Embed Size (px)

DESCRIPTION

Texas Professional Insurance Agents' Digital Journal.

Citation preview

In This Issue

Insuring Art and Collectables

Sinkholes—Are You Covered?

Time to “Ban the Box” in Hiring

Practices?

the

TEXAS CONNECTION TEXAS PROFESSIONAL INSURANCE AGENTS DIGITAL JOURNAL MARCH 2016

Our Partners ……..……………....…….… Page 2

Presidents Corner ……………………..…… Page 3

Insuring Art and Collectables ….....……… Page 5

By The Numbers …...…….………...…….… Page 8 Sinkholes—Are You Covered? ………….... Page 12

Time to “Ban the Box”? ………………...... Page 15

Word Scramble ……...…….…………..….… Page 17 Classifieds ………………………..……….… Page 24

TDI Enforcement Actions …….……..….…. Page 25

The Last Word …………………………….… Page 26

Every year the Texas PIA presents these awards at our convention:

Company/MGA of the Year

Agent of the Year

CSR of the Year

Company Rep of the Year

Volunteer of the Year

Voting Members will soon receive a ballot to name your candidates for these awards. Please take the time to complete & return these.

It’s your opportunity to reward those you believe are deserving of the honor.

These will be presented at the Awards Luncheon, May 20, 2016 at the Texas PIA Convention and Trade Show in San Antonio.

I hope to see you there!

Shirley Almany

Shirley

Built in 1877 in Aberdeen ,

Scotland, the tall ship Elissa

was purchased by the Gal-

veston Historical Society in

1975. She is one of the old-

est tall ships still in service

and is currently moored at

the Texas Seaport Museum

and can be toured year

round when not out at sea.

THE TEXAS CONNECTION - TEXAS PROFESSIONAL INSURANCE AGENTS DIGITAL JOURNAL Page 3

(continued on page 6)

THE TEXAS CONNECTION - TEXAS PROFESSIONAL INSURANCE AGENTS DIGITAL JOURNAL Page 5

Although prices for many fine arts and collectibles took a hit during the recession, collections might be worth more than you realize. Do your customers have the proper coverage?

Review their policy limits. Homeowners policies protect the contents of a home, in addition to the building itself. The typical policy limits “contents coverage” to somewhere between 50 and 70 percent of overall limits. Therefore, a policy with $1 million in property limits would pay a maximum of $700,000 to cover contents. In event of a total loss, this might not be enough to replace building and contents, particularly if there are a lot of valuables.

Check policy sub-limits. Although most homeowners policies don’t have separate (lower) sublimit for artworks, many have lower limits for antiques. Policies also typically have lower sub-limits for jewelry; guns; silverware, goldware and pewterware; as well as for other high-value collectibles.

