Embed Size (px)

DESCRIPTION

Treasury Deep Dive Forex Business Case V1

Citation preview

1

© 2013 IBM Corporation

Course Name – Treasury -Forex

Module Name – Treasury -Forex

© 2013 IBM CorporationModule Name2

Use this topic start slide when starting a new topic.

Topic #: Foreign Currency

2

© 2013 IBM CorporationModule Name3

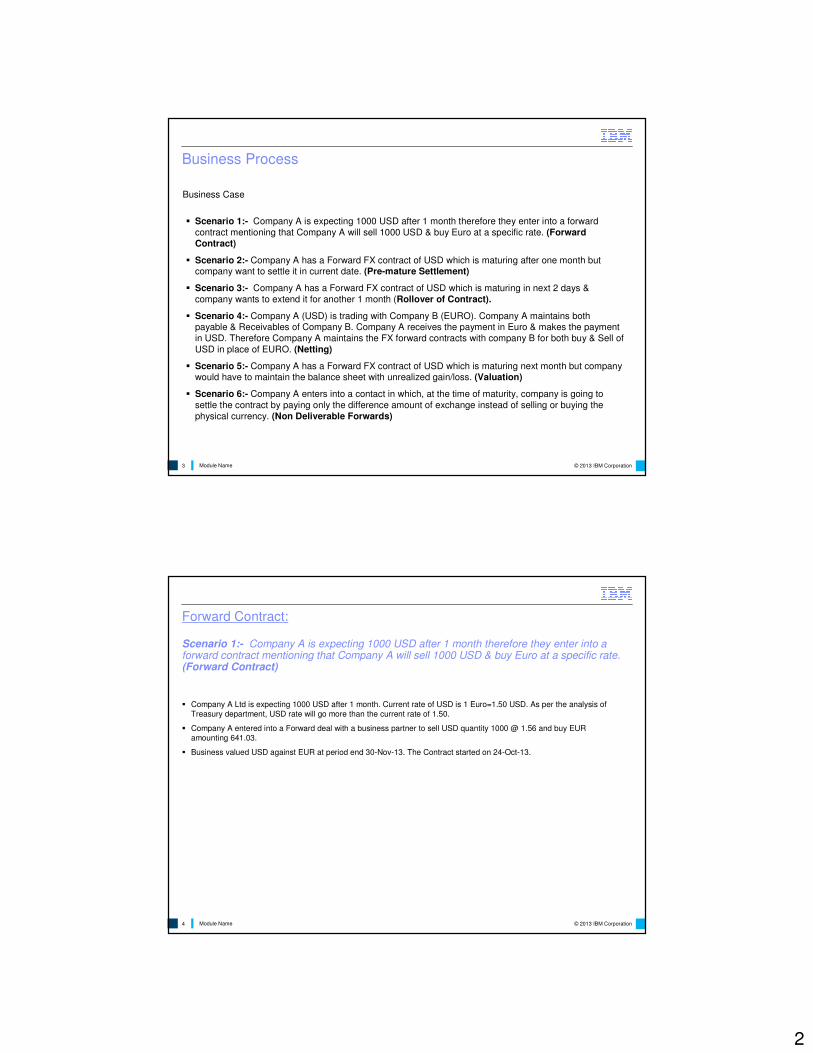

Business Process

Business Case

� Scenario 1:- Company A is expecting 1000 USD after 1 month therefore they enter into a forward

contract mentioning that Company A will sell 1000 USD & buy Euro at a specific rate. (Forward

Contract)

� Scenario 2:- Company A has a Forward FX contract of USD which is maturing after one month but company want to settle it in current date. (Pre-mature Settlement)

� Scenario 3:- Company A has a Forward FX contract of USD which is maturing in next 2 days &

company wants to extend it for another 1 month (Rollover of Contract).

� Scenario 4:- Company A (USD) is trading with Company B (EURO). Company A maintains both payable & Receivables of Company B. Company A receives the payment in Euro & makes the payment

in USD. Therefore Company A maintains the FX forward contracts with company B for both buy & Sell of

USD in place of EURO. (Netting)

� Scenario 5:- Company A has a Forward FX contract of USD which is maturing next month but company would have to maintain the balance sheet with unrealized gain/loss. (Valuation)

� Scenario 6:- Company A enters into a contact in which, at the time of maturity, company is going to

settle the contract by paying only the difference amount of exchange instead of selling or buying the

physical currency. (Non Deliverable Forwards)

© 2013 IBM CorporationModule Name4

Forward Contract:

Scenario 1:- Company A is expecting 1000 USD after 1 month therefore they enter into a forward contract mentioning that Company A will sell 1000 USD & buy Euro at a specific rate. (Forward Contract)

� Company A Ltd is expecting 1000 USD after 1 month. Current rate of USD is 1 Euro=1.50 USD. As per the analysis of

Treasury department, USD rate will go more than the current rate of 1.50.

