Embed Size (px)

Citation preview

Dr. Markus Holz ThyssenKrupp Titanium

The Global Titanium Market and the European Challenge Dr. Holz will provide an overview of the European Titanium industry as a vibrant global marketplace. His focus on industrial applications will address those major market segments where the business (plates and tube), though erratic, is mostly concentrated – power generation (strong need for construction/revamping of energy plants), PHE (booming market) and desalination (fast‐growing demand worldwide). Emphasis will be placed on the number of projects that are supplied by European fabricators. The presentation will also address military and civil aerospace ‐ where Europe is well represented by Airbus with the A400M and A380 respectively ‐ which appear a most challenging business (continuing to boom)as well as a very sensitive barometer of the world economic development that gages the excellence the titanium industry is successfully pursuing

1Dr. Markus Holz – ITA 2008

Th Gl b l Tit i M k tThe Global Titanium Market and the European Challengeand the European Challenge

Dr. Markus Holz

nKru

pp

Dr. Markus HolzThyssenKrupp Titanium

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

2Dr. Markus Holz – ITA 2008

The Global Titanium Market and the European Challengeand the European Challenge

Market Overview

Challenging Market Environment

Outlook and Summary

nKru

ppTh

ysse

n

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

3Dr. Markus Holz – ITA 2008

European Civil AerospaceTh tThreat:Declining passenger numbers caused by:

• increased taxes and fees

• record-high fuel cost

• GDP reduction in Europe

• weakening global economy

200

180

160

Relative value development of the oil price compared to aerospace

High Fuel cost grounds airplanes

weakening global economy

• noise and Co2 emissions

Production problems

Ai b A 380 18 th d lBrentöl (spot price)

DJ World Aerospace Index

120

140

100

• Airbus A 380 18 months delay

• Boeing 787 20 months delay

Possible consequences:

June 2006 June 2008

80

60

nKru

pp

Possible consequences:

• Airline market will be re-shaped

• Airlines could cancel or postpone orders for new aircrafts

N i i f t ti

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

• Non exercising of current options

4Dr. Markus Holz – ITA 2008

Civil Aviation Worldwide

10,000

Total per passenger-kilometer (billions)