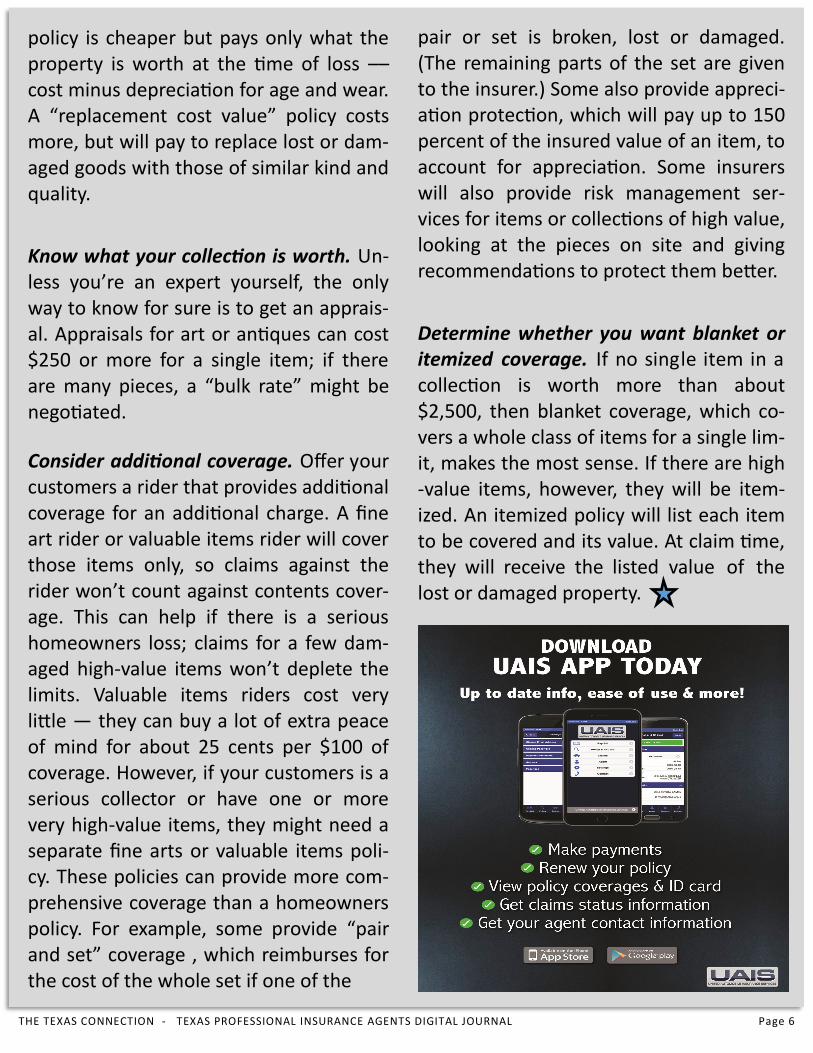

Check the type of coverage your homeowners policy provides. An “actual cash value”

THE TEXAS CONNECTION - TEXAS PROFESSIONAL INSURANCE AGENTS DIGITAL JOURNAL Page 6

policy is cheaper but pays only what the property is worth at the time of loss –– cost minus depreciation for age and wear. A “replacement cost value” policy costs more, but will pay to replace lost or dam-aged goods with those of similar kind and quality.

Know what your collection is worth. Un-less you’re an expert yourself, the only way to know for sure is to get an apprais-al. Appraisals for art or antiques can cost $250 or more for a single item; if there are many pieces, a “bulk rate” might be negotiated.

Consider additional coverage. Offer your customers a rider that provides additional coverage for an additional charge. A fine art rider or valuable items rider will cover those items only, so claims against the rider won’t count against contents cover-age. This can help if there is a serious homeowners loss; claims for a few dam-aged high-value items won’t deplete the limits. Valuable items riders cost very little — they can buy a lot of extra peace of mind for about 25 cents per $100 of coverage. However, if your customers is a serious collector or have one or more very high-value items, they might need a separate fine arts or valuable items poli-cy. These policies can provide more com-prehensive coverage than a homeowners policy. For example, some provide “pair and set” coverage , which reimburses for the cost of the whole set if one of the

pair or set is broken, lost or damaged. (The remaining parts of the set are given to the insurer.) Some also provide appreci-ation protection, which will pay up to 150 percent of the insured value of an item, to account for appreciation. Some insurers will also provide risk management ser-vices for items or collections of high value, looking at the pieces on site and giving recommendations to protect them better.

Determine whether you want blanket or itemized coverage. If no single item in a collection is worth more than about $2,500, then blanket coverage, which co-vers a whole class of items for a single lim-it, makes the most sense. If there are high-value items, however, they will be item-ized. An itemized policy will list each item to be covered and its value. At claim time, they will receive the listed value of the lost or damaged property.

