Embed Size (px)

Citation preview

TSR AND THE FRAYING LINK BETWEEN PAY AND PERFORMANCE

TSR and the Fraying Link Between Pay and Performance

Page 1

June 2014 Proxy Mosaic White Paper

Recent headlines have thrust execu1ve compensa1on back into the spotlight for all the wrong reasons. An over-‐reliance on total shareholder return – by both proxy advisors and corpora1ons – has contributed to outsized compensa1on packages that have repeatedly grabbed headlines. But with a be2er understanding of how performance metrics can mo0vate execu0ves, shouldn’t directors be able to create a compensa,on plan that helps deliver bo#om-‐line results and unlocks value for shareholders?

TSR and the Fraying Link Between Pay and Performance

Page 2

One | Introduc)on

As the 2014 proxy season winds to a close, the topic of execu:ve compensa:on is once again in the public eye. Despite the nearly four years since Dodd-‐Frank was signed into law, corporate say-‐on-‐pay is s'll a source of controversy as investors and the media have ques0oned whether certain corpora0ons are truly paying their execu/ves for performance, or simply paying their execu4ves. At the center of this ongoing controversy is Yahoo’s chief execu5ve Marissa Mayer, who, by the end of last year, had received compensa1on poten1ally worth $214 million for less than two years of work, according to the New York Times.1 Large payouts to CEO’s are not uncommon. In 2013, Charif Souki of Cheniere Energy received a compensa1on package worth $142 million, bea,ng out the perennially well-‐paid Larry Ellison of Oracle ($78.4 million) and asset management 9tans Mario Gabelli of Gamco Investors ($85 million) and James Levin of Och-‐Ziff Capital Management ($119 million). But whereas Mr. Souki’s compensa$on was earned by dras(cally re-‐shaping his company to become the first mover in expor+ng American natural gas, Ms. Mayer’s pay-‐day is the result of winning the execu1ve compensa1on lo6ery.

Yahoo acquired a stake in Chinese internet giant Alibaba in 2005, and the company’s valua7on has soared from $2.5 billion to a poten2al $130 billion. As Alibaba’s impending IPO reaches a fever pitch, Yahoo’s stock price has skyrocketed. Alibaba is one of the few remaining bright spots for the struggling internet company. 2013 was a dismal year for Yahoo, with revenue down to $4.68 from $4.98 billion in 2012 and nagging concerns about the company’s future. But Alibaba’s IPO could net Yahoo a cool $36 billion, and would give Ms. Mayer a huge personal windfall (via stock and op.ons that were granted to lure her to the company in 2012) despite Yahoo’s poor financial results.

This is probably the most dras%c example of how pay can be disconnected from performance, but it illustrates one of the fundamental problems with relying on shareholder returns to determine execu4ve compensa)on. Simply put: shareholder return is the result of good management performance, not the performance itself.2

We conducted a study on a random sample of 96 U.S. companies that filed their proxy statements in March 2014 and found that, despite an increased focus on TSR and other metrics, the gap between pay and performance is as wide as ever. We found numerous instances where execu5ve compensa5on actually increased despite the fact that shareholder returns were nega/ve. And we found no correla,on between changes in execu,ve compensa,on and return on invested capital, net income, or revenues.

Based upon our research, we believe that TSR is best u-lized as one element of an execu-ve compensa*on plan, supplemen+ng (or be1er yet, modifying) other performance metrics that more closely track bo1om-‐line results and are more easily influenced by execu3ve behavior. But before we focus on how to do that, it is important to take a step back and examine the current execu0ve compensa0on landscape and note how reliant the corporate governance community has become on TSR.

Two | Surveying the Execu0ve Compensa0on Landscape 1 Davidoff, Steven. “Yahoo Chief’s Pay Tied to Another Company’s Performance.” New York Times DealBook. The New York Times. 29 Apr. 2014. Web. 13 May 2014. <h8p://[email protected]/2014/04/29/yahoo-‐chiefs-‐pay-‐!ed-‐to-‐another-‐companys-‐performance/>. 2 McConnell, Paul and Dave McDaniel. “Are Rela6ve TSR Plans “The Answer”?”. Boardmember.com. NYSE Governance Services, n.d. Web. 13 May 2014. <h"ps://www.boardmember.com/Ar2cle_Details.aspx?id=9143>.