Prognosis before

7,500

Declining passenger numbersALITALIA - 25%

OLYMPIA AIRLINES - 14%

gthe fuel price shock

Possible new scenario

5,000

IBERIA - 10%

2,500

nKru

pp

Source: Boeing, AEA, IATA

0 1970 1980 1990 2000 2010 2020

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

Source: THE AIRLINE MONITOR

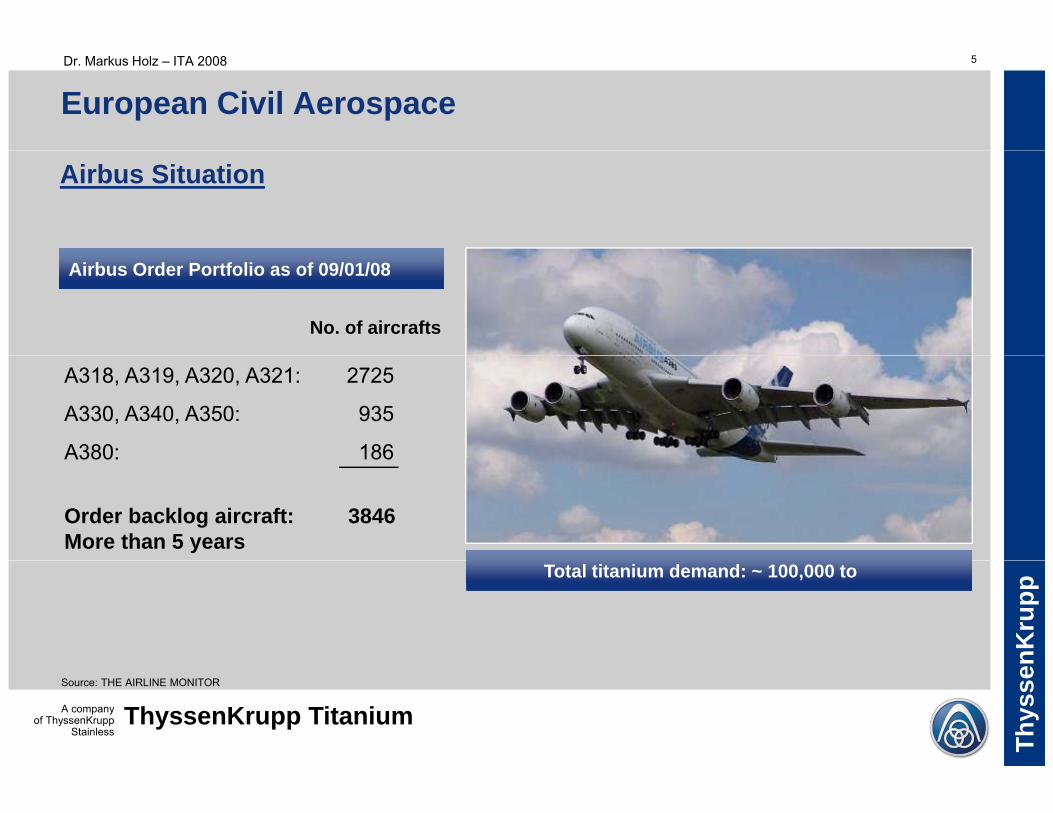

5Dr. Markus Holz – ITA 2008

European Civil Aerospace

Airbus Situation

No. of aircrafts

Airbus Order Portfolio as of 09/01/08

A318, A319, A320, A321: 2725

A330, A340, A350: 935

A380: 186A380: 186

Order backlog aircraft: 3846More than 5 years

nKru

pp

Total titanium demand: ~ 100,000 to

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

Source: THE AIRLINE MONITOR

6Dr. Markus Holz – ITA 2008

Airbus Titanium demand according to projected airplane deliveries 2008 to 2020 (by weight / mill products)

30000

deliveries 2008 to 2020 (by weight / mill products)

It is assumed that there will be a new Airbus single aisle family beginning in

*tons

25000

30000 g y g g2018.

This has a significant impact on the titanium demand.

15000

20000

252

25128 10 11 12 13

18 20 21 23

25

10000

nKru

pp

200

200

2200

8200

0200

1400

2000

3700

8200

0500

1300

3800

200

0

5000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020*

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020Source: THE AIRLINE MONITOR/own research

7Dr. Markus Holz – ITA 2008

Lower Titanium Consumption by AIRCRAFT Build-rate reduction

Production Planning Boeing B 787 Production Planning Airbus A 380

Short Term Difficulty B 787 and A 380 delayed – 18000 MT more material in cycle

60

706070

Production Planning Boeing B 787 Production Planning Airbus A 380

30

40

50

304050

0

1020

2007 2008 2009 2010 20110

1020

2007 2008 2009 2010 2011

nKru

pp

00 008 009 0 0 0

Planning 2006Pl i 2008

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

Planning 2008Source: Boeing, Airbus, THE AIRLINE MONITOR

8Dr. Markus Holz – ITA 2008

Estimated Lower Titanium Consumption by AIRCRAFT Build-rate reduction (A380 + B787)Build-rate reduction (A380 + B787)

