Embed Size (px)

Citation preview

The (Un)known of Indian Economy

Dr Soumya Kanti GhoshGroup Chief Economic Adviser

State Bank of India

January 05, 2018

2State Bank of India

Macro Developments

3State Bank of India

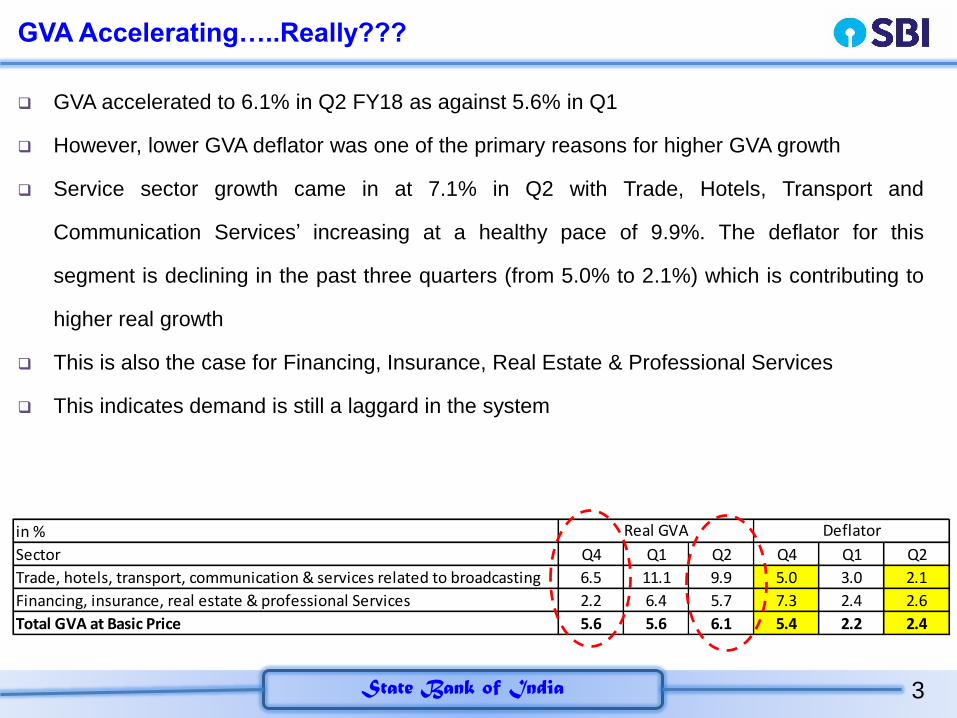

GVA Accelerating…..Really???

GVA accelerated to 6.1% in Q2 FY18 as against 5.6% in Q1

However, lower GVA deflator was one of the primary reasons for higher GVA growth

Service sector growth came in at 7.1% in Q2 with Trade, Hotels, Transport and

Communication Services’ increasing at a healthy pace of 9.9%. The deflator for this

segment is declining in the past three quarters (from 5.0% to 2.1%) which is contributing to

higher real growth

This is also the case for Financing, Insurance, Real Estate & Professional Services

This indicates demand is still a laggard in the system

in %

Sector Q4 Q1 Q2 Q4 Q1 Q2

Trade, hotels, transport, communication & services related to broadcasting 6.5 11.1 9.9 5.0 3.0 2.1

Financing, insurance, real estate & professional Services 2.2 6.4 5.7 7.3 2.4 2.6

Total GVA at Basic Price 5.6 5.6 6.1 5.4 2.2 2.4

Real GVA Deflator

4State Bank of India

Nominal GVA & Real Narrative

Real Core GVA (GVA ex agriculture & Public

administration, defence and Other Services)

which was declining in the entire FY17 is

showing upward trend in FY18 but this is

primarily due to decline in core GVA deflator

Nominal Core GVA not changed much and

remained in the range of 7.5%-9.5% since

Jun’16

5State Bank of India

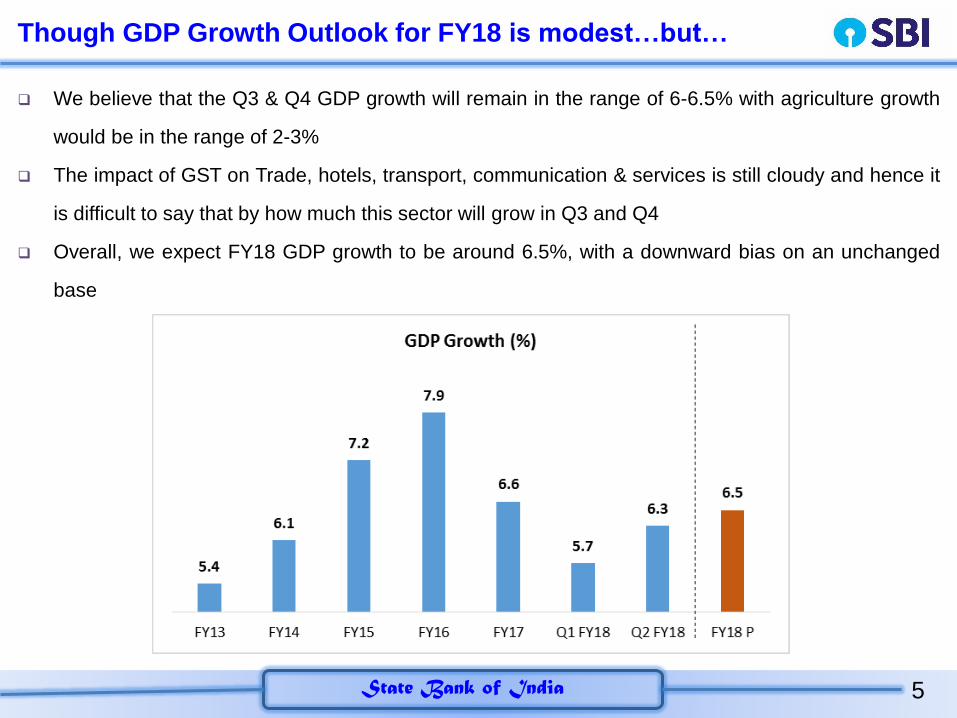

Though GDP Growth Outlook for FY18 is modest…but…

We believe that the Q3 & Q4 GDP growth will remain in the range of 6-6.5% with agriculture growth

would be in the range of 2-3%

The impact of GST on Trade, hotels, transport, communication & services is still cloudy and hence it

is difficult to say that by how much this sector will grow in Q3 and Q4

Overall, we expect FY18 GDP growth to be around 6.5%, with a downward bias on an unchanged

base

6State Bank of India

…Various Leading Indicators are in Green

Indicators Jan'17 Feb'17 Mar'17 Apr'17 May'17 Jun'17 Jul'17 Aug'17 Sep'17 Oct'17 Nov'17

Railway Freight 0.3 3.5 7.7 4.6 3.9 2.8 5.6 7.7 5.9 2.6 3.1

Commercial Vehicle Sales -2.4 5.7 6.7 -25.0 -9.3 -4.2 5.7 14.9 21.1 2.1 43.9

Cellular Mobile Subscribers 19.0 19.7 18.1 21.2 22.2 22.7 22.6 21.4 20.9 20.5 -

Foreign Exchange Earnings 18.0 15.6 15.4 27.8 20.9 22.6 4.9 10.9 19.1 18.6 16.7

Foreign Tourist Arrivals 16.4 12.7 11.8 25.0 19.5 22.5 7.4 11.0 18.9 18.1 14.4

Steel Output 11.2 8.6 11.0 9.0 3.9 6.0 9.2 2.1 3.7 8.4 16.7

Cement Output -13.3 -15.8 -6.8 -5.2 -1.4 -3.3 -2.0 0.7 0.1 -1.3 17.3

Core Sector 3.4 0.5 5.2 2.6 3.9 1.0 2.9 4.4 4.7 5.0 6.7

SBI Index (Yearly) 47.0 49.5 50.3 49.3 50.0 49.6 50.3 50.9 53.6 53.0 53.0

Source: SBI Research

Recovery in Economic Leading Indicators (% YoY)

