Embed Size (px)

Citation preview

Traditional Chinese Medicine Industry

Oct 31, 2016 Equity Research | Healthcare

Modernization creating opportunities and driving growth

Natalie Chiu SFC CE No. AVH029 [email protected] +852 3760 2030 GF Securities (Hong Kong) Brokerage Limited 29-30/F, Li Po Chun Chambers 189 Des Voeux Road Central Hong Kong

Traditional Chinese medicine market to expand rapidly Traditional Chinese Medicine

(TCM) in China enjoyed more rapid growth than other segments of the pharmaceutical industry in 2011-14. Driven by an increasingly aging population, rising GDP per capita, expanding medical insurance programs and urbanization, we believe it will continue to expand rapidly, delivering a 15%+ CAGR in sales during 2015-19. The industry will also benefit from favorable government policies for the Chinese medicine industry, and we expect it to be globally competitive over the long term. For Chinese patent/finished medicines, companies face a tougher operating environment due to slower organic growth amid tough competition. For modern Chinese medicines, favorable policies are leading to the emergence of new companies. Sector trading at an unjustified discount The Chinese medicine segment is now

trading at 15x 2017E P/E, vs 17x for chemical drugs players. We believe this discount is due to a lack of understanding among investors of individual companies’ business models. Solid earnings and industry consolidation could trigger a re-rating. Overall, we believe the near-term risk-reward profile is attractive. Initiating coverage of China TCM, Kingworld Medicines, and Beijing Tong Ren Tang

We initiate coverage of China TCM (570 HK, Buy), Kingworld Medicines (1110 HK, Buy), and Beijing Tong Ren Tang CM (8138 HK, Accumulate) with one-year target prices of HK$5.20, HK$1.80 and HK$12.30, respectively, implying 30%, 22% and 9% upside from their latest closing prices. China TCM is the TCM arm of China National Pharmaceutical Group Corporation, Sinopharm’s (1099 HK, NR) parent company The company produces traditional patent

medicines (finished TCM) and modern Chinese medicine (concentrated TCM granules, or CCMG). The company has a diversified finished TCM portfolio with more than 500 prescription and OTC products. In concentrated TCM granules, it is among the top-five CCMG players that together account for 50% of the market. Kingworld Medicines to grow through M&A and organic development Kingworld has

a sound growth strategy, aiming to: 1) expand its high-GM product offerings; 2) increase online sales, and; 3) penetrate lower-tier city markets. With a proven ability for product integration, we expect the company to continue to grow faster than the industry average during 2016-18, with further penetration into lower-tier provinces and cities, and improved profitability through a better product mix and greater operating efficiency. Beijing Tong Ren Tang Medicine is the largest proprietary Chinese medicine exporter in China With 62 self-operated stores outside China, Tong Ren Tang CM now

has one of the largest TCM retail networks in Asia. The company operates a TCM clinics-centric model and relies on product revenue generated from providing TCM consultation services. It currently offers two self-manufactured products: Angong Niuhuang Pills and ganoderma lucidum spores powder.

Stock valuations

Sources: Company data, GF Securities (Hong Kong) Note: As of Oct 18, 2016

Mkt Cap PEG (x)

Ticker Rating (HK$ m) Price TP FY15 FY16E FY17E FY18E FY15 FY16E FY17E FY18E FY15 FY16E FY17E FY18E FY17E FY15 FY16E FY17E FY18E FY15 FY16E FY17E FY18E

Guangzhou BYS 874 HK NR 44,629 19.08 NR 15.4 15.9 14.7 13.5 9 9 13 6 7 (4) 9 8 1.7 2 6 6 1 16.1 14 13 14

CTCM 570 HK Buy 17,682 3.99 5.20 20.4 13.5 11.3 9.8 51 85 21 17 3 51 20 16 0.6 40 83 17 16 9.1 10 11 12

TRT Tech 1666 HK NR 19,929 15.56 NR 30.0 26.9 23.6 21.7 17 32 14 13 14 12 14 9 1.7 19 14 14 6 14.4 13 14 15

TRT CM 8138 HK Accumulate 9,309 11.12 12.30 26.7 21.0 18.3 15.8 23 28 16 17 20 27 15 16 1.0 28 13 15 16 20.9 22 22 19

Kingworld Med 1110 HK Buy 915 1.47 1.80 26.7 15.4 10.4 8.2 (18) 79 50 28 (22) 73 48 27 0.2 8 41 20 17 5.0 9 12 14

Shineway 2877 HK NR 6,674 8.07 NR 8.2 10.1 10.1 12.6 (7) (22) (6) (5) (8) (19) 0 (20) NA (8) (13) (3) (1) 12.9 9 9 8

Simple average 21.2 17.1 14.7 13.6 13 35 18 13 2 23 18 9 1 15 24 11 9 13 13 13 14

P/E (x) Net profit growth (%) EPS growth (%) Revenue growth (%) ROE (%)

Oct 31, 2016

2

Sector report

Traditional Chinese medicine sector to grow faster than chemical drugs in 2016-20 In 2011-14, the traditional Chinese medicine (TCM) sector grew faster than chemical drugs but slower than biologics. Frost & Suillivan estimates that the segment will continue to expand rapidly and deliver an 8.2% CAGR in sales during 2016-20. In 2015, wholesale revenue for TCM products in China reached approximately Rmb392bn, and accounted for around 32% of the country’s total pharmaceutical market. In terms of sales volume, TCM currently represents around two-thirds of drug sales in China. The faster growth in TCM compared to the conventional drug industry is attributable to: 1) government investment and favorable policies for the healthcare sector; 2) increasing demand for TCM due to the high incidence of chronic diseases; 3) extended applications of Chinese medicines, and; 4) changing consumer perceptions of Chinese medicines.

Figure 1: Breakdown of China’s pharmaceutical market (2011-2020E)

Sources: Frost & Sullivan, GF Securities (Hong Kong)

Favorable government policy support The Chinese government has set TCM as a strategic

priority and has issued supportive policies. Most recently, the State Council issued a formal notice as part of the 13th Five-Year Plan on the development of the TCM industry. Specifically, by 2020, it wants every citizen to be able to enjoy quality TCM services through balanced progress in TCM medical care, scientific research, education and culture. The government will undertake efforts to ensure that for every 1,000 people, there will be 0.55 beds in public TCM hospitals and 0.4 licensed TCM doctors. The State Council encouraged the establishment of a TCM service network that covers both urban and rural areas. Additionally, it called for the protection and industrialization of TCM herbs, as well as innovation in the TCM industry.

Figure 2: Key TCM-related initiatives in the 13th Five-Year Plan

Sources: SATCM, GF Securities (Hong Kong)

473.3 529.7 595.3 646.3 683.6 720.5 748.8 790.1 790.1 878

210.3259.3

314359

391.8423.8 460.4

500.4 542.2580.6

59.475.2

86.2116.7

145.3180.1

225.4258.7

298.7

333.3

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

Chemical Drug TCM Biologics

Rmb bn, at wholesale level

Development plan Specific action points Target

Enhance TCM primary servicing capabilities Relax entry barriers to TCM services Increase the share of private TCM medical healthcare

institutions by 5% from 2015 to 20% of overall TCM services

Improve TCM services network to cover urban and rural areas Reach 70% TCM service coverage in all community health

service institutions, township hospitals and village clinics.

Ensure equal rights for private and public Chinese medical healthcare institutions

Promote TCM rehabilitation services Improve the function of TCM as emergency and preventive treatments Set up TCM rehabilitation departments in all Class-2 or above

TCM hospitals, 30% of maternal and child health centers, all

community health service institutions, and township hospitals.

50% of village clinics should provide TCM health intervention

services.

Support the development of TCM nursing homes for the elderly

Establish chains of TCM rehabilitaion institutions

Promote inheritance of TCM and other ancient Chinese

medicine

Organize personnel training, conduct scientific research, encourage technological

development and protect of intellectual property

Establish 3-5 international research platforms for TCM.

Develop 8-10 international scientific exchanges.

Establish 50 TCM innovation teams with a total oft 300 leading

scientists.

Accelerate TCM practitioner training Standardization of Chinese medicine residency training Ensure all Chinese medical practitioners possess postgraduate

medical degree with standardized training.

Strengthen TCM apprentice education Establish a national TCM training center and 50 TCM

apprentice education centers.

Nurture TCM culture and promote healthcare-related

tourism

Strengthen the cultural awareness and literacy on TCM Construction of 70 TCM education bases and 30 TCM culture

experience centers.

Promote TCM's core values and cultivate a healthy lifestyle

CAGR 2011-15 2016-20E

Chemical drug 9.6% 5.1%

TCM 16.8% 8.2%

Biologics 25.0% 18.1%

Total 13.2% 8.0%

Oct 31, 2016

3

Sector report

Competitive TCM landscape Traditional Chinese medicine is divided into 1) Chinese patent

medicines, 2) decoction pieces and 3) Chinese herbs. Chinese patent medicines are defined as any Chinese herbal medicine formulated into a finished dose form, while decoction pieces are mainly Chinese herbs that have been processed further. Historically, Chinese patent medicines account for about 50% of all traditional Chinese medicines sold, but decoction pieces now make up an increased share following their faster growth. Sales growth of Chinese patent medicines slowed from 40% in 2012 to 9% in 2014, while sales growth in the decoction pieces market rose from 22% in 2012 to 24% in 2014, based on industry data provided by chyxx. Development of modernized decoction technology such as ultra-fine pulverization has led to continued strong growth in the decoction pieces market.

Figure 3: TCM industry overview

Sources: IMS, GF Securities (Hong Kong)

Low market concentration Currently, the industry remains fragmented with different market

players of various sizes. According the China Association of TCM, there are more than 1,500 Chinese patent medicine manufacturers and 800 decoction pieces manufacturers in China. In terms of market revenue, the top 5 manufacturers of Chinese patent medicines and decoction pieces accounted for approximately 29% and 70% of the respective total revenue in 2013, including many state-owned enterprises.

Figure 4: Annual revenue at TCM companies Figure 5: Market share of top-10 TCM companies

Sources: chyxx, GF Securities (Hong Kong)

The rise of modern TCM Facing tough competition from local manufacturers and potential drug

quality issues, sales growth of Chinese patent medicines and traditional decoction pieces has continued to decline. Amid rising costs, the margins of these TCM players have remained under pressure and profitability has deteriorated. Industry players are expanding into new segments to seek higher growth. The introduction of concentrated Chinese medicine granules (CCMG) in China has created new opportunities for industry players. Over the long term, the market will be consolidated and we expect to see the emergence of several dominant national players.

