Embed Size (px)

Citation preview

The regulator’s trade-off: bank supervision vs. minimumcapital

Florian Buck & Eva SchliephakeUniversity of Munich & Otto-von-Guericke University

Workshop “Understanding Macroprudential Regulation”Norges Bank, Oslo

Florian Buck The regulator’s trade-off

institution-logo-filenameO

How to improve stability of the banking sector?

Stability of the banking sector responds to changes in the minimum capitalrequirement regulation (Barth et al. 2004; Laeven and Levine 2009) and tochanges in domestic supervision (Buch and DeLong, 2008).

The Basel Accords focus on the regulation of capital and liquidity standards,whereas there are considerable variations in supervisory standards injurisdictions that are adopting the Basel framework.

De facto outcome of international banking regulation depends on bothcapital regulation and national effort that is spent on supervision.

Florian Buck The regulator’s trade-off

institution-logo-filenameO

Motivation

The Research Question

Florian Buck The regulator’s trade-off

institution-logo-filenameO

Overview of the talk

Motivation:How to ensure financial intermediation?

A Small Model: Optimal Regulation in Closed Economies

Lemons equilibrium in an unregulated banking sectorThe effect of capital standardsThe effect of ex-ante supervisionRegulator’s preferences on the mix of both instruments

Outlook: Optimal Regulation with International Spillovers

The club view: observable domestic supervisionInternational deposit rates: unobservable supervision

Conclusion and Discussion

Florian Buck The regulator’s trade-off

institution-logo-filenameO

A small model: an unregulated banking sector

Banks finance projects with deposits (at rD) and costly capital (at rD + ρ)where projects return either R (success) with probability pL or 0 (failure).

Unregulated banks do not hold any capital.A natural fraction θn ∈ [0, 1) of banks is efficient having a monitoringtechnology; the other banks (1− θ) are said to be goofy.Using the monitoring technology at cost m increases the probability of thehigh return R of the project up to pH = pL +4p > pL.

Depositors, endowed with 1, either invest in a riskless storage technologywith a return of γ ≥ 1 or in an opaque bank at a deposit rate of rD .

Asymmetric information on bank quality and no deposit insurance.Goofy banking is inefficient: R · pH > γ > R · pL.

Florian Buck The regulator’s trade-off

institution-logo-filenameO

Two conditions for depositing

Efficient Bank’s “Monitoring condition”

Fraction θ of banks will choose to monitor their projects if(R − rD(1− k)) (pL +4p)−m ≥ (R − rD(1− k))pL.The incentive constraint of monitoring banks:

rD ≤ rMICkD :=

R − m4p

(1− k)> rMIC

D . (1)

If rD > rMICD : unconditional probability that project succeeds is pL.

Depositors Participation Constraint

With rD < rMICD depositors are willing to deposit their endowments if

(rD) · (pL + θ4p) ≥ γ.With perfect competition, depositors participate if

rPCDD :=

{γpLγ

pL+θ4p

iff rD > rMICD ,

iff rD ≤ rMICD .

(2)

Florian Buck The regulator’s trade-off

institution-logo-filenameO

When does financial intermediation take place?

DefinitionIn order to satisfy both constraints simultanously the natural fraction of efficientbanks needs to be large enough: θn < θ̂ := γ

4pR−m −pL4p .

Otherwise: If θn < θ̂, it follows that γpL+θn4p > R − m

4p : depositors correctly

foresee that no bank monitors.

The financial market is unable to channel funds effictively to those who havethe most productive investment opportunities.

This market inefficiency caused by asymmetric information could beeleviated by the introduction of a minimum capital requirement (CR).

