Embed Size (px)

Citation preview

Please refer to important disclosures at the end of this report 1

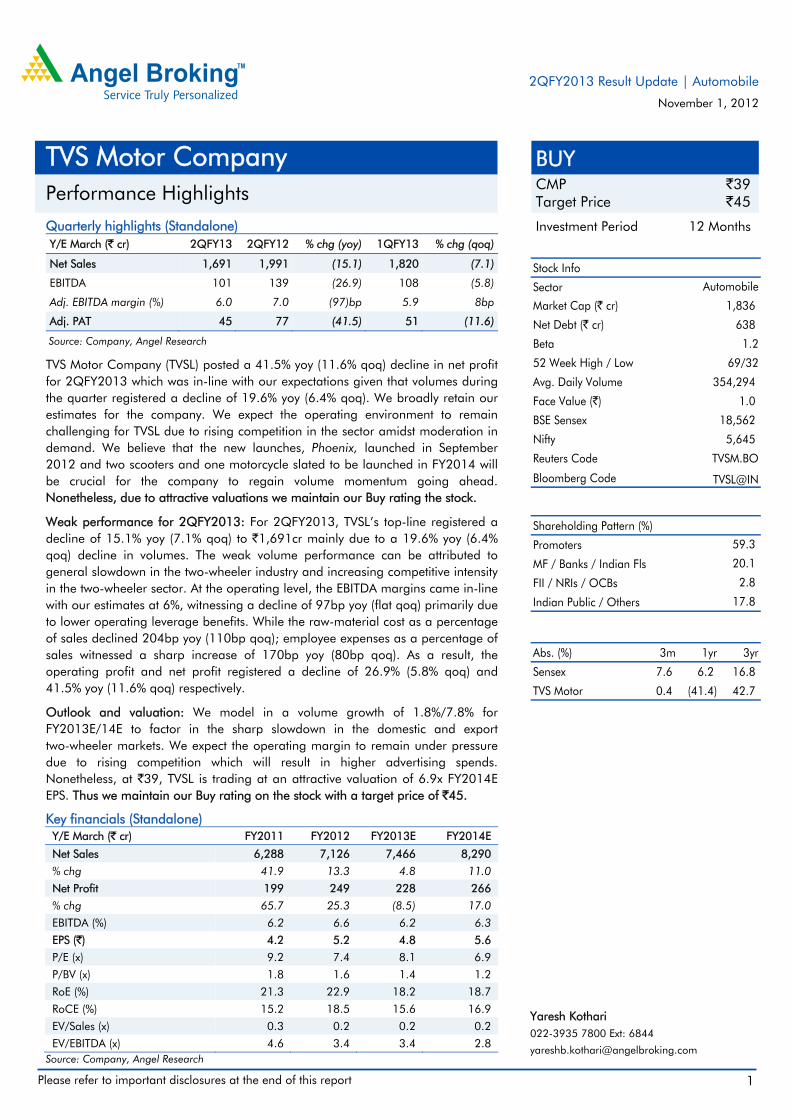

Quarterly highlights (Standalone) Y/E March (` cr) 2QFY13 2QFY12 % chg (yoy) 1QFY13 % chg (qoq)

Net Sales 1,691 1,991 (15.1) 1,820 (7.1)

EBITDA 101 139 (26.9) 108 (5.8)

Adj. EBITDA margin (%) 6.0 7.0 (97)bp 5.9 8bp

Adj. PAT 45 77 (41.5) 51 (11.6)

Source: Company, Angel Research

TVS Motor Company (TVSL) posted a 41.5% yoy (11.6% qoq) decline in net profit for 2QFY2013 which was in-line with our expectations given that volumes during the quarter registered a decline of 19.6% yoy (6.4% qoq). We broadly retain our estimates for the company. We expect the operating environment to remain challenging for TVSL due to rising competition in the sector amidst moderation in demand. We believe that the new launches, Phoenix, launched in September 2012 and two scooters and one motorcycle slated to be launched in FY2014 will be crucial for the company to regain volume momentum going ahead. Nonetheless, due to attractive valuations we maintain our Buy rating the stock.

