Embed Size (px)

Citation preview

Revised January 26, 2016

TRID

TRID

QUICK REFERENCE GUIDE 10.3.2015

© 2015 CMG Financial, All Rights Reserved. CMG Financial is a registered trade name of CMG Mortgage, Inc., NMLS #1820 in most, but not all

states. CMG Mortgage, Inc. is an equal opportunity lender, licensed by the Department of Business Oversight under the California Residential

Mortgage Lending Act No. 4150025, Loans made or arranged pursuant to a California Finance Lenders Law license No. 6053674. Offer of credit is

subject to credit approval. For information about our company, please visit us at www.cmgfi.com. To verify our complete list of state licenses,

please visit www.nmlsconsumeraccess.org. For more information on State licenses, please visit http://www.cmgfi.com/corporate/licensing. Not

intended to serve as a business solicitation for residents in Massachusetts. For Wholesale Brokers and Select Partner Clients only.

1 | P a g e Revised January 26, 2016

Contents TRID – Effective Date ..................................................................................................... 2

TRID – Definition of an Application ..................................................................................... 2

Important Definitions ..................................................................................................... 2

TRID – Creating New Loans ............................................................................................... 3

Create New Loan with an Application Dated on or after 10/3/2015 & Requesting an LE .................... 4

Creating New Loan with Applications Dated Prior to 10/3/2015 ................................................. 9

Transferred Loan ........................................................................................................ 12

Creating TBD Registration ............................................................................................. 15

Creating An AIO-All in One Registration ............................................................................. 19

Creating Quick Register to Advance Lock ........................................................................... 23

COC – Change of Circumstance ........................................................................................ 28

Ordering the Appraisal Using an Authorization Code ............................................................. 30

Generate the Closing Disclosure - CD ................................................................................ 31

2 | P a g e Revised January 26, 2016

TRID – Effective Date TRID rules go into effect with applications taken or after 10/3/2015. The following loans are exempt from TRID rules:

1. Loans with application dates before 10/3/2015. 2. All In One Loans 3. HELOCs 4. Reverse Mortgages 5. Mortgages secured by a mobile home or dwelling not attached to real property

At CMG Financial, you will only need to concern yourself with the first two exemptions. We do not originate HELOCS, Reverse Mortgages or mortgages secured by a mobile home or dwelling not attached to real property. Applications on or after 10/3/2015, will be originated with the new TRID forms, Loan Estimate (LE) and Closing Disclosure (CD). This document is meant to walk you through the new technology.

TRID – Definition of an Application With the implementation of TRID the CFPB has redefined the application. The CFPB states that when

you have the following six pieced of information, that is considered to be an application and the clock

starts for disclosing.

1. The Consumer’s Name

2. The Consumer’s Income

3. The Consumer’s Social Security Number to obtain a credit report (or unique identifier if the

consumer does not have a social security number).

4. The Property Address

5. An Estimate of the Value of the Property

6. Loan Amount

Important Definitions Wholesale/Broker definitions. For Select Partners, please refer to the TRID Select Partner

Presentation.

General Business Days: Monday – Friday, excluding Saturday, Sunday and specific federal holidays.

Specific Business Days: Monday – Saturday excluding Sunday and specific federal holidays.

3 | P a g e Revised January 26, 2016

TRID – Creating New Loans

On 10/3/2015, CMG’s website https://wt.cmgmortgage.com/DataTracWeb/Logon will be updated to include a new feature, ‘Create New Loan’. ‘Create New Loan’ is to be used as the starting point for all new loans. The ‘Create New Loan’ feature may be found under the Dashboard Tab.

After selecting the ‘Create New Loan’ option, you will be taken to the ‘New Loan’ screen. There you

will answer a series of questions to determine whether or not your loan is subject to the new TRID

Rules and the path that it will take during creation.

4 | P a g e Revised January 26, 2016

Create New Loan with an Application Dated on or after 10/3/2015 & Requesting an LE

Once you have an application, these instruction will walk you through creating a new loan and

requesting an LE/disclosure package.

After signing into CMG’s website, from the Dashboard tab choose ‘Create New Loan’.

