Embed Size (px)

Citation preview

ACN 004 201 307

Caltex Australia Limited

Treasury in AsiaFinance & Treasury Association Congress - November 2016

Overview

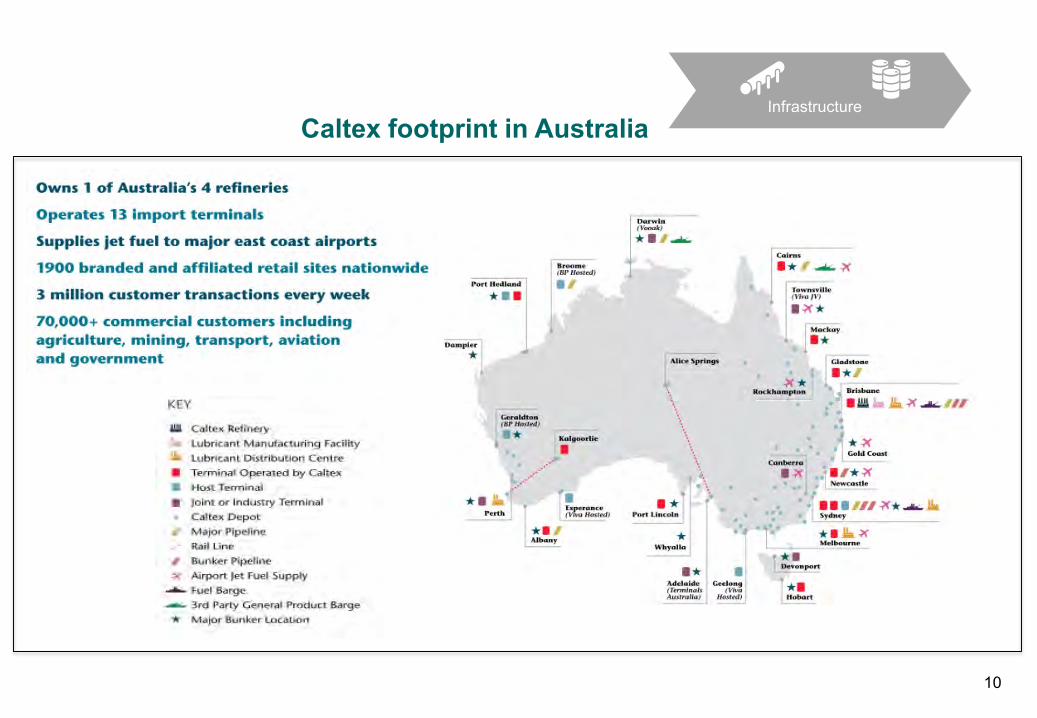

• Caltex is the nation’s leading transport fuel supplier

• Australian Securities Exchange top 50 company

• Market capitalisation of circa $8 billion

• Strong investment grade credit rating (BBB+)

• Operations in Australia and Singapore

2

Refresh Vision & Strategy

Capital Management

Growth

Value Chain Optimisation

Tabula Rasa

Ampol Singapore

Invest in Distribution Infrastructure

12

11

10

3

Supply Chain review

Business Model

Integrated Supply

Chain

Kurnell conversion

2010 2011 2012 2013 2014 2015 Beyond

4

5

3

6

7

8

9

10

Caltex Values

Establish Vision

Transport Fuels Leader

Measure of Success

TSR

2

1

9

A multi-year strategy to transform Caltex and drive Total Shareholder Returns (TSR)

Reduction in volatility of earnings and cash flow

• Conversion of Kurnell Refinery and financial risk management has reduced commodity price and FX volatility • Earnings are greater weighted to Caltex’s integrated supply and marketing of petroleum products

• Caltex has undertaken financial policy and operating model initiatives to substantially improve the quality and stability of its earnings and free cash flow

[dummy chart - data to follow]

Refining (Lytton) Refining (Lytton) Refining (Lytton) Refining (Lytton) Refining (Lytton)

Refining (Kurnell) Refining (Kurnell)

