Embed Size (px)

Citation preview

Third quarter 2017Vestas Wind Systems A/S

Copenhagen, 9 November 2017

Classification: Public

Disclaimer and cautionary statement

9 November, 2017Third quarter 2017 (Public)2

This document contains forward-looking statements concerning Vestas’ financial condition, results of operations and business. All statements otherthan statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements are statements of futureexpectations that are based on management’s current expectations and assumptions and involve known and unknown risks and uncertainties thatcould cause actual results, performance, or events to differ materially from those expressed or implied in these statements.

Forward-looking statements include, among other things, statements concerning Vestas’ potential exposure to market risks and statementsexpressing management’s expectations, beliefs, estimates, forecasts, projections and assumptions. A number of factors that affect Vestas’ futureoperations and could cause Vestas’ results to differ materially from those expressed in the forward-looking statements included in this document,include (without limitation): (a) changes in demand for Vestas’ products; (b) currency and interest rate fluctuations; (c) loss of market share andindustry competition; (d) environmental and physical risks, including adverse weather conditions; (e) legislative, fiscal, and regulatory developments,including changes in tax or accounting policies; (f) economic and financial market conditions in various countries and regions; (g) political risks,including the risks of expropriation and renegotiation of the terms of contracts with governmental entities, and delays or advancements in theapproval of projects; (h) ability to enforce patents; (i) product development risks; (j) cost of commodities; (k) customer credit risks; (l) supply ofcomponents; and (m) customer created delays affecting product installation, grid connections and other revenue-recognition factors.

All forward-looking statements contained in this document are expressly qualified by the cautionary statements contained or referenced to in thisstatement. Undue reliance should not be placed on forward-looking statements. Additional factors that may affect future results are contained inVestas’ annual report for the year ended 31 December 2016 (available at www.vestas.com/investor) and these factors also should be considered.Each forward-looking statement speaks only as of the date of this document. Vestas does not undertake any obligation to publicly update or reviseany forward-looking statement as a result of new information or future events other than as required by Danish law. In light of these risks, resultscould differ materially from those stated, implied or inferred from the forward-looking statements contained in this document.

Key highlightsSolid performance in Q3

9 November, 20173

Increased order intakeOrder intake in the quarter reached 2,615 MW – up 48 percent compared to Q3 2016

Revenue of EUR 2,743mRevenue 9M 2017 of EUR 6,834m – on par with 2016

EBIT of EUR 355mEBIT decreased 18 percent compared to Q3 2016

Service revenue continues to increaseRevenue increased 18 percent with an EBIT margin of 17.9 percent

Free cash flow reached EUR 193mFree cash flow improved 25 percent year-on-year

Outlook 2017Guidance for 2017 adjusted – mainly based on visibility for the remainder of the year

Third quarter 2017 (Public)

9 November, 20174 Third quarter 2017 (Public)

Agenda

9 November, 20174

1. Orders and markets

2. Financials

3. Outlook and questions & answers

Q3 Interim financial report,third quarter 2017

Third quarter 2017 (Public)

The wind power industry continues to evolve

9 November, 20175

Market is transitioning quickly to more competitive tenders and auction systems

EU introducing auctions and discussing electricity market better adapted for RES…

• First two of three total auctions in Germany in 2017 with high shares of citizen wind with longer realisation times, resulted in stricter rules for the first two rounds in 2018

• Auction expected in France in Q4 2017

And positive signals in MEA

• Steady growth and continued commitment, but coming from a low base

• 400 MW wind auction launched in Saudi Arabia – results expected in early 2018

EMEA Asia PacificAmericas

PTC timing in USA…• Strong US demand driven by current PTC

structure and competitiveness of wind • Proposed House Tax legislation creating

uncertainty

And several auctions coming up in Latin America

• Auctions expected in Brazil and Mexico for Q4

• Auctions recently completed in Bolivia and Chile

• Colombia expected to announce an auction in 2018

Continued commitment in China…• 13th 5-year plan wind target of 210 GW

cumulative installations by 2020• Curtailment being addressed in some

markets

India is uncertain…• Target of 60 GW by 2022 remains in place• First auctions executed and three more

expected before end of February 2018, although delays creating uncertainty

And broader Asia Pacific region on the move• Renewable targets in most markets• Auction expected in Australia in Q1 2018

Asia Pacific

As the market continues its transformation and as competition accelerates, Vestas maintains its global leadership position.

Vestas remains committed to its strategy, and continues to lower the cost of energy and optimise products and service offerings.

