Embed Size (px)

Citation preview

CB Richard Ellis | Page 1

705

655,646

OFFICE

4,812PROPERTY ENQUIRIES

M2600US$ WORTH MORE THAN

MILLION

21PROPERTIES

MANAGED

110,000RESIDENTIAL

325MILLION20092009

US$

RETAIL

DEALS CLOSEDWORTH

TRANSACTED VALUE

FOR

COMMERCIAL SPACE M2

400RESIDENTIAL UNITS

66CONSULTANCIES

38QUARTERLY REPORTS

Vietnam Real Estate Update & Market Overview 2010

Presented by:

Marc TownsendManaging DirectorCB Richard Ellis (Vietnam) Co., Ltd.

27th January 2010 Kuala Lumpur Convention Centre

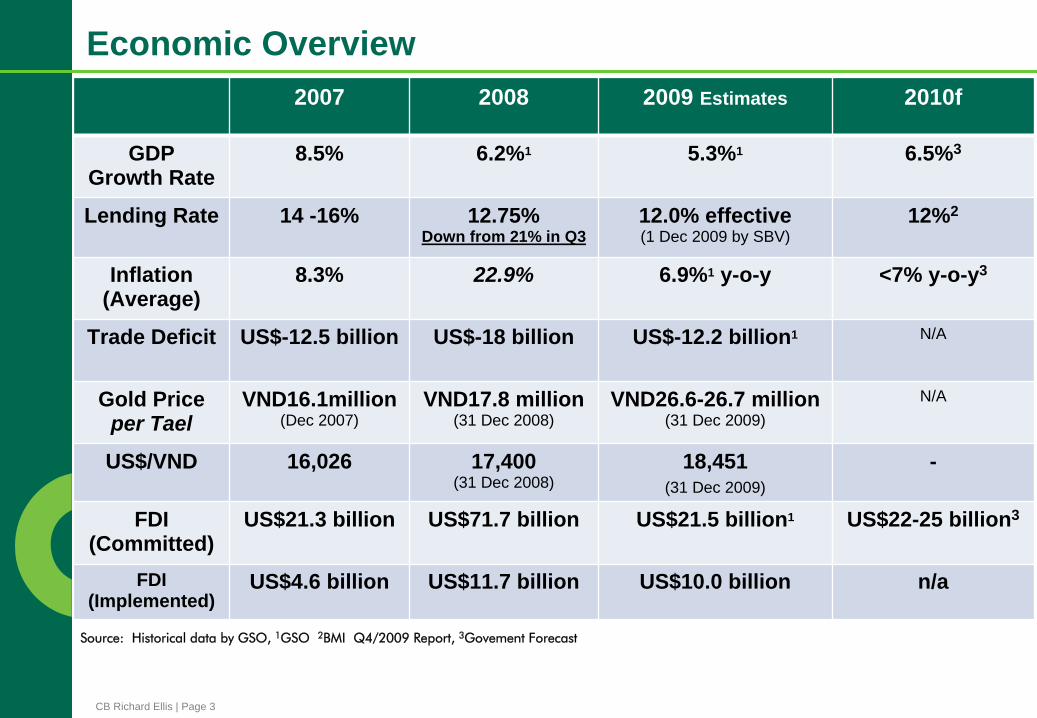

CB Richard Ellis | Page 3

Source: Historical data by GSO, 1GSO 2BMI Q4/2009 Report, 3Govement Forecast

Economic Overview2007 2008 2009 Estimates 2010f

GDP Growth Rate

8.5% 6.2%1 5.3%1 6.5%3

Lending Rate 14 -16% 12.75%Down from 21% in Q3

12.0% effective (1 Dec 2009 by SBV)

12%2

Inflation (Average)

8.3% 22.9% 6.9%1 y-o-y <7% y-o-y3

Trade Deficit US$-12.5 billion US$-18 billion US$-12.2 billion1 N/A

Gold Price per Tael

VND16.1million (Dec 2007)

VND17.8 million(31 Dec 2008)

VND26.6-26.7 million(31 Dec 2009)

N/A

US$/VND 16,026 17,400(31 Dec 2008)

18,451(31 Dec 2009)

-

FDI (Committed)

US$21.3 billion US$71.7 billion US$21.5 billion1 US$22-25 billion3

FDI (Implemented)

US$4.6 billion US$11.7 billion US$10.0 billion n/a

CB Richard Ellis | Page 4

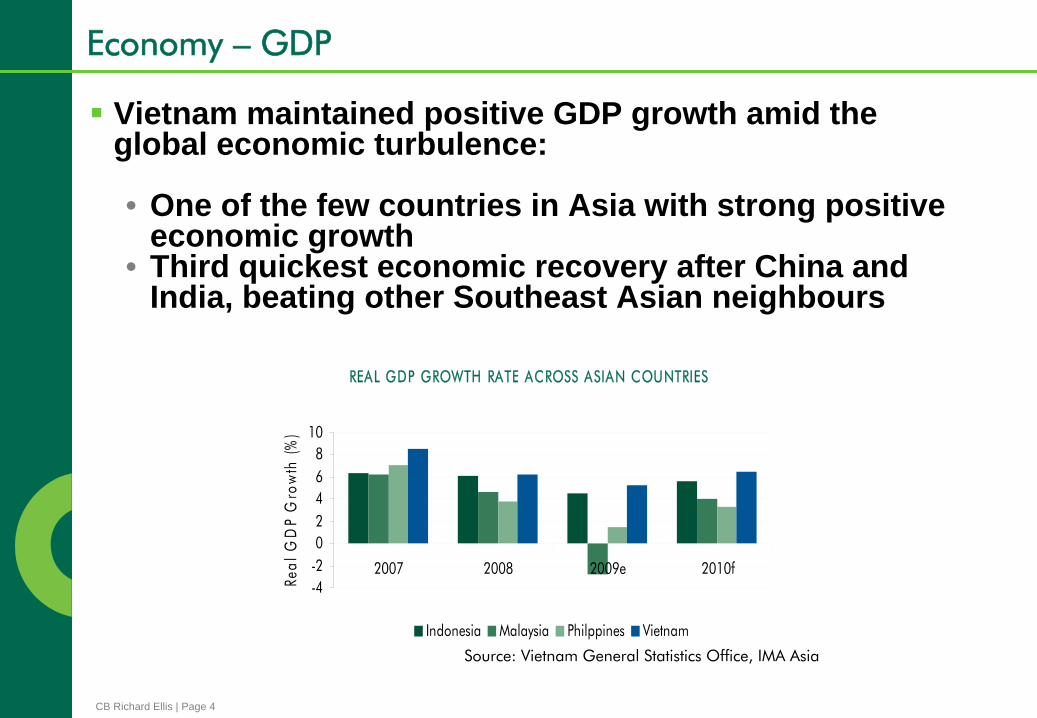

Vietnam maintained positive GDP growth amid the global economic turbulence:

• One of the few countries in Asia with strong positive economic growth

• Third quickest economic recovery after China and India, beating other Southeast Asian neighbours

REAL GDP GROWTH RATE ACROSS ASIAN COUNTRIES

-4-202468

10

2007 2008 2009e 2010f

Real

GD

P G

row

th (%

)

