Embed Size (px)

Citation preview

The spectre of tax harmonisation

Kitty Ussher

ABOUT THE AUTHOR

Kitty Ussher is the economist at the Centre for European Reform.Previous publications include The EU budget: an agenda for reform?written jointly with John Peet. She previously worked at the EconomistIntelligence Unit and, prior to the general election of 1997, as an adviserto the then shadow trade and industry ministerial team in the House ofCommons. She is an elected member of the London Borough of Lambeth.She writes in a personal capacity.

�

AUTHOR’S ACKNOWLEDGEMENTS

Particular thanks to Nina Marenzi, environmental specialist andcolleague, for undertaking the factual research that led to Chapter 5.Thanks also to Angelo Marcello Cardani, John Connors, Sylvain deForges, Bernard Grand, Charles Grant, Ben Hall, Dick Taverne, StephenTindale and James Wilson for their time and suggestions. Also to myfather for providing the idea for this pamphlet when, to avoid higher ratesof excise duty and VAT, he ordered a consignment of wine to be sent bymail order to a warehouse in a different EU country and then drovehundreds of miles across borders to fetch it. All errors of fact andjudgement are my own.

�

Contents

About the author

Author’s acknowledgements

1 Setting the scene, dispelling the myths 1

2 Reasons to harmonise I: to boost the single market 9

3 Reasons to harmonise II: to prevent revenue erosion 18

4 Reasons to harmonise III: to prevent tax evasion 24

5 Reasons to harmonise IV: to protect the environment 33

6 Prospects for 2000 and beyond 40

7 Summary of conclusions and recommendations 47

Philip Morris is Europe’s leading tobacco manufacturer. As a major collector oftaxes—in the European Union alone consumers pay over 120 billion in exciseduties and VAT on Philip Morris products to governments per annum—we are veryinterested in European tax policy and encourage public discussion on importantpolicy questions such as the harmonisation of taxes. We are therefore delightedto sponsor this thought-provoking pamphlet by Kitty Ussher of the Centre forEuropean Reform.

Tax harmonisation is not an end in itself. The Treaty of Rome asserts that theharmonisation of indirect taxes is only necessary to fulfill the smooth functioningof the Single Market. In an area we know well—tobacco taxation—this has led toa harmonised ‘tax framework’ but not full harmonisation of tax rates. Ultimately,harmonisation may result from the gradual convergence of European economies.Meanwhile, subsidiarity, flexibility and a degree of pragmatism will continue to beimportant in determining European tax policy. Without it, the policy cannot takeinto account the diversity of economic characteristics and of the political, social andfiscal objectives of the 15 member-states.

1 Setting the scene, dispelling themyths

Europe’s citizens, generally speaking, do not want their taxes set byBrussels. Taxation and representation still go hand in hand. So it is safeto assume that so long as people continue to look to their nationalgovernments to represent their interests (and turn out to vote for theirnational politicians in greater numbers than for MEPs), they will reject thenotion of taxation policies being decided at European Union level.

Before the launch of the euro the tax harmonisation issue was ofperipheral interest, seemingly confined to discussions of the single market.The establishment in 1977 of a common system of indirect taxation wasno more than a sensible correction of the market distortion produced byhaving different tax rates on tradable goods. With the launch of the singleEuropean currency in January 1999, however, the debate has sharpened.Surely, many commentators speculated, a common monetary policy acrossa number of countries would require a common fiscal policy, too? Andonce levels of spending were co-ordinated, would it not be only a matterof time before the ability to raise taxes was, as well? Others skipped therigour of economic logic, raising instead the spectre of the slippery slope:once one aspect of economic policy is handed over to central control,others must surely follow. Suddenly the tax debate was no longer aboutboosting the single market but whether the whole single-currency projectrequired national governments to relinquish their age-old right to raisetaxation.

This angst has been particularly deep in Britain, which has warily watchedfrom the sidelines the introduction of the single European currency, unsurewhether to join. In late 1998 a large section of the British popular pressgleefully ran stories implying that a single European currency wouldinevitably usher in a single European rate of tax. It did not take long forthe British public to conclude that joining the euro would mean tax rises,particularly as income-tax rates in Germany are ostensibly higher than in

1

the UK. British support for membership of economic and monetary union(EMU) dipped as a result. But are these fears grounded in fact?

The immediate answer is no. Even if there were an economic logic for taxharmonisation, any European initiative on taxation policy could becomelaw only with the unanimous approval of all EU member-states. It istherefore impossible that Britain, or any other EU nation, could find itstaxes put up, or altered in any way, against its will. And since the presentneed for unanimity may itself only be altered by a unanimous vote duringa revision of the EU treaties, the status quo is highly likely to prevail. Quitesimply, if Britain doesn’t want tax harmonisation, it won’t happen.

Neither does the euro of itself require a harmonised tax regime. Countrieswithin the euro-zone are bound only by two constraints. First, they mustkeep their overall budget deficits to within three per cent of gross domesticproduct (GDP, a country’s economic wealth)—and in a severe recessionthis constraint is relaxed. Second, overall levels of government debt shouldbe below, or declining towards, 60 per cent of GDP. Within these broadlimits, how taxes are raised and spent is immaterial.

A common error is to confuse net levels of government spending with theoverall size of state revenue and expenditure. To be part of the euro-zonerequires governments to keep net levels of spending within limits. But itdoes not matter whether a government pursues high-tax, high-spendpolicies or seeks to prune back the role of the state. As long as the amountof money spent is not much more than the amount of money raised, theeuro-zone rules of the game will have been met. To illustrate this point,look at how the size of the state in the national economy varies betweenEuropean countries (see Table 1 on next page). In France, for example,government spending accounts for around half of gross domestic product,whereas in Ireland it is one-third. The two governments need very differentlevels of tax revenues in order to balance their books, yet both haveadopted the euro.

The origin of the scare stories in Britain came from comments made inNovember 1998 by the leftist finance minister of Germany, OskarLafontaine, who saw fiscal harmonisation across Europe as a preferablealternative to unpopular supply-side reforms at home. On the fringe of ameeting of EU finance ministers Mr Lafontaine said that tax

2 The spectre of tax harmonisation

harmonisation would be a priority of the forthcoming German presidencyof the EU. A few days later he said that EU governments should beprepared to abolish the rule of unanimity in voting on taxation. Hiscomments found a natural home among those sections of the British pressthat were keen to push anti-European stories. Mr Lafontaine wassubsequently discredited by his abrupt departure from the German cabinet.But the question he raised should nonetheless be addressed. Is the spectreof tax harmonisation haunting Europe? Indeed, should we harmonise EUtaxes?

This pamphlet examines the various arguments that have been putforward in favour of harmonising EU taxes. The word ‘harmonisation’ isused loosely to mean simply a deliberate convergence of tax regimes,including rates of taxation. Most of the arguments do not stand up toscrutiny. Even where a theoretical case can be demonstrated, such as toprevent tax evasion and boost the single market, real-world politicalconstraints are likely to undermine the scope for further harmonisation.

These two factors—a slim theoretical basis plus realpolitik—have reducedthe EU’s current discussions of tax harmonisation to a much more mundaneset of issues than the eurosceptics had feared. There is a Commissionproposal on the table, part of a package put forward by Mario Monti, theformer EU Commissioner for the single market, which seeks to preventindividuals who hold savings abroad from evading tax by introducing acommon ‘withholding tax’; but this is contentious and may not be agreed.

Setting the scene: dispelling the myths 3

Austria 49.4Belgium 51.0Finland 49.1France 54.3Germany 46.9Italy 49.1Ireland 33.1Portugal 43.6Spain 41.8

TABLE 1: THE VARYING SIZE OF STATE SPENDING IN THE EURO-ZONE

PERCENTAGE OF GDP (1998)

SOURCE: OECD WORLD ECONOMIC OUTLOOK

The Monti package also includes a popular measure to abolish tax on cross-border payments of interest and royalties between associated companies(those with subsidiaries or formal partners). As another part of the package,EU ministers are trying to identify and eliminate instances where tax policyis used to grant unfair exemptions to certain companies and industries. Aproposal to extend the scope of EU-wide energy taxes has run into politicaldifficulties. The Commission also plans to publish a report on the extent towhich tax exemptions allow companies to deviate in practice from theheadline rate of corporation tax. And that is all. While the Commission hasthe authority to push for convergence in levels of value-added tax (VAT), itsattempts to do so have been stalled by huge political obstacles. There are noplans to harmonise rates of income tax or company tax.