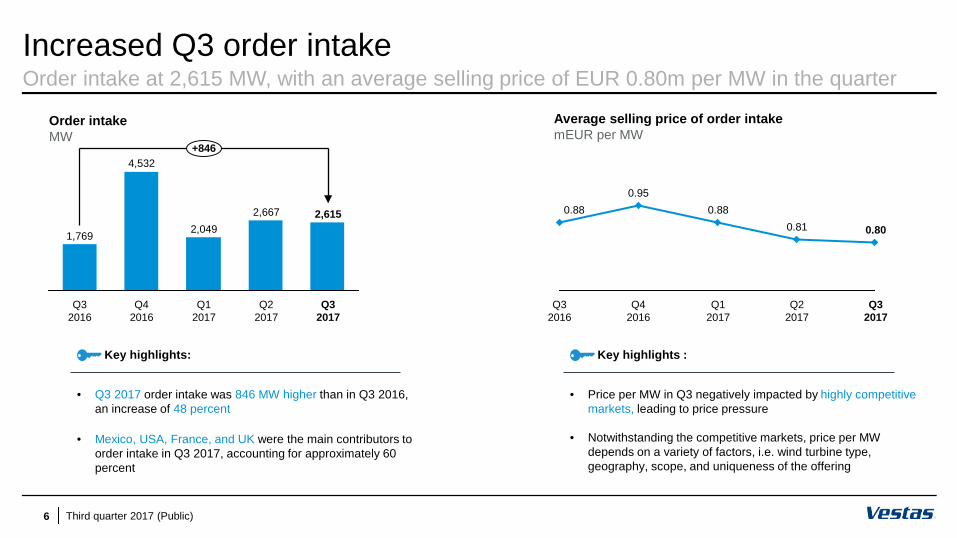

Increased Q3 order intakeOrder intake at 2,615 MW, with an average selling price of EUR 0.80m per MW in the quarter

9 November, 20176

Order intakeMW

Q42016

Q32017

4,532

Q22017

1,769

Q32016

+846

2,615

Q12017

2,6672,049

Average selling price of order intakemEUR per MW

Q32017

0.80

Q22017

0.88

Q42016

0.95

0.81

Q12017

Q32016

0.88

• Q3 2017 order intake was 846 MW higher than in Q3 2016, an increase of 48 percent

• Mexico, USA, France, and UK were the main contributors to order intake in Q3 2017, accounting for approximately 60 percent

Key highlights:

• Price per MW in Q3 negatively impacted by highly competitive markets, leading to price pressure

• Notwithstanding the competitive markets, price per MW depends on a variety of factors, i.e. wind turbine type, geography, scope, and uniqueness of the offering

Key highlights :

Third quarter 2017 (Public)

Strong order intakeOrder intake 9M 2017 increased 23 percent compared to 9M 2016, mainly driven by developing markets

9 November, 20177

340

9M9M

3,3023,435

1,097

2,7992,320

9M

+48%

+223%

-15% 20162017

AmericasMW

EMEAMW

Asia PacificMW

• Increase primarily driven by strong order intake in USA, Mexico, and Argentina

• Strong order intake across Europe, primarily driven by Germany and Sweden

• Increased order intake in France, UK, and Denmark partly offsetting decline from 1 GW Statkraft orderin Q1 2016

• Strong development in China, India, and Thailand

• Also good order intake in Australia, Mongolia, and South Korea

Third quarter 2017 (Public)

Regional delivery splitQ3 deliveries down 14 percent, mainly driven by the Americas

9 November, 20178

140504909 231405

1,733

9M

1,025

9M

-20%

Q3

2,676

-41%

Q3

1,148

+65%

-17%

Q3

+26%

-1%

2,6512,735

9M

3,307

20172016

AmericasMW

EMEAMW

Asia PacificMW

• Solid US market deliveries, albeit at a lower level

• Good activity in Brazil and Canada

• Strong development in Germany and France, driving increase in Q3

• Increased deliveries in UK compensating for 9M drops in South Africa and Sweden

• Positive development in other Asia Pacific markets such as Mongolia, South Korea, and Japan in Q3

• China and India remainfairly stable

Third quarter 2017 (Public)

* Compared to Q2 2017.

