Embed Size (px)

Citation preview

Managing EmployeeBenefits

Chapter 13Chapter 13

SECTION 4SECTION 4Compensating Compensating

Human ResourcesHuman Resources

Nice Benefits!

Benefits Benefit

An indirect compensation given to an employee or group of employees as a part of organizational membership.

Health benefits in the U.S. are provided by employers This is unique Benefit costs are being shifted even more on employers by

state and federal governments Strategic Perspectives on Benefits

Benefits vs. Salaries- which is preferred for addition or subtraction?

Benefits influence employee decisions about employers Retention Absenteeism Recruitment

Benefits are increasingly seen as entitlements. Benefit costs average over 40% of total payroll costs.

13–3

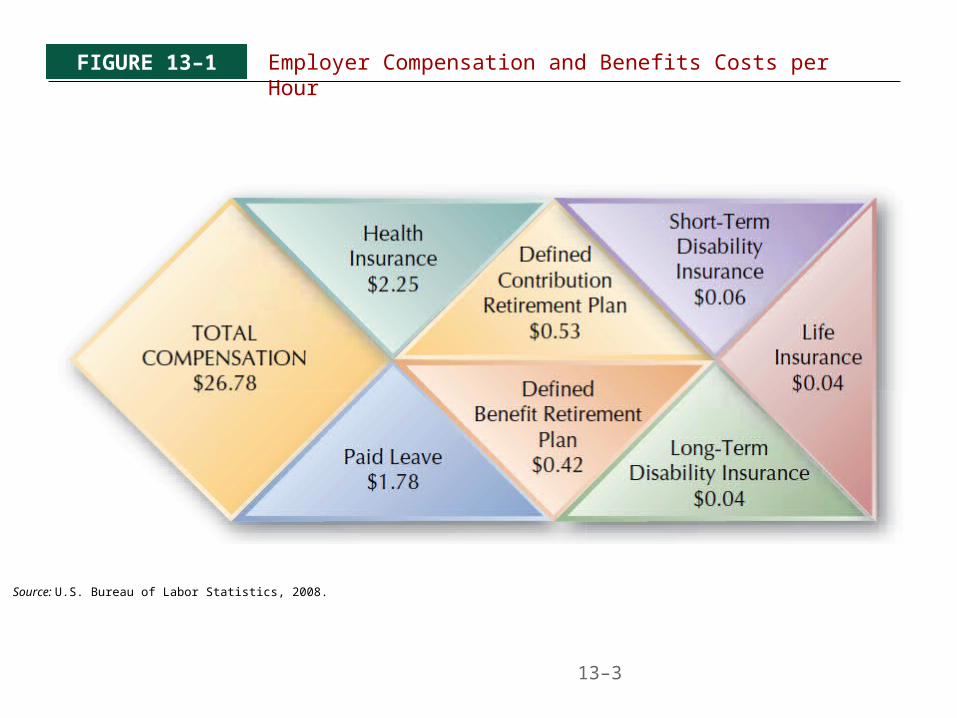

FIGURE 13–1 Employer Compensation and Benefits Costs per Hour

Source: U.S. Bureau of Labor Statistics, 2008.

13–4

FIGURE 13–8 Private Industry Workers with Health Benefits

Source: U.S. Bureau of Labor Statistics, www.bls.gov/ncs/home.htm.

