Embed Size (px)

Citation preview

Transparency and Political Moral HazardAuthor(s): M. Kadir DoganSource: Public Choice, Vol. 142, No. 1/2 (Jan., 2010), pp. 215-235Published by: SpringerStable URL: http://www.jstor.org/stable/40541956 .

Accessed: 10/06/2014 01:47

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Springer is collaborating with JSTOR to digitize, preserve and extend access to Public Choice.

http://www.jstor.org

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

Public Choice (2010) 142: 215-235 DOI 10.1007/sl 1127-009-9485-0

Transparency and political moral hazard

M. Kadir Dogan

Received: 7 December 2007 / Accepted: 14 July 2009 / Published online: 14 August 2009 © Springer Science+Business Media, LLC 2009

Abstract This paper analyzes the effects of asymmetric information on the public control of politicians in a world where the politicians' pre-election promises are not credible. We study a model with identical politicians and a representative voter whose interests conflict with those of the politicians'. The voter's decision to reelect the politician depends on both observable policies of the politician and the outcome of the unobservable policies. In equi- librium, either optimal decisions for the voter are not taken by the politician or if taken, the politician would extract more rent. In the latter case, politicians are also replaced more frequently.

Keywords Political Agency; Elections; Asymmetric Information

1 Introduction

In electoral competition, politicians run on a platform and make campaign promises. In turn, the electorate votes for the candidate whose platform they prefer. Once elected, politicians may behave as though they forget these campaign promises. In general, there are no legal remedies to enforce these promises. If the politician does not keep his promises, he loses his reputation and the electorate will not trust his promises in the future campaigns (Hinich and Munger 1994, pp. 74-75). However, if the politician's interests differ from those of the pub- lic (for example, the politician may simply be an office-seeker1 or the policies he puts forth may be contrary to what the public wants),2 then he may announce the campaign platform to maximize his votes and break his promises without considering his reputation after the

M.K. Dogan (El) Faculty of Political Sciences, Ankara University, Ankara, Turkey e-mail: [email protected] 1 Harrington (2000) shows an electoral model which results in pure office-seeking politicians looking like ideologues. 2 See Bender and Lott (1996) for a review of the literature on the role of ideology and the failure by the legislator to act in the interests of his constituents in legislator voting.

fi Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

216 Public Choice (2010) 142: 215-235

election. In such an environment, the voters will not pay any attention to the platform that the politicians advocate, so the campaign promises are not credible.

Political moral hazard arises as a consequence of two features. First, according to the constitutional provisions,3 the politician has the authority to apply his policies for a certain interval of time between the elections. He obtains that power from the public in the elections. Second, there is asymmetric information between the politician and the public. In many cases, people do not have access to all the decisions the politician makes.

The next election can be used as a mechanism to control the politicians. If electors vote by reflecting on the policies or the outcome during previous periods, then the politician may apply policies that satisfy the electorate and consequently not lose, although he may disagree with those policies.

The research on the public control of the politicians can be separated into two parts according to the transparency of the politician's policies. In the first part of the literature, it is assumed that the politician's policies are observed by the electorate; the voter's decision to reelect the politician therefore depends on the policies he has chosen (Barro 1973; Rogoff and Sibert 1988; Rogoff 1990). For example, Barro (1973) demonstrated that elections can be employed as a device to control politicians in a complete information environment. The decision of the voters to reelect the politician depends only on the politician's past policies and, in equilibrium, politicians get some rent for having the authority to apply their policies. In Rogoff (1990) the incumbent chooses the fiscal policy and his ability to produce the public good is private information. In equilibrium, the reelection decision of the politician depends on the past policy of the politician and is independent of the outcome of the policy.

In the second part of the literature, it is assumed that the politician's policies are not ob- served by the electorate and the decision to reelect the politician consequently cannot depend on the past policies; it depends on the outcome of the policies (Ferejohn 1986; Austen-Smith and Banks 1989; Alesina and Cukierman 1990; Banks and Sundaram 1993, 1998; Persson et al. 1997; Persson and Tabellini 2000: chapters four and nine). For example, in Ferejohn (1986) the electorate's utility depends on both the policy of the politician and the realiza- tion of a random variable. The politician observes the realization of a random variable and chooses the policy accordingly. The electorate observes only their utility and, in equilib- rium, if it is more than a threshold value, they reelect the politician. The politician obtains rent from both having the authority to apply his policy and having superior information to the electorate. Banks and Sundaram (1993, 1998) discussed a model in which the politician and the opponents differ according to their competency and the politician acts before uncer- tainty is resolved. They show the existence of equilibrium where the politician is reelected if and only if the outcome of the policies is greater than a cut-off level.4 In Alesina and Cukierman (1990) the voters have incomplete information on the politician's policy pref- erences. The electorate updates its information on the politician's preferences by observing the outcome. In those models, since the electorate does not observe the politician's actions, the reelection decision depends on the result of the policies.

Harrington (1993) discussed a two-period model in which the reelection decision of the politician depends on both the politician's policy and the outcome of the policy in equilib- rium. The politician chooses a policy in each period and the realized income is a noisy signal

3 See Laffont (2000) for a study of how the Constitution should be designed to give incentives to the politicians in order to maximize the social welfare. 4In Banks and Sundaram (1998) the politician can be elected only two periods, whereas there is no term limit in Banks and Sundaram (1993). Fearon (1999) has a similar model which ends in two periods. The reelection decision of the politician depends only on his performance at the end of the first period.

<ö Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

Public Choice (2010) 142: 215-235 217

of that policy. The voters observe the implemented policy, but they have different belief con- cerning the efficiency of the policy. Also, the politician has a type according to his belief on the efficiency of the policy. In that setting, since the realized income releases information about the type of the politician, in equilibrium, reelection of the politician depends on both the politician's policy and the level of realized income.

We develop here an alternative theory of public control of politicians. We have an infinite horizon principal-agent model with homogeneous politicians and a representative voter. In any period, there is an elected politician who chooses a two-dimensional policy that affects the voter's welfare. The politician's policy consists of a tax policy and an investment policy. His payoff increases in collected tax and decreases with the level of investment. The voter can observe the tax policy, but she is not able to observe the investment policy that stochasti- cally affects the income of the voter. The voter has a higher expected income if the politician invests more. The voter enjoys her net income, which is her income minus the tax that she pays. The model captures the conflict of interest between the politician and the voter. The politician wants to collect more tax and to invest less, whereas conversely, the voter wants him to collect less tax and to invest more.

The essential feature of the model is that it allows some of the politician's policies (tax policy) to be observable to the voter and some (investment policy) not to be observable. Hence, the voter uses a retrospective decision rule for reelection of the politician that de- pends not only on the results of the politician's unobservable policies, but also on his ob- servable policies. On this account, this paper combines the two lines of the literature which are separated according to the transparency of the politician's policies.

