Embed Size (px)

Citation preview

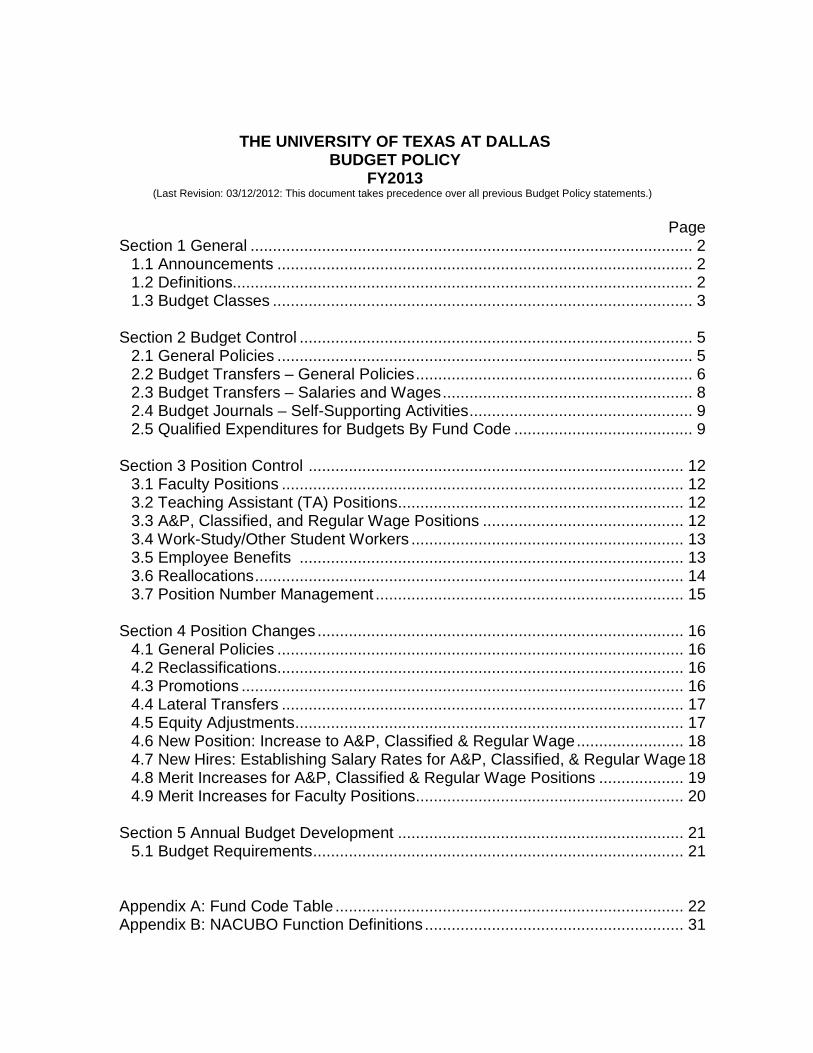

THE UNIVERSITY OF TEXAS AT DALLAS BUDGET POLICY

FY2013 (Last Revision: 03/12/2012: This document takes precedence over all previous Budget Policy statements.)

Page

Section 1 General ................................................................................................... 2 1.1 Announcements ............................................................................................. 2 1.2 Definitions....................................................................................................... 2 1.3 Budget Classes .............................................................................................. 3

Section 2 Budget Control ........................................................................................ 5

2.1 General Policies ............................................................................................. 5 2.2 Budget Transfers – General Policies .............................................................. 6 2.3 Budget Transfers – Salaries and Wages ........................................................ 8 2.4 Budget Journals – Self-Supporting Activities .................................................. 9 2.5 Qualified Expenditures for Budgets By Fund Code ........................................ 9

Section 3 Position Control .................................................................................... 12

3.1 Faculty Positions .......................................................................................... 12 3.2 Teaching Assistant (TA) Positions ................................................................ 12 3.3 A&P, Classified, and Regular Wage Positions ............................................. 12 3.4 Work-Study/Other Student Workers ............................................................. 13 3.5 Employee Benefits ...................................................................................... 13 3.6 Reallocations ................................................................................................ 14 3.7 Position Number Management ..................................................................... 15

Section 4 Position Changes .................................................................................. 16

4.1 General Policies ........................................................................................... 16 4.2 Reclassifications ........................................................................................... 16 4.3 Promotions ................................................................................................... 16 4.4 Lateral Transfers .......................................................................................... 17 4.5 Equity Adjustments ....................................................................................... 17 4.6 New Position: Increase to A&P, Classified & Regular Wage ........................ 18 4.7 New Hires: Establishing Salary Rates for A&P, Classified, & Regular Wage 18 4.8 Merit Increases for A&P, Classified & Regular Wage Positions ................... 19 4.9 Merit Increases for Faculty Positions ............................................................ 20

Section 5 Annual Budget Development ................................................................ 21

5.1 Budget Requirements ................................................................................... 21

Appendix A: Fund Code Table .............................................................................. 22 Appendix B: NACUBO Function Definitions .......................................................... 31

2

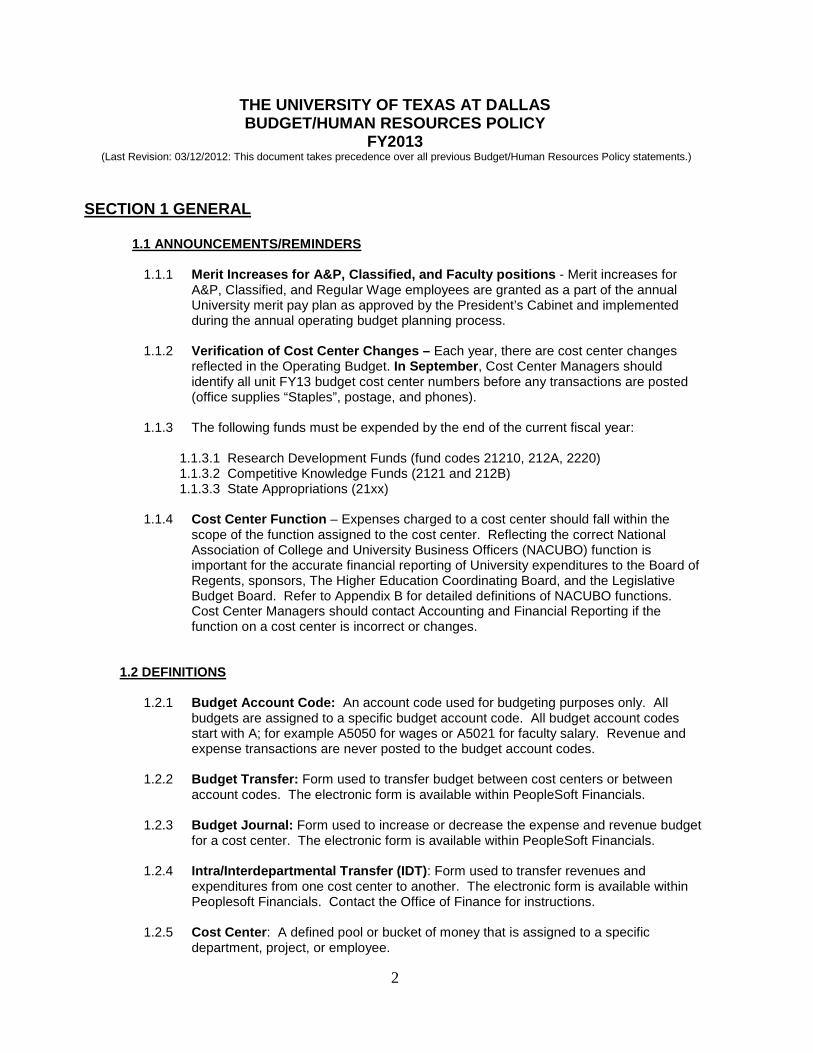

THE UNIVERSITY OF TEXAS AT DALLAS BUDGET/HUMAN RESOURCES POLICY

FY2013 (Last Revision: 03/12/2012: This document takes precedence over all previous Budget/Human Resources Policy statements.)

SECTION 1 GENERAL

1.1 ANNOUNCEMENTS/REMINDERS 1.1.1 Merit Increases for A&P, Classified, and Faculty positions - Merit increases for

A&P, Classified, and Regular Wage employees are granted as a part of the annual University merit pay plan as approved by the President’s Cabinet and implemented during the annual operating budget planning process.

1.1.2 Verification of Cost Center Changes – Each year, there are cost center changes

reflected in the Operating Budget. In September, Cost Center Managers should identify all unit FY13 budget cost center numbers before any transactions are posted (office supplies “Staples”, postage, and phones).

1.1.3 The following funds must be expended by the end of the current fiscal year:

1.1.3.1 Research Development Funds (fund codes 21210, 212A, 2220) 1.1.3.2 Competitive Knowledge Funds (2121 and 212B) 1.1.3.3 State Appropriations (21xx)

1.1.4 Cost Center Function – Expenses charged to a cost center should fall within the

scope of the function assigned to the cost center. Reflecting the correct National Association of College and University Business Officers (NACUBO) function is important for the accurate financial reporting of University expenditures to the Board of Regents, sponsors, The Higher Education Coordinating Board, and the Legislative Budget Board. Refer to Appendix B for detailed definitions of NACUBO functions. Cost Center Managers should contact Accounting and Financial Reporting if the function on a cost center is incorrect or changes.

1.2 DEFINITIONS 1.2.1 Budget Account Code: An account code used for budgeting purposes only. All

budgets are assigned to a specific budget account code. All budget account codes start with A; for example A5050 for wages or A5021 for faculty salary. Revenue and expense transactions are never posted to the budget account codes.

1.2.2 Budget Transfer: Form used to transfer budget between cost centers or between

account codes. The electronic form is available within PeopleSoft Financials.

1.2.3 Budget Journal: Form used to increase or decrease the expense and revenue budget for a cost center. The electronic form is available within PeopleSoft Financials.

1.2.4 Intra/Interdepartmental Transfer (IDT): Form used to transfer revenues and

expenditures from one cost center to another. The electronic form is available within Peoplesoft Financials. Contact the Office of Finance for instructions.

1.2.5 Cost Center: A defined pool or bucket of money that is assigned to a specific

department, project, or employee.

3

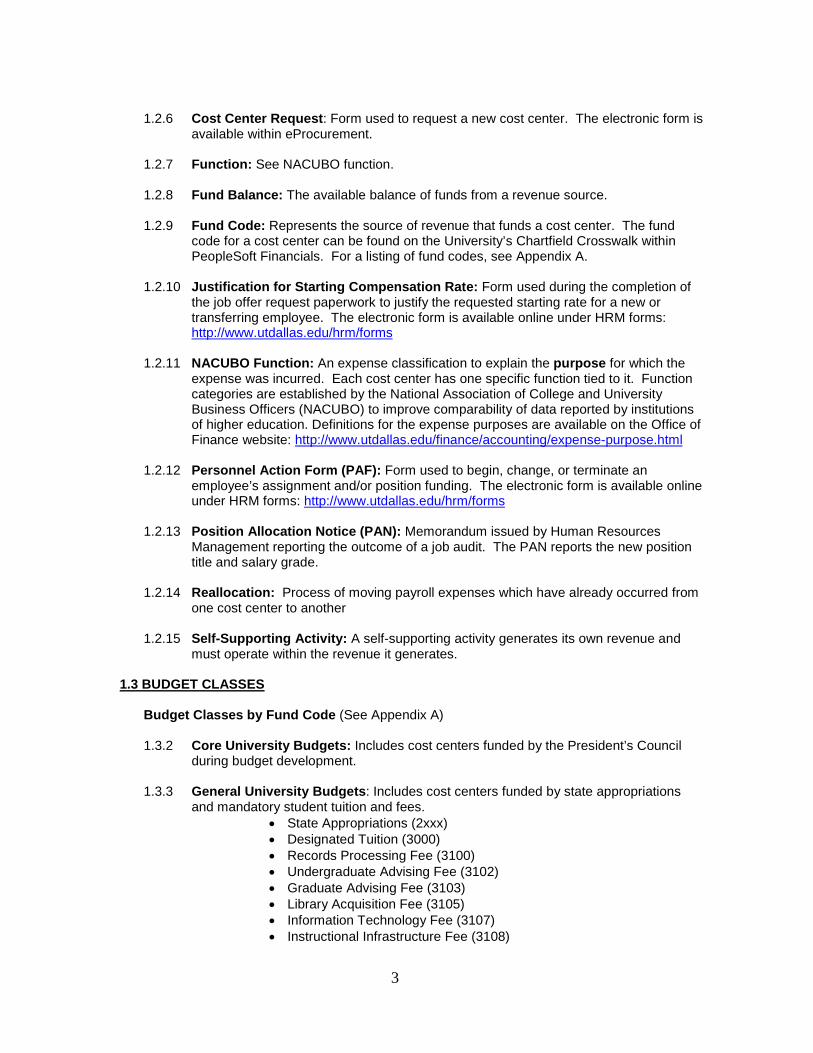

1.2.6 Cost Center Request: Form used to request a new cost center. The electronic form is

available within eProcurement.

1.2.7 Function: See NACUBO function.

1.2.8 Fund Balance: The available balance of funds from a revenue source.

1.2.9 Fund Code: Represents the source of revenue that funds a cost center. The fund code for a cost center can be found on the University’s Chartfield Crosswalk within PeopleSoft Financials. For a listing of fund codes, see Appendix A.