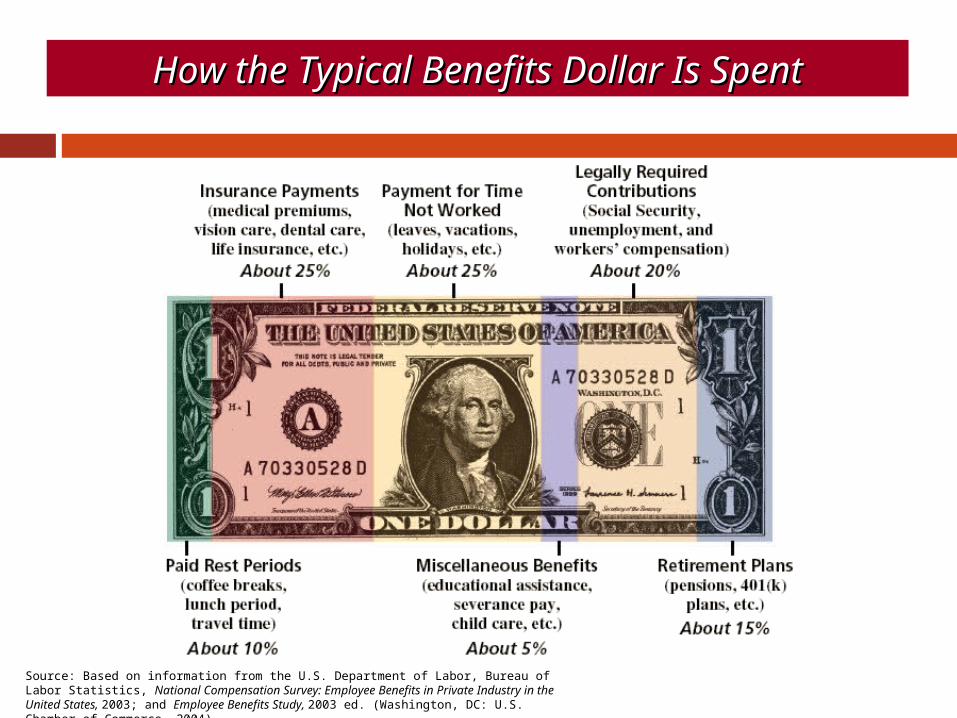

How the Typical Benefits Dollar Is SpentHow the Typical Benefits Dollar Is Spent

Source: Based on information from the U.S. Department of Labor, Bureau of Labor Statistics, National Compensation Survey: Employee Benefits in Private Industry in the United States, 2003; and Employee Benefits Study, 2003 ed. (Washington, DC: U.S. Chamber of Commerce, 2004).

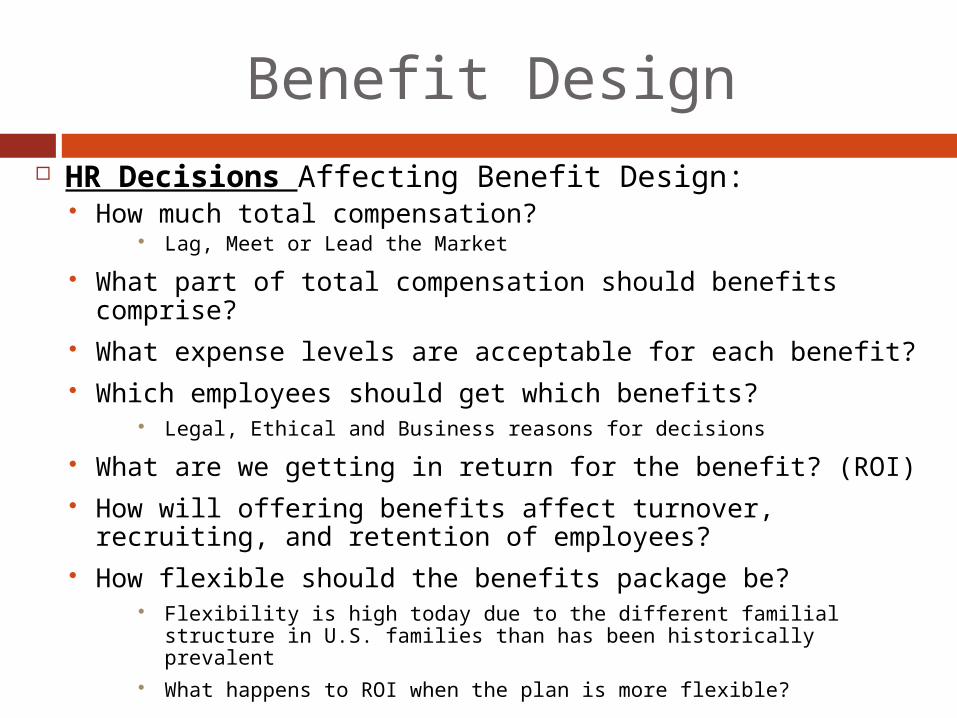

Benefit Design HR Decisions Affecting Benefit Design:

How much total compensation? Lag, Meet or Lead the Market

What part of total compensation should benefits comprise? What expense levels are acceptable for each benefit? Which employees should get which benefits?

Legal, Ethical and Business reasons for decisions What are we getting in return for the benefit? (ROI) How will offering benefits affect turnover, recruiting, and

retention of employees? How flexible should the benefits package be?

Flexibility is high today due to the different familial structure in U.S. families than has been historically prevalent

What happens to ROI when the plan is more flexible?