In a model with only a transparent policy of the politician, there is one type of equilibrium in stationary strategies. In this equilibrium, the politician gets some rent due to having the authority to apply the policy and is never replaced (e.g., Barro 1973). In a model with only a non-transparent policy of the politician, again there is one type of equilibrium in stationary strategies. In this equilibrium, the politician gets some rent due to having the authority to apply the policy and some rent due to asymmetric information. The politician is reelected with some probability depending on the realization of a random variable (e.g., Ferejohn 1986; Persson et al. 1997). However, in our model, there are two types of equilibria in stationary strategies. Depending on the effect of the politician's unobserved policy on the welfare of the voter and the politician, the power of the politician (the maximum tax that he can collect from the voter), and the politician's discount rate for future payoffs, one of these two types exists. In the first type of equilibrium, the politician does not invest, collects a low tax, gets some rent due to having the authority to apply the policy and is never replaced. In the second type of equilibrium, the politician invests, collects more tax and extracts more rent each period compared to the first type, and is replaced with positive probability.

We show that the politician may not make the optimal decisions for the voter in a non- transparent political system. Even if the politician makes the optimal decisions for the voter, he extracts more rent each period and is replaced more frequently. It is generally believed that an increase in the transparency of the political system makes the voter better off and the politician worse off.5 The politician therefore prefers the political system to be less transpar- ent, whereas the voter prefers it to be more transparent. Our results imply that an increase in

5For example, in Ferejohn (1986), Persson et al. (1997), Persson and Tabellini (2000, chapter four), the politician chooses his policy after the uncertainty resolved, and therefore the reelection of the politician depends on his policy with certainty. By choosing the policy, the politician either stays at the office and gets some information rent or leaves the office and gets the maximum rent he can reach. Consequently, the politician has a higher expected payoff under asymmetric information.

4jj Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

218 Public Choice (2010) 142: 215-235

the transparency of the political system increases the voter's payoff, but may have no effect on the politician's payoff. The reasoning for no change in the politician's payoff goes as fol- lows. When transparency increases, the politician extracts less rent each period while in the office, so his per-period payoff decreases. On the other hand, the politician's probability of being reelected for the next period increases and consequently his expected payoff from fu- ture periods increases. We show that when transparency increases, the negative effect of the reduction in the politician's per-period payoff on his lifetime payoff may cancel the positive effect of the increase in the probability of being reelected on his lifetime payoff. Therefore, a reform that would make the political system more transparent should be supported by the public and may also be welcomed by the politician.

The outline of the paper is as follows. In Sect. 2, we present the model. In Sect. 3, we consider the case of a transparent political system. In Sect. 4, we consider the case of a non-transparent political system. Section 5 demonstrates the welfare effects of asymmetric information. And finally, Sect. 6 concludes. All the proofs are relegated to Appendix A.

2 Model

There is one elected politician and one representative voter. The politician's investment in- creases the voter's expected income. The voter cannot observe whether the politician invests. Because of the informational asymmetry between the politician and the voter, a moral hazard problem arises.

The politicians and the voter are infinitely lived and the politician of the first period is elected at the end of period 0. Note that by saying "the politician", we mean the incumbent politician. In each period t > 1 , the politician chooses a two-dimensional policy: a tax policy and an investment policy. The payoff of the politician in period t is given by (τ, - /,), where τ, is the tax collected and /, is the amount of investment. We assume that τ, € [0, Y]. The politician can collect any positive amount of tax less than or equal to T, which is the maximum allowable tax level.6 For simplicity, we assume that It e {0, /}. The politician can invest either zero or some fixed positive level of / > 0. Hence, the cost of investment for the politician is equal to /. That is, the politician's payoff will decrease by / if he invests, and the politician must therefore trade this off against an increase in the probability of reelection. The politician discounts the future payoffs by a discount factor 8 < 1. In any period, if the politician loses an election, he is never reelected and his outside payoff is zero. We also assume that when there is an election, there exists at least one previously unelected opponent for the politician. The politician and his opponents are identical in terms of abilities and preferences. Thus the only reason for removing the politician from the office is to punish him ex post. Since the politicians and his opponents are identical it is (weakly) optimal for the voter to apply this punishment.

In each period, the voter observes the tax policy of the politician, but she cannot observe the investment policy. At the end of each period, there is an election and the voter may reelect the politician or his opponent for the next period. The payoff of the voter in period t is her net income, which is equal to (yt - τ,). yt e [0, y] is the income of the voter in period i, which is affected by the investment decision of the politician for that period.7 The

6Adserà et al. (2003, p. 481) state that there are two main factors affecting the maximum allowable tax level. First, Τ declines with the use of democratic procedures to elect the politician. Second, an economic structure with more diversified resources and/or low specificity of the assets should reduce T. 7 For simplicity, we assume that the investment amount in period / affects the income of the voter only in period /.

Ô Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

Public Choice (2010) 142: 215-235 219

voter has a higher expected income if the politician invests. Let f(yt 'It) be the conditional probability density function and F(yt | It ) be the conditional cumulative distribution function of the voter's income in period t.

We make three assumptions about the conditional probability density function. First, we assume that f(yt'It) > 0 for all yt e [0, J] and /, e {0, /}. Thus, any potential realization of yt can arise from any investment decision by the politician. The second assumption is the following.

[f ytfiyt I /) dyt - j ytf(yt |0) dyt] > I

This assumption implies that the expected benefit of the voter under the investment decision is more than the cost of investment. The investment decision of the politician therefore is optimal for the voter. The third assumption is that the densities have the strict monotone likelihood ratio property (strict MLRP, defined in Milgrom 1981).

- is strictly increasing in yt . /(y,|0)

As yt increases, the likelihood of getting income level yt if the politician invests relative to the likelihood if the politician does not invest is strictly increasing.

The model creates an obvious conflict of interests between the politician and the voter. The politician prefers to collect more tax and not to invest, whereas the voter prefers to pay less tax and that the politician invests.

The sequence of the events is as follows. In each period t > 1 :

1. The voter chooses a strategy whether to reelect the politician conditional on her informa- tion set before the election that will be revealed at the end of period t .

2. The politician chooses the tax policy and the investment policy. 3. The income of the voter is drawn from a distribution that depends on the investment

policy of the politician. 4. The election is held and the voter decides whether to reelect the politician according to

her strategy.

Our equilibrium concept is the subgame perfect equilibrium in pure strategies. The strate- gies of the players are as follows. Let W denote the set of all possible histories through period t. In period i, the politician's strategy pt = (τ,, /,) : Ζ/'"1 -► [0, Τ] χ {0, /} maps the set of all possible histories prior to period t into a policy. In period t, the voter's strategy Ht : H'~l χ [0, Ψ] χ [0, J] ->► {0, 1} maps the set of all possible histories prior to period i, the tax policy of the politician, and the income level into a decision: the voter reelects the politician (1) or removes the politician from the office by electing his opponent(O).

We restrict attention to the stationary subgame perfect equilibria (SSPE). This requires that players act identically and optimally when faced with identical continuation games, and hence imply history-independent strategies. In period t, the voter's strategy xt can depend only on the (rt1yt).

