Embed Size (px)

Citation preview

1

"The Remuneration Committee Process – some questions regarding remuneration committee

decision making"

Calvin Jackson+

Brian G M Main*

John Pymm+

and

Vicky Wright+

* University of Edinburgh + Watson Wyatt

5 October 2006

Draft background paper for presentation in the “Corporate Governance at the LSE” seminar series

on 12 October 2006.

2

"The Remuneration Committee Process – some questions regarding remuneration committee

decision making"

Abstract Before 1992, few people knew or cared whether a company determined the pay of its top executives by making use of a board sub-committee known as the remuneration committee. Starting with the Cadbury Committee, however, the subsequent decade saw this organisational arrangement move centre stage in what has become an increasingly heated debate regarding executive pay. While it is true to say that top executive pay remains unregulated in the UK, the same cannot be said for the process by which it is determined. The practices and procedures of the now near universal remuneration committee are carefully prescribed in self-regulating codes and institutional guidelines. This paper examines the available evidence on the functioning of remuneration committees and generates some questions regarding the effectiveness of current remuneration committee processes. The following hypotheses emerge: remuneration committees feel constrained in their choice in terms of remuneration design; they lack the time or resource to calibrate or confirm the effective operation of the chosen remuneration plan; much of their actions are dominated by a perceived need to be able to justify any high pay outcomes in communications with shareholders and institutional investors. We are therefore left with the possibility that the way in which remuneration committees currently conduct their business limits the effectiveness of remuneration policy in UK boardrooms.

3

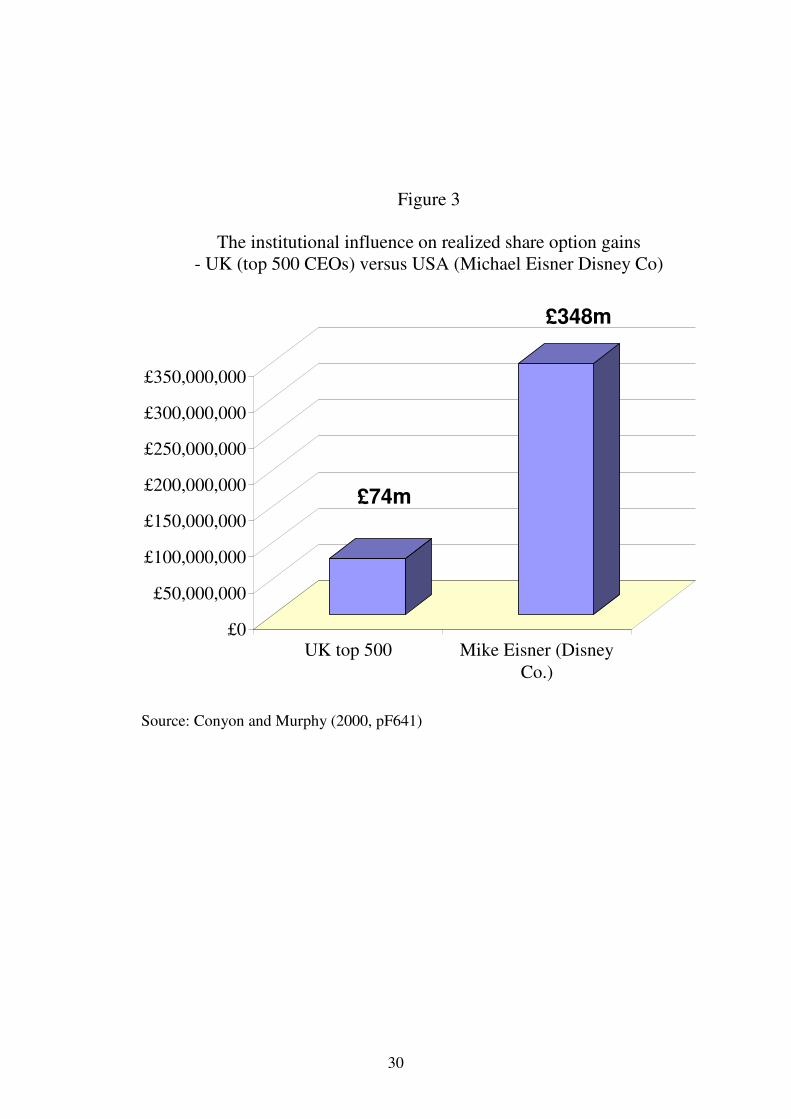

1. Introduction This paper sets out to make three basic points. The first of these is that over recent years what is expected of remuneration committees has changed markedly. The second is that some of the ways in which expectations have changed have attracted less attention than others in evolving remuneration committee practice. Finally, the third and most contentious point is that current practice may not be sufficient to meet fully the changed expectations regarding remuneration committee function. In the following discussion, extensive use is made of what has been a recent upsurge in research on the topic of remuneration committees and, because of what shall be argued to be the very strong institutional influence in this area, most of the discussion focuses on UK experience and practice. We also draw on a series of interviews recently conducted with members of remuneration committees in large UK companies. Responses gathered during these interviews are used to test our hypothesis that current remuneration committee practice has some way yet to evolve if it is to live up to expectations. The time period under discussion extends back only as far as the early 1990s. While companies, of necessity, always had a mechanism by which the remuneration of senior executives could be set and adjusted, the arrangement that is now identified with the remuneration committee did not appear in popular discussion until that time. The work of the Cadbury Committee (1992) created the first exposure of the arrangement in policy circles and interest has waxed and waned ever since – mostly reflecting subsequent governance reports (Greenbury, 1995; Hampel, 1998; and Higgs, 2003). The chart in Figure 1 is based on the number of articles concerning remuneration committees that appeared in the Financial Times each year over the period 1980-2006 and serves to make this point. The series of reports mentioned above define the emergence of what has come to be seen as the British ‘Comply or Explain’ approach to governance, set out in various versions of the ‘Combined Code’ (1998, 2003, 2006). A moment perusing Figure 2 confirms the extent to which things have changed since the early 1990s. Then, only a minority of companies published membership of their remuneration committee and, among those who did, it was common for CEOs and other executives to serve as full members. This is in stark contrast with the current situation where detailed membership, meeting frequency and attendance are published and the all-independent-director remuneration committee is essentially universal. This impetus to change was further bolstered by the activity of other institutions, such as the Association of British Insurers (ABI). These innovations will be discussed in some detail below but it is useful, at this point, to underline the extent to which they have impacted on the way in which directors’ remuneration is determined in the UK. One simple comparative statistic, taken from Conyon and Murphy (2000, p640), serves to make the point. For the year ending in 1997 the CEOs of the 500 largest companies in the UK realised share option gains that totalled £74million (or around £148k each). At the end of that same year in the USA, Michael Eisner, CEO at Disney

4

Company, personally exercised options that realized £348million. Figure 3 portrays the enormous difference here. While one can argue that Eisner had completed a remarkable period of performance at Disney and that these option gains should be considered over a longer period than simply one year, these numbers serve to underline the major difference between the UK and the USA in executive remuneration practice - the tendency to lump the two countries’ governance practices under the common label of the ‘Anglo-American’ model may make sense in terms of capital markets (the market for corporate control) but is inappropriate in terms of executive remuneration. Nor is this a matter of time having stood still in the UK. This paper will argue that there had been truly radical changes in practice in the UK, but that these changes reflected a very different institutional setting. The next section of the paper, spells out some of the changes that took place post-Cadbury to the (self-)regulatory environment in which directors’ remuneration is determined in the UK. This is followed, in section 3, by a discussion of the available theoretical explanations of how remuneration committees will conduct themselves as they attempt to comply with the various strictures of this new environment. Then, in section 4, there is a somewhat critical analysis of the extent to which current practice is really living up to expectations. This draws on recent interview evidence collected by the authors from remuneration committee members. The concluding section of the paper offers some thoughts as to how things might be changed to bring a closer alignment between expectations and outcomes. 2. Raised expectations This section tracks the increasing level of institutional involvement over recent years in the setting of executive remuneration in the UK. Readers familiar with this story may prefer to skip directly to section 3. Difficult as it may be to believe today, there was a time when public companies were basically allowed to set the pay of their senior executives with little fuss or attention. Following the passage of the 1967 Companies Act it was necessary to disclose the pay (‘emoluments’1) of the Chairman and of the (unnamed) Highest Paid Director in each company’s Annual Report, along with the pay of other executives – suitably presented in £5,000 bands. But when, following on from the collapse of some major companies, the Cadbury Committee (1992) was set up to consider governance practices in British boardrooms, it found itself addressing, among other things, the question of executive pay determination. This led to the first recommendations regarding the establishment and operation of remuneration committees2.