1.2.10 Justification for Starting Compensation Rate: Form used during the completion of

the job offer request paperwork to justify the requested starting rate for a new or transferring employee. The electronic form is available online under HRM forms: http://www.utdallas.edu/hrm/forms

1.2.11 NACUBO Function: An expense classification to explain the purpose for which the

expense was incurred. Each cost center has one specific function tied to it. Function categories are established by the National Association of College and University Business Officers (NACUBO) to improve comparability of data reported by institutions of higher education. Definitions for the expense purposes are available on the Office of Finance website: http://www.utdallas.edu/finance/accounting/expense-purpose.html

1.2.12 Personnel Action Form (PAF): Form used to begin, change, or terminate an

employee’s assignment and/or position funding. The electronic form is available online under HRM forms: http://www.utdallas.edu/hrm/forms

1.2.13 Position Allocation Notice (PAN): Memorandum issued by Human Resources

Management reporting the outcome of a job audit. The PAN reports the new position title and salary grade.

1.2.14 Reallocation: Process of moving payroll expenses which have already occurred from

one cost center to another

1.2.15 Self-Supporting Activity: A self-supporting activity generates its own revenue and must operate within the revenue it generates.

1.3 BUDGET CLASSES

Budget Classes by Fund Code (See Appendix A)

1.3.2 Core University Budgets: Includes cost centers funded by the President’s Council

during budget development.

1.3.3 General University Budgets: Includes cost centers funded by state appropriations and mandatory student tuition and fees.

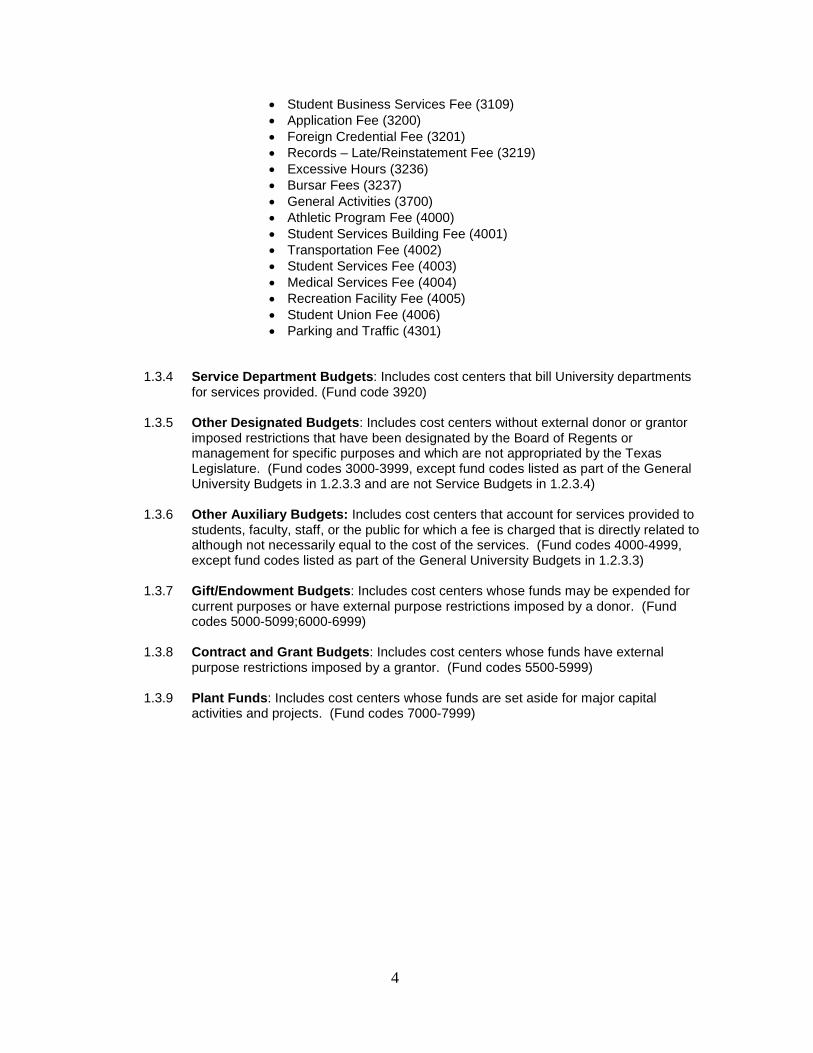

• State Appropriations (2xxx) • Designated Tuition (3000) • Records Processing Fee (3100) • Undergraduate Advising Fee (3102) • Graduate Advising Fee (3103) • Library Acquisition Fee (3105) • Information Technology Fee (3107) • Instructional Infrastructure Fee (3108)

4

• Student Business Services Fee (3109) • Application Fee (3200) • Foreign Credential Fee (3201) • Records – Late/Reinstatement Fee (3219) • Excessive Hours (3236) • Bursar Fees (3237) • General Activities (3700) • Athletic Program Fee (4000) • Student Services Building Fee (4001) • Transportation Fee (4002) • Student Services Fee (4003) • Medical Services Fee (4004) • Recreation Facility Fee (4005) • Student Union Fee (4006) • Parking and Traffic (4301)

1.3.4 Service Department Budgets: Includes cost centers that bill University departments for services provided. (Fund code 3920)

1.3.5 Other Designated Budgets: Includes cost centers without external donor or grantor

imposed restrictions that have been designated by the Board of Regents or management for specific purposes and which are not appropriated by the Texas Legislature. (Fund codes 3000-3999, except fund codes listed as part of the General University Budgets in 1.2.3.3 and are not Service Budgets in 1.2.3.4)

1.3.6 Other Auxiliary Budgets: Includes cost centers that account for services provided to

students, faculty, staff, or the public for which a fee is charged that is directly related to although not necessarily equal to the cost of the services. (Fund codes 4000-4999, except fund codes listed as part of the General University Budgets in 1.2.3.3)

1.3.7 Gift/Endowment Budgets: Includes cost centers whose funds may be expended for

current purposes or have external purpose restrictions imposed by a donor. (Fund codes 5000-5099;6000-6999)

1.3.8 Contract and Grant Budgets: Includes cost centers whose funds have external

purpose restrictions imposed by a grantor. (Fund codes 5500-5999)

1.3.9 Plant Funds: Includes cost centers whose funds are set aside for major capital activities and projects. (Fund codes 7000-7999)

5

SECTION 2 BUDGET CONTROL

2.1 GENERAL POLICIES

Each Cost Center Manager is responsible for ensuring that all commitments and expenditures are within the limits of the related budget. No commitments or payments should be made without identification of adequate qualified funding.

2.1.1 Transactions for all cost centers are subject to the available budget balances.

2.1.1.1 Adequate cost center and budget pool balance must be in the funding cost

center prior to the processing of requisitions, purchase vouchers, business expense reimbursements, travel vouchers, and travel advances by Procurement.

2.1.1.2 Adequate cost center and account balance must be in the funding cost center

before any position change is posted by the Budget Office.

2.1.1.2.1 For all non-general University budget cost centers, adequate funding includes adequate provision for Fringe Benefit costs in the A5500 account.

2.1.1.2.1 Budget Office verifies availability of funds for all cost centers except

Contracts & Grants.

2.1.1.2.2 Contract & Grant Accounting verifies availability of funds for positions funded from Contracts & Grants cost centers.

2.1.1.3 Payroll will not process requests for additional payments without adequate

budget funding in the correct cost center and budget account or if the total cost center balance is deficit.

2.1.1.4 Exceptions may be made in extraordinary circumstances to be approved by the

Budget Director or designee.

2.1.2 Student Information System items post without regard to budget funding. Cost Center Managers are expected to ensure that adequate funding is available to fulfill all scholarship, grant, and loan commitments.

2.1.3 Fund Balances

2.1.1.1 Year-end budget balances in General University Budgets cost centers will revert to University reserves. (See Appendix A for fund code list)

2.1.1.2 Year-end budget balances in non-general University budgets will close to the

related general ledger cost center identified by the fund code. (See Appendix A for fund code list)

2.1.4 Cost Center Deficit Policy: No deficit should exist on any operating cost center, except in extraordinary circumstances to be approved by the Budget Director or designee.

2.1.4.1 Budget deficits can be resolved by using a Budget Transfer to transfer in funds

from another cost center using the same funding source, by using an IDT to

6

transfer expenses to a different cost center, or by using a PAF to change position funding to a different cost center.

2.1.4.2 In addition to the above, for self-supporting accounts, budget deficits can be

resolved by using a Budget Journal to budget prior year funds or increase revenue. See Section 2.4.

2.1.4.3 Each unit is responsible for the resolution of its budget deficits. The President will review budget deficits in State and Designated Tuition cost centers at year-end. Unresolved budget deficits in these cost centers may be carried forward against the budget for the next fiscal year.

2.1.5 Fund Balance Deficit Policy: No deficit balance should exist in any fund balance, except in extraordinary circumstances to be approved by the Budget Director or designee.

2.1.5.1 During the last two weeks of September, Cost Center Managers should review

the Fund Balance Transfer Overview in PeopleSoft Financials for deficits. If a deficit exists, the Cost Center Manager is expected to reduce the FY2013 expenditure budget to eliminate the estimated year-end deficit.

2.1.5.2 During October, Budget Office Analysts will initiate required Budget Journals

for those units that fail to make the required adjustments described in Section 2.1.5.1.

2.1.5.3 No Budget Journals will be processed that will create a deficit fund balance.

2.1.5.3.1 There may be times that the available fund balance shows a deficit

balance. This is acceptable as long as the revenue estimate is realistic, and actual expenditures do not exceed the expenditure budget.

2.1.5.3.2 In order to prevent creation of fund balance deficits, it is critical that

budgeted revenues never exceed realistic expectations. If, after the budget is developed, additional information is available that indicates that the revenue estimate is not attainable, the Cost Center Manager should initiate a Budget Journal to adjust the revenue estimate accordingly. See Section 2.4.

2.1.5.3.3 If Cost Center Managers do not initiate appropriate adjustments to

address deficits during the year, the Budget Director is authorized to direct Budget Office Analysts to initiate such adjustments.

2.2 BUDGET TRANSFERS – GENERAL POLICIES

2.2.1 Absence Mode: When the Cost Center Manager, Dean, or Vice President (or designee) is scheduled to be out the office, that person may choose to register Absence Mode. This allows the individual to select another person to authorize or approve budget transfer requests in his or her absence. When authority is delegated to another person for approval of Budget Transfers, the Cost Center Manager, Dean, or Vice President is still responsible.

2.2.2 Limitations on transfers between accounts funded by these groups:

Budgets funded by this group: May only be transferred to:

7

State and Designated Tuition Cost Centers (fund codes 2000-2999 & 3000-3099)

Cost centers with fund codes 2000-2999 & 3000-3099, with the exceptions below.

Research Development Funds (fund codes 2120, 212A, 2220)

May not be transferred out of the Research Development Funds cost center groups. Note: All budgeted Research Development funds must be expended by the end of the current FY.

TARP/TATP Cost Centers (fund codes 2181, 2184, 2997)

May not be transferred out of the TARP/TATP cost centers. (Call the Office of Sponsored Projects concerning questions about transfers within these cost centers)

Budgets funded by this group: May only be transferred to: Special Item Cost Centers May not be transferred out of the

Special Item cost center groups. Note: All budgeted Special Item funds must be expended by the end of the current FY

American Recovery and Reinvestment Funds (ARRA) (fund code 2912)

May not be transferred out of the ARRA funds cost center groups.