Chinese patent

medicines, 46%

Decoction pieces,

42%

Chinese herbs ,

12%

traditional

decoction pieces, 41%

modern

decoction pieces (including CCMG),

1%

Rmb10m or below, 91.27%

Rmb10-30m, 3.79%

Rmb30-50m, 1.48%

Rmb50-100m, 1.43%

Rmb100-300m, 1.3%

Rmb300-500m. 0.3%

Rmb500-1bn, 0.23%

Rmb1-5bn, 0.16%

Rmb5bn or above, 0.04%

29%

69%

Chinese patent medicines Decoction pieces

Oct 31, 2016

4

Sector report

Figure 6: Historical and projected sales in the Chinese patent medicine market (2010-19)

Figure 7: Historical and projected sales of decoction pieces market (2010-19)

Sources: chyxx, GF Securities (Hong Kong)

TCM standardization crucial for its modernization The Chinese government has made

significant efforts to promote standardization of TCM in recent years. The aim is to align with practices in western medicine, meaning we could see the implementation of international standards, while TCMs will remain a drug class with unique features.

Figure 8: The national standards on TCM in China

Sources: Ministry of Health, CFDA, GF Securities (Hong Kong)

Evidence-based clinical trials In contrast to chemical drugs whose properties can be elucidated

via precise comparisons with current standards of care, proving the therapeutic value of TCMs is more difficult given its compound nature. The problem is more obvious in decoction TCMs with varying dosages. Despite this challenge, double-blind randomized controlled trials (RCTs) have been performed on various compound TCMs to study their safety and efficacy. Based on expert evaluations, it was found that the proportion of published RCTs in relation to all types of published clinical trials increased from 19% in 1999 to 36% in 2004. Academics generally believe Chinese medicine now has a better PK/PD profile compared with its previous status, but more effort is needed to ensure quality of the trials.

0%

10%

20%

30%

40%

50%

60%

0

50

100

150

200

250

300

350

400

450

2010 2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E

Revenue YoY %

Rmb bn

0%

10%

20%

30%

40%

50%

60%

70%

0

200

400

600

800

1000

1200

1400

1600

1800

2010 2011 2012 2013 2014 2015 1H16

Decoction pieces (Rmb100m) YoY %

Years A seies of standards

1953 Chinese Pharmacopoeia

1989 Drug Standards of the Ministry of Health (Finished Herbal Products Volume)

1992 Drug Standards of the Ministry of Health (Herbs Volume)

1999 Regulations for New Drug Approval

1999 Good Clinical Practices

1999 Good Laboratory Practices

2000 Good Supply Practices

2001 Good Manufacturing Practices

2002 Good Agriculture Practices

2005 Clinical Medicine Guidelines (Traditional Chinese Medicines Volume)

2010 Clinical Medicine Guidelines (Herbal Material Volume)

Oct 31, 2016

5

Sector report

China TCM (570 HK)

Buy (initiation)

Target price: HK$5.20

Emerging TCM leader

Natalie Chiu SFC CE No. AVH029 [email protected] +852 3760 2030 GF Securities (Hong Kong) Brokerage Limited 29-30/F, Li Po Chun Chambers 189 Des Voeux Road Central Hong Kong

TCM arm of CNPGC China TCM (CTCM) is the TCM arm of China National

Pharmaceutical Group Corporation, Sinopharm’s (1099 HK, NR) parent company. The company produces traditional patent medicine (finished TCMs) and modern Chinese medicine (concentrated TCM granules, or CCMG). It has a diversified finished TCM portfolio with more than 500 prescription and OTC products. In concentrated TCM granules, it is among the top-five CCMG players that together account for 50% of the market.

Becoming vertically integrated Five large acquisitions since 2006 have transformed

CTCM into an integrated TCM conglomerate covering decoction pieces, granules, patent medicines and supplement products. Total revenue and net profit rose at CAGRs of 30.1% and 62.2% respectively during 2007-15. Reform to lead to long-term shareholder value CTCM’s finished drug sales volume

growth and drug prices have come under pressure amid the currently severe market environment. To address pricing pressure, the company aims to: 1) actively adjust its product strategies to alleviate pressure on its finished drug business; 2) accelerate expansion of its concentrated TCM granules business, and; 3) overhaul its sales team. Strategic planning in its CCMG business The concentrated TCM granules market in

China has experienced rapid growth due to its regulated nature. With deregulation expected in the near future, the company has brought forward the integration of Tianjiang Pharma and promoted resource sharing to achieve synergy and improve core competitiveness. Attractive valuation The stock is currently trading at 11.4x 2017E P/E, compared to the

current average of 15x for other TCM manufacturers listed in Hong Kong. As an emerging leader in the TCM space with a faster-than-peers growth outlook, we believe CTCM’s discount to its HK-listed peers should narrow. Our one-year target price of HK$5.20 is based on a target P/E of 15x our 2017 EPS forecast of Rmb0.30 and represents 0.5x PEG. Risks 1) More aggressive price cuts for its key Essential Drug List drugs; 2) Weaker-than-

expected volume growth following tender withdrawals; 3) More intense competition after the CCMG market is liberalized.

Stock valuation

Sources: Company data, GF Securities (Hong Kong)

Turnover

(Rmb m)

Net profit

(Rmb m)

EPS

(Rmb)

EPS YoY

(%)

P/E BPS

(Rmb)

P/B ROE

(%)

2014 2,650 412 0.16 68% 21.2 1.3 2.7 13%

2015 3,709 622 0.17 3% 20.5 3.0 1.1 8%

2016E 6,805 1,150 0.25 51% 13.6 2.7 1.3 9%

2017E 7,930 1,388 0.30 20% 11.4 2.9 1.2 11%

2018E 9,218 1,623 0.35 16% 9.8 3.1 1.1 12%

Stock performance

Source: Bloomberg

Key data

Source: Bloomberg

-40%

-20%

0%

20%

40%

60%

80%

100%

Oct

-14

No

v-1

4

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

570 HK Equity Hang Seng Index

Oct 27 close (HK$) 4.01

Shares in issue (m) 4.43

Major shareholder Sinopharm HK (36%)

Market cap (HK$ bn) 17.903

3M avg. vol. (m) 12.67

52W high/low (HK$) 6.42/2.89

Oct 31, 2016

6

Sector report

Weak finished drug growth amid stringent drug pricing Reimbursement control hurting finished drug sales growth Since 2015, the Chinese

government has deepened healthcare reform with reform of the drug approval process, implementation of the “two-invoice system”, and secondary drug tender policies. While these initiatives have spurred development in the industry, sales growth has slowed from 23% (for finished TCMs) and 24% (for decoction pieces) in 2013 to 8% and 13% respectively in 1H16.

Figure 9: Finished drugs market revenue (2010-1H16) Figure 10: Decoction pieces market revenue (2010-1H16)

Sources: MIIT, GF Securities (Hong Kong)

Finished TCMs under more pricing pressure than overall pharma sector Sales growth of

finished TCMs was only half that of the overall pharma sector during 2015-1H16, due to: 1) the zero-mark up policy aimed at bringing the contribution from drug sales to hospital revenues to 30% by 2017, and; 2) TCM drugs being a common form of complementary medicine leading to more pricing control. Only companies with flexible growth strategies can survive in this dynamic industry environment. CTCM to adjust product strategy in 2016 CTCM has over 500 products (70 of which are national

exclusive products), used for musculoskeletal, respiratory, dermatology and central nervous system problems, as well as infectious and cardiovascular diseases. The Tongjitang acquisition in May 2013 led to rapid growth in finished products in 2014. However, sales growth momentum weakened to 3.8% in 2015 and -20% in 1H16 due to an inventory build-up following the elimination of the second and third layers of distributors under the “two-invoice system”. Inventory rose to four months by the end of 2015 (two months under normal conditions).

Figure 11: CTCM’s top-ten finished products in 2015

Sources: Company data, GF Securities (Hong Kong)

Sales restructuring began at end-2015 Rather than focusing on ex-factory sales, CTCM has

adopted a partner/responsible person system whereby sales are now focused on in-market sales. The company’s conventional marketing line has changed from geography-based to product-based, which includes three business units responsible for selling the seven exclusive Essential Drug List (EDL) products, OTC products and about 60 non-EDL national exclusive products respectively. This provides better financial flexibility allowing them to monitor stock across channels, manage sales planning and performance, and control inventory. The sales revamp should help to unlock product potential and digest inventory at hospitals or OTC channels more quickly, in our view.

