Embed Size (px)

Citation preview

Document of The World Bank

FOR OFFICIAL USE ONLY

Report No: 34792-CO

IMPLEMENTATION COMPLETION REPORT(TF-53133 FSLT-72800)

ON A

LOAN

IN THE AMOUNT OF US$100 MILLION

TO THE REPUBLIC OF

COLOMBIA

FOR A

PROGRAMMATIC FISCAL AND INSTITUTIONAL STRUCTURAL ADJUSTMENT LOAN III

December 28, 2005

Poverty Reduction and Economic Management UnitMexico and Colombia Country Management UnitLatin America and the Caribbean Region

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective December 21, 2005)

Currency Unit = Colombian Pesos 100 = US$ 0.04

US$ 1 = 2,283.10 Colombian Pesos

FISCAL YEARJanuary 1 - December 31

ABBREVIATIONS AND ACRONYMSCAS Country Assistance StrategyCFAA Country Financial Accountability AssessmentCGN Contaduría General de la Nación (Accountant General’s Office)CONFIS Consejo Superior de Política Fiscal (Superior Council of Fiscal Policy)CONPES Consejo Nacional de Política Económica y Social (National Council of

Economic and Social Policy)CPAR Country Procurement Assessment ReportCSR Commission for State ReformDAFP Departamento Administrativo de la Función Pública (Public Service

Administrative Department)DIAN Dirección de Impuestos y Aduanas Nacionales (National Directorate

of Taxes and Customs)DNP Departamento Nacional de Planeación (National Planning Department)FIAL Programmatic Fiscal and Institutional Adjustment LoanFNR Fondo Nacional de Regalías (National

Royalty Fund)FRL Fiscal Responsibility LawGDP Gross Domestic ProductIBRD International Bank for Reconstruction and DevelopmentICBF Instituto Colombiano de Bienestar Familiar (Colombian

Family Welfare Institute)IDB Inter-American Development BankIDF Institutional Development FacilityIMF International Monetary FundISS Instituto de Seguridad Social (Social Security Institute)IVA Impuesto al Valor Agregado (Value-added tax)LIL Learning and Innovation LoanMAFP Modernización de la Administración Financiera Pública (Public Financial

Management Project)MDGs Millennium Development GoalsMHCP Ministerio de Hacienda y Crédito Público (Ministry of Finance and

Public Credit)MIJ Ministerio del Interior y Justicia (Ministry of Interior and Justice)MTEF Medium Term Expenditure FrameworkMTFF Medium Term Fiscal FrameworkNFPS Non-Financial Public SectorOBC Organic Budget Code

PHRD Policy and Human Resources DevelopmentPLaRSSAL Programmatic Labor Reform and Social Sector Adjustment LoanPRAP Programa de Renovación de la Administración Pública (Public

Administration Renovation Program)SENA Servicio Nacional de Aprendizaje (National Training Service)SIIF Sistema Integrado de Información Financiera (Integrated Financial

Information System)SINERGIA Sistema Nacional de Evaluación de Resultados (Evaluation System for

Public Management)TAL Technical Assistance LoanVAT Value-added Tax

Vice President: Pamela CoxCountry Director Isabel M. GuerreroSector Manager Ronald E. Myers

Task Team Leader/Task Manager: Mario F. Sangines

COLOMBIAPROGRAMMATIC FISCAL AND INSTITUTIONAL STRUCTURAL ADJUSTMENT LOAN III

CONTENTS

Page No.1. Project Data 12. Principal Performance Ratings 13. Assessment of Development Objective and Design, and of Quality at Entry 24. Achievement of Objective and Outputs 165. Major Factors Affecting Implementation and Outcome 286. Sustainability 297. Bank and Borrower Performance 308. Lessons Learned 329. Partner Comments 3310. Additional Information 59Annex 1. Key Performance Indicators/Log Frame Matrix 60Annex 2. Project Costs and Financing 62Annex 3. Economic Costs and Benefits 63Annex 4. Bank Inputs 64Annex 5. Ratings for Achievement of Objectives/Outputs of Components 65Annex 6. Ratings of Bank and Borrower Performance 66Annex 7. List of Supporting Documents 67

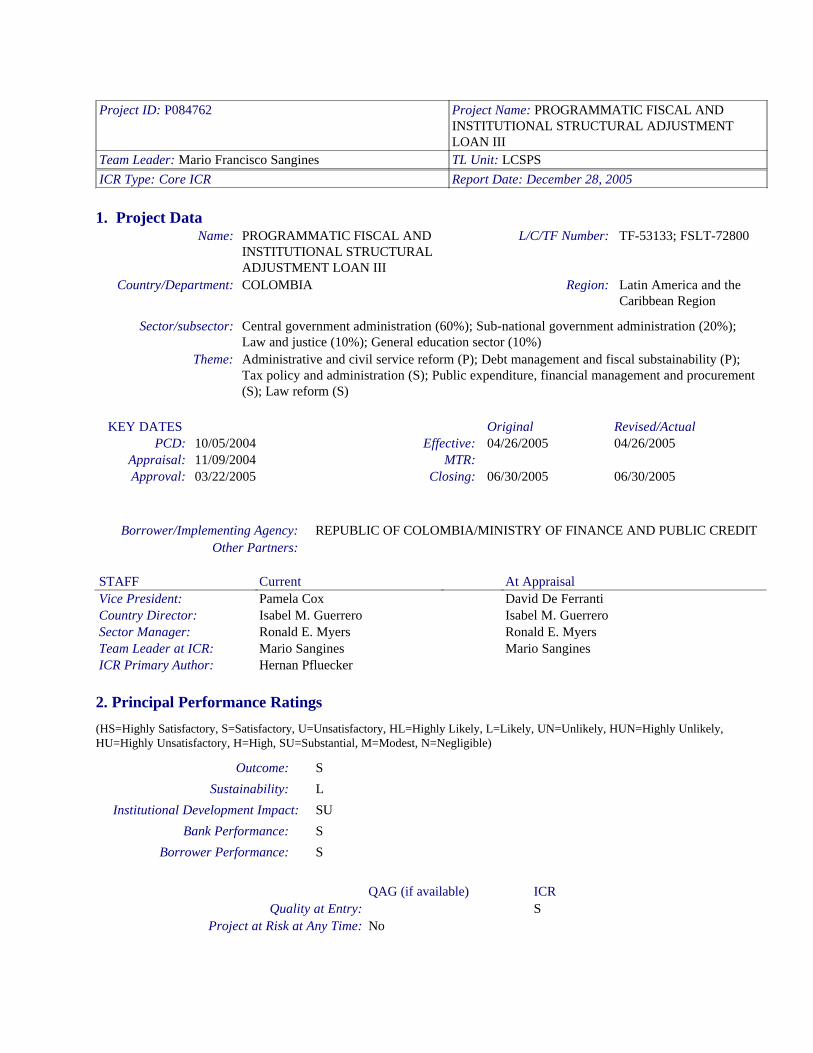

Project ID: P084762 Project Name: PROGRAMMATIC FISCAL AND INSTITUTIONAL STRUCTURAL ADJUSTMENT LOAN III

Team Leader: Mario Francisco Sangines TL Unit: LCSPSICR Type: Core ICR Report Date: December 28, 2005

1. Project DataName: PROGRAMMATIC FISCAL AND

INSTITUTIONAL STRUCTURAL ADJUSTMENT LOAN III

L/C/TF Number: TF-53133; FSLT-72800

Country/Department: COLOMBIA Region: Latin America and the Caribbean Region

Sector/subsector: Central government administration (60%); Sub-national government administration (20%); Law and justice (10%); General education sector (10%)

Theme: Administrative and civil service reform (P); Debt management and fiscal substainability (P); Tax policy and administration (S); Public expenditure, financial management and procurement (S); Law reform (S)

KEY DATES Original Revised/ActualPCD: 10/05/2004 Effective: 04/26/2005 04/26/2005

Appraisal: 11/09/2004 MTR:Approval: 03/22/2005 Closing: 06/30/2005 06/30/2005

Borrower/Implementing Agency: REPUBLIC OF COLOMBIA/MINISTRY OF FINANCE AND PUBLIC CREDITOther Partners:

STAFF Current At AppraisalVice President: Pamela Cox David De FerrantiCountry Director: Isabel M. Guerrero Isabel M. GuerreroSector Manager: Ronald E. Myers Ronald E. MyersTeam Leader at ICR: Mario Sangines Mario SanginesICR Primary Author: Hernan Pfluecker

2. Principal Performance Ratings

(HS=Highly Satisfactory, S=Satisfactory, U=Unsatisfactory, HL=Highly Likely, L=Likely, UN=Unlikely, HUN=Highly Unlikely, HU=Highly Unsatisfactory, H=High, SU=Substantial, M=Modest, N=Negligible)

Outcome: S

Sustainability: L

Institutional Development Impact: SU

Bank Performance: S

Borrower Performance: S

QAG (if available) ICRQuality at Entry: S

Project at Risk at Any Time: No

3. Assessment of Development Objective and Design, and of Quality at Entry

3.1 Original Objective:This is the final ICR for the programmatic series of Fiscal and Institutional Adjustment Loans originally envisioned in the 2002-2006 CAS as four loans totaling $900 million. Following the third loan in the series, approved in March 2005 for $100 million and a cumulative total of $550 million, the Government and the Bank agreed to suspend the program. As stated in the CAS Progress Report (CAS PR) of September 9, 2005 "During the CPPR and CAS PR discussions, the Government and Bank agreed that the reforms needed to trigger FIAL IV were not likely to be in place by FY06, and decided to redirect funds earmarked for FIAL IV to operations where reforms were moving more quickly." Although there is the possibility that FIAL IV might yet be brought back into the Bank's pipeline after FY06, there are no ongoing discussions regarding this fourth operation nor has it been included in the CAS PR for FY06 or FY07. These facts led to the decision to submit a complete ICR for the entire FIAL program at this time. Should FIAL IV be prepared and approved, a revised final ICR would be prepared afterwards which would replace the overall program assessment presented here.

The objectives and design of the programmatic series of Fiscal and Institutional Adjustment Loans (FIAL) need to be assessed within the context of: (i) an incoming administration with an ambitious program and an overwhelming popular mandate, having won the elections with over 50% of the vote in the first round; (ii) structural fiscal imbalances stemming from a highly distorted tax system and major rigidities in public expenditure; (iii) an economy barely recovering from the 1999-2000 recession, the first in recent history; and (iv) a track record of incomplete and/or postponed fiscal reforms by previous administrations.

Within this context, the FIAL program was designed as the main vehicle to channel Bank support for Colombia’s fiscal and institutional agenda. The main elements of the program had its origins in “The 100 Points of Alvaro Uribe Vélez” document, in which the then-candidate set forth a set of priority actions including tax and institutional reform measures designed to render the public sector more efficient and to reduce inflexibilities in the budget process. The Bank’s involvement began with the 2002 policy notes exercise (these have been published as a book by the World Bank: “Colombia: The Economic Foundations of Peace,” 2003), which provided a stage for close and intensive interaction with the incoming administration and helped establish the basic strategies for fiscal and institutional reform. Program design also benefited from close coordination with the Colombia team of the IMF, which in turn guaranteed full consistency between the FIAL program and the Fund’s Stand-By Agreement that began in December 2002.

The program’s development objectives were twofold: first, to promote reforms addressing fiscal rigidities needed to attain the substantial fiscal adjustment required for sustainable macroeconomic stability; and second, to improve the provision of public services and establish the institutional basis for greater efficiency and accountability in public expenditures. The program had the following specific objectives:

Increase tax revenue and reduce distortions in the tax systemlModernize tax administrationlImprove budget management with modern tools and legal reformslDevelop incentives for efficiency gains in sub-national entitieslPrevent massive losses to the State from judicial claimslStrengthen the public sector procurement systemlReduce losses and generate revenues through improved asset managementlImprove performance through management contracts for government agencieslPromote the development of a sound fiscal responsibility legal frameworkl

- 2 -

Support a coherent and comprehensive reform implementation processl

Project design was unquestionably ambitious. The government program brought in by the new administration was quite broad and comprehensive, making it a challenge to fully implement even with the abundant political capital of the Uribe administration. Substantial analytical work from within and outside Colombia further enriched it, and the FIAL program’s design was a conflux of both these elements. Most key actors (including the Bank) felt that the Uribe government provided the opportunity to overcome the frustration of years of unfinished fiscal reforms.

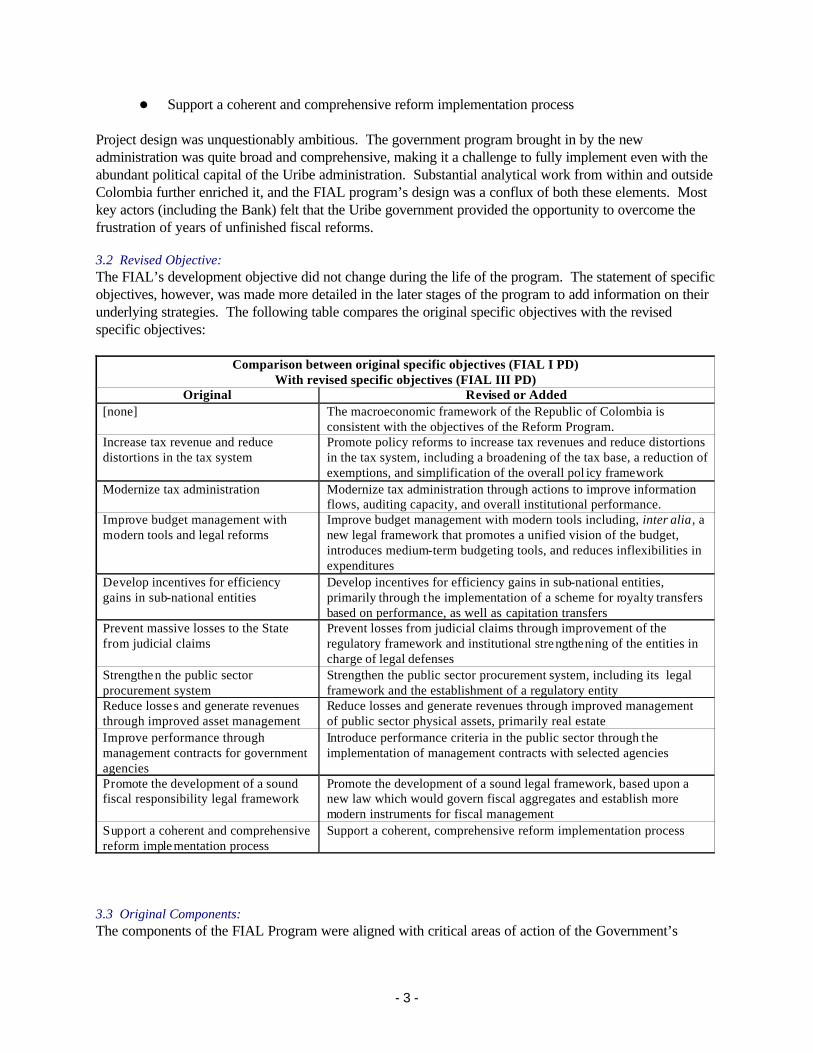

3.2 Revised Objective:The FIAL’s development objective did not change during the life of the program. The statement of specific objectives, however, was made more detailed in the later stages of the program to add information on their underlying strategies. The following table compares the original specific objectives with the revised specific objectives:

Comparison between original specific objectives (FIAL I PD) With revised specific objectives (FIAL III PD)

Original Revised or Added [none] The macroeconomic framework of the Republic of Colombia is

consistent with the objectives of the Reform Program. Increase tax revenue and reduce distortions in the tax system

Promote policy reforms to increase tax revenues and reduce distortions in the tax system, including a broadening of the tax base, a reduction of exemptions, and simplification of the overall pol icy framework

Modernize tax administration Modernize tax administration through actions to improve information flows, auditing capacity, and overall institutional performance.