Order backlog remains at a high levelCombined backlog of more than EUR 20bn

9 November, 20179

Wind turbines:

EUR 8.8bn

Service:

EUR 11.4bn

EUR (0.3)bn*

Third quarter 2017 (Public)

EUR +0.3bn*

JV continues positive developmentFirm and unconditional order for the 252 MW Deutsche Bucht project announced

9 November, 2017

10

Near-term project execution

• Final installation of Rampion (UK) and Blyth (UK): the last V164-8.4 MW turbine installed in record low time, showing the great learning curve of the installation teams

• Announcement of the 252 MW Deutsche Bucht project as firm and unconditional

• Preferred supplier announcement of the 860 MW Triton Knoll (UK) and950 MW Moray East* (UK) projects (V164-9.5 MW turbine)

WalneyExtension (UK)330 MWV164-8.0 MW

Projects currently in progress

Third quarter 2017 (Public)

Borkum Riffgrund (DE)450 MWV164-8.0 MW

~2.5 GW

Announced conditional & preferred supplier agreements*

~2.7 GW

Announced FOI*

Since JV formation…Aberdeen Bay (UK)92.4 MWV164-8.0 MW

Key highlights

* As at 9 November 2017 * Announced in Q4 2017

9 November, 201711 Third quarter 2017 (Public)

Agenda

9 November, 201711

1. Orders and markets

2. Financials

3. Outlook and questions & answers

Interim financial report,third quarter 2017

Q3

Third quarter 2017 (Public)12

Income statementLower activity in Q3 resulting in weaker margins

mEUR Q3 2017 Q3 2016 % change

Revenue 2,743 2,903 (6)%

Production costs (2,217) (2,312) 4%

Gross profit 526 591 (11)%

SG&A costs* (171) (158) (8)%

EBIT 355 433 (18)%

Income from investments in

associates and joint ventures(18) (20) 10%

Net profit 253 309 (18)%

Gross margins 19.2% 20.4% (1.2)%-pts

EBITDA margin 16.5% 18.2% (1.7)%-pts

EBIT margin 12.9% 14.9% (2.0)%-pts

9 November, 2017

• Revenue decreased 6 percent, primarily driven by Power solutions segment; partly offset by higherrevenue in Service

• Gross profit down by 1.2 percentage points, mainly driven by decreased volumes and lower average margins in the Power solution segment

• EBIT down by 18 percent, mainly driven by lower gross profit

Key highlights:

* R&D, administration, and distribution.

* R&D, administration, and distribution on trailing 12 months basis.

13

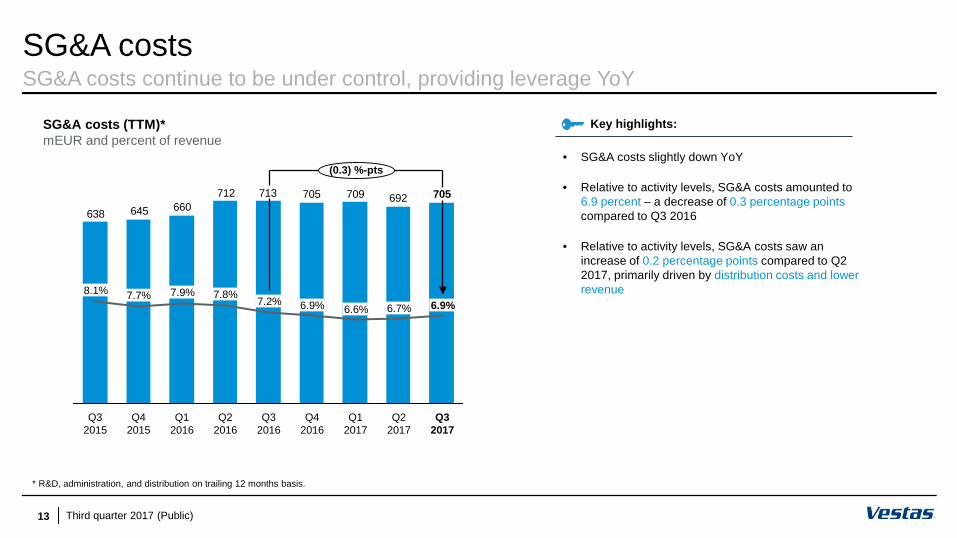

SG&A costsSG&A costs continue to be under control, providing leverage YoY

9 November, 2017

709705713712660645638

705692

Q32017

6.9%

(0.3) %-pts

Q22017

6.6%7.7% 7.2%7.8%

6.9%

Q42016

Q12016

Q22016

Q42015

Q32016

Q32015

7.9%6.7%

Q12017

8.1%

SG&A costs (TTM)*mEUR and percent of revenue

• SG&A costs slightly down YoY

• Relative to activity levels, SG&A costs amounted to 6.9 percent – a decrease of 0.3 percentage points compared to Q3 2016