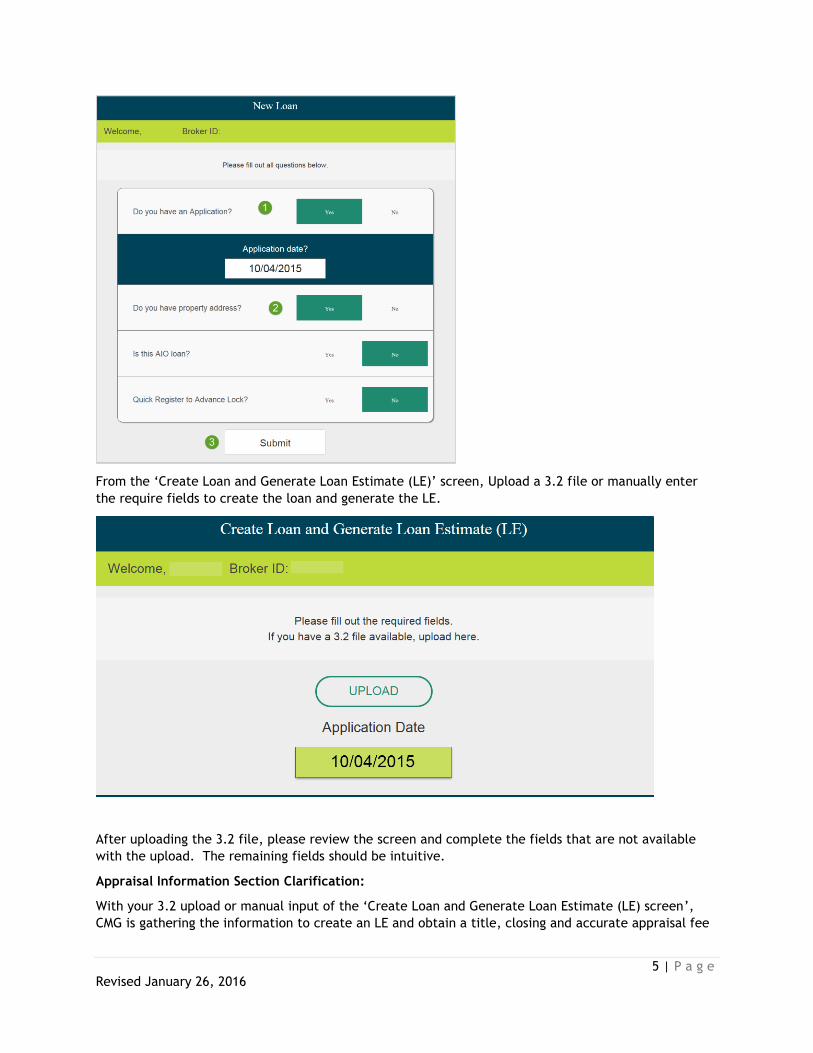

From the ‘New Loan’ screen, you will answer:

1. ‘Yes’ you have an application. Enter the application date or choose the date from the

calendar. For this scenario, the application date should be 10/3/2015 or after.

2. ‘Yes’ you have a property address

3. Submit, you will be taken to the ‘Create Loan and Generate Loan Estimate (LE)’ screen.

5 | P a g e Revised January 26, 2016

From the ‘Create Loan and Generate Loan Estimate (LE)’ screen, Upload a 3.2 file or manually enter

the require fields to create the loan and generate the LE.

After uploading the 3.2 file, please review the screen and complete the fields that are not available

with the upload. The remaining fields should be intuitive.

Appraisal Information Section Clarification:

With your 3.2 upload or manual input of the ‘Create Loan and Generate Loan Estimate (LE) screen’,

CMG is gathering the information to create an LE and obtain a title, closing and accurate appraisal fee

6 | P a g e Revised January 26, 2016

quote. You will be required to answer three items in the Appraisal Information section to complete the

quote.

NOTE: This section does not speak to the eTrac Appraisal ordering site. The information that we are

gathering here is for fee quote purposes only.

1. Final or Re inspection 1004D Required - From the dropdown choose ‘Yes’ or ‘No’.

2. Rush Fee – From the dropdown choose ‘Yes’ or ‘No’

3. Size (In Acres) – You will have 4 options to choose from.

After all of the information has been entered correctly, ‘Generate LE Request’ will appear green at the

bottom of the page. Click ‘Generate LE Request’.

If the ‘Generate LE Request’ field appears red, required items may have been missed. Please tab

through the fields or look for the item that may also be highlighted red. Once all fields are completed

correctly, the ‘Generate LE Request’ field will appear in green.

NOTE: Please do not use any punctuation in the fields when completing the form.

7 | P a g e Revised January 26, 2016

After clicking on the ‘Generate LE Request’ you will receive the following message that confirms that

your creation was successful and it includes the new loan number.

