Embed Size (px)

Citation preview

NORWEGIAN SCHOOL OF ECONOMICS

Bergen, Spring 2015

The use of awareness as a tool to mitigate biases

related to source credibility

-An experimental study

Idil Mahamed Abdi and Sultan Ul Arfeen

Thesis Advisor: Jonas Gaudernack

Master thesis, Regnskap og revisjon

NORWEGIAN SCHOOL OF ECONOMICS

This thesis was written as a part of the Master of Accounting and Auditing at NHH. Please

note that neither the institution nor the examiners are responsible − through the approval of

this thesis − for the theories and methods used, or results and conclusions drawn in this work.

2

Abstract:

Auditors have to rely on their professional judgment regularly while performing different

tasks in an audit. In some areas of audit the quality of their professional judgment is of very

sensitive nature and FVMs (fair value measurements) has been identified as one of them by

PCAOB (Public company accounting oversight board)

This study examines the relationship between source credibility and professional judgment of

auditors (students as surrogates) when awareness is applied as a tool to improve the judgment

quality. In Advertising and marketing previous studies have used awareness as a tool to

improve advertisement effectiveness but this study uses this tool to improve auditors’

professional judgment quality, which may contribute to the literature. This study has used

students of Norwegian School of Economics (NHH) as surrogates; it was made sure that

participating students have the necessary skills and knowledge to contribute to the study.

Data was collected from a population of 300 students who had taken intensive courses in

auditing and accounting at master’s level. The findings show that awareness has a significant

impact on professional judgment of auditors.

Key words: Source credibility, Awareness, Professional Judgment.

3

Abbreviation list:

PCAOB, Public company accounting oversight board

FVMs, Fair value measurements

JDM Judgment and decision-making

ISA International Standard on Auditing

HSM Heuristic-systematic model

NHH, Norwegian school of economics

4

Preface This thesis is part of our Master degree program MRR (Master in Accounting and Auditing)

at Norwegian School of Economics. This study is an experimental study that is carried out

with the help of Qualtrics, which is quite well known research tool. The target of our efforts

was to find out if awareness could be used as a measure to mitigate biases in professional

judgment towards source credibility in complex audit settings. We have tried to obtain

empirical evidence through an experiment, to see if awareness can reduce the auditors’

tendency of overreliance on expert valuations in areas where they lack expertise. The

experiment was carried out in May 2015 among students of MRR at Norwegian school of

Economics through Qualtrics.

We would like to pay our sincere gratitude to our supervisor, Jonas Gaudernack, for his

immense support and guidance throughout this thesis. Without his advices and personal

interest, the completion of this thesis was impossible. Special thanks also goes to all the

fellow students who participated in the study and gave their valuable support for this thesis.

Bergen , June 2015

Idil Abdi and Sultan ul Arfeen

5

Table of Contents

Abstract: ............................................................................................................................ 2

Abbreviation list: ............................................................................................................... 3

Preface .............................................................................................................................. 4

Table of Contents .............................................................................................................. 5

1. Introduction: .................................................................................................................. 8 1.1 Research objective and contribution of the study: ....................................................................................... 9 1.1.1 Judgment framing: ................................................................................................................................................ 10 1.1.2 Problem formulation: .......................................................................................................................................... 10

1.2 Research Question: .................................................................................................................................................. 11 1.3 Limitations of the study: ....................................................................................................................................... 11 1.4 Outline of the thesis: ............................................................................................................................................... 12 2. BACKGROUND & RELATED LITERAURE ......................................................................... 12 2.1 What is judgment and decision-‐making? ....................................................................................................... 13 2.1.1 Judgment and decision-‐making defined ...................................................................................................... 13 2.1.2 JDM Research .......................................................................................................................................................... 13 2.1.2 Heuristics and Biases Research ....................................................................................................................... 15 2.3.3 The Heuristic-‐Systematic model ..................................................................................................................... 15

2.2 Professional judgment defined ........................................................................................................................... 16 2.2.2 The KPMG Professional Judgment Framework ........................................................................................ 17 2.2.3 Judgment framing ................................................................................................................................................. 19

2.3 Source credibility ..................................................................................................................................................... 19 2.3.1 Source credibility in psychology ..................................................................................................................... 19 2.3.2 Source credibility in auditing (ISA 620) ...................................................................................................... 21 2.3.3 Reliance of experts in auditing: ....................................................................................................................... 22 2.3.4 Fair value measurement .................................................................................................................................... 22 2.3.5 PCAOB investigation ............................................................................................................................................ 24 2.3.6 Research findings of FVMs in auditing: ..................................................................................................... 26

3.1 Conceptual model and hypothesis .............................................................................. 27 3.2 Conceptual model ..................................................................................................................................................... 27 3. 2 Hypothesis .................................................................................................................................................................. 28

4. Methodology: .............................................................................................................. 30 4.1 Research approach: ................................................................................................................................................. 30 4.1.1 Experimental design of the study: .................................................................................................................. 30

4.2 Data type and research tool: ................................................................................................................................ 31 4.2.1 Time horizon: .......................................................................................................................................................... 31 4.2.2 Sample: ....................................................................................................................................................................... 31 4.2.3 Questionnaire: ......................................................................................................................................................... 32 4.2.4 Pre test and post experimental questions ................................................................................................... 34

4.3 Explanation of Variables ....................................................................................................................................... 34 4.3.1 Independent variables: ........................................................................................................................................ 34 4.3.2 Dependent variable: ............................................................................................................................................. 35

6

5. Statement of results .................................................................................................... 35 5.1 Manipulation checks ............................................................................................................................................... 35 5.2 Results ........................................................................................................................................................................... 36

6. Conclusion ................................................................................................................... 37 6.1 Answers to research question ............................................................................................................................ 37 6.2 Contribution to research ....................................................................................................................................... 38 6.3 Contribution to audit practice ............................................................................................................................ 38 6.4 Suggestions for future research ......................................................................................................................... 39

References ....................................................................................................................... 40

Appendix 1: Introduction ................................................................................................. 43

Appendix 2: Example of cases ........................................................................................... 44 Example for Expert*Awareness .................................................................................................................................. 44

Appendix 3: Post experimental survey .............................................................................. 48

Tables .............................................................................................................................. 50 Table 1: ................................................................................................................................................................................. 50 Table 2: ................................................................................................................................................................................. 50 Table 3: ................................................................................................................................................................................. 51 Table 4 .................................................................................................................................................................................. 52 Table 5: ................................................................................................................................................................................. 52

7

8

1. Introduction:

Professional judgment is a matter of considerable interest for both academics and

practitioners in the world of auditing and accounting services. A very decent amount of

literature has focused on the judgment and decision-making research; among this literature a

lot of papers have examined the factors, which affect the professional judgment of auditors.

Auditors and audit firms have a very key role in our current financial and economical

structure; legislating bodies, regulatory authorities, investors, shareholders and creditors, use

their reports before making important decisions.

During the process of auditing and preparation of audit reports, at many instances auditors

have to rely solely on their professional judgment. The three main areas where an auditor has

to rely on their professional judgment are evaluation of evidence, estimating probabilities and

making choices between different options. However, if professional judgment is a gift or a

skill that can be acquired through practice or knowledge has remained a focus of immense

discussion in literature.

This study has utilized the Heuristic-Systematic model towards an understanding of

possibilities of improvement in the quality of professional judgment of auditors. Previous

studies have found that ‘‘additional knowledge about common threats, together with tools

and processes for making good judgments, can improve the professional judgment abilities of

both new and seasoned professionals’’ (Eilifsen, Messier, Glover, & Prawitt, 2014)

Previous experimental studies on professional judgment have mainly focused on explaining

the process of decision-making or identification of the factors that affect this process. Some

parts have been focusing on improving the professional judgment quality of auditors. The

Public Company Accounting Oversight Board (PCAOB) has shown concerns about auditing

deficiencies and impairments in auditor’s professional judgments especially regarding fair

value measurements (PCAOB 2011). Because of this current relevance to the auditing world

this study has chosen FVMs as part of the experimental investigation.

9

Can professional judgment towards fair value measurements be improved somehow? One of

the most important footsteps towards avoiding judgment traps and diminishing bias produced

by subconscious mental shortcuts is what is termed as “Awareness”. By a better

understanding of traps and biases, and recognizing common situations where they are likely

to present themselves, we can identify potential problems and often formulate logical steps to

improve our judgment.

The purpose of this study is to determine if awareness can be used as a tool to improve the

professional judgment of auditors specially while evaluating authenticity of FVMs provided

through two different sources i.e. independent valuation specialists and in house managers.

1.1 Research objective and contribution of the study:

The main objective of this study is to contribute to the discussion in the auditing world about

improving professional judgment, specifically regarding complex accounting estimates where

auditors have to rely on the works of others. Auditing standards require auditors to perform

procedures to obtain evidence supporting expert’s opinion. However in reality research

suggests that auditors over rely on third part expert opinion especially in areas where auditors

lack expertise and experience. This study looks at how this bias can be mitigated?

