Embed Size (px)

Citation preview

The Quality of Institutions and Foreign Direct Investment

Christian Daude (*) University of Maryland at College Park

Ernesto Stein

Inter-American Development Bank

March 2001 This Version: February 2004

Abstract We study the role of the quality of institutions as a determinant of the location of FDI, using bilateral FDI stocks from OECD countries around the world. While the literature has placed special emphasis on the role of corruption on FDI, we explore a wider range of institutional aspects. We find that better institutions have overall a positive and significant effect on FDI. Especially, unpredictability of policies, excessive regulatory burden, deficient enforcement of property rights, and lack of commitment on the part of the government play a major role in deterring FDI flows. JEL Codes: F15, F23 Key Words: Foreign Direct Investment, Institutions We gratefully acknowledge helpful comments and suggestions made by Eduardo Levy Yeyati, Eduardo Lora, Alejandro Micco and Shang-Jin Wei, as well as participants at the 2001 Latin American Meeting of the Econometric Society and the VI Annual Meeting of the LACEA. The views expressed in this document are the authors� and do not necessarily reflect those of the Inter-American Development Bank. (*) Corresponding Author. Email: [email protected], 3105 Tydings Hall., Department of Economics, University of Maryland at

College Park, MD 20742, USA.

1

1. Introduction

One of the most notorious features of the trend towards globalization in recent times has

been the increased importance of foreign direct investment (FDI) around the world. Over

the last couple of decades, worldwide FDI flows have grown by a factor of almost 10. To

put this evolution in perspective, trade flows around the world, by comparison, only

doubled during a similar period. In this context, a deeper understanding of the

determinants of the location of multinational enterprises is becoming more and more

relevant for the design of successful policies to attract investors.

While the literature has focused mainly on the effects of corruption on FDI, we analyze a

broader set of institutional variables that may affect the decision of foreign investors to

undertake investment projects in a particular country. This allows us to assess what

dimensions of the quality of governance institutions affect foreign investors� location

decisions more. In addition, we use institutional indicators from several different sources

such that we can analyze the robustness of our results.

Corruption may deter investment by increasing the cost of doing business, as investors

need to bribe officials in order to obtain licenses and permits. In addition, corruption may

increase uncertainty, which may deter investment as well. According to Shleifer and

Vishny (1993), the secrecy of corruption is what makes it much more distortionary than

taxes. A standard reference in the empirical literature of FDI location decisions is

Wheeler and Mody (1992). They find that a composite measure of risk factors, which

2

includes institutional variables such as the extent of bureaucratic red tape, political

instability, corruption and the quality of the legal system, does not affect the location of

US foreign affiliates.1 However, their index aggregates these variables together with

others such as attitudes towards the private sector, living environment, inequality, risk of

terrorism, etc, making it impossible to assess the role of individual variables. In

particular, the question of whether any of the institutional aspects have a significant

impact on FDI is left unanswered. The first systematic empirical study on this topic is

Mauro (1995) who shows that corruption has a negative impact on the ratio of total and

private investment to GDP and therefore causes harm to economic growth. Wei (2000),

using data on bilateral FDI stocks from OECD countries, finds that corruption has a

significant and negative impact on FDI. He finds that an increase in the level of

corruption from Singapore to that of Mexico is equivalent to increasing the tax rate on

multinationals by more than twenty percentage points. In addition, Wei (1997) using the

same database, finds that uncertainty regarding corruption has also important negative

effects on FDI location.

However, investment decisions may depend on different dimensions of public institutions

in addition to corruption, like the regulatory framework, the predictability of economic

policy, the protection of property right, or the efficiency of law enforcement. In this

paper, we provide evidence on the impact of these different dimensions of governance

institutions on the location of FDI. In addition, we use different types of institutional

1 Wheeler and Mody's risk factor variables are from the Country Assessment Service of Business International.

3

variables based on experts� reports, surveys and a combination of both in order to ensure

the robustness of our results.

A different literature that is related to the present paper includes Albuquerque (2003),

Aizmann and Spiegel (2002), Hausmann and Fernández-Arias (2000), as well as Mody et

al (2003). This literature focuses on the effects of institutions on the composition of

capital flows. Albuquerque's paper develops an imperfect enforcement model, where FDI

has a risk-sharing advantage over other capital flows, because it contains more intangible

assets that are inalienable and make FDI therefore less attractive to expropriation. The

optimal contract implies that share of FDI in total capital flows is higher for financially

constrained countries. In a set of cross-country regressions with the average FDI shares in

gross private capital flows as dependent variable and controlling by GDP per capita and

trade openness, he finds that the ICRG variable of Law and Order2 has a negative but not

significant effect. However, once credit ratings are included in the regression, the

institutional quality has a positive and significant effect on the FDI share. Mody et al

present a model where multinational firms have an advantage over domestic firms in the

screening process of projects with a noisy signal concerning their real level of

profitability. In this context, the value of this advantage is decreasing in the host country's

degree of corporate transparency. Thus, their model predicts that the proportion of FDI in

comparison to portfolio investment is lower in countries where institutions are more

transparent. They present empirical evidence in favor of this prediction, using an index of

creditors' rights from La Porta et al (2000) in a gravity model to explain the ratio of FDI

flows to trade. Aizmann and Spiegel present an efficiency wage model where ex-post 2 Since we also use this variable, we will explain its construction in more detail in the next section.

4

monitoring costs and enforcement of labor contracts are lower for domestic firms than for

multinationals, but the later are more productive. In this situation, multinationals will be

more sensitive to changes in the enforcement cost (quality of institutions) and pay higher

wages than domestic firms do. They find that the share of FDI to gross fixed investment,

as well as the ratio of FDI to private domestic investment, is negatively and significantly

correlated with the level of corruption, such that FDI seems to be more sensitive than

domestic investment to the institutional quality. Finally, Hausmann and Fernández-Arias

study the effects of institutional variables on the composition of capital inflows, using six

different institutional variables compiled by Kaufmann et al (1999a), as well as indices of

creditor and shareholder rights from La Porta et al (1998).3 The authors find that better

institutions lead to a reduction of the share of inflows represented by FDI. They conclude

that, in comparison to FDI, other forms of capital are more sensitive to the quality of

institutions. When they look at the effects of their institutional variables on FDI as a share

of GDP, only a small subset of the institutional variables � regulatory quality,

government effectiveness and shareholder rights - remain significant after including some

controls. Their summary index of institutions, the first principal component of the six

institutional variables of Kaufmann et al, does not have significant effects on the ratio of

FDI to GDP.

One limitation of these studies is that they all test some prediction of their models in an

ad-hoc econometric model controlling for other possible determinants of FDI as GDP per

capita, openness, size, etc. Given this ad-hoc formulation and the fact that they use

3 The institutional variables from Kaufmann et al (1999a) are regulatory quality, voice and accountability, government effectiveness, political stability and lack of violence, control of corruption and rule of law. We will describe these in more detail below, as we will use them here as well.

5

different institutional variables, it is difficult to determine the source of the qualitative

and quantitative differences in their results.

Unlike these studies, our focus is on FDI per se, rather than on the composition of capital

inflows. As in Wei (1997, 2000), we use bilateral data on FDI stocks from the OECD

International Direct Investment Statistics, but we use a wider range of institutional

indicators. The use of bilateral data allows us to use a much richer set of control

variables.

Another contribution of our paper is that we avoid the shortcoming of the existing

empirical literature, especially the studies that analyze the effects of the some

institutional dimensions on FDI as Wheeler and Mody (1992), Hausmann and Fernández-

Arias (2000), Wei (1997, 2000), and Mody el al (2003), that they rely on ad-hoc

empirical formulations. In this sense, we test the significance of the quality of institutions

on FDI in an empirical model that follows recent developments in the theory of

multinational enterprise location (see Markusen, 1997 and 2001) more closely. Carr, et al

(2001) and Blonigen et al (2002) have used very similar econometrics specifications

recently.

The rest of the paper is organized as follows: In Section 2, we present the data, and

discuss our empirical strategy. Section 3 presents our main results on the institutional

quality as a determinant of the location of FDI. Section 4 presents some sensitivity

analysis, and Section 5 concludes.

6

2. Data and Empirical Strategy

FDI Data

We use bilateral outward FDI stocks for 1998 from the OECD International Direct

Investment Statistics in millions of dollars. The dataset covers FDI from 20 source

countries, all of them from the OECD, to 58 host countries.4 By using outward stocks, we

ensure that differences across countries in the definition and measurement of FDI do not

alter the relative allocation of FDI for each of the source countries. Wei (1997, 2000) has

used this database previously to study the effect of corruption on FDI. Levy Yeyati et al

(2003) use these data to analyze the relationship between FDI and regional integration,

while Blonigen et al (2002) have used it to test empirically different theories of FDI.

Institutional Variables

In order to assess the role of institutions as a determinant of the location of FDI, we will

use several institutional variables drawn from different sources. The first set of

institutional variables is the governance indicators database developed by Kaufmann et al

(1999a). These indicators are constructed based on information gathered through a wide

variety of cross-country surveys as well as polls of experts. The authors use a model of

unobserved components, based primarily on data for 1997 and 1998, which enables them

to achieve levels of coverage, for each of their indicators, of approximately 160

4 Thus the number of observations is 20x(58-1)=1140. However, data availability in our regressions will reduce the effective number of observations to around 700.

7

countries.5 They construct six different indicators, each representing a different

dimension of governance: Voice and Accountability, Political Stability and Lack of

Violence, Government Effectiveness, Regulatory Quality, Rule of Law, and Control of

Corruption. This clustering of institutional indicators into different dimensions allows us

to study whether some dimensions of governance matter for FDI location, while others do

not. Kaufmann et al (1999a) standardized their indicators so that they all have mean zero

and a standard deviation of one; in all cases larger values indicate better institutions.6

Voice and Accountability, as well as Political Stability and Lack of Violence aggregate

those aspects related to the way authorities are selected and replaced. The first variable

focuses on different indicators related to the political process, civil rights, and institutions

that facilitate citizens� control of government actions, such as media independence. The

second variable combines indicators that measure the risk of a destabilization or removal

from power of the government in a violent or unconstitutional way.

The indicators clustered in Government Effectiveness and in Regulatory Quality are

related to the ability of the government to formulate and implement policies. The first

variable aggregates indicators on the quality of bureaucracy, the competence of civil

servants, the quality of public service provision and the credibility of the government�s

commitment to its policies. The second brings together indicators related to the content of

5 For more technical details see Kaufmann et al (1999b). 6 In our empirical work, we re-standardize these variables to have mean zero and standard deviation of one in our own sample, in order to simplify the interpretation of the coefficients, as well as the comparison of their relative importance.

8

policies, like the existence of market-unfriendly regulations such as price controls and

other forms of excessive regulation.

The last two variables, Rule of Law and Control of Corruption, consider aspects related to

the respect, on the part of both citizens and the government, for the institutions that

resolve their conflicts and govern their interactions. The first one includes variables that

measure the perceptions on the effectiveness and predictability of the judiciary, as well as

enforceability of contracts, while the second aggregates different indicators of corruption.

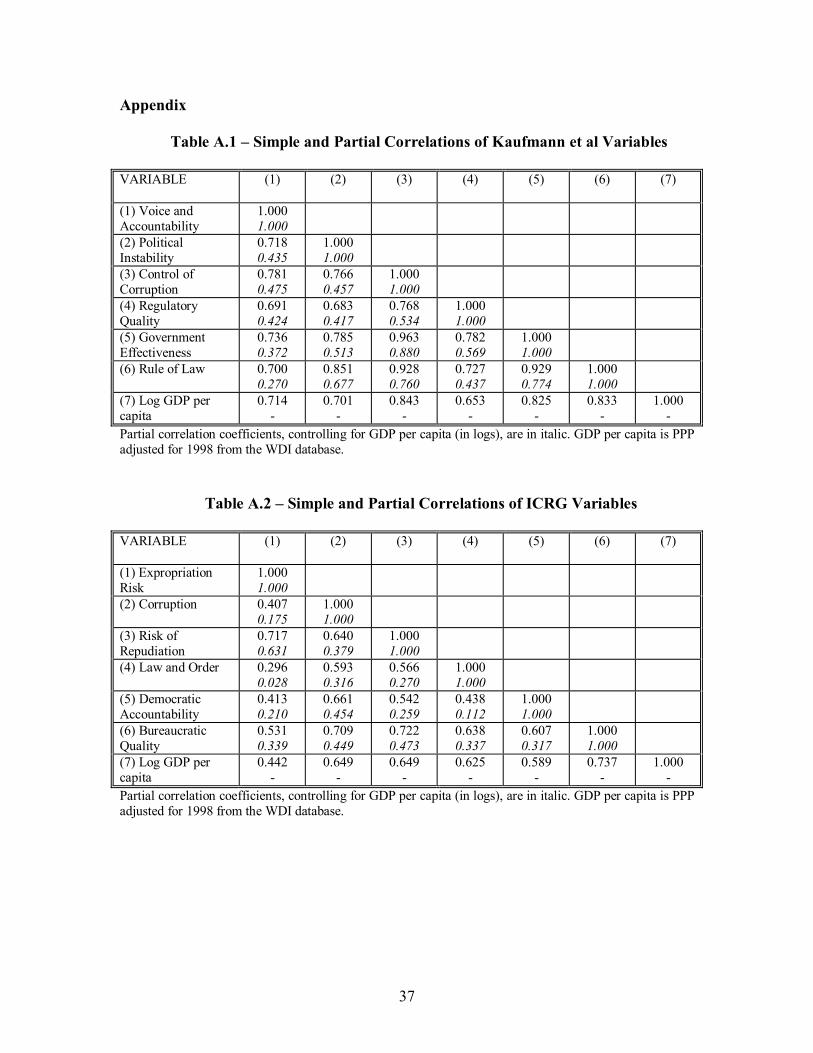

In Table A.1 of the Appendix, we present the simple correlations between the six

variables, and the partial correlation between them controlling for GDP per capita. There

is a remarkably significant correlation between the variables, even when controlling for

GDP per capita. For example, in our sample, the simple correlation between Rule of Law

and Control of Corruption is 0.93 and it remains at 0.76 once we control for GDP per

capita.

As Mauro (1995) points out, there may be good reasons to expect this positive correlation

between most variables. For example, Krueger (1993) argues that corruption may induce

a less efficient bureaucracy since officials may introduce requirements and additional

obstacles in order to receive bribes. However, from an econometric point of view this

correlation induces serious problems of multicollinearity and limits the extent to which

the relevance of each institutional dimension can be identified. The most standard

solution is to group those variables that capture similar dimensions. In this sense, in

9

several regressions we will use the average of Voice and Accountability and Political

Stability and Lack of Violence as Political Stability and Freedom, while we group Rule of

Law, Control of Corruption, Government Effectiveness and Regulatory Quality as

Government Efficiency.7

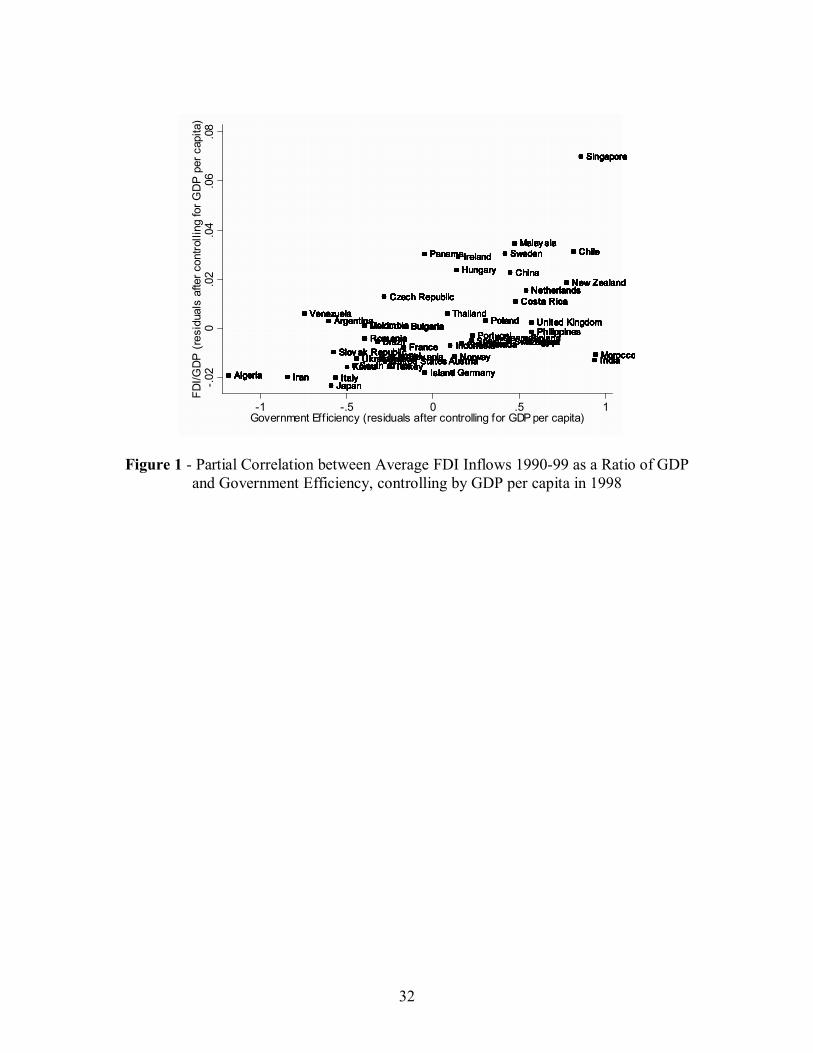

In Figure 1 we plot the ratio of average FDI inflows to GDP in the 1990's and

Government Efficiency � after controlling for GDP per capita - for the countries that will

be considered in our subsequent regression analysis. There is a strong positive and

significant partial correlation between this institutional variable and the rate of FDI to

GDP.8

[Insert Figure 1]

A second source for institutional variables is the International Country Risk Guide

(ICRG) compiled by the PRS Group. Unlike those of Kaufmann et al (1999a), these

indicators rely exclusively on polls of experts. The variables we consider are a subset of

the ones available from the ICRG database for the year 1995. Specifically, we use the

Risk of Repudiation of Contracts by the Government, Risk of Expropriation, Corruption

in Government, Law and Order, Bureaucratic Quality, and Democratic Accountability.9

While the first three variables are coded on a 0 to 10 scale, the last three are coded

7 This grouping may also reduce measurement problems of the individual components. 8 These results are reasonably robust to the fact that Singapore could be an influent outlier. The partial correlations between government efficiency and the ratio of FDI to GDP are 0.48 and 0.43 if we include or not Singapore, respectively. Both coefficients are significant at 99% of confidence. 9 Knack and Keefer (1995) use most of these variables: Risk of Repudiation of Contracts by the Government, Risk of Expropriation, Corruption in Government, Rule of Law, and Bureaucratic Quality.

10

between 0 and 6. In order to facilitate comparability we standardize all variables in our

sample to mean 0 and unit variance. In all cases, higher rankings imply better institutions.

In Table A.2 we present the correlation matrix for these indicators. As in the case of the

previous dataset, the ICRG variables are all positively correlated.

A third source of institutional variables is the World Business Environment Survey from

the Worldbank. This survey was conducted between 1999 and 2000, collecting

information regarding constraints to business activities that firms face, including

institutional and governance aspects. The sample covers 80 countries and approximately

100 enterprises in each country. The advantage of this kind of surveys is that they report

in a more accurate way the perception of entrepreneurs about the different risks and

constraints their business faces rather then relying on an expert�s perception about these

issues. In this sense, by using variables constructed on survey information it is possible to

reduce the subjectivity bias mentioned above. However, it should be kept in mind that the

main purpose of this survey is to ensure a representative measure at a country level, but

their comparability across countries may be lower than in the case of indicators based on

subjective perceptions of experts.

We consider the average by country of the answers to the following questions in the

survey: i) Quality of the courts (1 very good to 6 very bad); ii) Quality of central

government (1 very good to 6 very bad), iii) Corruption is a general constraint to do

business (1 no obstacle to 4 major obstacle), iv) Changes in economic and financial

policies are predictable (1 completely predictable to 6 completely unpredictable); v)

11

Change in law and regulations are predictable (1 completely predictable to 6 completely

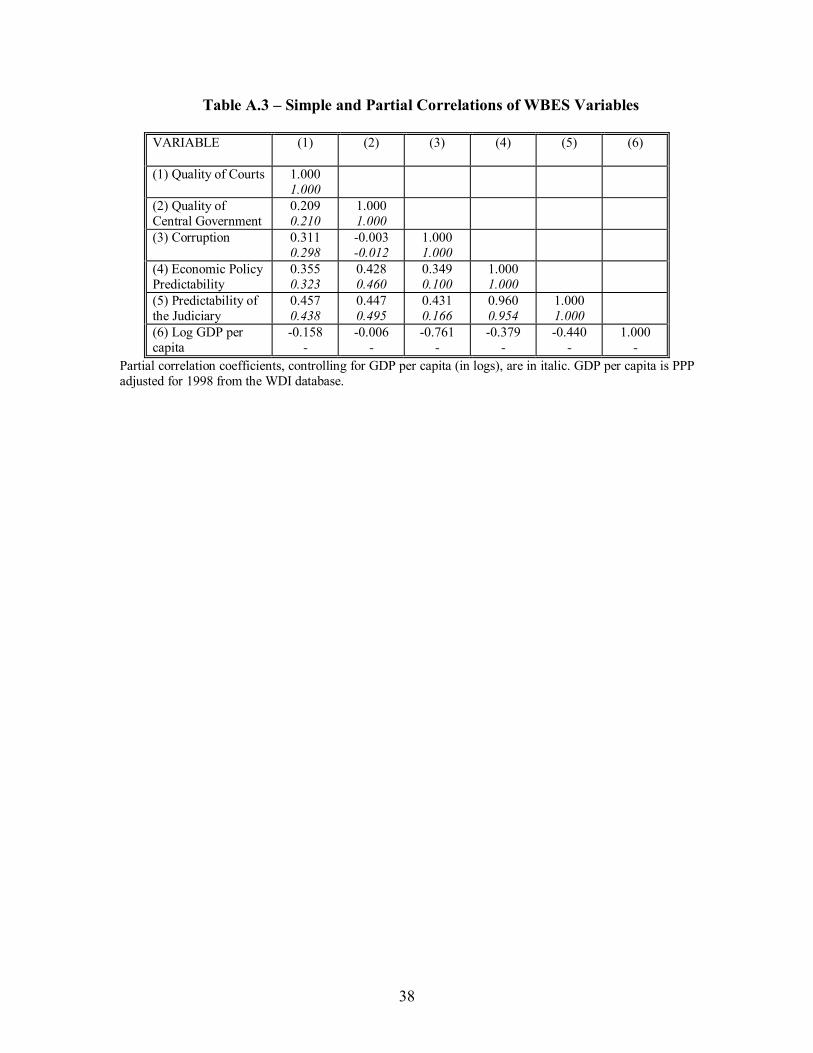

unpredictable).10 The correlation matrix is presented in Table A.3.

A fourth group of variables is composed by some more �objective� measures that have

been used in the literature as proxies and/or instruments for institutions. From Barro

(1991) we consider the average number of revolutions and successful coups per year, as

well as the number of assassinations per thousand inhabitants per year during the 1980�s.

These variables have been used in the empirical growth literature (see Barro, 1991) to

analyze the effects of political instability and crime on cross-country growth rates. From

Hall and Jones (1999) we take the fraction of the population that speaks English. Hall and

Jones use these variables to instrument their variable of social infrastructure in cross-

country regressions to explain the difference in GDP per capita levels. We also include

dummies regarding the origin of the legal code that have been used by La Porta et al

(1999) as explanatory variables of the quality of governance institutions. In addition, we

consider an index of ethnic fragmentation by Mauro (1995) who uses this indicator as an

instrument for his institutional variables. Finally, Acemoglu et al (2001) provide an

interesting instrument for institutions that is the mortality of settlers in former colonies.

We use this group of variables as instruments for institutions in our regression analysis.

10 Note that in this case, higher values of the variables represent a lower level of institutional quality. The database, a detailed description of the survey and related papers can be downloaded at http://www.worldbank.org/privatesector/ic/ic_resources.htm. We have also considered the WDR 1997 database that formulates very similar questions but covers fewer countries. The results do not differ from those presented here for the WBES and are available upon request.

12

The use of these different types of variables to study the effects of institutional variables

on the location of FDI should provide us with a good sense of the robustness of our

results.

Empirical Strategy

Most of the empirical studies of FDI location are based on the gravity model, which is a

standard specification in empirical models of bilateral trade.11 In its simplest formulation,

it states that bilateral trade flows (in our case bilateral FDI stocks) depend positively on

the product of the GDPs of both economies and negatively on the distance between them.

Typical variables added to the simplest gravity specification in the trade literature include

GDP per capita, as well as dummies indicating whether the two countries share a

common border, a common language, past colonial links, etc.

While in the trade literature the gravity model has good theoretical foundations, the use

of this model for the case of FDI is somewhat ad-hoc. Although we will look at the

results of the standard gravity model for reasons of robustness, we base our empirical

evaluation of the effects of the different institutional variables on FDI on an empirical

model recently developed by Carr et al (2001) which in turn follows closely a theoretical

model of location of multinational activity developed by Markusen (1997, 2001).

11 For a discussion of the empirical application and theoretical foundations of the gravity equation in trade theory see Frankel (1997). Papers that have used the gravity model to study the location of FDI include Wei (1997, 2000), Mody et al (2003), Stein and Daude (2002) and Levy-Yeyati et al (2003).

13

The model incorporates horizontal and vertical motives for FDI. The type of FDI that is

observed between two countries is determined endogenously in a general equilibrium

framework considering a two-country, two-factor, two-good world. The types of firms

that can arise in this context are: horizontal firms with plants in both countries and

headquarters in one, vertical firms that have a single production facility in one country

and headquarters in the other country, and national firms that maintain headquarters and

the production plant in only one country and may serve the other market through trade.

One good (A) is produced in a competitive industry with constant returns to scale using

unskilled labor, while the other good (B) is produced under imperfect competition with

increasing returns to scale at the firm level due to R&D, and management services. The

model includes similar assumptions as earlier models of vertical FDI as Helpman (1984),

Helpman, and Krugman (1985) such as the possibility of fragmenting the production and

the location of the headquarters and the operational plant. Also, plant scale economies are

assumed for this sector. Finally, a key assumption of the model is the factor intensity in

the different production facilities. In this sense, headquarters activities are the most

skilled-labor intense, followed by the firm that produces good B and has headquarters in

the same location. Moreover, a production plant in sector B is supposed to be less skilled-

labor intensive than the former, but more intensive than one in sector A. It is clear that

while differences in factor endowments tend to favor vertical FDI, firm level economies

of scale would favor horizontal FDI, given the existence of trade costs.

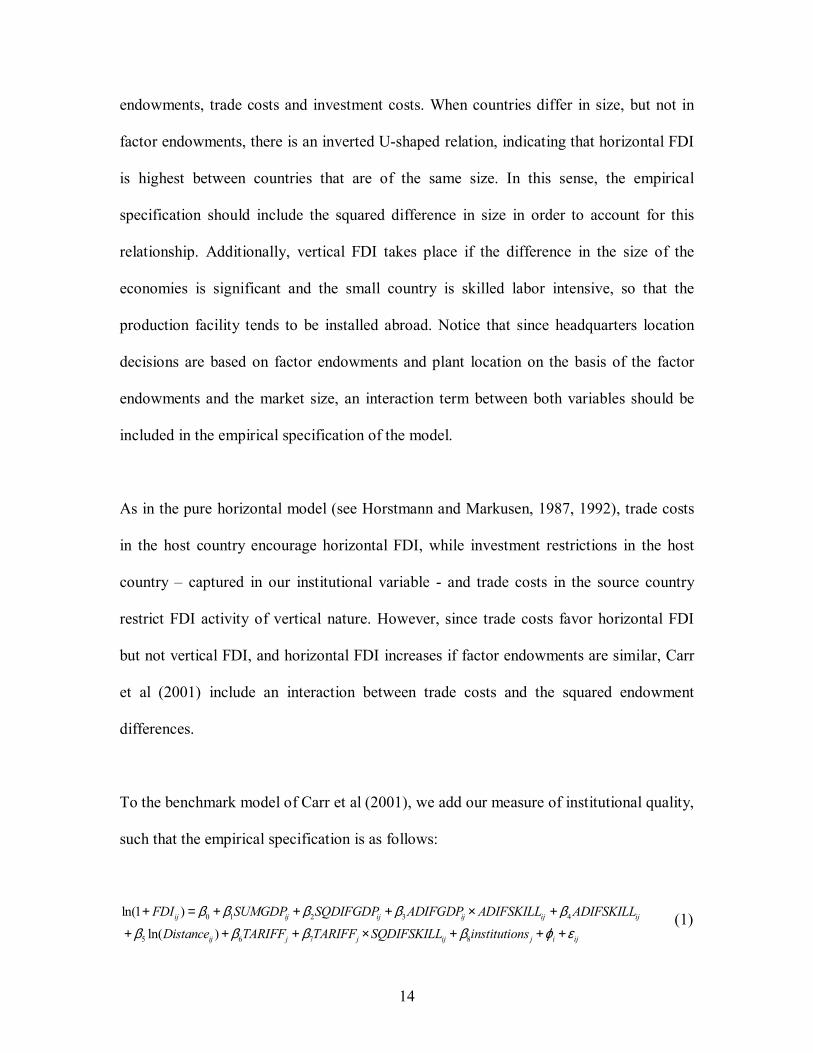

The type and volume of FDI between two countries depends on the size of each

economy, differences in the size between the host and the source country, relative factor

14

endowments, trade costs and investment costs. When countries differ in size, but not in

factor endowments, there is an inverted U-shaped relation, indicating that horizontal FDI

is highest between countries that are of the same size. In this sense, the empirical

specification should include the squared difference in size in order to account for this

relationship. Additionally, vertical FDI takes place if the difference in the size of the

economies is significant and the small country is skilled labor intensive, so that the

production facility tends to be installed abroad. Notice that since headquarters location

decisions are based on factor endowments and plant location on the basis of the factor

endowments and the market size, an interaction term between both variables should be

included in the empirical specification of the model.

As in the pure horizontal model (see Horstmann and Markusen, 1987, 1992), trade costs

in the host country encourage horizontal FDI, while investment restrictions in the host

country � captured in our institutional variable - and trade costs in the source country

restrict FDI activity of vertical nature. However, since trade costs favor horizontal FDI

but not vertical FDI, and horizontal FDI increases if factor endowments are similar, Carr

et al (2001) include an interaction between trade costs and the squared endowment

differences.

To the benchmark model of Carr et al (2001), we add our measure of institutional quality,

such that the empirical specification is as follows:

0 1 2 3 4

5 6 7 8

ln(1 )

ln( )ij ij ij ij ij ij

ij j j ij j i ij

FDI SUMGDP SQDIFGDP ADIFGDP ADIFSKILL ADIFSKILL

Distance TARIFF TARIFF SQDIFSKILL institutions

β β β β ββ β β β ϕ ε

+ = + + + × +

+ + + × + + + (1)

15

The definitions of the variables are as follows. FDI is the outward stock of FDI from

country i (source) in country j (host) from the OECD database. SUMGDP is the sum of

the logs of the host country and the source country GDPs, in current dollars from the

WDI database in 1998. The variable SQDIFGDP is the squared difference in the GDPs of

the host and the source country, while ADIFGDP is the absolute difference between

them. Similarly, ADIFSKILL is the absolute difference between the countries�

endowments of skilled labor and SQDIFSKILL is the corresponding squared difference.

We use the average percentage of the labor force with secondary education from the WDI

database over 1990 and 1995 as our variable of skilled labor endowment. DISTANCE is

the great circle distance between the countries� capitals.12 Trade costs are measured by

the average TARIFF level between 1990 and 1998.13 Finally, source country dummies

( iϕ ) are included in order to capture the effects of possible systematic differences in the

FDI accounting methodology of reporting countries, as well as other relevant source

country characteristics.

The log specification is used because it has typically shown the best adjustment to the

data in the empirical literature. A problem that arises when using the log of FDI as a

dependent variable, however, is how to deal with the observations with zero values. Our

dataset includes about one third of observations where FDI stocks are zero14, which

would be dropped by taking logs. The problem of zero values of the dependent variable is

typical in gravity equations for trade, and it has been dealt with in different ways. 12 The only exceptions are the U.S. and China, where we consider Chicago and Shanghai respectively. 13 Tariff data are from the Worldbank available at http://www.worldbank.org/data/wdi2001/pdfs/tab6_6.pdf 14 More specifically, there are 315 zero values in 1140 total observations.

16

Some authors (see for example Rose, 2000) simply exclude the observations in which the

dependent variable takes a value of zero. A problem with this approach is that those

observations may convey important information for the problem under consideration.

Given the importance of zero observations in our sample, this strategy could lead to a

serious estimation bias. We will follow Eichengreen and Irwin (1995, 1997) who use a

simple transformation to deal with the zeros problem: work with log (1 + trade), instead

of the log of trade. This has the advantage that the coefficients can be interpreted as

elasticities when the values of trade tend to be large, since in this case log (1 + trade) is

approximately equal to log (trade). Another approach has been to use Tobit instead of

OLS. In a subsequent section, we show that our results are robust to the use of alternative

estimation techniques.

3. Empirical Results

In the first column of Table 1, we present our estimate of equation (1) without including

any institutional indicator. A first interesting point is that the model explains a high

proportion - approximately 71 percentage points - of the total variation in FDI stocks.15

The significant variables are the sum of GDPs, the squared difference of GDPs, and

distance, tariffs in the host country, and - marginally - the interaction between tariffs and

15 While the source country dummies are jointly significant, they do not drive this result, since an estimation of equation (1) without fixed effects explains approximately 61 percent of the variation in the dependent variable, while a regression with only source country dummies as explanatory variables explains 31 percent of the total variation. In addition, the signs, levels of significance, and magnitudes of the estimated coefficients are very similar to those of column 1.

17

the squared absolute difference in factor endowments. The signs of the estimates are

consistent with those obtained by Blonigen et al (2002).

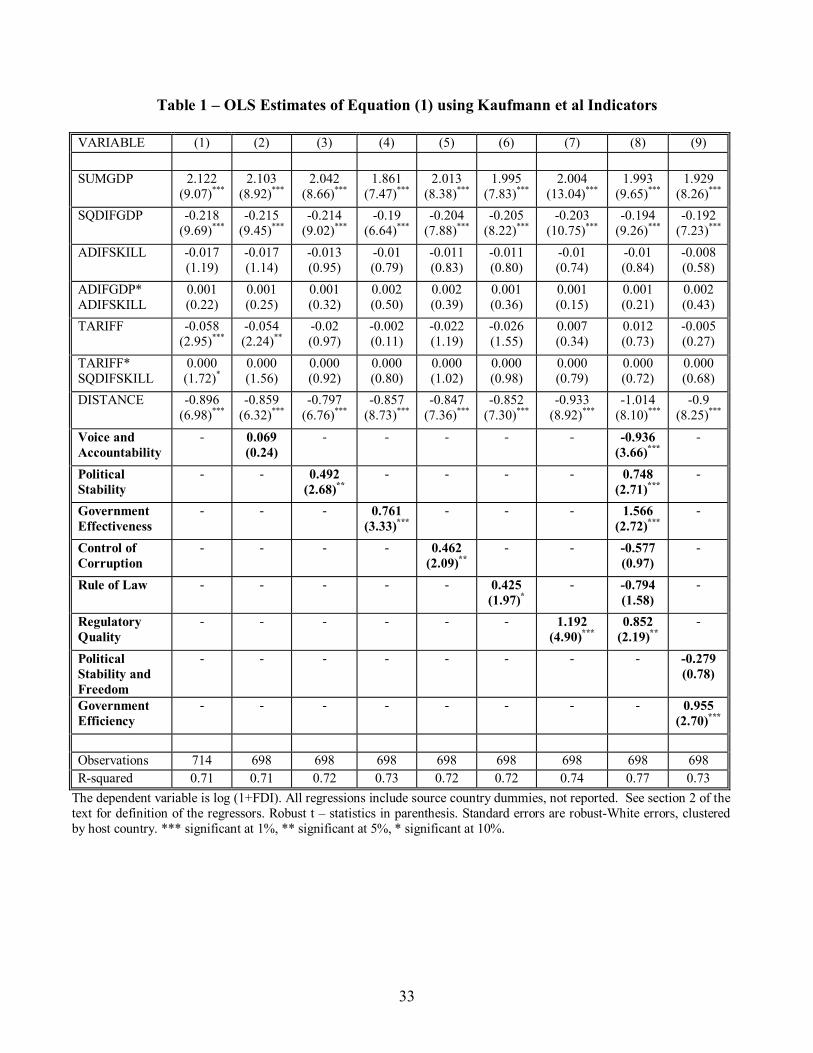

In columns 2 to 7 we introduce the Kaufmann et al (1999a) variables into equation (1).

The estimates show that overall the quality of institutions has a significant and positive

impact on FDI, except for Voice and Accountability whose effect is not significant and

Rule of Law, which has a positive impact, but is significant only at a 10 percent level. The

largest effect seems to be associated to Regulatory Quality where a one standard

deviation increase in this dimension of governance would increase FDI stocks by a factor

of 3.3.16 While initially the magnitude of this effect seems too extreme, it should be kept

in mind that a one standard deviation improvement in the regulatory quality of

government implies a substantial change in the regulatory framework, e.g. from the level

of Thailand to that of Canada or Germany. Slightly lower effects correspond to

Government Effectiveness and Corruption, where a one standard deviation improvement

would imply an increase in FDI stocks by a factor of 2.1 and 1.6 respectively.

Furthermore, Rule of Law and Political Stability and Lack of Violence have a positive

significant impact on FDI. This first evidence indicates that several dimensions of

government institutions clustered in Government Efficiency seem to be especially

relevant in explaining the location of FDI.

There are however at least two possible problems with the preceding regressions. On the

one hand, if various institutional dimensions determine simultaneously the location of

FDI, by including them one by one as before there might be an omitted variable bias, 16 exp(1.192)=3.294.

18

especially severe given the correlation among the different indicators reported in the

previous section. On the other hand, as mentioned previously, the different variables

might be subject to measurement errors. In order to address these problems, we run two

additional regressions, one including the six regressors simultaneously, and the other

clustering all variables into Political Stability and Freedom or Government Efficiency as

previously mentioned.

In column 8, we present the results from including all six variables together. Given the

high correlation among them, there might be important multicollinearity problems, as

indicated by the negative sign of Voice and Accountability or Rule of law. Taking into

account this caveat it is still interesting to point out that the variables Regulatory Quality

and Government Effectiveness seem to the most relevant governance dimensions. In the

last column of Table 1 we estimate equation (1) incorporating the clusters Political

Stability and Freedom and Government Efficiency. A one standard deviation

improvement in Government Efficiency � e.g. from Slovenia to Sweden or Argentina to

Chile - would increase FDI by a factor of 2.6. While the magnitude of the effect seems to

be very large, the previous examples show that it is reasonable. For 1998, the FDI stock

of OECD countries in Slovenia is approximately 0.30 percentage points of its GDP, while

in the case of Sweden it is 0.90 percent. Therefore, an improvement in Slovenia's

institutions to the level of Sweden would yield an FDI stock in Slovenia only slightly

below that of Sweden as a ratio of GDP. Similarly, the ratio of the OECD countries' FDI

stock in 1998 is 0.52 percentage points of GDP for Argentina, while in the case of Chile

it is 1.22. An improvement in Argentina's institutional quality to the level of Chile would

19

therefore lead to an FDI stock to GDP ratio of approximately 1.35 percent, quite similar

to that of Chile. Political stability and freedom has no significant effect on FDI.17

In Table 2, we consider alternatives measures of institutional quality from the ICRG. As

illustrated in columns 1 to 6, at a 10% level the only variable is Risk of Repudiation of

Contracts by the Government. The estimated effect is that an improvement in the Risk of

Repudiation of Contracts by the Government by one standard deviation � e.g. from the

level of Egypt to that of Finland - increases FDI by a factor of 1.4.18 This indicates that

the predictability of policies and the respect for contracts by the government are relevant

aspects of countries� institutions that foreign investors take into account in their location

decisions. Another significant result � given the relevance in the existing literature of

corruption - is that the estimated effect of Corruption in Government is not statistically

different from zero. Similar results hold for Law and Order, Expropriation Risk,

Bureaucratic Quality, and Democratic Accountability.19 In column 7, we present the

estimation including the simple average of the ICRG variables. Again, the resulting

estimate is not significant at conventional levels.

The low overall significance of these variables might be explained by the fact that these

variables are constructed to rank a wider range of countries than those in our sample. For

example, most less developed countries from Africa, the Middle East and North Africa

17 The fact that Political Stability and Freedom is not significant in our regression means that it has no direct effect on FDI. This does not exclude the possibility that it might still have an important indirect effect, for example via the accumulation of human capital. 18 exp(.356)=1.428 19 These results are robust to considering e.g. the average of these variables over 1982 to 1995 as Knack and Keefer (1995).

20

and Asia are not included in the sample.20 Since it is likely that these countries have bad

institutions and actually do not receive important FDI flows from the OECD, our

estimates would be biased against the hypothesis that the quality of institutions affects

FDI location by this sample selection bias. This leads to a low variation in the

institutional variables that does not allow to capture their effects on FDI properly. This

appears to be particularly relevant in the case of Risk of Repudiation of Contracts by the

Government and Risk of Expropriation by the Government. These variables are originally

rated on a scale from 1-10. However, in our sample the lowest ratings are 7 and 8,

respectively.

In the last column, we use the simple average between the aggregate average value of

Corruption in Government, Expropriation Risk, Bureaucratic Quality, Risk of

Repudiation of Contracts by the Government, and Law and Order from the ICRG during

1986-1995 and an indicator of economic openness by Sachs and Warner (1995). Hall and

Jones (1999) construct this variable to measure the social infrastructure understanding as

such the institutions and government policies that determine the relevant environment of

well functioning market economy.21 This variable has a positive and significant effect on

FDI, with a one-standard-deviation improvement in the quality of institutions increasing

FDI by a factor of 2.2.22

20 For example from Sub-Saharan Africa the sample only includes South Africa, which is the country with the relatively highest institutional quality in that region. 21 See Hall and Jones (1999) for more details. 22 This result seems is mainly driven by the Sachs and Warner variable, since regressions that consider the averages of the ICRG variables over the period 1986-1995 yield results that are identical to ours; only Risk of repudiation of contracts is significant at a 10% level.

21

Another problem that may be determining the overall low significance in the case of the

ICRG variables is that the quality of institutions might be endogenous. This problem

might arise because of two distinct causes. First, the presence of foreign investors might

constitute a group of interest that lobbies for better enforcement of property rights, such

that there might be a feedback effect from FDI to the quality of institutions. We will deal

with this problem in the robustness section. In addition, institutional indicators based on

polls of experts might be subject to a "subjectivity" bias. This may occur when the

amount of FDI a country receives affects the rating of a country's institutions made by the

expert. For example, the expert might infer that property rights are efficiently enforced

given that the amount of FDI is very high. Although the ICRG indicators we considered

above are not directly related to the macroeconomic performance of the country selected,

they might still be affected this subjectivity bias. In order to overcome this potential

problem, we use the survey-based variables from the WBES.

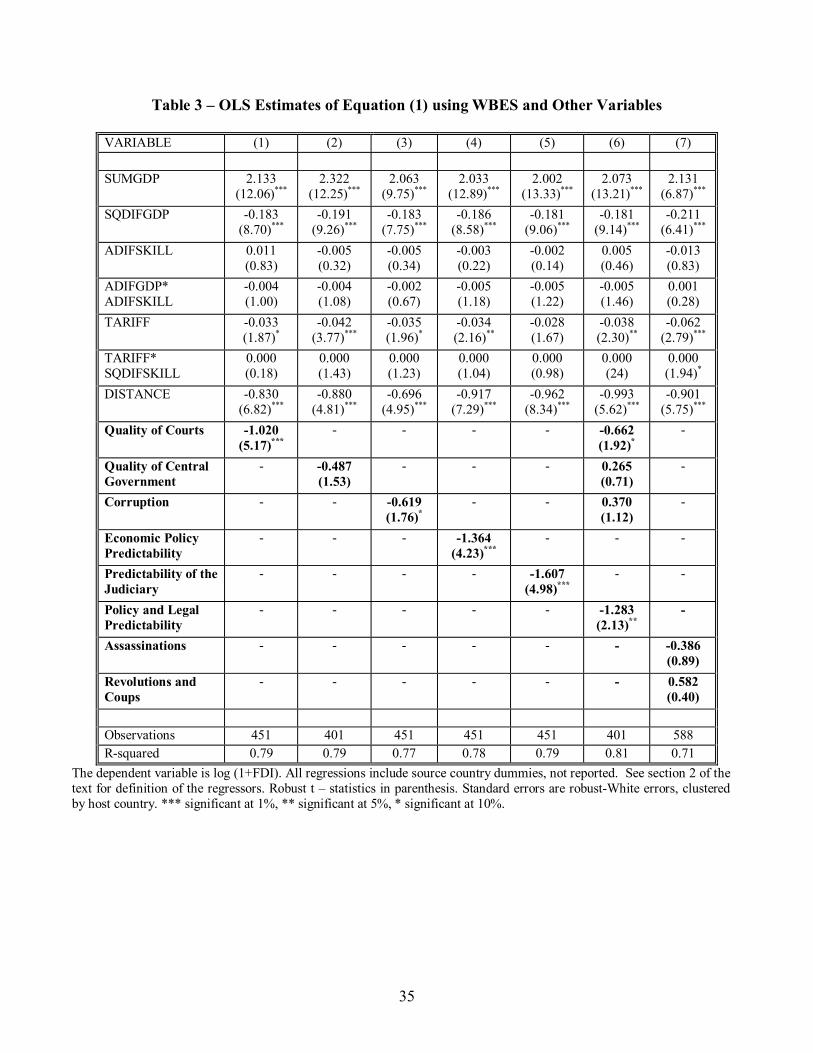

In Table 3, we present the estimates for this set of indicators. The estimates show that the

most relevant institutions seem to be those related to the predictability and stability of

policies and the legal framework. An improvement in the predictability of laws and

regulations in one standard deviation increases FDI by a factor of 2.23 Corruption is only

significant at a 10 percent level, and the Quality of Central Government � a variable

closely related to the red tape and the quality of bureaucracy in general � has no

significant impact on FDI, as we found also for the ICRG data. In addition, the Quality of

the Courts also has a significant impact on FDI. In column 6, we aggregate Economic

Policy Predictability and Predictability of the Judiciary into Policy and Legal 23 Given that the standard deviation of Law Predictability is .42, we have exp(-1.607*(-.42))=1.964.

22

Predictability and estimate equation (1) incorporating all additional variables.24 At a 5

percent level of significance, only the predictability of the rules that determine the

economic and legal environment have a significant impact on FDI, while the quality of

the legal system has a significant impact at a 10 percent level.

In the last column of Table 3, we include the average number of assassinations as well as

the number of revolutions and coups. We do not find a significant direct effect of these

more objective measures of political and social violence.

From the regressions we analyzed in this section, we can conclude the following. First,

the evidence shows that overall the quality of institutions has a significant and

economically important impact on the location of FDI. Second, not all dimensions of the

institutional framework have the same direct importance for foreign investors� investment

decisions. We find that the regulatory framework, the predictability of policies, laws and

regulations, the effectiveness of the government in �getting things done� and the

enforcement of property rights are the most sensitive aspects to foreign investors. This

finding is robust to a large variety of different indicators. Third, the results show no

evidence of a direct effect of civil liberties and the degree of democratic accountability of

FDI. However, as we already pointed out, there could be important indirect effects.

Finally, while several previous papers have focused exclusively on the level of corruption

as a deterrent to FDI, we find that this effect is weaker and less consistent across

24 From the correlations in Table A.3., it seems that in this case multicollinearity seems not to be a great problem among these variables.

23

indicators than the effect of the variables mentioned above. In the next section, we

analyze the robustness of these results.

4. Robustness

The first issue we address in our robustness tests is whether our results are sensitive to the

solution used to deal with the observations with zero FDI. In the first two columns of

Table 4, we present estimates of equation (1) considering simply the log of the bilateral

FDI stock, so that all zero-value observations are dropped, and the estimates considering

the transformation log(1+FDI) but restricting the sample to those observations with

strictly positive FDI stocks. Focusing on the institutional variables, the estimates are

virtually identical in both cases. Government Efficiency continues being significant and

Political Stability and Freedom does not, as in our benchmark case of the last column in

Table 1. In addition, the fact that the point estimate of the effect of both institutional

variables is lower shows that the sample selection bias goes in the assumed direction. If a

country that has bad institutions is less likely to receive positive FDI, the estimates in first

two columns of Table 3 are downward biased.

As we mentioned above, an alternative approach could be the estimation of a TOBIT

model of equation (1). In column 4 of Table 4, we present the estimates considering this

alternative estimation method. The estimated coefficient for Government Efficiency is

similar to that obtained by OLS, although it is slightly higher. However, if we consider

the correction proposed by Greene (1980) of rescaling the OLS estimates to make them

24

comparable to the TOBIT estimates, we would obtain very similar results. This

adjustment would be to divide the OLS estimate by the proportion of non-censored

observations in our estimation, which is 0.72.25 Thus, the estimated coefficient of

Government Efficiency from Table 1 would be 1.328, very similar to the point estimate of

the TOBIT model.26 In addition, as in the OLS case, Political Stability and Freedom has

no significant effect on FDI.

In the next column of Table 4, we estimated a standard gravity model in order to explore

the sensitiveness of our results to the specification of our baseline regression. We include

the GDP and GDP per capita of the host country, a common language dummy, a dummy

that equals unity if the source country was the colonizer of the host country, a common

border dummy, and a dummy for common membership in a Free Trade Area.27 The

estimates show that overall the gravity equation is successful in explaining the variation

in FDI across countries with an R-squared of 0.72.28 Regarding our variables of interest,

the estimates show that a one standard deviation improvement in the degree of efficiency

of the government would increase FDI by a factor of 3.8, which is higher than our

25 502/698=0.719. 26 .955/.719=1.328. 27 The common language, colonial links, and border dummies where constructed using information from the CIA�s World Factbook available at www.cia.gov/cia/publications/factbook/index.html. The Same FTA dummy is taken from Levy Yeyati et al (2003), GDP is 1998 GDP in current dollars while GDP per capita is for 1998 PPP adjusted from the WDI database. 28 It is important to point out that the estimate of GDP per capita of the host country is negative and significant. This reflects multicollinearity problems, due to the high correlation between GDP per capita and the institutional indicators. The correlation coefficients are 0.84 and 0.76 with Government Efficiency and Political Stability and Freedom, respectively.

25

estimate estimates in Table 1.29 As before, the estimated effect of Political Stability and

Freedom on FDI is not significant.

In the previous section, we presented evidence that our results hold over a wide range of

alternative measures of the quality of institutions. However, as we mentioned earlier, it

seems reasonable to consider the possibility that the quality of institutions might be

endogenous for two reasons. First, once foreign investors are located in a country, they

might become a constituency that demands better institutions. Therefore, there could be a

feedback effect on the quality of institutions. Second, the previously mentioned

subjectivity bias, where experts report a better score on the quality of institutions because

they observe a high level of FDI, generates the same econometric problems.

In order to address these possible endogeneity problems, we estimate 2SLS regressions of

equation (1), considering instrumental variables for the institutional quality indicators

that are standard in the literature. La Porta et al (1999) find that the origin of the legal

code is an important and significant determinant of a series of government institutions

and economic outcomes. Chong and Zanforlin (2000) find that countries with law

tradition based on the French Civil code display significantly lower levels of bureaucratic

development and the credibility of the government and higher levels of corruption, while

countries with English Common Law show a higher level of institutional quality. Thus,

we consider a set of dummy variables for Common Law, French Law, German Law and

29 exp(1.325)=3.762. While the quantitative difference with the previous estimates seems larger, we have to keep in mind that in general the precision of all estimates for the institutional variables is relatively low, given that we use robust clustered standard errors to account for the fact that the institutional variables vary only on a host country level. Also, the multicollinearity with GDP per capita might inflate the variance of the relevant estimates.

26

Scandinavian Law as one set of instruments. The simple correlations with Political

Stability and Freedom and Government Efficiency are 0.04, 0.19; -0.45, -0.54; 0.27, 0.19;

0.39, 0.38, respectively. From Hall and Jones (1999) we consider the fraction of the

population that speaks English (ENGFRAC), since it seems natural to assume that the

extent to which this constitutes the mother tongue of a country is positively correlated

with the degree of influence of Western Europe. For this instrument the correlations with

Political Stability and Freedom and Government Efficiency are 0.40 and 0.39,

respectively. In addition, we consider Mauro�s (1995) index of Ethnolinguistic

Fragmentation (FRAG), since ethnic conflict might induce more political violence and,

as Mauro argues, might also imply a higher level of corruption as officials favor members

of their same group. In this case, the correlations with the two institutional variables are -

0.30 and -0.29. Finally, from Acemoglu et al (2001), we consider the mortality rate of

European settlers (SETTLERM). These authors argue that the quality of early institutions

in the former colonies depends critically on the type of settlements that where installed.

In regions with very high mortality rates, colonizers only tried to extract the goods they

were interested in without building any institutional framework, which happened in

colonies with lower degrees of mortality. Since institutions are highly persistent, early

institutions are highly correlated with those observed today. The correlations of the

settlers� mortality (in logs) with our institutional variables are -0.64 and -0.76,

respectively. Although this seems to be the most appealing instrument, its limitation is

that it is only available for a small number of countries.

27

In column 5, we present the instrumental variables estimates using the legal code

dummies and the English-speaking fraction of the population. The results show that the

impact of Government Efficiency is positive and marginally significant, while in the case

of Political Stability and Freedom it is not significant. In column 6, we consider

alternatively the index of Ethnolinguistic Fragmentation and the English-speaking

fraction of the population. The results again show a positive and significant effect of

Government Efficiency and a non-significant effect of Political Stability and Freedom.

Finally, in the last column we present the estimates using the Ethnolinguistic

Fragmentation index and the logs of settlers� mortality. Again, only Government

Efficiency has a significant and positive effect on FDI, at a 10 percent level of

significance.

5. Conclusions

In this paper, we have shown the relevance of the institutional quality as a factor of

attraction of FDI. We find that the quality of institutions has positive effects on FDI. The

impact of institutional variables is statistically significant, and economically very

important. Additionally, not all institutional dimensions have the same importance for the

decision of where to invest. We find that unpredictable policies, excessive regulatory

burden, deficient enforcement of property rights and lack of commitment on the part of

the government seem to play a major role in deterring FDI flows. These results are robust

28

to the use of a wide variety of institutional variables, collected from different sources, and

using different methodologies. Furthermore, they are also robust to different

specifications, and different estimation techniques. Finally, unlike the previous empirical

literature, that has focused its attention nearly exclusively on corruption, we find that

although corruption has a negative impact on FDI, its magnitude and significance

depends on the specific indicator used to measure this institutional dimension.

29

References Acemoglu, D., S. Johnson and J.A. Robinson, 2001. �The Colonial Origins of Comparative Development: An Empirical Investigation�. American Economic Review, Vol. 91, 1369-1401. Aizmann, J. and M. Spiegel, 2002. �Institutional Efficiency, Monitoring Costs, and the Share of FDI�. NBER Working Paper 9324. Albuquerque, R., 2003. �The Composition of International Capital Flows: Risk Sharing Through Foreign Direct Investment�. Journal of International Economics, Vol. 61, 2:353-383. Barro, R., 1991. �Economic Growth in a Cross-section of Countries�. Quarterly Journal of Economics (May), Vol. 106, 2: 407-443. Blonigen, B.A., R.B. Davies and K. Head, 2002. �Estimating the Knowledge-Capital Model of the Multinational Enterprise: Comment�. NBER Working Paper 8929. Carr, D.L., J.R. Markusen and K.E. Maskus, 2001. �Estimating the Knowledge-Capital Model of the Multinational Enterprise�. American Economic Review, Vol. 87, 4 (September): 520-544. Chong, A. and L. Zanforlin, 2000. �Law Tradition and the Quality of Institutions: Some Empirical Evidence�. Journal of International Development, Vol. 12, 1057-1068. Eichengreen, B. and D. Irwin, 1995. �Trade Blocks, Currency Blocs and the Reorientation of Trade in the 1930s�. Journal of International Economics 38, no. 1-2 (February): 1-24. Eichengreen, B and D. Irwin. 1997. �The Role of History in Bilateral Trade Flows�, in The Regionalization of the World Economy, J. Frankel (ed.), University of Chicago Press, Chicago. Frankel, J. with E. Stein, and S. Wei. 1997. Regional Trading Blocs in the World Economic System. Institute for International Economics, Washington, DC Greene, W.H., 1980. �On the Asymptotic Bias of the Ordinary Least Squares Estimator of the Tobit Model.� Econometrica, Vol. 48: 505-14. Hall, R.E. and C.I. Jones, 1999. �Why Do Some Countries Produce So Much More Output Per Worker Than Others?�. Quarterly Journal of Economics (February), Vol. 114, 1: 83-116.

30

Hausmann, R. and E. Fernandez-Arias, 2000. �Foreign Direct Investment: Good Cholesterol?� Inter-American Development Bank, Research Department Working Paper 417, Washington D.C. Helpman, E., 1984. �A Simple Theory of Trade with Multinational Corporations�. Journal of Political Economy, Vol. 92: 451-71. ---------- and P. Krugman, 1985. Market Structure and International Trade. Cambridge, United States: MIT Press. Horstmann, I. and J.R. Markusen, 1987. �Strategic Investments and the Development of Multinationals." International Economic Review (February), Vol. 28, 1: 109-121 ---------- and J.R. Markusen, 1992. �Endogenous Market Structures in International Trade." Journal of International Economics (February), Vol. 32, 1-2: 109-129 Kaufmann, D., A. Kraay, and P. Zoido-Lobatón, 1999a. �Governance Matters.� World Bank Policy Research Working Paper 2196. Washington DC. ----------, A. Kraay, and P. Zoido-Lobatón, 1999b. �Aggregating Governance Indicators.� Policy Research Working Paper 2195. Washington DC Knack, S. and P. Keefer. 1995. �Institutions and Economic Performance: Cross-Country Tests Using Alternative Institutional Measures�. Economics and Politics 7, No. 3: p. 207-28. Krueger, A.O., 1993. �Virtuous and Vicious Circles in Economic Development�. Papers and Proceedings of the American Economic Association (1993), 351-56. La Porta, R., F. Lopez de Silvanes, A. Shleifer and R.W. Vishny, 1998. �Law and Finance�. Journal of Political Economy (December), Vol. 106, 6: 1113-55. ----------, F. Lopez de Silvanes, A. Shleifer and R.W. Vishny, 1999. �The Quality of Government�. Journal of Law, Economics and Organization (April). ----------, F. Lopez de Silvanes, A. Shleifer and R.W. Vishny, 2000. �Investor Protection: Origins, Consequences, and Reform�. Journal of Financial Economics (October) Levy Yeyati, E., E. Stein and C. Daude, 2003. �Regional Integration and the Location of FDI�. Inter-American Development Bank, Research Department Working Paper 492, Washington D.C. Markusen, J.R., 1997. �Trade versus Investment Liberalization�. NBER Working Paper 6231. ----------, 2001. Multinationals and the Theory of International Trade, Cambridge: MIT Press.

31

Mauro, P., 1995. �Corruption and Growth�. Quarterly Journal of Economics (August), Vol. 110, 3: 681-712. Mody, A., A. Razin and E. Sadka, 2003. �The Role of Information in Driving FDI Flows: Host-Country Transparency and Source-Country Specialization�. NBER Working Paper 9962. Rose, A., 2000. �One market, one money: the effect of common currencies on trade� Economic Policy, Vol. 14, 30: 7 � 46. Sachs, J.D. and A. Warner, 1995. �Economic Reform and the Process of Global Integration�. Brookings Papers on Economic Activity, 1: 1-118. Shleifer, A. and R.W. Vishny, 1993. �Corruption�. Quarterly Journal of Economics, Vol. 109, 599-617. Stein, E. and C. Daude, 2002. �Institutions, Integration and the Location of FDI�, in New Horizonts of Foreign Direct Investment, OECD Global Forum on International Investment, OECD, Paris. Wei, S., 1997. �Why is Corruption so Much More Taxing than Tax? Arbitrariness Kills�. NBER Working Paper 6255. ----------, 2000. �How taxing is corruption to international investors?� Review of Economics and Statistics, Vol. 0, 1:1-11. Wheeler, D. and A. Mody, 1992. �International Investment Location Decisions�. Journal of International Economics 33: 57-76

32

PhilippinesSwitzerlandIndonesia

Thailand

Japan

DenmarkSlov ak Republic

Poland

Singapore

Romania

IndiaIndia

Sweden

New Zealand

ColombiaFinland

India

Bulgaria

New Zealand

Greece Norway

PhilippinesFinland

Iran IslandSouth Af ricaKorea

Norway

Iran

Panama

Czech Republic

ThailandBulgaria

Israel

ColombiaMexicoPortugal

IndonesiaSlov ak Republic

Mexico

Czech Republic

Malay sia

Denmark

ChileChile

Turkey

Chile

Venezuela

Norway

MexicoVenezuela

Korea IslandAustriaSouth Af rica

Colombia

Japan

TurkeyUkraine

Iran

Greece

Australia

Sweden

Canada

India

Singapore

Thailand

Hungary

Iran

New Zealand

Switzerland

South Af rica

DenmarkIndonesia

TurkeySlov ak RepublicSlov ak Republic

Austria

Netherlands

Malay sia

China

India

SpainBulgaria

IsraelSwitzerland

Chile

Czech Republic

Germany

CanadaUkraine

Chile

Indonesia

BulgariaBulgaria

Slov eniaSouth Af rica

New Zealand

Thailand

New Zealand

UkraineSlov ak Republic

Denmark

Germany

Chile

Ukraine

Argentina

Island

Slov enia

New Zealand

Egy pt

Argentina

Slov enia MoroccoKorea

Malay sia

Japan

Portugal

Venezuela

Hungary

South Af ricaItaly

Turkey

Venezuela

Portugal

Japan

Australia

South Af ricaKorea

Philippines

Malay sia

Poland

Ireland

VenezuelaArgentina

Iran

MoroccoFrance

China

Japan

Venezuela

Greece

Hungary

South Af rica

Panama Chile

Italy

Poland

FinlandAustralia

United Kingdom

Slov ak Republic

Chile

United States

SpainMorocco

Hungary

Malay sia

Bulgaria

Australia

Chile

Egy ptPhilippines

Slov ak RepublicRomania

United States

New Zealand

Ukraine

Singapore

Thailand

Morocco

Japan

Argentina

RomaniaMexico

SpainIsrael Morocco

Thailand

FranceIndia

China

IsraelBrazil

MoroccoCanada

Italy

BrazilRomania

Sweden

South Af rica

ChileIreland

Thailand

IndiaSlov ak Republic

RomaniaColombia

Slov eniaBrazil Indonesia

Malay sia

Mexico

SingaporeSingapore

Brazil Switzerland

Hungary

Canada

United StatesKorea

Spain

Sweden

Norway

Mexico

New Zealand

United Kingdom

Ukraine

ThailandPoland

Ukraine

Italy

Egy pt

China

SpainRomaniaColombia

IndonesiaFrance

Malay sia

Australia

South Af rica Austria

Portugal

Algeria

Hungary

Morocco

Venezuela

Singapore

Egy pt

Germany

Egy ptBrazilPhilippines

KoreaIsrael India

Czech Republic

Italy

GreeceSouth Af rica

China

Netherlands

China

Malay sia

Slov enia

Malay sia

CanadaFranceAustria

Philippines

IndiaKorea

Ireland

Singapore

Australia

Austria

Mexico

Spain

United Kingdom

Japan

Romania Portugal

VenezuelaVenezuela

DenmarkEgy pt

Poland

Chile

Indonesia

Poland

FinlandDenmark

JapanItaly

Denmark

Czech Republic

IndiaIndia

Italy

ThailandVenezuela Thailand

Denmark

Germany

CanadaSlov ak Republic

Austria

Finland

Slov enia Norway

Colombia PolandPortugal

China

Chile

Romania

Czech Republic

Colombia

Korea

CanadaPhilippines

SwedenIreland

South Af rica

Finland

TurkeyKoreaGreece

Sweden

Japan

Canada

ChinaNew Zealand

Malay sia

Korea

IndonesiaIndonesia

Ireland

Japan

Australia

South Af rica

Chile

Netherlands

Greece Norway

Malay sia

FrancePortugal

Mexico Poland

Italy

ColombiaThailand

Portugal

Turkey

United Kingdom

Netherlands

PhilippinesMexico Poland

Hungary

Argentina

Ireland

Netherlands

Singapore

India

ChinaHungary

Canada

Thailand

Finland

AustriaGreeceSlov ak Republic

Singapore

Finland

Poland

Switzerland

Turkey

France

Philippines

Norway

Sweden

SpainMoroccoIndia

China

Austria

Finland

China

Turkey

Malay sia

CanadaFrance Indonesia

Mexico

Norway

Portugal

TurkeyGreece

Germany

Switzerland

Poland

Norway India

Czech Republic

Austria

New Zealand

Thailand

NorwayFrance

Czech Republic

GreeceUnited States

Czech Republic

Indonesia

Hungary

Indonesia

Mexico PhilippinesPortugalSpain

Austria

Japan

Hungary

Canada

Hungary

Argentina

Germany

United KingdomArgentina

India

FinlandPortugalUnited Kingdom

Korea

Argentina

Switzerland

Ireland

Portugal

Japan

South Af rica

Brazil

PolandMexico

Czech Republic

Chile

Argentina

Sweden

Egy pt

Singapore

Italy

Mexico Poland

Singapore

Australia

Costa RicaNetherlands

Japan

Argentina

SwitzerlandDenmark

Austria

Singapore

Australia

Singapore

Spain

South Af rica

PhilippinesAustraliaAustralia

Sweden

FranceBrazil Denmark

Germany

Brazil

Colombia

GermanyJapan

Ireland

Canada

New Zealand

Argentina

South Af rica

DenmarkBrazilIsrael

Sweden

JapanGermany

Netherlands

United States

Australia

Sweden

PortugalFrance

Sweden

Mexico

Brazil

Chile

Algeria

United Kingdom

Spain

Malay sia

China

Colombia

Australia

Austria

DenmarkPhilippines

China

Canada

Ireland

United States

Brazil Denmark

Korea

Canada

Singapore

Italy

Netherlands

Malay sia

CanadaFrance

Germany

Denmark

NorwayCanada

Poland

NetherlandsCzech Republic

Sweden

New Zealand

Thailand

Sweden

Italy

Brazil

Japan

Brazil

United States

Hungary

Italy

Malay sia

Spain

Ireland

ThailandVenezuela

GermanyUnited States

New Zealand

Switzerland

China

Ireland

Norway

United Kingdom

Finland

Korea

Brazil

Singapore

SpainBrazil SpainIndonesia SwitzerlandAustraliaCanada

Germany

Chile

Italy

Netherlands

Singapore

France

Sweden

Spain

United Kingdom

Ireland

SwitzerlandSpainIndonesia

United Kingdom

NetherlandsNetherlands

Argentina

Germany

Ireland

France

GermanyAustria

Spain

Italy

SwitzerlandSwitzerland

GermanyItaly Germany

Australia

United States

United Kingdom

France Switzerland

United States

Singapore

China

France

Ireland

United KingdomUnited Kingdom

France

United KingdomUnited Kingdom

Panama

Netherlands

United Kingdom

Netherlands

Mexico

United States

Netherlands

United Kingdom

AustraliaBrazil Switzerland

Japan

United StatesFrance

GermanyUnited StatesUnited StatesUnited States

NetherlandsNetherlands

United States

Canada

United States

United Kingdom

United States

Denmark

Hungary

South Af ricaIran

Venezuela

IslandKorea

Venezuela

Panama

Switzerland

Algeria

MoroccoEgy pt

Island

NorwaySlov enia India

Singapore

Panama

South Af rica

Romania

New Zealand

Romania

New Zealand

SpainPhilippines

Costa Rica

Morocco

Venezuela

Panama

Portugal

PanamaIrelandPanama

Thailand

IndonesiaSlov ak Republic

Czech Republic

Slov ak Republic

PhilippinesDenmarkBulgaria

Egy pt

Island

Netherlands

Philippines

GreeceIsland

MoroccoMoroccoIsrael

Thailand

ChinaHungary

Romania

Algeria

China

Slov enia

Malay sia

Slov ak Republic Slov enia

Thailand

Slov enia

Poland

KoreaSlov ak Republic Slov enia

Bulgaria

Greece

Argentina Bulgaria

Iran Italy

Chile

Korea

Romania Egy ptSpain

Turkey

Sweden

Austria

Romania

Israel

RomaniaColombia

SpainMorocco

Bulgaria Poland

Ireland

Romania

Turkey

Poland

Ukraine

Argentina

Germany

ThailandBulgaria

Egy ptSlov ak Republic

AlgeriaTurkey

Czech Republic

IndonesiaGreeceGreeceGreece Norway

Turkey

Sweden

Costa Rica

GreeceSlov enia

Island

Slov enia

Colombia

Ireland

Colombia

Algeria

Slov ak Republic

Malay sia

South Af ricaIsland

Egy pt

MexicoMexico

Hungary

MoroccoBrazil

Slov enia

Philippines

Costa Rica

Island

MoroccoIsrael Morocco

Panama

Mexico

NorwaySlov enia

Bulgaria

Israel

BulgariaRomania

Panama

Thailand

Egy pt

China

Portugal

Iran

Brazil

Panama

Czech Republic

Ukraine

Romania Egy ptAustralia

Ukraine

ItalyTurkey

Czech Republic

ItalyAlgeriaKorea

Italy

Ukraine

Venezuela

Algeria

IsraelIsraelTurkeyIsrael

Singapore

Costa Rica

Philippines

IsraelIsrael

Finland

TurkeyIslandIsland

Czech Republic

ColombiaColombiaArgentina

Island

Netherlands

Iran

Czech Republic

Morocco

Denmark

Chile

Slov enia

FinlandFinlandColombiaArgentina

PanamaIreland

IndiaAlgeria

Turkey

Ireland

Czech RepublicCzech Republic

Iran

India

Panama

Costa Rica

Malay sia

IranTurkey

Romania

Hungary

Mexico

Panama

Indonesia

Chile

India

Panama

Ukraine

Costa Rica

HungaryNew Zealand

ChilePanama

Iran IslandUkraineSouth Af rica

Iran Island

Romania

Hungary China

Morocco

Venezuela

UkraineSlov ak Republic

Bulgaria

New Zealand

Iran

Hungary

Colombia

CanadaGreece

Malay sia

DenmarkSlov ak Republic

FinlandFinland

Slov enia

FinlandAustralia FinlandSlov ak Republic

VenezuelaCosta Rica

Finland

Turkey

Philippines

Costa Rica

Iran

Portugal

Iran

Egy pt

Czech Republic

Greece

Poland

Norway

Panama

JapanAlgeriaAlgeria

China

Ukraine

JapanAlgeriaAlgeriaAlgeriaAlgeriaAlgeriaAlgeria

Switzerland

Panama

NorwayAustria

Portugal

Panama

NorwayTurkey

PortugalIndonesia

Mexico

IslandAlgeria

Portugal

Costa Rica

Korea

Singapore

Costa Rica

Iran

Ireland

Ukraine

Bulgaria Poland

Ukraine

Costa RicaCosta Rica

Egy pt

Malay sia

Egy ptIsrael

Romania

Costa Rica

PhilippinesBrazil

Island

Morocco

Denmark

Panama

Austria

Colombia

Costa Rica

Brazil

New Zealand

Slov eniaEgy pt

Colombia PolandArgentina Bulgaria

Ukraine India

Switzerland

Greece

Switzerland

United Kingdom

Algeria

Venezuela

Greece

Venezuela

Indonesia

Germany

Indonesia

Sweden

Iran

Sweden

NorwaySouth Af rica

Israel

Costa Rica

United States

Egy ptSlov eniaFrance

Bulgaria

Hungary

Israel

Bulgaria

Israel Austria

Bulgaria

AustriaSlov ak Republic

Iran

Egy pt

Venezuela

GreeceIsland

Philippines

MoroccoAustria

New Zealand

Algeria IslandUkraine

Argentina

Costa Rica

ArgentinaArgentina

Costa Rica

Australia

Bulgaria

IranKorea

Slov eniaFrance

Costa Rica

Colombia

IsraelUkraine

Costa Rica

-.02

0.0

2.0

4.0

6.0

8FD

I/GDP

(res

idua

ls a

fter c

ontro

lling

for G

DP

per

cap

ita)

-1 -.5 0 .5 1Government Eff iciency (residuals after controlling for GDP per capita)

Figure 1 - Partial Correlation between Average FDI Inflows 1990-99 as a Ratio of GDP and Government Efficiency, controlling by GDP per capita in 1998

33

Table 1 � OLS Estimates of Equation (1) using Kaufmann et al Indicators

VARIABLE (1) (2) (3) (4) (5) (6) (7) (8) (9) SUMGDP 2.122

(9.07)*** 2.103

(8.92)*** 2.042

(8.66)*** 1.861

(7.47)*** 2.013

(8.38)*** 1.995

(7.83)*** 2.004

(13.04)*** 1.993

(9.65)*** 1.929

(8.26)***

SQDIFGDP -0.218 (9.69)***

-0.215 (9.45)***

-0.214 (9.02)***

-0.19 (6.64)***

-0.204 (7.88)***

-0.205 (8.22)***

-0.203 (10.75)***

-0.194 (9.26)***

-0.192 (7.23)***

ADIFSKILL -0.017 (1.19)

-0.017 (1.14)

-0.013 (0.95)

-0.01 (0.79)

-0.011 (0.83)

-0.011 (0.80)

-0.01 (0.74)

-0.01 (0.84)

-0.008 (0.58)

ADIFGDP* ADIFSKILL

0.001 (0.22)

0.001 (0.25)

0.001 (0.32)

0.002 (0.50)

0.002 (0.39)

0.001 (0.36)

0.001 (0.15)

0.001 (0.21)

0.002 (0.43)

TARIFF -0.058 (2.95)***

-0.054 (2.24)**

-0.02 (0.97)

-0.002 (0.11)

-0.022 (1.19)

-0.026 (1.55)

0.007 (0.34)

0.012 (0.73)

-0.005 (0.27)

TARIFF* SQDIFSKILL

0.000 (1.72)*

0.000 (1.56)

0.000 (0.92)

0.000 (0.80)

0.000 (1.02)

0.000 (0.98)

0.000 (0.79)

0.000 (0.72)

0.000 (0.68)

DISTANCE -0.896 (6.98)***

-0.859 (6.32)***

-0.797 (6.76)***

-0.857 (8.73)***

-0.847 (7.36)***

-0.852 (7.30)***

-0.933 (8.92)***

-1.014 (8.10)***

-0.9 (8.25)***

Voice and Accountability

- 0.069 (0.24)

- - - - - -0.936 (3.66)***

-

Political Stability

- - 0.492 (2.68)**

- - - - 0.748 (2.71)***

-

Government Effectiveness

- - - 0.761 (3.33)***

- - - 1.566 (2.72)***

-

Control of Corruption

- - - - 0.462 (2.09)**

- - -0.577 (0.97)

-

Rule of Law - - - - - 0.425 (1.97)*

- -0.794 (1.58)

-

Regulatory Quality

- - - - - - 1.192 (4.90)***

0.852 (2.19)**

-

Political Stability and Freedom

- - - - - - - - -0.279 (0.78)

Government Efficiency

- - - - - - - - 0.955 (2.70)***

Observations 714 698 698 698 698 698 698 698 698 R-squared 0.71 0.71 0.72 0.73 0.72 0.72 0.74 0.77 0.73

The dependent variable is log (1+FDI). All regressions include source country dummies, not reported. See section 2 of the text for definition of the regressors. Robust t � statistics in parenthesis. Standard errors are robust-White errors, clustered by host country. *** significant at 1%, ** significant at 5%, * significant at 10%.

34

Table 2 � OLS Estimates of Equation (1) using ICRG Variables

Variable (1) (2) (3) (4) (5) (6) (7) (8) SUMGDP 2.041

(7.22)*** 2.104

(8.74)*** 1.951

(6.67)*** 2.05

(8.44)*** 2.076

(8.30)*** 2.076

(7.17)*** 2.003

(7.45)*** 1.575

(5.56)*** SQDIFGDP -0.209

(7.76)*** -0.215

(9.01)*** -0.201

(7.02)*** -0.212

(8.45)*** -0.213

(8.55)*** -0.213

(8.04)*** -0.208

(7.80)*** -0.143

(5.54)*** ADIFSKILL -0.017

(1.20) -0.017 (1.16)

-0.015 (1.08)

-0.017 (1.19)

-0.017 (1.23)

-0.016 (1.16)

-0.016 (1.10)

-0.005 (0.36)

ADIFGDP* ADIFSKILL

0.002 (0.42)

0.001 (0.29)

0.003 (0.62)

0.002 (0.50)

0.002 (0.40)

0.002 (0.38)

0.002 (0.57)

-0.001 (0.30)

TARIFF -0.057 (2.85)***

-0.060 (2.58)**

-0.039 (2.29)**

-0.045 (2.31)**

-0.058 (2.59)**

-0.056 (3.00)***

-0.045 (2.36)**

-0.012 (0.60)

TARIFF* SQDIFSKILL

0.000 (1.71)*

0.000 (1.70)*

0.000 (1.44)

0.000 (1.47)

0.000 (1.70)*

0.000 (1.71)*

0.000 (1.45)

0.000 (0.75)

DISTANCE -0.903 (6.87)***

-0.910 (6.83)***

-0.914 (7.25)***

-0.851 (6.07)***

-0.902 (6.83)***

-0.902 (6.53)***

-0.875 (6.49)***

-0.897 (6.96)***

Expropriation Risk

0.138 (0.59)

- - - - - - -

Corruption - -0.026 (0.12)

- - - - - -

Risk of Repudiation

- - 0.356 (1.93)*

- - - - -

Law and Order - - - 0.213 (1.29)

- - - -

Democratic Accountability

- - - - 0.065 (0.25)

- - -

Bureaucratic Quality

- - - - - 0.047 (0.19)

- -

Average ICRG variables

- - - - - - 0.277 (1.09)

-

Social Infrastructure

- - - - - - - 3.27 (3.14)***

Observations 698 698 698 698 698 698 698 636 R-squared 0.71 0.71 0.72 0.71 0.71 0.71 0.71 0.72

The dependent variable is log (1+FDI). All regressions include source country dummies, not reported. See section 2 of the text for definition of the regressors. Social Infrastructure is from Hall and Jones (1999). Robust t � statistics in parenthesis. Standard errors are robust-White errors, clustered by host country. *** significant at 1%, ** significant at 5%, * significant at 10%.

35

Table 3 � OLS Estimates of Equation (1) using WBES and Other Variables

VARIABLE (1) (2) (3) (4) (5) (6) (7) SUMGDP 2.133

(12.06)*** 2.322

(12.25)*** 2.063

(9.75)*** 2.033

(12.89)*** 2.002

(13.33)*** 2.073

(13.21)*** 2.131

(6.87)*** SQDIFGDP -0.183

(8.70)*** -0.191

(9.26)*** -0.183

(7.75)*** -0.186

(8.58)*** -0.181

(9.06)*** -0.181

(9.14)*** -0.211

(6.41)*** ADIFSKILL 0.011

(0.83) -0.005 (0.32)

-0.005 (0.34)

-0.003 (0.22)

-0.002 (0.14)

0.005 (0.46)

-0.013 (0.83)

ADIFGDP* ADIFSKILL

-0.004 (1.00)

-0.004 (1.08)

-0.002 (0.67)

-0.005 (1.18)

-0.005 (1.22)

-0.005 (1.46)

0.001 (0.28)

TARIFF -0.033 (1.87)*

-0.042 (3.77)***

-0.035 (1.96)*

-0.034 (2.16)**

-0.028 (1.67)

-0.038 (2.30)**