8 | P a g e Revised January 26, 2016

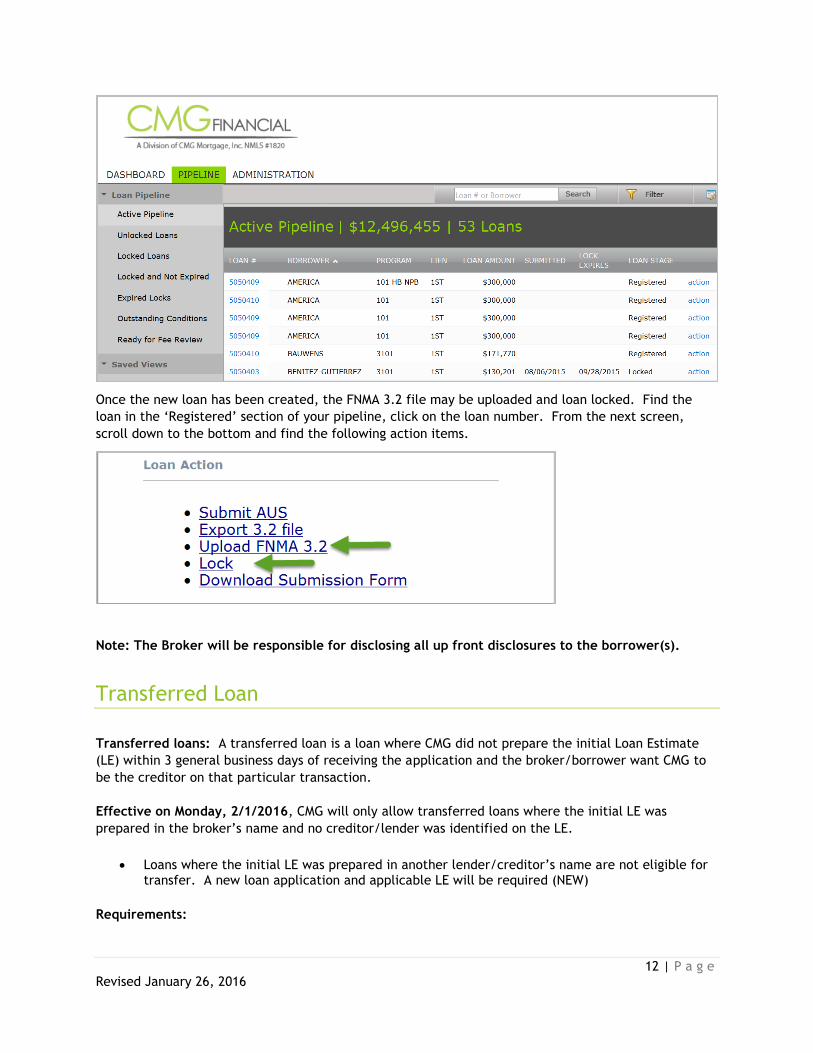

The newly created loan may be found in your pipeline under the Pipeline tab.

Once the new loan has been created, the loan may be locked. Find the loan in the ‘Registered’ section

of your pipeline, click on the loan number. From the next screen, scroll down to the bottom and find

the following action items.

Note: A new loan action item has been added to the menu of items available after clicking on the loan

number. ‘Upload FNMA 3.2’ may be used to upload an updated 3.2 file prior to submitting your loan to

CMG. Once loan has been submitted and status changed to Underwriter Received, this feature will no

9 | P a g e Revised January 26, 2016

longer be available. All additional updates must be requested by sending an updated 1003 for review

by the underwriter.

Creating New Loan with Applications Dated Prior to 10/3/2015

NOTE: Friday 2/12/2016 will be the last day CMG will accept Pre-TRID transactions. All Pre-TRID

transactions must be submitted to the CMG Wholesale office no later than 2/12/2016. Loans with application

dates prior to October 3, 2015 will not be accepted after 2/12/2016 and will require that the borrower re-apply

and the loan will be subject to TRID rules.

All loans with applications dated prior to 10/3/2015, must close and fund by 3/31/2016.

Note: Construction loans are excluded from having to close by 3/31/2016

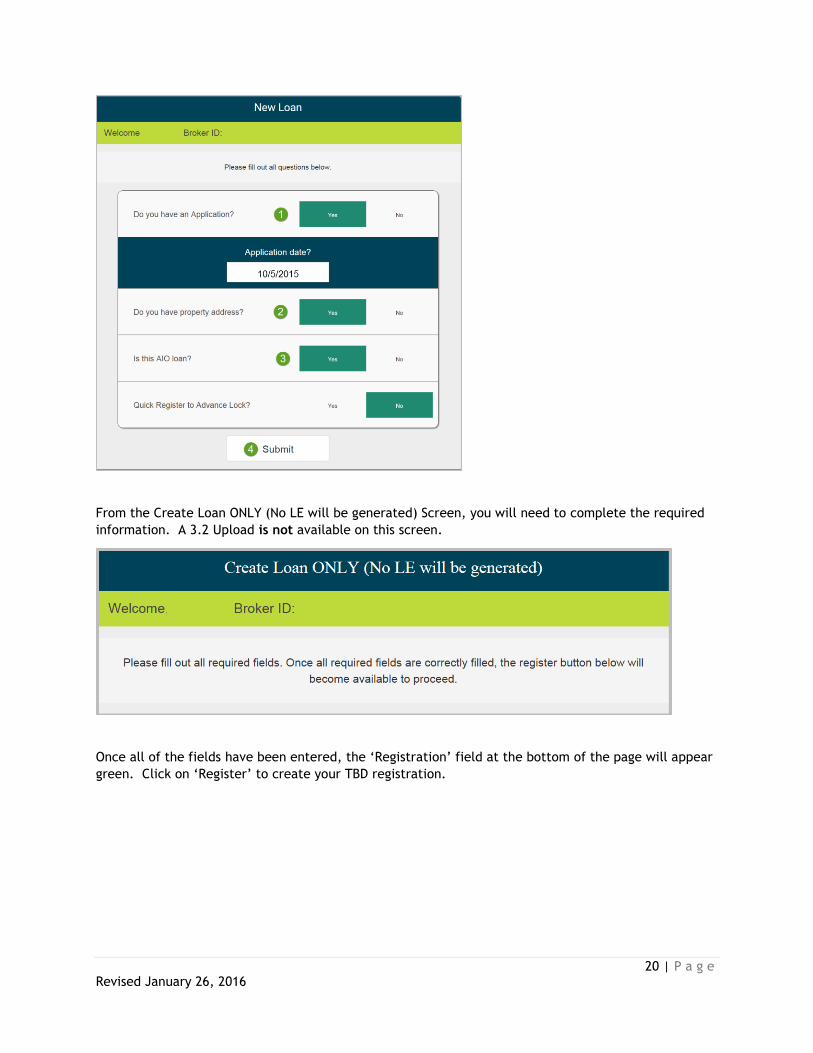

A New Loan may be created for loans with application dates prior to 10/3/2015 by following these

steps. Sign into CMG’s website, from the Dashboard tab choose ‘Create New Loan’.

