Embed Size (px)

Citation preview

Zurich Open Repository andArchiveUniversity of ZurichMain LibraryStrickhofstrasse 39CH-8057 Zurichwww.zora.uzh.ch

Year: 2021

The role of time-varying contextual factors in latent attrition models forcustomer base analysis

Bachmann, Patrick ; Meierer, Markus ; Näf, Jeffrey

Abstract: Customer base analysis of noncontractual businesses builds on modeling purchases and latentattrition. With the Pareto/NBD model, this has become a straightforward exercise. However, thissimplicity comes at a price. Customer-level predictions often lack precision. This issue can be addressedby acknowledging the importance of contextual factors for customer behavior. Considering contextualfactors might contribute in two ways: (1) by increasing predictive accuracy and (2) by identifying theimpact of these determinants on the purchase and attrition process. However, there is no generalizationof the Pareto/NBD model that incorporates time-varying contextual factors. Preserving a closed-formmaximum likelihood solution, this study proposes an extension that facilitates modeling time-invariantand time-varying contextual factors in continuous noncontractual settings. These contextual factors caninfluence the purchase process, the attrition process, or both. The authors further illustrate how tocontrol for endogenous contextual factors. Benchmarking with three data sets from the retailing industryshows that explicitly modeling time-varying contextual factors significantly improves the accuracy ofout-of-sample predictions for future purchases and latent attrition.

DOI: https://doi.org/10.1287/mksc.2020.1254

Posted at the Zurich Open Repository and Archive, University of ZurichZORA URL: https://doi.org/10.5167/uzh-197236Journal ArticlePublished Version

The following work is licensed under a Creative Commons: Attribution 4.0 International (CC BY 4.0)License.

Originally published at:Bachmann, Patrick; Meierer, Markus; Näf, Jeffrey (2021). The role of time-varying contextual factors inlatent attrition models for customer base analysis. Marketing Science, 40(4):783-809.DOI: https://doi.org/10.1287/mksc.2020.1254

This article was downloaded by: [130.60.36.151] On: 21 January 2021, At: 04:38Publisher: Institute for Operations Research and the Management Sciences (INFORMS)INFORMS is located in Maryland, USA

Marketing Science

Publication details, including instructions for authors and subscription information:http://pubsonline.informs.org

The Role of Time-Varying Contextual Factors in LatentAttrition Models for Customer Base AnalysisPatrick Bachmann, Markus Meierer, Jeffrey Näf

To cite this article:Patrick Bachmann, Markus Meierer, Jeffrey Näf (2021) The Role of Time-Varying Contextual Factors in Latent Attrition Modelsfor Customer Base Analysis. Marketing Science

Published online in Articles in Advance 15 Jan 2021

. https://doi.org/10.1287/mksc.2020.1254

Full terms and conditions of use: https://pubsonline.informs.org/Publications/Librarians-Portal/PubsOnLine-Terms-and-Conditions

This article may be used only for the purposes of research, teaching, and/or private study. Commercial useor systematic downloading (by robots or other automatic processes) is prohibited without explicit Publisherapproval, unless otherwise noted. For more information, contact [email protected].

The Publisher does not warrant or guarantee the article’s accuracy, completeness, merchantability, fitnessfor a particular purpose, or non-infringement. Descriptions of, or references to, products or publications, orinclusion of an advertisement in this article, neither constitutes nor implies a guarantee, endorsement, orsupport of claims made of that product, publication, or service.

Copyright © 2021, The Author(s)

Please scroll down for article—it is on subsequent pages

With 12,500 members from nearly 90 countries, INFORMS is the largest international association of operations research (O.R.)and analytics professionals and students. INFORMS provides unique networking and learning opportunities for individualprofessionals, and organizations of all types and sizes, to better understand and use O.R. and analytics tools and methods totransform strategic visions and achieve better outcomes.For more information on INFORMS, its publications, membership, or meetings visit http://www.informs.org

MARKETING SCIENCEArticles in Advance, pp. 1–38

http://pubsonline.informs.org/journal/mksc ISSN 0732-2399 (print), ISSN 1526-548X (online)

The Role of Time-Varying Contextual Factors in Latent AttritionModels for Customer Base Analysis

Patrick Bachmann,a Markus Meierer,a Jeffrey Näfb

aUniversity Research Priority Program Social Networks, University of Zurich, 8050 Zurich, Switzerland; bDepartment of Mathematics,Eidgenossische Technische Hochschule (ETH) Zurich, 8092 Zurich, Switzerland

Contact: [email protected], https://orcid.org/0000-0002-3938-2697 (PB); [email protected],https://orcid.org/0000-0003-1995-5897 (MM); [email protected], https://orcid.org/0000-0003-0920-1899 (JN)

Received: July 5, 2017

Revised: August 3, 2018; April 16, 2019;September 17, 2019; March 12, 2020

Accepted: May 12, 2020

Published Online in Articles in Advance:January 15, 2021

https://doi.org/10.1287/mksc.2020.1254

Copyright: © 2021 The Author(s)

Abstract. Customer base analysis of noncontractual businesses builds on modelingpurchases and latent attrition. With the Pareto/NBD model, this has become a straight-forward exercise. However, this simplicity comes at a price. Customer-level predictionsoften lack precision. This issue can be addressed by acknowledging the importance ofcontextual factors for customer behavior. Considering contextual factors might contributein twoways: (1) by increasing predictive accuracy and (2) by identifying the impact of thesedeterminants on the purchase and attrition process. However, there is no generalization ofthe Pareto/NBD model that incorporates time-varying contextual factors. Preserving aclosed-formmaximum likelihood solution, this study proposes an extension that facilitatesmodeling time-invariant and time-varying contextual factors in continuous noncontractualsettings. These contextual factors can influence the purchase process, the attrition process,or both. The authors further illustrate how to control for endogenous contextual factors.Benchmarking with three data sets from the retailing industry shows that explicitlymodeling time-varying contextual factors significantly improves the accuracy of out-of-sample predictions for future purchases and latent attrition.

History: Yuxin Chen served as the senior editor and Peter Fader served as associate editor for this article.Open Access Statement: This work is licensed under a Creative Commons Attribution- NonCommercial 4.0

International License. You are free to download this work and share with others for any purpose, exceptcommercially, and you must attribute this work as “Marketing Science. Copyright © 2020 The Author(s).https://doi.org/10.1287/mksc.2020.1254, used under a Creative Commons Attribution License: https://creativecommons.org/licenses/by-nc/4.0/.”

Funding: This work was funded by the University Research Priority Program Social Networks at theUniversity of Zurich and the Swiss National Science Foundation [Project 100018_163189].

Supplemental Material: The data files and online appendix are available at https://doi.org/10.1287/mksc.2020.1254.

Keywords: probability models • Pareto/NBD • customer relationship management • latent attrition • contextual factors • customer lifetime value

1. IntroductionModeling customer purchases and attrition in non-contractual businesses has become a straightforwardtask, but this simplicity comes at a price. Havingaccess to recency and frequency data of customers’past transactions allows marketers to apply the Pareto/NBD model (Schmittlein et al. 1987). However, pre-dictions are said to represent an educated guess ratherthan a precise value (Wübben andWangenheim 2008,Malthouse 2009, Fader 2012). If the focus is on theaggregated level, that is, the entire customer base, thisdifference can be rather negligible. In contrast, theapplicability of individual level predictions is oftenlimited. For example, an increased level of precision isrequired when allocating resources for customer re-tention activities to individual customers.

There have been many attempts to improve theoriginal Pareto/NBD model. However, there existsno generalization that allows modeling time-varying

contextual factors in a continuous noncontractualsetting. Extensions to the Pareto/NBD model or re-lated models mainly focus on the computationalcomplexity of the estimation procedure (Fader et al.2005a), the correlation between the modeled pro-cesses (Glady et al. 2015), or the integration of time-invariant contextual factors (Fader and Hardie 2007,Abe 2009, Singh et al. 2009). Recent studies illustratehow regularity patterns (Platzer and Reutterer 2016)and stationary transaction attributes can be includedin the customer’s purchase process (Braun et al. 2015)or how differences across customer cohorts may becaptured in latent attrition models (Gopalakrishnanet al. 2017). An approach by Schweidel and Knox(2013) goes one step further and provides the possi-bility of including other time-varying contextual fac-tors (i.e. direct mailing activity) into a discrete latentattrition model. Although the Pareto/NBD model isvery popular in research and practice, no extension

1

allows for the inclusion of time-varying contex-tual factors.

The impact of two broad categories of time-varyingcontextual factors on customer behavior has beenhighlighted in the previous literature (Schweidel andKnox 2013, Hanssens and Pauwels 2016): (1) sea-sonality in purchase patterns and (2) tactical mar-keting activities. Seasonality in purchase patternsis common in many noncontractual settings, espe-cially in the retailing industry. Customer behavior isheavily influenced at the aggregate level by publicholidays (e.g., Christmas and Thanksgiving) and atthe individual level by recurring personal events (e.g.,birthdays and paydays). In addition to seasonality,tactical marketing activities are an important time-varying determinant of customer behavior. Customerscan be targeted by either individual- or aggregate-leveltactical marketing activities, such as personalized ormass marketing campaigns. Explicitly modeling mar-keting variables, such as time-varying contextual factors,explains the heterogeneity across customers that wasintroduced by the firm in the first place. Including eitherkind of time-varying contextual factors improves thepredictive accuracy of probabilistic customer attritionmodels. However, the impact of these contextual factorsis likely to vary. Probabilistic customer attrition modelsoperationalize customer behavior through two pro-cesses: (1) the purchase process and (2) the attritionprocess. When contextual factors are added to themodel, they are allowed to influence customer be-havior through these two processes. However, thesefactors do not necessarily have to affect both pro-cesses. It is reasonable that some of the contextualfactors influence only customers’ purchases or attri-tion. For example, although personalized couponingwill likely impact only the purchase process, directmailing information about loyaltyprogrameventsmightonly impact the attrition process. Furthermore, it is avalid assumption that marketing activities irritate cus-tomers and thus increase customer attrition (Ascarzaet al. 2016). Similarly, seasonality patterns, such asthose caused by holiday seasons, are likely to have anexclusive impact on the purchase process, whereasother seasonality patterns, such as those caused byindividual paydays might additionally impact cus-tomer attrition. The latter may cause customers to re-consider their existing business relationships. Being ableto test such hypotheses is a desired feature when ana-lyzing contextual factors in latent attrition models.