Weak performance for 2QFY2013: For 2QFY2013, TVSL’s top-line registered a decline of 15.1% yoy (7.1% qoq) to `1,691cr mainly due to a 19.6% yoy (6.4% qoq) decline in volumes. The weak volume performance can be attributed to general slowdown in the two-wheeler industry and increasing competitive intensity in the two-wheeler sector. At the operating level, the EBITDA margins came in-line with our estimates at 6%, witnessing a decline of 97bp yoy (flat qoq) primarily due to lower operating leverage benefits. While the raw-material cost as a percentage of sales declined 204bp yoy (110bp qoq); employee expenses as a percentage of sales witnessed a sharp increase of 170bp yoy (80bp qoq). As a result, the operating profit and net profit registered a decline of 26.9% (5.8% qoq) and 41.5% yoy (11.6% qoq) respectively.

Outlook and valuation: We model in a volume growth of 1.8%/7.8% for FY2013E/14E to factor in the sharp slowdown in the domestic and export two-wheeler markets. We expect the operating margin to remain under pressure due to rising competition which will result in higher advertising spends. Nonetheless, at `39, TVSL is trading at an attractive valuation of 6.9x FY2014E EPS. Thus we maintain our Buy rating on the stock with a target price of `45.

Key financials (Standalone) Y/E March (` cr) FY2011 FY2012 FY2013E FY2014E

Net Sales 6,288 7,126 7,466 8,290

% chg 41.9 13.3 4.8 11.0

Net Profit 199 249 228 266

% chg 65.7 25.3 (8.5) 17.0

EBITDA (%) 6.2 6.6 6.2 6.3

EPS (`) 4.2 5.2 4.8 5.6

P/E (x) 9.2 7.4 8.1 6.9

P/BV (x) 1.8 1.6 1.4 1.2

RoE (%) 21.3 22.9 18.2 18.7

RoCE (%) 15.2 18.5 15.6 16.9

EV/Sales (x) 0.3 0.2 0.2 0.2

EV/EBITDA (x) 4.6 3.4 3.4 2.8 Source: Company, Angel Research

BUY CMP `39 Target Price `45

Investment Period 12 Months

Stock Info

Sector

Bloomberg Code

Shareholding Pattern (%)

Promoters

MF / Banks / Indian Fls

FII / NRIs / OCBs

Indian Public / Others

Abs. (%) 3m 1yr 3yr

Sensex 7.6 6.2 16.8

TVS Motor 0.4 (41.4) 42.7

59.3

20.1

2.8

17.8

TVSL@IN

1,836

1.2

69/32

354,294

Nifty

Reuters Code

1.0

18,562

5,645

TVSM.BO

Avg. Daily Volume

Market Cap (` cr)

Beta

52 Week High / Low

Net Debt (` cr) 638

Automobile

Face Value (`)

BSE Sensex

Yaresh Kothari 022-3935 7800 Ext: 6844

TVS Motor Company Performance Highlights

2QFY2013 Result Update | Automobile

November 1, 2012

TVS Motor Company | 2QFY2013 Result Update

November 1, 2012

2

Exhibit 1: Quarterly financial performance (Standalone) Y/E March (` cr) 2QFY13 2QFY12 % chg (yoy) 1QFY13 % chg (qoq) 1HFY13 1HFY12 % chg (yoy)

Net Sales 1,691 1,991 (15.1) 1,820 (7.1) 3,510 3,737 (6.1)

Consumption of RM 1,185 1,441 (17.7) 1,304 (9.1) 2,489 2,722 (8.5)

(% of Sales) 70.1 72.4 71.7 70.9 72.8 Staff Costs 108 93 15.8 102 5.2 210 184 14.2

(% of Sales) 6.4 4.7 5.6 6.0 4.9 Purchase of goods 37 40 (5.9) 32 15.5 70 72 (2.7)

(% of Sales) 2.2 2.0 1.8 2.0 1.9 Other Expenses 259 279 (7.2) 274 (5.4) 532 504 5.6