Improve budget management with modern tools and legal reforms

Improve budget management with modern tools including, inter alia, a new legal framework that promotes a unified vision of the budget, introduces medium-term budgeting tools, and reduces inflexibilities in expenditures

Develop incentives for efficiency gains in sub-national entities

Develop incentives for efficiency gains in sub-national entities, primarily through the implementation of a scheme for royalty transfers based on performance, as well as capitation transfers

Prevent massive losses to the State from judicial claims

Prevent losses from judicial claims through improvement of the regulatory framework and institutional strengthening of the entities in charge of legal defenses

Strengthen the public sector procurement system

Strengthen the public sector procurement system, including its legal framework and the establishment of a regulatory entity

Reduce losse s and generate revenues through improved asset management

Reduce losses and generate revenues through improved management of public sector physical assets, primarily real estate

Improve performance through management contracts for government agencies

Introduce performance criteria in the public sector through the implementation of management contracts with selected agencies

Promote the development of a sound fiscal responsibility legal framework

Promote the development of a sound legal framework, based upon a new law which would govern fiscal aggregates and establish more modern instruments for fiscal management

Support a coherent and comprehensive reform implementation process

Support a coherent, comprehensive reform implementation process

3.3 Original Components:The components of the FIAL Program were aligned with critical areas of action of the Government’s

- 3 -

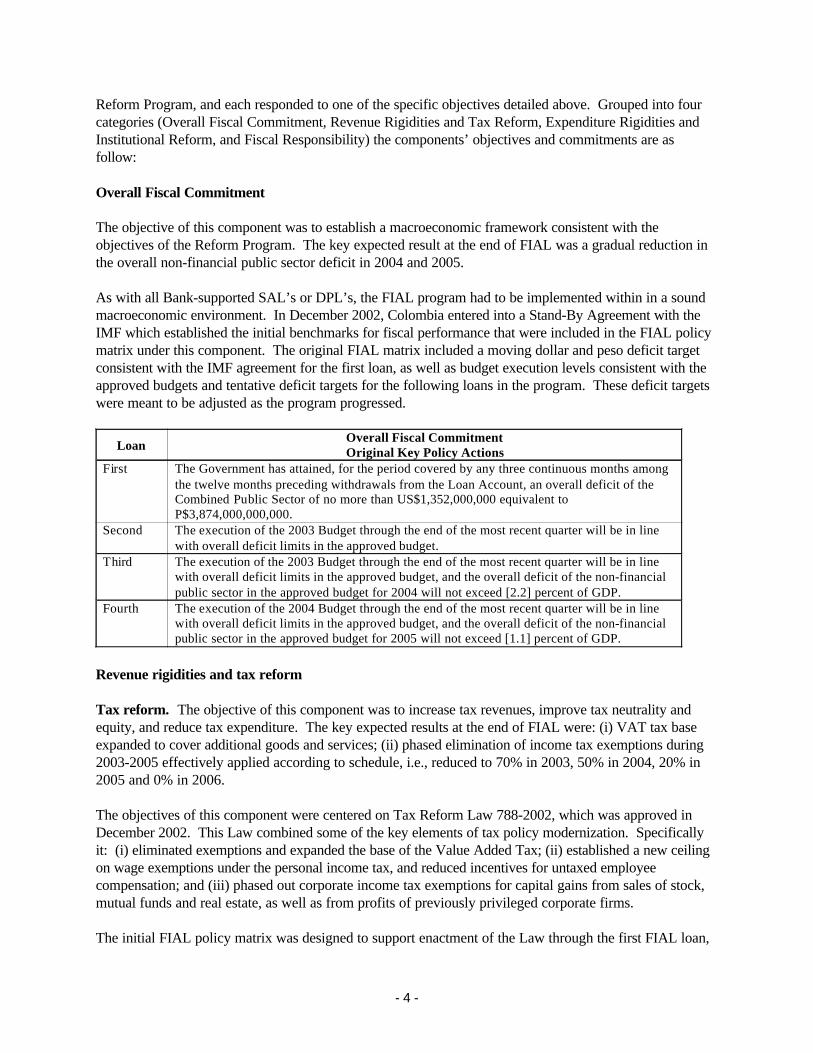

Reform Program, and each responded to one of the specific objectives detailed above. Grouped into four categories (Overall Fiscal Commitment, Revenue Rigidities and Tax Reform, Expenditure Rigidities and Institutional Reform, and Fiscal Responsibility) the components’ objectives and commitments are as follow:

Overall Fiscal Commitment

The objective of this component was to establish a macroeconomic framework consistent with the objectives of the Reform Program. The key expected result at the end of FIAL was a gradual reduction in the overall non-financial public sector deficit in 2004 and 2005.

As with all Bank-supported SAL’s or DPL’s, the FIAL program had to be implemented within in a sound macroeconomic environment. In December 2002, Colombia entered into a Stand-By Agreement with the IMF which established the initial benchmarks for fiscal performance that were included in the FIAL policy matrix under this component. The original FIAL matrix included a moving dollar and peso deficit target consistent with the IMF agreement for the first loan, as well as budget execution levels consistent with the approved budgets and tentative deficit targets for the following loans in the program. These deficit targets were meant to be adjusted as the program progressed.

Loan Overall Fiscal Commitment Original Key Policy Actions

First The Government has attained, for the period covered by any three continuous months among the twelve months preceding withdrawals from the Loan Account, an overall deficit of the Combined Public Sector of no more than US$1,352,000,000 equivalent to P$3,874,000,000,000.

Second The execution of the 2003 Budget through the end of the most recent quarter will be in line with overall deficit limits in the approved budget.

Third The execution of the 2003 Budget through the end of the most recent quarter will be in line with overall deficit limits in the approved budget, and the overall deficit of the non-financial public sector in the approved budget for 2004 will not exceed [2.2] percent of GDP.

Fourth The execution of the 2004 Budget through the end of the most recent quarter will be in line with overall deficit limits in the approved budget, and the overall deficit of the non-financial public sector in the approved budget for 2005 will not exceed [1.1] percent of GDP.

Revenue rigidities and tax reform

Tax reform. The objective of this component was to increase tax revenues, improve tax neutrality and equity, and reduce tax expenditure. The key expected results at the end of FIAL were: (i) VAT tax base expanded to cover additional goods and services; (ii) phased elimination of income tax exemptions during 2003-2005 effectively applied according to schedule, i.e., reduced to 70% in 2003, 50% in 2004, 20% in 2005 and 0% in 2006.

The objectives of this component were centered on Tax Reform Law 788-2002, which was approved in December 2002. This Law combined some of the key elements of tax policy modernization. Specifically it: (i) eliminated exemptions and expanded the base of the Value Added Tax; (ii) established a new ceiling on wage exemptions under the personal income tax, and reduced incentives for untaxed employee compensation; and (iii) phased out corporate income tax exemptions for capital gains from sales of stock, mutual funds and real estate, as well as from profits of previously privileged corporate firms.

The initial FIAL policy matrix was designed to support enactment of the Law through the first FIAL loan,

- 4 -

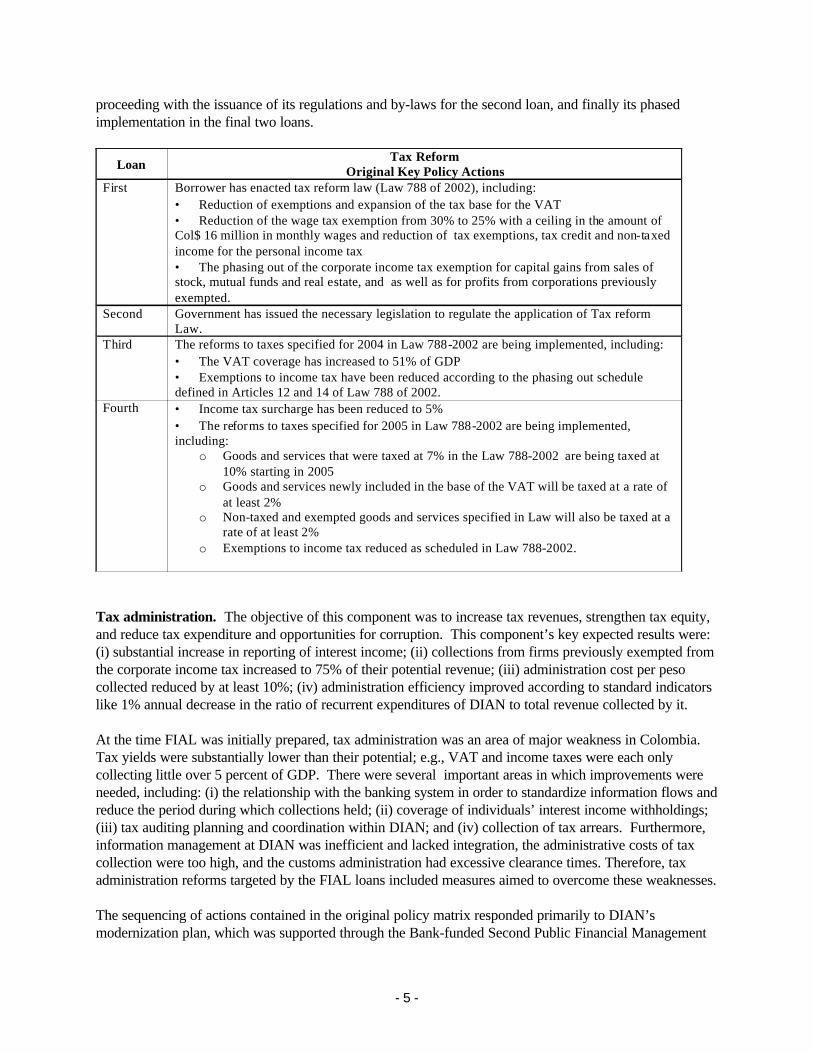

proceeding with the issuance of its regulations and by-laws for the second loan, and finally its phased implementation in the final two loans.

Loan Tax Reform

Original Key Policy Actions First Borrower has enacted tax reform law (Law 788 of 2002), including:

• Reduction of exemptions and expansion of the tax base for the VAT • Reduction of the wage tax exemption from 30% to 25% with a ceiling in the amount of Col$ 16 million in monthly wages and reduction of tax exemptions, tax credit and non-taxed income for the personal income tax • The phasing out of the corporate income tax exemption for capital gains from sales of stock, mutual funds and real estate, and as well as for profits from corporations previously exempted.

Second Government has issued the necessary legislation to regulate the application of Tax reform Law.

Third The reforms to taxes specified for 2004 in Law 788-2002 are being implemented, including: • The VAT coverage has increased to 51% of GDP • Exemptions to income tax have been reduced according to the phasing out schedule defined in Articles 12 and 14 of Law 788 of 2002.

Fourth • Income tax surcharge has been reduced to 5% • The reforms to taxes specified for 2005 in Law 788-2002 are being implemented, including:

o Goods and services that were taxed at 7% in the Law 788-2002 are being taxed at 10% starting in 2005

o Goods and services newly included in the base of the VAT will be taxed at a rate of at least 2%

o Non-taxed and exempted goods and services specified in Law will also be taxed at a rate of at least 2%

o Exemptions to income tax reduced as scheduled in Law 788-2002.

Tax administration. The objective of this component was to increase tax revenues, strengthen tax equity, and reduce tax expenditure and opportunities for corruption. This component’s key expected results were: (i) substantial increase in reporting of interest income; (ii) collections from firms previously exempted from the corporate income tax increased to 75% of their potential revenue; (iii) administration cost per peso collected reduced by at least 10%; (iv) administration efficiency improved according to standard indicators like 1% annual decrease in the ratio of recurrent expenditures of DIAN to total revenue collected by it.

At the time FIAL was initially prepared, tax administration was an area of major weakness in Colombia. Tax yields were substantially lower than their potential; e.g., VAT and income taxes were each only collecting little over 5 percent of GDP. There were several important areas in which improvements were needed, including: (i) the relationship with the banking system in order to standardize information flows and reduce the period during which collections held; (ii) coverage of individuals’ interest income withholdings; (iii) tax auditing planning and coordination within DIAN; and (iv) collection of tax arrears. Furthermore, information management at DIAN was inefficient and lacked integration, the administrative costs of tax collection were too high, and the customs administration had excessive clearance times. Therefore, tax administration reforms targeted by the FIAL loans included measures aimed to overcome these weaknesses.

The sequencing of actions contained in the original policy matrix responded primarily to DIAN’s modernization plan, which was supported through the Bank-funded Second Public Financial Management

- 5 -

Technical Assistance Loan (PFMP II, or MAFP II in Spanish).

Loan Tax Administration

Original Key Policy Actions First The Ministry of Finance, through DIAN, has enacted new rules for tax administration

including: • Daily interest payments higher than Col$900 are subject to withholding at the source • Obligation of financial institutions to report information on taxpayers’ accounts that are credited with annual interest of at least Col$5 million, and/or have total annual deposits equal or higher than Col$50 million • Establish a list of collectable tax debts on December 31 of 2002 • Elaborate a plan and set up a schedule to collect at least 20 percent of these collectable debts • Establish indicators of customs clearance time and procedures to select shipments for inspection based on a risk-management system for the customs offices of Bogotá and Medellín.

Second • The DIAN publishes regularly: o Semi-annual revenue indicators o Annual results of surveys of taxpayer’s satisfaction o Indicators of collection costs disaggregated by type of tax and of taxpayer

• The DIAN has: o Developed and implemented a cross reference system with financial institutions to

monitoring the interest reported by taxpayers o Audited at least 50% of large taxpayers affected by the new taxes o Established and published indicators of the cost and time required for compliance by

the taxpayer o Established unified accounts between customs and domestic taxes for large

taxpayers beginning in 2003. Third • All taxpayers that receive VAT refunds have unified the taxpayer current account for

VAT, income tax and customs in 2004 • The Import & Export module for integrated domestic tax and customs systems is in operation • Collections from firms previously exempted from the corporate income tax have increased to at least 75 percent of their estimated corporate income tax potential revenue • 100% of large contributors have unified accounts and are submitting electronic income tax returns by the end of 2003 • The DIAN has renegotiated agreements with banks with regard to submission of information in standard form and incentives for prompt processing of data and turning over funds.