Titanium Demand Actual vs. Plan

Assumption of TKL-TI

[MT/Y]Ti demand planTi demand actual▲

■22.240

25.000

▲

11.7449.40815.000

20.000

Demand vs. Actual supply

▲2.044

146

1.168

0

5.000

10.000 18.900 tons Ti semis

nKru

pp

14602007 2008 2009

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

9Dr. Markus Holz – ITA 2008

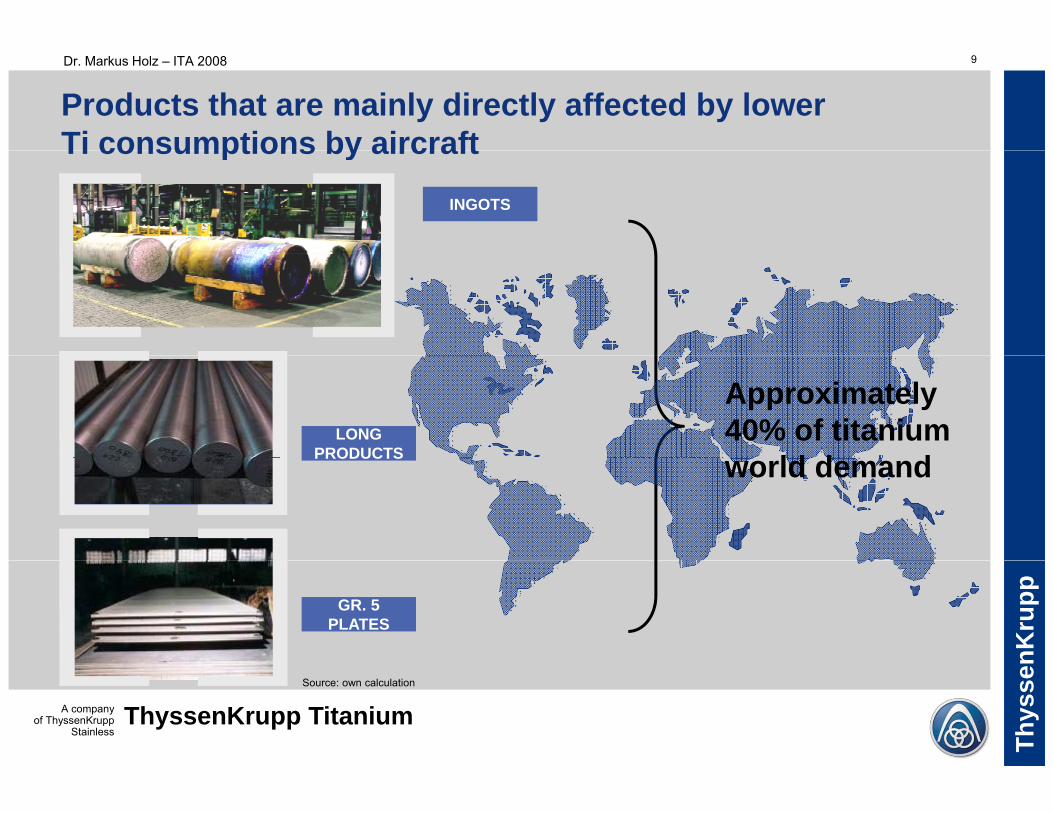

Products that are mainly directly affected by lower Ti consumptions by aircraftTi consumptions by aircraft

INGOTS

LONG PRODUCTS

Approximately 40% of titanium

ld d dPRODUCTS world demand

nKru

ppGR. 5 PLATES

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

Source: own calculation

10Dr. Markus Holz – ITA 2008

Industrial market still demanding

Stable growth Tube & Shell Heat Exchangers 2008 = 8.800 t 2015 = 10.400 t

Rapid growth Plate Heat Exchangers 2008 = 6.100 t 2015 = 10.400 t

Stable growth Medical 2008 = 2.200 t 2015 = 3.000 t

Rapid growth LNG Trade expected to expand Ti demand 250 t/plant4-fold till 2030 Ti demand 20 t/LNG carrierorder backlog LNG carrier: 140

nKru

pp

Rapid growth Nuclear Power Plants Ti demand 62 NPP in planning 2010 – 2012 = 4.000 t/year

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

p g ySource: own market research, IEA

11Dr. Markus Holz – ITA 2008

Titanium demand for liquified natural gas LNG (1)

Demand for transportation of LNG is increasing rapidly.

World gas consumption in 2007

= 2850 billion m³

Local consumption: 84 %

Transportation by pipeline: 12 %Transportation by pipeline: 12 %

Transportation by LNG tanker: 4 %

nKru

ppGas transportation <= 3200 km = pipeline

Gas transportation >= 3200 – 8000 km = LNG tanker

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

Source: Siemens, High Performance Tube

12Dr. Markus Holz – ITA 2008

Titanium demand for liquified natural gas LNG (2)

500

600

700

00 )

