Embed Size (px)

Citation preview

No. 61] Income and Business Tax 1

BELIZE:

STATUTORY INSTRUMENT

No. 61 of 2013____________

ORDER made by the Minister of Finance in exercise ofthe powers conferred upon him by section 95A of theIncome and Business Tax Act, Chapter 55 of Laws ofBelize, Revised Edition 2000-2003, as amended by theIncome and Business Tax (Amendment) Act, 2009(No. 6 of 2009), and all other powers thereunto himenabling.

(Gazetted 15th June, 2013.)____________

WHEREAS, section 95A(1) of the Income and BusinessTax Act, Chapter 55 of the Laws of Belize, Revised Edition2000-2003, as amended by the Income and Business Tax(Amendment) Act, 2009 (No. 6 of 2009) [hereinafter referredto as “the Act”] provides that the Minister [of Finance] mayenter into Tax Information Exchange Agreements with thegovernment of any country or territory outside Belize witha view to applying international standards on transparencyand effective exchange of information relating to tax matters;

AND WHEREAS, subsection (2) of section 95A of theAct further provides that every such agreement as aforesaidshall be incorporated in an Order which shall be publishedin the Gazette as a statutory instrument, and upon suchpublication, the Order shall have the force of law in Belizenotwithstanding anything in the Act or any other enactment,and the restrictions contained in section 4 of the Act on thedisclosure of information shall not apply with respect to arequest for information pursuant to such agreement;

AND WHEREAS, the Minister has entered into a TaxInformation Exchange Agreement with the Government ofthe Republic of Poland;

NOW, THEREFORE, IT IS HEREBY ordered asfollows:-

1. This Order may be cited as the

TAX INFORMATION EXCHANGE AGREEMENT(BELIZE/POLAND) ORDER, 2013.

2. In this Order, unless the context otherwise requires —

“Agreement” means the Agreement between Belize andthe Republic of Poland for the Exchange of Informationrelating to Tax Matters, signed on the 16th May of 2013, asset out in the Schedule hereto;

“authorised representative” of the Minister means theFinancial Secretary;

“competent authority” means, in the case of Belize, theMinister or the Financial Secretary; and in the case ofPoland, the Minister of Finance or his authorisedrepresentative;

“days” means calendar days;

“IFS Practitioner” means any person or entity licensed bythe International Financial Services Commission to carry onthe business of ‘international financial services’ as that termis defined in section 2 of the International Financial ServicesCommission Act;

Short title.

Interpretation.

Schedule.

CAP. 272.

2 Income and Business Tax [No. 61

“financial institution” means a bank or financial institutionas defined in the Domestic Banks and Financial InstitutionsAct or the International Banking Act, and includes brokeragefirms and insurance companies;

“Minister” means the Minister of Finance;

“reporting entity” shall have the meaning assigned to it insection 2 of the Money Laundering and Terrorism (Prevention)Act, 2008;

“supervisory authority” shall have the meaning assigned to itin section 2 of the Money Laundering and Terrorism (Prevention)Act, 2008.

3. For the purpose of complying with a request forinformation pursuant to the Agreement, the FinancialSecretary shall have power to obtain and provide all suchinformation, including (without limitation):

(a) information held by banks, other financialinstitutions, and any person acting in any agencyor fiduciary capacity including nominees andtrustees;

(b) information regarding the ownership ofcompanies, partnerships, trusts, foundationsand international limited liability companies,including ownership information on all suchpersons in an ownership chain; in the case oftrusts, information on settlors, trustees,beneficiaries and protectors; in the case offoundations, information on founders, membersof the foundation council and beneficiaries;and in the case of limited liability companies,information on its members and managers.

CAP. 267.

No. 18/2008.

No. 18/2008

Power of theFinancialSecretary toobtain andprovideinformation.

Act No. 11/2012

No. 61] Income and Business Tax 3

4. (1) Where the Financial Secretary is satisfied that arequest for information from the competent authority of theRepublic of Poland falls within the terms of the Agreement,he may under his hand require any bank, financial institution,reporting entity, supervisory authority, IFS Practitioner,Trust Agent, Registered Agent of Foundations, RegisteredAgent of International Limited Liability Companies, Registrarof (local) Companies, Registrar of International BusinessCompanies, Registrars of domestic and International Trusts,Registrar of Foundations, Registrar of International LimitedLiability Companies, Registrar of Limited LiabilityPartnerships, Supervisor of (domestic) Insurance, Supervisorof International Insurance, taxing authority, public statutorycorporations, public officers, or any other person or entitywhosoever, who the Financial Secretary believes may haverelevant information, to furnish such information or producesuch documents as may be required to comply with therequest for information.

(2) Every person who is required by the FinancialSecretary to provide information or produce documentspursuant to this Order shall provide the requisite informationor documents as soon as possible but no later than thirty (30)days from the date of the request for information.

(3) Every person who refuses or fails to supply suchinformation or documents to the Financial Secretary withinthe time specified, or wilfully supplies false or misleadinginformation or documents, shall be guilty of an offence andshall be liable on summary conviction to a fine not exceedingfive thousand dollars or to imprisonment for a term notexceeding two years, or to both such fine and term ofimprisonment.

(4) No restrictions on the disclosure of informationcontained in any other law shall apply to a request forinformation pursuant to the Agreement and no suit forbreach of confidentiality or other such action shall lie against

Duty to supplyinformation tothe FinancialSecretary.