TSR and the Fraying Link Between Pay and Performance

Page 3

Since § 162(m) of the Internal Revenue Code was passed into law in 1993, pay-‐for-‐performance has become the norm among corporate execu/ve compensa/on plans. § 162(m) caps corporate tax deduc4ons for covered employees at $1 million annually. However, certain shareholder-‐approved compensa-on is not counted toward the $1 million limit so long as it is “performance-‐based.” This change in the tax code has had far-‐reaching consequences in corporate governance. As companies turned en masse to a pay-‐for-‐performance model, total shareholder return has quickly become one of the favored financial metrics.

Nearly half of the 96 companies that we studied used TSR as a performance metric in their long-‐term incen%ve plans. Interes%ngly, TSR appears to be becoming more popular. Between 2009 and 2013, the number of companies in our study that used TSR increased from 28 to 39. This stands in contrast to the trend in Europe, where there has been a decline in the use of TSR as a performance metric, and a “more rigorous calibra,on of those TSR plans that remain.”3

Aside from the tax benefit for pay-‐for-‐performance plans generally, TSR-‐based execu"ve compensa"on plans are o*en favored for several reasons. First, TSR is “viewed as objec;ve, transparent and easy to communicate to par-cipants.”4 Second, se*ng internal goals based on metrics such as revenue or cash flow can be difficult; a TSR-‐based metric requires li/le long-‐term planning.5 There is also the concern that revealing internal performance targets can put companies at a compe22ve disadvantage. Finally, and perhaps most importantly, TSR is used extensively by shareholder advisory firms like Ins,tu,onal Shareholder Services (ISS) and Glass Lewis in their determina7on of say-‐on-‐pay vo'ng recommenda'ons.

ISS compares one, three, and five-‐year TSR with execu0ve pay to assess the degree of alignment between compensa)on and performance. Companies receive a ra/ng of “Pass,” “Medium Concern,” or “High Concern” on each test, which can then trigger a more detailed qualita6ve analysis.6 One “High Concern” ra#ng or two “Medium Concerns” will lead to such a review. Because of its use by ISS as a “screen” in its execu%ve compensa%on analysis, some companies believe that using rela%ve TSR as a performance metric can improve the vote results on their say-‐on-‐pay proposals, which has contributed to its rise as one of the

3 Patel, Hemant, and Katherine Edwards. “Execu4ve Compensa4on Bulle4n: A More ThoughAul Approach to Using Rela4ve TSR in Performance Plans | Towers Watson.” Execu&ve Pay Ma-ers. Towers Watson, n.d. Web. 13 May 2014. <h"p://www.towerswatson.com/en-‐US/Insights/Newsle#ers/Global/execu.ve-‐pay-‐ma#ers/2012/Execu/ve-‐Compensa)on-‐Bulle%n-‐A-‐More-‐Though&ul-‐Approach-‐to-‐Using-‐Rela%ve-‐TSR>. 4 Id. 5 Adamson, Terry, Guanying Liu, and Francis Sonne. “Key Design Considera;ons When Adop;ng a Rela;ve TSR Plan.” Radford Review. Radford, n.d. Web. 13 May 2014. <h"p://www.directorsforum.com/academy/pdfs/Radford%20-‐%20Key%20Design%20Elements%20When%20Adop6ng%20a%20Rela6ve%20TSR%20Plan.pdf>. 6 Cwirko-‐Godycki, Alexander. “Unlocking ISS’ Quan:ta:ve Approach for Assessing the Alignment of CEO Pay and Performance.” Radford Alert. Radford, n.d. Web. 13 May 2014. <h"ps://www.radford.com/home/press_room/pdf/Radford_alert_unlocking_ISS_ceo_pay_022012.pdf>.

