Embed Size (px)

Citation preview

SECTION 11.1UnderstandingCreditSECTION 11.2 Qualifying forCreditSECTION 11.3 Managing CreditCardsSECTION 11.4 Taking Out a LoanSECTION 11.5 Handling DebtProblems

• Write down the coloredheadings in this chapter.

• As you read the text undereach heading, visualize whatyou are reading.

• Reflect on what you read by writing a few sentencesunder each heading todescribe it.

• Reread your notes.

S E C T I O N 1 1 . 1

UnderstandingCredit

Credit can be a valuable tool. Likemany privileges, it comes with respon-sibilities. With discipline and wisedecision making, credit can be astrong personal asset.

THE MEANING OF CREDITCredit is the supplying of money, goods, or services at

present in exchange for the promise of future payment.When you borrow money from a bank or use a credit cardto purchase gasoline, you’re using credit. The business ororganization that extends the credit is the creditor.

Each party in any credit transaction trusts the other tocarry out his or her part of the agreement. For example, abank—the creditor—might loan a consumer $5,000 topurchase a used car. The creditor agrees to accept monthlyrepayments over a period of three years. The borroweragrees to repay a total of $5,724. That includes $5,000 ofprincipal, which is the original amount borrowed, plus$724 interest paid for the use of the creditor’s money.

Objectives

After studying this section, youshould be able to:• Explain basic principles of

credit.• Describe types of credit.• Analyze the benefits, costs,

and drawbacks of using credit.

Key Termscreditcreditorprincipalsecured creditcollateralclosed-end creditopen-end creditinstallmentfinance charge

261

262 • CHAPTER 11 Consumer Credit

now and wish to pay for it later, you’reusing sales credit.

• Secured and unsecured credit.Secured credit is backed by a pledge ofproperty. In other words, the borroweroffers something of value as assurancethat the loan will be repaid. The lender hasa security interest in the pledged property,meaning that the property can be taken bythe lender if the loan is not repaid. Theproperty that is pledged to guaranteerepayment is known as security or collat-eral. Because collateral reduces thelender’s risk, secured credit is generallyeasier to obtain than unsecured credit.

In this example, credit benefits everyoneinvolved. The borrower was able to purchasethe car, the seller found a willing buyer, andthe bank profits by receiving interest incomeover time.

TYPES OF CREDITThe credit available to consumers ranges

from credit cards to bank loans to merchantfinance contracts. In general, consumercredit can be categorized in the followingways.

• Cash credit and sales credit. If youtake out a loan and receive cash, you’reusing cash credit. If you buy something

Consumer Confidence and Credit

Suppose you see a new store at the mall. Is your first reaction “What do they sell?” or“How long will they last?” Your expectations for the shop’s success or failure are a sign ofyour consumer confidence—your feelings about the future of the economy.

Detailed surveys to measure these sentiments are done by universities, corporate finan-cial advisors, and the media. In these surveys, consumers are asked their views and pre-dictions about selected economic factors, such as the job market and household income.Consumers’ answers are given a numerical value to create a consumer confidence index.

Some surveys ask directly about using credit. In others, questions about buying “big-ticket items,” such as appliances, suggest consumers’ willingness to take on debt. Somesurveys show an interesting trend related tocredit: respondents who feel optimisticabout their own incomes are apt to makelarge purchases, even if they feel pessimisticabout the overall economy. Actual con-sumer spending bears this out.

Some economists question the value ofconsumer confidence surveys. Nonetheless,financial planning experts—fiscal policyadvisors, for example—consider the public’smood when making economic predictions.

FIGURE IT OUT

Develop and use a survey on credit useamong teens in your school. How often dothey use credit cards? Find out what makesteens feel confident about making credit pur-chases. What reduces their confidence? Doincome and debt have impact? Compare theinfluences on teens to factors that influenceadults.

Section 11.1 Understanding Credit • 263

• Closed-end and open-end credit.Closed-end credit is a one-time exten-sion of credit for a specific amount andtime period. The total amount of interestto be paid is known at the beginning ofthe loan. In contrast, open-end credit—sometimes referred to as a line of credit—can be used repeatedly. A typical creditcard provides open-end credit. The card-holder makes a monthly payment of all orpart of the account balance. The amountof interest that must be paid is based onthe account balance at any given time.

• Single-payment and installmentcredit. Some closed-end credit agree-ments call for the borrower to pay theentire amount due in a single payment.More commonly, however, closed-endcredit is paid in installments. An install-ment is a set portion of the loan amountthat the borrower must pay at regularlyscheduled intervals. For instance, a furni-ture store might advertise a sofa for sale in“four easy installments.” A payment sched-ule specifies the dates on which install-ment payments are due and the amountof each installment. It may also indicatehow much of each installment is appliedtoward principal and interest.

PROS AND CONS OFCREDIT

Credit is a privilege that benefits con-sumers in several ways. Its advantagesinclude:

• Temporary expansion of income.Credit allows you to use goods and serv-ices before you’ve paid for them or whileyou’re paying for them. This is especiallyhelpful for unexpected expenses that can’twait, such as replacing a worn-out refrig-

erator. Major purchases such as a car orhome might not be possible withoutcredit.

• Convenience. A credit card can give youthe secure feeling of being able to makepurchases without carrying a largeamount of cash. See Figure 11-1. You canalso shop online or by telephone with acredit card. Getting a refund on returneditems is usually easier if they werecharged, and monthly statements of creditcard purchases simplify record keeping.

• Financial responsibility. Good creditprovides proof to others of your financialresponsibility and can make it easier toobtain credit in the future.

11-1 When you’re on a vacation, having a

credit card reduces the need to carry cash.

Why is this an advantage?

264 • CHAPTER 11 Consumer Credit

• Security concerns. Using a credit cardrequires that you take precautions againstthe card being stolen or otherwise usedwithout your permission.

• Impulse buying. The power of creditmay make you more likely to buy items onthe spur of the moment, without the care-ful consideration that a purchasing deci-sion deserves.

• Overspending. Handing over a creditcard instead of “real” money can makeitems seem almost free. However, the debtthat mounts up is all too real. Consumerswho consistently spend more than theycan afford get into financial trouble thatmay take years to undo.

• Reclaimed merchandise. If you buyon credit and fail to pay for the items, theycould be taken back by the merchant.

DECIDING WHEN TO USECREDIT

Sometimes using credit is a wise and easychoice. Imagine how long it would take, andhow difficult it would be, to save enoughcash to pay the entire cost of a new car, yourcollege education, or a home. Using creditmakes these purchases possible.

The Costs of CreditUsing credit involves costs as well as ben-

efits. These costs include:

• Interest and fees. The cost of usingcredit, including interest and any fees, iscalled the finance charge. Financecharges can usually be avoided if a creditcard is paid in full each month.

• Increased cost of merchandise.Retailers who offer credit must pay banks tocollect on their credit sales and be preparedto write off unpaid debt. To offset thesecosts, many businesses increase prices. Someoffer a discount for paying cash.