From the ‘New Loan’ screen, you will answer:

1. ‘Yes’ you have an application. Enter the application date or choose the date from the

calendar.

2. ‘Yes’ you do have a property address

3. Submit, you will be taken to the ‘Create Loan ONLY (no LE will be generated)’ screen.

10 | P a g e Revised January 26, 2016

From the Create Loan ONLY (No LE will be generated) Screen, you will need to complete the required

information. A 3.2 Upload is not available on this screen.

Once all of the fields have been entered, the ‘Registration’ field at the bottom of the page will appear

green. Click on ‘Register’ to create your TBD registration.

11 | P a g e Revised January 26, 2016

If the ‘Register’ field appears red, required items may have been missed. Please tab through the fields

or look for the item that may also be highlighted red. Once all fields are completed correctly, the

‘Register’ field will appear in green.

NOTE: Please do not use any punctuation in the fields when completing the form.

After clicking ‘Register’ you will receive the following message that confirms that your creation was

successful and it includes the new loan number.

The newly created loan may be found in your pipeline under the Pipeline tab.

12 | P a g e Revised January 26, 2016

Once the new loan has been created, the FNMA 3.2 file may be uploaded and loan locked. Find the

loan in the ‘Registered’ section of your pipeline, click on the loan number. From the next screen,

scroll down to the bottom and find the following action items.

Note: The Broker will be responsible for disclosing all up front disclosures to the borrower(s).

Transferred Loan

Transferred loans: A transferred loan is a loan where CMG did not prepare the initial Loan Estimate

(LE) within 3 general business days of receiving the application and the broker/borrower want CMG to

be the creditor on that particular transaction.

Effective on Monday, 2/1/2016, CMG will only allow transferred loans where the initial LE was

prepared in the broker’s name and no creditor/lender was identified on the LE.

Loans where the initial LE was prepared in another lender/creditor’s name are not eligible for transfer. A new loan application and applicable LE will be required (NEW)

Requirements:

13 | P a g e Revised January 26, 2016

Expired Loan Estimates: Transaction where an LE (non-CMG LE) was prepared in the broker’s name and issued within 3 general business days of receiving the loan application. The borrower did NOT provide an Intent to Proceed (ITP) within 10 days of the LE being issued.

o CMG will accept that loan with a copy of the initial expired Broker LE (It must be a minimum of 11 days from the issue date) and a LOE from the loan officer stating that the Intent to Proceed (ITP) was never provided by the borrower(s).

Cancelled or Withdrawn loans: Transactions where an LE (non CMG LE) was prepared in the broker’s name and issued within 3 general business days of receiving the loan application. The borrower(s) DID provide an Intent to Proceed (ITP). The transaction is later withdrawn or cancelled by the borrower.

o CMG will accept that loan with a copy of the initial LE that was issued in the broker’s name within 3 business days of the application date and a LOE from the borrower that they wish to cancel their application with the initial investor/lender and want to proceed with an application with CMG Financial. The LOE must be dated and the CMG Loan Estimate must be requested within 2 business days form the date on the letter. The transfer letter does not need to include the name of the original lender. A Sample Copy of this letter may be found on the TRID Resource page in the Reference Material Section

Sign into CMG’s website, from the Dashboard tab choose ‘Create New Loan’.

From the ‘New Loan’ screen, you will answer:

1. ‘Yes’ you have an application. Enter the application date from the original application or

choose the date from the calendar.