� Company A entered into a Forward deal with a business partner to sell USD quantity 1000 @ 1.56 and buy EUR

amounting 641.03.

� Business valued USD against EUR at period end 30-Nov-13. The Contract started on 24-Oct-13.

3

© 2013 IBM CorporationModule Name5

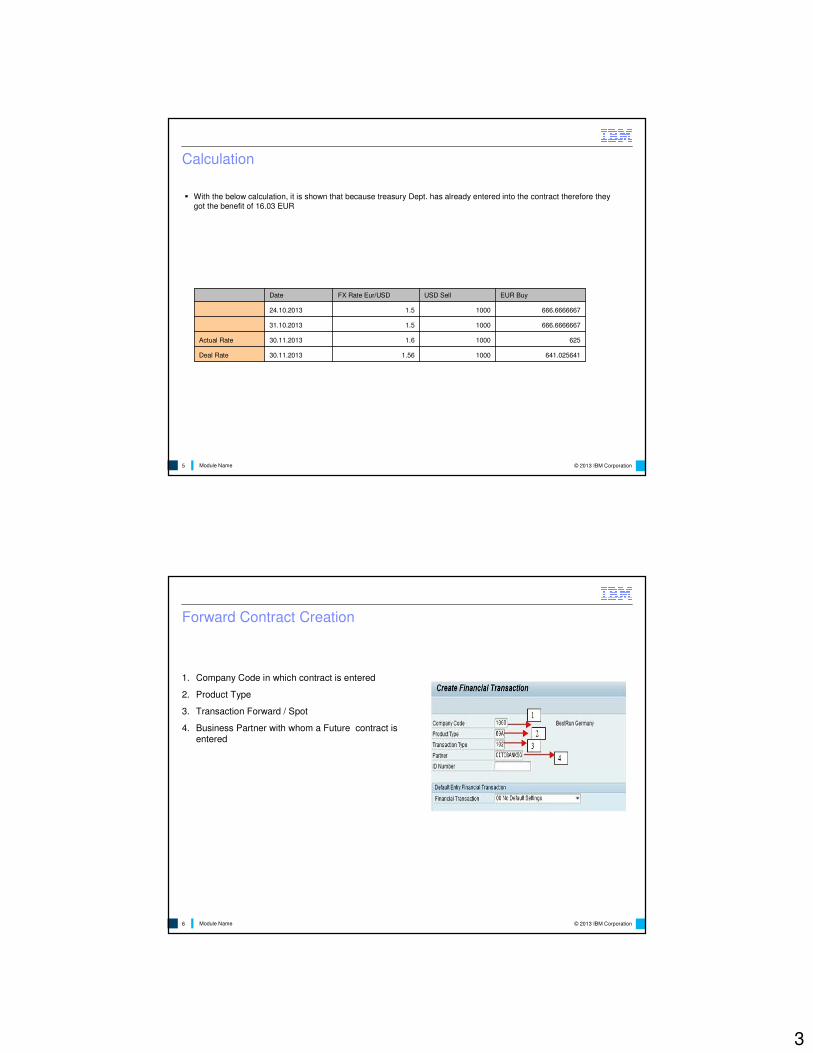

Calculation

641.02564110001.5630.11.2013Deal Rate

62510001.630.11.2013Actual Rate

666.666666710001.531.10.2013

666.666666710001.524.10.2013

EUR BuyUSD SellFX Rate Eur/USDDate

� With the below calculation, it is shown that because treasury Dept. has already entered into the contract therefore they