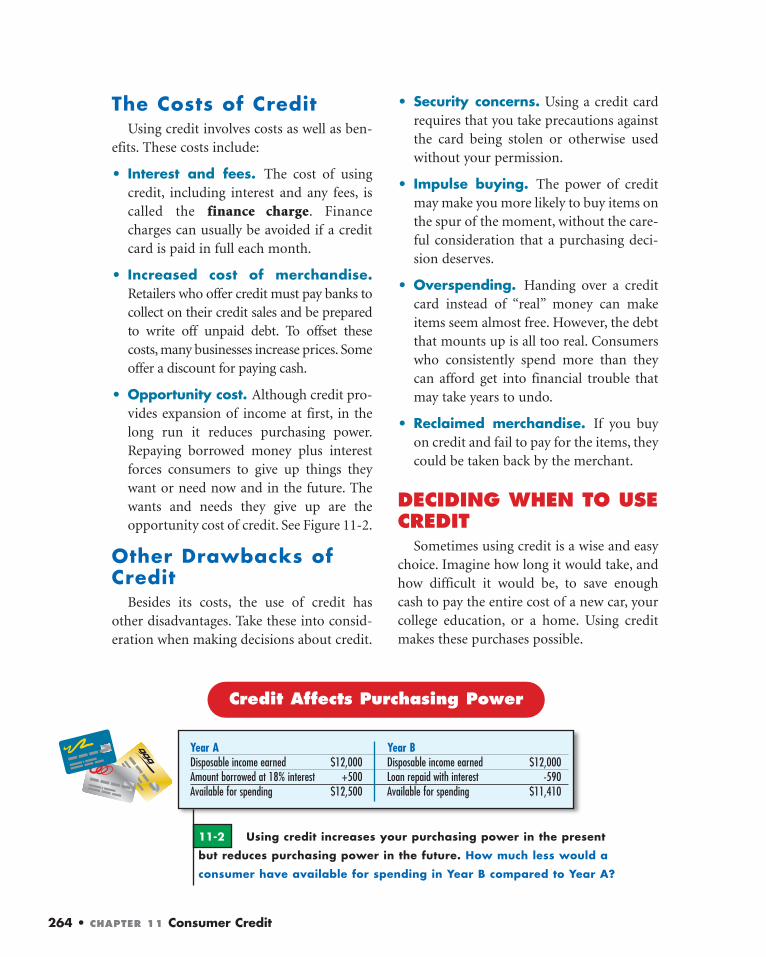

• Opportunity cost. Although credit pro-vides expansion of income at first, in thelong run it reduces purchasing power.Repaying borrowed money plus interestforces consumers to give up things theywant or need now and in the future. Thewants and needs they give up are theopportunity cost of credit. See Figure 11-2.

Other Drawbacks ofCredit

Besides its costs, the use of credit hasother disadvantages. Take these into consid-eration when making decisions about credit.

11-2 Using credit increases your purchasing power in the present

but reduces purchasing power in the future. How much less would a

consumer have available for spending in Year B compared to Year A?

Year A Year BDisposable income earned $12,000 Disposable income earned $12,000Amount borrowed at 18% interest +500 Loan repaid with interest -590Available for spending $12,500 Available for spending $11,410

Credit Affects Purchasing Power

Section 11.1 Understanding Credit • 265

In other situations, it may be harder todecide whether to buy on credit. In general,use credit only when you can repay comfort-ably and not neglect your other financialobligations. See Figure 11-3.

Before using credit, consider your alterna-tives. Paying by cash or check helps ensurethat you limit purchases to what you can

Section 11.1 Review

CHECK YOURUNDERSTANDING

1. How do creditors profit by offeringcredit?

2. How is open-end credit different fromclosed-end credit?

3. How does the use of credit affect a con-sumer’s future purchasing power?

CONSUMER APPLICATIONCash or Credit Suppose you’re buying asofa. Using the store’s credit plan, the pay-ments would be $60 a month for 24months. If you pay in cash, the cost is$1,200. What factors would you weigh indeciding whether to pay cash or buy oncredit? How would they affect your decision?

afford. If you want to buy online or by phone,using a prepaid card or debit card providesthe convenience of a credit card without thedebt. As you’ll learn in Chapter 12, saving tobuy an item at a later date has several advan-tages. Try giving yourself time to think aboutpurchases rather than using credit to buy onimpulse. You may decide that an item youthought you “couldn’t live without” is notthat important to you after all.

11-3 Many people limit their debt by

never using credit for consumables such

as food. What do you suppose is the

reasoning behind this guideline?

S E C T I O N 1 1 . 2

Qualifying forCredit

Consumers do not automatically getcredit or keep it. They must take stepsto build a record that shows they arefinancially responsible and can man-age debt wisely.

WHAT LENDERS CONSIDERBefore they will extend credit, banks and other lenders

want to know how much of a risk they are taking. Is theborrower likely to pay back the money on time? Sincelenders don’t have a crystal ball to see into the future, theyfocus on the borrower’s present and past.

The Three C’s of CreditIn deciding whether to extend credit, lenders consider

the three C’s—character, capacity, and capital. Characterrefers to a person’s reputation, especially concerning repay-ing debt on time. Capacity is a person’s earning power andability to pay debts from regular income. Capital refers toitems owned, or assets. The consumer who owns items ofvalue is a better credit risk than one who does not, becauseassets can be sold, if necessary, to repay debt.

Objectives

After studying this section, youshould be able to:• Analyze factors that affect the

ability to get credit.• Explain the significance of

credit reports.• Describe how to establish and

maintain a good credit history.

Key Termscredit historycredit bureaucredit reportcredit ratingcredit scorecosigner

266

Section 11.2 Qualifying for Credit • 267

Credit HistoryThe main way in which a consumer can

demonstrate the first C—character—is byestablishing a positive credit history, or pat-tern of past behavior in regard to repayingdebt. Without a credit history, lenders havelittle information with which to evaluate theconsumer’s reliability. On the other hand, ifthe potential borrower has a record of payingpast debts in full and on time, lenders feelmore confident in extending credit.

The Credit ApplicationThe questions on a credit application are

designed to assess whether you are a goodcredit risk based on the three C’s of credit.See Figure 11-4. Although applications vary,many ask for information about:

• Employment. You’ll be asked where youwork, how long you’ve been there, andhow much you’re paid. The lender willprobably contact your employer to verifythis information.

• Residence. The lender may want toknow how long you’ve lived at your pres-ent address. Maintaining the same resi-dence is a sign of stability.

• Home ownership. Owning a home isevidence of capital. Also, a homeowner isconsidered a more permanent residentthan a person who rents.

• Monthly housing costs. The lenderwants to know whether you’re paying somuch for housing that there is little leftfor payment of new debts.

• Credit references. You may be asked tolist businesses with which you have dealton a credit basis. Their records are the bestindication of your bill-paying habits. Ifyou haven’t used credit before, you may beasked to give the names of personal refer-ences, such as teachers and businesspeoplewho can provide information about yourcharacter.

• Collateral. You may be asked to identifyproperty that will serve as security for theloan.

11-4

A credit application provides the

lender with information about your

character, capacity, and capital.

Why are these factors important to

the lender?

268 • CHAPTER 11 Consumer Credit

credit-granting decisions on informationobtained from credit bureaus. A creditbureau, or credit reporting agency, is a firmthat collects information about the credit-worthiness of consumers. Credit bureaus gettheir information from stores, banks, andother creditors, as well as from publicrecords such as court judgments. In additionto local credit bureaus, there are threenational credit reporting agencies: Equifax,Experian, and TransUnion.

Credit bureaus and reporting agenciescompile the information into a creditreport, a record of a particular consumer’stransactions and payment patterns. Thereport is then sold to creditors who are eval-uating applicants. A credit report includesinformation such as the date each creditaccount was opened, the balance owed, themonthly payment amount, and whether pay-ments have been late. Figure 11-5 shows partof a sample credit report.

• Bank references. Any bank you list asa reference will usually be asked howmuch you owe the bank and what bal-ances you have in your checking and sav-ings accounts.

Equal CreditOpportunity Act

The Equal Credit Opportunity Act is afederal law ensuring that all consumers aregiven an equal chance to obtain credit. Theact protects credit applicants against dis-crimination on the basis of sex, marital sta-tus, race, religion, national origin, age, orincome from public assistance.