This study is going to perform an experimental investigation of one of the possible factors,

which can help auditors improve their professional judgment in situations where there is

maximum risk of overreliance and blind trust on expert´s work. By observing how awareness

moderates the relationship between source credibility and professional judgment, this study

can contribute to the efforts of improving judgment quality in areas that are on the top of

PCAOBs concerns list.

10

1.1.1 Judgment framing:

This study assumes a judgment setting where the auditors or judges are exposed to fair value

measurements (FVMs) and are asked to assess inherent risk on a given scale from 1 to 7.

Subjects will be divided into three treatment conditions: Expert, In-house and Expert with

awareness. In regards to subjects in the third-party expert condition, Half of participants are

made aware about what can possibly go wrong and the other half were free to make their

judgments in normal manner.

1.1.2 Problem formulation:

Unfortunately this study is not taking into account all the factors, which can affect the

professional judgment of auditors. For the purpose of this study we have taken PCAOBs

concern list as a guideline and identified professional judgment quality towards source

credibility of FVMs as an area of interest.

PCAOB has identified fair value measurement (FVM) as an area with huge increase in audit

deficiencies. This is related to the measurement of certain assets especially the price

determination of complex financial instruments. Fair value measurements and impairment

audit shortcomings are specifically significant as these two specific issues are responsible for

more than half of all latest audit deficiencies (PCAOB 2011).

In order to contribute to the discussion we have focused on collecting and analyzing

empirical evidence pertaining to the moderating role of awareness, in a setting where

professional judgment quality towards source credibility is evaluated. For the study we have

considered the inherent risk assessment as proxy for professional judgment quality. PCAOBs

reports are very clear about source of FVMs i.e. 3rd party evaluation experts but we have

added an additional dimension of in-house prepared FVMs as well to observe variations in

both cases.

11

Despite the importance of this issue, there is only limited empirical evidence available

relating to factors which can act as a catalyst to improve judgment quality in complex audit

settings. This thesis aims on contributing to the literature by examining the impact of the

awareness on mitigating judgment biases and improving professional judgment quality in

settings where auditors lack expertise and experience. It will be interesting to see whether and

how the relationship between source credibility and professional judgment quality differs

after the introduction of a tool called awareness, which has successfully been used in other

socio-psychological research studies to improve behavioral judgments.

Based on the above narrative we have arrived at the following research question

1.2 Research Question:

Can awareness be used as tool to help mitigate biases related to source credibility?

1.3 Limitations of the study:

Unfortunately due to the time constraint and the limited resources available it was not

feasible to access practicing auditors as subjects for the study. The data have been collected

from the NHH students who are studying auditing and accounting at an advanced level and

have all the necessary skills and knowledge required to take part in the study. The use of

students as surrogates has been supported by previous research where students and business

professionals made very similar judgments in decision-making studies (Ashton and Kramer

1980).

This study is a cross sectional study and the data is collected over a time period of 7 days.

Data is collected only from the students of NHH who have gone through the courses, which

provide essential knowledge base and skills required for taking part in the study. So if any

other researcher uses different set of subjects i.e. auditors with many years of experience and

longitudinal data he or she may arrive at different results.

12

The study is limited to few variables i.e. source credibility, professional judgment and

awareness. Hence results cannot be applied to all the situations where one of the given

variables is present but others are changed. Awareness can exhibit a different role in a

situation where there are many independent variables and dependent variables.

1.4 Outline of the thesis:

The rest of the thesis is organized as follows: Section two is an overview of related theories

and judgment and decision making literature relevant to the study. Section three further

develops the conceptual model and proposes the hypotheses for the study. Section four

describes the experimental design, sample, questionnaire and pretesting of the data collection

instrument.. Section five is a description of the statistical results from the data collected.

Section six is the final part of the study, which includes our conclusion and a discussion

about limitations, implications and suggestions for future research.

2. BACKGROUND & RELATED LITERAURE

This chapter serves as a backdrop for the empirical section and a foundation for discussion

and analysis throughout this thesis. This thesis is rooted in the area of judgment and decision-

making, therefore we will briefly define judgment and decision-making (JDM). We will also

include previous JDM research in accounting and auditing. Second, we will define and

summarize heuristics and biases research, which is our topic of choice in JDM research.

Third, we will define and discuss both professional judgment and source credibility.

13

2.1 What is judgment and decision-making?

2.1.1 Judgment and decision-making defined

The term judgment refers to “forming an idea, opinion, or estimate about an object, an event,

a state, or another type of phenomenon (Bonner, 1999, p. 385). In the dictionary the term

decision is defined as a “choice made between alternative courses of action in a situation of

uncertainty” The two terms are interlinked, it is said that generally decisions usually follow

judgments, meaning that judgment usually refers to the process of estimating outcomes and

their consequences…while decision-making involves an evaluation of these consequences

which leads to a choice among the alternatives ( (Trotman, Tan, & Ang, 2011, p. 279)

In auditing and accounting, judgment occurs in three areas.

1. Evaluation of evidence: e.g. assessing when a sufficient amount of appropriate

evidence has been obtained in order to determine the fairness of management´s

assertions.

2. Estimating probabilities: e.g. determining whether the probability-weighted cash

flows used by a company to determine the recoverability of long-lived assets are

reasonable.

3. Deciding between options: e.g. deciding between audit procedures to determine if

specific audit assertions are being met.

2.1.2 JDM Research

Since the mid 1970´s accounting and auditing researchers have focused more and more on

understanding individual and group judgments and decisions. The first study to

systematically examine auditor´s judgments was Ashton in 1974. Ashton´s research

examined experienced auditors judge the strength of a hypothetical client’s internal controls

14

in the payroll system based on six cues. Since then, thousands and thousands of JDM studies

have surfaced.

The aim of JDM research is to be descriptive, prescriptive and normative. This means that

JDM research in auditing; JDM research is intended to “describe how and how well auditors

make audit decisions and improving the judgments of auditors, preparers and users of

accounting information” (Trotman, Tan, & Ang, 2011, p. 279)

JDM research is often called experimental psychology, the reason for that is that the most

common method of understanding auditor judgments is through the use of experiments.

The main benefits of experiments are that the researcher creates the setting for the

experiment, manipulates the independent variables of choice, and examines the effect on

dependent variable while controlling the effect of any confounding variables. Experimental

design has an advantage that it can study the conditions, which either don’t exist or exist in an

insufficient volume or magnitude. Experimental design allows strong interferences to be

made and studied (Trotman, Tan et al. 2011). Research about JDM can then be defined as

research that focuses on factors of judgment and decisions as either dependent or independent

variables.

But why is judgment and decision-making in auditing so important and why should we bother

to studying it? Well there are both practical and theoretical reasons for studying JDM. From

a practical perspective financial statement audits have a very critical role for our economy

and important decisions depend on the results of such audits. Accounting at its core is about

the judgment and decision-making (JDM) of individuals such as investors, managers, and

auditors.

15

2.1.2 Heuristics and Biases Research

During the late 1970´s Amos Tversky and Daniel Kahneman developed a theory that

reformed JDM research, as a summarization this theory states that in general “people rely on

a limited number of heuristic principles which reduce the complex tasks of assessing

probabilities and predicting values to simpler judgmental operations" (Tversky &

Kahneman, 1974, p. 1124).

As we´ve referenced before the purpose of JDM research is to understand puzzling human

judgment and behavior. Kahneman and Tveraky's research has sparked a flame in the world

of psychology, since the 1970´s more and more researchers have adapted and applied

Kahneman and Tveraky's theory. The popularity hasn’t stopped with just psychology the

writer McKean states that “Kahneman and Tveraky's research has resulted in a theory that

provides a systematic explanation for some of the most puzzling aspects of human behavior,

and spearheaded the growth of a new discipline of science devoted to the behavioral aspects

of decision making.. Kahneman and Tveraky’s work has begun to attract the attention of a

wider audience such as doctors, lawyers, businessmen, and politicians, who see applications

for it in choosing therapies, devising legal arguments and corporate strategies, even

conducting foreign affairs." (McKean, 1985, p. 23)

As a result of this growing popularity, behavioral auditing researchers have developed an

interest in cognitive heuristics and biases.

Ashton (1983, p.34) concluded that, "the research on heuristics and biases in audit decision-

making has been somewhat limited and the results have been mixed”.

2.3.3 The Heuristic-Systematic model

The Heuristic-Systematic model was developed in 1980 by a social physiologist named

Shelly Chaiken. The model attempts to explain how individuals receive and process

persuasive messages.

16

Based on Chaiken’s model, there are two ways of processing a message, a heuristic approach

and a systematic approach. “Heuristic processing involves the use of judgmental rules known

as knowledge structures that are learned and stored in memory” (Chen, Duckworth, &

Chaiken, 1990). For example, people might have learned that messages from experts are

more valid, then those with less expertise. Or that people might agree more with long and

detailed arguments.

According to a systematic view, individuals exerts more cognitive efforts when processing

information, they evaluate the true merits of the information provided. “Judgment formed on

the basis of a systematic processing involves a relatively in-depth treatment of judgment-

relevant information” (Chen, Duckworth, & Chaiken, 1990).

