Embed Size (px)

Citation preview

‘Troubled Assets’: The FinancialEmergency and Racialized Risk

PHILIP ASHTON

Abstractijur_1077 1..18

This article examines the repositioning of racialized credit risk produced by newregulatory practices that have emerged in the neoliberal era. As increasingly volatilefinancial markets have periodically threatened the ability of the banking sector to supplycredit, US regulators have adopted more aggressive roles to isolate ‘troubled assets’andrestore the norms of risk management. Revisiting the emergence of the US subprimemortgage market in the early 1990s, I use this framework to assess a critical questionfor urban political economy: how could decades of racial exclusion from US creditmarkets have been transformed so quickly and decisively into the exploitation of minorityborrowers within the subprime market? The article identifies a series of regulatorypractices associated with the management of the late-1980s banking crisis, arguing theirdistinctive orientation towards the circulation of risk created a new legal and marketspace for high-risk loans. I then examine the migration of those emergency risk practicesinto the institutional venues that shaped the subprime market and that differentiallyexposed minority borrowers to heightened rent-seeking. The results suggest new avenuesfor urban political economy emerging from a broader conceptualization of staterelationships to financial risk.

IntroductionCredit risk has been distinctly racialized in the US since its assessment emerged as a‘science’ in the early twentieth century. As the post-Abolition institutions confiningAfrican Americans to the rural South began to break down after the first world war,pioneering housing analysts working in the wake of the Great Depression identifiedracial transition as a key threat to property values and promoted neighborhoodcategorization — redlining — as a ‘triage’ technique to limit the exposure of banks andthe federal mortgage insurance pool to the risks of devaluation (Stuart, 2003; Hernandez,2009). This placed race at the center of a series of rules for housing finance that, whileostensibly designed to ensure the safety and soundness of the banking system by limitingexcessive risk-taking, had the effect of reorganizing the conditions for social andeconomic advancement among different racial and ethnic groups.

As regulations governing the US banking sector advanced in tandem with increasingdisinvestment and decline in minority neighborhoods through the postwar period, overtracial treatment or ‘triage’ was transformed into a series of subtler, but no less powerful,financial proxies for race. For instance, fewer loans made in African-Americanneighborhoods meant diminishing resources for property upkeep and lower demandfor homeownership, further contributing to declining property values and making

This research was supported by the Faculty Scholar program at the Great Cities Institute at Universityof Illinois–Chicago. I am grateful to Bob Lake, Elvin Wyly, Ralph Cintron, Glenda Garelli and three IJURRreviewers for their feedback on earlier versions of this work.

International Journal of Urban and Regional ResearchDOI:10.1111/j.1468-2427.2011.01077.x

© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd. Published by Blackwell Publishing. 9600 Garsington Road, Oxford OX4 2DQ, UK and 350 Main St,Malden, MA 02148, USA

neighborhood ‘risk’ self-perpetuating. As a result, the federal and state regulatoryagencies overseeing the postwar banking system could enforce rules governing thetreatment of risk — such as the use of household financial ratios, credit history orproperty appraisal as risk assessment techniques — that produced credit scarcity inminority neighborhoods without necessarily making any direct reference to race (Stuart,2003). The regulatory and market apparatuses of risk management thus became critical‘institutional encasements’ crowding African Americans into the ghetto (to be followedby Puerto Ricans, Dominicans and subsequently Mexicans) and defining that space asone of economic and social dispossession (Wacquant, 2002: 50).

The study of these processes was among the foundations of urban political economy,with early analyses developing a significant vocabulary to conceptualize the role ofthe state and financial regulation in producing particular forms of social and spatialhierarchy through mortgage markets (Harvey, 1974; Harvey and Chatterjee, 1974;Bradford, 1979). However, this vocabulary has had to evolve through different phases inthe development of financial markets, marked since the early 1970s by increasinglyvolatile international financial flows and the emergence of ‘stateless money’ (Martin,1994). This evolution can be seen in several strands of empirical and theoretical workthat have emerged since the mid-1990s; one important strand has sought to map the newspaces of racial and class dispossession — such as those found in the crowding ofminority borrowers into the high-cost or subprime mortgage market, or in the devastatingforeclosure crisis that has hit minority neighborhoods — that have emerged from greaterintegration of housing and consumer finance with broader equity and capital markets(Wyly et al., 2006; 2009; Ashton, 2008; Newman, 2009).1

Underlying these analyses is the central question of how racial exclusion withincredit markets could have been so quickly and decisively transformed. Urban politicaleconomy has drawn on numerous arguments to conceptualize that transformation,ranging from the strategic restructuring of banking and financial intermediation (Ashton,2009; Dymski, 2009b) to fundamental shifts in the orientation and practices of financialregulation (Immergluck, 2009a). The rush to locate the state at the center of the ‘urbanproblematic’ (Dymski, 2009c) has been particularly important in the wake of the post-2007 financial crisis, as critical perspectives have sought to tie a highly racializedmortgage and foreclosure crisis to the retreat of the state from financial regulation(Immergluck, 2009a; Newman, 2009) or the neoliberal roll-out of new macro-structuresof risk-taking (Gotham, 2006; 2009; Ashton, 2008).

This sets the context for this article, which takes as its starting point the need to extendthese characterizations of the state to better understand its contemporary role in structuringracial exclusion in US mortgage markets. Here, my concern is less with the concrete socialor spatial patterns of racial exploitation that have emerged over the last 20 years; rather,I focus centrally on the role of regulatory practices in repositioning particular formsof risk — namely credit or default risk, and its association with racialized histories ofexclusion — within the financial system. I develop this analysis in two main parts.

First, I argue that the repositioning of credit risk is part of a broader restructuringof state relationships to financial risk that has emerged since the 1970s in response tothe decisional uncertainties of unstable international financial flows. This restructuringhas produced new regulatory capacities and practices oriented towards anticipating ormanaging periodic financial crises, clearly visible in the financial state of emergency andthe nearly unprecedented interventions into financial markets that have unfolded in theUS and elsewhere since 2007.

Second, I engage this framework by focusing on a signal moment: the inception andrapid expansion of the subprime mortgage market in the period after 1990. I examine thepractices of emergency interventions in the wake of the banking crisis of the late 1980s,arguing that they involved a distinctive orientation towards the circulation of financial

1 The subprime mortgage market refers broadly to a set of institutions that ‘concentrate on offeringterms and seeking borrowers generally not acceptable to prime lenders’ (Canner et al., 1999: 709).

2 Philip Ashton

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

risk — the financial exception (cf. Atia, 2007) — that aimed to triage insolvent institutionsand non-performing (‘troubled’) assets to prevent contagion. In contrast to recent work onthe re-regulation of mortgage markets, which has produced only generalized connectionsbetween state regulatory interventions and the subprime market, the central argument ofthis article is that these regulatory practices reconfigured market structures around certaintypes of credit risks, and played an active role in creating the legal and market spacesfor high-risk loans. I further examine the migration of emergency risk standards throughthe mid-1990s to the institutional venues and market segments that defined the crowdingof minority borrowers into the subprime mortgage market.

Whereas this analysis is limited to the ‘materialization’ of the subprime mortgagemarket (Langley, 2008) and does not pretend to account for the forms of hyper-competition and over-extension that characterized the market through the mid-2000s,it nevertheless situates the financial state of emergency as the latest form of financialregulation to reorganize the conditions for advancement among different racial and ethnicgroups. This framework suggests new possibilities to assess the ‘urban problematic’(Dymski, 2009c) in the wake of the present crisis, a topic that I take up in the conclusion.

Financial risk and the stateThe global financial crisis that has unfolded since mid-2007 provides an opportunity toengage with the central concepts underpinning its production and diffusion — inparticular, the nature of risk. Conventional interpretations of financial risk, as locatedwithin individual interactions between lenders and borrowers (including default or creditrisk) have tended to treat risk both as an object and a ‘primitive’: a characteristic whosesources are external to the financial system, to be assessed and priced by financial firms andmarkets (Dymski, 1998). Various accounts of the crisis have challenged this interpretation,focusing on the primary question of how shifting practices of risk-taking could have beenextended to the point of producing a global financial crisis. These accounts include: newnorms of risk assessment, based in probabilistic models of profit and loss that created thebasis for contradictory relationships between creditors and debtors (Langley, 2008); thecommodification of default risk through technologies such as risk-based pricing andsecuritization (Wyly et al., 2006; Wainwright, 2009); and the development of marketstructures that allowed lenders and borrowers alike to extend the boundaries of risk-takingacross the global financial system (Aalbers, 2009a; Ashton, 2009; French et al., 2009).