Price Timing Price Timing

Price TimingPrice Timing Price Timing

FXFX

FX

FX

Basis

Basis

Basis

2009 2010 2014 2015 2016

2 refineries +No Hedging

2 refineries +50% Hedge of FX

1 Refinery + 80% FX Hedging

1 Refinery + 80% FX Hedging +

Basis & Price Timing Hedging

1 Refinery + 100% FX Hedging

+ Basis & Price Timing Hedging

Cash Flow-at-Risk under different operating models – Illustrative Only

Other Commodity Risk1

Other Commodity Risk1

Other Commodity Risk1

FX Timing

FX Timing

FX TimingFX Timing

Other Commodity Risk1

Other Commodity Risk1

2017

1 Refinery + 80-100% FX Hedging + Basis & Improved Price

Timing Hedging

Pricing Timing

4

As Caltex has shifted its business model, investors recognise the de-risked cash flow profile, driving share price performance

5

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16

Reb

ased

to C

alte

x (A

$)

Caltex Share Price vs S&P/ASX100

ASX100 Caltex

22/8/2011Announcment of

27/2/2012Full yearresults release

16/12/2011Full year profit outlook'Flag of impairment'

31/7/2012Announcement of hybrid issue

26/7/2012Announcement of supply chain restructure

16/2/2012Caltex announces writedownof refinery assets

10/5/2012AGM advice that Kurnell weakest preformer

27/8/2012Half year results release

24/2/2014Flag Organisation reviewand Cost review

28/9/2012Confirmation that Kurnell will close in 2014

7/9/2012Strategy day- lower volatility- strength of marketing- focus on growth

20/6/2013Analyst Day at Lytton Refinery

27/6/2013Half year profit outlook- lower Marketing result

25/8/2014Annoucement of Tabular Rasa outcomes

1/10/2014Kurnell Refinery closure

Increased marketexpectations of

Source: Reuters as at 8 November 2016

23/2/20152014 results release- discussion on growth

27/3/2015Chevron announces sale of stake in Caltex

23/2/20162015 results release- discussion on growth

23/2/2016Off-market shareBuy-Back announced.

18/10/2016Confirms interest in WOW

2015 Strategy Update “Refresh Vision & Strategy”…whilst still aspiring for top quartile TSR

6

The Caltex supply chain

Crude + Products

sourced annually

~16bn litres

$9.2bn Infrastructure

(reinstatement cost)

~$20bn revenue

Commercial and Wholesale sales

Product delivery & inventory holding

Terminals, tankers, pipelines, depots,

airports, diesel stops, truck stops,

outlets and card

Lytton Refinery

Consumersales

Imported Crude & Product(Ampol Trading & Shipping)

Major fuel wholesalers (e.g. Viva, Mobil, BP)

Controlled Retail

Woolworths Caltex sites

Independent & branded resellers

Transport, Mining & Industrials

Other (lubricants, fuel oil)

Aviation

Other Australian refiners/

importers

Product sourcing Infrastructure Customer

Typically linked through buy-sell

agreements

Global suppliers/ counterparties

7

Caltex supply chain and risk

Transactions in USDSettlements in USD

Transactions in USD and AUDMajority of sales settled in AUD

Product cracks

Price timing

FXFreight

Product Basis Crude premiums

Product premiums

Caltex’s Supply Chain generates risk in a range of

categories

8

Ampol Singapore overview

• Established in late 2013, with ramp up of capabilities and activities during 2014 prior to closure of Kurnell refinery

• Activity in Ampol has increased significantly following the conversion of Kurnell in October 2014

• Ampol is now accountable for sourcing all crude, feedstock and refined product imports for Caltex

• Counterparties include refiners across the region, traders and integrated oil companies

• Ampol continues to expand and improve its capabilities to optimise the integrated value chain, and continue to evolve as a world class manager of complex supply chains, in line with the company strategy

Standalone Trading and Shipping

Product sourcing

9

Caltex footprint in AustraliaInfrastructure

10

CustomerCustomer

Controlled Retail

Woolworths Caltex sites

Independent & branded resellers

Transport, Mining & Industrials

Other (lubricants, bitumen & fuel oil)

Major fuel wholesalers (e.g.

