Embed Size (px)

Citation preview

Growth and Activity Diversification: the impact of financing non-traditional local activities

Thiago Christiano Silva and Benjamin Miranda Tabak

August 2019

498

ISSN 1518-3548 CGC 00.038.166/0001-05

Working Paper Series Brasília n. 498 August 2019 p. 1-64

Working Paper Series

Edited by Research Department (Depep) – E-mail: [email protected]

Editor: Francisco Marcos Rodrigues Figueiredo – E-mail: [email protected]

Co-editor: José Valentim Machado Vicente – E-mail: [email protected]

Head of Research Department: André Minella – E-mail: [email protected]

The Banco Central do Brasil Working Papers are all evaluated in double blind referee process.

Reproduction is permitted only if source is stated as follows: Working Paper n. 498.

Authorized by Carlos Viana de Carvalho, Deputy Governor for Economic Policy.

General Control of Publications

Banco Central do Brasil

Comun/Divip

SBS – Quadra 3 – Bloco B – Edifício-Sede – 2º subsolo

Caixa Postal 8.670

70074-900 Brasília – DF – Brazil

Phones: +55 (61) 3414-3710 and 3414-3565

Fax: +55 (61) 3414-1898

E-mail: [email protected]

The views expressed in this work are those of the authors and do not necessarily reflect those of the Banco Central or

its members.

Although these Working Papers often represent preliminary work, citation of source is required when used or reproduced.

As opiniões expressas neste trabalho são exclusivamente do(s) autor(es) e não refletem, necessariamente, a visão do Banco

Central do Brasil.

Ainda que este artigo represente trabalho preliminar, é requerida a citação da fonte, mesmo quando reproduzido parcialmente.

Citizen Service Division

Banco Central do Brasil

Deati/Diate

SBS – Quadra 3 – Bloco B – Edifício-Sede – 2º subsolo

70074-900 Brasília – DF – Brazil

Toll Free: 0800 9792345

Fax: +55 (61) 3414-2553

Internet: http//www.bcb.gov.br/?CONTACTUS

Non-Technical Summary

We study how financing non-traditional local activities, conceived here as a proxy for localactivity diversification, associates with economic growth. We use municipality-level datafrom Brazil, a country that provides an ideal experimental setup due to the large geographical,social, and economic disparities observed across its more than 5,500 cities.

Municipalities specialize in agricultural, industrial or service activities. We assume that thetraditional activity of a municipality is the one that contributes the most to its local GDP.The remainder sectors—those contributing less to the local GDP—are considered as non-traditional. Our proxy for finance to non-traditional local activities computes the share ofbank credit that is channeled to non-traditional sectors.

According to David Ricardo’s theory, countries should specialize in activities in which theyenjoy comparative advantage. From a cities viewpoint, if cities have different specializations—precisely their traditional local activities—then funding less important non-traditional sectorscould reduce their potential for development, which could otherwise be reached in case fund-ing were channeled to those activities with comparative advantage. In line with this theory, weshould expect a negative association between funding non-traditional local activities—whichcould promote activity diversification (less specialization)—and economic growth.

Using Brazilian data, our empirical exercises point to the opposite: funding non-traditionallocal activities associates with higher economic growth rates. Our finding can be relatedto several factors. First, non-traditional local sectors may be more profitable and thereforetheir funding is beneficial to growth. This could be due to a less competitive environmentor because some sectors experience decreasing returns of scale. Second, we could argue thatpromoting activity diversification can lead to a synergistic effect of these new activities andthe traditional local activity, making the city more attractive to new firms and households.

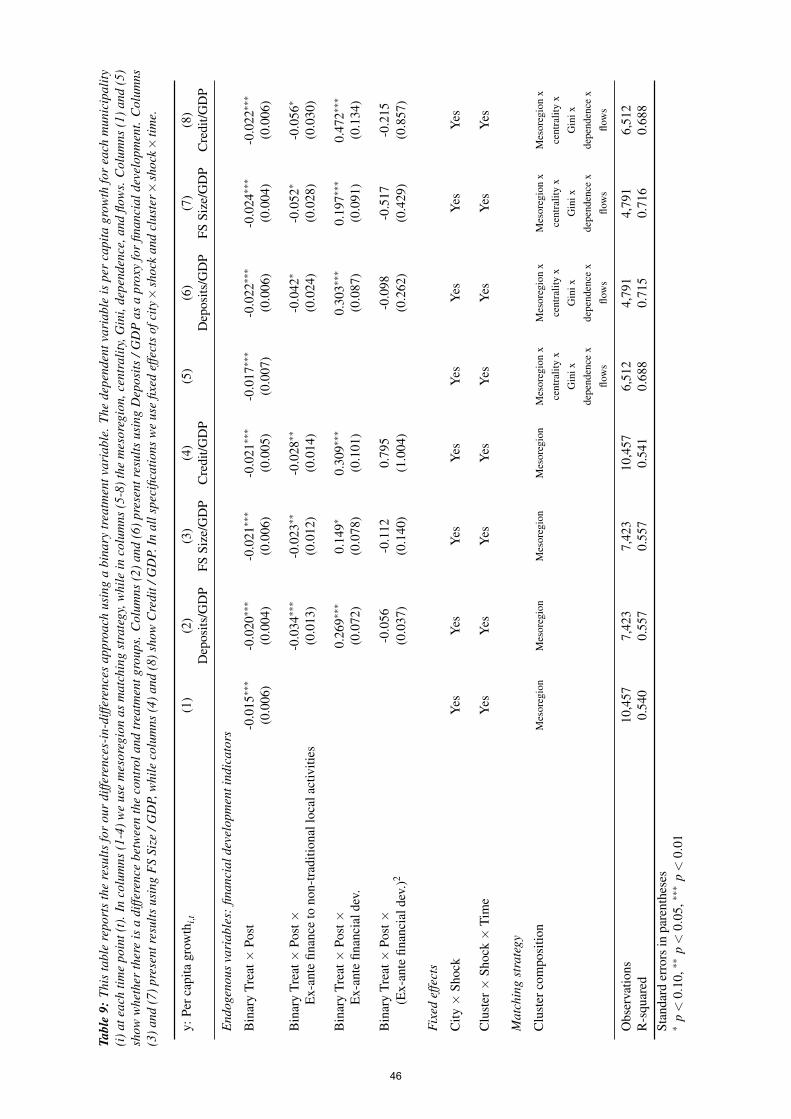

We show that funding non-traditional local activities associates with higher growth only inmoments of normality. We use natural disasters to test how financial development and fi-nancing non-traditional activities associate with economic growth in times of distress. Inadverse scenarios, we show that funding non-traditional local activities correlates negativelywith growth. That is, the focus on leveraging the comparative advantages seems to be morerelevant to achieve greater growth in times of distress.

3

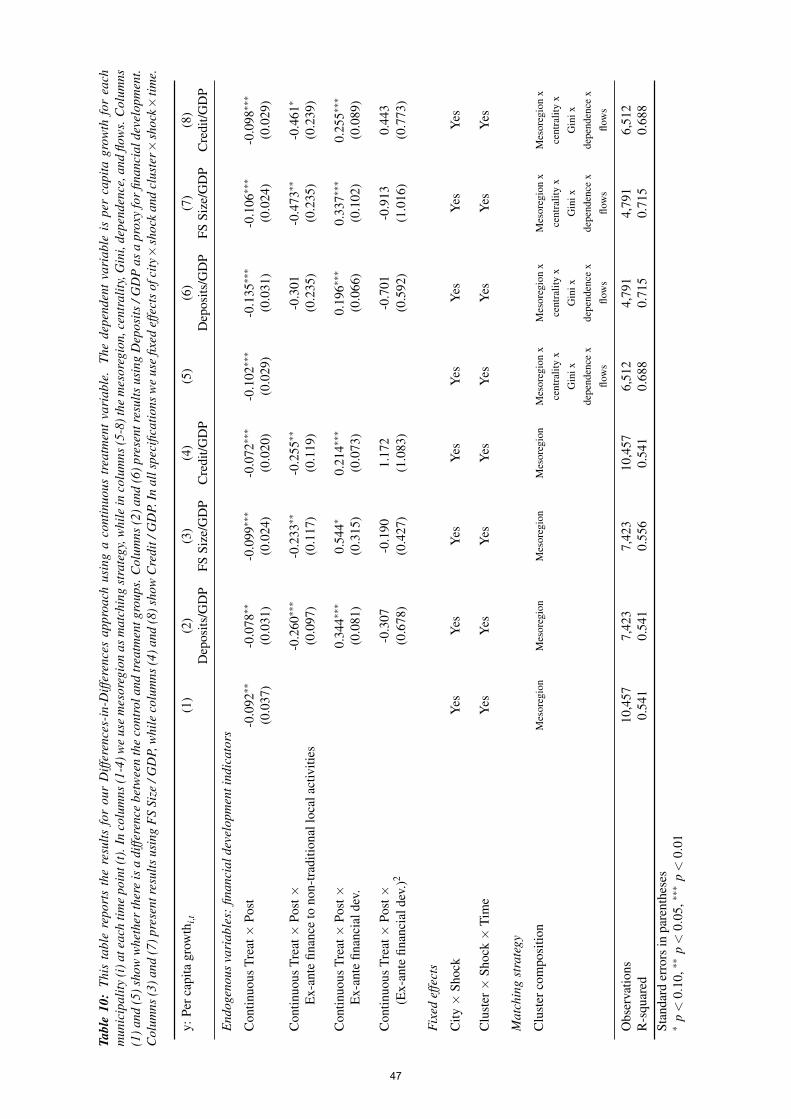

Sumario Nao Tecnico

O trabalho investiga como o financiamento a atividades locais nao tradicionais nas cidades,concebidas aqui como uma proxy para a diversificacao de atividades locais, associa-se aocrescimento economico. Usam-se dados em nıvel municipal do Brasil, um paıs que forneceuma configuracao experimental ideal devido as grandes disparidades geograficas, sociais eeconomicas observadas em suas mais de 5.500 cidades.

Municıpios especializam-se em atividades agrıcolas, industriais ou de servicos. Assume-seque a atividade tradicional de um municıpio e aquela que mais contribui para o seu PIB. Ossetores restantes—aqueles que contribuem menos para o PIB local—sao considerados naotradicionais. A proxy para financiamento de atividades locais nao tradicionais e dada pelaparcela de credito bancario que e canalizada para setores nao tradicionais relativamente atodo credito bancario no municıpio.

Segundo a teoria de David Ricardo, os paıses deveriam se especializar em atividades nasquais eles desfrutam de vantagem comparativa. Do ponto de vista das cidades, se as cidadestiverem especializacoes diferentes—precisamente suas atividades locais tradicionais—, entaofinanciar setores nao tradicionais menos importantes poderia reduzir seu potencial de desen-volvimento, que poderia ser alcancado caso o financiamento bancario fosse canalizado paraaquelas atividades com vantagem comparativa. De acordo com essa teoria, deveria-se esperaruma associacao negativa entre o financiamento de atividades locais nao tradicionais—que pro-movem a diversificacao de atividades (menor especializacao)—e o crescimento economico.

Usando dados brasileiros, nossos exercıcios empıricos apontam para o oposto: o financia-mento de atividades locais nao tradicionais esta associado a taxas de crescimento economicomais altas. Este resultado pode estar relacionado a varios fatores. Primeiro, setores locaisnao tradicionais podem ser mais lucrativos e, portanto, seu financiamento e benefico para ocrescimento. Isso pode ser devido a existencia de um ambiente menos competitivo ou porquealguns setores possuem retornos decrescentes de escala. Segundo, poderia-se argumentar quea promocao da diversificacao de atividades leva a um efeito sinergico delas com a atividadelocal tradicional, tornando a cidade mais atraente para novas empresas e famılias.

Mostra-se tambem que o financiamento de atividades locais nao tradicionais associa-se a ummaior crescimento apenas em momentos de normalidade. Usando desastres naturais, testa-secomo desenvolvimento financeiro e o financiamento a atividades nao tradicionais se associamcom crescimento economico em tempos de estresse. Durante cenarios adversos, financiaratividades locais nao tradicionais se correlaciona de forma negativa com crescimento. Ouseja, o foco em alavancar as vantagens comparativas parece ser mais relevante para alcancarum maior crescimento em tempos de estresse.