(% of Sales) 15.3 14.0 15.0 15.2 13.5 Total Expenditure 1,589 1,853 (14.2) 1,712 (7.2) 3,302 3,482 (5.2)

Operating Profit 101 139 (26.9) 108 (5.8) 209 256 (18.3)

OPM (%) 6.0 7.0 5.9 5.9 6.8 Interest 15 15 3.3 15 (1.7) 31 30 2.7

Depreciation 32 29 11.9 31 3.3 63 56 11.9

Other Income 4 6 (35.2) 5 (18) 9 10 (7.9)

PBT (excl. Extr. Items) 58 102 (42.7) 66 (12.0) 124 179 (30.7)

Extr. Income/(Expense) - - - - - - - -

PBT (incl. Extr. Items) 58 102 (42.7) 66 (12.0) 124 179 (30.7)

(% of Sales) 3.4 5.1 3.6 3.5 4.8 Provision for Taxation 13 24 (46.7) 15 (13.5) 28 43 (35.5)

(% of PBT) 22.3 24.0 22.7 (1.7) 22.5 24.2 Reported PAT 45 77 (41.5) 51 (11.6) 96 136 (29.2)

Adj PAT 45 77 (41.5) 51 (11.6) 96 136 (29.2)

Adj. PATM 2.7 3.9 2.8 2.7 3.6 Equity capital (cr) 47.5 47.5 47.5 47.5 47.5 Reported EPS (`) 1.0 1.6 (41.5) 1.1 (11.6) 2.0 2.9 (29.2)

Source: Company, Angel Research

Exhibit 2: 2QFY2013 – Actual vs Angel estimates Y/E March (` cr) Actual Estimates Variation (%)

Net Sales 1,691 1,719 (1.6)

EBITDA 101 102 (0.3)

EBITDA margin (%) 6.0 5.9 8bp

Adj. PAT 45 44 3.3

Source: Company, Angel Research

TVS Motor Company | 2QFY2013 Result Update

November 1, 2012

3

Exhibit 3: Quarterly volume performance

(unit) 2QFY13 2QFY12 % chg (yoy) 1QFY13 % chg (qoq) 1HFY13 1HFY12 % chg (yoy)

Total volumes 485,923 604,226 (19.6) 519,132 (6.4) 1,005,055 1,139,234 (11.8)

Domestic 430,029 519,727 (17.3) 454,293 (5.3) 884,322 978,056 (9.6)

Exports 55,894 84,499 (33.9) 64,839 (13.8) 120,733 161,178 (25.1)

Motorcycles Domestic 124,935 174,877 (28.6) 142,413 (12.3) 267,348 330,670 (19.1)

Exports 45,891 63,867 (28.1) 50,933 (9.9) 96,824 123,125 (21.4)

Total motorcycles 170,826 238,744 (28.4) 193,346 (11.6) 364,172 453,795 (19.7)

Scooters Domestic 117,220 148,341 (21.0) 105,366 11.3 222,586 257,620 (13.6)

Exports 1,881 9,121 (79.4) 7,466 (74.8) 9,347 17,365 (46.2)

Total scooters 119,101 157,462 (24.4) 112,832 5.6 231,933 274,985 (15.7)

Mopeds

Domestic 183,335 192,859 (4.9) 203,247 (9.8) 386,582 383,531 0.8

Exports 448 3,478 (87.1) 628 (28.7) 1,076 4,939 (78.2)

Total mopeds 183,783 196,337 (6.4) 203,875 (9.9) 387,658 388,470 (0.2)

Three-wheelers

Domestic 4,539 3,650 24.4 3,267 38.9 7,806 6,235 25.2

Exports 7,674 8,033 (4.5) 5,812 32.0 13,486 15,749 (14.4)

Total three-wheelers 12,213 11,683 4.5 9,079 34.5 21,292 21,984 (3.1)

Source: Company, Angel Research

Top-line down 15.1% yoy: For 2QFY2013, TVSL’s top-line registered a decline of 15.1% yoy (7.1% qoq) to `1,691cr mainly due to 19.6% yoy (6.4% qoq) decline in volumes during the quarter. The weak volume performance can be attributed to a general slowdown in the two-wheeler industry and also increasing competition from Honda Motorcycle and Scooters India Ltd (HMSI). As a result, motorcycle and scooters volume registered a sharp decline of 28.4% (11.6% qoq) and 24.4% yoy (up 5.6% qoq) respectively. Three-wheeler sales on the other hand staged a recovery, posting a 4.5% yoy (34.5% qoq) growth driven by 24.4% yoy (38.9% qoq) growth in the domestic markets.

