Embed Size (px)

Citation preview

CLASH OF THETITANS

The RBI and the government are at loggerheads over separation of public debt management from monetary policy

RNI No. MAHENG/2009/28962 | Volume 7 Issue 4 | 16th - 30th Apr ’15Mumbai | Pages 48 | For Pr ivate Circulat ion

Registered O�ce: 38-B, Khatau Building, 2nd Floor, Alkesh Dinesh Mody Marg, Fort, Mumbai - 400001. Tel: 3926 8600 / 01; Fax: 3926 8610, Corporate O�ce: B-2, 301/302, 3rd Floor, Marathon Innova, O� Ganpatrao Kadam Marg, Lower Parel (W), Mumbai - 400 013. Tel.: 39268000 / 8001 Fax: 39268010

Contact : +91-22-39269600E-mail: [email protected] | www.nirmalbang.com

It’s simplified...Beyond Market 16th - 30th Apr ’15 3

DB Corner – Page 5

Clash Of The TitansThe RBI and the government are at loggerheads over separation of Public Debt Management from Monetary Policy – Page 6On An Upbeat NoteRBI pegs GDP growth at close to 8% on the back of expectations of a normal monsoon, continuation of the cyclical upturn in a supportive policy environ-ment and no major structural change or supply shocks – Page 9Bonded By Civic SenseSEBI has come up with a list of guidelines to revive municipal bonds, aimed at raising resources for urban infrastructure projects – Page 12Breaking TraditionBancassurance, through ‘open architecture’, will free banks to sell products of more than one life insurer unlike in the past that will help expand insurance penetration in the country - Page 15Clean And GreenRecent policy announcements will give a thrust to the renewable energy sector, especially solar energy and wind power – Page 18North-South DivideWhile Delhi National Capital Region (NCR) is besieged with unsold inventory, Bengaluru is doing relatively well thanks to sales of reasonably priced apartments – Page 21Securing AirwavesThe government fetched significant returns from spectrum auction after days of fierce bidding, with Idea Cellular emerging as the highest bidder – Page 24Concrete StepsThe government has announced a series of tangible initiatives to boost the beleaguered construction sector – Page 27

Sarla Performance Fibers Ltd: A Damn Good YarnSarla Performance Fibers is spinning its success story by providing specialized and high value-added yarns in the US, along with upgradation of its existing facilities in India – Page 30

Important Statistics For The Fortnight Gone By – Page 33

Whetting Investor AppetiteMutual fund houses have in recent times launched a series of funds based on the ‘Make in India’ theme – Page 35

Prodding Start-upsBudget 2015 is indeed a godsend for start-ups as the government has proposed a series of measures to boost new entrepreneurs – Page 38

Dispelling UncertaintyDoji candlestick patterns appear on charts when market sentiment is indecisive and a trend is weakening – Page 40

Important Jargon For The Fortnight – Page 45

Volume 7 Issue: 04, 16th - 30th Apr ’15

Editor-in-Chief & Publisher: Rakesh BhandariEditor: Tushita NigamSenior Sub-Editor: Kiran V Uchil

Art Director: Sachin KambleJunior Designer: Harshad Pawar

PR & Communications: Dwiti BhutaOperations: Shreelatha Gollavathini

Printed and published by Mr Rakesh Bhandari on behalf of Nirmal Bang Financial Services Pvt Ltd, printed at Nimesh Offset Arts, 281, Bldg No 5-8, Mittal Indl. Estate, Andheri-Kurla Road, Marol, Andheri East, Mumbai-400059 and published at Nirmal Bang Financial Services Pvt Ltd, 19, Sonawala Building, 25 Bank Street, Fort, Mumbai-400001. Editor: Tushita Nigam

CORPORATE OFFICE B-2, 301/302, Marathon Innova,Off Ganpatrao Kadam Marg,Lower Parel (W), Mumbai - 400 013Tel: 022 - 3926 8000/8001

Web: www.nirmalbang.com [email protected] No: 022 - 3926 8047

Research Team: Sunil Jain, Silky Jain, Vikas Salunkhe

It’s simplified...Beyond Market 16th - 30th Apr ’154

Tushita NigamEditor

The Reserve Bank of India (RBI) is likely to see some major changes in its key roles. The separation of the public debt office from monetary management has been suggested and been a topic of debate for quite a while now. Among other things, a new monetary policy framework will help change the manner in which interest-rate decisions are taken and an independent public debt management agency will facilitate transparency in debt activities of the government.

However, the outcome of this ongoing clash between the central bank and the government is not yet known. The new framework, the agency to be set-up, and the views/counterviews have been elaborately discussed in the cover story of this issue. Read on for some clarity on this topic.

Among other articles, we have covered a synopsis of the recently-held monetary policy review, the various guidelines introduced by the Securities and Exchange Board of India to revive municipal bonds, the ‘open architecture’ model to be followed by bancassurance in India, the recent policy announcements to help propel sectors like renewable energy and construction, the state of the real estate market in the country and the outcome of the spectrum auction, among others.

The Beyond Basics section covers a very interesting article on new schemes being launched by mutual fund houses in India based on the ‘Make in India’ initiative introduced by the Narendra Modi-led government. In this article, we have tried to help our readers understand how lucrative such theme-based schemes can prove to be.

Out of the various positives announced in the Union Budget this year, those meant for start-ups were the most talked about. Several measures for start-ups were announced in Union Budget 2015-16, and have been covered in the Beyond Entrepreneurs sectioN.

A Note Of Discord

segment due to uncertainty in the upcoming quarterly earnings results and global events.

However, in the coming fortnight, the markets will be driven by the announcement of earnings resultS.

It’s simplified...Beyond Market 16th - 30th Apr ’15 5

Disclaimer It is safe to assume that my clients and I may have an investment interest in the stocks/sectors discussed. Investors are required to take an independent decision before investing. Investment in equity is subject to market risk. Our research should not be considered as an advertisement or advice, professional or otherwise. The investor is requested to take into consideration all the risk factors including their financial condition, suitability to risk return profile and the like and take professional advice before investing.

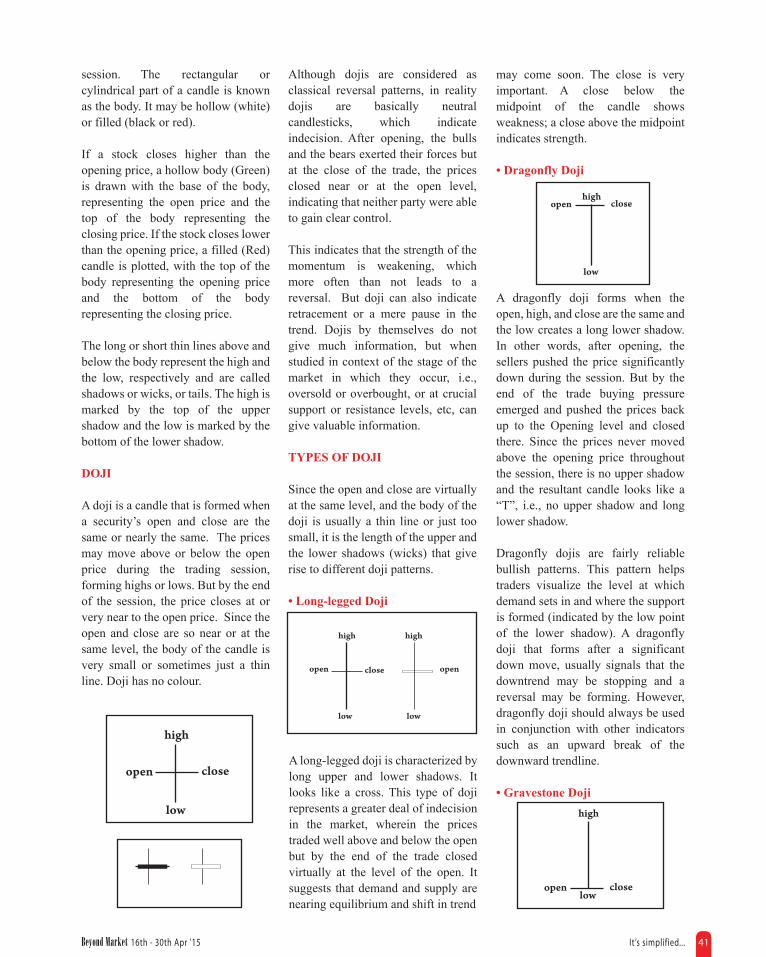

n the previous fortnight, India’s apex bank, the Reserve Bank of India (RBI) in its monetary policy review meet

kept key rates unchanged. While the repo rate stands at 7.50%, the cash reserve ratio (CRR) remains unchanged at 4%.

CPI inflation for the month of March eased to 5.17%, the lowest in three months, supported by lower food prices in spite of crop damage due to unseasonal rain.

European Central Bank (ECB) President Mario Draghi said that quantitative easing was meant to continue until the end of September 2016 or until the ECB sees enough improvement in inflation.

He reiterated that the decision to keep

I the benchmark refinancing rate at its current all-time low of 0.05% and the central bank’s aggressive monetary policies were “effective.”