For scholars of financialization, this conceptualization of risk provides a frameworkto assess the systemic power of high-risk capital and its role in reorganizing circuitsof investment and propelling global financial fragility. Nevertheless, such argumentsoften take the 2007 subprime crisis as their central referent, and focus their empiricalarguments on events after 2000 (Aalbers, 2008; 2009a; Konings, 2009; Schwartz, 2009).This focus, while valuable in its own right, obscures a more foundational question forurban political economists focused on US cities, one that is central to this article: how isit that decades of racial exclusion from credit markets, in which risk was mobilized as akey justificatory concept, could be transformed so quickly and decisively into a crowdingof minorities into the subprime mortgage market (Dymski, 2009b)? As this crowding wasconsolidated by 2000 (Bradford, 2002), I argue we need to examine more closely the‘materialization’ of the subprime market (Langley, 2008) in the early 1990s to fullyassess the reconfiguration of racialized risk.2

The urge to locate the state at the center of this materialization has been strongin urban political economy, with a brief survey of recent analyses highlighting twodominant frameworks. First, deregulation has been a central theme within this work,contrasting deep state involvement in organizing and structuring racialized risk under theNew Deal financial system (Stuart, 2003; Hernandez, 2009; Immergluck, 2009a) with the

2 For more focused arguments regarding this periodization of the subprime market into two phases,see Ashton (2009) and Immergluck (2009a).

Racialized credit risk in the United States 3

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

neoliberal reorganization of regulatory relationships (Panitch and Konings, 2009). Thisreorganization is often characterized as a rentier political project, drawing its ideologicalresources from neoliberalism and employing regulatory capture as a key strategy.Immergluck (2009a: 6) identifies ‘a deliberate and organized movement, aggressivelypromoted by the financial services sector and by some in Congress and federal regulatoryagencies to reduce public sector oversight of the financial services sector’ as criticalto what he calls the ‘high risk revolution’. Wyly et al. (2009: 337) and Aalbers (2009b)highlight the key role of ‘privatized public policy’ — ranging from regressive tax cutsto an emphasis on homeownership — as shaping decisive shifts in the orientation offinancial regulators to risk-taking within mortgage markets.

A second state-focused framework, which Aalbers (ibid.: 285) labels ‘re-regulation’,focuses on the active role of state interventions in establishing what Konings (2009: 111)similarly calls ‘a process of institutional construction and consolidation that hasinvolved not the destruction but precisely the creation of new social connections, culturalaffinities and political capacities’. Gotham’s (2009: 366) deep reading of the institutionaltransformation of US mortgage markets conceptualizes this as an ad hoc process wherein‘ “old” policies produce crises of liquidity that inevitably bring forth calls for “new”policies that, once implemented, create further contradictions and unforeseen crises’.Similar analyses share his focus on an ‘institutional fix’ of financial instability from the1980s onwards as producing a new framework for risk-taking emphasizing liberalizationwithin the banking system (Dymski, 1999; Ashton, 2008). Many of these accountsfocus on particular institutional parameters — such as consolidation, securitization,credit scoring and risk-based pricing — that were critical to the transformation of powerrelationships between creditors and debtors, arguing that they emerged directly orindirectly through state intervention (Aalbers, 2009b; Newman, 2009). These analyseshave assembled an impressive historical record of specific instances where stateintervention produced new frameworks for risk-taking within US mortgage markets.However, they suffer from two significant limitations that hamper their analyticalpurchase on integrative concepts such as risk.

First, much of the work in urban political economy has not overtly theorized thestate and its relationship to financial risk. In many cases, this is due to state strategiesbeing a secondary focus relative to the production of social and spatial hierarchiesthrough different moments of the circulation of financial capital (Wyly et al., 2006; 2009;Aalbers, 2008; Ashton, 2008; French et al., 2009).Alternatively, this derives from an overtorientation towards governmentality that eschews any connection to state strategy in itsconceptualization of risk (Langley, 2008). In these accounts, state actions function asbackground conditions, or they devolve to unspecified structural imperatives to explain thestate’s ‘aggressive role in ensuring the expansion of the new economy by increasingdemand for mortgage products’ (Newman, 2009: 317). Where the state is portrayed as aconscious agent in shaping power relationships between creditors and debtors — as inImmergluck’s (2004: 19) account of the ‘visible hand’ — reliance on concepts such as‘regulatory failure’ imply that, but for regulatory capture by neoliberal ideologues, stategovernance of financial risk might otherwise be cohesive and continuous. Suchframeworks may offer ways to track legislative politics since the 1980s, but they do notproblematize the broader relationship of the state to the circulation of financial capital inthe neoliberal era — which might require alternative accounts of state failure or capacity(cf. Jessop, 2007). Moreover, they offer little conceptual basis on which to theorize thetremendous forms of state restructuring underway since 2007, or any new power relationsbetween lenders and borrowers that may be emerging from those interventions.

Second, even the more explicitly state-centered accounts found in urban politicaleconomy tend to focus narrowly on formal actions within the housing finance sectorin their analyses of the transformation of risk relationships (cf. Seabrooke, 2006). Whilethis provides a lens into critical contradictions in the spatial economy of finance(Gotham, 2009), it has the effect of producing an empirical record that is often stylizedor incomplete. For instance, the common association of subprime lending with a set of

4 Philip Ashton

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

1980s deregulation measures focused on savings banks (Newman, 2009: 318) selectivelydisregards ‘the significant increases in supervisory regulation [that] occurred nearlysimultaneously with deregulation’ (FDIC, 1997: 88). It also produces a curious gap withearly trade accounts of the emergence of the mass subprime mortgage market, whichdate the ‘stampede to subprime’ as beginning around 1993 — a decade after deregulation(Wahl and Focardi, 1997). Re-regulatory accounts remedy this gap by focusing on keylegislative provisions between 1989 and 1992 that promoted securitization and creditscoring in the wake of the banking crisis of the late 1980s (Aalbers, 2009b; Gotham,2009: 361; Immergluck, 2009a; Newman, 2009). However, these provisions operatedwithin the mainstream secondary market — focused on the government-sponsoredenterprises Fannie Mae and Freddie Mac — which represented a distinct institutionalframework from that found within the subprime mortgage market from its inception(Ashton, 2009; Immergluck, 2009a).3 Other critical interventions identified — such asshifts in bank regulation from the late 1990s onwards (Gotham, 2009: 364; Immergluck,2009b) — occur only after the ‘the transformation of racial exclusion in US mortgagemarkets’ (Dymski, 2009b: 149) was essentially complete (Bradford, 2002).

In the absence of some set of state regulatory practices shaping the development ofthese alternative mortgage market channels into new forms of racial exclusion, we areoften left to infer that state interventions represent only points of ‘inflection’, with privatemarket actors working to rationalize these frameworks into new social and spatialstructures of risk-taking as part of a broader strategic transformation of banking(Dymski, 2009b). This may be a defensible analysis, but it emerges by implication inmost recent work and cannot be taken as settled until it is tested against competingconceptualizations.

In this article, I advance just such an alternative, which I summarize through twopropositions. First, deregulation and re-regulation accounts of the role of the state inUS mortgage markets find broader coherence in an approach that addresses moresystematically the strategic transformation of state relationships to financial risk as onecomponent of neoliberalization. In the remainder of this section, I draw together thewider international political economy literature on financial liberalization with policystudies within banking regulation to focus on the contingent construction of a spaceof regulatory maneuver after the breakdown of Bretton Woods (Newstadt, 2008).This review opens up a broader set of instrumentalities for consideration, highlightingregulatory strategies that have emerged since the 1970s — in particular, expandedlender-of-last-resort powers and the financial state of emergency — as new ‘institutionalmechanisms of control’ (Konings, 2009: 110) marked by their distinctive orientationtowards financial assets and institutions that constitute risks to the financial system.

