Embed Size (px)

DESCRIPTION

Transportation, Distribution & Logistics September 2004. Our Industry - Truckload. Source: American Trucking Association. $ in billions. Celadon is the tenth largest truckload carrier Point to point service with no intermediate handling of freight Demand growing 5% to 6% annually - PowerPoint PPT Presentation

Citation preview

Transportation, Distribution & Logistics September 2004

2

Our Industry - Truckload

Dry Van; $6150%

Temp Controlled; $87%

Intermodal; $97% Flatbed; $5

4% Specialized; $2621%

Misc.; $1411%

$ in billions Source: American Trucking Association

Celadon is the tenth largest truckload carrier Point to point service with no intermediate handling of freight Demand growing 5% to 6% annually Non-union

3

Truckload Industry2001 - 2004

Industry dynamics 15% of all fleets failed

Difficulty in obtaining insurance High fuel cost Lack of financing

Production of class 8 trucks declined 1998-2000 240,000 per year average 2001-2003 140,000 per year average 2004 250,000 - replacements

Barriers to entry - No new company start-ups Inability to obtain insurance High fuel cost Shortage of drivers Cost of technology

4

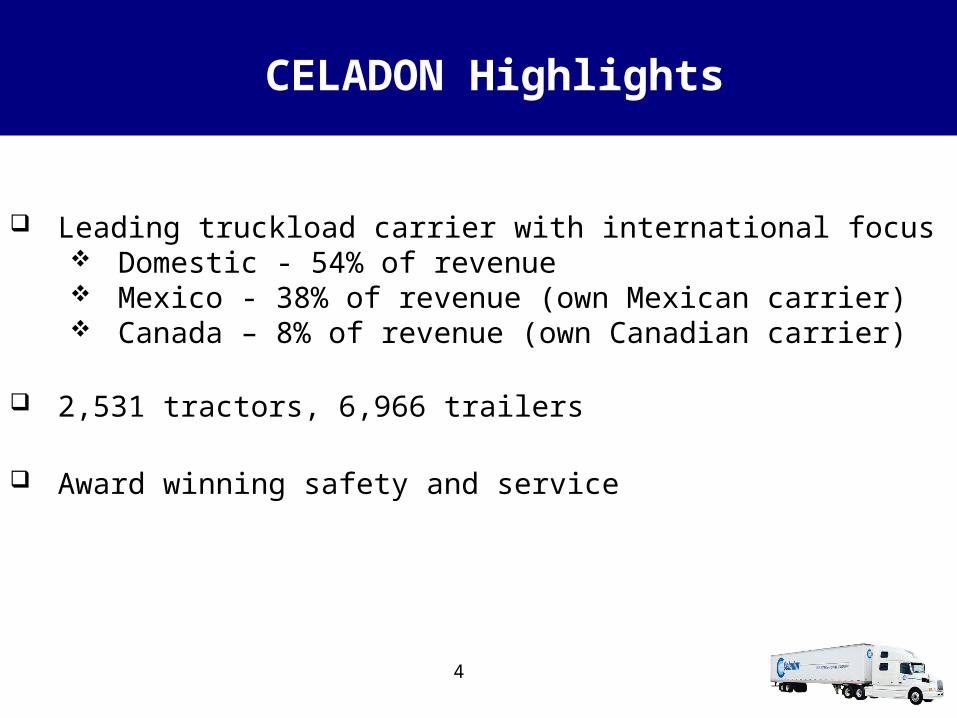

CELADON Highlights

Leading truckload carrier with international focus Domestic - 54% of revenue Mexico - 38% of revenue (own Mexican carrier) Canada – 8% of revenue (own Canadian carrier)

2,531 tractors, 6,966 trailers

Award winning safety and service

5

• REGULATORY EXPERTS –Pre-Deregulation– ABILITY TO DECIPHER GOVERNMENT REGULATIONS

• NEGOTIATORS – Post-Deregulation– SKILLED AT FINDING LOW COST PROVIDER

• SOPHISTICATED LOGISTICIANS – 1990’S to Present– Optimal mix of modes

– Sourcing Raw Materials

– Order Frequency

– Locating Plant & Distribution Centers

– Systems Development

SKILLS TRANSITION

6

• MARKETING

• SYSTEMS DEVELOPMENT

• SALES TRAINING

• ENGINEERING

• FACILITY MANAGEMENT

WORKFORCE SKILLS