Exhibit 4: Total volumes decline 19.6% yoy

Source: Company, Angel Research

Exhibit 5: Strong growth in net average realization

Source: Company, Angel Research

524,954 524,171 519,514 535,008

604,226

527,700 528,099 519,132 485,999

33.4 39.9 24.0

15.3 15.1

0.7 1.7 (3.0) (19.6)

(30.0)

(20.0)

(10.0)

0.0

10.0

20.0

30.0

40.0

50.0

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

2QFY

11

3QFY

11

4QFY

11

1QFY

12

2QFY

12

3QFY

12

4QFY

12

1QFY

13

2QFY

13

(%)(units) Total volume yoy growth (RHS)

30,285 30,781 30,968

31,911 32,300

32,808

30,352

34,502 34,191

6.8 7.6

8.9 8.1

6.7 6.6

(2.0)

8.1 5.9

(4.0)

(2.0)

0.0

2.0

4.0

6.0

8.0

10.0

28,000

29,000

30,000

31,000

32,000

33,000

34,000

35,000

2QFY

11

3QFY

11

4QFY

11

1QFY

12

2QFY

12

3QFY

12

4QFY

12

1QFY

13

2QFY

13

(%)(`) Net average realization yoy growth (RHS)

TVS Motor Company | 2QFY2013 Result Update

November 1, 2012

4

Exhibit 6: Better-than-expected top-line growth

Source: Company, Angel Research

Exhibit 7: Domestic market share trend

Source: Company, SIAM, Angel Research

EBITDA margin at 6.1%: On the operating front, the EBITDA margin came in-line with our estimates at 6%, witnessing a decline of 97bp yoy (flat qoq) primarily due to lower operating leverage benefits. While the raw-material cost as a percentage of sales declined 204bp yoy (110bp qoq); employee expenses as a percentage of sales witnessed a sharp increase of 170bp yoy (80bp qoq).

The management expects margins to improve going ahead, led by improved volumes and benign raw material prices. However, we believe that margins will remain under pressure, given the weak domestic demand scenario and increasing competition.

Exhibit 8: EBITDA margin mainatined at 6%

Source: Company, Angel Research

Exhibit 9: Net profit down 41.5% yoy

Source: Company, Angel Research

Net profit down 41.5% yoy: TVSL reported a 41.5% yoy (11.6% qoq) decline in its net profit to `45cr; which was broadly in-line with our estimates. The bottom-line performance during the quarter was weak led by weak performance at the operating level.

1,616 1,647 1,635 1,746 1,991

1,761 1,627

1,820 1,691

43.0 51.1

34.5

25.3 23.2

6.9 (0.5)

4.2

(15.1)

(20.0)

(10.0)

0.0

10.0

20.0

30.0

40.0

50.0

60.0

0

500

1,000

1,500

2,000

2,500

2QFY

11

3QFY

11

4QFY

11

1QFY

12

2QFY

12

3QFY

12

4QFY

12

1QFY

13

2QFY

13

(%)(` cr) Net sales (LHS) Net sales growth (RHS)