Foreign Credential Fee (fund code 3201)

Cost centers with fund code 3201

Application Fee (fund code 3200) Cost centers with fund code 3200 Records Processing Fee (fund code 3100)

Cost centers with fund code 3100

Bursar Fees (fund code 3237) Cost centers with fund code 3237 Library Acquisition Fee (fund code 3105)

Cost centers with fund code 3105

Undergraduate Advising Fee (fund code 3102)

Cost centers with fund code 3102

Records – Late/Reinstatement Fee (fund code 3219)

Cost centers with fund code 3219

Information Technology Fee (fund code 3107)

Cost centers with fund code 3107

Infrastructure Fee (fund code 3108) Cost centers with fund code 3108 Graduate Advising Fee (fund code 3103)

Cost centers with fund code 3103

Recreation Facility Fee (fund code 4005)

Cost centers with fund code 4005

Student Union Fee (fund code 4006) Cost centers with fund code 4006 Student Services Fee (fund code 4003)

Cost centers with fund code 4003

Medical Services Fee (fund code 4004)

Cost centers with fund code 4004

Athletic Program Fee (fund code 4000)

Cost centers with fund code 4000

Parking and Traffic Fee (fund code 4301)

Cost centers with fund code 4301

Student Business Services Fee (fund code 3109)

Cost centers with fund code 3109

8

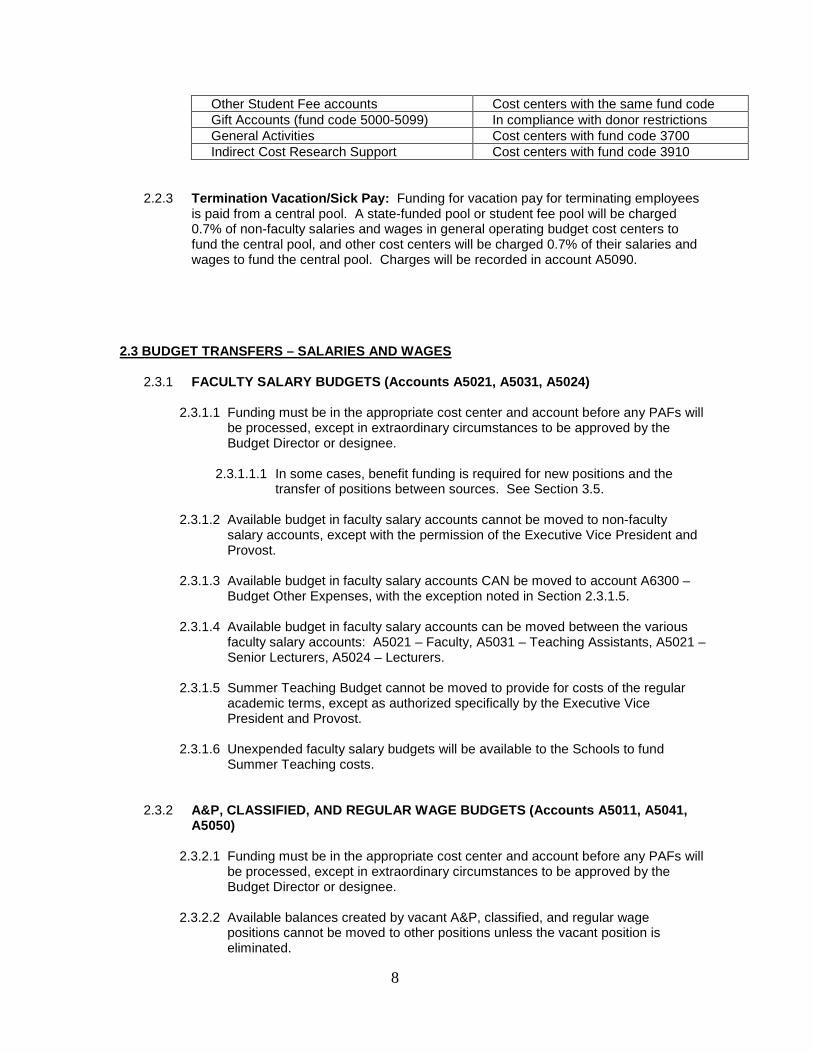

Other Student Fee accounts Cost centers with the same fund code Gift Accounts (fund code 5000-5099) In compliance with donor restrictions General Activities Cost centers with fund code 3700 Indirect Cost Research Support Cost centers with fund code 3910

2.2.3 Termination Vacation/Sick Pay: Funding for vacation pay for terminating employees is paid from a central pool. A state-funded pool or student fee pool will be charged 0.7% of non-faculty salaries and wages in general operating budget cost centers to fund the central pool, and other cost centers will be charged 0.7% of their salaries and wages to fund the central pool. Charges will be recorded in account A5090.

2.3 BUDGET TRANSFERS – SALARIES AND WAGES

2.3.1 FACULTY SALARY BUDGETS (Accounts A5021, A5031, A5024)

2.3.1.1 Funding must be in the appropriate cost center and account before any PAFs will

be processed, except in extraordinary circumstances to be approved by the Budget Director or designee.

2.3.1.1.1 In some cases, benefit funding is required for new positions and the

transfer of positions between sources. See Section 3.5. 2.3.1.2 Available budget in faculty salary accounts cannot be moved to non-faculty

salary accounts, except with the permission of the Executive Vice President and Provost.

2.3.1.3 Available budget in faculty salary accounts CAN be moved to account A6300 –

Budget Other Expenses, with the exception noted in Section 2.3.1.5.

2.3.1.4 Available budget in faculty salary accounts can be moved between the various faculty salary accounts: A5021 – Faculty, A5031 – Teaching Assistants, A5021 – Senior Lecturers, A5024 – Lecturers.

2.3.1.5 Summer Teaching Budget cannot be moved to provide for costs of the regular academic terms, except as authorized specifically by the Executive Vice President and Provost.

2.3.1.6 Unexpended faculty salary budgets will be available to the Schools to fund

Summer Teaching costs.

2.3.2 A&P, CLASSIFIED, AND REGULAR WAGE BUDGETS (Accounts A5011, A5041, A5050)

2.3.2.1 Funding must be in the appropriate cost center and account before any PAFs will

be processed, except in extraordinary circumstances to be approved by the Budget Director or designee.

2.3.2.2 Available balances created by vacant A&P, classified, and regular wage

positions cannot be moved to other positions unless the vacant position is eliminated.

9

2.3.2.3 With the exceptions listed below, available balance created by vacant A&P,

Classified, and regular wage positions CAN be moved to account A6300 – Budget Other Expenses.

2.3.2.3.1 Exceptions: Unused A&P and Classified Salaries in Administration,

Student Affairs, Budget and Finance, Enrollment Management, and Information Resources cost centers that are funded by General University Budgets will be lapsed monthly to central savings pools identified by source to be allocated by the appropriate Vice President. A&P and Classified Salaries in these areas cannot be moved to account A6300 – Budget Other Expenses, except in extraordinary circumstances to be approved by the Budget Director or designee.

2.3.2.4 If a position is reclassified between A&P, Classified, and Regular Wage, the

related budget for the newly reclassified position can be transferred into the appropriate account.

2.3.2.5 Transfers from account A6300 – Budget Other Expenses to fund increases in

current A&P, Classified, and Regular Wage positions or new positions are permitted only under the following conditions:

2.3.2.5.1 With the understanding, for non-academic units, that the Budget Transfer

used to fund the increase is your agreement for reduction in baseline M&O funding for the next budget development cycle (permanent budget transfer), in an amount equal to the full annual cost of the new position or position increase, including benefits.

2.4 BUDGET JOURNALS - SELF-SUPPORTING ACTIVITIES

2.4.1 Budgeted revenue estimates are expected to be realistic. If it is determined that any

budgeted revenue estimate is overstated, the unit must reduce the budgeted revenue.

2.4.2 If the reduced revenue estimate would result in a deficit budgeted fund balance, the unit must make necessary reductions in operating costs so that the operations are budgeted within available funding.

2.4.3 If the budgeted revenue estimate is understated, the unit may increase the budgeted

revenue. The reason for increased revenues must be documented. If this increase results in a budgeted fund surplus, the increased revenue may be used to increase the related operating budgets.

2.5 QUALIFIED EXPENDITURES FOR BUDGETS BY FUND CODE

2.5.1 State Appropriations: The expenditures listed below are not allowable on cost

centers funded by state appropriations (fund codes 2000-2999): • Food purchases, except for meal per diems associated with approved

business travel. • Alcohol purchases, which are never permitted with state funds even if

associated with meals while on approved business travel. • Expenses associated with holiday functions. • Flowers and non-cash gifts. • Employee achievement awards (length of service and retirement awards).

10

• Memberships to country clubs or exclusive dining clubs. • Charitable donations.

2.5.2 Designated Tuition and Fees: Alcohol purchases are not allowable on cost centers funded by student fees (fund codes 3000-3001 and all student fee fund codes)

• Alcohol purchases are not allowed on any cost center that includes student

fees.

2.5.3 Along with Designated Tuition, significant additional University resources are derived from five stipulated fees, the Instructional Infrastructure Fee, the Information Technology Fee, the Undergraduate Advising Fee, the Library Materials Fee and the Records Processing Fee. Unlike Designated Tuition funds, funds derived from these stipulated fees must be expended in accordance with the purposes for which the fees are charged. In particular, they cannot be expended directly for instruction.

2.5.4 Instructional Infrastructure Fee: Capital, Maintenance and Operation, and

Personnel costs that support Instruction. (fund code 3108)

2.5.4.1 Examples of appropriate uses are provision of, furnishing, and maintaining of classrooms, provision (capital, M&O and staff support) of instructional equipment to faculty, and equipping, supplying, maintaining and staffing of instructional laboratories.

2.5.4.2 Inappropriate uses would include support of faculty research not directly tied

to instruction, faculty salaries themselves, general departmental operations other than those described above, travel, and general University operations not directly tied to instruction.

2.5.5 Information Technology Fee: Capital, Maintenance and Operation, and Personnel

costs related to information technology. (fund code 3107)

2.5.5.1 Appropriate uses include essentially everything involved in the processing, transmitting and storing of “bits” or “digits” – software, hardware, personnel charges necessary to maintain computers and networks, and the administration and operation of the Information Resources division.

2.5.5.2 Inappropriate uses include costs of academic department telephones, non-

information processing devices tied to computers, such as projectors.

2.5.5.3 Overlaps: There are obviously significant overlaps between the appropriate uses of funds from Instructional Infrastructure and Information Technology Fees, but also some significant mutually excluded uses. For example, instructional computer laboratories could be funded from either fee, as could faculty computers for use in instruction. However, laboratory chemicals for course instruction could only be funded from the Instructional Infrastructure fee, while the costs of maintaining the central campus network could only be funded from the Information Technology fee.

2.5.6 Records Processing Fee: Personnel, Capital, and Maintenance and Operation

costs related to processing, distributing and storing academic records. (fund code 3100)

2.5.6.1 Appropriate uses are essentially noted in the fee description, with the

dominant offices supported by this fee being Records, Admissions, and Financial Aid, since these offices deal with student records.

11

2.5.6.2 Inappropriate uses would include costs of housing and maintaining the space

involved in records processing and extending the concept of “records” too broadly, to include for example, administrative correspondence or financial transactions not involving students.

2.5.7 Undergraduate Advising Fee: Personnel and some Maintenance and Operations costs of providing advisement to students on academic and career issues. (fund code 3102)

2.5.7.1 Appropriate uses include all costs (other than housing and basic utilities) of

providing advising on curricular planning, choices of major and electives, and post-graduation career choices. Appropriate personnel include professional advising staff and support staff, along with fractions of faculty and academic administration effort allocated to similar advising activities or supervision thereof.

2.5.7.2 Inappropriate uses would include direct instructional costs and costs of

general operations of academic instructional units.

2.5.8 Library Materials Fee: Purchase of and subscription to library materials, including books, periodicals, media, and electronic resources, along with expenses of procuring and installing these materials. (fund code 3105)

2.5.7 State Appropriations: The expenditures listed below are not allowable on cost

centers funded by state appropriations (fund codes 2000-2999)

• Food purchases, except for meal per diems associated with approved business travel.

• Alcohol purchases, which are never permitted with state funds even if associated with meals while on approved business travel.

• Expenses associated with holiday functions. • Flowers and non-cash gifts. • Employee achievement awards (length of service and retirement awards). • Memberships to country clubs or exclusive dining clubs. • Charitable donations.

12

SECTION 3 POSITION CONTROL

3.1 FACULTY POSITIONS

3.1.1 The Executive Vice President and Provost is responsible for position control for Faculty positions, and will, therefore, provide any necessary instructions to Deans and others relative to additions of FTE to the Faculty Salary category.

3.1.2 Faculty must be appointed for the full nine-month term. This funding can be derived

from multiple cost centers. 3.1.3 Appointments for less than nine months are permitted only if it is anticipated that the

position will exist for that lesser portion of the year.

3.1.4 If a cost center is coded as Function – Research (See Section 1.2.2.5), faculty positions on that account should use Job Code A00612 for Research Scientist – Faculty.

3.1.5 If a cost center is coded as Function – Public Service, Academic Support, Student

Services, or Instructional Support (See Section 1.2.2.5), faculty positions on that account should use Job Code A00611 – Administrative Assignment Faculty.

3.1.6 If a faculty member is to be funded in an advising fee cost center, the person should be

given an explicit advising assignment using the job code A00611 - Administrative Assignment Faculty – Job Group H.

3.1.7 All lecturers hired after the final budget prep worksheets have been completed (in August before the fiscal year begins) must be approved by the Executive Vice President and Provost or designee.

3.1.7.1 FY2013 Lecturer Salary Minimum: $23,100.

3.2 TEACHING ASSISTANT (TA) POSITIONS

3.2.1 TAs must be appointed for nine months. 3.2.2 TAs will be budgeted in Designated Tuition TA cost centers rather than State cost

centers. 3.2.3 All TAs hired after the final budget prep worksheets have been completed must be

approved by the Executive Vice President and Provost or designee. 3.2.4 FY2013 Teaching Assistant Salary Minimum: $20,100.

3.3 A&P, CLASSIFIED, AND REGULAR WAGE POSITIONS

3.3.1 Persons appointed to A&P, Classified, and Regular Wage positions must be appointed

for the full fiscal year. Position funding can include multiple cost centers. 3.3.2 Appointments for less than twelve months are permitted only if it is anticipated that the

position will exist for that lesser portion of the year.

3.3.3 Cost Center Managers are to ensure that adequate funding is in the appropriate wage pool prior to allowing a student or other hourly worker to perform services.

13

3.3.4 Academic units require approval of the Executive Vice President and Provost to fill any vacant A&P and Classified position. The Search Plan for A&P positions and the Job Requisition for Classified positions must be signed by the Executive Vice President and Provost or designee before it can be processed.