THE TEXAS CONNECTION - TEXAS PROFESSIONAL INSURANCE AGENTS DIGITAL JOURNAL Page 8

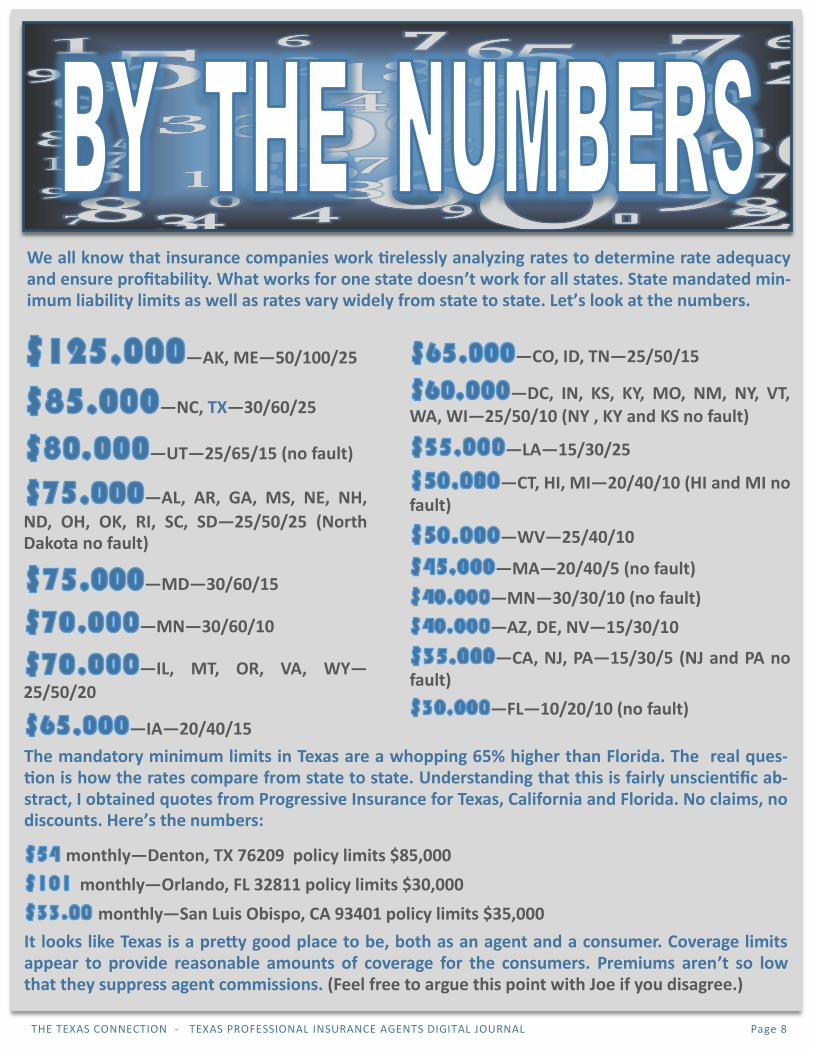

We all know that insurance companies work tirelessly analyzing rates to determine rate adequacy and ensure profitability. What works for one state doesn’t work for all states. State mandated min-imum liability limits as well as rates vary widely from state to state. Let’s look at the numbers.

—AK, ME—50/100/25

—NC, TX—30/60/25

—UT—25/65/15 (no fault)

—AL, AR, GA, MS, NE, NH,

ND, OH, OK, RI, SC, SD—25/50/25 (North Dakota no fault)

—MD—30/60/15

—MN—30/60/10

—IL, MT, OR, VA, WY—

25/50/20

—IA—20/40/15

—CO, ID, TN—25/50/15

—DC, IN, KS, KY, MO, NM, NY, VT, WA, WI—25/50/10 (NY , KY and KS no fault)

—LA—15/30/25

—CT, HI, MI—20/40/10 (HI and MI no fault)

—WV—25/40/10

—MA—20/40/5 (no fault)

—MN—30/30/10 (no fault)

—AZ, DE, NV—15/30/10

—CA, NJ, PA—15/30/5 (NJ and PA no fault)

—FL—10/20/10 (no fault)

The mandatory minimum limits in Texas are a whopping 65% higher than Florida. The real ques-tion is how the rates compare from state to state. Understanding that this is fairly unscientific ab-stract, I obtained quotes from Progressive Insurance for Texas, California and Florida. No claims, no discounts. Here’s the numbers:

monthly—Denton, TX 76209 policy limits $85,000

monthly—Orlando, FL 32811 policy limits $30,000

monthly—San Luis Obispo, CA 93401 policy limits $35,000

It looks like Texas is a pretty good place to be, both as an agent and a consumer. Coverage limits appear to provide reasonable amounts of coverage for the consumers. Premiums aren’t so low that they suppress agent commissions. (Feel free to argue this point with Joe if you disagree.)