Indonesia Malaysia Philppines Vietnam

Economy – GDP

Source: Vietnam General Statistics Office, IMA Asia

CB Richard Ellis | Page 5

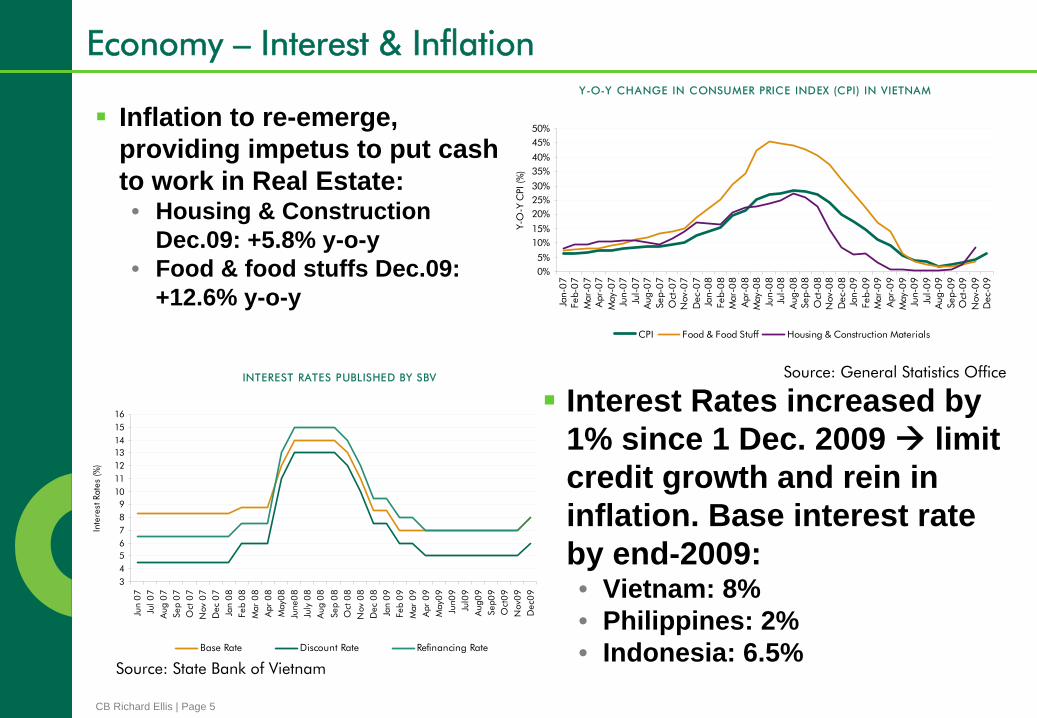

Inflation to re-emerge, providing impetus to put cash to work in Real Estate:• Housing & Construction

Dec.09: +5.8% y-o-y• Food & food stuffs Dec.09:

+12.6% y-o-y

INTEREST RATES PUBLISHED BY SBV

3456789

10111213141516

Jun

07

Jul 0

7A

ug 0

7Se

p 0

7O

ct 0

7N

ov 0

7D

ec 0

7Ja

n 0

8Fe

b 0

8M

ar 0

8A

pr 0

8M

ay0

8Ju

ne0

8Ju

ly 0

8A

ug 0

8

Sep

08

Oct

08

Nov

08

Dec

08

Jan

09

Feb

09

Mar

09

Apr

09

May

09

Jun0

9Ju

l09

Aug

09

Sep0

9O

ct0

9N

ov0

9D

ec0

9

Inte

rest

Rat

es (%

)

Base Rate Discount Rate Refinancing Rate

Economy – Interest & Inflation

Source: State Bank of Vietnam

Y-O-Y CHANGE IN CONSUMER PRICE INDEX (CPI) IN VIETNAM

0%5%

10%15%

20%25%30%

35%40%

45%50%

Jan-

07

Feb-

07

Mar

-07

Apr

-07

May

-07

Jun-

07

Jul-

07

Aug

-07

Sep-

07

Oct

-07

Nov

-07

Dec

-07

Jan-

08

Feb-

08

Mar

-08

Apr

-08

May

-08

Jun-

08

Jul-

08

Aug

-08

Sep-

08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

Feb-

09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-

09

Aug

-09

Sep-

09

Oct

-09

Nov

-09

Dec

-09

Y-O

-Y C

PI (%

)

CPI Food & Food Stuff Housing & Construction Materials

Source: General Statistics Office

Interest Rates increased by 1% since 1 Dec. 2009 limit credit growth and rein in inflation. Base interest rate by end-2009:• Vietnam: 8%• Philippines: 2%• Indonesia: 6.5%

CB Richard Ellis | Page 6

FDI dropped dramatically compared to 2008, but still second highest year on record2009 registered FDI: US$21.48 billion

•2009 implemented FDI: US$10 billion

•Implemented FDI dropped less than 15%

•2010: US$22-25 billion (MPI forecast)

FOREIGN DIRECT INVESTMENT (FDI) INTO VIETNAM

-5

1015202530354045505560657075

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009p

FDI (

US$

Bill

ions

)

Total Capital Implemented Capital

Source: General Statistics Office, Ministry of Planning and Investment

Economy – FDI

2007 2008 2009 Estimates

Vietnam US$21.3 bil

US$71.7 bil

US$21.4 bil

Philippines US$4.6 bil

US$4.1 bil

US$1.5bil

Malaysia n/a U$$12.9 bil

n/a

Indonesia US$10.3 bil

US$18.5 bil

US$30 bil

CB Richard Ellis | Page 7

Gold now consolidating: around VND26.6mil – 26.7mil/tael

Stock market slowed toward year end, but potential for more foreign funds in 2010

DOMESTIC GOLD PRICE

05,000,000

10,000,00015,000,00020,000,00025,000,00030,000,000

Dec

-08

Jan-

09

Feb-

09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-

09

Aug

-09

Sep-

09

Oct

-09

Nov

-09

Dec

-09

VND

/Tae

l

Source: Saigon Jewelry

Holding Company

Economy – Gold & Stock Market

CB Richard Ellis | Page 8

US$/VND QUARTERLY INTER-BANK EXCHANGE RATE

13,000

14,000

15,000

16,000

17,000

18,000

19,000

Mar

-99

Jun-

99

Sep-

99

Dec

-99

Mar

-00

Jun-

00

Sep-

00

Dec

-00

Mar

-01

Jun-

01

Sep-

01

Dec

-01

Mar

-02

Jun-

02

Sep-

02

Dec

-02

Mar

-03

Jun-

03

Sep-

03

Dec

-03

Mar

-04

Jun-

04

Sep-

04

Dec

-04

Mar

-05

Jun-

05

Sep-

05

Dec

-05

Mar

-06

Jun-

06

Sep-

06

Dec

-06

Mar

-07

Jun-

07

Sep-

07

Dec

-07

Mar

-08

Jun-

08

Sep-

08

Dec

-08

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Confidence in the Dong – still devaluation pressure in the short term but stability should return on export strength & reduction of stimulus

Source: State Bank of Vietnam

Economy – Exchange Rates

CB Richard Ellis | Page 9

2010 Government Decrees….

Further clarifications expected on the ownership regulations for Resident Foreigners and Viet Kieu

2010 Market waiting to feel impact of new announcement that does not permit residences to be used as offices

Current debate over allowing developers to pre-sell 20% of their development directly, outside of current regulations

The Personal Income Tax (PIT) on housing transactions went into effect on September 26, 2009• New flat tax on transactions rather than multiple options which simplifies

collections• 2010 will see the implementation of the collection of these taxes

CB Richard Ellis | Page 10

Half of Lang – Hoa Lac Highway opened in October 2009 with completion expected in late 2010 or early 2011

Major regional highways broke ground and made progress with Hanoi – Lao Cai, Hanoi – Thai Nguyen, and Hanoi – Hai Phong Highway all starting •