Definition 1 The voter's stationary strategy is defined to be monotone if it is such that if the voter reelects the politician in any period when the realized income is y and collected tax is τ for any τ e [0, τ], then she reelects the politician in that period also for any realization of income y ' > y when the politician collects the tax τ .

Ô Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

220 Public Choice (2010) 142: 215-235

In a monotone stationary strategy, in every period the voter reelects the politician if and only if her income is higher than some threshold level for a given tax level.

Proposition 1 Any SSPE outcome can be generated by an SSPE with monotone strategies.

The proposition implies that in any SSPE, either the voter's strategy is monotone or there exists another SSPE with monotone strategies, and the politician's policy and the voter's reelection decision both are identical in these two equilibria. Therefore, we can derive all the outcomes of SSPE by focusing solely on SSPE with monotone strategies.

Formally, any monotone stationary strategy of the voter can be represented by using a function g : [0, ?] -> [0, y] as follows.

χ : "x = 1 if y > #(τ) and κ = 0 if y < #(τ) in any period"

The threshold level of income in strategy κ is g (τ). For any arbitrary tax level τ, in any period, the politician is reelected if and only if the voter's realized income is greater than or equal to g (τ).

The politician's stationary strategy ρ is choosing a policy (τ, /) in every period. Let a(p'x) be the probability of being reelected for the politician when his strategy is ρ and the voter's strategy is x.

cc(p'x) = Γ f(y'I)dy Jg(T)

= l-F(g(T)'I) (1)

The left-hand side of (1), a(p'x), is simply the probability of having income greater than or equal to the threshold value determined by the voter's strategy. Let U(p'x) denote the expected payoff of the politician when he chooses the strategy ρ given that the voter's strategy is x.

Lemma 1 Given the voter's strategy x, the politician' s expected payoff from choosing the strategy ρ is as follows.

^Ικ)=1-δ(1-^(τ)|/))

The politician's payoff is composed of two parts: The current period's payoff and the dis- counted value of the expected future payoff. His payoff is increasing in the current period's payoff and in his probability of reelection. The voter's strategy does not affect the politi- cian's current-period payoff, but does affect the politician's reelection probability. Electoral control of the politician is based on this payoff structure. The voter's strategy can provide in- centives for the politician to lower his current-period payoff in order to raise his probability of reelection.

Note that for any strategy of the voter, the politician can always have a minimum payoff Τ by collecting the maximum tax and not investing in each period. Let po represent this strategy of the politician.

Ρο = (τ,Ο) Since the politician's payoff is at least τ" when he chooses po, in any SSPE, the payoff of the politician cannot be less than T.

Ô Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

Public Choice (2010) 142: 215-235 221

The following proposition states a necessary condition for the existence of an SSPE in which the politician invests.

Proposition 2 If Τ < |, then there exists no SSPE with investment.

If the cost of investment is close to the maximum allowable tax, then for any strategy of the voter, the increase in the politician's expected future payoff from investment is less than the cost of investment. Thus, the politician does not invest. The maximum allowable tax level can be interpreted as the power of the politician. Hence, this result reveals that even if the expected benefit of the investment is much more than the cost of it, if the politician does not have sufficient power, then he does not make the optimal decision for the voter.

Another implication of the proposition relates to the discount rate of the politician. If the politician has a high discount rate (low 8), then the voter is not able to give enough incentive to the politician to invest. Since the politician heavily discounts the future payoffs, the cost of investment is larger than the positive effect of the investment on his expected payoff. Consequently, the politician does not invest. For the remainder of the paper, we assume that

To address the effects of the asymmetric information between the politician and the voter, we first consider the case where the voter observes both the tax policy and the investment policy of the politician in every period. Then, we consider a setup of the model in which the voter observes only the tax policy of the politician in every period. The case in which the voter observes both the tax policy and the investment policy of the politician in every period is called "the case of a transparent political system", while the case in which the voter observes only the tax policy of the politician in every period is called "the case of a non- transparent political system".

3 The case of a transparent political system

Suppose now that the voter observes both the tax policy and the investment policy of the politician in every period. Hence, there is no information asymmetry between the politician and the voter. The voter's strategy therefore depends also on the investment policy of the politician.

We first find the lowest tax level that the voter can induce the politician to collect in the case of no investment. Then we find the lowest tax level that the voter can induce the politician to collect and also to invest. Note that the voter induces the politician to invest by allowing him to collect more in taxes than justified by the level of investment. The difference between these two tax levels is the cost of inducing the politician to invest. If the expected benefit of the investment is more than the cost of inducing the politician to invest, then in equilibrium the voter induces the politician to invest.

Lemma 2 There does not exist an SSPE without investment when the tax is less than (1-*)t.

When the politician does not invest, the lowest tax that the voter can induce him to collect is (1 - 8)T. The voter can achieve it by choosing the strategy "reelect the politician if and only if he collects the tax (1 - 8)T in every period". The politician's best response to this strategy is to collect the tax (1 - 8)T and not to invest. This is what Persson et al. (1997) call "rents from power". Even in a transparent political system, since the politician has the authority to choose his policies, he gets a positive payoff.

α Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

222 Public Choice (2010) 142: 215-235

Lemma 3 There does not exist an SSPE with investment when the tax is less than / + (1-5)τ.

/ + (1 - 8)Ύ is the lowest tax that the voter can induce the politician to collect and also to invest. The voter can achieve this by choosing the strategy "reelect the politician if and only if he invests and collects the tax / + (1 - 8)T in every period". The politician's best response to this strategy is to invest and to collect the tax / + (1 - 8)T. In the case of transparent political system, the cost of inducing the politician to invest is equal only to the cost of investment. The politician's payoff is the same whether the voter induces him to invest or not.

Proposition 3 When the politician 's policy is observable by the voter, there exist multiple SSPE with a unique outcome. In these equilibria, in every period the politician invests, collects the tax I + (1 - 8)T, and is never replaced.

The cost of inducing the politician to invest is equal to the cost of investment. Also, it is assumed that the expected benefit of the investment is greater than the cost of it. Thus, the expected benefit of the investment is more than the cost of inducing the politician to invest. Consequently, the voter induces the politician to invest in every period. In SSPE, the voter can choose the strategy "reelect the politician if and only if he invests and collects the tax / + (1 - 8) Ύ in every period". In addition to this strategy, there are infinitely many monotone and non-monotone strategies of the voter that constitute SSPE with the same outcome. In these strategies, the politician is reelected with certainty if he invests and collects the tax / + (1 - 8)T, and if the politician collects another tax level, then his expected payoff is less than or equal to Y.

Note that in equilibrium, the reelection decision of the politician does not depend on the voter's realized income and the politician is never replaced. The politician invests every period and thus makes the optimal decision for the voter.