2. ‘Yes’ you do have a property address

3. Submit

14 | P a g e Revised January 26, 2016

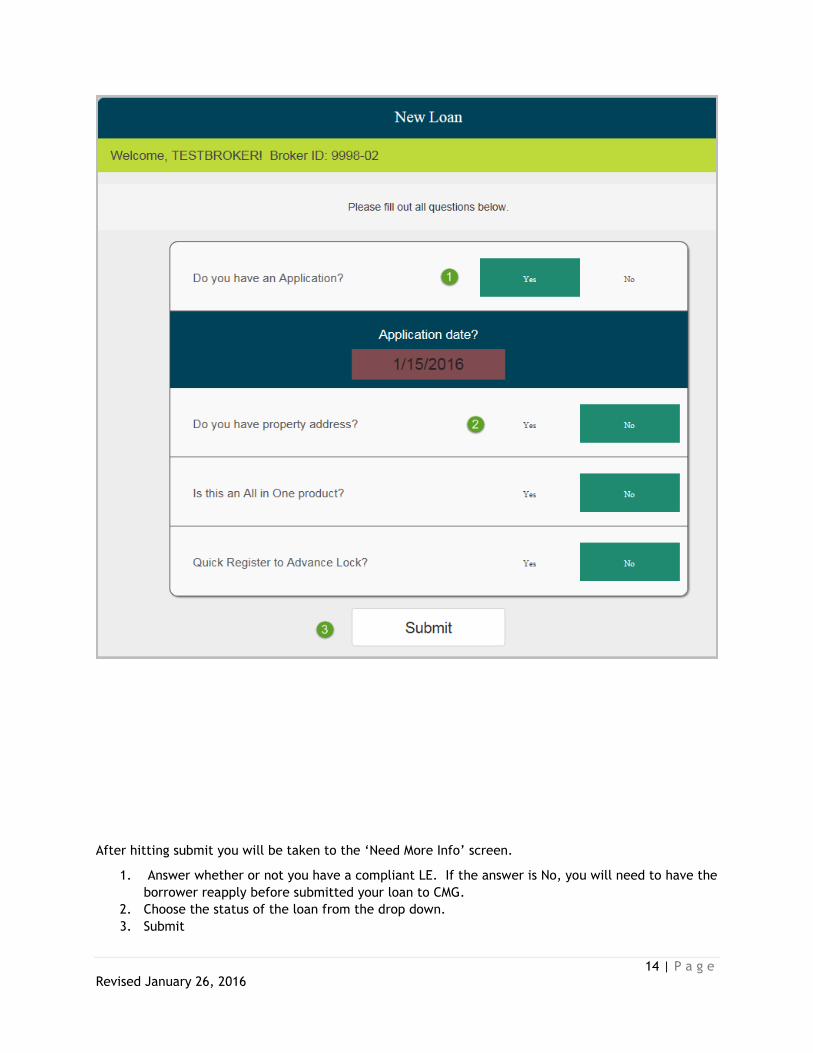

After hitting submit you will be taken to the ‘Need More Info’ screen.

1. Answer whether or not you have a compliant LE. If the answer is No, you will need to have the

borrower reapply before submitted your loan to CMG.

2. Choose the status of the loan from the drop down.

3. Submit

15 | P a g e Revised January 26, 2016

NOTE: When completing the ‘Create Loan and Generate LE’ screen, please consider the date of

the borrower’s written request expressing their desire to submit their application to CMG Financial

or denial letter as the application date.

Please refer to page 5 and follow the steps.

Creating TBD Registration

A TBD registration may be created by following these steps. Sign into CMG’s website, from the

Dashboard tab choose ‘Create New Loan’.

16 | P a g e Revised January 26, 2016

From the ‘New Loan’ screen, you will answer:

4. ‘Yes’ you have an application. Enter the application date or choose the date from the

calendar.

5. ‘No’ you do not have a property address

6. Submit, you will be taken to the ‘Create Loan ONLY (no LE will be generated)’ screen.

From the Create Loan ONLY (No LE will be generated) Screen, you will need to complete the required

information. A 3.2 Upload is not available on this screen.

17 | P a g e Revised January 26, 2016

Once all of the fields have been entered, the ‘Registration’ field at the bottom of the page will appear

green. Click on ‘Register’ to create your TBD registration.

If the ‘Register’ field appears red, required items may have been missed. Please tab through the fields

or look for the item that may also be highlighted red. Once all fields are completed correctly, the

‘Register’ field will appear in green.

NOTE: Please do not use any punctuation in the fields when completing the form.

After clicking ‘Register’ you will receive the following message that confirms that your creation was

successful and it includes the new loan number.

18 | P a g e Revised January 26, 2016

The newly created loan may be found in your pipeline under the Pipeline tab.

TBD Next steps:

The LE/Disclosure package will not be created or sent to the borrower.

Once a property has been identified, within 2 business days you will need to notify your Account

Manager and provide him/her with the property address. The Account Manager will update the account

with the property address and remove the TBD from the program code. Once these updates have been

made you will be able to request the LE. The ‘Generate a Loan Estimate’ option can be found by

locating the loan in your pipeline, clicking on the loan number and scrolling down to the Loan Action

items.

19 | P a g e Revised January 26, 2016

Creating An AIO-All in One Registration

The AIO-All In One program is exempt from TRID Rules. An AIO loan may be created following these

steps. Sign into CMG’s website, from the Dashboard tab choose ‘Create New Loan’.

From the ‘New Loan’ screen, you will answer:

1. ‘Yes’ you have an application. Enter the application date or choose the date from the

calendar.

2. ‘Yes’ you do have a property address.

3. ‘Yes’ this is an AIO loan.

4. Submit, you will be taken to the ‘Create Loan ONLY (no LE will be generated)’ screen.

20 | P a g e Revised January 26, 2016

From the Create Loan ONLY (No LE will be generated) Screen, you will need to complete the required

information. A 3.2 Upload is not available on this screen.

Once all of the fields have been entered, the ‘Registration’ field at the bottom of the page will appear

green. Click on ‘Register’ to create your TBD registration.

21 | P a g e Revised January 26, 2016

If the ‘Register’ field appears red, required items may have been missed. Please tab through the fields

or look for the item that may also be highlighted red. Once all fields are completed correctly, the

‘Register’ field will appear in green.

NOTE: Please do not use any punctuation in the fields when completing the form.

After clicking ‘Register’ you will receive the following message that confirms that your creation was

successful and it includes the new loan number.

22 | P a g e Revised January 26, 2016

The newly created loan may be found in your pipeline under the Pipeline tab.

Once the new loan has been created, the FNMA 3.2 file may be uploaded and loan locked. Find the

loan in the ‘Registered’ section of your pipeline, click on the loan number. From the next screen,

scroll down to the bottom and find the following action items.

NOTE: The AIO – All In One program is TRID exempt, it is the broker’s responsibility to send out

the early disclosures to the borrower(s).