Both heuristic and systematic processing can co-occur. Chaiken and Maheswaran (1994)

conducted a study, which showed that “source credibility affects the decision makers’

perception of the persuasion of the information through its impact on the importance of

systematic processing” (Chaiken & Maheswaran, 1994). This means that heuristics can effect

systematic processing.

This study adapts the Heuristic-Systematic model to understand the underlying influences of

professional judgment in order to effectively identify how to improve the quality of

professional judgment of auditors.

2.2 Professional judgment defined

Professional judgment is a requirement in so many fields, like the government, the legal

system or medicine. Basically any work environment where professionals need to make

important daily decisions.

According to the International Standard on Auditing 200 (ISA 200), professional judgment is

defined as “the application of relevant training, knowledge and experience, within the

17

context provided by auditing, accounting and ethical standards, in making informed

decisions about the courses of action that are appropriate in the circumstances of the audit

engagement”.

As an accounting and auditing student, you often find your instructor referring to

professional judgment as answers to auditing questions. In fact many auditing task require

decisions based on professional judgment and seeing that auditors are held liable for their

decisions, it is therefore important to understand the mechanics of good judgment.

Some believe that good judgment is a gift, either you have it or you don’t. Others believe that

good judgment is a skill that can be learned and improved with knowledge and practice.

Previous studies indicate that “additional knowledge about common threats, together with

tools and processes for making good judgments, can improve the professional judgment

abilities of both new and seasoned professionals” (Eilifsen, Messier, Glover, & Prawitt,

2014).

So based on previous studies, there seems to be hope for accountant and auditors to

develop/improve good professional judgment. Therefore KPMG has developed a monograph

that will help understand the underlying causes of good judgment in order to improve the

professional judgment of auditors. The monograph is titled Elevating Professional Judgment

in Auditing and Accounting: The KPMG Professional Judgment Framework. The contents of

this monograph sparked the initial idea for this thesis.

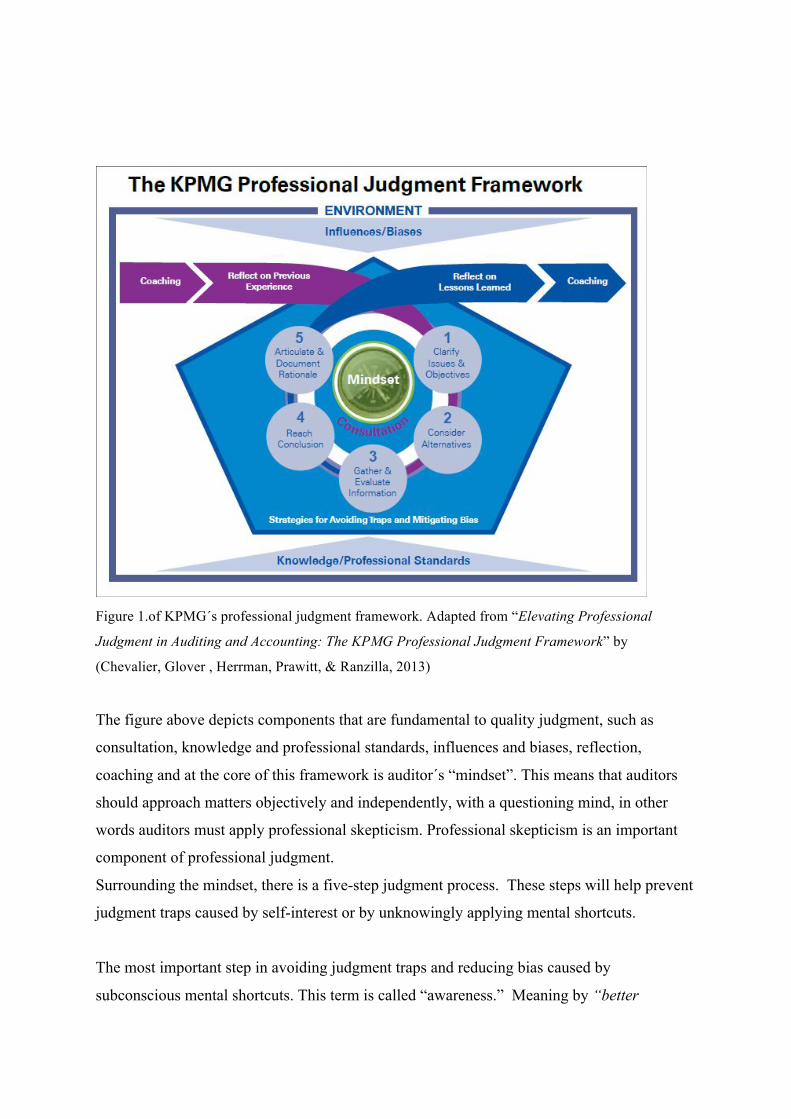

2.2.2 The KPMG Professional Judgment Framework

The monograph includes KPMG´s professional judgment framework. This framework was

developed to help auditors navigate through complex and uncertain tasks.

18

Figure 1.of KPMG´s professional judgment framework. Adapted from “Elevating Professional

Judgment in Auditing and Accounting: The KPMG Professional Judgment Framework” by

(Chevalier, Glover , Herrman, Prawitt, & Ranzilla, 2013)

The figure above depicts components that are fundamental to quality judgment, such as

consultation, knowledge and professional standards, influences and biases, reflection,

coaching and at the core of this framework is auditor´s “mindset”. This means that auditors

should approach matters objectively and independently, with a questioning mind, in other

words auditors must apply professional skepticism. Professional skepticism is an important

component of professional judgment.

Surrounding the mindset, there is a five-step judgment process. These steps will help prevent

judgment traps caused by self-interest or by unknowingly applying mental shortcuts.

The most important step in avoiding judgment traps and reducing bias caused by

subconscious mental shortcuts. This term is called “awareness.” Meaning by “better

19

understanding traps and biases, and recognizing common situations where they are likely to

present themselves, we can identify potential problems and often formulate logical steps to

improve our judgment” (Chevalier, Glover , Herrman, Prawitt, & Ranzilla, 2013, p. 33)

Awareness enables auditors to evaluate the true merits and also helps to avoid judgment

traps. Of course, this takes practice and experience. But when auditors are armed with

awareness and understanding of these traps and biases, they can improve the quality of their

professional judgments.

2.2.3 Judgment framing

This concept relates to the early steps in the judgment process. The definition of framing

follows: “Frames are mental structures that we use, usually subconsciously, to simplify,

organize, and guide our understanding of a situation” (Chevalier, Glover , Herrman, Prawitt,

& Ranzilla, 2013). One cognitive research that we believe support this concept is the heuristic

systematic model of information processing.

2.3 Source credibility

2.3.1 Source credibility in psychology

Source credibility is a” term commonly used to imply a communicator's positive

characteristics that affect the receiver's acceptance of a message” (Ohanion, 1990). The

source credibility theory is an established theory that was first studied by Carl I. Hovland and

Walter Weiss in the early 1950´s. The theory states that individuals are more likely to be

persuaded if the communicator is perceived as an expert, trustworthy or credible. In a sense

this means that “the effectiveness of the communication is dependent on the attitude of the

audience towards the communicator” (Hovland & Weiss, 1951).

In 1961 Helbert Kelman built on Howland and Weiss´ theory and proposed a theoretical

framework that could explain what characteristics would affect the receiver's acceptance of a

message. (Kelman, 1961) narrowed it down to three characteristics.

20

• Internalization: Which occurs when the individual accepts a message that is

congruent with his/her own value system. Meaning if the individual finds the

communicator trustworthy or an expert, he/she may be more persuade to accept the

message.

• Identification: Individuals may adopt the behaviors/attitudes of others because they

whish to establish/maintain a relationship with a desired group of people/ individuals.

A common example is attractive sources compared to unattractive sources

• Compliance: Occurs when individuals accepts a message in hopes of self gain, this

could include some type of reward. Compliance also occurs if the individual accepts

a message in fear of a specific punishment.

As a result of Kelman´s framework, each of the three characteristics have been research in

later years. However there is limited research on compliance, since both reward and

punishment must be studied. Researches have had a hard time establishing mundane/realistic

rewards and punishments.

In 1978 Sternthal, Phillips, and Dholakia researched if a communicator´s characteristic could

affect the persuasiveness of a message. Specifically they studied source credibility, where

they indicated that statements from an expert source had an effect on the acceptance/rejection

of a message.

Joshua L. Wiener and John C. Mowen conducted a 2 x 3 between subjects factorial

experiment in 1986. They used source expertise and trustworthiness as manipulators. Wiener

and Mowen concluded that the experiment should that source´s message is affected by

trustworthy and/or expert sources. They also found that the level of expertise of the source

strongly influenced the participants’ perceptions

21

2.3.2 Source credibility in auditing (ISA 620)

“The essence of a financial audit is to search for and evaluation of evidence regarding the

accuracy of management´s assertions” (AICPA 1980; Goodwin 1999; AICPA 2006a).

Sources for such evidences can be credible third parties such as lawyers, valuation experts

and internal auditors. It is very common for external auditors to use the works of others, and

in most cases this allows for the external auditor to reduce their planned auditing hours.