Florian Buck The regulator’s trade-off

institution-logo-filenameO

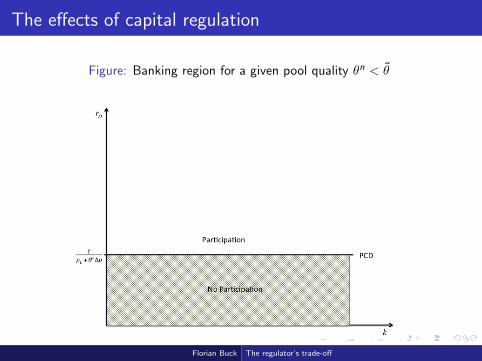

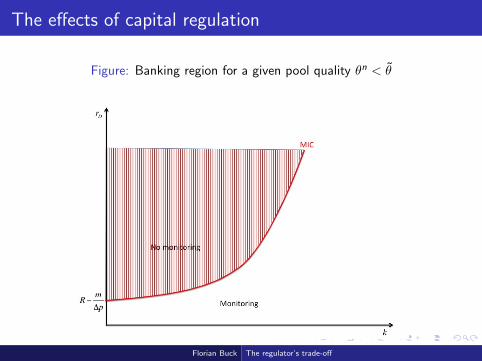

The effects of capital regulation

Figure: Banking region for a given pool quality θn < θ̃

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The effects of capital regulation

Figure: Banking region for a given pool quality θn < θ̃

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The effects of capital regulation

Figure: Banking region for a given pool quality θn < θ̃

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The effects of capital regulation

Figure: Banking region for a given pool quality θn < θ̃

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The effects of capital regulation

Figure: Banking region for a given pool quality θn < θ̃

Florian Buck The regulator’s trade-off

institution-logo-filenameO

Bank’s profits decrease in capital standards!

Efficient Bank’s Participation condition

Condition with non-negative profits is given by(R − rD(1− k))pH −m − ρk ≥ 0 and, hence:

rD ≤:=R − m+ρk

pH

(1− k). (3)

Since we assumed ρ > pH · R, the minimum capital requirement must be

small enough to keep efficient banks operating: k < pHR−mρ

. A fully equity

financed bank will never participate.

Goofy Bank’s Participation condition

Goofy banks will make non-negative profits whenever(R − rD(1− k))pL − ρk > 0,

rD ≤ rPCGD :=R − ρk

pL

(1− k). (4)

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The effects of capital regulation

Figure: Introducing the exit-option for efficient banks

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The effects of capital regulation

Figure: Introducing the exit-option for goofy banks

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The effects of capital regulation

Figure: Introducing the exit-option for banks

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The feasible set of capital standards

Figure: An Economy with a high fraction of efficient banks rD [θn] > rD[k̂]

Florian Buck The regulator’s trade-off

institution-logo-filenameO

Non-relevant capital standards

Figure: An Economy with a low fraction of efficient banks rD [θn] < rD[k̂]

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The Story so far

In a world without capital regulation

If θn < θ̃, depositing is on average less productive than investments in thestorage technology. The banking market breaks down (lemons equilibrium).

Capital requirements can decrease this critical fraction of efficientbanks.

Only for a sufficiently high natural proportion of efficient banks where

rD [θn] < rD[k̂], there exists a continuum of minimum capital

requirement rates k ∈[k∗, k̂e

]that solves the moral hazard problem.

Otherwise, capital requirements alone cannot guarantee financialintermediation, k ∈ [∅].

Florian Buck The regulator’s trade-off

institution-logo-filenameO

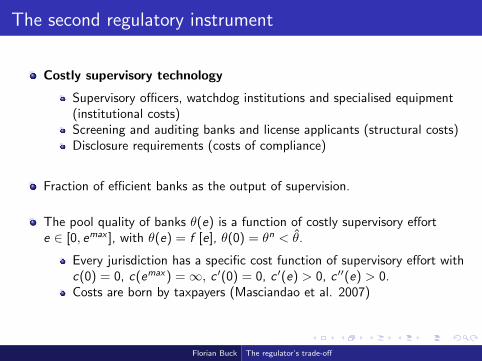

The second regulatory instrument

Costly supervisory technology

Supervisory officers, watchdog institutions and specialised equipment(institutional costs)Screening and auditing banks and license applicants (structural costs)Disclosure requirements (costs of compliance)

Fraction of efficient banks as the output of supervision.

The pool quality of banks θ(e) is a function of costly supervisory efforte ∈ [0, emax ], with θ(e) = f [e], θ(0) = θn < θ̂.

