Embed Size (px)

Citation preview

TRANSFER PRICINGINTRA GROUP SERVICES (IGS)CHAMBERS OF TAX CONSULTANT – 06th July, 2016

SN & Co.Chartered Accountants

INTRODUCTION

MNE group may obtain services directly or indirectly from independent

companies, or from companies of same MNE group (i.e. intra-group)

Benefits of intra group services

o Economies of scale, synergy, efficient use of resources & high degree of specialization

o Developing own expertise, coordination & control and avoiding duplication of work

Intra Group Service (“IGS”) includes

o Services by One member to other member or members of MNE

o Services provided by group of members for the benefit of overall group

o Service by Parent company to member & group of members

o Service from third party on behalf of member or members

SN & Co.Chartered Accountants 2

I

N

C

L

U

S

I

O

N

S

T

O

I

G

S

Planning and Budgetary control

Coordination

Financial and Legal advice

Management and Administrative services

Accounting and Auditing service

Computer services & SAP Consulting service

Human Resource services

Credit risk analysis service

Marketing & Distribution support service

Resource Sharing service

Reimbursement of ASP

R&D service

SN & Co.Chartered Accountants 3

INTRAGROUP SERVICES

IGS

Chargeable service

LVAS

TP Simplified

HVAS

Full TP

Non chargeable service

Shareholder Duplication Incidental

4

W

A

Y

T

O

A

L

P

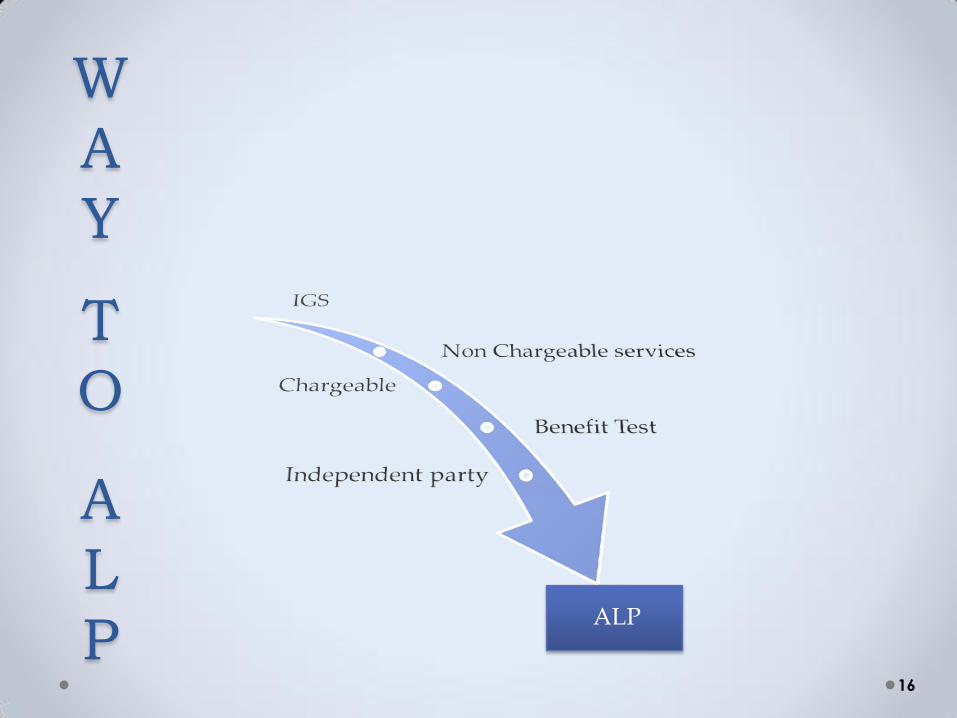

IGS

Non Chargeable servicesChargeable

services

Benefit Test

Independent party

ALP

5

WAY To ALP

Chargeable services

Benefit Test

Economic Benefit

Received Anticipated

Independent party

ALP

Charging

Direct Indirect

Calculation

CupCost plus

TNMM

6

7

Non Chargeable services

W

A

Y

T

O

A

L

P

SHAREHOLDER SERVICE

Activities carried out even though group members do not need the activity

Activity is performed solely because of its ownership interest in its capacity asshareholder

An independent entity would not be willing to pay for service and thus would notjustify a charge to the recipient

Examples:

o appointment and remuneration of parent company directors

o meetings of the parent company’s board of directors and shareholder

o activity of parent company’s in preparation and filing of consolidated financialreports

o activities of parent company for raising funds used to acquire share capital insubsidiary companies; and

o activities of the parent company to protect its capital investment in subsidiarycompanies.