By using the work of others the external auditor must keep in mind that he/she is solely

responsible for the audit opinion expressed. This means that the auditor must be mindful of

what he/she deems as appropriate audit evidence. The ISA (International Standard on

Auditing) 620 deals with “the auditor’s responsibilities relating to the work of an individual

or organization in a field of expertise other than accounting or auditing and when that work

is used to assist the auditor in obtaining sufficient appropriate audit evidence” (ISA 620).

The standard explains that it is the auditor´s job to determine whether there is a need to use

the work of an expert. If the auditor determines to use the work of others, then the auditor

must have an appropriate understanding of that field of expertise. Meaning that the auditor

must be able to evaluate the adequacy of that work.

In ISA 620 there are three main factors to determine the adequacy of an experts work. First

there is competence, which “relates to the nature and level of expertise of the auditor’s

expert”. Secondly there is capability, which relates to “the ability of the auditor’s expert to

exercise that competence in the circumstances of the engagement. Factors that influence

capability may include… the availability of time and resources”. Objectivity relates to the

possible “effects that bias, conflict of interest, or the influence of others may have on the

professional or business judgment of the auditor’s expert”.

22

Also the auditor should not overlie on the work of an expert and it is suggested that auditors

should perform procedures to obtain evidence to support the expert’s work. However in

practice there’s some evidence that show that auditors tend to overly on expert opinions.

Especially when the work is conducted in an area that the auditor lacks in expertise.

2.3.3 Reliance of experts in auditing:

In 2009 Jennifer Blaskovich and Natalia Mintchik, investigated how external auditors

perceive the involvement of external consultants. This study explained that since the

Sarbanes-Oxley Act of 2002, firms stated to use internal control consultant (IC consultant), to

help with compliance of accounting regulation and to guard against unexpected surprises

during the external audit. (Blaskovich & Mintchik, 2009)

Blaskovich and Mintchik hypothesis that the presence of such consultants would lead to

higher reliance on internal controls and lower budgeted audit hours. However they

manipulated management´s credibility and therefore also stated that auditor´s reliance on

internal control would be affect by the varying levels of management´s credibility.

Blaskovich and Mintchik´s experiment showed that “the involvement of the IC consultant

significantly impacts auditors’ planning decisions. Specifically, when a low credibility client

engaged an IC consultant, the auditors assessed a higher reliance on internal controls and

budgeted fewer audit hours, relative to the no consultant situation” (Blaskovich & Mintchik,

2009).

2.3.4 Fair value measurement

Recently the use of valuation specialist has been the area of investigation for the Public

Company Accounting Oversight Board (PCAOB). Especially pertaining to fair value

measurements. Auditors must have a good understanding of the accounting and auditing

frameworks associated with FMVs, however it is common for auditors to use a valuation

23

expert. It is not expected that all auditors are experts in the area of valuation, particularly

since the valuation of FVMs can be complex and judgment-based.

IFRS 13 established a framework for measuring fair value. According to IFRS 13 fair value is

defined as “the price that would be received to sell an asset or paid to transfer a liability in

an orderly transaction between market participants at the measurement date”. However

because orderly transaction between market participants may or may not be observable at

measurement date, IFRS 13 provides a hierarchy with three levels that are used to distinguish

the types of inputs used to value different types of assets and liabilities at their appropriate

fair values.

I. Level 1 inputs are quoted prices in active markets for identical assets or

liabilities that the entity can access at the measurement date.

II. Level 2 inputs are inputs other than quoted market prices 1 that are

observable for the asset or liability, either directly or indirectly. Level 2 inputs

include: quoted prices for similar assets or liabilities in active markets or

quoted prices for identical or similar assets/liabilities in markets that are not

active

III. Level 3 inputs are unobservable inputs for the asset or liability. Unobservable

inputs are used to measure fair value to the extent that relevant observable

inputs are not available, thereby allowing for situations in which there is little,

if any, market activity for the asset or liability at the measurement date. An

entity develops unobservable inputs using the best information available in the

circumstances, which might include the entity's own data, taking into account

all information about market participant assumptions that is reasonably

available

24

2.3.5 PCAOB investigation

PCAOB (Public company accounting oversight board) is an organization established by

Congress to examine the audits of public companies to make sure that interests of investors

are protected along with the public interest in the preparation of audit reports in an accurate

and independent manner.

The PCAOB keeps an oversight on public accounting firms in light of Sarbanes-Oxley Act of

2002. The inspections are tailor made to detect deficiencies in audit engagements and to

identify the shortcomings as either weakness or defect in the system of quality control put in

place by the firm. The PCAOB carries out annual inspections for over 100 issuers of audit

reports and Big 4 are among the firms that get inspected annually.

Audit Deficiency Trends

The PCAOBs reports from 2008 through 2012 indicate different trends. The ratio of deficient

audit engagements has increased manifolds since 2009. In current scenario almost one out of

three audits carries significant level of deficiencies. In 2012 yearly inspections, PCAOB

identified deficiencies in 42.5% of audits along with other related engagements; in 2009 this

percentage was 16.0% of the audits inspected.

PCAOB has identified fair value impairment (FVM) as an area with huge increase in audit

deficiencies related to the measurement of certain assets specially the price determination of

complex financial instruments.

The above-mentioned increase in audit deficiencies follows the pattern of a general increase

in overall audit deficiencies, and can be a consequence of uncertainty generated by economic

slump. Fair value measurements and impairment audit shortcomings are specifically

significant as these two specific issues explain for more than half of all latest audit

deficiencies.

25

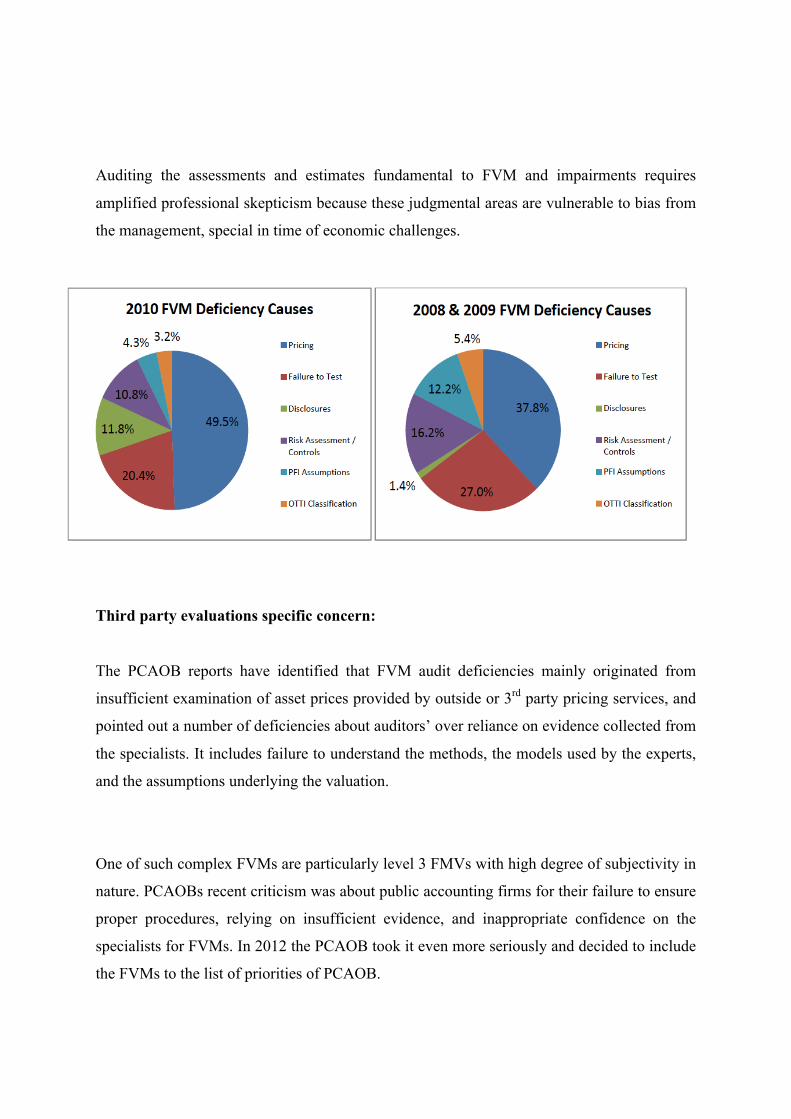

Auditing the assessments and estimates fundamental to FVM and impairments requires

amplified professional skepticism because these judgmental areas are vulnerable to bias from

the management, special in time of economic challenges.