7State Bank of India

Corruption and GDP Growth

In last two years, the number of punishment carried out by CVC though its own investigations has

increased significantly & the number of serious complaints out of total outside complaints received by

CVC is also declining

Empirical research suggests the direct link between corruption and GDP growth is difficult to assess

but it certainly have significant negative effects on investment (including FDI), competition,

entrepreneurship, government efficiency and human capital formation

Between 2011 and 2016, India, UK, Portugal and Italy have succeeded in reducing the corruption level by

improving their overall rank in corruption perception index and also achieved a positive GDP growth

Central Vigilance Commission Actions

Own Investigations Outside Complains

Year Prosecution PunishmentsYoY Gr%

YearComplaints

received

Of these considered

Serious

Of these considered Serious (%)

2008 138 2511 2008 10142 1147 11.31

2009 225 2204 -12.2 2009 14206 1714 12.07

2010 262 2720 23.4 2010 16260 945 5.81

2011 183 2312 -15.0 2011 16929 1023 6.04

2012 199 2507 8.4 2012 37039 913 2.46

2013 176 2680 6.9 2013 31432 1237 3.94

2014 133 2144 -20.0 2014 62362 1214 1.95

2015 132 3592 67.5 2015 29838 179 0.60

2016 154 3296 -8.2 2016 49847 86 0.17

Source: Central Vigilance commission

Changes in Corruption Rank and Economic Growth From 2011 to 2016

CountriesChange in Rank

(2016/2011)Change in GDP

(2016/2011)

Countries where Corruption

Decline/Growth increase

India -16 0.5

United Kingdom -6 0.3

Portugal -3 3.2

Italy -9 0.3

Countries where Corruption

increase/Growth decline

Singapore 2 -4.2

Hong Kong 3 -2.8

Mauritius 4 -0.4

Korea (South) 9 -0.9

Turkey 14 -8.2

Brazil 6 -7.6

China 4 -2.8

Source: SBI Research

8State Bank of India

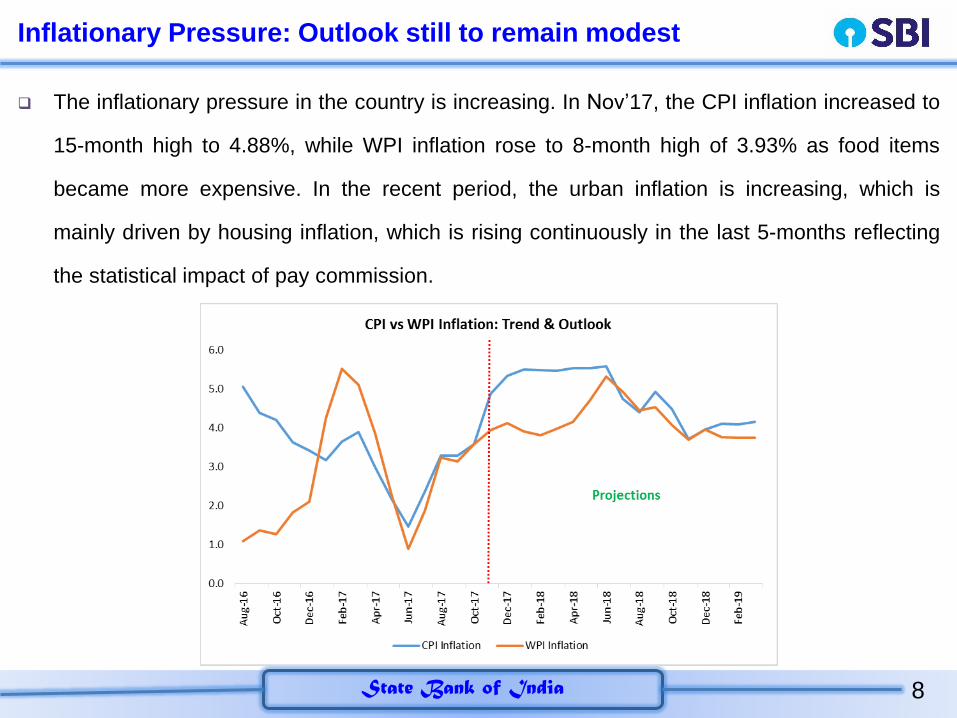

Inflationary Pressure: Outlook still to remain modest

The inflationary pressure in the country is increasing. In Nov’17, the CPI inflation increased to

15-month high to 4.88%, while WPI inflation rose to 8-month high of 3.93% as food items

became more expensive. In the recent period, the urban inflation is increasing, which is

mainly driven by housing inflation, which is rising continuously in the last 5-months reflecting

the statistical impact of pay commission.

9State Bank of India

Impact of Jan Dhan on Inflation (1)

We also analysed the impact of state-wise PMJDY accounts on rural and urban CPI

inflation. The data shows that the States where more number of Jan Dhan accounts

were opened, there is a meaningful drop in rural inflation

This suggests that one of the common concerns - that the PMJDY program may have led to

substantially higher price level due to a higher circulation of money and creation of additional

demand - may be unwarranted

We observed that there is both statistically significant and economically meaningful drop in

consumption of intoxicants such as alcohol and tobacco products in states where more

PMJDY accounts were opened

This could be because of behavioural changes like less spending post demonetisation

Also, Jan Dhan-Aadhaar-Mobile (JAM) Trinity has helped in better channelizing Government

subsidies and helped in curbing expenditure on demerit goods such as alcohol and tobacco

in rural areas

10State Bank of India

Impact on Inflation (2)

We also observed an increase in household medical expenditure in more exposed states

like Bihar, West Bengal, Maharashtra, Rajasthan, etc. since Oct’16 due to changing

lifestyles and increased demand for medical services

Number of

A/Cs (in Crore)

Rural

Share (%)

Urban

Share (%)Rural CPI Urban CPI

Health CPI

(Combined)

Pan, Tobacco &

Intoxicants CPI

(Combined)

Uttar Pradesh 4.73 60% 40% -3.6 -0.3 -0.1 -2.3

Bihar 3.20 65% 35% -1.0 0.6 2.3 -0.9

West Bengal 2.89 69% 31% -5.0 -1.5 1.5 -4.6

Madhya Pradesh 2.73 48% 52% -0.9 0.6 -0.6 0.6

Maharashtra 2.12 50% 50% 0.0 0.0 3.4 3.9

Rajasthan 2.04 62% 38% -1.7 -0.2 1.5 -2.7

Chhattisgarh 1.31 67% 33% 0.3 -0.5 1.0 -0.2

Assam 1.27 75% 25% 1.8 1.1 3.2 0.4

Odisha 1.22 73% 27% -4.8 -0.4 -3.3 -6.7

Gujarat 1.15 52% 48% -2.8 -0.8 -2.1 -2.3

Jharkhand 1.09 74% 26% -4.7 -0.8 5.8 0.4

Karnataka 0.97 61% 39% -0.7 -1.4 2.2 2.1

Tamil Nadu 0.90 48% 52% 1.6 1.8 2.3 -2.7

Telangana 0.88 57% 43% -4.8 -1.7 -1.8 -1.0

Andhra pradesh 0.77 50% 50% -3.4 -1.3 -0.6 1.8

Haryana 0.62 54% 46% -1.1 1.9 -1.0 -0.9

Punjab 0.57 57% 43% -1.4 -0.7 -2.0 14.1

Kerala 0.42 44% 56% 3.2 0.7 2.0 5.8

All India 30.38 60% 40% -1.6 -0.1 0.8 -0.1

Source: MOSPI, SBI Research

Jan Dhan Accounts and CPI Inflation

PMJDY

States

Change in CPI Inflation (Sep'17 over Oct'16)