Are you writing business with Aggressive Insurance?

You should be! Here’s why:

Competitive Auto Programs

Quick to the Phone when you need help.

Low Down Payment Plans

Easy Apps—eSignature

And They’re PIA PARTNERS

Get appointed today!

Go To Aggressive

Quality E&O Insurance Texas PIA offers members exclusive PIA programs

with Utica, Liberty Mutual, & other quality carriers.

Get an analysis of your current coverage.

Members who switch to exclusive PIA programs say

they found better coverage & price.

Marketing Assistance Website Design Help

Search Engine Optimization

Social Media Expertise

Advertising… Find what works before

you spend the money

Market Access Members gain access to new products & companies,

as well as reduced subscription rates with top quality

aggregators.

For more information go to www.piatx.org

Continuing Education CE for your entire staff:

4 hours for just being a member

Regular Local Meetings with CE

Big discounts on On-Line CE

Annual Convention: 2 days of CE

Business Building Tools PIA Branding Program: Add the PIA logo on your

business card, website, stationery and signage.

Identify your agency with a national association

of insurance professionals.

Agency websites: Cutting-edge website

tailored specifically for your agency… by the

world’s largest insurance agent website provid-

er. Offered at an incredible rate exclusively to

Texas PIA members

Consumer Brochures: PIA’s attractive brochures

answer customers’ questions about insurance.

Email: [email protected] Call: Joe Tipton 972.862.3333

Sinkholes can be serious business. A few years ago, a sinkhole swallowed eight valuable Cor-vettes at a Kentucky museum. And in 2013, Jeffrey Bush died in Florida when a 60-foot-deep sinkhole suddenly opened under his home, destroying his bedroom while he was sleeping. The U.S. Geological survey says, “Sinkholes are most common in what geologists call ‘karst terrain.’ These are regions where the type of rock below the land surface can naturally be dissolved by groundwater circulating through them. Soluble rocks include salt beds and domes, gypsum, and limestone and other carbonate rock. About 20 percent of our country is underlain by ‘karst terrain’ and is susceptible to a sinkhole event. The most damage from sinkholes tends to occur in Florida, Texas, Alabama, Missouri, Kentucky, Tennessee and Penn-sylvania.”

What Is a Sinkhole?

Geologically, a sinkhole is a depression in the ground that has no natural external surface drainage. When it rains, water stays inside the sinkhole and typically drains into the subsur-face. The U.S. Geological Survey explains: “When water from rainfall moves down through the soil, karst terrain begins to dissolve and spaces and caverns develop underground. If there is not enough support for the land above the spaces, then a sudden collapse of the land sur-face can occur. Sinkholes are dramatic because the land usually stays intact for a period of time until the underground spaces just get too big.” The U.S. Geological Service warns that, “…while collapses are more frequent after intense rainstorms, there is some evidence that

THE TEXAS CONNECTION - TEXAS PROFESSIONAL INSURANCE AGENTS DIGITAL JOURNAL Page 12

(continued on page 13)

droughts play a role as well. Areas where water levels have lowered suddenly are more prone to collapse formation.” Other factors that contribute to sinkholes are building on un-stable terrain and draining of underground aquifers

Other types of sinkholes form due to human activity. Sinkholes can develop above old mines, old cesspools or sewers or due to groundwater pumping and construction.

Are You Covered for Sinkholes?

Although the likelihood that a sinkhole will occur on your property is pretty small, damage can be extensive. In most states, the standard homeowners policy excludes coverage for damage due to “earth movement.”