Fourth • Collections per customs inspection increased by at least 30 percent in real terms in 2004 compared to 2002. • Administration cost reduced by at least 10% in real terms in 2004 compared to the collections of 2002. • At least 20 monthly tax audits have been performed jointly by the customs and the internal taxes units of DIAN

Expenditure rigidities and institutional reform

Budget management. The objective of this component was to transform the budget into a more effective tool for sound fiscal policy and improved service delivery. The key expected result was a budget that would include targets and performance indicators for at least six sector ministries in accordance with a

- 6 -

medium term budget plan like a medium term expenditure framework.

At the time of the program’s preparation, the Colombian budget system had been abundantly studied. Most studies coincided in that it had a number of important weaknesses that affected both control over the aggregate levels of expenditure as well as their composition. In terms of aggregate expenditure controls, budget allocations were actual authorizations to commit by spending agencies, which led to large accumulations of arrears in years when revenues fell below expected levels (which occurred quite often). In terms of the composition of expenditure, budget rigidity derived from high levels of both “structural” expenditures (such as pensions, debt service, and transfers) and law-based permanent earmarks basically left fiscal authorities with no room to maneuver.

The modernization of the budget system to correct these deficiencies and introduce a medium-term expenditure horizon had to rely on a number of different instruments. Although diagnoses were abundant, the Government lacked an official budget reform strategy, which needed be prepared and approved as a CONPES document (CONPES documents are policy documents that are officially reviewed and approved by the cabinet). Although some improvements could be achieved through a reform of the Organic Budget Code, establishing the Ministry of Finance's firm control over budget aggregates required a Constitutional amendment. While “forward budgeting," which also added to the inter-temporal budget rigidity, also needed to be brought under control, and something had to be done regarding legally-mandated permanent entitlements and earmarks, the highly sensitive and political nature of the issue called for a special high-level commission to initially study them and present a recommendation.

Technical aspects of budgeting, such as revising budget classifications and the introduction of the medium-term perspective, were also to be supported by the loan. Finally, an exercise in performance-based budgeting was to be phased in during the last loan of the FIAL program.

- 7 -

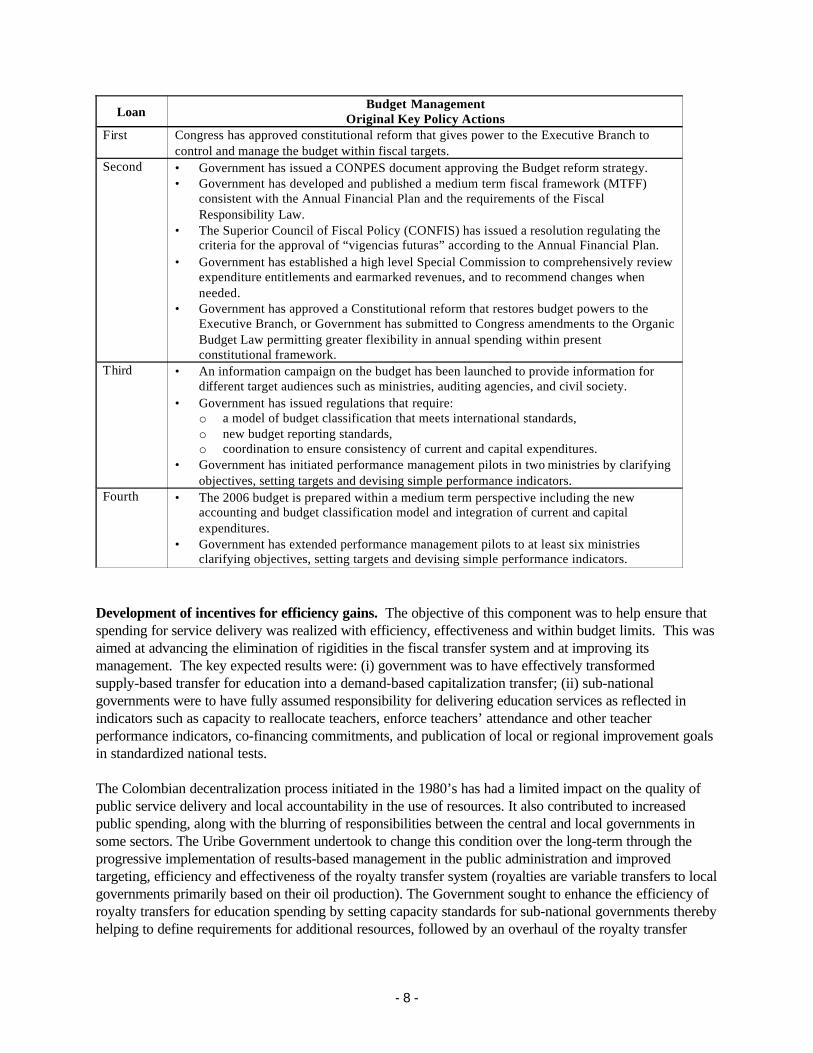

Loan Budget Management

Original Key Policy Actions First Congress has approved constitutional reform that gives power to the Executive Branch to

control and manage the budget within fiscal targets. Second • Government has issued a CONPES document approving the Budget reform strategy.

• Government has developed and published a medium term fiscal framework (MTFF) consistent with the Annual Financial Plan and the requirements of the Fiscal Responsibility Law.

• The Superior Council of Fiscal Policy (CONFIS) has issued a resolution regulating the criteria for the approval of “vigencias futuras” according to the Annual Financial Plan.

• Government has established a high level Special Commission to comprehensively review expenditure entitlements and earmarked revenues, and to recommend changes when needed.

• Government has approved a Constitutional reform that restores budget powers to the Executive Branch, or Government has submitted to Congress amendments to the Organic Budget Law permitting greater flexibility in annual spending within present constitutional framework.

Third • An information campaign on the budget has been launched to provide information for different target audiences such as ministries, auditing agencies, and civil society.

• Government has issued regulations that require: o a model of budget classification that meets international standards, o new budget reporting standards, o coordination to ensure consistency of current and capital expenditures.

• Government has initiated performance management pilots in two ministries by clarifying objectives, setting targets and devising simple performance indicators.

Fourth • The 2006 budget is prepared within a medium term perspective including the new accounting and budget classification model and integration of current and capital expenditures.

• Government has extended performance management pilots to at least six ministries clarifying objectives, setting targets and devising simple performance indicators.

Development of incentives for efficiency gains. The objective of this component was to help ensure that spending for service delivery was realized with efficiency, effectiveness and within budget limits. This was aimed at advancing the elimination of rigidities in the fiscal transfer system and at improving its management. The key expected results were: (i) government was to have effectively transformed supply-based transfer for education into a demand-based capitalization transfer; (ii) sub-national governments were to have fully assumed responsibility for delivering education services as reflected in indicators such as capacity to reallocate teachers, enforce teachers’ attendance and other teacher performance indicators, co-financing commitments, and publication of local or regional improvement goals in standardized national tests.

The Colombian decentralization process initiated in the 1980’s has had a limited impact on the quality of public service delivery and local accountability in the use of resources. It also contributed to increased public spending, along with the blurring of responsibilities between the central and local governments in some sectors. The Uribe Government undertook to change this condition over the long-term through the progressive implementation of results-based management in the public administration and improved targeting, efficiency and effectiveness of the royalty transfer system (royalties are variable transfers to local governments primarily based on their oil production). The Government sought to enhance the efficiency of royalty transfers for education spending by setting capacity standards for sub-national governments thereby helping to define requirements for additional resources, followed by an overhaul of the royalty transfer

- 8 -

system.

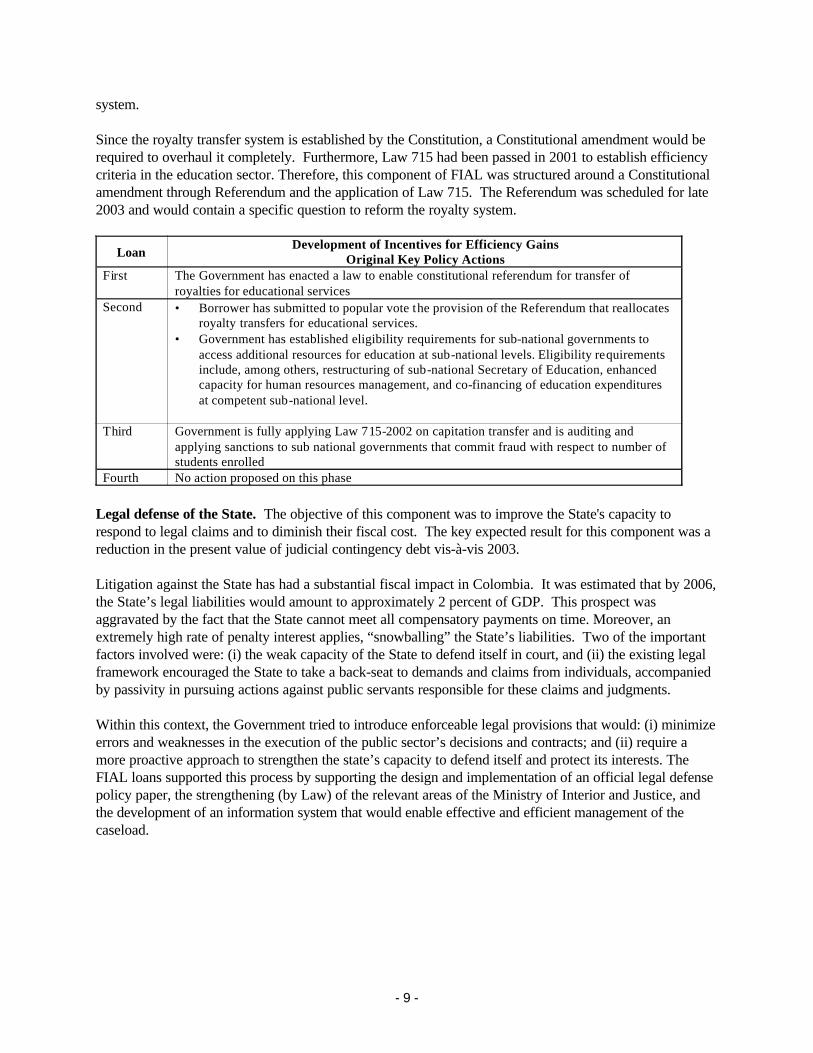

Since the royalty transfer system is established by the Constitution, a Constitutional amendment would be required to overhaul it completely. Furthermore, Law 715 had been passed in 2001 to establish efficiency criteria in the education sector. Therefore, this component of FIAL was structured around a Constitutional amendment through Referendum and the application of Law 715. The Referendum was scheduled for late 2003 and would contain a specific question to reform the royalty system.

Loan Development of Incentives for Efficiency Gains

Original Key Policy Actions First The Government has enacted a law to enable constitutional referendum for transfer of

royalties for educational services Second • Borrower has submitted to popular vote the provision of the Referendum that reallocates

royalty transfers for educational services. • Government has established eligibility requirements for sub-national governments to

access additional resources for education at sub-national levels. Eligibility requirements include, among others, restructuring of sub-national Secretary of Education, enhanced capacity for human resources management, and co-financing of education expenditures at competent sub-national level.

Third Government is fully applying Law 715-2002 on capitation transfer and is auditing and applying sanctions to sub national governments that commit fraud with respect to number of students enrolled