0%

5%

10%

15%

20%

25%

0

1000

2000

3000

4000

5000

6000

7000

2010 2011 2012 2013 2014 2015 1H16

Finished TCM (Rmb100m) YoY %

0%

10%

20%

30%

40%

50%

60%

70%

0

200

400

600

800

1000

1200

1400

1600

1800

2010 2011 2012 2013 2014 2015 1H16

Decoction pieces (Rmb100m) YoY %

Drug Name Drug Type Therapeutic Area Indication Sales (Rmb m) YoY %

Xianling Gubao TCM Musculoskeletal Osteoporosis 862.19 1.4%

Yupingfeng Granule TCM Infectious diseases Cold 271.14 8.4%

Jingshu Granule TCM Musculoskeletal Cervical spondylosis 224.91 12.2%

Moisturising & anti-itching Capsule TCM Dermatology 202.50 27.8%

Biyankang Granule TCM Respiratory Rhinitis 168.71 -34.1%

Sheng Tong Ping Chemical Cardiovascular Hypertension 99.51 3.60%

Fengshi Gutong Capsule TCM Musculoskeletal Rheumatoid arthritis 73.67 39.6%

Zaoren Anshen Capsule TCM CNS Insomnia 71.18 22.9%

Feng Liao Xing Medicinal Wine TCM Musculoskeletal Rheumatism 65.94 -19.2%

Gao De Chemical Infectious diseases Bacterial infection 59.33 -31.9%

2015

Oct 31, 2016

7

Sector report

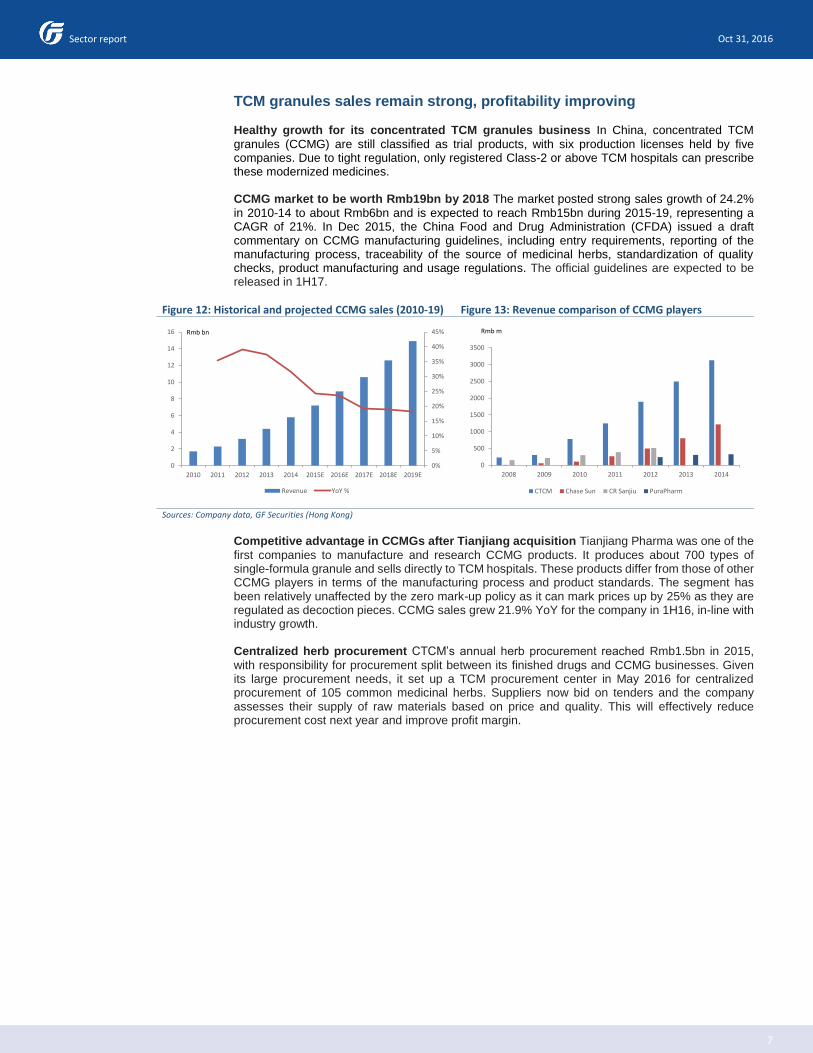

TCM granules sales remain strong, profitability improving Healthy growth for its concentrated TCM granules business In China, concentrated TCM

granules (CCMG) are still classified as trial products, with six production licenses held by five companies. Due to tight regulation, only registered Class-2 or above TCM hospitals can prescribe these modernized medicines. CCMG market to be worth Rmb19bn by 2018 The market posted strong sales growth of 24.2%

in 2010-14 to about Rmb6bn and is expected to reach Rmb15bn during 2015-19, representing a CAGR of 21%. In Dec 2015, the China Food and Drug Administration (CFDA) issued a draft commentary on CCMG manufacturing guidelines, including entry requirements, reporting of the manufacturing process, traceability of the source of medicinal herbs, standardization of quality checks, product manufacturing and usage regulations. The official guidelines are expected to be released in 1H17.

Figure 12: Historical and projected CCMG sales (2010-19) Figure 13: Revenue comparison of CCMG players

Sources: Company data, GF Securities (Hong Kong)

Competitive advantage in CCMGs after Tianjiang acquisition Tianjiang Pharma was one of the

first companies to manufacture and research CCMG products. It produces about 700 types of single-formula granule and sells directly to TCM hospitals. These products differ from those of other CCMG players in terms of the manufacturing process and product standards. The segment has been relatively unaffected by the zero mark-up policy as it can mark prices up by 25% as they are regulated as decoction pieces. CCMG sales grew 21.9% YoY for the company in 1H16, in-line with industry growth. Centralized herb procurement CTCM’s annual herb procurement reached Rmb1.5bn in 2015,

with responsibility for procurement split between its finished drugs and CCMG businesses. Given its large procurement needs, it set up a TCM procurement center in May 2016 for centralized procurement of 105 common medicinal herbs. Suppliers now bid on tenders and the company assesses their supply of raw materials based on price and quality. This will effectively reduce procurement cost next year and improve profit margin.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

2

4

6

8

10

12

14

16

2010 2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E

Revenue YoY %

Rmb bn

0

500

1000

1500

2000

2500

3000

3500

2008 2009 2010 2011 2012 2013 2014

CTCM Chase Sun CR Sanjiu PuraPharm

Rmb m

Oct 31, 2016

8

Sector report

Growth outlook We expect CTCM to deliver an 28% EPS CAGR during FY16-18, driven by a 36% rise in revenue during the period and improving margins from its integration of resources and improved utilization efficiency of labor, capital and production facilities.

Finished drugs to see negative revenue growth in FY16 In line with the company’s guidance,

we expect sales growth of CTCM’s finished drugs (both TCM finished drugs and chemical medicine) to slow from 3.8% YoY in FY15 to -20% YoY in FY16, due to: 1) The impact of medical insurance payments and the “two-invoice system”, which forced distributors to reduce inventory; 2) Price cuts from tenders of 3-4% for key EDL products; 3) Secondary price negotiations leading to tender withdrawals in several provinces, and; 4) Adjustments of the sales model and selling prices for some products sold through agencies. The restructuring of the sales team and increased focus on in-market sales (instead of ex-factory sales) should mean sales growth gradually returns to 5/7% in FY17/18. Evidence-based trials for eight exclusive EDL drugs To validate the clinical benefits of its TCM

finished product portfolio, the company has conducted evidence-based clinical research of all of its EDL products. Xianling Gubao has completed the relevant trials and was included in national clinical guideline for osteoporosis in early 2016. The company will conduct research into the other seven exclusive EDL products (Biyankang tablets, Yu Ping Feng Granules, Jingshu Granules, Moisturising & Anti-Itching Capsules, Zaoren Anshen Capsules and Fengshi Gutong Capsules) on their respective indications. We believe this will unlock product potential, reduce pricing pressure and support sales volume growth. Chinese medicine granules driving revenue growth Over the next three years, CTCM will focus

on the CCMG industry, where competition is limited. The company has guided for 15-20% revenue growth and higher earnings growth due to centralized procurement and integration of other resources. We believe CTCM could also enhance Tianjiang’s product portfolio through cross-selling, after they have been allowed to sell to comprehensive hospitals and Class-1 or below TCM hospitals as well as grassroots health centers. Higher inventory and receivables days following Tianjiang consolidation CTCM’s inventory

days increased from 125 in 1H15 to 173 in 1H16 due to the consolidation of Tianjiang, which sells CCMG products directly to hospitals. Receivable days also increased from 80 to 129 days due to the longer collection period from hospitals. Cash conversion cycle increased to 218 days from 160 days a year ago. Rmb300m capex in FY16 for Tianjiang and Tongjitang expansion This includes construction of

two CCMG production lines in Shandong and Liaoning for Rmb100 each, and another Rmb100m for Guizhou Tongjitang expansion.

Figure 14: Revenue mix Figure 15: Revenue and gross margin forecasts

Sources: Company data, GF Securities (Hong Kong)

73.6%

26.4%

2015

Finished drugs CCMG

35.8%

64.2%

1H16

Finished drugs CCMG

59.2%

62.0%

59.1%

58.7%

59.5%

59.9%

57%

58%

59%

60%

61%

62%

63%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2013 2014 2015 2016E 2017E 2018E

Revenue (Rmb m) GPM

Oct 31, 2016

9

Sector report

Figure 16: Operating profit and OPM forecasts Figure 17: Net profit and net margin forecasts

Sources: Company data, GF Securities (Hong Kong

Valuation Our one-year target price of HK$5.20 implies 30% upside, represents 0.5x PEG, and is based on a target P/E of 15x our 2017 EPS forecast of Rmb0.30, compared to the current average of 15x for other Chinese medicines manufacturers listed in Hong Kong. As the leading TCM manufacturer, we believe CTCM’s discount to its HK-listed peers should narrow. Concerns about slowing growth in the finished TCM industry have led to de-rating since mid-2015.

Figure 18: P/E band

Sources: Bloomberg

19%

19%

20%

20%

21%

21%

22%

22%

-

500

1,000

1,500

2,000

2,500

2013 2014 2015 2016E 2017E 2018E

Operating profit OPM

Rmb m

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2013 2014 2015 2016E 2017E 2018E

Net profit NPM

Rmb m

1

2

3

4

5

6

7

8

9

Share Price 11x 18x 21x 24x 27x

Oct 31, 2016

10

Sector report

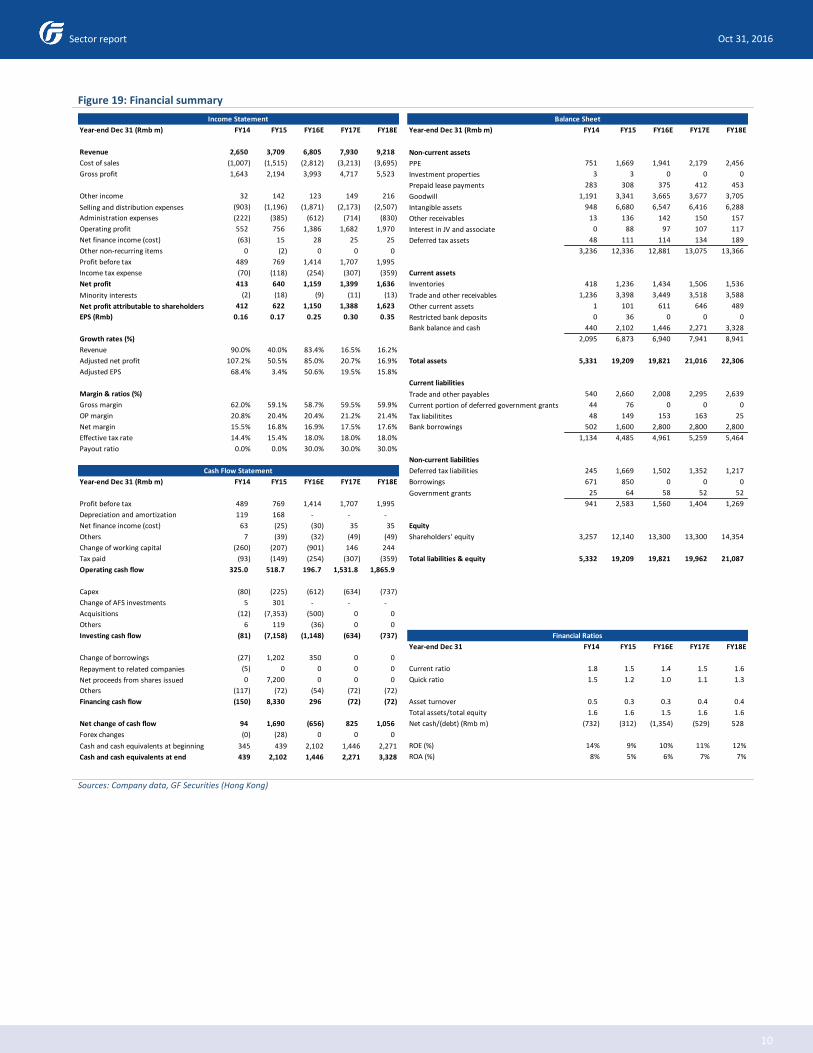

Figure 19: Financial summary

Sources: Company data, GF Securities (Hong Kong)