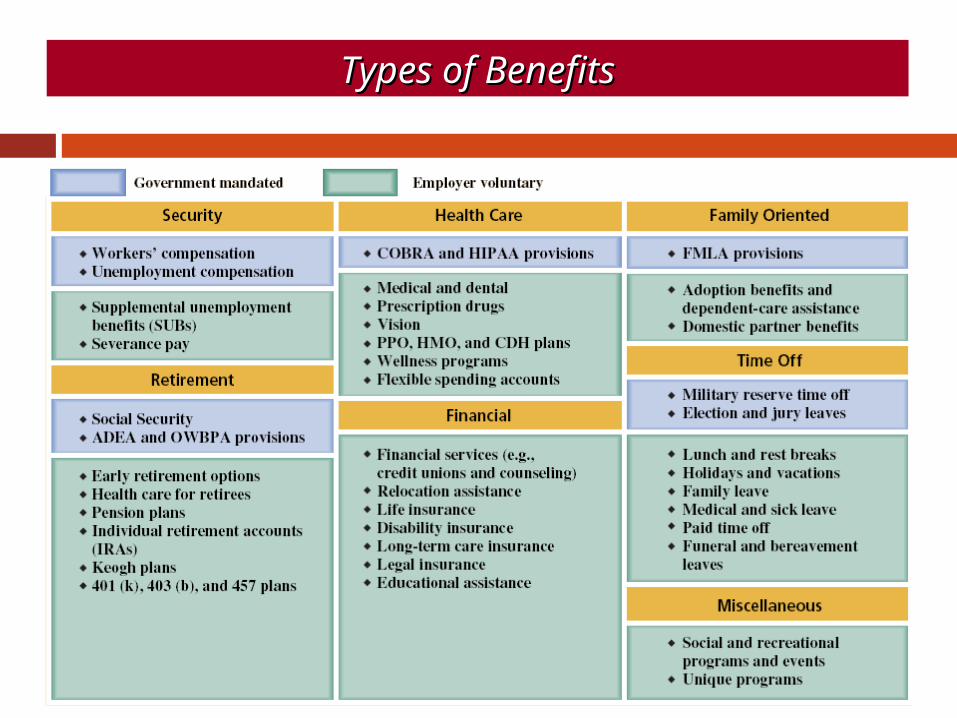

Types of BenefitsTypes of Benefits

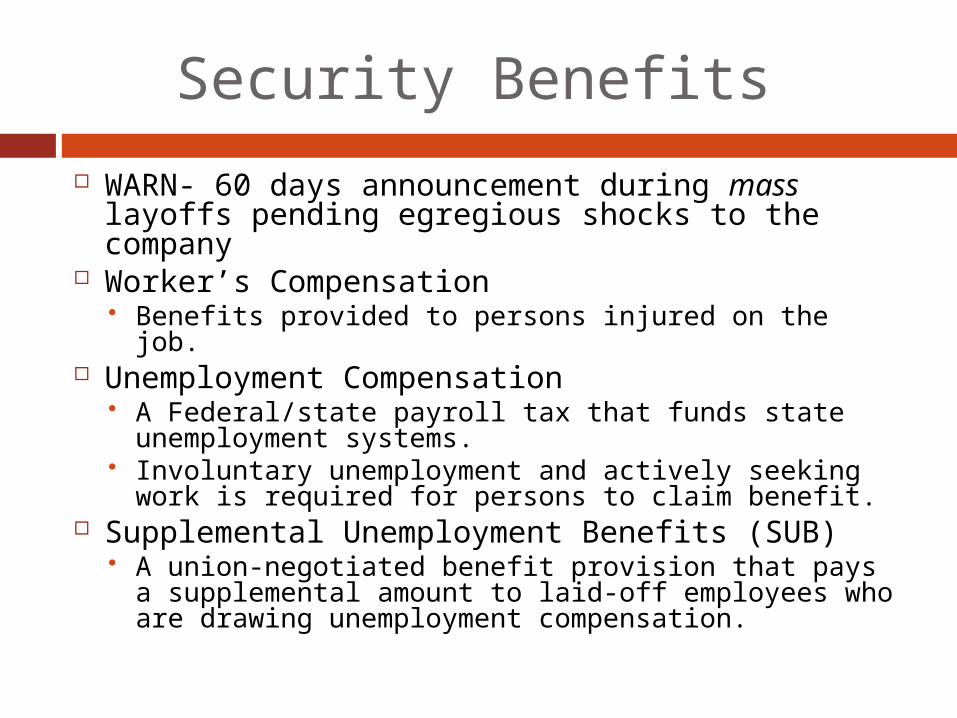

Security Benefits WARN- 60 days announcement during mass

layoffs pending egregious shocks to the company

Worker’s Compensation Benefits provided to persons injured on the job.

Unemployment Compensation A Federal/state payroll tax that funds state

unemployment systems. Involuntary unemployment and actively seeking work

is required for persons to claim benefit. Supplemental Unemployment Benefits (SUB)

A union-negotiated benefit provision that pays a supplemental amount to laid-off employees who are drawing unemployment compensation.