got the benefit of 16.03 EUR

© 2013 IBM CorporationModule Name6

Forward Contract Creation

1. Company Code in which contract is entered

2. Product Type

3. Transaction Forward / Spot

4. Business Partner with whom a Future contract is entered

4

© 2013 IBM CorporationModule Name7

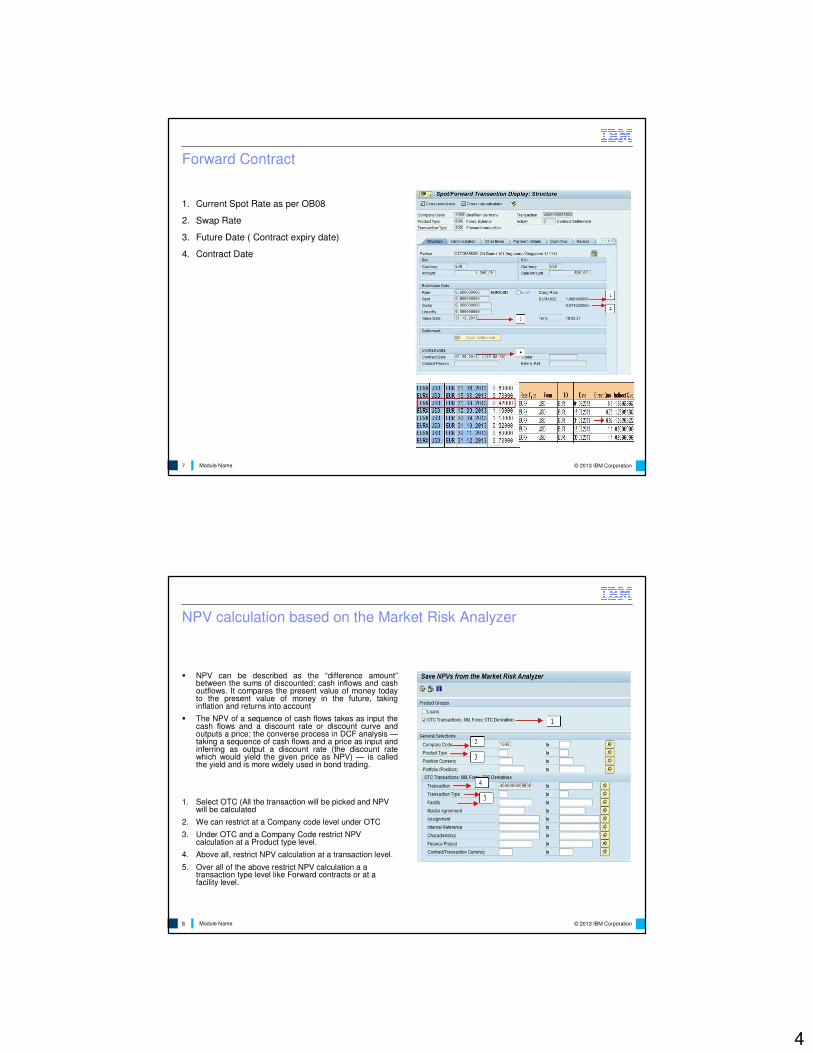

Forward Contract

1. Current Spot Rate as per OB08

2. Swap Rate

3. Future Date ( Contract expiry date)

4. Contract Date

© 2013 IBM CorporationModule Name8

NPV calculation based on the Market Risk Analyzer

� NPV can be described as the “difference amount”between the sums of discounted: cash inflows and cash outflows. It compares the present value of money today to the present value of money in the future, taking inflation and returns into account

� The NPV of a sequence of cash flows takes as input the cash flows and a discount rate or discount curve and outputs a price; the converse process in DCF analysis —taking a sequence of cash flows and a price as input and inferring as output a discount rate (the discount rate which would yield the given price as NPV) — is called the yield and is more widely used in bond trading.

1. Select OTC (All the transaction will be picked and NPV will be calculated

2. We can restrict at a Company code level under OTC

3. Under OTC and a Company Code restrict NPV calculation at a Product type level.

4. Above all, restrict NPV calculation at a transaction level.

5. Over all of the above restrict NPV calculation a a transaction type level like Forward contracts or at a facility level.