4 The case of a non-transparent political system

We now assume that the voter does not observe the investment policy of the politician in any period. Hence, the voter's strategy κ cannot depend on it. In any SSPE, the voter's strategy κ solves the following.

max I ydF(y'I) - τ {g(r)}J

subject to: (τ, /) € arg max ϋ(τ, Ι'χ) {T€|0,r],/€{0,/}}

In any SSPE, the voter chooses a strategy such that the optimal policy of the politician under that strategy maximizes her expected payoff. The previous subsection shows that in a transparent political system, in equilibrium the politician invests and the voter's strategy does not depend on her income. However, in a non-transparent political system, if the voter's strategy does not depend on income, then the politician will not invest. The reasoning for this is as follows. Investment is costly for the politician. If the voter's strategy is independent of the income, then the reelection probability of the politician will be the same whether or not he invests. The politician, then, does not have any incentive to invest. Therefore, in

<ö Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

Public Choice (2010) 142: 215-235 223

any period, in any SSPE with investment, the voter's strategy must depend on the income realized that period. Accordingly, the politician is replaced with some probability in any SSPE with investment.

Lemma 4 There does not exist an SSPE without investment when the tax is less than (l-8)Y.

Obviously, the ability to observe the politician's investment policy does not affect the equilibrium in which the politician does not invest. As in the case of transparent political system, in the case in which the politician does not invest, the lowest tax that the voter can induce the politician to collect is (1 - 8)Y. The voter can achieve this by selecting the strategy "reelect the politician if and only if he collects the tax (1 - 8)Y in every period". The politician's best response to this strategy is to collect the tax (1 - 8)Y and not to invest.

To characterize the SSPE, we first determine whether the voter is able to induce the politician to invest. If she is not able to do so, then there is no SSPE with investment. Con- sequently, the voter chooses the strategy "reelect the politician if and only if he collects the tax (1 - 8)Y in every period" in order to induce the politician to collect the lowest tax. The politician's best response to that strategy is to collect the tax (1 - 8)Ύ and not to invest. If the voter is able to induce the politician to invest, then we find the cost of inducing the politician to invest. The voter induces the politician to invest, and consequently there exist SSPE with investment if and only if the expected benefit of the investment is more than the cost of inducing the politician to invest.

Here, we define two functions, φ and ψ. First, φ : [0, Y] -> [0, y] is defined as follows.

0(r) = jF-i(I^M|/) ifr>/ + (i-5)r

1 0 otherwise

If the voter's strategy h is such that g(x) = φ (τ) for Υτ > / + (1 - 8)Y, then the politician's expected payoff is equal to Y when he chooses the strategy (τ, /) for any tax τ>/+(1-(5)τ.

Lemma 5 Given the voter's strategy x,for any tax τ > I + (1 - 8)Y,ifg(r) >0(r), then the politician prefers po to the strategy (τ, /).

The second function we define is ψ. Let ψ : (0, y) - > R be the following.

I(l-8 + 8F(y'0)) ú(y) = - δ F(y'0)-F(y'I)

ψ {y) can be interpreted as follows. Given the voter's strategy x, the politician prefers the strategy (τ, /) to the strategy (τ, 0) if and only if τ > ^(g(r)) for Vr € [0, T].

Note that lim^o Y(y) = +oo and lim^y '//(y) = +oo.

Lemma 6 i/s(y) has a unique minimum point.

Let v* be the unique minimum point of '/s(y) and τ* = ψ (y*). Since τ* is the minimum value of ψ (ν), for any strategy of the voter, the politician prefers the strategy (τ, 0) to the strategy (τ, /) for Υτ < τ*. Therefore, there is no strategy of the voter that induces the politician to invest and to collect a tax less than τ*.

4ü Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

224 Public Choice (2010) 142: 21 5-235

Lemma 7 If Τ < τ*, then there does not exist an SSPE with investment.

Since there is no strategy of the voter that induces the politician to invest and to collect a tax less than τ*, if the maximum allowable tax level, Y, is less than τ*, then the politician does not invest for any strategy of the voter. Consequently, there does not exist any SSPE with investment.

If τ* < 7, then the voter is able to induce the politician to invest. The lowest cost of it depends on the 0 (τ*) and y*.

If φ (τ*) > y*, then the politician prefers the strategy (τ*, /) to both (τ*, 0) and p0 under the voter's strategy "reelect the politician if and only if the collected tax is τ* and the income y >y* in any period".

Lemma 8 If the voter is able to induce the politician to invest and φ (τ*) > y*, then τ* is the lowest tax that the voter can induce the politician to collect and also to invest.

If φ (τ*) < y*, then the politician prefers the strategy (τ*, /) to the strategy (τ*, 0), but his payoff when he chooses the strategy (τ*, /) is less than Ύ. Therefore, he prefers p0 to the strategy (τ*, /). In this case, the voter cannot induce the politician to invest and to collect only tax τ*.

First, from Lemma 6 we see that 'jr{y) is decreasing in the interval (0, y*]. Second, by définition φ (τ) is an increasing function. These two conditions imply that if φ (τ*) < y*, there exists a unique tax level, say τ**, which satisfies the following requirement.

τ** = ι/τ(0(τ**)) and φ(τ**) < y* (2)

The politician prefers the strategy (τ**, /) to both the strategy (τ**, 0) and p0 under the voter's strategy "reelect the politician if and only if the collected tax is τ** and the income is y > 0(τ**) in any period".

Lemma 9 If the voter is able to induce the politician to invest and φ (τ*) < y*, then τ** is the lowest tax that the voter can induce the politician to collect and also to invest.

When the voter is able to induce the politician to invest, she does so if the expected benefit of the investment is greater than its cost to the voter. Lemmas 4 and 8 imply that if 0(τ*) > y*, then the lowest cost of inducing the politician to invest is τ* - (1 - δ)Ύ. Furthermore, Lemmas 4 and 9 imply that if φ (τ*) < y*, then the lowest cost of inducing the politician to invest is τ** - (1 - 8)Ύ . Therefore, the investment is worthwhile if and only if the following condition holds.

The equilibria of the game can be described as follows.

Proposition 4 When the voter cannot observe the investment policy of the politician, there exist SSPE. If the voter is not able to induce the politician to invest or the investment is not worthwhile, then in equilibrium, the politician does not invest, collects the tax (1 - δ)Ύ, and is never replaced. If the voter is able to induce the politician to invest, the investment is worthwhile and φ (τ*) > y*, then in equilibrium, the politician invests, collects the tax

α Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

Public Choice (2010) 142: 215-235 225

τ*, and is replaced with positive probability. If the voter is able to induce the politician to invest, the investment is worthwhile and φ (τ*) < y*, then in equilibrium, the politician invests, collects the tax τ**, and is replaced with positive probability.