SN & Co.Chartered Accountants 8

DUPLICATION SERVICE

Service provided to AE which has already obtain same service either by itself or

from independent entity – Eg. Legal opinion

Exceptions – Duplication service being IGS

Service providing benefit to AE for which an independent party would also be

willing to pay

Temporary service - Example - process of being centralized for an MNE group

Service undertaken to reduce risk of a wrong business decision (e.g. by getting a

second legal opinion on a subject)

SN & Co.Chartered Accountants 9

INCIDENTAL BENEFITS/PASSIVE

ASSOCIATION

IGS performed by a group member relates only to some group members but

incidentally provides benefits to other group members

AE has not received IGS when it obtains incidental benefits attributable solely

being part of a larger GROUP, and not to any specific activity being performed

SN & Co.Chartered Accountants 10

• Whether AE received enhance credit rating by reason of its affiliation with larger group; is IGS ?

• Whether guarantee given by group member increasing credit rating is IGS?

• Whether supplier giving additional credit based on guarantee given by IGS?

• Where the enterprise benefitted from global marketing and public relations campaigns done by Group Company ?

Contd…

SN & Co.Chartered Accountants 11

12

Chargeable

W

A

Y

T

O

A

L

P

CENTRALIZED SERVICES

MNE group often will

centralize certain business

functions within an associated

enterprise and wide variety of

services are centralized both

low and high-value adding

services

SN & Co.Chartered Accountants 13

ON CALL SERVICES

Parent company or a group service centre may be on call to provide services atany time, by having staff, equipment etc. available all the time

An intra-group service would exist to the extent that it would be reasonable toexpect an independent enterprise in comparable circumstances to incur ‘standby’charges to ensure the availability of the services when the need for them arises(e.g. a service contract for priority computer network repair in the event of abreakdown)

On call service can be considered as IGS even if the actual services are never orinfrequently provided

SN & Co.Chartered Accountants 14

INTRA GROUP SERVICES

52

3

14

1. Shareholder service

2. Duplication service

3. Incidental benefits/Passive Association

4. Centralized services

5. On call services

SN & Co.Chartered Accountants 15

16

ALP

W

A

Y

T

O

A

L

P

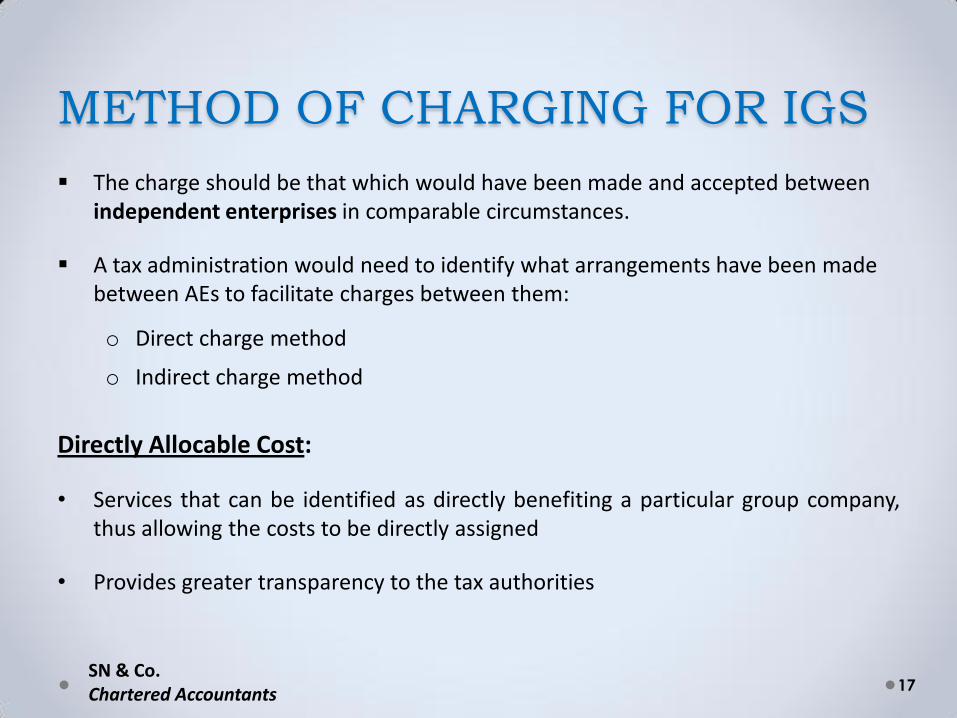

METHOD OF CHARGING FOR IGS

The charge should be that which would have been made and accepted between independent enterprises in comparable circumstances.