LNG trade is expected to increase 4 times

100

200

300

400

2001 2010 2020 2030

P ro duct io nP ipeline tradeLN G trade

Inde

x ( 2

001

= 10

2001 2010 2020 2030

World gas consumption 2007 = 2850 billion m³

2030 = 4275 billion m³

LNG in 2007 = 4 %

LNG in 2030 = 16 %2030 = 4275 billion m LNG in 2030 = 16 %

500600700800900

capa

city

Cost reduction of LNG procedure Titanium demand for LNG

LNG plant: 250 to

nKru

pp

0100200300400

1995 2002 2010 2030

$/to

n LNG plant: 250 to

LNG tanker: 20 to

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

Source: Siemens, High Performance Tube

13Dr. Markus Holz – ITA 2008

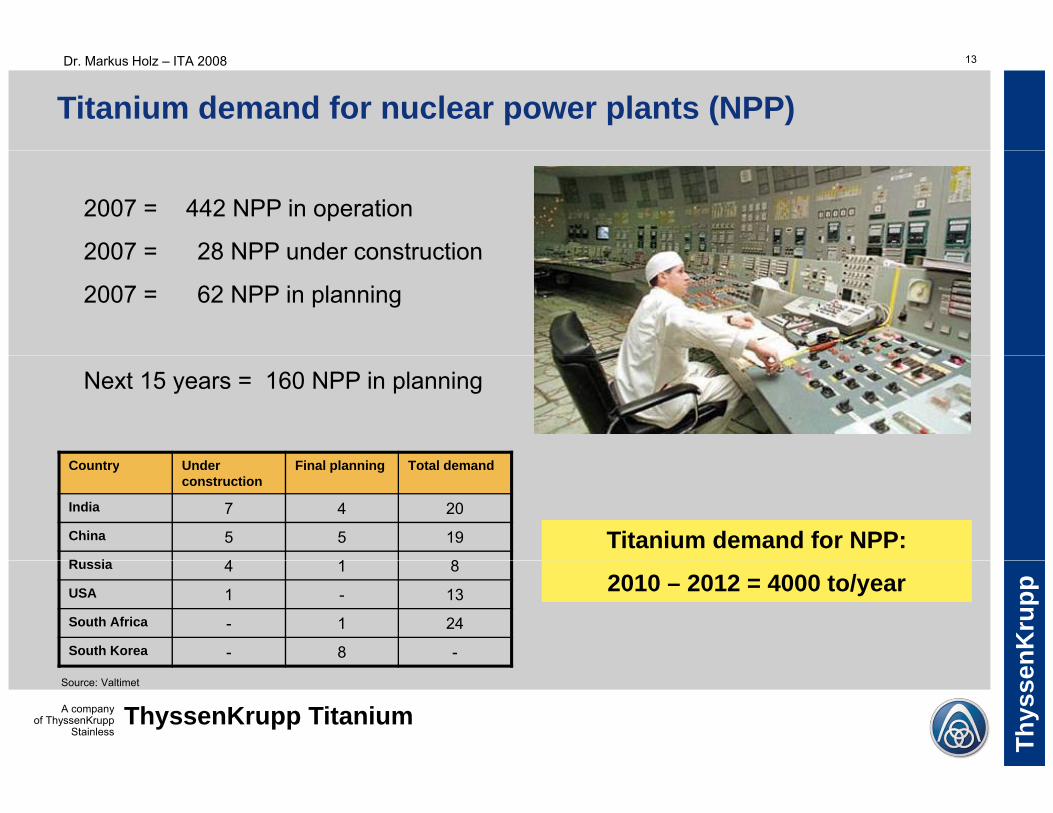

Titanium demand for nuclear power plants (NPP)

2007 = 442 NPP in operation

2007 = 28 NPP under construction2007 = 28 NPP under construction

2007 = 62 NPP in planning

Next 15 years = 160 NPP in planning

Country Under construction

Final planning Total demand

India 7 4 20China 5 5 19R i 4 1 8

Titanium demand for NPP:

nKru

pp

Russia 4 1 8USA 1 - 13South Africa - 1 24South Korea - 8 -

2010 – 2012 = 4000 to/year

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

Source: Valtimet

14Dr. Markus Holz – ITA 2008

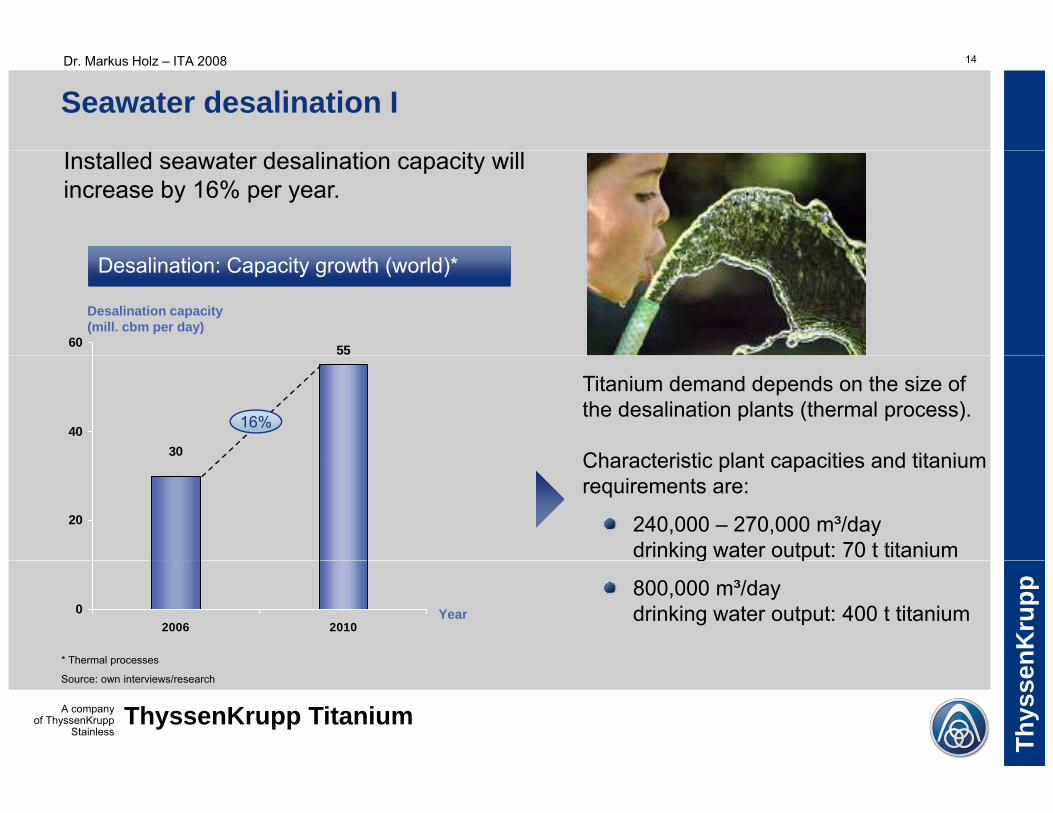

Seawater desalination I

Installed seawater desalination capacity will increase by 16% per year.

5560

Desalination: Capacity growth (world)*

Desalination capacity (mill. cbm per day)

3040 16%

Titanium demand depends on the size of the desalination plants (thermal process).

Characteristic plant capacities and titanium

20

Characteristic plant capacities and titanium requirements are:

240,000 – 270,000 m³/day drinking water output: 70 t titanium

nKru

pp

* Thermal processes

02006 2010

Year

g p

800,000 m³/day drinking water output: 400 t titanium

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

Thermal processes

Source: own interviews/research

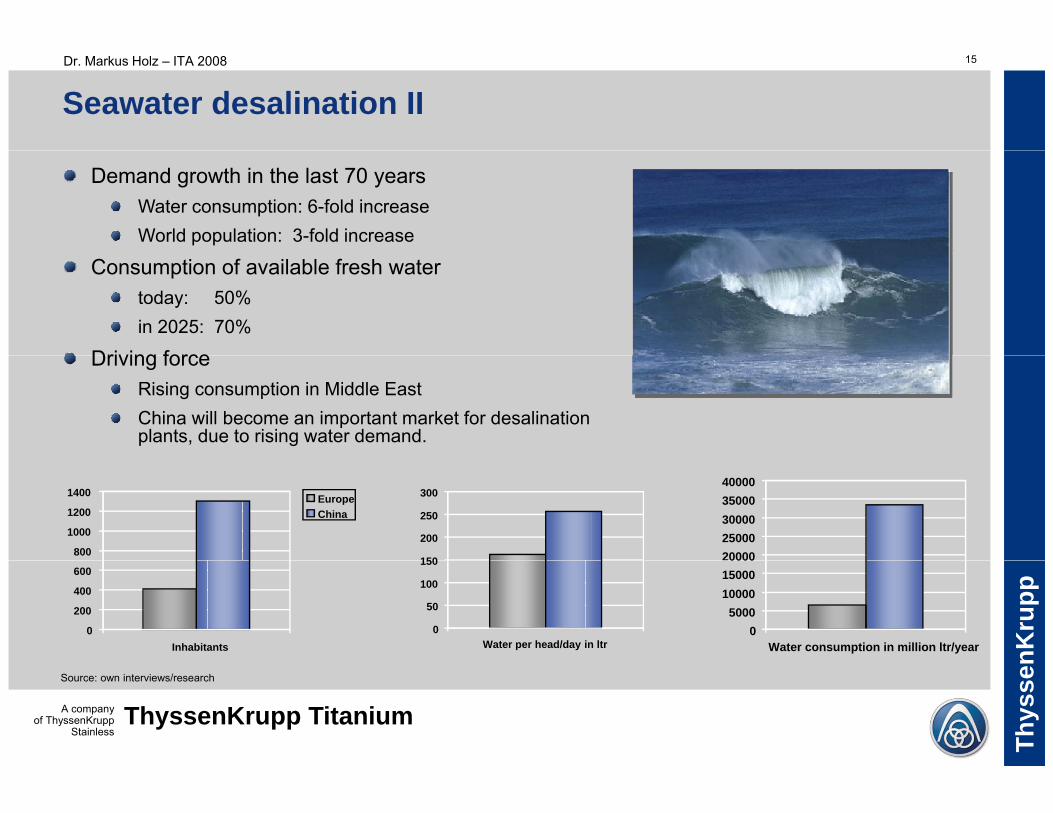

15Dr. Markus Holz – ITA 2008

Seawater desalination II

Demand growth in the last 70 yearsWater consumption: 6-fold increaseWorld population: 3-fold increase

Consumption of available fresh watertoday: 50%in 2025: 70%

Driving forceDriving forceRising consumption in Middle East China will become an important market for desalination plants, due to rising water demand.

800

1000

1200

1400 EuropeChina

150

200

250

300

2000025000300003500040000

nKru

pp

0

200

400

600

Inhabitants0

50

100

150

Water per head/day in ltr0

500010000150000000

Water consumption in million ltr/year

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

Source: own interviews/research

16Dr. Markus Holz – ITA 2008

World Medical Market (I)

8,5 9,711

12,314,1

on $

2003 2004 2005 2006 2007

Billio

d t

2003 2004 2005 2006 2007

Medical Market by application

knee joints40%

denture20%

extremety4%

nKru

pp

hip joints36%

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

Source: Zimmer

17Dr. Markus Holz – ITA 2008

World Medical Market (II)The orthopaedists use 2 2 Million different orthopaedic part of titaniumThe orthopaedists use 2,2 Million different orthopaedic part of titanium

World titanium demand by medical application in 2007

• Spinal columns 340 t 16 %p

• Denture 450 t 20 %

• Implants 1,150 t 52 %

• Surgical instruments 90 t 4 %

• Others 180 t 8 %

• Total 2,210 tAsia22%

Others3%

nKru

pp

Europe25%

USA50%

World Medical Market by Region

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

Source: Smith & Nephew, Zimmer25%

18Dr. Markus Holz – ITA 2008

The Global Titanium Market and the European Challengeand the European Challenge

Market Overview

Challenging Market Environment

Outlook and Summary

nKru

ppTh

ysse

n

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

19Dr. Markus Holz – ITA 2008

European Titanium Industry: The main challenge

• Price pressure by higher availability of more material due to aero crisisdue to aero crisis