The conclusion that emerges from this pamphlet is that the EuropeanCommission—and indeed national politicians and officials—shouldconcentrate not on tax rates, but rather on harmonising tax basesthroughout the EU. The Commission should devote its energies toeliminating tax exemptions in different member-states, enforcing EUcompetition policy more strongly and developing a common accountingstandard for EU companies.

For while there may be no direct link between the euro and tax policy now,in the longer term the two are connected. The adoption of a single currencywill increase competitive pressure in the single market, tending to erodeover time the differences in rates of taxation. This is a good thing as it willdraw attention to the underlying competitiveness of countries. But theprocess will be undermined if different countries maintain different taxbases—as a result of multiple tax exemptions, weakly-enforced competitionpolicy or variable accounting standards—and thus prevent the economicgains of the single market from being fully realised. It will take years ofmeticulous effort to harmonise tax bases, but that is what the technocratsare there for. And once all countries operate a common tax base, themarket will determine how far tax rates need to converge.

Before this conclusion is fleshed out, however, it is as well to tackle someof the myths and misinformation that dog the UK debate on taxharmonisation. The biggest culprits are newspaper editors who delight intaking a nugget of truth and extrapolating incorrectly to produce a scarestory that sells. For example:

4 The spectre of tax harmonisation

March of the euro tax man—Daily Mail, 24 November 1998The rush towards uniform taxes…could leave Britain facingthe nightmare prospect of being forced to accept taxharmonisation as a condition of membership if we decide tojoin the euro…. It would mean not only interest rates butalso key taxes being fixed in Frankfurt, the home of the newcentral bank.

Spectre of 53 per cent income tax—The Times, 28 November 1998…bringing Britain into line with the other European nationswould mean that a UK taxpayer would have to pay a further30p in the pound. This would give a basic income tax rateof 53 per cent, against 23 per cent at present.

Both stories raise the spectre of EU-determined rates of income tax. Yet theEuropean Union has no mandate to do this. Its governing treaties allowonly for the ‘harmonisation of legislation concerning…indirect taxation tothe extent that such harmonisation is necessary to ensure the establishmentand the functioning of the internal market.’ Thus in 1991 EU ministersagreed to adopt, with many exemptions, a minimum standard rate of VATof 15 per cent (the British minister who signed the proposal was theeurosceptic Norman Lamont), and minimum rates of excise duty onmineral oils, alcohol and tobacco. The same EU mandate was used toabolish customs duty within the free-trade area, and led to common-senseregulations to limit the double taxation of individuals across borders.

The European Commission believes that personal income tax is a matterfor sovereign national parliaments, not European institutions. When MrLafontaine spoke of having similar income and corporate tax rates acrossthe EU (so as to lessen the competitive pressure to reduce German taxes),he was doing no more than express a desire. Neither the Germangovernment nor the Commission—and certainly not the European CentralBank—has the power to do anything to translate that desire into practice.

Tax harmonisation ‘may be irresistible’—Daily Telegraph, 27 November 1998European politicians are demanding tax harmonisationbecause they say tax competition is ‘harmful’.

Setting the scene: dispelling the myths 5

EU may set rate of business tax—Daily Telegraph, 17 December 1998British tax rates for business and industry could be set byBrussels under EU moves to co-ordinate taxes acrossEurope… New signs of British flexibility follow lastweekend’s Vienna summit at which Mr Blair and otherleaders called for an EU Commission study into companytaxation across Europe to be ready by June. The study,chaired by Dawn Primarolo, the Financial Secretary to theTreasury, is assessing the business tax regimes of member-states to reduce ‘distortions’ in the EU’s single market anddevelop more ‘employment-friendly tax structures’.

These stories—a Daily Telegraph speciality—deliberately confuseharmonisation with the removal of ‘harmful’ tax competition. It is truethat a political committee known as the Code of Conduct Group, chairedby the British minister Dawn Primarolo, has been set up to seek out taxmeasures that ‘unduly affect’ where companies locate their business activitiesin the Union. The group’s job, however, is not to harmonise rates across theEU. It is to level the playing field of competition, in this instance bypreventing tax policy acting as a form of state subsidy to certain activitiesand industries at the expense of others within a national tax regime. Thegroup’s recommendations should complement the work of the Commissionas enforcer of competition policy.

The EU is not alone in its efforts to crack down on ‘harmful’ tax competition.The World Trade Organisation, as recently as September 1999, confirmedthat the common US corporate practice of avoiding tax by channellingexport earnings through offshore companies, known as foreign salescorporations, amounted to an illegal subsidy that should be eliminated. If andwhen the US complies with this demand, it is the EU that stands to benefit.European countries should not complain when the same principle is appliedto eliminate discriminatory tax breaks in their own continent. Hostility fromthe British press is particularly hollow, given that the conclusions of thePrimarolo group are likely to benefit the UK: only a small handful of theseveral hundred taxation measures under consideration refer to Britain.

The German menace—Daily Telegraph, 26 November 1998Chancellor Gerhard Schröder of Germany professes to be an

6 The spectre of tax harmonisation

Anglophile, but his government’s agenda is starting to posea serious threat to the prosperity and self-government ofthis country… If Mr Lafontaine wishes to ruin the Germaneconomy, that is a matter between him and the Germanpeople. If he tries to enlist Britain, we must resist.

Your country needs you to fight euro con—The People, 22 November 1998 Once the euro is in place the cry from Europhiles will be thatit is now inevitable that we have a common tax policy, asGermany’s new finance minister demanded grandly lastweek… If you want to stop this, act now. Refuse to accept thecon that is inevitable. Write to your MP. Remind him of whatthe vast majority of politicians believed to be inevitable in1939. Then, you could hardly get a hearing in Parliament ifyou opposed Chamberlain’s appeasement policy. But it wasthe men who sold out at Munich who were proved wrong.

Is this the most dangerous man in Europe?—The Sun, 25 November 1998Mr Lafontaine wants to increase your taxes, abolish yourpound, allow a German central bank to fix your mortgagerate…he is the biggest threat to the British way of lifesince 1945.

Most of all, Mr Lafontaine’s comments provided perfect ammunition forthose papers happy to play on the jingoistic tendencies of some of theirreaders. The temptation to create a new German enemy, this time economicrather than military, was too much to resist for some newspaper editors.

In the popular press the word ‘harmonisation’ has been used very loosely.From total equalisation of all tax rates, to efforts to introduce EU-widetaxation on polluting companies in line with Kyoto environmentalcommitments, to moves to iron out discrepancies in accounting methodsbetween countries, ‘tax harmonisation’ has become a catch-all cliché forthe British media.

In reality these issues are all very different. They have differentimplications and merits, and have been pursued as a result of very different

Setting the scene: dispelling the myths 7

motivations. In fact one of the most cogent ways of assessing the variousarguments for greater tax harmonisation is to classify the motivationsbehind them. The next four chapters examine the main arguments,namely: to boost the single market; to prevent erosion of tax revenuesthrough competition; to prevent illegal tax evasion; and to protect theenvironment.

8 The spectre of tax harmonisation

2 Reasons to harmonise I: to boost the single market

The single market case for tax harmonisation is based on the old economicargument that the better the market works, the better off we are. Byremoving barriers to trade between countries, competitive pressure oncompanies is intensified, forcing costs down and eliminating inefficientpractices. The result—through the mechanism described more than twocenturies ago by Adam Smith as the ‘invisible hand’—is greater productiveefficiency and therefore, according to the classical school of economics,greater economic wealth.

For a theoretical argument, this has been taken too literally in the past. TheEuropean Commission-funded Cecchini report of 1988, for example,attempted to quantify the effects of creating a European single market andconcluded that it could lead to a 4.5 per cent increase in EU-wide GDP, withfalling inflation. If combined with appropriate actions by governments,Cecchini added, that projection could be even more positive: a 7.5 per centgrowth in the European economy, creating 5.7 million new jobs.

The Cecchini report was a landmark text because it succeeded inpopularising, at least among policy-makers, ideas that had previouslybeen confined to ivory towers. But it did not take long for its gung-hoapproach to lose credibility. Its conclusions were soon seen as over-optimistic, arising from underlying economic assumptions of perfectlyfunctioning markets that were too simplistic. A more credible study by theEuropean Commission in 1996 (The impact and effectiveness of the singlemarket COM(96) 520) indicated that the effect of the single market untilthen had been to create up to 900,000 jobs, to increase EU GDP by a totalof between 1.1 per cent and 1.5 per cent in the period 1987-1993, and tocause inflation to fall by between 1 per cent and 1.5 per cent.