1 ‘Emoluments’ essentially being base plus bonus and the cash-equivalent of perquisites received. 2 Braiotta and Somner (1987) note that by 1985 in the USA 86% of top 1000 companies had compensation Committees and of these 70% comprised outside directors only. Cadbury’s (1992) recommendations for the UK essentially reflected those of the Institutional Shareholders' Committee (1991).

5

By this time, directors’ pay had been moving to move vigorously ahead reflecting the buoyant economic conditions of the period and the fact that after 1979 pay determination had been freed of the restraint imposed by decades of intermittent incomes policies. Directors’ remuneration had become a headline issue and the sense was that Cadbury had not gone quite far enough in terms of accountability or transparency. Consequently, the Greenbury Committee (1995) was created specifically to address directors’ pay determination. This was followed by the Hampel Committee (1998) which was tasked with pulling together the recommendations of the two previous committees into some unified whole and duly resulted in the Combined Code on Corporate Governance (1998). To a large extent, these developments resulted in the structure of the remuneration committee that exists today. But all this had brought the role of the ‘non-executive’ director into the spotlight and the Higgs Committee (2003) was called upon to address the concept and conduct of outside directors, leading to some important clarifications in terms of ‘independence’ and in the role of the Chairman. The Combined Code on Corporate Governance (2003, 2006) was modified to take these recommendations into account3. The upshot of these 14 years of corporate governance innovation is a code requirement on FTSE350 companies that the remuneration committee should comprise at least three members, all of whom should be independent non-executive directors. Its responsibilities extend to executives below board level. In formulating remuneration packages, it should aim to attract, retain and motivate executive directors of the quality required, and, in so doing, should take account of relative performance. Charged with agreeing with the board a framework for executive remuneration, the remuneration committee is simultaneously encouraged to consult the chairman and/or chief executive about their proposals relating to the remuneration of other executive directors and enjoined to ensure that no director should be involved in any decisions as to their own remuneration. These are the changes in expectations that are widely acknowledged and, with rare exception, honoured by remuneration committees in their current practice. All of these Code requirements operate under the condition (for listing on the London Stock Market) that a company either comply with the code or explain why they are not so doing. This is a very different approach from that in the USA with its legally backed strictures of the Securities and Exchange Commission (SEC, 1993, 2006) and mandatory conditions for listing on the NYSE (2004) or NASDAQ (2004). Only in terms of disclosure has any statutory intervention been made in the UK, and this in the form of the Directors Remuneration Report Regulations (2002), which require detailed reporting of directors’ remuneration at a level of detail consistent with the Combined Code.

3 In the 2006 revision, the Chairman is now permitted to serve as a member (but not chair) of the remuneration committee. The Chairman of the board has always been expected to ensure that the company maintains contact as required with its principal shareholders about remuneration, although it is, of course, the Chair of the remuneration committee who is accountable to shareholders at the AGM for remuneration policy.

6

But what truly distinguishes UK arrangement from those in the USA is the way that British institutional investors4 have been prepared to set about influencing the conduct (as opposed to the structure) of the remuneration committee. While UK institutional investors always took an interest in governance matters, it was the 1984 Finance Act that led them to exert an increasingly dominant influence. As part of the 1984 Budget, what was then a major tax concession was granted in the form of approved executive share options. Approved schemes allowed gains to be taxed as capital gains rather than income (a difference of 30% versus 60% marginal tax). The prospect of equity dilution caused the institutions (and, in particular, the ABI and the NAPF) to issue guidance as to how such schemes should be administered. There is a debate as to whether these Guidelines have, over the years, set expectations among institutional investors or have merely reflected and codified the emerging expectations among institutions as to what remuneration committee should be doing. The distinction is unimportant for the purposes of this paper, the key point being that such Guidelines provide a record of just what expectations were at any time. At the outset, these ‘Guidelines’ (for example, see ABI, 1987) were essentially concerned with regulating the uptake of share-based incentive schemes and imposing (initially) modest performance requirements. Most famously, the four-time-emoluments rule restricted the holdings of share options by any executive at any time to having a face value of four times that person’s current emoluments. This reflected the provisions of the 1984 Finance Act5. Although, under exceptional conditions, higher levels of award were possible6, the four-times-emoluments guideline quickly became the standard applied in UK Boardrooms. This remained true even after the 1988 Budget when income and capital gains tax rates were harmonized (with a top rate of 40%). It is possible to trace out the gradual emergence of the ABI Guidelines as a dominant influence in the way remuneration committees designed executive reward over the period (see Main, 1999, 2006). However, in July 1999, the ABI (1999) issued a markedly different set of Guidelines which moved away from the four-times-emoluments approach that had characterised much of the preceding period. In part, this was in recognition of the move away from executive share options towards performance share plans, as encouraged by Greenbury (1995). There was a marked increase in the discretion allowed to the remuneration committee but in return there was a firmer steer as to how remuneration committees should construct the overall remuneration package. Examples of the ways in which the text of the ABI Guidelines changes over these years are provided in Appendix A. It can clearly be seen that bit by bit the remuneration committee is asked to take increasing responsibility for ensuring that the

4 Identified for these purposes by Charkham and Simpson (1999, p166) as: the National Association of Pension Funds (NAPF): the Association of British Insurers (ABI); the Association of Unit Trusts and Investment Funds (AUITF); the Association of Investment Trust Companies (AITC); and the Institutional Fund Managers Association (IFMA). 5 Where the Inland revenue displayed a related concern of limiting the tax-expenditure consequences of such a concession. 6 The so-called ‘super-options’ which demanded a 5-year holding period and upper quartile FTSE100 standard of eps performance for vesting.

7

executive reward structure is aligned with the overall business strategy of the company. Thus, performance metrics in the pay-for-performance relationship should be chosen to align with the company’s key success indicators. The calibration of reward to such metrics should be such as to mark the relative importance of these performance indicators. Not only is this choice and calibration by the remuneration committee to be judged in the light of the company’s business strategy but choices are to be re-visited in order to confirm that the original choices are continuing to deliver in a way that is consonant with the company’s contemporaneous situation. This presses the remuneration committee to keep in view previously granted incentive schemes and there is an emphasis here on the remuneration committee exercising its discretion. There is an important shift that takes place here. Whereas remuneration committees were once merely seen as an arms-length administrative device to ensure an acceptable degree of probity in the setting of executive reward, things have now changes substantially. Remuneration committees are now seen as key agents in the process of choosing a remuneration package, ensuring that it is calibrated in a way that ensures the incentives faced by the executive directors are such as to incentivise the executive towards those decisions and actions necessary to best deliver the company’s chosen strategy. In so doing, there is also an expectation that the remuneration committee will periodically confirm that the extant bonus schemes, performance share plans, and share options are in reality behaving in accord to the company’s current needs. On top of all of this, of course, there is a requirement that the remuneration committee communicate effectively to the shareholders with regard to all the above. This is a big ‘ask’, and it is our hypothesis that current remuneration committee practice is not sufficient to deliver on these particular expectations. But, before turning to examine how remuneration committees are conducting their business so as to deliver on these expectations, the next section first reviews some theory as to what remuneration committees can be thought to do. 3. What Remuneration Committees are thought to do. The discussion above of the expectations placed on the remuneration committee by shareholders and other bodies suggests that one of its important roles is to craft remuneration packages that effect an alignment between the interests of the shareholders and those of the executive directors. This particular expectation goes significantly beyond the original quasi-audit role of being the arbiter on a benchmarking exercise or the regulator in administrating share option schemes. While none of these important monitoring functions has been diluted, there is now an overlaying strategic role that calls for a significantly heightened level of expertise and commitment of time. Before looking at the evidence on how remuneration committees currently conduct their business, this section reviews what management theory tells us about the nature of the process in which remuneration committees are engaged.