• Projects delayed due to financial crisis of worldfinancial crisis of world economy

nKru

ppTh

ysse

n

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

20Dr. Markus Holz – ITA 2008

Price/Cost Hysteresis of Cyclical Businesses

Price/Costs

Development

Market pricesMarket prices

+ -

nKru

pp

2005-2008 2008-20XX

Raw material costs

t

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

21Dr. Markus Holz – ITA 2008

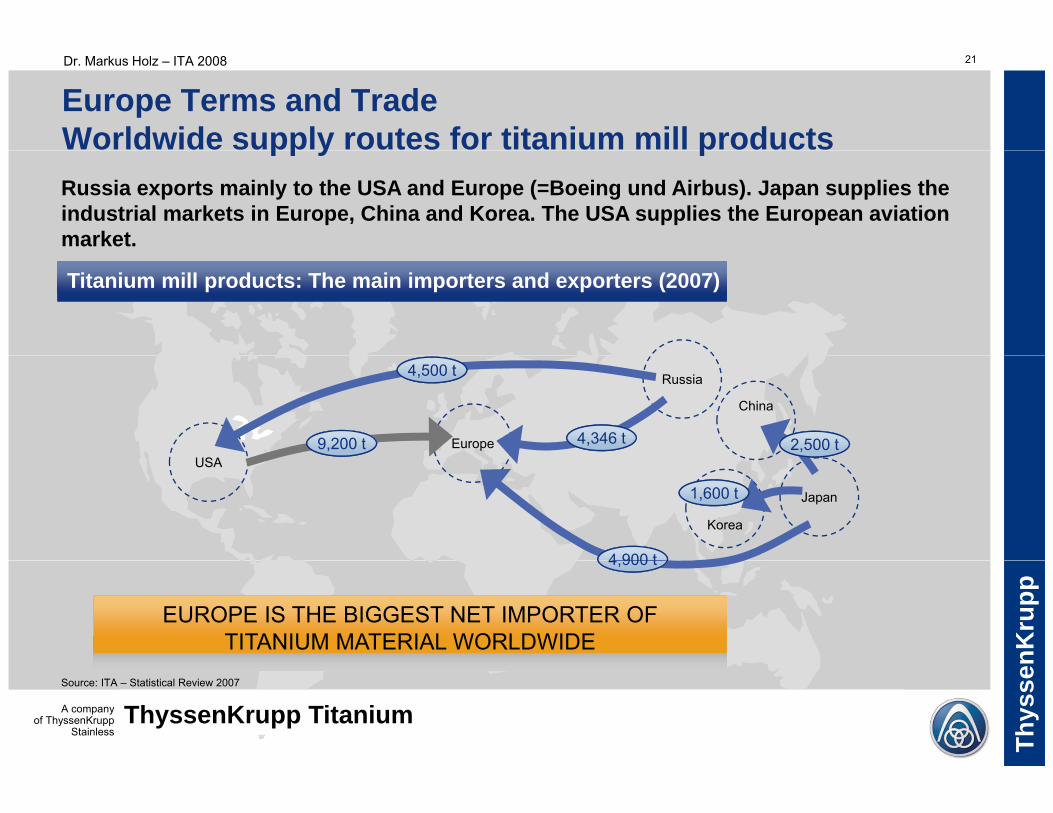

Europe Terms and TradeWorldwide supply routes for titanium mill productsRussia exports mainly to the USA and Europe (=Boeing und Airbus). Japan supplies the industrial markets in Europe, China and Korea. The USA supplies the European aviation market.

pp y p

Titanium mill products: The main importers and exporters (2007)

Europe

Russia

USA9,200 t9,200 t

China

2,500 t2,500 t4,346 t4,346 t

4,500 t4,500 t

USA

Japan

Korea

4 900 t

1,600 t1,600 t

nKru

pp

4,900 t4,900 t

EUROPE IS THE BIGGEST NET IMPORTER OF TITANIUM MATERIAL WORLDWIDE

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp TitaniumThyssenKrupp Titanium