Fourth No action proposed on this phase

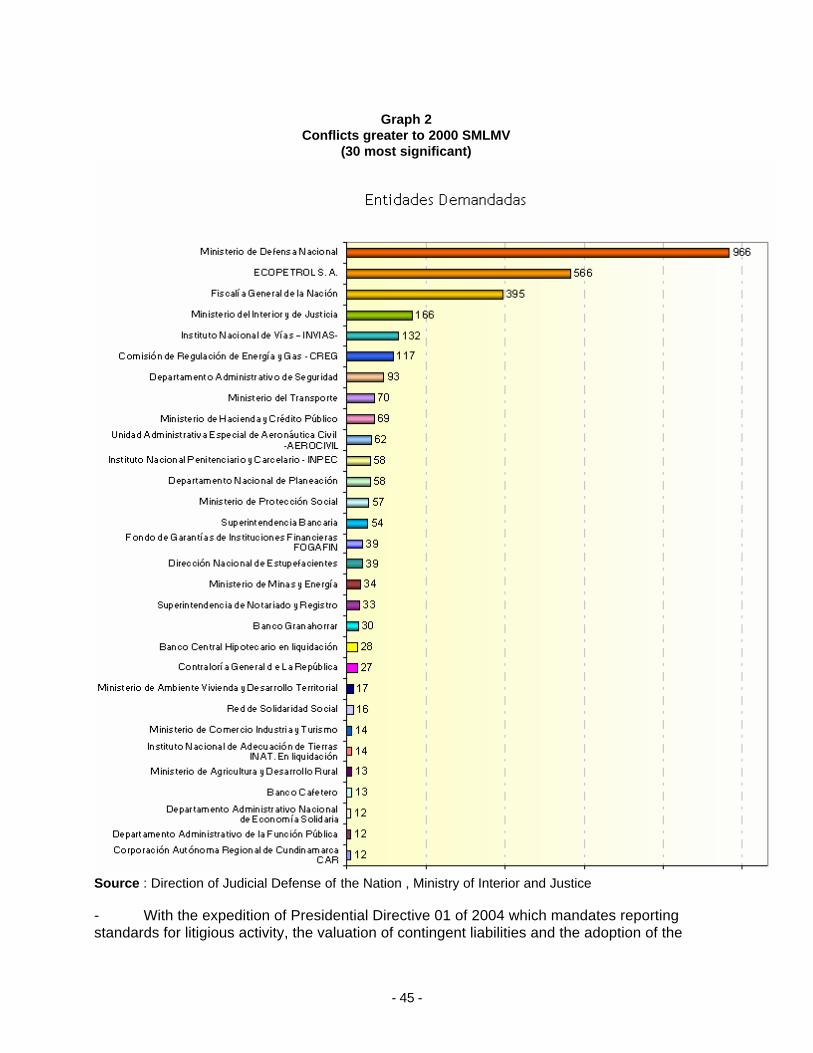

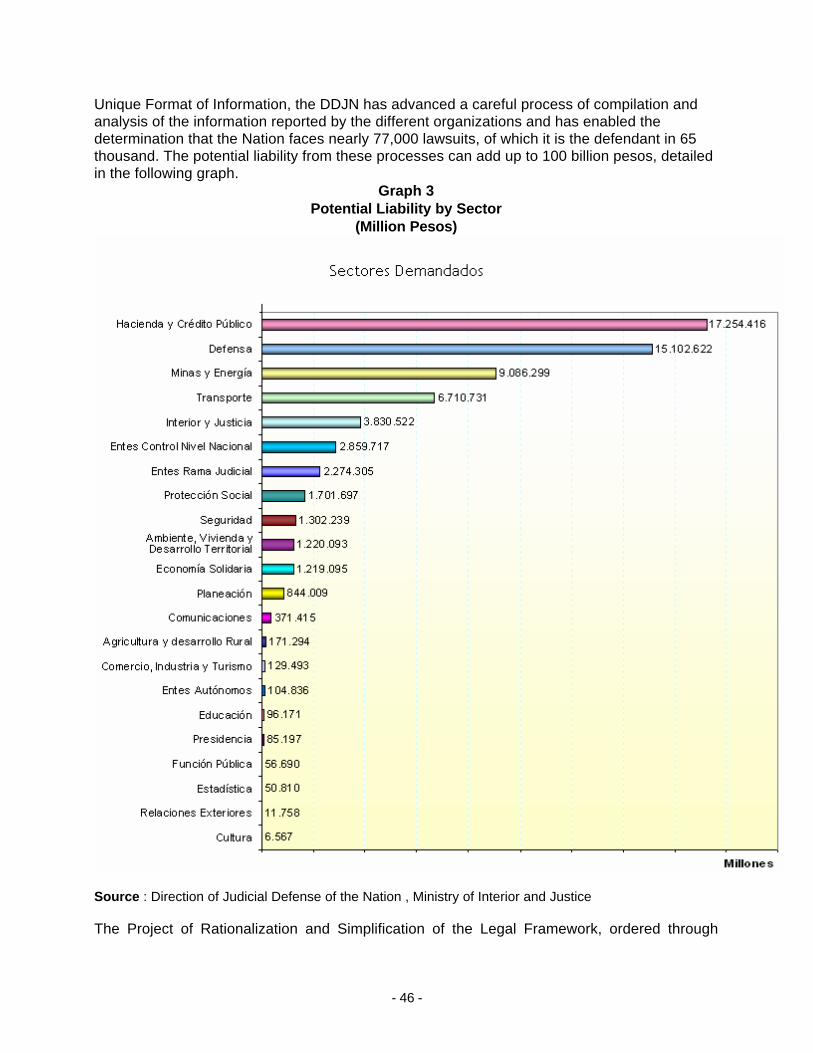

Legal defense of the State. The objective of this component was to improve the State's capacity to respond to legal claims and to diminish their fiscal cost. The key expected result for this component was a reduction in the present value of judicial contingency debt vis-à-vis 2003.

Litigation against the State has had a substantial fiscal impact in Colombia. It was estimated that by 2006, the State’s legal liabilities would amount to approximately 2 percent of GDP. This prospect was aggravated by the fact that the State cannot meet all compensatory payments on time. Moreover, an extremely high rate of penalty interest applies, “snowballing” the State’s liabilities. Two of the important factors involved were: (i) the weak capacity of the State to defend itself in court, and (ii) the existing legal framework encouraged the State to take a back-seat to demands and claims from individuals, accompanied by passivity in pursuing actions against public servants responsible for these claims and judgments.

Within this context, the Government tried to introduce enforceable legal provisions that would: (i) minimize errors and weaknesses in the execution of the public sector’s decisions and contracts; and (ii) require a more proactive approach to strengthen the state’s capacity to defend itself and protect its interests. The FIAL loans supported this process by supporting the design and implementation of an official legal defense policy paper, the strengthening (by Law) of the relevant areas of the Ministry of Interior and Justice, and the development of an information system that would enable effective and efficient management of the caseload.

- 9 -

Loan

Legal Defense of the State Original Key Policy Actions

First • Borrower has promulgated Law 790 of 2002 that grants authority to central government for strengthening the “Dirección de Defensa Judicial del Ministerio del Interior y de Justicia” with the purpose of: o limiting the state’s civil liability through improved policy formulation and

coordination, o seeking indemnification from borrower’s civil servants who act with gross

negligence and bad faith, o professionalizing judicial defense of the state.

Second Borrower has issued a CONPES document establishing the new policy for legal defense of

the state, including legal reform if necessary. Third Government has established a public monitoring, information and reporting system that

includes performance and result indicators and expected fiscal impact for the legal defense of the state.

Fourth Government is implementing the new policy for legal defense of the state and is publishing semi-annual reports on performance and results indicators, including expected fiscal impact, of the legal protection policy.

Strengthening public sector procurement. The objective of this component was to ensure that government purchases were transparent and efficient. The key expected results were: (i) the country’s legal framework for procurement reformed following guidelines agreed between the Government and the Bank, including guidelines such as measures to enhance transparency and objectivity, assignment of monitoring and evaluation responsibility in procurement policy to a competent agency; (ii) advances in coverage of e-procurement.

Preparatory studies for this component, including the Bank’s CPAR, indicated that public contracts in Colombia were affected by an unclear division between the private and public sectors and by an inadequate legal framework that had overlaps and omissions. These were exacerbated by the legacy of traditional State patronage systems which protected both buyers and vendors from being held accountable and provided opportunities for corruption. In addition, no central agency was in charge of promoting reforms or even of introducing the use of modern information technology.

The Government’s program, as supported by the FIAL, contained the following key elements: issuance of Decree 2170, through which some measures to improve transparency and to implement some international “best practices” in contracts were implemented; the establishment of a regulatory entity in charge of monitoring public sector procurement and issuing regulations; and the reform of the procurement bill (Law 80) to simplify the legal framework, ensure accountability, and promote more value-for-money in procurement processes.

- 10 -

Loan Strengthening Public Sector Procurement

Original Key Policy Actions of FIAL First • Government has issued Decree 2170 (September 30, 2002) that strengthens transparency

and objectivity in public sector procurement. • Bill of Law 018/2002 modifying current public sector procurement legal framework

being in consideration by the Congress.

Second • Government issued CONPES document that: o dictates the principles that apply to government procurement, o recommends the creation of a new agency or the assignment to an existing agency of

public sector procurement responsibilities, o defines a strategy for developing and implementing e -procurement.

• Government has proposed to Congress modifications to the legal bill amending Law 80 that incorporate the CONPES recommendations, emphasizing: o common principles for public sector procurement; o introduction of economic considerations into the procurement process; o institutional framework for public sector procurement.

Third The Government Agency responsible for monitoring, evaluating, and establishing common

guidelines in public sector procurement matters, started its operation. Fourth Government has issued the regulatory decrees for the implementation of the new procurement

legal framework.

Asset management. The objective of this component was to maximize the economic and social return of the State’s assets; generate revenues by liquidating those not directly linked to service delivery, reduce replacement and restoration costs, and eliminate opportunities for corruption. The key expected results at the end of the program were: (i) the State was to have institutionalized mechanisms to monitor, evaluate, maintain and dispose of public assets; and (ii) the State was to have received accumulated revenues for asset management equivalent to at least US$70 million.

Diagnostic work revealed the existence of a substantial body of idle public sector assets which contributed to inefficiencies in resource use. Many were not properly titled or adequately registered in institutional inventories; others were sub-utilized or misused, generating unnecessary costs. Numerous institutions spent a substantial portion of their budgets on property maintenance and leasing. At the time of the FIAL’s preparation, the State’s asset management suffered from: (i) unclear legal status and economic value, incomplete registration, and irregular control over properties and other public assets; and (ii) the existing legal framework's failure to recognize market principles and to provide a clear basis for managerial discretion.

The Government adopted a strategy to improve asset management through: (i) short-term policy actions to develop a framework for public asset management; and (ii) medium-term policy actions to develop a more flexible approach, e.g., concessions, leasing, privatization, and outsourcing. Through these reforms it was expected that assets worth approximately US$1 billion would be registered and prevented from further deterioration, with a beneficial fiscal impact.

The FIAL program originally envisioned support to this area through a combination of efforts including the creation of a regulatory body for asset management, the preparation and approval of a CONPES document, the enactment of legislation to enable more modern asset management practices, an updated asset inventory, and the generation of revenue through the short-term asset liquidation program.

- 11 -

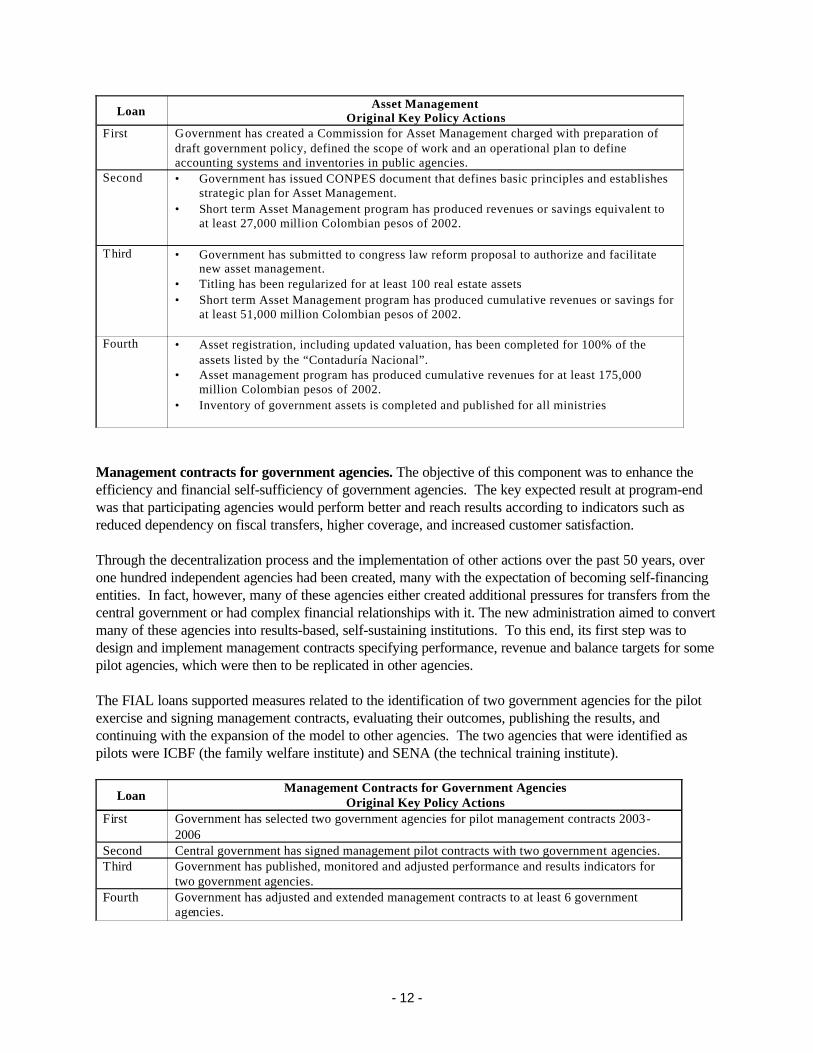

Loan Asset Management Original Key Policy Actions

First Government has created a Commission for Asset Management charged with preparation of draft government policy, defined the scope of work and an operational plan to define accounting systems and inventories in public agencies.

Second • Government has issued CONPES document that defines basic principles and establishes strategic plan for Asset Management.

• Short term Asset Management program has produced revenues or savings equivalent to at least 27,000 million Colombian pesos of 2002.

Third • Government has submitted to congress law reform proposal to authorize and facilitate

new asset management. • Titling has been regularized for at least 100 real estate assets • Short term Asset Management program has produced cumulative revenues or savings for

at least 51,000 million Colombian pesos of 2002.

Fourth • Asset registration, including updated valuation, has been completed for 100% of the assets listed by the “Contaduría Nacional”.

• Asset management program has produced cumulative revenues for at least 175,000 million Colombian pesos of 2002.

• Inventory of government assets is completed and published for all ministries

Management contracts for government agencies. The objective of this component was to enhance the efficiency and financial self-sufficiency of government agencies. The key expected result at program-end was that participating agencies would perform better and reach results according to indicators such as reduced dependency on fiscal transfers, higher coverage, and increased customer satisfaction.

Through the decentralization process and the implementation of other actions over the past 50 years, over one hundred independent agencies had been created, many with the expectation of becoming self-financing entities. In fact, however, many of these agencies either created additional pressures for transfers from the central government or had complex financial relationships with it. The new administration aimed to convert many of these agencies into results-based, self-sustaining institutions. To this end, its first step was to design and implement management contracts specifying performance, revenue and balance targets for some pilot agencies, which were then to be replicated in other agencies.

The FIAL loans supported measures related to the identification of two government agencies for the pilot exercise and signing management contracts, evaluating their outcomes, publishing the results, and continuing with the expansion of the model to other agencies. The two agencies that were identified as pilots were ICBF (the family welfare institute) and SENA (the technical training institute).

Loan Management Contracts for Government Agencies

Original Key Policy Actions First Government has selected two government agencies for pilot management contracts 2003-

2006 Second Central government has signed management pilot contracts with two government agencies. Third Government has published, monitored and adjusted performance and results indicators for

two government agencies. Fourth Government has adjusted and extended management contracts to at least 6 government

agencies.

- 12 -

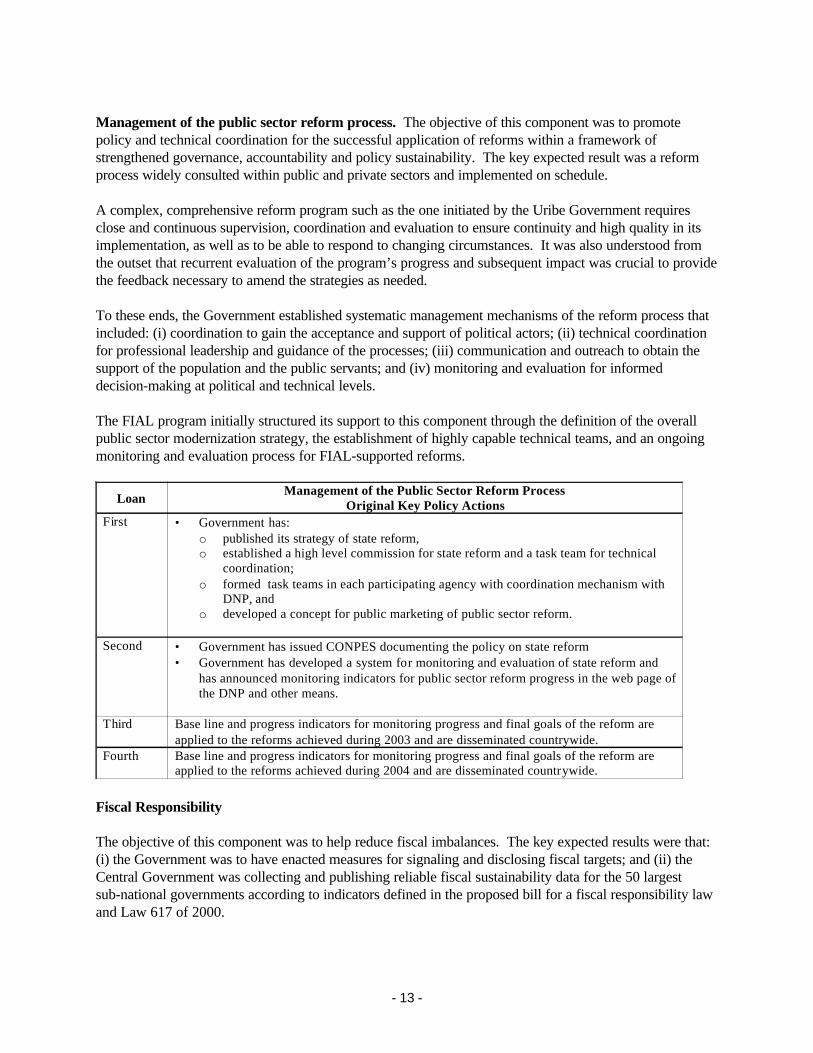

Management of the public sector reform process. The objective of this component was to promote policy and technical coordination for the successful application of reforms within a framework of strengthened governance, accountability and policy sustainability. The key expected result was a reform process widely consulted within public and private sectors and implemented on schedule.