Every jurisdiction has a specific cost function of supervisory effort withc(0) = 0, c(emax) =∞, c ′(0) = 0, c ′(e) > 0, c ′′(e) > 0.Costs are born by taxpayers (Masciandao et al. 2007)

Florian Buck The regulator’s trade-off

institution-logo-filenameO

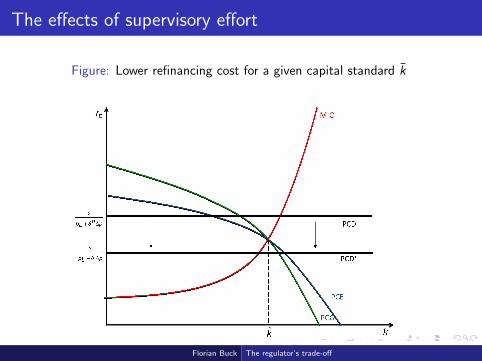

The effects of supervisory effort

Figure: Lower refinancing cost for a given capital standard k̄

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The regulator’s trade-off

The goal of the regulator is to prevent the market breakdown with minimumcosts.

She cares about the rent of domestic efficient banks (φ) and taxpayers(1− φ) .Linear increasing function of supervisory effort: c [e] = c

2· θ2.

Maximisation problem of the regulator

max U(e, k)e,k

= φ · {pH · (R − rD [θ, k] · (1− k))−m − ρ · k}︸ ︷︷ ︸rent of the banking sector

− (1− φ) · c2·θ2. (5)

s.t.

rD [θ] = γpL+θ4p

,

k ≥ 1−(R− m

∆p

)rD

,

k ≤ pH (R−rD )−mρ−pH rD

0 ≤ k ≤ 1, 0 ≤ θ ≤ 1.

Cost of capital can be interpreted as crowding out of deposits: The higherCRs, the lower depositing.

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The regulator’s cost minimisation problem

Figure: Optimal mix of CR and supervision

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The regulator’s cost minimisation problem

Figure: Optimal mix of CR and supervision

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The regulator’s cost minimisation problem

Figure: Optimal mix of CR and supervision

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The regulator’s cost minimisation problem

Figure: Optimal mix of CR and supervision

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The regulator’s cost minimisation problem

Figure: Optimal mix of CR and supervision

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The regulator’s cost minimisation problem

Figure: Optimal mix of CR and supervision

Florian Buck The regulator’s trade-off

institution-logo-filenameO

Who has a preference for loose capital standards?

e c [e] ρ m 4p

k∗ - + - + -

Within the feasible set capital standards and supervision are substitutes: Ajurisdiction in which high supervisory effort e is spent, has lower optimal capitalstandards k∗.

Lower cost efficiency in supervisory effort c [e] lead to higher k∗.

Lower cost of capital ρ will increase k∗.

Higher monitoring cost m decrease the profit of efficient banks which lowers theoptimal effort level thereby increasing k∗.

The less value added by monitoring 4p , the less likely the MIC of efficient banksholds. In terms of our model lower profits justify higher k∗.

Florian Buck The regulator’s trade-off

institution-logo-filenameO

Mobile banks: What are the consequences?

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The game of regulatory competition

Consider two identical countries A,B that are linked through perfect bankmobility.

Regulators in each country differ w. r. t the supervisory efficiency, wherecA < cB resulting in θ∗A > θ∗B .The respective optimal national minimum capital requirements arek∗A(θ∗A) < k∗B(θ∗B).

With differentiated regulatory “products” national banks will shift to themost appropriate regulator.

A bank of type i ∈ [E ,G ] that is settled in country B will move wheneverΠi (A)− ϑ > Πi (B) .As long as k̂ > k∗, efficient banks are able to generate higher marginalprofits than goofy banks.

What is the outcome of systems competition?

Florian Buck The regulator’s trade-off

institution-logo-filenameO

Case A: Competition of regulatory clubs

Complete information for all market participants regarding the quality andthe cost of banking supervision.

Re-allocation of banks

Migration of banks to the less regulated economy A: lower CRs and lowerdeposit rates strictly enhance the profits of banks: Πi (B) < Πi (A).For sufficient low moving costs, financial intermediation in jurisdiction Bbreaks down.

Feedback effect on the optimal policy mix in A

Depositors in country A demand higher deposit rates.The regulator in A has to adapt the optimal policy mix (increase k or e).

With convex effort costs, A will gradually increase the capitalrequirement compared to autarky (redistribution).Welfare-loss: Both countries lose in welfare terms compared to autarky.