Common rates of tax boost the single market because they improve theability of economic agents—consumers, investors or firms—to make

9

decisions that are less affected by tax levels and more an accurate reflectionof the real state of the economy. As a result, competitive pressure oncompanies is increased, driving out inefficient practices, lowering costs,and leading to greater economic wealth.

The arrival of the euro strengthens this economic rationale for commonlevels of taxation. A single European currency, by removing exchange-rate barriers to trade (the costs of hedging against adverse currencymovements or currency-transaction charges), highlights distortionsfrom other sources. Suddenly firms are able to make comparisons:once a company operates in the same currency across borders, theeffects of different tax regimes become more obvious. Such effectsmight seem less significant in the face of large currency fluctuations thatcan wipe out profits overnight, but once exchange rates are fixed,dealing with discrepancies in the tax system becomes a higher priority.

However, this argument has limited relevance. It is only applicable wherethere is, or is reasonably expected to be, significant cross-border activity.Table 2 provides a back-of-the-envelope ranking of the main factors ofproduction and general economic activity by cross-border mobility.

The single market will be boosted therefore by the removal of barriers totrade in goods and services, and by the cross-border movement of highlymobile capital, such as financial savings and investments. But where factorsof production are relatively immobile between EU countries, as is the casewith labour, land or small-business activity, little economic effect can beexpected from the removal of cross-border barriers to trade.

10 The spectre of tax harmonisation

very mobile quite mobile immobile

� financial capital � operations of � operations of large companies small companies

� trade in goods� labourand services� land and property

TABLE 2: MOBILITY OF DIFFERENT FACTORS OF PRODUCTION

There is, therefore, no single-market case for harmonising income tax,national insurance contributions and other labour taxes. But there is a casefor aligning levels of taxation on cross-border movements of financialcapital, and for similar levels of excise duties and VAT.

An interesting illustration is the decision by EU finance ministers inSeptember 1999 to allow a lower rate of VAT on labour-intensive services.Member-states will be able to reduce VAT on certain transactions such ashousehold repairs, the cost of renovating private homes (excludingexpensive building materials), window-washing and domestic cleaning,home-help care and hairdressing. Because such services are not tradedacross borders and are labour intensive, to permit lower levels of VAT willnot only boost employment but also do so without threatening to distortthe single market.

Less clear-cut is the case of non-financial capital, the ‘fixed’ assets oflarge companies: plant, machinery and equipment. In one sense theseare not fixed at all: until it is actually built, the production capacity ofa multinational is mobile in that it could be located in a number ofdifferent places. But two caveats are needed. The first is that, unlikemost purely financial transactions, an investment in fixed capital isimmobile once it has taken place. Factories and office blocks cannot bemoved around the globe at the press of a button. The response ofcompanies to changes in the level of business taxes is, in economicterms, quite ‘sticky’. A government can therefore increase corporationtaxes safe in the knowledge that there will not be an immediate exodusof business activity.

This phenomenon has led some academics to conclude that policy-makers have every incentive to offer low levels of capital taxationin order to attract inward investment, but then slap on the taxesonce the investment has been made.1 In reality, however, that wouldhave an impact, even if it was slow to emerge. Less profitable firmswould go out of business and there might be a considerable shiftabroad in the medium-term, led by the more mobile service-sectorindustries. Inevitably, there would also be a deterioration in the relationshipbetween business and national government, which would prevent policy-makers from being able to pursue such a ploy again.

Reasons to harmonise 1: to boost the single market 11

1 See, forexample, KRogoff,‘Journal ofInternationalEconomics’,1985

The second caveat is that decisions on where to invest in productionfacilities depend not only on the level of taxation but also on manyother factors—quality of labour and infrastructure, transport links,availability of suppliers, market size, political risk, culture, languageand so on—some of which are intangible. This is in contrast to financialinvestments, which are based on rates of return that are easy to calculatewith precision. The effect that taxes have on inward investment decisionsis therefore difficult to isolate.

In any case, were EU tax rates for companies to be equalised tomorrow,little economic benefit would follow. This is because what is treated astaxable varies hugely between member-states. There is little gain fromharmonising tax rates when tax bases remain so different.

Tax bases differ across the EU in two fundamental ways: in theaccountancy rules that firms must comply with, and in the extent to whichgovernments offer tax exemptions to companies.

Accounting systemsWhen the European Commission conducted a survey of 13,000European firms in 1996, it emerged that companies saw differences intax regimes as one of the main barriers to the single market. Nationaltax authorities often treat differently: depreciation rates of assets; costsof capital; methods of accounting for inflation when valuing stockinventories; provision for bad debts; and exchange-rate losses. Superficialsimilarities in headline tax rates between different countries maytherefore mask substantial differences in the effects that taxation systemshave on profitability. Were corporation tax rates to be instantlyequalised, for example, there would still be a need for armies ofexpensive accountants, technicians and tax lawyers to enablemultinationals to comply with (and in some cases, circumvent) the legalregulations in different countries.

Aside from the effect of different legal rules of tax accounting on corporateprofitability, the lack of standard accounting conventions is itself a barrier.It makes it difficult for investors to understand and compare companydata, and thus hampers the development of a single market in financialservices.

12 The spectre of tax harmonisation

During the 1960s and 1970s a series of European Commission reportsproposed the Community-wide harmonisation of corporate tax systems byone method or another. All were designed, under Article 100 of the EUTreaty, to improve the operation of the common market. None wasimplemented. The proposal that got the farthest—a draft directive putforward in 1975—was blocked by the European Parliament in 1979 andeventually withdrawn in 1990. A committee was subsequently set upunder the chairmanship of Dr Onno Ruding to investigate the disparitiesbetween member-states’ corporation tax regimes. It inflamed debate byrecommending, in 1992, specific minimum and maximum rates ofcorporate tax, in the context of parallel measures to eliminatediscrepancies in accounting practices across the EU.

One possible way forward would be to give companies operating acrossborders the option of adopting a standard EU set of tax-accounting rules.That way, multinationals could operate under the same rules and systemsthroughout their accounts, while smaller domestic companies would bespared the upheaval of an obligatory change. The advantage of such atwin-track approach is that it would be self-selecting: companies thatstood to gain from standardising their accounting information wouldadopt it; others would not. The difficulty would lie in agreeing what theaccounting standard should be. Companies that do a high proportion oftheir business in one country would lobby the government of that countryto push for its system to be adopted across the board. It is also not hardto envisage significant political resistance from some member-states, whichwould view it as a slippery slope to harmonised tax rates.

Tax exemptionsAnother reason why an immediate equalisation of corporate tax rateswould not be beneficial is the existence of considerable and varied taxexemptions in different member-states. So although the headline rate ofcorporate taxation in Germany is extremely high, the overall tax burden—the ‘effective’ rate—is far lower, thanks to extensive tax exemptions andgovernment incentive schemes. As a proportion of GDP Germany raisesless revenue from corporate taxation than Britain: 1.7 per cent of GDP in1996, compared to 3.6 per cent in Britain and an average of 2.6 per centacross the EU, according to the EU’s statistical agency Eurostat.

Reasons to harmonise 1: to boost the single market 13

A Union-wide study of 3,000 companies by the University of Maastricht,published by the Dutch finance ministry in April 1999, detailed the extentof the discrepancies between headline corporate tax rates set by member-states and the effective rate paid by companies. EU firms pay an average27 per cent tax on profits, despite the average headline rate being 36.5 percent (see Table 3 below).

The need to investigate effective rates of taxation has not been lost on EUpolicy-makers. In July 1999, after six months of wrangling, member-states agreed the terms of reference for a European Commission enquiryinto levels of effective taxation, to report by mid-2000. The mandate isbroad. But the key lies in its intention to ‘illuminate existing differencesin effective corporate taxation in the Community and the policy issues thatsuch differences may give rise to’, with particular emphasis on ‘the maintax provisions which may hamper cross-border economic activity andinvestment’. It will also look at the need to reform accountancy practices.