8

Direct supervision, in the conventional management sense, is difficult at the top of a company, owing to the informational disadvantage under which even the most diligent non-executive director labours. Such situations have been characterised as beset by Simon’s (1947) bounded rationality or by Akerlof’s (1972) asymmetric information. Add to this the further complication of Williamson’s (1985) ‘opportunism’ by the self-seeking agents7 (the executive directors, in this case) and the control problem becomes challenging. Jensen and Meckling (1976) suggest that in such circumstances reward mechanisms can align the otherwise potentially disparate interests of the executive directors (agents) and the shareholders (principals). In principal-agent theory, the challenge in designing a remuneration contract is to arrange the best incentive effect (‘pay for performance’) subject to a ‘participation constraint’ that requires that the expected reward from the employment be at least as good as is available elsewhere. One complicating factor is that risk aversion on the part of the employee means that placing a certain amount of ‘pay at risk’, in the form of pay for performance, will need to be compensated for through a higher actuarial payout of the remuneration package. The skill of the remuneration committee, therefore, lies in ‘negotiating’ with the executives the most cost-effective alignment of interests. Even at its best, however, it will never be costless and it will never be perfect. Gibbons (2005) explains how performance measurement issues further complicate matters by being difficult to quantify but that considerations of ‘career concerns8’ can address some of these issues. An important point remains, and it is one often overlooked in the focus on ‘pay for performance’, namely that the remuneration package must be expected to pay out a competitive reward. Otherwise, either the employee is the wrong person for the job, or the remuneration package is ‘broken’, i.e., poorly designed and not fit for purpose. Empirical studies of how well the principal-agent view captures what remuneration committees are doing in setting executive pay have tended to focus on the strength of the pay-performance relationship (i.e., how much better off is the CEO, say, for every extra £1,000 of shareholder value created). Initial empirical estimates were disappointing (Jensen and Murphy, 1990) but later results were somewhat more encouraging (Hall and Liebman, 1998; Core and Larcker, 1999) although far from fully convincing. More direct studies of the impact of remuneration committees on the level of CEO pay have been even more ambiguous, with Main and Johnson (1993) suggesting that the reported presence of a remuneration committee was actually associated with higher levels of pay award. Further studies along these lines recorded mixed results9. A robustly alternative view of the executive remuneration process has recently been promulgated by Bebchuk and Fried (2004). This sees the executives conniving with the non-executives (through the remuneration committee) to extract the largest amount of reward possible subject to the constraint of ‘social outrage costs’ (shareholder and public disquiet at particularly egregious self-dealing). From this

7 Williamson defines ‘opportunism’ as self-seeking with guile. 8 Career concerns include prospects of promotion within the firm, moves to jobs in other firms, the prospect of being sacked and so on. 9 For Europe see: Conyon, 1997; Conyon and Peck, 1998; Peck and Ruigrok, 2002. For the USA see: Daily, Johnson, Ellstrand, and Dalton, 1998; Newman and Mozes, 1999; Anderson and Bisjak, 2003; Vafeas, 2003; Chhaochharia and Grinstead, 2006.

9

perspective, payment devices such as executive share options, performance shares, pensions, corporate perquisites are seen as ‘stealth wealth’, whereby the executive extracts as much personal remuneration as possible out of the company’s available rents10. Importantly, this is seen to be accomplished with the connivance of remuneration committee directors who are portrayed as variously setting ‘soft’ performance targets or waiving through replacement options for those under water, and so on. The view is not new and represents an extreme form of the managerial power perspective, pithily summarized by John Kenneth Galbraith (1974, p79):

‘The salary of the chief executive of the large corporation is not a market reward for achievement. It is frequently in the nature of a warm personal gesture by the individual to himself.’

The Bebchuk and Fried (2004) critique has been roundly rejected by supporters of principal agent theory11 but, in truth, the existence of social influence within the boardroom has long been documented as an empirically significant effect in the remuneration committee’s determination of executive reward. It is generally not portrayed as tantamount to theft, but rather as the unavoidable outcome of human agents working together in the social construct known as the unitary board. In such circumstances, it is difficult for effects such as social influence and reciprocity not to have an empirical impact on remuneration decisions. In an early paper in the area, O'Reilly, Main and Crystal (1988) noted that the level of their pay in their own job affected the generosity of remuneration awarded by those remuneration committee members to the focal CEO. Main, O'Reilly and Wade (1995) extend these findings to document the influence on CEO remuneration of whether outside directors were appointed after the focal CEO (reciprocity) or are close in age to the CEO (similarity). In an impressive series of studies12, Westphal and Zajac (1994) confirm that there are indeed forces of influence and reciprocity at work within the boardroom. They specifically identify ingratiation, persuasion, friendship ties, similarity, and reciprocity as playing a significant role13. The idea is that, in a unitary board structure, decision making will be subject to social psychological forces that result in executive reward outcomes that are different (in terms of level of award, composition of award, pay-performance sensitivity, golden-parachute provisions, continuing employment, provision of perquisites, and post-retirement benefits) than might be suggested by a more clinical examination of the situation from a principal agent perspective. Importantly, these authors do not portray such influence effects as indicators of failure in the pay determination process. They highlight the tension that exists within a

10 Rents here in the economic sense of payments over and above what is currently needed to hold in place the factors of production. Bebchuk and Fried see executive pay is part of the problem (rent extraction) rather than as the remedy to it, as proposed by principal agent theorists. 11 See: Murphy, 2002; Core, Guay and Thomas, 2005; Holmstrom, 2005; Conyon, 2006. 12 See, for example: Westphal and Zajac, 1994, 1995, 1996; but also: Zajac and Westphal, 1995, 1996; Wade, O’Reilly and Chandratat, 1990; Wade, Porac and Pollock, 1997; Porac, Wade and Pollock, 1999; Westphal, 1999; and O’Reilly and Main, 2006. 13 These results are, to some extent, echoed in Jensen, Murphy and Wruck (2004: 10) who when talking about outside CEOs serving as NEDs point out that: ‘it is natural for them to subconsciously (if not consciously) view the board through CEO eyes’. But the results of Westphal and Zajac and others go beyond any mere ‘empathy’ to the more powerful and extensive effects of reciprocity and social influence.

10

unitary board between the twin roles of the outside director of providing ‘advice and counsel’ on one hand, and effective ‘monitoring’ on the other14. As Holmstrom (2005, p705) notes: ‘[Directors] are faced with a complex and difficult set of tasks that partly are in conflict with each other …..’ . In such a world, contracts are, by necessity, incomplete. And it is the glue of social influence that holds such incomplete contracts together. The idea is that for the executive team (and the CEO in particular) to be open to receiving advice and counsel from the outside directors then it helps if there are cordial social relations among the parties. An excess of such could clearly be regarded as ‘clubbishness’ but, at the other extreme, a complete emphasis on the monitoring role can easily degenerate to ‘strife and division’ within the boardroom15. Overarching all considerations of agency theory, managerial power and social influence there are strong institutional pressures which come to bear on the remuneration committee’s decision making. It is, indeed, difficult to examine the process of determining executive reward in large companies without being aware of strong institutional forces at work. The pervading ethos is one of ‘comply or explain’, and yet, in the overwhelming majority of cases, companies simply comply. This outcome can be taken as an example of the type of mimetic process that neo-institutionalists16 (DiMaggio and Powell, 1983; Scott, 1995) see as leading to an isomorphism in organizational practice. Faced with the uncertainty of public reaction, and seeking legitimacy, companies move to a uniformity of practice. With this strong drive to isomorphism, remuneration committees are guided by what other executives are being paid (O’Reilly et al., 1988), or at behaviour among cohesive groups of peer companies (Porac et al., 1999), or at the more general ‘going rate’ at other companies (Ezzamel and Watson, 1998). In the case of the UK, which enjoys what is generally accepted to be a self-regulatory environment, companies follow a near identical process of remitting the pay decision to a remuneration committee comprising independent directors. This committee is free to (and generally does) take independent advice from a remuneration consultant. A remuneration committee report explaining the logic behind the pay awards appears in the company’s annual report to be defended and voted upon at the AGM. There are marked movements towards certain aspects of remuneration design – adoption of options or Ltips, deployment of performance criteria - first absolute and then relative but generally based on total shareholder return, eps or one of a few other metrics. These are all consistent with of DiMaggio and Powell’s (1993) isomorphism of organisational practice. The following section of the paper scrutinises current day practice in UK remuneration committees and, bearing in mind the theoretical models introduced above, examines how effectively remuneration committees are delivering the expectations placed upon them.

14 The Hampel Report (1998, 3.7) expressed concern regarding an overemphasis on the monitoring role of non-executives which had emerged in Cadbury (1992) and Greenbury (1995). 15 In its 16th September 2006 discussion of recent developments within the Hewlett-Packard boardroom, the Economist used precisely this distinction of ‘clubbishness’ versus ‘strife and division’. 16 Scott (1995, p33) defines institutions as “cognitive, normative, and regulative structures and activities that provide stability and meaning to social behavior. Institutions are transported by various carriers – cultures, structures, and routines – and they operate at multiple levels of jurisdiction.”