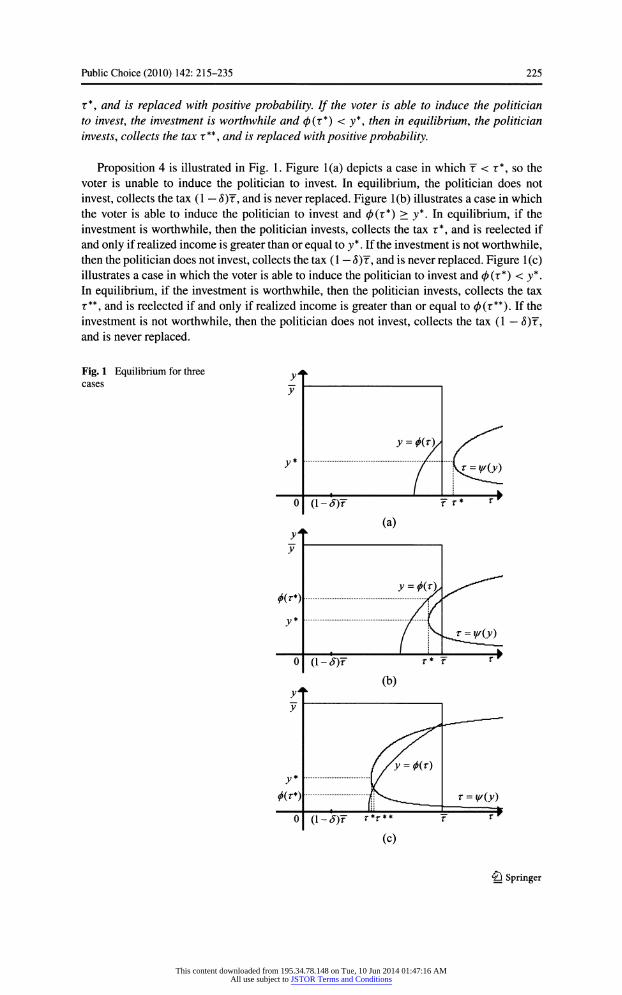

Proposition 4 is illustrated in Fig. 1. Figure l(a) depicts a case in which Ύ < τ*, so the voter is unable to induce the politician to invest. In equilibrium, the politician does not invest, collects the tax (1 - 8)T , and is never replaced. Figure l(b) illustrates a case in which the voter is able to induce the politician to invest and φ (τ*) > ν*. In equilibrium, if the investment is worthwhile, then the politician invests, collects the tax τ*, and is reelected if and only if realized income is greater than or equal to y * . If the investment is not worthwhile, then the politician does not invest, collects the tax (1 - <$)"?, and is never replaced. Figure l(c) illustrates a case in which the voter is able to induce the politician to invest and φ (τ*) < y*. In equilibrium, if the investment is worthwhile, then the politician invests, collects the tax τ**, and is reelected if and only if realized income is greater than or equal to φ (τ**). If the investment is not worthwhile, then the politician does not invest, collects the tax (1 - 5)7, and is never replaced.

Fig. 1 Equilibrium for three cases yf

J

y * Ύ 'r = v(y)

(Γ (l-S)T Tt* **

(a) ιΐ y

Φ(τ*) 7'/

(Γ (1 -<?)?" r* Τ **

(b) y y

ίΧ=φ{τ)

Φ(τ*) "/^-^^___ τ = ψ^

ο" (ΐ-δ)τ ^** τ ^

(c)

Ô Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

226 Public Choice (2010) 142: 215-235

In a non-transparent political system, the politician may not make the optimal decision for the voter as a consequence of two factors. First, the politician may be unable to collect tax revenue sufficient to induce him to invest. Second, the cost of inducing the politician to invest through taxation is so high that it overrides the returns of the investment for the voter. Consequently, the voter may prefer to induce the politician to choose a policy with a lower tax and no investment instead of a policy with investment, even though the investment decision of the politician is optimal for the voter.

In equilibrium, the voter's strategy can be as follows. If she is not able to induce the politician to invest or the investment is not worthwhile, then her equilibrium strategy can be "reelect the politician if and only if the collected tax is (1 - 8)T' If the voter is able to induce the politician to invest, the investment is worthwhile and φ(τ*) > y*, then it can be "reelect the politician if and only if the collected tax is τ* and income is greater than or equal to y*". If the voter is able to induce the politician to invest, the investment is worthwhile and φ (τ*) < y*, then it can be "reelect the politician if and only if the collected tax is τ** and income is greater than or equal to φ (τ**)".

Note that there are infinitely many monotone and non-monotone strategies that can be the voter's strategy in an SSPE with the same outcome. In these strategies, if the politician chooses the policy in Proposition 4, then the voter's decision to reelect the politician is the same with the strategy described above. Moreover, if the politician selects another policy, then his expected payoff will be less than or equal to that obtained when he chooses the policy in Proposition 4. Thus, the politician does not select another policy in any SSPE.

5 Welfare analysis

Here, we analyze the effects of the presence of asymmetric information on both the welfare of the voter and the politician. In a transparent political system, the politician invests, col- lects the tax (1 - <5)T, and is never replaced. Consequently, his payoff is equal to Ύ. In the case of non-transparent political system, in SSPE, the policy of the politician depends on the maximum allowable tax level, effect of investment on the welfare of the voter and the politician, and the politician's discount rate for future payoffs.

Proposition 5 The welfare effects of the asymmetric information can be described as fol- lows.

(i) If the politician does not invest in SSPE, then asymmetric information causes an ex- pected loss off yf(y'I)dy - fyf(y'O)dy - I in the voter's payoff in each period. The politician's per-period and expected payoffs are equal to those in the case of a trans- parent political system.

(ii) If the politician invests in SSPE and φ {τ*) < y*, then the politician collects the tax τ**. Asymmetric information causes a transfer of τ** - [/ + (1 - 8)T]from the voter to the politician in each period. Thus, the politician 's per-period payoff is greater than that in the case of a transparent political system. However, his expected payoff is equal to that in the case of a transparent political system.

(iii) If the politician invests in SSPE and φ (τ*) > y*, then the politician collects the tax τ*. Asymmetric information causes a transfer of τ* - [I + (1 - 8)T]from the voter to the politician in each period. The politician' s per-period payoff and expected payoff both are greater than those in the case of transparent political system.

Ô Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

Public Choice (2010) 142: 215-235 227

Proposition 5 implies the existence of three possible types of welfare effects of the asym- metric information. Depending of the dynamics of the society (the power of the politician, the influence of the politician's policies to the welfare of the society, the politician's discount rate for future payoffs), society faces one of these types.

The most severe effect of asymmetric information occurs in the first type: The politician does not make the optimal decision for the voter. The politician is indifferent to having a transparent or non-transparent political system.

In the second type, the optimal decision for the voter is made by the politician, but the voter transfers some of its benefits to the politician in order to induce him to make it. The politician's per-period payoff is greater than that in a transparent political system due to the transfer from the voter. However, now the politician is replaced with positive probability. We show that the negative effect of the reduction of the politician's reelection probability on his expected payoff cancels the positive effect of the increase in the politician's per-period payoff on his expected payoff. Therefore, the politician's expected payoff is the same in a transparent or non-transparent political system.

If the society faces one of these two types of welfare effects, then the voter suffers from the existence of asymmetric information but the politician is indifferent to having a trans- parent or non-transparent political system. Consequently, a reform intended to make the political system more transparent should be supported by the voter and should also be wel- comed by the politician.