14 The spectre of tax harmonisation

Headline Effective DifferenceAustria 36.02 17.67 18.35Belgium 40.28 20.99 19.29Denmark 35.78 29.40 6.38Finland 34.02 29.82 4.20France 34.70 32.82 1.88Germany 50.05 38.53 11.52Greece 32.53 20.85 11.68Ireland 21.94 13.86 8.08Italy 50.48 35.32 15.16Luxembourg 39.40 34.09 5.31Netherlands 35.00 31.80 3.20Portugal 39.29 17.19 22.10Spain 35.30 24.11 11.19Sweden 28.54 27.47 1.07UK 33.35 29.00 4.35EU average 36.45 26.86 9.59

TABLE 3: THE DIFFERENCE BETWEEN HEADLINE AND EFFECTIVE

CORPORATE TAX RATES 1990-1996 (%)

SOURCE: CORPORATE EFFECTIVE TAX RATES IN THE EUROPEAN UNION

UNIVERSITY OF MAASTRICHT (FOR DUTCH FINANCE MINISTRY), APRIL 1999

The Commission will start by assessing existing work, including the studyby the University of Maastricht, and will only undertake new research ifobvious gaps appear. That does not mean the Commission intends merelyto replicate the conclusions of work already in the public arena: it will beinfluenced by the opinions of two panels—one of business practitioners,the other of academics—set up to investigate the evidence. The size of thetask makes this a tough assignment, but nevertheless extremely useful forenhancing the single market.

Unfair taxes and harmful competitionThe issues of taxation and competition policy are closely linked in the EU.There is a critical distinction between ‘fair’ differences in tax treatment,which arise from the political priorities and macroeconomic policydecisions of national governments; and ‘unfair’ differences, which distortcompetition in a prejudicial way, similar to the operation of state aid. Asthe European Commission explains in its 1998 document The applicationof state aid rules to measures relating to direct business taxation:

Article 92(1) states that ‘any aid granted by a member-statethrough state resources in any form whatsoever whichdistorts or threatens to distort competition by favouringcertain undertakings or the production of certain goods shall,in so far as it affects trade between member-states, beincompatible with the common market’. In applying theCommunity rules on state aid, it is irrelevant whether themeasure is a tax measure, since Article 92 applies to aidmeasures ‘in any form whatsoever’.

The close relationship between state aid and company tax breaks allowsthe Commission, acting as the EU competition authority, to seek tosmooth out distortions in the taxation treatment of companies through theTreaty of Rome’s competition policy measures.

However, for the Commission to use these powers would be politicallycontroversial. It has not yet been brave enough to do so. Instead, theCommission has encouraged countries to reach political agreement toclamp down on tax breaks operating as thinly disguised state aid. Withthis aim in mind, in 1997 it drew a distinction between ‘harmful’ taxcompetition, which distorts the single market, and that which was not.

Reasons to harmonise 1: to boost the single market 15

Ireland’s ability to poach investment by levying very low tax rates incertain sectors of its economy prompted other member-states to take aninterest in the Commission’s work. By December 1997 EU financeministers had agreed to a Code of Conduct on business taxation, and setup the Code of Conduct Group, chaired by the British minister DawnPrimarolo, to single out cases where the taxation treatment of certainindustries or companies could be considered ‘harmful’. The methodologyused by the Group to decide whether tax measures are ‘harmful’ is laidout in the box below.

There is no obligation on the Council of Ministers to publish theconclusions of the Code of Conduct Group, but its deliberations willhave little effect unless the threat of publication is at least a credible one.The group has no legal status, deriving its power from its ability to bringstrong peer pressure to bear on member-states to smooth out discrepanciesin their taxation systems. Governments are encouraged to make progressfrom the knowledge that the Commission could pursue the same ends

16 The spectre of tax harmonisation

The EU code of conduct on business taxation states that, whenconsidering whether taxation measures are harmful, accountshould be taken of, inter alia:

� whether advantages are accorded only to non-residents or inrespect of transactions carried out with non-residents, or

� whether advantages are ring-fenced from the domesticmarket, so they do not affect the national tax base, or

� whether advantages are granted without any real economicactivity or substantial economic presence within the member-state offering such tax advantages, or

� whether the basis of profit determination in respect ofactivities within a multinational group of companies departsfrom internationally accepted principles, notably those agreedupon within the OECD, or

� whether the tax measures lack transparency, including wherestatutory rules are relaxed at administrative level in a non-transparent way.

WHEN IS TAXATION HARMFUL?

SOURCE: ECOFIN COUNCIL CONCLUSIONS 1 DECEMBER 1997

through legal means. Thus it is a carrot-and-stick approach: member-states are given a framework through which they can eliminate harmfultaxation measures—and those of their neighbours—by political agreement;but if they fail, they could be pursued through the courts by the EUcompetition authorities.

There was a healthy momentum behind the activities of the Code ofConduct Group during 1999. But if, for whatever reason, governments fallat the final hurdle and fail to give a political commitment to translate thegroup’s conclusions into action, the Commission should not have anyqualms about using its competition policy powers to secure the sameoutcome.

In conclusion, there is a single-market case for similar levels of indirect tax,and for harmonising levels of tax on mobile financial capital. As regardscorporate taxation, there are single-market grounds for a harmonised taxbase across the EU. To that end, member-states should be prepared toallow the standardisation of accounting systems—but not of tax rates—to take place by qualified majority voting (QMV). At the very least,companies that operate across borders should be given the option of usingEU-wide accounting standards, without prejudice to the national-basedsystems operated by smaller (and less mobile) domestic companies. TheEU also needs to step up its efforts to eliminate tax exemptions that causethe effective rate of taxation to differ from the headline rate. Although thereport of the Code of Conduct Group might well yield some results onbusiness taxation, the European Commission should, in its role ascompetition authority, proactively investigate instances where tax breaksmay be acting as state aid.

Reasons to harmonise 1: to boost the single market 17

3 Reasons to harmonise II: to prevent revenue erosion

One of the strongest incentives for harmonising taxes is the fear thatcompetition will prevent governments from raising sufficient tax revenues.Countries will simply undercut each other, the argument goes, poachinginvestment from their neighbours by offering lower tax rates, untilcompany tax rates are forced down to zero. As a result, government cofferswill wither away. In the long run, tax competition will createunemployment and threaten public services.

Tax competition and unemploymentThe theory behind the fear of unemployment goes like this: as countriescompete to attract private-sector investment, they cut business taxationand therefore have to compensate by increasing income tax or nationalinsurance rates. As companies shed expensive staff in favour of morecapital-intensive production methods, employment will fall.

This concern was highlighted in a paper presented to a meeting of EUfinance ministers in Verona in April 1996 by Commissioner Mario Monti.The aim of the Monti paper was to consider taxation in the wider contextof all EU policies; to pursue, in his words, a ‘global approach’ to taxpolicy. The paper noted that:

the stability of total tax revenues has been achieved at thecost of a progressive alteration in the structure of taxation;the tax burden has been shifted to the less mobile tax base—labour—in order to recover the tax lost from the erosion ofother more mobile tax bases.

The implication is that the erosion of more mobile tax bases—capital andcorporation tax—should be stemmed in order to prevent labour taxationfrom rising. Mr Monti’s paper builds on the work of the ‘Delors whitepaper’, Growth, competitiveness and employment: the challenges and ways

forward into the 21st century, presented by the European Commission toEU leaders in 1993. In that paper the Commission recommended that:

it is essential to reduce the non-wage costs of unskilled andsemi-skilled labour by an amount equivalent to 1 or 2 pointsof GNP by the year 2000. The improvement in tax revenueresulting from this measure would offset the cost by up to 30per cent. The remainder should be financed by savings orother revenue.

Although not made explicit, the white paper gave ample scope to thosein favour of tax harmonisation to argue that the ‘other revenue’ referredto company taxation, which they would fix at levels to prevent the erosionof overall government revenues.

On the surface this argument is convincing. Graph 1, based on figurespublished by Eurostat, shows that average labour taxes in the EU arerising, while taxes on capital have been falling since their peak in theearly 1980s. (The ‘implicit’ tax rate is an average rate obtained by dividingthe tax levied on each activity and/or production factor by thecorresponding tax base. For example, the implicit labour tax rate is thetotal of non-wage labour costs divided by total income.)

Reasons to harmonise II: to prevent revenue erosion 19

GRAPH 1: LABOUR TAX RATES RISING, CAPITAL TAX RATES FALLINGIMPLICIT TAX RATE (%)

SOURCE: STRUCTURES OF TAXATION SYSTEMS IN THE EUROPEAN UNION

EUROSTAT/DG21

There is certainly a strong case to be made that the increase in labourtaxes is a direct cause of unemployment. An empirical study publishedin 1997 by the Centre for Economic Policy Research (CEPR), forexample, strongly supports this suggestion2. It argues that thebargaining power of unions in Europe has meant that increases inlabour taxes have been borne not by employees but by firms. This hasled firms to replace labour with capital, causing unemployment to rise.The paper’s empirical results allow the authors to conclude that the9.4 per cent rise in EU labour tax rates between 1965 and 1991

accounted for a four per cent rise in European unemployment.