11

4. Gaps between outcomes and expectations Pettigrew and McNulty (1995) observe that because much discussion of corporate governance in the UK has focused on rules, regulations and structures (all easily observable) it has overlooked the important reality of boardroom power and influence without which it is difficult to comprehend boardroom dynamics and director effectiveness. Recent interview-based studies of boardroom processes have set out to remedy this shortcoming. Although much of this work has addressed issues concerning the entire board17, rather than the specific board sub-committee that is the remuneration committee, there have been a handful of studies examining remuneration committees. This section reviews these studies with an eye to formulating some testable hypotheses regarding the remuneration committee process. In an early effort in this field, Main (1993) conducted interviews on the director remuneration process at 24 large UK companies18. It is a revealing indication as to the extent to which perspectives have changed that all of these interviews were with executives. The general finding of these interviews was that companies, faced with mounting disquiet regarding directors’ pay awards, lacking any alternative consensus on practice and uncertain about what choices to make, were generally more than willing to comply with accepted codes of practice. In 1999, Conyon et al. (2000) interviewed directors at eight UK companies19. The main conclusion drawn from the interview data was that it revealed an emerging international perspective in choosing pay levels, in that executives were increasingly being regarded in the context of a global market for executive talent. More recently, Stiles and Taylor (2000) focused their 51 main-board director interviews20 on the wide spectrum of board work. Interviewee comment (p76) was used to cast doubt on the strength of pay as a motivating factor among executives, other than as a symbolic reward to individuals who were seen as essentially intrinsically motivated21. Three major roles for the board were identified as: strategic; control; and institutional. Remuneration committees were seen as playing a control role, the current appropriateness of which our analysis here will call into question. Looking specifically at remuneration committees, the interviews22 discussed in Spira and Bender23 (2004) bring out clearly the tension that exists within the remuneration committee between ‘Performance’ on the one hand (achieving an effective principal

17 For example: Pettigrew (1992) Pettigrew and McNulty (1995), Pye (2002), Pye and Pettigrew (2005), Stiles and Taylor (2000); or leading from the Higgs review: Roberts, McNulty, and Stiles (2005) and McNulty, Roberts, and Stiles (2005). 18 Interviews were conducted between October 1992 and April 1993 19 The eight companies were top 250 FTSE companies and they interviewed six non-executive directors and two human resource directors. 20 Interviews covered: 11 CEOs; 16 Chairmen; 13 executive directors; 11 non-executive directors. 21 See Layard (2005) for a recent general introduction to intrinsic motivation. 22 The Bender project interviewed [December 2001-May 2003] some 35 people involved in the executive reward process: 20 board directors, 3 company secretaries, and 12 HR professionals at 12 companies – including nine FTSE100. 23 See also: Bender and Moir (2005) and Bender (2003, 2004).

12

agent-type pay mechanism thereby strategically aligning incentives) and what they label ‘Conformance’ on the other. With ‘Conformance’ the emphasis is very much on being able to demonstrate in an ex-post sense that pay awards conform with the various governance codes reviewed above in section 2, i.e. monitoring. The authors present a useful diagrammatic representation of this which is reproduced in slightly modified form in Figure 4. The ‘Performance’ ‘Conformance’ distinction echoes the observation with which Hampel (1998, para 1.1) opens his report, namely that effective governance makes a contribution both in terms of ‘accountability’ but also in terms of ‘business prosperity’, and that a preoccupation with the former can be to the detriment of the latter. The Spira and Bender (2004) research aimed at distinguishing the work of the audit committee from that of the remuneration committee. There are, indeed, many similarities. But it can be argued that the conformance dimension looms larger in the work of the audit committee. In terms of performance, the remuneration committee performs a key role in the strategic human resource management of the company by crafting the incentive mechanisms that attempt to link the incentives of the top management team with the key success factors for corporate strategic success. There is a clear tension between the conformance and the performance roles. In a series of interviews24 with remuneration committees of water companies, Ogden and Watson (2004, 2006) conclude that remuneration committees feel highly constrained by political considerations. Although there seemed to be active involvement on the part of CEOs in formulating both financial and non-financial targets, the decision process was seen as beset by difficulties in formulating performance measures – for example, concerning which were the appropriate comparator companies to utilise. These perceived constraints on the part of the remuneration committee were felt to have led to some issues of competitiveness of remuneration and to recruitment difficulties. The underpayment issue was corroborated in Ogden and Watson’s (2004) statistical analysis, which contradicts Porac et al. (1999) who found that remuneration committees in the USA selected comparator groups in a self-serving manner. To the contrary, Ogden and Watson (2004) suggest that the remuneration committees were more concerned with the ‘conformance’ column of Figure 4, where uncertainty regarding public reaction led them to seek legitimacy through uniformity of practice. Institutional pressures are seen to result in DiMaggio and Powell’s (1983) isomorphism in organizational practice. Taking these findings together leads to our first hypothesis:

Hypothesis 1: Remuneration committee choices are being made with an eye to conforming.

Looking into the detailed mechanics of the design of the reward package, Perkins and Hendry (2005) made an explicit attempt to examine the extent to which the remuneration committee really adheres to the principal-agent vision of designing a 24 Ogden and Watson (2004) focused on five water companies, covering some 25 individuals including members of remuneration committees, CEOs and senior HR professionals servicing the remuneration committee.

13

remuneration package that provides incentives calibrated in the light of what labour market forces indicate. They interviewed seven people who, between them, had sat on 20 remuneration committees25. An important conclusion of this work is the recognition of the wide range of discretion afforded the remuneration committee in its deliberations (“space for interpretation”, p1446) and that “what matters is how rewards appear, not whether performance is being objectively over-valued” (p1464). The result is that “Ordering top pay may then prove to be contingent more on ‘communication’ than performance management considerations.” (p1464). Again, the dimension of conformance dominates performance considerations. But remuneration committee members also expressed frustration at the difficulty they confronted in ‘validating’ (Perkins and Hendry, 2005, p1457) the pay-performance relationship set in place, e.g., in terms of the appropriateness of the chosen comparator companies. We shall refer to this as the calibration process and, in a world of fast changing and noisy data, it presents the committee with a serious challenge but one that must be confronted if the tasks on the right hand column of Figure 4 are to be accomplished. Perkins and Hendry (2005, p1462) found that remuneration committees reached for ‘consultancy packaged benchmarks’ in an attempt to satisfy the twin tensions of external transparency/accountability and internal strategic human resource considerations. Conyon, Peck and Sadler (2006) attribute a significant upward lift in CEO pay (broadly defined to include share-based remuneration) to this reliance on and influence of remuneration consultants, which they explain by a combination of managerial power and social comparison theory26. Perkins and Hendry conclude that the principal-agent perspective provides a wholly distorted vision of what actually occurs in remuneration committees and boardrooms. They emphasise the empirical impact of wider social processes on the decisions of the remuneration committee and reject the view that remuneration packages are precisely calibrated to reflect labour market conditions. From this we can hypothesise:

Hypothesis 2: Social process considerations militate against remuneration committees allocating sufficient time and attention to the calibration of company and personal performance metrics to director reward.

The emphasis on the social and political processes surrounding the remuneration committee is also echoed in the work of Lincoln et al. (2006) who focused27 on some 25 Five search consultants were also interviewed in the Perkins and Hendry (2005) study. In terms of methodology, Perkins and Hendry (2005) and Lincoln (2006, discussed below) relied on note taking during interviews and subsequent transcription of these notes. Bender and Spira (2004) and Ogden and Watson (2004) used semi-structured interviews which they taped and transcribed. 26 Managerial power because the uplift in pay is greater when the remuneration consultant in question supplies other services to the firm and social influence because pay of the focal CEO is higher when the pay of other CEO’s advised by that remuneration consultant is higher. 27 Lincoln et al. (2006), a ‘Parc’ study, involved conversations with 28 people, including Remco members and HR executives from 19 large companies (FTSE20 or US-listed). Remuneration