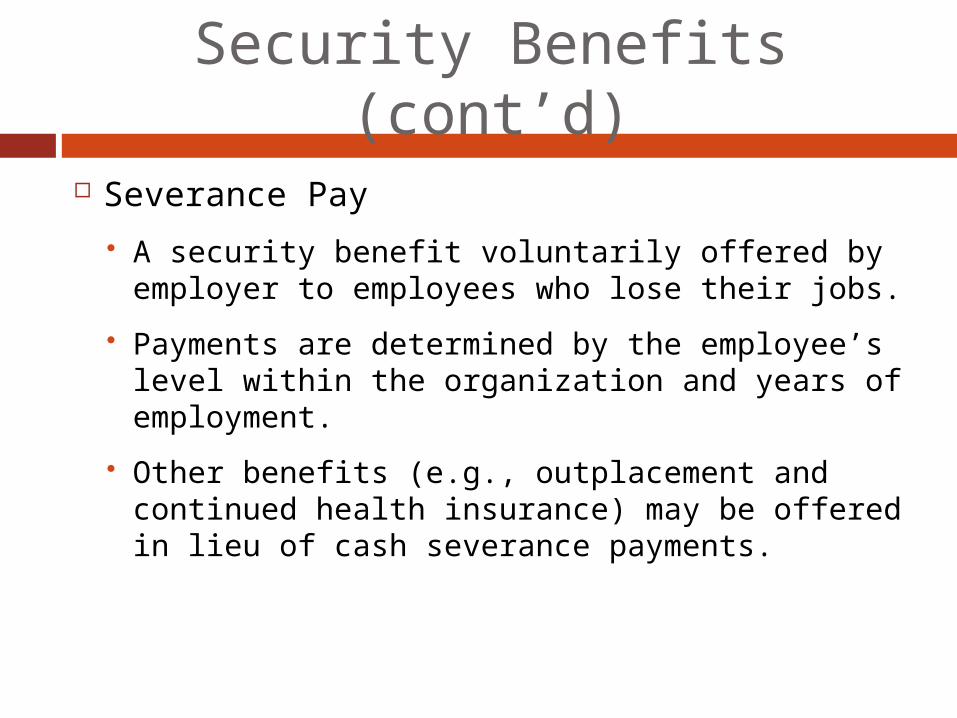

Security Benefits (cont’d) Severance Pay

A security benefit voluntarily offered by employer to employees who lose their jobs.

Payments are determined by the employee’s level within the organization and years of employment.

Other benefits (e.g., outplacement and continued health insurance) may be offered in lieu of cash severance payments.

Retirement Benefits Social Security Act of 1935

Established a system providing old age, survivor’s, disability, and retirement benefits. Federal payroll tax (7.65%) on both the employer

and the employee. Medicare taxes are 2.9% Benefit payments are based on an employee’s

lifetime earnings. Administered by the Social Security

Administration.

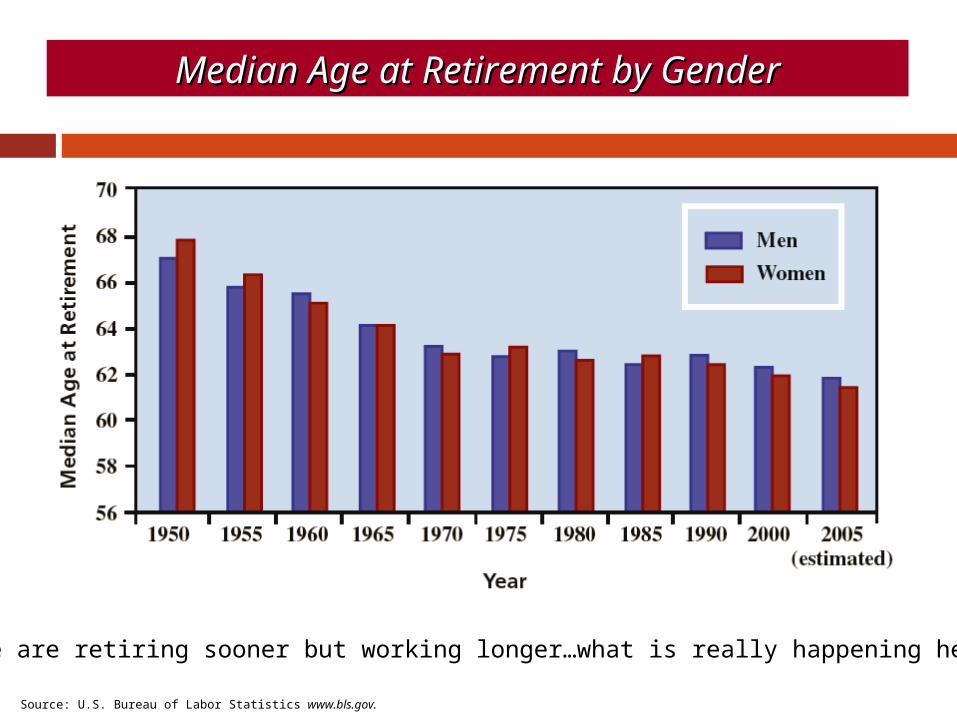

Median Age at Retirement by GenderMedian Age at Retirement by Gender

Source: U.S. Bureau of Labor Statistics www.bls.gov.