21.6 21.9 21.3 20.5 22.9

19.3

15.4 15.3 16.0

7.1 6.9 6.8 6.3 6.9 5.5 5.9 5.4 5.3

4.5 3.7 3.5 2.3 2.6 2.8 3.2 2.9 3.3

15.4 15.1 14.7 14.3 15.2 13.4 13.6 12.8 13.1

0.0

5.0

10.0

15.0

20.0

25.0

2QFY

11

3QFY

11

4QFY

11

1QFY

12

2QFY

12

3QFY

12

4QFY

12

1QFY

13

2QFY

13

(%) Scooters Motor CyclesThree Wheelers Total Two Wheelers

6.7 6.1 5.9 6.7 7.0 6.5 6.1 5.9 6.0

73.7 74.7 74.6 76.9 75.9 73.9 74.2 74.6 73.6

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

2QFY

11

3QFY

11

4QFY

11

1QFY

12

2QFY

12

3QFY

12

4QFY

12

1QFY

13

2QFY

13

(%) EBITDA margin Raw material cost/sales

55 56 44 59 77 57 57 51 45

3.4 3.4

2.7

3.4

3.9

3.2 3.5

2.8 2.7

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

0

10

20

30

40

50

60

70

80

90

2QFY

11

3QFY

11

4QFY

11

1QFY

12

2QFY

12

3QFY

12

4QFY

12

1QFY

13

2QFY

13

(%)(` cr) Net profit (LHS) Net profit margin (RHS)

TVS Motor Company | 2QFY2013 Result Update

November 1, 2012

5

Investment arguments

Success of new launches key to volume growth: TVSL posted a healthy 8.1% yoy growth in its volumes in FY2012 amidst slowdown in two-wheeler demand and rising competitive intensity in the sector. TVSL is in the process of launching three new models in FY2014 (executive segment bike, two scooters and a diesel three-wheeler), and we believe the success of these new launches is the key for the company to register volume growth going ahead. We expect the new launches to enable TVSL to ramp up its monthly run rate of two-wheelers and post annual volumes of 2.41mn units in FY2014E.

Adverse product mix to weaken margins: Declining contribution of

three-wheelers and scooters in the overall product mix coupled with rising

competition is likely to pressurize the company’s operating margin going

ahead. Nonetheless, weakening of commodity prices will provide some

comfort on the margin front. We expect the company’s margin to decline by

~40bp in FY2013.

Outlook and valuation

We model in a volume growth of 1.8%/7.8% for FY2013E/14E to factor in the sharp slowdown in the domestic and export two-wheeler markets. We expect operating margins to remain under pressure due to rising competition which will result in higher advertising spends. Nevertheless, we broadly retain our estimates for the company.

Exhibit 10: Change in estimates Y/E March Earlier Estimates Revised Estimates % chg

FY2013E FY2014E FY2013E FY2014E FY2013E FY2014E

Net Sales (` cr) 7,500 8,350 7,466 8,290 (0.5) (0.7)

OPM (%) 6.3 6.4 6.2 6.3 (10)bp (6)bp

EPS (`) 4.8 5.5 4.8 5.6 (0.4) 1.7

Source: Company, Angel Research

We expect the operating environment to remain challenging for TVSL due to rising competition in the sector amidst moderation in demand. We believe that the new launch, Phoenix, launched in September 2012 and two scooters and one motorcycle slated to be launched in FY2014 will be crucial for the company to regain volume momentum going ahead. At the current market price of `39, TVSL is trading at an attractive valuation of 6.9x FY2014E EPS. Thus we maintain our Buy rating on the stock with a target price of `45.

TVS Motor Company | 2QFY2013 Result Update

November 1, 2012

6

Exhibit 11: Key assumptions Y/E March FY09 FY10 FY11 FY12 FY13E FY14E Total volume (units) 1,321,534 1,536,895 2,032,404 2,196,138 2,234,662 2,410,041 Motorcycles 634,918 640,965 836,821 841,362 816,121 856,927 Scooters 246,153 309,501 452,006 529,095 555,550 622,216 Mopeds 435,589 571,563 703,717 785,942 825,239 891,258 Three-Wheelers 4,874 14,866 39,860 39,739 37,752 39,640 Change yoy (%) 3.8 16.3 32.2 8.1 1.8 7.8 Motorcycles 6.2 1.0 30.6 0.5 (3.0) 5.0 Scooters (6.9) 25.7 46.0 17.1 5.0 12.0 Mopeds 5.9 31.2 23.1 11.7 5.0 8.0 Three-Wheelers 3,707.8 205.0 168.1 (0.3) (5.0) 5.0 Domestic (units) 1,128,136 1,371,481 1,797,993 1,909,672 1,932,983 2,072,635 Exports (units) 193,398 165,414 234,411 286,466 301,679 337,406

