Embed Size (px)

Citation preview

TRANSASIA, Ltd. A successful Russian

regional FMCG distribution company

Boston, МА

October 29, 2003

Retail Business in Russia. The Past, 1993-1998

“Wild Times”…

How we started our business

• Time: 1994• Location: Krasnodar• Core business: Wholesale Distribution of FMCG (fast

moving consumer goods)• Partners: Western Manufacturers• Johnson & Johnson, L’Oreal, Procter & Gamble

What was the market

Retail market – total chaos!• Death of old Soviet system• Empty counters in the state stores• Outside kiosks & tables (open-air), flea markets• Flood of low quality or fake goods• Chaotic pricing• Quick (several days) money turnover

What were Transasia’s differences

Start of creation a Western distribution system according to common business practices!

• First distribution company in the city• Quality goods and products• Western brands• Advertising support • High quality customer service• Credit lines for retail outlets

Current Business Environment 1998 - 2003

Grow Market Share as fast as Possible Hyper Growth Period

The present period started in 1998…

Economic crisis in Russia – August 1998

• Consumer purchasing power decreased 3-4 times• Some Western companies left Russian marketplace• Russian manufacturers began to gain market share • Many banks and distributors went bankrupt

TRANSASIA – Facts

• Covers Southern Russia – 12 million people (8% of the total Russian population)

• 1 HQ + 8 regional branches• Over 1,000 employees• 141 delivery vans and trucks• 95 automobiles used by sales representatives

Map of Russia

TRANSASIA – geography of operations

TRANSASIA’s Suppliers

• Total number of suppliers 46

• “Procter & Gamble”• “Kraft Foods”• “Nestle”• “Mars”• “Wrigley”• “Chupa Chups”, “Bic”,

“Cadbury”• Numerous leading Russian

manufacturers

TRANSASIA – Sales Revenues SALES VOLUME (000's)