23 | P a g e Revised January 26, 2016

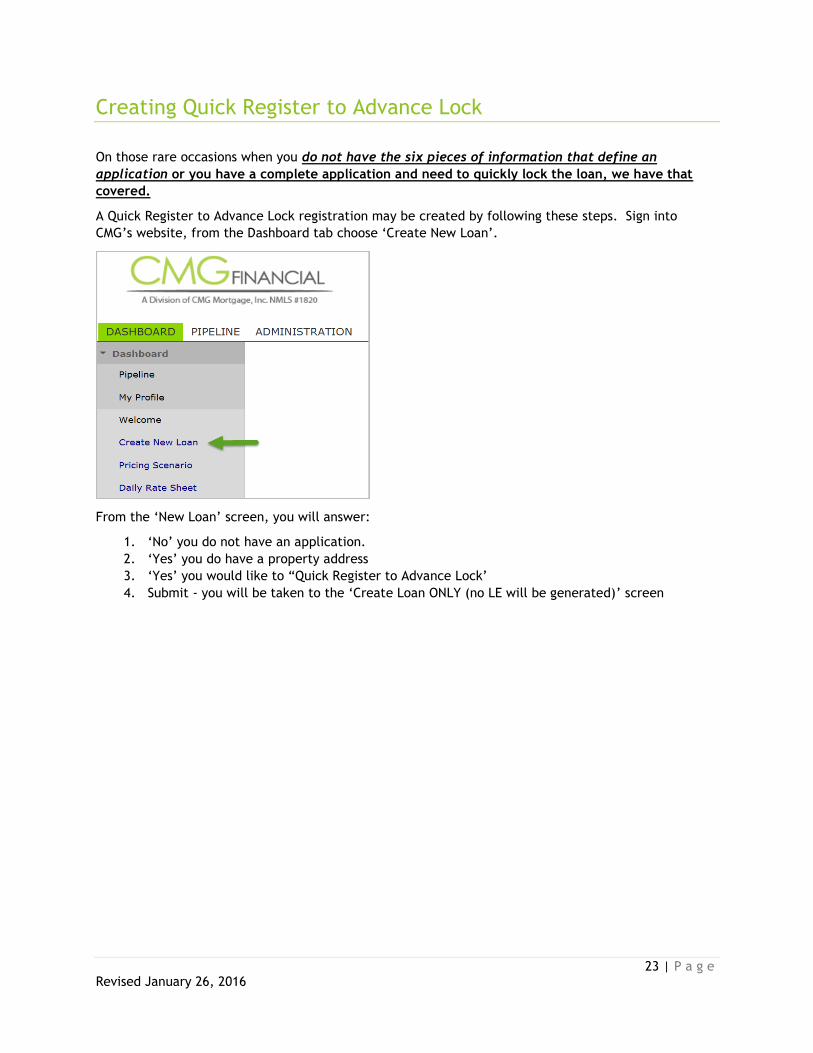

Creating Quick Register to Advance Lock

On those rare occasions when you do not have the six pieces of information that define an

application or you have a complete application and need to quickly lock the loan, we have that

covered.

A Quick Register to Advance Lock registration may be created by following these steps. Sign into

CMG’s website, from the Dashboard tab choose ‘Create New Loan’.

From the ‘New Loan’ screen, you will answer:

1. ‘No’ you do not have an application.

2. ‘Yes’ you do have a property address

3. ‘Yes’ you would like to “Quick Register to Advance Lock’