• Relative to activity levels, SG&A costs saw an increase of 0.2 percentage points compared to Q2 2017, primarily driven by distribution costs and lower revenue

Key highlights:

Third quarter 2017 (Public)

14

ServiceStrong service performance driven by high activity levels

9 November, 2017

369372

312

368371

+18%

Q32017

Q32016

Q42016

Q12017

Q22017

• Service revenue increased by 18 percent compared to Q3 2016, mainly driven by higher activity levels

• Q3 2017 EBIT: EUR 66m Q3 2017 EBIT margin: 17.9 percent

• Service order backlog growth of EUR 0.3bn compared to Q2 2017

Service revenuemEUR

Key highlights:

Third quarter 2017 (Public)

15

Balance sheetBalance sheet remains strong

9 November, 2017

Assets (mEUR) Q3 2017 Q3 2016 Abs. change % change

Non-current assets 2,778 2,557 221 9%

Current assets 7,784 6,780 1,004 15%

Total assets 10,562 9,337 1,225 13%

Liabilities (mEUR)

Equity 3,163 3,073 90 3%

Non-current liabilities 1,113 986 127 13%

Current liabilities 6,286 5,278 1,008 19%

Total equity and liabilities 10,562 9,337 1,225 13%

Key figures (mEUR)Interest bearing position (net)

2,609 2,116 493 23%

Net working capital (1,053) (787) (266) (34)%

Solvency ratio (%) 29.9 32.9 - 3.0%-pts

• Net cash position increased to EUR 2,609m

• Positive net working capital development of EUR 266m

Key highlights:

Third quarter 2017 (Public)

* Construction contracts in progress.

16

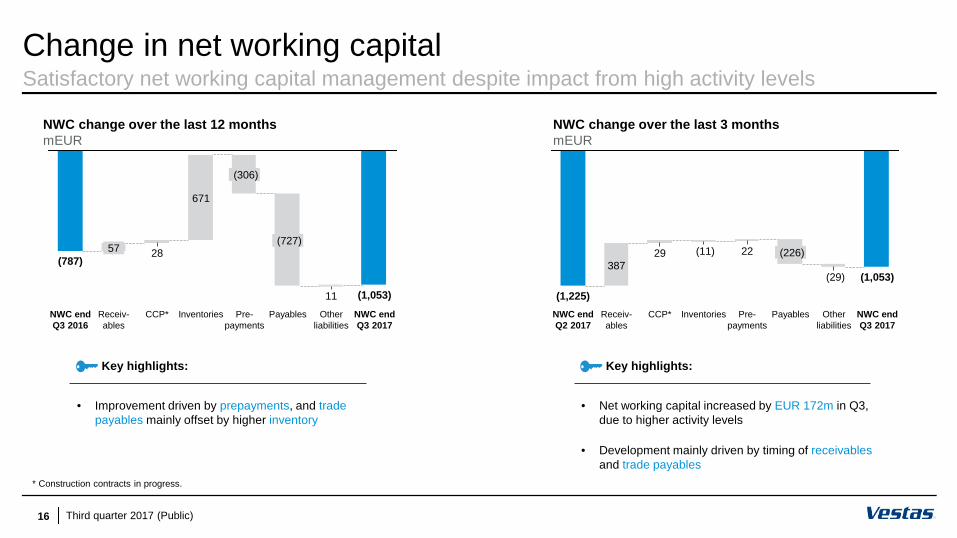

Change in net working capitalSatisfactory net working capital management despite impact from high activity levels

9 November, 2017

(787)57

NWC endQ3 2016

28

Receiv-ables

11

(727)

(306)

Inventories Other liabilities

Pre-payments

Payables

671

NWC endQ3 2017

CCP*

(1,053)CCP*

(1,053)

(226)29

Pre-payments

22

Other liabilities

(11)

Payables

(29)

NWC endQ3 2017

Inventories

387

NWC endQ2 2017

(1,225)Receiv-ables

NWC change over the last 3 monthsmEUR

NWC change over the last 12 monthsmEUR

• Improvement driven by prepayments, and tradepayables mainly offset by higher inventory

Key highlights:

• Net working capital increased by EUR 172m in Q3, due to higher activity levels

• Development mainly driven by timing of receivablesand trade payables

Key highlights:

Third quarter 2017 (Public)

0

1

2

3

4

5

6

Dec 2014

Dec 2013

Dec 2015

Dec 2010

Dec 2012

Dec 2011

Dec 2016

Dec 2009

Sep 2017

17

Warranty provisions and Lost Production FactorWarranty consumption and LPF continue at a low level