Huge impact in 5-10 years especially for the provinces

Regional Infrastructure

Photo of Hanoi –

Hai Phong Highway

Photo of Lang –

Hoa Lac Highway

CB Richard Ellis | Page 11

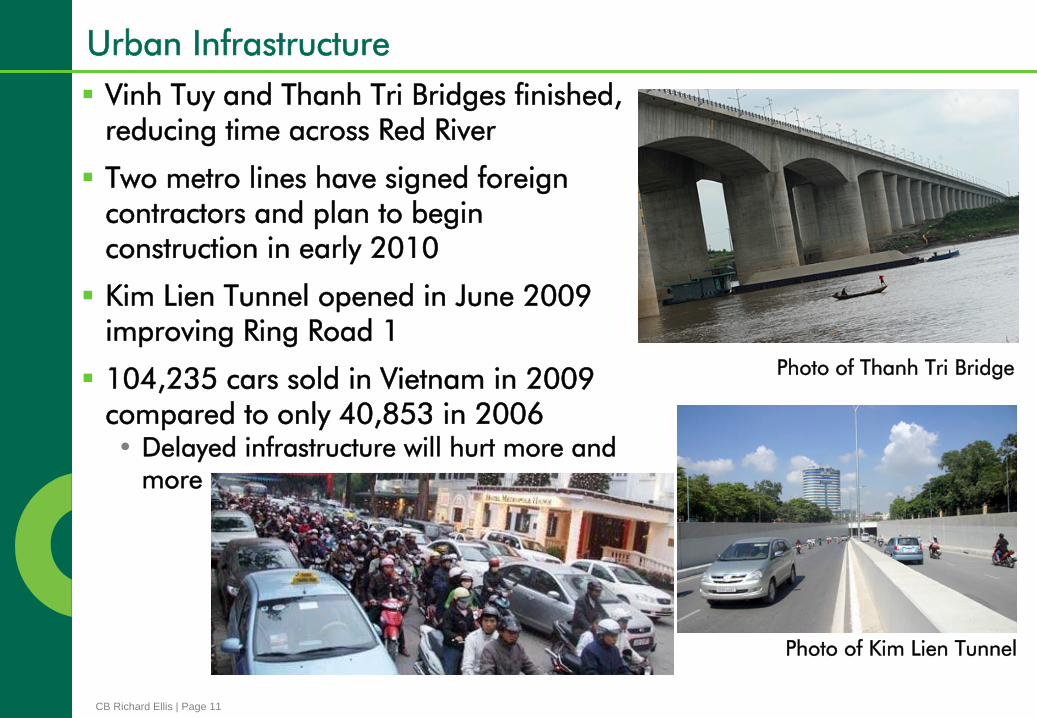

Urban Infrastructure

Photo of Thanh Tri Bridge

Photo of Kim Lien Tunnel

Vinh Tuy and Thanh Tri Bridges finished, reducing time across Red River

Two metro lines have signed foreign contractors and plan to begin construction in early 2010

Kim Lien Tunnel opened in June 2009 improving Ring Road 1

104,235 cars sold in Vietnam in 2009 compared to only 40,853 in 2006•

Delayed infrastructure will hurt more and more

CB Richard Ellis | Page 12

Seaports• First vessel into Saigon Premier

Container PortAirports• DANANG

First flight from Taipei. Planned 2010 flights from Japan. New International Airport to be completed 2010.

• DALATNew international airport completed

• NHA TRANG / CAM RANHFirst international flight from Singapore. Planned 2010 flights from Russia.

Lack of regular international flights to destinations outside of Hanoi and HCMC.

2009 Infrastructure Milestones – Air & Sea

Saigon Premier Container Port

Lien Khuong Int’l Airport - Dalat

CB Richard Ellis | Page 13

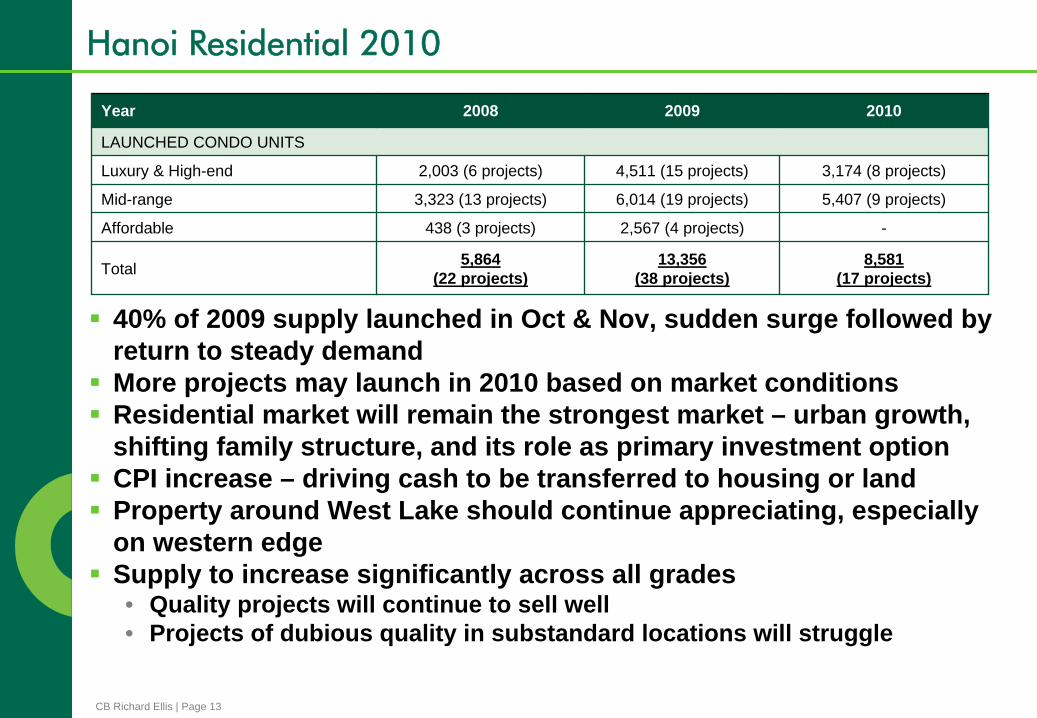

40% of 2009 supply launched in Oct & Nov, sudden surge followed by return to steady demandMore projects may launch in 2010 based on market conditionsResidential market will remain the strongest market – urban growth, shifting family structure, and its role as primary investment optionCPI increase – driving cash to be transferred to housing or landProperty around West Lake should continue appreciating, especially on western edgeSupply to increase significantly across all grades • Quality projects will continue to sell well• Projects of dubious quality in substandard locations will struggle

Hanoi Residential 2010

Year 2008 2009 2010

LAUNCHED CONDO UNITS

Luxury & High-end 2,003 (6 projects) 4,511 (15 projects) 3,174 (8 projects)

Mid-range 3,323 (13 projects) 6,014 (19 projects) 5,407 (9 projects)

Affordable 438 (3 projects) 2,567 (4 projects) -

Total 5,864(22 projects)

13,356(38 projects)

8,581(17 projects)

CB Richard Ellis | Page 14

Don’t fall into the trap• The market for units priced above $2,000 psm is limited. Projects

need prime location, high grade advisors / contractors (architects, marketing, quality control), extensive facilities, and limited units

• Handover of high-end and luxury projects in 2010. Good gauge of true demand (Vincom, Golden Westlake, Sky City Towers)

Anything over 1,000 units—cut costs, eliminate frills, create efficient unit sizes and target the middle to upper-middle class market ($1,000 to $1,600 psm)

Villas will remain the aspiration of most families, but people will come to terms with rising urban land costs• Choice between condominiums in urban core or villas on the fringe

Expect more pressure from government to progress with lower cost housing

Hanoi Residential - Outlook

CB Richard Ellis | Page 15

Mid-range market will dominate transaction activity with more launches if demand persistsSmall niche demand for luxury projects will remain•

Prime locations, limited units (~100), respected developers

Still heavy speculation, but end-users exist•

Observe hand-over of high end projects in 2010, who is living there?