Second, the primary contribution of this article is the proposition that focusing onthis distinctive orientation provides a novel lens into the role of state strategies inreconfiguring racialized risk. The next section fleshes out this argument by revisitinghistorical analyses of the emergence and consolidation of the subprime market in theearly 1990s. Here, closer attention to the practices of the financial state of emergency —practices that I refer to as the financial exception — highlights the often protractedstate-led processes of managing the circulation of system-threatening risk in the wake offinancial crises. In the case of the subprime mortgage market, this reassessment identifiesthe key role of US banking regulators in transforming non-performing loans at the centerof the banking crisis into a regularized market space open to a broader group of investors.It further identifies regulatory interventions that shaped the migration (or colonization) ofemergency risk practices into new institutional venues and new minority market spacesthrough the 1990s. Whereas some of these practices (such as mortgage scoring) can beidentified through a narrow focus on housing finance, others (such as Fed interest rate

3 Few studies address the high-yield bond market, which was critical to the expansion of the subprimemarket in the 1990s. Of the US $1.45 trillion in subprime loans issued between 1995 and 2003, only50% were securitized (Chomsisengphet and Pennington-Cross, 2006: 38).

Racialized credit risk in the United States 5

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

policy in the wake of the 1994–95 Mexican peso crisis) become legible only throughbroader attention to the strategic transformation of state relationships to financial risk.

Not only does this provide an alternative conceptual framework to address a centralquestion in urban political economy — the rapid transformation of racial exclusion inUS mortgage markets and the entrapment of minority borrowers within the subprimemortgage market — it also provides a forward-looking framework and a basis to buildout critical theories of risk as central to financialization. The final section concludes withthoughts on how such a framework could be turned to address new configurations ofracialized risk that may be emerging from the post-2007crisis.

Financial volatility and state strategy

The ability to protect the quality of money and ensure the integrity of credit transactionshave long been capacities at the center of any formal definition of state sovereignty(de Brunhoff, 1978; Arrighi, 1994). These capacities have not been immutable, but haveevolved through extraordinary moments — such as the financial crisis of 1907, which ledto the centralization of the money supply through the US Federal Reserve Act of 1913 —when significant threats to the circulation of money and credit elaborated a regulatoryapparatus focused on managing the production of risk (Kushmeider, 2005). In the wakeof the financial crisis of the 1930s, US policymakers developed a distinctive orientationthat anticipated financial risk within retail finance, deploying functional limits oncompetition, deposit insurance and regular assessment of bank solvency (prudentialregulation) to ensure an appropriate relationship between risk-taking and the productionof credit money (Isenberg, 2003). As indicated earlier, this regulatory frameworkpromoted racialized forms of risk assessment, both through appraisal of the quality ofcollateral in minority neighborhoods, as well as through the selective promotion of creditscarcity (Stuart, 2003). In the postwar period, anticipation of financial risk was expandedto include lender-of-last-resort authority that authorized open bank assistance throughdirect loans to, or even acquisition of, failing banks (FDIC, 1998). However, long periodsof macroeconomic stability meant there was little need for such authority, and open bankassistance was not employed until 1971 (ibid.). This placed forward-looking financialregulation among the distinctive capacities defining the sovereignty of the Keynesianwelfare state (Jessop, 2002).

The 1973 breakdown of Bretton Woods and the move to floating exchange ratesmarked a significant shift in the relationship of regulators and policymakers to financialrisk (Leyshon, 1992). While floating exchange rates seemed at first to enhance nation-state sovereignty by giving policymakers the autonomy to pursue policy directionswithout direct negotiation with trading partners, it also institutionalized and extended thegrowth in volatile international capital flows (Helleiner, 1994), producing decisionaluncertainties that ‘made financial governance less feasible and less effective than before’(Dymski, 2009a: 48). By the late 1970s, policymakers responded by engaging in a broadstrategic transformation of the state’s relationship to financial risk. Here, I draw togetherliteratures from international political economy, regulation theory and the mainstreampolicy literature on banking regulation to identify three dimensions to this strategictransformation.

First, the most visible transformation has involved the promotion of risk-taking by USfirms as part of a geo-economic strategy to secure and leverage US financial power(Duménil and Lévy, 2004). During the 1970s, US policymakers sought to reestablishstable international frameworks to manage volatile interdependencies among currencies(Helleiner, 1994). In the wake of the Volcker Shock of the early 1980s, however, theinstitutionalization of capacities to manage surging financial liquidity (within the FederalReserve and the Treasury Department) marked a shift to a larger state-led project toproduce asset inflation for US firms. This project was formalized through the 1988 Baselframework on financial leverage and risk-taking, but it was also evident in new regulatorypractices focused on reproducing the conditions for ongoing liquidity in US financial

6 Philip Ashton

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

markets (Newstadt, 2008; Sarai, 2008; Konings, 2009). Events as mundane as the monthlymeetings of the Federal Reserve Open Market Committee (Krippner, 2003), or as criticalas the Fed’s extension of liquidity backstops in the wake of the 1987 stock market crash orthe 1998 collapse of the hedge fund Long Term Capital Management (Newstadt, 2008;Rude, 2008), have marked the ongoing evolution of these capacities alongside the broaderconstruction of US competitive advantage around financial volatility.

More directly related to the dynamics of racial exclusion in credit markets were aseries of moves focused on the domestic banking system. A second critical area ofstrategic transformation involved giving banks the powers and resources necessary toadapt to a faster-paced financial world; this was accomplished through an overhaul ofbanking regulations from 1978 onwards (Ball, 1990; Olson, 2000). The collapse ofFranklin Federal Savings Bank in 1974, a result of significant bad bets in internationalcurrency hedges, had marked a critical breaking point with the postwar system ofbanking regulation (Helleiner, 1994: 171). A deteriorating domestic financial situationthrough the 1970s challenged regulators’ forward-looking orientation towards risk, ascurrency and interest rate volatility along with growing competition from non-bankfinancial firms eroded bank balance sheets, jeopardizing their ability to issue credit andproducing a growing insolvency crisis by the end of the decade. As Ball (1990: 100) hasargued, while proportionally these problems fell more heavily on the savings banks thatdominated housing finance at the time, commercial banks posed a greater threat to thesafety and soundness of the banking system both in absolute terms and in terms of theircritical role in the nation’s payments system.

By 1980, federal policymakers had designed a sweeping restructuring of bothfunctional and prudential regulation — commonly known as deregulation — that aimedto address the growing solvency crisis in the broader banking system. Whereasderegulation undoubtedly favored certain commercial banking interests (Isenberg,2003), its goals were much more pragmatic than ideological, rooted in ‘the inability ofgovernment policy to maintain a stable macroeconomic environment’ (Dymski, 2009a:277). As a regulatory strategy, this restructuring addressed insolvency pressures in twoways. On the one hand, it sought to recapitalize banks and allow them to better competefor household and business savings — increasing reserve requirements for savingsbanks (Olson, 2000: 12–13), and buttressing bank liabilities through increased depositinsurance limits, removal of interest caps on deposits and empowering banks to offerinterest-bearing checking accounts (Ball, 1990; Olson, 2000). On the other hand,related provisions sought to repair the asset side of banks’ balance sheets, diversifyingpermissible assets for thrifts, opening up growth opportunities in new product segmentsand allowing all banks to price and structure credit in response to increasingly volatilemarket pressures (FDIC, 1997; Olson, 2000). Securitization was one part of this ‘assetinflation’ strategy, and a parallel expansion of the powers of Fannie Mae and FreddieMac allowed banks to further recapitalize themselves by selling their underperformingmortgage assets to secondary market investors (Ball, 1990; Gotham, 2006). As anorientation to financial risk, then, this combination of liability deregulation and assetinflation retained and even expanded state managerial capacities focused on the safetyand soundness of the banking system; however, it empowered risk-taking on both sidesof a bank’s balance sheet (deposit-taking and lending/investment) by removing statutorylimits on bank competitive behavior.