4

Growth and Activity Diversification:the impact of financing non-traditional local activities

Thiago Christiano Silva*

Benjamin Miranda Tabak**

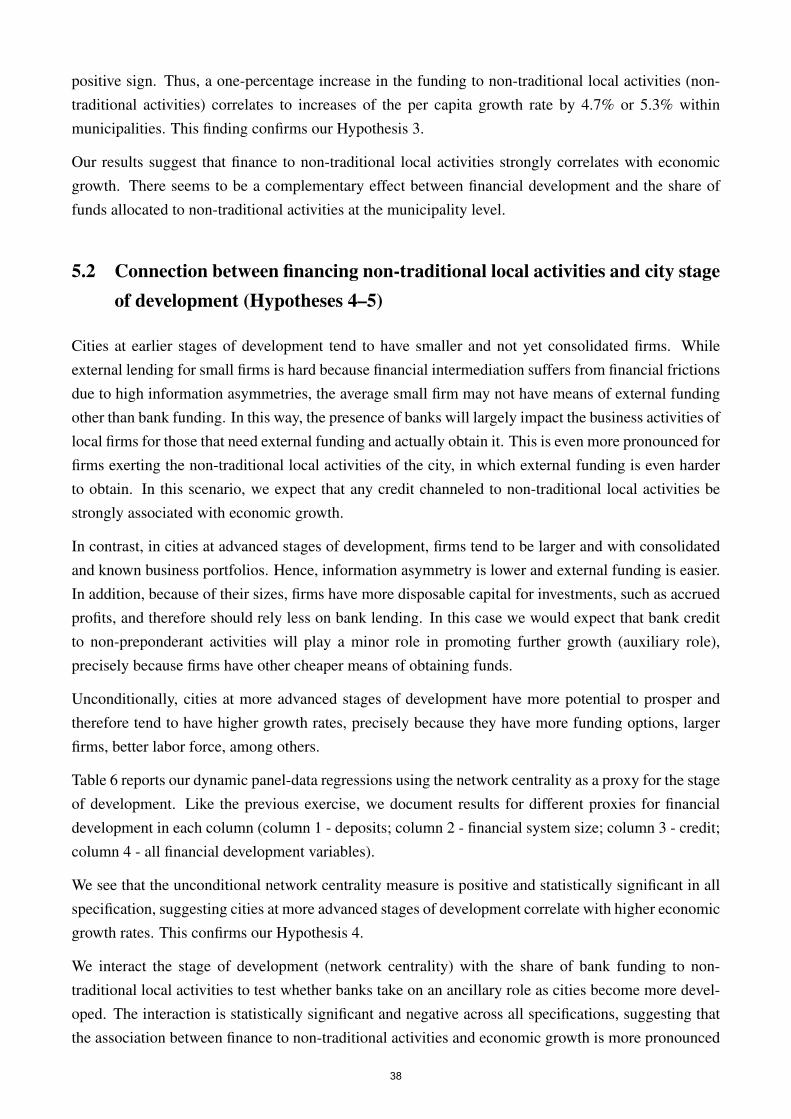

AbstractWe study how financing non-traditional local activities, conceived here as a proxy for activity diver-sification, associates with economic growth. We use municipality-level data from Brazil, a countrythat provides an ideal experimental setup due to the large geographical, social, and economic dis-parities observed across its more than 5,500 cities. We find that financing non-traditional localactivities matters to cities development and such association is stronger at their earlier stages of de-velopment. We use the centrality in the network of intercity economic flows as a proxy for the mu-nicipality stage of development. The centrality encodes the overall importance of the city in termsof economic intermediation to the entire network structure of business activities. The network isconstructed using every observed intercity wire transfers registered in the Brazilian Payments Sys-tem. Cities more nearby (geographic closeness) and that transact more (economic closeness) withadvanced centers have higher growth rates, suggesting the existence of positive spillovers. Eco-nomic spillovers are more critical than geographic spillovers for growth. Using natural disastersas sources of unexpected negative events, we also find that the inverted U-shaped association offinancial development variables with growth commonly documented in the finance-growth liter-ature breaks down. In addition, the association between financing non-traditional local activitiesand economic growth becomes negative in times of distress. Our results suggest that cities shouldrestrengthen their traditional activities when adverse conditions befall.

Keywords: activity diversification, finance-growth nexus, spillovers, financial intermediation, tradenetworks, payments networks.JEL Classification: O47, G32, G21, F15, F18, C10.

The Working Papers should not be reported as representing the views of the Banco Central doBrasil. The views expressed in the papers are those of the authors and do not necessarily reflectthose of the Banco Central do Brasil.

*Research Department, Banco Central do Brasil, e-mail: [email protected].**FGV/EPPG Escola de Polıticas Publicas e Governo, Fundacao Getulio Vargas (School of Public Policy and Govern-

ment, Getulio Vargas Foundation), e-mail: [email protected].

5

1 Introduction

In a seminal paper, King and Levine (1993) show that financial development positively impacts eco-nomic growth using a cross-country study.1 A new strand of the finance-growth literature argues thatsuch relationship lasts up to a point, above which the marginal benefits of financial development oneconomic growth start to decrease and can even become predatory.2

The finance-growth literature constructs proxies for financial development at the aggregate level whenexplaining local economic growth. Some few exceptions study the relationship between growth andfinancial development using bank credit operations from the creditor perspective.3 In contrast, thispaper looks at the borrower side of the credit relationship. We analyze how borrowers’ activities relateto the city traditional and non-traditional activities and whether they impact local economic growth indifferent ways. Thus, this paper documents the role of lending diversification in economic growth.

We show that the distribution of who gets the credit (borrowers) matters for economic growth. Accord-ing to David Ricardo’s theory, countries should specialize in activities in which they enjoy comparativeadvantage. From a cities viewpoint, if cities have different specializations—precisely their traditionallocal activities—then funding less important non-traditional sectors could reduce their potential for de-velopment, which would otherwise be reached in case funding were channeled to those activities withcomparative advantage.

Therefore, according to the Ricardian theory, we should expect a negative association between fundingnon-traditional local activities—which could promote activity diversification (less specialization)—and economic growth. Using a rich data set with all municipalities in Brazil, we show the opposite:funding non-traditional local activities associates with higher economic growth rates.4

Our finding can be related to several factors. First, non-traditional local sectors may be more profitableand therefore their funding is beneficial to growth. This could be due to a less competitive environmentor because some sectors experience decreasing returns of scale.5 Second, we could argue that promot-

1Since then, the literature has provided several empirical findings that corroborate this positive relationship. For in-stance, Jayaratne and Strahan (1996) document that financial markets can directly affect economic growth by studying therelaxation of bank branch restrictions in the United States. See also Levine and Zervos (1998), Rajan and Zingales (1998),Beck et al. (2000), Beck and Levine (2004), Levine (2005), Soedarmono et al. (2017), Beck et al. (2014a), and Beck et al.(2015).

2Law and Singh (2014), Rioja and Valev (2004), Samargandi et al. (2015), Soedarmono et al. (2017), and Abedifaret al. (2016) explore this non-linear dependency.

3For example, Abedifar et al. (2016) and Andersson et al. (2016) evaluate the contribution of public or private banks tolocal economic growth.

4We take Brazil as a case study due to several reasons. First, Brazil is a relevant emerging market country that ex-perienced a tremendous credit growth in the mid-2000s. Despite such strong credit growth, the pace of economic growthhas been somewhat lower and therefore the link between bank credit and growth is important to be explored. Second, thestructure of the economy is also bank-oriented. In this way, bank credit ends up being the only source of external fundingfor the average firm. Therefore, the study of the relevance of banks to economic growth of Brazilian cities is amplified.Third, Brazil has a large geographical territory with significant demographic, social and economic disparities observedacross its more than 5,500 existent cities. This setup provides a large cross-sectional and temporal heterogeneity to checkour empirical hypotheses.

5Imagine a city specialized in agriculture and industrial activities, but with no services facilities. The introduction ofa services facilities could make a bigger difference than the introduction of a new factory or a new farm. In the former,returns are much higher due to the low actual levels of services provided by the city.

6

ing activity diversification can lead to a synergistic effect of these new activities and the traditionallocal activity.6

We use natural disasters as sources of exogenous distress to measure whether the positive associationbetween activity diversification and economic growth still holds in times of distress. In these adversescenarios, we show that the correlation between funding non-traditional local activities and growthbecomes negative. That is, the focus on leveraging—or even restoring—the comparative advantagesseems to be more relevant to achieve greater growth in times of distress.

Economic growth not only depends on local characteristics of cities, but also on other city counterpartsto which they connect. Interconnections between two cities can arise due to geographical proximityand also to economic relationships, regardless of distances. While we find that the existence of bothtypes of interconnections correlates with higher economic growth—suggesting the existence of positivespillovers due to city integration—economic relationships associate with growth more strongly thangeographical proximity. This effect may be due to the large dimensions of Brazil and to the greatdistances between cities.

These results are relevant for thinking about the development of public policies seeking to create con-ditions for different regions of the country to develop. Infrastructure investments that allow citiesto increase trade flows between them should have positive effects on the cities benefiting from theseinvestments.

To the best of our knowledge, this is the first paper that shows evidence that trade connections andgeography matter for the relationship between financial development and economic growth, as well asdocumenting their relative importance to growth. Our results open a new avenue for further researchon the effect of distinct public policies on economic growth, and on the relationship between financialdevelopment and economic growth for other countries.

Municipalities specialize in agricultural, industrial or service activities. We assume that the traditionalactivity of a municipality is the one that contributes the most to its local GDP. The remainder sectors—those contributing less to the local GDP—are considered as non-traditional.7 Our proxy for finance tonon-traditional local activities computes the share of bank credit that is channeled to non-traditionalsectors.

We use loan-level data from the Brazilian Credit Risk Register (SCR) to identify how banks channelcredit to firms within cities. We then merge this loan-level data set with city-level data from theBrazilian Institute of Geography and Statistics (IBGE) and with firm-level data from the BrazilianInternal Revenue Service (IRS) to classify borrower’s activity as traditional or non-traditional within

6For instance, cities become more attractive to households and even firms when they have all services and facilities atdisposal of their residents.

7As cities develop, they naturally become complex and start performing several activities, potentially complementary toeach other. As a result, they may have more than a single traditional activity. For instance, Sao Paulo is the largest Braziliancity with similar total added values in the industry and services sectors. In this way, there is an ambiguity in defining thetraditional activity of such cities. In fact, the most complex and developed cities in Brazil often have this duality withrespect to their traditional activities. In unreported results, we also run regressions considering as the non-traditional localactivity the one that contributes the least to the local GDP, instead of all the sectors other than the one that contributes themost (baseline regressions shown in this paper). Results remain qualitatively the same.

7

the boundaries of the city where it resides. Therefore, we can track traditional and non-traditionalactivities in each municipality and evaluate how much bank financing each activity receives over time.We find a substantial heterogeneity of business specializations and degrees of finance to non-traditionallocal activities across Brazilian municipalities.

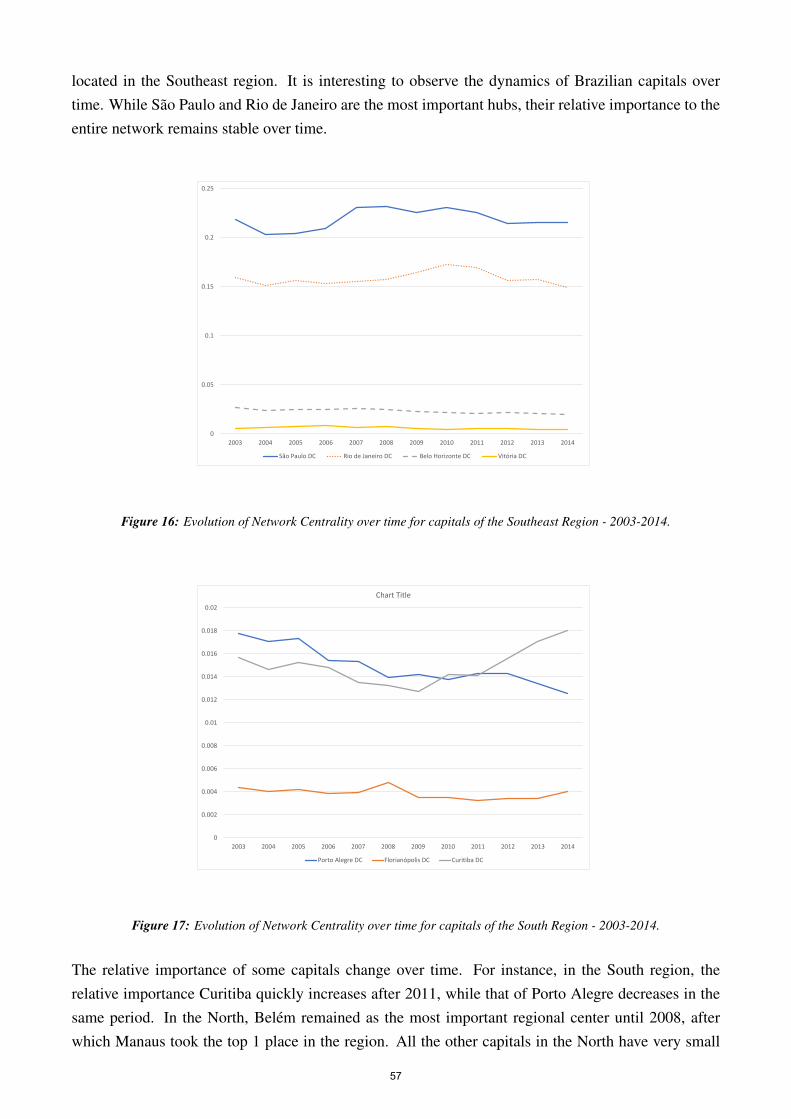

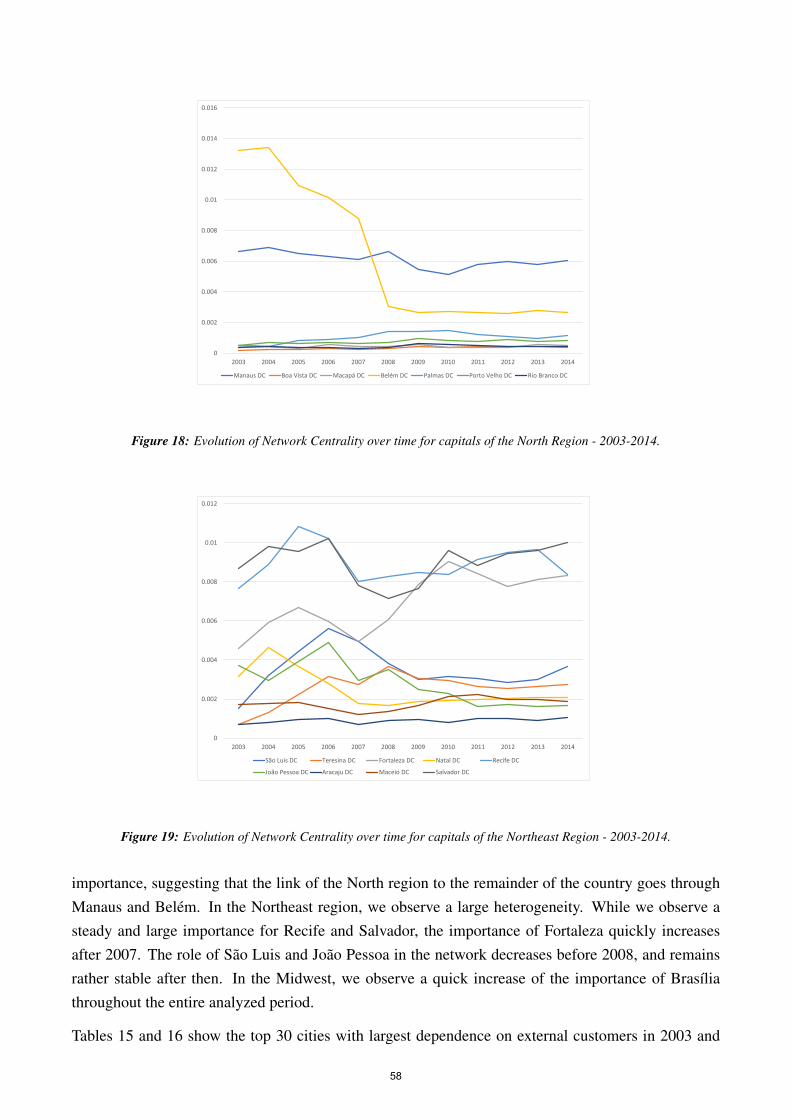

We find evidence that cities at advanced stages of development—higher network centrality—correlatewith higher rates of economic growth. We compute the city centrality using the network of intercitywire transfers built from more than 410 million business-oriented, firm-to-firm transfers in Brazil.8

We find the positive association between finance to non-traditional local activities and growth weakensas cities become more economically developed. In these municipalities, firms have other forms offunding, such as retained earnings, capital or corporate markets, and therefore rely less on bank lending.In this case, bank credit becomes ancillary to the local economy of advanced municipalities.