A tax administration would need to identify what arrangements have been made between AEs to facilitate charges between them:

o Direct charge method

o Indirect charge method

Directly Allocable Cost:

• Services that can be identified as directly benefiting a particular group company,thus allowing the costs to be directly assigned

• Provides greater transparency to the tax authorities

SN & Co.Chartered Accountants 17

Contd…

Indirectly Allocable Cost:

Used where proportion of the value of services rendered to each entity cannot beexactly quantified except on an approximate or estimated basis.

Identify all relevant costs and allocate them among all recipients using sensibleallocation key/s.

Allocation of cost should commensurate with the benefit derived by the recipient

Allocation method chosen must lead to a result that an independent enterpriseswould have been prepared to accept

SN & Co.Chartered Accountants 18

Indirectly Allocable Cost:

Allocation keys shall be based on the nature of service:

o IT: number of PCs

o Business management software (e.g. SAP): number of licences

o Human Resources: headcount

o Health and safety: headcount

o Management development: headcount

o Tax, Accounting, etc.: turnover or size of balance sheet

o Marketing services: turnover

o Vehicle fleet management: number of cars

Contd…

SN & Co.Chartered Accountants 19

Service Provider

How much does the service cost?

Service Recipient

How much is the service worth?

How much would a comparable independent enterprise be prepared to pay forthat service in comparable circumstances?

How much would it cost to provide the service in-house?

How much would an external service provider charge?