People are retiring sooner but working longer…what is really happening here?

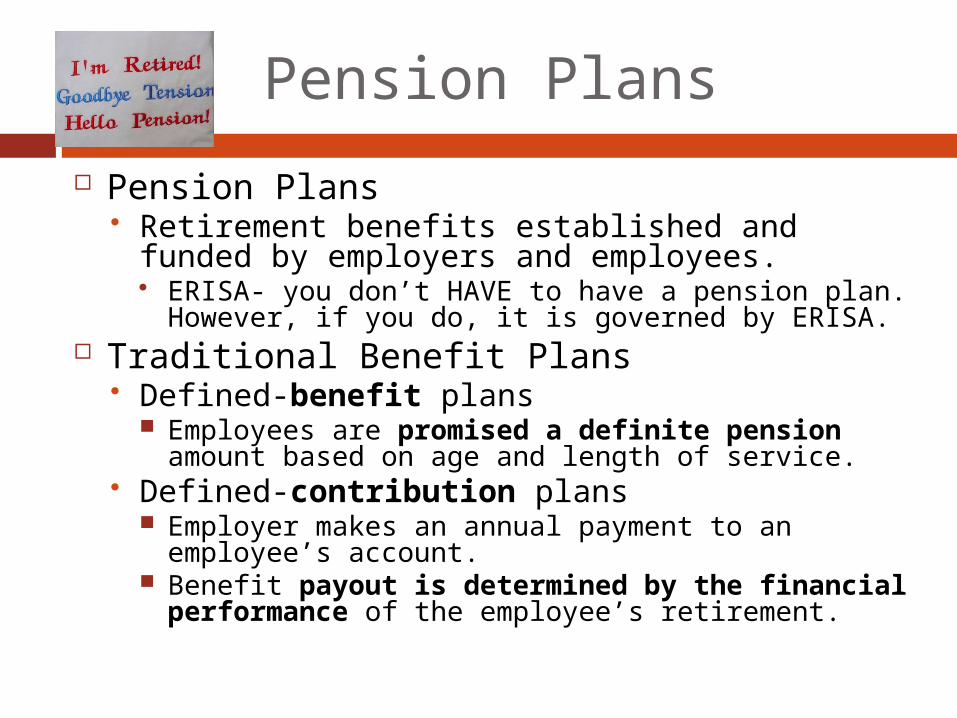

Pension Plans Pension Plans

Retirement benefits established and funded by employers and employees. ERISA- you don’t HAVE to have a pension plan.

However, if you do, it is governed by ERISA. Traditional Benefit Plans

Defined-benefit plans Employees are promised a definite pension

amount based on age and length of service. Defined-contribution plans

Employer makes an annual payment to an employee’s account.

Benefit payout is determined by the financial performance of the employee’s retirement.