Between 2009 and 2013, the number of companies in our study that used TSR increased from 28 to 39, sugges8ng that the use of TSR as a performance metric is becoming more and more prevalent.

TSR and the Fraying Link Between Pay and Performance

Page 4

predominant metrics.7 However, such an over-‐reliance on TSR as a performance metric, by both corpora&ons and proxy advisory firms, creates significant problems.

Three | Problems with TSR

There are numerous problems with relying too heavily on TSR as a performance metric. First, the nature of TSR is that it is a point-‐to-‐point metric, which makes it heavily dependent on the company’s choice of performance period. Companies with a low share price have a poten2al advantage over those going into the performance period with strong performance.8 Start and end dates ma+er, and can be the difference between nega)ve TSR and a banner year.

Second, the effects of TSR can “crowd out” other financial metrics. As men<oned above, Yahoo’s current share price is masking serious deficiencies with respect to revenues. But CEO Marissa Mayer will be rewarded handsomely because of Yahoo’s stock apprecia-on, and the effects that declining revenues would have on her annual and long-‐term compensa,on will be mi,gated by the ar,ficially high shareholder returns.

Third, and most importantly, TSR provides a poor “line of sight” to execu6ves. Execu&ves might know what it takes to raise income by 10%, but it is less clear what it takes to raise the company’s stock by 10%.9 Execu&ves, par)cularly those lower down the ranks, are not always able to influence the company’s stock price due to general market vola5lity and other exogenous factors.10 As a result, TSR can be seen as more of a lo-ery than a significant mo4vator.

This is par'cularly true at larger companies, where their sheer size makes it more difficult to effect change. Our research found that large companies (i.e. those with revenues of over $30 billion annually) that relied on TSR as a performance metric performed worse over five years than those that did not.

7 Patel and Edwards. 8 Harris, Richard. “Rela0ve Total Shareholder Return: Myths and Reali.es.” Execu&ve Compensa&on. Aon Hewi*, n.d. Web. 13 May 2014. <h"p://www.aon.com/human-‐capital-‐consul'ng/thought-‐leadership/compensa/on/market-‐trends/MarketTrends_07-‐30-‐12_Rela(ve_Total_Shareholder_Return_Detail.pdf>. 9 McConnell and McDaniel. 10 Hansell, Gerry, Lars-‐Uwe Luther, Frank Plaschke, and Mathias Scha7. “Fixing What’s Wrong with Execu@ve Compensa)on.” BCG Perspec+ves. The Boston Consul.ng Group, n.d. Web. 13 May 2014. <h"ps://www.bcgperspec.ves.com/content/ar.cles/people_management_human_resources_corporate_development_fixing_whats_wrong_execu0ve_compensa0on/>.