14

of the more practical aspects of the remuneration committee’s operation. In particular, they suggest that in the allocation of boardroom talent, recruitment to the remuneration committee is not the highest priority28. However, examination by the authors of the demographic characteristics of the membership of FTSE100 remuneration committees as compared to the board or to the audit committee, does not offer any ready proof of this claim, as Figures 5 through 10 demonstrate, although this is a very crude level of measurement. But Lincoln et al. (2006) also highlight the attention (in both time allocated and effort expended) given over to the pay for performance relationship. This is what we term the calibration and confirming stage of remuneration design. It requires detailed scrutiny (and re-scrutiny) of the performance of the company and the performance of the executives29. Rather than probe deeply on this issue, it is easy for a remuneration committee to fall back on an isomorphism of organisational practice and do what everyone else is doing – for example, by setting relative tsr targets on the vesting of options or performance shares, deferring STI bonus payments into unvested equity, and so on30. While the award of any package may be tested against ‘overpayment’ to minimise the risk of incurring outrage costs, the time and resource may not be available to allow a rigorous investigation of just which performance targets best ‘fit’ the company’s overall corporate strategy or reflect the existing tranches of options, performance shares, unvested bonus payments and accrued pension entitlement already awarded to the executive in question. Lincoln et al. (2006) offer Figure 11 to describe the difficulty confronting the remuneration committee concerned with the conformance versus monitoring dilemma. In two of the four cells the pay outcome is unambiguous, wholly good performance should be rewarded and wholly poor performance should not be. The institutional pressure to avoid ‘rewarding failure’ may place pressure on remuneration committees to pay little on the off-diagonals. That said, when there is relative performance but low absolute performance - the company has done badly but not nearly as badly as the comparator group – the new emphasis on relative performance will produce a payout (albeit a modest one, in terms of shares at depressed prices). But when there is high absolute performance but low relative performance - the company has done well but not as well as the comparator group – how much payment is called for? Principal agent theory would suggest a low payout, but this does not allow for the very bounded rationality and imperfect information that it seeks to consultants, academics, search consultants and representatives of the ABI and NAPF comprised the others. 28 Lincoln et al. (2006, p16) extend this observation beyond mere selection for committee service to a lack of induction or development training received for this function. 29 One extension of this analysis is into an evaluation of how the remuneration committee actually dispatches its duties or fulfils its terms of reference. This is thoughtfully examined in Likierman (2006). 30 Greenbury (1995) declared that on performance share plans – “..schemes along these lines may be as effective, or more so, than improved share option schemes in linking rewards to performance” and from literally nowhere the use of performance share plans in the FTSE100 had risen to 84% by 2005. The same report also declared that “Consideration should be given to criteria which reflect the company’s performance relative to a group of comparator companies in some key variables such as shareholder return (TSR)”, and by 2005 some 86% in of performance share plans used relative TSR. See Booker and Wright (2006)

15

confront. Such outcomes may be due to poorly chosen comparator groups, performance metrics, or performance hurdles. Equally unexpected changes in the company’s environment can lead to such outcomes. The key question is whether, mindful of the participation constraint introduced above, the remuneration committee is prepared to exercise discretion in adjusting the payout of the incentive schemes, a discretion it almost always possess. Such situations do not generally arise overnight and careful confirmation and re-calibration by the remuneration committee can minimise the danger of ending up with the wrong pay-out for the situation. This willingness on the part of the remuneration committee to confirm the efficacy of the chosen reward mechanisms is of critical importance in the dynamics of executive reward31. Key to this view is the notion that companies regularly confirm that the reward mechanisms in place are performing as required. This leads to our third hypothesis:

Hypothesis 3: Remuneration committees find it difficult to confirm their current choice of reward strategy by re-visiting existing components of long-term incentive before their vesting date.

An additional and potentially time consuming activity for the remuneration committee is the tailoring of a remuneration award for each executive. The granting of short-term and long-term incentive plans that encompass all executives (with possible variations for the CEO) scores high on grounds of procedural equity. But neither in terms of equity of outcome nor in terms of efficiency of incentive does it make much sense when executives on the same board vary so radically in circumstances, either in age, stage of career, accumulated pension, holdings of amounts of extant unvested share plans and options etc. Core et al. (2005. p1169) labels the distinction one between ‘Pay Incentives’ and ‘Portfolio Incentives’ and Main, Buck and Bruce (1996) use data from the Register of Directors’ Interests to illustrate the empirical significance of the latter. In a similar way, a plan that was suitable for an executive one year might no longer fit the bill a year or so later. Thus constant re-visiting of the executive’s portfolio of incentives and a willingness to personalise each executive’s incentives is necessary part of the role of any remuneration committee striving to effect the elusive pay-for-performance remuneration construct. But the overwhelming evidence from the interview studies discussed above is that remuneration committees see such personalised or individualised contracting to be overly complex and difficult to communicate. There is a strong drive to setting in place transparent and easily communicated remuneration arrangements. These have a great many of their structural details approved by shareholders and what discretion remains to the remuneration committee is seldom utilised.

31 This movement back to the optimum pay-performance sensitivity that lies at the heart of principal-agent theory is, according to Core and Larcker (2002), the only insight into the causal connection between pay and performance. Key to this view is the notion that companies regularly confirm that the reward mechanisms in place are performing as required.

16

So while remuneration committees have seen their roles shift from one of a quasi-audit role as an arbiter of benchmarking exercises to being charged with aligning remuneration policy with business strategy of the company, it is less clear that practice has evolved to accommodate this change. As external scrutiny of the outcome of remuneration committee decisions has heightened, so the need to be able to justify awards ex-post has become more of an urgent consideration if the ‘outrage costs’ levied by stakeholders and outside observers are to be avoided. This adds to the tension in unitary boards between the monitoring function and the advice and counsel function of outside directors.

Hypothesis 4: There is a heightened sensitivity felt by remuneration committees in terms of their communications with shareholders and executives alike. The priority placed on avoiding disapproval displaces meaningful analysis or exchange of views.

These four hypotheses form the backbone of an interview study currently being conducted by the authors. The results of this study will be reported in a separate paper to follow. The final section of this paper concludes by offering a summary of what the above review of the literature has established. 5. Conclusion and policy discussion The changes in the corporate governance environment since Cadbury (1992) have led to increased expectations regarding how remuneration committees should operate. Some of these expectations refer to structure and have, by and large, been universally adopted. Others point more to conduct and represent a serious demand on the capacity of any remuneration committee. Principal agent theory suggests a pay-for-performance reward mechanism is the answer to the bounded rationality and information impactedness problems that beset the effective management of the executive directors. It falls to the remuneration committee to design and implement such a reward mechanism in a way that is in tune with overall corporate strategy. The challenge facing the remuneration committee is to choose reward devices and to calibrate them in a way that aligns the interests of the executive directors with the accomplishment of the key success factors necessary for the delivery of corporate success. To do this, of course, there must be clear line of sight between the directors’ actions and reward delivery. Far from being a one-off decision, such are the vagaries of the global economy and the competitive business environment that these reward mechanism require regular confirmation as to whether they continue to be appropriate. Finally, the remuneration committee needs to communicate meaningfully with both shareholders and with the executive directors concerned as to how it has arrived at its decisions. But the remuneration committee is not a ‘black box’. As with the board itself, it is a social construct. Consequently, its decisions can be expected to be afflicted by the

17

forces of social influence and reciprocity that beset all agents. It is necessary to recognise the cognitive limitations arising out of finite information, limited computational capacity and finite time that confront the remuneration committee. In such a world, incomplete contracts will be the norm and they will be bound by the glue of social influence. Lincoln et al. (2006) suggest that remuneration committees may well lack the time and resource to adequately scrutinise the pay-performance relationship. Given that remuneration committees are indeed restricted on time32 and often limited on resource or stretched on expertise, they have a strong incentive to mimic what other remuneration committees are doing. The organizational isomorphism prediction of neo institutionalist theory is that all remuneration packages will come to look very similar and there will be an absence of individually tailored remuneration contracts. From the review above, it appears that structural considerations (who serves, etc.) for remuneration committees are now secondary in importance to procedural and resourcing considerations (how the business is done). We have set out some specific hypotheses above that focus on this issue and that we intend testing through a series of interviews with remuneration committee members. From this research we expect to be able to make recommendations regarding remuneration committee processes. Specifically as to: selection, induction and development; time allocated to committee in the form of both the length and frequency of meetings and committee scheduling relative to board meetings; attention to performance metrics (personal and corporate); linkages between reward mechanisms and the key performance indicators of company strategy; mechanisms for keeping the whole person in view rather than treating each year as a free standing reward event; and communication with the interested parties. As the focus of policy discussions, remuneration committees are relatively recently arrived on the scene. But, in their short time in the spotlight, they have attracted considerable attention and look likely to command that attention for some years to come. Their activities have started to attract serious research efforts but there seems to be much work remaining to be done.

32 Windram and Song (2004) report that in 2000 audit committees among the UK’s largest companies were meeting on average 3.256 times per year with each meeting lasting 121 minutes on average (range 40 to 260minutes) and preparation time averaging 294 minutes (with a range 180 to 960 minutes).

18

Appendix A

Recent changes in the expected behaviour of the remuneration committee A clear steer of the remuneration committee towards responsibility for aligning the company’s business strategy and its human resource levers (specifically executive reward, in this case) is available in ABI (2002, p3):

“3. Boards should demonstrate that performance based remuneration arrangements are clearly aligned with business strategy and objectives.”