In this paper, we propose a latent attrition modelthat allows time-varying contextual factors to bemodeled in continuous noncontractual settings. Com-plementing previous literature, we combine the fol-lowing characteristics in the proposed approach: (1) thecontinuous nature of both the purchase and the attrition

processes; (2) the inclusion of multiple time-varying andtime-invariant contextual factors that can separately in-fluence both, one, or none of the processes; (3) gammaheterogeneity for both processes; (4) the ability to reduceto the Standard Pareto/NBDmodel when it is estimatedwithout any contextual factors; (5) a closed-formmaximum-likelihood solution; and (6) the deriva-tion of relevant managerial expressions. We conducttwo simulation studies and an empirical analysis ofthree retailing datasets. Benchmarking the proposedapproach against state-of-the-art Pareto- and non–Pareto-type models, the results provide evidence onthe inferential and predictive ability of the extendedPareto/NBD model. We find that (a) predictive ac-curacy generally increases when the contextual fac-tors are included and (b) differences in the increasein predictive accuracy depend on the scope of themodeled contextual factors, that is, individual levelcontextual factors increase predictive accuracy morethan aggregated-level contextual factors. Furthermore,we can (c) reliably identify the impact of the exogenousfactors on both, the purchase and the attrition processand (d) reliably identify the impact of endogenous fac-tors on both processes when applying (latent) instru-mental variable (IV) approaches. Last, we provide evi-dence that (e) controlling for endogeneityhas akey role inreliably identifying parameter estimates but little im-portance for predictive accuracy. A latent attritionmodelwith such characteristics and performance could be usedfor numerous managerial applications. For example,combinedwith a Gamma/Gammamodel (Colombo andJiang 1999, Fader et al. 2005b), this model enablesacademics and managers to improve the identifica-tion of the best future customers. In addition, con-trolling for endogenous contextual factors allows forthe rigorous identification and quantification of driversof customers’ purchase and attrition processes.The remainder of the paper is structured as follows.

In the next section, we provide an overview of therelevant literature on latent customer attrition models.Then, we present our modeling framework. We derivethe likelihood function and related expressions for pre-dicting latent customer attrition and discuss modelidentification. In this context, we then propose threeapproaches for addressing potential endogeneity ofthe contextual factors. Next, the model is empiricallyvalidated with three real-world datasets from the re-tailing industry. We compare the proposed modelagainst the standard Pareto/NBDmodel, three relatedPareto-type models (Schweidel and Knox 2013, Braunet al. 2015, Platzer and Reutterer 2016), and a recentlypublished model, which builds on an Bayesian non-parametric framework with Gaussian process priors(Dew and Ansari 2018). We conclude with a discus-sion of limitations and future research possibilities.

Bachmann, Meierer, and Näf: The Role of Time-Varying Contextual Factors in Latent Attrition Models2 Marketing Science, Articles in Advance, pp. 1–38, © 2021 The Author(s)

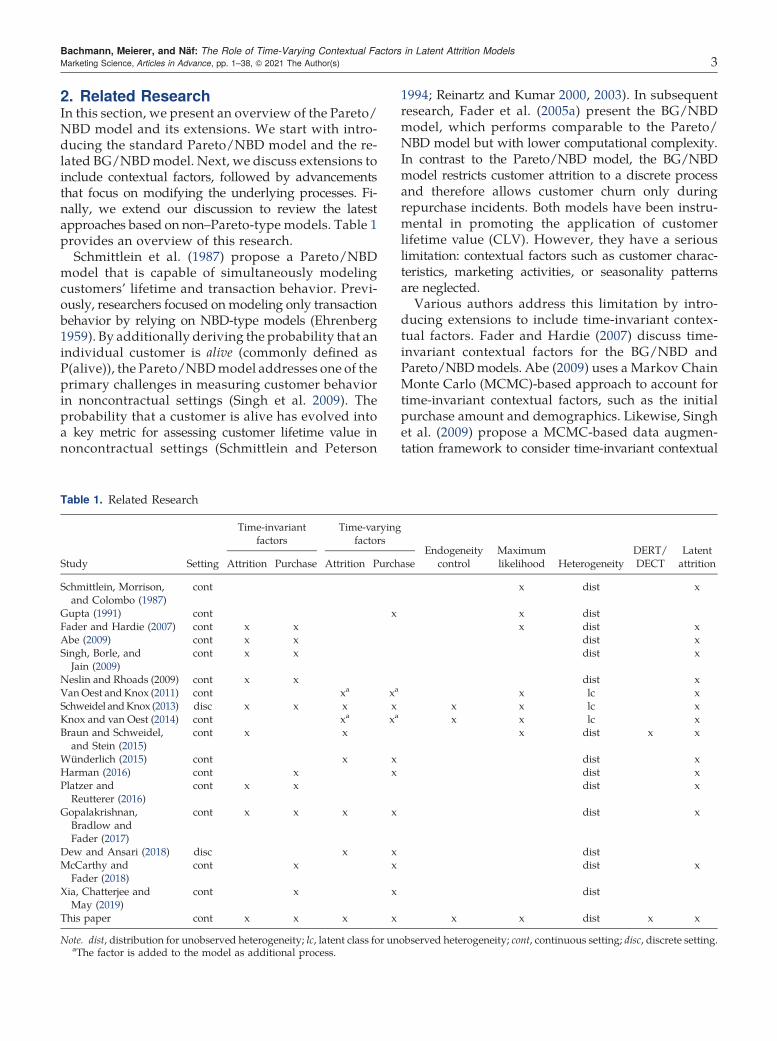

2. Related ResearchIn this section, we present an overview of the Pareto/NBD model and its extensions. We start with intro-ducing the standard Pareto/NBD model and the re-lated BG/NBDmodel. Next, we discuss extensions toinclude contextual factors, followed by advancementsthat focus on modifying the underlying processes. Fi-nally, we extend our discussion to review the latestapproaches based on non–Pareto-type models. Table 1provides an overview of this research.

Schmittlein et al. (1987) propose a Pareto/NBDmodel that is capable of simultaneously modelingcustomers’ lifetime and transaction behavior. Previ-ously, researchers focused onmodeling only transactionbehavior by relying on NBD-type models (Ehrenberg1959). By additionally deriving the probability that anindividual customer is alive (commonly defined asP(alive)), the Pareto/NBDmodel addresses one of theprimary challenges in measuring customer behaviorin noncontractual settings (Singh et al. 2009). Theprobability that a customer is alive has evolved intoa key metric for assessing customer lifetime value innoncontractual settings (Schmittlein and Peterson

1994; Reinartz and Kumar 2000, 2003). In subsequentresearch, Fader et al. (2005a) present the BG/NBDmodel, which performs comparable to the Pareto/NBD model but with lower computational complexity.In contrast to the Pareto/NBD model, the BG/NBDmodel restricts customer attrition to a discrete processand therefore allows customer churn only duringrepurchase incidents. Both models have been instru-mental in promoting the application of customerlifetime value (CLV). However, they have a seriouslimitation: contextual factors such as customer charac-teristics, marketing activities, or seasonality patternsare neglected.Various authors address this limitation by intro-

ducing extensions to include time-invariant contex-tual factors. Fader and Hardie (2007) discuss time-invariant contextual factors for the BG/NBD andPareto/NBDmodels. Abe (2009) uses a Markov ChainMonte Carlo (MCMC)-based approach to account fortime-invariant contextual factors, such as the initialpurchase amount and demographics. Likewise, Singhet al. (2009) propose a MCMC-based data augmen-tation framework to consider time-invariant contextual

Table 1. Related Research

Study Setting

Time-invariantfactors

Time-varyingfactors

Endogeneitycontrol

Maximumlikelihood Heterogeneity

DERT/DECT

LatentattritionAttrition Purchase Attrition Purchase

Schmittlein, Morrison,and Colombo (1987)

cont x dist x

Gupta (1991) cont x x distFader and Hardie (2007) cont x x x dist xAbe (2009) cont x x dist xSingh, Borle, and

Jain (2009)cont x x dist x

Neslin and Rhoads (2009) cont x x dist xVanOest andKnox (2011) cont xa xa x lc xSchweidel andKnox (2013) disc x x x x x x lc xKnox and van Oest (2014) cont xa xa x x lc xBraun and Schweidel,

and Stein (2015)cont x x x dist x x

Wünderlich (2015) cont x x dist xHarman (2016) cont x x dist xPlatzer and

Reutterer (2016)cont x x dist x

Gopalakrishnan,Bradlow andFader (2017)

cont x x x x dist x

Dew and Ansari (2018) disc x x distMcCarthy and

Fader (2018)cont x x dist x

Xia, Chatterjee andMay (2019)

cont x x dist

This paper cont x x x x x x dist x x

Note. dist, distribution for unobserved heterogeneity; lc, latent class for unobserved heterogeneity; cont, continuous setting; disc, discrete setting.aThe factor is added to the model as additional process.

Bachmann, Meierer, and Näf: The Role of Time-Varying Contextual Factors in Latent Attrition ModelsMarketing Science, Articles in Advance, pp. 1–38, © 2021 The Author(s) 3

factors when modeling latent customer attrition. How-ever, none of these extensions are able to model con-textual factors that vary over time.

Gupta (1991) is the first to introduce time-varyingcontextual factors to NBD-type models. However, incontrast to latent customer attrition models, NBD-type models focus only on customer purchases andneglect customer attrition. Recent extensions to latentcustomer attrition models include time-varying contex-tual factors for discrete and mixed noncontractualbusiness settings have been proposed. Schweidel andKnox (2013) present a discrete probabilistic latentattrition model, which captures the purchase processwith a discrete Bernoulli process and latent customerattrition with a Geometric distribution. The authorsfocus on time-discrete transactions in a charity set-ting, that is, whether a person has donated in a certainyear. Gopalakrishnan et al. (2017) present a vectorchangepointmodel in ahierarchicalBayesian frameworkto capture differences across a series of customer cohorts.Their approach allows for the probability of purchaseand attrition to vary by individual and time.

Another stream of research focuses on adding time-varying contextual factors to the transaction process.Building on the BG/NBD model (Fader et al. 2005a),Braun et al. (2015) propose an approach for incor-porating transaction-specific attributes. The authors’approach accounts for transaction characteristics atthe time of purchase as contextual factors. However,these characteristics remain constant after the trans-action and affect only the attrition process and notthe purchase process. The authors use the model toevaluate the impact of a customer’s service experienceat the time of purchase. Using a MCMC approach,Harman (2016) includes time-varying contextual factorsin the transaction process of the BG/NBD model.McCarthy and Fader (2018) develop an approach forcustomer-based corporate valuation in noncontrac-tual settings. The authors use a beta-geometric/mixed-log-normal model and allow time-varying contextualfactors to affect the purchase process.

