Embed Size (px)

Citation preview

TOPIC: PRESUMPTIVE INCOME TAX SYSTEM AND PROFITABILITY OF SMALL

BUSINESS ENTERPRISES IN UGANDA

CASE STUDY: NAKAWA DIVISION

BY:

WERE FRANCIS

07/U/15960/EXT

207015877

SUPERVISED BY: MR. TURYAKIRA NAZARIUS

A RESEARCH REPORT SUBMITTED TO MAKERERE UNIVERSITY

IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF

DEGREE OF BACHELOR OF COMMERCE OF

MAKERERE UNIVERSIY

JULY 2011

A

DECLARATION

I hereby declare that the work in this report is entirely attributed to my personal efforts and has

never been presented before for an award

Where earlier work was cited, acknowledgement has been made.

WERE FRANCIS

SIGNATURE:……………………………………….

DATE:…………………………………………….....

i

APPROVAL

I certify that this research work has been submitted for examination under my supervision

Signature: ……………………………………………… Date: …………………………………

MR. TURYAKIRA NAZARIUS

(Supervisor)

ii

DEDICATION

I dedicate this piece of work to my late grandmother ANNA NEKESA NAMUDEPI of Busia

district.

REST IN PEACE

iii

ACKNOWLEDGEMENTS

I am grateful to the following people for their contribution, support and assistance in having this

book accomplished. Am Indebted to my supervisor, Mr. Turyakira Nazarious without whose

guidance, support and encouragement the work would never have been.

I am also grateful to my parents Mr. and Mrs. Okumu Amolo Willingstone for their continued

support, encouragement and unwavering commitment in helping me towards attaining my goals.

Thank you dad and mum.

I am particularly thankful and would like to extend my sincere appreciation to my brother Were

Edrin, my sister Namudepi Tracy and all my family members for their moral support.

I would also like to thank all my dear friends for their moral, Social and academic support they

have given me during my stay at campus especially discussion group members;Nalumu

sara,Mugisha Julius, Eric lubanga ,Mbabazi Elizabeth ,lizzmo, Mutebi, Ngabirano

Kenneth,Nabakooza Florence,Kayiga Charles and Nandaula Maria you guys and girls were

great and I will miss u all.

Special thanks go to Arinaitwe Edith, Owen, Chris and Kemisa.I appreciate all the

encouragement and support you showed me.

Lastly, I would like to thank to all the staff department of distance education for their intellectual

and logistical support.

iv

LIST OF ACRONMY

SBES Small Business enterprises

AICPA American Institute for Certified Pub

GET German Economic Team

UNCTAD United Nations Conference on Trade and Development

URA Uganda Revenue Authority

USSIA Uganda Small Scale Industries Association

USAID United States Agency for International Development

UNDP United Nation Development Programme

IMENCC Informal, Micro and Small Enterprises Sector National Coordination Committee

ITA Income Tax Act

SEC Section

UN United Nation

v

TABLE OF CONTENTS

DECLARATION..............................................................................................................................i

APPROVAL....................................................................................................................................ii

DEDICATION...............................................................................................................................iii

ACKNOWLEDGEMENTS............................................................................................................iv

LIST OF ACRONMY.....................................................................................................................v

TABLE OF CONTENTS...............................................................................................................vi

LIST OF TABLES..........................................................................................................................ix

CHAPTER ONE............................................................................................................................1

1.1 Background................................................................................................................................1

1.2 Statement of a problem..............................................................................................................2

1.3 Purpose of the study...................................................................................................................2

1.4 Research objectives...................................................................................................................3

1.5 Research questions.....................................................................................................................3

1.6 Scope of the study......................................................................................................................3

1.6.1 Geographical scope.................................................................................................................3

1.6.2 Content Scope.........................................................................................................................3

1.6.3 Time scope..............................................................................................................................3

1.7 Significance of the study...........................................................................................................4

CHAPTER TWO: LITERATURE REVIEW.............................................................................5

2.0 Introduction................................................................................................................................5

2.1 Definitions.................................................................................................................................5

2.1.1 Taxation..................................................................................................................................5

2.1.2 Presumptive Taxation.............................................................................................................5

2.1.3 Small Business Enterprises.....................................................................................................6

2.2 Presumptive Income Tax system...............................................................................................7

2.2.1 Procedures of Paying Presumptive Tax..................................................................................9

2.2.2 Types of Presumptive Tax......................................................................................................9

2.2.3 Administration of Presumptive Tax......................................................................................11

2.2.4 According to the Income tax Act 1997................................................................................13

vi

2.3 Profitability of small business enterprises...............................................................................14

2.4 The concept of Profitability.....................................................................................................14

2.4.1 Indicators of profitability......................................................................................................18

2.4.2 Measurement of profitability................................................................................................18

2.4.3 Factors affecting profitability...............................................................................................19

2.5 Presumptive Income Tax System and Profitability of Small Business Enterprises................20

CHAPTER THREE.....................................................................................................................24

3.0 Introduction..............................................................................................................................24

3.1 Research design.......................................................................................................................24

3.2 Sampling design and procedure...............................................................................................24

3.2.1 Study population...................................................................................................................24

3.2.2 Sampling methods................................................................................................................24

3.2.3 Sample size...........................................................................................................................25

3.3 Data collection.........................................................................................................................25

3.3.1 Source of data.......................................................................................................................25

3.3.2 Procedure..............................................................................................................................25

3.4 Data collection methods and instruments................................................................................25

3.4.1 Questionnaires......................................................................................................................25

3.4.2 Interviews.............................................................................................................................26

3.5 Data processing and analysis...................................................................................................26

3.6 Limitations of the study...........................................................................................................26

CHAPTER FOUR: PRESENTATION, ANALYSIS AND INTERPRETATION OF

FINDINGS....................................................................................................................................27

4.0 Introduction..............................................................................................................................27

4.1 Characteristics of respondents.................................................................................................27

4.1.1 Gender...................................................................................................................................27

4.1.2 Age bracket...........................................................................................................................28

4.1.3 Education level.....................................................................................................................28

4.1.4 Nature of the respondents business.......................................................................................29

4.2 Presumptive income tax...........................................................................................................30

vii

4.2.1 Registration for presumptive tax..........................................................................................30

4.2.2 Awareness on tax paid..........................................................................................................31

4.2. 3 paying right amount.............................................................................................................31

4.2.4 Business survival..................................................................................................................32

4.2.5 Computation of presumptive tax..........................................................................................32

4.3 Profitability..............................................................................................................................33

4.3.1 Level of Profits.....................................................................................................................33

4.3.2 Cash Balances.......................................................................................................................34

4.3.4 Other sources of funds to gear business operations..............................................................35

4.4 Relationship between n between presumptive income tax and profitability levels.................36

CHAPTER FIVE: SUMMARY, CONCLUSIONS AND RECOMMENDATIONS.............38

5.0 Introduction..............................................................................................................................38

5.1Summary of findings................................................................................................................38

5.2 Conclusions..............................................................................................................................39

5.3 Recommendations....................................................................................................................39

5.4 Areas for further research........................................................................................................40

REFERENCES............................................................................................................................42

APPENDICES..............................................................................................................................46

APPENDIX I................................................................................................................................46

QUESTIONNAIRES...................................................................................................................46