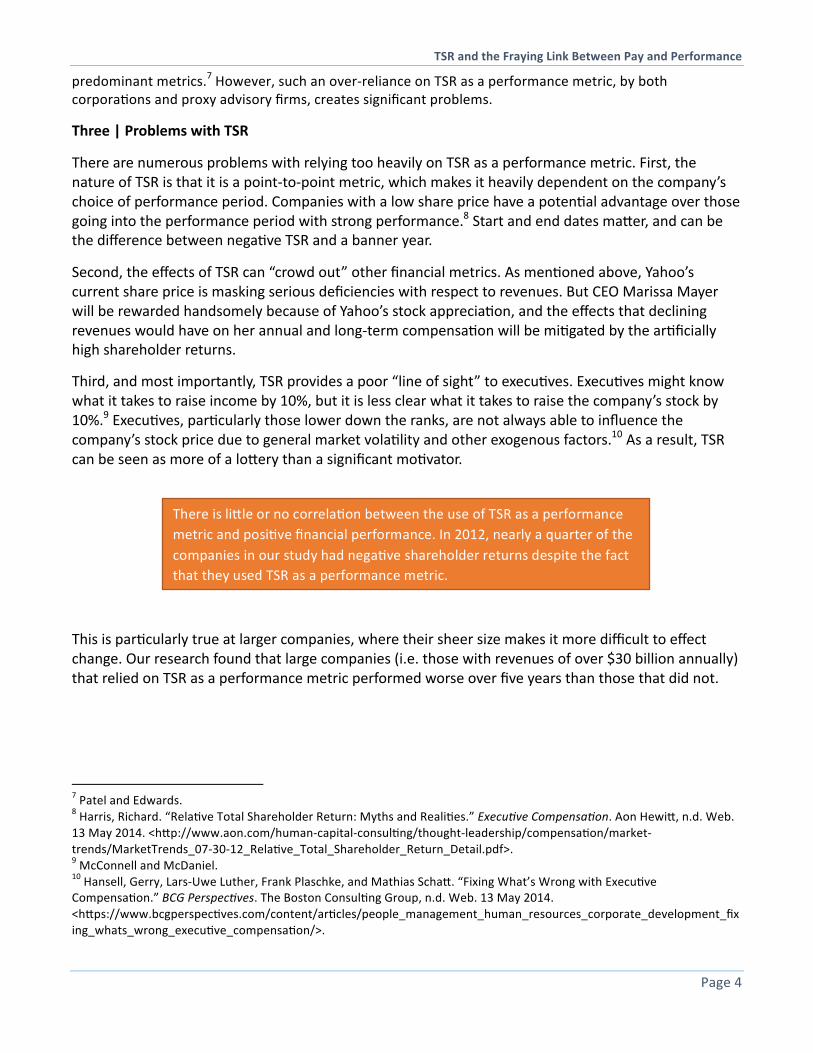

There is li)le or no correla.on between the use of TSR as a performance metric and posi.ve financial performance. In 2012, nearly a quarter of the companies in our study had nega2ve shareholder returns despite the fact that they used TSR as a performance metric.

TSR and the Fraying Link Between Pay and Performance

Page 5

This supports the idea that large companies can be unwieldy, so it is be7er to focus management on things it can control,11 such as opera+ng margins or cash flow.

The downsides of relying on TSR are apparent regardless of whether TSR is measured on a rela5ve or absolute basis. Absolute TSR can be difficult to forecast without a crystal ball, and can be drama:cally affected by markets as a whole and other factors beyond the control of the company and its execu#ves.

Rela%ve TSR is o-en seen as an appropriate response to the deficiencies of absolute TSR, because it “rewards execu,ves when the company outperforms its peers, not just when it enjoys a windfall in the stock market,”12 but it too has its problems. Rela(ve TSR is heavily dependent on peer group selec.on and peer group selec.on is arguably the most difficult aspect of a rela.ve TSR-‐based plan design.13 Choose a peer group that is too small (i.e. an industry-‐specific peer group) and the performance of one or two companies can drama/cally alter payouts; choose a group that is too large (i.e. a broad-‐based index like the S&P 500) and the comparison is no longer apples to apples but apples to oranges, pears, and bananas.

Further complica/ng the ma2er is the fact that, when TSR is used as a performance metric for grants of stock or op)ons, stock price has a double impact on the total compensa.on amount. If TSR is used to determine how many op/ons are given, for instance, those op/ons are also worth more or less based on the company’s share price during the relevant period – the larger element of TSR. In other words, TSR-‐based performance metrics “doubly incen4vize” management to focus on stock price – something over which they have li.le control – rather than opera*onal metrics such as revenue or net margins.

The problems inherent in using TSR as a performance metric were apparent in our data. Companies o"en view TSR as something that can support shareholder alignment, but the reality is somewhat different. Our data showed no posi%ve correla'on between the use of TSR as a performance metric and actual shareholder returns; nor did the use of TSR correspond to improved financial performance in other areas, such as revenue or net income growth. In fact, companies that used TSR as a performance metric actually performed about 30% worse over a five-‐year period than companies that did not. We even found a moderate nega%ve correla'on between the use of TSR and return on invested capital, which suggests that TSR use might have an adverse effect on other measures of performance.