A complementary stream of research modifies theunderlying processes to address issues caused byspecific contextual factors: Van Oest and Knox (2011)propose an extension of the BG/NBD model thatconsiders customer complaints by adding a thirdprocess to the customer purchase and attrition pro-cess of the standard model. Later, Knox and vanOest (2014) add the possibility for customer recov-ery after complaints. Wünderlich (2015) proposes thehierarchical Bayesian seasonal model with drop-out(HSMDO), which is capable of capturing individualand cross-sectional seasonality. The foundation forthis model is a discretely sampled inhomogeneousPoisson process with discrete periodic death op-portunities. Platzer and Reutterer (2016) propose an

extension of the Pareto/NBD model to describe reg-ularity patterns in purchase timing. They replace theNBD distribution with a mixture of gamma distribu-tions to allow for a varying degree of regularity acrosscustomers. The authors find empirical evidence on theimportance of the regularity of timing patterns acrossmultiple industries.Recently, non–Pareto-type models were proposed

as alternative approaches for customer base analysis.Dew and Ansari (2018) use a nonparametric frame-work for customer base analysis and propose theGaussian process propensity model (GPPM). Theauthors use Bayesian nonparametric Gaussian priorsto combine the latent functions of customer purchasebehavior and further include a latent function forcalendar-based time. Their model relies on a normalpopulation distribution to control for unobservedcustomer heterogeneity. Xia et al. (2019) apply deep-learning algorithms in the form of conditional re-stricted Boltzmann machines to predict customerpurchase patterns. Their approach does not distin-guish between purchases and attrition but rathermodels the customer’s purchase pattern as a whole.However, the model allows to include time-invariantand time-varying contextual factors, such as demo-graphics and marketing activities.

3. ModelOur approach builds on the Pareto/NBD model for con-tinuous noncontractual business settings (Schmittleinet al. 1987). To model time-varying contextual factors,we draw on Gupta (1991), who proposes an extensionto NBD-type models. Such models were widely usedin marketing research at this time (Jeuland et al. 1980,Schmittlein et al. 1985, Ehrenberg 1988). In contrast tolatent attrition models, NBD-type models do not takecustomer attrition into account and focus solely on thepurchase process.In the following, we explain how to include time-

varying contextual factors in the Pareto/NBD modelthat affect both the purchase and attrition rate. First,we introduce time-varying contextual factors into thepurchase process, and second, we introduce thesefactors into the customer attrition process. In bothcases, this will be achieved using a proportionalhazard approach. Third, we add both processes to asingle closed-form expression while also introducingcustomer heterogeneity to the two processes. Fourth,we derive the related expressions to determine theprobability that a customer is alive at the end of theestimation period (in previous studies sometimes alsonamed calibration period) (Schmittlein et al. 1987),the conditional expectation, and the discounted ex-pected conditional transactions (DECT; analogous tothe DERT proposed by Fader et al. 2005b, 2010). Fi-nally, we discuss model identification and propose

Bachmann, Meierer, and Näf: The Role of Time-Varying Contextual Factors in Latent Attrition Models4 Marketing Science, Articles in Advance, pp. 1–38, © 2021 The Author(s)

three generalized approaches to control for endoge-nous contextual factors. In this context, we also dis-cuss the impact of controlling for endogenous con-textual factors on predictive accuracy.

3.1. Purchase Process

Introducing time-varying contextual factors to thepurchase process consists of multiple steps. First,we build on the same assumptions as the standardPareto/NBD model, where customer purchases aremodeled according to a Poisson process with expo-nentially distributed interpurchase times. Second, weallow the purchase rate to be a function of the time-varying contextual factors and, therefore, also time.Next, to simplify all further derivations, we followGupta (1991) and assume that those contextual factorsare time invariant for a time interval of fixed length.Finally, we derive a general expression for the purchaseprocess. Later, we refer to these steps to facilitate abetter understanding of the model derivation. Wedenote variables specific for the purchase process withthe superscript P.

Without time-varying contextual factors being pres-ent, the purchase behavior of a customer i is modeledas a Poisson process with rate λi with regard to thenumber of purchases made during a specified timeinterval (i.e., the estimation period, (0, t]). It followsthat the probability of the number of purchases x in atime interval (0, t] is given by

P Y t( ) x( ) λit[ ]x

x!exp −λit[ ]. (1)

The probability of zero purchases for (1) defines thesurvivor function for the interpuchase time

P Y t( ) 0( ) SP t( ) exp −λit( ), (2)

and therefore, the density function for the inter-purchase time is given by

f P t( ) λi exp −λit( ). (3)

This corresponds to an exponentially distributed inter-purchase time for an individual customer.

To include time-varying contextual factors, we buildon theproportional hazardapproach.Thus,weallow thepurchase rate λi to be a function of the contextualfactors and therefore also of time:

λi t( ) λ0 exp γ′purchx

Pit

( ), (4)

where xPit denotes the vector of contextual factorsinfluencing the purchase process at time t, γpurch

represents a vector of contextual factor effect sizes, andλ0 is the base purchase rate. For simplicity, we assumeλ0 to be identical for all customers. This assumptionwill be relaxed later when customer heterogeneity is

introduced to the model. To simplify the notation, weremove the customer index i for all subsequent der-ivations. The coefficient γpurch may be directly inter-preted as rate elasticity. A 1% change in a contextualfactor xP changes the purchase rate by γ′

purchxP%. An

increase of the purchase rate corresponds to a de-crease in interpurchase time (Gupta 1991). Becauseλ(t) is now a function of time-varying contextual factors,the purchase process is now a nonhomogenous Poissonprocess (Ross 2014). In particular, the times betweenthe purchases of an individual customer are no longerindependent and identically distributed, except ifλ(t) λ. It follows that the probability of the numberof purchases x in a time interval (0, t] is given by (1)where we substitute λt by

θP0 t( )

∫ t

0λ τ( ) dτ. (5)

Note that (5) reduces to λt for a homogenous Poissonprocess. The survivor function and the density for theinterpurchase time are given as (2) and (3) with λtsubstituted by (5).In contrast to the standard Pareto/NBD model, the

timing of purchases becomes relevant when intro-ducing time-varying contextual factors. In particular,the interpurchase time between events j and j + 1mayhave a different distribution compared with the onebetween events j + 1 and j + 2. To account for this fact,we rewrite (1) using indices specifying the transac-tions. We denote for all subsequent derivations tj asthe time of transaction j with j 1, . . . , x and zj−1,j tj − tj−1 the time passed between transaction j − 1 and j.The probability of the number of purchases in a timeinterval (tj−1, tj] is then given by

P Y tj−1, tj( )

x( )

θPtj−1

zj−1,j( )[ ]x

x!exp −θP

tj−1zj−1,j( )[ ]

, (6)

with

θPtj−1

zj−1,j( )

∫ tj

tj−1

λ τ( ) dτ. (7)

With Zj−1,j as a random variable specifying the timebetween purchases j − 1 and j, we may derive thesurvivor function:

P Zj−1,j > zj−1,j|tj−1( )

P X tj−1, tj( )

0( )

exp −θPtj−1

zj−1,j( )[ ]

(8)

and arrive at the following density function of theinterpurchase time:

f P zj−1,j|tj−1( )

f P zj−1,j|z0,1, z1,2, . . . , zj−2,j−1( )

λ tj( )

exp −θPtj−1

zj−1,j( )[ ]

. (9)

Bachmann, Meierer, and Näf: The Role of Time-Varying Contextual Factors in Latent Attrition ModelsMarketing Science, Articles in Advance, pp. 1–38, © 2021 The Author(s) 5

Following Gupta (1991), we simplify θPtj−1

(t) by as-suming that the contextual factors are time-invariantfor time intervals of fixed length (e.g., one week).Therefore, the contextual factors change only fordifferent intervals while staying constant in between.In principle, these time intervals can be arbitrarilysmall. It is important to emphasize that while thetime-varying contextual factors are discretized, theunderlying purchase process remains continuous.In consequence, θP(t), will consist of multiple λ(t)components. We denote kj as the number of intervalssince purchase j − 1. Simplifying the notation, weindex the contextual factors as xP1 , . . . , x

Pkj. By doing so,

the factors are indexed relative to the purchases,where the interval count starts at one for every pur-chase. In particular, x1 specifies the contextual factorsin the interval that contains the (j − 1)th transaction,

whereas xkj specifies the ones in the interval of the jthtransaction. d1 is defined as the time of the transaction(j − 1) to the end of the first interval for any two suc-cessive transactions (j − 1) and j. Note that d1 is indexedrelative to the purchases. To illustrate the differentcomponents of θP

tj−1(t) in (7), let us outline three possible

cases. The different cases are illustrated in Figure 1.

Case 1. The two purchases that define the interpurchasetime occur during the same time interval (e.g., the firsttime interval),

λ t( ) λ1 λ0 exp γ′purchx

P1

( )

θPtj−1

t( )

∫ tj

tj−1

λ τ( ) dτ

∫ zj−1,j

0λ1 dτ

λ1zj−1,j.

Figure 1. Timeline of the Purchase Process Adapted from Gupta (1991)

Bachmann, Meierer, and Näf: The Role of Time-Varying Contextual Factors in Latent Attrition Models6 Marketing Science, Articles in Advance, pp. 1–38, © 2021 The Author(s)

Case 2. The two purchases that define the interpurchasetime occur in two consecutive time intervals (e.g., the firstand the second time interval),

λ t( ) λ2 λ0 exp γ′purchx

P2

( )

θPtj−1

t( )

∫tj

tj−1

λ τ( ) dτ

∫d1+tj−1

tj−1

λ1 dτ +

∫tj

d1+tj−1

λ2 dτ

λ1d1 + λ2 zj−1,j − d1( )

.

Case 3. The two purchases that define the inter-purchase time occur in two nonconsecutive time in-tervals (e.g., the first and the third time interval),

λ t( ) λ3 λ0 exp γ′purchx

P3

( )

θPtj−1

t( )

∫tj

tj−1

λ τ( ) dτ

∫d1+tj−1

tj−1

λ1 dτ

+

∫ 1+d1+tj−1

d1+tj−1

λ2 dτ +

∫tj

1+d1+tj−1

λ3 dτ

λ1d1 + λ2 + λ3 zj−1,j − d1 − 1( )

.

All further cases, with more time intervals betweenthe two purchase events, are composed in the samemanner. To derive a general expression for this pat-tern, we define

λ t( ) λ0 exp γ′purchx

Pl

( ), (10)

where l 1, . . . , kj denotes the interval in which t lies.It follows that λ(tj) λkj , and we arrive at a morepractical version of (7):

θPkjzj−1,j( )

λ1d1+∑kj−1

l2

λl+λkj zj−1,j−d1−δ kj−2( )[ ]

, (11)

where δ 0 if kj 1 and δ 1 if kj ≥ 2. δ accounts forthe special case, where two subsequent purchasesoccur within the same time interval. Substituting λ(t)and θP

kj(zj−1,j) from (10) and (11) into (8) and (9) pro-

vides the survivor and density functions with time-varying contextual factors. Remember that contextualfactors which are constant over time, result in a ho-mogeneous process (i.e., λ(t) λ and θ(t) λt).

