Embed Size (px)

DESCRIPTION

Today’s Business Context. Nic Wilmot. The Nordic Association of Marine Insurers. 1. Zooming in – where in the galaxy will we be exploring. Business context is a very large galaxy We cannot look at all of it so we need to know where we are and We need perspective. A question of perspective. - PowerPoint PPT Presentation

Citation preview

Today’s Business ContextNic Wilmot

The Nordic Association of Marine Insurers1

Zooming in – where in the galaxy will we be exploring

Business context is a very large galaxy

We cannot look at all of it so we need to know where we are and

We need perspective

2

3

Cefor Hansteens gt 2, Oslo

A question of perspective

Business context is a very broad subject:

We have looked at:• Global trade history and present• History of marine insurance

Later we will look at:• Marine insurance markets• Legal and regulatory framework

Business context could include much more e.g.:• Shipping markets not forgetting the cruise industry• Transport and logistics – the basic value chain • Ship technical - Ship management• Flag state and ship registration• Ship finance, International Law of the Sea, etc. etc.

4

Our perspective is insurance and as we have already seen we cannot talk about insurance without talking about risk

5

6

Contents

• The concept of risk• Risk in the shipping industry• Rocknes – a major casualty• Insurance as a risk management tool

Risk is the potential for:loss or failure to meet business objectives

as a consequence of internal or external events

Something, in fact lots of things, might go wrong

Why the concept of risk is so fundamental

• Where there is life there is risk• The future is uncertain – the best laid plans ….• The defining characteristic of a capitalist economy is the

way it handles risk • Capital markets should more correctly be called risk

markets• The most important strategic decision for any business is

how it should manage risk in its broadest sense

Risk distribution

UNACCEPTABLE

TRANSFER

RETAIN & CONTROL

ACCEPTABLE

PROBABILITY/FREQUENCY

SE

VE

RIT

Y

Risk – Threat and Opportunity

Equity, loan and insurance capital

have different functions

accept different risks

expect different rewards

Key to your successUnderstanding and managing your chosen areas of risk

Risk and reward

are correlated

Content

• The concept of risk• Risk in the shipping industry• Rocknes – a major casualty• Insurance as a risk management tool

Shipowner’s risks

Risk management

Strategicrisk

Marketrisk

Creditrisk

Financialrisk

Operationalrisk

Legalrisk

Organisationalrisk

Eventrisks

Source: Drewry Shipping Consultants Ltd

Shipowners’ risksRisk Type Examples

Source: Drewry Shipping Consultants Ltd

Strategic risk

Market risk

Credit risk

Financial risk

Operational risk

Legal risk

Organisational risk

Sovereign risk

Loss of key partnersCompany reputation riskLoss of competitivenessUninsurable/unhedgeable risks

Freight marketLiquidity risk, market depth, basis risk

Clearing

Income stream/Cash Flow riskAccounting- related risksCapital costs risks

Transport chain and customer issuesShip-focused operational areas of riskInsurance

IMO and ”Global” issuesDeveloping issues in IMOOther regulatory issues

PersonnelSystems risk

War and terrorism riskPolitical riskBusiness culture riskFlag states

Charterers, customers, suppliers

Derivatives, S&P

Norwegian Futures and Option Clearing House (NOS)

Charterers, customers

Currency risk, interest ratesMark-to-market, tonnage tax regimesOrderbook, loans, mortgages

Manning, criminalisation, R&M, victuallingH&M, P&I, US Oil Poll., FD&D, War

SOLAS (ISM and ISPS), STCW, MarpolBallast water, demolition, PSSAs, arrest, flag statesAnti-money laundering, FSA rules, corruption

Loss of key personnel, manningIT

Trade, human trafficking, drug issues, piracy

BACK-UP

Spot rate risk is significant for a shipping company…

Source: Platou

VLCC, high last 12 m,

75 000

VLCC, low last 12 m, 25 000

Difference:

50 000

…and huge compared to claims risk:Payback time for a claim if spot rate is at median level

Shipowner with 1 ship 100 ships

Median claim: 32 000 USD 15 hours 10 min.

90 % Percentile: 200 000 USD 4 days 1 hour

99 % Percentile: 2 000 000 USD 40 days 10 hours

99.9 % Percentile: 11 000 000 USD 7 months 2 day

Why then should shipowners choose to transfer casualty risks?