Four | Moving Beyond TSR: Poten2al Solu2ons

While the problems with relying too heavily on TSR are apparent, that doesn’t mean that it has no value in forming execu0ve compensa'on plans. When properly calibrated, TSR can provide an important part of a well-‐balanced execu+ve compensa+on plan. The following is a list of just some of the uses for TSR:

§ Modifier of Primary Target: TSR can be used to modify other financial performance metrics, either as an “on/off switch” or as a “cap.”14 With an on/off switch, TSR can either “turn on”

11 Morgensen, Gretchen. “Pay for Performance? It Depends on the Measuring S=ck.” The New York Times. The New York Times, 12 Apr. 2014. Web. 14 May 2014. <h"p://www.ny(mes.com/2014/04/13/business/pay-‐for-‐performance-‐it-‐depends-‐on-‐the-‐measuring-‐s"ck.html>. 12 Hansell, Luther, Plaschke, and Scha3. 13 Adamson, Liu, and Sonne. 14 Id.

TSR and the Fraying Link Between Pay and Performance

Page 6

compensa)on if a certain target is achieved, or compensa)on can be forfeited (or “turned off”) if results fall below expecta4ons. If TSR is used as a cap, then compensa.on can be set at a maximum of, for example, 100% of target if TSR is nega8ve, even if other financial performance goals are exceeded. This would help ensure that execu3ves would not receive large rewards while shareholders are concurrently losing value.

§ In Conjunc)on with “Malus Awards”: Malus awards are also known as “nega0ve bonuses,”15 which reduce an execu-ve’s already-‐granted equity or accumulated bonus (held in an escrow account) if certain targets – in this case, a set rela-ve TSR percen-le or absolute TSR value – are not met. Malus awards can also help address the issue that execu%ves are “immunized from the risk of poor performance”16 by tradi)onal compensa)on structures.

§ In Cyclical/Vola,le Industries: Certain industries are naturally going to be affected by market condi-ons. The financial performance of a gold mining company, for example, will be highly dependent on the market price for gold at a given 5me. The company might have a dismal year, despite the best efforts of its execu6ves, simply because the price of gold has declined. In these cases, rela0ve TSR may be an appropriate subs0tute for other financial metrics,17 as it can give a rough approxima2on of whether a company outperforms its industry peers in ,mes of macroeconomic pressure.

§ During Corporate Restructuring/Turnaround: While a corpora,on is undergoing strategic or financial reorganiza-on, the uncertainty involved makes se3ng performance targets difficult.18 And, financial performance may be mixed at best, despite the fact that the company’s long-‐term health is improving. In this case, TSR can be used to gauge whether or not the market is op.mis.c about the company’s changes and how it feels about management’s leadership performance.

§ Absolute/Rela,ve TSR Hybrid: If a company is intent on using TSR as a performance metric, a slightly more effec0ve way of doing so would be to create a plan that uses both absolute and rela%ve TSR. For example, equity awards might vest only if the company’s absolute TSR is posi&ve and outperforms its peer group median.

As an alterna*ve to TSR, some financial metrics can provide a be8er picture of a company’s overall financial health while providing a clear line of sight to its execu5ves. Farient Advisors conducted a study, comparing data from 1,800 companies from 1998-‐2011 to examine which metrics were most strongly linked with

15 Hansell, Luther, Plaschke, and Scha3. 16 Zhou, Xianming, and Peter L. Swan. “Performance Thresholds in Managerial Incen;ve Contracts.” The Journal of Business 76.4 (2003): 665-‐696. Print. 17 Harris. 18 McConnell and McDaniel.

Despite its shortcomings, TSR can s4ll play an important role in an execu%ve compensa%on plan, as a modifier of a primary target, in conjunc&on with “malus” awards, in cyclical or vola&le industries, or as part of an absolute/rela.ve TSR hybrid.