But this rise in labour taxes has not occurred as a form of compensation fordeclining revenues from capital taxation. How could it, when the absolutesums of money raised from capital taxation have not fallen? The picture canbe seen more clearly by looking at total tax receipts as a proportion of theoverall size of the economy (see Graph 2). The data shows that revenuesfrom capital taxes have remained broadly steady over the past two decades.So while revenues from labour taxation have gone up—from 17 per centof GDP in 1970 to 24 per cent in 1996—there is no evidence that this hasbeen to compensate for lower revenues from capital taxation.

20 The spectre of tax harmonisation

GRAPH 2: REVENUE FROM LABOUR TAXES RISING, REVENUE FROM

CAPITAL TAXES CONSTANT (% OF GDP)

SOURCE: STRUCTURES OF TAXATION SYSTEMS IN THE EUROPEAN UNION

EUROSTAT/DG21

2 F Daveri and G Tabellini,‘Unemployment,growth andtaxation inindustrialcountries’, CEPRDiscussion Paper1681, 1997

In fact, the higher revenues from labour taxation have fed through intohigher overall levels of taxation: European Union taxes rose from 33.5 percent of EU GDP in 1970 to 42.3 per cent in 1996. Thus, the impositionof a floor of minimum corporate taxes across the EU would not necessarilyhave the effect of reducing labour taxes and levels of unemployment.

So why do Graphs 1 and 2 show such different pictures? The answer isthat the first graph shows taxation rates, the second taxation revenues.Advocates of minimum levels of corporate taxation confuse the two: inasserting the need to protect overall revenues, they illustrate their pointwith data on taxation rates. Yet there is no automatic relationship betweenthe two concepts: higher rates do not automatically lead to higher revenuesany more than lower rates do; the relationship depends on the elasticityof demand for the item in question.

It would seem that demand for labour is fairly elastic in the EU: higherimplicit tax rates on labour are associated with lower levels ofemployment, but not so low as to cause a fall in overall tax revenues fromlabour. Indeed, to cut labour taxes might even achieve the dual benefit ofraising government revenues while reducing unemployment throughencouraging firms to switch back to labour from capital.

The real cause of high EU unemployment lies in the high total costs oflabour: wage costs, non-wage costs and protective regulations. One reasonthese costs are prohibitively high, as the same CEPR paper (and manyothers before it) makes clear, is that the system of wage bargaining favoursthose in work rather than the whole workforce. It is a familiar insider-outsider debate: social protection and wages rise to benefit those in work(the ‘insiders’); unemployment rises as a result, but that does not matterto the unions because they do not represent the unemployed (the‘outsiders’). The textbook solutions are either to centralise wage-bargaining arrangements so that negotiators are forced to take account ofthe effect of their demands on the national economy; or to decentraliseradically so that negotiators have a direct interest in the profitability of thefirm whose employees they represent, compared to that of its competitors.The current situation in many European countries, where employeesnegotiate on an industry-wide basis, does little to help their economies.

It is easy to make this argument from a British perspective, where much

Reasons to harmonise II: to prevent revenue erosion 21

of the political and economic dislocation arising from an overhaul of thewage-bargaining process has already taken place, as a result of policiespursued vigorously by right-wing governments in the 1980s. The centre-left governments on the European continent would face significant politicalresistance if they advocated the same policies. Perhaps that is why it hasbeen more attractive for some European politicians to advocate minimumlevels of corporate taxation, rather than a shake-up of the wage-bargainingsystem, as a purported solution to the problem of high unemployment.

Tax competition and public servicesAnother fear is that tax competition will cause a fall in revenues, threatening

public-sector budgets and forcing governments to cut back onessential services. Therefore, the argument goes, taxes should beharmonised, or at least their minimum rates fixed, in order topreserve the role of the state. This argument is particularly resonantin countries with relatively high levels of public investment andstate-funded social protection. They fear they will be unable tocompete in an international environment that favours low taxes.And rather than to go down the politically-troubled route ofwelfare reform, they argue for the fixing of corporate taxation atlevels that will not threaten their own tax regimes. This wascertainly the motivation behind the outbursts of the then Germanfinance minister, Oskar Lafontaine, in late 1998. It is well

illustrated by an extract from an essay3 by his influential economic adviser,and deputy at the finance ministry, Heiner Flassbeck:

The widely held view that nation-states should compete witheach other is based on the same rationale as mercantilism—the idea that a country can only get richer to the detriment ofothers… But this ‘competition of systems’ is wrong andcounterproductive if it takes place by depreciating a nation’scosts—wages, taxes, regulations and public investment—inthe manner of devaluing a nation’s currency. As exchangerates are no longer an economic instrument in a singlecurrency area, member-states might resort to this type of realdevaluation in order to improve their competitiveness. Such amercantilist strategy is not compatible with the functioning ofproper European markets. The most important example ofreal depreciation is that of wage increases that are below

22 The spectre of tax harmonisation

3 H Flassbeck‘Employment,stability andefficiency: theessentials ofEuropean economicpolicy’ in “WillEMU lead to aEuropean economicgovernment?”Centre for EuropeanReform, 1999

improvements in productivity. But real depreciation also takesplace when the tax burden is artificially lowered, causing areduction of public spending and the restriction of publicservices. Each strategy that aims at real depreciation iscontrary to the idea of free trade. Within a single currencyarea, it is even destructive.

The idea that countries which lower the tax burden on companies so asto encourage private-sector investment are ‘destructive’ and acting‘contrary to the idea of free trade’ is an excellent example of a pseudo-economic argument being used for political gain. One obvious fallacy isthe assumption that lower company taxes produce lower public spendingand reduced public services. On the contrary, lower tax rates couldactually raise tax revenues by encouraging greater levels of businessactivity. The ensuing reduction in unemployment would, in addition,reduce government spending on social-security payments. A second fallacyis that companies’ decisions are based on tax alone. In fact, the type ofpublic investment that Mr Flassbeck espouses, such as in publicinfrastructure and education, could well be seen as attractive to investors,thereby compensating for higher marginal rates of corporate taxation.

Competition in taxation regimes does not lead inexorably to the erosionof public services, any more than harmonising corporate taxation is thesolution to high unemployment. There is not much of a case, therefore, toargue that tax harmonisation is necessary to prevent government taxrevenues from being eroded.

But such was the confusion caused by Mr Lafontaine and his advisers thathis political master, Chancellor Gerhard Schröder, felt compelled in late1998 to issue a clarification jointly with the British prime minister:

We do not favour a unified system of corporate taxation…wewill not support measures leading to a higher tax burdenand jeopardising competitiveness and jobs in the EU.

In March 1999, not long after this hasty clarification, Mr Lafontaineresigned, followed in due course by Mr Flassbeck. It seems that, for themoment, realpolitik has put paid to this particular argument for EU-widetax harmonisation.

Reasons to harmonise II: to prevent revenue erosion 23

4 Reasons to harmonise III: to prevent tax evasion

While the fear that governments will lose revenues through taxcompetition may be misplaced, there is little doubt that tax authorities dolose revenue as a result of illegal evasion. Where there are markeddifferences between tax regimes on mobile goods and services inneighbouring countries, there is a clear incentive to trade across bordersin ways that reduce tax payments. To harmonise taxes across borderswould go a long way towards eliminating this incentive.

There is a particularly powerful incentive for people to engage in cross-border arbitrage when the taxes on consumer goods vary substantially. TheEU’s single market programme increased the incentive by allowingindividuals to import legally large quantities of goods across internal EUborders, without completing any paperwork or paying duty. Although suchgoods must, in theory, be for personal use only, this restriction has provednigh-impossible to enforce. It is both simple and lucrative to buy off-the-shelfin low-tax regimes and sell illegally—off the back of a lorry, without payingtax—in high-tax regimes.

Britain suffers acutely from this problem: higher excise duties on tobaccoand alcohol than in France and Belgium allow people to make large profitsby importing goods across the Channel to sell on the black market. Theresult is lost revenues to the UK Treasury: in a parliamentary answer on 18May 1999, the British government estimated lost excise duty and VATfrom tobacco smuggling to be £1.7 billion in 1998—not far off the amountneeded to knock a penny from the basic rate of income tax. Although thisfigure refers to all tobacco smuggling into the UK, not just that from the EU,cross-channel activity from France (whether or not the goods originatedfrom farther afield) forms by far the largest part.

