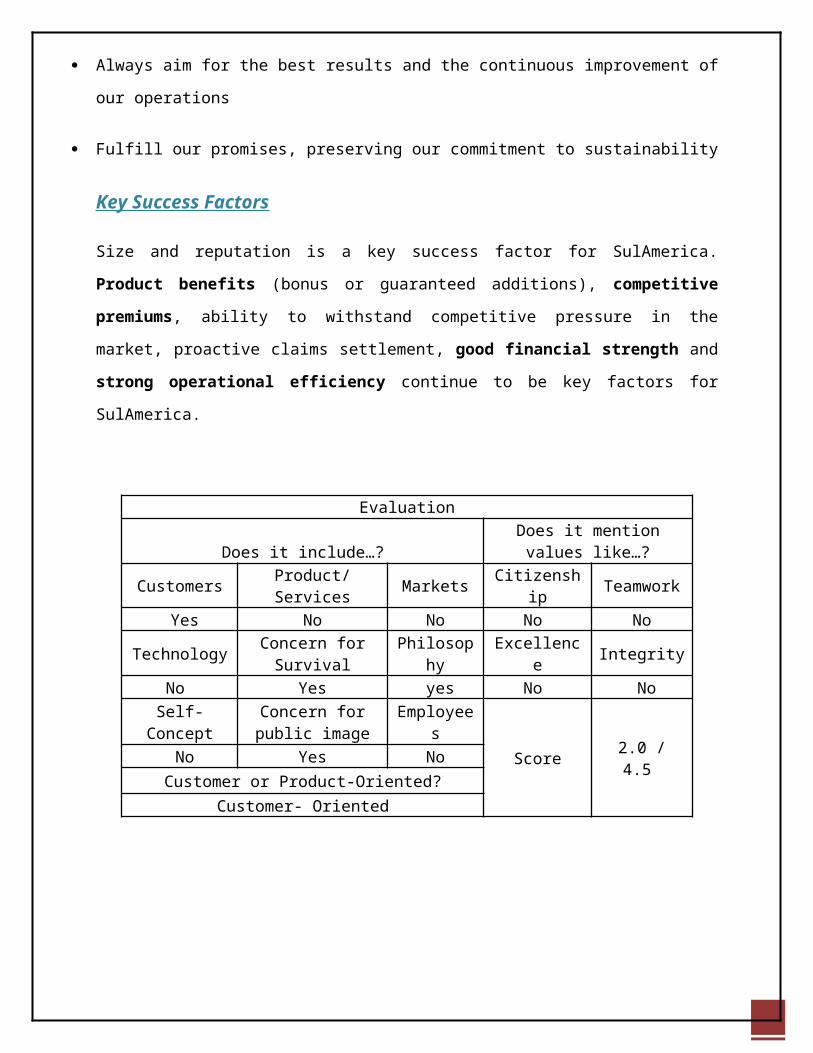

b. Diversified Service Provider in South America (SulAmerica )

Vision

To be recognized as the best option in the markets we serve, fulfilling our clients’ needs with

excellence through a close and solid relationship with our colleagues, brokers and business

partners, seeking a balance between growth and profitability

Mission

To provide protection and well-being to individuals and organizations, at all stages of life,

creating value in a sustainable manner, in a relationship of trust and respect.

Objectives

Guided by the satisfaction of our customers and brokers

Value our staff and teamwork

Seek healthy and long-lasting relationships with our partners

Always aim for the best results and the continuous improvement of our operations

Fulfill our promises, preserving our commitment to sustainability

Key Success Factors

Size and reputation is a key success factor for SulAmerica. Product benefits (bonus or

guaranteed additions), competitive premiums, ability to withstand competitive pressure in the

market, proactive claims settlement, good financial strength and strong operational efficiency

continue to be key factors for SulAmerica.

Evaluation

Does it include…?Does it mention values

like…?

Customers Product/ Markets Citizenship Teamwork

Services Yes No No No No

TechnologyConcern for

SurvivalPhilosoph

yExcellence Integrity

No Yes yes No No

Self- Concept

Concern for public image

Employees

Score 2.0 / 4.5 No Yes No

Customer or Product-Oriented?