CREDIT REPORTING ANDRATING

In addition to the information suppliedon the credit application, lenders base their

ReliableCreditBureau

Prepared for Social Security Number

Report Date Report Number

Date of Birth

JANE X. ANYONE

Creditor/Account Number

Community BankBig City, TX125551674

First Credit CardLas Vegas, NV5678-1234-5555-5555

Dateopened/Reportedsince

6-2000/6-2000

10-2001/10-2001

Date of status/Last reported

12-2002/12-2002

12-2002/12-2002

Type/Term/Monthlypayments

Line of credit/18 months/$60

Revolving/NA/$0

Credit limit/High balance

$1,000/NA

$5,000/$2,349

Recent balance/Recent payment

$0 as of 12-2002/$54

$0 as of 12-2002/$434

Status/Comments

Closed/never late

Open/never late

000-10-5454

January 5, 2— 1896758

10/16/1979

Page 1 of 3

11-5 Information about a consumer’s payment history is kept on file by

credit bureaus. How is this information used by prospective creditors?

Credit Report

Section 11.2 Qualifying for Credit • 269

Credit Ratings andScores

Credit bureaus and reporting agencies donot judge whether consumers deserve credit.They only provide information for lenders tointerpret. When deciding whether to grantcredit, a lender uses the credit report andother information to arrive at a credit rat-ing, an evaluation of a consumer’s credit history.

As part of their evaluation process,lenders may obtain or calculate a consumer’scredit score. A credit score is a numericalrating, based on credit report information,that represents a person’s level of creditwor-thiness. Individual lenders decide for them-selves what scoring method to use and whatscore is needed to obtain approval.

Credit reporting agencies don’t developthese scores, but they play a role in makingthem available to creditors. They also offer aservice that enables consumers to view theirown credit score for a fee. Along with thescore, consumers receive an explanation ofhow it was influenced by various risk factors,such as payment history and the amount

currently owed. This information is actuallymore important to consumers than the scoreitself, because it helps them understand whatthey can do to improve their credit historyover time.

Fair Credit ReportingAct

Credit bureaus work to keep their recordsas accurate as possible. However, errors canoccur that may result in consumers beingunfairly denied credit. The Fair CreditReporting Act assures a consumer’s right toaccess his or her credit file and dispute incor-rect information.

It’s a good idea to check your credit reportat least once a year. If you find an error, youcan request that the credit bureau reinvesti-gate the information. Inaccurate informa-tion must be corrected or removed fromyour file. You may then ask that anyone whohas recently been given the incorrect infor-mation be notified. When a dispute betweenyou and the credit bureau can’t be resolved,you may request that your version of the dis-pute be filed and included in future reports.

To get a copy of your credit report, contact one of the three national credit reportingagencies: Equifax, Experian, or TransUnion. Creditors can put you in touch withthem, or you can visit the agencies on the Web. If you wish, you can obtain yourcredit report online using a secure browser connection. Under certain circumstances,you are entitled to a copy of your report for free. Otherwise, there may be a smallcharge.

Your Credit Report

270 • CHAPTER 11 Consumer Credit

Another way to establish credit is to applyfor a secured credit card, one that requires youto keep a savings account as security. A dis-advantage is that the money used as securityis tied up so you can’t use it for other pur-poses. In addition, you may have to pay ahigher interest rate than for an unsecuredcard, as well as high fees. Make sure youunderstand the terms of a secured cardbefore applying for one.

No matter what steps you take to establishcredit, manage your new credit wisely bypaying bills reliably and avoiding excess debt.You’ll soon be on your way to establishingand maintaining a good credit history thatwill help you accomplish your financial goalsthroughout life.

The Fair Credit Reporting Act also statesthat information from your credit file maybe given only to those who have a legitimateneed for it. An employer or prospectiveemployer can check your credit report only ifyou give your written consent.

ESTABLISHING ANDMAINTAINING CREDIT

Since lenders evaluate applicants by look-ing at credit history, you may wonder howanyone obtains credit for the first time.Actually, there are several steps you can taketo establish credit.

• Open checking and savings accounts.Make regular deposits and avoid over-drawn checks.

• Put a utility, such as telephone or Internetservice, in your name and pay the billspromptly. Be sure the creditor reportsyour payment history to a credit bureau.

• Apply for a credit card from a local store.Without a credit history, you may qualifyfor only a small line of credit, but it’s astart. Use the card and pay the bills ontime. After several months, apply for acard from another business.

Some consumers who don’t qualify forcredit on their own seek the help of acosigner. A cosigner is a person with astrong established credit history who signsthe credit application and contract alongwith the borrower. In the event that theapplicant fails to make payments, thecosigner is responsible for making them. Thenew credit applicant can build a good credithistory by making prompt, regular pay-ments. Once this is done successfully, nocosigner will be needed for future creditapplications.

Section 11.2 Review

CHECK YOURUNDERSTANDING

1. What are the three C’s of credit and whatdo they indicate to lenders?

2. Why should consumers make sure theircredit reports are accurate?

3. What are five possible ways to establishcredit for the first time?

CONSUMER APPLICATIONLoan Application Create your own loanapplication form, referring to page 267. Usefictitious information to fill in two copiesof the application: one that a lender wouldprobably turn down, and one that wouldlikely be accepted. Explain why each appli-cation would be accepted or turned down.

S E C T I O N 1 1 . 3

ManagingCredit Cards

Credit cards are perhaps the mostwidely used type of credit. The termsof a credit card agreement and theway you manage your account willaffect your financial health.

TYPES OF CREDIT CARDSConsumers can choose from thousands of credit cards

issued by different companies and with different features.To sort them out, two basic distinctions are especiallyimportant to consumers: where the card is accepted andwhen charges must be paid.

Private Label and GeneralPurpose Cards

Some cards, called private label cards, can be used only ata single retailer. Many department store chains and gasolinecompanies, for example, offer private label credit cards.

In contrast, a general purpose card—also known as abank card or major credit card—can be used at millions ofdifferent businesses across the country or around theworld. The familiar logo of a card network is found on thecard and can be seen at places of business that accept it.The largest card networks are each owned by an associa-tion of thousands of financial institutions. Most generalpurpose cards can be used not only to make purchases butalso in other ways, such as to obtain cash advances fromautomatic teller machines.

Objectives

After studying this section, youshould be able to:• Identify sources and types of

credit cards.• Evaluate credit card terms and

conditions.• Give guidelines for using credit

cards wisely.• Explain how to resolve credit

card billing problems.

Key TermsAPRgrace periodcredit limit

271

272 • CHAPTER 11 Consumer Credit

for example. Typically, by using the cardyou can earn a reward from the partnercompany, such as points toward a free stayat the sponsoring hotel chain.

• An affinity card carries the name of a non-profit or charitable organization, such as aschool or an animal welfare organization.The organization receives money from thecard issuer, such as a percentage of everydollar charged or a portion of the annualfees collected. See Figure 11-6.

• A smart card has a computer chip in it.The chip can store information used foronline shopping, such as user names,passwords, and billing and shipping infor-mation. When inserted into a special cardreader connected to a computer, the cardmakes it possible to fill out Web orderforms quickly and easily. A passwordkeeps the information secure.

COMPARING CREDITCARD TERMS

It’s wise to shop carefully for a credit cardjust as you would for any major purchase.Here are some of the features and costs ofcredit cards that you should consider.

11-6

Prestige cards and affinity cards

are both designed to attract

consumers. How do they differ?

Revolving Credit Cardsand Charge Cards

Some credit cards use an arrangementcalled revolving credit. On receiving a bill, thecardholder has several payment options: payfor all charges in full, make only a minimumpayment, or pay any amount in between. If abalance is carried over, the cardholder mustpay interest on it. Other cards do not allow abalance to be carried over. All charges mustbe paid in full each month. Card issuersoften refer to this type as a charge card ratherthan a credit card.