3.4 WORK-STUDY / OTHER STUDENT WORKERS

3.4.1 Work-study assignment start/end dates are determined by the Financial Aid Office and Career Center each year.

3.4.2 PAFs for work-study assignments must be routed through the Career Center before

going to Human Resources Management.

3.4.3 Job Code S09996 must be used for work-study students.

3.4.4 Position funding should be split as follows:

Federal Work-Study: 25% to the department’s cost center and 75% to the federal work-study cost center. Community Service Work-Study: 100% to community work-study cost center.

3.4.5 After the work-study end date, a new PAF would be required if a student were to

continue employment as non-workstudy funded 100% by the department.

3.4.6 For academic units, all PAFs related to student appointments exceeding $2,000 per semester should be routed to the Provost’s Office for signature before Budget can process them. The Executive Vice President and Provost or designee must authorize the appointment before the student begins work.

3.4.6.1 Note: In the case of work-study the $2,000 per semester appointment referred to

in Section 3.4.6 refers to the position funding paid by the department, not the total work-study award.

3.5 EMPLOYEE BENEFITS

3.5.1 State Cost Centers - Benefit budgets have been centralized for all cost centers funded from General University Budgets (See section 1.2.3.3). During payroll distribution, benefits are charged to the state benefit budget pools.

3.5.2 General University Cost Centers - If adding a new position or transferring a position

into cost centers funded by the following fees, a one-sided Budget Transfer should be prepared to transfer the cost of benefits to the central fee benefit cost center from the cost center funding the position. For salaries $90,000 or more, transfer 25% of the salary; for salaries under $90,000, transfer 30% of the salary.

o Records Processing Fee (3100) o Undergraduate Advising Fee (3102) o Graduate Advising Fee (3103) o Library Acquisition Fee (3105) o Information Technology Fee (3107) o Instructional Infrastructure Fee (3108) o Student Business Services Fee (3109) o Application Fee (3200) o Foreign Credential Fee (3201)

14

o Records – Late/Reinstatement Fee (3219) o Bursar Fees (3237) o Athletic Program Fee (4000) o Student Services Fee (4003) o Medical Services Fee (4004) o Recreation Facility Fee (4005) o Student Union Fee (4006) o Parking and Traffic (4301)

3.5.3 Designated Tuition Teaching Assistant Cost Centers - Benefit costs for Teaching

Assistants (TAs) paid from Designated Tuition TA cost centers are budgeted and funded centrally. Benefits for TAs assigned to other cost centers must be funded by the department.

3.5.4 Self-Supporting Cost Centers - For all non-general University budget cost centers, excluding the exceptions listed above, benefit costs are budgeted and paid from the cost center paying the salary.

3.6 REALLOCATIONS

3.6.1 Requirements:

3.6.1.1 No reallocations of salaries involving State cost centers will be allowed. This includes moving costs both from and to State cost centers, except in extraordinary circumstances to be approved by the Budget Director.

3.6.1.2 Exceptions are allowed for persons paid with Texas Advanced Technology

Program (TATP) and Texas Advanced Research Program (TARP) grants.

3.6.1.2.1 These exceptions must be processed within the two month period described in Section 3.6.2.1.

3.6.1.3 Salaries and wages cannot be paid from cost centers with fund code 9xxx;

therefore, individuals budgeted in those cost centers must be moved to a valid operating budget cost center with available funding prior to the related payroll deadline. Failure to move these positions to the appropriate cost center, along with required funding, and within the appropriate deadline will delay a payroll disbursement to the affected individual.

3.6.1.3.1 Cost transfers for Contract and Grants occurring after 90 days of the

original transaction and/or exceeding five percent (5%) of the annual award, must be approved by the VP for Budget and Finance and the Office of Sponsored Projects.

3.6.2 Frequency:

3.6.2.1 Reallocations of salary and wage expenditures may only be processed within two months of the current date, except in extraordinary circumstances to be approved by the Budget Director.

3.6.2.1.1 For example: If today is March 1st, then reallocations can only go back to

January 1st.

15

3.6.2.2 Year-end Limitation: Reallocation of July expenditures can be accepted only until August 15, and August payroll expenses cannot be reallocated.

3.7 POSITION NUMBER MANAGEMENT 3.7.1 Positions that have been vacant for more than 12 consecutive months will be

deactivated by Budget and Resource Planning.

3.7.2 Positions that have been reclassified will use the same position number.

3.7.3 New Position Numbers

3.7.3.1 An approved New Position Request (NPR) form must be submitted to Budget and Resource Planning before any new positions numbers will be created with the exceptions noted in section 3.7.3.3.

3.7.3.2 A Position Allocation Notice (PAN) must be attached to all New Position Requests for Administrative and Professional job codes and Classified job codes.

3.7.3.3 New position numbers for job codes listed below will be created by Budget and Resource Planning when an approved Personnel Action Form (PAF) is received which has a blank position number. An NPR is not required.

3.7.3.3.1 Part-time Lecturers (job codes F0051 and F0050) 3.7.3.3.2 Graduate Student Teaching Assistants (job code S00061) 3.7.3.3.3 Graduate Student Research Assistants (job code S000634) 3.7.3.3.4 Work-Study Students (job code S00996) 3.7.3.3.5 Hourly Student Workers (job code S00997)

16

SECTION 4 POSITION CHANGES

4.1 GENERAL POLICIES

4.1.1 All changes in personnel appointments and salaries require submission of the appropriate approved HRS forms by the established Payroll deadlines. Please see the Payroll website for the calendar: http://www.utdallas.edu/hrm/payroll/.

4.1.2 Funding must be provided before any actions resulting in a pay increase can be processed, except in extraordinary circumstances to be approved by the Budget Director or designee. See Section 2.3.

4.2 RECLASSIFICATION

4.2.1 Definition: A reclassification is the change of a current position from one title to a different title.

4.2.2 Requirements: Reclassifications are appropriate when the essential duties and

responsibilities of a position have markedly changed and must be supported by a job audit conducted by Human Resources Management (HRM).

4.2.3 Approval: The Position Description Form (PDF) requesting a job audit must be

approved by the appropriate Vice President, Executive Vice President and Provost, or Executive Director.

4.2.4 Frequency: Positions may not be submitted for audit more than one time within a 12

month period.

4.2.5 Timing of submissions: Reclassifications should be submitted to HRM during the annual operating budget development process to be effective in the next budget cycle.

4.2.6 Title Changes: If justified by the classification audit, HRM will authorize use of the

appropriate job title via a Position Allocation Notice (PAN). 4.2.7 Salary Changes: Subject to available funding, incumbents in reclassified positions will

receive an increase to a salary within the first third of the new salary range commensurate with their job-related education, experience, and skills, or a 3% increase in salary, whichever is higher. However, such employees may not receive more than the maximum rate of their assigned range.

4.3 PROMOTION

4.3.1 Definition: A promotion is defined as the situation where an existing employee is

competitively selected as the most qualified candidate for an existing vacant position. 4.3.2 Requirements:

4.3.2.1 The vacant position must have been posted (internally posted vacancies satisfy

this requirement) in accordance with current Human Resources Management (HRM) guidelines.

4.3.2.2 Written justification for the selection of the employee must be provided.

17

4.3.2.3 The current performance appraisal for the employee must be on file in HRM. 4.3.3 Approval: Promotions must be approved by the appropriate Vice President or

Executive Vice President and Provost. 4.3.4 Frequency:

4.3.4.1 The employee must have been employed by UT Dallas for at least six continuous

months, and 4.3.4.2 At least six months must have lapsed since the employee’s last promotion,

demotion, or equity adjustment. 4.3.4.2.1 Exception: Police cadets who graduated from the Police Academy in less

than six months are eligible for reclassification, including a title change and rate change to the base salary for a Police Officer.

4.3.5 Salary Changes: Subject to available funding, classified employees who are

promoted to another classified position will receive an increase to a salary within the first third of the new salary range commensurate with their job-related education, experience, and skills, or a 3% increase in salary, whichever is higher. However, such employees may not receive more than the maximum rate of their assigned range.

4.4 LATERAL TRANSFER

4.4.1 Definition: A lateral transfer is a change-in-duty assignment of an UT Dallas employee

that moves the employee to a classified title in the same salary range of their previous assignment. This applies to transfers within a department and transfers to another department.

4.4.2 Salary Changes: The salary can be increased, it can remain the same, or it can

decrease within the salary range. If an increase is provided, it can be no more than 3% above the pre-transfer salary and cannot exceed the maximum rate of their assigned range.

4.5 EQUITY ADJUSTMENT

4.5.1 Definition: An equity adjustment is a change in pay rate based on internal salary

parity, external labor market parity, or as a counteroffer to a written job offer. 4.5.2 Approval: Any request for an equity adjustment outside the regular budget process

must include a written justification and be recommended by the appropriate Vice President, Executive Vice President and Provost, Executive Director, or President.

4.5.2.1 Approved exceptions will be included on a monthly report of salary increases

provided to the President by the Budget Office. 4.5.3 Frequency:

4.5.3.1 Equity adjustments will be addressed during the annual budget process to be effective at the beginning of the new fiscal year.

4.5.3.2 During the year, counteroffer equity adjustments may be authorized if:

18

4.5.3.2.1 The counteroffer is approved in writing by the appropriate Vice President, Executive Vice President and Provost, or President.

4.5.3.2.2 A copy of the written job offer and justification for the specific amount of

equity adjustment is attached to the Personnel Action Form (PAF). 4.6 NEW POSITION: INCREASE TO A&P, CLASSIFIED, AND REGULAR WAGE FTE

4.6.1 Approval:

4.6.1.1 New positions must be approved by the appropriate Vice President or Executive Vice President and Provost.

4.6.1.1.1 Exception: Callier Center is exempt from this requirement. 4.6.1.1.2 Movement of positions from other funding sources to accounts funded by

General University Budgets (see Section 1.2.3.3) is considered increases in FTE, and this provision applies.

4.6.1.1.3 Approved new positions in General University Budgets will be included

on a monthly report of new positions provided to the President by the Budget Office.

4.6.2 Frequency: New positions should be added during the annual operating budget

development process.

4.6.2.1 Exception: Positions added outside the annual operating budget development process may be approved by the appropriate Vice President, Executive Vice and Provost, or the President.

4.6.3 Title: HRM will authorize use of the appropriate job title via a Position Allocation

Notice (PAN).

4.7 NEW HIRES: ESTABLISHING SALARY RATES FOR A&P, CLASSIFIED, AND REGULAR WAGE POSITIONS

Salary ranges for Classified and A&P positions require the approval of the Assistant VP for Human Resources Management. For Classified positions, a Justification for Starting Compensation Rate form should be attached to the job offer paperwork.

4.7.1 Salary Rates for New Classified Staff

4.7.1.1 Within the first third: Subject to availability of funding, administrative unit heads

may approve the hiring of classified employees within the first third of the classified salary range. Unit heads should use the following standards when exercising this responsibility:

4.7.1.1.1 Applicants whose job related education, experience and skills match the

minimum requirements stated in the job description should start at the range minimum.

4.7.1.1.2 Applicants whose job related education, experience and skills exceed the

minimum requirements stated in the job description may be started at a commensurately higher salary within the first third of the range.

19

4.7.1.2 Within the second third: Subject to available funding, administrative unit heads

may recommend to the Assistant VP for Human Resources Management and the appropriate Vice President, Executive Vice President and Provost, or Executive Director the hiring of classified employees within the second third of the classified salary range. Unit heads should use the following standards when exercising this responsibility:

4.7.1.2.1 The applicant has job related education, experience and skills markedly

superior to the minimum requirements stated in the job description, and 4.7.1.2.2 The applicant should possess education, skills, and experience

equivalent to those of individuals in similar positions who are “mid-career,” or

4.7.1.2.3 An unusual market condition has put a special premium on the particular

knowledge and skills required by the job.

4.7.1.2.4 Unit heads should use the Justification for Starting Compensation Rate form, available from Human Resources, to obtain approvals for the recommended starting rate.

4.7.1.3 Within the upper third: Subject to availability of funding, administrative unit

heads may recommend to the Assistant VP for Human Resources Management and the appropriate Vice President, Executive Vice President and Provost, or Executive Director the hiring of classified employees within the upper third of the classified salary range. Unit heads should use the following standards when exercising this responsibility:

4.7.1.3.1 Such recommendations to hire above the market rate must be based on

unusual circumstances and thoroughly justified. 4.7.1.3.2 Unit heads should use the Justification for Starting Compensation Rate

form, available from Human Resources, to obtain approvals for the recommended starting rate.

4.7.2 Salary Rates for New or Promoted A&P Staff

The salary of a new Administrative and Professional position or an increase for an employee promoted to an Administrative and Professional position shall be established in consultation with the Assistant VP for Human Resources Management and the appropriate Vice President, Executive Vice President and Provost, or Executive Director.

4.8 MERIT INCREASES FOR A&P, CLASSIFIED, AND REGULAR WAGE POSITIONS

4.8.1 Definition: A merit increase is a performance-based salary increase granted to an employee whose performance and productivity is consistently above that normally expected and required.

4.8.2 Requirements: The current performance appraisal for the employee must be on file in

Human Resources Management (HRM).

4.8.3 Approval: Merit increases must be approved by the appropriate Vice President, Executive Vice President and Provost, or Executive Director.