Customer- Oriented

4. Conduct an External as well as Industry Environment Analysis for the industry in which the company (PESTEL and Porter's 5 Force Analysis) is operating. Identify the strategy of the company's closest competitor? Who are the complimentary of the organization?

External Environment Analysis of Insurance Industry

A. PESTEL Analysis

Pestel analysis is a tool which analyzes the macro environment of any industry by using

Political, Economic, Social, Technological, Environmental and Legal dimensions. It is a part

of the external analysis when conducting a strategic analysis or doing market research, and gives

an overview of the different macro environmental factors that the company has to take into

consideration. It is a useful strategic tool for understanding market growth or decline, business

position, potential and direction for operations.

a. Political Factors Affecting Insurance Industry:

Within India political ambitions and rise of communalism, fissiparous tendencies are on the rise

and may well continue for quite some time to time. Therefore, it expected that the insurance

companies might consider offering political risk coverage also. The only area where Indian

insurers consider giving cover is with regard to customs duty change under certain conditions.

Certain type of political risk at the international level has serious implications for exporters. The

term ‘political risk’ has a wider connotation than commonly understood or assumed. It covers

events arising not just from politics, but risks in the course of international transactions. In this

connection, it may be noted that export credit insurance has evolved out of uncertainties relating

to international trade, particularly due to problems arising out of foreign legal jurisdiction,

political changes and currency exchange difficulties faced by many developing countries.

Role of the government: -

As insurance is an important service sector, hence it is highly regulated by government. Since

1956 insurance sector was highly regulated by government of India. On March 16, 1999, the

Indian cabinet approved on Insurance Regulatory Authority Bills that was designed to liberalize

the insurance sector.

IRDA: Insurance Regulatory and Development Authority:-

The Insurance Regulatory and Development Authority, constituted under the IRDA Act, 1999,

provide for the establishment of an authority to protect the interest policyholders, to regulate,

promote and ensure orderly growth of the insurance industry.

a. Business Requirement:-

A company will not be issued a license unless the IRDA is satisfied with the sound financial

condition, the general character of management, the volume of business, the capital structure,

earning prospects for the insurers and that the interests of the general public will be served if

registration is granted to the insurer.

Foreign insurance companies have been allowed to have a maximum 26% share holding. No

insurance company can be registered under the Act unless they have a paid up capital of Rs. 100

crores. Every insurer shall deposit with the reserve bank of India one percent of the total gross

premium written in India in any financial year, not exceeding Rs. 10 crores.

This amount would not be susceptible to any assignment or charge nor would it be available for

the discharge of any liabilities other than liabilities arising out of policies issued, so long as any

such liabilities remain undercharged.

b. Investment of Assets:-

Every insurer is required to invest, and keep invested, assets equivalent to not less than the net

liabilities as follows:

(a) 25 % in government securities,

(b) a least 25% of the said sum in government securities or other approved securities and

(c) the balance in any approved investment rated as “very strong” or more by reputed rating

agencies, which include various debt instruments on which dividend on its ordinary shared for

the five years immediately preceding or for at least five out of the six or seven years immediately

preceding have been paid and which have priority in payment over ordinary shares of the

company in winding up.

In order to ensure that the company does not risk the money of the policyholder’s, the Act

provides that an insurer who does not comply with the aforesaid provisions may be deemed to be

insolvent and may be would up by the court.

Insurers are required to get an actuary to investigate the financial conditions of the life insurance

business including a valuation of liabilities every year in order to ensure continual compliance.

In order to maintain transparency in its dealings, insurers would have to keep separate account

relating to funds of shareholders and policyholders.

b. Economical Factors Affecting Insurance Industry

Interest rate at bank and interest rate of P.F variation very much affect to insurance industry,

because people always attract by higher return. Therefore, they do not prefer lower return policy.