Florian Buck The regulator’s trade-off

institution-logo-filenameO

Case B: International deposit rates

Asymmetric information makes it hard for depositors to distinguish regulatorysytems: rD [θ∗A] < r̄D < rD [θ∗B ].

Re-allocation of banks

In B banks benefit from lower overall lending rates.In A a higher deposit rate prevents efficient banks from monitoring, i.e.,k∗A(θ∗A) is too low to satisfy the monitoring incentive constraint.Banks move to country A where the financial sector does not monitor.

Feedback effect on the optimal policy mix

Dilemma: Regulators do not benefit from an increase in CRs, sincedepositors do not punish non-monitoring efficient banks.It is individual rational to decrease CRs, but this implies the breakdown ofthe global financial market.

Incentives to harmonise regulatory policy

A policy cartel is self-enforceable.

Florian Buck The regulator’s trade-off

institution-logo-filenameO

Regulatory competition with international deposit rates

Figure: Pooling of deposit rates creates an unstable global economy

Florian Buck The regulator’s trade-off

institution-logo-filenameO

Conclusion and discussion

Regulators seek to prevent the breakdown of the financial sector at lowestcosts.

Direct forms of regulation (supervision) enhances the average ability ofbanks to control risk.Indirect regulation via capital requirements incentives monitoringactivity by banks.The expected costs of a breakdown are minimised with a mix of bothinstruments.

Once we allow for cross-boder banking, the optimal policy is not feasible.

If domestic supervision is not observable, without collusion our modelpredicts a global financial breakdown.

Countries are better off by harmonising regulation.

Problem: non-contractability of supervision.

Florian Buck The regulator’s trade-off

institution-logo-filenameO

End

Thank you very much for your questions!

Further comments please send to [email protected]

Florian Buck The regulator’s trade-off

institution-logo-filenameO

What will happen with deposit insurance?

With a risk-adjusted deposit insurance scheme, we get the same results; only thecomposition of costs differs

Depositors will get their outside option, regardless of the risk behaviour of banks;

their PCD will not change(rD = γ

pL+θ4pL

).

Now, banks have to pay a risk-premium ρ [p] that is equal to the value at risk withprobability p.The new deposit rate (that equals the MIC) is rD = γ + ρ [p, θ].All participation constraints and the monitoring incentive constraint remain thesame.

The deposit insurance policy is welfare-neutral resulting in the same allocation of

banks.

The effect of subsidized deposit insurance is benign (Morrison, White, JBF 2011)

Requiring banks to contribute part of their capital to a deposit insurance fundreduces the banker’s stake in any investment of a given size.More deposit insurance reduces the interest rate that bankers have to pay to enticedepositors to deposit, and so increases the share of any given return from asuccessful project that a banker can extract.The optimal level of deposit insurance (safety net) varies inversely with the qualityof the banking system.

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The impact of capital regulation

Figure: Deposit rates and capital regulation

Florian Buck The regulator’s trade-off

institution-logo-filenameO

Optimal regulation in closed economies

Figure: Feasible policies

Florian Buck The regulator’s trade-off

institution-logo-filenameO

Optimal Choices

The regulator does not care about profits (φ = 0)

If the PC of banks never becomes binding before the MIC, i.e.,k̂ = pL

∆p· mρ> 1, the regulator just sets k = 1 and e = 0;

Otherwise, he sets k = k̂ and e = f -1(θ = γ·(1−k̂)

4pR−m− pL4p

)> 0.

The regulator cares about the profits of efficient banks (φ > 0)

A “captured” regulator implements

θ∗ =

[12

(√(1−φ)2·p2

L−φ· 4·pH ·∆p(R·∆p−m)

c(1−φ)·∆p

− pL∆p

)], and

k(θ∗) = 1− 1γ

(pL + θ∗4p)(R − m

∆p

).

Taking the partial derivative of the regulator’s optimal supervisory effort

w.r.t. k, gives ∂2U∂k∂θ

= −φ(

pH∆pγ

(pL+θ4p)2

)< 0.

Capital requirements and supervision are substitutes (higher optimal k, loweroptimal effort e, vice versa).