13–14

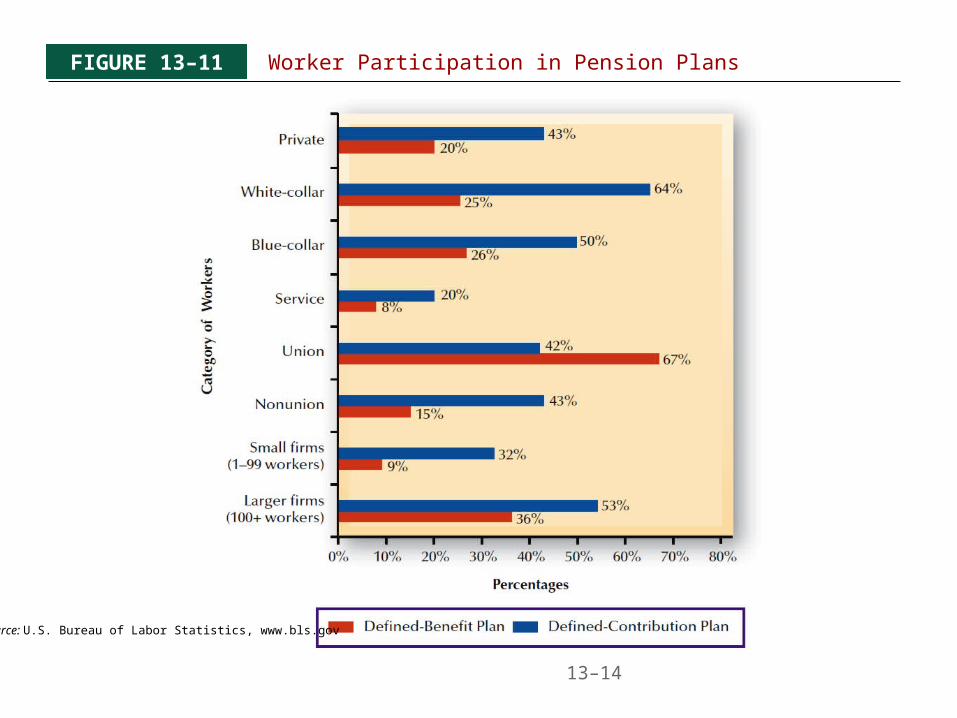

FIGURE 13–11 Worker Participation in Pension Plans

Source: U.S. Bureau of Labor Statistics, www.bls.gov

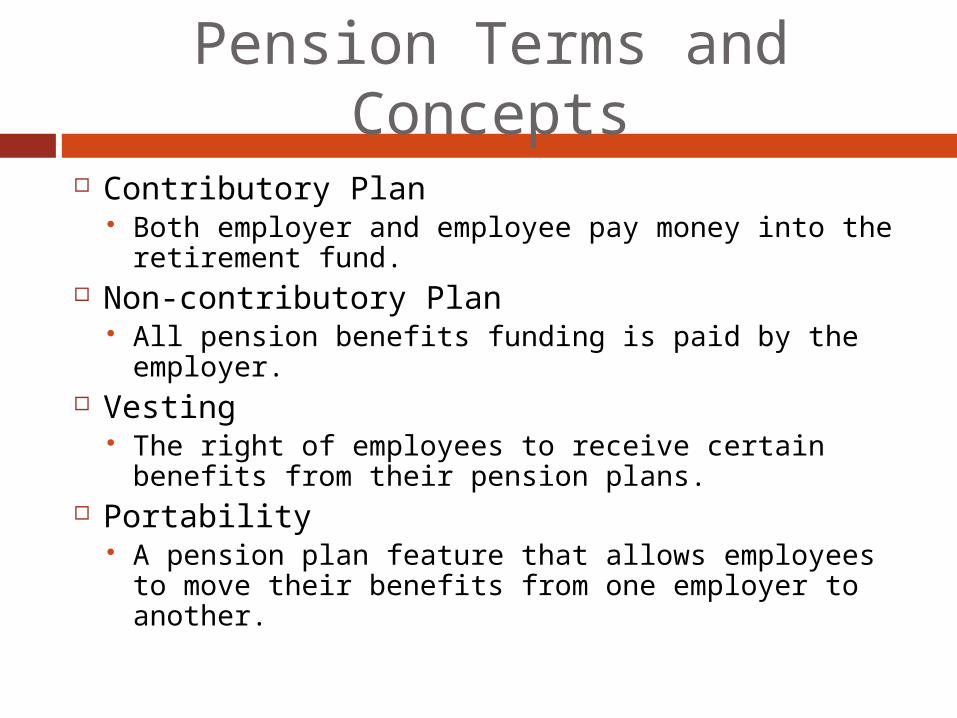

Pension Terms and Concepts

Contributory Plan Both employer and employee pay money into the

retirement fund. Non-contributory Plan

All pension benefits funding is paid by the employer.

Vesting The right of employees to receive certain benefits

from their pension plans. Portability

A pension plan feature that allows employees to move their benefits from one employer to another.

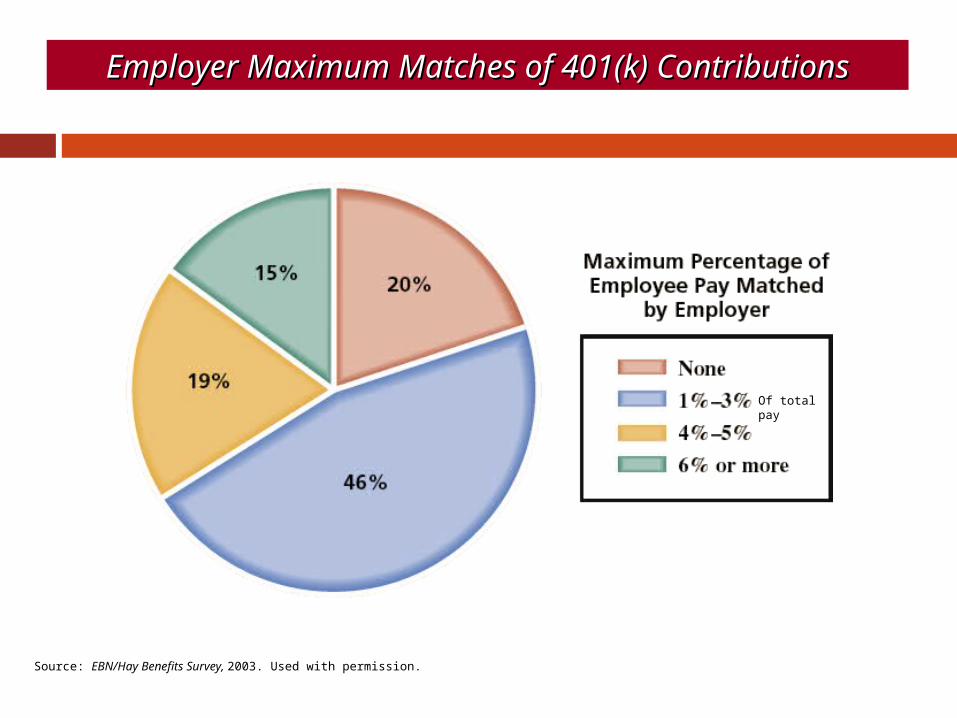

Employer Maximum Matches of 401(k) Employer Maximum Matches of 401(k) ContributionsContributions

Source: EBN/Hay Benefits Survey, 2003. Used with permission.