Unemployment also affects insurance industry, because the unemployment people will not have

earning, so saving also affect to insurance sector. Insurance industry will directly affected by

Earthquake, Monsoon, and Natural calamity. Because of these events turns into lots of death, so

the \ insurance companies have to pay claim against policy.Typical Indian want luxurious

product against low income, so that they prefer installment or annuity (EMI), so that they may

not have extra saving to invest in insurance.

1. Adequacy of capital:

Capital adequacy is a matter of attention in view of the nature of the insurance business, where in

the case a contingency arises, the insurers should be in a position to meet its long-term

contractual obligations and pay up the dues or claims. In that sense, insurance is a capital-

intensive business and must be backed by an adequate capital base on the part of the owners and

the companies should not be running their business purely on other people’s money. So

minimum start up amounts and long running capital adequacy norms are absolutely essential, in

consideration of this, the Malhotra committee suggested and subsequently the IRDA stipulated a

minimum capital base of Rs 1 billion for any entity wanting to enter the insurance business.

2. Increased Economical Activity:

Although economic activity has slowed down since 1996, sooner or later there will be an

upswing. The increase in the growth rate in various sectors accompanied by the growth in trade

in the context of fulfilling of commitments to the WTO will signal a growth in the demand for

insurance covers of new types.

3. Interest Rates: -

During the last years the government has rationalized interest rate creating better business

opportunities for the insurance sector because the substitute products are graded lower by the

customers. On the other hand the value of the holdings of the insurance companies will increase.

Rationalized of the interest rates is still expected, and it is an opportunity for the company.

Low interested rates mean low investment return for reinsures causing negative impact on their

overall net profitability as pricing is to a certain extent sensitive to interest rate fluctuations. The

negative impact therefore, lead to higher pricing level for reinsures in order to sustain their

profitability. But, in reinsurance market, which is characterized by over capitalization a resulting

intense competition.

c. Socio-Cultural factors affecting Insurance Industry:

The basic social factors that affect the insurance sector are as under: -

Population

Life style

Educational level

Level of earning

Societal benefits

These are the major social factors, which affect the insurance sector.

Population:

Growth in the population is a major factor pushing up the demand. It is also going to exert a

special influence on the life insurance market in other ways. Apart from exerting pressure on

demand for goods and services, and through that, ill effects of uncontrolled growth of population

also could spur the growth of demand. For example, overcrowding in public places of

entertainment, public support, or too many vehicles on the road can result in hazards like

stampedes and pollution, which require covers and still are not sold on a large scale today. Thus

the positive as well as the negative aspects of population growth are going to spur demand.

Life style:

The peculiar lifestyle of a country or an age also influences the insurance business. Change

therein produces different demands for insurance. For e.g. All over the world, family size is

shrinking and the fact that in decades to come, both presents are more frequently likely to work

outside the home will mean that there could be a greater possibility of property loss. Similarly, a

larger number of vehicles on the roads for people commuting to their jobs or business would

mean larger incidence of accidents. This will increase the demand for life insurance products.

Of course, there is also the other possibility that wherever it is possible, some people will try to

spend a part of their time working at home either because they would like to be with their

families or because they find it more convenient. Activities like insurance and financial services

are particularly well suited for such arrangements.

Level of education:

India is one of the developing countries: the level of education is very low here. The literacy rate

is very poor. More than 50% of the population is still uneducated or more or less not educated.

Thus the people are not able to understand the concept of the insurance. Among the educated

people the quality of the education is still a big question mark. Thus the awareness is not created

and it has become a big challenge for the industry. Thus one of the factors, which affect the

insurance sector, is low level of education.

Level of earning:

Another factor, which affects the insurance sector, is the level of earning. In India the rule of 80-

20 is working. The 80% of the total population is having the 20% of the wealth and the 20% of

the total population is having 80% of total wealth. Thus the richer are richer and poorer are

poorer. Due to this the insurance sector is affected very much.

d. Technological Factors Affecting Insurance Industry:

Internet as an intermediary in the current Indian market customer is not aware about the

intrinsic value of insurance. He thinks of insurance only in the mount of March as a tax saving

measure. The security provide by an insurance cover is rarely thought about. In such a scenario

Internet can be an effective medium for educating the consumers about insurance. It serves as a

single window for disseminating product, process and procedural information to the consumers.