Source: Company, Angel Research

Exhibit 12: Angel vs consensus forecast

Angel estimates Consensus Variation (%)

FY13E FY14E FY13E FY14E FY13E FY14E

Total op. income (` cr) 7,466 8,290 7,497 8,380 (0.4) (1.1) EPS (`) 4.8 5.6 4.5 5.5 6.7 2.8

Source: Bloomberg, Angel Research

Exhibit 13: One-year forward P/E band

Source: Company, Angel Research

Exhibit 14: One-year forward P/E chart

Source: Company, Angel Research

Exhibit 15: One-year forward EV/EBITDA band

Source: Company, Angel Research

Exhibit 16: Two-wheeler stocks’ performance vs Sensex

Source: Company, Angel Research

0102030405060708090

100

Apr

-03

Mar

-04

Mar

-05

Feb-

06

Jan-

07

Jan-

08

Dec

-08

Dec

-09

Nov

-10

Nov

-11

Oct

-12

(`) Share Price (`) 6x 9x 12x 15x

0.0 2.0 4.0 6.0 8.0

10.0 12.0 14.0 16.0 18.0 20.0

Jul-0

9

Oct

-09

Jan-

10

Apr

-10

Jul-1

0

Oct

-10

Jan-

11

Apr

-11

Jul-1

1

Oct

-11

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

(x) One-yr forward P/E Three-yr average P/E

0

1,000

2,000

3,000

4,000

5,000

6,000

Apr

-03

Mar

-04

Mar

-05

Feb-

06

Jan-

07

Jan-

08

Dec

-08

Dec

-09

Nov

-10

Nov

-11

Oct

-12

(` cr) EV (` cr) 4x 6x 8x 10x

0 50

100 150 200 250 300 350 400 450 500

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Apr

-12

Oct

-12

TVSL HMCL BJAUT Sensex

TVS Motor Company | 2QFY2013 Result Update

November 1, 2012

7

Exhibit 17: Automobile - Recommendation summary

Company Reco. CMP (`)

Tgt. price (`)

Upside (%)

P/E (x) EV/EBITDA (x) RoE (%) FY12-14E EPS

FY13E FY14E FY13E FY14E FY13E FY14E CAGR (%)

Ashok Leyland Buy 24 30 27.9 10.9 8.6 5.5 4.7 13.3 15.6 14.1

Bajaj Auto Neutral 1,845 - - 17.0 15.0 11.7 9.9 46.2 41.6 7.3

Hero MotoCorp Neutral 1,905 - - 16.1 14.6 8.4 7.0 48.3 41.9 9.7

Maruti Suzuki Neutral 1,455 - - 22.0 15.4 11.4 7.6 11.9 15.1 36.6 Mahindra & Mahindra Accumulate 899 986 9.6 16.4 14.3 9.5 7.9 24.3 23.4 15.9

Tata Motors Buy 267 316 18.4 6.9 5.9 3.8 3.2 32.6 28.8 11.6

TVS Motor Buy 39 45 16.0 8.1 6.9 3.4 2.8 18.2 18.7 3.5

Source: Company, Angel Research

Company background

TVS Motor (TVSL), a flagship company of the TVS Group, is the third largest 2W manufacturer in India. The company is present across the motorcycles, scooters and mopeds segments, having a market share of ~8%, ~22% and 100%, respectively. The company successfully ventured into the 3W segment in FY2009 and garnered a ~5% market share as of March 31, 2012. The company has three manufacturing facilities in India, located at Hosur (Tamil Nadu), Mysore (Karnataka) and Solan (Himachal Pradesh) with 2W and 3W capacity of 2.75mn and 75,000 units, respectively. TVSL is also the second largest exporter of two-wheelers in the country.