In each subsequent annual revision of the Guidelines, the ABI strengthened this expectation. Thus, in ABI (2003, p8), pointing to shareholder value:

“4.1 Remuneration Committees should: • regularly review share incentive schemes to ensure their continued effectiveness, compliance with current Guidelines and contribution to shareholder value”

And, again, in ABI (2004, p3) encouraging calibration and confirmation of the performance metrics tied to performance pay:

“4. Remuneration Committees must guard against the possibility of unjustified windfall gains when designing and implementing share-based incentives and other associated entitlements. They must also ensure that variable and share- based remuneration is not payable unless the performance measurement governing this is robust. They should satisfy themselves as to the accuracy of recorded performance measures that govern vesting of such remuneration. They should work with audit committees in evaluating performance criteria.”

There is a considerable expectation in the quotation above of the technical analysis of the performance measures chosen for use in the pay-for-performance relationship. In ABI (2005, p3), the 2002 clause quoted above is further strengthened by the addition of a qualifying paragraph, thus:

“3. Boards should demonstrate that performance based remuneration arrangements are clearly aligned with business strategy and objectives and are regularly reviewed. They should ensure that overall arrangements are prudent, well communicated, incentivise effectively and recognise shareholder expectations. It is particularly important that Remuneration committees should bring independent thought and scrutiny to the

19

development and review process together with an understanding of the drivers of the business which contribute to shareholder value.”

This clearly and explicitly ties in the company’s business strategy and objectives with the design of the executive reward relationship. The original 2002 clause is further strengthened by a second paragraph in ABI (2005, p9):

“4.1 Remuneration Committees should: • regularly review share incentive schemes to ensure their continued effectiveness, compliance with current Guidelines and contribution to shareholder value • provide a statement in the Remuneration Report as to whether a review of the current share incentive schemes has been undertaken both as regards their operation, including how discretion has been exercised, and whether grant levels, performance criteria and vesting schedules which have been previously approved by shareholders remain appropriate to the company’s current circumstances and prospects.”

This guideline presses the remuneration committee to keep in view previously granted incentive schemes and there is an emphasis here on the remuneration committee exercising its discretion. Thus, not only is the ABI requiring calibration of the pay-performance relationship but it is also asking that the committee periodically confirm that existing arrangements continue to operate as would be desired in the light of the company’s contemporaneous circumstances. Further emphasis on calibration is seen in the added final sentence at 7.1 and new 7.2 in ABI (2005, p11):

“7.1 All types of performance measures should be fully explained. It should be demonstrated that they are robust and demanding, and linked clearly to the achievement of enhanced shareholder value. Remuneration Committees should satisfy themselves that the vesting of awards accords with these objectives. 7.2 Remuneration Committees should take particular care to ensure that comparator groups used for performance purposes remain both relevant and representative. Where only a small number of companies are used for a comparator group, Remuneration Committees should satisfy themselves that the comparative performance will not result in arbitrary outcomes which are inconsistent with the Guidelines. Awards should not be made for less than median performance.”

20

As discussed in more detail in the text above, the cumulative impact of these successive editions of the ABI Guidelines clearly mark an increased level of expectations as to what the remuneration committee should be doing. There is an emphasis on choice of reward arrangements to fit the company’s business strategy; the need to calibrate the alignment of rewards and performance metrics and, equally, to confirm that they remain appropriate with the passage of time. This is a long way from simply underwriting the probity of remuneration arrangements as being free of the taint of self-dealing.

21

References: Akerlof, George A. (1970). ‘The market for ‘lemons’: Quality uncertainty and the market mechanism. Quarterly Journal of Economics, vol. 84, pp. 488–500. Anderson, Ronald C. and Bizjak, John M. (2003). ‘An Empirical Examination of the Role of the CEO and the Compensation Committee in Structuring Executive Pay’. Journal of Banking and Finance, vol. 27, no 7, pp. 1323-1348. Association of British Insurers (2005). Principles and Guidelines on Remuneration. (28 November). ABI, 51 Gresham Street, London EC2V 7HQ. Association of British Insurers (2004). Principles and Guidelines on Remuneration. (7 December). ABI, 51 Gresham Street, London EC2V 7HQ. Association of British Insurers (2003). Principles and Guidelines on Executive Remuneration. (1 December). ABI, 51 Gresham Street, London EC2V 7HQ. Association of British Insurers (2001). Guidelines for Share Incentive Schemes. (1 March). ABI, 51 Gresham Street, London EC2V 7HQ. Association of British Insurers (1999). Share-Based Incentive Schemes - Guideline Principles. Interpretation and Application in the Context of Currently Evolving Practice. (19 July). ABI, 51 Gresham Street, London EC2V 7HQ. Association of British Insurers (1995). Share Option and Profit Sharing Incentive Schemes. (February). ABI, 51 Gresham Street, London EC2V 7HQ. Association of British Insurers (1994). Long Term Remuneration for Senior Executives, (May). ABI, 51 Gresham Street, London EC2V 7HQ. Association of British Insurers (1993). Share Scheme Guidance. A joint statement from the investment committees of the ABI and NAPF. ABI, 51 Gresham Street, London EC2V 7HQ. Association of British Insurers (1991). Share Incentive Scheme Guidelines. Memorandum. ABI, 51 Gresham Street, London EC2V 7HQ. Association of British Insurers (1987). Share Option and Profit Sharing Incentive Schemes. Summary of Revision to Guidelines to Requirements of Insurance Offices as Investors. ABI, 51 Gresham Street, London EC2V 7HQ (13 July, addendum 6 May 1988, and amended 14 August 1991). Bebchuk, Lucian A, and Fried, Jesse M. (2004). Pay without performance. The unfilled promise of executive compensation. Cambridge, Mass.: Harvard University Press. Bender, Ruth and Moir, Lance (2005). ‘Does “Best Practice” in setting executive pay in the UK encourage “Good” behaviour?’ Paper presented at the 27th Annual Congress of the European Accounting Association, Gothenberg, (May).

22

Bender, Ruth (2004). ‘Why do companies use performance-related pay for their executive directors?’ Corporate Governance, vol. 12, no. 4, pp. 521-533. Bender, Ruth (2003). ‘How executive directors’ remuneration is determined in two FTSE 350 utilities’, Corporate Governance, vol. 11, no. 3, pp. 206-217. Booker, Robert C and Wright, Vicky (2006) ‘Relative shareholder return – the best measure of executive performance?’ What if? Perspective. Watson Wyatt (June). Braiotta, Louis Jr. and Sommer, A.A. Jr. (1987). The essential guide to effective corporate board committees. Prentice Hall. Cadbury Committee (1992). The Financial Aspects of Corporate Governance. London: Professional Publishing Ltd. Charkham, Jonathan and Simpson, Anne (1999). Fair Shares. The Future of Shareholder Power and responsibility, Oxford: Oxford University Press. Chhaochharia, Vidhi and Grinstead, Yaniv (2006). ‘CEO compensation and board oversight’, Paper presented to FMG, LSE (April 20) Combined Code (1998). The Combined Code of the Committee on Corporate Governance. London: Gee Publishing Ltd. (June). Combined Code (2003). The Combined Code on Corporate Governance. London: Financial Reporting Council, (July). Combined Code (2006). The Combined Code on Corporate Governance. London: Financial Reporting Council, (June). Conyon, Martin J (2006) ‘Executive compensation and incentives’, Academy of Management Perspectives, (February), pp. 25-44. Conyon, M.J. and Murphy, K.J. (2000). ‘The Prince and the Pauper? CEO Pay in the United States and United Kingdom’, Economic Journal, 110 (647), 640-671. Conyon, M.J, Peck, Simon, Read, Laura and Sadler, Graham V. (2000). ‘The structure of executive compensation contracts: UK evidence’. Long Range Planning, vol. 33, pp. 478-503. Conyon, M.J, Peck, Simon and Sadler, Graham V. (2006). ‘Compensation consultants and executive pay’. University of Pennsylvania: Working Paper (July). Conyon, M.J. and Peck, Simon (1998). ‘Board control, remuneration committees, and top management compensation’. Academy of Management Journal, vol. 41, no. 2, pp. 146-157. Conyon, Martin J (1997). ‘Corporate governance and executive compensation’, International Journal of Industrial Organization, vol. 15, pp. 493-509.