The paper proceeds as follows. Section 2 discusses the related literature. Section 3 presents the data.Section 4 introduces the variables and discusses the econometric methodology. Section 5 discusses theempirical results. Section 6 concludes the paper.

2 Related Literature

Our work connects to existing researches by reinforcing the classical link between financial develop-ment and economic growth (King and Levine (1993), Levine and Zervos (1998), Rajan and Zingales(1998), Beck et al. (2000), Beck and Levine (2004), Levine (2005), Soedarmono et al. (2017), Becket al. (2014a), and Beck et al. (2015)). In line with the literature, we document a positive associa-tion between financial development—proxied by deposits, credit, and financial system size—and localeconomic growth rates using municipality-level data from Brazil. Our work also reports that such mu-tualistic relationship lasts up to a point, above which it weakens and can eventually become negative.Such non-linearity and the existence of this critical point in the finance-growth nexus reinforce empir-ical evidence reported in more recent finance-growth papers using cross-country data (Law and Singh(2014), Rioja and Valev (2004), Samargandi et al. (2015), Soedarmono et al. (2017), and Abedifar et al.(2016)).

The non-linearity in the finance-growth relationship may arise for several reasons. The financial systemmay compete with the real sector for resources and may attract talented people that would be otherwiseworking in the real sector. Therefore, with lower levels of human capital, the real sector would havelower productivity and growth as a consequence (Tobin (1984)).

8The intercity trade network is a large-scale, weighted digraph. The weights are the payments and the link orientationarises from the payment flow nature (payer and receiver). By aggregating firm-to-firm to city-to-city transfers, we computethe network centrality of each municipality with the aid of the complex network theory (Silva et al. (2016a,b), Rossi et al.(2018), and El-Khatib et al. (2015)). We use the Google PageRank centrality, which is a feedback-based network measurethat depends on two components: the degree and the quality of interconnectivity. While the degree of interconnectivityrelates to the number of transactions that municipalities perform with other cities, the quality of interconnectivity pertainsto the relative importance of the peers with which cities transact. Higher centrality for a city means that it transacts a lot(degree) and with outstanding (quality) municipalities.

8

As the financial sector develops, several financial intermediaries may incur in excessive leverage, whichmay induce more significant economic fluctuations with an adverse effect on economic growth (Rajan(2006)). The incentive to take excessive risks in more developed financial systems is one of the poten-tial channels that may explain a non-linear relationship between finance and growth, dampening theeffect of financial development on growth after a certain threshold.

The development of the financial sector may increase the number of non-intermediation activities andtheir relevance to financial intermediaries. These non-traditional activities may have a smaller effecton economic growth than the traditional financial intermediation activity. Therefore, with the increasein the development of the financial sector, there may be a threshold from which financial developmenthas little or a negative effect on economic growth (Beck et al. (2014b)).

It is important to stress that most studies that relate financial development to economic growth usea cross-country sample (Rousseau and Wachtel (2002), Slesman et al. (2019) Morganti and Garofalo(2019), Herwartz and Walle (2014), and Law et al. (2013)). There are substantial differences amongcountries, suggesting that we have to evaluate the results of these studies carefully. It is difficult tocontrol for all possible distinctions among countries, such as differences in the legal framework, qualityof institutions, levels of human development, corruption, among many others. Our focused study ona single country with more granular data is useful to avoid eventual omitted variable biases that arelikely to appear in cross-country studies. Municipalities in Brazil are roughly subject to the same legalconstraints all over the country, which minimizes omitted variable issues. Such microdata also allowsstudying the relevance of the geographical distribution of financial development on economic growthwithin a country (Kendall (2012)).

The Ricardian theory on comparative advantage has some support from empirical research. It is es-tablished by now that if a country specializes in specific products or services using its comparativeadvantages, then it will have trade gains with other countries. Konstantakopoulou and Tsionas (2019)show that for the Euro area comparative advantages positively affect export specialization.9 However,the case of Brazil is that of a continental country with a large variety of comparative advantages. Inthis case, there may be gains from economic diversification. This is most true when they have comple-mentary effects that help foster production in the main traditional sector. For example, Freire (2019)shows empirical evidence that economic diversification is essential for developing countries in orderto create jobs and foster economic development.

3 Data Description

In this paper, we put together and match supervisory and public data from several sources. We analyzethe period from 2003 to 2014 in Brazil.10 This section reports how we construct, collect, and pre-

9They find reverse causality for several countries as well.10On the one hand, we cannot move the lower bound date limit because of unavailability of credit data. On the other

hand, we cannot move further the upper bound date limit because of the absence of municipality-level data on growth andtraditional business activity. Data on natural disasters and intercity and intracity payment flows do not bind the limits of theanalyzed period in neither directions.

9

process each variable used in the empirical part of the paper.

According to the IBGE, Brazil had 5,570 municipalities in 2014. In light of its vast territorial exten-sion, Brazil has five central regions: North (550 municipalities), Northeast (1,794), Midwest (467),Southeast (1,668), and South (1,191). The number of Brazilian municipalities grows until 2010, afterwhich it stagnates. Such dynamics is explained by the fact that the creation of new municipalities hadto comply with more stringent regulation after 2010, leading to a reduction of new municipalities.11

We use the SCR to keep track of ongoing credit operations of firms in Brazil.12 Information is con-fidential and comes from the Banco Central do Brasil (BCB). The data set includes the bank andclient identification (tax identifier); loan-level characteristics, such as time to maturity, overdue parcels,modality, the origin of the credit (earmarked and non-earmarked), interest rate, risk classification; andcollateral information. We use this dataset to identify the bank credit volume across municipalities inBrazil.

There are over 24 million outstanding bank credit operations channeled to firms from 2003 to 2014.We consider credit operations granted from all commercial (159 banks), investment (72), developmentbanks (5) and also credit unions (1,235) operating in Brazil. The banking sector comprises state-owned banks—which hold a substantial share of the business loans market—domestic private, andalso foreign private banks. Our sample includes business (profit-oriented) and non-profit firms, whichexert activities in the agriculture, industry, and/or services sectors.13 We have over 6.2 million firmheadquarters in our sample.

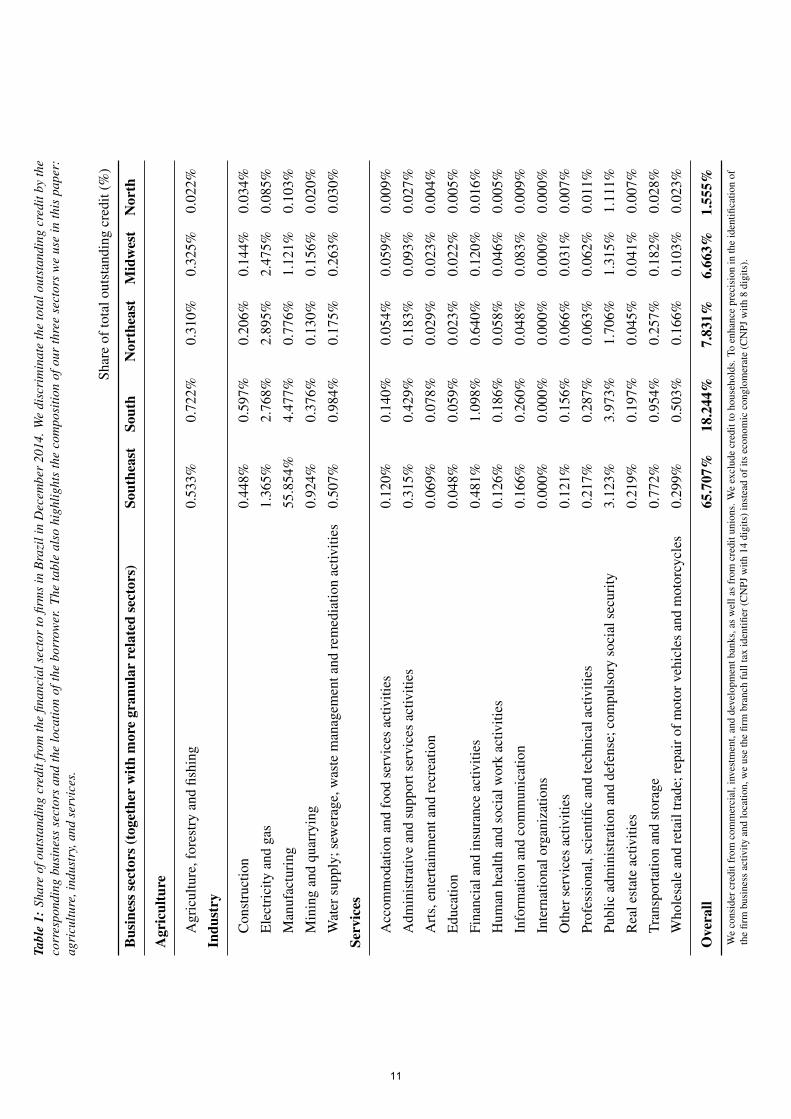

Table 1 reports the share of the total outstanding bank credit to firms in Brazil during 2014 broken downby the borrower’s location and business activity. Bank credit goes predominantly to the Southeast andSouth regions, which have the highest levels of development in Brazil. For example, the Southeastregion accounts for 65.71% of the total outstanding bank credit of the country in 2014. Less devel-oped regions, such as the North and Midwest, are responsible for only 8.22% in 2014. The relativeimportance of Brazilian regions remains stable over time.

In the Southeast region, firms in the manufacturing business sector respond with more than 50% of alloutstanding bank credit in 2014, fact that evidences the massive industrialization in the region. Creditin the South region has a higher dispersion across different sectors. Though manufacturing firms also

11The constitutional amendment (CA) 15 in 2006 made more rigorous the creation of new municipalities. Despite that,many municipalities were created after that mainly due to financial benefits that municipalities enjoy from compulsoryfederal government transfers guaranteed by the Federal Constitution. The establishment of new municipalities did not stopeven with the publication of the CA 15/2006 because such law was not auto-executory: it required further legislation to belegally enforceable. In 2008, another CA came into force and validated those municipalities created after 2006 to put anend to the uncertainty revolving around their legal status. The creation of municipalities after 2010 is facing considerablelegal uncertainty, which has been preventing the constitution of new cities. One of the main recent requirements is thatparties involved in the municipality creation have to show the economic viability of the act and the population needs to voteand confirm its creation.

12SCR is a comprehensive data set which records every single credit operation within the Brazilian financial systemworth R$200 or above. Up to June 30th, 2016, this lower limit was R$1,000. Therefore, most of the data we are assessingfollows this rule.

13We exclude credit to the public administration and extraterritorial entities with branches located in Brazil, such asforeign diplomatic representations. In this way, we focus on credit to business firms and how it affects local growth. Wefollow the same arguments when matching and filtering other datasets.

10

T abl

e1:

Shar

eof

outs

tand

ing

cred

itfr

omth

efin

anci

alse

ctor

tofir

ms

inB

razi

lin

Dec

embe

r20

14.W

edi

scri

min

ate

the

tota

lout

stan

ding

cred

itby

the

corr

espo

ndin

gbu

sine

ssse

ctor

san

dth

elo

catio

nof

the

borr

ower

.Th

eta

ble

also

high

light

sth

eco

mpo

sitio

nof

our

thre

ese

ctor

sw

eus

ein

this

pape

r:ag

ricu

lture

,ind

ustr

y,an

dse

rvic

es.

Shar

eof

tota

lout

stan

ding

cred

it(%

)

Bus

ines

s sec

tors

(tog

ethe

rw

ithm

ore

gran

ular

rela

ted

sect

ors)

Sout

heas

tSo

uth

Nor

thea

stM

idw

est

Nor

th

Agr

icul

ture

Agr

icul

ture

,for

estr

yan

dfis

hing

0.53

3%0.

722%

0.31

0%0.

325%

0.02

2%

Indu

stry

Con

stru

ctio

n0.

448%

0.59

7%0.

206%

0.14

4%0.

034%

Ele

ctri

city

and

gas

1.36

5%2.

768%

2.89

5%2.

475%

0.08

5%

Man

ufac

turi

ng55

.854

%4.

477%

0.77

6%1.

121%

0.10

3%

Min

ing

and

quar

ryin

g0.

924%

0.37

6%0.

130%

0.15

6%0.

020%

Wat

ersu

pply

;sew

erag

e,w

aste

man

agem

enta

ndre

med

iatio

nac

tiviti

es0.

507%

0.98

4%0.

175%

0.26

3%0.

030%

Serv

ices

Acc

omm

odat

ion

and

food

serv

ices

activ

ities

0.12

0%0.

140%

0.05

4%0.

059%

0.00

9%

Adm

inis

trat

ive

and

supp

orts

ervi

ces

activ

ities

0.31

5%0.

429%

0.18

3%0.

093%

0.02

7%

Art

s,en

tert

ainm

enta

ndre

crea

tion

0.06

9%0.

078%

0.02

9%0.

023%

0.00

4%

Edu

catio

n0.

048%

0.05

9%0.

023%

0.02

2%0.

005%

Fina

ncia

land

insu

ranc

eac

tiviti

es0.

481%

1.09

8%0.

640%

0.12

0%0.

016%

Hum

anhe

alth

and

soci

alw

ork

activ

ities

0.12

6%0.

186%

0.05

8%0.