APPENDIX II...............................................................................................................................51

viii

LIST OF TABLES

Table 1: Presumptive Income tax rates..........................................................................................13

Table 2: showing sex of respondents.............................................................................................27

Table 3: showing the age distribution............................................................................................28

Table 4: showing the education level of the respondents..............................................................28

Table 5: showing the nature of the respondents business..............................................................29

Table 6: showing duration of business..........................................................................................29

Table 7: showing whether the business is registered for presumptive tax....................................30

Table 8: showing whether the tax payers knew the type of taxes they are supposed to pay.........31

Table 9: Showing whether Amount paid match with the amount earned......................................31

Table 10: showing whether business closed after failing to pay taxes..........................................32

Table 11: Showing whether tax payers know how presumptive income tax is computed............32

Table 12: showing whether businesses generate enough profits to carry out business operations33

Table 13: showing whether the business is left with some cash to acquire more stock................34

Table 14: showing whether presumptive tax affect profits of SBES.............................................34

Table 15: showing whether businesses use some external sources of funds to acquire stock.......35

Table 16: showing whether presumptive tax system affects the following elements of business.36

ix

ABSTRACT

The purpose of the study was to examine the relationship between presumptive income tax

system and profitability of small business enterprises in Uganda. The conceptual framework was

based on the relevant literatures on presumptive income tax system. The specific objectives of

the study were:,to evaluate the effectiveness of presumptive income tax system, to examine the

profitability of small business enterprises and to examine the relationship between presumptive

income tax system and profitability of small business enterprises.

In order to achieve the above objectives data was got from both primary and secondary sources.

Primary data was collected through administering of questionnaires to sample of 50 traders in

five areas of nakawa market, bugolobi, kitintale, ntinda and mbuya while secondary data was got

from dissertations, books, journals and unpublished research reports.

The findings show that most traders are not registered for tax and ignorant about the type of

taxes they pay and a majority of them agree that presumptive income tax system affects their

profitability levels.

Recommendations have been made which include the following;

i. Tax payers should employ professionals’ like accountants to keep for them proper books

of accounts.

ii. The government should introduce tax education in schools so that people know the

importance of tax.

iii. URA should embark on intense tax education programmes

iv. URA should as well also embark on a nationwide registration exercise of all small scale

businesses.

x

CHAPTER ONE

1.1 Background

Presumptive income tax system is a method used to tax small business enterprises in Uganda

with annual turnover of Uganda shs.50 million and below sole traders and self employed

categories. (ITA 1997 SEC (5). It was introduced during the 1997 tax reforms in order to ease

the taxation of Small Business Enterprises, which are hard to tax and were characterized by high

non – compliance levels (Sserwanga and Walter; 2003).

This system of taxation is uncertain, inequitable to the investors and the tax payers. Unlike

individual income tax however, the tax rates are varied. While some Small Business Enterprises

pay a fixed rate ranging from shs. 100,000 to shs. 450,000 per annum, others pay 1% of their

gross turnover whichever is lower. Equity therefore does not prevail across the board for tax

payer in the same bracket. This mean that the amount to be paid is not certain (un predictable) to

the tax payer because assessment is based on presumed income (Kirambaire 2003).

Presumptive income tax system is imposed on the gross turnover without any deductions; small

firms are neither entitled to generous initial allowances for investments in machinery or subject

to any restrictions on writing off business expenditure. This deprives them of the benefits that

could enhance their growth and profitability. (Reinikka and Collier, 2003). It should be noted

that, Uganda is private sector is dominated by Small Business Enterprises, providing backward

and forward linkage to the large scale enterprises. (Government of Uganda, 1997).

Profitability may mean the excess of revenues over expenses incurred in generating those

revenues. According to Pandey (2002), profitability is a measurement of overall performance and

effectiveness of the firm. It represents an increase in cash flows plus changes in the value of

assets. Profitability can be measured by the degree of cost reduction that is the ability to

minimize costs and maximize revenues in the business.

The research therefore focused on Small Business Enterprises owner which include private

investments of individual or group of individuals in an attempt to generate more revenue and

expand on their profits alongside taxes.

1

The research will be carried out in Nakawa division because of the numerous numbers of Small

Business Enterprises there. In Nakawa division, presumptive income tax rates have had a

negative impact on the profitability of Small Business Enterprises. Despite the endeavors of

Small Business Enterprises to generate adequate sales turnover, the Ugandan tax structure does

not favor them. The high presumptive income tax rates on their gross turnover tend to threaten

them away from the industry yet they account for 93% of total number of Uganda firms and

generate more than 52% of total turnovers employing 82% of the private sector workforce

(Akileng 2003). Therefore, the vitality of Small Business Enterprises in Uganda is essential to

government’s objectives to raise the rate of productivity growth in the economy.

1.2 Statement of a problem

Presumptive income tax rate system was enacted by government as per second schedule of

section 5 of the income tax act (1997) to promote SBES. However, it has affected their

profitability as measured by the return on capital employed.

The presumptive income tax system operates in such a way that those business whose annual

turnover is less than five million are exempt from tax. Those whose gross turnover is more than

five million but less than twenty million pay 100,000,those whose annual turnover is more than

twenty million but less than fifty million pay 250,000 or 1% of gross turnover.lastly,those whose

gross turnover is more than fifty million pay 450,000 or 1% of gross turnover which is ever

lower(Pius K Bahemuka).

Despite the fact that presumptive income tax system was enacted to promote Small Business

Enterprises, they have continued to perform poorly(Kiiza, 2005), 35% of Small Business

Enterprises do not survive for more than one year after commencement (UN development paper

1998).

1.3 Purpose of the study

The study was to find out the relationship between the presumptive income tax system and the

profitability small business enterprises in Nakawa division.

2

1.4 Research objectives

a. To evaluate the effectiveness of the presumptive income tax system

b. To examine the profitability of Small Business Enterprises.

c. To determine the relationship between presumptive income tax system and profitability of

Small Business Enterprises.

1.5 Research questions

The research questions to guide this study are:-

a). How effective is the presumptive income tax system in Uganda?

b). what is the annual turnover and profitability of Business Enterprises?

c).Is there any relationship between presumptive income tax system and profitability of Small

Business Enterprises?

1.6 Scope of the study

1.6.1 Geographical scope

The study focused on Small Business Enterprises in Kampala Nakawa division. This is because

the division has many business enterprises and business activities. The study was restricted to

Nakawa division due to limited funds and time.

1.6.2 Content Scope

The research focused at how the presumptive income system is a major threat to the profitability

performance of Small Scale Enterprises.

1.6.3 Time scope

The study examined the effect of the presumptive income tax rates on the performance of Small

Scale Business Enterprises from 2006 to 2010.

3

1.7 Significance of the study

The study intends to make the following contribution.

a) To create knowledge for policy makers and tax administrators on the relationship between

the presumptive income tax system and the profitability of Small business Enterprises in

Uganda.

b) To make a contribution in terms of knowledge in the area of taxation and performance of

small business enterprises since little research has been done in this area.

c) To stimulate further research in investment and taxation in Uganda; with specific interest in

Small business enterprises.

d) To enable potential and existing investors to appreciate the effects of taxation in investment

returns and capital flow.

4

CHAPTER TWO: LITERATURE REVIEW

2.0 Introduction

This chapter is preceded by the chapter on the introduction that brings an insight on the

background. This chapter therefore reviews the existing literatures on presumptive income tax

system and profitability of small business enterprises. The literature tries to justify the existence

of a relationship between the presumptive income tax system of small business tax payers and

the profitability of small business enterprises.