Finally, the expansion of state managerial capacity surrounding financial risk wasevident in a third dimension of strategic transformation, evident by the mid-1980s inheightened prudential regulation and lender-of-last-resort powers (FDIC, 1997; 1998;Olson, 2000; Duménil and Lévy, 2004). Even as deregulation reduced limitations oncompetition, legislative initiatives such as the Garn St-Germain Act expanded open bankassistance and added new regulatory tools — such as net worth certificates — to allowregulators to buttress capital for distressed institutions (Olson, 2000: 57–8). This wasprompted by continuing deterioration in the operating environment for commercial andsavings banks, as well as by new situational threats to bank solvency. Many of these

Racialized credit risk in the United States 7

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

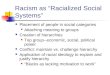

threats emerged as banks used their expanded powers to compete more intensively forhousehold and business deposits, and sought higher returns in non-traditional assets suchas LDC (least developed countries) debt, oil patch loans, commercial real estate, junkbonds and other speculative investments (Ball, 1990; FDIC, 1997; Gotham, 2006). Asthese speculative bets began to fail — evident as early as 1982 with the failure ofContinental Illinois Bank on its exposure to oil patch loans — regulators faced anescalating scale of lender-of-last-resort interventions (see Figure 1) and new questions ofcapacity and coordination (Olson, 2000). Not only were bank failures growing in size(Continental Illinois was then the largest bank failure in US history), but the threats tosolvency were increasingly diverse; they exposed complex interconnections betweenbanks with increased possibilities for contagion; and they threatened to overwhelm thefinancial safety net of deposit insurance, which was under significant stress and neededto be bailed out by 1987 (ibid.: 179). Thus, the 1980s involved ongoing experimentationwith more aggressive resolution techniques and forbearance programs, alongside ageneral concern over the regulatory capacity to manage the systemic risks of volatilefinancial markets (FDIC, 1998: 21, 80).

The pinnacle of extended lender-of-last-resort functions, however, was when federalregulators were forced to intervene on a much more dramatic scale to isolate threats tothe safety and soundness of the financial system. Here, the extraordinary events of 2007and 2008, as well as the ‘huge de facto nationalization of a major part of the US financeindustry’ (Ball, 1990: 73) in the wake of the late 1980s banking crisis — when over 750savings banks and 650 commercial banks collapsed between 1988 and 1990 (FDIC,2010) — stand as signal moments in the strategic transformation of state relationships tofinancial risk. Whereas the details of each of these crises differ significantly, their statusas significant threats to the safety and soundness of the financial system highlightsseveral commonalities in the subsequent regulatory interventions. In both cases, growinglosses on financial assets recast non-performing loans into ‘troubled’ assets that weighedon the profitability and solvency of individual firms and whose circulation increaseduncertainty in the market as a whole (Fender and Hördahl, 2007). Also common was thesudden expansion of federal powers, invoking a financial state of emergency to facilitate

Figure 1 Bank failure and assistance transactions, 1970–90 (source: FDIC, 2010)

8 Philip Ashton

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

direct acquisition of failing institutions and risky financial assets, removing themfrom circulation to prevent losses from overwhelming the financial safety net andreverberating more widely throughout the financial system and the real economy(Panitch and Konings, 2009). Even as the post-2007 emergency interventions have beenmuch broader in scope — encompassing traditional depository institutions and a widevariety of other firms and markets whose role in producing credit money has becomeindispensable in the era of financial liberalization — these commonalities highlight thedegree to which the financial state of emergency has become a recurrent feature ofthe economic and political landscape and a characteristic logic of financial regulation inthe neoliberal era (Scheuerman, 2000; 2004).

The practices of the financial emergency andthe rise of the subprime mortgage marketWhile a narrow focus on deregulation suggests reduced state capacities in favor ofheightened risk-taking by financial firms, a broader conceptualization indicates that thistransformation produced a temporal and scalar displacement of those capacities toparticular moments where ‘the temporality of deregulated exchange value . . . becomesproblematic [as] market forces provoke economic crises and states are expected torespond’(Jessop, 2007: 193). Such an approach opens new lenses into the re-regulation ofmortgage markets. As the resolution of large-scale financial crises can engage thesecapacities over a number of years, we must approach financial emergencies not as singlepoints of inflection, but rather as protracted processes of managing the circulation ofparticular types of financial risks. It also focuses our attention on the practices of riskmanagement during emergency interventions and their aftermath — such as how troubledassets or institutions are ‘triaged’ or removed from circulation, and the means developedto dispose of them or facilitate their re-absorption into the financial system. At the sametime, the scale of these interventions provides a basis to assess how those practicesestablish foundations for new power relationships between creditors and debtors throughnew significations of credit risk or new institutional structures of risk-taking.

As argued at the beginning of this article, this provides a conceptual methodology tore-approach a central question for urban scholars focused on racial exclusion from creditmarkets — namely, how could racialized risk be transformed so quickly and decisivelyinto the heightened exploitation found in the subprime mortgage market? The answer, Iargue, lies in the reconfiguration of risk relationships through the management of thebanking crisis of the late 1980s, which institutionalized the subprime market spaces thatcame to define the entrapment of minority borrowers. Here, I revisit this moment throughadministrative documentation on the management of the banking crisis, as well as earlytrade accounts of the emergence of the subprime market. This investigation identifies twosets of practices that I characterize as the financial exception at the heart of thisreconfiguration of racialized risk: those aimed at triaging troubled assets, either byremoving them from circulation or by developing forward-looking assessments of losspotential and severity; and those promoting liquidity in order to restore the norms ofrisk-taking.

Triaging troubled assets: non-performingmortgages and the financial exception

First, in the wake of the savings bank crisis of the late 1980s, as during the post-2007mortgage crisis, repairing the banking system and preventing its troubles fromreverberating more widely meant having to identify those banks and bank assets thatposed the most significant risks to the financial system. The central piece of legislationauthorizing federal intervention, the Financial Institutions Reform, Recovery and

Racialized credit risk in the United States 9

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

Enforcement Act of 1989 (FIRREA), established the Resolution Trust Company (RTC)as a temporary agency with broad powers to seize more than 750 insolvent savings banksand sell over US $400 billion in assets (FDIC, 1998: 427). RTC was to act as a ‘receiver’of risk, removing failing institutions or toxic assets from circulation by absorbing themonto its books before looking for least-cost ways to dispose of them (FDIC, 1997; 1998).This orientation towards the financial exception — in this case, measures intended toremove system-threatening institutions or assets from circulation to avoid contagion —sought to secure the financial safety net of deposit insurance and allow the norms ofrisk management to function within the broader financial system according toprevailing expectations and models (cf. Agamben, 2005). In the process of managingthe overwhelming number of failed banks, regulators were forced to address lossesassociated with particular categories of troubled assets, including speculativecommercial real estate projects as well as ‘non-performing’ mortgages — loans wherehomeowners were delinquent or in default, often because of recession-induced job loss.Unlike real property or performing mortgages — assets which RTC could sell directlyto other investors — direct sale was not feasible for non-performing loans because oftheir poor risk profile. The risk of these loans also complicated the use of governmentguarantees to make them palatable to investors (FDIC, 1998: 408–9).

Instead, RTC developed several practices that lay at the heart of the financialexception. First, it adapted and generalized innovations in securitization to maximizedisposal of troubled assets while minimizing direct costs to taxpayers. It pooled non-performing mortgages into independent trusts, which then issued securities backed by ahierarchy of claims on any cashflow generated by the pooled loans. These claims weredivided into risk classifications, or tranches, each defined by the degree of exposure tounderlying risk of loss; those classes least exposed to default risk resembled investment-grade assets and were able to qualify for good credit ratings (ibid.: 413). These mortgage-backed securities (MBS) were similarly priced according to risk exposure, with tranchesmost exposed to default risk earning a much higher return based on RTC’s inclusion ofa ‘delinquency pricing concession’ (ibid.: 415).