046%

0.00

5%

Info

rmat

ion

and

com

mun

icat

ion

0.16

6%0.

260%

0.04

8%0.

083%

0.00

9%

Inte

rnat

iona

lorg

aniz

atio

ns0.

000%

0.00

0%0.

000%

0.00

0%0.

000%

Oth

erse

rvic

esac

tiviti

es0.

121%

0.15

6%0.

066%

0.03

1%0.

007%

Prof

essi

onal

,sci

entifi

can

dte

chni

cala

ctiv

ities

0.21

7%0.

287%

0.06

3%0.

062%

0.01

1%

Publ

icad

min

istr

atio

nan

dde

fens

e;co

mpu

lsor

yso

cial

secu

rity

3.12

3%3.

973%

1.70

6%1.

315%

1.11

1%

Rea

lest

ate

activ

ities

0.21

9%0.

197%

0.04

5%0.

041%

0.00

7%

Tran

spor

tatio

nan

dst

orag

e0.

772%

0.95

4%0.

257%

0.18

2%0.

028%

Who

lesa

lean

dre

tail

trad

e;re

pair

ofm

otor

vehi

cles

and

mot

orcy

cles

0.29

9%0.

503%

0.16

6%0.

103%

0.02

3%

Ove

rall

65.7

07%

18.2

44%

7.83

1%6.

663%

1.55

5%W

eco

nsid

ercr

edit

from

com

mer

cial

,inv

estm

ent,

and

deve

lopm

entb

anks

,as

wel

las

from

cred

itun

ions

.We

excl

ude

cred

itto

hous

ehol

ds.T

oen

hanc

epr

ecis

ion

inth

eid

entifi

catio

nof

the

firm

busi

ness

activ

ityan

dlo

catio

n,w

eus

eth

efir

mbr

anch

full

tax

iden

tifier

(CN

PJw

ith14

digi

ts)i

nste

adof

itsec

onom

icco

nglo

mer

ate

(CN

PJw

ith8

digi

ts).

11

lead in terms of bank financing, firms in the electricity and gas sector also take representative amounts,which is partly explained by the geographical water potentials in the region. The shares of credit toagriculture, forestry, and fishing are also noteworthy. The Northeast, Midwest, and North regions havea very different bank credit profile for firms. The share of bank credit to manufacturing firms is not asmuch representative. Electricity and gas firms lead the bank credit share, along with firms in the publicadministration and defense and compulsory social security sectors.

We use the Municipalities Banking Statistics (ESTBAN) to keep track of branch deposit levels and thelocal financial system size of Brazilian municipalities. Information is public and is reported by theBCB every month. Local bank branches report to ESTBAN accounting aggregates at the municipalitylevel that we use as proxies for financial development indicators.

We also use the Receita Federal dataset—the Brazilian IRS—to extract firm-level information. Thedatabase keeps track of every active and non-operating firm in Brazil. It includes data on firm taxidentification, location, age, social capital, primary business activity, legal nature, and shareholders.As of February 2018, there were more than 20 million active firms in Brazil, according to the Receita

Federal database.

We use the occurrence of natural disasters in Brazil as exogenous negative shocks to test the finance-growth nexus and the association of bank finance to non-traditional local activities in municipalitygrowth during times of distress. Information on disasters comes from the Brazilian Integration Min-istry. Table 2 reports the number of natural disasters that occurred in Brazil from 2003 to 2014. Thedata set contains climate, geological, chemical and biological, among many other hazardous events.Most natural disasters are prolonged droughts that mainly happen in the Northeast region and heavyrainfalls and alike in the North region. Cold and frosts occurrences concentrate in the South region.

Table 2: Occurrence and frequency of natural disasters in Brazil from 2003 to 2014.

Natural Disaster #Ocurrences Share Natural Disaster #Ocurrences Share

Drought 16,267 51.08% Cold 39 0.12%Flash floods 5,642 17.72% Tornadoes 34 0.11%

Flooding 3,891 12.22% Earthquakes 29 0.09%Gales 1,917 6.02% Collapse of dams 20 0.06%

Hailstorms 893 2.80% Other infestations 10 0.03%Landslides 761 2.39% Subsidence and collapses 9 0.03%

Waterloggings 629 1.98% Animal infestations 7 0.02%Wildfires 380 1.19% Low air humidity 5 0.02%

Heavy rainfalls 366 1.15% Heatwaves 4 0.01%Erosion 361 1.13% Ray storms 2 0.01%

Mass collapse of buildings 236 0.74% Tsunami 1 0.00%Transport accidents 159 0.50% Hazardous radioactivity 1 0.00%Infectious diseases 84 0.26% Storm tides 1 0.00%

Frost 53 0.17% Coastal winds 1 0.00%Hazardous chemical spills 45 0.14%

Overall 31,847 100%

We use transaction-level data from the SPB, which encompasses the Sistema de Transferencia de

Reservas (STR) and the Sistema de Transferencia de Fundos (CIP-Sitraf), to construct our firm-to-

12

firm network.14 The BCB maintains both STR and CIP-Sitraf, which are real-time gross settlementpayment systems that record electronic interbank transactions in Brazil.15 This is a high-frequency dataset that provides information on the exact time of the transaction, the identification of the payer andreceiver of the money, the purpose of the transaction,16 and the respective branches of their accounts.

The payment transfers data has about 410 million transactions with a total commercial trading value ofR$ 48 trillion among firms between January 2003 and December 2014. To get a sense of the transactedvolume, this corresponds to more than 20 times the annual nominal GDP of Brazil in 2014. Ourpayment data contains about 9 million firm local branches that transacted at least once, which is almosthalf of the total universe of firms registered at the Receita Federal database. The difference that weobserve in the data to this firm catalog is mostly due to individual microentrepreneurs, which are firmsof a single employee, the owner, that mostly offer services to the final customer and pay their inputsand receive their revenues by cash or debit cards.

We classify firms as suppliers or customers by following the direction of money transfers. Suppliersare receivers of money and therefore reside in the creditor side of the monetary transaction. Customerfirms are the payers of the money and are on the debtor side of the transaction. This identificationpermits us to navigate through the entire supply chain in Brazil. For instance, by following the chainsof the supplier to the customer, we navigate downstream in the supply chain.

Using this data set, we can construct firm-specific measures of total cash inflow and cash outflow.With this, we can evaluate the economic dependence of each supplier to each customer, and viceversa. By aggregating inflows and outflows of firms residing in the same city, we can map the entirenetwork of economic dependencies among Brazilian cities over time. Figure 1 shows an schematicof the methodology we use to transform the firm-to-firm wire transfers network into a city-to-citynetwork. We exclude payments involving transfers to the public administration institutions.17 Thisintercity network of economic dependencies will be used later to construct the network centrality ofeach municipality.

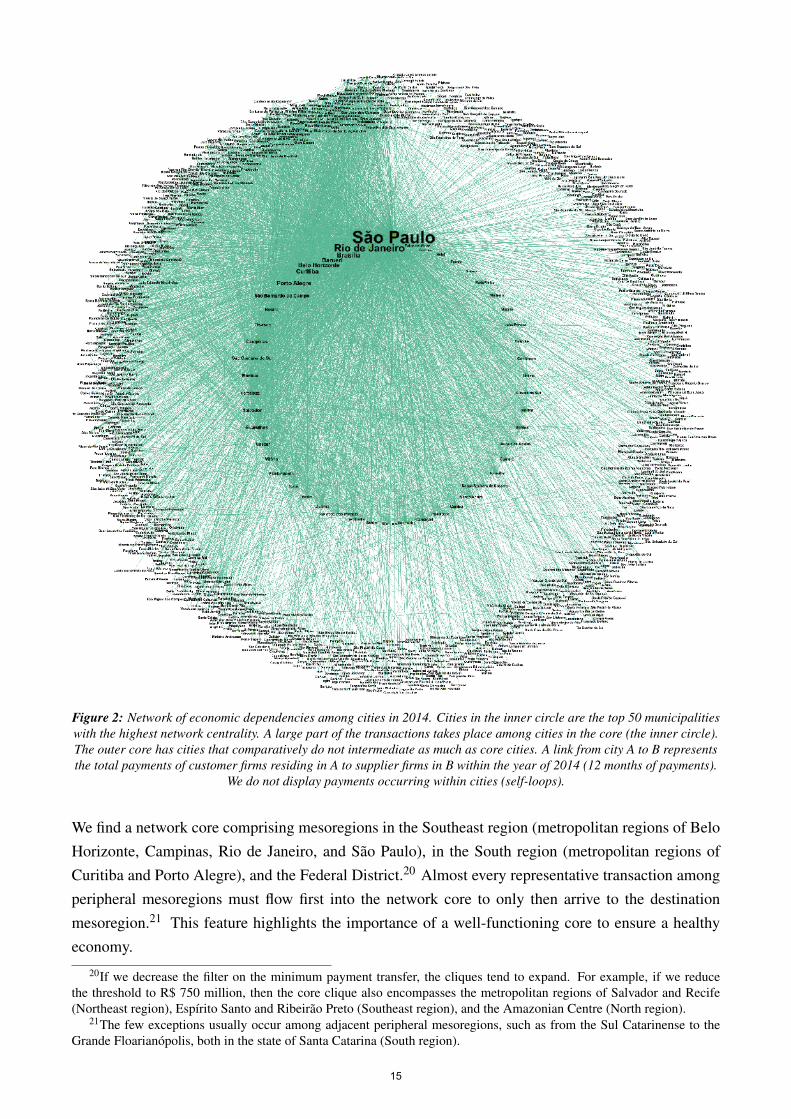

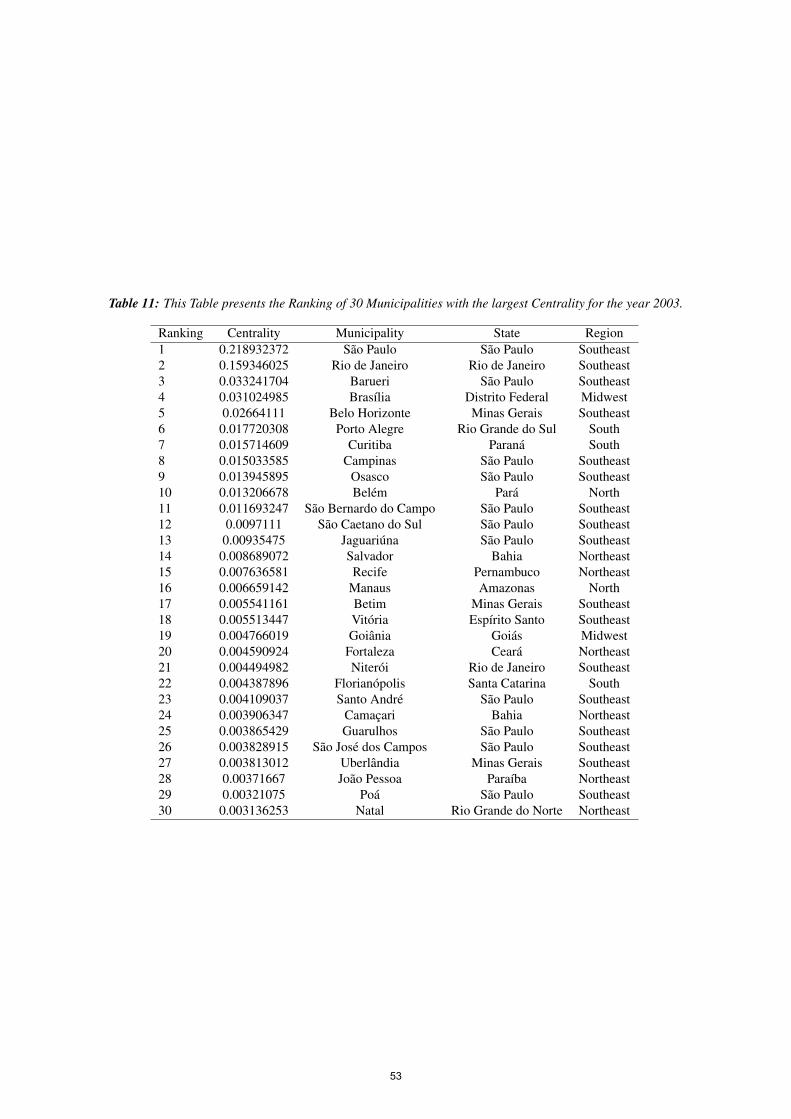

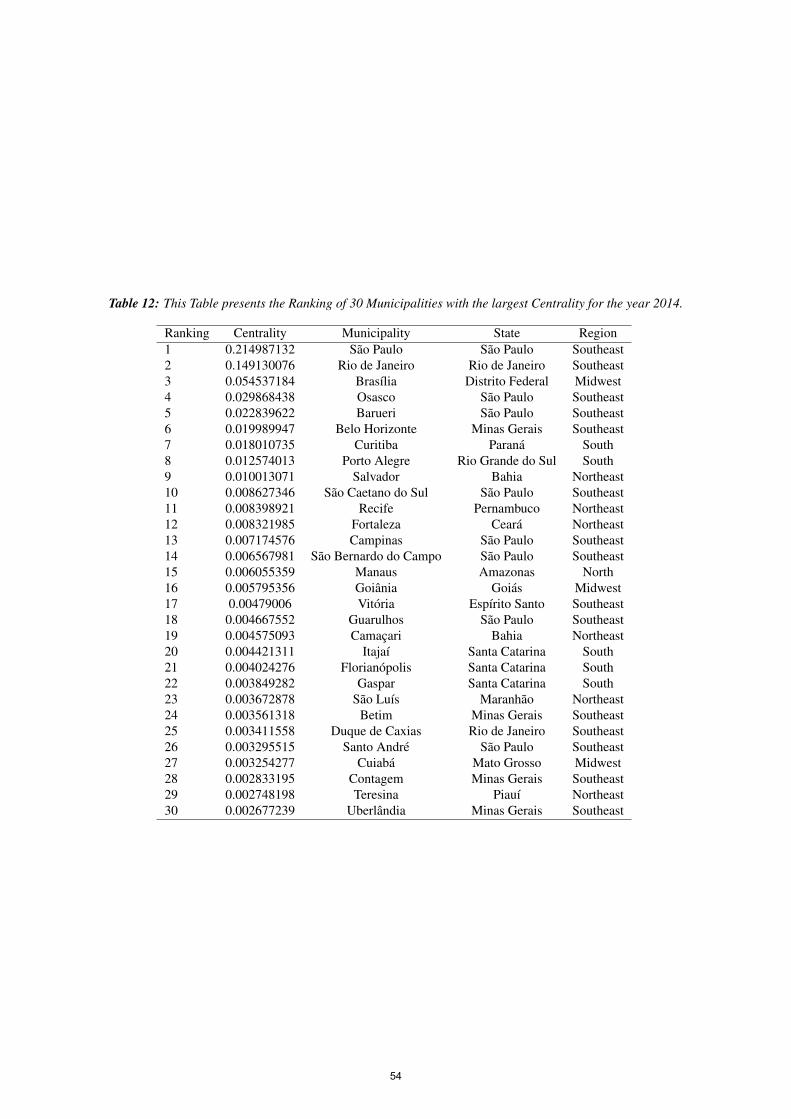

Figure 2 portrays the network of economic dependencies among cities shaped by firm-to-firm commer-cial transactions in 2014 after aggregation to the city level. Vertices are cities and a link from vertexA to B represents the total payment transfers of customer firms residing in A to supplier firms in Bwithin the year of 2014 (12 months of payments). Municipalities located in the inner circle are the 50most central cities in Brazil. On average, they receive and pay more to other cities (economic interme-diation). Label size is proportional to the city network centrality, whose computation we discuss later.