2.1 Definitions

2.1.1 Taxation

Taxation is process by which government or municipal quasi public body raises monies to fund

its operations. It’s the impact an investment has on the investor’s liability for the payment of

federal, states, and local taxes. It is a process of administration and collection of taxes. ,

(Tumuhimbise, 2001).

A tax is defined as a tool used by government to raise revenue to finance activities that benefit

the community as a whole which if left undone, no individual community as a private concern

would undertake to perform it. (Minister of Finance Hon. Nkanji, Budget speech presented on

June 1995).

Economists define a tax as a leakage from the circular flow of income into the public sector.

2.1.2 Presumptive Taxation

The oldest example of presumptive taxation can be found in ancient Egypt. The amount of corn

to be handled over the treasury in kind differed from year to year. The level of taxation was

decided by linking the amount of corn to be handed over a constant factor and a variable one

(Grapper Haus, 1997).

5

Presumptive taxation involves the use of indirect means of ascertaining tax liability, which is

different from the usual rules based on the tax payer’s accounts. The term “presumptive”, is used

to indicate that there is legal presumption that the tax payer’s income is no less than the amount

resulting from application of the indirect method (Thuronyi, 1996).

In Uganda, presumptive taxation is meant to cater for the incomes of small business enterprises

in the informal sector who do not keep records. Presumptive taxation is basically a method of

determining income and tax liability of small tax payer with the view of widening the tax base

and increasing the tax revenue yield. (Tindimawe 1999)

2.1.3 Small Business Enterprises.

The definition of Small Business Enterprises varies from person to person and from one

economy to another. Thus its hard to get a concrete definition. The definition is usually based on

the number of employees, turnover or value of assets.

Small business enterprises are defined in respect to the number of people employed, capital

employed and sales turnover (Astley, 1997), while Belkaovi and Karpic, (1989) used nets sales

to define small business enterprises, while (Trotman and Bracley, 1981) used both sales and total

assets to define small Business Enterprises, UNCTAD,(2000)defines small business enterprises

as a business involving one to two persons, with simple enough activities to be managed directly

on a person to person basis.

A small business enterprise is defined as a business involving one to five persons, with simple

enough activities to be managed directly on a person to person basis.(Kizza ,2006).

Ministry of finance, planning and economic development defines a small business enterprises as

a unit within a capital investment not exceeding $300,000.

A small business enterprise is one employing between 1-25 persons / people and with assets and

capital not exceeding US$ 100.000 (Uganda small scale industries Association (USSIA).

6

Because of lack of consistency of the definitions of Small business enterprises, the difference in

the definitions will not be fundamental to this research (Hall berg, 2000). However, for the

purposes of this study, Small business enterprises are defined as those resident business units

with gross annual turnover of not more than fifty million Uganda shillings. This definition

includes any business irrespective of number of employees or capital invested but excludes any

professional and public utility business (ITA 1997).

2.2 Presumptive Income Tax system

Presumptive income tax system refers to a method of collecting taxes from tax payers using the

gross annual turnover (ITA, 1997). The income tax liability of the tax payers is determined

without using financial reports. The presumptive method applies to resident, non professionals

with a gross annual turnover of not exceeding fifty million shilling (Akileng, 2006).

Presumptive income tax system was introduced in the 1997 income tax reforms to streamline

income tax collection (Background to the budget 1996) and widen the income tax base (Bird,

1992).

This tax system does not apply to resident’s tax payers who are in the business of providing

medical, dental, architectural, engineering, accounting, legal or other professional services,

public entertainer’s public utility services and construction services (ITA 1997 and Waliya

2005).

Presumptive income tax system is based on some measures of economic activity that proxies for

taxable income, rather than taxable income itself (Christian 2004). The accounting requirements

are not completely absent, as tax payers must be able to prove that the qualities to presumptive

tax regime.

Presumptive income tax system is employed in economies where specific groups of individuals

of tax payers are hard to tax, these groups of tax payers lack financial transparency that allows

for effective taxation by the government. (GET, 2004)

7

Chen and Reinikka (1999), concerned with this view, they stated that the non taxable small

business enterprises in Uganda are now subject to a presumptive income tax, unless they opt to

file an income tax return.

Omara (2004) makes a case for presumptive income tax system and appreciates that this kind of

tax is necessary for the hard to tax payers who comprise a majority of the payers.

Sunley etal, (1996), recognizes the complex and complicated nature of taxation of small business

that existed under the deposit system before 1995, in making a recommendation for Uganda to

re-adopt a farm of presumptive income taxation for small business enterprises based upon

standard assessments did not show whether it was an efficient kind of tax for small business tax

payers as to qualify for a good tax system.

Aaron and Slemrod (1999) assert that presumptive income tax system is appropriate in an

economy with a sizeable illiterate population and a big informal sector like Uganda.

However, the problem with the presumptive income tax system is how to keep out the system

large and medium enterprises that hide themselves from the tax men’s eye. Thus as the small

become bigger, they will graduate into the normal tax system, so one must also ensure that, those

who are in the normal system already or should be in the system do not migrate a shift into the

simplified system and take on the disguise of smallness to shield / themselves from taxation

(Bird and Walter, 2003).

As pointed out by Bird and Wallace (2004) the critical issue is whether these presumptive

methods of taxation are really effective first in bringing firms into the formal economy and then,

after few years, forcing them to move into the normal tax system, while minimizing the number

of firms that move from the normal tax regime into the simplified one. The main problem is that

these objectives are to some extent inconsistent. To be attractive for informal firms the methods

need not to be simple and based on readily available information to reduce compliance costs

(Araujo, Bonjean and Chambas, 2004), they should also provide for an effective taxation that

8

will be lower than that based on the normal tax rules. However, this would discourage them from

moving into the normal tax regime and attract firms that are in the formal sector to move to the

presumptive regime, resulting in loss of revenue to the Tax Authority. One solution to this

conundrum might be a periodical revision of the threshold for eligibility for the simplified

regime.

2.2.1 Procedures of Paying Presumptive Tax

In order to enjoy the benefits of paying the lower tax in each market, a tax payer is required to

file a return of gross turnover for a given year of income otherwise a tax payer will automatically

be assessed to the standards (Pius K Bahemuka 2000) and Uganda Revenue Authority (URA)

The payment of Presumptive Income Tax can be paid in full amount during the financial year or

tax payer may opt to pay the tax provisionally during the year in four equal quarterly installments

in case of individuals. Then the two equal semiannual installments in case of companies (URA

journals, 2005).

According to revenue Staff Magazine volume 4 No. 1 July December 2003 presumptive tax

contributed 2.16 billion Uganda Shillings in the year 2002-2003.

2.2.2 Types of Presumptive Tax

Unified tax. The unified tax is the most important presumptive tax. It applies to business

operated by natural persons with up to 10 employees and an annual gross income of not more

than $500,000. Legal entities are subject to the unified tax in case they have not more than 50

employees and an annual gross income of not more than $1000. The tax rates are 6% on

turnover.