4.8.4 Frequency:

20

4.8.4.1 Merit increases for A&P, Classified, and Regular Wage employees are granted

as a part of the annual University merit pay plan as approved by the President’s Cabinet and implemented during the annual operating budget planning process.

4.8.4.2 No merit increases for these groups will be authorized outside the annual

University merit pay plan.

4.8.4.3 Merit increases may be granted only if the employee has been employed by the

University in that position for at least six continuous months before the effective date of the increase, and

4.8.4.4 The effective date of the increase must be at least six months after the

employee’s last promotion, transfer, or merit salary increase.

4.8.4.5 See Equity Adjustments in section 4.5 concerning requests for pay increases as a counteroffer.

4.9 MERIT INCREASES FOR FACULTY POSITIONS

4.9.1 Definition: Merit increases for faculty are based on job performance and are granted as a part of the annual University merit pay plan as approved President’s Cabinet and implemented during the annual operating budget planning process.

4.9.2 Frequency:

4.9.2.1 No merit increases for these groups will be authorized outside the annual

university merit pay plan. 4.9.2.2 Merit increases may be granted only if the employee has been employed by the

University in that position for at least six continuous months before the effective date of the increase, and

4.9.2.3 The effective date of the increase must be at least six months after the

employee’s last promotion, transfer, or merit salary increase.

21

SECTION 5 ANNUAL BUDGET DEVELOPMENT

5.1 Budget Requirements

5.1.1 Revenue Cost Centers: A justification must be submitted for any revenue projection that increases by 25% or more from the previous year’s actual revenue.

5.1.2 Service Centers: Any service center (fund code 3920) must have a rate study approved by Financial Accounting and Reporting before the annual budget will be approved and uploaded by Budget and Resource Planning. The rate study must be renewed each year.

5.1.3 Salaries for all active employees must be budgeted during the budget process with the exceptions listed below:

5.1.3.1 Employees who have submitted written notification of their intent to resign prior to the start of the fiscal year being budgeted.

5.1.3.2 Graduate Student Research and Teaching Assistants (RA or TA) who have exhausted the ten semester cap for being an RA or TA.

5.1.3.3 Part-time lecturers who are not scheduled to teach in the fall semester for the fiscal year being budgeted.

5.1.4 Salaries for positions which have been approved and are intended to be filled for the fiscal year being budgeted should be listed on the department’s budget submission.

5.1.5 Cost centers which have a zero fund balance and zero activity projected for the following year will be deactivated.