IGS – A DOUBLE EDGED SWORD

SN & Co.Chartered Accountants 20

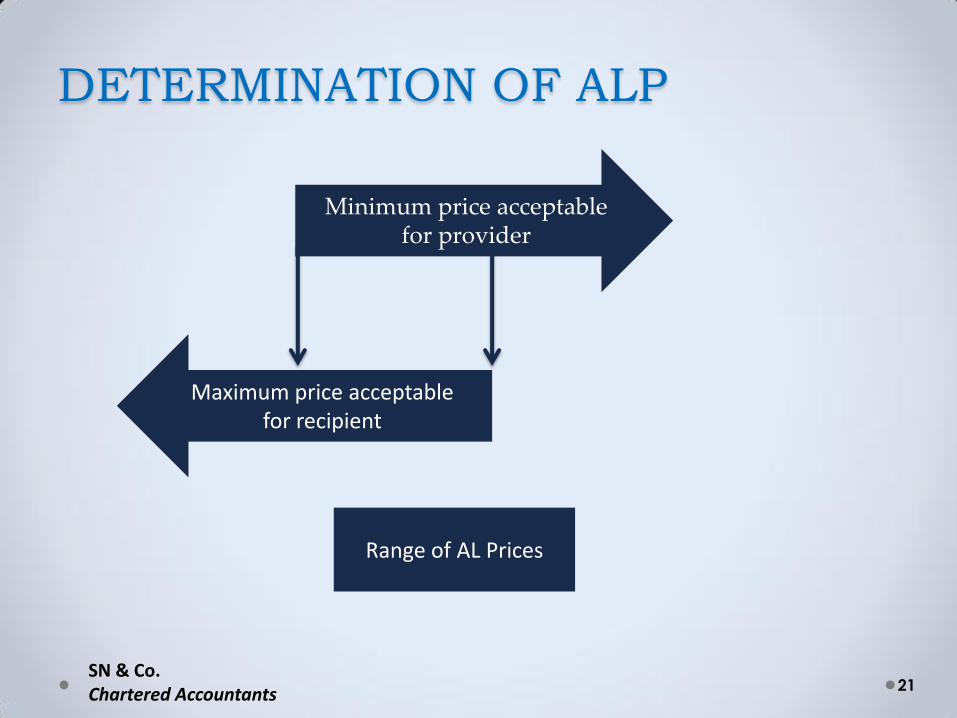

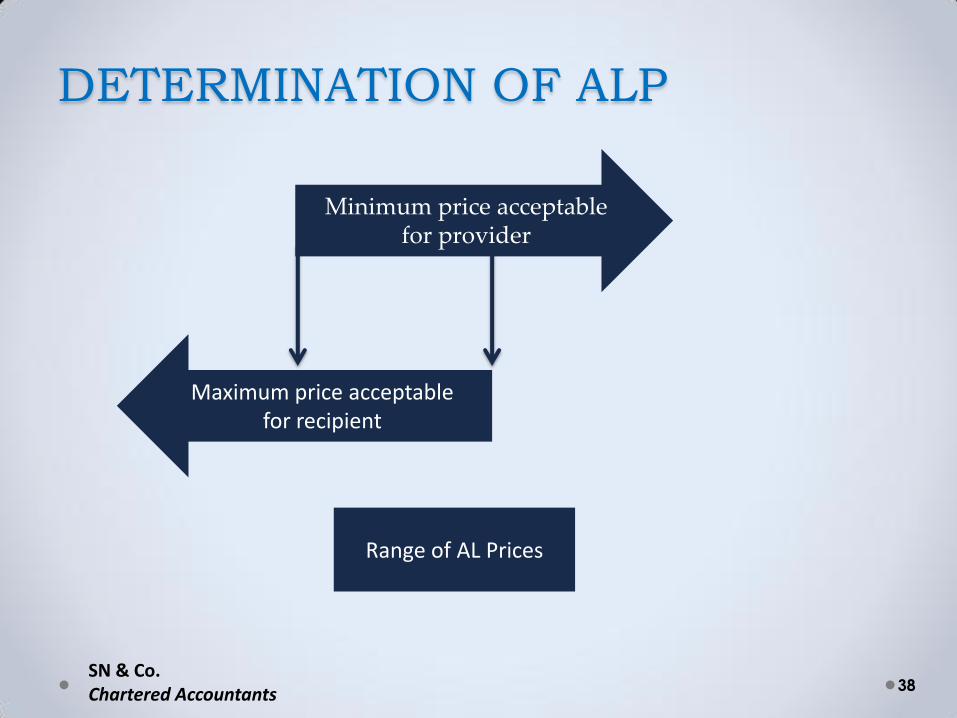

DETERMINATION OF ALP

Minimum price acceptable for provider

Maximum price acceptable for recipient

Range of AL Prices

SN & Co.Chartered Accountants 21

CALCULATION OF ALP

• ALP generally is calculated using methods:

o CUP

o CPM

o TNMM

• A CPM would most likely be the most appropriate method where thenature of the activities involved, assets used and risks assumed arecomparable to those undertaken by independent enterprises

• Challenge in Cost Plus : Cost comparison & availability of gross margin inservice industry