14CIP-Sitraf clears most of the transfers in Brazil. STR is used to clear high-valued transactions. In this way, CIP-Sitrafhas the largest quantity of payments, mainly of low values. STR, on the other hand, has fewer transactions but concentratethe most representative volume of monetary transfers.

15The minimum amount that a person could transact electronically was R$ 5 millions in April 2002, R$ 5 thousands inJuly 2003, R$ 3 thousands in May 2010, R$ 2 thousands in November 2012, R$ 1 thousand in March 2013, R$ 750 in July2014, R$ 500 in January 2015, R$ 250 in July 2015, and R$ 0.01 since January 2016. Transactions below the minimumamount would have to be done using cash or cheques and, therefore, would not be recorded in these systems.

16This is a self-declared field, in which the payer classifies the intent of the transaction. The field domain is very detailedand includes transfers due to salary, rent, imports, advocative hours, other professional fees, among many others.

17Excluding public institutions will avoid us considering payments of tax, public fines, or services fees as production-related transfers.

13

City 1 City 2

$600 $500

$800

Firm-to-firm economic network

City-to-city economic network

Figure 1: Schematic of the methodology to transform the firm-to-firm wire transfers network into city-to-city wiretransfers networks. For each ordered pair of cities (1, 2), we aggregate payments from customer firms (payers) in city 1

and the supplier firms (suppliers) in city 2. The edge linking 1 to 2 is the sum of these payments. If the supplier andcustomer reside in the same city, then we create a self-loop for that city.

The network centrality gives a sense of the economic importance of the city to the entire economy. Thefive most central cities in 2014 are, in this order, Sao Paulo, Rio de Janeiro, Brasılia, Barueri, and BeloHorizonte. The outer circle represents the remainder of more than 5,500 cities that do not transact asmuch as the central counterparts.

The network layout suggests a core-periphery network, as peripheral cities (outer circle), tend to trans-act more with core cities (the inner circle) than with other peripheral cities. This feature suggests thatcore cities act as hubs in the supply chain, being key players in the economic intermediation of severalbusiness sectors. We discuss the structural features of this network in Annex A using complex networktheory.

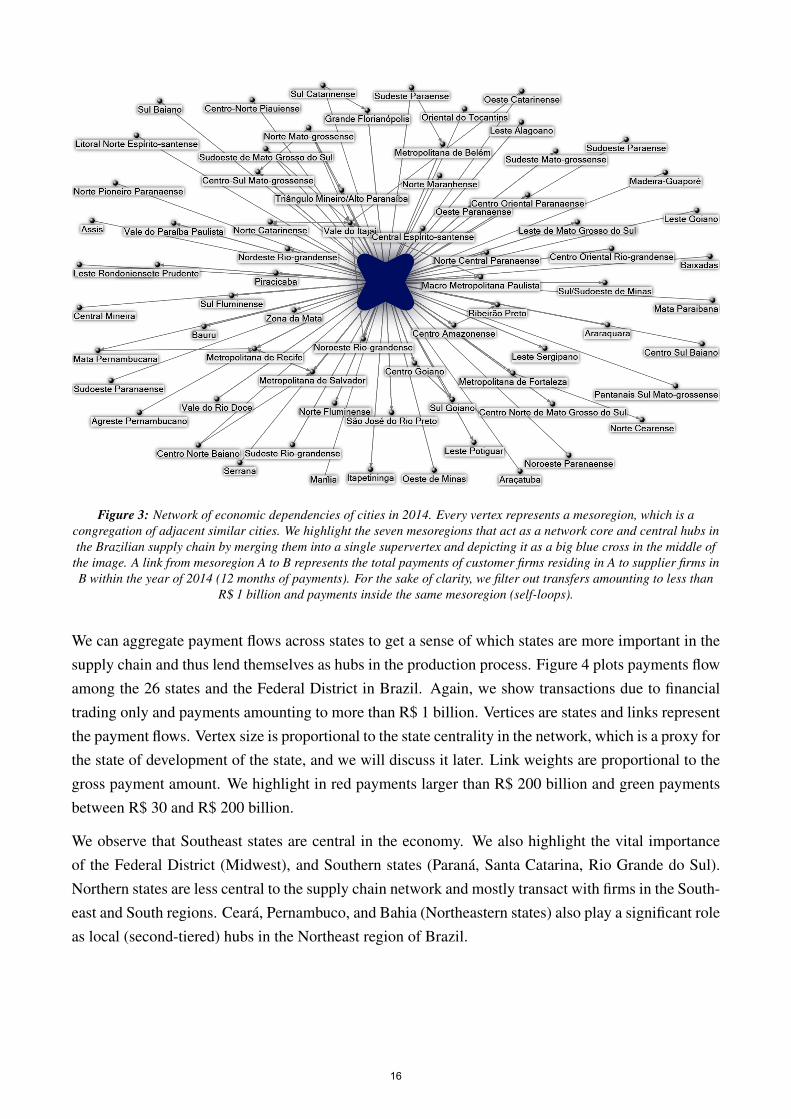

Figure 3 displays the same network of economic dependencies among cities but now grouped bymesoregions.18 Figure 3 makes clear the existence of a network core. The core comprises mesore-gions that share two properties: (i) they all strongly interconnect to each other and (ii) they close thedistance between peripheral members by intermediating economic transactions among them. To ensurethat we do not capture noise, we find cliques in the network by considering payments greater than R$1 billion only.19

18We follow the IBGE methodology to delineate the mesoregions. These are regions that congregate several municipal-ities that share economic and social similarities. They cover an agglomeration of immediate geographical regions, basedon one or more metropolises, regional capitals and/or representative urban centers.

19Network cliques are subsets of vertices that form a complete graph, i.e., a network in which every vertex has aconnection to each other. By imposing a threshold for the filter of transfers in R$ 1 billion, the existence of a clique meansthat every mesoregion transacts in both sides values greater than that threshold.

14

Figure 2: Network of economic dependencies among cities in 2014. Cities in the inner circle are the top 50 municipalitieswith the highest network centrality. A large part of the transactions takes place among cities in the core (the inner circle).The outer core has cities that comparatively do not intermediate as much as core cities. A link from city A to B representsthe total payments of customer firms residing in A to supplier firms in B within the year of 2014 (12 months of payments).

We do not display payments occurring within cities (self-loops).

We find a network core comprising mesoregions in the Southeast region (metropolitan regions of BeloHorizonte, Campinas, Rio de Janeiro, and Sao Paulo), in the South region (metropolitan regions ofCuritiba and Porto Alegre), and the Federal District.20 Almost every representative transaction amongperipheral mesoregions must flow first into the network core to only then arrive to the destinationmesoregion.21 This feature highlights the importance of a well-functioning core to ensure a healthyeconomy.

20If we decrease the filter on the minimum payment transfer, the cliques tend to expand. For example, if we reducethe threshold to R$ 750 million, then the core clique also encompasses the metropolitan regions of Salvador and Recife(Northeast region), Espırito Santo and Ribeirao Preto (Southeast region), and the Amazonian Centre (North region).

21The few exceptions usually occur among adjacent peripheral mesoregions, such as from the Sul Catarinense to theGrande Floarianopolis, both in the state of Santa Catarina (South region).

15

Figure 3: Network of economic dependencies of cities in 2014. Every vertex represents a mesoregion, which is acongregation of adjacent similar cities. We highlight the seven mesoregions that act as a network core and central hubs inthe Brazilian supply chain by merging them into a single supervertex and depicting it as a big blue cross in the middle of

the image. A link from mesoregion A to B represents the total payments of customer firms residing in A to supplier firms inB within the year of 2014 (12 months of payments). For the sake of clarity, we filter out transfers amounting to less than

R$ 1 billion and payments inside the same mesoregion (self-loops).

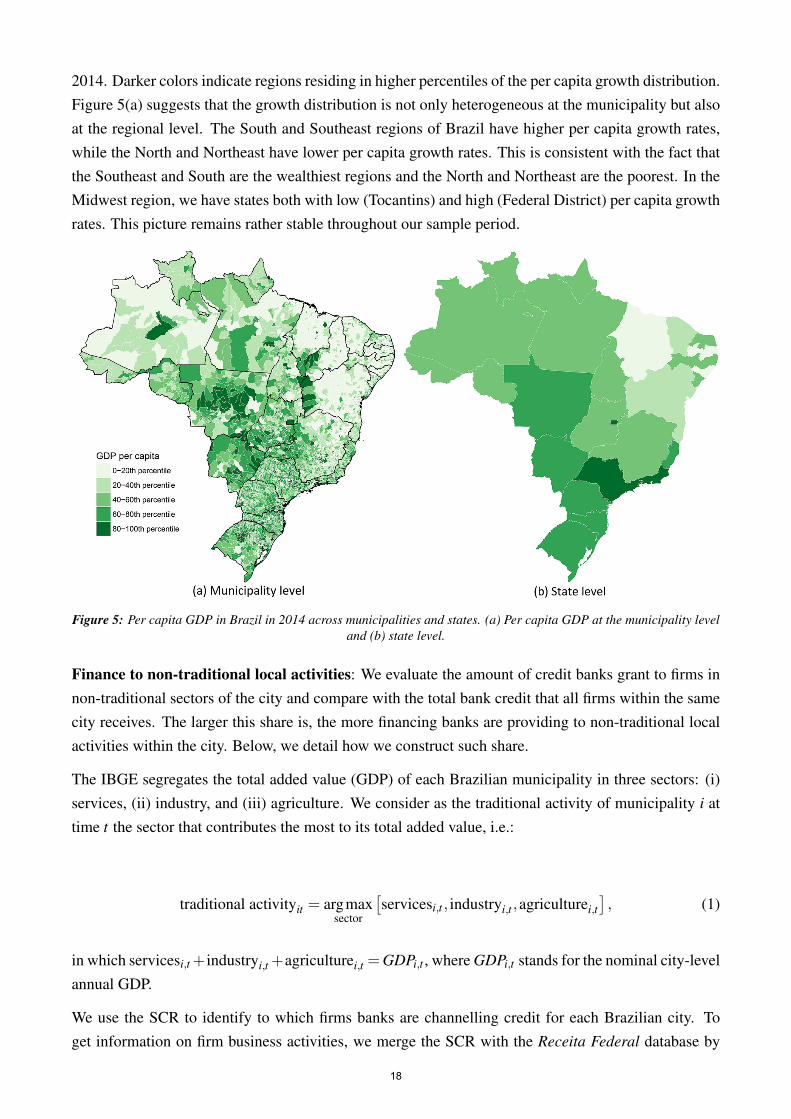

We can aggregate payment flows across states to get a sense of which states are more important in thesupply chain and thus lend themselves as hubs in the production process. Figure 4 plots payments flowamong the 26 states and the Federal District in Brazil. Again, we show transactions due to financialtrading only and payments amounting to more than R$ 1 billion. Vertices are states and links representthe payment flows. Vertex size is proportional to the state centrality in the network, which is a proxy forthe state of development of the state, and we will discuss it later. Link weights are proportional to thegross payment amount. We highlight in red payments larger than R$ 200 billion and green paymentsbetween R$ 30 and R$ 200 billion.

We observe that Southeast states are central in the economy. We also highlight the vital importanceof the Federal District (Midwest), and Southern states (Parana, Santa Catarina, Rio Grande do Sul).Northern states are less central to the supply chain network and mostly transact with firms in the South-east and South regions. Ceara, Pernambuco, and Bahia (Northeastern states) also play a significant roleas local (second-tiered) hubs in the Northeast region of Brazil.

16

Figure 4: Network of payments flows due to financial trading among Brazilian states in 2014. Each vertex is a state, anda link from state A to B represents the total gross payments from B to A within the year of 2014 (12 months of payments).Vertex shape and color indicate the state region: diamond/blue is the Southeast, square/green is the South, sphere/red is

the Midwest, square/magenta is the Northeast, and circle/brown is the North region. Vertex size portrays the statecentrality (PageRank centrality), which we will discuss later and use as a proxy for the state of development of cities. We

consider as state centrality the city with the maximum centrality. Link width symbolizes the gross payments flowingbetween states, in which red links are payment flows greater than R$ 200 billion, green are payments between R$ 30 and

200 billion, and gray are the other payments. For the sake of clarity, we do not show transfers amounting to less than R$ 1billion and within-state payments (self-loops).

4 Model Specification

This section discusses how we build our proxies for financial development, finance to non-traditionallocal activities, among others. We also formally define the empirical specifications employed in thepaper.

4.1 Description of Variables

City development, wealthiness and demographics: We use the municipality annual GDP and pop-ulation to construct the per capita growth rate for each Brazilian municipality, which serves as thedependent variable in all specifications. In addition to time-invariant idiosyncrasies of the municipalitythat may impact the per capita growth, we also control for time-variant social inequality levels and hu-man capital development using the Gini index and the Human Development Index (HDI), respectively.