Thus far, we have introduced time-varying con-textual factors into the purchase process. In the nextsection, we introduce time-varying contextual factorsinto the attrition process.

3.2. Attrition Process

To include time-varying contextual factors in theattrition process, we proceed analogously. AlthoughGupta (1991) introduces contextual factors to thepurchase process only, the underlying methodol-ogy is also applicable for the attrition process. In a

first step, we build on the assumption of the standardPareto/NBD model, where customer attrition is mod-eled by an exponential distribution. Next, we allow theattrition rate to be a function of the time-varying con-textual factors and then assume that those contextualfactors are time invariant for a time interval of fixedlength. Finally, we derive a general expression for theattrition process. The following discussion is structuredanalogously to the model derivation of the purchaseprocess. We denote variables specific for the attritionprocess with the superscript A.Without time-varying contextual factors being pres-

ent, the unobserved lifetime Ω of an individual cus-tomer is exponentially distributed. At the end of thislifetime, the customer is considered inactive. Thisleads to the following density and the survivor functionfor the attrition process:

fA ω( ) μi exp −μiω( )

, (12)

SAi ω( ) P Ω > ω( ) exp −μiω( )

, (13)

where μi is the attrition rate of an individual customer i.To compare the attrition process to the purchaseprocess, we can express attrition as a purchase-likeprocesswith two events for every customer: the initialtransaction is the first and a customer’s (unobserved)attrition is the second event. Therefore, the propertiesand derivations of the two processes are very similar.When including time-varying contextual factors,

the attrition rate becomes a function of the contextualfactors and of time:

μi ω( ) μ0 exp γ′attrx

Aiω

( ), (14)

where xAiω denotes the vector of contextual factorsinfluencing a customer’s attrition process during hislifetime ω. The variable γattr represents a vector ofeffect sizes for contextual factors. μ0 is the base at-trition rate. These contextual factors may or may notbe the same as xPit. Initially, we assume that μ0 is thesame for all customers. This assumption will be re-laxed later. The interpretation of the effect sizes γattr isidentical to the purchase process: a 1% change in acontextual factor xA changes the attrition rate byγ′attrx

A%. Again, we remove the customer index i in allsubsequent derivations to simplify the notation.Based on the density derived for the transaction

process (9), the density of a customer’s lifetime Ω isgiven by

f A ω( ) μ ω( ) exp −θA0 ω( )

[ ], (15)

where

θA0 ω( )

∫ω

0μ τ( ) dτ. (16)

Bachmann, Meierer, and Näf: The Role of Time-Varying Contextual Factors in Latent Attrition ModelsMarketing Science, Articles in Advance, pp. 1–38, © 2021 The Author(s) 7

The cumulative distribution function is given by

F ω( )

∫ ω

0fA τ( ) dτ 1 − exp −θA

0 ω( )[ ]

. (17)

We simplify θA(ω) by assuming that the contextualfactors are time invariant for certain time intervals offixed length. For simplicity reasons, we assume thatthe time intervals are identical to the ones from thepurchase process. However, this is not required. Inconsequence, θA

0 (ω) also consists of multiple com-ponents, which are composed in the same manner asθPtj(t) of the purchase process. Let kω denote the

number of the time intervals from zero to the end of acustomer’s lifetime ω. Then, the general case for allcomponents of θA

kωis given by

θAkω

ω( ) μ1d2 +∑kω−1

l2

μl + μkω ω − d2 − δ kω − 2( )[ ], (18)

where μl μ0 exp(γ′attrx

Al ) and δ 0 if kω 1 and δ 1

if kω ≥ 2, d2 is defined as the time between 0 and theend of the first interval. Finally, δ accounts for thespecial case where a customer’s first purchase andattrition occur in the same time interval.

3.3. Likelihood Derivation

Thus far, we modeled the customer purchase andattrition processes separately. To derive the indi-vidual likelihood,we combine the two processes. Thisconsists of multiple steps. First, we take a closer lookat the purchase process in order to identify differentways customer attrition can affect it. Then, we com-bine the purchase and the attrition process. Next, weintroduce customer heterogeneity and relax the as-sumption of identical purchase and attrition ratesacross customers. Finally, we arrive at a closed-formsolution for the individual likelihood. Our approachuses a similar methodology as the one illustrated byFader and Hardie (2005) for the standard Pareto/NBD model. In this section, we discuss the steps forderiving the individual likelihood; more detailedmathematical derivations are presented in Appen-dix A.1 and Appendix B.

Before combining the purchase and the attritionprocess, we need to distinguish two cases that affectthe purchase process. When observing a customerduring the estimation period (0,T], the followingscenarios are possible: either (1) he is alive at the endof the estimation periodT or (2) the customer becomesinactive between the last observed transaction and T.We compose the individual likelihood as the productof the densities for the interpurchase times and thesurvivor function. With regard to the latter, we usethe survivor function between the first transactionafter the end of the estimation period T and the very

last transaction of the customer (note that both ofthese transactions are unobserved).

Case 1. The customer is still alive at the end of theestimation period T. This means that the lifetime ofthe customer is longer than the observed period (i.e.,ω > T). To compose the individual likelihood in thiscase, the survivor function is evaluated at the timebetween the last observed transaction and the end ofthe estimation period.

Case 2. The customer becomes inactive between thelast transaction and T. This means that the customer’slifetime ends somewhere before the end of the esti-mation period (i.e., ω ∈ (tx,T]). To compose the indi-vidual likelihood in this case, the survivor functionis evaluated at the time between the last observedtransaction and the end of the customer’s lifetime ω.

In a next step, we combine the two cases and derivethe individual likelihood conditional on λ0 and μ0:

L λ0, γpurch, γattr, μ0|t,T,XP,XA, x

( )

L λ0, γpurch | t,T,XP, x ,Ω > T

( )P Ω > T|μ0

( )

+

∫ T

tx

L λ0, γpurch | t,T,XP, x, ω ∈ tx,T( ]

( )

× fA ω|μ0

( )dω. (19)

The integral in expression (19) depends on ω throughkx,ω. To solve it, we use the assumption that thecontextual factors are constant during fixed time in-tervals. Therefore, we are able to split the integral intoparts, where kx,ω is constant, with kx,ω 1, . . . , kT.Finally, we relax the assumption that all customers

have the same purchase and attrition rate and in-troduce customer heterogeneity (i.e., we allow λ0 andμ0 to vary across customers). Following Schmittleinet al. (1987), we assume the purchase rate Λ0 and theattrition rateM0 to be Gamma distributed with shapeparameter r and scale parameter α, respectively, sand β,

g λ0( ) αrλr−1

0 e−λ0α

Γ r( )and g μ0

( )βsμs−1

0 e−μ0β

Γ s( )

and arrive at

L α , r, β , s, γpurch, γattr | t,T,XP,XA, x

( )

∫∞

0

∫∞

0L λ0, μ0, γpurch, γattr | t,T,X

P,XA, x( )

× g λ0( )g μ0

( )dλ0dμ0. (20)

By removing the conditioning on λ0 and μ0, we areable to derive the final individual likelihood. For theclosed-form solution of (20), see Appendix A.1. Thedetailed steps for deriving the closed-form solutionincluding solving the integral in (20) are provided inAppendix B.

Bachmann, Meierer, and Näf: The Role of Time-Varying Contextual Factors in Latent Attrition Models8 Marketing Science, Articles in Advance, pp. 1–38, © 2021 The Author(s)

3.4. P(alive)

In noncontractual settings, customer churn is notobserved. Therefore, the probability of being alive atthe end of the estimation period T, P(alive), is a keycomponent of predicting future purchase behavior.P(alive) is the probability that the lifetime of thecustomer is larger than T, P(Ω > T), given all availableinformation. To obtain P(alive), we first apply theBayes’ theorem to obtain the posterior probability ofbeing alive. Because the purchase rate λ0 and theattrition rate μ0 are not directly observed, we furtherneed to include the posterior distribution of (λ0, μ0),before we can integrate them out and arrive at theclosed-form solution for P(alive).

Applying Bayes’ theorem to the individual likeli-hood (19) results in

P Ω > T|λ0, μ0,XP,XA, γpurch, γattr, x, t,T

( )

L λ0, γpurch|X

P, x, t,T,Ω > T( )

P Ω > T|μ0

( )

L λ0, γpurch, γattr, μ0|t,T,XP,XA, x( ) . (21)

Because the purchase rate λ0 and the attrition rate μ0

are not directly observed, we multiply (21) by theposterior distribution of (λ0, μ0), which is given as

g λ0, μ0|r, α, s, β, γpurch, γattr,XP,XA, x, t,T

( )

L λ0, γpurch, γattr, μ0|X

P,XA, x, t,T( )

g λ0( )g μ0

( )

L α, r, β, s, γpurch, γattr|XP,XA, x, t,T

( ) .

(22)

Then, we take the integral with respect to this jointdistribution to obtain the final P(alive) expression:

P Ω > T|r, α , s, β , γpurch, γattr,XP,XA, x, t,T

( )

∫∞

0

∫∞

0P Ω > T|λ0, μ0,X

P,XA, γpurch, γattr, x, t,T( )

× g λ0, μ0|r, α , s, β , γpurch, γattr,XP,XA, x, t,T

( )

× dλ0dμ0. (23)

The closed-form solution to (23) is reported inAppendix A.2, and related derivations are reportedin Appendix C.

3.5. Conditional Expectation

The conditional expectation metric allows practi-tioners and researchers to predict the future numberof purchases of an individual given a customer’s pastpurchase behavior. To derive the expression, wefollow multiple steps. We start with the assumptionthat the customer did not stop purchasing before theprediction period. However, we still have to distin-guish two cases for a customer’s possible attritionduring the prediction period. We use the character-istics of nonhomogenous Poisson processes and the

fact that the contextual factors are assumed to be timeinvariant for an interval of fixed length to derive thefirst conditional expectation. Last, we relax our initialassumption and allow attrition before the predictionperiod. In this section, we discuss the steps for de-riving the conditional expectation; more mathemat-ical derivations are presented in Appendix C.We start by deriving E[Y(T,T + t)|r, α, s , β, γpurch,

γattr,XP,XA, x, t,T], where Y(T,T + t) is a random var-

iable specifying the number of purchases made afterthe estimation period in the interval (T,T + t]. Our ap-proach is based on Fader and Hardie (2005). We startderiving the conditional expectation under the as-sumption that the customer is alive after the end of theestimation period T. This assumption is relaxed later.Under this assumption, the conditional expectationis a special case of the purchase process, where wehave two transactions, the first one at T and thesecond one at ω, with ω ∈ (T,T + t].Although we assume that all customers are alive at

the end of the estimation period, there are still twodifferent cases to consider about the timing of cus-tomer attrition. The customer may stop buying afterthe end of the prediction period or during the pre-diction period.