Credit Card VariationsThe credit card business is very competi-

tive. Card issuers continually come up withways to entice consumers to apply for theircards. Here are a few examples.

• Prestige or status cards, such as “gold” and“platinum” cards, offer consumers anincreased line of credit and a variety ofother benefits. They might charge anannual fee. These cards are highly pro-moted to consumers with establishedcredit.

• Co-branded cards carry the name of notonly a card network and possibly a bank,but also another company—a retail store,a hotel chain, or a long distance service,

Section 11.3 Managing Credit Cards • 273

• Annual fee. Few private label cardscharge an annual fee, but some generalpurpose cards do.

• Annual percentage rate. The APR, orannual percentage rate, is the annual rateof interest that is charged for using credit.The APR of revolving credit cards canvary significantly and makes a big differ-ence in the cost of using credit.

• Whether the APR may change. Avariable rate means that the APR can goup or down depending on economic fac-tors. The agreement must explain how avariable rate is determined and how oftenit may change. Even with a fixed APR,check the fine print of the agreement tosee whether the rate can increase for anyreason, such as if you are late making pay-ments. Also watch out for cards that havea teaser rate—a low introductory rate thatis in effect for only a limited time.

• Computation method. The agreementspecifies how finance charges are com-puted. The method used can make a sig-nificant difference in how much interestyou’ll pay. Figure 11-7 on page 274 com-pares several common computationmethods.

• Minimum payment. You must make atleast a minimum payment by the duedate. The credit agreement will state howthe minimum payment is determined. Itwill also state what happens if you fail tomake a required monthly payment whendue. The creditor may, for example,require payment at once of the entire out-standing balance of your account.

• Grace period. Many credit cards allowa grace period, or period of time duringwhich the balance may be paid in full toavoid finance charges. A grace period of20 to 25 days is common. Check the termscarefully to see how the grace periodworks. For instance, it might not apply ifthere is an unpaid balance carried overfrom the previous bill.

• Minimum finance charge. Somecards specify that in months when youowe a finance charge, it will be at least acertain amount. For instance, if you carryover a balance of only $1, a minimumfinance charge of 50 cents may apply.

• Other fees. The cardholder agreementmay specify fees for late payments, cashadvances, exceeding your credit limit, andreturned checks, for example.

DOLLARSandSENSE

Many credit card companies visit college cam-puses to recruit new cardholders. They set uptables outside bookstores and student centers,handing out goodies and persuading studentsto sign up. For students who can successfullymanage it, a credit card is an opportunity to

build a positive credit history. However, somestudents quickly run up more debt than theycan handle. They end up in the credit cardtrap—and sometimes out of school, too. Forthis reason, some colleges have banned on-campus credit card pitches.

Campus Credit Card Lures

274 • CHAPTER 11 Consumer Credit

11-7 The finance charge you pay depends on the computation method used by the creditor.

Why might you choose a card with a slightly higher APR than another?

METHOD

Previous Balance MethodOne of the most costly to the consumer.1. The amount owed at the end of the last billing cycle is the previous balance.2. The previous balance is multiplied by the monthly interest rate.

Adjusted Balance MethodUsually the best method for the consumer, but not common.1. Any payments or credits made during the billing cycle are subtracted from the previous bal-

ance. This is the adjusted balance.2. The adjusted balance is multiplied by the monthly interest rate.

Average Daily Balance Method (excluding new purchases)Favorable to the consumer.1. For each day in the billing cycle, payments made are deducted from the previous balance.2. All daily balances are totaled, then divided by the number of days in the billing cycle to find

the average daily balance.3. The average daily balance is multiplied by the monthly interest rate.

Average Daily Balance Method (including new purchases)The most common method.1. For each day in the billing cycle, payments made are deducted from the previous balance

and new purchases are added.2. All daily balances are totaled, then divided by the number of days in the billing cycle to find

the average daily balance.3. The average daily balance is multiplied by the monthly interest rate.

Two-Cycle Average Daily Balance MethodOne of the most costly to the consumer.Computed like the average daily balance method, except that the average is based on the pre-vious billing cycle as well as the current one.

EXAMPLE

$6.00

$1.50

$3.75

$4.05

Depends on activity in previousbilling cycle.

Finance Charge Computation Methods

Suppose the APR is 18% and the previous balance is $400. The current billing cycle (the period of time between monthly state-ments) is 30 days. You made a payment of $300 on the 16th day and a purchase of $50 on the 19th day. The “Example”column shows how much you would pay in finance charges using each computation method.

Section 11.3 Managing Credit Cards • 275

• Credit limit. The credit limit is the max-imum amount of credit that the creditorwill extend to the borrower. If the creditlimit is $1,000, your unpaid charges can-not total more than that amount at anytime.

• Special features and services. Somecredit cards offer incentives such as rebatesor discounts, frequent flyer miles, insur-ance coverage, and other special features.Be sure to weigh these benefits againstother factors, such as the card’s annual feeand interest rate. See Figure 11-8.

As you compare credit card offers, con-sider how you plan to use the card. If youthink you’ll carry over a balance, look for alow interest rate. If you intend to pay the bal-ance in full every month, a card with noannual fee—regardless of its interest rate—would be a good choice.

Truth in Lending ActThe federal government has made it easier

for consumers to understand the terms ofcredit and loan agreements by passing theTruth in Lending Act. The act requires cred-itors to adequately inform consumers aboutcredit terms and costs. Lenders must disclosespecific information such as the APR, howvariable rates are calculated, when paymentsare due, and all fees. On most credit cardapplications, information required by theTruth in Lending Act is clearly labeled andeasy to find. This can be very helpful as youcompare the terms and costs of differentcards.

Before you apply for a credit card, makesure you have read the disclosures andunderstand the basic terms of the account. Ifyour application is accepted, you will receivea cardholder agreement that spells out theterms in detail. Read this information care-fully. Once you begin using the card, you arelegally bound by those terms.

11-8

When evaluating credit card

incentives, consider whether you’ll

actually make use of them.

Frequent flyer miles, for example,

often have restrictions on when

and how they may be used.

made only the minimum payment eachmonth, it could take you more than 20years to pay off the balance!

• Pay bills on time to avoid late fees andprotect your credit history.

Safeguarding YourCard

Credit card fraud—unauthorized use ofcredit cards or account numbers that havefallen into the wrong hands—is a seriousproblem. To protect yourself, keep your cardswith you or in a safe place at all times. Whenyou hand over a credit card to make a pur-chase, be sure it’s returned to you before youleave. If possible, keep it in your sight. SeeFigure 11-9.

Remember to safeguard not only the carditself, but the number. Keep receipts andother documents containing your credit cardnumber in a safe place, and shred thembefore discarding them. Don’t give the num-ber to just anyone. Know to whom you aregiving it and that the reason is legitimate.Before sending your card number over theInternet, make sure you’re using a secureconnection.

276 • CHAPTER 11 Consumer Credit

USING CREDIT CARDSWISELY

Once you have a credit card, wisely man-aging its use will help you maintain a goodcredit history. Follow these pointers:

• Remember that your credit limit is a max-imum, not a goal. It may be more thanyou want to, or can afford to, borrow.

• Save your credit card receipts. Use them tokeep a running total of how much you’vecharged each month. You’ll also want tocheck them against your monthly bill.

• Set your own limit for how much youwant to charge each month. When you getclose to the limit, slow down. If you reachthe limit, put the card away in a safe place.

• Whenever possible, pay the full balanceeach month to avoid finance charges.