Overall market pricing should trend down as more projects focus on large middle and upper-middle class market with price points below $1,500 psmSuburban projects will introduce Hanoi to benefits of living outside core city• More space• Dramatically reduced prices for similar quality• Air quality, improved environment

Hanoi Residential - Outlook

CB Richard Ellis | Page 16

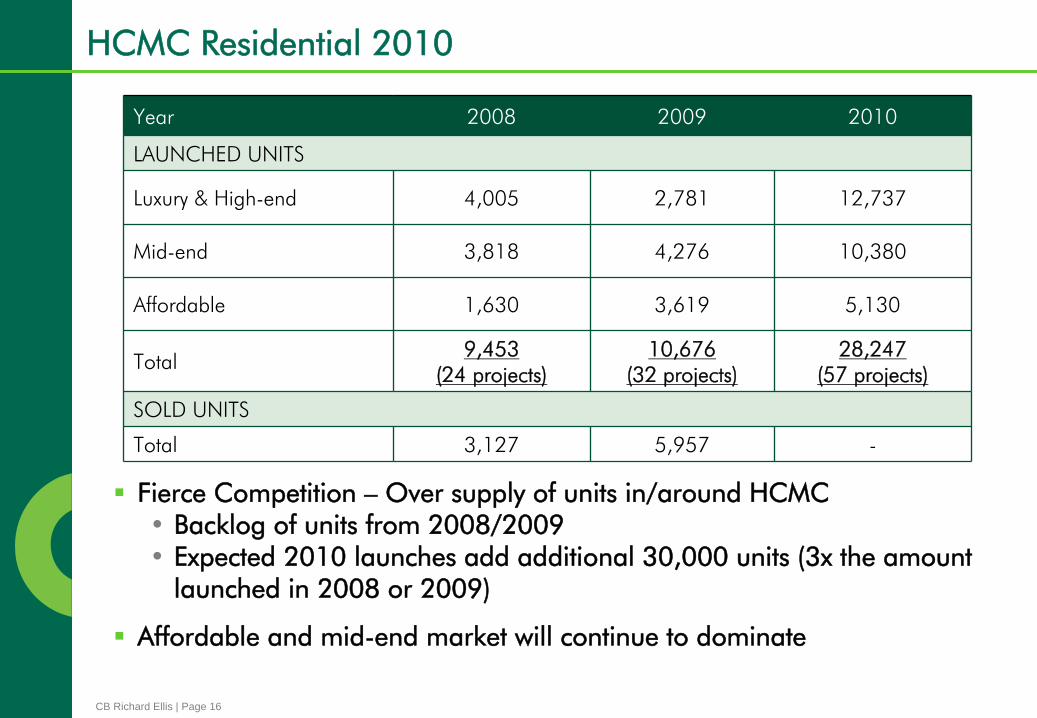

Fierce Competition – Over supply of units in/around HCMC •

Backlog of units from 2008/2009•

Expected 2010 launches add additional 30,000 units (3x the amount launched in 2008 or 2009)

Affordable and mid-end market will continue to dominate

HCMC Residential 2010

Year 2008 2009 2010

LAUNCHED UNITS

Luxury & High-end 4,005 2,781 12,737

Mid-end 3,818 4,276 10,380

Affordable 1,630 3,619 5,130

Total 9,453(24 projects)

10,676(32 projects)

28,247(57 projects)

SOLD UNITS

Total 3,127 5,957 -

CB Richard Ellis | Page 17

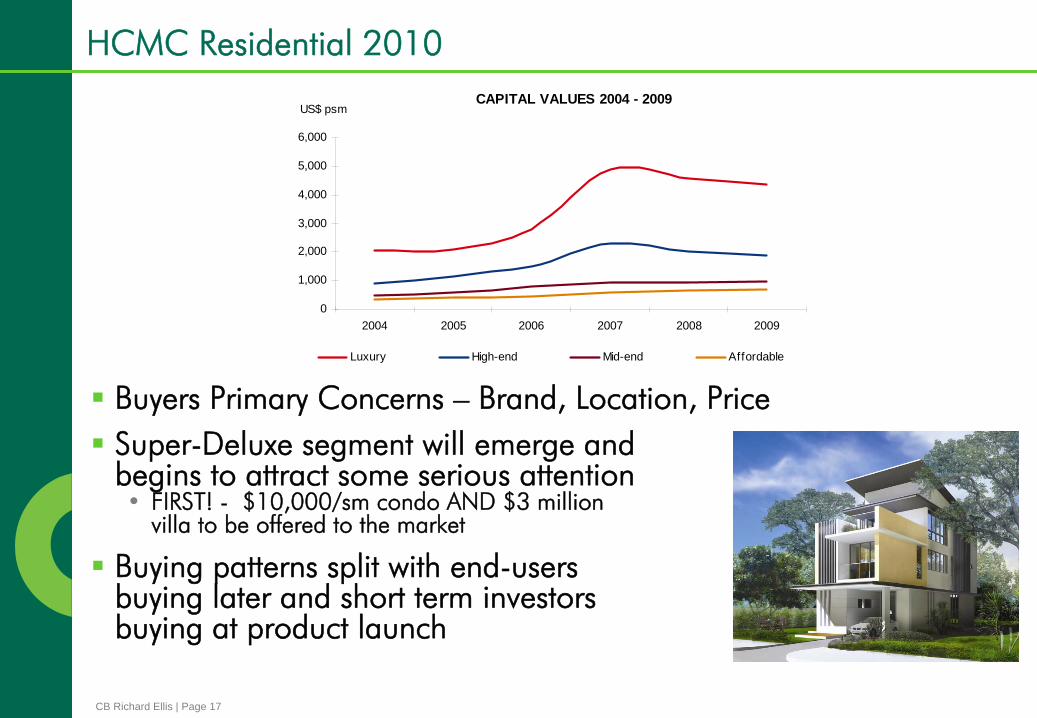

Buyers Primary Concerns – Brand, Location, PriceSuper-Deluxe segment will emerge and begins to attract some serious attention •

FIRST! -

$10,000/sm condo AND $3 million villa to be offered to the market

Buying patterns split with end-users buying later and short term investors buying at product launch

HCMC Residential 2010 CAPITAL VALUES 2004 - 2009

0

1,000

2,000

3,000

4,000

5,000

6,000

2004 2005 2006 2007 2008 2009

US$ psm

Luxury High-end Mid-end Affordable

CB Richard Ellis | Page 18

Second Home Markets•

Hoa Binh / Ha Tay

–

Different concept (mountains) but still early. Need to be near traditional resort area (Mai Chau, Ba Vi, Tam Dao)

•

Danang

–

Strong supply, demand may diminish due to the rise of other locations

•

Nha Trang –

Enters the Residential home market with multiple condominium projects launching in 2010. Strong competitor to Danang with more developed tourist market (local & international)