However, until 2011 reforms, Florida required all homeowners policies to include coverage for sinkhole damage. Policies defined “sinkhole damage” so broadly that the number of claims surged, tripling between 2006 and 2010, and costing insurers more than $1.6 billion. After the 2011 reforms, homeowners insurers authorized by the state of Florida must cover “catastrophic ground cover collapse,” but your policy might not cover other sinkhole-related damage unless it specifically includes sinkhole coverage.

Tennessee recently amended its laws on sinkhole coverage in homeowners insurance poli-cies. Current law requires homeowners insurers to “make available” coverage for sinkhole losses to dwellings and contents. A new law effective July 1, 2014 clarifies that coverage is optional for policyholders. It also clarifies that new policies must cover “structural damage” to the property, rather than “physical damage,” which would not include land stabilization. The law also outlines inspection requirements for insurers. Insurers sought the changes, say-ing that fraudulent sinkhole claims were driving up the cost of coverage. Consumer advo-cates say the changes will make it more difficult for homeowners to obtain coverage for sink-hole claims.

California also requires homeowners insurers in that state to offer coverage for damage re-sulting from “earth movement.” Since coverage is optional—and expensive—the majority of homeowners opt to go without coverage.

Although some states, such as Florida and Tennessee, map known sinkholes, engineering surveys and other technology goes only so far to detect developing or potential sinkholes.

THE TEXAS CONNECTION - TEXAS PROFESSIONAL INSURANCE AGENTS DIGITAL JOURNAL Page 13

Two-thirds of employers include a question on criminal history on their job application forms, report-ed EmployeeScreen, a company that conducts background checks for employers. The EEOC recom-mends against this practice, however.

Should you “ban the box” on your job application forms?

Approximately 70 million Americans have criminal records, many for non-violent offenses or offenses committed while they were young. Proponents of “ban the box” laws say that checking “yes” on a job application’s criminal conviction box can reduce a qualified applicant’s chances of a callback by 50 per-cent.

The EEOC does not regulate employer communications, so it does not prohibit employers from asking questions about an applicant’s arrest/conviction history on job applications. However, it notes that an employer’s use of information requested before employment may have a disparate impact on minori-ties that amounts to unlawful discrimination under Title VII. Title VII of the Civil Rights Act of 1964 pro-hibits employment discrimination based on race, color, religion, sex and national origin. Currently, 11 states plus 60 cities and counties prohibit their own agencies from asking about criminal convictions on job application forms. Four states—Hawaii, Massachusetts, Minnesota and Rhode Is-land—also prohibit private employers from asking about criminal convictions on application forms. To find the best possible job candidates and avoid claims of discrimination, employers might consider eliminating questions about criminal records from application forms. If a criminal record comes up dur-ing a background check or interview, the employer can discuss it with the applicant in person to better determine its relevance to the position. If it is relevant, you can eliminate the candidate from consider-ation. The EEOC says, “…the legal standard is that the criminal conduct is recent enough and sufficiently job related to be predictive of performance in the position sought, given its duties and responsibilities.” Hiring and firing employees has become more complicated. Employment practices liability coverage can protect your organization from the high costs of employment discrimination and other employment-related lawsuits.

THE TEXAS CONNECTION - TEXAS PROFESSIONAL INSURANCE AGENTS DIGITAL JOURNAL Page 15

THE TEXAS CONNECTION - TEXAS PROFESSIONAL INSURANCE AGENTS DIGITAL JOURNAL Page 17

Arrange each of the following anagrams to form a single insurance related word.

Keep in mind that the anagram is not a clue. It has nothing to do with the insurance

related word. Send us your answers to be entered in a drawing to win a fabulous

CASH prize! Feel free to call us if you’re stuck.