• If for some reason you can’t pay the fullbalance, make the largest payment youcan afford. If you charged $1,000 and

11-9

Giving your credit card number over

the phone can be risky. Would it be

safer to give the number if you made

the call or if someone called you?

Section 11.3 Managing Credit Cards • 277

Keep a record of your credit card numbersin a safe place separate from the cards. If acard is lost or stolen, notify the credit cardcompany immediately. Under the ConsumerCredit Protection Act, the maximumamount for which you may be held liable ifsomeone uses the card illegally is $50. If,however, you inform the company beforesomeone else uses the card, you have no lia-bility at all.

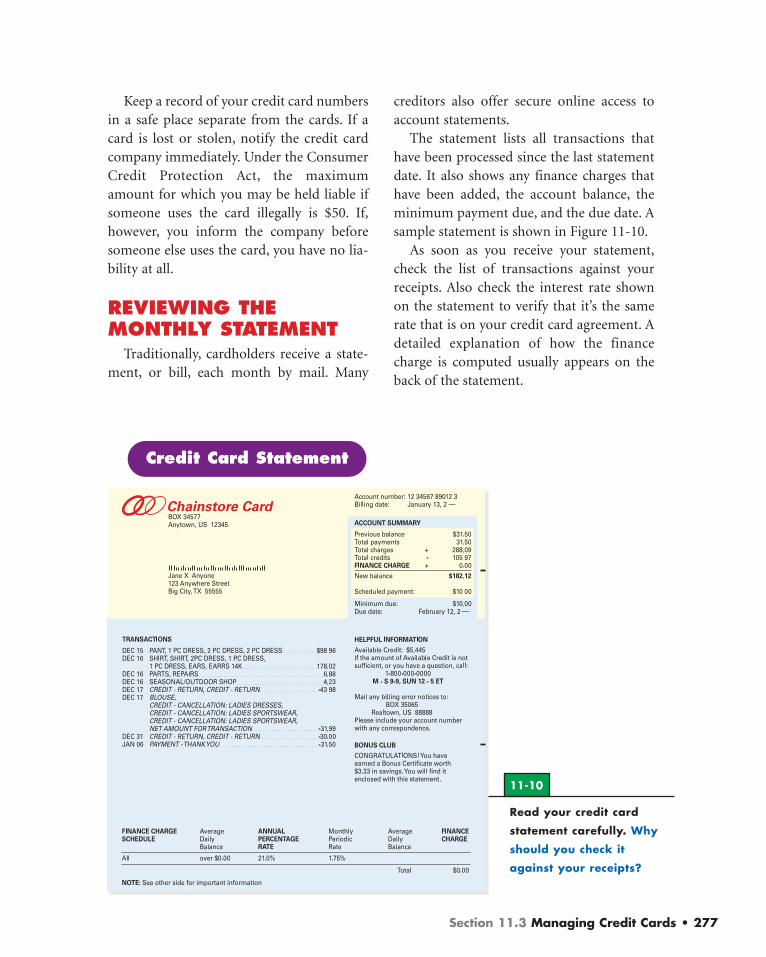

REVIEWING THEMONTHLY STATEMENT

Traditionally, cardholders receive a state-ment, or bill, each month by mail. Many

creditors also offer secure online access toaccount statements.

The statement lists all transactions thathave been processed since the last statementdate. It also shows any finance charges thathave been added, the account balance, theminimum payment due, and the due date. Asample statement is shown in Figure 11-10.

As soon as you receive your statement,check the list of transactions against yourreceipts. Also check the interest rate shownon the statement to verify that it’s the samerate that is on your credit card agreement. Adetailed explanation of how the financecharge is computed usually appears on theback of the statement.

11-10

Read your credit card

statement carefully. Why

should you check it

against your receipts?

Credit Card Statement

278 • CHAPTER 11 Consumer Credit

the name of the consumer who made thepurchase. During the investigation, you maywithhold payment on the disputed amount,but you are still obligated to pay the rest ofthe bill as usual.

If the investigation shows that the bill wascorrect, you must pay the disputed amountand any finance charges that have accumu-lated. However, if the error is confirmed, thecreditor must credit your account for the dis-puted amount and remove any relatedfinance charges.

RESOLVING BILLINGPROBLEMS

Sometimes there is an error on a billingstatement. The amount of a transaction maybe incorrect, a charge may be listed twice, oryour statement may not reflect a paymentthat you’ve made. If a charge you don’t rec-ognize appears on your statement, yourcredit card number may have been usedwithout your consent.

Consumers have legal rights that protectthem in case of billing errors and unautho-rized use of their credit cards. Knowing whatto do in case of a problem will help you pre-serve your rights.

Fair Credit Billing ActThe Fair Credit Billing Act outlines proce-

dures for settling credit card billing disputes.To preserve your rights, you must write a let-ter to the creditor at the address the creditcard statement says to use for billing errors.Your letter must reach the creditor within 60days after you received the first bill contain-ing the error. In the letter, include yourname, account number, and a detaileddescription of the problem. Enclose copies ofreceipts or other documents that supportyour position, and keep a copy of your letter.Send the letter by certified mail, returnreceipt requested, so that you’ll have proof ofwhat the creditor received.

The creditor is required to respond inwriting within 30 days and resolve the claimwithin 90 days. The creditor will first investi-gate the problem. For example, if you say youdid not make a purchase listed on your state-ment, the creditor will ask the merchant toproduce a copy of the signed receipt showing

Section 11.3 Review

CHECK YOURUNDERSTANDING

1. What is the difference between a revolv-ing credit card and a charge card?

2. What is APR, and why is it an importantconsideration when shopping for acredit card?

3. What can you do to help prevent unau-thorized charges from appearing onyour credit card bill? If they do appear,what should you do?

CONSUMER APPLICATIONCredit Card Choices Imagine that a bankoffers its customers a choice of three creditcards. Card 1 charges no interest for thefirst six months, but 15 percent after that.Card 2 charges a flat interest rate of 9 per-cent, with a guarantee of no interest hikesfor at least two years. Card 3 has an annualfee of $25 and a rate of 8 percent for thefirst six months with a possibility of a hikeafterward. Under what circumstancesmight a consumer choose each card?

S E C T I O N 1 1 . 4

Taking Out a Loan

Most consumers, at some point oranother, choose to take out a loan—perhaps for a car, a house, or a majorappliance. Knowing how to get andmanage the right loan will help youavoid financial difficulties.

SOURCES AND TYPES OF LOANSLoans are available from a number of sources. The

choice of where to borrow and what type of loan to get hasan impact on the overall cost of credit. Make sure yourchoice is the right one.

Loans from FinancialInstitutions

Many consumers prefer getting a loan from a bank.Most financial institutions offer a variety of loans to meetdifferent needs. Interest rates and other terms depend onthe type of loan.

• Home loans are closed-end installment loans for thepurchase of a home. The repayment plan is typically 15,20, or 30 years. The home serves as security for the loan.

Objectives

After studying this section, youshould be able to:• Discuss sources and types of

loans.• Explain provisions that may be

found in loan contracts.• Describe the loan process from

application to payment.

Key Termsconsumer finance companies

loan sharksdown paymentballoon paymentacceleration clauseadd-on clauseright of rescission

279

280 • CHAPTER 11 Consumer Credit

• A personal line of credit is an open-end,usually unsecured loan. After the loan isapproved, the consumer can draw upon itwhen needed up to a preset limit.

• Education or student loans, used to pay forhigher education, often have low interestrates and flexible repayment schedules.

Loans from FinanceCompanies

Consumer finance companies are busi-nesses that specialize in making small or per-sonal loans. Often, they give credit to thosewho cannot get it elsewhere because of anegative credit history, low income, or mini-mal assets. Compared to banks, finance com-panies usually charge more for their loansfor the following reasons:

• Finance companies do not have deposi-tors to supply the money they lend. Theymust borrow the money they lend and payinterest on it.