Fixed tax: The second most important presumptive tax is a fixed tax in form of patent. This

option may be used by the natural persons with a gross income from entrepreneurial activities in

the 12 months preceding the grant of the patent of up to 7000 times the “tax-fee minimum

income, in case the business has no more than 5 employees. A person applies for such a patent to

the local revenue authority; patent fees are set by local councils between $1000 and $ 1200

(Amon, 2000).

9

Presumptive systems based on indicators have become increasingly popular in transition

countries, these systems aim at being more precise than turnover – based systems in estimating

the profit potential of the individual entrepreneur (Hughes, 1999). However, this brings up a

clear conflict of the objective. The objective to tax the true potential profit of the small business

conflicts with the objective to design a simple and transparent system policy makers in transition

countries face considerable difficulties designing indicator based systems that establish an

acceptable balance these objectives. Systems tend to be extremely complicated and unclear or

they do not sufficiently differentiate between business activities (Drake, 2000). The latter is in

case Georgia, where presumptive system only distinguishes between five groups of activities.

The gap left will be filled by the current study using the case study of Uganda.

In this case, except for retail trade, transportation and jewellery shops (and restaurants, which are

subject to a different regime) all small business production and service activities are in the same

category and thus subject to the same tax burden. The system therefore has not achieved its

objectives to tax according to the profitability of small businesses

Brighton (1993) observed that there are three presumptive taxes for very small businesses that

can be assessed by the local administration within certain limits; the so-called trade permit (for

service), the small enterprise tax (for intermittent trade activities), and the market fee (for selling

agricultural produce).

As Thiessen (2002) notes correctly, it is hard to understand why sole entrepreneurs in the service

sector with no employees and a gross income below $1000 per year should have the choice of

three presumptive taxes. Such entrepreneurs can either opt for the unified, tax the fixed tax, or

for the trade permits. Many other small businesses have at least a choice between two taxes, the

unified tax and the fixed tax. The Ukraine approach offers small business the possibility of tax

shopping, unnecessarily complicates the tax system, and reduces the revenue collection from this

sector of the economy.

10

2.2.3 Administration of Presumptive Tax

In Ukraine, a USAID report lists presumptive taxation administration as an instrument to

facilitate the collection of revenues from the shadow economy. Similarly, the letter of intent of

the government of Moldova of November 30, 2000, which describes the policies that Moldova

intends to implement in the context of its request for financial support from the IMF, includes a

commitment to analyze the appropriateness of a presumptive tax administration on small

enterprises to draw private business into the tax net. Along the same lines, a senior IMF official

considers the administration of presumptive to be influenced by a number of factors such as

micro economic policy decisions, the efficiency and effective of the administrative and also the

degree of fiscal corruption.

Therefore in regulations dealing with taxation, the introduction of threshold levels or reduced

monitoring and reporting requirements can significantly reduce the burden and compliance costs

administration for 5, MBE’s. On the other hand several World Bank reports also have pointed to

the weaknesses and risks of presumptive tax systems. The FAIS (2001) report on Georgia, a part

from highlighting the potential benefits of a simplified scheme, considers a fixed tax to be very

complicated, and a recent World Bank report on tax policy and tax administration in Ukraine

discusses the risk of lack of focus and unjustified generosity of presumptive systems (Ivonavich,

2001). Obviously there is a relatively short history of small business taxation in transition

countries.

In the initial stage of tax reform some countries experimented with the use of tax incentive

schemes not only for large business and foreign investments but also for large businesses and

foreign investments but also for small business development. In Kazakhstan, in the first stage of

transition (1990-1993) incentives for SMBE’S were introduced, exempting Sambas from profit

tax for the first three years after establishment. For the fourth years they paid 50% of the tax rate,

with the full rate applied only after five years.

During that period, the number of small businesses grew rapidly, in part because of re-

registration of the previously established coops. Many small business were set up by big state-

owned enterprises whose managers, using incentive granted to small businesses, often put state

11

resources into them. This resulted in serious abuse and embezzlement since there were no legal

criteria for the status of small business entities in order to improve the situation, the government

had to take extreme measures and abolished all privileges.

Similarly in Moldovan the law, on supporting and protecting “small businesses” of May 1994,

established tax holidays for five years. For micro – enterprises and two years for small

enterprises engaged in priority activities, such as construction, production of medical equipment

and production of children’s food stuff. In case of non – priority activities the tax holidays were

reduced to three years for

micro – enterprises and one year tax holiday schemes are not an appropriate instrument to

address tax evasion in the small businesses sector, and the specific compliance problems of

micro enterprises and self – employed, transition countries generally have moved to the design of

simplified for hard – to – tax payers along the lines of systems applied in other developing and

developed countries. There are three main types of systems in place in the region.

They are based on turnover/gross incomes,

Specific indicators for the size and output of the business, such as the floor space, the number of

employees or the location of business or they are;

General patents for specific professions irrespective of the size, location and turnover of the

business.

A number of transition countries use turnover or gross income as a parameter to determine the

tax liability of small business (Hoyte, 2007). Turnover or gross – income – based systems can be

structured in different ways. One alternative is to apply the same tax rate to all businesses subject

to the tax, irrespective of the business activity. This approach fails to consider that profit margins

can be substantially different in different business sectors. Examples are the unified tax in

Ukraine, which operates in principle with only one rate of six percent on sales.

Alternatively, you divide the small business community into a number of business segments with

different tax rates for the individual segments. This is supposed to take into account the different

profit margins in business segments, although the number of segments under a turnover based

systems is relatively small (Nair, 1990). It is generally tax far less differentiated than an indicator

12

based systems. Examples for this alternative are the Armenian small business tax, which

distinguishes three categories of business traders, who pay 4% of gross turnover. Caters with a

7% rate on gross turnover and other businesses, for which the rate is 7% for turnover up to Dram

30 million and 12% for the portion of turnover exceeding Dram 30 million (Baros, 2004).

2.2.4 According to the Income tax Act 1997, Small Business enterprises whose annual gross

turnover is less than 50 millions have the following as their rates as per 2nd schedule sec. 5.

Table 1: Presumptive Income tax rates

Class Tax applicable

Gross turnover does not exceed 5 million per annum

5 million per annum

0 (NIL)

Where gross turnover exceeds 5 million but not exceeding 20

million per annum

100,000

Where gross turnover exceeds 20 million but does not

exceed 300 million per annum

250,000 1% of

gross turnover

which ever is

lower.

Where gross turnover exceeds 30 million but does not

exceed 40m per annum

350,000 or 1% of

gross turnover

which ever is

lower

Where gross turnover exceeds 40m but does not exceed 50m

per annum

450,000 or 1% of

gross turnover

whichever is

lower

Source: Secondary data (Pius K. Bahamuka)

Basing on the presumptive tax rates in table 1 above the rates do not favour performance of

Small Business Enterprise. These rates are high and are computed on gross turnover rather than

profits, thus scaring away Small Business Enterprise since this will reap the invested funds.

13

Several presumptive tax assessment programs can be used to improve Small Business Enterprise

compliance, but they are not properly managed in many countries. The system used in a country

should presumable be related to the policy objective. For example to reduce evasion in general or

simplify the system for small tax payers as well as to the sophistication of its tax administration

(bird and Wallace, 2003).

2.3 Profitability of small business enterprises.

The assessment of financial performance of profit entities has a well established methodology

that includes the computation and interpretation or univariate and multi-variate modes.

Univeriate predictors of performance of periods and there ratios assess liquidity position,

profitability levels and efficiency, (Makerere Business Journal, 1996).