22

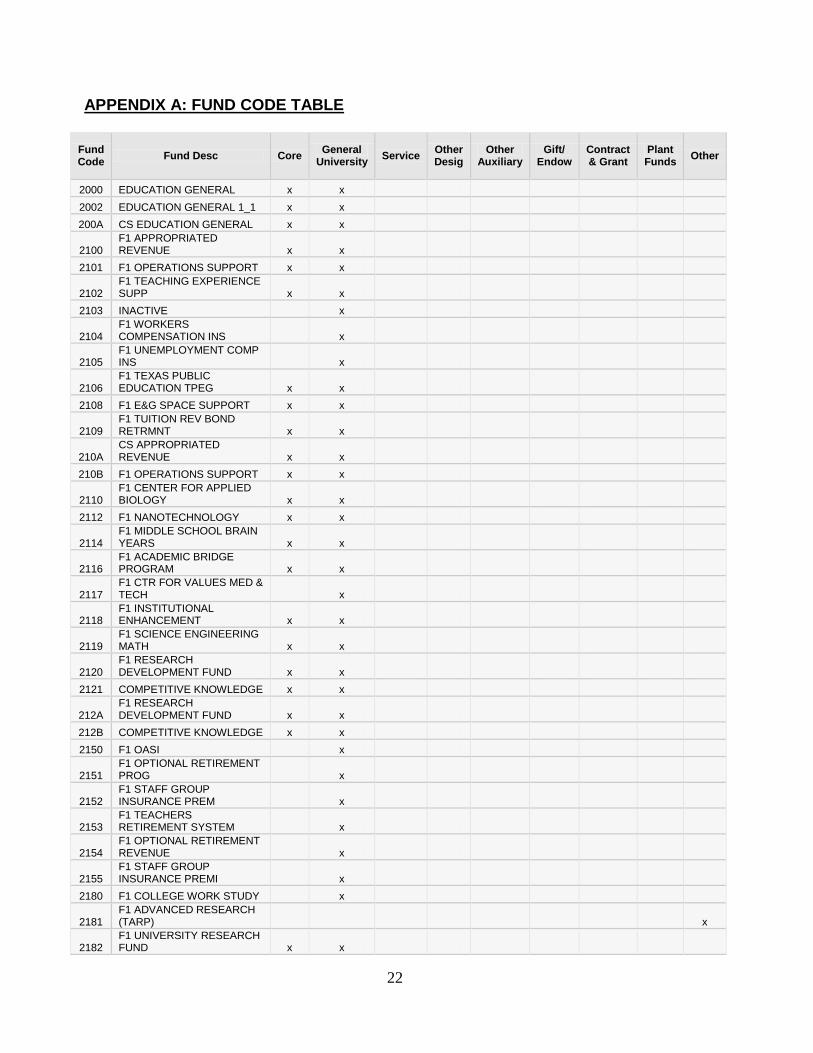

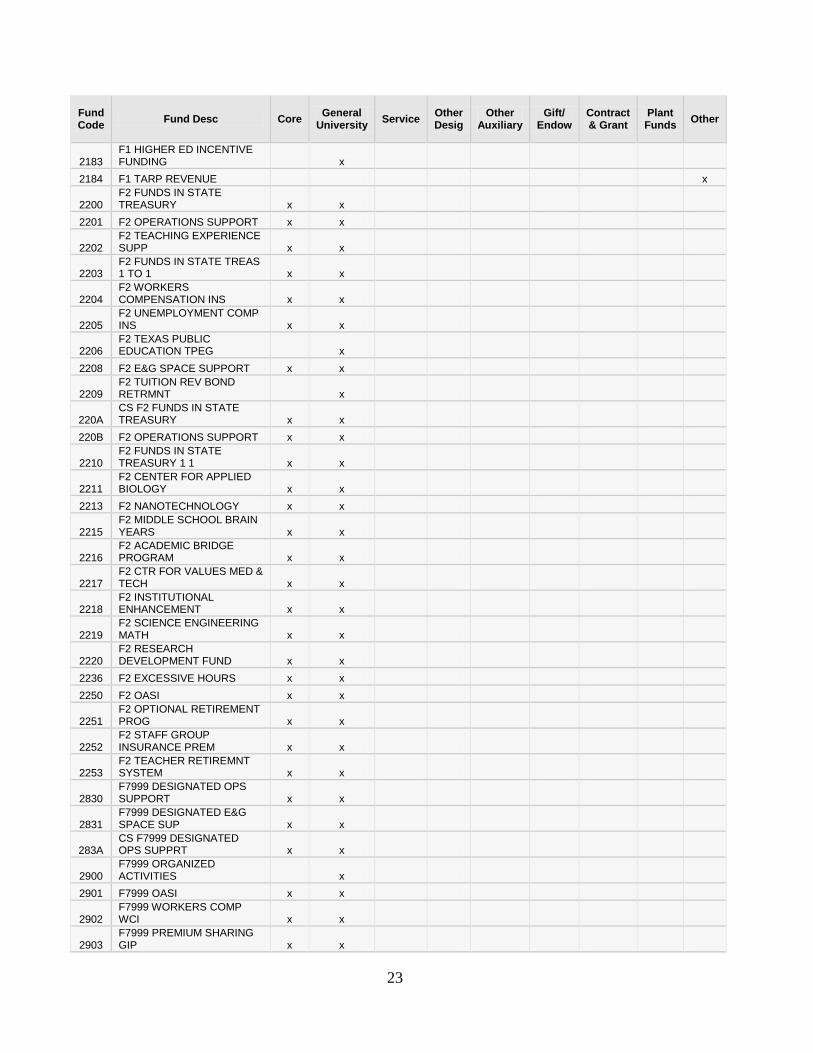

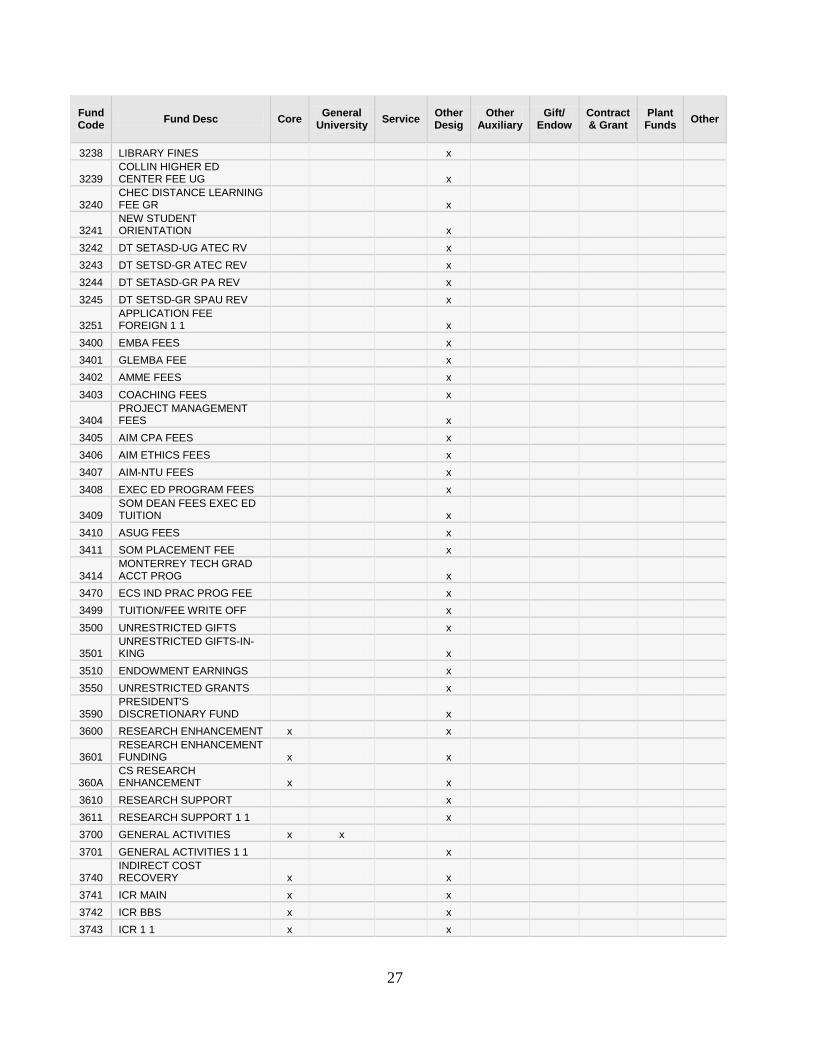

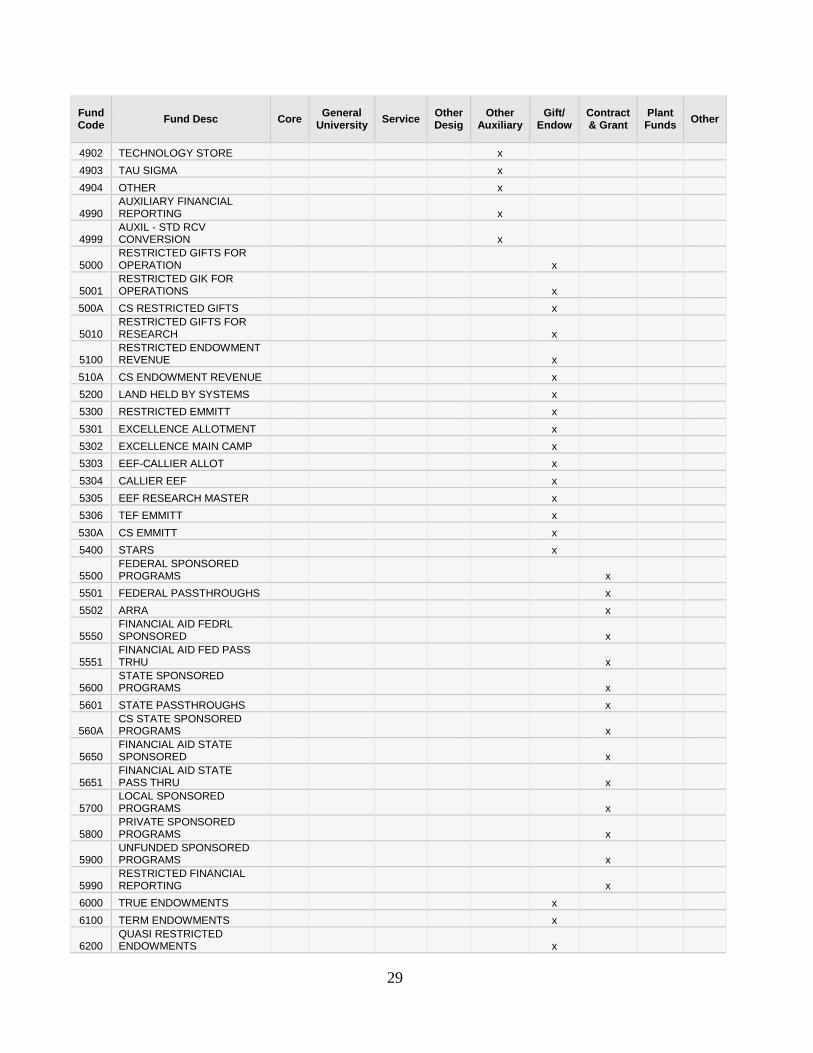

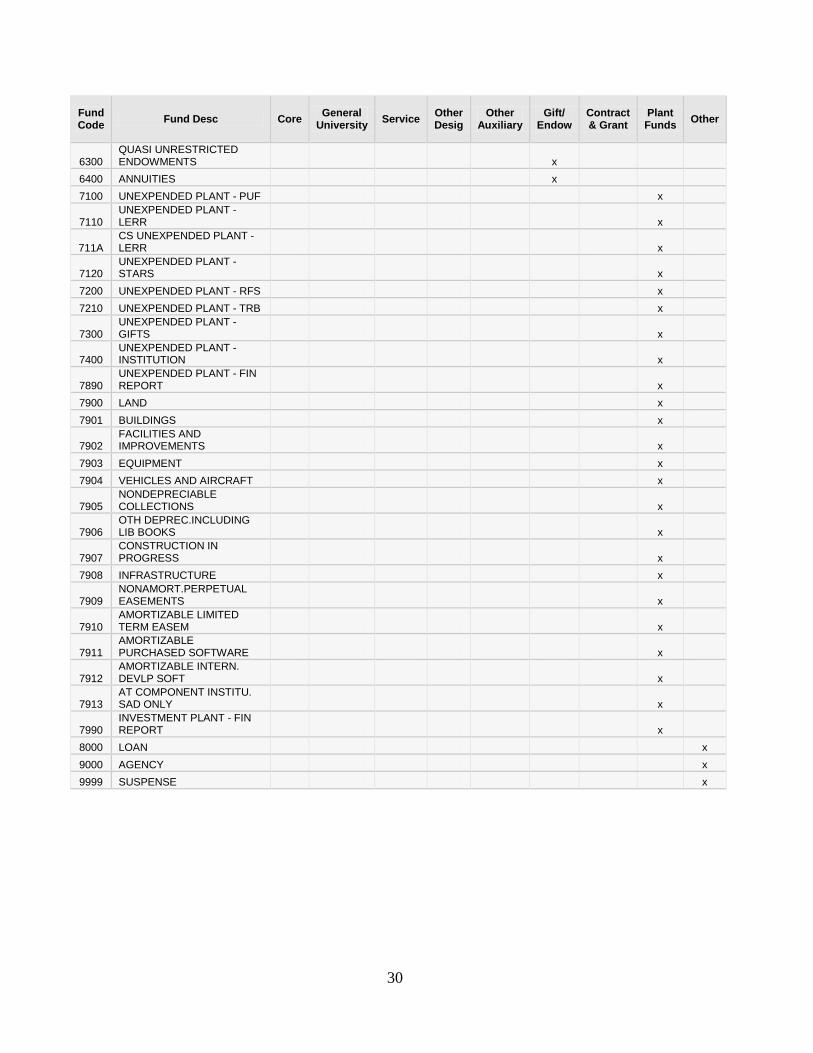

APPENDIX A: FUND CODE TABLE

Fund Code Fund Desc Core General

University Service Other Desig

Other Auxiliary

Gift/ Endow

Contract & Grant

Plant Funds Other

2000 EDUCATION GENERAL x x 2002 EDUCATION GENERAL 1_1 x x 200A CS EDUCATION GENERAL x x

2100 F1 APPROPRIATED REVENUE x x

2101 F1 OPERATIONS SUPPORT x x

2102 F1 TEACHING EXPERIENCE SUPP x x

2103 INACTIVE x

2104 F1 WORKERS COMPENSATION INS x

2105 F1 UNEMPLOYMENT COMP INS x

2106 F1 TEXAS PUBLIC EDUCATION TPEG x x

2108 F1 E&G SPACE SUPPORT x x

2109 F1 TUITION REV BOND RETRMNT x x

210A CS APPROPRIATED REVENUE x x

210B F1 OPERATIONS SUPPORT x x

2110 F1 CENTER FOR APPLIED BIOLOGY x x

2112 F1 NANOTECHNOLOGY x x

2114 F1 MIDDLE SCHOOL BRAIN YEARS x x

2116 F1 ACADEMIC BRIDGE PROGRAM x x

2117 F1 CTR FOR VALUES MED & TECH x

2118 F1 INSTITUTIONAL ENHANCEMENT x x

2119 F1 SCIENCE ENGINEERING MATH x x

2120 F1 RESEARCH DEVELOPMENT FUND x x

2121 COMPETITIVE KNOWLEDGE x x

212A F1 RESEARCH DEVELOPMENT FUND x x

212B COMPETITIVE KNOWLEDGE x x 2150 F1 OASI x

2151 F1 OPTIONAL RETIREMENT PROG x

2152 F1 STAFF GROUP INSURANCE PREM x

2153 F1 TEACHERS RETIREMENT SYSTEM x

2154 F1 OPTIONAL RETIREMENT REVENUE x

2155 F1 STAFF GROUP INSURANCE PREMI x

2180 F1 COLLEGE WORK STUDY x

2181 F1 ADVANCED RESEARCH (TARP) x

2182 F1 UNIVERSITY RESEARCH FUND x x

23

Fund Code Fund Desc Core General

University Service Other Desig

Other Auxiliary

Gift/ Endow

Contract & Grant

Plant Funds Other

2183 F1 HIGHER ED INCENTIVE FUNDING x

2184 F1 TARP REVENUE x

2200 F2 FUNDS IN STATE TREASURY x x

2201 F2 OPERATIONS SUPPORT x x

2202 F2 TEACHING EXPERIENCE SUPP x x

2203 F2 FUNDS IN STATE TREAS 1 TO 1 x x

2204 F2 WORKERS COMPENSATION INS x x

2205 F2 UNEMPLOYMENT COMP INS x x

2206 F2 TEXAS PUBLIC EDUCATION TPEG x

2208 F2 E&G SPACE SUPPORT x x

2209 F2 TUITION REV BOND RETRMNT x

220A CS F2 FUNDS IN STATE TREASURY x x

220B F2 OPERATIONS SUPPORT x x

2210 F2 FUNDS IN STATE TREASURY 1 1 x x

2211 F2 CENTER FOR APPLIED BIOLOGY x x

2213 F2 NANOTECHNOLOGY x x

2215 F2 MIDDLE SCHOOL BRAIN YEARS x x

2216 F2 ACADEMIC BRIDGE PROGRAM x x

2217 F2 CTR FOR VALUES MED & TECH x x

2218 F2 INSTITUTIONAL ENHANCEMENT x x

2219 F2 SCIENCE ENGINEERING MATH x x

2220 F2 RESEARCH DEVELOPMENT FUND x x

2236 F2 EXCESSIVE HOURS x x 2250 F2 OASI x x

2251 F2 OPTIONAL RETIREMENT PROG x x

2252 F2 STAFF GROUP INSURANCE PREM x x

2253 F2 TEACHER RETIREMNT SYSTEM x x

2830 F7999 DESIGNATED OPS SUPPORT x x

2831 F7999 DESIGNATED E&G SPACE SUP x x

283A CS F7999 DESIGNATED OPS SUPPRT x x

2900 F7999 ORGANIZED ACTIVITIES x

2901 F7999 OASI x x

2902 F7999 WORKERS COMP WCI x x

2903 F7999 PREMIUM SHARING GIP x x

24

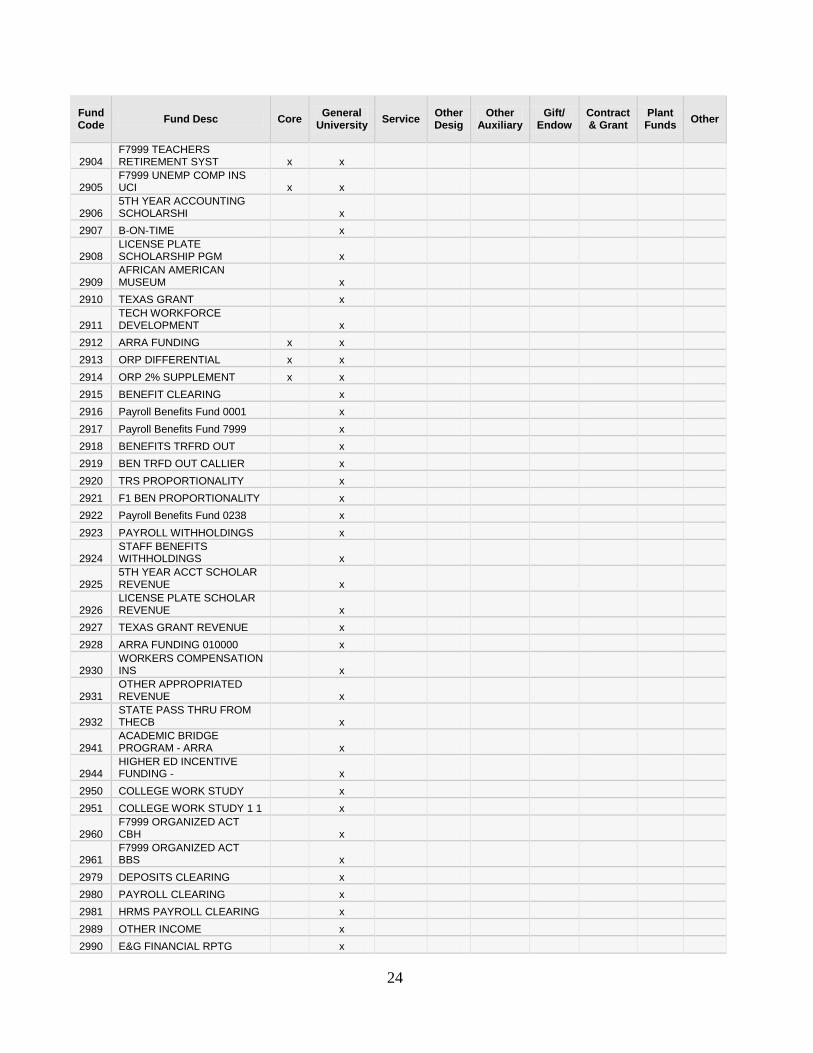

Fund Code Fund Desc Core General

University Service Other Desig

Other Auxiliary

Gift/ Endow

Contract & Grant

Plant Funds Other

2904 F7999 TEACHERS RETIREMENT SYST x x

2905 F7999 UNEMP COMP INS UCI x x

2906 5TH YEAR ACCOUNTING SCHOLARSHI x

2907 B-ON-TIME x

2908 LICENSE PLATE SCHOLARSHIP PGM x

2909 AFRICAN AMERICAN MUSEUM x

2910 TEXAS GRANT x

2911 TECH WORKFORCE DEVELOPMENT x

2912 ARRA FUNDING x x 2913 ORP DIFFERENTIAL x x 2914 ORP 2% SUPPLEMENT x x 2915 BENEFIT CLEARING x 2916 Payroll Benefits Fund 0001 x 2917 Payroll Benefits Fund 7999 x 2918 BENEFITS TRFRD OUT x 2919 BEN TRFD OUT CALLIER x 2920 TRS PROPORTIONALITY x 2921 F1 BEN PROPORTIONALITY x 2922 Payroll Benefits Fund 0238 x 2923 PAYROLL WITHHOLDINGS x

2924 STAFF BENEFITS WITHHOLDINGS x

2925 5TH YEAR ACCT SCHOLAR REVENUE x

2926 LICENSE PLATE SCHOLAR REVENUE x

2927 TEXAS GRANT REVENUE x 2928 ARRA FUNDING 010000 x

2930 WORKERS COMPENSATION INS x

2931 OTHER APPROPRIATED REVENUE x

2932 STATE PASS THRU FROM THECB x

2941 ACADEMIC BRIDGE PROGRAM - ARRA x

2944 HIGHER ED INCENTIVE FUNDING - x

2950 COLLEGE WORK STUDY x 2951 COLLEGE WORK STUDY 1 1 x

2960 F7999 ORGANIZED ACT CBH x

2961 F7999 ORGANIZED ACT BBS x

2979 DEPOSITS CLEARING x 2980 PAYROLL CLEARING x 2981 HRMS PAYROLL CLEARING x 2989 OTHER INCOME x 2990 E&G FINANCIAL RPTG x