11State Bank of India

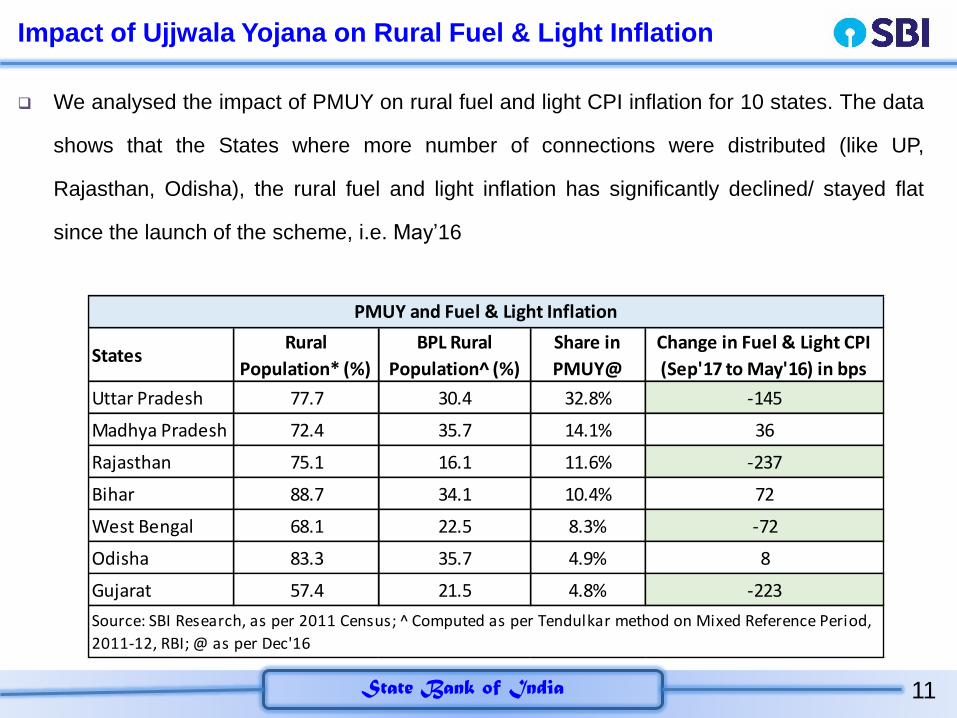

Impact of Ujjwala Yojana on Rural Fuel & Light Inflation

StatesRural

Population* (%)

BPL Rural

Population^ (%)

Share in

PMUY@

Change in Fuel & Light CPI

(Sep'17 to May'16) in bps

Uttar Pradesh 77.7 30.4 32.8% -145

Madhya Pradesh 72.4 35.7 14.1% 36

Rajasthan 75.1 16.1 11.6% -237

Bihar 88.7 34.1 10.4% 72

West Bengal 68.1 22.5 8.3% -72

Odisha 83.3 35.7 4.9% 8

Gujarat 57.4 21.5 4.8% -223

PMUY and Fuel & Light Inflation

Source: SBI Research, as per 2011 Census; ̂Computed as per Tendulkar method on Mixed Reference Period,

2011-12, RBI; @ as per Dec'16

We analysed the impact of PMUY on rural fuel and light CPI inflation for 10 states. The data

shows that the States where more number of connections were distributed (like UP,

Rajasthan, Odisha), the rural fuel and light inflation has significantly declined/ stayed flat

since the launch of the scheme, i.e. May’16

12State Bank of India

Banking the UnbankedHow PMJDY Changed Banking Behaviour

13State Bank of India

Overview

The Pradhan Mantri Jan Dhan Yojna (JDY from now) launched in India on August 14, 2014,

the world’s largest financial inclusion program with the aim to provide universal access to

banking services

As of November 2017, approximately 300 million accounts have been opened under this

program attracting total deposits approximately Rs 690,000 million ($11 billions), substantially

expanding access to banking services

Our empirical setting serves as a useful laboratory to study importance of access to basic

financial products for the poor

Our research throw some interesting findings

14State Bank of India

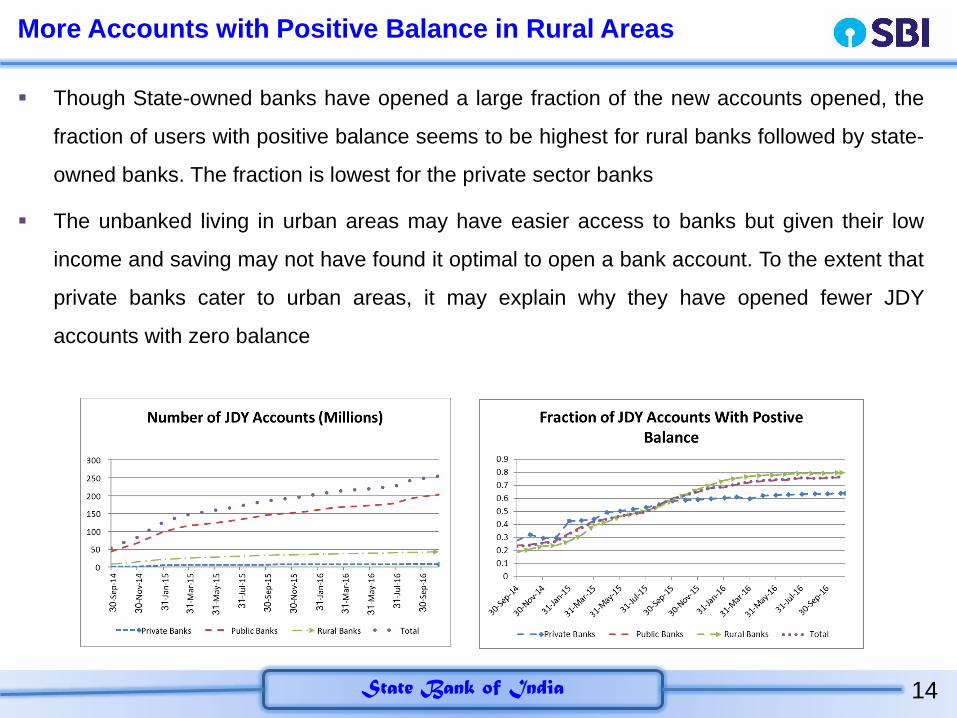

More Accounts with Positive Balance in Rural Areas

Though State-owned banks have opened a large fraction of the new accounts opened, the

fraction of users with positive balance seems to be highest for rural banks followed by state-

owned banks. The fraction is lowest for the private sector banks

The unbanked living in urban areas may have easier access to banks but given their low

income and saving may not have found it optimal to open a bank account. To the extent that

private banks cater to urban areas, it may explain why they have opened fewer JDY