Official estimates of the total revenue lost to the UK Treasury from cross-channel smuggling of both tobacco and alcohol tell a similar story. A

report by UK Customs and Excise in November 1998 estimated this at£1.22 billion in 1998, a very substantial figure that can be magnified if weassume that the smugglers are also unlikely to be paying corporate orpersonal income tax on the proceeds. Smuggling is also bad news forlocal retailers, which stand to lose trade as a result, leading to lowergovernment revenues from corporation tax.

We saw in Chapter 2 that there is a good single-market case to harmoniseindirect taxes—VAT and excise duty—on goods that are traded acrossborders. The argument here is that there is also a very strong case for taxconvergence in order to clamp down on smuggling and illegal tax evasion.

Excise dutiesSubstantial differences persist in the rates of excise duty charged across theEU, as Table 4 on the next page shows. The indirect tax levied oncigarettes in the UK, for example, is double the rate in France; the UK taxon beer is six times as great; petrol duties are 30 per cent higher; and thetax on wine is more than 60 times greater in the UK than in France.

This is not for want of effort by the European Commission to iron out thedifferences. Minimum rates of duty have been introduced on a number ofproducts, such as cigarettes and unleaded petrol. Although these have hadthe effect of forcing some countries to increase taxation to nearer the EUaverage, it has not stopped others from continuing to levy far higher duties.Similarly, EU attempts to iron out differences in beer duty by introducinga target rate have not always had the desired effect. Although the Councilof Ministers agreed a target beer duty of ∞18.7 per hectolitre in 1992(equal to less than a third of the rate of duty imposed by Britain at thetime), the UK carried on increasing its beer duty in subsequent years.Between 1992 and 1999, Britain’s beer duty increased by almost 18 percent in current prices; it is now more than four times the EU target level.

With such good economic reasons to reduce differentials on excise duty,why do the governments of Britain, Denmark, Sweden and Finland persistin keeping their rates so high? The answer is that there are, in the eyes ofgovernments, equally good political and social reasons for maintainingthe status quo. Governments use excise duties to influence consumerbehaviour. Britain, for example, believes that cigarette prices should be kepthigh as a way of curbing consumption in the interests of public health.

Reasons to harmonise II: to prevent tax evasion 25

Still

win

eU

nlea

ded

petr

olBe

erC

igar

ette

sf

per

hect

olit

ref

per

1,00

0 lit

res

fpe

r he

ctol

itre

fpe

r 1,

000,

st

anda

rd, e

x V

AT

ex V

AT

5% a

bv, 1

Jan

99

ex V

AT

Aus

tria

040

6.89

6.70

66.5

8Be

lgiu

m47

.049

2.49

8.23

74.7

4G

erm

any

053

0.73

3.95

76.5

4D

enm

ark

141.

561

497.

6618

.66

124.

13G

reec

e0

334.

542

5.86

51.0

0Sp

ain

040

2.59

33.

3635

.43

Finl

and

234.

7155

8.78

457

.36

107.

30Fr

ance

3.35

584.

755.

2086

.24

UK

214.

3275

1.30

532

.67

171.

64Ir

elan

d28

7.57

477.

766

39.9

212

0.05

Ital

y0

541.

567.

0255

.38

Luxe

mbo

urg

034

6.55

3.80

52.7

2N

ethe

rlan

ds48

.70

471.

688.

5469

.12

Port

ugal

047

7.15

5.64

56.7

2Sw

eden

292.

9748

4.69

31.0

397

.54

EU m

inim

um

028

7

18

.77

57%

of

to

tal p

rice

1 ove

r 15

% v

ol; 2 o

ver

95.6

oct

ane;

3 ove

r 97

oct

ane;

4 nor

mal

; 5 sup

er; 6 h

igh-

octa

ne; 7 t

arge

t

SOU

RC

E:

EU

RO

PEA

NC

OM

MIS

SIO

N;

BA

SSPL

C

TA

BL

E4:

DIF

FER

ING

RA

TE

SO

FE

XC

ISE

DU

TY

(JU

LY19

99 U

NL

ESS

STA

TE

D)

26 The spectre of tax harmonisation

A further explanation of differential duties lies in the diverse economicstructures of EU countries. Those member-states with significant wine(and, to a lesser extent, tobacco) industries are subject to greater lobbyingfrom local producers to keep prices down. In the northern states, wheresuch goods have to be imported, the health lobbies have a stronger voice.

Value-added tax There are still significant variations in levels of VAT among EU member-states, despite the attempts of the European Commission to bring them intoline. In 1991 EU ministers agreed to set a standard minimum of 15 per centin all countries and to eliminate higher VAT bands. Reduced rates of fiveper cent were permitted for essential items not traded across nationalborders. Britain was allowed to keep its even lower VAT rates, includingzero rating on children’s clothes. These exemptions had to have been inplace before December 1991; member-states agreed not to introduce anynew exemptions. Nevertheless, as Table 5 shows, beyond an across-the-board rise of a couple of percentage points in the past ten years or so, anyconvergence of standard VAT rates across the EU has been slight.

There remain political reasons for different levels of VAT. The UK usesindirect taxation to perform functions normally assigned to welfare policyin other countries. Britain’s insistence on zero-rated VAT on children’s

Reasons to harmonise III: to prevent tax evasion 27

TABLE 5: STANDARD VAT RATES RISING, HARDLY CONVERGING (%)

SOURCE: DICK LEONARD GUIDE TO THE EUROPEAN UNION

ECONOMIST PUBLICATIONS 1998; EUROPEAN COMMISSION

1987 1999Belgium 19 21Denmark 22 25Germany 14 16Greece 18 18Spain 12 16France 18.6 20.6Ireland 21 21Italy 19 20Luxembourg 12 15

1987 1999Netherlands 18.5 17.5Austria - 20Portugal 17 17Finland - 22Sweden - 25UK 15 17.5

average 17.2 19.4SD* 3.3 3.1

* standard deviation—a measure of thedispersion from the average

clothes, food and books, and on the lowest possible rate for domestic-fuelconsumption, is equivalent to other nations’ use of food vouchers andhigher social-security benefits to assist the least well-off.

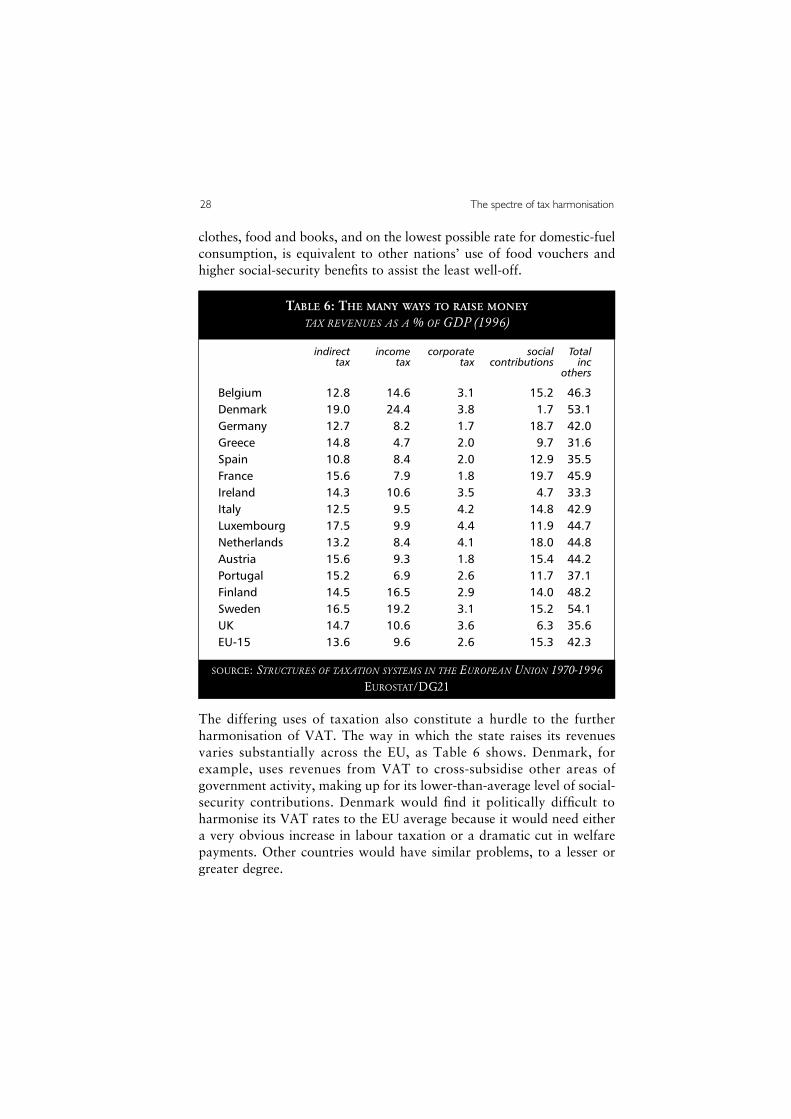

The differing uses of taxation also constitute a hurdle to the furtherharmonisation of VAT. The way in which the state raises its revenuesvaries substantially across the EU, as Table 6 shows. Denmark, forexample, uses revenues from VAT to cross-subsidise other areas ofgovernment activity, making up for its lower-than-average level of social-security contributions. Denmark would find it politically difficult toharmonise its VAT rates to the EU average because it would need eithera very obvious increase in labour taxation or a dramatic cut in welfarepayments. Other countries would have similar problems, to a lesser orgreater degree.