•

Long Hai / Vung Tau –

Continued interest in these convenient vacation get-aways

but with limited opportunities

•

Mui

Ne / Phan Thiet –

The Superstar of 2010 with multiple opportunities for home ownership, golfside, beachside or hillside, villa or condo, traditional or modern. Access is limited to buses and cars

•

Dalat

Target buyers will be Vietnamese. Foreign buyers are no longer the main target of these homes.•

Beach units will rely on foreigners for rental pool after completion

Second Home Market 2010

CB Richard Ellis | Page 19

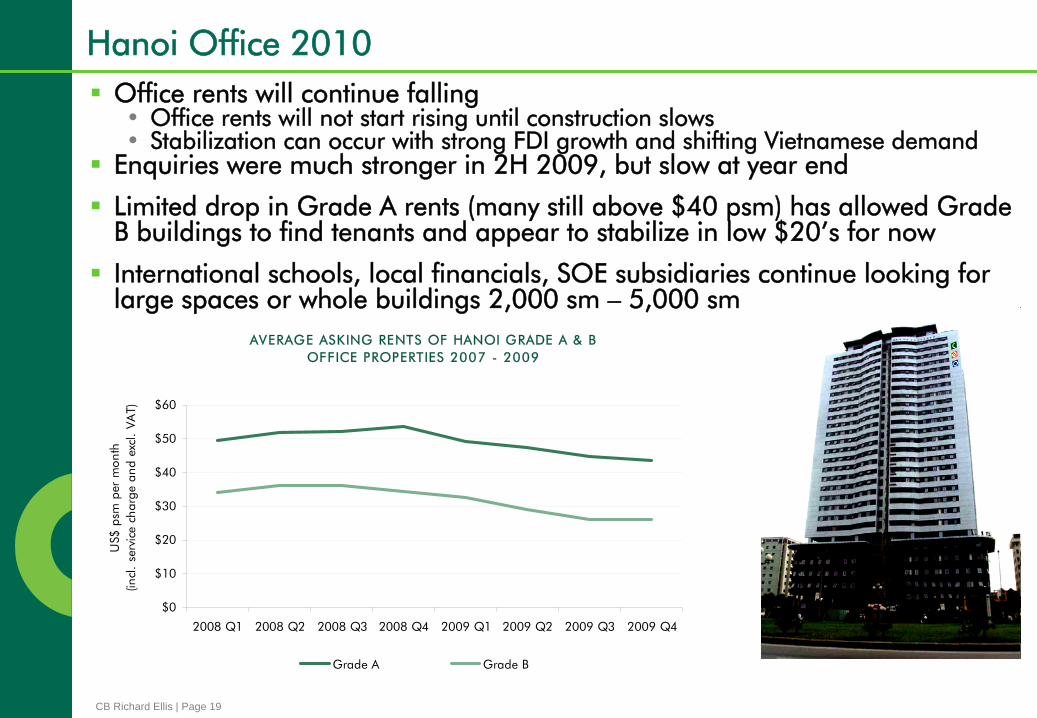

Office rents will continue falling•

Office rents will not start rising until construction slows•

Stabilization can occur with strong FDI growth and shifting Vietnamese demandEnquiries were much stronger in 2H 2009, but slow at year end

Limited drop in Grade A rents (many still above $40 psm) has allowed Grade B buildings to find tenants and appear to stabilize in low $20’s for now

International schools, local financials, SOE subsidiaries continue looking for large spaces or whole buildings 2,000 sm – 5,000 sm

Hanoi Office 2010

AVERAGE ASKING RENTS OF HANOI GRADE A & B OFFICE PROPERTIES 2007 - 2009

$0

$10

$20

$30

$40

$50

$60

2008 Q1 2008 Q2 2008 Q3 2008 Q4 2009 Q1 2009 Q2 2009 Q3 2009 Q4

US$

psm

per

mon

th(in

cl.

serv

ice

char

ge a

nd e

xcl.

VAT)

Grade A Grade B

CB Richard Ellis | Page 20

Most of the take-up is at new buildings and generally at rents under $25 per sm

2010 should see absorption at almost double 2009, but still moresupply

Despite continued strong net absorption, 53,000 sm of Grade A and B space is still empty and looking for tenants at the end of2009 with over 150,000 sm of more space coming in 2010

Concerns about oversupply with huge market changing buildings guaranteed to open in the next two years: Keangnam (90,000 sm NFA), Grand Plaza (Charmvit) (45,000 sm NFA); EVN Tower (45,000 sm NFA); Capital Tower (23,000 sm NFA); Crown Complex (16,000 sm NFA) and more

Hanoi Office 2010

2008 2009

Net absorption (sm) 16,769 52,730

Lowest net absorption during Q2.08 –

Q1.09: -13,346 sm

CB Richard Ellis | Page 21

Developers finally coming to terms with the idea of stable or falling rental levels•

Long terms leases are a win-win with both the tenant and landlord getting security

•

Developers will follow example of CEO Tower (10-50 year leases), only new building to stabilize in current market (5% vacancy, 3 months after opening)

More large companies, mainly local, will look to consolidate offices, expecting longer leases and favorable rentalsStabilizing new buildings will continue to rent at rates below comparable existing buildings•

May outperform existing offices in mid-term, but need to stabilize firstIf rentals continue to fall in new well located Grade A or B+ buildings, beware of major movement when the rent saved actually covers the cost of the move•

Remember most tenants did not lease at the market peak. Most Grade A tenants are paying between $25 and $40 psm

Hanoi Office - Outlook

CB Richard Ellis | Page 22

Significant increase in office enquiries at the end of 2009, expected to continue

Over 100,000 sm of vacant space carries over

2010 will see a more new space come on-line than 2008 & 2009 combined – more than 350,000 sm

Take up will double from 2009 - c.300,000 sm

Amount of new and existing supply ensures that 2010 is the year of the tenant

Demand will come from existing Vietnamese firms and MNC’s expanding into Vietnam

Image is key – your office/building is a reflection of your business

HCMC Office 2010AVERAGE ASKING RENTS, HCMC OFFICE MARKET

$0.0

$20.0

$40.0

$60.0

$80.0

Q1.07 Q2.07 Q3.07 Q4.07 Q1.08 Q2.08 Q3.08 Q4.08 Q1.09 Q2.09 Q3.09 Q4.09

US$

/sm

/mon

th

Grade A Grade B Grade C Average rents (US$/sm/month)