accounts with zero balance

15State Bank of India

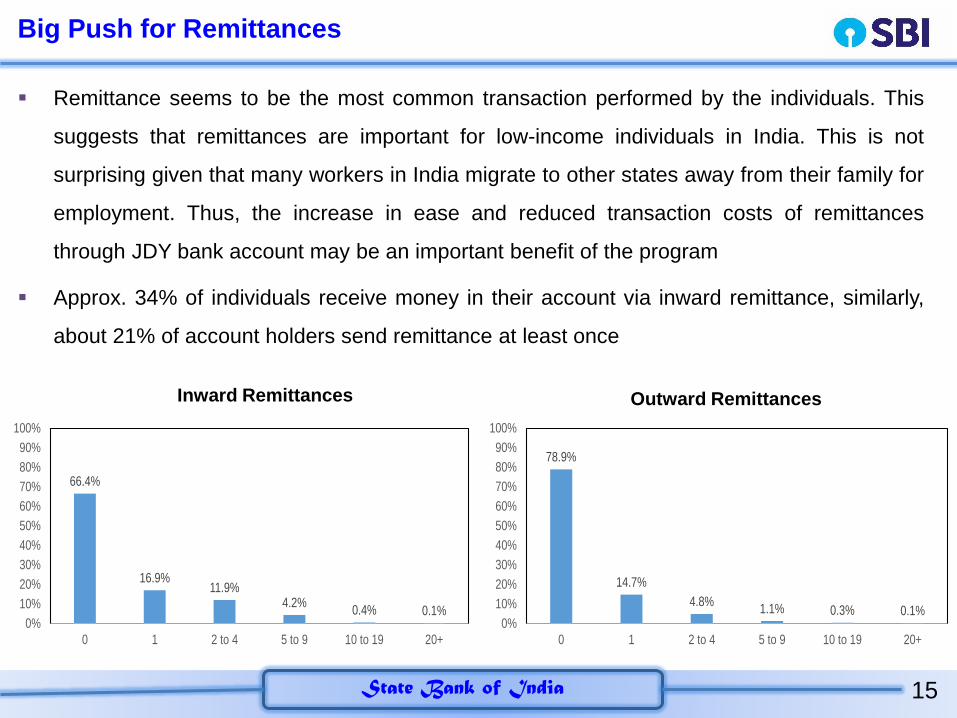

Big Push for Remittances

Remittance seems to be the most common transaction performed by the individuals. This

suggests that remittances are important for low-income individuals in India. This is not

surprising given that many workers in India migrate to other states away from their family for

employment. Thus, the increase in ease and reduced transaction costs of remittances

through JDY bank account may be an important benefit of the program

Approx. 34% of individuals receive money in their account via inward remittance, similarly,

about 21% of account holders send remittance at least once

66.4%

16.9%11.9%

4.2%0.4% 0.1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0 1 2 to 4 5 to 9 10 to 19 20+

78.9%

14.7%

4.8%1.1% 0.3% 0.1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0 1 2 to 4 5 to 9 10 to 19 20+

Inward Remittances Outward Remittances

16State Bank of India

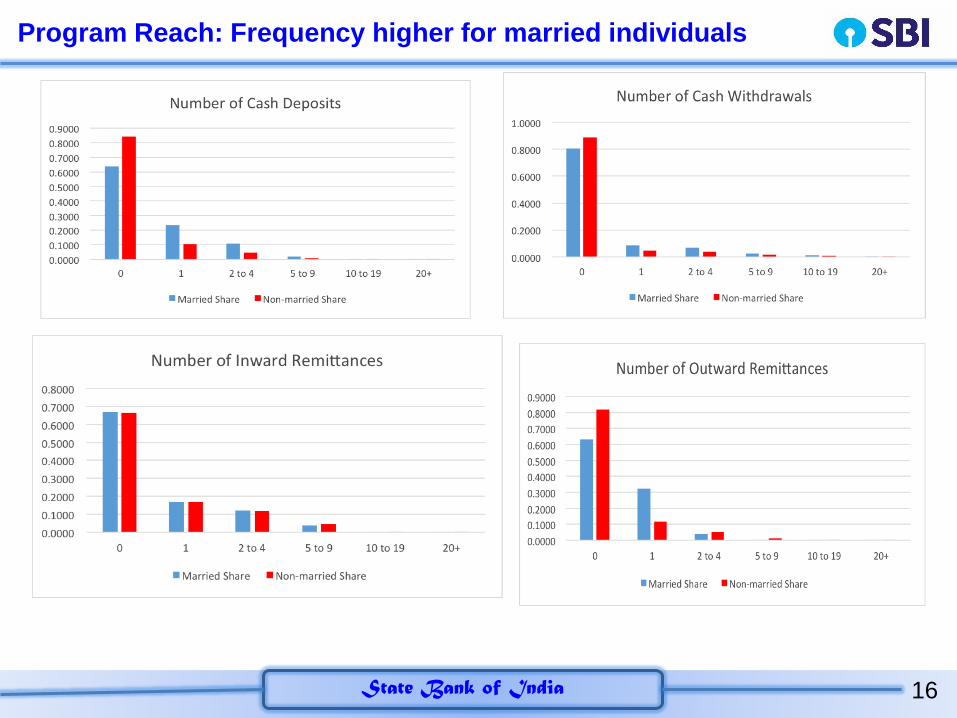

Program Reach: Frequency higher for married individuals

17State Bank of India

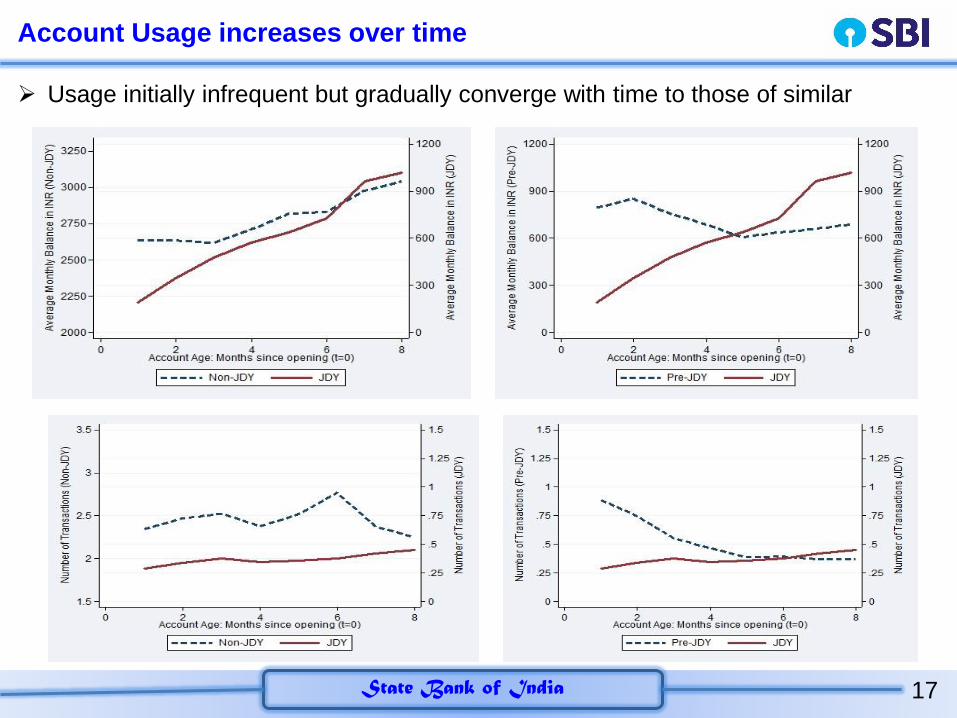

Account Usage increases over time

Usage initially infrequent but gradually converge with time to those of similar

18State Bank of India

PMJDY are silently making economic & social progress

Our findings suggest that JDY may have allowed banks to meet the unmet demand for

credit for some households that did not have prior access to formal banking products.