• Consumers who already own a home maytake out a home equity loan, using theirownership interest (equity) in their homeas security. These loans can be used for avariety of purposes. Some are closed-endloans; others are an open-end line ofcredit, available whenever the homeownerneeds or wants to use it.

• A home improvement loan helps thehomeowner make needed repairs orimprovements to a home, thus increasingits value when it comes time to sell. It’s aclosed-end loan, typically with a five-yearterm, and is usually secured by the home.See Figure 11-11.

• A vehicle loan is a closed-end, secured loanfor the purchase of a new or used vehicle.Repayment terms vary but generally arefrom three to five years.

11-11

Some loans can be used for any

reason, while others have a specific

purpose. What type of loan might

best fit this situation?

11-12

The fee for a small payday loan may not

seem excessive when stated in dollars

and cents. However, the actual APR could

be 300% or more.

Section 11.4 Taking Out a Loan • 281

• With each loan, a lender incurs costs forcredit investigations and record keeping.Since they make relatively small loans,finance companies can’t absorb such costsas easily as banks.

• The typical borrower handled by a con-sumer finance company is a greater creditrisk than the typical bank borrower. Thus,collection costs and bad debts are higher.

“Payday” LoansSome check-cashing facilities, finance

companies, and other establishments makesmall, short-term, high-interest-rate loansknown as payday loans, or cash advanceloans. Usually, a borrower writes a personalcheck payable to the lender for the amounthe or she wishes to borrow plus a fee. Thecompany gives the borrower the amount ofthe check minus the fee and holds the check

until the borrower’s next payday. The fee fora payday loan might be a percentage of theloan amount or a certain fee for every $50 or$100 loaned.

Wise consumers steer clear of paydayloans. The APR—which must be disclosedunder the Truth in Lending Act—can beextremely high. See Figure 11-12. Borrowingagainst the next paycheck often creates acycle of debt that can be difficult to break.Consumers who need to borrow would bebetter off applying for a loan from a bank,savings and loan, or credit union.

Insurance Policy LoansSome life insurance policies are a source

of loans. The policyholder can borrowmoney against the amount he or she hasalready paid in premiums. The insurancecompany gives the money quickly, no creditinvestigation is needed, and the policy servesas the only security. The interest rate is usu-ally lower than bank rates. However, borrow-ers should keep two potential drawbacks inmind:

• The main purpose of life insurance is topay a benefit to survivors in the event ofthe policyholder’s death. If there is an out-standing loan, the company will deductany amount still owed before paying thebenefit.

• Be prepared to prove that you can payback the loan. Provide a copy of yourcheck stub or have the lender contact youremployer to verify your salary.

• Agree with the lender on the interest rate.See Figure 11-13.

• Agree on a payment plan. Specify the dateand amount of each payment.

• Be specific about the terms of the loan.Put everything in writing. Use loan formsfrom an office supply store, or write yourown agreement.

• Pay promptly. If you lose your source ofincome, talk to the lender immediatelyabout making other arrangements for theloan payments.

• Get and keep a signed receipt for eachpayment to prove that you paid back theloan.

Loans from OtherSources

Some consumers borrow money againsttheir credit cards. Cash advances and “con-venience checks” are available from creditcard companies at interest rates that are gen-erally as high as the original credit cardagreement. Loans from other sources oftencost less.

• Some companies do not regularly remindthe borrower to pay back the loan. Theborrower often pays only the interest,allowing the loan to ride. This increasesthe total amount of interest that must bepaid.

Private LoansSometimes people turn to family mem-

bers or friends when they need to borrowlarge sums of money. While this can be ahelpful option, it has the potential to causestrained relationships if the debt is notrepaid. Private loans work best when theseguidelines are followed:

• Keep the loan as small as possible.Remember to consider your otherexpenses.

282 • CHAPTER 11 Consumer Credit

11-13

Loans between friends or family members can

cause problems when not handled carefully.

What might cause such problems?

11-14

If you’re not expecting it, a balloon

payment can come as a shock. How

can you find out whether a loan has

a balloon payment?

Section 11.4 Taking Out a Loan • 283

Another costly way to get a loan isthrough the services of a pawnbroker. Theconsumer trades an item of value, such asjewelry, to the pawnbroker for a sum ofmoney usually far below the item’s worth.The pawnbroker holds the item for a periodof time—usually 30 days—during whichtime the consumer has use of the money. Theconsumer then essentially has to buy backhis or her property at a substantially higherprice than the pawnbroker paid.

Consumers should avoid dealing withloan sharks, unlicensed lenders who operateillegally and charge excessive interest. Theyprey on consumers who are unable to get aloan from a legitimate creditor. If the bor-rower has difficulty repaying, the loan sharktypically renews the loan with even lessfavorable terms. Soon the borrower is in animpossible financial situation.

LOAN CONTRACTPROVISIONS

Before you take out a loan, shop around toget the best terms you can. Because of theTruth in Lending Act, the creditor is requiredto clearly specify all provisions of the loan inwriting. For example, the contract must statethe APR, when payments are due, andwhether you will be charged a penalty if youpay back the loan ahead of schedule.

If you’re financing the purchase of anitem, a down payment may be required. Adown payment is a portion of a purchaseprice paid by cash or check at the time ofpurchase. For example, if you were buyingfurniture that cost $1,000, you might make a$100 down payment and finance (take out aloan for) the other $900. Loan contractsshould spell out the amount of down pay-ment, if any, and the amount financed.

When you apply for a loan, keep an eyeout for the following clauses. Understandingthem in advance will help you avoid unpleas-ant surprises.

Balloon PaymentClause

A final payment that is much larger thanthe other installments is called a balloonpayment. Suppose you’ve been makingweekly payments of $50 on an installmentcontract for an entertainment center. Whenyou receive the final bill, you discover thatthe amount due is $500—ten times morethan you expected. See Figure 11-14.

284 • CHAPTER 11 Consumer Credit

Add-On ClauseAn add-on clause allows additional pur-

chases to be added to an installment con-tract, with earlier purchases used as securityfor later ones. Suppose you buy a sofa on aninstallment contract. Before you finish pay-ing for it, you buy a refrigerator under thecontract’s add-on clause. If you later stopmaking payments, the creditor can take backboth the sofa and the refrigerator, no matterhow much you had paid toward the sofa.

In some states, the consumer is protectedby laws that require payments to be prorated,or divided proportionately. Each payment isapplied to each item until those bought firstare paid in full. Those goods that are paid forno longer serve as security for later purchases.

GETTING THE LOANAfter you’ve shopped for the best terms

and have decided on a lender and type ofloan, you are ready to apply. You may be ableto apply for a loan by telephone, online, or inperson. To streamline the process, be pre-pared to provide information about yourincome, employment history, residence, andcredit history. See Figure 11-15.

Balloon payments often lead to refinanc-ing—that is, getting another loan, with morefinance charges, to pay off the first loan. Tomake matters worse, the new contract mayhave a balloon payment clause, too. As aresult, buyers find it increasingly difficult toget out of debt. If you can’t avoid a balloonpayment clause, be sure to plan ahead for thefinal payment.

Acceleration ClauseAn acceleration clause gives the seller the

right to declare the whole balance due if thebuyer misses even one installment payment.For example, suppose you have made 15 pay-ments of $75 a week and still have 15 pay-ments remaining. If you miss the 16th pay-ment because of illness or for any otherreason, the merchant could demand imme-diate payment of the $1,125 balance.

If you think you may have difficulty mak-ing a payment by the required date, contactthe lender as soon as possible. With advancenotice, the merchant might be willing towork out a solution that is satisfactory toboth of you.