28 The spectre of tax harmonisation

indirect income corporate social Totaltax tax tax contributions inc

others

Belgium 12.8 14.6 3.1 15.2 46.3Denmark 19.0 24.4 3.8 1.7 53.1Germany 12.7 8.2 1.7 18.7 42.0Greece 14.8 4.7 2.0 9.7 31.6Spain 10.8 8.4 2.0 12.9 35.5France 15.6 7.9 1.8 19.7 45.9Ireland 14.3 10.6 3.5 4.7 33.3Italy 12.5 9.5 4.2 14.8 42.9Luxembourg 17.5 9.9 4.4 11.9 44.7Netherlands 13.2 8.4 4.1 18.0 44.8Austria 15.6 9.3 1.8 15.4 44.2Portugal 15.2 6.9 2.6 11.7 37.1Finland 14.5 16.5 2.9 14.0 48.2Sweden 16.5 19.2 3.1 15.2 54.1UK 14.7 10.6 3.6 6.3 35.6EU-15 13.6 9.6 2.6 15.3 42.3

TABLE 6: THE MANY WAYS TO RAISE MONEY

TAX REVENUES AS A % OF GDP (1996)

SOURCE: STRUCTURES OF TAXATION SYSTEMS IN THE EUROPEAN UNION 1970-1996EUROSTAT/DG21

Withholding taxDifferences in the ways that member-states tax income from financialinvestments has led many people to hold their savings abroad, as a meansof avoiding domestic taxes. In Germany, for example, high-street bankshave faced legal action following allegations that they routinely advisedcustomers to transfer their savings abroad. Strong banking-secrecy lawsin neighbouring Luxembourg mean that Germans can invest there, fairlyconfident that they can hide the income from the German tax authorities.The German state prosecution service believes there may be half a millioncases of illegal earnings from tax evasion by private investors. The Belgiantax authorities face a comparable problem of lost revenue.

There are two potential solutions. The first is for countries to shareinformation about who is investing where. By co-operating, national taxauthorities can alert each other to income earned by cross-borderinvestors. The second solution is for national authorities to slap a tax onincome earned by private investors who are based in another country.Such a tax is known in the jargon as a ‘withholding tax’, defined as anytax deducted from payments (usually deriving from investment income)to non-residents. A withholding tax would diminish the incentive forprivate savers to invest outside their own borders, making it easier fornational tax authorities to keep tabs on who was earning what.

Among the EU member-states each of these options has its supporters andopponents. Least popular is the idea of sharing information between taxauthorities: for a number of countries this threatens their culture of banksecrecy. Luxembourg has an explicit legislative provision for bankingsecrecy, Austria has recently enshrined it in the constitution, and inGermany tax authorities may not request information on bank accountsto verify the correct reporting of interest. Other countries, such as Belgium,Spain and Portugal, allow information to be given if there is a suspicionof fraud; but only a handful, including the UK, have legislation requiringbanks to give access to the tax authorities.

Most member-states support a withholding tax, as it would bring greaterrevenues to their national tax authorities. But there are two exceptions:Luxembourg and the UK. Luxembourg’s objection is straightforward: ifit lost foreign investors, its banks—which are crucial to its economic

Reasons to harmonise III: to prevent tax evasion 29

success—would suffer. It vetoed a similar proposal put forward ten yearsago. In Britain, the City of London argues that the extra burden ofadministering a withholding tax would threaten its high-volume, low-margin international bond business by increasing transaction costs andthus driving it to markets outside the EU, such as New York or Zurich.

Since any EU-wide initiative on taxation policy requires unanimity, theEuropean Commission has tried hard to find a compromise acceptable toeveryone. In May 1998 it published a draft directive that would givemember-states the option to either introduce a withholding tax of at least20 per cent on income earned by non-resident private savers, or provideother EU tax authorities with information on who is investing in theirbanks and financial markets. The directive would allow most member-states to have a withholding tax while Britain and Luxembourg sharedinformation with other tax authorities.

Under this proposal every country apart from Britain and Luxembourgwould gain in two ways: increased revenue from the new tax, and anopportunity to clamp down on tax evasion within their own bordersthanks to the extra information provided. Britain and Luxembourg, bycontrast, would end up simply increasing their administrative costs byhaving to provide information to other countries. In the City of London,financial institutions argued loudly that the costs of sharing informationwould be just as damaging as the costs of administering a withholding tax.

The City, however, is protesting too much. It makes much of its moneyfrom trading international bonds, known as “Eurobonds”. But retailholdings of Eurobonds are only around five per cent of total holdings. Theremainder are held by institutional investors and would not be subject tothe withholding tax. Furthermore, holdings of non-resident investors area fraction of the total retail market. To complain—as the City has—thatthe whole of the London Eurobond market is under threat from theproposal is an exaggeration. The City would certainly suffer some net costif the Commission’s draft directive were implemented, so it isunderstandable that it chooses to press its case forcefully. But no oneshould be under the illusion that the adoption of a withholding tax or thesharing of information between authorities poses a serious threat toLondon’s dominance of the Eurobond market.

30 The spectre of tax harmonisation

There are some other, more technical aspects of the 1998 draft directive,however, that do require attention. One concern is the need to find legaldefinitions of the types of securities to which it applies, and of the financialinstitutions that would be responsible for administering any tax.Otherwise, the directive could create an incentive for the invention ofnew types of securities and trading entities, in order to avoid taxation.Another very serious problem is that many existing international bondscontain a clause that covers the possibility of a new tax being introducedbefore the bond reaches maturity. This usually gives the issuer a choiceeither to compensate the investor for the tax (known as ‘grossing-up’), orto redeem the entire issue at its face value. As interest rates have beenfalling for some time, a large number of outstanding bond issues aretrading at a price higher than their original value, which would make itprofitable for many issuers simply to redeem at face value. The ensuingredistribution of assets would cause massive market disruption anduncertainty.

Both concerns need to be addressed before the directive is adopted, whichmeans that the 1998 draft needs rewriting. In September 1999 Britainsuggested two ways of doing this. First, the directive could exempt fromthe tax all existing bonds, all future bonds that are held in a clearingsystem, and all holdings above ∞40,000. This, Britain argues, wouldprevent the mass redemption at par of existing bonds and allow thewholesale market of the City of London to continue trading relativelyunscathed. Second, the directive should specify which types of assets itapplied to, rather than which types it excluded, thereby targeting retailinvestors more directly.

Although the British paper was not particularly well-received (the Germanfinance minister, Hans Eichel, described it as ‘totally insufficient’), it didrepresent a step forward in the negotiating process. For a start, itpersuaded other EU countries to accept that, were a withholding tax tobe introduced, it should apply only to new bonds, so as to avoid theproblem of a mass redemption of bonds at their face value. Moreover, itallowed other countries to understand the UK’s point of view fully, evenif they did not agree with it. Based on this understanding of Britain’sconcerns, the European Commission, in conjunction with the Finnishpresidency of the EU, came up with a compromise proposal in the fewdays before the Helsinki summit of December 1999. This compromise

Reasons to harmonise III: to prevent tax evasion 31

reduced the amount of information that would have to be provided by theCity financial institutions to the level already required under an existingmoney-laundering directive—namely the account number and name of thenon-resident.

If accepted, this compromise proposal would allow the UK to opt toshare information with other EU tax authorities at an extremely low cost.Other EU countries, meanwhile, would still be free to impose awithholding tax. In the event, however, this last-minute proposal wasnot good enough for Tony Blair and Gordon Brown. Whether the problemwas lack of time to study the proposal, or a sudden concern that thewhole directive was fundamentally flawed, or simply grumpiness derivedfrom France’s refusal to lift the ban on British beef, they would not agreeto it. Instead the whole decision was postponed for a further six months,ostensibly to give the UK more time to consider.