TVS Motor Company | 2QFY2013 Result Update

November 1, 2012

8

Profit and loss statement (Standalone)

Y/E March (` cr) FY2009 FY2010 FY2011 FY2012 FY2013E FY2014E

Total operating income 3,739 4,430 6,288 7,126 7,466 8,290

% chg 14.2 18.5 41.9 13.3 4.8 11.0

Total expenditure 3,552 4,243 5,896 6,657 7,006 7,764

Net raw material costs 2,783 3,137 4,614 5,261 5,524 6,126

Other mfg costs 111 133 171 202 220 245

Employee expenses 205 248 327 370 396 439

Other 453 724 784 823 866 953

EBITDA 187 187 392 469 459 526

% chg 94.9 0.4 109.2 19.7 (2.2) 14.5

(% of total op. income) 5.0 4.2 6.2 6.6 6.2 6.3

Depreciation & amortization 103 103 107 118 128 137

EBIT 84 85 285 352 331 388

% chg 6,824.8 1.3 235.5 23.5 (5.8) 17.2

(% of total op. income) 2.3 1.9 4.5 4.9 4.4 4.7

Interest and other charges 65 75 72 57 61 60

Other income 12 67 36 22 25 27

(% of PBT) 40.4 61.7 14.1 6.9 8.4 7.6

Recurring PBT 31 76 248 316 296 355

% chg (12.1) 144.9 225.7 27.6 (6.6) 20.1

Extraordinary income/(exp.) 2 (32) (4) - - -

PBT 30 108 252 316 296 355

Tax 0 (12) 54 67 68 89

(% of PBT) 0.1 (11.0) 21.2 21.3 23.0 25.0

PAT (reported) 31 88 195 249 228 266

ADJ. PAT 29 120 199 249 228 266

% chg 872.9 306.6 65.7 25.3 (8.5) 17.0

(% of total op. income) 0.8 2.7 3.2 3.5 3.0 3.2

Basic EPS (`) 0.7 1.9 4.1 5.2 4.8 5.6

Adj. EPS (`) 0.6 2.5 4.2 5.2 4.8 5.6

% chg 872.9 306.6 65.6 25.3 (8.5) 17.0

TVS Motor Company | 2QFY2013 Result Update

November 1, 2012

9

Balance sheet statement (Standalone)

Y/E March (` cr) FY2009 FY2010 FY2011 FY2012 FY2013E FY2014E

SOURCES OF FUNDS

Equity share capital 24 24 48 48 48 48

Reserves & surplus 786 842 952 1,122 1,282 1,477

Shareholders’ Funds 810 865 999 1,169 1,330 1,524

Total loans 906 1,003 633 715 740 710

Deferred tax liability 148 115 96 98 98 98

Other long term liabilities - - - - - -

Long term provisions - - 43 49 49 49

Total Liabilities 1,864 1,983 1,771 2,031 2,216 2,381

APPLICATION OF FUNDS Gross block 1,865 1,909 1,972 2,154 2,324 2,495

Less: Acc. depreciation 869 953 1,035 1,129 1,257 1,394

Net Block 996 956 938 1,026 1,068 1,101

Capital work-in-progress 40 27 57 53 58 62

Goodwill - - - - - -

Investments 478 739 661 931 931 931

Long term loans and advances - - 96 53 53 53

Other noncurrent assets - - - - - -

Current assets 894 965 1,106 1,078 1,234 1,510

Cash 42 101 6 13 63 159

Loans & advances 350 354 301 247 299 332

Other 502 511 799 819 872 1,019

Current liabilities 619 734 1,086 1,110 1,127 1,277

Net current assets 275 231 19 (31) 107 233

Misc. exp. not written off 75 30 - - - -

Total Assets 1,864 1,983 1,771 2,031 2,216 2,381

TVS Motor Company | 2QFY2013 Result Update

November 1, 2012

10

Cash flow statement (Standalone)

Y/E March (` cr) FY2009 FY2010 FY2011 FY2012 FY2013E FY2014E

Profit before tax 31 76 248 316 296 355

Depreciation 103 103 107 118 128 137

Change in working capital (29) 103 (67) 63 (83) (31)

Others 66 112 35 33 - -

Other income (12) (67) (36) (22) (25) (27)