A study carried out by USAID 1995) revealed that the small business enterprises sector employ

about 20% or the population of working age and 60% of entrepreneurs in Uganda depend on

their business for at least half of their business income.

Profitability of Small Business Enterprises is therefore vital to the economy because a large

percentage of the population depend on them for their livelihood, there is thus need to support

these Small Business Enterprises (Kiiza, 2005).

2.4 The concept of Profitability

Boggers (1967) described profitability as the organization’s desired state where turnover is the

greater than input costs. This was corroborated by Herman son et al (1987) who said profitability

is the organizations ability to generate income. Therefore, profitability must reflect only in the

income statement of the organization to certify that the income generated is greater than the input

costs.

The growth of Small Business Enterprises has retarded due to lack of knowledge on taxes. Mitra

(1997) found out that most enterprises in Uganda are struggling with no profit and hence no

14

taxable income yet they would not have paid it they were to use the corporate rate. This is due to

the fact that most Small Business Enterprises do not keep proper books of accounts. Taxation has

thus greatly reduced their profits thereby undermining their struggle to expand.

Taxes directly affect the profitability of business resources (Mutebi 2004). Presumptive income

taxation on small business enterprises greatly reduces their profitability, limits their leverage of

growth and creates poor revenue performance, (Asio, 2004).

Also, Mitra (1997) asserts that income tax mismanagement is one of the principal causes of

persistent budget deficits, he said that mismanagement of taxes forces business to close down

most of the time, making them earn less than expected revenue since then usually loose

customers on closing, Small Business Enterprises have little capital investments such that if this

capital is taxed, as it usually is, the business are left with no means of survival.

Generally speaking the principal motive of most small business enterprises is profitability.

Maximization of profits is not the only motivation of small business enterprises but typically the

most important therefore the success of any business depends on the profits it enjoys, (Batty

1978). The greater the percentage returns, the more successful the business is regarded Birabwa

(1996) says profits of Small Business Enterprises are maximized through cost reduction, good

management skills and good budgetary control.

Pandey (1995) indicates that profits are made to measure the operating efficiency of business

firm. The ownership of the small business enterprises is interested in the profitability of the firm

which enables the owners to get a reasonable return on capital employed

Liversey (1987) concurred with this view. He argues that profits are a reward for successful

entrepreneurial activities and so profits are a source of finance for future ventures and growth of

Small Business Enterprises. The owner should evaluate the performance of his business in terms

of profits.

Further more, a study carried out by Tumwine (2001) revealed that high taxes hinder business

expansions, with a big proportion of business profits ending up being paid as taxes. Therefore

profits of Small Business Enterprises may be greatly reduced because of the taxes paid by them.

15

In order to survive, traders have been forced to increase prices of their commodities so as to

incorporate the tax element but this has left most of them unhappy as the number of customers

has decreased hence a reduction in their sales, (Kiiza, 2003).

It should be noted that taxation is likely to encroach on expected revenue thus reduced

investment finance because most Small Business Enterprises are financed out of their profits and

savings. This is in line with the argument that Small Business Enterprises depend entirely on

internally generated funds for their growth and survival since they can hardly access loan capital

from financial institutions due to the high borrowing rates and requirements for collateral

security. Therefore over taxation of their profits means depleting their major source of funds for

expansion (Mugulausi, 2001)

In the recent surveys, small businesses in Uganda have blamed unfair taxes for their poor profits

and in some cases, their business failure. According to the report by Ministry of Finance (2004)

people are angry about the taxes. The plethora of local taxes more especially presumptive tax in

damaging local enterprises and undermining the credibility of government (report by MOF,

http//www.afrika.no).

The World Bank “ Business Environment and Enterprise performance survey 2”, carried out in

transition countries in 2002, indicates that the introduction of simplified tax systems has not

substantially changed the perception of the small business community that the tax burden for

Small Business Enterprise is too high and create an obstacle for business development. The

survey shows that even in countries operating a simplified system, complaints about high taxes

are as frequent as or even more frequent among Small Business Enterprise than among large

businesses.

Presumptive income taxation techniques have been employed for variety of reasons; one is for

compliance burden on tax payers with low turnover and to combat tax avoidance or evasion.

Presumptive income taxation methods provide a more certain and equitable distribution of the

tax burden that stimulate profitability of the business firms (Thuronyi, 1996). The certainty and

16

equity of the presumptive income tax system can be considered desirable because of their

incentive effects on the tax payers’ ability to earn more income as he meets his tax liability

Small business enterprises owners are aware and bitter that businesses of dramatically different

assets and levels of income are often assessed the same amount of taxes. The primary concern

was in there nature of assessments which are random. These remote assessments generate

uncertain and inequitable tax liability which pushes businesses into terminal poverty of their

assets that have declined but they are expected to pay the same amount of tax liability

(Muhumuza and Ehhart, 2000). Certainty and equity are important to tax system because it helps

to improve on the performance of the firms in terms of revenue which increases the level of tax

compliance. (AICPA, 1992).

The efficiency and convenience of the presumptive income taxation may be difficult to evaluate

in the success of their goals. The efficiency and convenience of the presumptive income tax

system should aim at obtaining some basic level of revenue from all economic agents of small

business enterprises (Bird and Wallace, 2003).

Convenient and efficient presumptive income tax system minimizes the burden of payment by

coordinating it with the level of profitability of the small business enterprises. The quality of

convenient and efficient income tax system should be able to increase the ability of the small

business enterprise to generate high revenue (Muhumuza and Ehrhart, 2000) This view is

supported by AICPA 1992, who stress that a convenient and efficient tax system reduces the cost

to collect and to pay taxes to both the government and small enterprises, and hence increasing

the ability of the Small Business Enterprises performance.

2.4.1 Indicators of profitability

According to Kamukama (2008), contribution is excess of sales revenue over the variable costs

incurred by the company in generating these revenues. Profit – volume ratio is a good indicator

of the rate at which profit is being earned in the business.

The high profit volume ratio indicates that there is low profitability in the business.

17

According to Arura (2004), the profitability of different sectors of a business such as sales areas,

class of customers, product lines and methods of production may be compared with the help of

profit – volume ratios.

The profit level of a business can also be indicated by an increase in the sales. If the sales of a

business increase, there will be corresponding increase in the costs, or when the marginal

increase in sales is greater than the marginal increase in costs varied in generating the revenue,

profits also increase (Arura, 2004).

2.4.2 Measurement of profitability

According to Rose Mary (2011), every firm is most concerned with its profitability and one of

the most frequent used tools of financial ratio analysis is profitability ratios which are used to

determine the company’s bottom line.

Profitability ratios show a company’s efficiency and performance. The commonly used ratios are

Gross Profit margin, net profit and operating profit margin.

Net profit margin

The net profit margin shows how much of each sales shillings shows up as net income after all

expenses are paid (Apollo 2011) For example if the net profit margin is 10% it means that 10%

of every shilling is profit. It measures profits after consideration of all expenses including taxes,

interest and depreciation.

Net II margin (%) = Profit after tax x 100%

Sales revenue

Gross profit margin

Looks at the cost of goods sold as a % of sales. This ratio looks at how well a company controls

the cost of its inventory and the manufacturing of products and subsequently passes on the cost

to its customers. The larger the margin the better for the firm.