Year-end Dec 31 (Rmb m) FY14 FY15 FY16E FY17E FY18E Year-end Dec 31 (Rmb m) FY14 FY15 FY16E FY17E FY18E

Revenue 2,650 3,709 6,805 7,930 9,218 Non-current assets

Cost of sales (1,007) (1,515) (2,812) (3,213) (3,695) PPE 751 1,669 1,941 2,179 2,456

Gross profit 1,643 2,194 3,993 4,717 5,523 Investment properties 3 3 0 0 0

Prepaid lease payments 283 308 375 412 453

Other income 32 142 123 149 216 Goodwill 1,191 3,341 3,665 3,677 3,705

Selling and distribution expenses (903) (1,196) (1,871) (2,173) (2,507) Intangible assets 948 6,680 6,547 6,416 6,288

Administration expenses (222) (385) (612) (714) (830) Other receivables 13 136 142 150 157

Operating profit 552 756 1,386 1,682 1,970 Interest in JV and associate 0 88 97 107 117

Net finance income (cost) (63) 15 28 25 25 Deferred tax assets 48 111 114 134 189

Other non-recurring items 0 (2) 0 0 0 3,236 12,336 12,881 13,075 13,366

Profit before tax 489 769 1,414 1,707 1,995

Income tax expense (70) (118) (254) (307) (359) Current assets

Net profit 413 640 1,159 1,399 1,636 Inventories 418 1,236 1,434 1,506 1,536

Minority interests (2) (18) (9) (11) (13) Trade and other receivables 1,236 3,398 3,449 3,518 3,588

Net profit attributable to shareholders 412 622 1,150 1,388 1,623 Other current assets 1 101 611 646 489

EPS (Rmb) 0.16 0.17 0.25 0.30 0.35 Restricted bank deposits 0 36 0 0 0

Bank balance and cash 440 2,102 1,446 2,271 3,328

Growth rates (%) 2,095 6,873 6,940 7,941 8,941

Revenue 90.0% 40.0% 83.4% 16.5% 16.2%

Adjusted net profit 107.2% 50.5% 85.0% 20.7% 16.9% Total assets 5,331 19,209 19,821 21,016 22,306

Adjusted EPS 68.4% 3.4% 50.6% 19.5% 15.8%

Current liabilities

Margin & ratios (%) Trade and other payables 540 2,660 2,008 2,295 2,639

Gross margin 62.0% 59.1% 58.7% 59.5% 59.9% Current portion of deferred government grants 44 76 0 0 0

OP margin 20.8% 20.4% 20.4% 21.2% 21.4% Tax liabilitites 48 149 153 163 25

Net margin 15.5% 16.8% 16.9% 17.5% 17.6% Bank borrowings 502 1,600 2,800 2,800 2,800

Effective tax rate 14.4% 15.4% 18.0% 18.0% 18.0% 1,134 4,485 4,961 5,259 5,464

Payout ratio 0.0% 0.0% 30.0% 30.0% 30.0%

Non-current liabilities

Deferred tax liabilities 245 1,669 1,502 1,352 1,217

Year-end Dec 31 (Rmb m) FY14 FY15 FY16E FY17E FY18E Borrowings 671 850 0 0 0

Government grants 25 64 58 52 52

Profit before tax 489 769 1,414 1,707 1,995 941 2,583 1,560 1,404 1,269

Depreciation and amortization 119 168 - - -

Net finance income (cost) 63 (25) (30) 35 35 Equity

Others 7 (39) (32) (49) (49) Shareholders' equity 3,257 12,140 13,300 13,300 14,354

Change of working capital (260) (207) (901) 146 244

Tax paid (93) (149) (254) (307) (359) Total liabilities & equity 5,332 19,209 19,821 19,962 21,087

Operating cash flow 325.0 518.7 196.7 1,531.8 1,865.9

Capex (80) (225) (612) (634) (737)

Change of AFS investments 5 301 - - -

Acquisitions (12) (7,353) (500) 0 0

Others 6 119 (36) 0 0

Investing cash flow (81) (7,158) (1,148) (634) (737)

Year-end Dec 31 FY14 FY15 FY16E FY17E FY18E

Change of borrowings (27) 1,202 350 0 0

Repayment to related companies (5) 0 0 0 0 Current ratio 1.8 1.5 1.4 1.5 1.6

Net proceeds from shares issued 0 7,200 0 0 0 Quick ratio 1.5 1.2 1.0 1.1 1.3

Others (117) (72) (54) (72) (72)

Financing cash flow (150) 8,330 296 (72) (72) Asset turnover 0.5 0.3 0.3 0.4 0.4

Total assets/total equity 1.6 1.6 1.5 1.6 1.6

Net change of cash flow 94 1,690 (656) 825 1,056 Net cash/(debt) (Rmb m) (732) (312) (1,354) (529) 528

Forex changes (0) (28) 0 0 0

Cash and cash equivalents at beginning 345 439 2,102 1,446 2,271 ROE (%) 14% 9% 10% 11% 12%

Cash and cash equivalents at end 439 2,102 1,446 2,271 3,328 ROA (%) 8% 5% 6% 7% 7%

Income Statement Balance Sheet

Cash Flow Statement

Financial Ratios

Oct 31, 2016

11

Sector report

Kingworld Medicines (1110 HK)

Buy (initiation)

Target price: HK$1.80

Beneficiary of rising demand for health supplements in China

Natalie Chiu SFC CE No. AVH029 [email protected] +852 3760 2030 GF Securities (Hong Kong) Brokerage Limited 29-30/F, Li Po Chun Chambers 189 Des Voeux Road Central Hong Kong

Kingworld is a Chinese proprietary medicine and health supplement distributor in southern China The company distributes Hong Kong and overseas’ OTC and other

healhcare products and sells via distributors in south and southeastern China. It has a network of about 200,000 drug retailers and benefits from close relationships with distributors. Strong market capabilities and product selectivity offers above-peer profitability and revenue growth Kingworld posted revenue and gross profit CAGRs of 13% and 31%

respectively in 2013-15 and had a gross margin of 31.8% in 2015. This was attributable to its focus on selling high-margin products (e.g. distribution of foreign healthcare supplements in eastern and southern China, which carry a gross margin of about 60% vs the industry average of 30%). Sound growth strategy, active marketing and close distributor partnerships

Kingworld aims to: 1) expand its high-GM product offerings; 2) increase online sales, and; 3) penetrate into lower-tier cities. With a successful track record of product marketability, we expect Kingworld to continue to grow faster than the industry average in 2016-18 with improved profitability through a better product mix and superior operating efficiency. We project a CAGR of 23% and 42% for revenue and earnings respectively in 2016-18. Compelling valuation offers near-term upside Our target price of HK$1.80 represents

13x our 2017 diluted EPS estimate. The stock is trading at 11x our 2017 EPS estimate, a 27% discount to its peer group average of 15x. We believe early signs of growth acceleration will narrow this valuation discount. Risks: 1) Failure to renew distribution rights and registration certificates; 2) early

termination of distribution agreements with Nin Jiom Pei Pa Koa if guaranteed sales volume is not achieved; 3) damage to products’ brand image due to quality issues or aggressive discounts.

Stock valuation

Sources: Company data, GF Securities (Hong Kong)

Turnover

(Rmb m)

Net profit

(Rmb m)

EPS

(Rmb)

EPS YoY

(%)

P/E BPS

(Rmb)

P/B ROE

(%)

2014 660 38 0.06 -20% 19.6 1.6 0.7 4%

2015 714 31 0.05 -18% 25.1 1.7 0.7 3%

2016E 1,004 56 0.08 79% 14.5 1.8 0.7 5%

2017E 1,200 84 0.12 50% 9.8 2.0 0.6 6%

2018E 1,398 107 0.15 28% 7.7 2.2 0.5 7%

Stock performance

Source: Bloomberg

Key data

Source: Bloomberg

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Oct

-14

No

v-1

4

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

1110 HK Equity Hang Seng Index

Oct 27 close (HK$) 1.38

Shares in issue (m) 623

Major shareholder Zhao Li Sheng (47.84%)

Market cap (HK$ bn) 0.87

3M avg. vol. (m) 0.12

52W high/low (HK$) 1.945/1.13

Oct 31, 2016

12

Sector report

Retail pharmacies offer stronger growth outlook than hospitals China’s over-the-counter market reached Rmb1.8bn in 2015 Revenue growth in the over-the-

counter (OTC) market (+8.9% YoY) overtook the prescription market (+7.4% YoY) in 2015 due to government healthcare budget controls and more restrained use of medicines by doctors, and will be supported by 1) a demand shift from prescription to OTC drugs as the government tries to reduce healthcare spending and free up hospital capacity by encouraging self-diagnosis for non-serious conditions, and 2) overall pharmaceutical industry growth due to an increasingly aging population, rising GDP per capita and urbanization.

Figure 20: Revenue in China’s OTC and prescription drug markets (2012-15)

Sources: IMS, GF Securities (Hong Kong)

Retail pharmacies and community health centers driving growth in the OTC market China’s

OTC drugs are sold via three main channels (hospitals, retail pharmacies and community health centers). Retail pharmacies and community health centers posted faster growth than hospitals in 2015 with sales growth of 11.6% and 11.1% YoY respectively.

Figure 21: Drug sales by channel in Beijing (2014-15) Figure 22: Revenue growth at major drug channels in China (2013-15)

Sources: IMS, GF Securities (Hong Kong)

Finished Chinese medicine represents over 60% of all retail pharmacies sales Although

overall finished Chinese medicine wholesale revenue growth slowed significantly from 13.1% YoY in 2014 to 5.7% YoY in 2015, we believe much of the slowdown is from sales to hospitals. This is evident in Beijing’s drug market, where sales growth of finished Chinese medicines and OTC drugs was 12.9% YoY and 8.5% YoY respectively in 2015.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

200

400

600

800

1000

1200

1400

2012 2013 2014 2015

OTC Rx OTC YoY Rx YoY

Rmb bn

70%

16%

14%

Hospitals Retail pharmacies Community health centers

13.40%11.70%

5.00%

9.50%

6.90%

8.30%

13.80% 15.60%

13.10%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2013% 2014 2015

Hospitals Retail pharmacies Community health centers

Oct 31, 2016

13

Sector report

Figure 23: Channel mix and revenue growth in Beijing’s pharma market (2014-15)

Figure 24: Channel mix and revenue growth in Beijing’s finished TCM market (2014-15)

Sources: IMS, GF Securities (Hong Kong)

Figure 25: Channel mix and revenue growth in Beijing’s OTC drug market (2014-15)

Sources: IMS, GF Securities (Hong Kong)

Proprietary Chinese medicine distribution market grew at a CAGR of 16.8% to Rmb392bn in 2011-15 Finished Chinese medicine can be classified into: 1) proprietary Chinese medicines, which

are exclusive formulas protected by the government, and 2) common TCM. Based on Euromonitor estimates, the proprietary Chinese medicine market in China is expected to grow at a CAGR of 17% during 2016-20.