25

Fund Code Fund Desc Core General

University Service Other Desig

Other Auxiliary

Gift/ Endow

Contract & Grant

Plant Funds Other

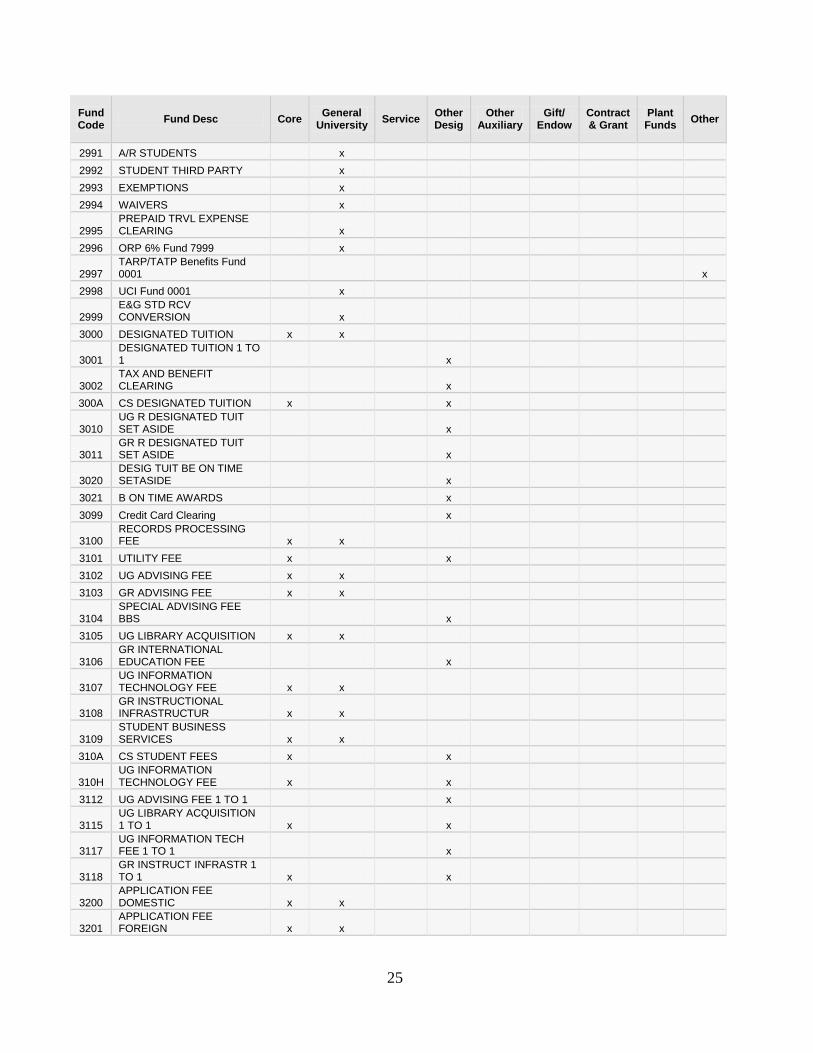

2991 A/R STUDENTS x 2992 STUDENT THIRD PARTY x 2993 EXEMPTIONS x 2994 WAIVERS x

2995 PREPAID TRVL EXPENSE CLEARING x

2996 ORP 6% Fund 7999 x

2997 TARP/TATP Benefits Fund 0001 x

2998 UCI Fund 0001 x

2999 E&G STD RCV CONVERSION x

3000 DESIGNATED TUITION x x

3001 DESIGNATED TUITION 1 TO 1 x

3002 TAX AND BENEFIT CLEARING x

300A CS DESIGNATED TUITION x x

3010 UG R DESIGNATED TUIT SET ASIDE x

3011 GR R DESIGNATED TUIT SET ASIDE x

3020 DESIG TUIT BE ON TIME SETASIDE x

3021 B ON TIME AWARDS x 3099 Credit Card Clearing x

3100 RECORDS PROCESSING FEE x x

3101 UTILITY FEE x x 3102 UG ADVISING FEE x x 3103 GR ADVISING FEE x x

3104 SPECIAL ADVISING FEE BBS x

3105 UG LIBRARY ACQUISITION x x

3106 GR INTERNATIONAL EDUCATION FEE x

3107 UG INFORMATION TECHNOLOGY FEE x x

3108 GR INSTRUCTIONAL INFRASTRUCTUR x x

3109 STUDENT BUSINESS SERVICES x x

310A CS STUDENT FEES x x

310H UG INFORMATION TECHNOLOGY FEE x x

3112 UG ADVISING FEE 1 TO 1 x

3115 UG LIBRARY ACQUISITION 1 TO 1 x x

3117 UG INFORMATION TECH FEE 1 TO 1 x

3118 GR INSTRUCT INFRASTR 1 TO 1 x x

3200 APPLICATION FEE DOMESTIC x x

3201 APPLICATION FEE FOREIGN x x

26

Fund Code Fund Desc Core General

University Service Other Desig

Other Auxiliary

Gift/ Endow

Contract & Grant

Plant Funds Other

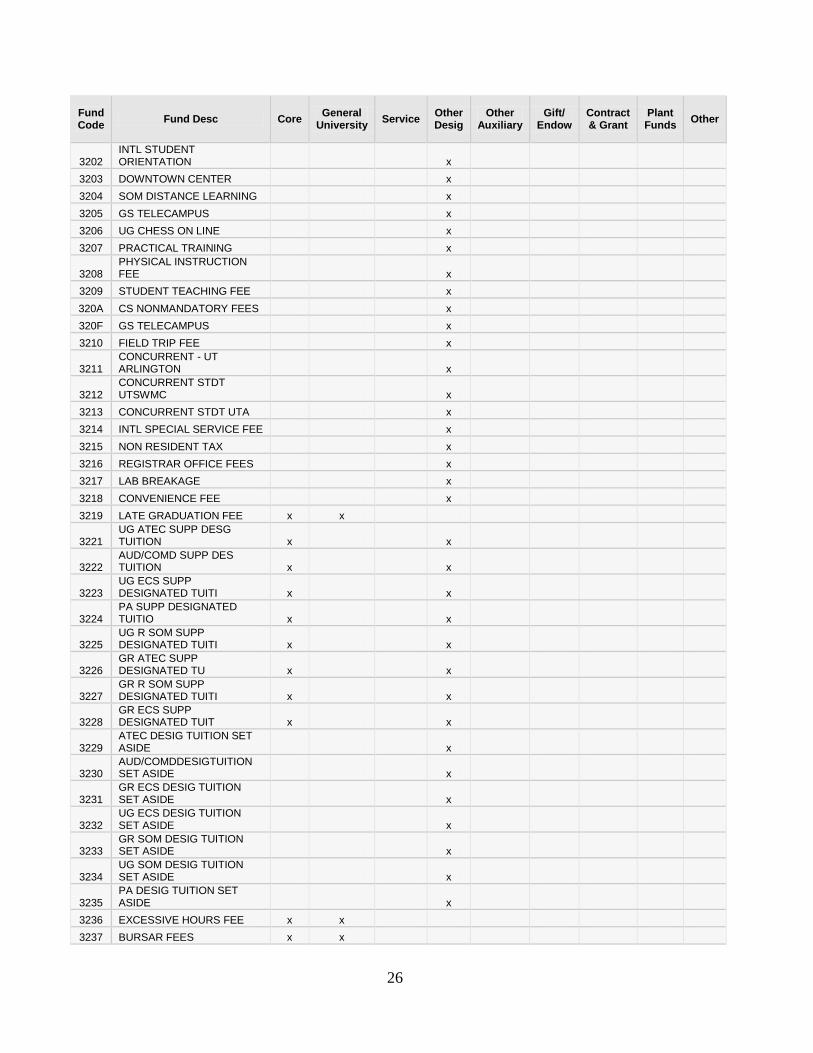

3202 INTL STUDENT ORIENTATION x

3203 DOWNTOWN CENTER x 3204 SOM DISTANCE LEARNING x 3205 GS TELECAMPUS x 3206 UG CHESS ON LINE x 3207 PRACTICAL TRAINING x

3208 PHYSICAL INSTRUCTION FEE x

3209 STUDENT TEACHING FEE x 320A CS NONMANDATORY FEES x 320F GS TELECAMPUS x 3210 FIELD TRIP FEE x

3211 CONCURRENT - UT ARLINGTON x

3212 CONCURRENT STDT UTSWMC x

3213 CONCURRENT STDT UTA x 3214 INTL SPECIAL SERVICE FEE x 3215 NON RESIDENT TAX x 3216 REGISTRAR OFFICE FEES x 3217 LAB BREAKAGE x 3218 CONVENIENCE FEE x 3219 LATE GRADUATION FEE x x

3221 UG ATEC SUPP DESG TUITION x x

3222 AUD/COMD SUPP DES TUITION x x

3223 UG ECS SUPP DESIGNATED TUITI x x

3224 PA SUPP DESIGNATED TUITIO x x

3225 UG R SOM SUPP DESIGNATED TUITI x x

3226 GR ATEC SUPP DESIGNATED TU x x

3227 GR R SOM SUPP DESIGNATED TUITI x x

3228 GR ECS SUPP DESIGNATED TUIT x x

3229 ATEC DESIG TUITION SET ASIDE x

3230 AUD/COMDDESIGTUITION SET ASIDE x

3231 GR ECS DESIG TUITION SET ASIDE x

3232 UG ECS DESIG TUITION SET ASIDE x

3233 GR SOM DESIG TUITION SET ASIDE x

3234 UG SOM DESIG TUITION SET ASIDE x

3235 PA DESIG TUITION SET ASIDE x

3236 EXCESSIVE HOURS FEE x x 3237 BURSAR FEES x x

27

Fund Code Fund Desc Core General

University Service Other Desig

Other Auxiliary

Gift/ Endow

Contract & Grant

Plant Funds Other

3238 LIBRARY FINES x

3239 COLLIN HIGHER ED CENTER FEE UG x

3240 CHEC DISTANCE LEARNING FEE GR x

3241 NEW STUDENT ORIENTATION x

3242 DT SETASD-UG ATEC RV x 3243 DT SETSD-GR ATEC REV x 3244 DT SETASD-GR PA REV x 3245 DT SETSD-GR SPAU REV x

3251 APPLICATION FEE FOREIGN 1 1 x

3400 EMBA FEES x 3401 GLEMBA FEE x 3402 AMME FEES x 3403 COACHING FEES x

3404 PROJECT MANAGEMENT FEES x

3405 AIM CPA FEES x 3406 AIM ETHICS FEES x 3407 AIM-NTU FEES x 3408 EXEC ED PROGRAM FEES x

3409 SOM DEAN FEES EXEC ED TUITION x

3410 ASUG FEES x 3411 SOM PLACEMENT FEE x

3414 MONTERREY TECH GRAD ACCT PROG x

3470 ECS IND PRAC PROG FEE x 3499 TUITION/FEE WRITE OFF x 3500 UNRESTRICTED GIFTS x

3501 UNRESTRICTED GIFTS-IN-KING x

3510 ENDOWMENT EARNINGS x 3550 UNRESTRICTED GRANTS x

3590 PRESIDENT'S DISCRETIONARY FUND x

3600 RESEARCH ENHANCEMENT x x

3601 RESEARCH ENHANCEMENT FUNDING x x

360A CS RESEARCH ENHANCEMENT x x

3610 RESEARCH SUPPORT x 3611 RESEARCH SUPPORT 1 1 x 3700 GENERAL ACTIVITIES x x 3701 GENERAL ACTIVITIES 1 1 x

3740 INDIRECT COST RECOVERY x x

3741 ICR MAIN x x 3742 ICR BBS x x 3743 ICR 1 1 x x

28

Fund Code Fund Desc Core General

University Service Other Desig

Other Auxiliary

Gift/ Endow

Contract & Grant

Plant Funds Other

374A CS INDIRECT COST RECOVERY x x

374B CS ICR MAIN x 3800 TRIP x

3900 UNRESTRICTED ENDOWMENT REVENUE x

3901 UNRESTRICTED REV 1 1 x 3910 EXTERNAL SALES x 3920 SERVICE CENTERS x x 3930 TPEG x

3940 FINANCIAL AID ADMINISTRATION x

3950 SURPLUS SALES x 3960 OTHER INCOME x

3989 GENERAL CLEARING ACCOUNT x

3990 DESIGNATED FINANCIAL REPORTING x

3999 DESIG - STD RCV CONVERSION x

4000 ATHLETIC FEE x

4001 STUDENT SERVICES BUILDING FEE x

4002 TRANSPORTATION FEE x 4003 STUDENT SERVICES FEE x 4004 MEDICAL SERVICES FEE x

4005 RECREATIONAL FACILITY FEE x

4006 STUDENT UNION FEE x

4007 STUDENT SERVICES BUILDING FEE x

4008 STUDENT SERV FEE KM x 4009 STUDENT HEALTH x 4300 INTERLIBRARY LOAN FEE x 4301 PARKING FEES/FINES x 4302 MEAL PLANS x 4303 STUDENT INSURANCE x 4304 PARK AND TRAFFIC x 4600 STUDENT ACTIVITIES x 4610 ATHLETICS x 4620 BOOKSTORE x 4630 LAB MEDICAL REVENUE x

4640 LIVING AND LEARNING CENTER x

4650 FOOD SERVICE x 4651 FOOD SERVICE 1 1 x 4652 CALLIER FOOD x 4660 HOUSING x 4661 UNIV PRK RENTAL x 4662 UNIV PRK RESERVE x 4900 STATE FORFEITURE FUND x 4901 NEWSPAPER x

29

Fund Code Fund Desc Core General

University Service Other Desig

Other Auxiliary

Gift/ Endow

Contract & Grant

Plant Funds Other

4902 TECHNOLOGY STORE x 4903 TAU SIGMA x 4904 OTHER x

4990 AUXILIARY FINANCIAL REPORTING x

4999 AUXIL - STD RCV CONVERSION x

5000 RESTRICTED GIFTS FOR OPERATION x

5001 RESTRICTED GIK FOR OPERATIONS x

500A CS RESTRICTED GIFTS x

5010 RESTRICTED GIFTS FOR RESEARCH x

5100 RESTRICTED ENDOWMENT REVENUE x

510A CS ENDOWMENT REVENUE x 5200 LAND HELD BY SYSTEMS x 5300 RESTRICTED EMMITT x 5301 EXCELLENCE ALLOTMENT x 5302 EXCELLENCE MAIN CAMP x 5303 EEF-CALLIER ALLOT x 5304 CALLIER EEF x 5305 EEF RESEARCH MASTER x 5306 TEF EMMITT x 530A CS EMMITT x 5400 STARS x