A complex, comprehensive reform program such as the one initiated by the Uribe Government requires close and continuous supervision, coordination and evaluation to ensure continuity and high quality in its implementation, as well as to be able to respond to changing circumstances. It was also understood from the outset that recurrent evaluation of the program’s progress and subsequent impact was crucial to provide the feedback necessary to amend the strategies as needed.

To these ends, the Government established systematic management mechanisms of the reform process that included: (i) coordination to gain the acceptance and support of political actors; (ii) technical coordination for professional leadership and guidance of the processes; (iii) communication and outreach to obtain the support of the population and the public servants; and (iv) monitoring and evaluation for informed decision-making at political and technical levels.

The FIAL program initially structured its support to this component through the definition of the overall public sector modernization strategy, the establishment of highly capable technical teams, and an ongoing monitoring and evaluation process for FIAL-supported reforms.

Loan Management of the Public Sector Reform Process

Original Key Policy Actions First • Government has:

o published its strategy of state reform, o established a high level commission for state reform and a task team for technical

coordination; o formed task teams in each participating agency with coordination mechanism with

DNP, and o developed a concept for public marketing of public sector reform.

Second • Government has issued CONPES documenting the policy on state reform

• Government has developed a system for monitoring and evaluation of state reform and has announced monitoring indicators for public sector reform progress in the web page of the DNP and other means.

Third Base line and progress indicators for monitoring progress and final goals of the reform are

applied to the reforms achieved during 2003 and are disseminated countrywide. Fourth Base line and progress indicators for monitoring progress and final goals of the reform are

applied to the reforms achieved during 2004 and are disseminated countrywide.

Fiscal Responsibility

The objective of this component was to help reduce fiscal imbalances. The key expected results were that: (i) the Government was to have enacted measures for signaling and disclosing fiscal targets; and (ii) the Central Government was collecting and publishing reliable fiscal sustainability data for the 50 largest sub-national governments according to indicators defined in the proposed bill for a fiscal responsibility law and Law 617 of 2000.

- 13 -

During the Pastrana administration, a draft bill for fiscal responsibility was prepared, and its discussion continued into the Uribe administration which in turn submitted it to Congress. Among the key principles of this new law were the establishment of a medium-term fiscal framework, guidelines for ensuring debt sustainability, definition of macroeconomic targets and transparency measures such as the publication of tax expenditures and improved fiscal reports to Congress. This effort was undertaken in tandem with other initiatives carried out through the Ministry of Finance to collect and publish financial information from sub-national governments.

Loan Original Key Policy Actions of FIAL First The borrower has submitted to Congress the bill od the Law for Fiscal Responsibility. Second • Government has approved the Fiscal Responsibility Law, that contains, at a minimum,

rules for: o setting fiscal targets linked to debt sustainability and primary balance for the NFPS; o annual reports of fiscal results to Congress, including floating debt; o publication of the financial plan that will include, among others, information on

floating and contingency debt; o the obligation to include the fiscal impact and source of financing within any law

that creates new tax expenditures.

Third • Government has: o disclosed fiscal targets for 2004 in accordance with the new law of fiscal

responsibility; o submitted reports to Congress of fiscal results of 2003.

Fourth • Government has:

o disclosed fiscal targets for 2005 in accordance with the new law of fiscal responsibility;

o submitted reports to congress of fiscal results of 2004.

3.4 Revised Components:The overall structure of components and their individual objectives were not changed during program implementation. However, changing circumstances (particularly the defeat of the 2003 Referendum and delays in the approval of key legislation) required adjustments to the specific policy actions within each component. Some of these, such as budget reform or incentives for efficiency gains, were clearly weakened by these circumstances and although a “Plan B” was in place, the desired structural effects were not achieved. Others, such as tax reform, were actually strengthened during implementation as a new Law (Law 863), which was not originally forecast, was approved and accelerated the tax exemption phase-out process.

The changes in policy actions undergone in each component are as follow:

Overall fiscal commitment. As was expected at the outset, the actual deficit targets were adjusted as the program progressed, keeping them either in line with or below the targets in the IMF SBA. Some definitional changes were made, such as adopting the concept of combined public sector for deficit measurement. In FIAL III, the measurement of the fiscal stance was further strengthened by requiring that the overall public sector debt to GDP ratio be below 47%; the original matrix did not incorporate a debt/GDP target.

Tax reform. The Government’s tax reform strategy evolved over time, and was reflected in changes in the policy content of this component. Law 788, which was the single tax policy reform initiative envisioned at

- 14 -

the outset, was later complemented by a second law (Law 863). The failure of the Referendum in late 2003 (which had expenditure-containment measures), the Constitutional restriction on reducing public sector wages, and the rejection by the Constitutional Court of the 2% VAT on basic foodstuffs and services (discussed later in this report), forced the Government to submit the bill to Congress that later became Law 863. While this law contained some highly desirable elements such as the acceleration of the tax exemption phase-out schedule, it also introduced some undesirable quick-revenue items such as a 0.1% increase in the financial transactions tax.

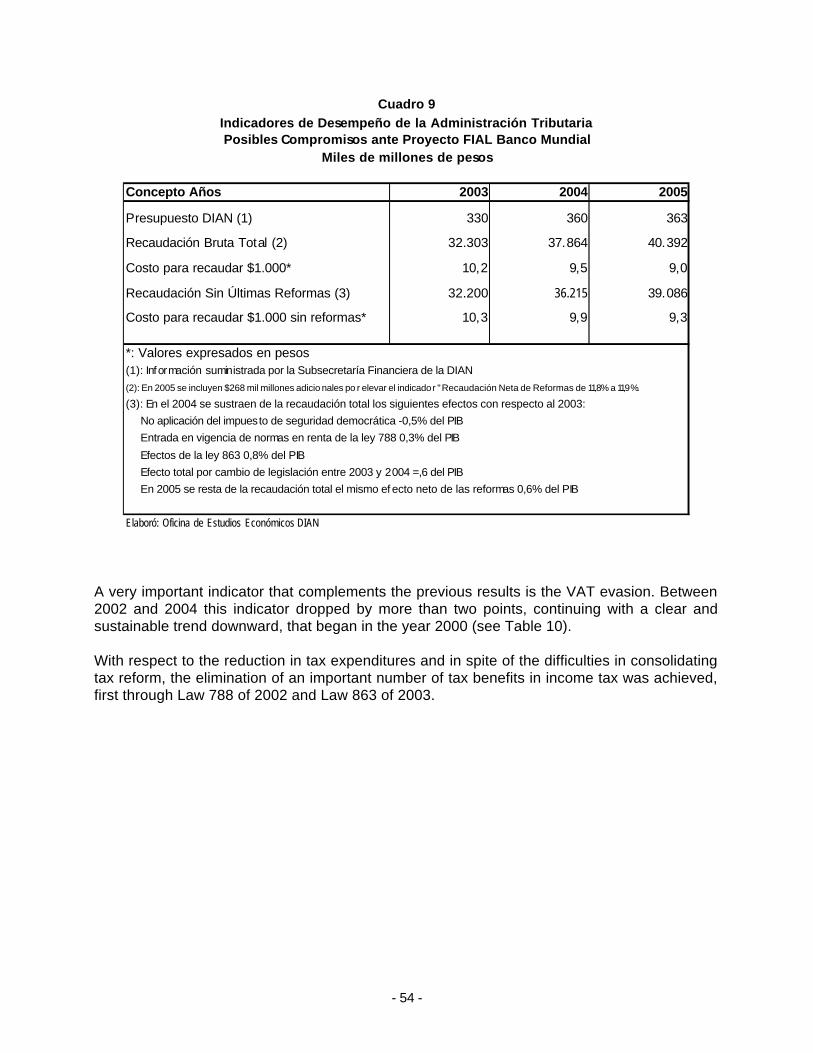

Tax administration. This component underwent a conceptual shift in the way progress was measured. Originally, the FIAL program measured progress in terms such as the deployment of systems, unification of taxpayer accounts, or a particular number of audits. For the third loan, the Bank and the Government jointly decided that these elements, while important, did not provide an adequate picture of the actual overall improvement in tax administration. These indicators were replaced by two internationally-accepted measurements of tax administration capacity: (i) administrative cost per peso collected; and (ii) an estimate of tax evasion as a percentage of GDP.

Budget management. The Government’s budget reform agenda suffered two major setbacks early in the program: (i) the rejection of a Constitutional amendment by the Senate that would have given the executive branch greater control over public expenditure; and (ii) the rejection of the 2003 Referendum, which contained expenditure-control measures. While the Government subsequently attempted to introduce reforms within the Constitution through a new Organic Budget Code, this effort was also rejected by Congress. The lack of structural progress in the budget system constituted one of the reasons why the FIAL program did not progress into its fourth and final loan.

Development of incentives for efficiency gains. After the failed Referendum to authorize the permanent reallocation of royalty transfers for educational services, the Government restructured the National Royalty Commission, facilitating the allocation of some additional funds for educational purposes. The FIAL Policy Matrix was amended to support this alternative solution.

Legal Defense of the State. Although there were no major adjustments to the policy actions of this component, greater comprehension of the complexity of the issue as the program progressed required a reassessment of what was achievable in the short term. For example, it became evident that a real reduction in the value of liabilities during the life of the FIAL program could not be achieved; the effect of strengthening legal defense on the actual balance sheet would only be evident in the longer term.

Strengthening public sector procurement. The policy content of this component was affected by delays (and eventual non-consideration by Congress) of the reforms to the procurement law (Law 80). However, some key elements such as the creation of a normative body and improvements in accountability and transparency were achieved via presidential decree and reflected in the program matrix. The failure to pass the reforms to Law 80 also constituted one of the reasons for discontinuing the FIAL program.

Asset management. As was decided during the Bank’s internal review process of FIAL II, the focus of the policy actions in asset management shifted from quantitative, revenue-generation targets to institutional development targets. In addition, some new elements were introduced such as reforms to the procurement bill related to asset management, which were presented to Congress but did not pass.

Management contracts for government agencies. There were no changes in this component.

- 15 -

Management of the public sector reform process. There were no changes in this component.

Fiscal Responsibility. As the program progressed, it was decided that given the successful implementation of the Fiscal Responsibility Law supported by FIAL II, there was no need to continue introducing policy actions in this regard throughout the rest of the FIAL program. The conditions originally stipulated for FIAL III and IV, which related to the publication of information and compliance with the Medium Term Fiscal Framework, were therefore dropped in an effort to simplify the program matrix.

3.5 Quality at Entry:Quality at entry is rated Satisfactory, given the statement of development objectives. The elements of the program are critical inputs to achieve fiscal sustainability and institutional development, the reform agenda - though admittedly ambitious - was developed in a highly collaborative manner between Bank and Government, and capitalized successfully on a significant stock of analytical work. Each component had a logical sequence and generally began with the formalization of the Government’s strategy in a CONPES document, followed by the necessary legal reforms, and finally their implementation.

However, questions have been raised during the internal Bank review process of the FIAL (in particular during the preparation of FIAL III) regarding its comprehensiveness as a fiscal adjustment program, since it is clear that FIAL does not cover all of the areas that have an effect on fiscal balances. As stated in the FIAL I MOP, “The program to be supported by the (…) FIAL is, nevertheless, not intended to deal exhaustively and conclusively with all areas where action could improve Colombia’s fiscal outlook. Rather, it is conceived as a first-step package that focuses on a core set of critical policies of fiscal reform that can sufficiently strengthen and consolidate public finances.” Furthermore, FIAL followed on the Bank’s Structural Fiscal Adjustment Loan (SFAL) of 2001-2002, which supported reforms in sub-national transfers through the creation of the single Sistema General de Participaciones, helped regulate borrowing in decentralized entities, and promoted a discussion around social security reform. This context suggests that FIAL was appropriately designed, building upon the achievements of previous Bank-supported programs while admittedly focusing on a core set of areas which were understood to be necessary, but not sufficient, to achieve fiscal adjustment.

4. Achievement of Objective and Outputs

4.1 Outcome/achievement of objective:The FIAL program had a two-fold development objective: first, to promote reforms addressing fiscal rigidities needed to attain the substantial fiscal adjustment required for sustainable macroeconomic stability; and second, to improve the provision of public services and establish the institutional basis for greater efficiency and accountability in public expenditures.

Regarding the first objective, the program achieved mixed results. On the revenue side, tax reform measures proceeded largely as planned and produced good results, as is illustrated in the following sections. Tax administration results are also good, and progress in reducing tax evasion and increasing administrative efficiency of DIAN is moving along at a fast pace. On the expenditure side, however, much less has been achieved. Any substantial modification to the way public expenditure is managed involves Constitutional reform, and both attempts supported by the FIAL program failed. Some external factors (such as the devaluation of the dollar, high oil prices and surpluses at the sub-national level) helped buoy the overall fiscal stance in recent years and lifted some pressure from the need for structural expenditure reform. Nonetheless, the Colombian budget remains very rigid and continued efforts will be required to truly transform it into a flexible fiscal policy instrument.

- 16 -

As regards the second objective, the program has influenced quality in service delivery in at least three areas: education, as it has promoted a more efficient use and allocation of royalty transfers to sub-national entities for education; and family welfare and technical education, as it supported performance contracts with the two corresponding entities, establishing service delivery and revenue generation benchmarks. In terms of setting the institutional basis for efficiency and accountability in public expenditures, the overall package of expenditure reforms except budget reform (asset management, procurement, incentives for efficiency gains, and management contracts with government agencies) produced a significant impact on efficiency and accountability, albeit from different angles and varying degrees of depth.

The discontinuation of the program after the third loan has clearly adversely influenced the achievement of the objectives set out at the beginning of the reform process. Elements not yet achieved but that remain in the government’s agenda, such as the new procurement law and Organic Budget Code, would bring the program much closer to full achievement of objectives. Furthermore, substantial results expected shortly in areas such as asset management and tax administration are obviously not part of this assessment, and would also bring the program closer to full success.

Given this assessment, the overall achievement of objectives is rated as Moderately Satisfactory.