Third party evaluations specific concern:

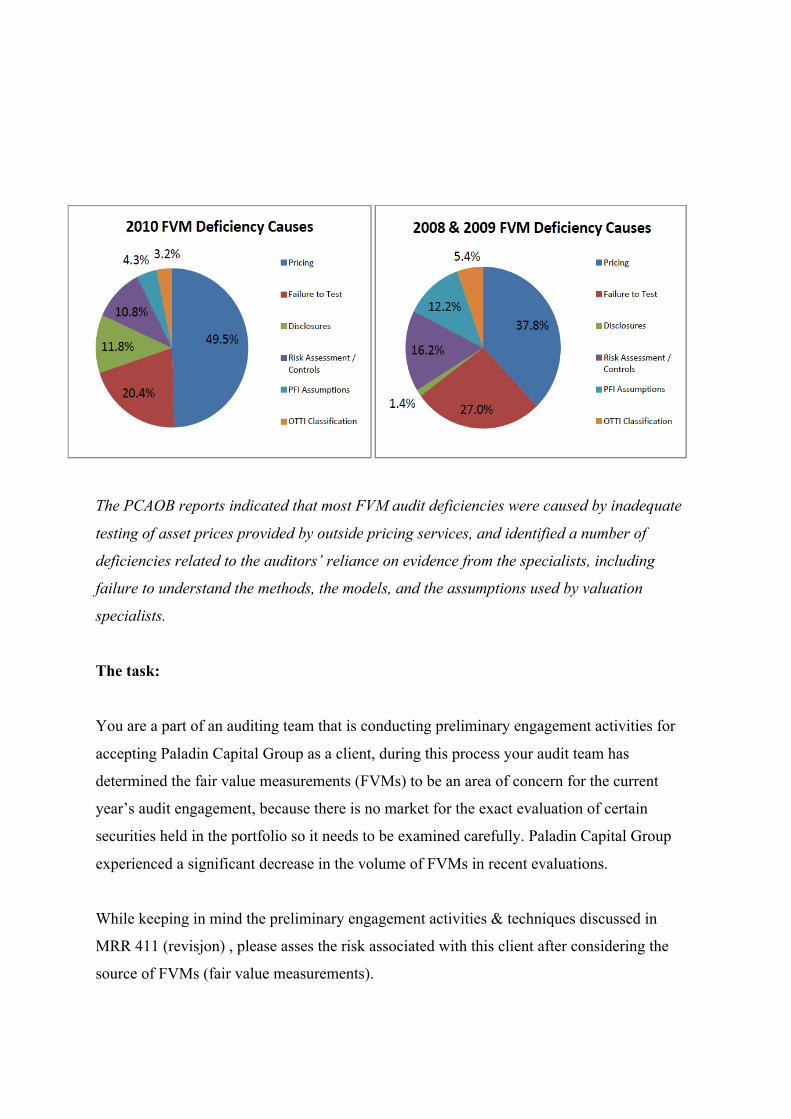

The PCAOB reports have identified that FVM audit deficiencies mainly originated from

insufficient examination of asset prices provided by outside or 3rd party pricing services, and

pointed out a number of deficiencies about auditors’ over reliance on evidence collected from

the specialists. It includes failure to understand the methods, the models used by the experts,

and the assumptions underlying the valuation.

One of such complex FVMs are particularly level 3 FMVs with high degree of subjectivity in

nature. PCAOBs recent criticism was about public accounting firms for their failure to ensure

proper procedures, relying on insufficient evidence, and inappropriate confidence on the

specialists for FVMs. In 2012 the PCAOB took it even more seriously and decided to include

the FVMs to the list of priorities of PCAOB.

26

2.3.6 Research findings of FVMs in auditing:

After the release of PCAOB´s inspection report, more researchers have conducted studies

investigating auditors’ judgments about accounting estimates. Brian Bratten, Lisa Milici

Gaynor, Linda McDaniel, Norma R. Montague and Gregory E. Sierra conducted the most

recent review of those studies in 2013.

Bratten, Gaynor, McDaniel, Montague, and Sierra (Bratten et al 2013) used Bonner´s

theoretical framework and organized their review into three categories, environmental,

personal and task. In the environmental section of this review they discussed the use of

external valuation specialists. Auditors do use pricing services, but a review of surveys

conducted showed that auditors do not believe that the use of pricing services can cause…

Bratten et all also indicated that there is a lack of empirical research, that studies the effect of

using pricing services on audit quality or perceived audit quality is lacking.

Steven M. Glover, Mark H. Taylor and Yi-Jing Wu (2014) conducted a survey to gather data

that the possible causes of the FVM expectation gap (a concept describing the differences in

what auditors and regulators consider “enough” evidence to support audits of FVMs) Glover,

Taylor and Wu surveyed 32 audit partners from five audit firms that were annually inspected

by the PCAOB. All 32 participants had experience with planning, supervising and executing

FVM audits.

Results of the survey showed 60 percent of participants suggested that the current

requirement to provide a high level of assurance that a point estimate is fairly stated within

auditor materiality be reconsidered because providing such assurance on point estimates is

unrealistic and potentially misleading given the level of subjectivity, complexity and

uncertainty. Nearly all participants (93 percent) supported the idea of revising auditing

standards to provide additional clarity and guidance around estimates characterized by

extreme measurement uncertainty (Glover, Taylor, & Wu, 2014, p. 4)

27

Emily E. Griffith, Jacqueline S. Hammersley and Kathryn Kadous interviewed 24 auditors

that all have sustainable experiences with complex accounting estimates. The main objective

of this survey was to understand the process of auditing complex accounting estimate. The

study also provided an understanding to the problems associated with this task, and also the

underlying reason for those problems.

Griffith, Hammersley and Kadous (2012) found out that an “overwhelming” amount of

auditors would test the management´s valuation process for complex estimates rather than

using an approach that relies less on management´s assertion. Griffith, Hammersley and

Kadous concluded that based on this observation this indicates “an overreliance on

management assertions, and such overreliance is corroborated by our analysis of PCAOB

inspection reports. That is, auditors sometimes fail to adequately test assumptions and data

underlying the estimation model, fail to consider controls over management’s process and

the data, and fail to fully understand the model “ (Griffith, Hammersley & Kadous , 2012)

There is a lack of empirical studies conducted as a result of PCAOB´s investigation. However

we have found the results of one particular working paper interesting. In 2014 Liburd, Mason

and Shelton examined the effect of third-party specialists and internal control effectiveness

on auditors’ assessment of risk related to auditing FVMs.

3.1 Conceptual model and hypothesis

3.2 Conceptual model

Based on Bratten et all 2013 there is a need for empirical research that studies the use of

third-party valuation specialists and factors that affect auditors’ risk assessments around

FVMs. This study examines the effect of awareness on auditors risk assessments.

28

Prior research shows an overreliance on external valuation specialist, especially complex

accounting estimates where the auditor is lacking in expertise. As stated in the KPMG

framework, there are different components that make up professional judgment, one of those

components is the biases and influences that affect an auditors professional judgment.

Liburd, Mason and Shelton found that source credibility (heuristic processing) affected

auditors risk assessment of complex FVMs. Following the HSM theory, this study examines

if awareness can affect the direction and/or strength of the relation between source credibility

and professional judgment.

3. 2 Hypothesis

This study aims to test the interaction effect of awareness on source credibility and professional

judgment. The following 2 hypotheses predict the outcome of this study.

Independent Variable: Source credibility

Dependent Variable: Professional judgment

Moderating variable: Awareness

29

Awareness ON Awareness OFF

Third-party specialist

Treatment 1= H1 Treatment 2= H2

In house manager N/A Treatment 3= H1

H1: If third-party valuation specialists provide fair value measurements and

participants are aware of PCAOB concerns, then they will assess a higher inherent risk,

than those without the PCAOB´s concerns list.

H0: Awareness has no effect on inherent risk when third-party specialist provides fair

value measurements.

H2: If a third-party valuation specialist provides fair value measurements then

participants will assess a lower inherent risk, than those provided by in-house

managers.

H0: Source cues will not have an effect on inherent risk

We believe that if individuals are provided with an understanding of the increase FVM

deficiencies, this will cause them to be more skeptics and question the credibility of the third-

part provider. By engage in a greater extent of systematic processing, participants will

evaluate the true merits of the information provided and will assess a higher inherent risk,

then those without the PCAOB´s concerns list.

A hypothesis for in-house manager with PCAOB concern list is not provided, because this

thesis aims to study the use of awareness as a tool to mitigate the biases of source credibility.

30

In summary inherent risk is predicted to be highest in treatment3 and treatment 1 will have

the lowest inherent risk. Awareness is used in H2 in order to reduce the gap between

treatment 1 and 2.

4. Methodology:

4.1 Research approach:

The focus of this master thesis is judgment and decision-making (JDM) in auditing. Judgment

and decision making research is taken up to understand judgments and decisions of

individuals and groups. Those who make these judgments include auditors, preparers of

financial statements, and users like investors, analysts, bankers who make judgments and

decisions regarding investments and lending. JDM research includes evaluating the quality of

judgments made by the above-mentioned actors, explaining the process of decision-making,

identification of the factors that affect this process, and improving the judgment quality of

auditors, users and preparers of financial statements (Trotman, Tan et al. 2011).

The purpose of this study is to determine if awareness can be used as a tool to improve the

professional judgment of auditors specially while evaluating authenticity of FVMs provided

through two different sources i.e. independent valuation specialists and in house managers.

Our research design uses the experimental method and quantitative data is collected to

support our theory and hypotheses.

4.1.1 Experimental design of the study:

This study is going to perform a factorial experimental to investigation if awareness can help

auditors improve their professional judgment in situations where there is maximum risk of

overreliance and blind trust on expert´s work.