We observe an increase in the fraction of households borrowing from banks in regions

with greater ex-ante JDY exposure relative to regions with lower exposure

We observe a contemporaneous decrease in the fraction of households borrowing from

non-bank sources

We observe a significant decrease in the monthly volatility of consumption expenditure

We find some evidence suggesting that the program was associated with an increase in

investments

19State Bank of India

Fiscal Policy stance

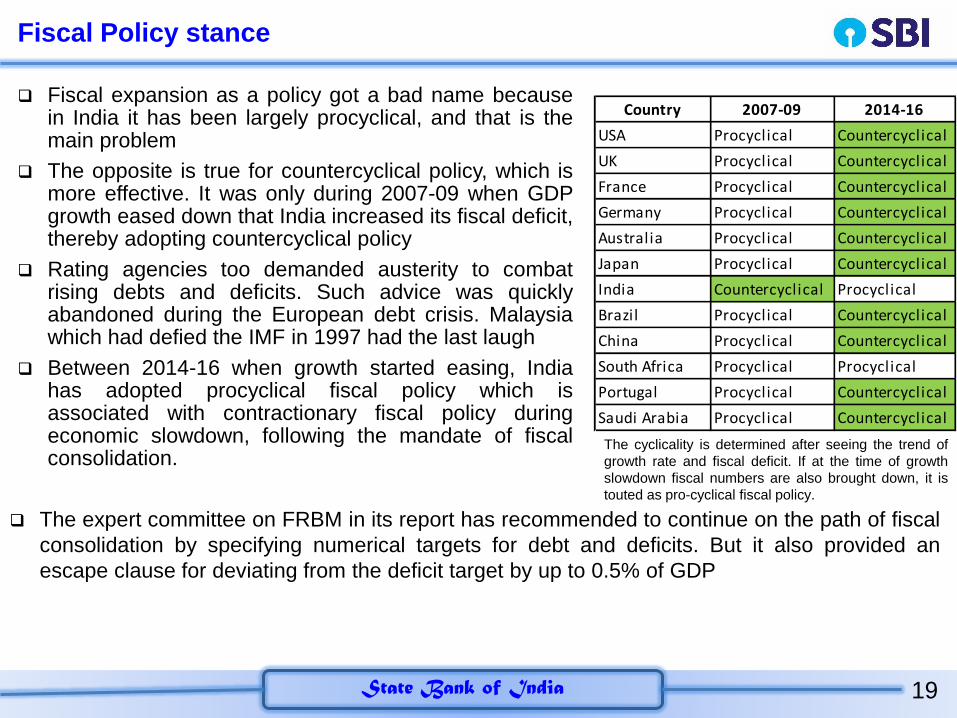

Fiscal expansion as a policy got a bad name becausein India it has been largely procyclical, and that is themain problem

The opposite is true for countercyclical policy, which ismore effective. It was only during 2007-09 when GDPgrowth eased down that India increased its fiscal deficit,thereby adopting countercyclical policy

Rating agencies too demanded austerity to combatrising debts and deficits. Such advice was quicklyabandoned during the European debt crisis. Malaysiawhich had defied the IMF in 1997 had the last laugh

Between 2014-16 when growth started easing, Indiahas adopted procyclical fiscal policy which isassociated with contractionary fiscal policy duringeconomic slowdown, following the mandate of fiscalconsolidation.

Country 2007-09 2014-16

USA Procyclical Countercyclical

UK Procyclical Countercyclical

France Procyclical Countercyclical

Germany Procyclical Countercyclical

Australia Procyclical Countercyclical

Japan Procyclical Countercyclical

India Countercyclical Procyclical

Brazil Procyclical Countercyclical

China Procyclical Countercyclical

South Africa Procyclical Procyclical

Portugal Procyclical Countercyclical

Saudi Arabia Procyclical Countercyclical

The expert committee on FRBM in its report has recommended to continue on the path of fiscal

consolidation by specifying numerical targets for debt and deficits. But it also provided an

escape clause for deviating from the deficit target by up to 0.5% of GDP

The cyclicality is determined after seeing the trend of

growth rate and fiscal deficit. If at the time of growth

slowdown fiscal numbers are also brought down, it is

touted as pro-cyclical fiscal policy.

20State Bank of India

Fiscal Policy & non-tax revenue

Increased fiscal prudence has brought the fiscal deficit to manageable levels. The

increased efforts of the Government to raise resources from non-tax sources have

also helped

However, this has put stress on other sectors like telecom which has seen increase

in leverage after the spectrum auctions

In the non-tax revenue, economic services alone accounted for close to 40% in

2016-17. Within this “other communication services” constituted 60%. For receipts

under 'Other Communication Services', the Department of Telecom collects

recurring license fees from Telecom Services Providers licensed by it

It also collects one time Entry fees from new operators. This also includes one-time

spectrum charges in the years in which auctions are held. These fees affect the

balance sheets of telecom companies

21State Bank of India

Fiscal Deficit for FY18: Though supposed to slip, there is a but..

On 27 Dec’17, Government reviewed the market borrowing programme

Government has budgeted only Rs 2002 crore of short-term borrowings but with

this new borrowing programme, Government will now do incremental short-term

borrowing of Rs 25,000 crore more, hence an extra borrowing of around Rs

23,000 crore (Rs 25,000 crore minus Rs 2,000 crore)

This along-with an additional market borrowing of Rs 50,000 crore through dated

Government securities leads to an aggregate additional borrowing of Rs 73,000

crore

The impact of this additional borrowing would be around 43 bps of GDP and

therefore the fiscal deficit target of 3.24% may shoot up to 3.5% of GDP, but….

Budget Revised Incremental

Short term Borrowing 2,002 25,000 22,998 -

Gross Market Borrowing 5,80,000 6,53,000 73,000 -

Fiscal Deficit 5,46,532 6,19,532 73,000 6,60,420

Fiscal Deficit (% of GDP) 3.24 3.67 0.43 3.50

FY18FY19 P

Fiscal Deficit Arithmetic

Item

Source: SBI Research; P: SBI Projections

22State Bank of India

Fiscal Deficit: Outlook for FY19

By assuming nominal GDP grow of 12% in FY19, if Government target fiscal

deficit of 3.5%, it will be stay on the path of fiscal consolidation and there will be

more fiscal space for the Government to spend in the election year ahead. This is

expected to augur well for the market.

23State Bank of India

Outlook on Monetary Policy: Global Economy

With the ongoing synchronized pick-up in global growth, central banks across countries would

likely to continue the normalization of monetary policy in FY19

The U.S. Federal Reserve has stopped its unconventional program of security purchases, hiked

rates four times and set out a plan for the gradual reduction of its balance sheet

The Bank of Japan will face mounting pressure to lift its foot off the stimulus accelerator. In addition

to this the bank would likely to moderate its asset purchase program in FY19

The ECB will try its utmost to stick to its recently announced plan of halving monthly purchases to

30 billion euros ($34 billion) until September- a prelude to ending the large-scale purchase

program altogether before taking policy interest rates out of negative territory

With growth prospects having been revised downward and with the inflation rate remaining well

above target, the Bank of England finds itself in an unwelcomed policy dilemma, particularly after

having been forced to hike this year for the first time in about 10 years

Putting all this together, there is good news for the global economy as the world’s most powerful

central bank - the Fed - faces the lowest relative degree of policy difficulty in compare to others

24State Bank of India

Monetary Policy: No Need for Coordination

Recently (in Dec) the Central banks of US and Mexico increased their benchmark policy rates by

25 bps while Brazil and Russia reduced their policy rates by 50 bps. Though most of the central

banks are exiting from their quantitative easing cycle yet there is no coordination among them,

which is quite obvious and necessary as every central bank is following its own pace for exit

depending upon the county-specific issues/challenges

Country Policy Rate Name

Recent

increase/decrease

(in BPS)

Policy Date

USA Funds Rate 25 Dec 13, 2017

South Korea Base Rate 50 Nov 30, 2017

Mexico Benchmark Rate 25 Dec 14, 2017

Georgia Refinancing Rate 25 Dec 13, 2017

UAE Repo Rate 25 Dec 13, 2017

Ukraine Discount Rate 100 Dec 14, 2017

Argentina Benchmark Rate 150 Nov 07, 2017

Czech Republic Repo Rate 25 Nov 02, 2017

UK Bank Rate 25 Nov 02, 2017

Brazil Selic Rate -50 Dec 06, 2017

Colombia Key Rate -25 Nov 24, 2017

Ghana Monetary Policy Rate -100 Nov 27, 2017

Peru Policy Interest Rate -25 Nov 09, 2017

Zambia Policy Rate -75 Nov 22, 2017

Russia Key Rate -50 Dec 15, 2017

25State Bank of India

Exports Growth

During Apr-Sep’17 period exports have shown growth of 12% compared to the same period

last year. Exports growth turned positive from Aug’16 after remaining negative for months.