- 17 -

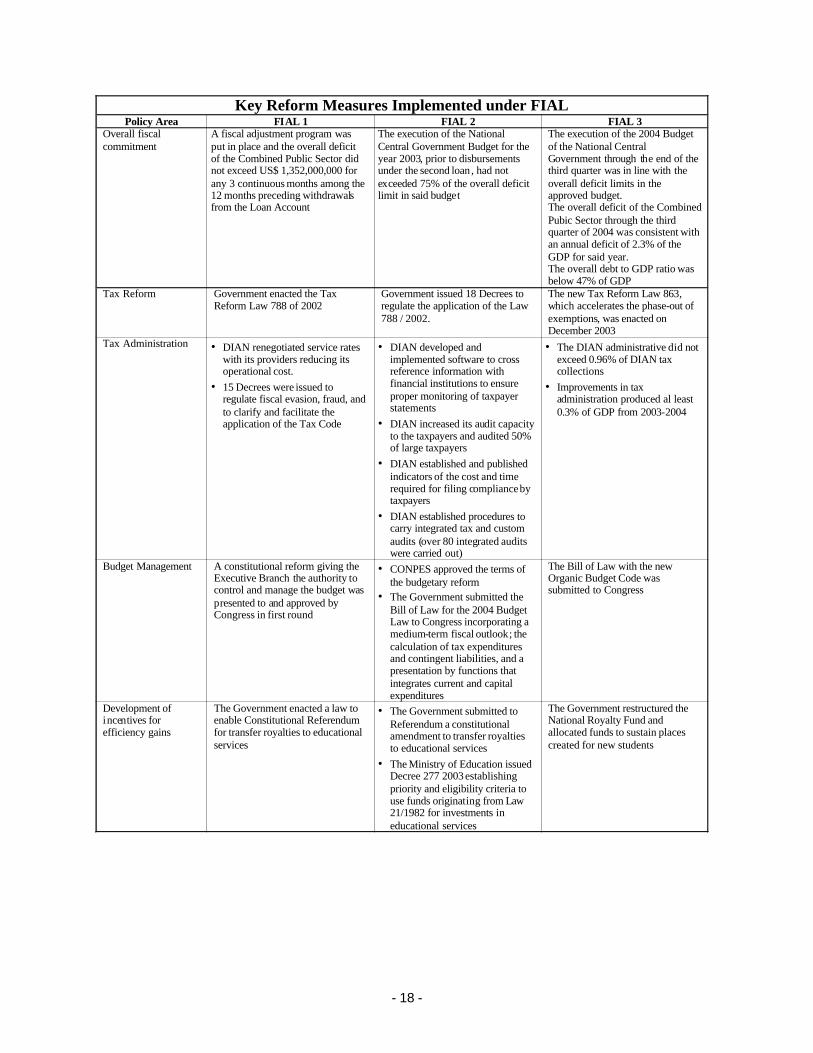

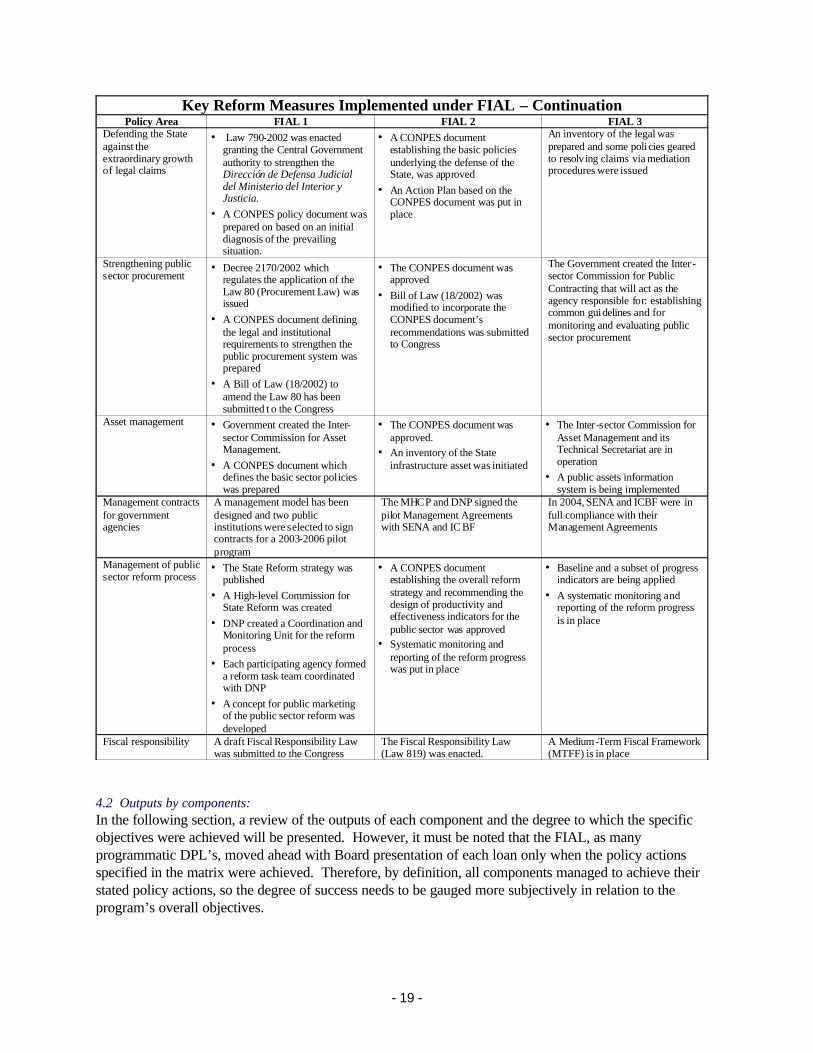

Key Reform Measures Implemented under FIAL Policy Area FIAL 1 FIAL 2 FIAL 3

Overall fiscal commitment

A fiscal adjustment program was put in place and the overall deficit of the Combined Public Sector did not exceed US$ 1,352,000,000 for any 3 continuous months among the 12 months preceding withdrawals from the Loan Account

The execution of the National Central Government Budget for the year 2003, prior to disbursements under the second loan, had not exceeded 75% of the overall deficit limit in said budget

The execution of the 2004 Budget of the National Central Government through the end of the third quarter was in line with the overall deficit limits in the approved budget. The overall deficit of the Combined Pubic Sector through the third quarter of 2004 was consistent with an annual deficit of 2.3% of the GDP for said year. The overall debt to GDP ratio was below 47% of GDP

Tax Reform Government enacted the Tax Reform Law 788 of 2002

Government issued 18 Decrees to regulate the application of the Law 788 / 2002.

The new Tax Reform Law 863, which accelerates the phase-out of exemptions, was enacted on December 2003

Tax Administration • DIAN renegotiated service rates with its providers reducing its operational cost.

• 15 Decrees were issued to regulate fiscal evasion, fraud, and to clarify and facilitate the application of the Tax Code

• DIAN developed and implemented software to cross reference information with financial institutions to ensure proper monitoring of taxpayer statements

• DIAN increased its audit capacity to the taxpayers and audited 50% of large taxpayers

• DIAN established and published indicators of the cost and time required for filing compliance by taxpayers

• DIAN established procedures to carry integrated tax and custom audits (over 80 integrated audits were carried out)

• The DIAN administrative did not exceed 0.96% of DIAN tax collections

• Improvements in tax administration produced al least 0.3% of GDP from 2003-2004

Budget Management A constitutional reform giving the Executive Branch the authority to control and manage the budget was presented to and approved by Congress in first round

• CONPES approved the terms of the budgetary reform

• The Government submitted the Bill of Law for the 2004 Budget Law to Congress incorporating a medium-term fiscal outlook; the calculation of tax expenditures and contingent liabilities, and a presentation by functions that integrates current and capital expenditures

The Bill of Law with the new Organic Budget Code was submitted to Congress

Development of incentives for efficiency gains

The Government enacted a law to enable Constitutional Referendum for transfer royalties to educational services

• The Government submitted to Referendum a constitutional amendment to transfer royalties to educational services

• The Ministry of Education issued Decree 277 2003 establishing priority and eligibility criteria to use funds originating from Law 21/1982 for investments in educational services

The Government restructured the National Royalty Fund and allocated funds to sustain places created for new students

- 18 -

Key Reform Measures Implemented under FIAL – Continuation Policy Area FIAL 1 FIAL 2 FIAL 3

Defending the State against the extraordinary growth of legal claims

• Law 790-2002 was enacted granting the Central Government authority to strengthen the Dirección de Defensa Judicial del Ministerio del Interior y Justicia.

• A CONPES policy document was prepared on based on an initial diagnosis of the prevailing situation.

• A CONPES document establishing the basic policies underlying the defense of the State, was approved

• An Action Plan based on the CONPES document was put in place

An inventory of the legal was prepared and some policies geared to resolving claims via mediation procedures were issued

Strengthening public sector procurement

• Decree 2170/2002 which regulates the application of the Law 80 (Procurement Law) was issued

• A CONPES document defining the legal and institutional requirements to strengthen the public procurement system was prepared

• A Bill of Law (18/2002) to amend the Law 80 has been submitted t o the Congress

• The CONPES document was approved

• Bill of Law (18/2002) was modified to incorporate the CONPES document’s recommendations was submitted to Congress

The Government created the Inter -sector Commission for Public Contracting that will act as the agency responsible for: establishing common guidelines and for monitoring and evaluating public sector procurement

Asset management • Government created the Inter-sector Commission for Asset Management.

• A CONPES document which defines the basic sector policies was prepared

• The CONPES document was approved.

• An inventory of the State infrastructure asset was initiated

• The Inter -sector Commission for Asset Management and its Technical Secretariat are in operation

• A public assets information system is being implemented

Management contracts for government agencies

A management model has been designed and two public institutions were selected to sign contracts for a 2003-2006 pilot program

The MHCP and DNP signed the pilot Management Agreements with SENA and IC BF

In 2004, SENA and ICBF were in full compliance with their Management Agreements

Management of public sector reform process

• The State Reform strategy was published

• A High-level Commission for State Reform was created

• DNP created a Coordination and Monitoring Unit for the reform process

• Each participating agency formed a reform task team coordinated with DNP

• A concept for public marketing of the public sector reform was developed

• A CONPES document establishing the overall reform strategy and recommending the design of productivity and effectiveness indicators for the public sector was approved

• Systematic monitoring and reporting of the reform progress was put in place

• Baseline and a subset of progress indicators are being applied

• A systematic monitoring and reporting of the reform progress is in place

Fiscal responsibility A draft Fiscal Responsibility Law was submitted to the Congress

The Fiscal Responsibility Law (Law 819) was enacted.

A Medium-Term Fiscal Framework (MTFF) is in place

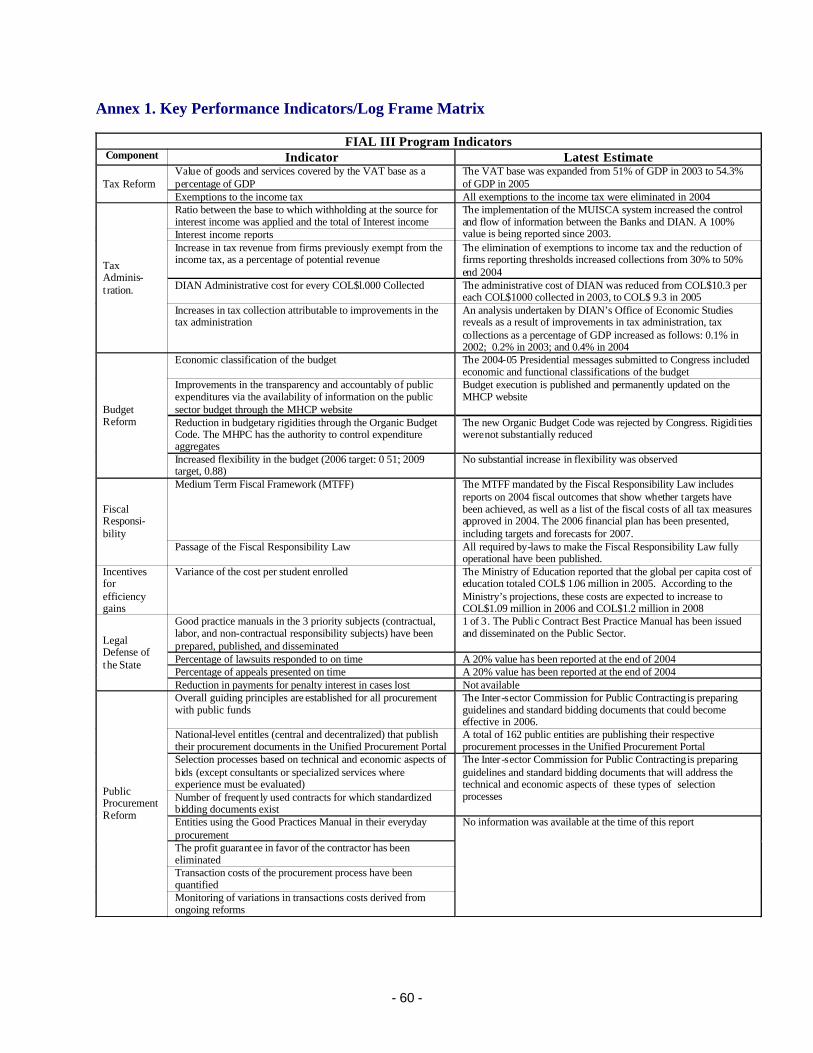

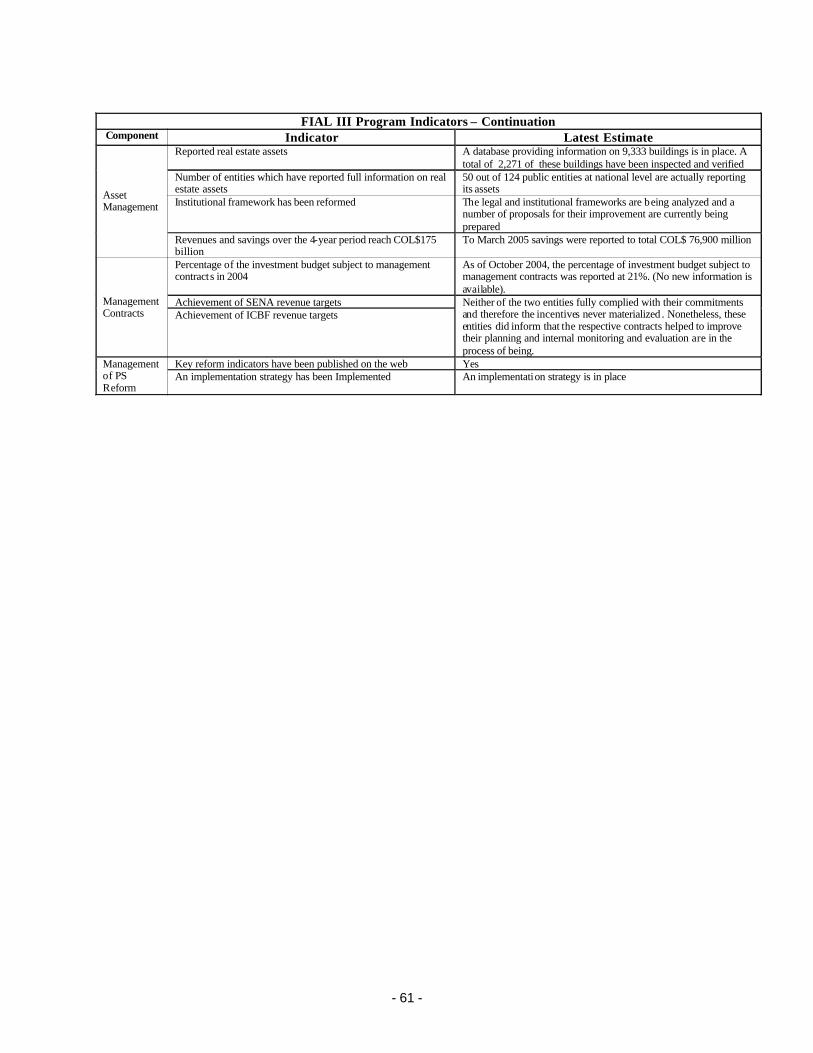

4.2 Outputs by components:In the following section, a review of the outputs of each component and the degree to which the specific objectives were achieved will be presented. However, it must be noted that the FIAL, as many programmatic DPL’s, moved ahead with Board presentation of each loan only when the policy actions specified in the matrix were achieved. Therefore, by definition, all components managed to achieve their stated policy actions, so the degree of success needs to be gauged more subjectively in relation to the program’s overall objectives.