Case 1. The lifetime of the customer is longer than theprediction period, that is, ω > T + t. In this case, we getthe expectation of the nonhomogenous purchase pro-cess with ω > T + t:

E Y T,T + t( )|λ0,XP, γpurch,Ω > T + t

[ ].

Case 2. The customer stops purchasing betweenthe end of the observation period and the end ofthe prediction period. In this case, we get the ex-pectation of the nonhomogenous attrition processwith ω ∈ (T,T + t]:

E Y T,T + t( )|λ0,XP, γpurch,Ω ∈ T,T + t( ]

[ ].

We combine the two cases, but because we do notobserve the customer lifetime ω, we also have toconsider the attrition process:

E Y T,T + t( )|λ0, μ0,XP,XA, γpurch, γattr,Ω > T

[ ]

E Y T,T + t( )|λ0,XP, γpurch,Ω > T + t

[ ]

× P Ω > T + t|μ0,Ω > T( )

+

+

∫ T+t

TE Y T,T + t( )|λ0,X

P, γpurch,[(

ω ∈ T,T + t( ]])

× fA ω|μ0,Ω > T( )

dω. (24)

For expression (24), we assume that customers are aliveat the end of the observation period T, that is, ω > T.

Bachmann, Meierer, and Näf: The Role of Time-Varying Contextual Factors in Latent Attrition ModelsMarketing Science, Articles in Advance, pp. 1–38, © 2021 The Author(s) 9

To relax this assumption, we add the posterior distri-butionof being alive atT, P(alive), fromEquation (A.2).

E Y T,T + t( )|λ0, μ0,XP,XA, γpurch, γattr, x, t,T

[ ]

E Y T,T + t( )|λ0, μ0,XP,XA, γpurch, γattr,

[x, t,Ω > T

]

× P Ω > T|λ0, μ0,XP,XA, γpurch, γattr, x, t,T

( ). (25)

By removing the conditioning on λ0 and μ0, we arriveat the closed-form solution reported in Appendix A.3.

3.6. DECT

To estimate individual customer lifetime values withthe proposed model in combination with a Gamma/Gamma model (Colombo and Jiang 1999, Fader et al.2005b), we need to derive the present value of the ex-pected future transactions and account for the discountrate. We define the DECT. The concept of this metricis very similar to the discounted expected residualtransactions (DERT) (Fader et al. 2005b, 2010).

The general formulation of the customer lifetimevalue (CLV) is

E CLV( )

∫∞

0

v t( )S t( )d t( )dt,

where v(t) is the customer value at t, S(t) 1 − F(t) P(Ω > t) denotes the survivor function ofΩ and d(t) aspecific discount factor. Assuming that the value ofeach transaction remains constant, v(t) can be factoredout leaving only the purchase rate λ(t) in the integral:

∫∞

0λ t( )S t( )d t( )dt.

These are the discounted expected transactions (DETs).Starting instead at t T, the end of the estimation

period, for continuous discounting with a rate of ∆,gives the DERT (Fader et al. 2005b, 2010):

DERT ∆|λ0, μ0,XP,XA, γpurch, γattr,Ω > T

( )

∫∞

T

λ t( )P Ω > t|Ω > T( )d t( )dt

∫∞

Tλ0 exp xPt

( )exp −μ0 θ0 t( ) −θ0 T( )( )

[ ]

× exp −∆ t−T( )[ ]dt.

Whenmodeling time-varying contextual factors, we facethe issue that the measurements of the time-varyingcontextual factors are likely not known up to infinity.Thus, we make predictions only within a time frame forwhich the time-varying contextual factors are known.Therefore, we truncate the time horizon of our predic-tions and approximate the DERT as DECT:

DECT ∆, t|r, α, s , β, γpurch, γattr,XP,XA, x, t,T

( )

∫ T+t

Tλ0 exp xPτ

( )exp −μ0 θ0 τ( ) − θ0 T( )( )

[ ]

× exp −∆ τ − T( )[ ] dτ, (26)

where t > 0 is theprediction length.Wepresent theclosed-form solution to the integral in (26) in Appendix A.4.

3.7. Model Identification

When considering contextual factors in the Pareto/NBDmodel,model identification has to be addressed.In the following, we focus on the ability of the ex-tended Pareto/NBD model to separately identify theeffects of time-varying contextual factors on the pur-chase process and the attrition process. The identifica-tion of standard latent customer attrition models with-out contextual factors has been thoroughly discussed inprior studies (Schmittlein et al. 1987, Fader andHardie2005, Schweidel and Knox 2013).First, we describe the effects of contextual factors:

modeling contextual effects means that a part of theunobserved heterogeneity is substituted by system-atic differences, which are expressed by the contex-tual factors. As such, the parameter r, whichmeasureshomogeneity in the purchase process, and the pa-rameter s, which measures homogeneity in the attritionprocess, should increase when modeling contextual ef-fects (Gupta 1991). The effects of contextual factors mayinfluence both the purchase and the attrition processes,just one of the processes, or neither of the processes.Although this applies to both time-invariant and time-varying contextual factors, the identification of these twocategories of contextual effects relies on different sourcesof variation.To identify time-invariant contextual factors, it is

possible to leverage the variation across customergroups. For example, female customers might pur-chase more. However, their loyalty is the same as thatof male customers. Thus, gender will influence onlythe purchase process and not the attrition process.Another example is that older customers might bemore loyal to the retailer, and, therefore, more timemust pass until they stop purchasing. However, theirpurchase rate may be the same as that of youn-ger customers.The identification of time-varying contextual fac-

tors, which allow us to capture the effects of dynamicchanges in a customer’s context (e.g., personalizedmarketing), is more complex. Individual customersare allowed to change their purchase and attritionbehavior over time. Temporal events may cause astrictly temporary change in the purchase rate (e.g.,shortly after receiving a personalized marketing of-fer, customers tend to purchasemore). However, suchan event may also influence a customer’s futurepurchase behavior. For example, personalized mar-keting might encourage customers to return to thestore in the future and therefore can reduce thelikelihood that a customerwill stop purchasing at thispoint in time. To identify such patterns, variationacross time must be considered.

Bachmann, Meierer, and Näf: The Role of Time-Varying Contextual Factors in Latent Attrition Models10 Marketing Science, Articles in Advance, pp. 1–38, © 2021 The Author(s)

Building on a comprehensive simulation study, weanalyze various scenarios and find support for theidentification of contextual factors in the extendedPareto/NBD model. The fitted model recovers thetrue parameters for the contextual factors of thesimulated data. The simulation study was conductedas follows: we generate transactional data of 3,000 cus-tomers for Poisson-distributed purchases and incorpo-rate the exponentially distributed attrition assumptionincluding effects for time-varying contextual factors.Thereby, a contextual factor may affect the two under-lying processes in four different ways: (1) only thepurchase process is affected; (2) only the attrition processis affected; (3) both processes are affected; or (4) thecontextual factor does not have an effect on either pro-cess. We generate contextual factors as both a binaryvariable (i.e., dummy variables for seasonal patterns)and a count variable (i.e., direct marketing actions)ranging from [0, 16]. The true effect sizes of the con-textual factors vary across three levels (0.5, 1, and 1.5).These effect sizes may be interpreted as rate elastic-ities for the purchase and attrition rates. To test themodel identification for different levels of homoge-neity across customers for both the purchase rateand attrition rate, we vary the shape parameters(r and s, respectively) between a high and a low levelof customer homogeneity (high r 4.5, s 1.5 andlow r 1.5, s 0.5). The scale parameters (α and β) arekept constant (α 170, β 8). Both the shape andscale parameters are set to correspond to the valuesobserved in the empirical analyses of real-world datasets in this paper (see Section 4). In total, we analyze48 scenarios. Every scenario is simulated 50 times toaccount for sample variation in the data genera-tion process.

To determine the effect sizes, we apply the ex-tended Pareto/NBD model to the simulated datasetsover a two-year estimation period. Table 2 shows theresults of the simulation study. The reported figuresare mean values of 50 repeated simulations. Themodel is capable of accurately recovering the pa-rameter values for all settings. Notably, we observe agreater variance for the attrition process than for thepurchase process. This occurs because the customerattrition rate is, in contrast to the purchase rate, notdirectly observed in the model. In addition, we alsoobserve a greater variance for the binary variable thanfor the count variable. This is expected, because bi-nary factors provide less information.

3.8. Endogenous Contextual Factors and

Recovering the True Parameter Values

The extended Pareto/NBD model assumes that thecontextual factors are exogenous. Although this istrue for contextual factors such as seasonal patterns,marketing activities are nonrandom in most cases,

as they are often based on an individual customer’sprevious performance (Shugan 2004, Schweidel andKnox 2013). To accurately quantify effects of mar-keting activities and similar contextual factors, wehave to account for their nonrandom nature. In thefollowing, we discuss three different approaches tocontrol for endogenous contextual factors in the ex-tended Pareto/NBD model for the purchase process.The approaches are identical for the attrition pro-cess. We start discussing an IV approach, followedby a control function and finally a copula correctionmethod. Furthermore, we present the results of anadditional simulation study that provides evidence ofthe capability of the extended Pareto/NBD model torecover the actual effect sizes of endogenous con-textual factors.Let us consider the purchase process of one ran-

domly chosen customer with a mean purchase rategiven as

Λk Λ0 exp γpurchxk( )

, (27)

where k 1, . . . ,K denotes the predefined time in-tervals for the contextual factors. For simplicity, weassume there is only one contextual factor. In inter-val k, thenumberof transactions isdistributedaccordingto a standard homogenous Poisson process. We canrewrite (27) as

log Λk( ) γpurchxk + log Λ0( ). (28)

The heterogeneity in Λ0 is Gamma distributed withthe parameters r and α; therefore, the density ofN : log(Λ0) can be derived as

f ν( ) αr

Γ r( )exp rν − α exp ν( )

( ), (29)

which is known as the Loggamma distribution: N ∼LogGam(r, α). Accordingly, log(Λk) is log-gamma dis-tributed with an additional location term γpurchxk:

log Λk( ) γpurchxk +Nk.