Figure 5 shows a geographical map with the per capita GDP of every municipality and state in Brazil in

17

2014. Darker colors indicate regions residing in higher percentiles of the per capita growth distribution.Figure 5(a) suggests that the growth distribution is not only heterogeneous at the municipality but alsoat the regional level. The South and Southeast regions of Brazil have higher per capita growth rates,while the North and Northeast have lower per capita growth rates. This is consistent with the fact thatthe Southeast and South are the wealthiest regions and the North and Northeast are the poorest. In theMidwest region, we have states both with low (Tocantins) and high (Federal District) per capita growthrates. This picture remains rather stable throughout our sample period.

Figure 5: Per capita GDP in Brazil in 2014 across municipalities and states. (a) Per capita GDP at the municipality leveland (b) state level.

Finance to non-traditional local activities: We evaluate the amount of credit banks grant to firms innon-traditional sectors of the city and compare with the total bank credit that all firms within the samecity receives. The larger this share is, the more financing banks are providing to non-traditional localactivities within the city. Below, we detail how we construct such share.

The IBGE segregates the total added value (GDP) of each Brazilian municipality in three sectors: (i)services, (ii) industry, and (iii) agriculture. We consider as the traditional activity of municipality i attime t the sector that contributes the most to its total added value, i.e.:

traditional activityit = argmaxsector

[servicesi,t , industryi,t ,agriculturei,t

], (1)

in which servicesi,t + industryi,t +agriculturei,t =GDPi,t , where GDPi,t stands for the nominal city-levelannual GDP.

We use the SCR to identify to which firms banks are channelling credit for each Brazilian city. Toget information on firm business activities, we merge the SCR with the Receita Federal database by

18

the borrower’s tax identifier (CNPJ). We then aggregate these loan-level credit operations to city-levelcredit information over time broken down by business activities.

We then merge the city-level credit data with the IBGE by municipality code and year, so that wecan identify the traditional local activities of each city. Finally, we compute our proxy for finance tonon-traditional local activities in the municipality i at time t as:

finance to non-traditional local activitiesi,t =total crediti,t− credit to traditional activityi,t

total crediti,t,

=credit to non-traditional local activitiesi,t

total crediti,t, (2)

in which credit to traditional activityi,t is the total credit that banks grant to firms in the traditionalsector of municipality i at time t, which we identify using (1).

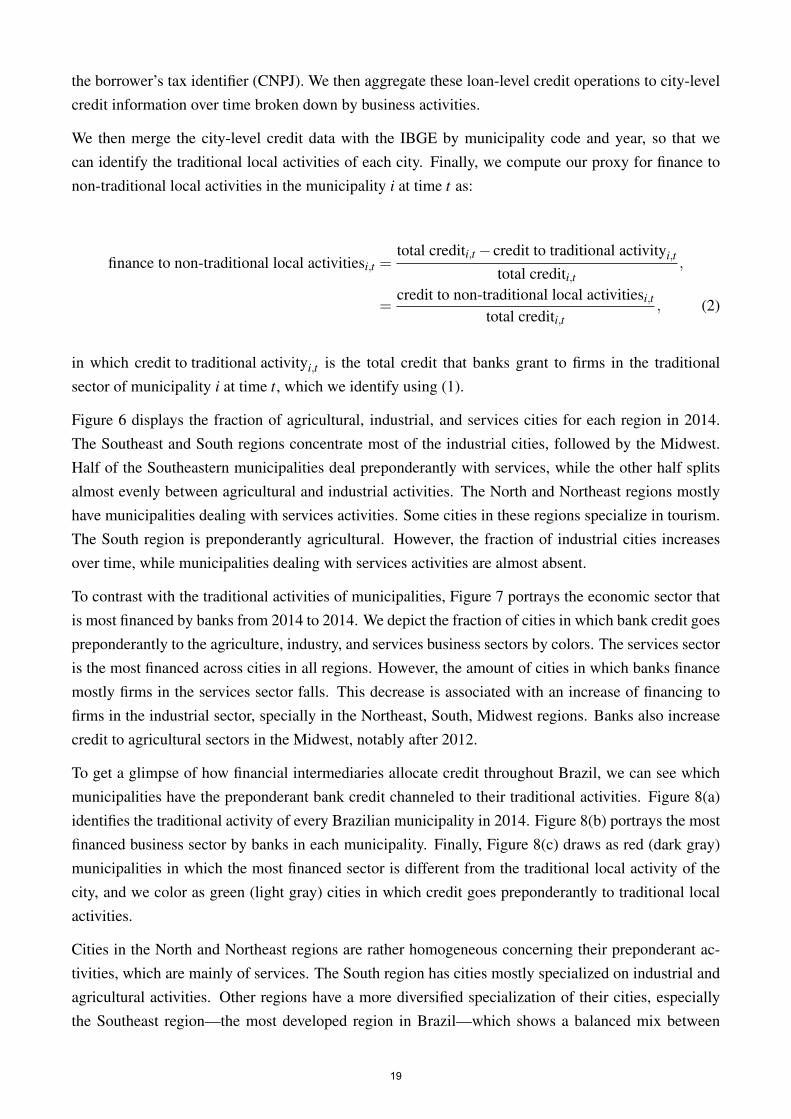

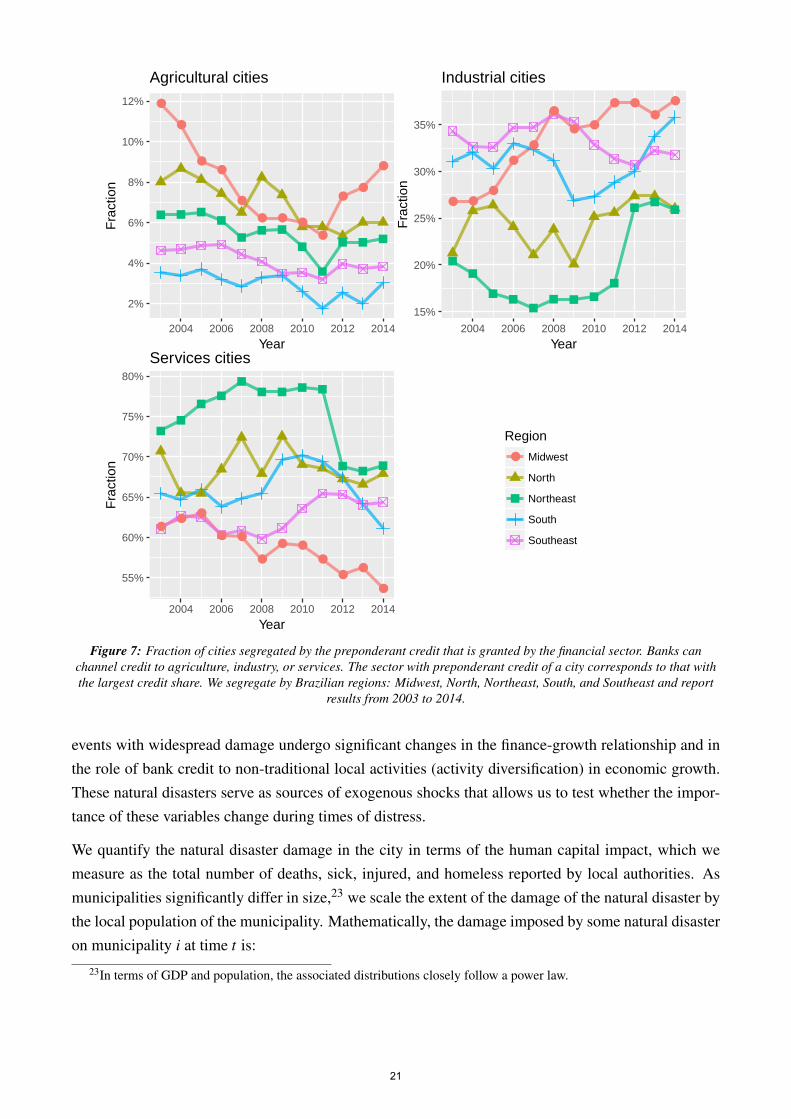

Figure 6 displays the fraction of agricultural, industrial, and services cities for each region in 2014.The Southeast and South regions concentrate most of the industrial cities, followed by the Midwest.Half of the Southeastern municipalities deal preponderantly with services, while the other half splitsalmost evenly between agricultural and industrial activities. The North and Northeast regions mostlyhave municipalities dealing with services activities. Some cities in these regions specialize in tourism.The South region is preponderantly agricultural. However, the fraction of industrial cities increasesover time, while municipalities dealing with services activities are almost absent.

To contrast with the traditional activities of municipalities, Figure 7 portrays the economic sector thatis most financed by banks from 2014 to 2014. We depict the fraction of cities in which bank credit goespreponderantly to the agriculture, industry, and services business sectors by colors. The services sectoris the most financed across cities in all regions. However, the amount of cities in which banks financemostly firms in the services sector falls. This decrease is associated with an increase of financing tofirms in the industrial sector, specially in the Northeast, South, Midwest regions. Banks also increasecredit to agricultural sectors in the Midwest, notably after 2012.

To get a glimpse of how financial intermediaries allocate credit throughout Brazil, we can see whichmunicipalities have the preponderant bank credit channeled to their traditional activities. Figure 8(a)identifies the traditional activity of every Brazilian municipality in 2014. Figure 8(b) portrays the mostfinanced business sector by banks in each municipality. Finally, Figure 8(c) draws as red (dark gray)municipalities in which the most financed sector is different from the traditional local activity of thecity, and we color as green (light gray) cities in which credit goes preponderantly to traditional localactivities.

Cities in the North and Northeast regions are rather homogeneous concerning their preponderant ac-tivities, which are mainly of services. The South region has cities mostly specialized on industrial andagricultural activities. Other regions have a more diversified specialization of their cities, especiallythe Southeast region—the most developed region in Brazil—which shows a balanced mix between

19

● ●

●

●●

● ● ●

● ● ● ●

20%

40%

60%

2004 2006 2008 2010 2012 2014

Year

Fra

ctio

n

Agricultural cities

●

● ● ●● ● ●

● ●● ● ●

5%

10%

15%

20%

25%

30%

2004 2006 2008 2010 2012 2014

Year

Fra

ctio

n

Industrial cities

● ●

●

●●

● ● ●● ● ● ●

20%

40%

60%

80%

2004 2006 2008 2010 2012 2014

Year

Fra

ctio

n

Services cities

Region

● Midwest

North

Northeast

South

Southeast

Figure 6: Fraction of cities classified by their preponderant activity. We segregate by Brazilian regions: Midwest, North,Northeast, South, and Southeast and report results from 2003 to 2014. Preponderant activity is the business sector that

contributes the most the municipal GDP.

activities oriented to the industry and services.

Figure 9 shows the geographical distribution of our proxy for finance to non-traditional local activitiesacross (a) municipalities and (b) states. Banks finance non-traditional local activities mostly in South-ern regions, notably Parana and Rio Grande do Sul, and also in the Federal District. The fraction ofmunicipalities that preponderantly receives bank credit channeled to non-traditional activities is note-worthy in Sao Paulo (Southeast region) and the Midwest. Banks seem to prefer funding traditionalactivities rather than non-traditional local activities in Northeast municipalities. Looking at the statelevel, we observe a large heterogeneity in how banks finance non-traditional activities of states.22

Natural disasters: We merge information on natural disasters with municipality-level data from theIBGE using as composite key the municipality code and year. If several natural disasters occur in thesame municipality within a year, we sum the adverse outcomes of each of these natural disasters tocompose the annual damage suffered by the city due to natural disasters.

We include the natural disasters database to assess whether localities that suffer unexpected negative

22Our conclusions about how banks finance non-traditional local activities across municipalities and states remain qual-itatively the same for other years.

20

●

●

●●

●

● ● ●●

●●

●

2%

4%

6%

8%

10%

12%

2004 2006 2008 2010 2012 2014

Year

Fra

ctio

n

Agricultural cities

● ●●

●

●

●

● ●

● ●●

●

15%

20%

25%

30%

35%

2004 2006 2008 2010 2012 2014

Year

Fra

ctio

n

Industrial cities

●● ●

● ●

●

● ●●

●●

●55%

60%

65%

70%

75%

80%

2004 2006 2008 2010 2012 2014

Year

Fra

ctio

n

Services cities

Region

● Midwest

North

Northeast

South

Southeast

Figure 7: Fraction of cities segregated by the preponderant credit that is granted by the financial sector. Banks canchannel credit to agriculture, industry, or services. The sector with preponderant credit of a city corresponds to that withthe largest credit share. We segregate by Brazilian regions: Midwest, North, Northeast, South, and Southeast and report

results from 2003 to 2014.

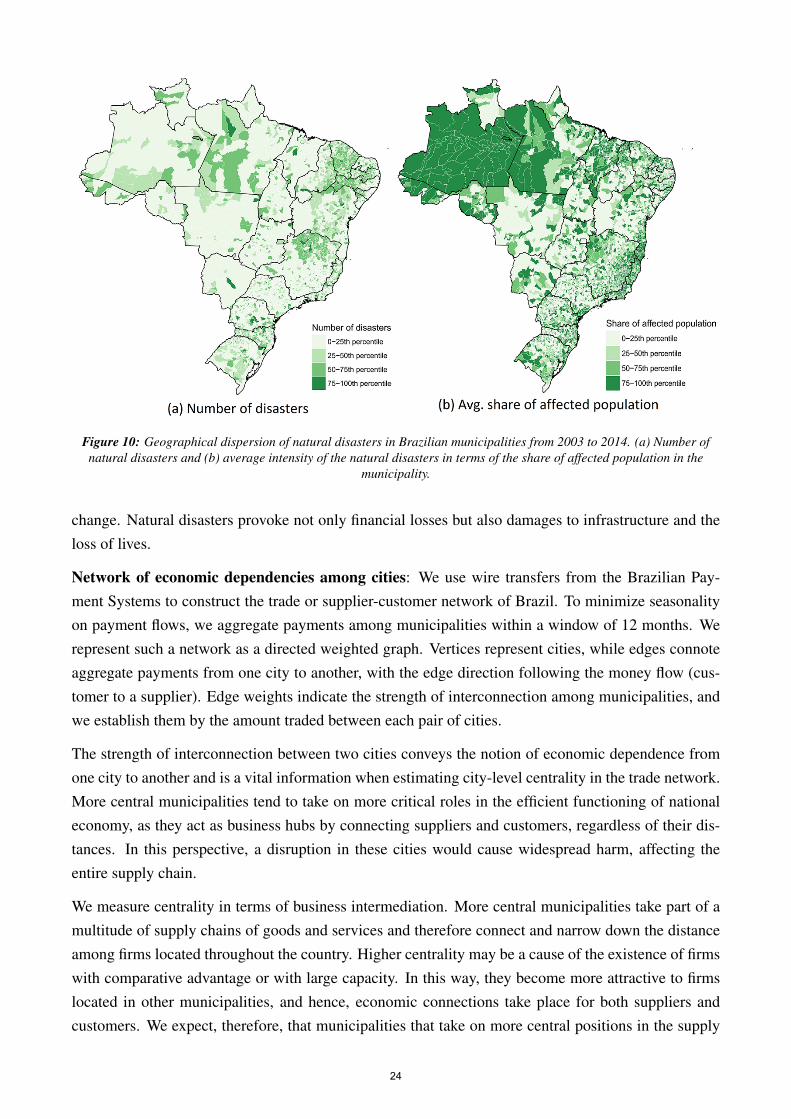

events with widespread damage undergo significant changes in the finance-growth relationship and inthe role of bank credit to non-traditional local activities (activity diversification) in economic growth.These natural disasters serve as sources of exogenous shocks that allows us to test whether the impor-tance of these variables change during times of distress.