5

© 2013 IBM CorporationModule Name9

NPV calculation based on the Market Risk Analyzer…contd

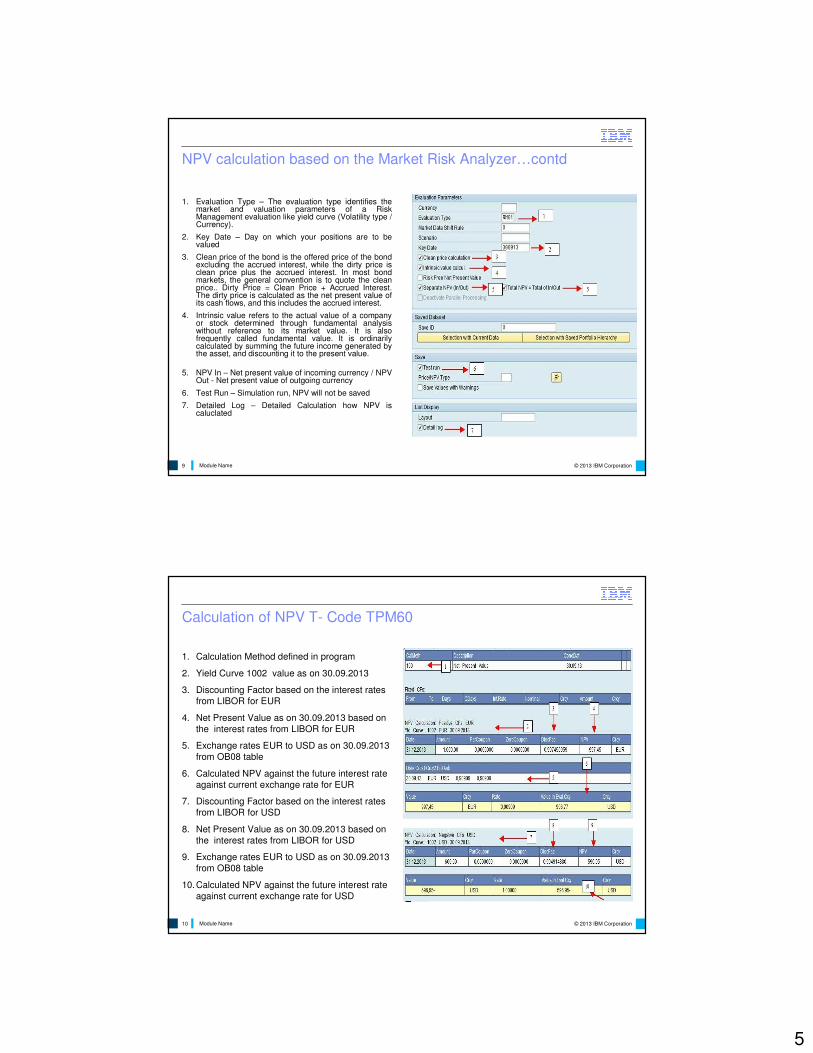

1. Evaluation Type – The evaluation type identifies the market and valuation parameters of a Risk Management evaluation like yield curve (Volatility type / Currency).

2. Key Date – Day on which your positions are to be valued

3. Clean price of the bond is the offered price of the bond excluding the accrued interest, while the dirty price is clean price plus the accrued interest. In most bond markets, the general convention is to quote the clean price.. Dirty Price = Clean Price + Accrued Interest. The dirty price is calculated as the net present value of its cash flows, and this includes the accrued interest.

4. Intrinsic value refers to the actual value of a company or stock determined through fundamental analysis without reference to its market value. It is also frequently called fundamental value. It is ordinarily calculated by summing the future income generated by the asset, and discounting it to the present value.