If the contextual factor is endogenous, xk is correlatedwith Nk. If there is a positive correlation, a high basetransaction rate λ0 will lead to a high v log(λ0) andconsequently, to a high xk biasing γpurch.To address this issue, we introduce an IV zk that

correlates with xk but is independent of Nk:

xk β0 + β1zk + ǫk, (30)

where ǫk is independent and identically distributedand correlatedwith the Loggammadistribution ofNk.In the case of marketing activities, previous research(Schweidel and Knox 2013) relies on lagged recency,frequency, and monetary value (RFM) scores to model

Bachmann, Meierer, and Näf: The Role of Time-Varying Contextual Factors in Latent Attrition ModelsMarketing Science, Articles in Advance, pp. 1–38, © 2021 The Author(s) 11

a firm’s targeting decision. This leads us to the fol-lowing two-step approach: first, we estimate (30) usingleast squares to obtain xk : β0 + β1zk. Second, weestimate the extended Pareto/NBD model, but in-stead of using the endogenous contextual factor xk, weuse xk. The procedure is similar for the attritionprocess. The proposed two-step IV approach assumesa linear combination of the explanatory variables

(i.e., linear-in-parameters model). A second methodto control for endogenous variables is the controlfunction approach (Rivers and Vuong 1988, Petrinand Train 2010). It offers a parsimonious way to ac-count for endogeneity of a contextual factor even if itinteractswith other exogenous variables (Wooldridge2015). Instead of estimating the extended Pareto/NBD model with xk, we add the error term ǫk in (30)

Table 2. Simulation Results for Recovering Exogenous Contextual Factors

Contextualfactor type Homogeneity

True valueγpurch

Meanestimateγpurch

Estimate SDγpurch

True valueγattr

Meanestimateγattr

EstimateSD γattr

Contextual factor influences Binary High 0.5 0.516 0.081 0.5 0.555 0.135both processe Binary High 1 0.989 0.072 1 0.990 0.149

Binary High 1.5 1.473 0.074 1.5 1.538 0.118Binary High 0.5 0.482 0.106 1.5 1.539 0.149Binary High 1.5 1.488 0.065 0.5 0.518 0.060Binary Low 0.5 0.488 0.070 0.5 0.506 0.241Binary Low 1 0.998 0.066 1 0.968 0.285Binary Low 1.5 1.509 0.073 1.5 1.439 0.312Binary Low 0.5 0.516 0.085 1.5 1.462 0.313Binary Low 1.5 1.516 0.070 0.5 0.553 0.209Count High 0.5 0.516 0.045 0.5 0.527 0.071Count High 1 1.006 0.043 1 1.043 0.071Count High 1.5 1.436 0.019 1.5 1.483 0.089Count High 0.5 0.480 0.095 1.5 1.452 0.114Count High 1.5 1.433 0.029 0.5 0.506 0.058Count Low 0.5 0.480 0.095 0.5 1.452 0.114Count Low 1 0.999 0.033 1 0.975 0.120Count Low 1.5 1.454 0.028 1.5 1.429 0.092Count Low 0.5 0.496 0.051 1.5 1.450 0.157Count Low 1.5 1.454 0.019 0.5 0.492 0.087

Contextual factor influences Binary High 0.5 0.488 0.065 0 0.002 0.125only purchase process Binary High 1 1.018 0.066 0 −0.002 0.108

Binary High 1.5 1.508 0.063 0 0.032 0.093Binary Low 0.5 0.512 0.072 0 0.056 0.179Binary Low 1 0.999 0.061 0 0.011 0.227Binary Low 1.5 1.500 0.051 0 −0.017 0.186Count High 0.5 0.507 0.040 0 0.020 0.083Count High 1 0.995 0.028 0 0.023 0.067Count High 1.5 1.414 0.018 0 0.016 0.057Count Low 0.5 0.505 0.039 0 0.004 0.163Count Low 1 0.964 0.023 0 0.005 0.094Count Low 1.5 1.449 0.019 0 −0.024 0.095

Contextual factor influences Binary High 0 −0.008 0.111 0.5 0.528 0.172only attrition process Binary High 0 0.021 0.102 1 1.012 0.174

Binary High 0 −0.039 0.121 1.5 1.467 0.179Binary Low 0 0.007 0.095 0.5 0.054 0.261Binary Low 0 0.002 0.085 1 0.925 0.271Binary Low 0 −0.006 0.098 1.5 1.451 0.345Count High 0 0.006 0.066 0.5 0.507 0.077Count High 0 −0.002 0.095 1 0.984 0.117Count High 0 −0.046 0.136 1.5 1.486 0.129Count Low 0 −0.006 0.052 0.5 0.472 0.193Count Low 0 0.014 0.061 1 1.013 0.178Count Low 0 0.005 0.067 1.5 1.421 0.212

No influence Count High 0 0.001 0.059 0 0.002 0.102Count Low 0 0.010 0.050 0 0.058 0.161Binary High 0 −0.007 0.080 0 −0.009 0.100Binary Low 0 0.018 0.091 0 0.068 0.268

Bachmann, Meierer, and Näf: The Role of Time-Varying Contextual Factors in Latent Attrition Models12 Marketing Science, Articles in Advance, pp. 1–38, © 2021 The Author(s)

as an additional contextual factor, to the model (inaddition to the endogenous contextual factor).

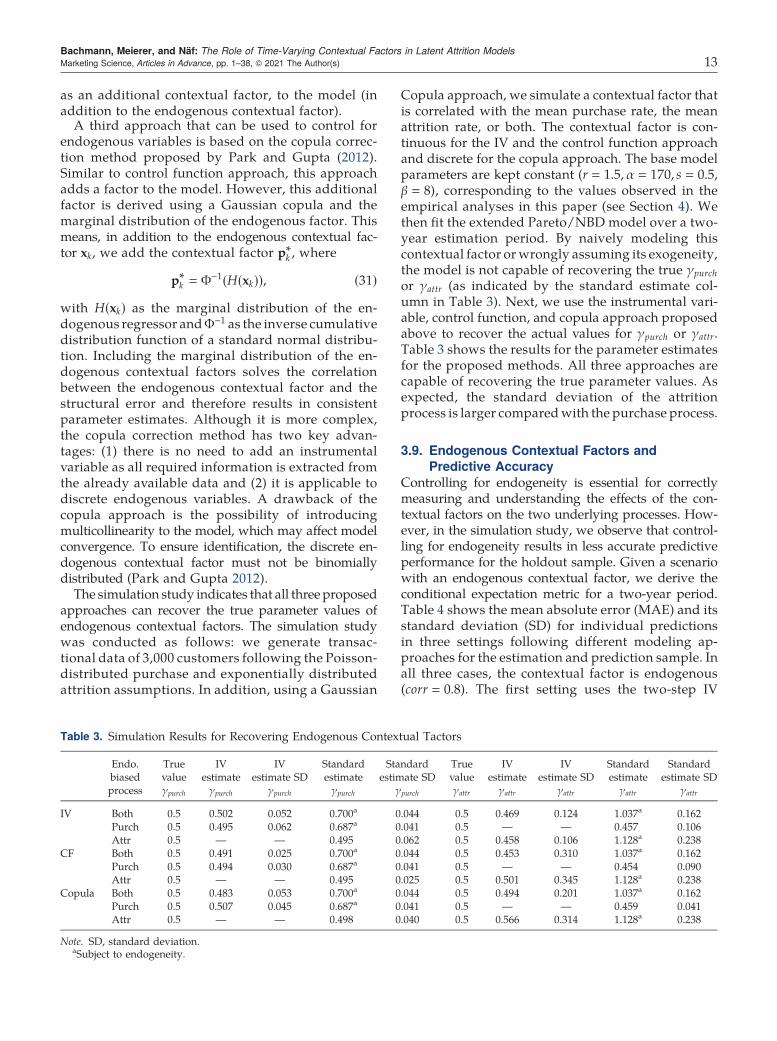

A third approach that can be used to control forendogenous variables is based on the copula correc-tion method proposed by Park and Gupta (2012).Similar to control function approach, this approachadds a factor to the model. However, this additionalfactor is derived using a Gaussian copula and themarginal distribution of the endogenous factor. Thismeans, in addition to the endogenous contextual fac-tor xk, we add the contextual factor p∗k , where

p∗k Φ−1 H xk( )( ), (31)

with H(xk) as the marginal distribution of the en-dogenous regressor andΦ−1 as the inverse cumulativedistribution function of a standard normal distribu-tion. Including the marginal distribution of the en-dogenous contextual factors solves the correlationbetween the endogenous contextual factor and thestructural error and therefore results in consistentparameter estimates. Although it is more complex,the copula correction method has two key advan-tages: (1) there is no need to add an instrumentalvariable as all required information is extracted fromthe already available data and (2) it is applicable todiscrete endogenous variables. A drawback of thecopula approach is the possibility of introducingmulticollinearity to the model, which may affect modelconvergence. To ensure identification, the discrete en-dogenous contextual factor must not be binomiallydistributed (Park and Gupta 2012).

The simulation study indicates that all three proposedapproaches can recover the true parameter values ofendogenous contextual factors. The simulation studywas conducted as follows: we generate transac-tional data of 3,000 customers following the Poisson-distributed purchase and exponentially distributedattrition assumptions. In addition, using a Gaussian

Copula approach, we simulate a contextual factor thatis correlated with the mean purchase rate, the meanattrition rate, or both. The contextual factor is con-tinuous for the IV and the control function approachand discrete for the copula approach. The base modelparameters are kept constant (r 1.5, α 170, s 0.5,β 8), corresponding to the values observed in theempirical analyses in this paper (see Section 4). Wethen fit the extended Pareto/NBD model over a two-year estimation period. By naively modeling thiscontextual factor orwrongly assuming its exogeneity,the model is not capable of recovering the true γpurch

or γattr (as indicated by the standard estimate col-umn in Table 3). Next, we use the instrumental vari-able, control function, and copula approach proposedabove to recover the actual values for γpurch or γattr.Table 3 shows the results for the parameter estimatesfor the proposed methods. All three approaches arecapable of recovering the true parameter values. Asexpected, the standard deviation of the attritionprocess is larger comparedwith the purchase process.

3.9. Endogenous Contextual Factors and

Predictive Accuracy

Controlling for endogeneity is essential for correctlymeasuring and understanding the effects of the con-textual factors on the two underlying processes. How-ever, in the simulation study, we observe that control-ling for endogeneity results in less accurate predictiveperformance for the holdout sample. Given a scenariowith an endogenous contextual factor, we derive theconditional expectation metric for a two-year period.Table 4 shows the mean absolute error (MAE) and itsstandard deviation (SD) for individual predictionsin three settings following different modeling ap-proaches for the estimation and prediction sample. Inall three cases, the contextual factor is endogenous(corr 0.8). The first setting uses the two-step IV

Table 3. Simulation Results for Recovering Endogenous Contextual Tactors

Endo.biasedprocess

Truevalueγpurch

IVestimateγpurch

IVestimate SD

γpurch

Standardestimateγpurch

Standardestimate SD

γpurch

Truevalueγattr

IVestimateγattr

IVestimate SD

γattr

Standardestimateγattr

Standardestimate SD

γattr

IV Both 0.5 0.502 0.052 0.700a 0.044 0.5 0.469 0.124 1.037a 0.162Purch 0.5 0.495 0.062 0.687a 0.041 0.5 — — 0.457 0.106Attr 0.5 — — 0.495 0.062 0.5 0.458 0.106 1.128a 0.238

CF Both 0.5 0.491 0.025 0.700a 0.044 0.5 0.453 0.310 1.037a 0.162Purch 0.5 0.494 0.030 0.687a 0.041 0.5 — — 0.454 0.090Attr 0.5 — — 0.495 0.025 0.5 0.501 0.345 1.128a 0.238

Copula Both 0.5 0.483 0.053 0.700a 0.044 0.5 0.494 0.201 1.037a 0.162Purch 0.5 0.507 0.045 0.687a 0.041 0.5 — — 0.459 0.041Attr 0.5 — — 0.498 0.040 0.5 0.566 0.314 1.128a 0.238

Note. SD, standard deviation.aSubject to endogeneity.