Of total pay

Cost of Health Care Why is health care so expensive?

Uninsured workers Retirees Older generations in the workplace FDA rules versus pharmaceutical ROI Lawsuits? Other?

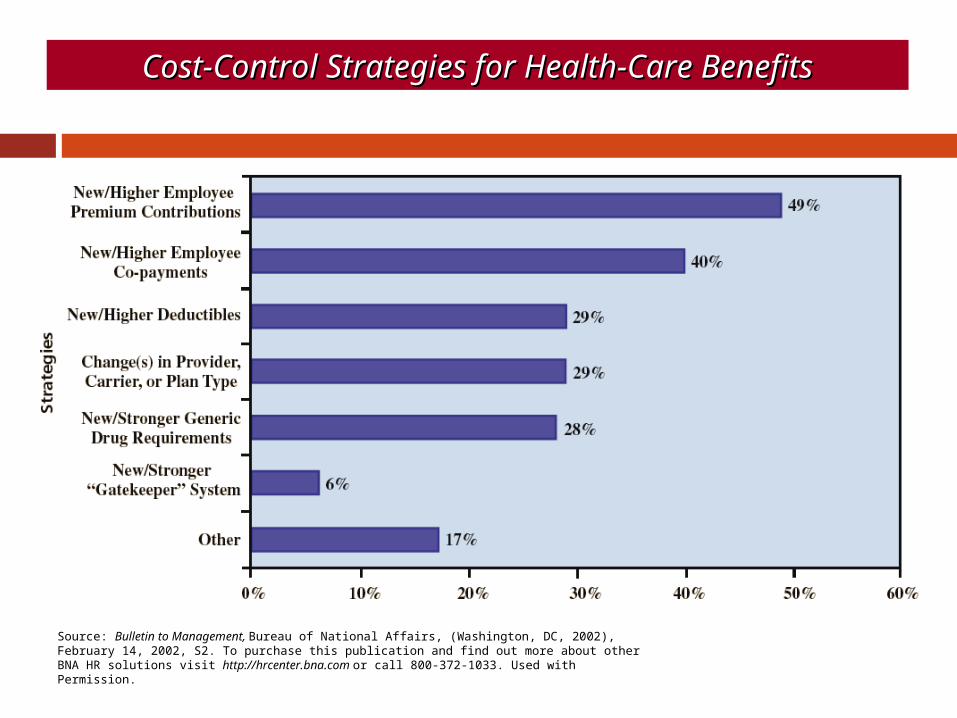

Cost-Control Strategies for Health-Care BenefitsCost-Control Strategies for Health-Care Benefits

Source: Bulletin to Management, Bureau of National Affairs, (Washington, DC, 2002), February 14, 2002, S2. To purchase this publication and find out more about other BNA HR solutions visit http://hrcenter.bna.com or call 800-372-1033. Used with Permission.

Controlling Health-Care Costs

Managed Care Approaches that monitor and reduce medical

costs using restrictions and market system alternatives.

Preferred Provider Organization A health-care provider that contracts with an

employer group to provide health-care services to employees at a competitive rate.

Health Maintenance Organization (HMO) A managed care plan that provides services for

a fixed period on a prepaid basis.

Different Types of Insurance

HMO PPO

Medicare

Medicaid

Uninsured

Medicare

HSATrad

Medical

HSATrad

Medical

Health-Care Legislation Consolidated Omnibus Budget

Reconciliation Act (COBRA) Provisions Former employees are eligible to purchase

group insurance at no more than 102% of group insurance premium rate.

Former employees, their spouses, and eligible dependents are covered for 18 to 36 months

COBRA requirements incur additional paperwork and related costs for employers.

Health-Care Legislation (cont’d)

Health Insurance Portability and Accountability Act (HIPAA) of 1996 Provisions Allows employees to switch their health

insurance plan from one company to another, regardless of pre-existing health conditions. Health plans must continue to cover sick employees.

Require employers to provide privacy notices to employees.

Regulate the disclosure of protected health information without authorization.

Health Care Reform: Obamacare One of Obama’s major campaign issues Attempts to deal with uninsured workers Attempts to make good on Obama’s

promise not to heavily tax the middle class to pay for it.