9 November, 2017

4135

100

52 54

36232627

41

Q32017

Q42016

Q32016

Q22017

Q12017

Provisions made

Provisions consumed

Lost Production Factor (LPF)Percent

Warranty provisions made and consumedmEUR

• Warranty consumption increased, in line with past provisions made

• Warranty provisions made correlates with revenue in the quarter, corresponding to under 2 percent in Q3 2017

Key highlights:

• LPF continues at a low level – below 2.0

• LPF measures potential energy production not captured by Vestas’ wind turbines

Key highlights:

Third quarter 2017 (Public)

18

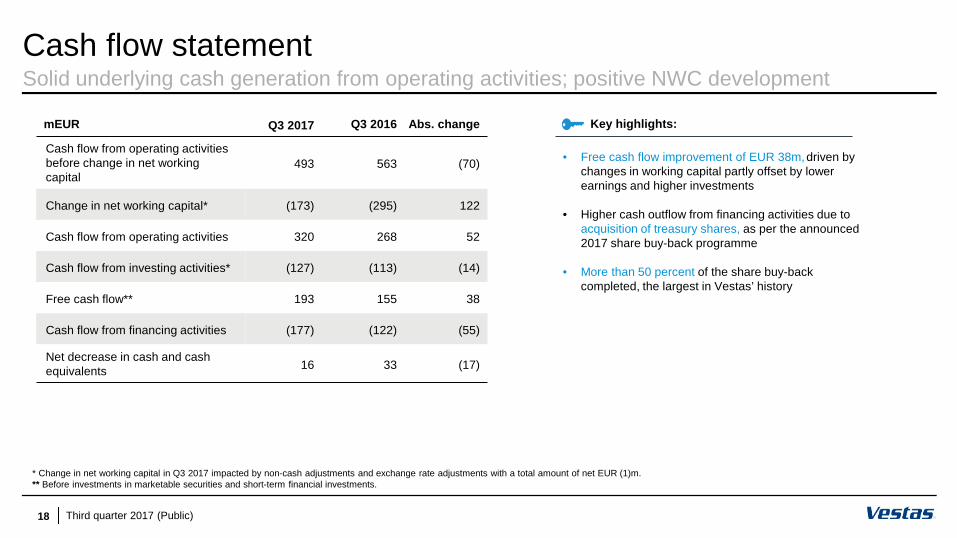

Cash flow statementSolid underlying cash generation from operating activities; positive NWC development

mEUR Q3 2017 Q3 2016 Abs. change

Cash flow from operating activities before change in net working capital

493 563 (70)

Change in net working capital* (173) (295) 122

Cash flow from operating activities 320 268 52

Cash flow from investing activities* (127) (113) (14)

Free cash flow** 193 155 38

Cash flow from financing activities (177) (122) (55)

Net decrease in cash and cash equivalents 16 33 (17)

9 November, 2017

• Free cash flow improvement of EUR 38m, driven by changes in working capital partly offset by lower earnings and higher investments

• Higher cash outflow from financing activities due to acquisition of treasury shares, as per the announced 2017 share buy-back programme

• More than 50 percent of the share buy-back completed, the largest in Vestas’ history

* Change in net working capital in Q3 2017 impacted by non-cash adjustments and exchange rate adjustments with a total amount of net EUR (1)m.** Before investments in marketable securities and short-term financial investments.

Key highlights:

Third quarter 2017 (Public)

19

Total investmentsTotal investments in line with expectations

9 November, 2017

226

127116

91 87

22

+14

(99)

Q32016

(12)

Q22017

Q42016

Q12017

113

Q32017

Other acquisitions and divestments Cash flow from investing activities

Total investments*mEUR

Key highlights:

• Investments increased by EUR 14m compared to Q3 2016, primarily driven by tangible blade investments

* Before investments in marketable securities and short-term financial investments.