5. NPV In – Net present value of incoming currency / NPV Out - Net present value of outgoing currency

6. Test Run – Simulation run, NPV will not be saved

7. Detailed Log – Detailed Calculation how NPV is caluclated

© 2013 IBM CorporationModule Name10

Calculation of NPV T- Code TPM60

1. Calculation Method defined in program

2. Yield Curve 1002 value as on 30.09.2013

3. Discounting Factor based on the interest rates

from LIBOR for EUR

4. Net Present Value as on 30.09.2013 based on

the interest rates from LIBOR for EUR

5. Exchange rates EUR to USD as on 30.09.2013

from OB08 table

6. Calculated NPV against the future interest rate

against current exchange rate for EUR

7. Discounting Factor based on the interest rates

from LIBOR for USD

8. Net Present Value as on 30.09.2013 based on

the interest rates from LIBOR for USD

9. Exchange rates EUR to USD as on 30.09.2013

from OB08 table

10.Calculated NPV against the future interest rate

against current exchange rate for USD

6

© 2013 IBM CorporationModule Name11

Execute Valuation T-code TPM1

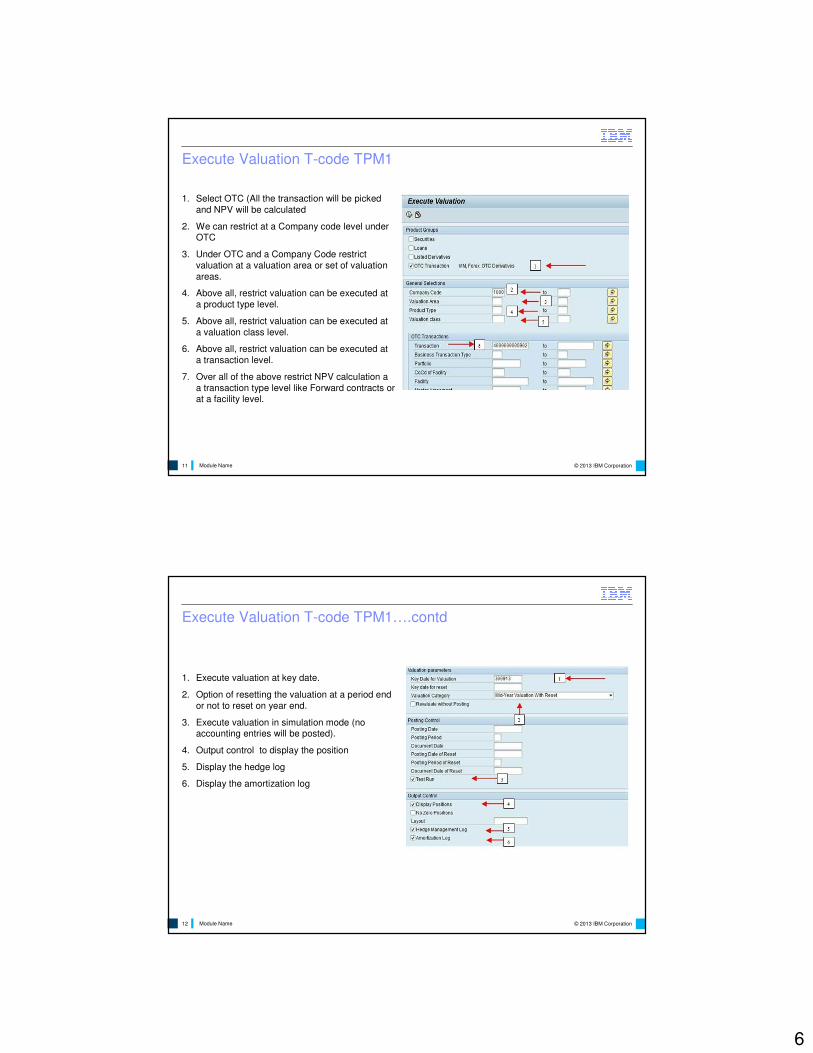

1. Select OTC (All the transaction will be picked

and NPV will be calculated

2. We can restrict at a Company code level under OTC

3. Under OTC and a Company Code restrict

valuation at a valuation area or set of valuation

areas.

4. Above all, restrict valuation can be executed at

a product type level.

5. Above all, restrict valuation can be executed at

a valuation class level.

6. Above all, restrict valuation can be executed at

a transaction level.

7. Over all of the above restrict NPV calculation a

a transaction type level like Forward contracts or at a facility level.

© 2013 IBM CorporationModule Name12

Execute Valuation T-code TPM1….contd

1. Execute valuation at key date.

2. Option of resetting the valuation at a period end

or not to reset on year end.