• TNMM : Sustains variables as comparison is at Net margin

SN & Co.Chartered Accountants

22

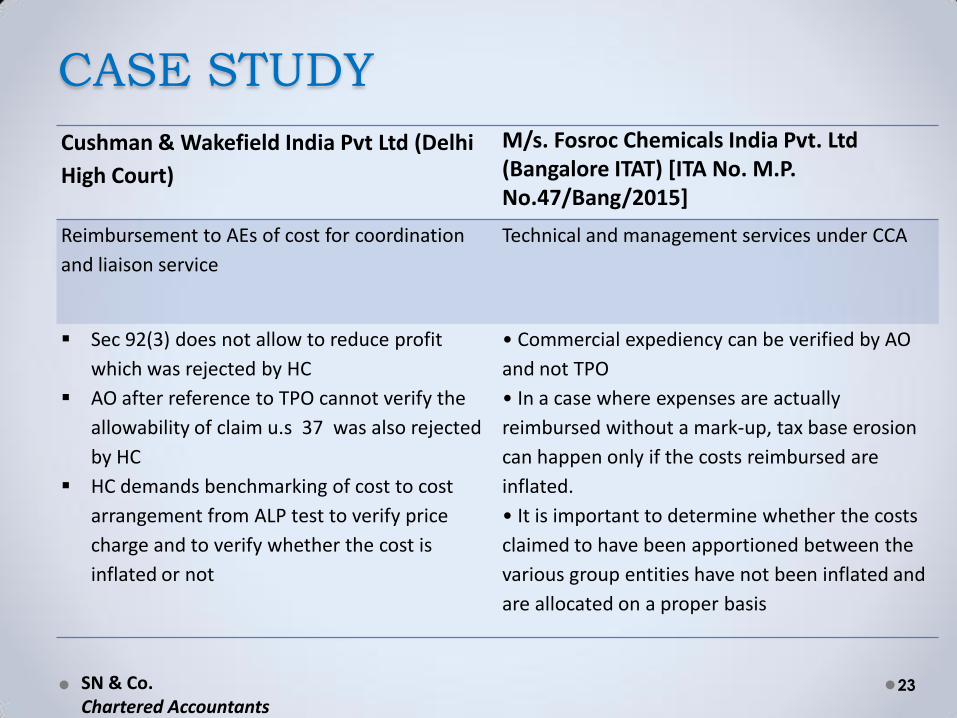

CASE STUDY

Cushman & Wakefield India Pvt Ltd (Delhi

High Court)

M/s. Fosroc Chemicals India Pvt. Ltd (Bangalore ITAT) [ITA No. M.P. No.47/Bang/2015]

Reimbursement to AEs of cost for coordination

and liaison service

Technical and management services under CCA

Sec 92(3) does not allow to reduce profit

which was rejected by HC

AO after reference to TPO cannot verify the

allowability of claim u.s 37 was also rejected

by HC

HC demands benchmarking of cost to cost

arrangement from ALP test to verify price

charge and to verify whether the cost is

inflated or not

• Commercial expediency can be verified by AO

and not TPO

• In a case where expenses are actually

reimbursed without a mark-up, tax base erosion

can happen only if the costs reimbursed are

inflated.

• It is important to determine whether the costs

claimed to have been apportioned between the

various group entities have not been inflated and

are allocated on a proper basis

SN & Co.Chartered Accountants

23

• Documents evidence for rendering of service

• Cost allocation methodology

• Benchmarking study

• Intercompany agreement

SN & Co.Chartered Accountants 24

DOCUMENTATION

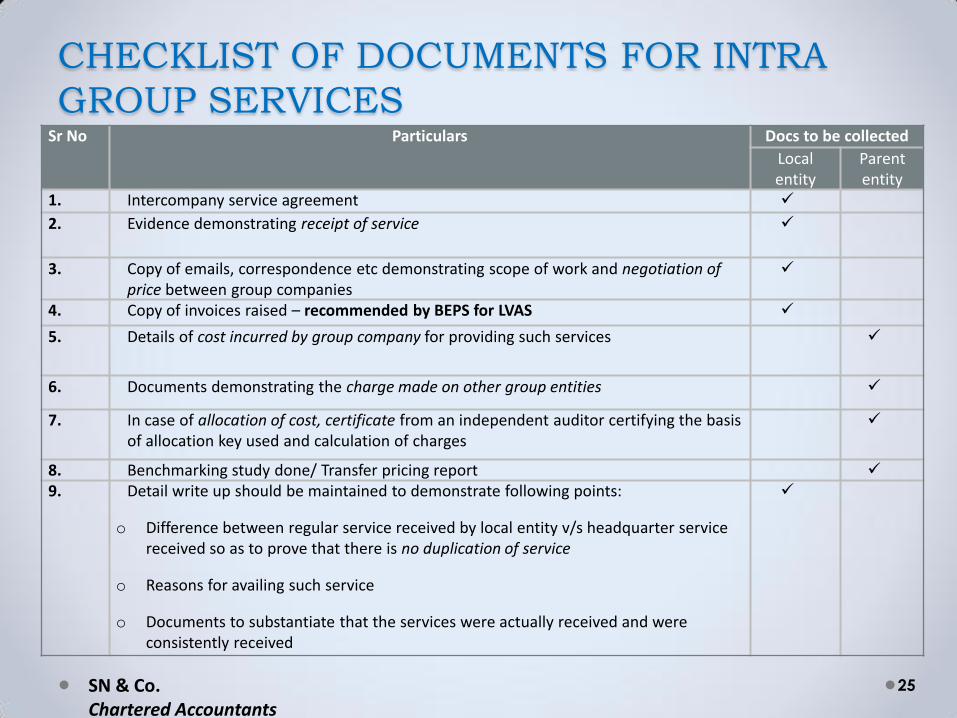

CHECKLIST OF DOCUMENTS FOR INTRA

GROUP SERVICES Sr No Particulars Docs to be collected

Local entity

Parent entity

1. Intercompany service agreement

2. Evidence demonstrating receipt of service

3. Copy of emails, correspondence etc demonstrating scope of work and negotiation of price between group companies

4. Copy of invoices raised – recommended by BEPS for LVAS

5. Details of cost incurred by group company for providing such services

6. Documents demonstrating the charge made on other group entities

7. In case of allocation of cost, certificate from an independent auditor certifying the basis of allocation key used and calculation of charges