Gross profit margin = Gross profit x 100%

18

Sales revenue

Operating profit margin

Operating profit margin is also known as earnings before interest and taxes. The operating profit

margin looks at the earnings before interest and taxes as percentages of sales.

Operating profit margin = earnings before interest and tax x 100

Net sales

2.4.3 Factors affecting profitability

Segmentation of the market

According to Nigel and Christine (2007), indiscriminate use of the marketing mix is a wasteful

use of precious resources. Competitive advantage is a relative concept that involves

differentiating an organization from its rivals in the eyes of the customer.

Individual demand

According to Charles and Coven, 1992), an individual demand schedule for a specific

commodity is the quantity of that commodity a person is willing and able to purchase at each

possible price during a particular time. A reduction in demand of a commodity reduces the

revenues. This leads to a reduction in profits.

Customer acquisition strategies

Christine and Nigel (2007) argue that increasingly it is recognized that the retention of existing

customer is seen as important as acquisition of a new customers. Increased customers imply

increased revenue.

Profit planning

According to Pandey (2002) a profit plan is a short term plan. It’s an action plan to guide

managers in achieving the objectives of the firm. It is comprehensive and conducted plan

expressed in financial terms for the operations and resources of an enterprises for some specific

period of time.

Marketing strategy

Is a statement of how an organization plans to compete for business on its particular market.

Effective planning must establish targets, identify how and when those targets are to be achieved

19

and establish who will take responsibility for the relevant marketing tasks (Christine and Nigel,

2007)

Pricing

Pricing is concerned with determination of revenues. Pricing plays a crucial role in the derivation

of the product margin and profit. The emergencies of profits is similar easy and simple to grasp;

it’s the purchase price minus all direct and indirect costs (Christine and Nigel, 2007). According

to Malta (2008), the competitive structure of the market makes it aptly clear whether the decision

variable for management in a particular situation would be price or output or both. In a situation

where there are many buyers and sellers, the firm has to sell its product at prevailing market

price and its control will be limited in the amount of units to be sold.

Motivation of workers

Motivation improves the productivity of workers. Regardless of the type of endeavor, the

management task is essentially the same; that is, to create and maintain an internal environment

in with individuals working together as a group attain efficient performance in conformity with

the broad objectives of the firm. The environment should motivate individuals to make their

maximum contribution to the efforts of the group (Thomson, 1979).

2.5 Presumptive Income Tax System and Profitability of Small Business Enterprises.

According to Keith (1994), Taxes affect performance of Small Business Enterprises in two ways.

First by influencing the aggregate supply of the main factors of production by raising or lowering

net (after tax) returns or profits and secondly by influencing the efficiency of resources

utilization.

Presumptive Income Tax system introduces a single gross turn over Tax that leads to creation of

unequal conditions for different Enterprises and therefore violates Tax equity and efficiency as it

distorts economic processes. This raises the question of introducing the different tax rates in

order to meet the different gross turn over ratios. But this has provoked tax saving adjustments

among the Small Business Enterprises. These processes lead to lobbying pressure in order to get

a lower tax rate. More over government has to specify suited Tax rate according to the gross turn

over.

20

In a country like Uganda, were the Tax authorities have a high degree of discretion (Chen and

Reinikka, 1999) and under the presumptive income tax system, we expect that the relationship

between effective tax rates small business enterprises needs to pay to influence the growth and

profitability of these firms (Raymond and Jacob, 2002).

Dalton (1991) noted that taxes reduce the efficiency of the tax payers advisory, affect their

ability to work and hence produce resulting into growth effects and profitability of the

investments. High growth firms are less likely to see presumptive income taxation more

problematic than low growth Small Business Enterprises. However, more Small Business

Enterprises firms would enter the high growth and performance category if the tax regimes were

not demanding (foreman-peck et al, 2004). This is consistent with Hanford et al (2003) finding

that small business enterprises that perceive taxes as most burdensome also experienced higher

costs of growth.

Hendy (2003) believes that fiscal policies are drivers that facilitate small business enterprises

growth and profitability by promoting high productivity and demand. He argues that poor

taxation regulation effectively work against and inhibits the achievement of these objectives.

Business Taxes, cost of compliance with government regulations is the most critical issues to

small business investment performance.

Businessmen regard a simpler and a fairer system of taxation as essential conditions of any

operational Programmes to support Small Business Enterprises Investment activities. When

Small Business Enterprises are in initial stages of development its investment requirements are

particularly high while the in house capacity to finance these requirements is inevitably limited

and considering the job creation potential of Small Business Enterprises, the Presumptive

Income Tax system should provide an active existence of these firms irrespective of any negative

side effects such a measure might produce (Pripisnov, 1996).

Reinikka and Sven son (1998), while comparing investment and profitability rates among firms

in Africa found that, Uganda’s Investment rates are similar to those in other African countries

21

but profit rates are 56 percentage points lower than in other African countries. They argue that,

while there many other constraints, to investment, high taxes, contributed to a greater extent to

this disparity.

Tindimwebwa (1999) stated that capturing the informal sector using the presumptive income tax

system into the tax bracket is inevitable considering its growth in the economy and the shift of

economic activities from the formal into the informal sector.

The problems and obstacles have to be carefully handled,” there is no doubt that hurdles must be

overcome before gains and profits are achieved. By contributing towards government revenue

the informal sector will truly be a partner in the economic development of Uganda”.

Collin, (2000) asserts that if a tax system makes it difficult for the entrepreneur to accumulate

and keep wealth he or she will not think it worthwhile to take the large down side risk of starting

or expanding a business irrespective of size. There is need for government to balance its revenue

requirements against the need to crush the establishment, development or growth of small

business enterprises. The government should not kill the goose that lays the golden eggs,

(PMSEDU, 1997).

However Sona (2002) put it, despite its streamed line requirements, presumptive income taxation

is not always effective….” Developing countries employ crude methods of estimating income

because they lack sufficiently qualified resources to analyze the profitability of various economic

activities leading to unfair and ineffective taxation of small businesses.

Conclusion

From the literature discussed it can be concluded that there is a relationship between the

presumptive income tax system and the profitability of the small business enterprises in Uganda.

However like any descriptive analyses, these relationships have been investigated in different

areas, different time periods and conditions.

22

CHAPTER THREE

3.0 Introduction

This chapter discuses the research methods and instruments used by the researcher when

carrying out the study. It provides a description of the research design, the sample description,

data collection methods and analysis procedures used by researcher.

3.1 Research design

A cross – sectional research design was used to generate data on profitability of small business

enterprises. This was supplemented with exploratory research design to determine the

relationship between presumptive income tax and profitability of small business enterprise. The

study was conducted on a few small scale businesses in Nakawa division.

3.2 Sampling design and procedure

3.2.1 Study population

The study population covered 50 small scale business in Nakawa division, including its suburbs

Kitintale, Mbuya, Ntinda, Nakawa market and Bugolobi market. Reponses were obtained from

those Small Business Enterprise paying presumptive income tax.

3.2.2 Sampling methods

In order to obtain representative and relevant population sample, judgment sampling was used to

select different types of small business enterprises to obtain the required data and information.

The researcher also used proportionate stratified sampling technique to ensure fair representation

of Small Business Enterprise. The division of Nakawa will be divided into strata inform of

suburbs

23

3.2.3 Sample size

A total of 50 respondents were selected and these constitute the sample size. The sample size

was selected from within and around Nakawa division particularly Nakawa market, Bugolobi

market, Kitintale and Ntinda.