CB Richard Ellis | Page 23

Tenant/Investor Strategies•

Extend lease lengths as rental prices bottom out

•

Strata titling –

buy floors

•

Take a headlease

on a building, lease extra space

•

Buy a completed building, it’s cheaper than developing

Landlord Strategies•

New realism to attract tenants –

fit out cost contribution, lower asking

prices, greater overall flexibility•

The most profitable landlords will look for incomesother than rent -

building sponsorship,

communication company income•

Lead with a LEED building

•

Keep the faith –

buildings will fill out

HCMC Office 2010

CB Richard Ellis | Page 24

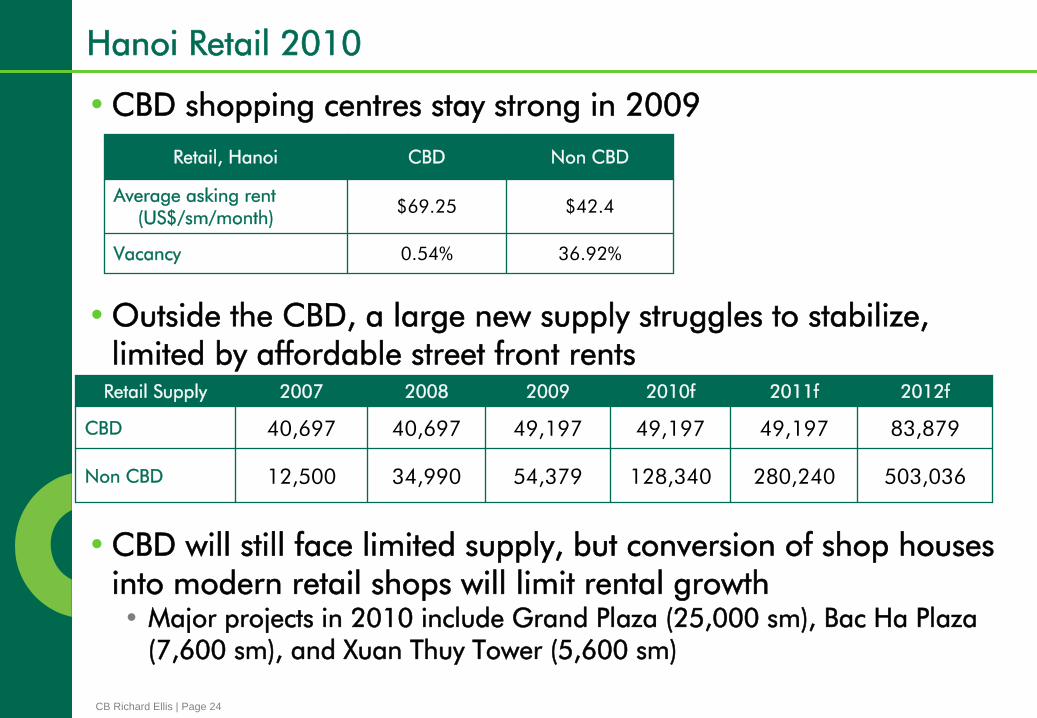

• CBD shopping centres stay strong in 2009

• Outside the CBD, a large new supply struggles to stabilize, limited by affordable street front rents

• CBD will still face limited supply, but conversion of shop houses into modern retail shops will limit rental growth•

Major projects in 2010 include Grand Plaza (25,000 sm), Bac Ha Plaza (7,600 sm), and Xuan Thuy Tower (5,600 sm)

Retail, Hanoi CBD Non CBD

Average asking rent

(US$/sm/month)

$69.25 $42.4

Vacancy 0.54% 36.92%

Hanoi Retail 2010

Retail Supply 2007 2008 2009 2010f 2011f 2012f

CBD 40,697 40,697 49,197 49,197 49,197 83,879

Non CBD 12,500 34,990 54,379 128,340 280,240 503,036

CB Richard Ellis | Page 25

• Wet markets are in the process of converting to enclosed shopping centres. What will be the outcome?

• Hanoi now has 6.5 million residents with growing urbanization along major transport routes. Suburban retail will follow•

Decentralization over the Red River (Savico

Plaza) and to the west (The Garden, Grand Plaza Hanoi, Keangnam etc)

• Renovated shophouses will continue to play main role in CBD (Nine West, FCUK, Calvin Klein Jeans, Converse, Mango all in shophouses)

• Challenge of ENT hampers access for overseas retailers• Biggest expansion came from F&B

•

Not JV’s or foreign entrants, just local franchisee with branding rightsCBD rental rates should remain stable despite limited new supply due to rapid redevelopment of existing shophousesOutside the CBD, newer shopping centres will stabilize as more local and mid-market brands take advantage of the major population centres to the west and south of the city

Hanoi Retail - Outlook

CB Richard Ellis | Page 26

Supply of prime CBD retail space to triple in 2010New retail space shifts from shophouse to shopping mallsNon CBD space to increase almost 50% All CBD space to be absorbed as demand remains strong and current supply is limited – top rental prices to increaseDemand to come from:•

Expanding Vietnamese retail chains –

nationwide rollout•

International and Vietnamese F & B•

Arriving International brands as WTO hangover wears off

Large scale international brand operators (Tesco/Wal-Mart) remain on the sidelinesFranchising will be key to (local) F&B expansion

HCMC Retail 2010

Retail New Supply (sm)

2007 2008 2009 2010f

CBD 1,280 11,882 18,781 65,050

Non CBD 24,000 50,300 46,687 68,000

CB Richard Ellis | Page 27

Underground retail:•

Growing as traditional street-side retail space is limited•

Vincom

Centre leading the pack with this trend•

Others join in with adaptations –

La Van Tam Park to break ground in 2010

Market-style retail to expand:•

Saigon Square I & II will be copied•

Consumers have confidence in what they know

•

Short-term developments capitalisingon underused land slated for redevelopment

•

Located in densely populated areas•

Quick set-up allows investors to gainalmost immediate returns

•

Rental rates higher than formal settings

HCMC Retail Opportunities 2010

CB Richard Ellis | Page 28

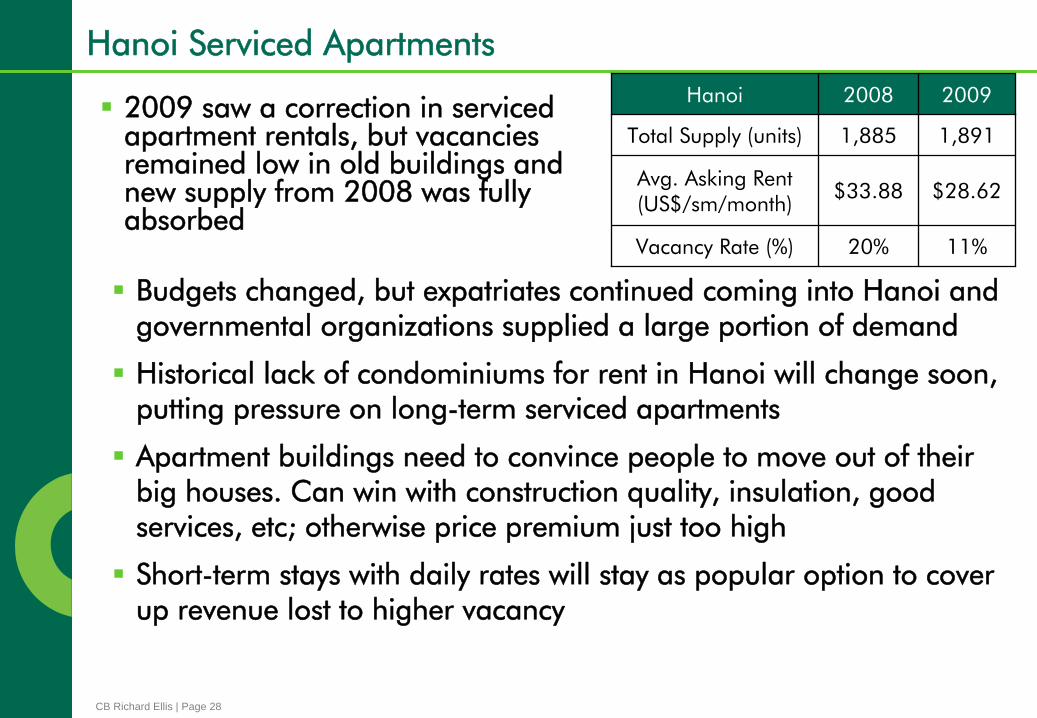

2009 saw a correction in serviced apartment rentals, but vacancies remained low in old buildings and new supply from 2008 was fully absorbed