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

1996 1997 1998 1999 2000 2001 2002 2003

$K

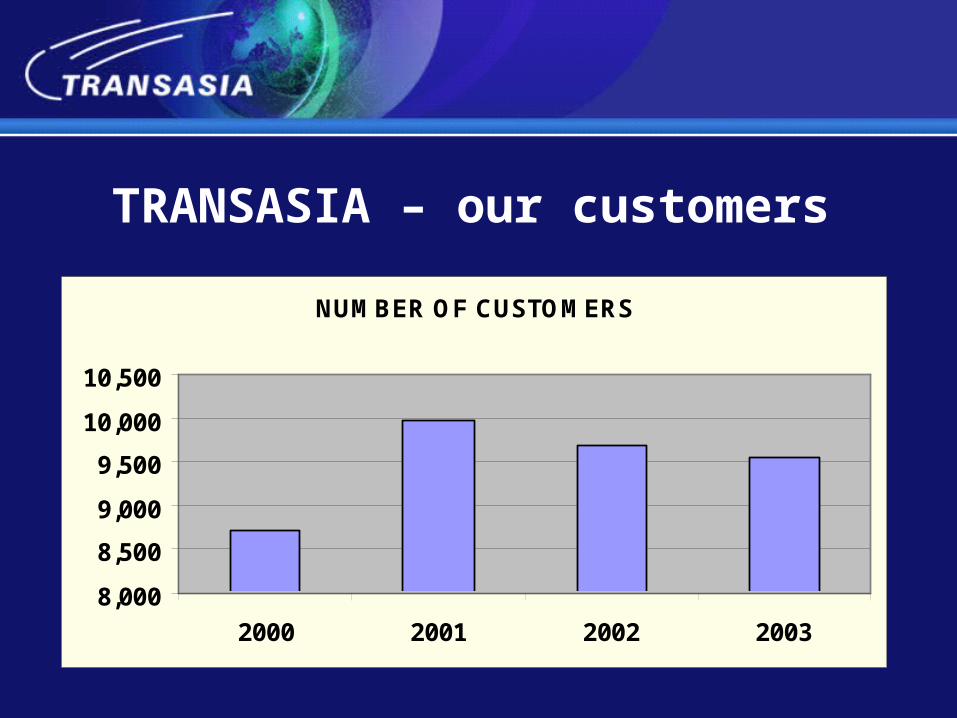

TRANSASIA – our customers

NUMBER OF CUSTOMERS

8,000

8,500

9,000

9,500

10,000

10,500

2000 2001 2002 2003

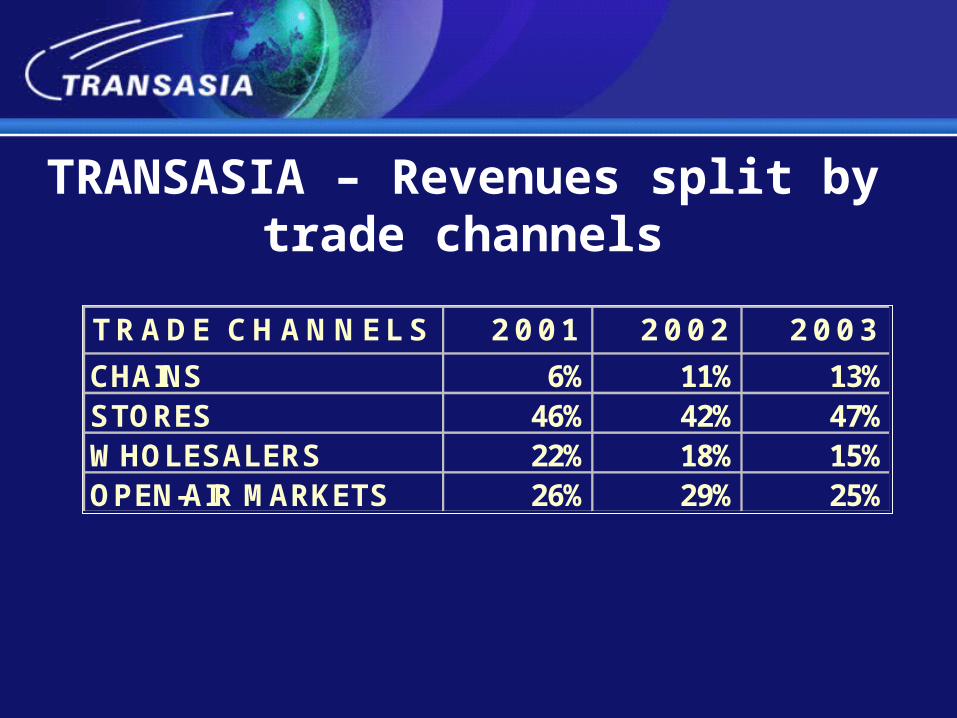

TRANSASIA – Revenues split by trade channels

TRADE CHANNELS 2001 2002 2003

CHAINS 6% 11% 13%STORES 46% 42% 47%WHOLESALERS 22% 18% 15%OPEN-AIR MARKETS 26% 29% 25%

TRANSASIA – Operations

• Our key business – distribution of fast-moving consumer goods (FMCG) to open markets and small shops (50 to 100 sq. m.)

• Sales representatives get orders from clients• All orders are delivered in 24 hours• Our clients are spread all over the region, both in

urban and rural areas• Revenues come mostly in cash

TRANSASIA – Logistics

• During the daytime sales representatives visit our clients to get new orders (use handheld computers)

• In the evening these orders are processed and sent through Internet to main office

• At night time orders are loaded into the big trucks in the distribution center and shipped to the branch offices

• In the morning our vans deliver the goods to the clients

TRANSASIA – geography of operations

TRANSASIA – P&G experience

• P&G products comprise 60% of total revenues• During the period between 1996-98, P&G corporate

loaned Transasia $4 million dollars for capital expenditure purchases (e.g. vans, autos, machinery, etc.). Transasia paid back the capital to P&G in 4 years.

• Working together Transasia and P&G have enabled P&G’s products to capture leading market share positions in the Russian marketplace.