972.965.2025 Email to: [email protected] or fax to 972. 307.7888

AT BAD DECK

SO SONIC ILL

GENIUS ART

BERATES

EPIC SOIL

MENTORS NEEDS

GLAMOUR PET

NO ROSE MIMICS

USE CAR INN

IF AT A FIELD

B

O

G

A

C

S

G

O

E

R

M

U

L

T

O

E

A

E

D

Competitive Rates

Agency Compensation

No Minimum Premium

Personal & Commercial Lines Financing

Full Lines Premium Finance Servicing Center

Document Delivery via web, fax, email or mail

Multiple Payment Options

Funding by Check, Laser Draft or Direct Deposit

Multiple Installment Schedules

Easy Online quoting & account management system

available 24/7/365

Jack Roehrig

ssistan Vi sid n and usin ss D lop n Offi

& FCO C di Corp.

Tel: 2 1 4 - 4 0 2 - 3 1 3 7

j r o e h r i g @ a f c o . c o m

THE TEXAS CONNECTION - TEXAS PROFESSIONAL INSURANCE AGENTS DIGITAL JOURNAL Page 19

TRY A STOUT

I OMIT GIANT

MALLS INTENT

NO DEERS

RENT IDEA

EAR DEPICTION

A CLAN EDICT

TOPICAL PAIN

BY DIM RIOT

RISE DUMBER

Here’s the answers to last month’s puzzle. Remember there’s a $50 prize for the first person to

STATUTORY

MITIGATION

INSTALLMENT

ENDORSE

RETAINED

DEPRECIATION

ACCIDENTAL

APPLICATION

MORBIDITY

REIMBURSED

THE TEXAS CONNECTION - TEXAS PROFESSIONAL INSURANCE AGENTS DIGITAL JOURNAL Page 21

Ad Size Monthly Pre-Pay 6 Issues

Full Page $200.00 $1,000.00

Half Page $150.00 $750.00

Third Page $100.00 $500.00

Quarter Page $50.00 $250.00

Check out the rates for the most cost effective method of keeping your

message in front of your customers… professional insurance agents.

Questions? Contact Joe Tipton at [email protected] or (972) 862-3333.

Texas Insurance Professional Services

Ray Reyes or Bob Dixon

(214) 618-2365 (832) 375-0787

The Skeet Shoot on May 19th will be at

The National Shooting Complex

The National Shooting Complex is one of the premier shooting

facilities in the world, spanning 671 acres of San Antonio coun-

tryside. As the headquarters for the National Skeet Shooting As-

sociation and National Sporting Clays Association, it hosts elite

tournaments for both sports, including the World Skeet Champi-

onships and National Sporting Clays Championship. In addition,

it is the venue for a wide range of shooting and non-shooting

events for thousands of serious competitors, casual shooters,

and outdoors enthusiasts each year.

Golf legend and award-winning course designer, Arnold Palmer

and The Arnold Palmer Design Company, have created a new

championship course that features a variety of holes touched

with dramatic waterfalls, beautiful views and a majestic land-

scape.

One of the course's Signature Holes, number 4, requires a long

carry over a lake with waterfalls along the front of the

green. Hole 18 is a spectacular finale that plays slightly up and

then to an 80-foot downhill slope, providing incredible views of

the clubhouse and a lake fed by waterfalls.

Rating/Slope:

BLACK (74.2/142); GOLD (72.4/139);

SILVER (70.6/134); COPPER (69.3/128); JADE (65.3/116)

The Golf Scramble on May 19th will be on

The Palmer Course at La Cantera Resort

THE TEXAS CONNECTION - TEXAS PROFESSIONAL INSURANCE AGENTS DIGITAL JOURNAL Page 22

Texas PIA Offers Members Satisfying E&O Solutions

“Fifteen minutes could save you 15%.... Everyone knows that… but did you know that not all E&O poli-cies are the same? E&O is like other types of insur-ance… you buy it hoping you’ll never need it… but if you do… E&O can be the difference in whether you stay in business or not. How about it? Do you know what your policy covers…. And more importantly, what it doesn’t? Texas PIA offers members, quali-ty E&O markets and coverage. And members say they have saved as much as 40% when they switch to exclusive PIA pro-grams. Call today and get an analysis of your coverage and a competitive quote from multiple markets. Call Texas Insurance Profession-al Services:

Ray Reyes or Bob Dixon (214) 618-2365 (832) 375-0787 [email protected] [email protected]

This space is dedicated to

all Member Agents or

Companies.