Hanoi Serviced Apartments

Budgets changed, but expatriates continued coming into Hanoi andgovernmental organizations supplied a large portion of demand

Historical lack of condominiums for rent in Hanoi will change soon, putting pressure on long-term serviced apartments

Apartment buildings need to convince people to move out of theirbig houses. Can win with construction quality, insulation, good services, etc; otherwise price premium just too high

Short-term stays with daily rates will stay as popular option to coverup revenue lost to higher vacancy

Hanoi 2008 2009

Total Supply (units) 1,885 1,891

Avg. Asking Rent (US$/sm/month)

$33.88 $28.62

Vacancy Rate (%) 20% 11%

CB Richard Ellis | Page 29

310 units in 2010, plus further boutique projects

Demand could grow with more businesses entering Hanoi•

New entrants to Vietnam and firms already in HCMC hoping to take

advantage of growth in Hanoi

Yet to see many large scale standard rental apartments (The Manor), but more buy-to-let will be available in 2010

Best serviced apartments already stabilized, newer projects or older buildings may continue to see rentals slip but could stabilize during 2010•

Hanoi tenants stayed during recession but asked for rent adjustments or moved to cheaper buildings

Will hotel sponsored serviced apartments succeed? (Charmvit, Crown Complex, Keangnam) Can tenants afford the premium?

Hanoi Serviced Apartments – 2010: Stable Year

Est. New Supply (units) 2010f 2011f 2012f

Hanoi 310 254 260

CB Richard Ellis | Page 30

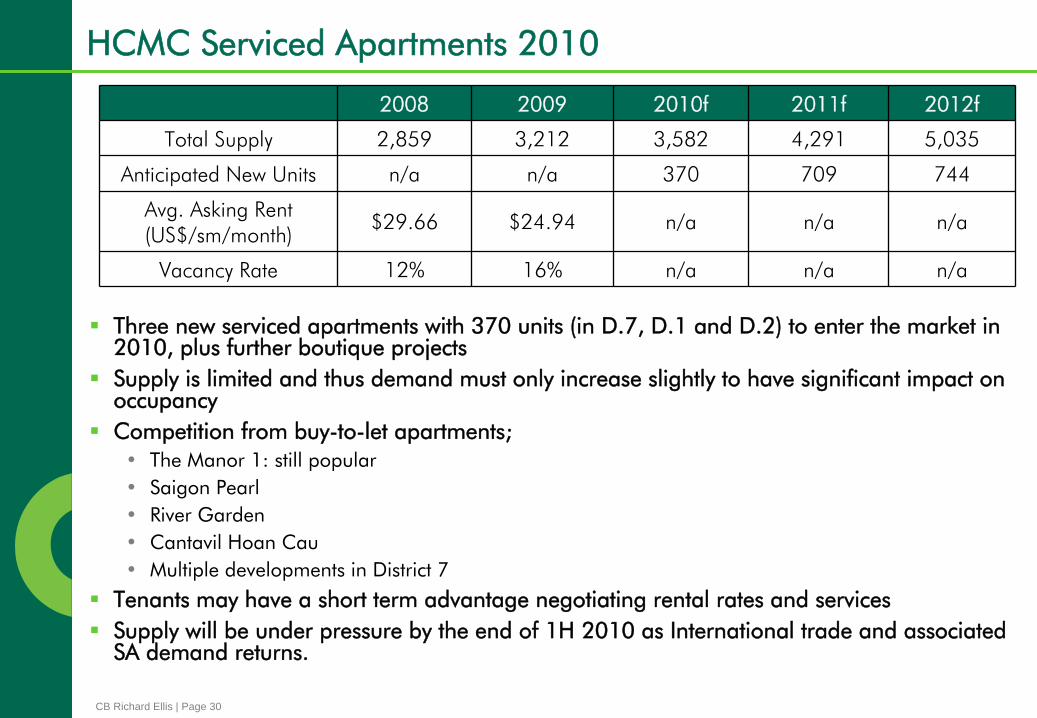

Three new serviced apartments with 370 units (in D.7, D.1 and D.2) to enter the market in 2010, plus further boutique projectsSupply is limited and thus demand must only increase slightly to have significant impact on occupancyCompetition from buy-to-let apartments;

•

The Manor 1: still popular •

Saigon Pearl•

River Garden•

Cantavil

Hoan

Cau•

Multiple developments in District 7

Tenants may have a short term advantage negotiating rental rates and servicesSupply will be under pressure by the end of 1H 2010 as International trade and associated SA demand returns.

HCMC Serviced Apartments 2010

2008 2009 2010f 2011f 2012f

Total Supply 2,859 3,212 3,582 4,291 5,035

Anticipated New Units n/a n/a 370 709 744

Avg. Asking Rent (US$/sm/month)

$29.66 $24.94 n/a n/a n/a

Vacancy Rate 12% 16% n/a n/a n/a

CB Richard Ellis | Page 31

New brands are entering the market, creating variety (Mercure, Marriott, Pullman, Holiday Inn, and more)

Arrivals to Hanoi in 2009 / in comparison with 2008• International arrivals

: 1.03 million, 11.7%

• Local arrivals

: 6.7 million, 1.8%

Hanoi Hotel 2010

QUARTERLY ADR AND OCCUPANCY RATE OF HANOI 5-STAR HOTELS IN 2008 - 2009

0.00

50.00

100.00

150.00

200.00

Q1/08 Q2/08 Q3/08 Q4/08 Q1/09 Q2/09 Q3/09 Q4/09

0.00%

20.00%

40.00%

60.00%

80.00%

Average Daily Rate (ADR) Occupancy rate

Occupancies looking much better in Q3 and Q4 2009 with improving numbers for 2010

•ADR will remain in current position longer

CB Richard Ellis | Page 32

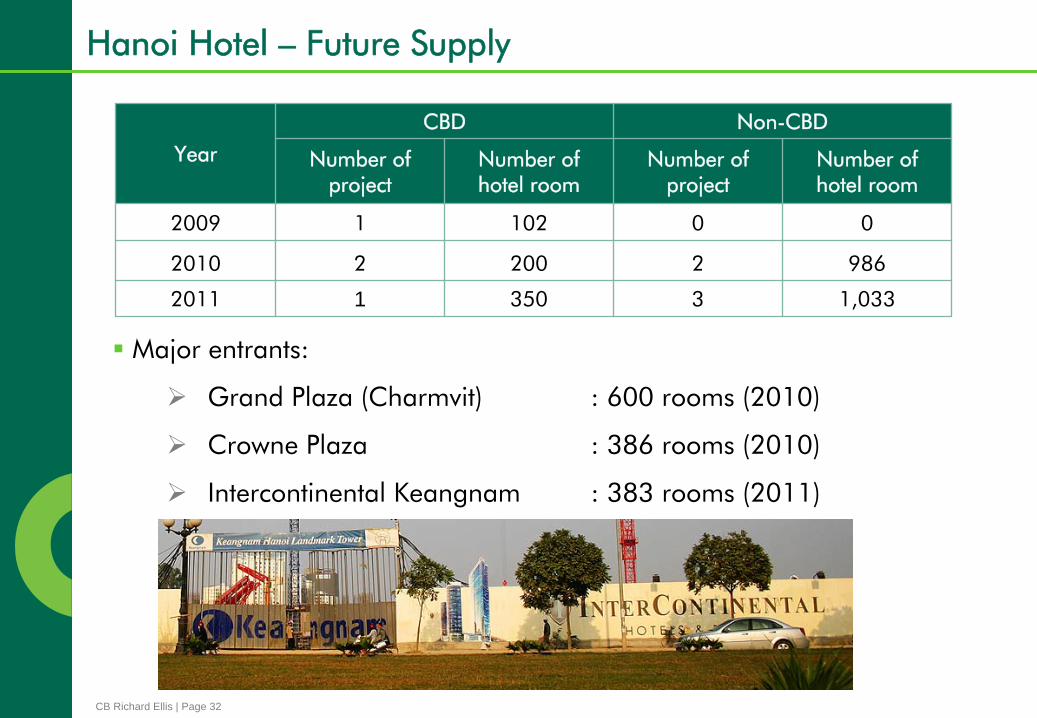

Year

CBD Non-CBD

Number of project

Number of hotel room

Number of project

Number of hotel room

2009 1 102 0 0

2010 2 200 2 986

2011 1 350 3 1,033

Major entrants:

Grand Plaza (Charmvit) : 600 rooms (2010)

Crowne Plaza : 386 rooms (2010)

Intercontinental Keangnam : 383 rooms (2011)

Hanoi Hotel – Future Supply

CB Richard Ellis | Page 33

Huge recovery of hotel occupancy occurred in 2H 2009 and will carry into 2010•

This will not create any sustained growth in ADR•

Temporary spike in ADR should occur in Q3 2010 due to 1000th

anniversary

CBD hotels could see ADR growth by year end with upswing in tourism and business travel. New hotels to the west limited by lack of tourist appealMore local brands will expand, taking advantage of strong domestic travelInternational budget flags will continue to expand in Hanoi, HCMC and the tier-2 cities

Hanoi Hotel - Outlook

CB Richard Ellis | Page 34

High season occupancy rates (to date) on par with previous years and expected to steadily recover the remainder of the year •

Already 85%-95% occupancy during peak weeks

Strong growth in local demand

Return of international business travelers and MICE

Vietnamese companies going international•

Saigon Tourist in the US, Saigon Investment Group in Laos

Local developers invest in/develop hotels

Expansion of hotel brands and styles•

Local brands expand nationally•

Increased competition in the top end segment •

New International Brands -

IBIS (D1&D7) & Nikko (D1)•

International Budget Brands will enter•

Smaller boutique hotels (not star rated)• Business hotels in Industrial Parks

HCMC Hotels 2010

CB Richard Ellis | Page 35

HCMC Hotel – Future Supply

Year of Completion

Project Management Location No. of rooms

2010

(473 rooms)

LIBERTY 6 Self D.1 144

GOLDEN TOWER Self D.1 120

SAIGON GIVRAL Self Phu Nhuan 209

2011

(1,175 rooms)

NEW PACIFIC Self D.3 120

GRAND EXTENTION Self D.1 170

NIKKO SAIGON Nikko D.1 335

TIMES SQUARE Self D.1 230

LE MERIDIEN SAIGON Starwood D.1 320

2012

(858 rooms)

NOVOTEL SAIGON CENTRE Accor D.1 350

IBIS BEN THANH PALACE Accor D.1 338

IBIS SAIGON SOUTH Accor D.7 170

2013SAIGON CONVENTION AND EXHIBITION

Self D.7 1,000

Total 3,506

CB Richard Ellis | Page 36

Demands for high quality and strategically positioned logistics warehousing will continue to increase though will not be fully met in 2010

Industrial market will return to an inbound market as foreign manufacturers rebound

Industrial park landlords and managers will reluctantly begin to soften their positions on pricing and fees

Industrial park developers will come back to the market seeking opportunities

Northern industrial market will gain attention as road infrastructure improves and airports and seaports support more international transport

Hanoi Industrial 2010

CB Richard Ellis | Page 37

Carry over vacancy from 2009 results in•Industrial park landlords may soften on

pricing and fees •Factory owners have offered the lower prices.

Strong demand for small-to-middle size manufacturers requiring for land lots between 1,000-5,000sm

Opportunities for ready-built/build-to-suit developers as manufacturers enter with specific needs that current supply can not meet

Demand for Logistic Centres (Warehouse/Distribution Centres/ICDs)

•In the new port areas; SPCT (Hiep

Phuoc), Port of Singapore Authority and Saigon New Port (in Cai

Mep-Thi Vai). •Warehousing in Cat Lai Port Area.

HCMC Industrial 2010

CB Richard Ellis | Page 38

Change in land prices driven by infrastructure•

Three Stages–

Planned–

Under Construction–

Opening (Completion)

As a road or other project progresses through each stage, risk of delay or failure decreases•

Leading to adjustment in land prices•

Longer delay between stages makes any progress more unexpected

Major projects that could change stages in 2010:•

Cat Linh –

Ha Dong Metro Line (starting construction)•

Lang –

Hoa Lac Highway (completion)•

Ring Road 3 •

Nhat Tan Bridge for Dong Anh (bridgehead construction)•

Hanoi –

Hai Phong Highway (starting construction in Hanoi)

Land in Hanoi 2010

CB Richard Ellis | Page 39

Vietnamese investors will continue to dominate

Foreign investment will begin to trickle back in slowly, but will focus on an equal basis, Hanoi - HCMC

Foreign investors going to the provinces/under developed districts to combat land prices

Real Estate Funds to continue to divest and consolidate

More IPO listings as capital markets recover

Local developers will utilise increasingly sophisticated fundraising options in Vietnam and abroad Investors/retailers look at purchasing long-term lease of retail podiums• Failure of self-managed podiums present opportunities

Investment 2010

CB Richard Ellis | Page 40

Office take up will double but rents not to recover until 2011

Hotel occupancies to recover by the second half of 2010

ENT problems persist, local retail demand will be insatiable

Local developers continue to lead the way – tallest, biggest and most expensive

Traffic congestion will restrict daily life and limit spending

The super-deluxe condo / villa market will attract some serious attention

District 9 will spawn ten new villa projects

The number of real estate funds will shrink and characteristics will change

Serviced apartment demand will recover by the end of the first half

“Go on, be a Tiger”

CBRE’s MOST Fearless Forecasts 2010

CB Richard Ellis | Page 41

A Millennium of Thang Long - HanoiHanoi and HCMC converging in developmentInvestment and development market from local and foreign groups swung away from HCMC to Hanoi in 2009 and this trend will continue throughout 2010Residential market continues in popularity as Hanoians show preference for real estate over stocksServiced apartment, hotel & office market not just supported by stable demand from embassies, NGOs, Development Organizations (ADB, World Bank)Townships and complexes have struggled for many years to go through clearance and approvals – become a sub-developer and start building in one!Government pressure and support for the 1000th anniversary will lead to strong progress for Hanoi throughout 2010

Hanoi – Coming of Age –

Final Thoughts

CB Richard Ellis | Page 42

Economic Overview

Current Rents and Prices

Office

Retail

Hotel

Residential for Sale

Investment

Serviced Apartments

Construction Costs

Quarterly Reports for Ho Chi Minh City and Hanoi

Available for each city, in English or Vietnamese

CB Richard Ellis | Page 43

5153

THANK YOUwww.cbrevietnam.com

© 2009 CB Richard Ellis, We obtained the information above from sources we believe to be reliable. However, we have not verified its accuracy and make no guarantee, warranty or representation about it. It is submitted subject to the possibility of errors, omissions, change of price, rental or other conditions, prior sale, lease or financing or withdrawal without notice. We include projections, opinions, assumptions or estimates for example only, and they may not represent current or future performance of the property. You and your tax and legal advisors should conduct your own investigation of the property and transaction.