The third type of welfare effect of asymmetric information is as follows. As in the second type, the politician makes the optimal decision for the voter and she transfers some of its benefits to induce the politician to make it. The politician's per-period payoff is greater than that in a transparent political system due to the transfer from the voter and the politician is replaced with positive probability. However, here the positive effect of the increase in the politician's per-period payoff on his expected payoff is greater than the negative effect of the reduction in the politician's reelection probability on his expected payoff. Consequently, the politician prefers the non-transparent political system to the transparent political system.

As an example to the third type of welfare effect of the asymmetric information, consider the case illustrated in Fig. l(b) and assume that the investment is worthwhile. By definition of the function </>(τ), when the politician invests, collects the tax τ*, and is reelected if and only if the realized income is greater than or equal to 0(τ*), his expected payoff is equal to T. In equilibrium, the politician invests, collects the tax τ* and is reelected if and only if the realized income is greater than or equal to y*. Since φ (τ*) > y*, in equilibrium, the expected payoff of the politician is greater than Ύ.

6 Conclusion

We presented here a model with identical politicians and a representative voter whose in- terests conflict with those of the politicians. The politician makes decisions on two policies that affect the voter's welfare. The voter observes only one of the politician's policies and her strategy whether or not to reelect the politician depends both on her welfare and on the politician's decision on the observable policy.

In a transparent political system, the politician makes the optimal decision for the voter. However, in a non-transparent political system, depending on the power of the politician, the effect of politician's unobserved policy on the welfare of the voter and the politician, and the politician's discount rate for future payoffs, either optimal decision for the voter is not taken by the politician or, if taken, the politician would extract more rent in each period. In the latter case, politicians are also replaced more frequently.

4il Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

228 Public Choice (2010) 142: 215-235

The voter prefers the political system to be more transparent. We also demonstrated that the politician may prefer the lower per-period payoff in a transparent political system to the higher per-period payoff in a non-transparent political system, since he is reelected more frequently in the former one. Consequently, a reform that would make the political sys- tem more transparent should be supported by the public and may also be welcomed by the politician.

Acknowledgements I am grateful to Christophe Chamley and Zvika Neeman for their advice. I also would like to thank J. Miguel Flores, Hsueh-Ling Huynh, Barton Lipman, Ching-to Albert Ma, Tolga Yuret, work- shop participants at Boston University, seminar participants at Ankara University and Koç University, the editors and anonymous reviewers.

Appendix A

Proof of Proposition 1 The proof is based on the following lemma.

Lemma 10 Assume that in an SSPE, the politician's strategy is (V, Γ) and he is reelected if the income y G /, where the greatest lower bound of the set J is y. Then, J = [y, ~y].

Proof First, we will show that if Γ = 0, then J = [y,y]. Second, we will show that if Γ = /, then J = [j, J]. Let Jo c [y, y] with Jo # 0 and J = [j, y]'J0.

First, assume that V = 0. In SSPE, the politician does not invest and collects the tax t ' . Since the politician prefers the strategy (V, 0) to strategy (T, 0),

τ'

'-t>ïjf{y'V)dy-T'

Since Jo φ 0, fj f(y |0) dy > 0. So, there exists a tax level τ" < τ' such that

τ" τ1

'-8fJf(y'0)dy> I - 8 fj f(y'0)dy'

Therefore, the voter can induce the politician to collect a lower tax by choosing the strategy "reelect the politician if and only if the collected tax is τ" and the income y€[j, 3T'· Thus, if J φ |j, y], then the voter's strategy cannot be an equilibrium strategy.

Second, assume that Γ = /. In SSPE, the politician invests and collects the tax τ' . Since the politician prefers the strategy (τ', I) to both strategy (?, 0) and strategy (τ', 0), it can be written as follows.

!'-7' >T (3) l-8fjf(y'I)dy

r'-î > l-Sjjf{y'î)dy τ' -

l-í/y/(y|0)dy

Since the greatest lower bound of Jo is greater than y, there exists a subset of 7, say /', and a subset of 7o» say Jq, such that:

sup(/r) < inf(7o) and (5)

<ö Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

Public Choice (2010) 142: 215-235 229

í f(y'0)dy= f f(y'O)dy. (6) ir Jr0

Strict MLRP requires that

frf(y'î)dy /(supin I /) /(inf(^)l/) IijfWhdy frf(y'0)dy

< /(sup(7')|0)

"" /(inf^lO)

< /,,/(y|0)<//

Since sup(/') < inf(/ó), strict MLRP implies that

/(sup(7')|7) /(inf(^)[/) ^ < . ^ (θ)

/(sup(J')IO) /(inf(7,5)|O)

Consequently, (7) and (8) implies that

frf(y'hdy fj>f(y'ndy frf(y'0)dy fj,ny'0)dy'

Then, (6) and (9) requires that

[ f(y'î)dy< [ f(y'î)dy. (10) Jr Jj^

Let us define the set /* as follows.

J* = J'J'UJÓ

Then, (6) implies that

1-5 Í f(y'0)dy = l-8 [ f(y'0)dy, (11) Jj* Jj

and (10) implies that

l-*[ f(y'I)dy<l-8 [ f(y'I)dy. (12) Jj* Jj

From (11) and (12), it can be written as:

'-&îj»f{y'î)dy 1-Sfjf(y'î)dy 1 - « îj> f(y'°) dy

< l - s fj /(yio) dy'

Therefore, (3), (4), (12) and (13) implies that there exists a tax level τ'" < τ' satisfying the following two conditions.

τ'" -Î

l-SfJtf(y'î)dy-T τ'"-Ϊ ^ l-Sf^f(y'î)dy τ'" -l-8fj.f{y'0)dy

4y Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

230 Public Choice (2010) 142: 215-235

Therefore, if the voter chooses the strategy "reelect the politician if and only if the col- lected tax is τ'" and the income y e /*", the politician will collect a lower tax than τ' and still invest. Thus, if J φ [y, ~y], then the voter's strategy cannot be an equilibrium strategy. D

Suppose that in an SSPE, the politician's strategy is (V, /') and he is reelected if the income y e [y,y]. The same outcome can be generated by an SSPE in which the voter's strategy is "reelect the politician if and only if the collected tax is τ' and the income y e [y,y]". Consequently, any SSPE outcome can be generated by an SSPE with monotone strategies. D

Proof of Lemma 1 Since the players's strategies are stationary, U(p'x) can be written as

ϊ/(ρ|χ) = τ - / + Sa(p'x)U(p'x). (14)

By solving (14) for i/(p|x) and substituting a(p|x) with (1 - F(g(r)|/)), we obtain

"<*'*>= 1-,<ΐΙ^(τ)|/))· D

Proof of Proposition 2 When the politician invests, his expected payoff is maximized if he collects the maximum allowable tax, T, and is reelected every period. Therefore, ί/((τ, /) |x) has the following upper bound.

t/((T,/)|x)<^- £ ι - ο

The politician can get an expected payoff at least Ύ by choosing po- Therefore, if

H<?' (i5) then the politician does not invest. The inequality in (15) can be written as

/

Proof of Lemma 2 If the politician does not invest and collects the tax (1 - 8)Y every period, then his expected payoff is equal to