Because:• they don’t want to compound the market risks they

have accepted - market and casualty risks can cumulate

• casualty risks compromise much more than just damage to their vessel

• vessels in a large fleet may have different ownership and financing arrangements

Contents

• The concept of risk• Risk in the shipping industry• Rocknes – a major casualty• Insurance as a risk management tool

Even the best can be hit by the worst

Need for effective claimshandling to manage and mitigate losses

The moments of a maritime casualty

Maritimecasualty

Death and personal injury

Loss or damage to vessel

Loss of income

Environmental damage

Damage to third party property

General average and salvage

Wreck removal

Relationship toauthorities

Media handling

Reputation

Care of next of kinand survivors

Emergencyresponse

Normalisation ofsituation

Illustrative example - Rocknes

•Capsized off Vatlestraumen

after hitting a submerged rock

•18 people lost their lives

•Massive pollution

•Vessel and special purpose

equipment severely damaged

•Cargo lost

-Losses in total excess of USD

170 million

The first 45 minutes

16:30 Rocknes capsizes in Vatlestraumen.

17:00 Jebsen in contact with H&M claims leader,

Norwegian Hull Club and P&I Club, Gard.

17:00 onwards emergency procedures activated

by all parties concerned.

Red alert!!

17:15 Red alert!! – Gard Mobilisation

17:55 12 staff in contingency room. In operation.

18:45 Liaison from Gard at Jebsen’s office.

18:50 Liaison from Gard at Bergen Police Office.

19:30 3 staff despatched to Bergen by chartered airplane.

Arrive Jebsen’s office at 23:30.

Contingency room manned at all times next 48 hours

Corresponding procedures activated at Norwegian Hull

Club

The next 2 hours

Priorities

Pri 1 Human

Pri 2 Pollution

Pri 3 Property

Liaison our member and handle media

When the alarm bell sounds…The human element

3 Dutch, 8 Filipino and 1 Norwegian survived

3 crew members immediately found dead

15 crew members missing It is estimated that on 19th

January, 600 persons were involved in the rescue operation

Situation on 19th January

Emotional

Practical

Strategic

Survivors Relatives Missing/Dead

When the alarm bell sounds …

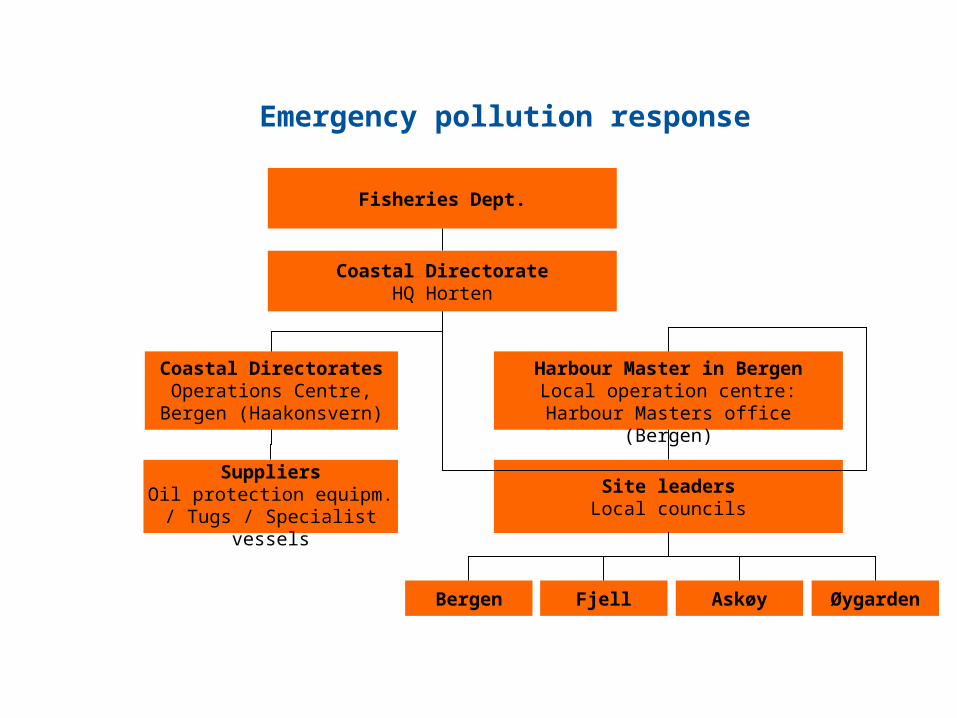

ROCKNES - Pollution response

Coastal DirectoratesOperations Centre,

Bergen (Haakonsvern)

SuppliersOil protection equipm. / Tugs / Specialist vessels

Bergen Fjell Askøy Øygarden

Site leadersLocal councils

Harbour Master in BergenLocal operation centre:

Harbour Masters office (Bergen)

Coastal DirectorateHQ Horten

Fisheries Dept.