Figure 26: Proprietary Chinese medicine market

Sources: Euromonitor, GF Securities (Hong Kong)

Local companies represent 86% of the OTC market in China, and finished TCM companies account for 50% The top-ten manufacturers/importers of OTC and healthcare supplement products

in China account for 26% of the market. By-Health (300146 CH) is the biggest OTC and health supplement player and Dong-E E-Jiao’s (000423 CH) E-Jiao is the best-selling product.

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

0%

20%

40%

60%

80%

100%

120%

2014 2015

Hospitals Retail pharmacies

Community health centers Hospitals YoY

Retail pharmacies YoY Community health centers YoY

0%

2%

4%

6%

8%

10%

12%

14%

0%

20%

40%

60%

80%

100%

120%

2014 2015

Hospitals Retail pharmacies

Community health centers Retail pharmacies YoY

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0%

20%

40%

60%

80%

100%

120%

2014 2015

Hospitals Retail pharmacies

Community health centers Retail pharmacies YoY

33.8%

33.8%

21.6%20.3%

19.2% 18.3% 17.4%16.2%

15.1%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E

Retail sales value (Rmb m) YoY %

Oct 31, 2016

14

Sector report

Figure 27: Top-10 OTC and healthcare supplement product companies in China

Figure 28: Top-10 OTC and healthcare supplement products in China

Sources: IMS, GF Securities (Hong Kong)

Greater growth potential in lower-tier cities Sales growth at retail pharmacies in first and second-

tier cities has slowed since 2014, while third and fourth-tier cities have seen faster growth both in terms of sales value and volume. Sales growth in top tier cities is driven by price hikes from product upgrade, while in lower tier cities sales are driven by urbanization and the upgrading of infrastructure in these less-accessed markets.

Selective product sourcing to drive growth Quality portfolio of 60 products Kingworld was set up in 1996 and began by signing three major

distribution agreements with Tai San Enterprise, Nin Jiom Medicine and Great Pleasure, and Etta Trading, which supplies the best-selling proprietary Chinese medicines and health supplements in Hong Kong. Since then it has expanded its product portfolio and currently manages 60 products used for cough and phlegm relief, vitamins, and gastrointestinal, orthopedic, cardiovascular and influenza issues. These include 12 pharmaceutical products, seven healthcare products, 28 general foodstuffs and two medical products, and are manufactured in Japan, Canada, Hong Kong, Taiwan, Thailand and mainland China and sourced from 13 different suppliers.

Figure 29: Kingworld’s revenue mix

Sources: Company data, GF Securities (Hong Kong)

Stable relationship with suppliers Kingworld has maintained stable relationships with its five

largest suppliers for periods of between 10-20 years. Nin Jiom Pei Pa Koa was introduced to the company by Kingworld’s chairman, Zhao Li Sheng, as he believed there was a potential market for the product in mainland China. Mr Zhao secured the distribution rights of Nin Jiom Pei Pa Koa for Kingworld in 1997. In Apr 2010, before listing, Kingworld entered into a written three-year distribution agreement with the manufacturer and supplier of Nin Jiom Pei Pa Koa to sell the product in 14 regions in China. The agreement has been renewed twice, most recently in 1H16.

Rank OTC and health supplement company

1 BY-Health

2 Dong-E E-Jiao

3 Wyeth

4 Bayer Healthcare

5 Yunnan Baiyao

6 Xi'an Janssen Pharm

7 Jiangsxi Huiren

8 Xiuzheng Pharm

9 Fupai E-jiao

10 Nin Jiom Medicine

Rank Product Manufacturer Drug type

1 E-Jiao Dong-E E-Jiao TCM

2 Caltrate Wyeth Chemical

3 Kidney treasure tablets Jiangsxi Huiren TCM

4 E-Jiao Fupai E-jiao TCM

5 Hong Mao Medicinal Wine Hong Mao pharma TCM

6 Nin Jiom Pei Pa Koa Nin Jiom Medicine TCM

7 Compound E Jiao Jiang Dong-E E-Jiao TCM

8 Shujin Jinyao Wan Guangzhou Chenliji TCM

9 BY-Health protein powder BY-Health Chemical

10 Centrum Wyeth Chemical

Nin Jiom Chuan Bei Pei Pa series,

80.39%

Culturelle probiotic series, 3.94%

Taiko Seirogan,

9.63%

Others, 2.26%Mentholatum Menthol

Cream, 3.78%

2014

Nin Jiom Chuan Bei Pei Pa series,

45.69%

Culturelle probiotic

series, 13%Flying Eagle Wood Lok Medicated Oil,

5.87%

Taiko Seirogan, 6.96%

Others, 22.26%

Imada Red Flower Oil, 1.87%

Mentholatum Menthol Cream,

4.35%

2015

Oct 31, 2016

15

Sector report

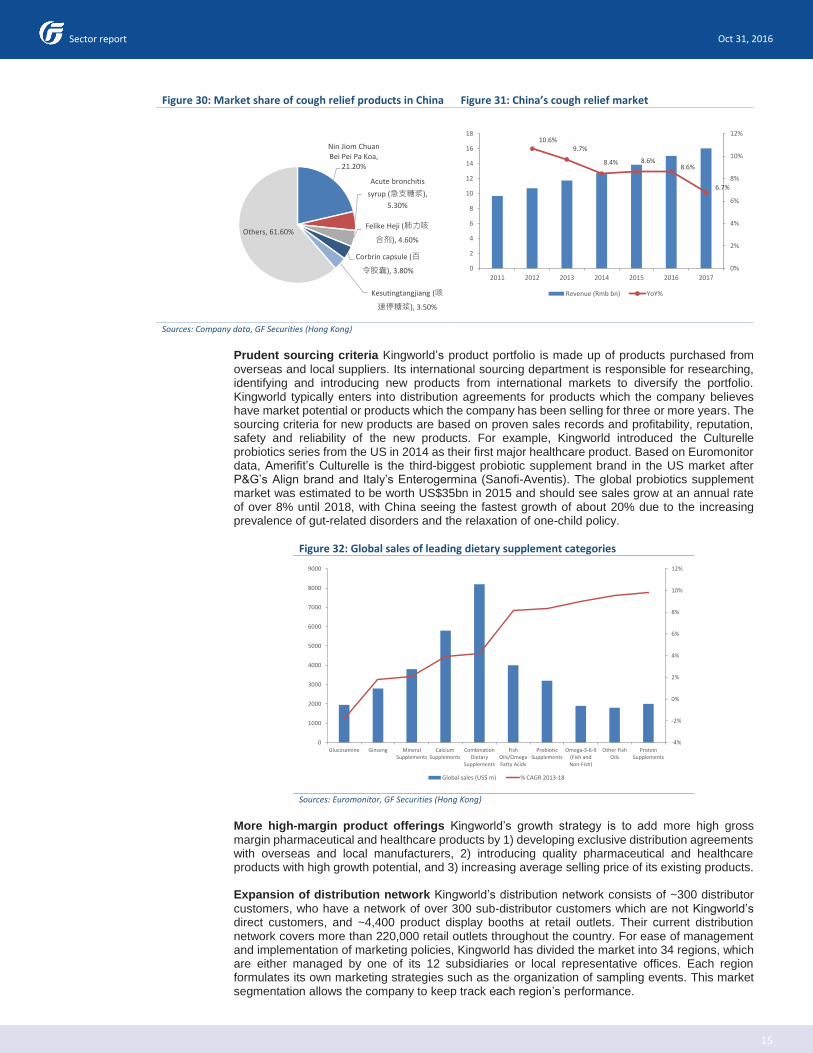

Figure 30: Market share of cough relief products in China Figure 31: China’s cough relief market

Sources: Company data, GF Securities (Hong Kong)

Prudent sourcing criteria Kingworld’s product portfolio is made up of products purchased from

overseas and local suppliers. Its international sourcing department is responsible for researching, identifying and introducing new products from international markets to diversify the portfolio. Kingworld typically enters into distribution agreements for products which the company believes have market potential or products which the company has been selling for three or more years. The sourcing criteria for new products are based on proven sales records and profitability, reputation, safety and reliability of the new products. For example, Kingworld introduced the Culturelle probiotics series from the US in 2014 as their first major healthcare product. Based on Euromonitor data, Amerifit’s Culturelle is the third-biggest probiotic supplement brand in the US market after P&G’s Align brand and Italy’s Enterogermina (Sanofi-Aventis). The global probiotics supplement market was estimated to be worth US$35bn in 2015 and should see sales grow at an annual rate of over 8% until 2018, with China seeing the fastest growth of about 20% due to the increasing prevalence of gut-related disorders and the relaxation of one-child policy.

Figure 32: Global sales of leading dietary supplement categories

Sources: Euromonitor, GF Securities (Hong Kong)

More high-margin product offerings Kingworld’s growth strategy is to add more high gross

margin pharmaceutical and healthcare products by 1) developing exclusive distribution agreements with overseas and local manufacturers, 2) introducing quality pharmaceutical and healthcare products with high growth potential, and 3) increasing average selling price of its existing products. Expansion of distribution network Kingworld’s distribution network consists of ~300 distributor

customers, who have a network of over 300 sub-distributor customers which are not Kingworld’s direct customers, and ~4,400 product display booths at retail outlets. Their current distribution network covers more than 220,000 retail outlets throughout the country. For ease of management and implementation of marketing policies, Kingworld has divided the market into 34 regions, which are either managed by one of its 12 subsidiaries or local representative offices. Each region formulates its own marketing strategies such as the organization of sampling events. This market segmentation allows the company to keep track each region’s performance.

Nin Jiom Chuan Bei Pei Pa Koa,

21.20%

Acute bronchitis

syrup (急支糖浆),

5.30%

Felike Heji (肺力咳

合剂), 4.60%

Corbrin capsule (百

令胶囊), 3.80%

Kesutingtangjiang (咳

速停糖浆), 3.50%

Others, 61.60%

10.6%9.7%

8.4% 8.6%8.6%

6.7%

0%

2%

4%

6%

8%

10%

12%

0

2

4

6

8

10

12

14

16

18

2011 2012 2013 2014 2015 2016 2017

Revenue (Rmb bn) YoY%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

Glucosamine Ginseng MineralSupplements

CalciumSupplements

CombinationDietary

Supplements

FishOils/OmegaFatty Acids

ProbioticSupplements

Omega-3-6-9(Fish andNon-Fish)

Other FishOils

ProteinSupplements

Global sales (US$ m) % CAGR 2013-18

Oct 31, 2016

16

Sector report

Figure 33: Flying Eagle Wood Lok Medicated Oil product display booth

Figure 34: Taiko Seirogan product display booth

Sources: Company data, GF Securities (Hong Kong)

Figure 35: Kingworld’s segmentation of distribution network

Sources: Company data, GF Securities (Hong Kong)

Oct 31, 2016

17

Sector report

Growth outlook We expect Kingworld Medicines to deliver CAGRs of 48% in EPS and 25% in revenue during FY16-18, driven by its expanding retail and distribution network and greater number of high-margin product offerings. Sustainable gross margin improvement supported by launch of higher-margin products The

company has actively adjusted its product mix by distributing high margin OTC and healthcare products. Overall GM improved from 23.7% in 2014 to 33% in 1H16, driven by improved sales of high-margin products such as the Culturelle probiotics series and Flying Eagle Wood Lok Medicated Oil. We expect margin expansion to continue driven by a better product mix.