- 19 -

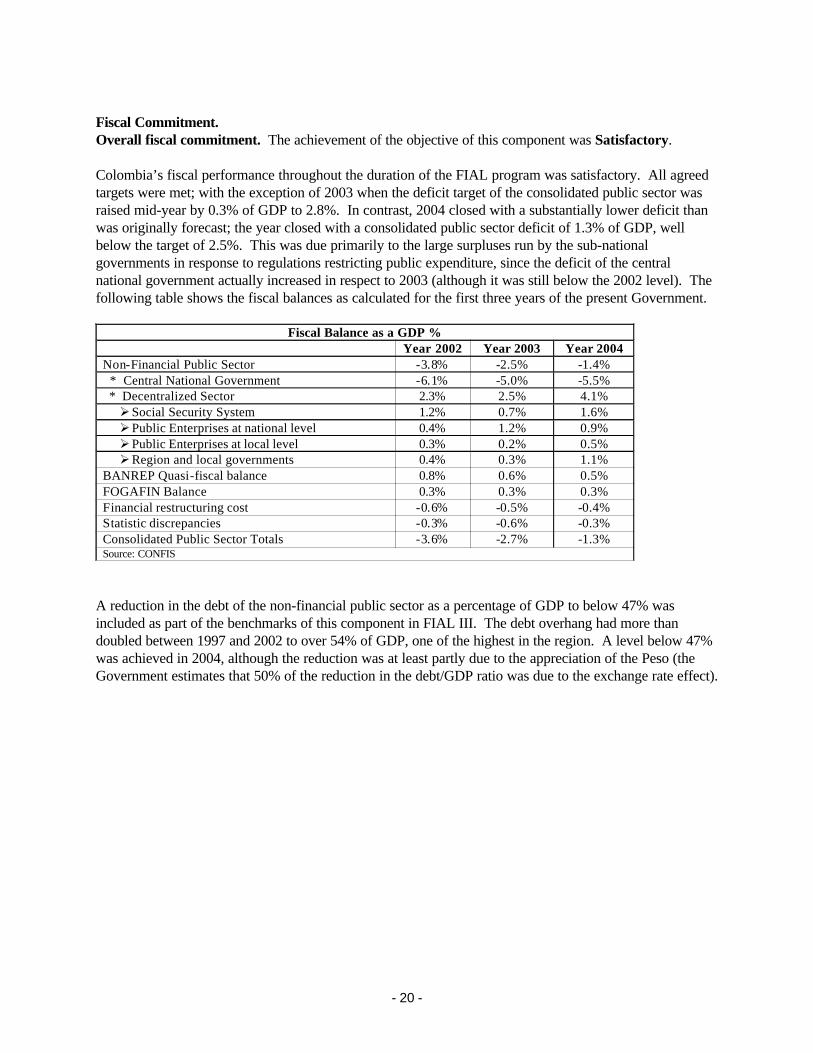

Fiscal Commitment.Overall fiscal commitment. The achievement of the objective of this component was Satisfactory.

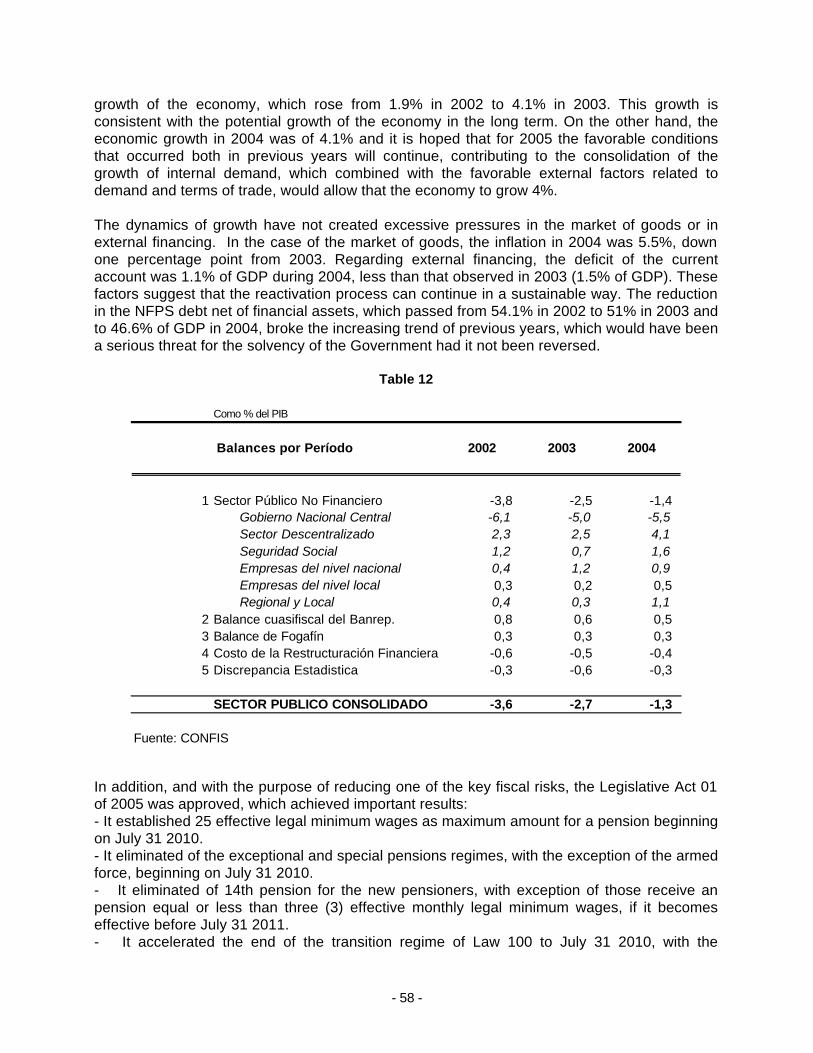

Colombia’s fiscal performance throughout the duration of the FIAL program was satisfactory. All agreed targets were met; with the exception of 2003 when the deficit target of the consolidated public sector was raised mid-year by 0.3% of GDP to 2.8%. In contrast, 2004 closed with a substantially lower deficit than was originally forecast; the year closed with a consolidated public sector deficit of 1.3% of GDP, well below the target of 2.5%. This was due primarily to the large surpluses run by the sub-national governments in response to regulations restricting public expenditure, since the deficit of the central national government actually increased in respect to 2003 (although it was still below the 2002 level). The following table shows the fiscal balances as calculated for the first three years of the present Government.

Fiscal Balance as a GDP % Year 2002 Year 2003 Year 2004 Non-Financial Public Sector -3.8% -2.5% -1.4% * Central National Government -6.1% -5.0% -5.5% * Decentralized Sector 2.3% 2.5% 4.1% Ø Social Security System 1.2% 0.7% 1.6% Ø Public Enterprises at national level 0.4% 1.2% 0.9% Ø Public Enterprises at local level 0.3% 0.2% 0.5% Ø Region and local governments 0.4% 0.3% 1.1%

BANREP Quasi-fiscal balance 0.8% 0.6% 0.5% FOGAFIN Balance 0.3% 0.3% 0.3% Financial restructuring cost -0.6% -0.5% -0.4% Statistic discrepancies -0.3% -0.6% -0.3% Consolidated Public Sector Totals -3.6% -2.7% -1.3% Source: CONFIS

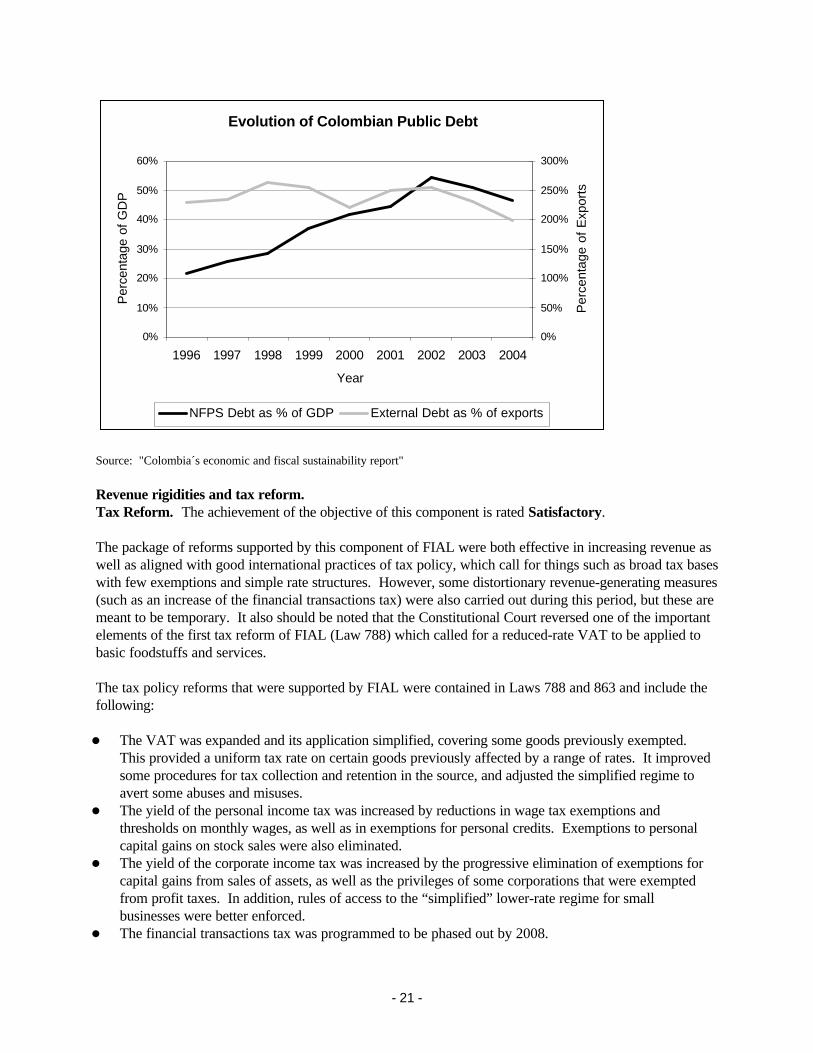

A reduction in the debt of the non-financial public sector as a percentage of GDP to below 47% was included as part of the benchmarks of this component in FIAL III. The debt overhang had more than doubled between 1997 and 2002 to over 54% of GDP, one of the highest in the region. A level below 47% was achieved in 2004, although the reduction was at least partly due to the appreciation of the Peso (the Government estimates that 50% of the reduction in the debt/GDP ratio was due to the exchange rate effect).

- 20 -

Evolution of Colombian Public Debt

0%

10%

20%

30%

40%

50%

60%

1996 1997 1998 1999 2000 2001 2002 2003 2004

Year

Per

cent

age

of G

DP

0%

50%

100%

150%

200%

250%

300%

Per

cent

age

of E

xpor

ts

NFPS Debt as % of GDP External Debt as % of exports

Source: "Colombia´s economic and fiscal sustainability report"

Revenue rigidities and tax reform.Tax Reform. The achievement of the objective of this component is rated Satisfactory.

The package of reforms supported by this component of FIAL were both effective in increasing revenue as well as aligned with good international practices of tax policy, which call for things such as broad tax bases with few exemptions and simple rate structures. However, some distortionary revenue-generating measures (such as an increase of the financial transactions tax) were also carried out during this period, but these are meant to be temporary. It also should be noted that the Constitutional Court reversed one of the important elements of the first tax reform of FIAL (Law 788) which called for a reduced-rate VAT to be applied to basic foodstuffs and services.

The tax policy reforms that were supported by FIAL were contained in Laws 788 and 863 and include the following:

The VAT was expanded and its application simplified, covering some goods previously exempted. lThis provided a uniform tax rate on certain goods previously affected by a range of rates. It improved some procedures for tax collection and retention in the source, and adjusted the simplified regime to avert some abuses and misuses.The yield of the personal income tax was increased by reductions in wage tax exemptions and lthresholds on monthly wages, as well as in exemptions for personal credits. Exemptions to personal capital gains on stock sales were also eliminated.The yield of the corporate income tax was increased by the progressive elimination of exemptions for lcapital gains from sales of assets, as well as the privileges of some corporations that were exempted from profit taxes. In addition, rules of access to the “simplified” lower-rate regime for small businesses were better enforced.The financial transactions tax was programmed to be phased out by 2008.l

- 21 -

Sub-national tax revenue was enhanced through an adjustment of the alcohol tax in departments and ldistricts, as well as to the tax surcharge rate for transfer to sub-national governments.