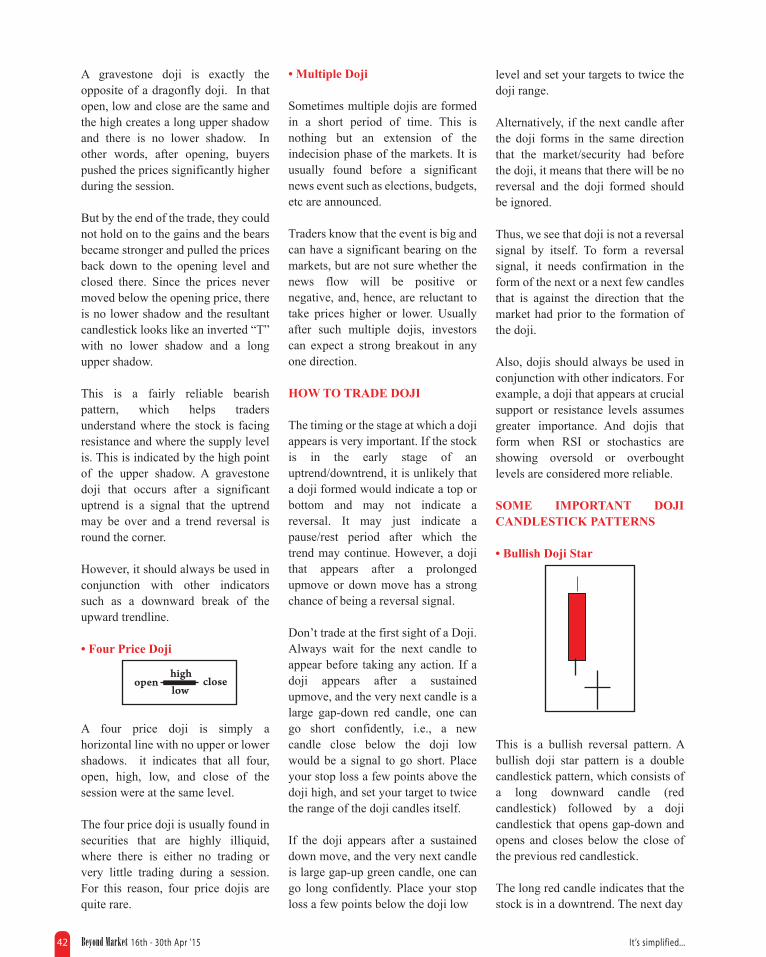

Quarterly earnings results of India Inc are expected to be rather weak.

In the coming fortnight, the Indian stock markets are likely to remain range-bound.

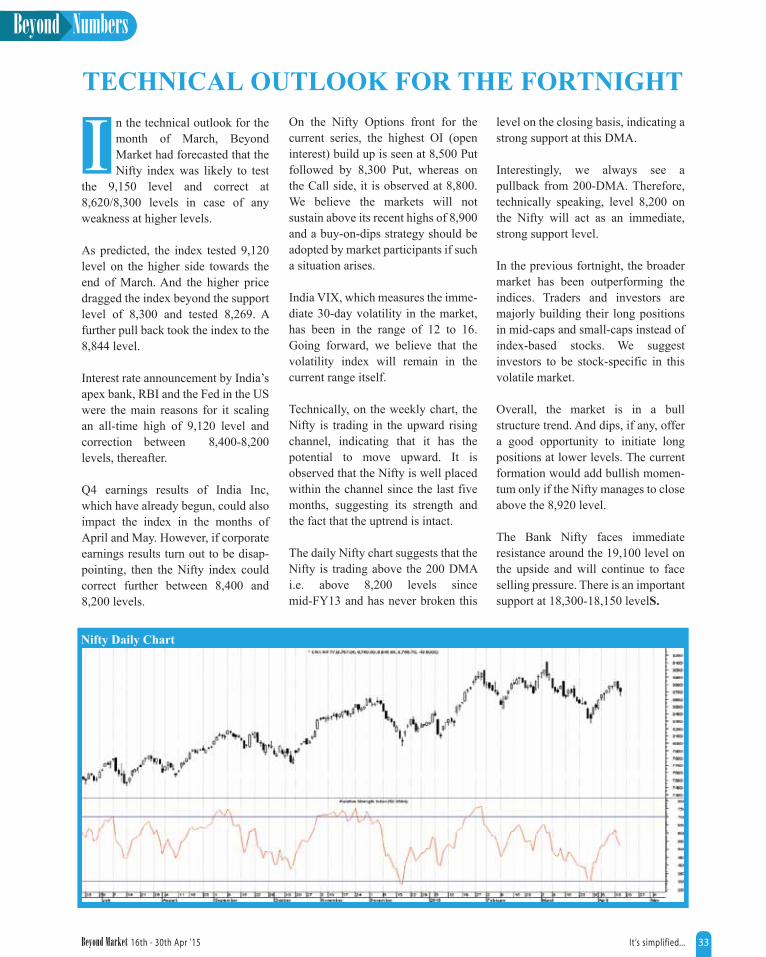

The Nifty has support at the 8,650 level. If it breaks this level, then the index is likely to touch the 8,450 level on the downside.

On the upper side, the Nifty is likely to be around the 8,760 level and the 8,840 level, thereafter.

Market participants are advised to avoid taking positions in the F&O

In the coming fortnight,the Indian stock markets

are likely to remainrange-bound.

Sensex: 28,442.10Nifty: 8,606

(As on 17th Apr ’15)

CLASHOF THETITANS

The RBI and the government are at loggerheads over separation of

public debt management from monetary policy

It’s simplified...Beyond Market 16th - 30th Apr ’156

It’s simplified...Beyond Market 16th - 30th Apr ’15 7

the public.

Analysis: World over, there are three principal targets used by central banks - money supply, inflation and the exchange rate. Each has its own pros and cons. Given the challenges and size of the Indian economy, it was decided to target inflation in India.

Inflation targeting was first adopted by New Zealand in 1990. Since then it has gained popularity around the world. Currently, there are around 25 central banks that have inflation targeting as their basic monetary policy framework. Central banks of all major economies target inflation.

The RBI oversees many key areas like issuing currency, supervision of the banking sector, financial inclusion, payment and settlement, liquidity management in the system, banker and debt manager for the government and manager of foreign exchange. It is difficult for the RBI to do justice to all roles.

With inflation targeting, the RBI has a mission and cannot offer excuses in case a target is missed. The move will also help better coordination between the government and the central bank.

Historically, there have been political pressures on the central bank, especially before and after elections, to cut rates. With inflation targets, the RBI can preserve its autonomy. Most importantly, targets will lead to greater scrutiny of MPC’s decisions.

Monetary Policy Committee

While the monetary policy agreement is silent on the setting-up of MPC, both the government and the RBI are negotiating how the committee will be set up. Both the FSLRC and the RBI committee report (Urjit Patel report) have recommended MPC to conduct monetary policy. More than

mportant changes are underway in key roles of the Reserve Bank of India (RBI). And the separation of the public debt

office from monetary management is being widely debated.

The debate has grown after Finance Minister Arun Jaitley, in his Budget speech, said the government has concluded a monetary policy framework agreement with the RBI. A separate PDMA also found a mention in the Budget speech.

There is a conflict of interest in the RBI managing both the roles. On one side, the RBI needs to ensure lower interest rates in the system for lower cost of borrowing for the government. The government borrows from the market to bridge its fiscal deficit. But lower interest rate pushes inflation up. Keeping interest rates low goes against inflation targeting.

To resolve the conflict of interest, the RBI and the government have already agreed on a new monetary policy framework. But both are not on the same page as far as a separate debt office and setting up of a monetary policy committee (within the new policy framework) are concerned.

THE GENESIS

The idea of separating the public debt office from monetary management has been debated for quite some time now. Many committees have vouched for it. However, it was the financial sector legislative reforms commission (FSLRC) that was more vocal about the subject.

The FSLRC set up by the government intends to overhaul the archaic financial sector regulation in India. It submitted a report in 2013 and many provisions within FSLRC need parliament’s approval. (Beyond Market covered FSLRC in April ’13.)

I FSLRC also talked about setting up of a monetary policy committee (MPC) to take policy decisions and set inflation target. Many committees in the past have suggested a vote-based monetary policy decision, as is practiced in developed economies.

THE NEW MONETARY POLICY FRAMEWORK

20th Feb ’15 was a watershed moment as the government and the RBI signed an agreement for a new monetary policy framework. The agreement mandates the RBI to work towards an inflation target. However, the framework is silent on the formation of the monetary policy committee (MPC).

For starters, it is the central bank’s role, among other things, to control interest rates in the system and find a balance between growth and inflation. The RBI achieves its set mission through monetary policies and various tools at its disposal.

Inflation Targeting

The agreement gives RBI an inflation target of 6% by January ’16 and 4% thereon with a band of plus or minus 2 percentage points. Inflation targeting arrangement provides the RBI with the flexibility to use any tool it deems fit to bring inflation under control. Inflation targeting means that when inflation goes above the comfort zone, the primary objective of the central bank will be to bring the inflation down. Below that particular level, the RBI can look at other objectives, but beyond the comfort zone, taming inflation will be RBI’s central policy objective. To ensure accountability, if the RBI is unable to meet the target, it will have to explain to the government why the target was missed and disclose it to

It’s simplified...Beyond Market 16th - 30th Apr ’158

80 central banks in the world use MPCs for their monetary policies.