Bachmann, Meierer, and Näf: The Role of Time-Varying Contextual Factors in Latent Attrition ModelsMarketing Science, Articles in Advance, pp. 1–38, © 2021 The Author(s) 13

approach to correct for endogenous contextual factorsfor the model estimation, but no IV is used to predictcustomer behavior during the holdout period. In thesecond setting, we control for endogenous contextualfactors during both model estimation and prediction.In the third setting, we naively use the endogenousfactor to estimate the model and predict customerbehavior, that is, we do not control for endogeneity.The prediction period is two years. We observe thatthe setting that does not control for endogenouscontextual factors outperforms the other two ap-proaches. These findings are in line with those inEbbes et al. (2011). Consistent with these authors, wesuggest that researchers carefully think about theirkey model objective and thus decide whether con-trolling for endogenous contextual factors is advis-able in their specific research context. Although it israrely advisable if the study’s focus is primarilypredictive modeling, controlling for endogeneity is ofutmost importance if the study’s focus is on disen-tangling causal relationships.

4. Empirical AnalysisWe use three real-world data sets from the retailingindustry to test the extended Pareto/NBDmodel. Thefirst data set is from amultichannel catalogmerchant,the second data set is from an electronic retailer, andthe third data set is from a sporting goods retailer. Thefirst two data sets are publicly available.

Although all three datasets are from the retailingindustry, they have distinct characteristics that relateto commonly observed scenarios across various in-dustry groups. First, the nature of available time-varying contextual factors differs across firms. Somefirms can rely on detailed information about contex-tual factors for individual customers. This is not thecase for other firms, which either do not store suchrecords or are not allowed to use them for customerbase analyses, for example, because of data privacyregulations. Second, customer transactions across firmsare characterized by varying interpurchase times. Al-though some firms record multiple transactions forindividual customers eachmonth, the time between thetransactions of individual customers is considerablylonger for other firms. To account for these varyingcharacteristics, we analyze data sets that include threecommonly observed scenarios in this context. The firstdata set corresponds to the scenario where firms have

access to a wide set of contextual factors for each in-dividual and at the aggregate level. Furthermore, thetransactions for customers occur rather frequently. Thesecond data set is widely comparable to the first dataset, but information on contextual factors is limited.This means that information is only available foraggregate-level time varying contextual factors. Ad-ditionally, interpurchase times are longer than those inthe first data set. The third data set again includesinformation on both individual and aggregate-levelcontextual factors and is characterized by longer inter-purchase times. Analyzing multiple datasets facilitatesa more robust discussion of when and how modelingcontextual factors contribute to increasing the pre-dictive accuracy of latent probabilistic customer at-trition models.First, we compare our extended Pareto/NBDmodel,

which includes time-varying and time-invariant con-textual factors, with the standard Pareto/NBDmodel,which does not account for any contextual factors. Wecompare the parameter estimates and the in-sampleperformance of these two models. To evaluate the in-sample performance during the estimation period, weuse the Bayesian information criteria (BIC) and the log-likelihood (LL) values. Because these two models arenested, the parameters and LL values are directlycomparable. Second, for the customer base analysis,we benchmark the out-of-sample predictive perfor-mance at the individual and aggregate level andcompare it with that of the standard Pareto/NBDmodel and four state-of-the-art models. We compareit with that of the pareto/GGG model (Platzer andReutterer 2016), which is the latest published Pareto-typemodel, and the transaction attributemodel (TAM),which was introduced by Braun et al. (2015). More-over, we apply the GPPM, a Bayesian nonparametricframework proposed by Dew and Ansari (2018),which is the latest published non–Pareto-type ap-proach used for customer base analysis. Finally, webenchmark it against the latent attrition model withdirect marketing activities (LAMDMA) proposed bySchweidel and Knox (2013). The parameter estimatesare obtained either by maximum likelihood estima-tion or by using a MCMC-based approach in accor-dance with the original studies. Comparisons aremade for each of the three datasets. To evaluate out-of-sample performance at the individual level, we usethe mean absolute error (MAE) and the correlation

Table 4. Simulation Results for Predictive Accuracy with Endogenous Contextual Factors

Two-year prediction period MAE Standard deviation of MAE

Approach used IV only during estimation 0.347 0.107Approach used IV during estimation and prediction 0.130 0.020Approach did not use IV 0.125 0.010

Bachmann, Meierer, and Näf: The Role of Time-Varying Contextual Factors in Latent Attrition Models14 Marketing Science, Articles in Advance, pp. 1–38, © 2021 The Author(s)

between the predicted and observed number of trans-actions for the individual customers. The MAE is basedon the absolute difference between the predictednumber of transactions and the observed transac-tions up to the specified time point for every cus-tomer. We report the mean of these errors acrossindividual customers. Similarly, the individual-levelcorrelation measures the relationship between thepredicted number of transactions and the observednumber of transactions of individual customers up tothe specified time point. We use the conditional ex-pectation metric. To examine the robustness of ourfindings, we assess the predictive accuracy of themodels for different prediction periods. Furthermore,we compare model performance in terms of identifyingthe future best 10% and 20% of customers (Wübben andWangenheim 2008). We measure MAE at the aggre-gate level for both the predicted and observedweeklycumulative transactions.

4.1. Multichannel Catalog Merchant

The first data set is from a multichannel catalogmerchant. We analyze the purchase history of 1,402customers who made a purchase for the first timebetween January 2005 andMarch 2005. The data set ispublicly available from Marketing EDGE (MarketingEDGE 2013). The customer cohort accounts for 2,929transactions between January 2005 and September2012. A transaction record consists of the purchasedate and customer ID. Table 5 summarizes the keydescriptive statistics. We fit the models based onrepeated transactions during a one-year estimationperiod and examine the predictive performance of allfour models based on different prediction periods.

In the Extended Pareto/NBD model, we considerthree contextual factors: (1) catalog mailings, (2) sea-sonal purchase patterns, and (3) acquisition channels.Although the first two contextual factors are timevarying on a weekly basis, the last is time invariant,that is, does not change over time. Customers receivemultiple catalogs by mail every year, with timingof these mailings differing across customers. Catalogmailings are sent to the customers irrespective of theirprevious purchase histories. We include catalog mail-ings as an individual-level time-varying contextual

factor in the extended Pareto/NBD model. Thevariable is operationalized as a dummy variable. Fur-thermore, like many retailing companies, this multi-channel merchant is subject to seasonal purchase pat-terns. During the Christmas season, the firm observes asignificant increase in purchases, for example. We in-clude the seasonal pattern as a time-varying contextualfactor at the aggregate level, that is, although varyingover time, this contextual factor is the same for all cus-tomers. The information on high season is derived fromhistorical data and expert knowledge. Finally, we dis-tinguish between online and offline customers and in-clude the first-purchase channel for every customer as atime-invariant contextual factor.Our results show that the extended Pareto/NBD

model has a better in-sample fit in terms of the LL andBIC. The parameter estimates andmodel fit are shownin Table 6. The frequency plot of repeat transactionsin Figure 2 indicates a good in-sample fit. Becauseheterogeneity in the data are captured by Gammadistributions, the parameters r and s are direct mea-sures of the extent of heterogeneity in customers’purchase and attrition rates, respectively. The higherthe value of parameter r, the higher the homogene-ity in the purchase process, and the higher the valueof parameter s, the higher the homogeneity in theattrition process (Gupta 1991). Explicitly modelingcontextual factors in the extended Pareto/NBD modelexplains unobserved heterogeneity among customers.In the extended Pareto/NBD,we observe higher valuesfor r and s, indicating more homogeneity among cus-tomers for both processes.The coefficients of the contextual factors may be

directly interpreted as rate elasticity. A 1% change in acontextual factor XP or XA changes the purchase orattrition rates by γpurchX

P or γattrXA%, respectively

(Gupta 1991). Every contextual factor has two coeffi-cients. While the first coefficient represents the influenceon the transaction rate, the second coefficient representsthe effects on the customer’s lifetime. The coefficients ofthe contextual factors suggest that (1) seasonal pat-terns increase purchase levels but do not significantlyaffect customer attrition and (2) the first-purchasechannel does not significantly affect purchase levels,but the customers acquired online churn faster.

Table 5. Descriptive Statistics for the Multichannel Catalog Merchant Data Set

Three-month cohort Estimation period Holdout period Total

Sample size — — 1,402Available timeframe and split 1 year 6.7 years 7.7 yearsAverage number of purchases per customer 1.242 2.682 2.089Standard deviation of repeated purchases 0.619 2.202 2.449Number of purchases 1741 1188 2929Zero repeaters 1156 959 850

Bachmann, Meierer, and Näf: The Role of Time-Varying Contextual Factors in Latent Attrition ModelsMarketing Science, Articles in Advance, pp. 1–38, © 2021 The Author(s) 15