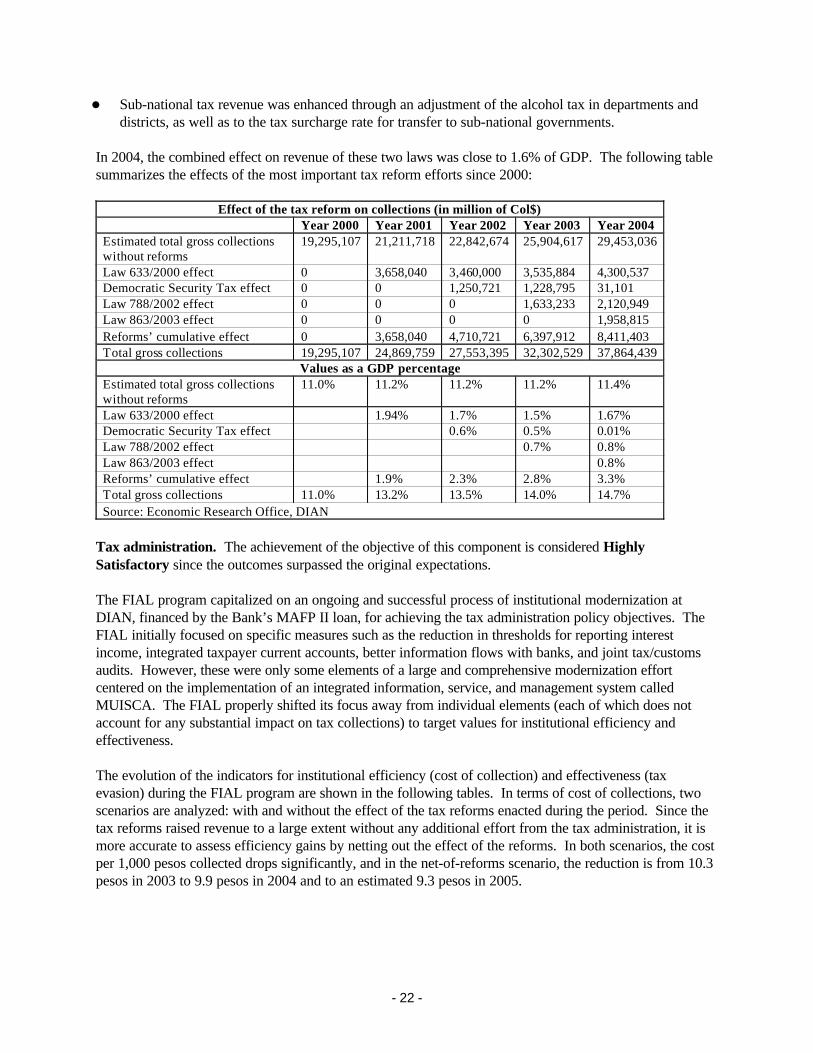

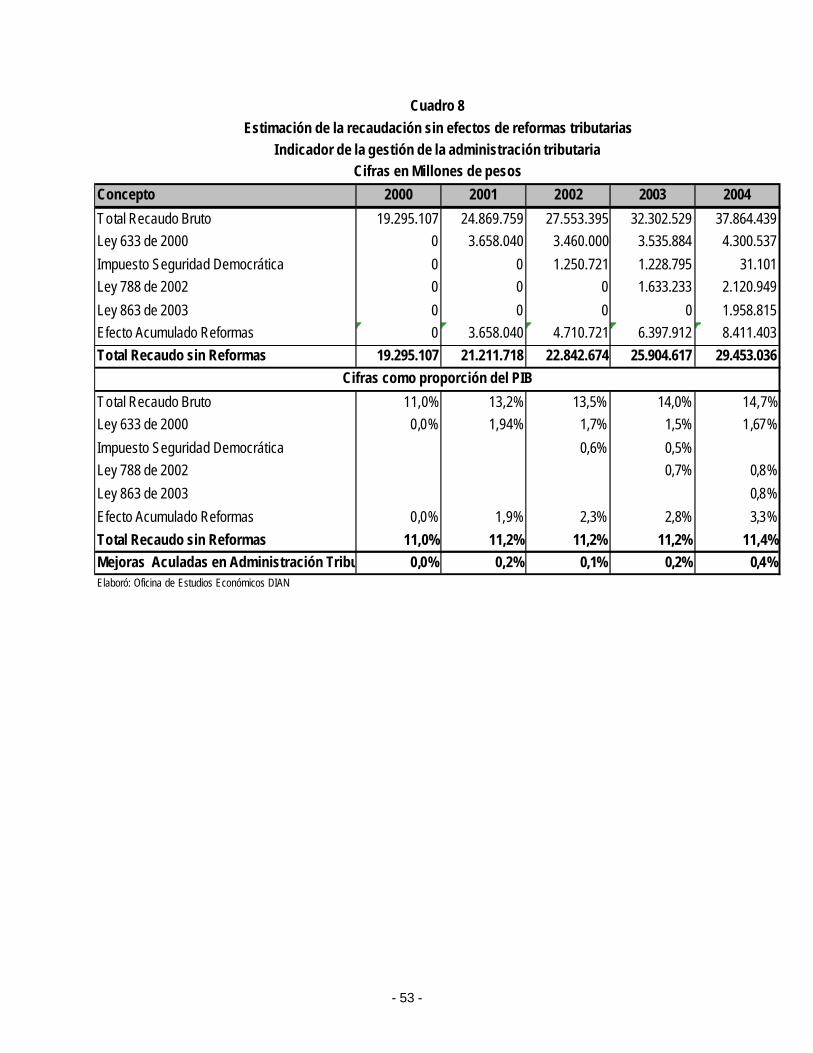

In 2004, the combined effect on revenue of these two laws was close to 1.6% of GDP. The following table summarizes the effects of the most important tax reform efforts since 2000:

Effect of the tax reform on collections (in million of Col$) Year 2000 Year 2001 Year 2002 Year 2003 Year 2004 Estimated total gross collections without reforms

19,295,107 21,211,718 22,842,674 25,904,617 29,453,036

Law 633/2000 effect 0 3,658,040 3,460,000 3,535,884 4,300,537 Democratic Security Tax effect 0 0 1,250,721 1,228,795 31,101 Law 788/2002 effect 0 0 0 1,633,233 2,120,949 Law 863/2003 effect 0 0 0 0 1,958,815 Reforms’ cumulative effect 0 3,658,040 4,710,721 6,397,912 8,411,403 Total gross collections 19,295,107 24,869,759 27,553,395 32,302,529 37,864,439

Values as a GDP percentage Estimated total gross collections without reforms

11.0% 11.2% 11.2% 11.2% 11.4%

Law 633/2000 effect 1.94% 1.7% 1.5% 1.67% Democratic Security Tax effect 0.6% 0.5% 0.01% Law 788/2002 effect 0.7% 0.8% Law 863/2003 effect 0.8% Reforms’ cumulative effect 1.9% 2.3% 2.8% 3.3% Total gross collections 11.0% 13.2% 13.5% 14.0% 14.7% Source: Economic Research Office, DIAN

Tax administration. The achievement of the objective of this component is considered Highly Satisfactory since the outcomes surpassed the original expectations.

The FIAL program capitalized on an ongoing and successful process of institutional modernization at DIAN, financed by the Bank’s MAFP II loan, for achieving the tax administration policy objectives. The FIAL initially focused on specific measures such as the reduction in thresholds for reporting interest income, integrated taxpayer current accounts, better information flows with banks, and joint tax/customs audits. However, these were only some elements of a large and comprehensive modernization effort centered on the implementation of an integrated information, service, and management system called MUISCA. The FIAL properly shifted its focus away from individual elements (each of which does not account for any substantial impact on tax collections) to target values for institutional efficiency and effectiveness.

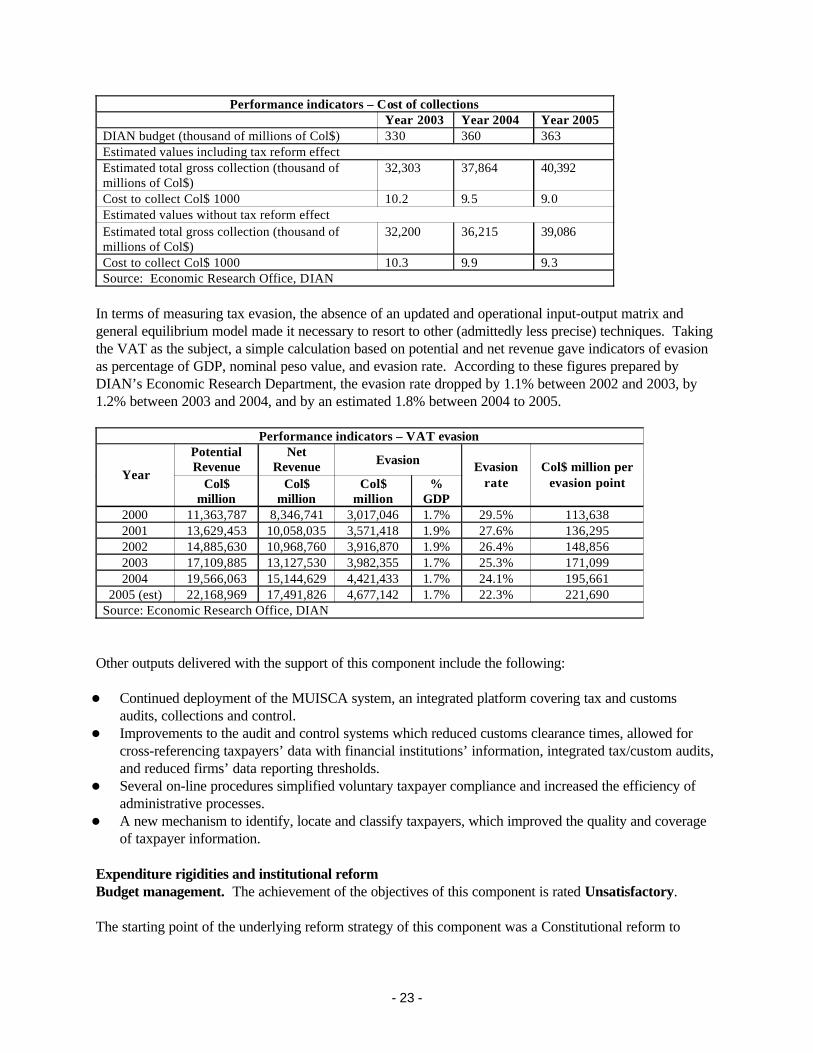

The evolution of the indicators for institutional efficiency (cost of collection) and effectiveness (tax evasion) during the FIAL program are shown in the following tables. In terms of cost of collections, two scenarios are analyzed: with and without the effect of the tax reforms enacted during the period. Since the tax reforms raised revenue to a large extent without any additional effort from the tax administration, it is more accurate to assess efficiency gains by netting out the effect of the reforms. In both scenarios, the cost per 1,000 pesos collected drops significantly, and in the net-of-reforms scenario, the reduction is from 10.3 pesos in 2003 to 9.9 pesos in 2004 and to an estimated 9.3 pesos in 2005.

- 22 -

Performance indicators – Cost of collections Year 2003 Year 2004 Year 2005 DIAN budget (thousand of millions of Col$) 330 360 363 Estimated values including tax reform effect Estimated total gross collection (thousand of millions of Col$)

32,303 37,864 40,392

Cost to collect Col$ 1000 10.2 9.5 9.0 Estimated values without tax reform effect Estimated total gross collection (thousand of millions of Col$)

32,200 36,215 39,086

Cost to collect Col$ 1000 10.3 9.9 9.3 Source: Economic Research Office, DIAN

In terms of measuring tax evasion, the absence of an updated and operational input-output matrix and general equilibrium model made it necessary to resort to other (admittedly less precise) techniques. Taking the VAT as the subject, a simple calculation based on potential and net revenue gave indicators of evasion as percentage of GDP, nominal peso value, and evasion rate. According to these figures prepared by DIAN’s Economic Research Department, the evasion rate dropped by 1.1% between 2002 and 2003, by 1.2% between 2003 and 2004, and by an estimated 1.8% between 2004 to 2005.

Performance indicators – VAT evasion Potential Revenue

Net Revenue Evasion

Year Col$

million Col$

million Col$

million %

GDP

Evasion rate

Col$ million per evasion point

2000 11,363,787 8,346,741 3,017,046 1.7% 29.5% 113,638 2001 13,629,453 10,058,035 3,571,418 1.9% 27.6% 136,295 2002 14,885,630 10,968,760 3,916,870 1.9% 26.4% 148,856 2003 17,109,885 13,127,530 3,982,355 1.7% 25.3% 171,099 2004 19,566,063 15,144,629 4,421,433 1.7% 24.1% 195,661

2005 (est) 22,168,969 17,491,826 4,677,142 1.7% 22.3% 221,690 Source: Economic Research Office, DIAN

Other outputs delivered with the support of this component include the following:

Continued deployment of the MUISCA system, an integrated platform covering tax and customs laudits, collections and control.Improvements to the audit and control systems which reduced customs clearance times, allowed for lcross-referencing taxpayers’ data with financial institutions’ information, integrated tax/custom audits, and reduced firms’ data reporting thresholds.Several on-line procedures simplified voluntary taxpayer compliance and increased the efficiency of ladministrative processes.A new mechanism to identify, locate and classify taxpayers, which improved the quality and coverage lof taxpayer information.

Expenditure rigidities and institutional reform Budget management. The achievement of the objectives of this component is rated Unsatisfactory.

The starting point of the underlying reform strategy of this component was a Constitutional reform to

- 23 -

restore the authority of the executive branch (or more specifically, to the MHCP) to regulate expenditure aggregates. The Acuerdo Legislativo to carry this out was thrown out by the Senate in July 2003, a few months after the approval of FIAL I. A second attempt at Constitutional reform was made via the October 2003 Referendum, this time to reduce expenditure rigidities through major reforms in the pensions system, implementing a freeze on recurrent expenditures, especially wages, and shutting down certain public sector entities. This attempt failed as well.

As agreed with both the Bank and the IMF, the Government proceeded to submit to Congress a new version of the public sector’s budget code (Estatuto Orgánico de Presupuesto, or EOP) in December 2003. The bill contained important measures such as the redefinition of social expenditure, a revised budgetary classification, improved monitoring and evaluation, control of forward budgets, and a medium-term expenditure framework, among others. The EOP lingered in Congress for over a year, and was eventually “archived” (or dismissed without being approved) in early 2005.

Even without the above-mentioned structural reforms, the Ministry of Finance did manage to make some improvements to the quality of the budget. Furthermore, it is now working closely with the IMF on an executive decree that will make up at least some of the ground lost with the dismissal of the EOP bill. Among the improvements that have been observed so far are:

Improved transparency through a budget information portal in the MHCP’s websitelThe budget submitted to Congress now includes a comprehensive explanation of many of its functional, lfinancial and economic elements, as well as a debt sustainability analysis and an analysis of budgetary rigiditiesBudget preparation is now done on-line, reducing transaction costs for spending agencieslThe budget itself is of higher quality, as was shown by the fact that there were no budget amendments lin 2005

Development of incentives for efficiency gains. The achievement of the objective of this component is considered Moderately Satisfactory.

The central element for achieving a structural reform to the way royalty funds are managed was the 2003 Referendum, which contained a question proposing their explicit distribution for education (56%), sanitation (36%), a sub-national pension fund (7%), and the conservation of the Cauca river (1%). This measure was meant to counteract what was widely perceived as corrupt and inefficient use of these funds, often in poorly planned or otherwise inappropriate investment projects. Existing laws (especially Law 715) established efficiency and accountability standards for decentralized services, so by earmarking funds for these services, there was the expectation of improved value-for-money.

The failure of the Referendum prevented this rule to be hard-wired into the Constitution. Nevertheless, as an alternative measure, the Government decided to have DNP “absorb” the management of the National Royalties Fund, fostering a better planning environment and responsiveness to local priorities. This enabled the Government to reallocate funds to enroll approximately 30,000 new students in 2003 and some 12,000 more in 2004.