Even if agreed, an EU savings directive would not prevent individualinvestors who want to cheat their national tax authorities from turningto markets outside the EU, such as Zurich or New York. Indeed there isno particular reason why the problem of cross-border tax avoidance onincome earned from financial investments should be tackled at an EUlevel, rather than by an international body. A voluntary agreement byOECD countries to operate common rates of taxation on income earnedby non-resident investors, or to disclose income earned by non-residentsto domestic tax authorities, would be more effective than an EU directive.But in the absence of unanimity among all OECD governments as to themerits of such a scheme, agreement is unlikely. After all, the OECD is onlya think-tank of which individual countries are members; it has nolegislative powers. The advantage of taking action at an EU level is thepurely practical reason that there is some hope of an agreement beingreached, and that that may spur other OECD countries to follow suit.However, the Commission’s 1998 proposal clearly needs substantialrevisions in order to gain the support of all EU countries.

32 The spectre of tax harmonisation

5 Reasons to harmonise IV: to protect the environment

The issue of environmental taxation deserves to be dealt with separately.Although many of the environmentally-driven arguments for taxharmonisation sound familiar—for example to prevent distortions to thesingle market and to promote an employment-friendly tax structure—inone key respect this debate is very different. It operates on the premise thathigher taxes on polluting activities are, all else being equal, better for theenvironment.

The point of environmental taxation is to ensure that the market pricesof goods and services reflect their full costs to society. It is about pricestelling the truth. A polluting factory may do a roaring trade for manyyears but leave behind contaminated land, air and water which futuregenerations have to pay to clean up. But if the factory is taxed for eachtruckload of waste that it dumps, not only will it have an immediateincentive to invest in cleaner technology, but also the state gains incomewhich it can spend on helping future generations meet the clean-up costs.Thus the cost to the environment will have been ‘internalised’ within thedecision-making process of the polluter. Similarly, taxes on the use ofenergy can make consumers take into account the effects of their actionson the environment. The key concept is to make the polluter pay for theenvironmental damage he causes: it puts a market price on environmentalpollution, creating an immediate incentive today to minimise the costssociety will incur tomorrow.

Economic theory aside, there are practical justifications for levyingenvironmental taxes. They tend to be straightforward to administer, andcan be more acceptable to voters than other taxes. They can be adjustedwith relative ease, to achieve the level of taxation that is needed to alterbehaviour. They also create a market for cleaner forms of technology,boosting investment and employment in high-tech industries. Furthermore,higher environmental taxes can also give governments the freedom to cut

33

taxes elsewhere to benefit the economy. The 1993 Delors white paper, forexample, advocated a shift from labour taxes to environmental taxes, toachieve the twin virtues of boosting employment while simultaneouslyimproving the protection of the environment.

It is difficult to argue against higher environmental taxation. But that isnot the same thing as arguing for harmonised taxation. Environmentalistsoften, wrongly, use ‘harmonisation’ as a synonym for common minimumrates of taxation on certain products. Advocates of harmonised tax ratesmight be equally happy were the rate fixed at 10 per cent or 40 per cent.Advocates of minimum tax rates would prefer the rate to be set high, soas to have the greatest possible effect on the decision-making of economicagents, be they firms or households. There is an environmental case forhigh minimum rates of environmental tax, but not for harmonised rates.

Yet the European Commission’s recent efforts to broaden the areas towhich minimum rates of environmental taxation apply should still besupported. The current proposal, the brainchild of Mario Monti, wouldratchet up the existing minimum rate of tax levied on mineral oils, andextend minimum rates to coal, natural gas and electricity. Althoughenvironmental groups in northern Europe have criticised the proposal fornot being radical enough—for many countries the EU’s proposed tax wouldstill be below national levels—the setting of minimum levels would establishan important principle and would create the possibility of those levels beingraised at a later date. So the main reason for supporting this proposal is thatit is a means to achieving higher levels of tax. In the context ofenvironmental policy, minimum taxes are not an end in themselves.

Spillover effectsBecause pollution does not respect national borders, EU member-stateshave a legitimate interest in each other’s environmental policies. The 1986explosion at the Chernobyl nuclear-power station in Ukraine affectedmuch of Europe; any country’s greenhouse-gas emissions contribute tooverall climate change; a factory that pollutes the Danube upstream inGermany will affect water quality downstream in Austria; the Irish rightlyassert their interest in any contaminating effects of substances dumped inthe Irish Sea by the Sellafield nuclear reprocessing plant in Cumbria.

It is these ‘spillover effects’ that give any international body a mandate to

34 The spectre of tax harmonisation

tackle environmental concerns. For the EU, they provide part of thejustification for its governing treaties to state that economic and socialprogress should take into account ‘the principle of sustainabledevelopment’ and that its activities shall include ‘a policy in the sphere ofthe environment’ with the objectives of ‘preserving, protecting andimproving the quality of the environment; protecting human health;prudent and rational utilisation of natural resources; promoting measuresat international level to deal with regional or world-wide environmentalproblems’ and ‘taking as its base a high level of protection’.

The EU is the right institution to promote environmental protection notonly within its borders but also on the world stage. It signed, in its ownright, the 1992 Rio declaration on global environmental development, andthe protocol on climate change agreed at Kyoto in 1997. As anorganisation, the EU has therefore committed itself to addressing globalwarming and—if the Kyoto protocol ever comes into force—to specifictargets for reducing the emissions of the main six greenhouse gases byeight per cent below 1990 levels in the period 2008-2012.

Another argument for EU-level action is that it might persuade otherwiserecalcitrant member-states to attach greater importance to environmentalissues. The Monti draft directive, if adopted, would lead to some rises inenergy taxes: 1998 figures from the European Commission indicate thatpetrol and diesel prices in Greece, Luxembourg and Spain would have torise by between 6 and 11 per cent as a result of the increased tax onmineral oils. It would also introduce a tax on coal in Britain andGermany—a fuel which to date has received a subsidy—and a tax on gasin many EU countries.

But the prospect of higher tax rates may scupper the proposal: Spain haslobbied hard against the tax, arguing that its effect would be inflationaryand damaging to industry. The Commission counters that any member-state is free to use the revenue generated to reduce taxes elsewhere, whichcould be deflationary, and if used to lower labour taxes, could be goodfor business and employment. But because all taxation measures aresubject to unanimity, Spain has been able to stall progress by threateningto use its veto. The UK was opposed under the Conservatives but hassoftened its line under Labour. It is now supportive in principle, providedit can obtain a guaranteed permanent exemption for domestic gas and

Reasons to harmonise IV: to protect the environment 35

electricity; the regressive nature of domestic energy taxation makes itunpopular in Britain.

If the Monti directive fails, those member-states that do support it—mainly the northern EU countries—may try to reach their own agreement.In September 1999, the environment committee of the EuropeanParliament proposed a kind of ‘energy-tax Schengen’, to allow the Montiproposals to move forward without Spain. Backed by the Finnishenvironment minister, Satu Hassi, MEPs suggested that those countriesin favour of the Monti directive could invoke Article 11 of the Treaty ofAmsterdam. This allows a group of EU member-states to push ahead withpolicy initiatives if an EU-wide agreement cannot be found. Germanymight well favour this approach: it could then increase its own energytaxes in tandem with its northern European neighbours, and so moderatebusiness concerns that higher environmental taxes would underminecompetitiveness.

Whatever happens to the Monti proposal, many European countries willcontinue to favour a common approach to environmental taxation, for thesimple reason that there are large differences in the scope of energy andenvironmental taxes across the EU. An OECD study from 1997 showsSweden, Denmark and Finland with more than 20 kinds of environmentaltax, closely followed by Belgium and the Netherlands. Greece, Ireland,Italy and Luxembourg lag behind with only a handful. The importance ofenergy and other environmental taxes (such as taxes on waste) to themember states’ finances varies significantly, as the chart on the next pageshows.

The desire to harmonise, rather than simply to raise environmental taxes,is based on the assumption that the existence of very different systems inthe EU must cause economic distortions.

Preserving a single marketThe first set of arguments in favour of environmental tax harmonisationrelates to the single market. Just as significant differences in excise dutieson alcohol and tobacco lead to market distortions (see Chapter 2), so largedifferences in environmental excise duties on tradable consumer goods alsodistort economic decision-making. One illustration is a problem thatoccurred on the Dutch/German border: higher fuel prices in the

36 The spectre of tax harmonisation