Figure 36: Sales of Kingworld’s high-margin products increasing

Sources: Company data, GF Securities (Hong Kong)

License renewal of Nim Jiom Pei Pa Koa in April 2016 The Imported Drug Registration Certificate

and the Pharmaceutical Product Registration Certificate were issued and approved by the CFDA, with a validity period of five years. For Nim Joim Pei Pa Koa, the expiry date of the Pharmaceutical Product Registration Certificate was March 2015 and product sales were affected during the renewal process. In 2015, revenue from Nim Jiom reached Rmb290m, down 40% from 2014. It booked Rmb230m in 1H16 and is on track to post Rmb575m in revenue in 2016, based on its 40/60% conventional yearly split. Lower costs in online pharmacy Kingworld gained access to an e-commerce platform in 2015

and built an online sales network to distribute its pharmaceutical and healthcare products. It opens online stores that 1) are commercially attractive, 2) have a good reputation, and are 3) within their target group and industry, such as professional retail channels related to maternity and babies. In 1H16, online sales reached Rmb39m and contributed 9% of revenue. We believe the surge in online pharmacy sales will help to improve margins and increase sales by diverting customer traffic away from traditional brick-and-mortar drugstores, especially in second and third-tier cities. Strategic cooperation with Sinopharm Capital Sinopharm Capital, a sister company of

Sinopharm Holdings (1099 HK, NR), became a strategic investor in Kingworld Medicines in Sept 2014 with the purchase of a 9.99% stake and HK$134m worth of convertible bonds which can be converted into shares at HK$2.15/share. Both parties extended the conversion period from 18 months to 36 months, ending in Dec 2017, and the annual interest rate was reduced from 7.4% to 5.0%. We believe Sinopharm Capital’s involvement is positive for Kingworld, as it could leverage Sinopharm’s resource network to distribute its products and pursue a more aggressive M&A strategy.

0%

10%

20%

30%

40%

50%

60%

70%

>50% 30-50% 20-30% 10-20%

1H16

Kingworld GM: 33%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

>50% 30-50% 20-30% 10-20%

2014

Kingworld GM: 23.7%

Oct 31, 2016

18

Sector report

Figure 37: Kingworld’s pharmaceutical business Figure 38: Kingworld’s healthcare business

Sources: Company data, GF Securities (Hong Kong)

Figure 39: Kingworld’s margins Figure 40: Revenue mix by business segment (1H16)

Sources: Company data, GF Securities (Hong Kong)

Valuation Our one-year target price of HK$1.80 implies 22% upside and is based on a target P/E of 13x our 2017 EPS forecast of Rmb0.12, compared to the current average of 15x for its HK-listed peers. The stock is currently trading at 10.5x our 2017 EPS forecast. Concerns about the company’s slowing product sales growth have led to de-rating since mid-2015. We believe early signs of growth acceleration in 2016 will narrow the valuation discount to its peers.

Figure 41: P/E band

Sources: Bloomberg

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

100

200

300

400

500

600

700

800

2013 2014 2015 2016E 2017E 2018E

Pharmaceutical products revenue (Rmb m) YoY growth

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

0

50

100

150

200

250

300

350

400

450

500

2013 2014 2015 2016E 2017E 2018E

Healthcare products revenue (Rmb m) YoY growth

31.8%33.3%

34.5% 35.3% 36.1%

6.9%

9.6%11.2% 12.0%

13.2%

4.4%5.6%

7.0% 7.7% 8.6%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

2014 2015 2016E 2017E 2018E

Gross margin Operating margin Net margin

Pharmaceutical

products61%

Healthcare

products19%

Medical devices

20%

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

2.5

2.7

2.9

10

/20

14

11

/20

14

12

/20

14

01

/20

15

02

/20

15

03

/20

15

04

/20

15

05

/20

15

06

/20

15

07

/20

15

08

/20

15

09

/20

15

10

/20

15

11

/20

15

12

/20

15

01

/20

16

02

/20

16

03

/20

16

04

/20

16

05

/20

16

06

/20

16

07

/20

16

08

/20

16

09

/20

16

10x 13x 16x 19x 22x Share Price

Oct 31, 2016

19

Sector report

Figure 42: Financial summary

Sources: Company data, GF Securities (Hong Kong)

Year-end Dec 31 (Rmb m) FY14 FY15 FY16E FY17E FY18E Year-end Dec 31 (Rmb m) FY14 FY15 FY16E FY17E FY18E

Revenue 660 714 1,004 1,200 1,398 Non-current assets

Cost of sales (504) (487) (670) (786) (904) PPE 5 16 21 27 34

Gross profit 156 227 334 414 493 Investment properties 92 108 129 155 186

Interest in a joint venture 45 63 68 74 81

Other income 27 10 30 36 42 Goodwill 0 91 91 91 91

Selling and distribution expenses (88) (119) (178) (208) (242) Intangible assets 0 116 215 187 155

Administration expenses (46) (69) (90) (108) (126) Other receivables 75 75 99 104 109

Operating profit 49 49 96 134 168 Available for sales investments 0 10 17 19 21

Net finance income (cost) (7) (16) (5) (7) (7) 218 478 640 657 676

Other non-recurring items 6 18 5 6 7

Profit before tax 49 51 97 133 167 Current assets

Income tax expense (11) (12) (21) (29) (37) Inventories 70 79 96 112 129

Net profit 38 39 76 104 130 Trade and other receivables 418 287 335 400 466

Minority interests 0 (8) (20) (20) (23) Other current assets 0 105 87 92 93

Net profit attributable to shareholders 38 31 56 84 107 Restricted bank deposits 84 0 0 0 0

EPS (Rmb) 0.06 0.05 0.08 0.12 0.15 Bank balance and cash 230 132 132 190 279

802 604 649 794 967

Growth rates (%)

Revenue 19.0% 8.1% 40.7% 19.5% 16.5% Total assets 1,019 1,082 1,289 1,451 1,643

Adjusted net profit -19.7% -17.6% 78.9% 49.8% 28.0%

Adjusted EPS -19.9% -21.9% 73.3% 48.3% 26.7% Current liabilities

Trade and other payables 186 159 167 197 226

Margin & ratios (%) Other financial l iabil ity 7 21 20 20 0

Gross margin 23.7% 31.8% 33.3% 34.5% 35.3% Tax liabilitites 13 17 19 47 61

OP margin 7.5% 6.9% 9.6% 11.2% 12.0% Bank borrowings 229 168 190 200 200

Net margin 5.7% 4.4% 5.6% 7.0% 7.7% 435 364 396 463 487

Effective tax rate 22.2% 23.3% 22.0% 22.0% 22.0%

Payout ratio 24.9% 27.0% 25.0% 25.0% 25.0% Non-current liabilities

Deferred tax l iabilities 10 30 32 165 335

Other l iabilities 3 0 98 93 0

Year-end Dec 31 (Rmb m) FY14 FY15 FY16E FY17E FY18E 14 30 130 258 335

Profit before tax 49 51 97 133 167 Equity

Depreciation and amortization 2 4 28 34 39 Shareholders' equity 571 687 763 728 818

Net finance income (cost) 5 11 (0) 1 1

Others (9) (9) (13) (10) 9 Total liabilities & equity 1,019 1,082 1,289 1,449 1,639

Change of working capital (44) 61 (56) (53) (53)

Tax paid (8) (16) (21) (29) (37)

Operating cash flow (5.2) 103.2 34.8 76.1 126.7

Capex (2) (6) (34) (18) (21)

Change of AFS investments - (31) (15) 5 5

Acquisitions 0 (148) 0 0 0

Others (28) 17 5 6 6

Investing cash flow (30) (168) (44) (8) (10)

Year-end Dec 31 FY14 FY15 FY16E FY17E FY18E

Change of borrowings 130 (61) 22 10 0

Decrease /(increase) in pledged bank deposits (66) 84 0 0 0 Current ratio 1.8 1.7 1.6 1.7 2.0

Proceeds from issuance of mandatorily convertible bonds 105 0 0 0 0 Quick ratio 1.7 1.2 1.0 1.2 1.3

Others (26) (24) (14) (21) (28)

Financing cash flow 144 (1) 9 (11) (28) Asset turnover 0.8 0.7 0.8 0.9 0.9

Total assets/total equity 1.8 1.6 1.7 2.0 2.0

Net change of cash flow 109 (66) (1) 58 89 Net cash/(debt) (Rmb m) 85 (35) (58) (10) 79

Forex changes (0) (1) 0 0 0

Cash and cash equivalents at beginning 91 200 132 132 190 ROE (%) 7% 5% 9% 12% 14%

Cash and cash equivalents at end 200 133 132 190 279 ROA (%) 4% 3% 5% 6% 7%

Income Statement Balance Sheet

Cash Flow Statement

Financial Ratios

Oct 31, 2016

20

Sector report

Beijing Tong Ren Tang Chinese Medicine (8138 HK)

Accumulate (initiation)

Target price: HK$12.30

Expanding global footprint

Natalie Chiu SFC CE No. AVH029 [email protected] +852 3760 2030 GF Securities (Hong Kong) Brokerage Limited 29-30/F, Li Po Chun Chambers 189 Des Voeux Road Central Hong Kong

Largest proprietary Chinese medicine exporter in China Tong Ren Tang Group

restructured its overseas business in 2010 and listed Beijing Tong Ren Tang Chinese Medicine (Tong Ren Tang CM) in 2013. With 62 self-operated stores outside China, Tong Ren Tang CM now has one of the largest TCM retail networks in Asia. The company operates a TCM clinics-centric model and relies on product revenue generated from providing TCM consultation services. It currently offers two self-manufactured products:

Angong Niuhuang Pills (安宮牛黃丸) and ganoderma lucidum spores powder (靈芝孢子

粉). It developed ten new healthcare products under four series in 2015, including omega-

3 extracted from plants, probiotics, etc. 3Q16 revenue grew 15.2%yoy to HK$266.3mn reversing the slowdown in 1H16.