With MPC, policy decisions will depend on votes by committee members as against the current practice of a single individual (governor) taking the decision with inputs from his team members. Decision-making is very discretionary and accountability measures are absent.

Analysis: The bone of contention between the RBI and the government is the size and composition of the committee. FSLRC has recommended a total of seven members in MPC. The RBI committee report has recommended a five-member committee. Both the government and the RBI want a higher say in MPC. Most experts expect the composition of MPC to be an amalgamation of FSLRC and the Urjit Patel report.

As per FSLRC recommendations, MPC would look like this: MPC (7 members): 2 (RBI members)+ 2 (government appointee in consultation with RBI) + 3 (government appointees)

As per the Urjit Patel Committee report, MPC would look like this: MPC (5 members): 3 (RBI member) + 2 (government appointee in consultation with RBI) Public Debt Management Agency

As per this year’s Budget, a separate PDMA will be formed to manage government debt: both internal and external. Currently, external debt is being managed by the government, while internal debt is being managed by the RBI. With PDMA, both will come under one umbrella.

Since late 1980s, almost every nation from the Organization of Economic

Cooperation and Development (OECD) and major emerging markets have established such an agency. Internationally, a separate PDMA from monetary management is considered to be the best practice.

The creation of PDMA is a matter of intense debate in India. The main objective of debt management is to ensure that the government’s financing needs and its payment obligations are met at low cost over the medium to long run. While PDMA can minimize cost for government borrowing, the RBI is worried about risk to markets and system in the short term. Here are views and counterviews about the creation of a separate PDMA.

Lastly, unifying both internal and external debt management under one umbrella will lead to better information on government debt, thus yielding better decisions and subsequently improved debt management for the government.

Counterview: While a separate PDMA can lower the cost of borrowing for the government, there are prerequisites for that assumption. One, bond market needs to be very liquid to absorb all offerings from the government, otherwise it can blow up government’s interest costs. Therefore, bond market reforms are required for PDMA to succeed.

Two, the government needs to put its house in order as far as its fiscal deficit is concerned, else taking RBI away from debt management can be disruptive for the bond markets and offer risks to the system. There are fears about potential market volatility if debt management is shifted to the new agency.

Analysis: PDMA is caught-up in controversies between the RBI and the government. Both parties will have to work closely to minimize any collateral damage to the bond market. PDMA will need co-ordination between the RBI and the government.

The biggest positive of a separate PDMA is that once created, the RBI will reduce banks’ SLR requirements. This will free up funds to lend for private enterprise. It will also lead to the emergence of different classes of investors, especially retail investors who can directly participate in the G-Sec market without many hurdles. The new monetary policy framework will change the way interest-rate decisions are taken, while an independent PDMA will bring a lot of transparency to the government’s debt management operatioN.

100%

80%

60%

40%

20%

0%2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Internal Debt External Debt

11.89

88.11

11.37

88.63

11.98

88.02

9.65

90.35

9.44

90.56

9.12

90.88

8.16

91.84

7.41

92.59(% o

f Tot

al)

Composition of Public Debt*

Source: RBI *Central Government’s Public Debt

View: Key conflict of interests warrants a separate PDMA. One, higher rates to fix inflation leads to higher borrowing cost for the government. Two, the RBI can be considered as an insider as it acts as a merchant banker for the government and is an owner as well as an operator of government securities market.

Three, the RBI can mandate banks to invest more in government securities, since it regulates the banking sector. Thus, setting up the PDMA is important as it takes away few key conflict areas, and allows the RBI to solely focus on inflation.

Banks are captive buyers for government securities as they are mandated to maintain a statutory liquidity ratio (SLR). This has led to underdevelopment of the G-Sec market in India. Retail participation is non-existent. This has led to wrong pricing of government bonds.

n AnUpbeatNote

RBI pegs GDP growth at close to 8% on the back of expectations of a normal monsoon, continuation of the cyclical upturn in a supportive policy environment and no major structural change or supply shocks

he ‘will he, won’t he’ question has been answered, at least for now. The Reserve Bank of India

(RBI) Governor Raghuram Rajan maintained a status quo on its

T benchmark repo rate during the first bi-monthly monetary policy review for this fiscal (FY16) held on 7th April. The repo rate stands at 7.5%, and accordingly the reverse repo rate remains at 6.5%.

Repo rate is defined as the rate at which the central bank of a country (in India, it is the Reserve Bank of India) lends money to commercial banks in the event of any shortfall of funds. The reverse repo rate is the rate

It’s simplified...Beyond Market 16th - 30th Apr ’15 9

It’s simplified...Beyond Market 16th - 30th Apr ’1510

expecting inflation to firm up by the year-end to 5.8%, Raghuram Rajan will be cautious with repo rate cuts. The chances of the repo rate hovering around 7% or just a little above it are, therefore, very high.

The Reserve Bank is encouraged by the fact that inflation is under control and there is no immediate upside threat. Inflation (barring food and fuel) has, in fact, been on a downward trend in the nine months till February this year, mainly driven by price cuts in petrol and diesel caused by a slump in international crude oil prices.

Housing inflation has eased while weak demand conditions have helped reduce upside pressures affecting prices of services such as education and health.

Another important point highlighted by the apex bank relates to the rate of growth of rural wages, which has come off substantially from double-digit levels that prevailed up to November ’13.

Further, adding to the downward pressure on inflation is the fact that there has been substantial easing of input price pressures.

Present indications are that inflation will not pose a great threat this year, barring unforeseen circumstances. The Reserve Bank, in fact, expects Consumer Price Index (CPI) inflation to fall to around 4% by August before climbing to around 5.8% by the end of this year.

However, inflation-control has always been a priority for the Reserve Bank and it has flagged a few concerns on the issue.

Unseasonal rainfall in end-February and March of this year has adversely affected crop production and this could potentially push food prices up.

bank is committed to an accommodative policy regime in the coming months - in layman’s language, it means that a cut in the repo rate can be expected in the coming months.

“Going forward, the accommodative stance of monetary policy will be maintained….the Reserve Bank will await the transmission by banks of its front-loaded rate reductions in January and February into their lending rates.

“Second, developments in sectoral prices, especially those of food, will be monitored, as will the effects of recent weather disturbances and the likely strength of the monsoon, as the Reserve Bank stays vigilant to any threats to the disinflation that is underway,” the apex bank’s policy statement said.

It further said that “progress on repurposing of public spending from poorly targeted subsidies towards public investment and on reducing the pipeline of stalled investment will also be helpful in containing supply constraints and creating room for monetary accommodation.

“Finally, the Reserve Bank will watch for signs of normalization of the US monetary policy, though it anticipates India is better buffered against likely volatility than in the past.”

More reductions in the repo rate can, therefore, be expected this calendar year and there is a high likelihood of at least a further 0.25% cut in the next two-three months. The middle class and lower-income groups will have to wait until then before they can expect some relief in the form of lower equated monthly installments (EMIs).

A further rate cut will, however, depend on the direction inflation takes. With the Reserve Bank

at which the central bank borrows money from commercial banks within the country.

The Reserve Bank also kept unchanged the Cash Reserve Ratio (CRR) at 4% while the bank rate stands at 8.5%. The Statutory Liquidity Ratio (SLR) has also been kept unchanged at 21.5%.

Banking, corporate and financial communities were divided in their opinions as to what RBI Governor Rajan would do on 7th April. While a section expected that he would cut rates and indeed clamoured for the same, the other section expected him to maintain a status quo. The latter sentiment was mainly because of inflation, which had increased marginally in the last few weeks. Inflation still remains a cause of concern, especially food inflation, and therefore, Rajan was expected to be cautious during the April monetary policy review.

Inflation apart, the two rate cuts affected by the Reserve Bank (a total of 50 basis points or 0.5%) in the first three months of this year, have not yet translated into lower lending rates by banks and the credit off-take has been rather weak.

“With little transmission, and the possibility that incoming data will provide more clarity on the balance of risks on inflation, the Reserve Bank will maintain status quo in its monetary policy stance in this review,” the Reserve Bank said in its policy statement.

The apex bank’s stance is, however, clear - it will reduce the repo rate going forward, most probably in June as many banking experts opine. Rajan himself made it clear that the monetary policy direction will not change, which means that the apex

It’s simplified...Beyond Market 16th - 30th Apr ’15 11

A less-than-normal monsoon in the June-September period could compound the problem as a shortfall in crop production has the potential to play havoc with food prices.

“Larger than anticipated administered price revisions, a faster closing of the output gap, geo-political developments leading to hardening of global commodity prices and a spill-over from external developments through exchange rate and asset price channels” are the other upside risks to inflation, the apex bank said.

On the brighter side, it noted that “however, at this juncture, these upside risks appear to be offset by downsides originating from global deflationary/ disinflationary

tendencies, the still soft outlook on global commodity prices; and slack in the domestic economy.”