Woolworths, Shell, Mobil, BP)

AviationCommercial

and Wholesale

sales

Consumersales

Caltex Service Station Retail Network • Caltex supplies 1,971 card accepting sites, including:

Caltex owned (477) or leased (319) 796 Dealer owned 653 Woolworths supplied 522

• Caltex’s controlled 796 sites are either company operated by Caltex (138 sites) or by a franchisee (645 sites)

• Caltex is one of Australia’s largest franchisors

11

Developing a comprehensive financial risk management framework

The role of Treasury in Australia and Singapore

Transformation of the business required a review of our financial risk management framework

• In 1H15 reviewed commodity risk management systems, governance and process controls

• In 1H16 implemented a revised commodity risk management operating model across Sydney and Singapore

• Capability, and improved systems, processes and policies were added

13

Jan to Apr 2015

Apr 2016

Jul 2016

Apr to Sept 2016 Dec 2016

Oct 2016Aug 2016Apr to Jul 2016Jan to Mar 2016May 2015 to present

PwC Review of commodity risk

framework

Proposed limitstructure andpolicy update

Policy and limitspresented to

Board for approvalDefine scenarios

Commodity risk improvementproject

Risk appetite andlimits projectlaunched +

commodity hedging commenced in Singapore

Design and build CFaR & VaR models

Established direct executionhedging capability

Modelling analysis

Board workshop

Establish key principles & agree

philosophical approach

CURRENTSTATUS

Nov 2015

Regional Treasury established

Commodity risk policies and limits now anchored in an overarching framework across all risks and linked to strategy

Developing a comprehensive financial risk management framework in 2016 has involved:

1) Aligning with Caltex strategy & positioning2) Establishing risk capacity3) Setting risk appetite4) Allocating risk 5) Setting risk tolerance6) Setting operating risk limits7) Building organisational capability8) Investment in financial systems 9) Revising the Group Treasury policy

Ultimately the enhancements to our Risk Management Framework, Systems and Capabilities will deliver increased certainty that risk is managed within our appetite, while enabling us to pursue strategy faster and with greater confidence.

14

Proposed risk limit structure

The following commodity sub-risk categories will be used for monitoring Commodity risk VaR on a day to day basis:- Outright price exposure (price timing)- Time spread exposure- Basis exposure- Other**

CAL – Overall Financial Risk CFaR limit

CAL – Commodity risk CFaR limit (excluding refining

margin)

CAL – Commodity risk VaR limit (excluding refining

margin & freight)

CAL – Volumetric (% of USD Notional) FX Limit

CAL – Interest rate risk volumetric limit (%floating

limit)

CAL – *Financial counterparty credit risk

exposure limit

Commodity risk sub-category management

guideline limits

Policy limits

Management guidelines

* The term “financial counterparties” refers to banks or other financial services providers. ** There may be other categories (e.g. premiums)

Commodity risk CFaR (inc. refining margin & freight), FX CFaR, Interest rate CFaR, *Financial

Counterparty credit CFaR

15

Caltex operates a centralised Group Treasury

• However for commodity price risk management, front office responsibilities rest with the Singapore Trading team• Our regional Treasury based in Singapore performs commodity risk analysis and oversight in a Middle Office role

CFO

Front Office

Middle Office

Back Office

Group Treasury

Ampol Trading & Shipping

Commodity Risk

Front Office

16

• One financial risk management policy• Cohesive risk management framework• Strategic alignment• Centralised decisions• Central funding planning and evaluation• Efficient cash/liquidity management• Key relationships (Banks, ratings agencies)• Effective use of financial risk systems and tools• Deeper subject matter expertise

Benefits of centralisation retained

Reduced volatility and improved risk management also enables prudent growth in Trading & Shipping

With the expansion in Ampol’s role and capabilities, the strategy and future development of the business is being placed in a carefully designed framework

TOP QUARTILE TSR IS THE OVERIDING OBJECTIVE

TRADING & SHIPPING STRATEGY

PILLARS

KEY EXECUTION ENABLERS

POLICIES & FINANCIAL RISK

APPETITE

STANDALONE PHYSICAL TRADING

STANDALONE SHIPPPING

COMMODITY RISK

MANAGEMENT

SKILLS & PEOPLEASSET &

CAPITAL BASE

RISK MANAGEMENT & OVERSIGHT

PHYSICAL SYSTEM

CFAR1 MODELS

RISK ALLOCATION

VAR

EXPOSURE MANAGEMENT(TIMING, BASIS, FX)

POLICYPROCESSES

REPORTING SYSTEMS

FUNDING LEVELSMONITORING SYSTEMS

SUPERVISIONDOA

EARNINGS GROWTH

SYSTEM BACKED

USE OF HEDGING

KEY RISK TOOLS

STRATEGY IS SUBJECT TO HAVING…

STRATEGY IS SUBJECT TO HAVING…UNDERPINNED BY…

AMPOL IS A GROWTH DRIVER…

MULTIPLE EXPANSION CAPITAL RETURNS++ + INVESTOR ENGAGEMENT

17

Questions?