31

A factorial design suits best in our study because we want to study how source cues and

awareness can affect professional judgment. A factorial design will help us study both main

effects and interaction effects.

Our experiment allocated subjects randomly to a 2 (source: third-party/in-house) x 2

(Awareness: Off/On) between subjects factorial design. However since we are interested in

predicting the use of awareness to mitigate biases related to source credibility, we have

omitted to use awareness on in-house management condition. Instead we use the in-house

condition to observe variations between source cues.

Therefore we have reduced it to three treatment conditions:

• Third-party specialist with awareness

• Third-party specialist without awareness

• In-house management without awareness

4.2 Data type and research tool:

We used primary data for this study. We used questionnaire for collecting the data, which

provided us with better control over sample structure and suitability of the data collected. We

choose to use questionnaires because of economical cost and greater/easier access to subjects

in minimum possible time.

4.2.1 Time horizon:

Considering the limited resources and time available at disposal our study is a cross-sectional

study. We collected the data through questionnaires over a time period of a week.

4.2.2 Sample:

Our experiment is based on the data collected from eligible participants who had the ability

and necessary skills to answer the questionnaire. In such situation a non-probability sampling

was more practical than probability sampling. So we chose convenience-sampling technique

to access the subjects who are familiar to the task in questionnaire.

32

We have chosen students of NHH who are studying auditing and accounting at an advanced

level. All of them have taken an intensive course in auditing in 1st semester at masters level,

they have necessary skills to take part in the research and have performed similar tasks as part

of their auditing course MRR 411. Due to time constraint and other practical reasons like

access to the practicing auditors it was not possible to engage auditors with many years of

professional experience.

The use of students as subjects is very common in accounting research and other behavioral

sciences. Past results of research in accounting decision-making provides evidence that

students as surrogates and business professionals made very similar judgments and shared

common reasoning for their decisions. (Ashton and Kramer 1980) argues that students are an

acceptable choice for decision-making research in accounting.

4.2.3 Questionnaire:

Our study is a cross sectional study, so it is very important that the questionnaire we use for

collecting the data answers all the questions important for our study. Our questionnaire is

adopted from the study of (BROWN LIBURD 2014) . However we added some

modifications that were necessary to make it suitable for our research. We removed all

internal control information that was provided in the original case, since information about

internal controls is not necessary for assessment of inherent risk. We also altered the

description of in-house management expertise, previous description showed too much

similarity to third-party specialist.

We created and conducted the questionnaire through a well-known research instrument called

Qualtrics because Qualtrics makes it easy for the subjects to respond online and helps us to

collect and transfer the data to statistical analysis software efficiently. Qualtrics helped us

distributing the questionnaires randomly and subjects were exposed to one of the three

experimental conditions.

33

4.2.3.1 Questionnaire Design:

Our questionnaire consists of a total of 3 to 4questions and all of them are closed ended

questions. We selected closed ended questions because they are simple to interpret and

responses are easier to use in a data analysis. The two main questions are rating questions

using the traditional Likert Scale. We have used a seven-value scale for assessment of

inherent risk and source credibility. The two dichotomous questions were used for

manipulation checks with only two answers True/False. The questionnaire is presented in the

appendix.

4.2.3.2 Questionnaire description:

The questionnaire starts with the description of the task, which is followed by the description

of the company and its assets, which are the focus of our study. The subjects are informed

that this study is part of our Master thesis. In the introduction of the questionnaire subjects

are encouraged to answer and it is told that it will not more than 5-7 minutes and requested to

answer to the best of their capabilities.

Our questionnaire can be divided in to 3 main parts; it starts with the description of the task,

facts about the company, source of evaluations and the questions section. One out of three

types of questionnaires have an extra part related to awareness manipulation. All the

respondents are randomly assigned one of the three treatments.

There are three questionnaires used in the experiment according to the experimental research

design applied:

Questionnaire 1:

Questionnaire 1 is the experiment condition where subjects are exposed to 3rd party prepared

FVMs and awareness treatment is on as well. The questionnaire begins with a short

34

paragraph about the PCAOBs concern about the FVMs preparations and Auditors pattern of

professional judgment.

Questionnaire 2:

Questionnaire 2 is the experiment condition where the subjects are exposed to 3rd part

prepared FVMs but awareness treatment is off here so there is no information about PCAOBs

concerns.

Questionnaire 3:

Questionnaire 3 represents the experimental condition where subjects are provided with in-

house prepared FVMs and no awareness treatment is applied, which means subjects are not

informed about PCAOBs concerns about FVM preparation.

4.2.4 Pre test and post experimental questions

The questionnaire and post experimental survey was pre-tested on six participants. Two

participants were used in each treatment condition. The post experimental survey is

presented in appendix 3.

4.3 Explanation of Variables

4.3.1 Independent variables:

In our experimental study there are two independent variables, which are operationalized as

two independent factors in the experimental factorial design. These two factors are source

credibility and awareness; source credibility has two levels and awareness as one level.

Source credibility is the critical independent variable here and its role is discussed in the

theoretical framework in the light of previous literature. In the early phase of our study we

were taking awareness just as an independent variable but in the later phase of the study our

35

interest developed in how awareness plays a role of moderating the relationship between

source credibility and professional judgment. Since then our study focused on studying the

interaction effect of awareness in the experimental design.

According to (Baron 1986) moderator is in general terms a variable which can be either

qualitative or quantitative and it affects the direction and strength of the causal relationship

between independent and dependent variables. So this experimental design can help us

finding out if awareness can improve auditor’s judgment when there are fair chances of

existence of bias towards source credibility.

4.3.2 Dependent variable:

We are using auditor’s professional judgment as dependent variable in our study and

evidence of using professional judgment as dependent variable in recent studies is the

research done by (Siddhartha Sankar Saha 2015) on studying the effects of engagement

issues on professional judgment. The dependent variable is operationalized through the

inherent risk assessment process where auditors perform an assessment of inherent risk

5. Statement of results

5.1 Manipulation checks In order to determine if participants realized the source condition of the experiment, we asked

participants the following statement:

• Expert cue: True or false, in developing fair value measurement and disclosures,

Paladin Capital Group uses the services of an independent third-party valuation firm.

• In-house management cue: True or false, in developing fair value measurement and

disclosures, Paladin Capital Group uses the services of a manager from within the

firm.

36

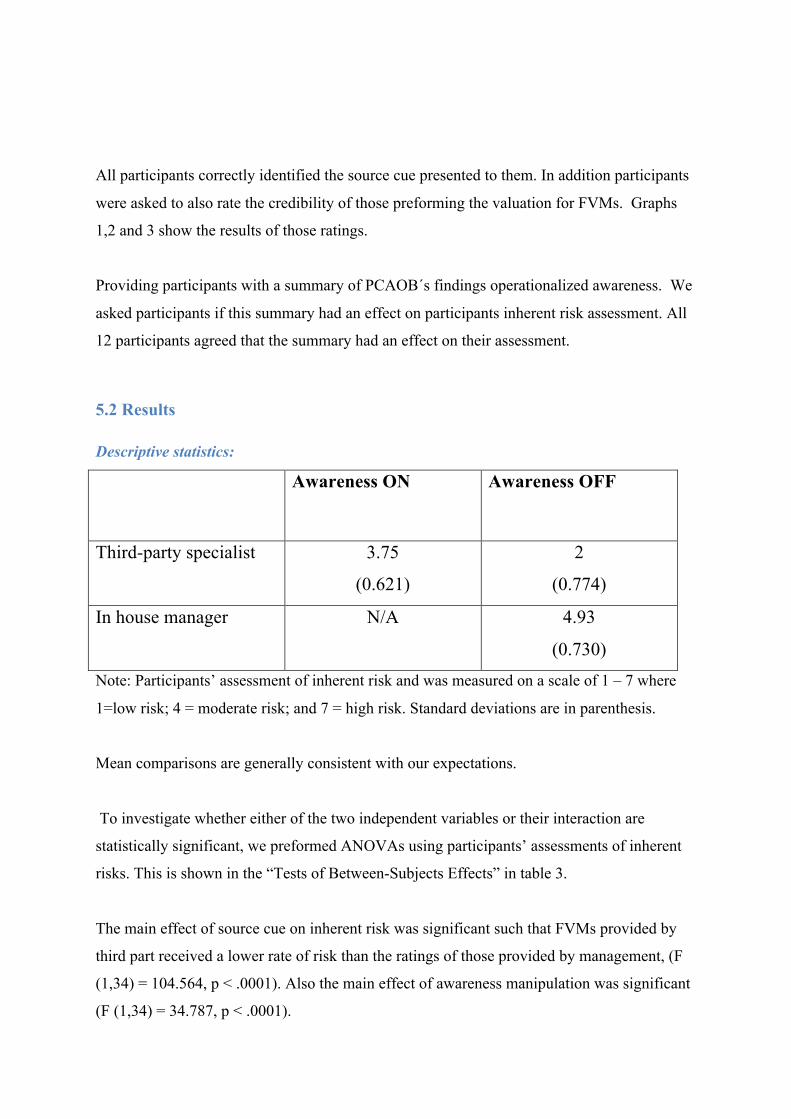

All participants correctly identified the source cue presented to them. In addition participants

were asked to also rate the credibility of those preforming the valuation for FVMs. Graphs

1,2 and 3 show the results of those ratings.