However’ in Oct’17 the growth negative as GST implementation issues led to working capital

problem for exporters, due to which exports are expected to grow by 5% this fiscal. For the

next fiscal exports are expected to grow in double digits

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

-

5,000

10,000

15,000

20,000

25,000

30,000

Ap

r-1

7

May

-17

Jun

-17

Jul-

17

Au

g-1

7

Sep

-17

Oct

-17

No

v-1

7

Exports (Rs million) Exports Growth Rate (RHS)

26State Bank of India

Exports Growth and Global Linkage

Historically, it can be seen that the positive movement of world exports has been mirrored by

Indian exports. With global trade recovering Indian exports have also recovered, save for the

issues arising out of GST implementation. Once the issues are resolved completely, Indian

exports are expected to grow robustly. The 30% growth witnessed in Nov’17 is a step in that

direction

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

20

06

Q1

20

06

Q3

20

07

Q1

20

07

Q3

20

08

Q1

20

08

Q3

20

09

Q1

20

09

Q3

20

10

Q1

20

10

Q3

20

11

Q1

20

11

Q3

20

12

Q1

20

12

Q3

20

13

Q1

20

13

Q3

20

14

Q1

20

14

Q3

20

15

Q1

20

15

Q3

20

16

Q1

20

16

Q3

20

17

Q1

20

17

Q3

Percentage change, year-on-year of Exports

World India

Source : WTO

27State Bank of India

Rupee Dollar Nominal Exchange Rate

Rupee has started appreciating after India’s rating upgrade. From the day of the

announcement till 1st Jan’18 rupee has appreciated by more than a rupee. Till March

Rupee is expected to stay in this range of 63.5-64.0 per dollar.

63.764.8

66.3

62.6

60.1

54.4

1-J

an-1

8

20

16

-17

20

15

-16

20

14

-15

20

13

-14

20

12

-13

Rupee Dollar Exchange Rate End Financial Year

28State Bank of India

Rupee Appreciation and Exports Growth?

Since Feb’17, Indian Rupees has appreciated by around 3.0% against US dollar. It

is widely believed that currency appreciation will lead to decline in Exports keeping

other things equal

However, our finding suggests something different. The estimated result shows that,

there is a positive and significant relationship between these two

During the period between Feb-Sep’17, when rupee appreciated by average 3.3%,

exports increased by on an average by 14.7%.The same has been validated by

other studies

Imports and the import tariffs are playing a major role in boosting exports growth,

thus indicating ‘import-led exports growth’ mechanism operates in India. So, at the

aggregate level, India’s exports are significantly more responsive to changes in

external demand than to price/exchange rate

29State Bank of India

Current Account Deficit Trends( as % of GDP)

After moderating continuously for 4 fiscals, CAD as % of GDP is expected to go up

in the next fiscal. This is due to higher trade deficit brought about by a larger

increase in merchandise imports relative to exports.

-2.5

-1.2

-4.8

-1.7-1.3

-1.1-0.7

-1.5 -1.5

Q1

FY1

8

Q2

FY1

8

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8(P

)

FY1

9(P

)

30State Bank of India

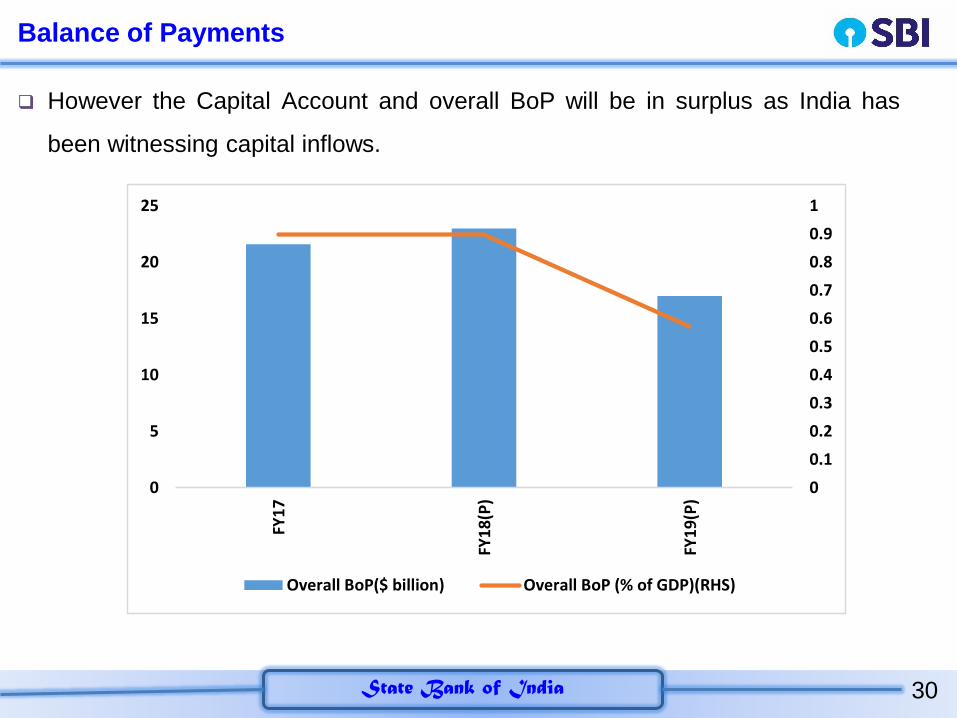

Balance of Payments

However the Capital Account and overall BoP will be in surplus as India has

been witnessing capital inflows.

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0

5

10

15

20

25

FY1

7

FY1

8(P

)

FY1

9(P

)

Overall BoP($ billion) Overall BoP (% of GDP)(RHS)

31State Bank of India

Banking | Corporate Sector

32State Bank of India

Credit growth is showing an upward momentum

The fortnightly data of ASCB indicates that credit off-take (YoY) has been taking place but deposits

growth is declining, which is mainly due to base effect

In FY18 so far (till 22 Dec’17), ASCBs aggregate deposits YoY growth has declined to 4.0% (last

year 14.6%), while credit growth has improved to 10.7% (4.7%)

In FY18, credit may grow at 6.0-6.5%, while deposits growth may decline to 4.0-4.5%, due to base

effect

33State Bank of India

Credit Flows to Sectors

Sectoral deployment of credit for November 2017 indicates that credit to industry and

personal loans sector is slowly picking up

FY17 (Nov'16) FY18 (Nov'17) FY17 (Apr-Nov) FY18 (Apr-Nov)

Bank Credit 4.0 8.3 -0.8 0.2

NF Credit 4.8 8.8 -0.2 0.3

Agr. & Allied 10.3 8.4 3.2 -0.4

Industry -3.4 1.0 -5.5 -2.8

Services 7.1 14.0 0.1 -2.4

Personal Loans 15.2 17.3 8.0 8.8

Housing 15.6 13.1 9.2 7.2

Vehicle Loans 21.4 8.0 9.4 6.0

Source: SBI Research, RBI

YoY Growth (%) YTD Growth

Sectoral Deployment of Credit

34State Bank of India

Insolvency code to boost credit growth

T-3 T-2 T-1Year of

Implementation (T)T+1 T+2 T+3

Argentina 1995 23.2 20.5 11.1 5.3 6.6 15.7 8.7

Austria 2010 3.5 6.5 4.9 2.7 2.5 5.2 -2.0

Chi le 2014 17.4 13.3 11.4 10.8 11.3 6.0 -

China 2006 19.5 8.8 10.7 16.3 17.6 11.7 30.7

Colombia 2006 7.6 17.3 13.8 20.0 15.3 14.0 9.9

Czech Republ ic 2008 3.1 20.5 20.1 13.9 5.8 4.8 9.1

Egypt 1999 - 19.7 17.5 17.1 11.8 9.2 11.1

Germany 2010 -0.7 3.5 0.9 34.5 3.0 -1.1 -10.6

Hong Kong 1998 8.6 18.0 18.7 -15.0 -8.3 3.3 0.4

Kazakhstan 2014 15.5 12.8 13.1 5.7 20.9 -0.2 -

Poland 2003 8.0 11.8 2.3 7.6 2.1 8.6 21.2

Singapore 1999 17.2 19.5 18.2 -0.3 4.0 14.2 -16.1

Spain 2003 12.0 12.2 10.4 14.6 14.3 22.9 24.6

UAE 1993 -3.1 5.5 12.4 5.6 20.4 7.2 12.0

India 2016 13.9 9.0 10.9 4.5 6.3 - -

Source: CEIC, SBI Research, Credit growth as of end of year (Dec). For India: March end