These ‘senior subordinate’ structures had been used with jumbo mortgages andconsumer loans since the mid-1980s to redistribute cash flows to investors (DeLiban andLancaster, 1995); however, those securitizations typically involved loans to borrowerswith strong credit performance, where the risks of loss were low across all tranches(Fabozzi, 2006: 116). Faced with higher loss potentials for non-performing loans, RTCfurther innovated with a variety of credit enhancements (such as cash reserve funds andcross-index structures) to sustain cashflows across predicted losses probabilities — thenormal route of paying a third party for insurance being too expensive relative to thepricing concessions necessary to make delinquent loans palatable to ratings agenciesand investors. These innovations allowed RTC to issue the first ever mortgage-backedsecurities that included non-performing or delinquent loans in June 1991, and by Octoberof that year it had completed 12 securitizations totaling US $5 billion includingsuch higher-risk loans (FDIC, 1998: 415). By 1993, Bear Stearns and a variety of othersecondary market conduits were mimicking these innovations, issuing private-label MBSusing internal credit enhancements (DeLiban and Lancaster, 1995).

Second, RTC also instituted a number of complementary joint venture and equitypartnership programs to develop the capacity of private market actors to acquire andmarket non-performing loans (FDIC, 1998). Whereas private firms had often beencontracted to maximize recovery of bank assets before, RTC’s N-series equitypartnership program was the first to try to maximize asset disposal by tying investorcompensation to the entrepreneurial management of both upside and downside risk;profit margins depended on the ability of servicers to extract value from non-performingborrowers (ibid.: 433). Instead of securitization, these programs allowed investorsto issue high-yield bonds to fund purchases of sub- and non-performing mortgages,using a pricing methodology — derived investment value or DIV — developed byRTC to calculate ‘the present value of future cash flows expected from liquidating a

10 Philip Ashton

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

nonperforming asset net of expenses’ (ibid.: 449). As Gotham (2006: 263) has arguedgenerally about RTC’s interventions, these practices ‘produced a “cultural template” [forrisk management] that affected investor understandings and perceptions of how themarket works and how they should act to control investment’. More directly, RTCdeveloped a network of servicers, trustees, underwriters and rating agencies to producea liquid market for bonds and mortgage-backed securities backed by non-performingloans (FDIC, 1998: 422). A number of the firms involved in equity partnerships migratedfrom managing non-performing loans to become early leaders in subprime originationsand servicing — such as Amresco, originally a loss collection firm (and subsidiary ofNationsBank) that disposed of US $17 billion in troubled bank assets for RTC beforetransforming itself into one of the top originators of subprime loans by 1996 (O’Hara,1993; Chomsisengphet and Pennington-Cross, 2006: 39).

To summarize, the need to mitigate systemic risks during extraordinary moments offinancial crisis involved regulatory practices that isolated credit risk into more precisecorners of the financial market, with two effects that relate directly to the transformationof racialized risk. First, it divorced selected categories of high-risk loans from thetraditional institutional venues of the mortgage market (retail banks and the goverment-sponsored enterprises, or GSEs, comprising the mainstream secondary mortgagemarket). The exercise of the financial exception created a new legal and market space —the credit-enhanced tranche — where the risks posed by non-performing loans could beisolated and where creditors could contractually clarify their exposure to loss. Second,it mitigated those higher risks by assigning higher rates of return, employing creditenhancements and the calculative techniques of DIV to price claims on the underlyingloans relative to the downside potential for loss. This had the effect of defining non-performing loans as sources of profitability in order to facilitate their disposition.Moreover, it expanded this space through the institutionalization of private marketsfor non-conforming mortgage-backed securities and high-yield bonds, both distinctchannels for funding mortgages that functioned outside of the prevailing marketframework for ‘plain vanilla’ loans. In so doing, it created the basis for transforminghigh-risk mortgage loans into a market space integrated with broader capital markets.

Triaging troubled assets: mortgage scoring and risk colonization

Second, the protracted management of the banking crisis was not only confined to RTCand existing non-performing loans, but migrated to new institutional venues as regulatorssought to develop forward-looking ‘mechanisms of control’ (Konings, 2009: 110)focused on the circulation of credit risk. This facilitated a process of risk colonization(Rothstein et al., 2006), whereby the techniques of risk management embodied in thefinancial exception came to ‘colonize aspects and domains of the lending process beyondthe original problematic’ (Marron, 2007: 116). This lens into regulatory practice allowsus to further distinguish those practices institutionalizing a new market space thatisolated certain types of risk from those that transformed that market space intosomething durable and expansionary.

Of particular concern in the wake of the 1989 banking crisis were the government-sponsored enterprises (GSEs) that formed the core of the US secondary mortgage marketand a growing component of the Treasury–money market nexus anchoring foreigncapital flows into US financial markets (Sarai, 2008; Schwartz, 2009). Experience withnon-performing loans in the lead-up to the banking crisis led federal regulators to auditFannie Mae and Freddie Mac in 1990 for their safety and soundness (CBO, 1991), andto focus on tools for ‘improved screening or pricing of the highest-risk “tail” of loans thathad previously been included under manual underwriting and . . . accounted for a muchhigher percentage of actual and expected default losses’ (Straka, 2000: 217). Fannie Maeand Freddie Mac were instrumental in developing mortgage scoring models, which theypackaged with automated underwriting software and promoted as standard industrypractices by 1994 (Straka, 2000). These techniques worked by comparing a borrower’s

Racialized credit risk in the United States 11

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

loan and risk profile against statistical models to produce an anticipated likelihood ofadverse credit events that could be used to price risk and allocate borrowers to specificloan products (Avery et al., 1996). While similar to (and often employing) the creditscoring techniques that have been the focus of much academic work on mortgagemarkets (Aalbers, 2008; Langley, 2008), mortgage scoring incorporated a wider range ofborrower and neighborhood factors to assess both loss likelihood and severity, includingloan-to-value ratio, local property value decline and prepayment likelihood (Vandell,1993; Straka, 2000).

Even as the early 1990s recession disproportionately harmed minority households andheightened their status as credit risks (Abu-Lughod, 1999), the growing use of mortgagescoring and automated underwriting as industry best practices meant that it was nolonger direct experience of non-performance (default) that solely defined risk. Mortgagescoring produced new forward-looking significations of credit risk defined not only bydefault but also by prepayment, with ‘the systematic determination of default risk[continuing] but under conditions whereby that risk is subsumed and integrated intoanother, wider and more complex determination of risk — the risk that the creditconsumer will be unprofitable to the lender’ (Marron, 2007: 121).

While the nascent subprime market did not initially adopt mortgage or creditscoring internally (Straka, 2000), the broader use of scoring and automated underwritingwithin mainstream mortgage channels sharpened the boundaries between those marketsegments and the residual space of the subprime market (Temkin et al., 2002). Non-performance found its equivalence in the high-risk borrower, as the social proximity ofmany minority households to risk factors — including recent histories of labor marketdisconnection, experience with default or other forms of financial distress, low levels ofliquid assets, high loan-to-value ratios at purchase or declining property values — wascaptured by mortgage scoring and formed the basis for the colonization of emergencypractices into new market segments (Marron, 2007). The strategic preferences of FannieMae and Freddie Mac for lower levels of risk shaped the subprime market into a residualspace targeted by a growing number of non-bank lenders and private secondary marketconduits, many of them specialist firms who had developed significant experience ofbundling, pricing, marketing and servicing high-risk loans through their work withRTC. Together, they formed the distinct institutional parameters shaping the growingconcentration of lenders on minority markets that patterned the rapid growth of subprimelending during the 1990s (Ashton, 2009; Immergluck, 2009a).

Restoring the norms of risk-taking:liquidity and speculative market development

Even as the exercise of the financial exception is oriented to the triage of system-threatening risks, financial states of emergency have simultaneously been moments wherecapital flows are liberalized on a situation-specific basis. As Gotham (2009) has noted,liquidity was a key tool in the management of financial crises, although we can lookbeyond his focus on securitization to identify a wide range of liquidity strategies andpractices (Kindleberger, 2000). During the 1980s, liquidity was at the heart of thewidening use of regulatory forbearance, a practice employed by regulators that ‘reducedcapital standards, liberalized ownership restrictions for stockholder-owned thrifts, andcapital and accounting forbearance that allowed [banks] to operate with minimal or noequity while their true condition was obscured’ (FDIC, 1997: 41). Loosened regulationsand forbearance were pragmatic strategies to allow solvent banks to purchase the assets offailed banks, or to allow failing banks to operate outside of prevailing risk managementnorms while they attempted to raise additional capital or grow their way out of insolvency.