3. Execute valuation in simulation mode (no accounting entries will be posted).

4. Output control to display the position

5. Display the hedge log

6. Display the amortization log

7

© 2013 IBM CorporationModule Name13

Valuation Log of TPM1

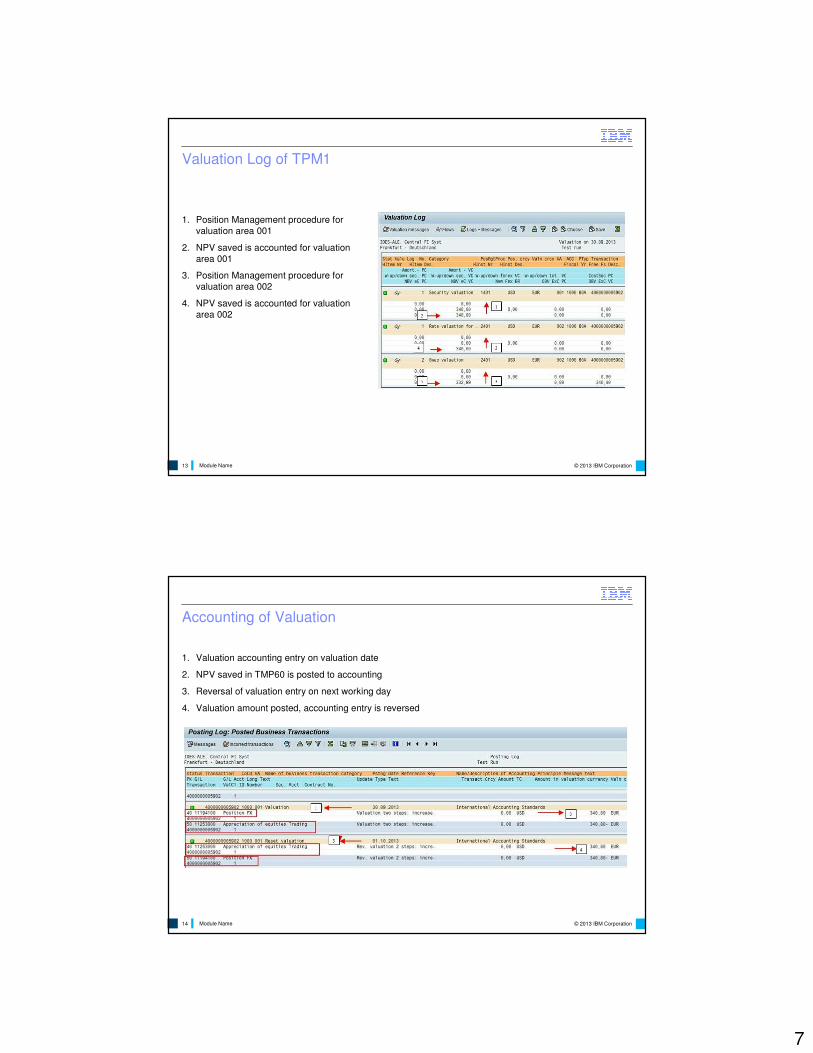

1. Position Management procedure for

valuation area 001

2. NPV saved is accounted for valuation

area 001

3. Position Management procedure for

valuation area 002

4. NPV saved is accounted for valuation

area 002

© 2013 IBM CorporationModule Name14

Accounting of Valuation

1. Valuation accounting entry on valuation date

2. NPV saved in TMP60 is posted to accounting

3. Reversal of valuation entry on next working day

4. Valuation amount posted, accounting entry is reversed

8

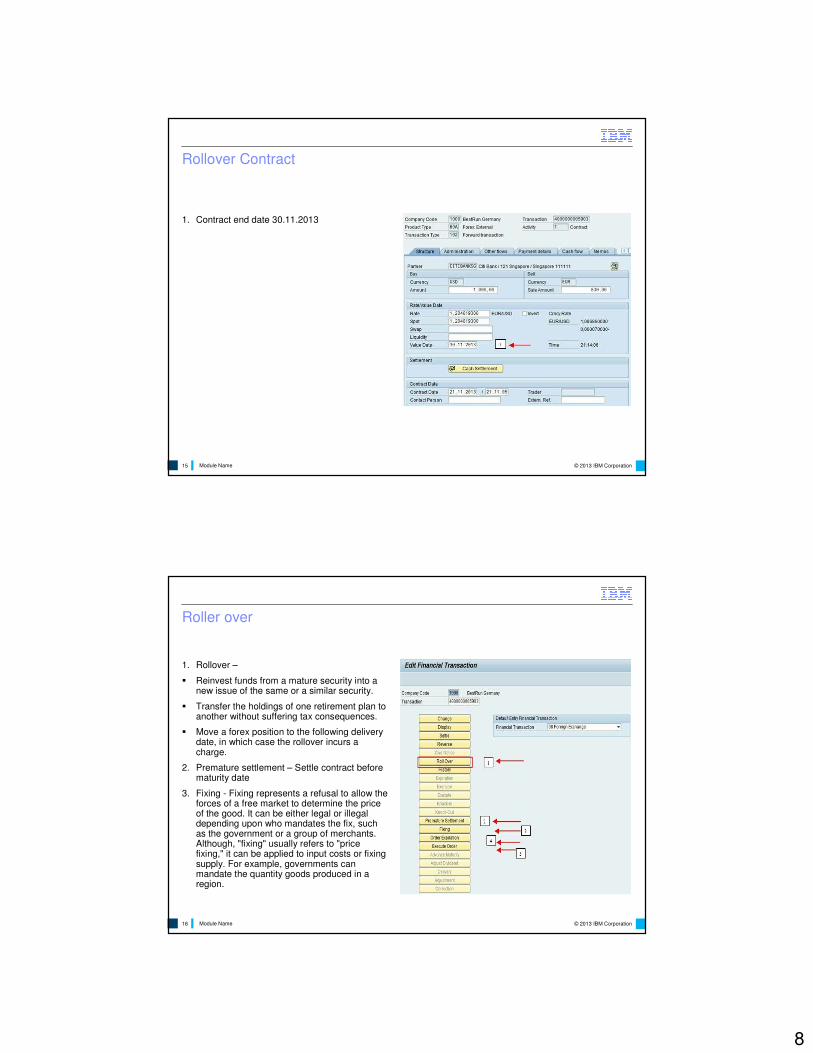

© 2013 IBM CorporationModule Name15

Rollover Contract

1. Contract end date 30.11.2013

© 2013 IBM CorporationModule Name16

Roller over

1. Rollover –

� Reinvest funds from a mature security into a new issue of the same or a similar security.

� Transfer the holdings of one retirement plan to another without suffering tax consequences.

� Move a forex position to the following delivery date, in which case the rollover incurs a charge.

2. Premature settlement – Settle contract before maturity date

3. Fixing - Fixing represents a refusal to allow the forces of a free market to determine the price of the good. It can be either legal or illegal depending upon who mandates the fix, such as the government or a group of merchants. Although, "fixing" usually refers to "price fixing," it can be applied to input costs or fixing supply. For example, governments can mandate the quantity goods produced in a region.