23

Core, John E, Guay, Wayne R, and Thomas, Randall S (2005). ‘Is US CEO compensation inefficient pay without performance?’ Michigan Law Review, vol. 103 (May), pp. 1142-1185. Core, John E, Holthausen, Robert W and Larcker, David F (1999). ‘Corporate governance, chief executive officer compensation, and firm performance’, Journal of Financial Economics, vol. 51, pp. 371-406. Core, John E, and Larcker, David F (2002). ‘Performance consequences of mandatory increases in executive stock ownership’, Journal of Financial Economics, vol. 64, pp. 317-340. Daily, Catherine M, Johnson, Jonathan L, Ellstrand, Alan E and Dalton, Dan R (1998). ‘Compensation committee composition as a determinant of CEO compensation’, Academy of Management Journal, vol. 41, no. 2, pp. 209-220. DiMaggio, Paul J and Powell, Walter W (1983). ‘The iron cage revisited: institutional isomorphism and collective rationality in organizational fields’, American Sociological Review, vol. 48, (April), pp. 147-160. DTI (2002). Directors’ Remuneration Report Regulations, Statutory Instrument 2002 No. 1986. Edelman, Lauren B. and Suchman, Mark C. (1997) ‘The legal Environments of Organizations’, Annual Review of Sociology, vol. 23 Issue 1, p479-515. Ezzamel, Mahmoud and Watson, Robert (1998).‘Market comparison earnings and the bidding-up of executive cash compensation: Evidence from the United Kingdom’, Academy of Management Journal, vol. 41, no. 2, pp. 221-231. Galbraith, John Kenneth (1974). ‘What comes after General Motors’, The New Republic, (2 November), reprinted in Annals of an Abiding Liberal. London: André Deutsch Limited, 1979. Gibbons, Robert (2005) ‘Incentives between firms (and within)’. Management Science, vol. 51, no. 1 (January), pp. 2-17. Greenbury, Sir Richard (1995). Directors’ Remuneration. Report of a study group chaired by Sir Richard Greenbury. London: Gee Publishing Ltd (July). Hall, Brian J. and Murphy, Kevin J. (2002). ‘Stock options for undiversified executives’, Journal of Accounting and Economics, vol. 33, no. 2 (April), pp. 3-42. Hall, B. J. and Liebman, J.B. (1998). ‘Are CEOs really paid like bureaucrats?’ Quarterly Journal of Economics, vol. 113, no. 3, pp. 653-691. Hampel, Ronnie (1998). Committee on Corporate Governance. Preliminary Report, August 1997; final report January 1998. London: Gee Publishing Ltd.

24

Higgs, Derek (2003). Review of the role and effectiveness of non-executive directors. Department for Trade and Industry (January). Holmstrom, Bengt (2005). ‘Pay without performance and the managerial power hypothesis’. Journal of Corporation Law, (Summer), pp. 703-715. Institutional Shareholders' Committee (1991). The Responsibilities of Institutional Shareholders in the UK. Institutional Shareholders' Committee, 51 Gresham Street, London EC2V 7HQ Jensen, Michael C., Murphy, Kevin J. and Wruck, Eric G. (2004). ‘Remuneration: Where we’ve been, how we got to here, what are the problems, and how to fix them’, Harvard Business School, Finance Working Paper no. 44/2004 (July). Jensen, Michael C, and Meckling, William H. (1976). ‘Theory of the firm: managerial behaviour, agency costs and ownership structure’, Journal of Financial Economics, vol. 3, (October), pp. 305-360. Jensen, Michael C. and Murphy Kevin J. (1990). ‘Performance pay and top-management incentives’, Journal of Political Economy, vol. 98, pp.225-264. Layard, Richard (2005) Happiness: lessons form a new science. London: Allen Lane. Likierman, Sir Andrew (2006). ‘Measuring the success of the remuneration committee’, Benefits & Compensation International, (January/February), pp. 3-6. Lincoln, David, Young, Don, Wilson, Tim and Whiteley, Philip [Parc] (2006). ‘The Role of the Board Remuneration Committee. How Remcos function in determining top executive pay’. Parc: Performance and Reward Centre, Research Report (March). McNulty, Terry, Roberts, John and Stiles, Philip (2005) ‘Undertaking governance reform and research: further reflections on the Higgs Review’. British Journal of Management, vol. 16, pp. S99-S107. Main, Brian G. M. (2006) ‘The ABI Guidelines for share-option based incentive schemes. Setting the hurdle too high?’. Accounting and Business Research, forthcoming. Main, Brian G. M. (1999). ‘The Rise and Fall of Executive Share Options in Britain’ in Jennifer N. Carpenter and David Yermack (eds.). Executive Compensation and Shareholder Value: Theory and Evidence, London: Kluyer Academic Publishers, pp. 83-113. Main, Brian G. M. (1993). ‘Pay in the Boardroom: Practices and procedures’, Personnel Review, vol.22, pp.1-14. Main, Brian G.M., Bruce, Alistair and Buck, Trevor (1996). ‘Total board remuneration and company performance’, Economic Journal, vol. 106, no.439 (November), pp.1627-1644.

25

Main, Brian G. M. and Johnston, James (1993), ‘Remuneration Committees and Corporate Governance’, Accounting and Business Research, vol.23, no.91A, pp.351-362. Main, Brian G. M. and Johnston, James (1992), Remuneration Committees as an Instrument of Corporate Governance, Hume Occasional Paper no. 35. Edinburgh: The David Hume Institute, 54pp. Main, Brian G. M. and Neate, Jeffrey (2006) ‘The ABI Guidelines: compliance and performance in the FTSE-100’, (March). Main, Brian G. M., O'Reilly, Charles A., and Wade, James (1995). ‘The CEO, the board of directors, and executive compensation: Economic and psychological perspectives’, Industrial and Corporate Change, vol.4, no.2, pp. 293-332. Murphy, Kevin (2002). ‘Explaining executive compensation: Managerial power vs. perceived cost of stock options’, University of Chicago Law Review, vol. 69, (Summer), pp. 847-869. NASDAQ (2003). Corporate Governance Summary of Rules Changes. November. http://www.nasdaq.com/about/CorpGovSummary.pdf New York Stock Exchange (2004) Listed Company Manual: Section 303A.00 Corporate Governance Standards. www.nyse.com/regulation/listed/ Newman, Harry A. and Mozes, Haim (1999). ‘Does the composition of the compensation committee influence CEO compensation practices?’. Financial Management, vol. 28, no. 3 (Autumn), pp. 41-53. Ogden, Stuart and Watson, Robert (2006). ‘The search for legitimacy: the use of pay and performance comparisons in determination of CEO remuneration’. Manchester School of Management, UMIST: Working Paper. Ogden, Stuart and Watson, Robert (2004). ‘Remuneration committees and CEO pay in the UK privatized water industry’. Socio-Economic Review, vol. 2, pp. 33-63. O'Reilly, Charles A. III and Main, Brian G. M. (2006). “Setting the CEO's Pay: Economic and Psychological Perspectives”. Presented at the Academy of Management Meetings, Atlanta, August 2006. O'Reilly, Charles A. III, Main, Brian G. M. and Crystal, Graef S. (1988). ‘CEO compensation as tournament and social comparison: A tale of two theories’ Administrative Science Quarterly, vol.33, (June), pp. 257-274. Peck, Simon I and Ruigrok, Winfried (2002). ‘Corporate governance and executive incentives in Germany’. University St Gallen, Working Paper (April). Pye, Annie and Pettigrew, Andrew (2005). ‘Studying board context, process and dynamics: some challenges for the future’. British Journal of Management, vol. 16, S27-S38.

26

Pye, Annie (2002. ‘The changing power of ‘explanations’: directors, academics and their sensemaking from 1989 to 2000’. Journal of Management Studies, vol. 39, no. 7 (November), pp. 908-925. Perkins, Stephen and Hendry, Chris (2005). “Ordering top pay: interpreting the signals”, Journal of Management Studies, vol. 42, no.7 (November), pp. 1443-1468. Pettigrew, Andrew (1992) ‘On studying managerial elites’, Strategic Management Journal, vol. 13, pp. 163-182. Pettigrew, Andrew and McNulty, Terry (1995). 'Power and influence in and around the boardroom’, Human Relations, vol. 48, no. 8, pp. 845-873. Porac, J.F., Wade, J.B. and Pollock, T.G. (1999). ‘Industry Categories and the Politics of the Comparable Firm in CEO Compensation’. Administrative Science Quarterly, 44, 1, 112-144. Roberts, J., McNulty, T. and Stiles, P. (2005). ‘Beyond agency conceptions of the work of the non-executive director: creating accountability in the boardroom’, British Journal of Management, vol. 16, Special Issue, S5- S26. Scott, Richard W (1995). Institutions and Organizations. Thousand Oaks, California: Sage Publications. Securities and Exchange Commission (2006). Executive compensation and related person disclosure. Securities and Exchange Commission, Washington, D.C. 20549. http://www.sec.gov/rules/final/2006/33-8732a.pdf Securities and Exchange Commission (1993). ‘Securities Act Release no. 6962 and no. 7009’, Securities and Exchange Commission, Washington, D.C. 20549. Simon, Herbert A. (1947). Administrative Behavior, New York: Macmillan (3rd edition, 1976). Spira, Laura F and Bender, Ruth (2004). ‘Compare and contrast: perspectives on board committees’, Corporate Governance, vol. 12, No 4 (October), pp. 489-499. Stiles, Phillip and Taylor, Bernard (2000). Boards at Work. Oxford University Press: Oxford. Tricker, R. (1994). International Corporate Governance: Text, Readings and Cases. Singapore: Simon and Schuster. Vafeas, N. (2003) ‘Further evidence on compensation committee composition as a determinant of CEO compensation’, Financial Management, vol. 32, pp. 53-70. Wade, James B, Porac, Joseph F and Pollock, Timothy G (1997). ‘Worth, words, and the justification of executive pay’, Journal of Organizational Behavior, vol. 18, pp. 641-664.