The practices of the financial exception implemented by RTC were similarly concernedwith maximizing the disposal of troubled assets by transforming them back into negotiablefinancial instruments through a wide range of market-making activities. There are at leasttwo additional liquidity strategies we can point to that shaped the emergent subprime

12 Philip Ashton

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

market space, each involving different parameters and techniques. First, during the 1990s,regulatory forbearance became a forward-looking project of financial modernization,which sought to regularize bank liquidity through a more thorough integration of bankliabilities and assets with highly liquid equity and capital markets (Dymski, 1999;Newstadt, 2008).This project was enshrined in several pieces of legislation that removedgeographic restrictions on banking and branching (the Riegle-Neal Act of 1994) anddismantled remaining walls between banking and other financial services (the FinancialModernization Act of 1999). It was also evident in a growing set of regulatory practices,such as the shift away from regulation to supervision by the Federal Reserve andother regulatory agencies (Newstadt, 2008), which promoted firms’ own internal riskmanagement systems as the appropriate framework for governing the circulation offinancial risk. In order to consolidate and rationalize this regime, regulators began toinvoke federal powers of pre-emption, allowing financial firms to disregard state lawssetting limits on certain practices or products (Immergluck, 2004). This subsumed riskregulation to firm strategy, which during the 1990s became ever more focused on intensecompetition for market share within the growing subprime market (Ashton, 2009).

Second, just as important for the development of the subprime mortgage market andthe transformation of racialized risk were the spillover effects of monetary policyinterventions aimed at sustaining liquidity in the wake of new rounds of financialinstability — in particular, the Mexican currency crisis of late 1994 and early 1995. Asmonetary policy in the post-Bretton Woods era has become oriented towards creatingcertainty for financial markets — for instance, by keeping inflation low to ensure therelative stability of the national currency — sudden shifts in interest rates or currencyvalues to address actual or threatened instability have provided the fault lines aroundwhich markets take shape. With substantial US bank exposure to the collapse of theMexican peso in late 1994, financial regulators faced significant concerns over thestability of US financial asset values from a growing ‘flight to quality’. Respondingto these threats, the Fed and Treasury adopted a two-fold approach to liquidity: on theone hand, they coordinated a significant international ‘swap-line’ to allow Mexicanbondholders to roll over their debt (Whitt, 1996); on the other hand, the Federal ReserveBank continued a program of monetary tightening, raising short-term interest rates tosustain foreign purchases of US currency and protect the dollar from eroding relativeto the yen and the mark.4 This latter strategy was successful: foreign investment in USgovernment securities (including mortgage-backed securities issued by Fannie Mae andFreddie Mac) tripled between 1995 and 1997 relative to the early 1990s (Brenner, 2002:141). However, the Fed’s policy moves had the effect of driving down yields on Treasuryand GSE securities, and with them interest rates on prime mortgages, making thoseforms of lending much less profitable by comparison. Thus, a strategy focused onsustaining foreign investment in US financial markets had the effect of reorganizingthe landscape of profitability, ‘freeing a cascade of liquidity to purchase US equities’(ibid.) — including subprime securities and high-yield bonds — as domestic investorssearched elsewhere for higher returns and growth potential.

The Mexican peso crisis became a signal moment in the speculative development ofthe subprime mortgage market and the colonization of emergency risk practices into newsettings. Within a reconfigured risk-return landscape, the practices that had characterizedthe financial exception — the risk management and pricing techniques associated withRTC’s securitization and partnership programs — signaled to lenders and investors that

4 At the Federal Reserve’s Open Market Committee meeting in January 1995, Chairman AlanGreenspan put the issue succinctly in the context of a discussion dominated by the Mexican crisis:‘The problem is not so much a decline [in the dollar] as how quickly and how far it would decline inthe context of the way world markets have been behaving, where countries that are viewed asslightly suspicious find the foreign exchange vigilantes running at them. The United States is justbarely investment grade, if I may put it that way. I don’t think we have much leeway on the down sideto take those risks’ (Federal Reserve Board of Governors, 1995: 108).

Racialized credit risk in the United States 13

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

their exposure to the full risks of lending to borrowers with poor credit histories could belimited even as it was tied to significant interest premiums over conforming loan rates.Subprime mortgage lending quickly grew, increasing four-fold from US $40 billion inoriginations in 1994 to US $160 billion in 1999 (Temkin et al., 2002), and by 1997 tradesources were characterizing the growth in the market as a ‘stampede’ (Wahl and Forcardi,1997). As the rush into the subprime market began to put pressures on profits, lenders andinvestors pushed the market towards new market segments or new loan products thatfurther allowed borrowers to leverage their incomes or household assets. This set inmotion new patterns of risk-taking, with ‘institutions [trading] the apparent lowering ofcredit risk — accomplished through the mechanisms of securitization as well as themovement of the market into higher quality borrowers — for loosened underwritingstandards and nontraditional loan terms’ (Ashton, 2009: 1434).

Conclusion: the financial exception and racialized riskFollowing Ong (2006), interventions such as RTC or the Fed response to the peso crisistake their place within a range of governance practices that attempt to manage thedecisional uncertainties produced by neoliberalization. System-threatening risks couldlie in any form of fictitious capital whose unraveling threatens to leverage further lossesand reverberate through the broader economy; the growing weight of financial volatilityand the periodic financial crises that accompany it force policymakers and regulators intosituation-specific attempts to protect the ability of financial institutions to coordinatecritical aspects of economic and social policy. This has involved not only the expansionof key state capacities, such as lender-of-last-resort powers, but has produced newregulatory practices — the financial exception — that display a distinctive orientation tothe circulation of risk during periodic financial crises.

Whereas this reflects a particular form of state selectivity that has evolved sincethe breakdown of Bretton Woods (Jessop, 2002; 2007), the results of these practicesproduce spaces of exception with significant degrees of variegation — differentoutcomes, temporalities or spatialities — according to the context of their application(Mitchell, 2006; Ong, 2006). In the case of the subprime mortgage market, I have arguedthat the market space produced by the exercise of the financial exception in the wake ofthe banking crisis of the late 1980s was both durable and expansionary. RTC developeda number of programs and innovations focused on isolating ‘troubled’ assets, elaboratingnew techniques of risk management that transformed non-performing loans intoprofitable financial instruments that could be disposed of within broader capital markets.Even as this was oriented towards restoring the norms of risk-taking to prevailing modelsand expectations, it produced the basis for a new set of power relationships betweencreditors and minority debtors, evident in two areas. First, it established new normsfor the treatment and pricing of credit risk, and spurred the establishment ofdistinctive market structures where those norms could prevail. Second, a process ofrisk colonization mapped those risk management and pricing techniques into newinstitutional venues and onto inherited geographies of racialized risk and financialdisconnection. As monetary policy produced conditions for the intensification ofrisk-taking within those market spaces, the resulting patterns of market developmentdisproportionately exposed minority households and neighborhoods to a cycle of high-cost lending and over-competition, with ‘the “normal” laws governing lendingpractices . . . suspended for this territory, and the rent gap territory in which their homesare located [becoming] the new spaces of exception’ (Mitchell, 2006: 101).