8. Benchmarking study done/ Transfer pricing report

9. Detail write up should be maintained to demonstrate following points:

o Difference between regular service received by local entity v/s headquarter service received so as to prove that there is no duplication of service

o Reasons for availing such service

o Documents to substantiate that the services were actually received and were consistently received

SN & Co.Chartered Accountants

25

SN & Co.Chartered Accountants 26

INDIAN APPROACH – TP AUDIT

Benefits Test – IGS service been

provided?

Justification of mark-up – Routine

services vs. value added services

Intra group charge - Cost

allocation / cost base working

Documentation

CHALLENGES

Evidencing that

the recipient

required these

services

Evidencing that

the recipient has

actually received

the services

Evidencing the

commercial/econ

omic benefit

derived by the

recipient

Need Test Evidence Test Benefit TestChargeable

services

Non

Chargeable

services

SN & Co.Chartered Accountants 27

No No No

McCann Erickson India Pvt Ltd. - (Delhi ITAT) ITA No. 5871/Del/2011 -Management and co- ordination service

o Need Test: Only a business expert can evaluate true intrinsic and creativevalue of services received. Reference of need test complied by the taxpayer

o Benefit Test: Over the years 14% revenue growth substantiated by Taxpayer

o TNMM justified if

o Transaction if interrelated

o Nexus with core revenue generating activity

o No revenue generating capacity in isolation

o Only one class of business

o DRP direction of reducing adjustment to 40% cannot by denied by the TPO &AO

CASE STUDY

SN & Co.Chartered Accountants 28

Dresser Rand India Pvt. Ltd. - (Mumbai ITAT) ITA No. 8753/Mum/2010 - HR, Treasury, various support services

o Need Test : Tax authorities cannot question the commercial expediency, Inhouse presence of team does not stop AE to take specialised service

o Evidence Test : Contemporaneous documentation submitted – 300 pages

o Benefit Test : TPO did trend analysis of growth in the business (being firstyear of service) and in absence of increase in growth contented that theservice was not required – not accepted by Tribunal

o Separation of transaction and benchmarking it not possible and TNMMaccepted as most appropriate method

Contd…

SN & Co.Chartered Accountants 29

TNS India Pvt Ltd (HYD ITAT) ITA No 944/HYD/2007 – Evidence test accepted based ondetailed submission of functions performed by AE without corroborateddocumentation

Contd…

SN & Co.Chartered Accountants 30

Gemplus India Pvt. Ltd.

(Bangalore ITAT) ITA

No.352/Bang/2009

Marketing and sales and

other support, customer

No details available on record in respect

of services rendered

Taxpayer has not proved any

commensurate benefits against the

payments of service charges to its

Singapore affiliate

Cost must be allocated on actual basis

and not on pre determine basis

Knorr-Bremse India Pvt. Ltd.

(Delhi ITAT) ITA No. 5097/Del/2011

SAP implementation fees CUP method rejected

AWB India Pvt. Ltd.

(Delhi ITAT) ITA No.

4454/Del/2011

o Not possible to document every receipt of the service in

question

o Tax authorities cannot question the commercial expediency

o CUP method applied by the TPO cannot be considered in

view of non-availability of CUP data

Avery Dennison India Private

Limited v. ACIT (Delhi ITAT) (ITA

No.4868/Del/2014)

o The HC held in the case of the taxpayer that mere

profitability or benefit cannot be the basis for determination

of ALP for intra-group service fee payments.

o The Tribunal, has observed that the intra-group services, if

part of a composite contract, cannot be unbundled for the

purpose ALP determination, and thereby allowed

aggregation of the transaction under TNMM.

Contd…

SN & Co.Chartered Accountants 31

SN & Co.Chartered Accountants 32

BEPS GUIDELINES – ACTION PLAN 10

LOW VALUE ADDED INTRA-GROUP

SERVICES

The guidance defines LVAS are services which are:

o are supportive in nature,

o are not part of the core business of the group,

o do not use or create unique and valuable intangibles, and

o do not involve significant risk.