Product sales, service income and royalty fee income rose 15.2%/13.1%/10.8% yoy respectively. During the period, Hong Kong sales decline has narrowed. Net profit grew 25.2%yoy to HK$105.3mn, vs 32%yoy growth in 1H16. The company opened its first 2 US stores in Sept leading to higher SG&A expenses. Sustained growth of self-manufactured products has led to above-peer profitability and sales growth Tong Ren Tang CM posted total revenue and net income CAGRs of

43% and 32% respectively in 2013-15, and a gross margin of 70.2% and operating margin of 47.5% in 2015. This rapid growth and strong profitability are attributable to its self-manufacturing and wholesale-focused distribution model. Angong Niuhuang Pills have seen the fastest growth among its products. Overseas expansion to be accelerated in 2016-18 through partnership model Tong

Ren Tang CM aims to 1) penetrate overseas TCM markets with significant growth potential, and 2) expand the therapeutic focus of Angong Niuhuang Pills from curative to preventive. The company is targeting the US and Europe as long-term growth drivers and should see stable growth in Hong Kong and other Asian markets. Valuation offers limited upside in the near term We initiate Tong Ren Tang CM with

an Accumulate rating and a one-year target price of HK$12.30, which implies 9% upside and is based on a target P/E of 20x our 2017 EPS forecast of HK$0.61. The target P/E represents 1.0x PEG against FY16-18 EPS growth of 19.8%. The stock is trading at 18.3x our 2017 EPS estimate, a 19% premium to its peer group average of 15.3x. We think this premium is justified given its above-peer profitability and solid execution. However, further share price upside will be capped by slower organic growth in Hong Kong while new markets are still in ramp-up phase. Risks: 1) Unfavorable regulation for the TCM industry in its overseas markets; 2) over-

reliance on Angong Niuhuang Pills for the company’s revenue; 3) market risk as a GEM board-listed company.

Stock valuation

Sources: Company data, GF Securities (Hong Kong)

Turnover

(HK$ m)

Net profit

(HK$ m)

EPS

(HK$)

EPS YoY

(%)

P/E BPS

(HK$)

P/B ROE

(%)

2014 761 287 0.35 21% 31.7 1.8 5.3 21%

2015 970 354 0.42 20% 26.4 2.2 4.4 19%

2016E 1,097 452 0.54 27% 20.7 2.6 3.7 20%

2017E 1,266 524 0.61 15% 18.1 3.0 3.2 19%

2018E 1,473 611 0.71 16% 15.6 3.5 2.7 19%

Stock performance

Source: Bloomberg

Key data

Source: Bloomberg

-30%

-20%

-10%

0%

10%

20%

30%

40%

Oct

-14

No

v-1

4

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

8138 HK Equity Hang Seng Index

Oct 27 close (HK$) 11.10

Shares in issue (m) 837.1

Major shareholder TRT Tech (38.05%)

Market cap (HK$ bn) 9.39

3M avg. vol. (m) 0.47

52W high/low (HK$) 12.2/7.55

Oct 31, 2016

21

Sector report

Stable growth for proprietary Chinese medicines in Hong Kong in 2011-15 Stable growth for proprietary Chinese medicine products in Hong Kong Proprietary Chinese

medicine products refers to any proprietary product composed of any Chinese herbal medicines and formulated in a finished dose form. The segment is expected to sustain stable growth over the next five years. According to Frost & Sullivan, it grew from HK$1.0bn in 2011 to HK$1.3bn in 2015, a CAGR of 7.0%, and is expected to grow to HK$1.7bn by 2020, meaning a CAGR of 6.3%.

Figure 43: Breakdown of Hong Kong pharmaceutical market by western medicine and proprietary Chinese medicine

Sources: Tong Ren Tang CM’s prospectus, GF Securities (Hong Kong)

Cardiovascular proprietary Chinese medicines have grown faster than the industry average

The major proprietary Chinese medicines in Hong Kong covers therapeutic categories such as cardiovascular, respiratory, musculoskeletal, gastrointestinal, gynecological and genitourinary. Cardiovascular proprietary Chinese medicines can be used for both preventative and curative uses. Angong Niuhuang Pills account for a dominant share of the Hong Kong cardiovascular proprietary Chinese medicine market. Tong Ren Tang CM’s Angong Niuhuang Pills accounted for >90% of Angong Niu Pills in Hong Kong in 2011.

Figure 44: Industry sales of Angong Niuhuang pills in Hong Kong

Figure 45: Sales and market share of Angong Niuhuang pills in Hong Kong (2011)

Sources: Tong Ren Tang CM’s prospectus, GF Securities (Hong Kong)

Rising global demand for high value proprietary Chinese medicines Export value of Chinese medicine products posted two-year CAGR of 18.8% in 2013-15

According to the China Chamber of Commerce for Import and Export of Medicine and Health Products, exports of Chinese medicine products have been steadily growing over the years and totaled US$3.77bn in 2015, representing a two-year CAGR of 18.8% (2013-15). Exports of proprietary Chinese Medicines accounted for 7% of the total export value of Chinese medicine products in 2015 and posted growth of 4.7% YoY to US$262m. The slower segment growth in 2015

0

2

4

6

8

10

12

14

16

18

20

2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

Western medicines Proprietary Chinese medicines

HK$ bn

2011-15 CAGR: Western medicine: 8.4%

Proprietary chinese medicine: 7.0%

2015-20 CAGR: Western medicine: 6.8%

Proprietary chinese medicine: 6.3%

HK$ m

172 190 218294

516

831

1018

1221

1445

1662

0

200

400

600

800

1000

1200

1400

1600

1800

2007 2008 2009 2010 2011 2012E 2013E 2014E 2015E 2016E

CAGR: 18.9%

HK$486m: 94%

HK$30m: 6%

Beijing Tong Ren Tang Others

Oct 31, 2016

22

Sector report

was partly due to the loss of TRT Group’s export revenue to its subsidiary Tong Ren Tang CM, which is a Hong Kong entity.

Tong Ren Tang CM accounts for the majority of proprietary Chinese medicine exports The

TRT Group was the largest Chinese Medicines exporter in 2011 according to the China Chamber of Commerce for Import & Export of Medicine & Health Products. Tong Ren Tang Ltd. was the top exporter and Tong Ren Tang Tech was third in terms of export value of Chinese Medicines in China in 2011. Together they contributed ~19% of total export value of Chinese Medicines. Since 2013, Tong Ren Tang CM has assumed overseas distribution of “Tong Ren Tang” branded products and thus its market share largely represents the combined share of TRT Ltd and TRT Tech which currently holds 33.62% and 38.05% interest in the company.

Figure 46: TRT Group’s export market share and their respective relevant export value in 2011

Sources: Tong Ren Tang CM’s prospectus, GF Securities (Hong Kong)

Hong Kong is the top export destination for Chinese medicine products in terms of export value, but the United States is the fastest growing key export market Asia accounted for 58.8%

of total export value of Chinese medicine products from China in 2015, down from 73.5% four years ago. The US continued to be the third biggest Chinese medicine product export market, and its share has increased from 8.0% in 2011 to 14.3% in 2015. During the year, the Chinese regulator forged a mutual agreement for recognition of herbal extraction standards with the United States Pharmacopeia (USP), which contributed to the faster growth in Chinese medicine herbs. We believe improved regulation and supervision of the Chinese medicine industry by foreign counterparts will promote further growth in these countries.

Above-peer profitability ensures sustainable growth Competitive advantage for Angong Niuhuang Pills Tong Ren Tang CM’s Angong Niuhuang Pills

is a major TCM proprietary product in Hong Kong’s cardiovascular proprietary Chinese medicines market. The product differs from other Angong Niuhuang Pills as it contains natural musk, a regulated Chinese medicinal herb with limited supply. Most other Angong Niuhuang Pills in China do not contain these Chinese herbs. Together with ganoderma spores powder in Hong Kong, the two self-manufactured products contributed two-thirds of their product sales in 2015. Increasing stroke prevalence in Hong Kong and other Asian countries provides long-term upside Strokes are the fourth leading cause of death in Hong Kong. The prevalence rate for strokes

in people aged above 65 years is around 5%, with 55,000 patients in need of, or under, long-term treatment. This implies significant growth potential for Angong Niuhuang Pills as a preventive medicine. Higher profitability than competitors Tong Ren Tang CM has one of the largest Chinese

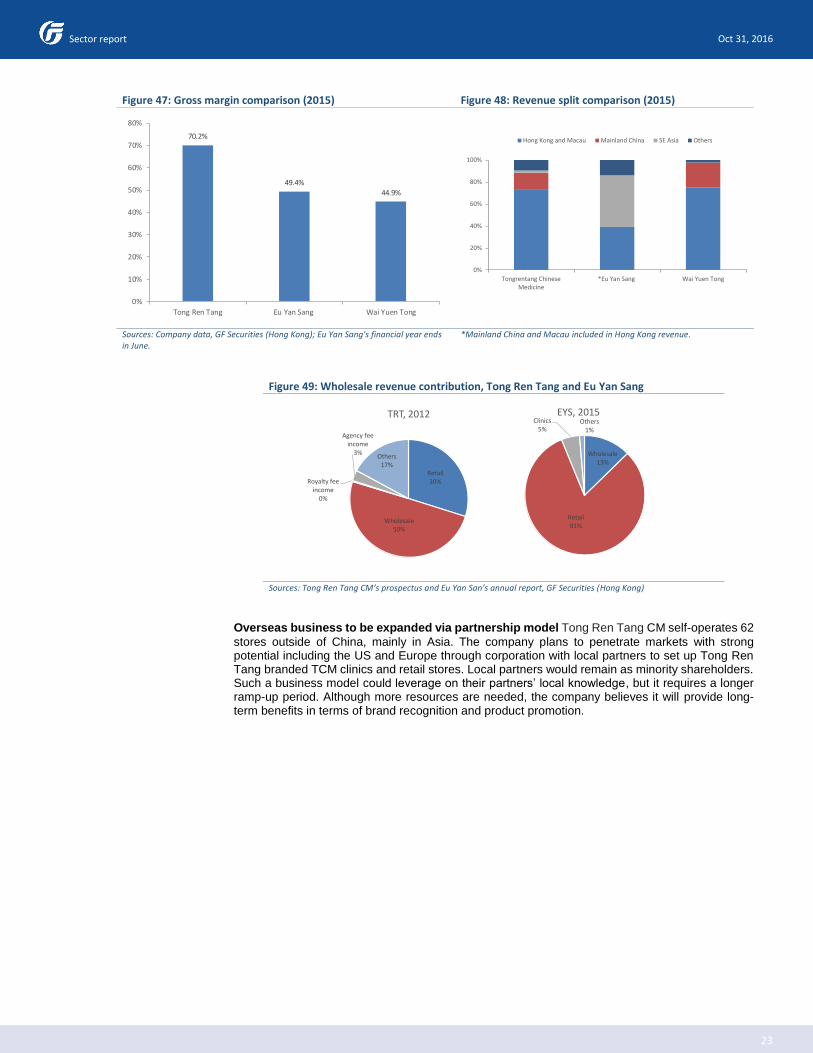

medicine retail networks in Hong Kong. Other TCM retail chain operators include Singapore-based Eu Yan Sang and Hong Kong-based Wai Yuen Tong (897 HK, NR). In contrast to its competitors, Tong Ren Tang CM’s products are mainly based on therapeutic efficacy while its peers target TCMs as health supplements. In terms of profitability, Tong Ren Tang CM has the highest gross margin in sales of key products, which is attributable to its bigger wholesale business and higher retail segment margins.