9

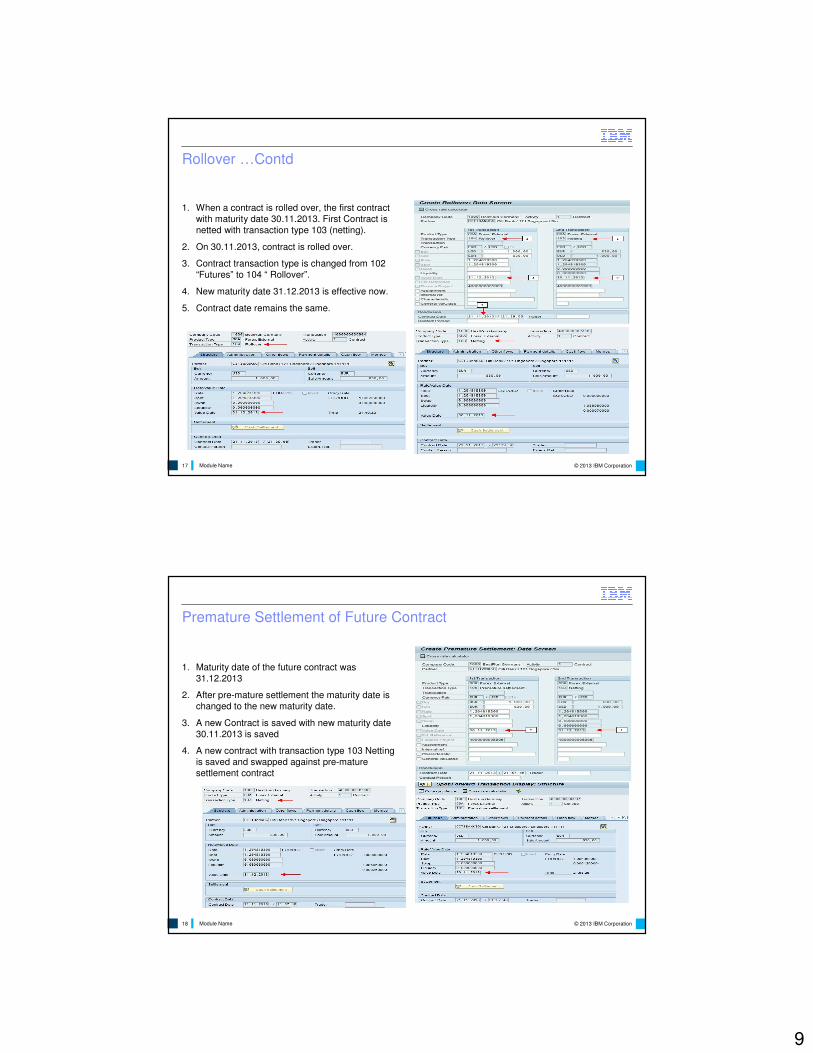

© 2013 IBM CorporationModule Name17

Rollover …Contd

1. When a contract is rolled over, the first contract

with maturity date 30.11.2013. First Contract is

netted with transaction type 103 (netting).

2. On 30.11.2013, contract is rolled over.

3. Contract transaction type is changed from 102

“Futures” to 104 “ Rollover”.

4. New maturity date 31.12.2013 is effective now.

5. Contract date remains the same.

© 2013 IBM CorporationModule Name18

Premature Settlement of Future Contract

1. Maturity date of the future contract was

31.12.2013

2. After pre-mature settlement the maturity date is

changed to the new maturity date.