We quantify the natural disaster damage in the city in terms of the human capital impact, which wemeasure as the total number of deaths, sick, injured, and homeless reported by local authorities. Asmunicipalities significantly differ in size,23 we scale the extent of the damage of the natural disaster bythe local population of the municipality. Mathematically, the damage imposed by some natural disasteron municipality i at time t is:

23In terms of GDP and population, the associated distributions closely follow a power law.

21

Figu

re8:

Pre

pond

eran

tact

iviti

esan

dcr

edit

tom

unic

ipal

ities

inB

razi

ldur

ing

2014

.(a

)Th

etr

aditi

onal

activ

ityof

ever

yB

razi

lian

mun

icip

ality

.W

eco

nsid

erth

atth

ebu

sine

ssse

ctor

that

cont

ribu

tes

the

mos

tto

GD

Pof

am

unic

ipal

ityis

itstr

aditi

onal

activ

ity.

(b)

The

mos

tfina

nced

busi

ness

sect

orby

bank

sin

each

mun

icip

ality

.(c

)M

atch

orm

ism

atch

betw

een

the

trad

ition

allo

cala

ctiv

ityan

dth

em

ostfi

nanc

edbu

sine

ssse

ctor

inea

chB

razi

lian

mun

icip

ality

.Mis

mat

ches

are

inre

d(d

ark

gray

)and

mat

ches

are

ingr

een

(lig

htgr

ay).

22

Figure 9: Share of credit provided to non-traditional local activities of municipalities and states in 2014. (a) municipalitylevel and (b) state level.

damage by natural disasteri,t =deathsi,t + sicki,t + injuredi,t +homelessi,t

populationi,t, (3)

in which the numerator only counts deaths, sick, injured, and homeless due to the natural event. There-fore, it equals zero if the city i did not undergo a natural disaster at time t. We also test whether theeffects of natural disasters persist over time.

Figure 10(a) gives a geographical view of how natural disasters occur around Brazil. We sum the natu-ral disasters that occur in each municipality from 2003 to 2014. Darker colors represent municipalitiesthat underwent more natural disasters in the period. Figure 10(b) displays our proxy for the damagelevel imposed by natural disasters, which we evaluate using (3). We plot the average damage of naturaldisasters from 2003 to 2014. Again, darker colors represent municipalities that suffered more humandamage in terms of the local population at the time of the event.

Heavy rainfalls, flash floods, and waterlogging are the main natural disasters affecting the North re-gion due to the proximity to the Amazonian forest. The damage is significant because rainfalls arewidespread across cities. In the Southeast region, Haddad and Teixeira (2015) analyze the case ofSao Paulo (megacity, the largest in Brazil) and show that floods result in a reduction of the rate ofcity growth and citizens welfare, hampering local competitiveness in both local and international mar-kets. The authors estimate that more than 20,000 firms were affected by flood events in 2008, withan estimated foregone output of 80 million reais. Debortoli et al. (2017) find that intense rainfall andlandslides were responsible for almost three-quarters of deaths related to natural disasters during theperiod 2001-2010. They find an increase in vulnerability to landslides and flash floods due to climate

23

Figure 10: Geographical dispersion of natural disasters in Brazilian municipalities from 2003 to 2014. (a) Number ofnatural disasters and (b) average intensity of the natural disasters in terms of the share of affected population in the

municipality.

change. Natural disasters provoke not only financial losses but also damages to infrastructure and theloss of lives.

Network of economic dependencies among cities: We use wire transfers from the Brazilian Pay-ment Systems to construct the trade or supplier-customer network of Brazil. To minimize seasonalityon payment flows, we aggregate payments among municipalities within a window of 12 months. Werepresent such a network as a directed weighted graph. Vertices represent cities, while edges connoteaggregate payments from one city to another, with the edge direction following the money flow (cus-tomer to a supplier). Edge weights indicate the strength of interconnection among municipalities, andwe establish them by the amount traded between each pair of cities.

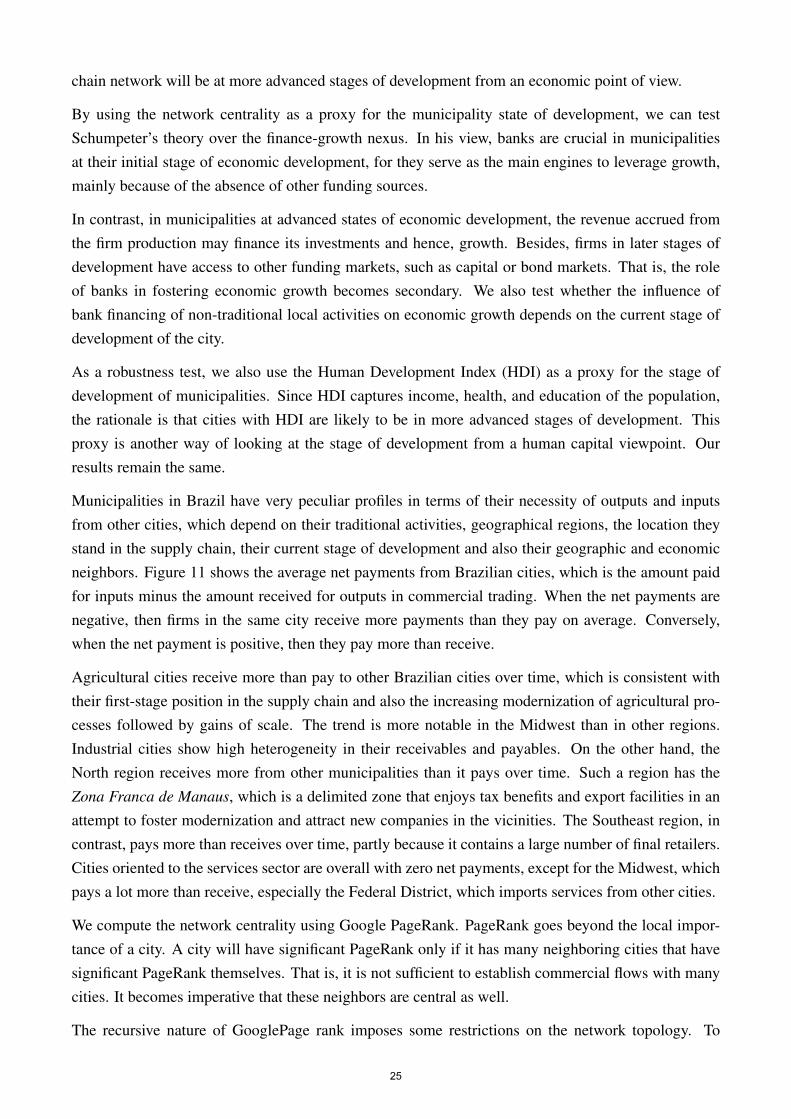

The strength of interconnection between two cities conveys the notion of economic dependence fromone city to another and is a vital information when estimating city-level centrality in the trade network.More central municipalities tend to take on more critical roles in the efficient functioning of nationaleconomy, as they act as business hubs by connecting suppliers and customers, regardless of their dis-tances. In this perspective, a disruption in these cities would cause widespread harm, affecting theentire supply chain.

We measure centrality in terms of business intermediation. More central municipalities take part of amultitude of supply chains of goods and services and therefore connect and narrow down the distanceamong firms located throughout the country. Higher centrality may be a cause of the existence of firmswith comparative advantage or with large capacity. In this way, they become more attractive to firmslocated in other municipalities, and hence, economic connections take place for both suppliers andcustomers. We expect, therefore, that municipalities that take on more central positions in the supply

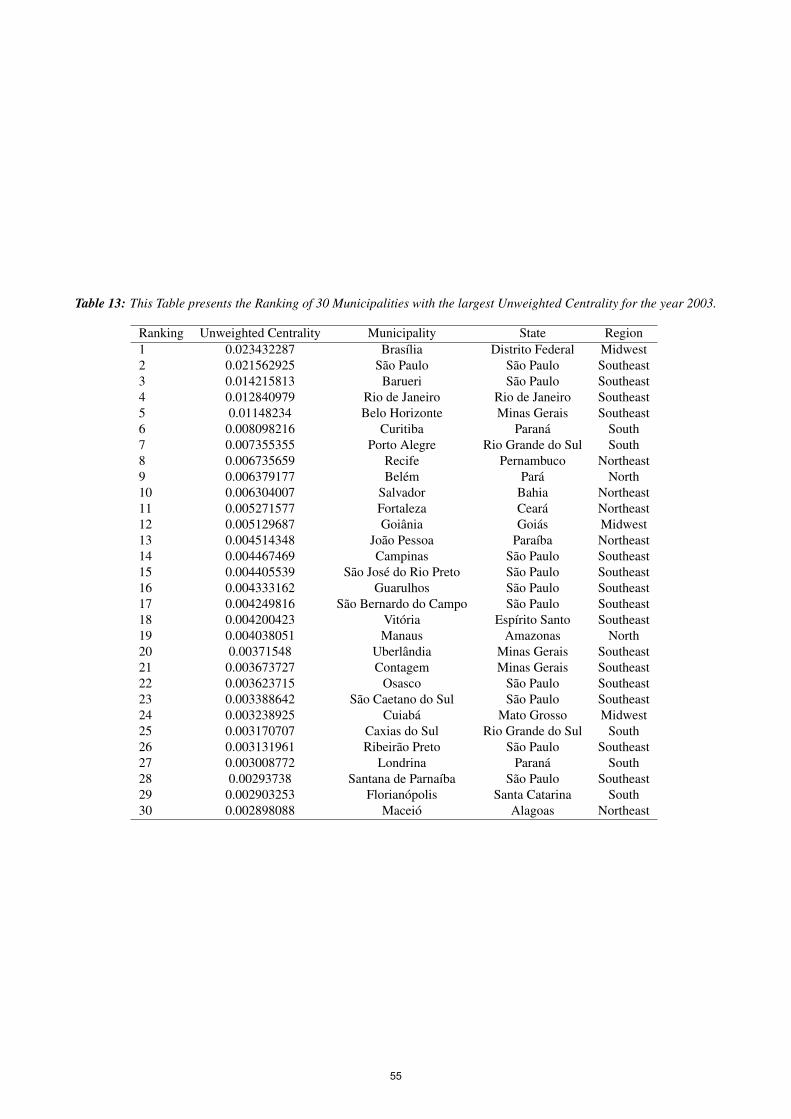

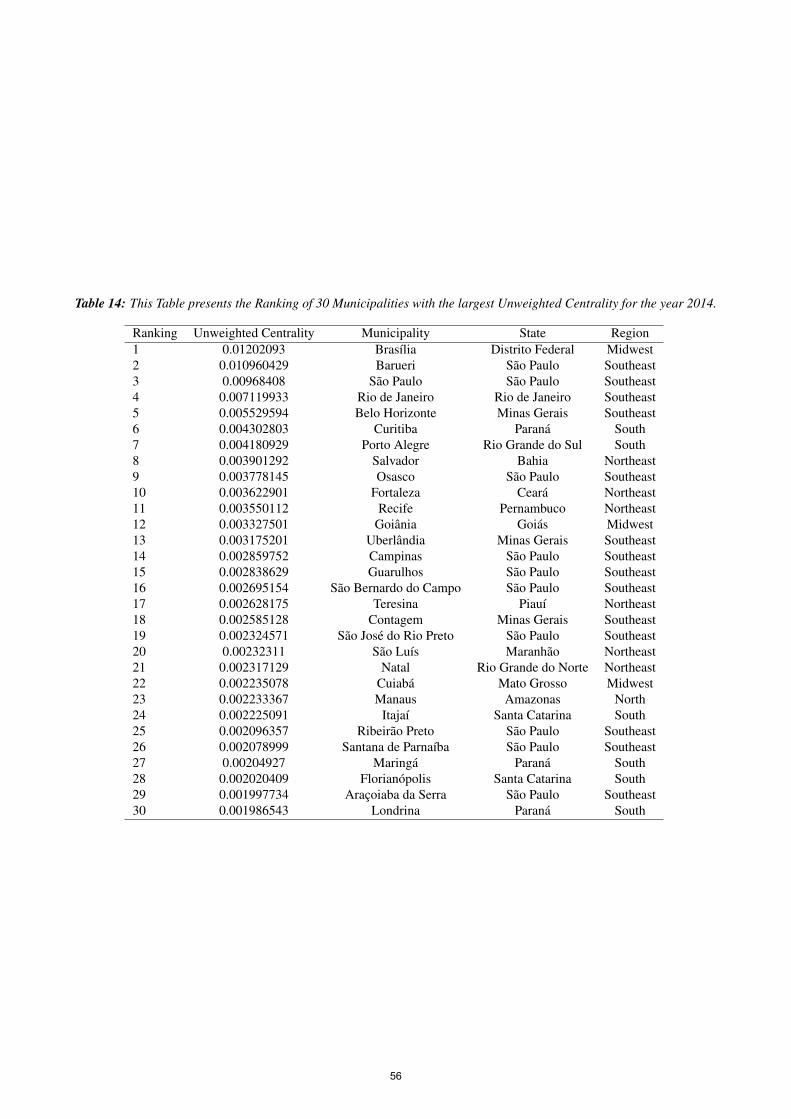

24

chain network will be at more advanced stages of development from an economic point of view.