11-15

Applying for a loan is easier if you’re

prepared for the questions that will be

asked. What materials might you want

to have with you?

Section 11.4 Taking Out a Loan • 285

Once you complete the application, you’llhave to wait while the creditor runs a creditcheck. This can sometimes be done immedi-ately; in other cases, you may need to wait aday or longer for approval.

After you’ve been approved, you’ll berequired to sign the loan contract. Read itcarefully and make sure the terms are exactlyas you agreed when you were shopping.

At this time, the lender might suggest thatyou purchase credit life insurance. This insur-ance, which is optional, is designed to pay offthe loan in the event of your death. Keep inmind that it’s expensive compared to othertypes of insurance. Don’t feel pressured topurchase it.

If you are pledging your home as securityfor a loan or other credit transaction, youhave the right to cancel the loan within threebusiness days. This right, called the right ofrescission, is provided by the Truth inLending Act. Notice of cancellation must begiven in writing.

The loan contract will outline your pay-ment schedule. Whether you agree to pay theloan back by making monthly payments orby using another schedule, you will mostlikely pay in installments. Repaymentoptions may include paying online, settingup automatic deductions from your bankaccount, or using a payment booklet asshown in Figure 11-16.

Section 11.4 Review

CHECK YOURUNDERSTANDING

1. Explain one benefit and one drawback ofgoing to a consumer finance companyfor a loan.

2. What is a balloon payment clause, andhow does it affect consumers?

3. In what ways can one apply for a loan?

CONSUMER APPLICATIONComparing Rates Compare the interestrates of three different types of loansoffered by one financial institution. Givepossible reasons why some rates are higherthan others, based on other characteristicsof the loans.

11-16 A payment booklet contains

dated coupons to be enclosed when you

mail payments.

S E C T I O N 1 1 . 5

Handling DebtProblems

A prospective creditor who says “no”to a request for credit may be doingthe consumer a favor. Becoming over-loaded with debt can lead to seriousfinancial difficulty. For consumers whodo find themselves with more debt thanthey can handle, help is available.

DANGERS OF EXCESS DEBTConsumers can get into trouble with debt for a number

of reasons. Crises such as the loss of a job, a serious illness,or a divorce can make it difficult for even a careful moneymanager to keep up with payments. In other cases, the lureof overspending leads consumers into debt. Whatever thereason, taking on too much debt can have serious effects,including:

• Inability to keep up with normal expenses from onepaycheck to the next.

• Getting caught in a cycle of taking on new debt to payoff old debt.

• Stress over constant financial worries.

• Serious damage to one’s credit history.

• Inability to save or invest sufficiently to reach financialgoals.

Objectives

After studying this section, youshould be able to:• Analyze the consequences of

excess debt.• Identify warning signs of

excess debt.• Describe assistance and reme-

dies for debt problems.

Key Termsdelinquentdefaultrepossessioncollection agencyliengarnishmentcredit counselingdebit consolidation loanbankruptcy

286

Section 11.5 Handling Debt Problems • 287

DEBT COLLECTIONMETHODS

When you sign a loan contract or creditcard agreement, you are legally obligated topay back the debt. What happens if you failto make payments when they are due? Atfirst, the creditor may simply send notices ofyour overdue, or delinquent, payments. Bypaying promptly, you may be able to avoidmore serious consequences. Should pay-ments continue to be delinquent, the credi-tor will probably report this information toone or more credit bureaus. You may receivea notice that you are in default, which meansfailure to fulfill the obligations of the loan,and a warning that the creditor is takingmore aggressive actions toward collecting thedebt.

Repossession and Shut-offs

Suppose you buy a television throughstore credit and fail to make payments. Inmost cases, the creditor can take back the TV.Taking away property due to failure to makeloan or credit payments is called reposses-sion. See Figure 11-17. If you fail to makepayments for services, such as electricity ortelephone service, those creditors may shutoff or discontinue providing the service.

Collection AgenciesAfter exhausting its own efforts to get a

consumer to make past-due payments, acreditor may turn the account over to a col-lection agency. This is a business that col-lects unpaid debt for others. The debtor’scredit report will reflect the fact that a collec-tion agency has been called in, seriously low-ering his or her credit rating.

In most cases, agencies earn a percentageof the debt collected, giving them strongincentives for being relentless and aggres-sive in their collection tactics. However, theFair Debt Collection Practices Act protectsconsumers against abusive practices of debtcollectors, such as harassment, overcharg-ing, and disclosing consumers’ debt to thirdparties.

11-17

When a consumer doesn’t keep up with car

payments, the vehicle may be towed away.

Why does the creditor have the right of

repossession in this case?

288 • CHAPTER 11 Consumer Credit

AVOIDING EXCESS DEBTBy far the best solution to the problem of

excess debt is avoiding too much debt in thefirst place. Individuals and families shouldset reasonable limits for debt, taking intoconsideration their income, fixed expenses,savings, and other assets. Then they musthave the discipline to stay within those lim-its. For example, they may have to postponeor reconsider some purchases instead ofcharging everything they want to a creditcard. Setting aside some “rainy day” savingswill reduce the need to borrow when unex-pected expenses come up.

Warning SignsConsumers who constantly worry about

credit cards and loans—and continue tospend more than they make—probablyalready know that they have debt problems.See Figure 11-18.

Judgments and LiensIf other efforts fail, a creditor may go to

court and get a judgment, or court ruling,that says the debt must be paid. The con-sumer may be ordered to pay the creditor’sattorney fees in addition to the original debt.

If the debtor owns a home, the judgmentmay appear on record as a lien. A lien(LEEN) is a claim upon property to satisfy adebt. When the home is sold, money fromthe sale is first used to pay any lien holders.The debtor receives only the amount that isleft, if any. Judgments and liens are a matterof public record, appear on the debtor’scredit report, and lower his or her credit rating.

GarnishmentGarnishment is the legal withholding of a

specified sum from a person’s wages in orderto collect a debt. If ordered by the court, thedebtor’s employer must withhold part of theworker’s wages and send the money to thecourt, which then passes it on to the creditor.Money is withheld from the worker’s pay-check until the debt and all court costs arepaid.

11-18

Financial problems can be a major

source of stress.

Section 11.5 Handling Debt Problems • 289

Other warning signs of a debt probleminclude:

• Reaching the credit limit on most creditcards.

• Skipping payments on some bills in orderto pay others, or using cash advances onone credit card to pay off another.

• Using credit cards for day-to-day pur-chases like groceries, movie tickets, or fastfood—not simply as a convenience or toearn cardholder rewards, but due to lackof cash.

CLIMBING OUT OF DEBTIf you find yourself in financial difficulty,

here are some options that can help yourecover.

• Working with creditors. Contactcreditors immediately to let them knowyou are having problems. See whether youcan adjust payment terms. Most creditorswill be willing to work with you to find amutually beneficial solution.

• Self-help measures. Although credi-tors and others can provide help, much ofwhat needs to be done is up to you. Beginby stopping your use of credit cards. Makepaying off debts your top priority. SeeFigure 11-19.

• Credit counseling. Many consumershave overcome debt problems with thehelp of credit counseling, guidance pro-vided by trained people who help con-sumers learn to live within their means.Money that the consumer deposits eachmonth with the counseling service is usedto pay creditors according to a paymentschedule developed by the counselor.Some credit counseling services charge lit-tle or nothing for managing the plan; oth-ers charge a monthly fee that could add upto a significant amount over time.

11-19

Recovering from excess debt is possible.

Getting rid of credit cards and contacting

creditors are two simple ways to begin.