While this article has abstracted away from the investigation of concrete socialand spatial structures of financial exclusion — as found in studies of geographicsegmentation of mortgage markets or concentrated foreclosure — I argue it neverthelessfills in critical gaps in the empirical record regarding the transformation of racialized riskand the production of those very spaces. Moreover, placing foundational concepts such as

14 Philip Ashton

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

risk at the center of this process opens up new avenues to investigate the urban problematicwithin financialization and to once more ‘relate national policies to local and individualdecisions . . . [that] create localized structures within which class-monopoly rents can berealized’ (Harvey, 1974: 247). It also offers the means to engage in dialogue withcomplementary perspectives in IPE, regulation and heterodox economics (cf. Dymski,2009c). For instance, the restructuring of power relations within credit or property marketsthrough IMF emergency interventions has been well studied inAsia and LatinAmerica (cf.Centner, 2007; Dymski, 2009a); a more systematic account of state practices in relation tofinancial risk could potentially offer fruitful grounds for comparative research into theglobal role of finance in producing the ‘urban problematic’ (Dymski, 2009c).

Embedding the state in relational risk also provides a basis to assess new geographiesof state intervention, including those that have unfolded since the global financial crisisof 2007–08. These interventions have characteristically aimed to triage troubled assetsand restore liquidity in US and global financial markets, and have ranged from far-reaching lender-of-last-resort interventions (including the nationalization of AIG, FannieMae and Freddie Mac) to extensive policies focused on reducing foreclosure activity. Asthe latter are overtly oriented towards altering power relations between lenders andborrowers by restructuring or refinancing subprime loans, a critical question is whetherthese interventions represent an opportunity to remedy historic inequities in creditmarkets, or a further deepening of financial exclusion. While remedial programs such asthe 2009 ‘Making Home Affordable’ initiative ostensibly aim to aid at-risk borrowers,closer examination of the practices of loan modification indicate they are stronglypatterned by the financial exception — employing eligibility or decision criteria todistinguish those loans worth saving from those deemed too risky. For instance, loansowned by GSEs are automatically eligible for modification, whereas those in private-label MBS pools have to pass a profitability test.5 As many of these eligibility ordecision-making criteria directly map onto the characteristics of concentrated subprimelending (which was defined by its reliance on private-label MBS), remedial programscome to function as their own form of financial exception or triage — isolating borrowersegments or neighborhoods where the subprime market and its speculative developmentran aground in the most severe fashion. Individual borrowers may win or lose in thisprocess, and the full parameters of the legal and market spaces emerging from the presentcrisis are not yet evident. What seems certain is that the exercise of the financialexception will continue to redraw the lines of risk in ways that will further conditionracial exclusion from credit markets.

Philip Ashton ([email protected]), College of Urban Planning and Public Affairs, Universityof Illinois–Chicago, 412 S. Peoria, 231 CUPPA Hall (MC 348), Chicago, IL 60607, USA.

ReferencesAalbers, M. (2008) The financialization of

home and the mortgage market crisis.Competition & Change 12.2, 148–66.

Aalbers, M. (2009a) Geographies of thefinancial crisis. Area 41.1, 34–42.

Aalbers, M. (2009b) The sociology andgeography of mortgage markets:reflections on the financial crisis.International Journal of Urban andRegional Research 33.2, 281–90.

Abu-Lughod, J. (1999) New York, Chicago,Los Angeles: America’s global cities.University of Minnesota Press,Minneapolis.

Agamben, G. (2005) State of exception.University of Chicago Press, Chicago.

Arrighi, G. (1994) The long twentiethcentury: money, power, and the originsof our times. Verso, London andNew York.

5 For more details on the Home Affordable Modification Program’s profitability test, see https://www.hmpadmin.com/portal/docs/hamp_servicer/npvoverview.pdf (accessed 24 March 2010).

Racialized credit risk in the United States 15

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

Ashton, P. (2008) Advantage or disadvantage?The changing institutional landscape ofunderserved mortgage markets. UrbanAffairs Review 43.3, 352–402.

Ashton, P. (2009) An appetite for yield: theanatomy of the subprime mortgage crisis.Environment and Planning A 41.6,1420–41.

Atia, M. (2007) In whose interest? Financialsurveillance and the circuits of exceptionin the war on terror. Environment andPlanning D: Society and Space 25.3,447–75.

Avery, R., R. Bostic, P. Calem and G. Canner(1996) Credit risk, credit scoring, and theperformance of home mortgages. FederalReserve Bulletin 82.7, 621–48.

Ball, M. (1990) Under one roof: retailbanking and the international mortgagefinance revolution. St. Martin’s Press,New York.

Bradford, C. (1979) Financing homeownership: the federal role inneighborhood decline. Urban AffairsQuarterly 14.3, 313–35.

Bradford, C. (2002) Risk or race? Racialdisparities and the subprime refinancemarket. Center for Community Change,Washington, DC.

Brenner, R. (2002) The boom and the bubble:the US in the world economy. Verso,New York.

Canner, G., W. Passmore and E. Laderman(1999) The role of specialized lenders inextending mortgages to lower-income andminority homebuyers. Federal ReserveBulletin 85 November, 709–23.

CBO (Congressional Budget Office) (1991)Controlling the risks ofgovernment-sponsored enterprises. CBO,Washington, DC.

Centner, R. (2007) Redevelopment from crisisto crisis: urban fixes of structuraladjustment in Argentina. Berkeley Journalof Sociology 51, 3–32.

Chomsisengphet, S. and A. Pennington-Cross(2006) The evolution of the subprimemortgage market. Federal Reserve Bank ofSt. Louis Review 88.1, 31–56.

de Brunhoff, S. (1978) The state, capital andeconomic policy. Pluto Press, London.

DeLiban, N. and B. Lancaster (1995)Understanding nonagency mortgagesecurity credit. Journal of HousingResearch 6.2, 197–216.

Duménil, G. and D. Lévy (2004) Capitalresurgent. Roots of the neoliberal

revolution. Translated by D. Jeffers.Harvard University Press, Cambridge, MA.

Dymski, G. (1998) Disembodied risk or thesocial construction of creditworthiness?In R. Rotheim (ed.), New Keynesianeconomics/post Keynesian alternatives,Routledge, London.

Dymski, G. (1999) The bank merger wave:the economic causes and socialconsequences of financial consolidation.M.E. Sharpe, Armonk, NY.

Dymski, G. (2009a) Financial governance inthe neo-liberal era. In G. Clark, A. Dixonand A. Monk (eds.), Managing financialrisks: from global to local, OxfordUniversity Press, Oxford.

Dymski, G. (2009b) Racial exclusion and thepolitical economy of the subprime crisis.Historical Materialism 17.2, 149–79.

Dymski, G. (2009c) Mortgage markets andthe urban problematic in the globaltransition. International Journal of Urbanand Regional Research 33.2, 427–42.

Fabozzi, F. (2006) Credit enhancements fornonagency MBS products. In F. Fabozzi(ed.), The handbook of mortgage-backedsecurities, McGraw-Hill, New York.

FDIC (Federal Deposit InsuranceCorporation) (1997) An examination ofthe banking crises of the 1980s and early1990s, Volume 1. Division of Researchand Statistics, Washington, DC.

FDIC (Federal Deposit InsuranceCorporation) (1998) Managing the crisis:the FDIC and RTC experience. FDIC,Washington, DC.

FDIC (Federal Deposit InsuranceCorporation) (2010) Historical statisticson banking — failure and assistancetransactions [WWW document].URL http://www2.fdic.gov/hsob/SelectRpt.asp?EntryTyp=30 (accessed1 August 2010).

Federal Reserve Board of Governors (1995)Federal open market committee, minutesof the January 31–February 1 meeting[WWW document]. URL http://www.federalreserve.gov/monetarypolicy/fomchistorical1995.htm (accessed 1February 2011).

Fender, I. and P. Hördahl (2007) Creditretrenchment triggers liquidity squeeze.BIS Quarterly Review September,1–16.

French, S., A. Leyshon and N. Thrift (2009)A very geographical crisis: the making andbreaking of the 2007–2008 financial crisis.

16 Philip Ashton

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

Cambridge Journal of Regions, Economyand Society 2.2, 287–302.

Gotham, K. (2006) The secondary circuit ofcapital reconsidered: globalization and theUS real estate sector. American Journalof Sociology 112.1, 231–75.

Gotham, K. (2009) Creating liquidity out ofspatial fixity: the secondary circuit ofcapital and the subprime mortgage crisis.International Journal of Urban andRegional Research 33.2, 355–71.