Third quarter 2017 (Public)

20

Capital structureNet debt to EBITDA well below threshold; solvency ratio declined due to share buy-back

9 November, 2017

(1.5)(1.8)

Q32016

Q42016

(1.2)

Q22017

(1.4) (1.5)

Q12017

Q32017

<1.0

Net debt to EBITDA, financial target

Net debt to EBITDA, last 12 months

28

30

32

34

36

30.0

35.0

Q32016

32.130.8

29.9

Q12017

Q42016

Q22017

32.232.9

Q32017

Solvency ratio, financial target range

Solvency ratio

Solvency ratioPercent

Net debt to EBITDAxEBITDA

• Net debt to EBITDA remains at low level of (1.5) in Q3 2017

Key highlights:

• Solvency ratio of 29.9 percent in Q3 2017

• Decrease driven by share buy-back programme

Key highlights:

Third quarter 2017 (Public)

21

Return on invested capitalROIC at very high level of 452.5 percent

9 November, 2017

0

50

100

150

200

250

300

350

400

450

500

353.3

Q12017

Q22017

400.8

265.2

Q42016

Q32016

162.5

452.5

Q32017

ROIC, last 12 months

• ROIC increased to 452.5 percent in Q3 2017, an improvement of 290 percentage points compared to Q3 2016

• Development primarily driven by lower net invested capital due to working capital elements

Return on invested capital (ROIC)Percent

Key highlights:

Third quarter 2017 (Public)

9 November, 201722 Third quarter 2017 (Public)

Agenda

9 November, 201722

1. Orders and markets

2. Financials

3. Outlook and questions & answers

Interim financial report,Third quarter 2017

Q3

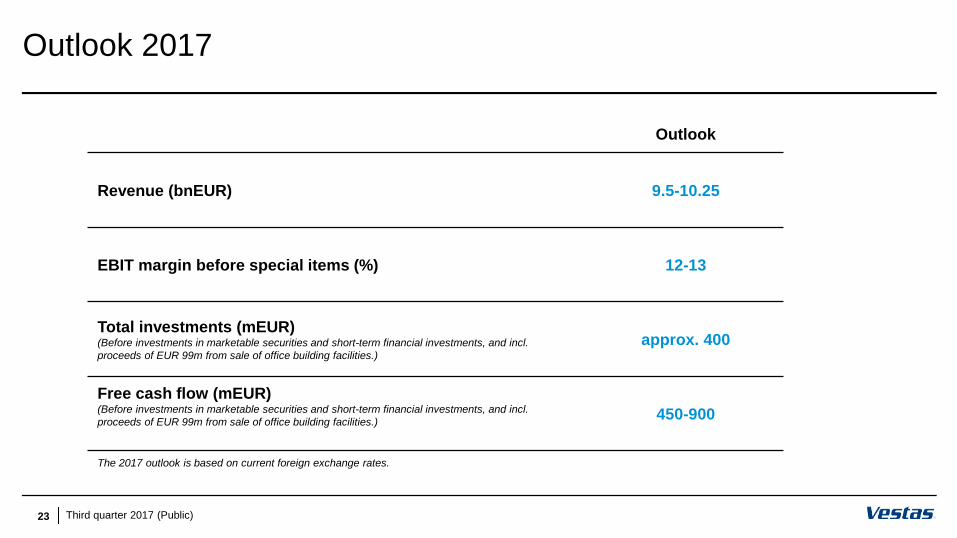

Outlook 2017

9 November, 201723

Outlook

Revenue (bnEUR) 9.5-10.25

EBIT margin before special items (%) 12-13

Total investments (mEUR)(Before investments in marketable securities and short-term financial investments, and incl. proceeds of EUR 99m from sale of office building facilities.)

approx. 400

Free cash flow (mEUR)(Before investments in marketable securities and short-term financial investments, and incl. proceeds of EUR 99m from sale of office building facilities.) 450-900

The 2017 outlook is based on current foreign exchange rates.

Third quarter 2017 (Public)

9 November, 201724

Q&AFinancial calendar 2018:

• Disclosure of annual report 2017 and outlook for 2018 (7 February)

• Annual General Meeting in Aarhus (3 April)

• Disclosure of Q1 2018 (4 May)

• Disclosure of Q2 2018 (15 August)

• Disclosure of Q3 2018 (7 November)

Third quarter 2017 (Public)

Thank you for your attention

Copyright NoticeThe documents are created by Vestas Wind Systems A/S and contain copyrighted material, trademarks, and other proprietary information. All rights reserved. No part of the documents may be reproduced or copied in any form or by anymeans - such as graphic, electronic, or mechanical, including photocopying, taping, or information storage and retrieval systems without the prior written permission of Vestas Wind Systems A/S. The use of these documents by you, oranyone else authorized by you, is prohibited unless specifically permitted by Vestas Wind Systems A/S. You may not alter or remove any trademark, copyright or other notice from the documents. The documents are provided “as is” andVestas Wind Systems A/S shall not have any responsibility or liability whatsoever for the results of use of the documents by you.