TSR and the Fraying Link Between Pay and Performance

Page 7

shareholder returns.19 While TSR is shareholders’ ul#mate goal, it is an “output” rather than an “input”; these metrics, on the other hand, can be seen as the engines that drive shareholder returns. The following is a breakdown of some of the most strongly-‐correlated metrics, ranked in order from highest to lowest correla'on:

§ Earnings Growth: EPS, Net Income, Opera2ng Income, EBITDA § Revenue: Revenue Growth, Sales Contracts, Same Store Sales § Returns: ROIC, ROE, ROA

It is important to note here that our data showed that there is no correla3on between the number of performance metrics and a company’s actual shareholder returns. Cra6ing an op8mal execu8ve compensa)on plan is not simply a ma/er of including all of the aforemen+oned metrics that are correlated with performance. Execu3ve compensa3on is one instance where too many cooks can in fact spoil the broth, so it is important to select only those financial metrics that are appropriate given the goals of the par$cular company. Nor does constantly chopping and changing the execu4ve compensa4on plan help. While it is important to periodically recalibrate a plan, our data showed that companies whose long-‐term incen%ve plans remained constant performed about 40% be7er than those that changed their plans repeatedly. Consistency is important, and companies should resist the tempta/on to “move the goalposts” and change their plans too frequently, even in challenging macroeconomic condi7ons. Performance metrics help determine execu/ve behavior, so making frequent changes to the plans can send mixed signals and cause management to lose focus. The key to any good execu0ve compensa0on plan is finding the right balance between providing a line of sight for management and aligning shareholder interests.

Five | Conclusions

Choosing performance metrics that are strategically important to shareholder value is a cri6cal aspect of designing an execu,ve compensa,on plan that truly links pay with performance. Unfortunately, while using TSR as a performance metric has become common prac/ce in the design of execu/ve pay packages, it does not necessarily create strong shareholder alignment. Our data suggests that the use of TSR as a performance metric does not correlate to improved shareholder returns. The problems with an over-‐reliance on TSR are numerous, but essen3ally boil down to the fact that it provides a poor “line of sight” for management. As noted earlier, execu%ves don’t necessarily know what it takes to raise a company’s stock by 10%, and even if they do know, the markets might not agree with them.

Rela%ve TSR is o-en seen as a reasonable alterna%ve to absolute TSR-‐based plans, which are subject to the mercies of the market. But rela)ve TSR too has its problems. With rela)ve TSR-‐based plans, execu%ves can receive huge pay-‐days even as the company’s shareholders suffer. This inequity is compounded by the difficul1es inherent in choosing an adequate peer group.

However, despite its shortcomings, TSR s6ll has significant value as a poten6al performance metric. It can be a very effec+ve modifier, amplifying, diminishing, limi+ng, or triggering awards if certain performance criteria are met. TSR can also be effec&ve if paired with at least one (and preferably two or more) other metrics. Metrics that measure things like earnings per share and revenue growth are

19 Ferracone, Robin, and Jack Zwingli. “Performance Metrics and Their Link to Value.” www.farient.com. Farient Advisors, n.d. Web. 13 May 2014. <h"p://www.farient.com/wp-‐content/uploads/2012/11/20140130-‐Farient-‐Study-‐on-‐Performance-‐Metrics.pdf>.

TSR and the Fraying Link Between Pay and Performance

Page 8

generally strongly-‐correlated with shareholder returns, but corporate boards should undertake their own analysis to determine which metrics drive value for their company and include the most relevant.

No ma&er which combina/on of metrics they choose, corpora/ons should communicate with investors and be able to make a compelling case that their metrics enhance shareholder value. There is no one-‐size fits all approach to execu1ve compensa1on, and each company can and should have a compensa)on plan that is tailored to meet its business needs and the needs of its investors. Ul)mately, designing an execu,ve compensa,on plan is about striking a balance between pay and performance. TSR can be one way of achieving that balance, but it is by no means a panacea, and the recent shi; away from its use as a performance metric in Europe suggests that some companies are beginning to take no#ce of the fact that a well-‐cra$ed plan can not only benefit the company as a whole but unlock shareholder value.