SN & Co.Chartered Accountants 33

Specific areas to be considered:

o Has a service been provided? : Service that provides economic or commercial value and thatthe recipient would have paid for the activity or else performed the service itself.

o Cost pools: Calculate pool of all costs incurred by all members of the group in performing lowvalue-adding intra-group services. Reduce specific cost and Shareholder costs From it.

o Invoicing: Invoices are often not available where the costs attributed are internallyapportioned direct or indirect costs. In those circumstances an explanation of the logic andprocess applied to arrive at the attributed costs will be needed.

o Allocation keys: Different rationales will be applied in deciding upon the allocation key. Whatis important is that any allocation key can be justified, consistently applied and reviewed on aregular basis.

o Mark-up considerations: As it concerns low value added services, only a modest mark up toan appropriate cost base should be applied. The Guidelines indicate that typically agreedprofit elements tend to falling a range between 3-10%, often around 5%.

Contd…

SN & Co.Chartered Accountants 34

SN & Co.Chartered Accountants 35

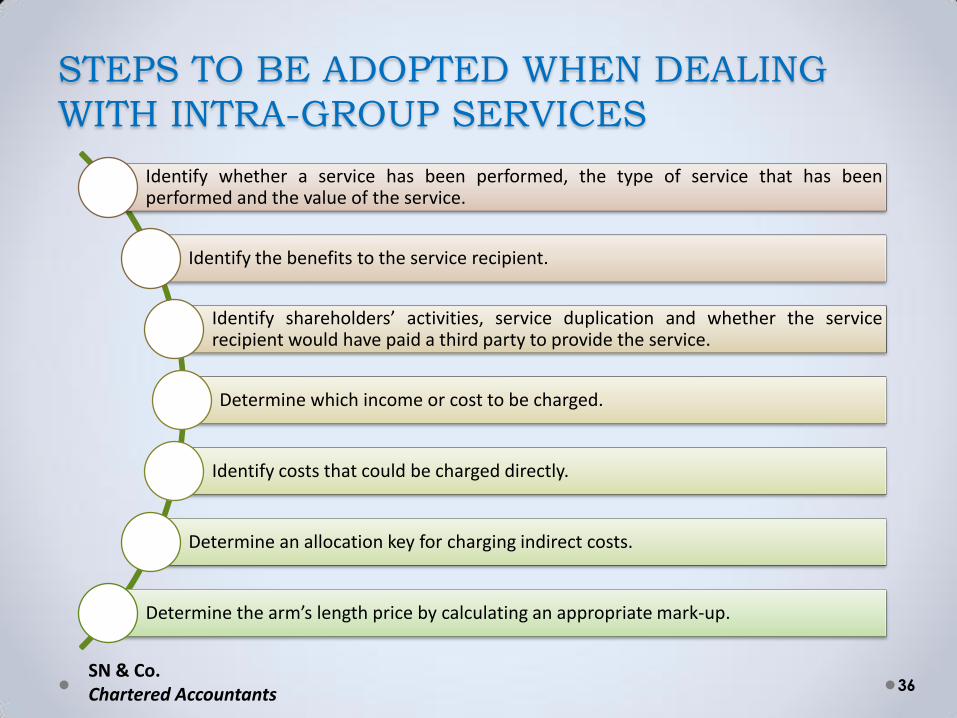

STEPS TO BE ADOPTED WHEN DEALING

WITH INTRA-GROUP SERVICES

Identify whether a service has been performed, the type of service that has beenperformed and the value of the service.

Identify the benefits to the service recipient.

Identify shareholders’ activities, service duplication and whether the servicerecipient would have paid a third party to provide the service.

Determine which income or cost to be charged.

Identify costs that could be charged directly.

Determine an allocation key for charging indirect costs.

Determine the arm’s length price by calculating an appropriate mark-up.

SN & Co.Chartered Accountants 36

INTRAGROUP SERVICES

IGS

Chargeable service

LVAS

TP Simplified

HVAS

Full TP

Non chargeable service

Shareholder Duplication Incidental

37SN & Co.Chartered Accountants

DETERMINATION OF ALP

Minimum price acceptable for provider

Maximum price acceptable for recipient

Range of AL Prices

SN & Co.Chartered Accountants 38

39

QUESTIONS

SN & Co.Chartered Accountants

40

CA. Darshak Shah S N & CoChartered Accountantso Tax o Audit o Consulting

Borivali (w) :::: Sion (w)Tel No. 022-28910968

+91-9699915474Website: www.snco.inEmail Id: [email protected]