A price of about $1 trillion. Titles HR 3962 Passed the House in November 2010

220-215 with 39 dems voting against

“Americans want a common sense approach to health care reform, not Speaker Nancy Pelosi’s 2,000-page government takeover that increases costs, adds to our skyrocketing debt, destroys jobs with tax hikes and new mandates, and cuts Medicare benefits,” said House Minority Leader Rep. John Boehner, R-Ohio. “Americans who ask ‘where are the jobs?’ are getting more of the same from out-of-touch Washington Democrats: more spending, more debt and more government.”

The legislation as passed by the House would require employers with annual payrolls above $500,000 to provide health benefits to their employees or pay a penalty or payroll tax of up to 8 percent. The money would go to fund a new health insurance exchange and lower-cost health plans, which would be offered by the government.

“Cadillac” health insurance will also be taxed to help pay for the plan.- Kicks in 2018

Up to a 5.4% tax will be leveled on incomes greater than 280k (individual ) or 350k (couple) to help pay for the program.

Individuals without coverage from employers or other sources would be required to purchase insurance or pay a penalty of up to 2.5 percent of their taxable income. Medicaid coverage would be extended to nearly 15 million additional lower-income people who do not currently qualify for coverage. Federal subsidies would be available to low- and middle-income families that still could not afford to pay for health coverage after the reforms are enacted.

The legislation would extend COBRA health insurance continuation benefits until an individual becomes eligible for health insurance coverage through the health insurance exchange. The insurance exchange would be a health insurance marketplace where individuals would have the choice of purchasing coverage from private-sector providers or from a government-run insurance plan.

Primary Concern “As we have stated repeatedly over the past

several months, the House bill’s regulatory framework will, unintentionally, compel many employers to cease offering health coverage and simply ‘pay’ a penalty rather than ‘play’ through sponsoring a plan, thereby losing all the innovation that employers bring through promoting wellness programs and insisting on good quality outcomes,” said Jim Klein, president of the American Benefits Council.

Current Evidence One basic premise of Obamacare is that people

with health insurance are paying for ER visits for people without Health Insurance. Thus, will all people having health insurance costs will go down for everyone.

You can’t get those savings if those people are still going to the emergency room.- President Barack Obama, March 3, 2010

[P]eople are no longer going to the emergency room and they now have good health care, they’re now getting preventive care.- President Barack Obama, September 24, 2013

Current Evidence Contd. Study published in Science by Harvard

Researchers called the Oregon Health Insurance Experiment Considered the best empirical study to date on

Obamacare Shows when people do not have to pay for health

insurance or are given significant discounts Emergency Room Visits increase 40%

Suggests the cost savings will not be realized in the immediate or over time.

Forbes article in full

Other Benefits

BenefitsBenefits

Relocation Relocation ExpensesExpenses

Life, Disability, Life, Disability, Legal InsurancesLegal Insurances

Educational Educational AssistanceAssistance

Social and Social and RecreationalRecreational

Family-Oriented Family-Oriented BenefitsBenefits

Family-Care Family-Care BenefitsBenefits

Credit Unions Credit Unions Purchase Discounts Purchase Discounts

Stock InvestmentStock Investment

Family Medical Leave Act (FMLA)

Coverage Employers with 50 or more employees Employees who have worked at least 12

months and 1,250 hours in the previous year.

Requirements Employers must allow eligible employees to

take up to a total of 12 weeks of unpaid leave in a 12-month period to attend to a family or serious medical condition.

Employees have the right to continued health benefits and the right to return to their job.

New Changes to FMLA 1/2008 Requires that employers provide 12 weeks of

FMLA leave to the immediate family members (spouses, children or parents) of reservists or members of the National Guard who are called to active duty in the U.S. military. Under the new law, employers also must offer up to 26 weeks of unpaid leave to employees who are providing care for family members wounded while serving in the U.S. military. Workers can take the leave in increments of the shortest time periods tracked by their employers’ payroll system.

Benefits for Domestic Partners

Domestic Partners or Spousal Equivalents Unmarried employees who are living with

individuals of the opposite sex Gay and lesbian employees who have partners

Affidavit of Spousal Equivalence Each is the other’s only spousal equivalent. They are not blood relatives. They are living together and jointly share

responsibility for their common welfare and financial obligations.

Flexible Benefits Flexible Benefit Plan

A plan (flex or cafeteria plan) that allows employees to select the benefits they prefer from groups of benefits established by the employer.

Problems with Flexible Plans Inappropriate benefits package choices Adverse selection and use of specific benefits by

higher-risk employees Higher administrative cost

Discussion

What future events do we see affecting benefits in organizations?

What will be their impact? How will we manage them?

Workers Compensation and Unemployment Insurance Activity

USERRA SHRM National Survey on Benefits

Microsoft Office Word 97 - 2003 Document