Implementation of Bankruptcy/Solvency Code vs Credit Growth

Country

Bankruptcy/Solvency

Code Implementation

Year

Credit Growth (% YoY)

We find that in most of the countries the bank credit growth increased manifold post the

implementation of Insolvency and Bankruptcy Code

35State Bank of India

Recapitalisation of PSBs

The Government took a massive step to capitalise PSBs in a front-loaded manner, with a

view to support credit growth and job creation

The Rs 2.11 lakh crore over the next two years, through (i) budgetary provision Rs

18,139 crore; (ii) recapitalisation bond Rs 1.35 lakh crore; (iii) Raising of capital by banks

from the market while diluting non-Government equity (estimated Rs 58,000 crore)

India had used this tool before during 1985-86 to 2000-01, wherein the Government

recapitalised PSBs with the total amount of Rs 20,446 crore. The total, interest paid by

the Government to the nationalised banks on special securities works out to be Rs 7,888

crore / 0.07% of GDP per annum on average. While, the banks have paid Rs 15,222

crore as dividend to the government / 0.04% of GDP on average. So, the net impact was

only 0.03% of GDP. Also, coupon payments could improve profitability of the banks

The Rs 1.35 lakh crore package in itself seems largely adequate and sufficient for

tackling the problem of stressed assets. We believe, if the structure of 1990 would

adopted, it would not alter any fiscal math in current scenario

36State Bank of India

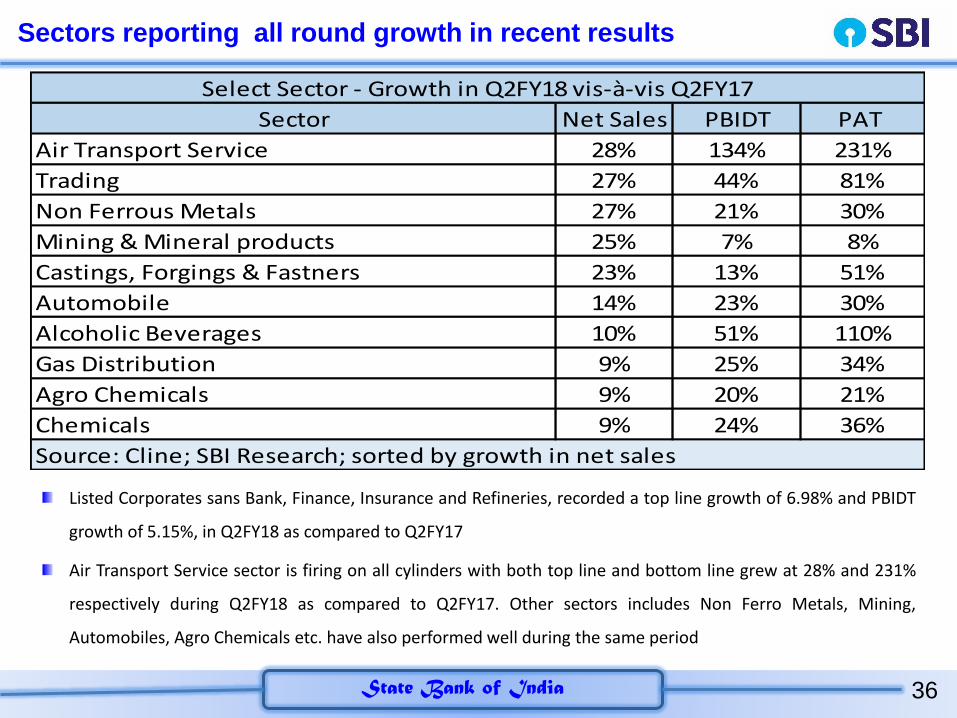

Sectors reporting all round growth in recent results

Sector Net Sales PBIDT PAT

Air Transport Service 28% 134% 231%

Trading 27% 44% 81%

Non Ferrous Metals 27% 21% 30%

Mining & Mineral products 25% 7% 8%

Castings, Forgings & Fastners 23% 13% 51%

Automobile 14% 23% 30%

Alcoholic Beverages 10% 51% 110%

Gas Distribution 9% 25% 34%

Agro Chemicals 9% 20% 21%

Chemicals 9% 24% 36%

Select Sector - Growth in Q2FY18 vis-à-vis Q2FY17

Source: Cline; SBI Research; sorted by growth in net sales

Listed Corporates sans Bank, Finance, Insurance and Refineries, recorded a top line growth of 6.98% and PBIDT

growth of 5.15%, in Q2FY18 as compared to Q2FY17

Air Transport Service sector is firing on all cylinders with both top line and bottom line grew at 28% and 231%

respectively during Q2FY18 as compared to Q2FY17. Other sectors includes Non Ferro Metals, Mining,

Automobiles, Agro Chemicals etc. have also performed well during the same period

37State Bank of India

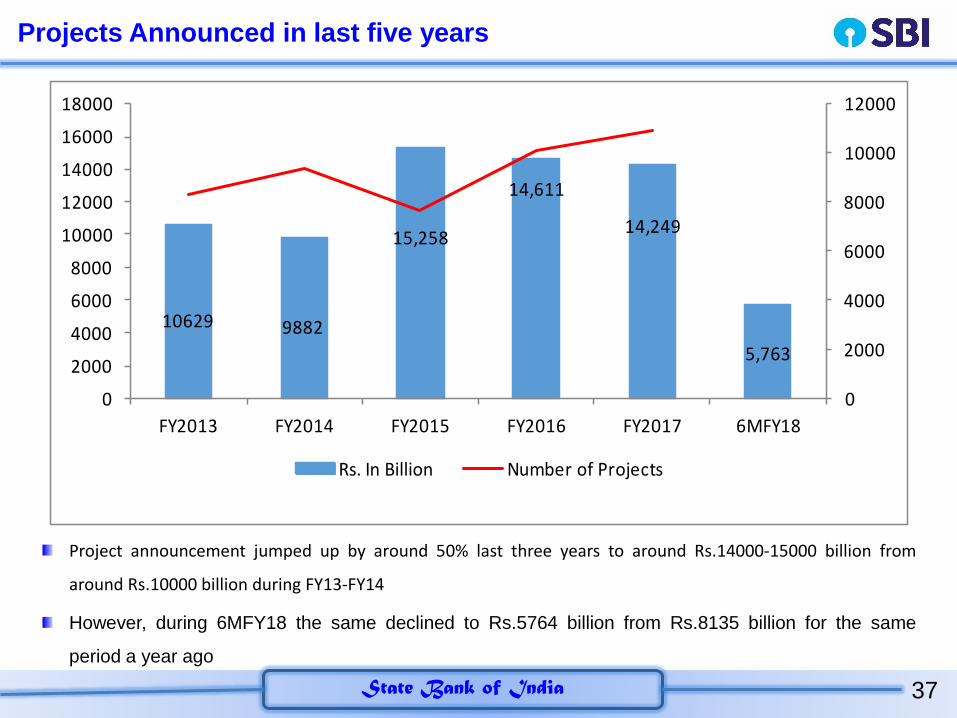

Projects Announced in last five years

10629 9882

15,258

14,611

14,249

5,763

0

2000

4000

6000

8000

10000

12000

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

FY2013 FY2014 FY2015 FY2016 FY2017 6MFY18

Rs. In Billion Number of Projects

Project announcement jumped up by around 50% last three years to around Rs.14000-15000 billion from