US$36.6m:16% US$7.5m: 3%

US$37.1m: 81%

TRT Ltd TRT Technologies Others

Oct 31, 2016

23

Sector report

Figure 47: Gross margin comparison (2015) Figure 48: Revenue split comparison (2015)

Sources: Company data, GF Securities (Hong Kong); Eu Yan Sang's financial year ends in June.

*Mainland China and Macau included in Hong Kong revenue.

Figure 49: Wholesale revenue contribution, Tong Ren Tang and Eu Yan Sang

Sources: Tong Ren Tang CM’s prospectus and Eu Yan San’s annual report, GF Securities (Hong Kong)

Overseas business to be expanded via partnership model Tong Ren Tang CM self-operates 62

stores outside of China, mainly in Asia. The company plans to penetrate markets with strong potential including the US and Europe through corporation with local partners to set up Tong Ren Tang branded TCM clinics and retail stores. Local partners would remain as minority shareholders. Such a business model could leverage on their partners’ local knowledge, but it requires a longer ramp-up period. Although more resources are needed, the company believes it will provide long-term benefits in terms of brand recognition and product promotion.

70.2%

49.4%44.9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Tong Ren Tang Eu Yan Sang Wai Yuen Tong

0%

20%

40%

60%

80%

100%

Tongrentang ChineseMedicine

*Eu Yan Sang Wai Yuen Tong

Hong Kong and Macau Mainland China SE Asia Others

Retail30%

Wholesale50%

Royalty fee income

0%

Agency fee income

3%Others

17%

TRT, 2012

Wholesale13%

Retail81%

Clinics5%

Others1%

EYS, 2015

Oct 31, 2016

24

Sector report

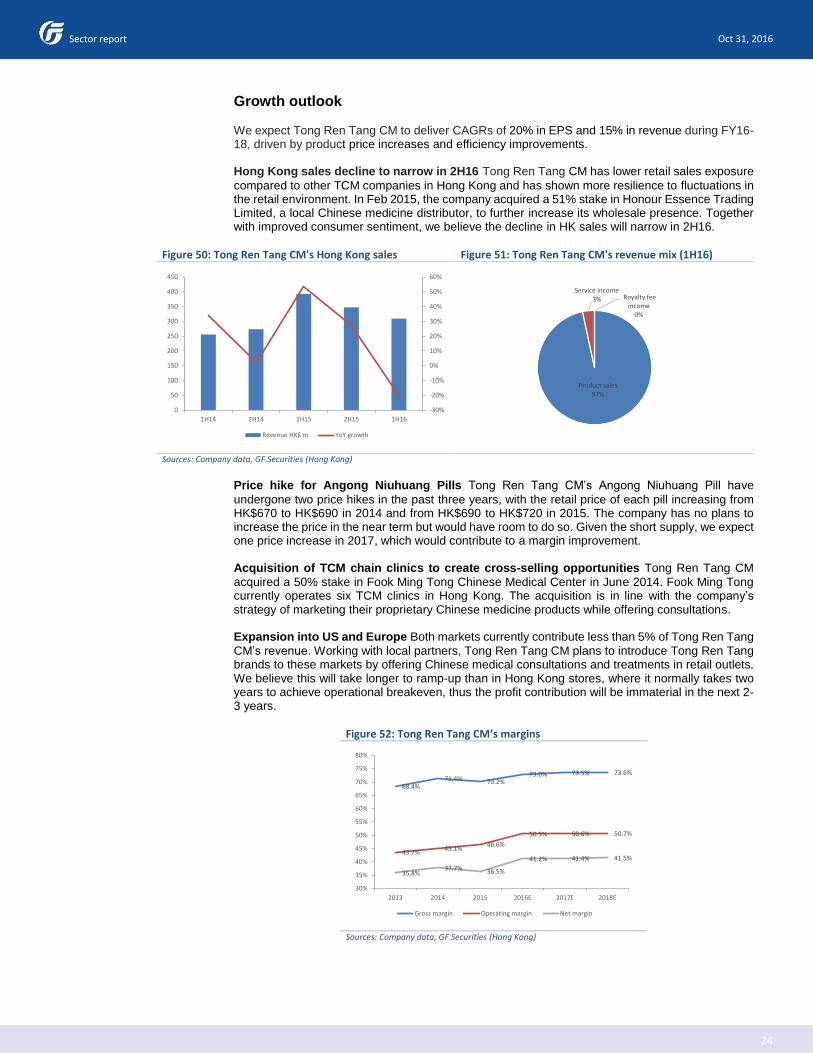

Growth outlook We expect Tong Ren Tang CM to deliver CAGRs of 20% in EPS and 15% in revenue during FY16-18, driven by product price increases and efficiency improvements. Hong Kong sales decline to narrow in 2H16 Tong Ren Tang CM has lower retail sales exposure

compared to other TCM companies in Hong Kong and has shown more resilience to fluctuations in the retail environment. In Feb 2015, the company acquired a 51% stake in Honour Essence Trading Limited, a local Chinese medicine distributor, to further increase its wholesale presence. Together with improved consumer sentiment, we believe the decline in HK sales will narrow in 2H16.

Figure 50: Tong Ren Tang CM's Hong Kong sales Figure 51: Tong Ren Tang CM's revenue mix (1H16)

Sources: Company data, GF Securities (Hong Kong)

Price hike for Angong Niuhuang Pills Tong Ren Tang CM’s Angong Niuhuang Pill have

undergone two price hikes in the past three years, with the retail price of each pill increasing from HK$670 to HK$690 in 2014 and from HK$690 to HK$720 in 2015. The company has no plans to increase the price in the near term but would have room to do so. Given the short supply, we expect one price increase in 2017, which would contribute to a margin improvement. Acquisition of TCM chain clinics to create cross-selling opportunities Tong Ren Tang CM

acquired a 50% stake in Fook Ming Tong Chinese Medical Center in June 2014. Fook Ming Tong currently operates six TCM clinics in Hong Kong. The acquisition is in line with the company’s strategy of marketing their proprietary Chinese medicine products while offering consultations. Expansion into US and Europe Both markets currently contribute less than 5% of Tong Ren Tang

CM’s revenue. Working with local partners, Tong Ren Tang CM plans to introduce Tong Ren Tang brands to these markets by offering Chinese medical consultations and treatments in retail outlets. We believe this will take longer to ramp-up than in Hong Kong stores, where it normally takes two years to achieve operational breakeven, thus the profit contribution will be immaterial in the next 2-3 years.

Figure 52: Tong Ren Tang CM’s margins

Sources: Company data, GF Securities (Hong Kong)

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

0

50

100

150

200

250

300

350

400

450

1H14 2H14 1H15 2H15 1H16

Revenue HK$ m YoY growth

Product sales97%

Service income3% Royalty fee

income 0%

68.4%71.4% 70.2%

73.0% 73.5% 73.6%

43.7%45.1%

46.6%

50.5% 50.6% 50.7%

35.8%37.7% 36.5%

41.2% 41.4% 41.5%

30%

35%

40%

45%

50%

55%

60%

65%

70%

75%

80%

2013 2014 2015 2016E 2017E 2018E

Gross margin Operating margin Net margin

Oct 31, 2016

25

Sector report

Valuation Our one-year target price of HK$12.30 implies 9% upside and is based on a target P/E of 20x our 2017 EPS forecast of HK$0.61, and represents 1.0x PEG. Other HK-listed Chinese medicine companies are trading at 15.3x 2017E P/E. The stock is currently trading at 18.3x our 2017 EPS forecast. We think this premium is justified given its above-peer profitability and solid execution. However, further share price upside will be capped by slower organic growth in Hong Kong, and as new markets are still in ramp-up phase.

Figure 53: P/E band

Sources: Bloomberg

1

3

5

7

9

11

13

15

10

/20

14

11

/20

14

12

/20

14

01

/20

15

02

/20

15

03

/20

15

04

/20

15

05

/20

15

06

/20

15

07

/20

15

08

/20

15

09

/20

15

10

/20

15

11

/20

15

12

/20

15

01

/20

16

02

/20

16

03

/20

16

04

/20

16

05

/20

16

06

/20

16

07

/20

16

08

/20

16

09

/20

16

10

/20

16

10x 13x 16x 19x 22x Share Price

Oct 31, 2016

26

Sector report

Figure 55: Financial summary

Sources: Company data, GF Securities (Hong Kong)

Year-end Dec 31 (HK$ m) FY14 FY15 FY16E FY17E FY18E Year-end Dec 31 (HK$ m) FY14 FY15 FY16E FY17E FY18E

Revenue 761 970 1,097 1,266 1,473 Non-current assets

Cost of sales (218) (290) (296) (335) (389) PPE 260 262 339 428 531Gross profit 543 681 801 931 1,084 Leasehold land 18 17 17 16 15

Intangible assets 0 61 60 61 61

Other income 1 4 4 5 6Investments accounted for using the

equity method26 23 24 24 23

Selling and distribution expenses (123) (142) (157) (181) (211) Deposits paid for purchase of PP&E 2 0 0 0 0Administration expenses (78) (90) (94) (114) (133) Deferred income tax assets 7 9 10 11 13Operating profit 344 452 554 641 747 313 373 451 540 645Net finance cost 11 9 11 13 15Other non-recurring items 0 (4) (3) (2) (1) Current assetsProfit before tax 355 457 562 651 761 Inventories 121 160 169 167 222Income tax expense (61) (82) (101) (117) (137) Trade and other receivables 165 214 364 320 455Net profit 295 375 461 534 624 Restricted bank deposits 471 520 531 541 552Minority interests (8) (20) (9) (11) (12) Bank balance and cash 563 760 917 1,380 1,495Net profit attributable to shareholders 287 354 452 524 611 1,320 1,654 1,981 2,408 2,725EPS (HK$) 0.35 0.42 0.54 0.61 0.71

Total assets 1,633 2,027 2,432 2,949 3,370Growth rates (%)Revenue 24.0% 27.5% 13.1% 15.4% 16.4% Current liabilitiesAdjusted net profit 30.5% 23.4% 27.5% 15.9% 16.7% Trade and other payables 71 77 114 221 168Adjusted EPS 20.7% 20.0% 27.4% 14.7% 15.6% Current income tax liabilities 20 36 153 175 195