»"-'"'"Ί-ιι-ΐ,Β- Since the reelection probability of the politician is less than or equal to one, i.e., [l-F(g(T)'I)]<l,

l-8(l-F(g(T)'I))-T' (16)

If the politician collects a tax lower than (1 - 5)T, then the inequality in (16) is strict. Therefore, for any strategy of the voter, the politician prefers to choose p0 to the strategy (τ, 0) for Υτ < (1 - 8)Y. Consequently, there does not exist an SSPE without investment when the tax is less than (1 - δ)Τ. D

τΏ Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

Public Choice (2010) 142: 215-235 231

Proof of Lemma 3 If the politician invests and collects the tax / + (1 - 8)T every period, then his expected payoff is equal to

w/+a-8)T,/V)=,_a(1(1_-;^t)|f))<^ (17,

If the politician collects a lower tax than / + (1 - 8) τ' then the inequality in (17) is strict. Therefore, for any strategy of the voter, the politician prefers to choose po to the strategy (τ, /) for Vr < / + (1 - 8)T. Consequently, there does not exist an SSPE with investment when the tax is less than / + (1 - 8)Y. D

Proof of Proposition 3 The cost of inducing the politician to invest is equal to the cost of investment. Since the cost of investment is lower than the expected benefit of investment, the voter induces the politician to invest. The voter can induce the politician to collect the tax / + (1 - 8)T and also to invest by reelecting him with probability one if and only if he chooses this policy in each period. Consequently, in SSPE, the politician invests, collects the tax / + (1 - <$)?, and is reelected every period. D

Proof of Lemma 4 If the politician collects a tax less than (1 - 8)Y, then for any strategy of the voter, his expected payoff is less than Ύ. Therefore, for any strategy of the voter, the politician prefers to choose po to the strategy (τ, 0) for Υτ < (1 - 8)Ύ. Consequently, there does not exist an SSPE without investment when the tax is less than (1 - 8) T. D

Proof of Lemma 5 Assume that τ e [I + (1 - δ)Τ, τ7]. Given the voter's strategy x, the politician's expected payoffs when he chooses po and the strategy (τ, /) are as follows.

U(po'x) = - ,_.,m, > τ l-8(l-F(g(T)'0)) ,_.,m,

ί/((τ, /)|x) = - - - l-8(l-F(g(T)'I))

First, note that if g(x) = φ(τ), then ί/((τ, î)'x) = τ. Second, ί/((τ, /)|χ) is strictly de- creasing in g (τ). Consequently,

g{x) > 0(t) =► C/((t, I)'x) < τ < U(po'x).

Therefore, if g(r) > φ(τ), then the politician prefers to choose po to the strategy (τ, /). D

Proof of Lemma 6 Let us define χ : (0, ~y) -> R as follows.

l-8 + 8F(y'I) Ay l-8 + 8F(y'O)

Note that ψ(γ) = t_7( }. Hence, if we prove that χ(ν) has a unique minimum point, it implies that ψ(γ) has a unique minimum point.

Note that χ'(0) < 0 and χ' Çy) > 0. Hence χ (y) has at least a minimum point. Fix a point y* in which x(y) is non-decreasing. Let us say χ(ν*) = π. Since χ (ν) is non-decreasing at y*, for an ε -> 0+,

X(y* + e)>x(y*).

Ô Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

232 Public Choice (2010) 142: 215-235

Hence, it can be written as

. l-8 + 8F(y* + s'I) ÁKy γ(ν

. +ε) J = > - π. (18) V ÁKy γ(ν +ε) J = l-8 + 8F(y* + 6'0)

- π. V

By using Taylor approximation of F(y |·) of order one at y*, inequality in (18) can be rewrit- ten as follows.

l-8 + SF(y*'î) + Sef(y'î) > l-S + SF(y*'0) + 8ef(y'0)

> " *

Since x(y*) = π, by substituting [1 - S + SF(y*'î)] with ττ[1 - £ + áF(y*|0)] in (19) and arranging the terms, we obtain

l^l>n. (20) /(rio)- Equation (20) and strict MLRP imply that for Vf G (0, y - y*),

/(/+f|/)>jr/(y* + f|O). (21)

By integrating both sides of (21) over [y*, y* + 1], we obtain

[F(y* + t'î) - F(y*'î)] > n[F(y* + f|0) - F(/|0)]. (22)

Let us define λ(^*, /) as the difference between LHS and RHS of (22) as follows.

λ(/' f) = [F(y* + t'h - F(y*'!)] - n[F(y* + 1'0) - F(y*'0)]

Note that (22) implies that k(y*, t) > 0. X (y* + 1) can be written as follows.

. l-6 + 6F(y*'î) + S[F(y*+t'î)-F(y*'î)] X(y i-s + SF(y*'0) + 8[F(y* + t'0)-F(y*'0)]

By substituting

[l-S + SF(y*'I)] with7r[l-á+SF(>>*|0)], and

[F(y* + t'î) - F(y*'î)] with λ(/, ί) + n[F(y* + φ) - F(y*'0)]

in (23) and by arranging the terms, we obtain

x(/ + ̂x(/) + M/.o[1_3 + ,;(r + f|0)]. (24) Since λ(^*,ί) >0, (24) implies that x(y* + t) > x(y*) for Wt e (0,y- y*). Soif χ (y) is non-decreasing at point y*, then it is strictly increasing when y > y*. Also, since χ'(0) < 0 and xf(y) > 0, there exists a point in the interval (0,y) where x(y) is non-decreasing. Consequently, χ (y) has a unique minimum point. D

Proof of Lemma 7 For any strategy of the voter, if the politician prefers the strategy (τ, 0) to the strategy (τ, /) for Vt € [0, τ], then the voter is not able to induce the politician to

4y Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

Public Choice (2010) 142: 215-235 233

invest, and thus there is no SSPE with investment. Therefore, a necessary condition for the existence of an SSPE with investment is that for at least a tax τ' e [0, Y] and a strategy κ of the voter, the following inequality should hold.

£/((τ',/)|χ)>ί/((τ',0)|χ) (25)

Equation (25) can be written as follows.

i-a(i-F(g(T')|/)) "

i-Ä(i-F(g(r')|0)) (26)

By arranging the terms in (26), we obtain that it is equivalent to

τ'>ψ(8(τ')). (27)

Lemma 6 shows that there is a unique minimum of ψ(·) and τ* denotes the minimum value of ψ{-). Therefore, if Υ < τ*, then the maximum possible value of the LHS of (27) is less than the minimum value of the RHS of (27). Consequently, the necessary condition for the existence of an SSPE with investment does not hold. Hence, if Υ < τ*, then there does not exist an SSPE with investment. D

Proof of Lemma 8 By construction of ψ(-), the lowest tax τ that the politician prefers the strategy (τ, /) to the strategy (r, 0) is τ*. Given the voter's strategy x*, "reelect the politician if and only if the collected tax is τ* and the income y > y*", the politician prefers the strategy (τ*, /) to the strategy (τ*, 0). Thus, to prove the lemma we have to show that if φ (τ*) > y*, then the politician also prefers the strategy (τ*, /) to p0 under the voter's strategy k*.