290 • CHAPTER 11 Consumer Credit

Bankruptcy: A LastResort

When all other options fail, a consumermay be forced to file personal bankruptcy.Bankruptcy is legal relief from repaying cer-tain debts. The decision to file for bank-ruptcy is a serious one and should be givenmuch consideration.

Two types of personal bankruptcy arecommonly used by consumers. They arenamed after chapters of the federalBankruptcy Code.

• Chapter 7 requires, in most cases, thesale of all the debtor’s property except thatprotected from bankruptcy under state orfederal law. The money from the sale ofthe property is distributed to creditors.

• Chapter 13 allows the debtor to keepproperty. The debtor proposes a plan,which must be approved and supervisedby the court, to pay off some or all of the

• Debt consolidation loans. A con-sumer who has several debts and is notable to make payments on all of themevery month may find a debt consolida-tion loan appealing. A debt consolida-tion loan combines all existing debt into anew loan with a more manageable pay-ment schedule. You use the money fromthe new loan to pay off all previous credi-tors. Then you can make just one paymenteach month to the lending agency. Beforetaking on a debt consolidation loan,investigate its terms thoroughly. The loanmay achieve lower monthly payments bysimply spreading out debt over a longerperiod of time, resulting in additionalinterest charges. Some debt consolidationloans are actually home equity loans inwhich the home is pledged as security.

DOLLARSandSENSE

Bad Credit? No Credit? No Problem! That’swhat the ads would have you believe. When itcomes to credit repair offers, be suspicious ofcompanies that:

• Want you to pay for credit repair servicesup front.

• Don’t tell you your legal rights and whatyou can do yourself for free.

• Recommend against contacting creditbureaus directly.

• Advise you to create a “new” credit identityunder a different name or identificationnumber. This is illegal, and you could beprosecuted for fraud.

Credit “Cures” to Avoid

If you suspect that a business is acting in an ille-gal way to help you “erase” your debts, contactthe Federal Trade Commission immediately.

Section 11.5 Handling Debt Problems • 291

debt over time. Debtors who have regularincome and debt under a certain amountqualify for Chapter 13.

During bankruptcy proceedings, thedebtor is protected from debt collectionactivities. After complying with all of thebankruptcy requirements, the debtor is ingeneral relieved of the responsibility to payany remaining prior debt. However, certaindebts, such as taxes, child support, and most student loans, are still the debtor’s legalobligation.

A serious disadvantage of bankruptcy isthe damage to the person’s credit history. Abankruptcy filing remains on a person’scredit report for ten years.

Rebuilding CreditImproving one’s credit history after debt

problems is largely a matter of time. By law,most delinquencies and judgments remainin a credit report for seven years. Bankruptcyremains for seven to ten years. The goodnews is that after that time, there will be noindication of the past debt problems.

Aside from waiting it out, consumers witha poor credit history can take several steps to

improve it. Paying bills on time is the mostimportant factor. Avoiding high balances oncredit cards and resisting the temptation toopen additional credit accounts will alsohelp. See Figure 11-20. With diligence, care,and patience, consumers can overcome debtproblems and make a new start.

Section 11.5 Review

CHECK YOURUNDERSTANDING

1. Explain three actions a creditor may taketo collect debt. How do they affect thedebtor’s credit history?

2. How can consumers recognize that theyhave a serious debt problem?

3. How can credit counseling help con-sumers?

CONSUMER APPLICATIONCredit Guidelines Assume that you arewriting credit guidelines for teen con-sumers. List the five most important piecesof advice you would offer them for avoid-ing debt problems.

11-20

By practicing financial discipline,

consumers can overcome debt

problems and build a positive

credit history.

1. Briefly describe how credit works. (11.1)2. What is collateral, and why might a creditor

require it? (11.1)3. Explain the difference between single-payment

and installment credit. (11.1)4. What are the costs of using credit? (11.1)5. How can your credit history demonstrate that

you will be a good credit risk? (11.2) 6. How is a credit score related to a credit

rating? (11.2)7. Give two examples of how to establish a good

credit rating and two examples of how tomaintain it. (11.2)

8. What is the difference between private labeland general purpose cards? (11.3)

9. Name three types of credit card terms andconditions you would compare before choos-ing a card. (11.3)

10. How does having a grace period benefitconsumers? (11.3)

11. How can you use a credit limit wisely? (11.3)12. How does the Truth in Lending Act protect

consumers? (11.3)13. Why is making only minimum payments on a

very large credit card bill a problem? (11.3)14. What is an add-on clause? (11.4)15. Identify the sequence of steps from the time

you decide the type and source of loan youwant. (11.4)

16. How does a lien work? (11.5)17. Which option should you try first to solve debt

problems—a debt consolidation loan orbankruptcy? Explain. (11.5)

C H A P T E R S U M M A R Y

•Using credit can temporarily expand purchas-ing power. Analyze the benefits and costs ofcredit carefully when you use it. (11.1)

•Lenders look at character, capacity, and capi-tal. A good credit rating is valuable. (11.2)

•Choose a credit card wisely by comparingterms and conditions. (11.3)

•Compare loans and lenders and be sure youunderstand the contract before signing. (11.4)

•Avoid the dangers of excess debt by recogniz-ing its warning signs. Options are availablefor recovering from excess debt. (11.5)

What’s That Charge? Sarah sees twocharges on her credit card statement that shedoesn’t recall making to companies shedoesn’t recognize. She wonders whethersomeone stole her card number and madethe purchases. What should she do beforedisputing the charges? If the charges werenot hers, what action should she take? (11.3)

292 • CHAPTER 11 Consumer Credit

Using a loan calculator on a financial Web site,determine the monthly payment and total costof the car for each loan. What factors wouldinfluence your loan choice? (11.4)

5. Excess Debt: Suppose someone is unable topay the bills each month and wants to get outof debt. Write diary entries over a period oftime as written by this person. Show the diffi-culties of the problem, including the differentmethods considered, such as payday loans andprivate loans. Through the diary, indicate howthe debt problem is eventually resolved in arealistic way. (11.4, 11.5)

• Family: Ask an adult family member toexplain his or her thoughts about cosign-ing a loan with you. How would thedecision be affected by the purpose ofthe loan? The amount? What might besome reasons for and against cosigning?(11.4)

• Community: Survey teens about theiruse of credit. Include frequency of use,average amount charged per month, use of personal or parents’ accounts,and pros and cons of using credit.Summarize your findings. (11.1, 11.2, 11.3)

Review & Activities • 293

1. Drawing Conclusions: Consumers often usecredit to buy food and other items that arereadily consumed. The debt remains long afterthe item is gone. Do you think it’s wise to usecredit in this way? Consider the benefits, costs,and drawbacks of using credit. (11.1)

2. Making Predictions: Suppose the graceperiod on a credit card is very short, and thecompany charges a late-payment fee of $25.What might happen? (11.3)

3. Analyzing Economic Concepts: How dointerest rates influence buying decisions? (11.1,11.3, 11.4)

4. Making Comparisons: Prepare a chart thatyou could use to compare information abouttwo different loans. Explain how the informa-tion in the chart would be helpful. (11.4)

1. Credit Report: Imagine that your credit reportmistakenly indicates you made several latepayments to a creditor. Write a letter to thecredit bureau requesting that the error be corrected. (11.2)

2. Credit Card Comparisons: Find informationabout three credit cards currently offered toconsumers. Read the terms and conditions andnote the APR of each card. Create a chart thatcompares the cards. (11.3)

3. Sources and Types of Loans: Compare thetypes of loans offered by the following sources:banks, consumer finance companies, andpawnbrokers. (11.4)

4. Loan Costs: Suppose you’re making a downpayment of $1,500 on a car that costs $18,000.You have the option of taking out a 36-month,48-month, or 60-month loan at 8% interest.