4 Income and Business Tax [No. 61

any person who discloses information, produces documentsor renders other assistance in compliance with a request forinformation under this Order.

MADE by the Minister of Finance this 31st day of May,2013.

(DEAN O. BARROW)Minister of Finance

No. 61] Income and Business Tax 5

6 Income and Business Tax [No. 61

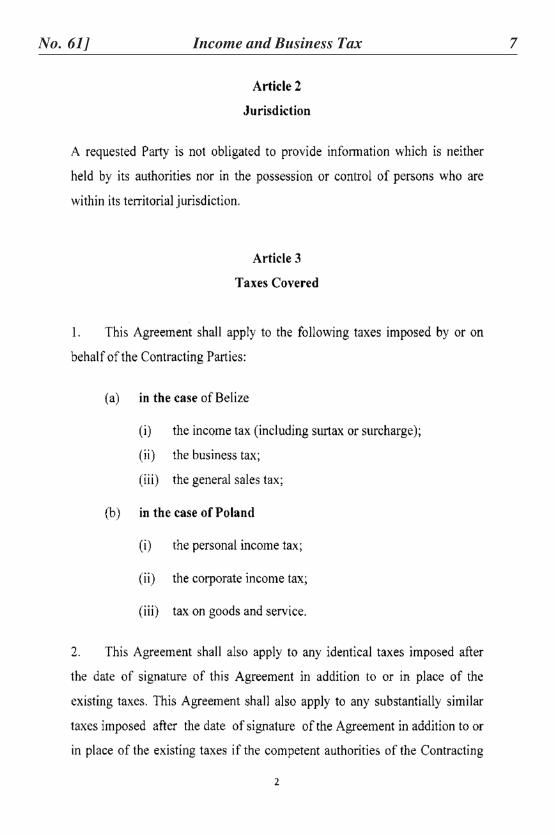

No. 61] Income and Business Tax 7

8 Income and Business Tax [No. 61

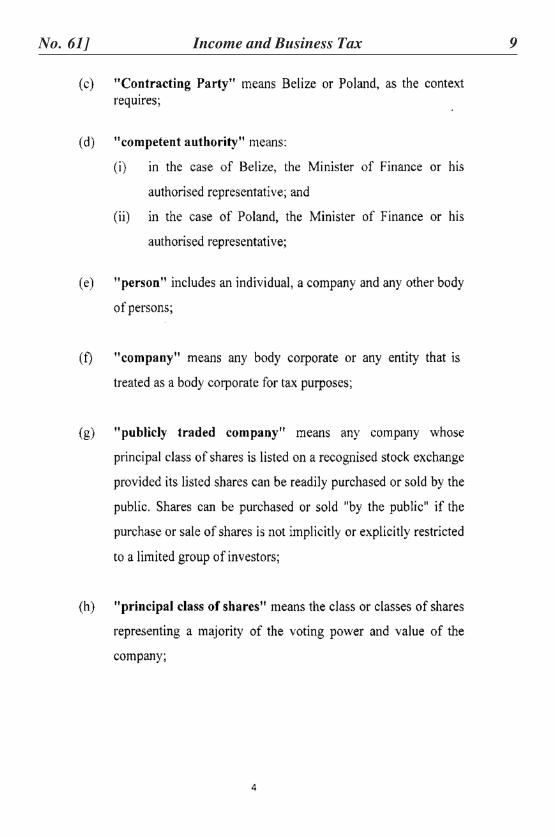

No. 61] Income and Business Tax 9

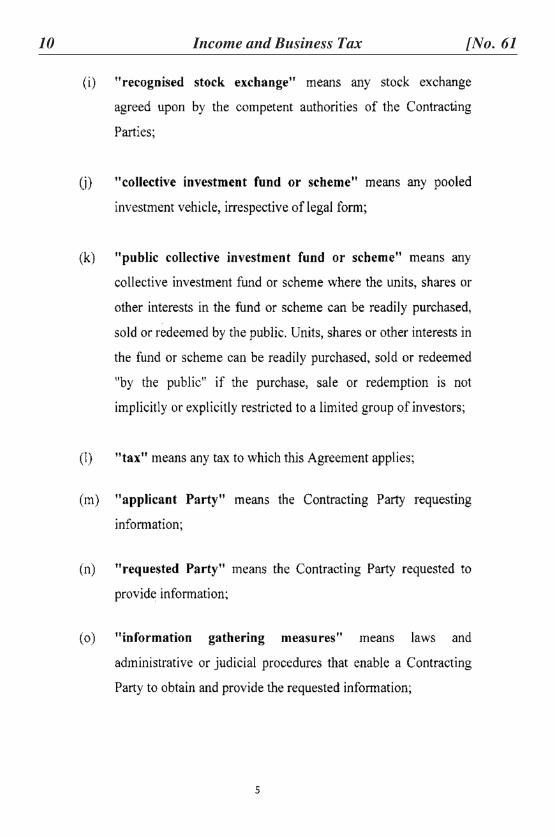

10 Income and Business Tax [No. 61

No. 61] Income and Business Tax 11

12 Income and Business Tax [No. 61

No. 61] Income and Business Tax 13

14 Income and Business Tax [No. 61

No. 61] Income and Business Tax 15

16 Income and Business Tax [No. 61

No. 61] Income and Business Tax 17

18 Income and Business Tax [No. 61

No. 61] Income and Business Tax 19

20 Income and Business Tax [No. 61

Printed in Belize by the Government Printer

No. 61] Income and Business Tax 21