27

Wade, James and O’Reilly, Charles A., Chandratat, Ike (1990). ‘Golden parachutes: CEOs and the exercise of social influence’, Administrative Science Quarterly, vol. 35, pp. 587-603. Westphal, J.D. (1999). ‘Collaboration in the boardroom: behavioural and performance consequences of CEO-board social ties’. Academy of Management Journal, vol. 42, no. 1, pp. 7-24. Westphal, James D and Zajac, Edward J (1996). ‘Director reputation, CEO-board power, and the dynamics of board interlocks’, Administrative Science Quarterly, vol. 41, pp. 507-529. Westphal, J.D. and Zajac, E.J. (1995). ‘Who shall govern? CEO/Board power similarity and new director selection’, Administrative Science Quarterly, vol. 40, pp. 60-83. Westphal, J.D. and Zajac, E.J. (1994). ‘Substance and symbolism in CEOs’ long-term incentive plans’, Administrative Science Quarterly, vol. 39, pp. 367-390. Williamson, Oliver E. (1985). The Economic Institutions of Capitalism. New York: Free Press. Windram, Brian and Song, Jihe (2004) ‘Non-executive directors and the changing nature of audit committees: Evidence from UK audit committee chairmen’. Corporate Ownership & Control, vol. 1, no. 3 (Spring), pp. 108-115. Zajac, E.J. and Westphal, J.D. (1996). ‘Director reputation, CEO-Board power, and the dynamics of board interlocks’. Administrative Science Quarterly, 41, September, 507-529. Zajac, E.J. and Westphal, J.D. (1995). ‘Accounting for the explanations of CEO compensation: substance and symbolism’. Administrative Science Quarterly, 40, June, 283-308.

28

0

20

40

60

80

100

120

140

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Year

Num

ber

of A

rtic

les

Figure 1

Number of articles concerning remuneration committees appearing in the Financial Times, 1980-2006

Source: Year-by-year search on ‘Factiva’. The observation for 2006 is the first 6-months of the year doubled.

29

Figure 2

Remuneration committees in 1990

Remco membership

30%

No Remco membership

70%

0 execs48%

1 exec33%

2 execs15%

3+ execs4%

No CEO58%

CEO42%

2a. Percentage of companies declaring membership of Remco (N=220)

2b. Percentage of Remcos by number of executive members (N=67)

2c. Percentage of Remcos by CEO membership (N=67)

Source: Main, Brian G.M. and Johnston, James (1992), Remuneration Committees as an Instrument of Corporate Governance, Hume Occasional Paper no. 35. Edinburgh: The David Hume Institute, 54pp.

30

Figure 3

The institutional influence on realized share option gains - UK (top 500 CEOs) versus USA (Michael Eisner Disney Co)

£0

£50,000,000

£100,000,000

£150,000,000

£200,000,000

£250,000,000

£300,000,000

£350,000,000

UK top 500 Mike Eisner (DisneyCo.)

£74m

£348m

Source: Conyon and Murphy (2000, pF641)

31

Conformance

[judging; questioning; supervising; watchdog.]

Performance

[contributing: know-how; expertise; external information; networking.]

External facing

Accountability:

Reporting to shareholders

Strategic Thinking:

Attracting and retaining

directors

Internal facing

Supervision:

Implementing STI and

LTI awards

Corporate policy:

Designing compensation

package

Figure 4

Representation of remuneration committee roles

Source: Adapted from Spira and Bender (2004) and Tricker (1994)

32

Age (years):

Average: 59.4

Median: 60

Range: 36 – 76

MALE87.4%

FEMALE12.6%

Age (years):

Average: 54.9

Median: 55

Range: 41- 68

Age (years):

Average: 59.4

Median: 60

Range: 36 – 76

MALE87.4%

FEMALE12.6%

Age (years):

Average: 54.9

Median: 55

Range: 41- 68

Age (years):

Average: 59.3

Median: 60

Range: 38 – 76

Age (years):

Average: 54.5

Median: 55

Range: 41- 68

MALE87.7%

FEMALE12.3%

Age (years):

Average: 59.3

Median: 60

Range: 38 – 76

Age (years):

Average: 54.5

Median: 55

Range: 41- 68

MALE87.7%

FEMALE12.3%

Figure 5

Comparison of all non-executives and remuneration committee members

5a. All non-executives on board:

5a. All non-executives on Remuneration Committee:

Source: Watson-Wyatt Database on Directors’ Remuneration (DDR) FTSE 100 firms, fye 2004-05.

33

Figure 6

Comparison of all remuneration committee and audit committee members

MALE87.5%

FEMALE12.5%

MALE90.3%

FEMALE9.7%

Average age: 58.3 years

Range: 37 – 75 years

Average age: 58.4 years

Range: 37 – 75 years

6a. Remuneration Committee 6b. Audit Committee

Source: Watson-Wyatt Database on Directors’ Remuneration (DDR) FTSE 100 firms, fye 2003-04.

Remco only20%

Audit Co only19%

Both Remco and Audit

36%

Neither25%

Figure 7

Service on Remuneration Committee and Audit Committee

34

8144.1Audit CommitteeNominating Committee

Remuneration Committee

4.1

4.2

Mean

914

92 4

Max.Min.Median

Committee Size

8144.1Audit CommitteeNominating Committee

Remuneration Committee

4.1

4.2

Mean

914

92 4

Max.Min.Median

Committee Size

Figure 7

Board sub-committee size (2003-04)

Source: Watson-Wyatt Database on Directors’ Remuneration (DDR) FTSE 100 firms, fye 2003-04.

12244.6Audit CommitteeNominating Committee

Remuneration Committee

3.1

5.4

Mean

803

122 5

Max.Min.Median

Number of Meetings per year

12244.6Audit CommitteeNominating Committee

Remuneration Committee

3.1

5.4

Mean

803

122 5

Max.Min.Median

Number of Meetings per year

Figure 8

Board sub-committee frequency of meetings (2003-04)

35

Figure 9

Title by board committee membership (non-executives)

On Audit Committee

On Remco

Non Executive Directors

73.96.74.514.9

70.48.64.616.4

69.17.44.619.0

None of these

Prof/Dr etc.

OBE/CBE etc.

Lord/Sir etc.

% with title

On Audit Committee

On Remco

Non Executive Directors

73.96.74.514.9

70.48.64.616.4

69.17.44.619.0

None of these

Prof/Dr etc.

OBE/CBE etc.

Lord/Sir etc.

% with title

Figure 10

Fee paid by board committee membership (non-executives)

On Audit Committee

On Remco

All Non Exec Directors

£52,680

£58,149

£78,138

Mean

£250,000£1,000£45,000

£538,000£1,000 £44,000

£1,296,342£1,000£47,000

Max.Min.Median

Fee Paid

On Audit Committee

On Remco

All Non Exec Directors

£52,680

£58,149

£78,138

Mean

£250,000£1,000£45,000

£538,000£1,000 £44,000

£1,296,342£1,000£47,000

Max.Min.Median

Fee Paid

Source: Watson-Wyatt Database on Directors’ Remuneration (DDR) FTSE 100 firms, fye 2003-04.

36

????LowPayout

Low

HighPayout

????HighAbsolutePerformance

HighLow

Relative Performance

????LowPayout

Low

HighPayout

????HighAbsolutePerformance

HighLow

Relative Performance

Figure 11

Remuneration committee pay-performance design challenges

Source: Lincoln et al. (2006, p25)

37

38