3.3 Data collection

3.3.1 Source of data

Primary data: This was obtained from personal interviews and responses from questionnaires

issued to owners of SBES and where necessary observation was brought Secondary data: On

other hand included documents and journals obtained from school library, world bank, URA

records and online journals, articles and publication and newspapers.

3.3.2 Procedure

The procedure pertaining to the study included submission of research topic to the supervisor for

approval, writing of a research proposal and obtaining an introductory utter after he proposal

which allowed the researcher to go to the field and gather data. The study took two months

whereby the researcher requested Small Business Enterprise owner to fill in the distributed

questionnaires and in some instances, interviews will be used. The filled questionnaires therefore

were collected for presentation, interpretation, discussion and analysis of the findings.

3.4 Data collection methods and instruments

3.4.1 Questionnaires

These were used to collect data from different respondents. The questionnaires designed for sizes

owners had both open and closed ended questions. Open ended questions were used to enable

respondents give their opinion on the effect of taxation on their business. The questionnaire was

simply worded and relatively short to encourage response and compliance. The questionnaires

were chosen as a research instrument because it is easy to administer and scores relatively high

results.

24

3.4.2 Interviews

Personal interviews will be carried out in hand with the questionnaires to increase the response

rate. The interviewing method was used because of its flexibility to enable probing especially

where specific answers were needed and where some respondents were unable to read and write.

50 respondents were interviewed to understand more on the subject.

3.5 Data processing and analysis

Once the relevant data is got, it will be edited, sorted and summarized. The data will be

analyzed and tabulated into percentage and presented using tables. The researcher chose this

method of analysis because it is easy to use and make interpretation of findings easy.

3.6 Limitations of the study

There was inadequate time to allow the researcher to carry out nationwide study. The

research was limited to Nakawa division and worked within the limited time. However the

little time available was budgeted for.

Owners and managers of small business enterprises were reluctant to disclose some

information about the profitability regarding it confidential. Business owners were convinced

that the information given was purely for academic purposes.

There were inadequate resources to carry out a comprehensive study. Since the study

involved going to the field. However, the researcher managed to work within the developed

budget without compromising on the quality of the study.

25

CHAPTER FOUR

PRESENTATION, ANALYSIS AND INTERPRETATION OF FINDINGS

4.0 Introduction

This chapter presents the findings and interprets the findings of the study. The findings are

presented in relation with the research variable that is presumptive tax and profitability,

objectives of the study and research questions.

4.1 Characteristics of respondents

4.1.1 Gender

There was a need to know the sex respondents for purposes of gender balance and this was

shown in the table below.

Table 2: showing sex of respondents

SEX Frequency Percent Valid Percent Cumulative

Percent

Male 34 68.0 68.0 68.0

Female 14 32.0 32.0 100.0

Total 50 100.0 100.0

Source: Primary Data

The majority of the respondents were male representing 68% of the total respondents. However,

it was important to note that small businesses are not run by men alone since 32% of the

respondents were female.

.

26

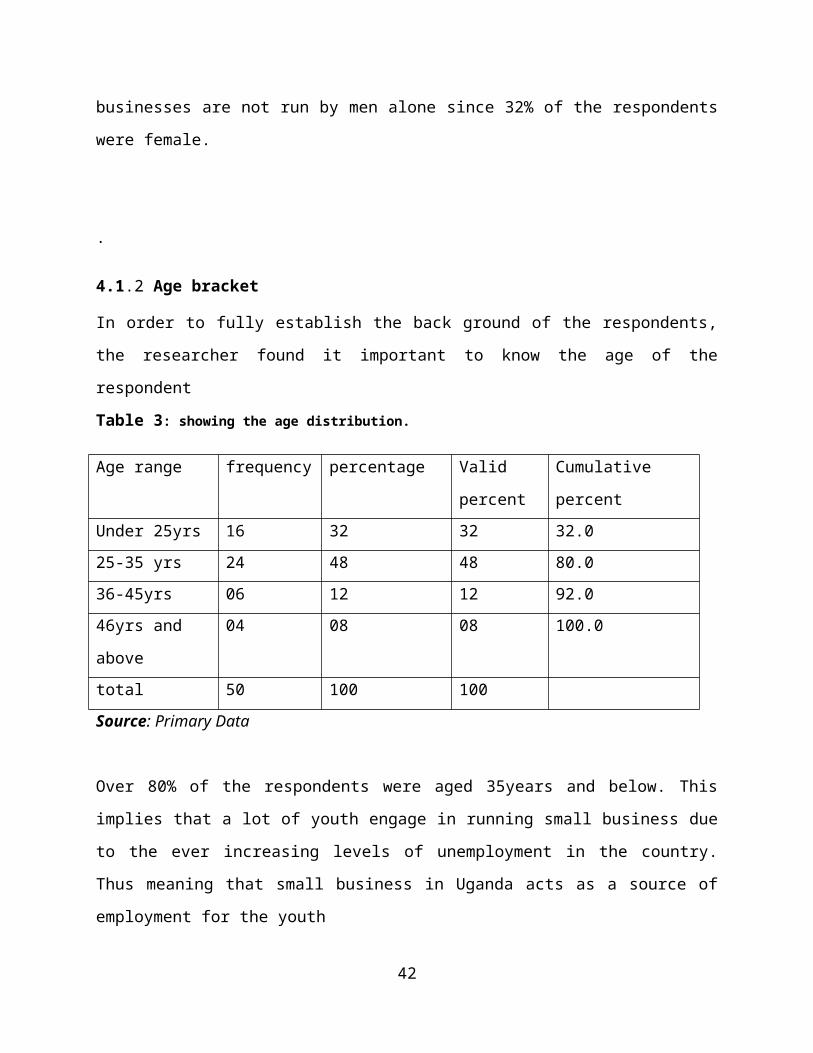

4.1.2 Age bracket

In order to fully establish the back ground of the respondents, the researcher found it important

to know the age of the respondent

Table 3: showing the age distribution.

Age range frequency percentage Valid

percent

Cumulative percent

Under 25yrs 16 32 32 32.0

25-35 yrs 24 48 48 80.0

36-45yrs 06 12 12 92.0

46yrs and above 04 08 08 100.0

total 50 100 100

Source: Primary Data

Over 80% of the respondents were aged 35years and below. This implies that a lot of youth

engage in running small business due to the ever increasing levels of unemployment in the

country. Thus meaning that small business in Uganda acts as a source of employment for the

youth

4.1.3 Education level

Table 4: showing the education level of the respondents.

Level of education Frequency Percent Valid Percent

Cumulative

Percent

Certificate 26 52.0 52.0 52.0

Diploma 16 32.0 32.0 84.0

Degree 8 16.0 16.0 100.0

Post graduate 0 0.0 0.0

Total 50 100.0 100.0

Source: Primary Data

27

The findings revealed that the majority of the respondents, 52% were certificate holders, 32%

were diploma holders, while 16% had bachelor’s degrees. This implies that in order to ascertain

back ground and authenticity of the information gathered, the researcher considered it imperative

to find out the education level of the respondents. The study revealed that most of the people

running small business were certificate holders and this is attributed to the low rate of earning

from these businesses.