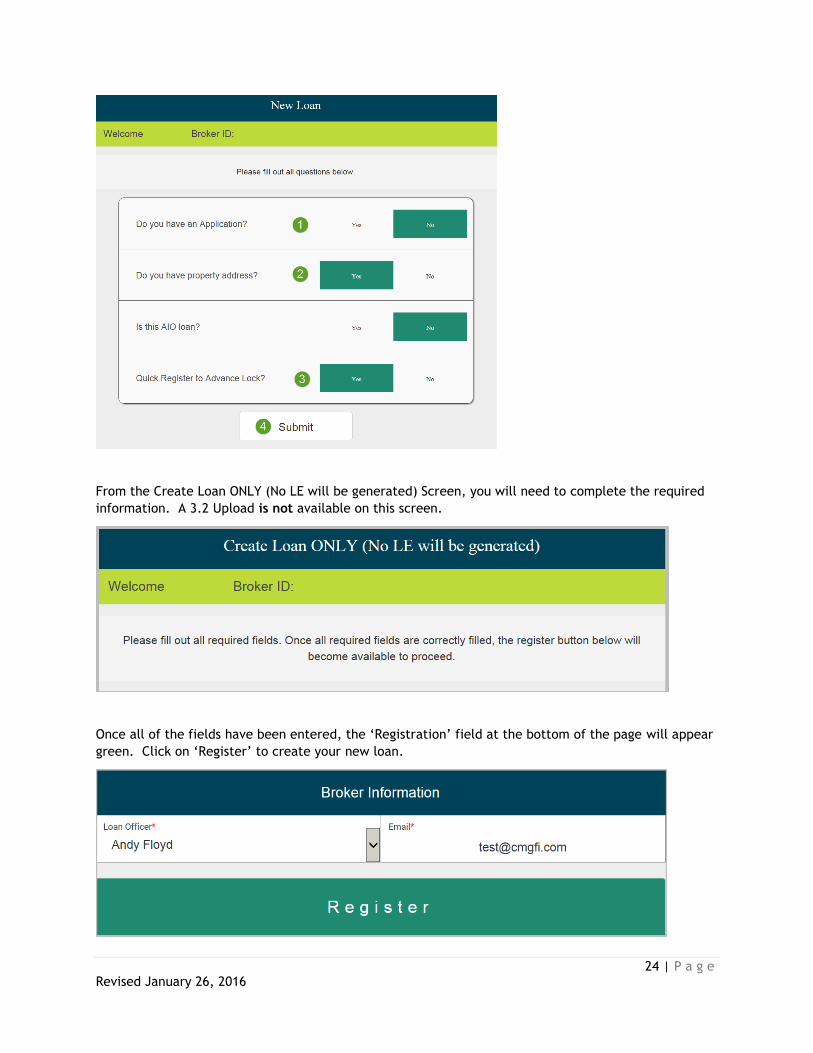

4. Submit - you will be taken to the ‘Create Loan ONLY (no LE will be generated)’ screen

24 | P a g e Revised January 26, 2016

From the Create Loan ONLY (No LE will be generated) Screen, you will need to complete the required

information. A 3.2 Upload is not available on this screen.

Once all of the fields have been entered, the ‘Registration’ field at the bottom of the page will appear

green. Click on ‘Register’ to create your new loan.

25 | P a g e Revised January 26, 2016

If the ‘Register’ field appears red, required items may have been missed. Please tab through the fields

or look for the item that may also be highlighted red. Once all fields are completed correctly, the

‘Register’ field will appear in green.

NOTE: Please do not use any punctuation in the fields when completing the form.

After clicking ‘Register’ you will receive the following message that confirms that your creation was

successful and it includes the new loan number.

The newly created loan may be found in your pipeline under the Pipeline tab.

26 | P a g e Revised January 26, 2016

Search for the loan within the pipeline. Once found, click on the loan number. This will open the loan

and appropriate action items. To lock the loan, choose the ‘Lock’ action item and complete the

required fields to lock the loan.

Note: An LE has not been generated. The LE must be requested within two ‘General Business

Days’ of the loan being locked or risk the lock being cancelled. Automated email reminders will be

sent to the contacts provided when loan created.

The LE may be requested by accessing the loan within the pipeline. Click on the loan number, scroll

down to the action items and choose, ‘Generate Loan Estimate’.

27 | P a g e Revised January 26, 2016

After choosing ‘Generate Loan Estimate’, the ‘Create Loan and Generate Loan Estimate (LE)’ screen

will open. From here you will upload your FNMA 3.2 file or manually complete the fields to create your

LE. Refer to page 5 of this document and follow the steps.

28 | P a g e Revised January 26, 2016

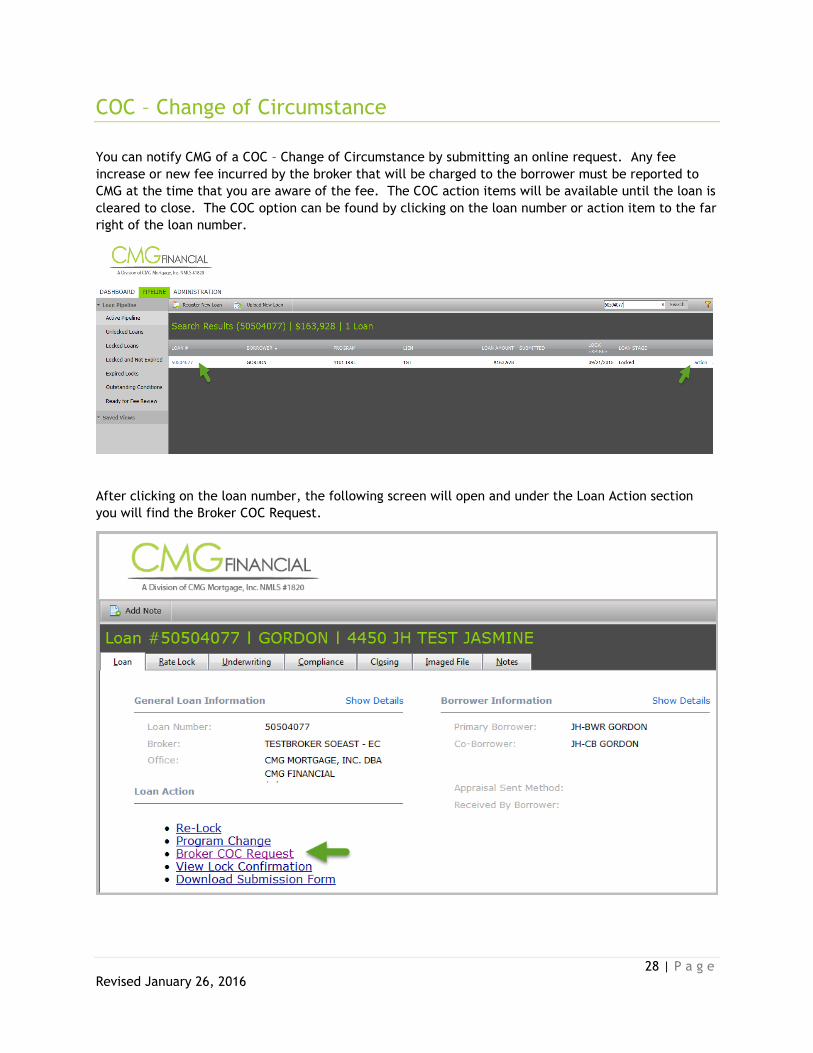

COC – Change of Circumstance

You can notify CMG of a COC – Change of Circumstance by submitting an online request. Any fee

increase or new fee incurred by the broker that will be charged to the borrower must be reported to

CMG at the time that you are aware of the fee. The COC action items will be available until the loan is

cleared to close. The COC option can be found by clicking on the loan number or action item to the far

right of the loan number.