Emergency pollution response

Division of labour between public and private sectors

Shipping industry provides• Finance through insurance and fund conventions• Organisation of own responsibilities, salvage agreements• On site participation • Command structures for its sphere

Public sector provides• Funding of resources and equipment• Rescue and pollution clean up services• Command structures

Summary losses

• Cost of salvage - H&M plus Scopic to P&I• Cost of repair - H&M• Loss of income – LOH but only for time lost up to

completion of repairs• Liabilities – P&I

• People

• Pollution

• Other• Media handling – mostly uninsured• Other administrative and organisational costs – mostly

uninsured• General disruption of business and Loss of reputation -

uninsured

The Nordic Association of Marine Insurers 54

Lessons learned on media

• Media policy in place

• Day to day handling of media

• Distribution of reliable information to involved parties

• The need for competence to distribute electronic

information and web publishing

• Enough resources available when needed

• Organization of own resources (endurance)

Conclusions: Rocknes illustrates increasing complexity in the shipping industry and its context

• Technology

• Business systems

• Legislative framework

• Social context

The moments of a maritime casualty

Maritimecasualty

Death and personal injury

Loss or damage to vessel

Loss of income

Environmental damage

Damage to third party property

General average and salvage

Wreck removal

Relationship toauthorities

Media handling

Reputation

Care of next of kinand survivors

Emergencyresponse

Normalisation ofsituation

How is risk distributed within the maritime transport industry

• By general maritime law – liability and funding conventions ref, session on Maritime Law

AND

• Through the contractual network

• Examples – freight risk, risk of damage to cargo, risk of delay, etc.

Examples: ”freight risk”

• Risk of incurring costs of performance without achieving the planned result – safe delivery of cargo at destination.

• Can be placed on ship owner – freight payable on delivery - or on the cargo owner – freight payable in advance

Examples: Risk of damage to cargo

• Risk of damage to cargo during transport• Can be placed entirely on carrier, entirely on cargo

owner or apportioned e.g by reference to whether carrier is at fault

• Apportionment in various forms has been the norm • Leads ultimately to settlement between two sets of

insurers and provides a living for a large number of lawyers

Examples: Ship owner and time charterer - delay due to unforseen events

• Each party carries risk for events within their control or within their ”sphere of choice”

• Choice of port, cargo handler etc within charterers’ control or sphere

• Crew and condition of the vessel within Owners sphere

• Ref off-hire clauses

Event and operational risks – ship owner’s options

Retain and manage by: Transfer by:

Contract:

Allocation of risk between contracting parties, e.g. ‘freight’ risk

Insurance:

Assets

Income

Liabilities

Quality systems

Maintenance budget

Loss Prevention activities

Summing up – our platform for going forward

• Managing risk in its broadest sense is the central task of any business enterprise

• The consequences of event risks are varied and can be life threatening for a company – ref Rocknes

• Shipping and the risks associated with it are becoming increasingly complex

• Risk is distributed through legislation and the contractual network

• Ship owner can retain and control or transfer risk• We must now understand how insurance functions as a

practical risk management tool

Contents

• The concept of risk• Risk in the shipping industry• Rocknes – a major casualty• Distribution of risk in the shipping

industry• Marine insurance as a risk

management tool

Understanding insurance – the little old lady of Monte Carlo

• The difference between a bet and a counter bet

• What would fall heavily on one falls lightly on the many

• The law of large numbers – making the unpredictable predictable

Assured must have an insurable interest

• Assured must be exposed to a possibility of economic loss

• Economic loss must be capable of being quantified – at least in principle

Insurance is a risk management tool

• Only works in relation to certain types of risk• Insurer must be able to spread the risk by building a

portfolio of similar risks but at same time control accumulation

• Contrast casualty risks with market risks, ref previous discussion

• Rationale for having war risks as a separate market

Summary – marine insurance markets today

• Marine insurance is a small part of the insurance industry and insurance is a small part of the global financial (risk) industry

• Large risk carrying capacity established in a global marine insurance market with geographical and product focused market segments

• Major division between capital structures that support liability/ P&I and non-marine insurers

• Sophisticated reinsurance arrangments including unlimited liability for most P&I risks through IG system

How risk transfer by insurance is organised – the mechanics

• Each party takes out separate insurance for their own account – leads to final settlement between insurers.

• Principal assured, project leader or main contractor takes out single policy on behalf of some or all participants.

Examples; Traditional shipping

• Shipowner, time charterer and cargo owner insure their interests separately

• But mortgagee and ship manager are co-assured under Owners’ policies

• NB diferent consequences of co-insurance

Examples: Offshore industry and knock for knock

• Underlying contract distributes risk on knock for knock principle – each party retains risk for own property, personnel and liability to third parties

• Each party is obliged to insure own risks• Insurance arrangements reflect the underlying allocation

of risk by allowing each party to be co-assured under the others insurance policy

Shipowner

Role of marine insurers - Value proposition capacity only or something more?