Given the voter's strategy x*, the politician's payoff when he chooses po is equal to Y. The politician's payoff when he chooses the strategy (τ*, /) is as follows.

1/((τ*. /)|x*) = T-- - l-8(l-F(y*'I))

If Φ (τ*) >y*, then

ί/((τ*. /)|x*) > T-- l- - = τ. 1-5(1-F(0(r*)|/))

Consequently, the politician prefers the strategy (τ*, /) not only to the strategy (τ*, 0), but also to po· D

Proof of Lemma 9 The proof here is by contradiction. Assume that tax τ' < τ** and the voter is able to induce the politician to collect the tax τ' and also to invest. Then, there exists a strategy of the voter such that g(r') satisfies the following two conditions.

8(τ')<φ(τ') (28)

τ' > ψ(8(τ')) (29)

The condition in (28) is necessary for the politician to prefer the strategy (rr, /) to po· The condition in (29) is necessary for the politician to prefer the strategy (rr, /) to the strategy (τ', 0). If one of these two conditions is violated, then the politician will not invest.

<ö Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

234 Public Choice (2010) 142: 215-235

Since 0(·) is an increasing function, if τ' < τ**, then φ{τ') < φ(τ**). Therefore, if g{x') satisfies the condition in (28), then

g(x') < 0(r~). (30)

Note first that ψ(γ) is decreasing when y < y*. Second, 0(τ**) < y* because of the re- quirement in (2). Consequently, if g(j') satisfies the condition in (28), then (30) implies that

VKs(t')) > VK0(r**)). (31)

Also, ψ(φ(τ**)) = τ** because of the requirement in (2). Thus, both (2) and (31) imply that

VKS(O) > τ**.

Therefore, to satisfy the condition in (29), τ' must be grater than τ**. This is a contradiction to our initial assumption. D

Proof of Proposition 4 Proof of the proposition follows the Lemmas 4, 8 and 9. The reason- ing for the replacement of the politician with positive probability while investing is the fol- lowing. In SSPE, if the politician invests and collects the tax τ*, then he is removed from of- fice if the income is less than y*. Thus, he is replaced with probability F(y* 'I) > 0. In SSPE, if the politician invests and collects the tax τ**, then he is removed from office if the income is less than 0(τ**). Thus, the politician is replaced with probability F(0(r**)|7) > 0. D

Proof of Proposition 5 In a transparent political system, the politician invests, collects the tax / + (1 - 8)T, and is reelected. His per-period payoff is (1 - 8)T and his expected payoff is T. The voter's expected payoff is f yf(y'I)dy - [I + (1 - 5) τ]. In a non-transparent political system, in SSPE, the following occurs.

(i) If the politician does not invest, then he collects the tax (1 - δ)Τ and is reelected. His per-period payoff is (1 - 8)T and his expected payoff is T. Therefore, the politician's per- period and expected payoffs are equal to those in the case of a transparent political system. The voter loses the expected benefit of the investment, but pays less tax when compared to a transparent political system in each period. Therefore, the expected welfare loss of the voter is fyf(y'I)dy-f yf(y'0) dy - I in each period.

(ii) If the politician invests in SSPE and φ(τ*) < y*, then he collects the tax τ** and is reelected with probability α((τ**, /)|χ), where

a((T",/)|x) = l-F(0(T**)|7)

_ T + /-T** ~

ST '

By plugging α ((τ**, I)'k) into the expected payoff function in Lemma 1, the politician's expected payoff can be found as 7, which is the same with the politician's payoff in a transparent political system. His per-period payoff is τ** - /, which is more than that in the transparent political system. Consequently, asymmetric information causes a transfer of τ** - [/ + (1 - δ)Ύ] from the voter to the politician in each period.

<Ö Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions

Public Choice (2010) 142: 215-235 235

(iii) If the politician invests in SSPE and φ(τ*) > y*, then the politician collects the tax τ* and is reelected with probability α((τ*, /)|χ), where

a((T*J)'x) = l-F(y*'I) T+Î -τ*

>[l-F(0(r*)|/)] = .

Both the per-period and the expected payoff of the politician is greater when compared to a transparent political system. Asymmetric information causes a transfer of τ* - [/+ (1 - 8)Ύ] from the voter to the politician in each period. D

References

Adserà, Α., Boix, C, & Payne, M. (2003). Are you being served? Political accountability and quality of government. The Journal of Law, Economics, & Organization, 19(2), 445-490.

Alesina, Α., & Cukierman, A. (1990). The politics of ambiguity. Quarterly Journal of Economics, 105, 829- 50.

Austen-Smith, D., & Banks, J. (1989). Electoral accountability and incumbency. In P. C. Ordeshook (Ed.), Models of strategic choice in politics (pp. 121-148). Ann Arbor: University of Michigan Press.

Banks, J., & Sundaram, R. K. (1993). Adverse selection and moral hazard in a repeated elections model. In W. A. Barnett, B. J. Hinich & N.J. Schofield (Eds.), Political economy: institutions, competition and representation (pp. 295-31 1). Cambridge: Cambridge University Press.

Banks, J., & Sundaram, R. K. (1998). Optimal retention in agency problems. Journal of Economic Theory, 82, 293-323.

Barro, R. (1973). The control of politicians: an economic model. Public Choice, 14, 19^2. Bender, B., & Lott, J. R. (1996). Legislator voting and shirking: a critical review of the literature. Public

Choice, 87, 67-100. Fearon, J. (1999). Electoral accountability and the control of politicians: selecting good types versus sanc-

tioning poor performance. In A. Przeworski, S. Stokes & B. Manin (Eds.), Democracy, accountability and representation (pp. 55-97). Cambridge: Cambridge University Press.

Ferejohn, J. (1986). Incumbent performance and electoral control. Public Choice, 50, 5-25. Harrington, J. E. (1993). Economic policy, economic performance, and elections. American Economic Re-

view, 83, 27-42. Harrington, J. E. (2000). Progressive ambition, electoral selection, and the creation of ideologues. Economics

of Governance, 1, 13-24. Hinich, M. J., & Munger, M. C. (1994). Ideology and the theory of political choice. Ann Arbor: University

of Michigan Press. Laffont, J. J. (2000). Incentives and political economy. Oxford: Oxford University Press. Milgrom, P. (1981). Good news and bad news: representation theorems and applications. Bell Journal of

Economics, 12, 380-391. Persson, T., & Tabellini, G. (2000). Political economics- explaining economic policy. Cambridge: MIT

Press. Persson, T., Roland, G., & Tabellini, G. (1997). Separation of powers and political accountability. Quarterly

Journal of Economics, 112, 1163-1202. Rogoff, K. (1990). Equilibrium political budget cycles. American Economic Review, 80, 21-36. Rogoff, K., & Sibert, A. (1988). Elections and macroeconomic policy cycles. Review of Economic Studies,

55, 1-16.

Ô Springer

This content downloaded from 195.34.78.148 on Tue, 10 Jun 2014 01:47:16 AMAll use subject to JSTOR Terms and Conditions