4.1.4 Nature of the respondents business

The researcher found it important to know the nature of the business from where respondents

originated, as to whether they were Sole proprietorship, Retailers and Wholesalers.

Table 5: showing the nature of the respondents business.

Nature of the business Frequency Percent Valid Percent

Cumulative

Percent

Sole proprietorship 28 56.0 56.0 56.0

Retailer 14 28.0 28.0 84.0

Wholesaler 8 16.0 16.0 100.0

Total 50 100.0 100.0

Source: Primary Data

From the table above, 56% of the respondents were sole proprietors, 28% were retailers while

the remaining 16% of the respondents were wholesalers. This is attributed to the amount of

capital/ money required to start business in any of the above categories

4.1.5 Duration of your business

Table 6: showing duration of business

Duration of the

business Frequency Percent Valid Percent

Cumulative

Percent

Less than 1yr 12 24.0 24.0 24.0

1-3yrs 24 48.0 48.0 72.0

More than 3yrs 14 28.0 28.0 100.0

Total 50 100.0 100.0

Source: Primary Data

28

The findings revealed that the majority of the respondents, 48% of the business had survived for

the period between 1-3yrs, 28% for more than 3yrs while the remaining 24% of the had survived

for the period less than 1yr. This implies that very few small businesses enterprises survive for

the period more than 3years and this can the result of harsh working conditions such as high

taxes, stiff competition `and high taxes.

4.2 Presumptive income tax

4.2.1 Registration for presumptive tax

Table 7: showing whether the business is registered for presumptive tax

Response

Frequency Percent Valid Percent

Cumulative

Percent

Strongly agree 5 10.0 10.0 10.0

Agree 8 16.0 16.0 26.0

Not sure 4 8.0 8.0 34.0

Disagree 30 60.0 60.0 94.0

Strongly disagree 3 6.0 6.0 100.0

Total 50 100.0 100.0

Source: Primary Data

From the table above, 66% of the respondents had not registered for presumptive income tax,

26% of the respondent’s businesses had not registered while the remaining 8% were not sure of

if they are registered or not. This implies that there are gaps between the revenue collecting body

(URA) and business owners and thus more effort on educating tax payers is needed.

29

4.2.2 Awareness on tax paid

Table 8: showing whether the tax payers knew the type of taxes they are supposed to pay

Response

Frequency Percent Valid Percent

Cumulative

Percent

Strongly agree 4 8.0 8.0 8.0

Agree 10 20.0 20.0 28.0

Not sure 10 20.0 20.0 48.0

Disagree 20 40.0 40.0 88.0

Strongly disagree 6 12.0 12.0 100.0

Total 50 100.0 100.0

Source: Primary Data

From the table above, 26 respondents representing 52% did not know the type of tax they

supposed to pay, 14 respondents representing 28% knew the type of taxes they supposed to pay

while the remaining 20% of the respondents were not sure. This implies that the tax collecting

body has not done enough to educate SBES owners about the type of taxes they supposed to be

paying.

4.2. 3 paying right amount

Table 9: Showing whether Amount paid match with the amount earned

Response

Frequency Percent Valid Percent

Cumulative

Percent

Strongly agree 2 4.0 4.0 4.0

Agree 14 28.0 28.0 32.0

Not sure 25 50.0 50.0 82.0

Disagree 7 14.0 14.0 96.0

Strongly disagree 2 4.0 4.0 100.0

Total 50 100.0 100.0

Source: Primary Data

The study revealed that, 50% of the respondents were not sure whether they were paying the

right amount, 32% of the respondents claim that they are paying similar amount compared to

30

bigger businesses while 18% of the respondents that the amount is not similar to what bigger

businesses pay. This implies that the government favors bigger businesses by giving them tax

incentives such as tax holidays which does not favour SBES.

4.2.4 Business survival

Table 10: showing whether business closed after failing to pay taxes

Response

Frequency Percent Valid Percent

Cumulative

Percent

Strongly agree 25 50.0 50.0 50.0

Agree 16 32.0 32.0 82.0

Not sure 0 0.0 0.0 82.0

Disagree 5 10.0 10.0 92.0

Strongly disagree 4 8.0 8.0 100.0

Total 50 100.0 100.0

Source: Primary Data

According to the table above, 82% of the respondents agree that businesses have closed due to

failure to pay taxes, while 18% of the respondents do not believe that failure to pay taxes is not

the only cause of their business failure. This implies that taxes have a negative effect business

survival.

4.2.5 Computation of presumptive tax

Table 11: Showing whether tax payers know how presumptive income tax is computed.

Response Frequency Percent Valid Percent

Cumulative Percent

Strongly agree 0 0.0 0.0 0.0Agree 3 6.0 6.0 6.0Not sure 2 4.0 4.0 10.0Disagree 37 74.0 74.0 84.0Strongly disagree 8 16.0 16.0 100.0Total 50 100.0 100.0Source: Primary Data

31

From the table above,45 respondents(37+8) representing 90% do not how presumptive tax is

computed, 6% of the respondents knew how presumptive income tax is computed while the

remaining 4% were not sure of whether of they know or not. This implies that there is little

involvement of tax payers in the process of tax assessment which leads to doubt in any figures

raised.

4.3 Profitability

4.3.1 Level of Profits.

Table 12: showing whether businesses generate enough profits to carry out business operations.

Response

Frequency Percent Valid Percent

Cumulative

Percent

Strongly agree 3 6.0 6.0 6.0

Agree 12 24.0 24.0 30.0

Not sure 2 4.0 4.0 34.0

Disagree 32 64.0 64.0 98.0

Strongly disagree 1 2.0 2.0 100.0

Total 50 100.0 100.0

Source: Primary Data

From the table above 33 respondents representing 66% disagreed, 15 respondents representing

30% agreed while the remaining 2% of the respondents were not sure whether they generate

enough profits to carry out their business operations. This implies that most SBES did not

generate enough profits to cater for their business operations

32

4.3.2 Cash Balances

Table 13: showing whether the business is left with some cash to acquire more stock

Response

Frequency Percent Valid Percent

Cumulative

Percent

Strongly agree 3 6.0 6.0 6.0

Agree 20 40.0 4.0 46.0

Not sure 4 8.0 8.0 54.0

Disagree 20 40.0 40.0 94.0

Strongly disagree 3 6.0 6.0 100.0

Total 50 100.0 100.0

Source: Primary Data

According to the table above, 23 respondents representing 46% agreed that after paying

presumptive tax the businesses are left with cash to acquire more stock, 23 respondents

representing 46% disagreed while the remaining 8% were not sure whether their businesses are

left with some cash to acquire more stock. This is attributed to poor financial practices used by

owners of SBES for example lack of proper book keeping practices.

4.3.3 Effect on profits

Table 14: showing whether presumptive tax affect profits of SBES

Response

Frequency Percent Valid Percent

Cumulative

Percent

Strongly agree 1 2.0 2.0 2.0

Agree 40 80.0 80.0 82.0

Not sure 0 0.0 0.0 82.0

Disagree 8 16.0 16.0 98.0

Strongly disagree 1 2.0 2.0 100.0

Total 50 100.0 100.0

Source: Primary Data

From the table above, 82% of the respondents agreed that presumptive affects profits earned by

SBES while 18% of the respondents disagreed. This implies that presumptive income tax affects

33