After clicking on the loan number, the following screen will open and under the Loan Action section

you will find the Broker COC Request.

29 | P a g e Revised January 26, 2016

By clicking on the action item to the far right hand side of the screen, the following screen will open

and you will find the Broker COC Request under the action items.

After opening either action item, you will be taken to the COC screen. Please enter any new or

updated fees as they incur, provide instructions and hit submit. CMG will be notified of the fee change

or update and process accordingly.

Please note that ALL changes to loan amounts, program/product, appraised value, sales price and

appraisal inspections will be processed by CMG once the underwriter has reviewed and approved.

30 | P a g e Revised January 26, 2016

Ordering the Appraisal Using an Authorization Code

At the time that CMG generates the LE, we will also create the authorization code that is needed to

order the appraisal via the eTrac Appraisal ordering site. This code will be emailed to the email

address or addresses provided at the time that the LE was requested. This authorization code will also

be placed in the ‘Notes’ tab inside of the loan for future reference.

The email will be sent from [email protected] and the subject line will be Global DMS Code and

reference your CMG loan number. See below for a sample of the email that will be sent.

The authorization code must be entered into the ‘Authorization Code’ field inside of the eTrac

appraisal ordering site when placing the order.

Note: The appraisal cannot not be ordered until the a primary borrower has opened/received the

LE and he/she has indicated their Intent to Proceed.

31 | P a g e Revised January 26, 2016

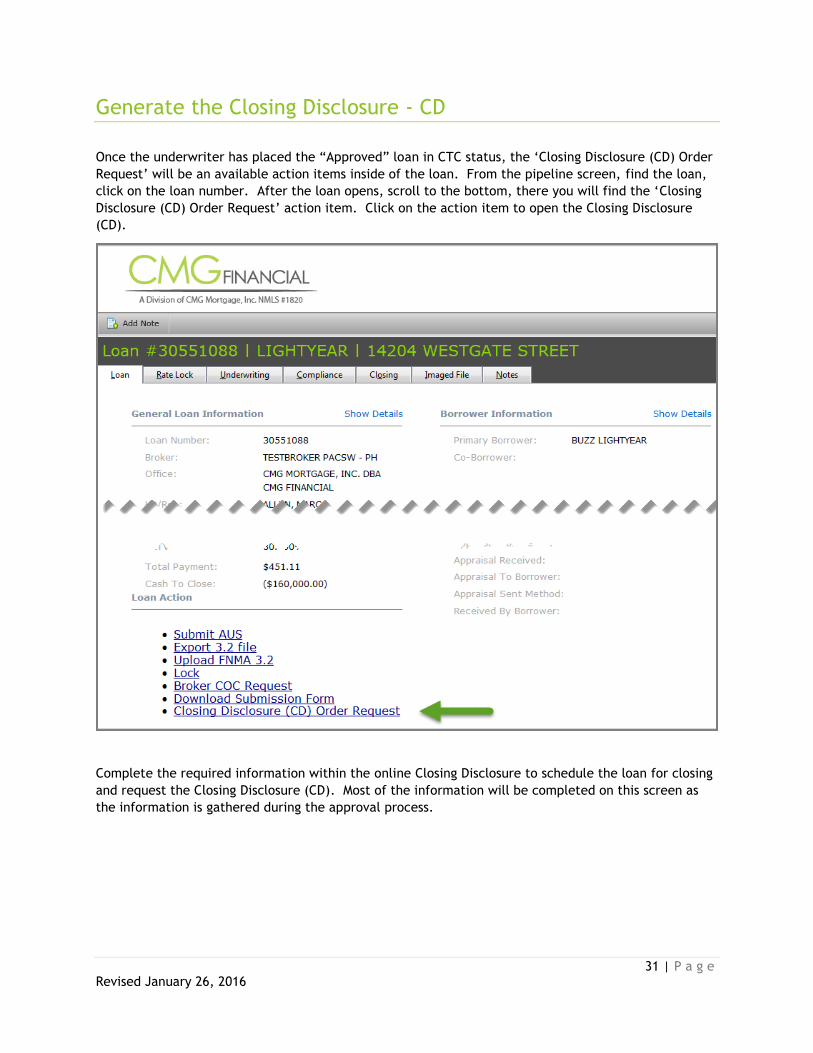

Generate the Closing Disclosure - CD

Once the underwriter has placed the “Approved” loan in CTC status, the ‘Closing Disclosure (CD) Order

Request’ will be an available action items inside of the loan. From the pipeline screen, find the loan,

click on the loan number. After the loan opens, scroll to the bottom, there you will find the ‘Closing

Disclosure (CD) Order Request’ action item. Click on the action item to open the Closing Disclosure

(CD).

Complete the required information within the online Closing Disclosure to schedule the loan for closing

and request the Closing Disclosure (CD). Most of the information will be completed on this screen as

the information is gathered during the approval process.