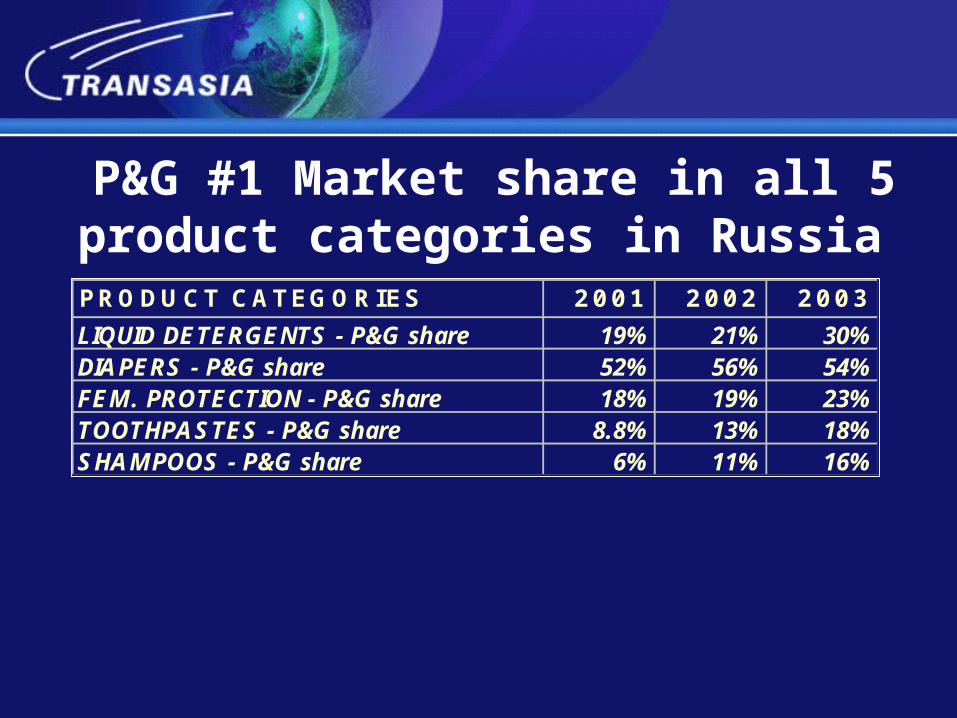

P&G #1 Market share in all 5 product categories in Russia

PRODUCT CATEGORIES 2001 2002 2003

LIQUID DETERGENTS - P&G share 19% 21% 30%DIAPERS - P&G share 52% 56% 54%FEM. PROTECTION - P&G share 18% 19% 23%TOOTHPASTES - P&G share 8.8% 13% 18%SHAMPOOS - P&G share 6% 11% 16%

P&G’s competitors in Russia

• All main P&G competitors work in Russia: “Henkel”, “Unilever”, Kimberly Clark”, “Johnson & Johnson”, “Colgate”, “L’Oreal”

• Low investments into distributors’ development resulted into smaller market share, sales inefficiency, and lack of brand recognition

Conclusions on Current Marketplace• Markets will continue to grow• Small players will disappear and others consolidate• Retail chains are here to stay, their market share will

continue growing quickly• Western retail companies have just recently come to

Russia, mostly to Moscow and St-Petersburg• Open-air markets and small shops still have 70%

market share in the regions• Many opportunities still exist for manufacturers,

distributors, and retailers in the Russian retail marketplace. Capital investment is critical.

The Future for Retail Business in Russia.

90% of Russia’s population lives outside Moscow & St. Petersburg. Wal-Mart

started in the “region” of Arkansas while Target started in the “region” of Minnesota

Future of Retail in Russia – what we start from

• The large territory of Russia and scattered population significantly increases the importance of logistics for retail, especially in the regions

• Although competition currently among distribution companies is fierce, only those companies with technological focus and investment will survive

• Although the opportunities in Russia are huge, it’s critical for Western manufacturers to have local partners to help them navigate the “risks” of Russia.

What will happen in Russia’s regions?

• Purchasing power will increase• Sales volume in each category will grow annually• Rapid growth of the civilized retail channels:

shopping malls, hypermarkets, etc.• Barriers to entry to late players will increase. All the

good locations will be taken.

Additional important information

• Middle class in Russian provinces – ready consumers for your products

• Russian consumer market – moneymaker for number of multinationals (a new ones to come to Russia)

• Krasnodar region – safe, stable and dynamic = “Russian California”

• My other business ventures – how I diversified• Leisure business: “Strike” and “Orange Fitness” =

great success. Payback period less than 3 years.

![ма*!но, витрат'1 /'{'р|к · Аодаток | до ]ф01151770_5 двклАРАц1я про ма*!но, доходи, витрат'1 1 зобов'язання ф|нансового](https://img.dokumen.tips/doc/110x75/5f5ef431d663247f935d7a30/-1-011517705-1.jpg)