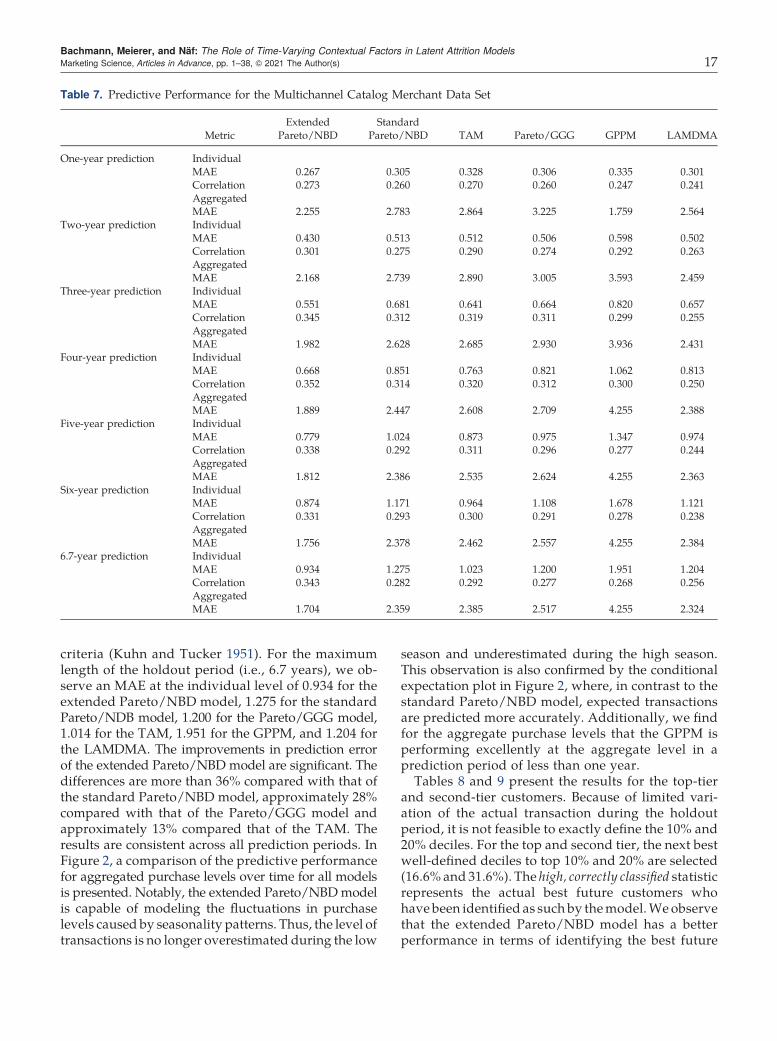

Table 7 compares the aggregate and individual out-of-sample performance of the extended Pareto/NBDmodel with that of the standard Pareto/NBD model,the TAM, the Pareto/GGGmodel, the GPPM, and theLAMDMA based on the future level of transactions

(conditional expectation). The extended Pareto/NBDmodel outperforms all other models at the individ-ual and aggregate level except for the aggregateone-year prediction of the GPPM. The TAM andLAMDMA do not fulfill the Karush-Kuhn-Tucker

Table 6. Parameter Estimates for the Multichannel Catalog Merchant Data Set

Extended Pareto/NBD

Standard Pareto/NBD Description

LL value −2,025.322 −2,056.098BIC 4,123.100 4,141.178r 1.548* 1.137* Homogeneity (purchase process)α 174.482* 108.174** Scale parameter (purchase process)s 0.531 0.181*** Homogeneity (attrition process)β 8.954 0.373 Scale parameter (attrition)γpurch, 1 0.194 — Direct marketing (purchase process)γpurch, 2 0.821*** — Seasonality (purchase process)γpurch, 3 0.210 — Channel (purchase process; online = 1, offline = 0)γattr, 1 −5.131 — Direct marketing (attrition process)γattr, 2 −0.132 — Seasonality (attrition process)γattr, 3 1.907** — Channel (attrition process; online = 1, offline = 0)

*p < 0.05; **p < 0.01; ***p < 0.001.

Figure 2. In- and Out-Sample Performance for the Multichannel Catalog Merchant Data Set

Bachmann, Meierer, and Näf: The Role of Time-Varying Contextual Factors in Latent Attrition Models16 Marketing Science, Articles in Advance, pp. 1–38, © 2021 The Author(s)

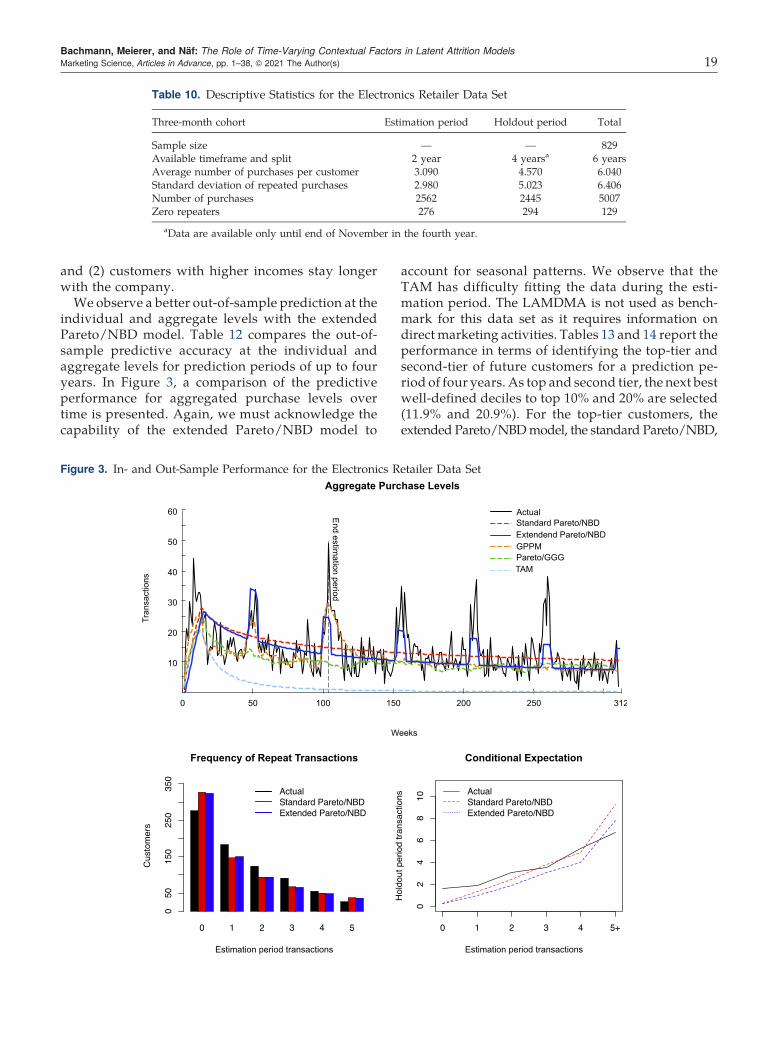

criteria (Kuhn and Tucker 1951). For the maximumlength of the holdout period (i.e., 6.7 years), we ob-serve an MAE at the individual level of 0.934 for theextended Pareto/NBD model, 1.275 for the standardPareto/NDB model, 1.200 for the Pareto/GGG model,1.014 for the TAM, 1.951 for the GPPM, and 1.204 forthe LAMDMA. The improvements in prediction errorof the extended Pareto/NBD model are significant. Thedifferences are more than 36% compared with that ofthe standard Pareto/NBD model, approximately 28%compared with that of the Pareto/GGG model andapproximately 13% compared that of the TAM. Theresults are consistent across all prediction periods. InFigure 2, a comparison of the predictive performancefor aggregated purchase levels over time for all modelsis presented. Notably, the extended Pareto/NBDmodelis capable of modeling the fluctuations in purchaselevels caused by seasonality patterns. Thus, the level oftransactions is no longer overestimated during the low

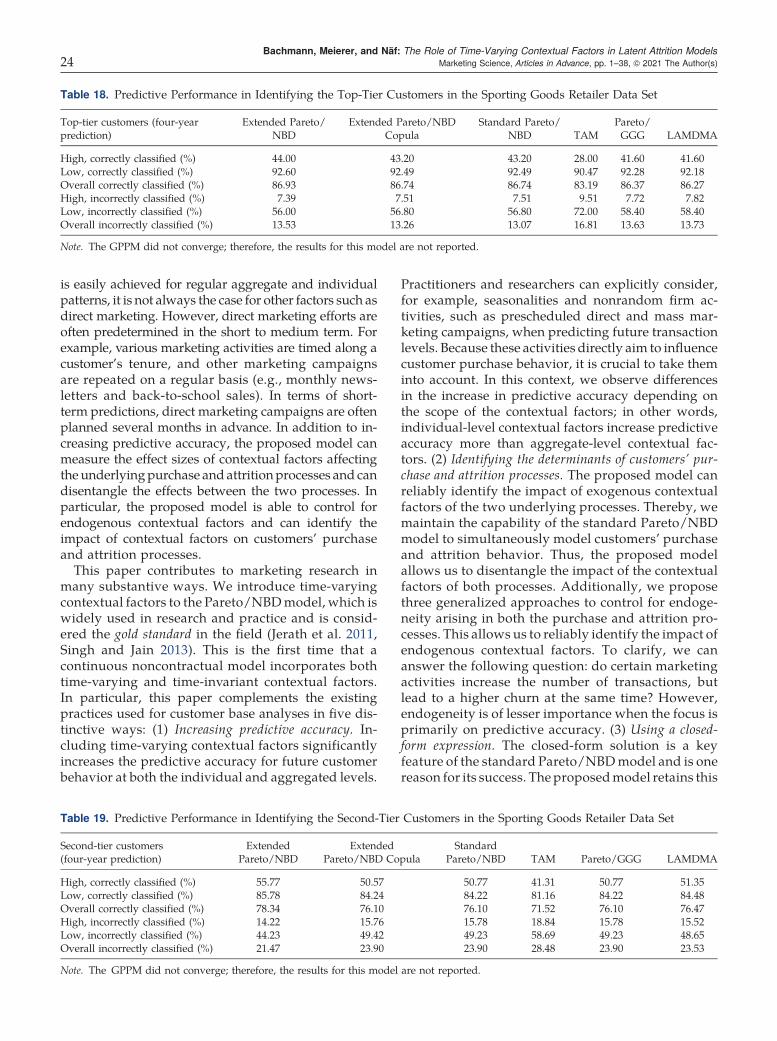

season and underestimated during the high season.This observation is also confirmed by the conditionalexpectation plot in Figure 2, where, in contrast to thestandard Pareto/NBD model, expected transactionsare predicted more accurately. Additionally, we findfor the aggregate purchase levels that the GPPM isperforming excellently at the aggregate level in aprediction period of less than one year.Tables 8 and 9 present the results for the top-tier

and second-tier customers. Because of limited vari-ation of the actual transaction during the holdoutperiod, it is not feasible to exactly define the 10% and20% deciles. For the top and second tier, the next bestwell-defined deciles to top 10% and 20% are selected(16.6% and 31.6%). The high, correctly classified statisticrepresents the actual best future customers whohave been identified as such by themodel.We observethat the extended Pareto/NBD model has a betterperformance in terms of identifying the best future

Table 7. Predictive Performance for the Multichannel Catalog Merchant Data Set

MetricExtended

Pareto/NBDStandard

Pareto/NBD TAM Pareto/GGG GPPM LAMDMA

One-year prediction IndividualMAE 0.267 0.305 0.328 0.306 0.335 0.301Correlation 0.273 0.260 0.270 0.260 0.247 0.241AggregatedMAE 2.255 2.783 2.864 3.225 1.759 2.564

Two-year prediction IndividualMAE 0.430 0.513 0.512 0.506 0.598 0.502Correlation 0.301 0.275 0.290 0.274 0.292 0.263AggregatedMAE 2.168 2.739 2.890 3.005 3.593 2.459