Source: ITA – Statistical Review 2007

22Dr. Markus Holz – ITA 2008

European Titanium Industry: Strategic Position

RussiaUSA Japan Kazakhstan UkraineChina

Production, consumption of titanium by regions (2007)Value chain, products

Titanium spongeproduction 9% 32% 5% 28% 20% 6%

9% 24% 28% 20% 14% 5%

2005

2007

32% 11% 24% 13% 20%Titanium

mill productshipments

Europe

Titanium mill product

marketsOthers

EmergingIndustr Aerospace

37% 26% 15% 14% 6% 2%

nKru

pp

Titaniumuser markets

y10%47% 43%

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

Source: own research/-interviews/-calculations

23Dr. Markus Holz – ITA 2008

Europe is the 2nd scrap generator worldwide

USA

Titanium scrap production by regions (2007) Remarks

Large volumes on mill scrapand aerospace process scrap

Japan110027050

30000

Productionvolume

(1,000 tpy)Mill scrap:ingot/mill

Mill scrap:sponge/ingot

Process scrap:aerospace

Process scrap:non-aerospace

JapanMainly mill scrap due to largeexports of mill products

E

11600

1100

1405014500

20000

EuropeSmall mill scrap volumes(small mill production) butlarge aerospace process 12800

1550

1800

5450

113009800

6600

450 500700

300

9200

1230014050

10000

nKru

pp

scrap volume6800

650 1300 7001600 1600500 200

0USA Europe Japan Russia China Other

regions

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

Source: AMCG-research/own calculations/-interviews

24Dr. Markus Holz – ITA 2008

Consequences for ThyssenKrupp as a major European Titanium producerEuropean Titanium producer

Using internal raw material/scrap by electron beammaterial/scrap by electron beam melting

I i dImproving downstream– Sophisticated melting

processes– New forging press– Ti dedicated plate mill– Ti optimised cold rolling line

nKru

pp

p g– Ti dedicated VCF– Ti optimised tube lines

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

25Dr. Markus Holz – ITA 2008

Electron beam cold hearth melting

Typical General Lay Out

Zero level

Sub level

nKru

pp

E-Beam distribution on the Hearth/Crucible Assembly

1

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

Source: ALD

26Dr. Markus Holz – ITA 2008

EB-Furnace15 MT

Targets of Investment

15 MT

• Quasi continuous melting

• Single melting of ingot or slab in large geometrical dimensionsdimensions→ Reduction of production

steps; increase of yield

• Usage of entire variety of• Usage of entire variety of sponge to scrap raw material, depending on price

17th of March '08 first slab produced

nKru

ppTh

ysse

n

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

27Dr. Markus Holz – ITA 2008

VCF – Vacuum Creep Flattener

nKru

pp

Capacity: 700 tons

Plate thickness: 3-150 mm

Inauguration: Oct. 2006

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

Inauguration: Oct. 2006

28Dr. Markus Holz – ITA 2008

ThyssenKrupp VDM -DIVISION FORGING-

40/45 MN Forging Press

YOB: 2007; SMS Meer, Germany

open die forging press

2 manipulators

4 column design (pre stressed)4 column design (pre stressed)

4 sides flat guiding system each column

daylight 4300 mm

width between columns 3125 mm

nKru

pp

max stroke rate 120 min-1

penetration speed 120-170 mm/s

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

29Dr. Markus Holz – ITA 2008

ThyssenKrupp Aerospace Service Center

TK Aerospace, operating from 30 service centres in 13 countries throughout the Americas, Europe and Asia Pacific, has been created to provide their customers

with

More choice

More market coverage More value for money

More options

nKru

pp

More optionsMore experience

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

30Dr. Markus Holz – ITA 2008

The Global Titanium Market and the European Challengeand the European Challenge

Market Overview

Challenging Market Environment

Outlook and Summary

nKru

ppTh

ysse

n

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

31Dr. Markus Holz – ITA 2008

Outlook and Summary

Reduce sponge requirements by using scrap at a maximum

Reduce dependance on imports by enlarging fabrication capacity

Verticalization of manufacturing process / increasing service

Improving performance and services to the

nKru

pp

Improving performance and services to the European Titanium consumer in a more

difficult market environment

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

difficult market environment.

32Dr. Markus Holz – ITA 2008

All statements as to the properties or utilization of the materials and products mentioned in this presentation

are for the purpose of description onlyare for the purpose of description only.

Guarantees in respect of the existence of certainGuarantees in respect of the existence of certain properties or utilization of the material mentioned are

only valid if agreed upon in writing.

nKru

ppTh

ysse

n

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium

33Dr. Markus Holz – ITA 2008

nKru

ppThank you for your attention!

Thys

sen

A company of ThyssenKrupp

StainlessThyssenKrupp Titanium