Providing participants with a summary of PCAOB´s findings operationalized awareness. We

asked participants if this summary had an effect on participants inherent risk assessment. All

12 participants agreed that the summary had an effect on their assessment.

5.2 Results

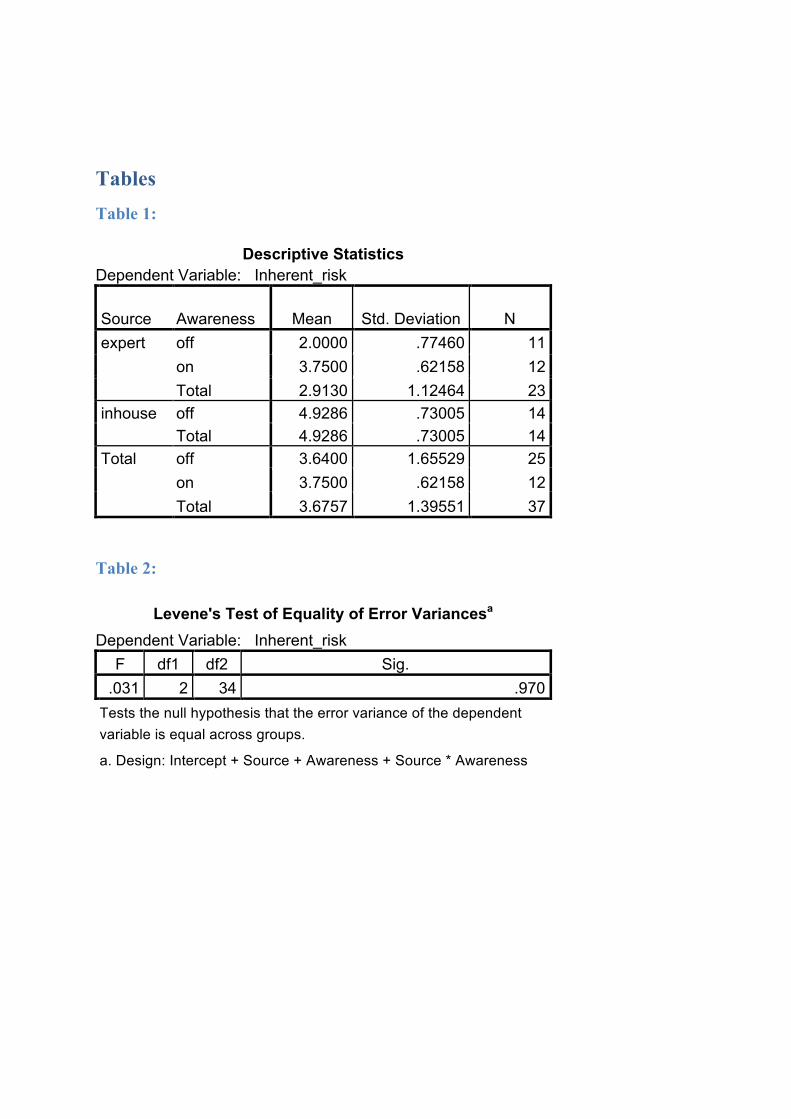

Descriptive statistics:

Awareness ON Awareness OFF

Third-party specialist

3.75

(0.621)

2

(0.774)

In house manager N/A 4.93

(0.730) Note: Participants’ assessment of inherent risk and was measured on a scale of 1 – 7 where

1=low risk; 4 = moderate risk; and 7 = high risk. Standard deviations are in parenthesis.

Mean comparisons are generally consistent with our expectations.

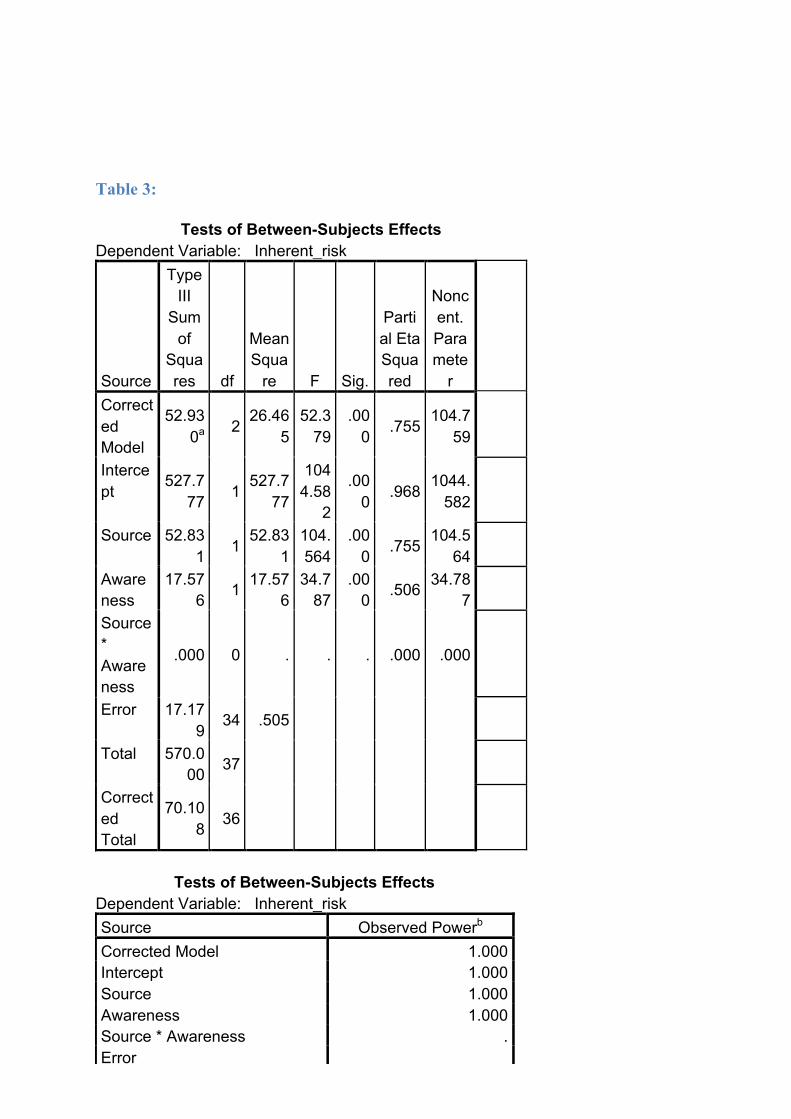

To investigate whether either of the two independent variables or their interaction are

statistically significant, we preformed ANOVAs using participants’ assessments of inherent

risks. This is shown in the “Tests of Between-Subjects Effects” in table 3.

The main effect of source cue on inherent risk was significant such that FVMs provided by

third part received a lower rate of risk than the ratings of those provided by management, (F

(1,34) = 104.564, p < .0001). Also the main effect of awareness manipulation was significant

(F (1,34) = 34.787, p < .0001).

37

Testing of hypothesis:

To test the two hypotheses, we used a two-tailed correlation test. Table 4 and 5 show the

results of those test. To summarize there is a significant relationship between “expert” and

“expert with awareness “because our p-value is less then 0.05. Therefore we can reject the

null hypothesis for H1.

There is also a significant relationship between the two different source cues, “expert and in-

house”. P test is at 0.006 and is less then 0.05. Therefore we can reject the null hypothesis

for H2. All tested hypothesis were supported at the 0.01 level.

Awareness ON Awareness OFF

Third-party specialist

H1

Supported

H2

Supported

In house manager N/A H2

Supported

6. Conclusion

6.1 Answers to research question

RQ1: Can awareness be used as tool to help mitigate biases related to source

credibility?

The aim of this study was to see of professional judgment towards fair value measurements

could be improved somehow. Our theory suggested that participants would perceive third

38

party specialist as more credible then in-house management and that this would be caused by

subconscious mental shortcuts.

We hypothesized that if participants were informed of the consequences that lead to judgment

traps and bias, participants would try to diminish the effect produced by subconscious mental

shortcuts.

Using a 2 x 2 experimental design, we asked 37 auditing students to make an inherent risk

assessment involving FVMs, Results showed that auditors assessment of inherent risk as

lower for when the client uses a third-party valuation specialist. Inherent risk was highest

when the client used in-house management. We used awareness as a moderator and found

out that participants were significantly affected by the PCAOB concerns list.

6.2 Contribution to research Bratten et all 2013 indicated that there is a lack of empirical research, that studies the effect

of using external pricing services on audit quality or perceived audit quality.

This study hopes to contribute to this discussion. Therefore we have focused on collecting

and analyzing empirical evidence pertaining to the moderating role of awareness, in a setting

where professional judgment quality towards source credibility is evaluated.

6.3 Contribution to audit practice

This study has implications for the auditing profession, the PCAOB inspection reports has

for a number of years cited that a number of deficiencies related to auditing FVMs for the

large audit firms. PCAOB stated that they state that a number of the deficiencies cited are

due to overreliance of external valuation firms. By observing how awareness moderates

the relationship between source credibility and professional judgment, this study can

contribute to the efforts of improving judgment quality in areas that are on the top of

PCAOBs concerns list.