Florian Buck The regulator’s trade-off

institution-logo-filenameO

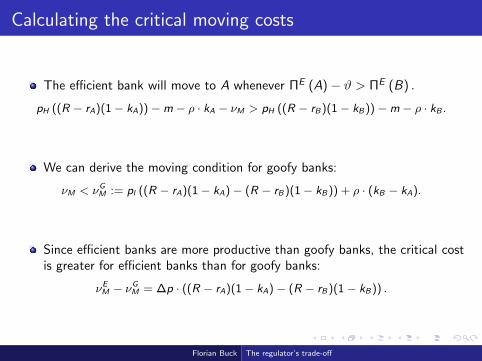

Calculating the critical moving costs

The efficient bank will move to A whenever ΠE (A)− ϑ > ΠE (B) .

pH ((R − rA)(1− kA))−m − ρ · kA − νM > pH ((R − rB)(1− kB))−m − ρ · kB .

We can derive the moving condition for goofy banks:

νM < νGM := pl ((R − rA)(1− kA)− (R − rB)(1− kB)) + ρ · (kB − kA).

Since efficient banks are more productive than goofy banks, the critical costis greater for efficient banks than for goofy banks:

νEM − νGM = ∆p · ((R − rA)(1− kA)− (R − rB)(1− kB)) .

Florian Buck The regulator’s trade-off

institution-logo-filenameO

The case of club competition

Figure: Choice of jurisdiction for banks

Florian Buck The regulator’s trade-off

institution-logo-filenameO

Divergence in supervisory regulation

Figure: What was the global relative budget (in $ per 100.000 $Assets) for supervision of banks in 2005?

0 20 40 60 80 100 120 140 160

Germany

United Kingdom

France

Ireland

Luxembourg

Portugal

South Africa

Brazil

Poland

United States

Relative Budget

Source: World Bank 2008

Florian Buck The regulator’s trade-off

institution-logo-filenameO

How is this Possible in a Basel-World?

The implementation of the Basel Accord agreements into national lawallows for some discretion of national regulators.

“Supervisors should have the discretion to use the tools suited tothe circumstances of the bank and its operating environment.”(Basel II Accord, Supervisory Review Process, Section 759)

National regulators have two choice parameters:(1) a preferred capital requirement (equity to deposit ratio) and (2) alevel of effort spend on sophisticated supervision (monitoring),represented by the average banking pool quality.

Florian Buck The regulator’s trade-off

institution-logo-filenameO

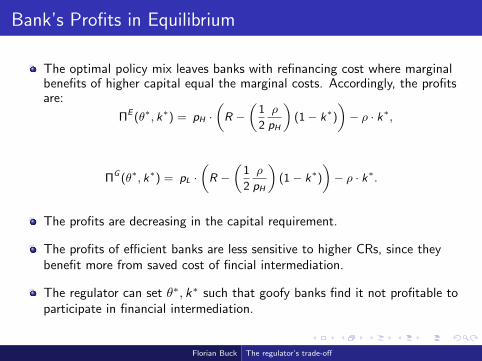

Bank’s Profits in Equilibrium

The optimal policy mix leaves banks with refinancing cost where marginalbenefits of higher capital equal the marginal costs. Accordingly, the profitsare:

ΠE (θ∗, k∗) = pH ·(R −

(1

2

ρ

pH

)(1− k∗)

)− ρ · k∗,

ΠG (θ∗, k∗) = pL ·(R −

(1

2

ρ

pH

)(1− k∗)

)− ρ · k∗.

The profits are decreasing in the capital requirement.

The profits of efficient banks are less sensitive to higher CRs, since theybenefit more from saved cost of fincial intermediation.

The regulator can set θ∗, k∗ such that goofy banks find it not profitable toparticipate in financial intermediation.

Florian Buck The regulator’s trade-off

institution-logo-filenameO

Participation Constraints in an Unregulated Banking Sector

Efficient Bank’s Participation condition

Condition of non-negative profits: (R − rD)pH −m ≥ 0 and hence:

rD ≤ rPCED := R − m

pH. (6)

The lower bound on the deposit rate of the efficient bank’sparticipation is always above the incentive constraint, since pH > ∆p.

Goofy Bank’s Participation condition

Goofy banks will make non-negative profits whenever (R − rD)pH > 0,

rD ≤ rPCGD := R. (7)

Florian Buck The regulator’s trade-off

institution-logo-filenameO

End

Thank you very much for your questions!

Further comments please send to [email protected]

Florian Buck The regulator’s trade-off