around Rs.10000 billion during FY13-FY14

However, during 6MFY18 the same declined to Rs.5764 billion from Rs.8135 billion for the same

period a year ago

38State Bank of India

Project Announced by ownership

Ownership Share (%) FY13 FY14 FY15 FY16 FY17 H1FY18

Government 46.1 69.05 63 66.26 71.36 71.13

State Government 45.57 56.66 53.96 45.15 51.58 54.89

Central Government 54.43 43.34 46.04 54.85 48.42 45.11

Private Sector 53.9 30.95 37 33.74 28.64 28.87

Indian Private Sector 95.36 92.33 86.68 79.69 13.97 21.55

Foreign Private Sector 4.64 7.67 13.32 20.31 86.03 78.45

All Sectors 100 100 100 100 100 100

Source: Projects Today; SBI Research

Projects Announced by Ownership

Share of Project announcement by Government increased substantially from 46% in FY13 to

71% in FY17

Share of Investment from Private sector declined from around 50% in FY13 to 28% in FY17

It appears that Foreign Private sector have shown confidence in Indian growth story and

increased their share substantially to around 80% in project announcement last year and first

six months also

39State Bank of India

Sectors FY15 FY16 FY17Total in 3

yearsFY17/FY16 H1FY18

Roadways 1,713 2,160 2,835 6,708 31% 1,059

Railways 2,304 1,354 2,625 6,283 94% 636

Electricity 1,691 1,483 204 3,378 -86% 345

Basic Chemicals 757 1,333 1,109 3,199 -17% 332

Community Services 1,067 978 934 2,978 -5% 466

Basic Metals 1,093 853 496 2,442 -42% 355

Non Conventional Energy 677 799 873 2,350 9% 172

Irrigation 430 404 1,229 2,063 204% 388

Mining 536 926 343 1,806 -63% 188

Machinery 408 645 732 1,785 14% 71

Power Distribution 634 433 69 1,136 -84% 284

Storage & Distribution 230 325 83 638 -74% 48

Gas Pipeline 23 63 416 502 557% 25

Food Products 218 114 138 470 21% 20

Commercial Complexes 106 129 225 460 75% 32

Airways (Aviation Infrastructure) 18 119 189 327 58% 51

Source: Projects Today; SBI Research

Projects announced by Sectors (Rs. In Billion)

Hot Spot – Roadways, Railways, Non Conventional Energy, Irrigation, Gas Pipe Lines etc.

40State Bank of India

Sector News

Road Sector - Govt. recently approved Rs. 7 trillion road construction plan, including BharatmalaPariyojana with a Rs. 5.35 trillion outlay for 34,800 kms with NHAI likely to spend Rs. 1.57 trillion for48,877 km of roads

Railways - Indian Railways (IR) targeting Rs.8.56 trillion investments over the next 5 years, IR is setfor a structural change. While High Speed Trains, Metros, Dedicated Freight Corridors (DFC) andRedevelopment of stations etc. Mumbai-Ahmedabad High Speed Rail (MAHSR) project (popularlyknown as Bullet Train is one of the big infra project with cost of Rs.1100 bn

Renewable Energy – Ambitious target capacity of 175 GW RE. Of this solar energy generationcapacity is at 100 GW (60 GW ground based and 40 GW roof top) and wind energy is at 60 GW by2022. India has an estimated renewable energy potential of about 900 GW from commerciallyexploitable sources

Port - Indian Ports saw the highest capacity addition in FY17 at 101 mtpa taking total capacity atIndian ports to 1066 mt as on March 17. Expected capacity addition at all major to grow by 5-6% CAGRin the next five years between fiscal 2017 and 2022, adding 275-325 MT of capacity

Initiation of an aggressive port infrastructure programme named as ‘Sagarmala’ with an objective ofrapid up-gradation of port connectivity and modernization to ensure efficient and cost effectiveevacuation of cargos. Under Sagarmala project, 415 projects have been identified with investment ofRs. 8000 bn

41State Bank of India

Financial Inclusion

42State Bank of India

Financial Inclusion

There are two aspects to financial inclusion: one is bank accounts and the second

is access to credit. PMJDY addresses the first problem. The issue of making credit

available to small borrowers remains

A very shallow penetration of insurance (3.5%) and social security (8%) is

another major issue. Although the government has launched a number of schemes

to provide pension and insurance services to the poor and those working in the

unorganised sector, these efforts are mainly supply-driven and results will depend

upon efforts to improve financial awareness among the poor

Strengthening the BC/BF model, to promote digital financial inclusion in the country

Need to reduce the excess cash in the economy, by accepting and giving money

through mobile payments etc.

Making banking habit of the people

43State Bank of India

Formalization of Economy: Rs 84,000 crore & Counting …

Considering the avg. balance of Rs 3000 in Jan Dhan account, so Rs 84,000 crore has been formalized into the system, through 28 crore A/cs

44State Bank of India

Mudra surge

Till now, the average ticket size of 10.17 crore units of PMMY loans disbursed is

around Rs 43,000 and around 80% of these loans have been sanctioned to women

entrepreneurs

Loans under Pradhan Mantri Mudra Yojana (PMMY)

FY16 FY17 FY18 (29-Dec) Total

No. of PMMY Loans ( in crores) 3.49 3.97 2.71 10.17

Amount Disbursed (Rs lakh crore) 1.33 1.75 1.29 4.37

45State Bank of India

Traction between Jan Dhan accounts and Mudra

In an in-house study within SBI we have found that there is a traction across Jan

Dhan and Mudra accounts

23% of Mudra loan account holders are women with an average ticket size of around

Rs 55,000

Distribution of the women entrepreneurs across India, with 36% of the accounts coming

from southern India (Andhra Pradesh, Tamil Nadu and Telengana) and 16% from

eastern India (West Bengal, Odisha and Assam) – laggard states witnessing more

traction

The Government must think seriously of creating a database pool of women

entrepreneurs across India. This will create a successful Mudra-Bank linkage

The experience of successful SHG-Bank linkage is a case in point in the Indian context.

There is no harm in emulating this in the context of better Mudra loan targeting by using

Jan Dhan account interface

46State Bank of India

Way Forward

47State Bank of India

Budget 2018-19: Expectations

Fiscal Deficit: We expect the Government to continue on its fiscal consolidation

path. However, this may not be construed as the overarching criterion and should

not come in the way of growth

Agriculture: The MSP determination at central level should be abolished and it

should be made state specific

Job Creation: Employment generation needs a major push so as to absorb the

ever growing workforce. Issues of adequacy of the capacity relation of the existing

training institutions, standardization and quality of trainers available in the country

and agencies who can certify these trainees need to be addressed on a war footing

MSME: The Budget can initiate a process for definitional change of MSMEs to be

revisited based on turnover of the enterprise

48State Bank of India

Urgent Need for Agri Reforms

Examine the APMC Act, Land Tenancy Act, and any such legally created structures

whose provisions are restrictive and create barriers to free trade

Rigorously pursue alternate marketing initiatives, like direct marketing and contract

farming

Establish stable trade policy based on tariff interventions instead of non-tariff trade

barriers

Develop and initiate competition in the agro-processing sector

Price support programme

Abolish the MSP determination at central level and make it state specific

The Agriculture sector can be digitalised in such a way that farmer can get a

platform to get farm inputs through online like e-Commerce services (delivery can

be through Post, e-Logistics) and get a platform to sell his products through online

49State Bank of India