Product development and target marketing through the Internet: with increase in the number of

insurance companies there will be a need for market segmentation and subsequently product

designed for each of them. In such a scenario Internet can be an effective channel for pushing

product specific information to a particular market segment. Consumer feedback about a

particular product as well as suggestions for different types or covers can also be generated

through the Internet.

Maintaining the database:

The most important factor that is affecting the insurance industry is the marinating the database

of the customers. The insurance industry is having a huge list of the customers.

In order to maintain it in manual format it is really the work of stupidity. With the change in time

the computers has taken the work of this things. Thus with the development of the technology it

has becoming possible to maintain such huge database very easily. A person can switch over to

the computer and get the details of the customer very easily. Thus maintaining the database has

really become easy due to the development in technology.

E-business insurance in India: -

The Internet has played a vital role in transforming the business of the 21st century. Computers

are now being used extensively for creating a storing data, information with the help of complex

and sophisticated technological tools in every kind of business. This change having been widely

accepted, the advantages are numerous such as fast processing improved. Efficiency, cost

reduction among several other benefits. However, with every positive change, there is an evil

attached and technology is no exception. In technical is an evil attached and technology is no

exception. In technical terms, increased sophistications of technology brings with it, an increased

factor of risk involved. The risk can be of various attributes, for example, the risk of data being

lost due to a virus attack, the theft of important and confidential information and so on, which

ultimately results in losses for the business entity. With this change in the business process,

insurers have to devise new methods for assessing, underwriting and servicing claims for the so-

called e-business insurance.

f. Legal Factors Affecting Insurance Industry:

A company failing to comply with the IRDA act shall be liable for panel action. Further, IRDA

is empowered to investigate into the affairs of the company. Failure to comply with the

directions may lead to cancellation of the license for the company.

Also, if the IRDA has reason to believe that a company is doing business in a manner likely to be

prejudicial to the interest of policyholders, it is required to report to the central government.

The central government may base on the report, appoint an administrator to manage the affairs of

the company. This would act as a further assurance to the consumers, as their interests would at

all times be a priority and that in the event that the company acts in the manner prejudicial to

their interests, than an administrator would be appointed to serve their needs.

The court may also wind up the company if it fails to deposit or keep deposits as per the

requirements of the act or if the continuance of the company is prejudicial to the interest of the

policyholders or public interest.

But an insurance company cannot be wound up voluntarily or on the grounds that by reasons of

its liabilities it cannot continue its business, except for the purpose of affecting an amalgamation

or a reconstruction of the company. Therefore, a company after issuing a policy cannot escape

liability by seeking voluntary winding up.

The four amendments, made in the life insurance Bill by the Lok Sabha, are as under:

1. The Insurance Regulatory and Development Authority should give priority to health

insurance.

2. Policyholder’s fund will be invested in the social sector and infrastructure.

The percent may be specified by the IRDA and such regulations will apply to all insurers

operating in the country.

3. Insurers will be expected to undertake a certain percent of business in rural areas, and cover

workers in the unorganized and informal sectors and economically backward classes.

4. In the event of insurers failing to fulfill the social sector obligations, a fine of Rs. 25 lakh

would be imposed the first time. Subsequent failures would result in cancellation of licenses.

B. Industry Environment Analysis of Insurance Industry

Porters Five-Force of Insurance Industry

1. Threat of new entrants: -

The future of insurance market scenario will be marked by the active presence of many

international players, beside several Indian players. As far as insurance industry there would be

fewer entries due to more specialized firm with lower expenses ratios and better capitalization.

Threat of entry is determine by the entry barriers which act to prevents firms from entering the

industry. In insurance industry entry barriers is moderate so that it becomes profitable, it attracts

new entrants, thereby increasing the number of competitors.

The Indian market is highly brand oriented, it is difficult to introduce new brand.

The acceptability of new brand is also very low.

The capital requirement in insurance is Rs. 100 crores, which attract more companies to invest

in. promoters, can hold paid up equity capital up to 26% in an Indian insurance company. In case