It’s FREE!

Look for employees

buy & sell agencies

Sell your mother-in-law’s

cat

Sell your mother-in-law!

Send Ads to

Contact Us

Need more information on the

benefits of membership?

Have a question about member

services? Give us a call:

Texas PIA & Young Insurance Professionals

3632 Frankford Rd 200B

Dallas, Texas 75287

(972) 862.3333 [email protected]

www.piatx.org

If you get to thinking

you're a person of some

influence, try ordering

someone else's dog

around.

The Insurance Sage

THE TEXAS CONNECTION - TEXAS PROFESSIONAL INSURANCE AGENTS DIGITAL JOURNAL Pa ge 23

TEXAS DEPARTMENT OF INSURANCE ACTIONS

Vivona, Carmella Date of Action: 8/10/2015 Location: Fort Worth Action Taken: Indicted Violation: Fraud Use/Possession of ID Info, State Jail Felony

Lowe, Leonard P Date of Action: 7/30/2015 Location: Fort Worth Action Taken: Indicted Violation: Misapplication of Fiduciary Property, 3rd Degree Felony

Halsell, James D Date of Action: 7/23/2015 Location: San Antonio Action Taken: Indicted Violation: Count 1-Securing Execution of a Document by Deception, 1st Degree Felony Count 2- 5-Money Laundering Count 6-Forgery

Tarco, Virgilio Date of Action: 7/22/2015 Location: Houston Action Taken: Sentenced to 3 years deferred adjudication. Violation: Securing Execution of a Document by Deception, 3rd De-gree Felony

Current, Clarence J Date of Action: 7/20/2015 Location: Houston Action Taken: Sentenced to 4 years deferred adjudication and or-dered to pay $19,907.89 in restitution. Violation: Unauthorized Insurance, Class A misdemeanor

Ribas, Marissa Date of Action: 7/20/2015 Location: Belton Action Taken: Sentenced to 11 months deferred adjudication and fined $400.00 Violation: Insurance Fraud, Class B Misdemeanor

Ruiz, Melanie Date of Action: 7/16/2015 Location: Mount Pleasant Action Taken: Sentenced to 2 years deferred adjudication, fined $500.00 and ordered to pay $1,914.00 in restitution. Violation: Insurance Fraud, State Jail Felony

: https://wwwapps.tdi.state.tx.us/inter/asproot/fraud/indictments/clips.asp

This year, the Convention & Trade Show will be in May rather than

June… It should be cooler, and exhibitors will not have to work two trade

shows in the same week. The dates: May 19-21, 2016.

This year, the convention will half a day shorter… 3 days vs. 3 1/2 days.

Golf & Skeet on Thursday the 19th, then Friday & Saturday, we will have

CE, Luncheons, Trade Shows, and a party Saturday evening.

This year, the Skeet Shoot will be held at the National Shooting Complex,

one of the nations finest sport shooting facilities.

This year, the Golf Scramble will be a 12:30 PM ‘Shotgun Start” on the

Palmer Course at La Catera Resort. If you want to Shoot & Golf, you will

be able to do both.

This year, we will be at Hotel Contessa which USA Today named as one of

the “Top 10 Hotels in America” in 2015. Every room is a suite… Right on

the Riverwalk… pool & spa on the roof… it’s beautiful.

This year, the Trade Show theme is: “Meet at the Fair” and exhibitors are

planning to include “midway” type carnival games at their booth. We

tried, but no one was willing to ‘guess your age or weight’ so I guess we

have to go with the other type amusements… You can register on-line.

Door Prizes include $1,000 cash and other ‘good stuff.’ See you there!

the Last word

Well, it’s almost convention time again. We’re

back in San Antonio again this year, but just about

everything else will change… new hotel, new golf

course, new skeet range, and new date.