39

6.4 Suggestions for future research As like all studies, this research has its limitations. However these limitations can represent

opportunities for future research.

First our study is limited to few variables i.e. source credibility, professional judgment and

awareness. Future research can investigate other factors that can improve judgment quality in

the areas that are on the top of PCAOBs concerns list. One of the areas that PCAOB is

concern with is gathering sufficient evidence, they state that auditors are not obtaining

sufficient evidence to support audits of FVMs. Therefore it could be interesting to investigate

the relationship between planning risk assessments and audit effort.

Also due to the time constraint and the limited resources available, it was not feasible to

access practicing auditors as subjects for the study. Future research can see the effect of using

practicing auditors.

40

References Ashton, R. H. and S. S. Kramer (1980). "Students As Surrogates in Behavioral Accounting

Research: Some Evidence." Journal of Accounting Research 18(1): 1-15.

Baron, R. M. k. D. A. (1986). "The moderator–mediator variable distinction in social

psychological research: Conceptual, strategic, and statistical considerations." Journal of

Personality and Social Psychology Volume 51(6).

Blaskovich, J., & Mintchik, N. (2009, September). Party Of Three? A Source Credibility

Perspective On The Use Of Consultants For Internal Control Assessments. The Journal of

Applied Business Research , 51-68.

Bonner, S. E. (1999). Judgment and Decision-Making Research in Accouting. Accounting

Horizons , 13 (4), 385-398.

BROWN L. S. A. M., SANDRA WALLER SHELTON (2014). "The Effect of Reliance on

Third-Party Specialists under Varying Levels of Internal Control Effectiveness on the Audit

of Fair Value Measurements." Rutgers , The State University of New Jersey.

Chaiken, S., & Maheswaran, D. (1994). euristic processing can bias systematic processing:

Effects of source credibility, argument ambiguity, and task importance on attitude judgment.

Journal of Personality and Social Psychology , 66 (3), 460-473.

Chen, S., Duckworth, K., & Chaiken, S. (1990). Motivated Heuristic and Systematic

Processing. Psychological inquiry , 10 (1), 44-49.

Chevalier, R., Glover , S., Herrman, G., Prawitt, D., & Ranzilla, S. (2013). The KPMG

Professional Judgment Framework. Elevating Professional Judgment in Auditing and

Accounting: The KPMG Professional Judgment Framework , 1-55.

41

Dholakia, R. and B. Sternthal (1977), Highly Credible Sources: Persuasive Facilitators or

Persuasive Liabilities?" Journal of Consumer Research, 3, 223-232.

Eilifsen, A., Messier, J. W., Glover, S. M., & Prawitt, D. F. (2014). Auditing & Assurance

services Third International Edition. Berkshire, United Kingdom: McGraw-Hill.

Glover, S. M., Taylor, M. H., & Wu, Y.-J. (2014). Closing the Gap between Auditor

Performance and Regulators’ Expectations when Auditing Fair Value Measurements:

Evidence from Practicing Audit Partners. 1-46.

Griffith, E. E., J. S. Hammersley, K. Kadous, and D. Young. 2012. Auditing Complex

Estimates: Understanding the Process Used and Problems Encountered, The University of

Georgia, Emory University, 1-47

Hovland, C. I., & Weiss, W. (1951). The Influence of Source Credibility on Communication

Effectiveness. Oxford journals , 635-650.

Kelman, H. C. (1961). PROCESSES OF OPINION CHANGE. Oxford journal .

Kerlinger, F. N. (1973). "Foundations of Behavioral Research." Holt, Rinehart and Winston,

Inc. 3rd Edition.

McKean, K. (1985). Decisions, decisions, decisions. Discover , 22-31.

Mowen, J. C., & Wiener, J. L. (1986). Source Credibility: on the Independent Effects of Trust

and Expertise", in NA - Advances in Consumer Research Volume 13, eds. Richard J. Lutz,

Provo, UT : Association for Consumer Research, Pages: 306-310

Ohanion, R. (1990). Construction and Validation of a scale to Measure Celebrity Endorsers’

Perceived Expertise , Trustworthiness, and Attractiveness. Journal of Advertising .

42

Siddhartha Sankar Saha, M. N. R. (2015). "Impact of Audit Engagement Issues on Statutory

Auditors’ Professional Judgment: An Empirical Analysis." Siddhartha Sankar Saha, Mitrendu

Narayan Roy Volume 6.

Trotman, K. T. (2001). "Design Issues in Audit JDM Experiments." International Journal of

Auditing 5(3): 181-192.

Trotman, K. T., Tan, H. C., & Ang, N. (2011, March). Fifty-year overview of judgment and

decision-making research in accounting. Accounting and Finance , 278-360.

Tversky, A., & Kahneman, D. (1974). Judgment under Uncertainty: Heuristics and Biases.

Science , 185, 1124-1131.

43

Appendix 1: Introduction

Introduction

This study attempts to collect information about differences in individual perception of

source credibility

Procedures

You will be shown a paragraph about a hypothetical company named Paladin Capital Group.

Imagine that you are a part of an auditing team that is conducting preliminary engagement

activities for accepting Paladin Capital Group as a client, during this process your audit team

has determined the fair value measurements (FVMs) to be an area of concern for the current

year’s audit engagement, because there is no market for the exact evaluation of certain

securities held in the portfolio so it needs to be examined carefully. Paladin Capital Group

experienced a significant decrease in the volume of FVMs in recent evaluations. You will in

the next slide be shown information concerning the company´s FVMs

Afterwards you are asked to complete a short questionnaire about the information provided.

The questionnaire consists of a few questions and will take approximately 5 minutes or less.

Confidentiality

All data obtained from participants will be kept confidential and will only be reported in an

aggregate format (by reporting only combined results and never reporting individual ones).

All questionnaires will be concealed, and no one other than then primary investigator will

have access to them. The data collected will be stored for one week and then deleted by the

primary investigator.

44

I have read, understood, and printed a copy of, the above consent form and desire of my own

free will to participate in this study.

Yes

No

Thank you very much for participating in this research study.

Appendix 2: Example of cases

Example for Expert*Awareness Before reviewing the company´s information, here is a summarization of an

inspection report conducted by the Public Company Accounting Oversight

Board According to the Public Company Accounting Oversight Board (PCAOB) there is a dramatic

increase in the number of fair value impairment (FVM) audit deficiencies relating to

impairment testing and the measurement of certain assets, particularly the pricing of

financial instruments.

The increase in audit deficiencies related to FVM and impairment are consistent with a

general increase in all audit deficiencies, and is a likely result of uncertainty created by the

economic downturn. FVM and impairment audit deficiencies are particularly significant

because these two particular issues account for over half of all recent audit deficiencies.

Auditing the estimates and assumptions underlying FVM and impairments requires

heightened professional skepticism as these judgmental areas are susceptible to management

bias, particularly in difficult economic times

45

The PCAOB reports indicated that most FVM audit deficiencies were caused by inadequate

testing of asset prices provided by outside pricing services, and identified a number of

deficiencies related to the auditors’ reliance on evidence from the specialists, including

failure to understand the methods, the models, and the assumptions used by valuation

specialists.

The task:

You are a part of an auditing team that is conducting preliminary engagement activities for

accepting Paladin Capital Group as a client, during this process your audit team has

determined the fair value measurements (FVMs) to be an area of concern for the current

year’s audit engagement, because there is no market for the exact evaluation of certain

securities held in the portfolio so it needs to be examined carefully. Paladin Capital Group

experienced a significant decrease in the volume of FVMs in recent evaluations.

While keeping in mind the preliminary engagement activities & techniques discussed in

MRR 411 (revisjon) , please asses the risk associated with this client after considering the

source of FVMs (fair value measurements).

46

The company:

Paladin Capital Group is a multinational corporation with a multi-stage private equity

division that invests in growing companies. Over last two decades the company has extended

itself to multiple business lines and is now operating in a variety of industries throughout the

world. Company is highly profitable and has a financial segment that manages an investment

portfolio of $ 500 million used to fund operations as needed.

The portfolio represents approximately 15 % of the consolidated total assets, and for the past

years it has consisted of equity securities, investment grade bonds and alternative

investments. Alternative investments consist primarily of collateralized debt obligation (A

structured financial product that pools together cash flow generating assets and repackages

this asset-pool in to discrete tranches that can be sold to investors) securities.

The source:

For securities with an inactive market and where significant inputs are unobservable, Paladin

Capital Group retains the services of a third-party valuation specialist named Primus

Valuations. This specialist has extensive expertise in FVMs with complex Level 2 and 3

securities. Primus Valuations has a strong standing in the industry; and has worked with

Paladin Capital Group for over 10 years. Additionally, the director at Primus Valuations was

a former VP of Finance at Paladin Capital Group and as a result, the specialist is

knowledgeable about the company’s business. Further, senior management at Paladin Capital

Group believes that it is necessary to review evidence used to support the specialist’s FVMs

and relevant assumptions, and challenges the assumptions and inputs when considered