By using the network centrality as a proxy for the municipality state of development, we can testSchumpeter’s theory over the finance-growth nexus. In his view, banks are crucial in municipalitiesat their initial stage of economic development, for they serve as the main engines to leverage growth,mainly because of the absence of other funding sources.

In contrast, in municipalities at advanced states of economic development, the revenue accrued fromthe firm production may finance its investments and hence, growth. Besides, firms in later stages ofdevelopment have access to other funding markets, such as capital or bond markets. That is, the roleof banks in fostering economic growth becomes secondary. We also test whether the influence ofbank financing of non-traditional local activities on economic growth depends on the current stage ofdevelopment of the city.

As a robustness test, we also use the Human Development Index (HDI) as a proxy for the stage ofdevelopment of municipalities. Since HDI captures income, health, and education of the population,the rationale is that cities with HDI are likely to be in more advanced stages of development. Thisproxy is another way of looking at the stage of development from a human capital viewpoint. Ourresults remain the same.

Municipalities in Brazil have very peculiar profiles in terms of their necessity of outputs and inputsfrom other cities, which depend on their traditional activities, geographical regions, the location theystand in the supply chain, their current stage of development and also their geographic and economicneighbors. Figure 11 shows the average net payments from Brazilian cities, which is the amount paidfor inputs minus the amount received for outputs in commercial trading. When the net payments arenegative, then firms in the same city receive more payments than they pay on average. Conversely,when the net payment is positive, then they pay more than receive.

Agricultural cities receive more than pay to other Brazilian cities over time, which is consistent withtheir first-stage position in the supply chain and also the increasing modernization of agricultural pro-cesses followed by gains of scale. The trend is more notable in the Midwest than in other regions.Industrial cities show high heterogeneity in their receivables and payables. On the other hand, theNorth region receives more from other municipalities than it pays over time. Such a region has theZona Franca de Manaus, which is a delimited zone that enjoys tax benefits and export facilities in anattempt to foster modernization and attract new companies in the vicinities. The Southeast region, incontrast, pays more than receives over time, partly because it contains a large number of final retailers.Cities oriented to the services sector are overall with zero net payments, except for the Midwest, whichpays a lot more than receive, especially the Federal District, which imports services from other cities.

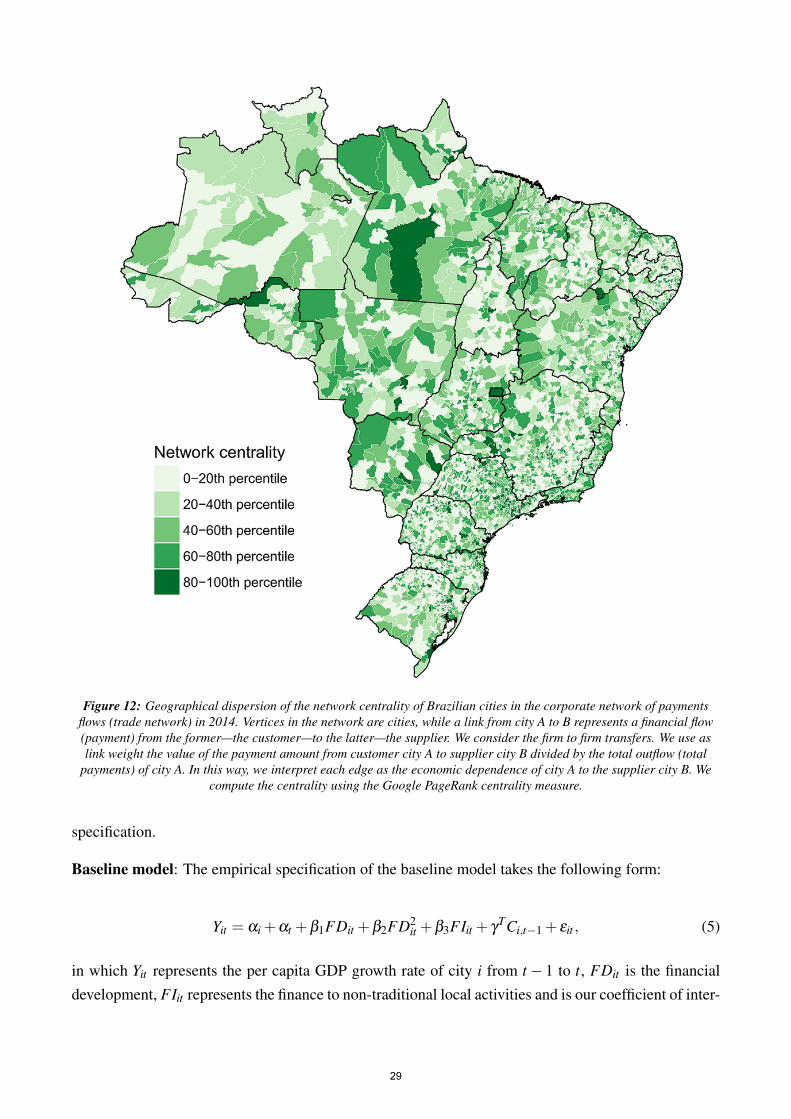

We compute the network centrality using Google PageRank. PageRank goes beyond the local impor-tance of a city. A city will have significant PageRank only if it has many neighboring cities that havesignificant PageRank themselves. That is, it is not sufficient to establish commercial flows with manycities. It becomes imperative that these neighbors are central as well.

The recursive nature of GooglePage rank imposes some restrictions on the network topology. To

25

● ● ●●

●●

●●

●

●●

●

−0.06

−0.04

−0.02

0

2004 2006 2008 2010 2012 2014

Year

Net

pay

men

ts [R

$ bi

]

Agricultural cities

● ● ● ●●

●●

●●

● ● ●

−0.8

−0.6

−0.4

−0.2

0

0.2

0.4

2004 2006 2008 2010 2012 2014

Year

Net

pay

men

ts [R

$ bi

]

Industrial cities

●

● ● ● ●

●

● ●

● ●

●

●

0

0.1

0.2

0.3

0.4

2004 2006 2008 2010 2012 2014

Year

Net

pay

men

ts [R

$ bi

]

Services cities

Region

● Midwest

North

Northeast

South

Southeast

Figure 11: Average net payments from Brazilian cities, which is the amount paid minus the amount received incommercial trading. When the net payments are negative, then firms in the same city receive more payments than they pay.When the net payment is positive, then they pay more than receiving. We segregate by Brazilian regions: Midwest, North,

Northeast, South, and Southeast and report results from 2003 to 2014.

ensure that the diffusion process reaches stationarity, we normalize the network links by introducing thenotion of economic dependency between municipalities. We consider that the downstream economicimportance of supplier city A to customer city B is:

downstream economic importanceA→B =payments from B to A

total payments received by A, (4)

i.e., the economic importance is the share of payments that A receives from B divided by the totalpayments received by A. We term as downstream economic importance because we are looking at theimportance of the customer (closer to the final consumer) to the supplier. The upstream economic

26

importance is the reverse of this definition: it is the importance of the supplier A to cash outflows ofcustomer B. Equation (4) ensures that the weighted adjacency matrix of the graph has all entries in therange [0,1], and therefore the PageRank diffusion process is stationary (Silva and Zhao (2016)). Thisis an important transformation to assure well-defined centrality measures for every city (vertex) in thenetwork.

Figure 12 depicts the geographical dispersion of the network centrality of Brazilian cities in 2014. Aswe can see, there is significant heterogeneity in the degree of centrality of Brazilian municipalities.The Southeastern and Southern regions of Brazil are among the most central cities in Brazil. Thereare also relevant municipalities in other regions, mainly the state capitals, because they require manyinputs from others to be able to offer their goods and services. This considerable heterogeneity andspread throughout the national territory makes the Brazilian case as exciting as the object of study.

Classical financial development indicators: We expect the finance-growth nexus to hold at the mu-nicipality level: financial development helps drive economic growth. To confer robustness to ourfindings, we include in our regressions three proxies for financial development: (i) Credit/GDP, (ii)Deposits/GDP, and (iii) Financial System Size/GDP. We aggregate these ratios by city level. The creditrelates to the total outstanding credit to firms situated in the same city, deposits relate to the totalamount of private deposits both by individuals and firms in local bank branches, the financial systemsize is the sum of the total assets of every bank branch based at the city, and GDP is the nominalcity-level annual GDP.

Following recent work on the finance-growth nexus, financial development helps spur economic growthbut only up to a limit. Too much credit can lead to excessive indebtedness of both individuals and firmsand therefore may backfire to banks in the form of defaults. In an extreme credit-taking scenario,banks may relax screening procedures, increasing provisioning levels, and thus the cost of the creditoperation. In this way, following the standard in the literature, we also include the square of our proxiesfor financial development to empirically test whether there is a non-linear effect.

Table 3 compiles the variables included in the model specification and the associated source that wecollected the data. In Table 4, we present summary statistics for the variables that we use in oureconometric specification. We present the number of observations (N), mean, standard deviation (SD),5th percentile (P5), 25th percentile (P25), median, 75th percentile (P75), 95th percentile (P95), theminimum (Min) and maximum (Max) values.

4.2 Econometric Specification

We employ as dependent variable the per capita growth rate for each municipality i ∈ {1,2, . . . ,n},in which n is the number of municipalities in Brazil. The growth rate is computed as the differencein log of per capita GDP between periods t and t− 1, t ∈ {2003, . . . ,2014}. We use as independentvariables proxies for financial development, such as the outstanding credit to firms, total deposits, andfinancial system size (the sum of total assets), all as a share of the municipality’s GDP. We also includethe finance to non-traditional local activities indicator—our variable of interest—in the econometric

27

Tabl

e3:

Des

crip

tion

ofva

riab

les.

All

vari

able

sar

ere

late

dto

city

-lev

elm

easu

res.

Vari

able

Des

crip

tion

Sour

ce

Per

capi

tagr

owth

ln( 1

+Pe

rcap

itaG

DP t

Perc

apita

GD

P t−

1

)IB

GE

Fina

nce

tono

n-tr

aditi

onal

ln(1

+sh

are

ofcr

edit

tono

n-tr

aditi

onal

activ

ities)

Bra

zilia

nC

redi

tReg

istr

ylo

cala

ctiv

ities

(BC

B)

Cre

dit/

GD

Pln(1

+ou

tsta

ndin

gpr

ivat

ecr

edit

GD

P)

Bra

zilia

nC

redi

tReg

istr

y(B

CB

)

Dep

osits

/GD

Pln( 1

+to

talp

rivat

ede

posi

tsin

the

bank

ing

syst

emG

DP

)B

anki

ngSt

atis

tics

(BC

B)

Fina

ncia

lSys

tem

Size

/GD

Pln( 1

+to

tala

sset

sof

city

bank

bran

ches

GD

P

)B

anki

ngSt

atis

tics

(BC

B)

Shar

eof

affe

cted

pop

bydi

sast

erln( 1

+#d

eath

s+#s

ick+

#inj

ured+

#hom

eles

sPo

pula

tion

)B

razi

lian

Inte

grat

ion

Min

istr

y

Net

wor

kce

ntra

lity

ln(1

+C

ity’s

Page

Ran

k)B

razi

lian

Paym

ents

Syst

em(B

CB

)

Eco

nom

icsp

illov

erln( 1

+∑

j∈ne

ighb

orim

port

ance

jnet

wor

kce

ntra

lity

j)B

razi

lian

Paym

ents

Syst

em(B

CB

)

Geo

grap

hic

spill

over

max

j∈m

esor

egio

nln( 1

+ne

twor

kce

ntra

lity

j)B

razi

lian

Paym

ents

Syst

em(B

CB

)

Gin

iIn

equa

lity

inde

xIB

GE

HD

IH

uman

Dev

elop

men

tInd

exIB

GE

Incl

udes

inco

me,

educ

atio

nan

dhe

alth

28

Figure 12: Geographical dispersion of the network centrality of Brazilian cities in the corporate network of paymentsflows (trade network) in 2014. Vertices in the network are cities, while a link from city A to B represents a financial flow(payment) from the former—the customer—to the latter—the supplier. We consider the firm to firm transfers. We use aslink weight the value of the payment amount from customer city A to supplier city B divided by the total outflow (total

payments) of city A. In this way, we interpret each edge as the economic dependence of city A to the supplier city B. Wecompute the centrality using the Google PageRank centrality measure.

specification.

Baseline model: The empirical specification of the baseline model takes the following form:

Yit = αi +αt +β1FDit +β2FD2it +β3FIit + γ

TCi,t−1 + εit , (5)

in which Yit represents the per capita GDP growth rate of city i from t− 1 to t, FDit is the financialdevelopment, FIit represents the finance to non-traditional local activities and is our coefficient of inter-

29

Table 4: Summary statistics of the regressors and dependent variable. Values are for the period from 2003 to 2014.

Variable N Mean SD P5 P25 Median P75 P95 Min Max

Per capita growth 60,825 0.747 0.077 0.645 0.715 0.745 0.776 0.852 0.000 4.123Finance to non-traditional local activities 66,459 0.533 0.343 0.000 0.238 0.521 0.878 1.000 0.000 1.000

Credit / GDP 66,458 0.009 0.034 0.001 0.002 0.004 0.008 0.024 0.000 2.367(Credit / GDP)2 66,458 0.001 0.041 0.000 0.000 0.000 0.000 0.001 0.000 5.602Deposits / GDP 42,669 0.013 0.025 0.001 0.005 0.009 0.016 0.032 0.000 1.585

(Deposits / GDP)2 42,669 0.001 0.024 0.000 0.000 0.000 0.000 0.001 0.000 2.513Financial system size / GDP 42,669 0.177 0.221 0.021 0.073 0.128 0.212 0.456 0.000 5.829