3. A new Contract is saved with new maturity date

30.11.2013 is saved

4. A new contract with transaction type 103 Netting

is saved and swapped against pre-mature

settlement contract

10

© 2013 IBM CorporationModule Name19

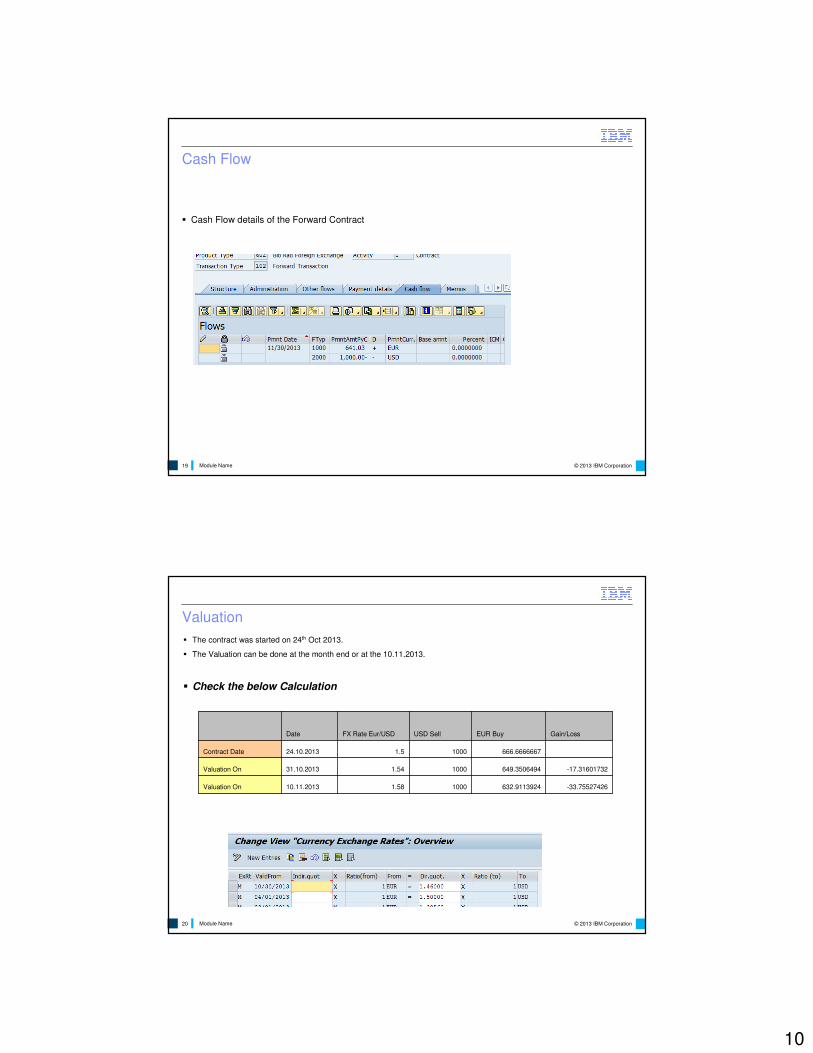

Cash Flow

� Cash Flow details of the Forward Contract

© 2013 IBM CorporationModule Name20

Valuation

� The contract was started on 24th Oct 2013.

� The Valuation can be done at the month end or at the 10.11.2013.

� Check the below Calculation

-33.75527426632.911392410001.5810.11.2013Valuation On

-17.31601732649.350649410001.5431.10.2013Valuation On

666.666666710001.524.10.2013Contract Date

Gain/LossEUR BuyUSD SellFX Rate Eur/USDDate

11

© 2013 IBM CorporationModule Name21

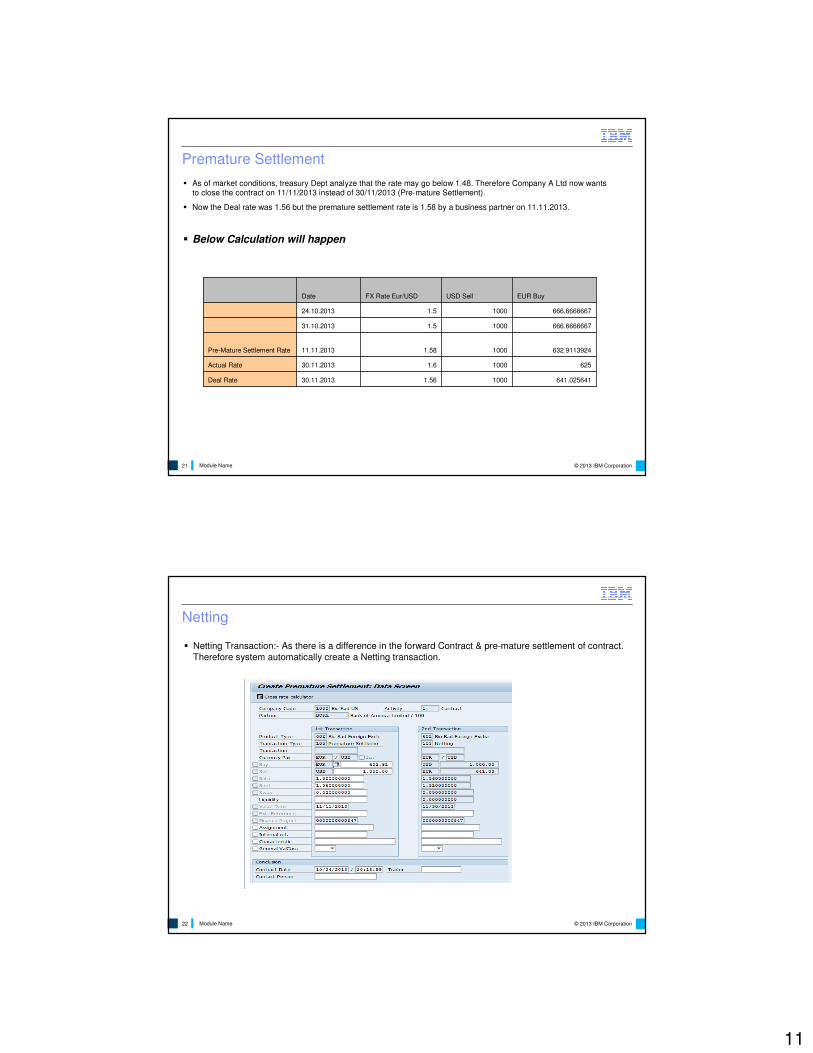

Premature Settlement

� As of market conditions, treasury Dept analyze that the rate may go below 1.48. Therefore Company A Ltd now wants to close the contract on 11/11/2013 instead of 30/11/2013 (Pre-mature Settlement).

� Now the Deal rate was 1.56 but the premature settlement rate is 1.58 by a business partner on 11.11.2013.

� Below Calculation will happen

641.02564110001.5630.11.2013Deal Rate

62510001.630.11.2013Actual Rate

632.911392410001.5811.11.2013Pre-Mature Settlement Rate

666.666666710001.531.10.2013

666.666666710001.524.10.2013

EUR BuyUSD SellFX Rate Eur/USDDate

© 2013 IBM CorporationModule Name22

Netting

� Netting Transaction:- As there is a difference in the forward Contract & pre-mature settlement of contract.

Therefore system automatically create a Netting transaction.