Harvey, D. (1974) Class-monopoly rent,finance capital and the urban revolution.Regional Studies 8, 239–55.

Harvey, D. and L. Chatterjee (1974) Absoluterent and the structuring of space byfinancial institutions. Antipode 6.1,22–36.

Helleiner, E. (1994) States and there-emergence of global finance: fromBretton Woods to the 1990s. CornellUniversity Press, Ithaca, NY.

Hernandez, J. (2009) Redlining revisited:mortgage lending patterns in Sacramento1930–2004. International Journal ofUrban and Regional Research 33.2,291–313.

Immergluck, D. (2004) Credit to thecommunity: community reinvestment andfair lending policy in the United States.M.E. Sharpe, Armonk, NY.

Immergluck, D. (2009a) Foreclosed: high-risklending, deregulation, and theundermining of America’s mortgagemarket. Cornell University Press, Ithaca,NY.

Immergluck, D. (2009b) Private risk, publicrisk: public policy, market developmentand the mortgage crisis. Fordham UrbanLaw Journal 36, 447–88.

Isenberg, D. (2003) The national origin offinancial liberalization: the case of theUnited States. In P. Arestis, M. Baddeleyand J. McCombie (eds.), Globalization,regionalism and economic activity, EdwardElgar, Northampton.

Jessop, B. (2002) The future of the capitaliststate. Polity, Cambridge.

Jessop, B. (2007) State power: astrategic-relational approach. Polity,Cambridge.

Kindleberger, C. (2000) Manias, panics andcrashes. Wiley, New York.

Konings, M. (2009) Rethinking neoliberalismand the subprime crisis: beyond there-regulation agenda. Competition &Change 13.2, 108–27.

Krippner, G. (2003) The fictitious economy:financialization, the state, andcontemporary capitalism. PhD dissertationin Sociology, UW–Madison, Wisconsin.

Kushmeider, R. (2005) The US federalfinancial regulatory system: restructuringfederal bank regulation. FDIC BankingReview 17.4, 1–30.

Langley, P. (2008) Sub-prime mortgagelending: a cultural economy. Economyand Society 37.4, 469–94.

Leyshon, A. (1992) The transformation ofregulatory order: regulating the globaleconomy and environment. Geoforum23.3, 249–67.

Marron, D. (2007) ‘Lending by numbers’:credit scoring and the constitution of riskwithin American consumer credit.Economy and Society 36.1, 103–33.

Martin, R. (1994) Stateless monies, globalfinancial integration and national economicautonomy: the end of geography? In S.Corbridge, N. Thrift and R. Martin (eds.),Money, power and space, Blackwell,Oxford.

Mitchell, K. (2006) Geographies of identity:the new exceptionalism. Progress inHuman Geography 30.1, 95–106.

Newman, K. (2009) Post-industrial widgets:capital flows and the production of theurban. International Journal of Urbanand Regional Research 33.2, 314–31.

Newstadt, E. (2008) Neoliberalism and theFederal Reserve. In L. Panitch and M.Konings (eds.), American empire andthe political economy of global finance,Palgrave Macmillan, New York.

O’Hara, T. (1993) Reaping a whirlwind:prodigal son vows to devourNationsBank’s bad loan glut. Warfield’sBusiness Record 8.11, 1.

Olson, G. (2000) Banks in distress: lessonsfrom the American experience of the1980s. Kluwer Law International, London.

Ong, A. (2006) Neoliberalism as exception:mutations in citizenship and sovereignty.Duke University Press, Durham, NC.

Panitch, L. and M. Konings (2009) Myths ofneoliberal deregulation. New Left Review57 May/June, 67–83.

Rothstein, H., M. Huber and G. Gaskell(2006) A theory of risk colonization: thespiralling regulatory logics of societal andinstitutional risk. Economy and Society35.1, 91–112.

Rude, C. (2008) The role of financialdiscipline in imperial strategy. In L.

Racialized credit risk in the United States 17

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.

Panitch and M. Konings (eds.), Americanempire and the political economy of globalfinance, Palgrave Macmillan, New York.

Sarai, D. (2008) US structural power and theinternationalization of the US Treasury.In L. Panitch and M. Konings (eds.),American empire and the politicaleconomy of global finance, PalgraveMacmillan, New York.

Scheuerman, W. (2000) Exception andemergency powers: the economic state ofemergency. Cardozo Law Review 21.5/6,1869–94.

Scheuerman, W. (2004) Liberal democracyand the social acceleration of time. JohnsHopkins University Press, Baltimore.

Schwartz, H. (2009) Subprime nation. CornellUniversity Press, Ithaca, NY.

Seabrooke, L. (2006) The social sources offinancial power. Cornell University Press,Ithaca, NY.

Straka, J. (2000) A shift in the mortgagelandscape: the 1990s move to automatedcredit evaluations. Journal of HousingResearch 11.2, 207–32.

Stuart, G. (2003) Discriminating risk: the USmortgage lending industry in the twentiethcentury. Cornell University Press, Ithaca,NY.

Temkin, K., J. Johnson and D. Levy (2002)Subprime markets, the role of GSEs, andrisk-based pricing. Office of PolicyDevelopment and Research, USDepartment of Housing and UrbanDevelopment, Washington, DC.

Vandell, K. (1993) Handing over the keys: aperspective on mortgage default research.Journal of the American Real Estate &Urban Economics Association 21.3,211–46.

Wacquant, L. (2002) From slavery to massincarceration: rethinking the ‘racequestion’ in the US. New Left Review13.1, 41–60.

Wahl, M. and C. Focardi (1997) Thestampede to subprime. Mortgage Banking1 October, 26–36.

Wainwright, T. (2009) Laying the foundationsfor a crisis: mapping thehistorico-geographical construction ofresidential mortgage backed securitizationin the UK. International Journal ofUrban and Regional Research 33.2,372–88.

Whitt, J. (1996) The Mexican peso crisis.Economic Review, Federal Reserve Bankof Atlanta 81.1, 1–20.

Wyly, E., M. Atia, H. Foxcroft, D. Hammeland K. Phillips-Watts (2006) Americanhome: predatory mortgage capital andneighbourhood spaces of race andclass exploitation in the UnitedStates. Geografiska Annaler 88b.1,105–32.

Wyly, E., M. Moos, D. Hammel and E.Kabahizi (2009) Cartographies of race andclass: mapping the class-monopoly rentsof American subprime mortgage capital.International Journal of Urban andRegional Research 33.2, 332–54.

RésuméDans la mouvance néolibérale, de nouvelles pratiques réglementaires ont entraîné lerepositionnement du risque de crédit ‘racialisé’. Aux États-Unis, la volatilité accrue desmarchés financiers a régulièrement menacé la capacité du secteur bancaire à fournir ducrédit. Les auteurs des réglementations se sont donc montrés plus agressifs, afin d’isolerles ‘actifs toxiques’ et de rétablir les normes de gestion des risques. Revenant sur lacréation du marché américain des prêts hypothécaires à haut risque (subprimes) audébut des années 1990, cet article étudie une question essentielle pour l’économiepolitique urbaine: comment des décennies d’exclusion raciale des marchés du crédit auxÉtats-Unis sont-elles passées si vite et si radicalement à une exploitation des membresdes minorités empruntant sur le marché des subprimes? Ce travail identifie un ensemblede pratiques régulatrices liées à la gestion de la crise bancaire de la fin des années 1980,et soutient que leur orientation spécifique vers la circulation du risque a créé à la fois unnouvel espace juridique et un nouvel espace de marché pour les prêts à haut risque. Ilanalyse ensuite la migration de ces pratiques à risque exceptionnelles vers les sitesinstitutionnels qui ont configuré le marché des subprimes et ont exposé les emprunteursissus des minorités à un parasitisme plus intense. On peut en déduire de nouvellespossibilités pour l’économie politique urbaine à partir d’une conceptualisation élargiedes rapports entre l’État et le risque financier.

18 Philip Ashton

International Journal of Urban and Regional Research© 2011 The Author. International Journal of Urban and Regional Research © 2011 Joint Editors and BlackwellPublishing Ltd.