The Reserve Bank is buoyed by the macro-economic climate in the country and has pegged its GDP forecast for this fiscal at 7.8%, up by 30 basis points from 7.5% of 2014-15.

With liquidity conditions comfortable, banks should be able to transmit the recent policy rate reductions into their lending rates and this, in turn, will improve financing conditions for the productive sectors of the economy.

The policy announcements in the recently-announced Union Budget 2015-16, especially on the

infrastructure front, should help boost investment in this sector. The Narendra Modi-led government has focused on creating a conducive and business-friendly economic and investment climate, and this coupled with the conducive outlook on inflation, should help brighten the country’s economic prospects. In conclusion, the message from the April monetary policy statement of the Reserve Bank is that assuming a normal monsoon, continuation of the cyclical upturn in a supportive policy environment and no major structural change or supply shocks, India’s economy can be expected to chug along smoothly at close to 8%. Not bad for a country that had to endure a sub-5% growth for some years in the recent pasT.

Now, Commodity TradingIs No More A Puzzle.

Commodity trading can be confusing

especially if one is inexperienced and lacks the

necessary skills to trade successfully. At Nirmal

Bang, our team of seasoned analysts with years

of experience and in-depth knowledge can

help you spot the underlying clues and create

the investment strategies that best suit your

commodity trading requirements.

EQUITIES* | DERIVATIVES* | COMMODITIES | CURRENCY* | MUTUAL FUNDS^ | IPOs^ | INSURANCE^ | DP* www.nirmalbang.com

Contact: 022 39269600 | E-mail: [email protected]. OFFICE: Sonawala Building, 25 Bank Street, Fort, Mumbai - 400 001. Tel: 022 - 39267500 / 7501; Fax: 022 - 39267510 CORPORATE OFFICE: B-2, 301/302, Marathon Innova, O� Ganpatrao Kadam Marg, Lower Parel (W), Mumbai - 400 013. Tel: 022 - 39268000 / 8001; Fax: 022 - 39268010BSE SEBI REGN No. INB011072759, INF011072759 & INE011072759, NSE SEBI REGN No. INB230939139, INF230939139 & INE230939139 DP SEBI REGN. No NSDL: IN-DP-NSDL-136-2000, CDS(I)l: IN-DP-CDSL-37-99, AMFI REGN. No. arn-49454 NCDEX REGN. NO. 00362, FMC Code-0075, MCX REGN. No. 16590, FMC Code-MCX/TCM/CORP/0490, MCX SX-INE260939139, PMS-INP000002981

Disclaimer: Insurance is a subject matter of solicitation. Mutual Fund investments are subject to market risk. Please read the scheme related document carefully before investing. Please read the Do’s and Don’ts prescribed by Commodity Exchange before trading. The PMS Service is not o�ering for commodity segment. *Through Nirmal Bang Securities Pvt. Ltd. ^Distributors #Prepared by Research Analyst of Nirmal Bang Commodities Pvt. Ltd.

apital markets regulator, Securities and Exchange Board of India (SEBI) recently issued fresh

guidelines for the issuance and listing C

SEBI has come up with a list of guidelines to revive municipal bonds, aimed at raising resources for urban infrastructure projects

of municipal bonds in India.

New rules will help revive the lifeless municipal bond market in India and deepen India’s capital markets.

Municipal bonds or munibonds as they are famously called abroad are bonds issued by a municipal corporation. These bonds are generally used to raise resources for

It’s simplified...Beyond Market 16th - 30th Apr ’1512

It’s simplified...Beyond Market 16th - 30th Apr ’15 13

information and improper ratings parameter by credit ratings agencies are other reasons for poor demand from pension and insurance funds. Further, lack of an active secondary market for municipal bonds has made this instrument illiquid.

On the supply side, the budgeting and accounting systems of ULBs still lack transparency. There is poor project evaluation. There are bureaucratic and political interferences. Further, there is no specific law, which governs the insolvency aspect of urban local bodies like corporates.

THE NEED

India is urbanizing like never before. The urban population is expected to rise to around 40% of the population by 2020 from around 31% currently. This projected growth will take urban population to approximately 65 crore by the year 2050 from around 35 crore at present.

Urbanizing is an irreversible phenomenon in India. The gradual increase in urban population will put a heavy strain on urban infrastructure.

This will lead to increase in demand for urban services including schools, roads, transportation, water supply, sanitation, health care, etc.

first tier, state governments and union territories comprise the second, while the urban and rural local self-governments (local bodies) make up the third tier.

Urban local bodies (ULB) are further divided into municipal corporations for larger urban areas, municipal councils for smaller urban areas, and nagar panchayat for rural-urban transition areas.

ULB can issue a municipal bond. At present there are 3,842 ULBs in India. Out of these, 139 are municipal corporations, 1,595 are municipalities and 2,108 are nagar panchayats. Rural local bodies are divided into district level, block level and village level.

From 1997 to 2010, several urban local bodies with strong balance sheets have been able to mobilize over ̀ 13 billion. However, since 2010 there has been no municipal bond issuance in India.

urban infrastructure projects as defined by law such as water supply, schools, sanitation, public health, transportation, etc.

Unlike shares that give no fixed returns, bonds give fixed returns to investors. The bond issuer (government, municipality or corporation) issues bonds with a promise to pay the holder of the bond on maturity a specified rate of interest during the lifetime of the bond.

Limited fiscal space available to the central government and higher infrastructure needs due to rapid urbanization warrant an alternative financing route like municipal bonds to finance infrastructure in India.

The government’s plan to create 100 smart cities across the country will need a vibrant municipal bond market to finance the plan. It also complements the cooperative federalism theme of the government.

Many developed and developing countries from around the world have relied extensively on the municipal bond market for their infrastructure funding needs. The United States and Canada have been the world’s largest market for municipal securities. In contrast, the decade-and-half-old municipal bond market in India is still in its nascent stage.

THE BEGINNING

It all started with the empowerment of urban local bodies (ULB) after the seventy-fourth amendment to the Indian constitution in 1992. The amendments empowered ULB to function as an institution and mobilize resources independently.

For starters, Indian federation for administration purposes is divided into a three-tier structure: Government of India comprises the

0

500

1000

1500

2000

2500

(` in million)

3000

3500

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Municipal Bond Issuance In India

India’s Population THE ISSUE

Even though municipalities were allowed by the government to issue tax-free bonds in 2001 to incentivize investors, the size of the municipal bond market remains meagre. This is mainly due to issues both on the demand and the supply side. On the demand side, big investors like insurance and pension funds still have a conservative approach to investment in municipal bonds. There is always the worry of who will guarantee these bonds. Lack of

1.8

1.5

1.2

0.9

0.6

0.3

01960 65 70 75 80 85 90 95 2000 05 10 15 20 25 30 35 40 45 50

Urban

(Forecast)(p

opul

atio

n in

bill

ion)

Rural

Traditionally, major sources of revenue for ULBs are property tax, profession tax, advertisement, user charges, fees or charges for usage of municipal assets and facilities; assigned revenues like share of entertainment tax, stamp duty, etc.

It’s simplified...Beyond Market 16th - 30th Apr ’1514

These revenue areas are not adequate to build infrastructure. ULBs also have relied on grants and subsidized funds provided by the Central and State governments for their needs. The government’s hands are tied due to limited fiscal space.

It is estimated that total investment requirements in urban infrastructure could exceed `7 lakh crore over the next 20 years.

NEW GUIDELINES

In this backdrop, SEBI issued new guidelines for the issuance and listing of municipal bonds. SEBI has balanced the needs of both the issuer and the investor of municipal bonds.

Investors

SEBI has mandated higher disclosure needs from the issuer. To ensure quality of the issuer, only the issuer that has not defaulted on its repayment obligations in the last one year will be allowed to tap the municipal bond market. The issuer should not have a negative net worth (total assets minus total liabilities) in any of the last 3 financial years. Further, the ULB will have to put in at least 20% of the project cost from internal accruals or from state grants. This will ensure their skin in the game. Besides, SEBI has mandated a

monitoring agency - which can be a bank or a financial institution - to keep a tab on the performance of these securities in the market.

Further, an investment grade rating is needed from a credit ratings agency. Better the rating, lower will be the cost for the issuer and lesser is the chance of the bond defaulting on its payments in the future.

For better servicing of urban local bodies, only revenue bonds i.e. municipal bonds that invest in a single project and have consistent operating revenue flowing (toll, octroi, etc), will be allowed for public issue. This will ensure regular interest payments and provide greater safeguard to investors.

Issuers

From an issuer’s perspective, the bonds would need to have a minimum tenure of three years. They can also issue general obligation bonds via private placements. A general obligation bond is a common type of municipal bond that is secured by a state or local government’s pledge to tax revenues to repay bond holders. This will ensure some sort of backing for ULBs with weak balance sheets. The proposed regulations also permit either the ULB itself or a subsidiary of the ULB to raise funds via the

municipal bond market. All these moves offer incentives for issuers to tap the municipal bond market.

IN A NUTSHELL

Ratings agency CARE estimates that large municipalities in India could raise `1,000 to `1,500 crore every year through municipal bond issues.

Should investors, therefore, invest in such bonds? The revised regulation will allow investors to make an informed decision before investing in municipal bonds. This will certainly attract institutional investors and pave the way for infrastructure building in the country.

A conservative retail investor mainly invests in fixed deposits, small savings schemes or gold. Bonds issued by municipalities having good financial track record can be a good alternative investment destination for such conservative investors, especially given the tax-free nature of some of these bonds.

Further, interest rates for municipal bonds are market-linked and investors can trade and exit on the exchanges and need not hold them till maturity. Municipal bonds are the best way to boost quality of life in cities with locals having a say in the process. Job prospects in that locality may also look uP.

Pareto-optimal / Pareto Efficiency:

An economic state where resources are allocated in the most efficient manner. Pareto efficiency is obtained when a distribution strategy exists where one party’s situation cannot be improved without making another party’s situation worse. Pareto efficiency does not imply equality or fairness.

Pareto optimality are conditions under which the state of economic efficiency occurs (where no one can be made better off by making someone worse off). The importance of pareto optimality results from its widespread use as a standard for comparing and judging outcomes. While pareto optimality provides only a weak standard because it does not provide a mechanism for discerning between the relative efficiency of competing pareto improvements, it offers standard judging criteria that many can comfortably accept in areas of economics, engineering and business.

he Indian life insurance industry has made significant progress since it was opened up to the private sector in the year 2000. Yet, penetration continues to be a big challenge for insurance

companies in the country. Only 2.3% of the Indian population is insured at present.

In order to enhance its reach and distribution, the life insurance industry has deployed a single corporate agency tie-up model in Bancassurance. Under this model, banks were allowed to tie-up with one insurer to distribute a life, non-life and an health insurance product.

Recently, the government passed the Insurance Act,

T

BreakingTradition

Bancassurance, through ‘open architecture’, will free banks to sell products of more than one life insurer unlike in the past that will help expand insurance penetration in the country

It’s simplified...Beyond Market 16th - 30th Apr ’15 15

It’s simplified...Beyond Market 16th - 30th Apr ’1516

25% to new business sales of private life insurers.

Consumers too, have been large beneficiaries of bancassurance as they have higher trust in banks and feel more comfortable about getting need-based advice and better quality of service from banks as compared to insurance agents.

Besides, there is also the ease of making premium payments on insurance products as they can be linked to their bank accounts directly.

WILL MULTIPLE CORPORATE AGENCY MODEL WORK

While a single corporate agency tie-up has worked well in the Indian context, a multiple corporate agency arrangement may indeed open up a Pandora’s box as customers already find it difficult to comprehend the various aspects of life insurance.

The nitty-gritties of the structure of the insurance product seem intimidating to them and they prefer to rely on the intermediary, be it the insurance agent or the bank selling the products to them.

If multiple corporate agency tie-ups come into place, bank employees will be forced to explain the features of multiple product options from more than one insurer, which will be available for each life stage need of the customer, further adding to his or her confusion.

Banks, on their part, will have to spend more time and resources to train and retrain their sales cadre on various aspects of products and processes of different insurers.

Besides, a large amount of investments will also have to be made to align their technology infrastructure to that of multiple

have tie-ups with only two insurance companies to begin with.

This is being thought of as an opportunity for the customized development of insurance products and an unique opportunity for consumers to experience the variety of products that several insurers will bring to the table.

But the question that remains to be answered is that in a country like ours where insurance is still a product, that is barely understood by customers, will a multiple corporate agency tie-up really achieve the goal of increased penetration of insurance products or will it turn into a nightmarish experience for banks and customers when deployed?

WHY SINGLE CORPORATE AGENCY TIE-UP HAS WORKED SO FAR

The single corporate agency model has worked well so far. This is because insurance products are not as easily understood as banking products. Yet, banks as corporate agents have spent a significant amount of time and engaged resources to understand products of single insurance companies they have had tie-ups with. Subsequently, they explained these products to their customers depending upon their financial needs and life stages.

This has emerged as a win-win model for banks as well as insurance companies. Banks see insurance products as another means of grabbing eyeballs of their customers and earning an income through fees by making a little investment.

Insurance companies, on the other hand, get the advantage of reach that has deluded them thus far. Little wonder then that bank channels currently contribute approximately

whereby insurance companies will have greater access to foreign direct investment (49% instead of the earlier 26%). Now, a change in the existing structure of bancassurance is being considered by the regulator.

The Insurance Regulatory and Development Authority or IRDA is keen on an open architecture for insurance distribution on the basis of the recommendations made by a committee headed by former LIC Chairman NM Govardhan. CHANGES IN THE OFFING

The Govardhan Committee had recommended that IRDA pave the way for banks to have multiple tie-ups with insurance companies.

This means that in lieu of the single corporate agency tie-up that exists currently, there will be multiple corporate agency tie-ups that will give consumers access to a wider range of products, thus increasing the penetration of insurance products across the nation.

The benefits of open architecture, for those who are propogating it, are plenty. According to those who have recommended these changes, currently, banks are forced to push a non-performing product just because they have a tie-up with the said insurance company.

A multiple corporate agency tie-up will encourage banks to select from amongst a plethora of insurance products that have a better cost structure and are more suited to the needs of their clients.

In order to avoid confusion, there is likely to be a cap on the number of insurers a bank can have with individual insurance companies, to help create a level-playing field. For instance, a bank may be allowed to

It’s simplified...Beyond Market 16th - 30th Apr ’15 17

insurance providers.

Another grave risk that banks will face is that of mis-selling as insurers are likely to create artificial sales limits on their products that may not be best suited to the needs of customers who will approach the bank at various life stages.

Banks too run the risk of being driven by profitability that each insurer brings to the table rather than concentrating on the needs of the customer. Both insurers as well as banks must, therefore, tread with caution as the controversy over Unit Linked Insurance Plans (ULIPs) has in the past, brought to the fore rampant mis-selling in which banks

sadly, had a significant role to play.

Therefore, there is also a grave risk of reputation being sullied, something that neither banks nor insurers can afford again.

WHY ROCK THE BOAT

While the concept of multiple corporate agencies is being considered on the premise of increasing penetration of life insurance industry, one must not forget the basic difference that banks and insurance companies have towards selling.

While banks have a reactive selling philosophy and sell demand-driven

products (pull strategy), insurance companies have an aggressive selling strategy that is need-driven (push strategy). These essential cultural differences between banks and insurance companies must be respected for any bancassurance venture to succeed.

IN A NUTSHELL

Perhaps the need of the hour is to not put spokes in the wheel, but ensure that the wheel of bancassurance, as it exists today, runs more smoothly and efficiently. This is likely to help achieve the core objective of penetration as well as ensure that customers’ need for insurance cover are adequately met by insurerS.

Registered O�ce: Nirmal Bang Securities Private Limited. 38-B, Khatau Building, 2nd Floor, Alkesh Dinesh Mody Marg, Fort, Mumbai - 400001. Tel: 3926 8600 / 01; Fax: 3926 8610Disclaimer: Insurance is a subject matter of solicitation. Mutual Fund investments are subject to market risk. Please read the scheme related document carefully before investing. Please read the Do’s and Don’ts prescribed by Commodity Exchange before trading. Through Nirmal Bang Securities Pvt. Ltd. *Through Nirmal Bang Commodities Pvt. Ltd. #Distributors investment in securities is subject to market risk. investment in securities is subject to market risk

EQUITIES | DERIVATIVES | COMMODITIES* | CURRENC Y | MUTUAL FUNDS# | IPOs# | INSURANCE# | DP

Contact: 022-39269600 | e -mail: [email protected] | www.nirmalbang.com

The most intelligent strategy in Chess is to be ready

with the next move. Similarly, currency trading

involves moves that are a combination of knowledge

and skill, backed by years of experience.

Currency Derivatives Trading with us keeps you a few

steps ahead, always.

CLEANAND

GREENRecent policy

announcements will give a thrust to the renewable energy

sector, especially solar energy and wind power

It’s simplified...Beyond Market 16th - 30th Apr ’1518

It’s simplified...Beyond Market 16th - 30th Apr ’15 19

support for these projects. Besides, the removal of excise duty on solar photovoltaic panels, reduction in custom duty and Renewal Energy Certificate (REC) are some of the policy measures initiated by the government to create a right policy environment for investments.

Subsidies are also granted by the Ministry of New & Renewable Energy (MNRE) to investors who set up their solar photovoltaic power plants in the north eastern region at 70% and to the others at 30%.

Through these initiatives, the government is trying to create a right policy and investment climate, which will be crucial for growth. That apart, thinking innovatively and coming out with smart solutions and speeding up implementation of projects will be critical as well.

The government is working to build a team of 50 countries to share and exchange new technologies and research advancements so that innovation can allow this source of energy to reach maximum people.

Prime Minister Narendra Modi has suggested installation of solar panels over all water bodies, which can be used for farming and watering of fields. In rural areas, input cost of farmers can be reduced by using solar pumps along with micro irrigation.

The government is also looking to set up hybrid energy parks in the area where sun’s radiation is high, thus tapping those high potential areas with large plants.

For instance, like in the coal and gas sector, the government plans to construct Ultra Mega Solar Power Projects or high capacity plants in radiation-rich states of Rajasthan, Gujarat, Tamil Nadu, and Ladakh in Jammu & Kashmir.

apid urbanization and industrialization have pushed the demand for power in the country.

However, supply is woefully inadequate in comparison with the demand, leading to huge deficit and power cuts in India. The problems will compound if the economy grows at a faster pace, leading to more demand in the sector.

Today, the challenge is to not only produce more power but also generate green power or renewable energy so as to rely less on fossil fuels due to their limited availability and environmental concerns. That apart, reliance on imported coal and gas is going to be a big challenge for the country, both in terms of viability of plans and the financial health of the economy in the coming years.

Of about 94% of the power generated through conventional sources of energy like coal and gas in present times, only about 5.2% of power is generated through renewable resources. The renewable energy space has thus far lacked intent, investments and right policies.

However, all this is set to change. Recently, at a conference, Minister for Power Piyush Goyal said India will raise its energy mix from renewables to 15% in 10 to 12 years from 6% now.

According to ministry data, the current installed power generation capacity of the country is 2,49,488 mw. Of this, renewables account for merely 31,692 mw.

This also indicates that India has huge untapped potential. The total estimated medium-term potential (till year 2032) for power generation from renewable energy sources such as wind, small hydro, solar, waste to energy and biomass in the country is

R about 1,83,000 mw, which is 14 times higher than the current installed capacity from these sources of energy. India is a developing nation and this step is aimed at reducing the country’s dependency on fossil fuels.

The government is expecting public and private sector investments in the sector. A total of 293 companies, including NTPC, Suzlon, and Reliance Power are expected to set up energy generating plants with a target of 26,600 mw energy generation in the next 5 years.

State Bank of India (SBI) is slated to lend `75,000 crore for generating energy upto 15,000 mw over the next 5 years. Apart from investments in power generation, the government is also looking to speed up the implementation of the Green Energy Corridor Project, in the current fiscal year, to facilitate evaluation of renewable energy across the country.

SOLAR

The Modi government has set a goal of reaching 1,00,000 mw of solar energy by 2022. India has a huge potential given its geographical advantages and huge expanse of deserts. Desert and barren land alone have the potential to build solar-based capacity of about 45,000 mw. The government has already directed companies to build solar power plants in the country.

In his Union Budget speech, Finance Minister Arun Jaitley called it a ‘high priority’ area and allocated `1,000 crore for the solar power sector, aiming to support investment in the renewable energy sector.

Not just announcements, the government has been doing road shows in international markets to attract investments. That apart, the government has offered budgetary

It’s simplified...Beyond Market 16th - 30th Apr ’1520

WIND POWER

Currently, India has a wind energy capacity of about 21,000 mw. However, this is nothing compared to its potential in India.

As per industry estimates, the country can increase its wind power generation capacity to 50,000 mw-1,00,000 mw, which is over 3 to 5 times higher than the current installed capacity.

Investments are now pouring in from both government and private sector companies, which are seeking to diversify and tap this potential source of renewable energy. On ground, the industry has suffered

in recent years due to the lack of adequate investments and policy revisions by the government.

Over the last two years, the wind sector has been awarded a mere 600-1,000 mw of projects, which are now gathering pace.

No wonder in 2014, the wind market grew at 44% compared to last year.

Thankfully, policies are again in place. The government recently restored the accelerated depreciation benefit for companies investing in wind projects, thus attracting a lot more investments.

That apart, power generation-based benefits which expired in 2012, were

again extended.

This allows existing power producers to again consider the renewable energy space as a strategy to diversify and have a mixed fuel portfolio.

Additionally, the government has eased policies pertaining to approvals, land acquisition and foreign direct investment (FDI) in wind power thus attracting huge investments into the country.

Almost all large wind energy producers, some of who left India early, are now promising higher investments and capacities in India because of clarity and commitment of the government towards the renewable energy sectoR.

Micro analysis.Mega gains.Trading at Nirmal Bang is based on extensive

research and in-depth analysis, where we focus

on the smallest of details and turn them into an

advantage for you.

Over the years, the analytical approach coupled

with decades of experience has helped us

maximize returns for our investors and thereby

inspire con�dence in them.

EQUITIES* | DERIVATIVES* | COMMODITIES | CURRENCY* | MUTUAL FUNDS^ | IPOs^ | INSURANCE^ | DP* www.nirmalbang.com

REGD. OFFICE: Sonawala Building, 25 Bank Street, Fort, Mumbai - 400 001. Tel: 022 - 39267500 / 7501; Fax: 022 - 39267510 CORPORATE OFFICE: B-2, 301/302, Marathon Innova, O� Ganpatrao Kadam Marg, Lower Parel (W), Mumbai - 400 013. Tel: 022 - 39268000 / 8001; Fax: 022 - 39268010

Disclaimer: Insurance is a subject matter of solicitation. Mutual Fund investments are subject to market risk. Please read the scheme related document carefully before investing. Please read the Do’s and Don’ts prescribed by Commodity Exchange before trading. The PMS Service is not o�ering for commodity segment. *Through Nirmal Bang Securities Pvt. Ltd. ^Distributors #Prepared by Research Analyst of Nirmal Bang Commodities Pvt. Ltd.

Contact at: 022-3926 9600 | e-mail: [email protected]

NORTH-SOUTHDIVIDE

While Delhi National Capital Region (NCR) is besieged with unsold inventory, Bengaluru is doing relatively well

thanks to sales of reasonably priced apartments

udget 2015 was arguably the most awaited one in recent years by Indian corporates. After years of

policy paralysis and economic slowdown, India Inc was hoping that the newly formed government will usher in necessary changes to improve economic sentiments.

Needless to say, when Finance Minister Arun Jaitley presented Union Budget 2015-16 in the Lok Sabha, corporate czars were eagerly awaiting announcement of reforms in their respective sectors.

This also included the Indian real

B estate sector, which has been facing a slump since a long time now, partly because of government policies and party due to its own shortcomings.

After the NDA-led government came to power, there were announcements regarding affordable housing, relaxation of FDI norms and construction of 100 smart cities in the interim Budget.

The real estate sector was expecting more such announcements as it meant revival of the sector. But Budget 2015 was a letdown for most real estate players as neither big-ticket announcements were made, nor direct

measures to boost the growth of the sector were announced.

According to Sanjay Dutt, Executive Managing Director, South Asia, Cushman & Wakefield, “Real estate is an important sector which can help the country achieve high growth. But the government missed the opportunity to use it to boost growth.”

A few industry experts are optimistic. They say schemes such as ‘Housing for All’ will help the growth of the sector in the long term. Under the ‘Housing for All’ scheme, by 2022, the government will build 2 crore urban housing units and 4 crore rural

It’s simplified...Beyond Market 16th - 30th Apr ’15 21

It’s simplified...Beyond Market 16th - 30th Apr ’1522

The condition of Mumbai real estate developers is not looking bright either. There has been a steady rise in debt level of Mumbai real estate companies due to slow property sales.

According to a report by Knight Frank, a real estate research and brokerage firm, Mumbai witnessed a 9% decline in property sales in 2014. This has resulted in inventory pile-up and would require a total of 50 months to clear existing stock at the prevalent absorption rate.

Under-constructed area worth `53,400 crore is lying unsold. Developers are neither able to sell these assets fast nor is their cash flow improving as industry experts believe that Mumbai real estate market is yet to recover.

New launches have also been subdued. In April-September period, new launches were down almost 51%. However, recently Mumbai Metropolitan Region (MMR) saw a number of new launches by developers such as Oberoi Realty, Lodha Group and Runwal Group.

Experts believe that for Mumbai and NCR markets, there is a huge lack of trust and confidence among buyers who fear investments would not reap near-term returns. Also, Mumbai developers have focused more on premium and luxury segments when demand was for affordable housing.

Pankaj Kapoor added, “On one side, there’s a housing shortage and on the other, you have rising inventory and that’s a very big paradox.”

While Mumbai and NCR have seen lacklustre growth, some markets such as Bengaluru and Chennai have been growing steadily. Bengaluru has become one of the fastest growing real estate markets in India, with growth seen in all segments such as

estate is only an indirect beneficiary.”

Experts believe that the beneficial impact on real estate because of REITs will take a few years to materialize. Moreover, increase in service tax will also affect the real estate market.

This is not good news for the troubled real estate market in Delhi National Capital Region (NCR). It has been suffering from project delays and severe liquidity crunch.

Among all the markets, Delhi NCR has been the worst affected. The house absorption rate is lowest in decades, with sales volume declining by 43% year-on-year in 2014. As a result, there has been a huge inventory pile-up.

According to a report by property research firm Liases Foras, NCR has a total of 303.48 million sq ft (about 3,03,000 apartments) of unsold real estate, which will require about 53 months to be completely sold off at the current pace.

One of the main reasons for this unsold inventory is uninhabitable localities. Builders have constructed apartments without providing necessary infrastructure like roads, sewage systems and water connections for the buyer.

Pankaj Kapoor, MD of Liases Foras says, “NCR is a very inefficient market where a lot of projects were launched in undeveloped areas.”

Even the organized retail space saw limited traction. Strong transaction happened only in the office space segment, which constituted 30% of the total transacted space. Major demand was driven by IT/ITeS, banking/financial services and telecommunication majors for their office space requirements.

housing units through allocation of `22,407 crore for housing development in the country.

According to Surabhi Arora, Associate Director, Research, Colliers International, “The intention to construct 6 crore housing units for rural and urban India by 2022 was a positive move. This will help to fill the huge demand-supply gap in housing sector and will make housing the next booming sector in India.”

Another important announcement was the introduction of the Benami Transaction Bill. Under this bill, cash transactions related to advances or payments of immovable property will be limited to `20,000. Once passed, this bill will help flush out black money from all sectors, especially real estate.

Also, the Finance Minister touched upon the much talked about Real Estate Investment Trusts (REITs). REIT is a security that sells like a stock on major exchanges and invests directly in real estate. It gives opportunity to individuals to invest in shares directly on an open exchange or in a mutual fund.

It will allow small savers to invest in real estate and enjoy the benefits of owning an interest in the securitized real estate market. The creation of REITs was approved in the last annual Budget and in this Budget, the Finance Minister announced allowing of pass-through status, which includes rental income also, wherein income generated would be taxed in the hands of the investor and the fund itself would not have to pay tax.

But, unfortunately, apart from these announcements, the real estate sector did not get much attention and as Anuj Puri, Chairman & Country Head, JLL India put it, “The Budget is low on big bang reforms and real

It’s simplified...Beyond Market 16th - 30th Apr ’15 23

luxury, mid-income housing and affordable housing.

The IT industry in Bengaluru has been a major driving force behind this growth, which has contributed to its multicultural population. Of all the office space transacted in India, the city of Bengaluru accounted for almost 50% transactions.

Among concluded transactions, Tech Mahindra committed around 1,40,000

sq ft in Goldhill Supreme, Walmart took up around 1,30,000 sq ft in Salarpuria Aura, and RBS Business Services leased around 1,00,000 sq ft in RMZ Ecoworld.

Bengaluru and Chennai are two places where most number of residential projects were launched by realty majors. According to a report by CBRE, a large section of new project launches were concentrated at Gudunvanchery, Tambaram, Siruseri,

Anna Nagar, Ambattur and Chembarambakkam in Chennai, as well as at Whitefield, Koramangala and Sarjapur ORR in Bengaluru.

Bengaluru developers have been able to push sales because they have priced their apartments reasonably. In India, where affordability of homes remains a key driver of demand, maybe it is time NCR and Mumbai developers looked at offering homes that are affordablE.

EQUITIES | DERIVATIVES | COMMODITIES* | CURRENC Y | MUTUAL FUNDS # | IPOs # | INSURANCE # | DPDisclaimer: Insurance is a subject matter of solicitation. Mutual Fund investments are subject to market risk. Please read the scheme related document carefully before investing. Please read the Do’s and Don’ts prescribed by Commodity Exchange before trading. The PMS Service is not o�ering for commodity segment. *Through Nirmal Bang Commodities Pvt. Ltd. #Distributors

BSE SEBI REGN No. INB011072759, INF011072759 & INE011072759, NSE SEBI REGN No. INB230939139, INF230939139 & INE230939139 DP SEBI REGN. No NSDL: IN-DP-NSDL-136-2000, CDS(I)l: IN-DP-CDSL-37-99, AMFI REGN. No. arn-49454 NCDEX REGN. NO. 00362, FMC Code-0075, MCX REGN. No. 16590, FMC Code-MCX/TCM/CORP/0490, MCX SX-INE260939139, PMS-INP000002981

Registered O�ce: 38-B, Khatau Building, 2nd Floor, Alkesh Dinesh Mody Marg, Fort, Mumbai - 400 001. Tel: 39268600 / 01; Fax: 39268610 Corporate O�ce: B-2, 301/302, 3rd Floor, Marathon Innova, O� Ganpatrao Kadam Marg, Lower Parel (W), Mumbai - 400 013. Tel.: 39268000 / 8001; Fax: 39268010

Contact at: 022 - 3926 9600E-mail: [email protected]

SECURINGAIRWAVES

The government fetched significant returns from spectrum auction after days of fierce bidding, with Idea Cellular emerging as the highest bidder

It’s simplified...Beyond Market 16th - 30th Apr ’1524

It’s simplified...Beyond Market 16th - 30th Apr ’15 25

These two players intend to take on Reliance-Jio Infocomm, a company owned by Mukesh Ambani and be early birds when it comes to offering high speed data. All in all, the government has been able to sell 89.8% of the total spectrum that was put up on sale.

Here is a detailed picture of the strategy adopted by each key player in buying spectrum:

a) Bharti Airtel

Bharti added fresh spectrum apart from few renewals of spectrums. In six renewal circles, Bharti was holding 40MHz in 900MHz band but it bought 50MHz. It added 900MHz spectrum in four additional circles apart from renewal circles.

The company had bought additional spectrum in 900 MHz from Reliance Communications (RCom) since RCom in those circles had not renewed 900MHz spectrum holding.

The company also showed active participation in 2100MHz. It bought the spectrum in seven circles, adding 6 new circles to the bouquet and top-up spectrum in Tamil Nadu.

In 1800MHz, the company partly renewed spectrum which was set to expire. However, it added spectrum in other circles and bought a total of 15.4MHz in the 1800MHz band.

It is quite clear that the addition of fresh spectrum in 2100MHz and 900MHz shows that Bharti Airtel is focusing majorly on developing and enhancing its data services offerings to its customers.

The company will have to pay `29,100 crore in total, which includes `7,800 crore as upfront payment to the government.

ndia’s telecommunications industry is at an interesting juncture. From being just call service providers, these

companies have come a long way.

The telecom companies are evolving to such an extent that efforts are being directed at replacing computer desktops with mobiles.

Today, thanks to the wide acceptance and adoption of 2G and 3G services, data and voice services are revolutionizing the way mobile handsets are being used.

Not only mobile, even Direct-to-Home (DTH), Internet Protocol television (IPTV) and other services are changing the way we browse the Internet, watch television and more importantly, the way we connect with people.

After the recent conclusion of spectrum auction by the government, it is quite clear that the battle to provide the aforementioned services seems to be tightening up.

The spectrum auction this time around was keenly observed and analyzed as it comes at a stage where data penetration in India is sweeping and deep.

Here is a low-down on the strategies that the already incumbent (well-established) players adopted to buy spectrum. We also present to you the set of players that would gain from the spectrum auction.

THE BASICS

Spectrum auction, which concluded on 25th Mar ’15, was open for 19 days. The industry’s spectrum investment stands at `1,09,800 crore. In comparison with reserve prices, spectrum prices were 64% higher for 800MHz, 111% for 900MHz, 16%

I for 1800MHz and 5% for 2100MHz. Recently, the Department of Telecommunications (DoT) declared the provisional winning price of all spectrums put up for auction. Here are key highlights of the auction by geography:

a. 900MHz spectrum was sold at 118% premium to reserve price. According to DoT, `7,400 crore for each MHz was paid for 17 circles where it was being auctioned.

b. 800MHz spectrum has been sold in 18 out of 20 circles where spectrum was made available.

For these 18 circles, the provisional winning price is 65% higher than the reserve price of `4,540 crore per MHz. 800MHz spectrum remained unsold in Karnataka and Tamil Nadu.

c. In Delhi, Maharashtra, Madhya Pradesh and Mumbai, 800MHz spectrum was sold at higher rates than 900MHz spectrum.

Analysts say that well-established telecommunications companies, also called incumbent telcos or operators, such as Bharti Airtel, Vodafone and Idea, have made spectrum-grabbing difficult and expensive for new entrants or smaller telecom companies in the industry by setting high benchmark prices.

STRATEGIES

Analysts say that incumbent operators renewed their majority of spectrum holdings across circles.

It is observed that Bharti and Vodafone focused on adding fresh spectrum in 2100MHz to offer 3G services in six new circles.

This addition of spectrum in 2100MHz has a long-term vision.

It’s simplified...Beyond Market 16th - 30th Apr ’1526

b) Idea Cellular

Idea Cellular renewed 54 MHz spectrum out of its total holding of 59 MHz in 900 MHz band. Circles like Andhra Pradesh, Punjab and Karnataka where Idea has foregone some of the spectrum have been bought by Bharti.

Idea bought 2100MHz spectrum in one new circle, which is Kolkata.

Idea will now have 3G offering on 2100MHz in 12 circles, while it has already launched 3G services on 900MHz band in Delhi (this spectrum was bought in the auctions held in February ’14 ).

Idea Cellular will have to shell out a total of `30,300 crore, which includes `7,800 crore as upfront payment to the Indian government.

c) Vodafone

Vodafone has bought 35.6MHz (this does not include Tamil Nadu since spectrum in that circle was not put up for sale) in 900MHz in comparison with its holding of 38.8MHz.

Vodafone has foregone spectrum in Maharashtra and Gujarat, while Idea added the foregone spectrum of Vodafone in Maharashtra.

The telecom company had lost 900MHz spectrum bidding in Gujarat, which it compensated by buying in 1800MHz.

Like Bharti Airtel, Vodafone actively participated in the 2100 MHz band and bought spectrum in as many as six new circles.

At present, it has 2100MHz spectrum in 15 circles. Vodafone will have to shell out `26,000 crore in total and `6,900 crore as upfront payment to the government.

d) Reliance Communications

Reliance Communications renewed its 900MHz holding in only two out of seven circles.

The company lost 900MHz in Odisha and North East. However, it compensated for the loss by purchasing 5MHz in 800MHz band.

Given these purchases, analysts opine that the company may shut operations in three circles - West Bengal, Assam and Bihar. It is estimated that these circles contribute around 16% of its adjusted gross revenues.

It bought a total of 26.3MHz in 800Mhz band, 10MHz in 900MHz and 11.8MHz in 1800MHz. Its total payout stands at `4,300 crore, which includes an upfront payment of `1,100 crore to the government.

e) Reliance-Jio (R-Jio)

Given the presence of Mukesh Ambani-owned Reliance-Jio, most analysts are keenly watching out for the strategy being adopted by the company to buy spectrum.

R-Jio’s focus remained in buying 800MHz spectrum and adding 1800MHz. The company bought 48.8MHz spectrum in 800MHz band with 5MHz across the circles.

It also added spectrum in 1800MHz in four new circles and added spectrum in two existing circles. In total, it bought 28MHz spectrum in 1800MHz band. The company will pay a total sum of `10,100 crore, which has an upfront payment of `2,700 crore to the government.

f) Tata Teleservices

The company’s focus was in 800MHz band where it bought 11.3 MHz in five circles by shelling out `7,200

crore. In 1800MHz, it bought 2.6 MHz spectrum in Andhra Pradesh.

At present, the total payment due from Tata Teleservices stands at `7,800 crore. Of this, it has to pay `2,000 crore as upfront payment to the government.

g) Aircel

The company only bought 10MHz in 1800 MHz band with a total payout of `2,200 crore which includes an upfront payment of `740 crore.

Most analysts are of the opinion that regulatory issues concerning network of telecommunications companies would not be a concern in the coming years. They estimate that FY15 auction would be the last big renewal auction for telcos. It is believed that the next renewal auction is in 2021, which is mainly for CDMA telcos.

Given these factors, it is estimated that the top three telcos, namely, Bharti Airtel, Vodafone and Idea, would be in a better position to make the most of higher spectrum and offer high quality data services.

These companies have not renewed their 900MHz spectrum, which analysts say will help them reduce network disruptions.

Also, by securing 2100 MHz, the top three telcos will be able to gain market share in data services in the long term.

For new entrants, given the size of their balance sheets and presence, a large amount of funds will be used to service their interest expense.

Through price-war and deep pocket presence in smaller cities in the country, new entrants may also gain some market share in voice and data service offeringS.

ndia’s construction sector has been sluggish since the past few years as irrational bidding and fall in traffic estimates in

road projects due to economic slowdown has exhausted the bidding appetite of roads developers.

However, things are set to change with the government initiating steps to boost the beleaguered construction industry in the country.

THE RECENT PAST

In the past seven years ending FY14, analysts have estimated that the construction sector contributed close to 7.8% (at constant prices) to India’s GDP through two primary segments:

I

The government has announced a series of tangible initiatives to boost the beleaguered construction sector

buildings and infrastructure.

While buildings comprised residential, commercial, institutional and industrial; infrastructure encompassed rail, road, dams, irrigation, airports, power, telecommunication systems and urban infrastructure like water supply, sewerage, drainage as well as rural infrastructure in the country.

Between FY13-FY14, the construction sector’s growth declined at a compounded annual growth rate of 1.4% from 7.8% between FY07 and FY12 mainly on account of policy hurdles like environmental clearances and land acquisitions on fresh investments.

Despite this, business activity in the construction sector, has remained more or less stable.

With the new government at the centre, there is revival in growth in the construction sector.

According to the first quarter GDP growth numbers of the present fiscal, the construction sector grew by 4.8% on a year-on-year basis. This was much higher than the average growth of 1.4% in FY13 and FY14.

The BJP-led NDA government at the centre is implementing effective policies as well as granting faster clearances of stuck infrastructure projects in the country.

CONCRETESTEPS

It’s simplified...Beyond Market 16th - 30th Apr ’15 27

It’s simplified...Beyond Market 16th - 30th Apr ’1528

terms have been changed to lump-sum from item rate contracts. Contractors will now be paid only after the completion of a specific stage or length of the road.6. The Ministry of Road Transport & Highways (MoRTH) has signed a memorandum of understanding (MoU) with the Ministry of Railways to remove all infrastructural hurdles related to the construction of Road Overbridge (RoBs)/ Road Underbridge (RuBs) on national highways.7. The Reserve Bank has allowed banks to issue long-term infrastructure bonds, which are exempt from CRR, SLR and priority sector lending requirements.

Moreover, the government proposes to amend the Land Acquisition Act, which will lead to faster execution of infrastructure projects.

RESULTANT IMPACT

These initiatives are paying off. There are signs of business activity gaining momentum in the past few months. The MoEF granted environment clearances to 232 projects between May ’14 and November ’14.

The government awarded contracts to construct 3,419 kms of roads in the April-October ’14 period, which is 40% of the total target of 8,500 kms in FY15 and much higher than 1,116 kms and 1,436 kms awarded in FY13 and FY14, respectively.

And the total road construction was 1,984 kms during April-October ’14 (31% of target of 6,300 kms in FY15), which is far higher than 637 kms constructed in FY14.

Besides, competitive pressures seem to be easing in the past few months. There is higher inflow of orders with better margins for players from the construction space.

has been changed to immediate exit of FDI, either post completion of the project, or after that

II) Policy Reforms

There have been significant changes in policies too to pace up growth of the construction sector. These changes are primarily for railways and road segments. Here are the changes in policies:

Railway

1. Up to 100% FDI allowed in key areas, such as freight corridor, high-speed trains, ports and mining connectivity projects through different modes.2. Up to 100% FDI permitted in most cases in rail projects, such as gauge conversion, construction of new lines, doubling of new lines and maintenance of Public Private Partnership (PPP) projects.

Roads

1. E-clearance for infrastructure and industrial projects in order to quickly clear stalled projects by the Ministry of Environment & Forests.2. The government plans to relax exit rules for road developers by allowing 100% exit after two years from project’s commissioning against a minimum 26% holding.3. NHAI is considering re-drafting of the Model Concession Agreement (MCA) to give itself more power for stuck bids, re-bidding and cancelled projects that fail to meet expected conditions.4. The cabinet has approved the formation of an independent entity called ‘National Highways Connectivity Company Ltd’, which will supervise the execution of road projects by NHAI, BRO and state PWDs.5. In order to speed up the execution of road projects awarded, payment

GOVERNMENT INITIATIVES

In Union Budget 2015-16, the government proposed the linking of 1,78,000 unconnected habitations by all-weather roads. This means completing construction of 2,00,000 kms of roads. This development is likely to help construction companies to acquire fresh orders.

Some of the prominent measures taken by the government are relaxation in construction FDI, 100% FDI in railways, e-clearance for infrastructure and industrial projects, and long-term bonds by banks.

Of these, two key policy initiatives are relaxation of FDI norms and policy changes. I) FDI In Construction

It is estimated that in the two-and-a-half years ending first quarter of FY15, FDI in the construction sector fell far below its 14-year average of US$ 1,705 million, down by 8.2% on a year-on-year (y-o-y) basis in FY14.

Here are a few norms relaxed in case of FDI in construction projects: 1. No minimum land area criteria for the development of serviced plots, as compared to the earlier norm of minimum 10 hectares.2. Minimum floor area reduced to 20,000 sq mt from 50,000 sq mt for construction-development projects.3. Minimum FDI cap lowered to US$ 5 million from US$ 10 million and will need to be brought within 6 months from the start of the project. Subsequent FDI can be brought within 10 years from the start of the project or before its completion.4. The earlier condition of at least 50% of project to be developed within five years has been removed.5. The minimum lock-in period of three years after project completion

EQUITIES | DERIVATIVES | COMMODITIES* | CURRENCY | MUTUAL FUNDS | IPOs | INSURANCE | DP# # #

QUAL AT NIRMAL BANG, YOU’RE MORE THANJUST A BUSINESS ASSOCIATE,YOU’RE AN EQUAL PARTNER.

Contact Person: Gaurav Mohta - 07738380299Nilesh Sonawane - 07738380027

Address: B-2, 301/302, 3rd Floor, Marathon Innova, O�. G. K. Marg, Lower Parel (W), Mumbai - 400013.

BSE SEBI REGN No. INB011072759, INF011072759 & INE011072759, NSE SEBI REGN No. INB230939139, INF230939139 & INE230939139 DP SEBI REGN. No NSDL: IN-DP-NSDL-136-2000, CDS(I)l: IN-DP-CDSL-37-99, AMFI REGN. No. arn-49454 NCDEX REGN. NO. 00362, FMC Code-0075, MCX REGN. No. 16590, FMC Code-MCX/TCM/CORP/0490, MCX SX-INE260939139, PMS-INP000002981