5500 FEDERAL SPONSORED PROGRAMS x

5501 FEDERAL PASSTHROUGHS x 5502 ARRA x

5550 FINANCIAL AID FEDRL SPONSORED x

5551 FINANCIAL AID FED PASS TRHU x

5600 STATE SPONSORED PROGRAMS x

5601 STATE PASSTHROUGHS x

560A CS STATE SPONSORED PROGRAMS x

5650 FINANCIAL AID STATE SPONSORED x

5651 FINANCIAL AID STATE PASS THRU x

5700 LOCAL SPONSORED PROGRAMS x

5800 PRIVATE SPONSORED PROGRAMS x

5900 UNFUNDED SPONSORED PROGRAMS x

5990 RESTRICTED FINANCIAL REPORTING x

6000 TRUE ENDOWMENTS x 6100 TERM ENDOWMENTS x

6200 QUASI RESTRICTED ENDOWMENTS x

30

Fund Code Fund Desc Core General

University Service Other Desig

Other Auxiliary

Gift/ Endow

Contract & Grant

Plant Funds Other

6300 QUASI UNRESTRICTED ENDOWMENTS x

6400 ANNUITIES x 7100 UNEXPENDED PLANT - PUF x

7110 UNEXPENDED PLANT - LERR x

711A CS UNEXPENDED PLANT - LERR x

7120 UNEXPENDED PLANT - STARS x

7200 UNEXPENDED PLANT - RFS x 7210 UNEXPENDED PLANT - TRB x

7300 UNEXPENDED PLANT - GIFTS x

7400 UNEXPENDED PLANT - INSTITUTION x

7890 UNEXPENDED PLANT - FIN REPORT x

7900 LAND x 7901 BUILDINGS x

7902 FACILITIES AND IMPROVEMENTS x

7903 EQUIPMENT x 7904 VEHICLES AND AIRCRAFT x

7905 NONDEPRECIABLE COLLECTIONS x

7906 OTH DEPREC.INCLUDING LIB BOOKS x

7907 CONSTRUCTION IN PROGRESS x

7908 INFRASTRUCTURE x

7909 NONAMORT.PERPETUAL EASEMENTS x

7910 AMORTIZABLE LIMITED TERM EASEM x

7911 AMORTIZABLE PURCHASED SOFTWARE x

7912 AMORTIZABLE INTERN. DEVLP SOFT x

7913 AT COMPONENT INSTITU. SAD ONLY x

7990 INVESTMENT PLANT - FIN REPORT x

8000 LOAN x 9000 AGENCY x 9999 SUSPENSE x

31

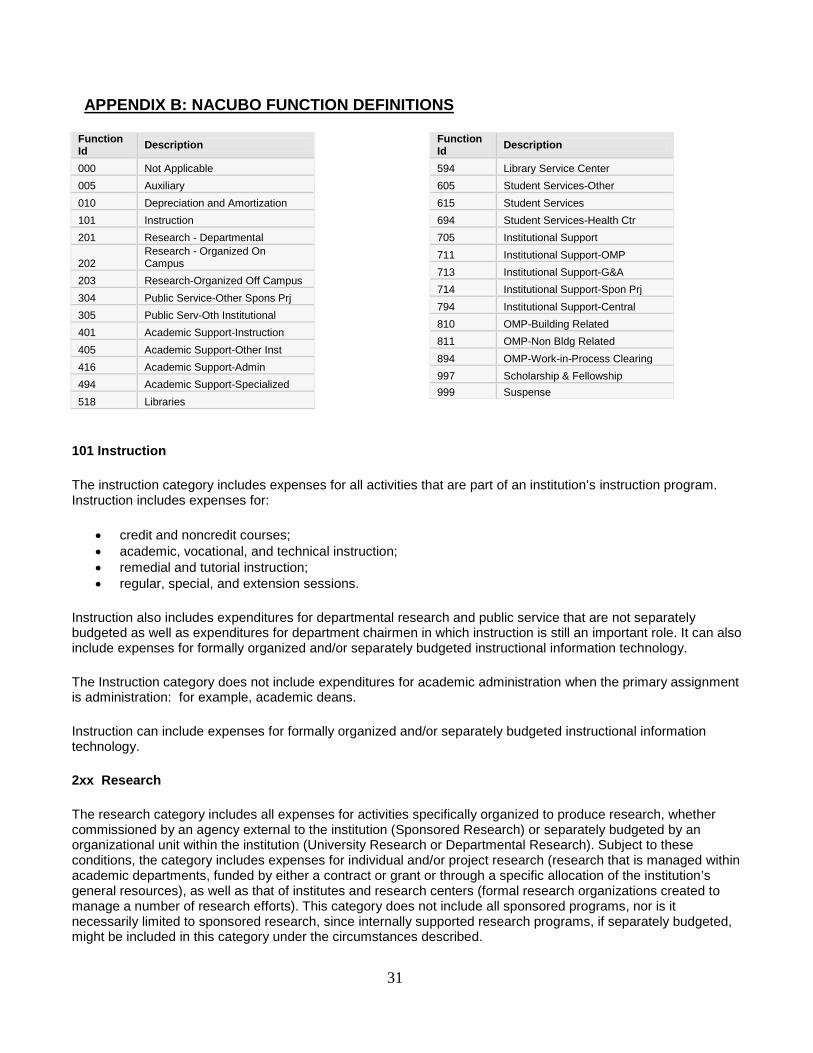

APPENDIX B: NACUBO FUNCTION DEFINITIONS

Function Id Description

000 Not Applicable 005 Auxiliary 010 Depreciation and Amortization 101 Instruction 201 Research - Departmental

202 Research - Organized On Campus

203 Research-Organized Off Campus 304 Public Service-Other Spons Prj 305 Public Serv-Oth Institutional 401 Academic Support-Instruction 405 Academic Support-Other Inst 416 Academic Support-Admin 494 Academic Support-Specialized 518 Libraries

Function Id Description

594 Library Service Center 605 Student Services-Other 615 Student Services 694 Student Services-Health Ctr 705 Institutional Support 711 Institutional Support-OMP 713 Institutional Support-G&A 714 Institutional Support-Spon Prj 794 Institutional Support-Central 810 OMP-Building Related 811 OMP-Non Bldg Related 894 OMP-Work-in-Process Clearing 997 Scholarship & Fellowship 999 Suspense

101 Instruction

The instruction category includes expenses for all activities that are part of an institution’s instruction program. Instruction includes expenses for:

• credit and noncredit courses; • academic, vocational, and technical instruction; • remedial and tutorial instruction; • regular, special, and extension sessions.

Instruction also includes expenditures for departmental research and public service that are not separately budgeted as well as expenditures for department chairmen in which instruction is still an important role. It can also include expenses for formally organized and/or separately budgeted instructional information technology.

The Instruction category does not include expenditures for academic administration when the primary assignment is administration: for example, academic deans.

Instruction can include expenses for formally organized and/or separately budgeted instructional information technology.

2xx Research

The research category includes all expenses for activities specifically organized to produce research, whether commissioned by an agency external to the institution (Sponsored Research) or separately budgeted by an organizational unit within the institution (University Research or Departmental Research). Subject to these conditions, the category includes expenses for individual and/or project research (research that is managed within academic departments, funded by either a contract or grant or through a specific allocation of the institution’s general resources), as well as that of institutes and research centers (formal research organizations created to manage a number of research efforts). This category does not include all sponsored programs, nor is it necessarily limited to sponsored research, since internally supported research programs, if separately budgeted, might be included in this category under the circumstances described.

31

Expenses for departmental research that are separately budgeted are included in this category. However, the research category does not include expenses for departmental research that are not separately budgeted, such expenses are included in the instruction category.

Research can include expenses for formally organized and/or separately budgeted research information technology.

3xx Public Service

The public service category includes expenses for activities established primarily to provide non-instructional services beneficial to individuals and groups external to the institution. These activities include community service programs, excluding instructional activities. Community service activities make available to the public various resources and special capabilities that exist within the institution. Examples include conferences and institutes, general advisory services and reference bureaus, consultation, testing services, and similar activities.

Public Service can include expenses for formally organized and/or separately budgeted public service information technology.

4xx Academic Support

The academic support category includes expenses incurred to provide support services for the institution’s primary missions: instruction, research, and public service. Academic support includes:

1. The retention, preservation, and exhibition of historical materials, art objects, and scientific displays; for example libraries, museums, and galleries;

2. The provision of services that directly assist the academic functions of the institution, such as demonstration schools associated with a department, school, or college of education which provide a mechanism through which students can gain practical experience;

3. Media such as audio-visual services and technology such as computing support if these expenses are not formally organized and/or separately budgeted within another expense category;

4. Academic administration (including academic deans but not department chairmen) and personnel development (including professional conferences) providing administration support and management direction to the three primary missions; and

5. Separately budgeted support for course and curriculum development and formal academic counseling activities.

6xx Student Services

The student services category includes expenses incurred for offices of admissions and the registrar and activities with the primary purpose of contributing to students’ emotional and physical well-being and intellectual, cultural, and social development outside the context of the formal instruction program. It includes expenses for student activities, cultural events, student newspapers, intramural athletics, student organizations, intercollegiate athletics (if the program is not operated as an essentially self-supporting activity), counseling and career guidance (excluding informal academic counseling by the faculty in relation to course assignments, which is instruction), student aid administration, and student records, and student health service (if not operated as an essentially self-supporting activity), and enrollment management.

The student services category does not include the activities of the institution’s chief administrative officer for student affairs, whose activities are institution-wide and, therefore, are classified as institutional support.

32

Student services can include expenses for formally organized and/or separately budgeted student services information technology.

7xx Institutional Support

The institutional support category includes expenses for all officers with institution-wide responsibilities, such as the president, chief academic officer, chief business officer, chief student affairs officer, and chief development officer. Institutional support also includes expenditures for:

1. Central, executive-level activities concerned with management and long-range planning for the entire institution, such as the governing board, planning and programming operations, and legal services;

2. Fiscal operations, including the investment office; 3. Administrative data processing; 4. Space management; 5. Employee personnel and records; 6. Logistical activities that provide procurement, storerooms, printing; 7. Transportation services to the institution; 8. Support services to faculty and staff that are not operated as auxiliary enterprises; and 9. Activities concerned with community and alumni relations, including development and fund raising.

Institutional support can be distinguished from academic support by identifying who benefits from the activities. Institutional support activities benefit the entire university whereas academic support activities benefit only those who participate directly in the institution’s primary missions of instruction, research, and public service.

8xx Operations and Maintenance of Plant

The operation and maintenance of plant category includes all expenses for the administration, supervision, operation, maintenance, preservation, and protection of the institution’s physical plant. They include expenses normally incurred for such items as:

1. Janitorial and utility services; 2. Repairs and ordinary or normal alterations of buildings, furniture, and equipment; 3. Care of grounds; 4. Maintenance and operation of buildings and other plant facilities; 5. Security; 6. Earthquake and disaster preparedness; 7. Safety; 8. Hazardous waste disposal; 9. Property, liability and all other insurance relating to property; 10. Space and capital leasing; 11. Facility planning and management; and 12. Central receiving.

This category does not include interest expense on capital related debt, which is classified as institutional support.

Operations and Maintenance of Plant can include expenses for formally organized and/or separately budgeted operation and maintenance information technology.

997 Scholarships and Fellowships

The scholarships and fellowships category includes expenses for scholarships and fellowships from restricted or unrestricted funds in the form of grants to students, resulting from selection by the institution or from an entitlement program. The category also includes trainee stipends, prizes, and awards. Trainee stipends awarded

33

to individuals who are not enrolled in formal course work should be charged to instruction (1100), research (1200), or public service (1300). Recipients of grants are not required to perform service to the institution as consideration for the grant, nor are they expected to repay the amount of the grant to the funding source. When services are required in exchange for financial assistance, as in the College Work-Study program, charges should be classified as expenses of the department or organizational unit to which the service is rendered. Aid to students in the form of tuition or fee remissions also should be included in this category. However, remission of tuition or fees granted because of faculty or staff status, or family relationship of students to faculty or staff, should be recorded as staff benefits expenses in the appropriate functional expense category.

005 Auxiliary Enterprises

The auxiliary enterprise category includes all expenses relating to the operation of auxiliary enterprises. An auxiliary enterprise exists to furnish goods or services to students, faculty, staff, other institutional departments, or incidentally to the general public, and charges a fee directly related to, although not necessarily equal to, the cost of the goods or services. The distinguishing characteristic of an auxiliary enterprise is that it is managed as an essentially self-supporting activity. Examples are residence halls, food services, intercollegiate athletics (only if essentially self-supporting), college stores, faculty clubs, parking and faculty housing. Student health services, when operated as an auxiliary enterprise, also are included.

010 Depreciation

This category should include depreciation expense for GASB 35 reporting purposes.