• Loss prevention• Technical guidance•

• Claims handling• Emergency response•

Provide large and stable risk carrying capacity to the shipping industry

Develop innovative solutions to solve important risk management and mitigation needs

Recognise quality operations and price accordingly

Develop and capitalize on the platformCreate value for owners

? ??

Examples: Shipping companies become integrated supply chain participants and the network complexity increases …

Plant

Trucker

Stevedore Stevedore

Shipping Line Trucker

Dealer

Shipping companies take control of door-to-door logistics chains

Strategic alliances with ports and inland carriage providers

Marine insurance in a form that we can recognise was well established by the early 19th century

• Both Lloyds, commercial companies and mutual associations active

• De Vaux v Salvador 1836 – collision liability not covered by standard hull policy

• 3/4ths RDC clause introduced to hull policies• Merchant Shipping Act 1854• Creation of first P&I club to cover 1/4th collision and

passenger liabilities

Development of maritime liabilities

Media – criminalisation of seafarers – state authorities complexity

Liability becomes an issue

1836 De Vaux v Salvador

1854 British Merchant Shipping Act

Creation of the first P&I clubs to cover collision and personal injury liability

Expansion of liabilities to include cargo etc.

Pollution comes into focus

1967 Torrey Canyon 1978 Amoco Cadiz 1989 Exxon Valdez 1999 Erika 2002 Prestige

The Athens Convention

Increased compensation limit

Coverage

Asset insurances

Income insurances

Liability insurances

• Protection and Indemnity (P&I): Protects the owner against third party claims

• Freight, Defence & Demurrage (FD&D)

• Hull and Machinery (H&M): Protect the value of property

• Increased value (IV)• War Risks: Covers H&M and P&I

Risks caused by war risks

• Loss of hire (LoH): Protects the owner against loss of income

• Strike

Marine

P&I

Marine insurance industry segments- for shipowners

Marine risks War risks

Assets H&M / IV Segment

War risk segment

Income Business Interruption Segment

Liabilities P&I industry segment

Additional liabilities

Non-mutual marine liability segment

Seafarers General and Life insurance industry

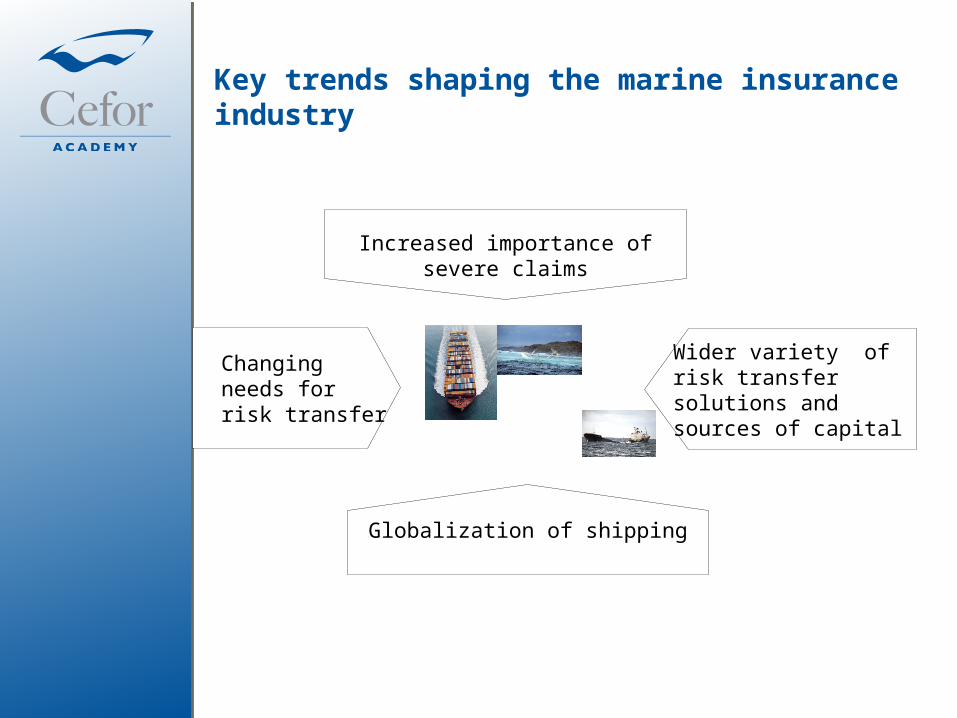

FUTURE TRENDS

Looking aheadThe risk picture is changing - new technology and increased values

Wider variety of risk transfer solutions and sources of capital

Changing needs for risk transfer

Globalization of shipping

Increased importance ofsevere claims

Key trends shaping the marine insurance industry

We shall not cease from exploration. And the end of all our exploring will be to arrive where we started and know the place for the first time. T.S. Eliot

Business ContextNic Wilmot

The Nordic Association of Marine Insurers82