Direct taxes paid (0) 12 (54) (67) (68) (89)

Cash Flow from Operations 160 339 234 441 247 346

(Inc.)/Dec. in fixed assets (88) (30) (93) (177) (175) (175)

(Inc.)/Dec. in investments (139) (262) 78 (270) - -

Other income 12 67 36 22 25 27

Cash Flow from Investing (215) (225) 20 (425) (150) (148)

Issue of equity - - 24 - - -

Inc./(Dec.) in loans 240 97 (295) (72) 25 (30)

Dividend paid (Incl. Tax) 19 33 60 72 72 72

Others (226) (102) (218) (150) - -

Cash Flow from Financing 33 28 (428) (150) (47) (102)

Inc./(Dec.) in cash (22) 142 (174) (135) 50 96

Opening Cash balances 4 42 101 6 13 63

Net cash credit adjustment (60) 83 (79) (142) - -

Closing Cash balances 42 101 6 13 63 159

TVS Motor Company | 2QFY2013 Result Update

November 1, 2012

11

Key ratios

Y/E March FY2009 FY2010 FY2011 FY2012 FY2013E FY2014E

Valuation Ratio (x) P/E (on FDEPS) 62.3 15.3 9.2 7.4 8.1 6.9

P/CEPS 13.7 8.3 6.0 5.0 5.2 4.6

P/BV 2.3 2.1 1.8 1.6 1.4 1.2

Dividend yield (%) 0.9 1.6 2.8 3.4 3.4 3.4

EV/Sales 0.6 0.5 0.3 0.2 0.2 0.2

EV/EBITDA 18.7 16.6 4.6 3.4 3.4 2.8

EV / Total Assets 1.2 1.0 1.0 0.8 0.7 0.6

Per Share Data (`) EPS (Basic) 0.7 1.9 4.1 5.2 4.8 5.6

EPS (fully diluted) 0.6 2.5 4.2 5.2 4.8 5.6

Cash EPS 2.8 4.7 6.4 7.7 7.5 8.5

DPS 0.4 0.6 1.1 1.3 1.3 1.3

Book Value 17.1 18.2 21.0 24.6 28.0 32.1

DuPont Analysis EBIT margin 2.3 1.9 4.5 4.9 4.4 4.7

Tax retention ratio 1.0 1.1 0.8 0.8 0.8 0.8

Asset turnover (x) 2.2 2.4 3.4 3.8 3.6 3.8

ROIC (Post-tax) 4.9 5.2 12.3 14.6 12.2 13.3

Cost of Debt (Post Tax) 8.2 8.8 7.0 6.7 6.4 6.2

Leverage (x) 0.4 0.3 0.1 (0.1) (0.2) (0.2)

Operating ROE 3.5 4.0 12.7 13.7 11.1 11.7

Returns (%) ROCE (Pre-tax) 4.8 4.4 15.2 18.5 15.6 16.9

Angel ROIC (Pre-tax) 0.9 0.9 16.1 17.4 15.4 17.5

ROE 3.6 14.3 21.3 22.9 18.2 18.7

Turnover ratios (x) Asset Turnover (Gross Block) 2.0 2.3 3.2 3.5 3.3 3.4

Inventory / Sales (days) 36 26 24 28 30 32

Receivables (days) 13 17 14 13 13 13

Payables (days) 53 51 49 53 53 52

WC cycle (ex-cash) (days) 21 15 4 (1) (0) 3

Solvency ratios (x) Net debt to equity 0.5 0.2 (0.0) (0.2) (0.2) (0.2)

Net debt to EBITDA 2.1 0.9 (0.1) (0.5) (0.6) (0.7)

Interest Coverage (EBIT / Int.) 1.3 1.1 3.9 6.2 5.5 6.4

TVS Motor Company | 2QFY2013 Result Update

November 1, 2012

12

Research Team Tel: 022 - 39357800 E-mail: [email protected] Website: www.angelbroking.com DISCLAIMER This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so. This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement TVS Motor Company

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Ratings (Returns): Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%) Reduce (-5% to 15%) Sell (< -15%)

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors