Embed Size (px)

Citation preview

THE PROGRESSIVE CORPORATION

2020 ANNUAL REPORT TO SHAREHOLDERS

AnnualR

eport

App.-A-1

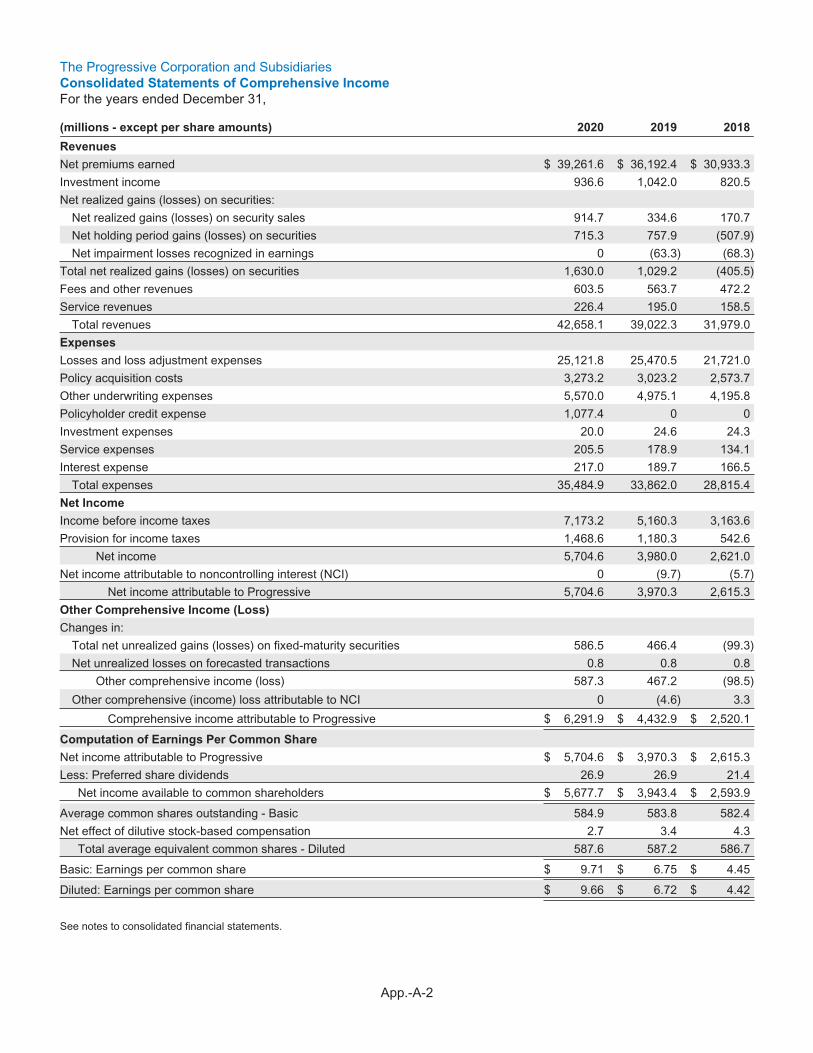

The Progressive Corporation and SubsidiariesConsolidated Statements of Comprehensive Income

For the years ended December 31,

(millions - except per share amounts) 2020 2019 2018

Revenues

Net premiums earned $ 39,261.6 $ 36,192.4 $ 30,933.3

Investment income 936.6 1,042.0 820.5

Net realized gains (losses) on securities:

Net realized gains (losses) on security sales 914.7 334.6 170.7

Net holding period gains (losses) on securities 715.3 757.9 (507.9)

Net impairment losses recognized in earnings 0 (63.3) (68.3)

Total net realized gains (losses) on securities 1,630.0 1,029.2 (405.5)

Fees and other revenues 603.5 563.7 472.2

Service revenues 226.4 195.0 158.5

Total revenues 42,658.1 39,022.3 31,979.0

Expenses

Losses and loss adjustment expenses 25,121.8 25,470.5 21,721.0

Policy acquisition costs 3,273.2 3,023.2 2,573.7

Other underwriting expenses 5,570.0 4,975.1 4,195.8

Policyholder credit expense 1,077.4 0 0

Investment expenses 20.0 24.6 24.3

Service expenses 205.5 178.9 134.1

Interest expense 217.0 189.7 166.5

Total expenses 35,484.9 33,862.0 28,815.4

Net Income

Income before income taxes 7,173.2 5,160.3 3,163.6

Provision for income taxes 1,468.6 1,180.3 542.6

Net income 5,704.6 3,980.0 2,621.0

Net income attributable to noncontrolling interest (NCI) 0 (9.7) (5.7)

Net income attributable to Progressive 5,704.6 3,970.3 2,615.3

Other Comprehensive Income (Loss)

Changes in:

Total net unrealized gains (losses) on fixed-maturity securities 586.5 466.4 (99.3)

Net unrealized losses on forecasted transactions 0.8 0.8 0.8

Other comprehensive income (loss) 587.3 467.2 (98.5)

Other comprehensive (income) loss attributable to NCI 0 (4.6) 3.3

Comprehensive income attributable to Progressive $ 6,291.9 $ 4,432.9 $ 2,520.1

Computation of Earnings Per Common Share

Net income attributable to Progressive $ 5,704.6 $ 3,970.3 $ 2,615.3

Less: Preferred share dividends 26.9 26.9 21.4

Net income available to common shareholders $ 5,677.7 $ 3,943.4 $ 2,593.9

Average common shares outstanding - Basic 584.9 583.8 582.4

Net effect of dilutive stock-based compensation 2.7 3.4 4.3

Total average equivalent common shares - Diluted 587.6 587.2 586.7

Basic: Earnings per common share $ 9.71 $ 6.75 $ 4.45

Diluted: Earnings per common share $ 9.66 $ 6.72 $ 4.42

See notes to consolidated financial statements.

App.-A-2

The Progressive Corporation and SubsidiariesConsolidated Balance Sheets

December 31,

(millions - except per share amount) 2020 2019

Assets

Available-for-sale securities, at fair value:Fixed maturities (amortized cost: $35,589.1 and $32,643.1) $ 36,810.9 $ 33,110.3Short-term investments (amortized cost: $5,218.5 and $1,798.8) 5,218.5 1,798.8

Total available-for-sale securities 42,029.4 34,909.1Equity securities, at fair value:

Nonredeemable preferred stocks (cost: $1,358.7 and $971.3) 1,447.9 1,038.9Common equities (cost: $1,187.3 and $1,125.5) 4,053.0 3,306.3

Total equity securities 5,500.9 4,345.2Total investments 47,530.3 39,254.3

Cash and cash equivalents 76.5 226.2

Restricted cash 0 1.2Total cash, cash equivalents, and restricted cash 76.5 227.4

Accrued investment income 176.4 181.3Premiums receivable, net of allowance for credit losses of $356.2 and $283.2 8,160.1 7,507.3Reinsurance recoverables 4,019.4 3,378.9Prepaid reinsurance premiums 368.1 626.5Deferred acquisition costs 1,237.2 1,056.5Property and equipment, net of accumulated depreciation of $1,291.4 and $1,138.1 1,106.0 1,213.7Goodwill 452.7 452.7Intangible assets, net of accumulated amortization of $326.1 and $314.0 171.4 228.3Other assets 800.2 783.6

Total assets $ 64,098.3 $ 54,910.5

Liabilities

Unearned premiums $ 13,437.5 $ 12,388.8Loss and loss adjustment expense reserves 20,265.8 18,105.4Net federal deferred income taxes 310.0 118.0Dividends payable on common shares 2,694.5 1,375.4Accounts payable, accrued expenses, and other liabilities1 4,955.8 4,617.0Debt2 5,396.1 4,407.1

Total liabilities 47,059.7 41,011.7Redeemable noncontrolling interest (NCI)3 0 225.6Shareholders’ Equity

Serial Preferred Shares (authorized 20.0)Serial Preferred Shares, Series B, no par value (cumulative, liquidation preference of $1,000 pershare) (authorized, issued, and outstanding 0.5) 493.9 493.9

Common shares, $1.00 par value (authorized 900.0; issued 797.5, including treasury shares of 212.3and 212.9) 585.2 584.6

Paid-in capital 1,672.9 1,573.4Retained earnings 13,354.9 10,679.6Accumulated other comprehensive income (loss):

Net unrealized gains (losses) on fixed-maturity securities 947.3 360.8Net unrealized losses on forecasted transactions (15.6) (16.4)Accumulated other comprehensive income attributable to NCI 0 (2.7)

Total accumulated other comprehensive income (loss) attributable to Progressive 931.7 341.7Total shareholders’ equity 17,038.6 13,673.2

Total liabilities, redeemable NCI, and shareholders’ equity $ 64,098.3 $ 54,910.51See Note 1 – Reporting and Accounting Policies for Commitments and Contingencies and Note 12 – Litigation for further discussion.2Consists of both short-term and long-term debt. See Note 4 – Debt for further discussion.3See Note 15 – Redeemable Noncontrolling Interest for further discussion.See notes to consolidated financial statements.

App.-A-3

The Progressive Corporation and SubsidiariesConsolidated Statements of Changes in Shareholders’ Equity

For the years ended December 31,

(millions - except per share amounts) 2020 2019 2018

Serial Preferred Shares, No Par Value

Balance, beginning of year $ 493.9 $ 493.9 $ 0

Issuance of Serial Preferred Shares, Series B 0 0 493.9

Balance, end of year 493.9 493.9 493.9

Common Shares, $1.00 Par Value

Balance, beginning of year 584.6 583.2 581.7

Treasury shares purchased (1.3) (1.3) (1.4)

Net restricted equity awards issued/vested 1.9 2.7 2.9

Balance, end of year 585.2 584.6 583.2

Paid-In Capital

Balance, beginning of year 1,573.4 1,479.0 1,389.2

Amortization of equity-based compensation 89.4 90.1 76.2

Treasury shares purchased (3.6) (3.2) (3.3)

Net restricted equity awards issued/vested (1.9) (2.7) (2.9)

Reinvested dividends on restricted stock units 18.2 10.6 12.2

Adjustment to carrying amount of redeemable noncontrolling interest (2.6) (0.4) 7.6

Balance, end of year 1,672.9 1,573.4 1,479.0

Retained Earnings

Balance, beginning of year 10,679.6 8,386.6 6,031.7

Net income attributable to Progressive 5,704.6 3,970.3 2,615.3

Treasury shares purchased (106.7) (86.8) (74.3)

Cash dividends declared on common shares ($4.90, $2.65, and $2.5140 per share)1 (2,865.9) (1,548.4) (1,466.0)

Cash dividends declared on Serial Preferred Shares, Series B ($80.625, $53.75, and$27.024 per share)1 (40.2) (26.8) (13.5)

Reinvested dividends on restricted stock units (18.2) (10.6) (12.2)

Cumulative effect of change in accounting principle 0 0 1,300.2

Reclassification of disproportionate tax effects 0 0 4.3

Other, net 1.7 (4.7) 1.1

Balance, end of year 13,354.9 10,679.6 8,386.6

Accumulated Other Comprehensive Income (Loss) Attributable to Progressive

Balance, beginning of year 341.7 (120.9) 1,282.2

Attributable to noncontrolling interest 2.7 (4.6) (0.1)

Other comprehensive income (loss) 587.3 467.2 (98.5)

Cumulative effect of change in accounting principle 0 0 (1,300.2)

Reclassification of disproportionate tax effects 0 0 (4.3)

Balance, end of year 931.7 341.7 (120.9)

Total shareholders’ equity $17,038.6 $13,673.2 $10,821.8

1See Note 14 – Dividends for further discussion.

There are 5.0 million Voting Preference Shares authorized; no such shares have been issued.

See notes to consolidated financial statements.

App.-A-4

The Progressive Corporation and SubsidiariesConsolidated Statements of Cash FlowsFor the years ended December 31,

(millions) 2020 2019 2018

Cash Flows From Operating Activities

Net income $ 5,704.6 $ 3,980.0 $ 2,621.0

Adjustments to reconcile net income to net cash provided by operating activities:

Depreciation 274.9 239.8 190.4

Amortization of intangible assets 56.9 66.3 72.0

Net amortization of fixed-income securities 100.9 33.3 34.3

Amortization of equity-based compensation 89.4 90.2 77.2

Net realized (gains) losses on securities (1,630.0) (1,029.2) 405.5

Net (gains) losses on disposition of property and equipment 12.5 11.0 32.1

Changes in:

Premiums receivable (652.8) (1,010.2) (1,074.6)

Reinsurance recoverables (640.5) (682.8) (422.7)

Prepaid reinsurance premiums 258.4 (316.8) (106.4)

Deferred acquisition costs (180.7) (104.9) (171.1)

Income taxes (23.1) 227.2 (158.7)

Unearned premiums 1,048.7 1,702.3 1,783.0

Loss and loss adjustment expense reserves 2,160.4 2,704.6 2,313.9

Accounts payable, accrued expenses, and other liabilities 328.9 611.6 746.6

Other, net (2.9) (260.8) (57.7)

Net cash provided by operating activities 6,905.6 6,261.6 6,284.8

Cash Flows From Investing Activities

Purchases:

Fixed maturities (32,037.5) (28,765.2) (21,153.0)

Equity securities (951.2) (379.9) (538.8)

Sales:

Fixed maturities 22,727.2 18,412.7 7,835.6

Equity securities 431.8 471.4 823.5

Maturities, paydowns, calls, and other:

Fixed maturities 7,109.4 6,145.5 5,099.8

Equity securities 113.8 49.9 26.6

Net (purchases) sales of short-term investments (3,393.2) 31.5 1,116.3

Net unsettled security transactions 83.6 6.0 11.7

Purchases of property and equipment (223.5) (363.5) (266.0)

Sales of property and equipment 21.9 53.3 9.4

Net cash used in investing activities (6,117.7) (4,338.3) (7,034.9)

Cash Flows From Financing Activities

Dividends paid to common shareholders (1,551.0) (1,643.2) (654.9)

Dividends paid to preferred shareholders (26.8) (26.8) (13.5)

Acquisition of treasury shares for restricted stock tax liabilities (68.7) (84.4) (78.6)

Acquisition of treasury shares acquired in open market (42.9) (6.9) (0.4)

Acquisition of additional shares of ARX Holding Corp. (243.0) (11.2) (296.9)

Net proceeds from debt issuance 986.3 0 1,134.0

Proceeds from exercise of equity options 7.3 1.6 3.3

Net proceeds from issuance of Serial Preferred Shares, Series B 0 0 493.9

Payments of debt 0 0 (37.1)

Net cash provided by (used in) financing activities (938.8) (1,770.9) 549.8

Increase (decrease) in cash, cash equivalents, and restricted cash (150.9) 152.4 (200.3)

Cash, cash equivalents, and restricted cash - beginning of year 227.4 75.0 275.3

Cash, cash equivalents, and restricted cash - end of year $ 76.5 $ 227.4 $ 75.0

See notes to consolidated financial statements.

App.-A-5

The Progressive Corporation and SubsidiariesNotes to Consolidated Financial Statements

December 31, 2020, 2019, and 2018

1. REPORTING AND ACCOUNTING POLICIES

Nature of Operations The Progressive insuranceorganization began business in 1937. The financialresults of The Progressive Corporation include itssubsidiaries and affiliates (references to “subsidiaries” inthese notes include affiliates as well). Our insurancesubsidiaries provide personal and commercial autoinsurance, personal residential and commercial propertyinsurance, general liability insurance, and otherspecialty property-casualty insurance and relatedservices. Our Personal Lines segment writes insurancefor personal autos and recreational vehicles, which werefer to as our special lines products. Our CommercialLines segment writes auto-related primary liability andphysical damage insurance, and general liability andproperty insurance, predominately for small businesses.Our Property segment writes residential propertyinsurance for homeowners, other property owners, andrenters. We operate our businesses throughout theUnited States through both the independent agency anddirect channels.

Basis of Consolidation and Reporting Theaccompanying consolidated financial statements includethe accounts of The Progressive Corporation, our whollyowned insurance and non-insurance subsidiaries, andaffiliates, in which we have a controlling financialinterest. All intercompany accounts and transactions areeliminated in consolidation. All revenues are generatedfrom external customers and we do not have a relianceon any major customer.

Estimates We are required to make estimates andassumptions when preparing our financial statementsand accompanying notes in conformity with accountingprinciples generally accepted in the United States ofAmerica (GAAP). As estimates develop into fact, resultsmay, and will likely, differ from those estimates.

Investments Our fixed-maturity securities and short-term investments are accounted for on anavailable-for-sale basis. Fixed-maturity securities includedebt securities and redeemable preferred stocks, whichmay have fixed or variable principal payment schedules,may be held for indefinite periods of time, and may beused as a part of our asset/liability strategy or sold inresponse to changes in interest rates, anticipatedprepayments, risk/reward characteristics, liquidity needs,or other economic factors. These securities are carried atfair value with the corresponding unrealized gains

(losses), net of deferred income taxes, reported inaccumulated other comprehensive income.

Short-term investments may include Eurodollardeposits, commercial paper, repurchase transactions,and other securities expected to mature within one year.From time to time, we may also invest in municipalbonds that have maturity dates that are longer than oneyear but have either liquidity facilities or mandatory putfeatures within one year.

Equity securities include common stocks,nonredeemable preferred stocks, and other riskinvestments. These securities are carried at fair value,with the changes in fair value reported as a componentof net holding period gains (losses) on securitiesreported in net income.

Derivative instruments may include futures, options,forward positions, interest rate swap agreements, andcredit default swaps and may be used in the portfolio forgeneral investment purposes or to hedge the exposureto variable cash flows of a forecasted transaction (cashflow hedge).

We did not have any derivatives outstanding atDecember 31, 2020 or 2019. To the extent we havederivatives held for general investment purposes, thesederivative instruments would be recognized as eitherassets or liabilities and measured at fair value, withchanges in fair value recognized in net income as acomponent of net holding period gains (losses) onsecurities.

Derivatives designated as hedges are required to beevaluated on established criteria to determine theeffectiveness of their correlation to, and ability to reducethe designated risk of, specific securities ortransactions. Effectiveness is required to be reassessedregularly. For cash flow hedges that are deemed to beeffective, the changes in fair value of the hedge wouldbe reported as a component of accumulated othercomprehensive income and subsequently amortizedinto earnings over the life of the hedged transaction. If ahedge is deemed to become ineffective or discontinued,changes in fair value of the derivative instrument wouldbe reported in income for the current period.

App.-A-6

For derivatives settled through a clearinghouse,collateral is required to post initial margin and is subjectto increases in margin beyond changes in fair value.Exposure to credit risk is limited to the carrying value;collateral may be required to limit credit risk. Forbi-lateral derivative positions, net cash requirements arelimited to changes in fair values, which may vary as aresult of changes in interest rates, currency exchangerates, and other factors. We have elected not to offsetfair value amounts that arise from derivative positionswith the same counterparty under a master nettingarrangement.

Investment securities are exposed to various risks suchas interest rate, market, credit, and liquidity risk. Fairvalues of securities fluctuate based on the nature andmagnitude of changing market conditions; significantchanges in market conditions could materially affect theportfolio’s value in the near term. We routinely monitorour fixed-maturity portfolio for pricing changes thatmight indicate potential credit losses exist and performdetailed reviews of securities with unrealized losses. Foran unrealized loss that we determined to be related tocurrent market conditions, we will not record anallowance for credit losses or a write-off of the fair valuefor securities we do not intend to sell. We will continueto monitor these securities to determine if the unrealizedloss is due to credit deterioration. If we believe that apotential credit loss exists, we will record an allowancefor the credit loss and recognize the realized loss as acomponent of realized gains and losses in the incomestatement. Once a credit loss allowance has beenestablished, we will continue to evaluate the security, atleast quarterly, to determine if changes in conditionshave created the need to either increase, or decrease,the allowance recorded. If we determine that a securitywith a credit loss allowance, previously recorded, islikely to be sold prior to the potential recovery of thecredit loss or if we determine that the loss isuncollectible, we will reverse the allowance and write-offthe security to its fair value.

Investment income consists of interest, dividends, andaccretion (net of amortization). Interest is recognized onan accrual basis using the effective yield method,except for asset-backed securities, discussed below.Depending on the nature of the equity instruments,dividends are recorded at either the ex-dividend date oron an accrual basis.

Asset-backed securities, which are included in our fixed-maturity portfolio, are generally accounted for under theretrospective method. The retrospective methodrecalculates yield assumptions (based on changes ininterest rates or cash flow expectations) historically tothe inception of the investment holding period, and

applies the required adjustment, if any, to the costbasis, with the offset recorded to investment income.The prospective method is used primarily for interest-only securities, asset-backed securities below highinvestment-grade status (i.e., below AA-), and certainasset-backed securities with sub-prime loan exposureor where there is a greater risk of non-performance andwhere it is possible the initial investment may not besubstantially recovered. The prospective methodrequires a calculation of expected future repaymentsand resets the yield to allow for future periodadjustments; no current period impact to investmentincome or the security’s cost is made based on the cashflow update. Prepayment assumptions are updatedquarterly.

Realized gains (losses) on securities are computedbased on the first-in first-out method. Realized gains(losses) also includes holding period valuation changeson equity securities, hybrid instruments (e.g., securitieswith embedded options, where the option is a feature ofthe overall change in the value of the instrument), andderivatives, as well as initial credit allowance losses,subsequent changes in credit loss allowances, andwrite-offs for losses deemed uncollectible or securitiesin a loss position that are expected to be sold prior tothe recovery of the credit loss.

Insurance Premiums and Receivables Insurancepremiums written are earned into income on a pro ratabasis over the period of risk, based on a daily earningsconvention. Accordingly, unearned premiums representthe portion of premiums written that are applicable tothe unexpired risk. We provide insurance and relatedservices to individuals and commercial accounts andoffer a variety of payment plans. Generally, premiumsare collected prior to providing risk coverage, minimizingour exposure to credit risk.

For our Personal Lines and Commercial Linesbusinesses, we perform a policy level evaluation todetermine the extent to which the premiums receivablebalance exceeds the unearned premiums balance. Wethen age this exposure to establish an allowance forcredit losses based on prior experience.

For our Property business, the risk of uncollectibility isrelatively low. If premiums are unpaid by the policy duedate, we provide advance notice of cancellation inaccordance with each state’s requirements and, if thepremiums remain unpaid after receipt of notice, cancelthe policy and write off any remaining balance.

To determine an allowance for credit losses, weevaluate the collectibility of premiums receivables basedon historical and current collections experience using

App.-A-7

actuarial analysis. Our estimate of the futurerecoverability of our projected ultimate at-risk exposuresalso takes into consideration any unusualcircumstances that we may encounter, such asmoratoriums or other programs that may suspendcollections. The following table summarizes changes inour allowance for credit loss exposure on our premiumreceivables:

(millions) 2020 2019

Balance at January 1 $ 283.2 $ 252.1

Increase in allowance1 472.0 433.5

Write-offs2 (399.0) (402.4)

Balance at December 31 $ 356.2 $ 283.21Represents the incremental increase in other underwriting expenses.2Represents the portion of allowance that is reversed when premiumreceivables are written off.

Premiums receivable balances are written off once wehave exhausted our collection efforts. The increase in theallowance during 2020 in part reflects the greaterpotential for credit losses due to financial hardships ofpolicyholders as a result of the economic impacts relatedto the spread of the novel coronavirus, COVID-19.

Deferred Acquisition Costs Deferred acquisitioncosts include commissions, premium taxes, and othervariable underwriting and direct sales costs incurred inconnection with the successful acquisition or renewal ofinsurance contracts. These acquisition costs, net ofceding allowances, are deferred and amortized over thepolicy period in which the related premiums are earned.We consider anticipated investment income indetermining the recoverability of these costs.Management believes these costs will be fullyrecoverable in the near term.

We do not defer any advertising costs. Total advertisingcosts, which are expensed as incurred, for the yearsended December 31, were:

(millions) Advertising Costs

2020 $ 2,175.7

2019 1,837.3

2018 1,422.4

Loss and Loss Adjustment Expense Reserves Lossreserves represent the estimated liability on claimsreported to us, plus reserves for losses incurred but notrecorded (IBNR). These estimates are reported net ofamounts estimated to be recoverable from salvage andsubrogation. Loss adjustment expense reservesrepresent the estimated expenses required to settlethese claims. The methods of making estimates and

establishing these reserves are reviewed regularly, andresulting adjustments are reflected in income in thecurrent period. Such loss and loss adjustment expensereserves are susceptible to change in the near term.

Reinsurance Our reinsurance activity includestransactions which are categorized as Regulated andNon-Regulated. Regulated refers to plans in which weparticipate that are governed by insurance regulationsand include state-provided reinsurance facilities (e.g.,Michigan Catastrophic Claims Association, NorthCarolina Reinsurance Facility, Florida HurricaneCatastrophe Fund), as well as state-mandatedinvoluntary plans for commercial vehicles (CommercialAutomobile Insurance Procedures/Plans – CAIP) andfederally regulated plans for flood (National FloodInsurance Program – NFIP); we act as a servicing agentfor CAIP and as a participant in the “Write Your Own”program for the NFIP. Non-Regulated includes voluntarycontractual arrangements primarily related to ourProperty business and to the transportation networkcompany business written by our Commercial Linessegment. Prepaid reinsurance premiums are earned on apro rata basis over the period of risk, based on a dailyearnings convention, which is consistent with premiumsearned. See Note 7 – Reinsurance for further discussion.

We routinely monitor changes in the credit quality andconcentration risks of the reinsurers who are counterparties to our reinsurance recoverables to determine ifan allowance for credit losses should be established.

Income Taxes The income tax provision is calculatedunder the balance sheet approach. Deferred tax assetsand liabilities are recorded based on the differencebetween the financial statement and tax bases of assetsand liabilities at the enacted tax rates. The principalitems giving rise to such differences are investmentsecurities (e.g., net unrealized gains (losses), netholding period gains (losses) on securities, write-downson securities determined to be other-than-temporarilyimpaired), loss and loss adjustment expense reserves,unearned premiums reserves, deferred acquisitioncosts, property and equipment, intangible assets, andnon-deductible accruals. We review our deferred taxassets regularly for recoverability. See Note 5 – IncomeTaxes for further discussion.

Property and Equipment Property and equipment arerecorded at cost, less accumulated depreciation.Depreciation is recognized over the estimated usefullives of the assets using accelerated methods forcomputer equipment and the straight-line method for allother fixed assets. We evaluate impairment wheneverevents or circumstances warrant such a review andwrite-off the impaired assets if appropriate.

App.-A-8

The cost and useful lives for property and equipment at December 31, were:

($ in millions) 2020 2019 Useful Lives

Land $ 151.6 $ 161.6 NA

Buildings, improvements, and integrated components 872.7 927.1 7-40 years

Capitalized software 392.6 367.1 3-10 years

Software licenses (internal use) 335.5 286.8 1-5 years

Computer equipment 253.8 223.3 3 years

All other property and equipment 391.2 385.9 3-10 years

Total cost 2,397.4 2,351.8

Accumulated depreciation (1,291.4) (1,138.1)

Balance at end of year $ 1,106.0 $ 1,213.7

NA = Not applicable; land is not a depreciable asset.

Included in other assets in the consolidated balance sheets are “held for sale” property, which represents the fairvalue of these properties less the estimated costs to sell, of $56.6 million and $32.9 million, at December 31, 2020and 2019, respectively, and capitalized cloud computing arrangement implementation costs, net of amortization, of$25.3 million at December 31, 2020. We adopted the new accounting standard for cloud computing arrangements inJanuary 2020; see New Accounting Standards below in this Note 1 for further discussion.

Goodwill and Intangible Assets Goodwill is theexcess of the purchase price over the estimated fairvalue of the assets and liabilities acquired andrepresents the future economic benefits arising fromother assets acquired that could not be individuallyidentified and separately recognized.

Intangible assets are non-financial assets lackingphysical substance, such as customer and agencyrelationships and software rights, and represent thefuture economic benefit of those acquired assets. SeeNote 16 – Goodwill and Intangible Assets for furtherdiscussion.

We evaluate our goodwill for impairment at leastannually using a qualitative approach. If events orchanges in circumstances indicate that the carryingvalue of goodwill or intangible assets may not berecoverable, we will evaluate such items for impairmentusing a quantitative approach.

Guaranty Fund Assessments We are subject to stateguaranty fund assessments, which provide for thepayment of covered claims or other insuranceobligations of insurance companies deemed insolvent.These assessments are accrued after a formaldetermination of insolvency has occurred, and we havewritten the premiums on which the assessments will bebased. Assessments that are available for recoupmentfrom policyholders are capitalized when incurred; allother assessments are expensed.

Fees and Other Revenues Fees and other revenuesprimarily represent fees collected from policyholdersrelating to installment charges in accordance with ourbill plans, as well as late payment and insufficient fundsfees and revenue from ceding commissions. Fees andother revenues are generally earned when invoiced,except for excess ceding commissions, which areearned over the policy period.

Service Revenues and Expenses Our servicebusinesses provide insurance-related services. Servicerevenues and expenses from our commission-basedbusinesses are recorded in the period in which they areearned or incurred. Service revenues generated fromprocessing business for involuntary CAIP plans areearned on a pro rata basis over the term of the relatedpolicies. Service expenses related to these CAIP plansare expensed as incurred.

Equity-Based Compensation We issue time-basedand performance-based restricted stock unit awards tokey members of management as our form of equitycompensation, and time-based restricted stock awards tonon-employee directors. Collectively, we refer to theseawards as “restricted equity awards.” Compensationexpense for time-based restricted equity awards withinstallment vesting is recognized over each respectivevesting period. For performance-based restricted equityawards, compensation expense is recognized over theestimated vesting periods. Dividend equivalent units arecredited to outstanding restricted stock unit awards, bothtime-based and performance-based, at the time a

App.-A-9

dividend is paid to shareholders and paid upon vesting ofthe underlying award. We record an estimate forexpected forfeitures of restricted equity awards based onour historical forfeiture rates.

The total compensation expense recognized for equity-based compensation for the years ended December 31,was:

(millions) 2020 2019 2018

Pretax expense $ 89.4 $ 90.2 $ 77.2Tax benefit 18.8 18.9 16.2

Earnings Per Common Share Net income attributableto Progressive is reduced by preferred share dividendsto determine net income available to commonshareholders, and is used in our calculation of the percommon share amounts. Basic earnings per commonshare is computed using the weighted average numberof common shares outstanding during the reportingperiod, excluding unvested time-based restricted stockawards. Diluted earnings per common share includescommon stock equivalents assumed outstanding duringthe period. Our common stock equivalents include theincremental shares assumed to be issued for:

• earned but unvested time-based restricted equityawards, and

• performance-based restricted equity awards thatsatisfied certain contingency conditions for unvestedcommon stock equivalents during the period and arehighly likely to continue to satisfy the conditions untilthe date of vesting.

Supplemental Cash Flow Information Cash and cashequivalents include bank demand deposits and dailyovernight reverse repurchase commitments of fundsheld in bank demand deposit accounts by certainsubsidiaries, and are not considered part of theinvestment portfolio. The amount of reverse repurchasecommitments held by these subsidiaries atDecember 31, 2020, 2019, and 2018, were$93.5 million, $46.3 million, and $117.3 million,respectively. Restricted cash on our consolidatedbalance sheets represents cash that is restricted to payflood claims under the NFIP’s “Write Your Own”program, for which certain subsidiaries areadministrators.

For the year ended December 31, 2020, non-cashactivity includes declared but unpaid common sharedividends of $2,694.5 million and preferred sharedividends of $13.4 million, and operating lease liabilitiesarising from obtaining right-of-use assets of

$60.3 million (see Note 13 – Leases and Note 14 –Dividends for further discussion).

For the years ended December 31, we paid thefollowing:

(millions) 2020 2019 2018

Income taxes $1,446.3 $ 954.3 $ 702.6Interest 206.0 184.9 154.0Operating lease

liabilities 86.5 84.0 NA

NA = Not applicable prior to the adoption of the newaccounting standard in 2019.

Commitments and Contingencies We have certainnoncancelable purchase obligations for goods andservices with minimum commitments of $830.4 millionat December 31, 2020, primarily consisting of softwarelicenses, maintenance on information technologyequipment, and media placements. In addition, we haveseveral multiple-layer property catastrophe reinsurancecontracts with various reinsurers with terms rangingfrom one to three years; the minimum commitmentunder these agreements at December 31, 2020, was$191.1 million.

New Accounting Standards On January 1, 2020, weadopted the following new Accounting StandardsUpdates (ASU).

Cloud Computing ArrangementsThis ASU, which provides guidance on the requirementsfor capitalizing and amortizing implementation costsincurred in a cloud computing arrangement that doesnot include a software license, was adopted on aprospective basis. See the Property and Equipmentdiscussion above for the cloud computing arrangementimplementation cost capitalized at December 31, 2020.

Fair Value MeasurementsWe early adopted a portion of this ASU in 2018 and theremaining provisions in 2020. This ASU amended thedisclosure requirements for fair value measurements torequire companies to disclose the changes in unrealizedgains and losses for the period included in othercomprehensive income for recurring Level 3 fair valuemeasurements held at the end of the reporting periodand the range and weighted average of significantunobservable inputs used to develop Level 3 fair valuemeasurements and removed current disclosurerequirements for the amount of and reasons fortransfers between Level 1 and Level 2 of the fair valuehierarchy, the policy for timing of transfers between

App.-A-10

levels, and the valuation processes for Level 3 fair valuemeasurements. The adoption of this ASU had no impacton our financial condition, cash flows, or results ofoperations.

Goodwill Impairment Test SimplificationThe ASU eliminated the requirement to determine theimplied fair value of goodwill in measuring animpairment loss and now requires the measurement ofa goodwill impairment to represent the excess of thereporting unit’s carrying value over fair value, limited tothe carrying value of goodwill. The adoption of this ASUhad no impact on our financial condition, cash flows, orresults of operations.

Measurement of Credit Losses on Financial InstrumentsThis ASU modified the existing accounting guidancerelated to the impairment evaluation for our

available-for-sale debt securities, reinsurancerecoverables, and premiums receivable. The ASU isintended to improve the timing, and enhance theaccounting and disclosure, of credit losses on financialassets. To the extent a credit loss is determined toexist, an allowance for credit losses would be requiredto be recorded as a contra asset, with changes to thecredit loss allowance recorded prospectively. Based onour analysis for available-for-sale debt securities andreinsurance recoverables as described in Note 2–Investments and Note 7– Reinsurance, respectively, noadjustment to the beginning balance of retainedearnings was required upon adoption. See theInsurance Premiums and Receivables discussion abovefor changes in the allowance for credit losses related tothe premiums receivable balance.

2. INVESTMENTS

The following tables present the composition of ourinvestment portfolio by major security type, consistent withour classification of how we manage, monitor, andmeasure the portfolio. Our securities are reported in ourconsolidated balance sheets at fair value. The changes infair value for our fixed-maturity securities (other thanhybrid securities) are reported as a component ofaccumulated other comprehensive income, net of deferred

income taxes, in our consolidated balance sheets. The netholding period gains (losses) reported below represent theinception-to-date changes in fair value of the securities.The changes in the net holding period gains (losses)between periods for the hybrid securities and equitysecurities are recorded as a component of net realizedgains (losses) on securities in our consolidated statementsof comprehensive income.

($ in millions) Cost

GrossUnrealized

Gains

GrossUnrealized

Losses

NetHolding

PeriodGains

(Losses)Fair

Value

% ofTotalFair

Value

December 31, 2020Available-for-sale securities:

Fixed maturities:U.S. government obligations $ 12,437.9 $ 305.8 $ (3.7) $ 0 $ 12,740.0 26.8%State and local government obligations 3,099.4 123.1 (0.7) 0 3,221.8 6.8Corporate debt securities 9,579.7 601.7 (0.1) 3.9 10,185.2 21.4Residential mortgage-backed securities 503.3 7.1 (0.9) 0 509.5 1.1Commercial mortgage-backed securities 6,042.6 142.5 (10.0) 0 6,175.1 13.0Other asset-backed securities 3,745.0 40.1 (0.5) 0 3,784.6 7.9Redeemable preferred stocks 181.2 3.6 (1.4) 11.3 194.7 0.4

Total fixed maturities 35,589.1 1,223.9 (17.3) 15.2 36,810.9 77.4Short-term investments 5,218.5 0 0 0 5,218.5 11.0

Total available-for-sale securities 40,807.6 1,223.9 (17.3) 15.2 42,029.4 88.4Equity securities:

Nonredeemable preferred stocks 1,358.7 0 0 89.2 1,447.9 3.1Common equities 1,187.3 0 0 2,865.7 4,053.0 8.5

Total equity securities 2,546.0 0 0 2,954.9 5,500.9 11.6Total portfolio1 $ 43,353.6 $ 1,223.9 $ (17.3) $ 2,970.1 $ 47,530.3 100.0%

App.-A-11

($ in millions) Cost

GrossUnrealized

Gains

GrossUnrealized

Losses

NetHolding

PeriodGains

(Losses)Fair

Value

% ofTotalFair

Value

December 31, 2019

Available-for-sale securities:Fixed maturities:

U.S. government obligations $ 13,100.7 $ 194.1 $ (43.7) $ 0 $ 13,251.1 33.7%

State and local government obligations 1,686.0 30.0 (2.7) 0 1,713.3 4.4

Corporate debt securities 6,860.3 206.6 (0.5) 1.3 7,067.7 18.0

Residential mortgage-backed securities 625.0 4.5 (2.0) 0 627.5 1.6

Commercial mortgage-backed securities 5,020.7 61.5 (6.0) 0 5,076.2 12.9

Other asset-backed securities 5,164.7 16.2 (1.4) 0 5,179.5 13.2

Redeemable preferred stocks 185.7 4.1 (1.3) 6.5 195.0 0.5

Total fixed maturities 32,643.1 517.0 (57.6) 7.8 33,110.3 84.3

Short-term investments 1,798.8 0 0 0 1,798.8 4.6

Total available-for-sale securities 34,441.9 517.0 (57.6) 7.8 34,909.1 88.9

Equity securities:

Nonredeemable preferred stocks 971.3 0 0 67.6 1,038.9 2.7

Common equities 1,125.5 0 0 2,180.8 3,306.3 8.4

Total equity securities 2,096.8 0 0 2,248.4 4,345.2 11.1

Total portfolio1 $ 36,538.7 $ 517.0 $ (57.6) $ 2,256.2 $ 39,254.3 100.0%1Our portfolio reflects the effect of net unsettled security transactions; at December 31, 2020, $95.5 million was included in “other liabilities,”compared to $11.9 million at December 31, 2019.The total fair value of the portfolio at December 31, 2020 and 2019 included $6.2 billion and $3.2 billion, respectively, of securities held in aconsolidated, non-insurance subsidiary of the holding company, net of any unsettled security transactions. A portion of these investments weresold and proceeds used to pay our common share dividends; see Note 14 – Dividends for additional information.

At December 31, 2020, bonds and certificates ofdeposit in the principal amount of $298.2 million wereon deposit to meet state insurance regulatoryrequirements. We did not hold any securities of any oneissuer, excluding U.S. government obligations, with anaggregate cost or fair value exceeding 10% of totalshareholders’ equity at December 31, 2020 or 2019. AtDecember 31, 2020, we did not hold any debt securitiesthat were non-income producing during the preceding12 months.

Short-Term Investments Our short-term investmentsmay include commercial paper and other investmentsthat are expected to mature or are redeemable withinone year.

We invested in repurchase and reverse repurchasetransactions during 2020 and 2019, but did not haveany open positions at December 31, 2020 or 2019. Tothe extent we enter into repurchase or reverserepurchase transactions, consistent with past practice,we would elect not to offset these transactions and

would report them on a gross basis on our consolidatedbalance sheets, despite the option to elect to offsetthese transactions as long as they were with the samecounterparty and subject to an enforceable masternetting arrangement.

Hybrid Securities Certain securities in our fixedmaturities portfolio are accounted for as hybridsecurities because they contain embedded derivativesthat are not deemed to be clearly and closely related tothe host investments. These securities are reported atfair value at December 31:

(millions) 2020 2019

Fixed Maturities:

State and local governmentobligations $ 0 $ 3.5

Corporate debt securities 188.4 91.2

Other asset-backed securities 34.8 2.6

Redeemable preferred stocks 131.4 92.1

Total hybrid securities $ 354.6 $ 189.4

App.-A-12

Since the embedded derivatives (e.g., change-in-control put option, debt-to-equity conversion, or any other featureunrelated to the credit quality or risk of default of the issuer that could impact the amount or timing of our expectedfuture cash flows) do not have observable intrinsic values, we have elected to record the changes in fair value ofthese securities through income as a component of net realized gains or losses.

Fixed Maturities The composition of fixed maturities by maturity at December 31, 2020, was:

(millions) Cost Fair Value

Less than one year $ 5,734.9 $ 5,765.4

One to five years 20,769.2 21,377.3

Five to ten years 8,939.8 9,512.2

Ten years or greater 145.2 156.0

Total $ 35,589.1 $ 36,810.9

Asset-backed securities are classified in the maturity distribution table based upon their projected cash flows. All othersecurities that do not have a single maturity date are reported based upon expected average maturity. Contractualmaturities may differ from expected maturities because the issuers of the securities may have the right to call orprepay obligations.

Gross Unrealized Losses The following tables show the composition of gross unrealized losses by major securitytype and by the length of time that individual securities have been in a continuous unrealized loss position:

Total

No. of

Sec.

Total

Fair

Value

Gross

Unrealized

Losses

Less than 12 Months 12 Months or Greater

($ in millions)

No. of

Sec.

Fair

Value

Unrealized

Losses

No. of

Sec.

Fair

Value

Unrealized

Losses

December 31, 2020

U.S. government obligations 9 $ 1,511.0 $ (3.7) 9 $ 1,511.0 $ (3.7) 0 $ 0 $ 0

State and local governmentobligations 30 208.7 (0.7) 30 208.7 (0.7) 0 0 0

Corporate debt securities 7 129.4 (0.1) 7 129.4 (0.1) 0 0 0

Residential mortgage-backedsecurities 21 44.4 (0.9) 0 0 0 21 44.4 (0.9)

Commercial mortgage-backedsecurities 43 893.3 (10.0) 9 93.6 (0.3) 34 799.7 (9.7)

Other asset-backed securities 22 183.7 (0.5) 9 74.4 (0.1) 13 109.3 (0.4)

Redeemable preferred stocks 1 11.0 (1.4) 0 0 0 1 11.0 (1.4)

Total fixed maturities 133 $ 2,981.5 $ (17.3) 64 $ 2,017.1 $ (4.9) 69 $ 964.4 $ (12.4)

Total

No. of

Sec.

Total

Fair

Value

Gross

Unrealized

Losses

Less than 12 Months 12 Months or Greater

($ in millions)

No. of

Sec.

Fair

Value

Unrealized

Losses

No. of

Sec.

Fair

Value

Unrealized

Losses

December 31, 2019

U.S. government obligations 23 $ 5,152.4 $ (43.7) 19 $ 5,057.2 $ (43.6) 4 $ 95.2 $ (0.1)

State and local governmentobligations 67 314.3 (2.7) 52 287.5 (2.6) 15 26.8 (0.1)

Corporate debt securities 16 247.6 (0.5) 12 191.4 (0.5) 4 56.2 0

Residential mortgage-backedsecurities 41 292.8 (2.0) 12 163.7 (0.9) 29 129.1 (1.1)

Commercial mortgage-backedsecurities 98 1,742.4 (6.0) 79 1,400.0 (5.3) 19 342.4 (0.7)

Other asset-backed securities 61 1,000.6 (1.4) 43 938.5 (0.9) 18 62.1 (0.5)

Redeemable preferred stocks 1 11.2 (1.3) 0 0 0 1 11.2 (1.3)

Total fixed maturities 307 $ 8,761.3 $ (57.6) 217 $ 8,038.3 $ (53.8) 90 $ 723.0 $ (3.8)

App.-A-13

During 2020, we had seven securities that had their credit ratings downgraded, with a combined fair value of$65.0 million and an unrealized loss of $1.6 million as of December 31, 2020, comprised of residential andcommercial mortgage-backed securities.

A review of the securities in an unrealized loss position indicated that the issuers were current with respect to theirinterest obligations and that there was no evidence of deterioration of the current cash flow projections that wouldindicate we would not receive the remaining principal at maturity.

Allowance For Credit and Uncollectible Losses Weare required to measure the amount of potential creditlosses for all fixed-maturity securities in an unrealizedloss position. We did not record any allowances forcredit losses or any write-offs for amounts deemed tobe uncollectible during 2020 and did not have a creditloss allowance balance as of December 31, 2020. Weconsidered several factors and inputs related to theindividual securities as part of our analysis. Themethodology and significant inputs used to measure theamount of credit losses in our portfolio included:

• current performance indicators on the businessmodel or underlying assets (e.g., delinquencyrates, foreclosure rates, and default rates);

• credit support (via current levels of subordination);• historical credit ratings; and• updated cash flow expectations based upon these

performance indicators.

In order to determine the amount of credit loss, if any,we initially reviewed securities in a loss position todetermine whether it was likely that we would berequired, or intended, to sell any of the securities priorto the recovery of their respective cost bases (whichcould be maturity). If we were likely to, or intended to,sell prior to a potential recovery, we would write off theunrealized loss. For those securities that we determinedwe were not likely to, or did not intend to, sell prior to a

potential recovery, we calculated the net present value(NPV) of the cash flows expected (i.e., expectedrecovery value) using the current book yield for eachsecurity. The NPV was then compared to the security’scurrent amortized value to determine if a credit lossexisted. In the event that the NPV was below theamortized value, and the amount was determined to bematerial individually, or in aggregate, a credit loss wouldbe deemed to exist, and either an allowance for creditlosses would be created, or if an allowance currentlyexisted, either a recovery of the previous allowance, oran incremental loss, would be recorded to net realizedgains (losses) on securities.

As of December 31, 2020, we believe none of theunrealized losses relate to material credit losses on anyspecific securities, or in the aggregate, based on ourreview. We continue to expect all the securities in ourportfolio to pay their principal and interest obligations.

In addition, we reviewed our accrued investment incomeoutstanding on those securities in an unrealized lossposition at December 31, 2020, to determine if theaccrued interest amounts were determined to beuncollectible. Based on our analysis, we believe theissuers have sufficient liquidity and capital reserves tomeet their current interest, and future principal,obligations and, therefore, did not write off any accruedincome as uncollectible at December 31, 2020.

App.-A-14

Realized Gains (Losses) The components of net realized gains (losses) for the years ended December 31, were:

(millions) 2020 2019 2018

Gross realized gains on security sales

Available-for-sale securities:U.S. government obligations $ 612.5 $ 164.4 $ 6.7State and local government obligations 102.4 6.1 9.5Corporate and other debt securities 161.9 100.1 2.4Residential mortgage-backed securities 0 0.2 0Commercial mortgage-backed securities 23.7 8.1 2.0Other asset-backed securities 0.2 0.8 0.1Redeemable preferred stocks 0 2.2 4.5

Total available-for-sale securities 900.7 281.9 25.2Equity securities:

Nonredeemable preferred stocks 24.4 36.2 4.1Common equities 88.6 61.7 286.6

Total equity securities 113.0 97.9 290.7

Subtotal gross realized gains on security sales 1,013.7 379.8 315.9

Gross realized losses on security sales

Available-for-sale securities:U.S. government obligations (9.6) (20.4) (98.7)State and local government obligations (0.7) (0.7) (2.9)Corporate and other debt securities (6.5) (7.9) (10.4)Residential mortgage-backed securities 0 (2.3) (0.1)Commercial mortgage-backed securities (12.8) (2.2) (6.3)Other asset-backed securities 0 (0.1) (1.1)Redeemable preferred stocks 0 (0.4) (0.1)

Total available-for-sale securities (29.6) (34.0) (119.6)Equity securities:

Nonredeemable preferred stocks (8.7) (3.2) (3.9)Common equities (60.7) (8.0) (21.7)

Total equity securities (69.4) (11.2) (25.6)

Subtotal gross realized losses on security sales (99.0) (45.2) (145.2)

Net realized gains (losses) on security sales

Available-for-sale securities:U.S. government obligations 602.9 144.0 (92.0)State and local government obligations 101.7 5.4 6.6Corporate and other debt securities 155.4 92.2 (8.0)Residential mortgage-backed securities 0 (2.1) (0.1)Commercial mortgage-backed securities 10.9 5.9 (4.3)Other asset-backed securities 0.2 0.7 (1.0)Redeemable preferred stocks 0 1.8 4.4

Total available-for-sale securities 871.1 247.9 (94.4)Equity securities:

Nonredeemable preferred stocks 15.7 33.0 0.2Common equities 27.9 53.7 264.9

Total equity securities 43.6 86.7 265.1

Subtotal net realized gains (losses) on security sales 914.7 334.6 170.7

Net holding period gains (losses)

Hybrid securities 7.4 18.0 (10.4)

Equity securities 706.5 739.9 (497.5)Derivatives 1.4 0 0

Subtotal net holding period gains (losses) 715.3 757.9 (507.9)

Other-than-temporary impairment lossesOther asset impairment 0 (63.3) (68.3)

Subtotal other-than-temporary impairment losses 0 (63.3) (68.3)

Total net realized gains (losses) on securities $ 1,630.0 $ 1,029.2 $ (405.5)

App.-A-15

Realized gains (losses) on securities sold are computed using the first-in-first-out method. During 2020, we sold U.S.Treasury securities in order to selectively increase holdings across the remainder of the portfolio, predominantly in ourcorporate debt securities.

For 2019 and 2018, the other asset impairment losses related to federal renewable energy tax credit fundinvestments, which were reported in other assets on the consolidated balance sheets, and are based on an analysisthat our investments in those funds will not generate the cash flows that we anticipated.

The following table reflects our holding period realized gains (losses) on equity securities recognized for therespective years ended December 31, for equity securities held at the respective year end:

(millions) 2020 2019 2018

Total net gains (losses) recognized during the period on equity securities $ 750.1 $ 826.6 $ (232.4)

Less: Net gains (losses) recognized on equity securities sold during the period 43.6 86.7 265.1

Net holding period gains (losses) recognized during the period on equity securitiesheld at period end $ 706.5 $ 739.9 $ (497.5)

Net Investment Income The components of net investment income for the years ended December 31, were:

(millions) 2020 2019 2018

Available-for-sale securities:

Fixed maturities:

U.S. government obligations $166.3 $ 268.6 $196.8

State and local government obligations 62.7 36.5 37.7

Corporate debt securities 284.0 268.9 217.9

Residential mortgage-backed securities 11.8 21.6 27.6

Commercial mortgage-backed securities 152.9 150.1 93.9

Other asset-backed securities 96.7 117.3 75.7

Redeemable preferred stocks 14.9 19.0 12.3

Total fixed maturities 789.3 882.0 661.9

Short-term investments 29.0 41.7 52.9

Total available-for-sale securities 818.3 923.7 714.8

Equity securities:

Nonredeemable preferred stocks 60.6 61.8 45.9

Common equities 57.7 56.5 59.8

Total equity securities 118.3 118.3 105.7

Investment income 936.6 1,042.0 820.5

Investment expenses (20.0) (24.6) (24.3)

Net investment income $916.6 $1,017.4 $796.2

The amount of investment income (interest anddividends) we earn varies based on the average assetsheld during the year and the book yields of thesecurities in our portfolio. On a year-over-year basis,investment income decreased 10%, compared to lastyear, due to a decrease in the portfolio yield, which waspartially offset by an increase in average assets. Therecurring investment book yield decreased 23%,compared to 2019, as a result of investing cash from

operations and reinvesting cash from sales, maturities,paydowns, and other redemptions at market yields thatwere significantly lower than the portfolio’s overall yield.The income reduction from the negative yield changewas partially offset by an increase in income earned asa result of investing the $1.0 billion of proceeds from thedebt issued during March 2020, as well as strongpremium growth, underwriting profitability, and strongportfolio results, net of common and preferred stock

App.-A-16

dividends. The year-over-year increase in netinvestment income in 2019 compared to 2018, was dueto a combination of an increase in average assets andan increase in portfolio yields. The decrease ininvestment expenses in 2020, compared to 2019,primarily reflects lower expenses incurred due to ourdecision to no longer maintain an actively managedequity portfolio, and lower incentive-basedcompensation recognized.

Derivative Instruments During 2020, we opened andclosed U.S. Treasury Note futures to manage theportfolio duration and recorded a net realized gain of$1.4 million. The maximum notional value held at onetime during the year was $114.6 million. AtDecember 31, 2020, 2019, and 2018, we had no openderivative positions.

3. FAIR VALUE

We have categorized our financial instruments, basedon the degree of subjectivity inherent in the method bywhich they are valued, into a fair value hierarchy ofthree levels, as follows:

• Level 1: Inputs are unadjusted, quoted prices inactive markets for identical instruments at themeasurement date (e.g., U.S. governmentobligations, which are continually priced on adaily basis, active exchange-traded equitysecurities, and certain short-term securities).

• Level 2: Inputs (other than quoted pricesincluded within Level 1) that are observable forthe instrument either directly or indirectly (e.g.,certain corporate and municipal bonds andcertain preferred stocks). This includes:(i) quoted prices for similar instruments in activemarkets, (ii) quoted prices for identical or similarinstruments in markets that are not active,(iii) inputs other than quoted prices that areobservable for the instruments, and (iv) inputs

that are derived principally from or corroboratedby observable market data by correlation or othermeans.

• Level 3: Inputs that are unobservable.Unobservable inputs reflect our subjectiveevaluation about the assumptions marketparticipants would use in pricing the financialinstrument (e.g., certain structured securities andprivately held investments).

Determining the fair value of the investment portfolio isthe responsibility of management. As part of theresponsibility, we evaluate whether a market isdistressed or inactive in determining the fair value forour portfolio. We review certain market level inputs toevaluate whether sufficient activity, volume, and newissuances exist to create an active market. Based onthis evaluation, we concluded that there was sufficientactivity related to the sectors and securities for whichwe obtained valuations.

App.-A-17

The composition of the investment portfolio by major security type and our outstanding debt was:

Fair Value

(millions) Level 1 Level 2 Level 3 Total Cost

December 31, 2020

Fixed maturities:

U.S. government obligations $ 12,740.0 $ 0 $ 0 $ 12,740.0 $ 12,437.9

State and local government obligations 0 3,221.8 0 3,221.8 3,099.4

Corporate debt securities 0 10,185.2 0 10,185.2 9,579.7Subtotal 12,740.0 13,407.0 0 26,147.0 25,117.0

Asset-backed securities:

Residential mortgage-backed 0 509.5 0 509.5 503.3

Commercial mortgage-backed 0 6,175.1 0 6,175.1 6,042.6

Other asset-backed 0 3,784.6 0 3,784.6 3,745.0

Subtotal asset-backed securities 0 10,469.2 0 10,469.2 10,290.9

Redeemable preferred stocks:

Financials 0 51.6 0 51.6 51.1

Utilities 0 11.7 0 11.7 10.0

Industrials 10.8 120.6 0 131.4 120.1

Subtotal redeemable preferred stocks 10.8 183.9 0 194.7 181.2

Total fixed maturities 12,750.8 24,060.1 0 36,810.9 35,589.1

Short-term investments 4,704.9 513.6 0 5,218.5 5,218.5

Total available-for-salesecurities 17,455.7 24,573.7 0 42,029.4 40,807.6

Equity securities:

Nonredeemable preferred stocks:

Financials 117.7 1,212.3 35.0 1,365.0 1,278.6

Utilities 0 41.9 0 41.9 40.0

Industrials 0 24.3 16.7 41.0 40.1

Subtotal nonredeemable preferredstocks 117.7 1,278.5 51.7 1,447.9 1,358.7

Common equities:

Common stocks 4,049.9 0 0 4,049.9 1,184.2

Other risk investments 0 0 3.1 3.1 3.1

Subtotal common equities 4,049.9 0 3.1 4,053.0 1,187.3

Total equity securities 4,167.6 1,278.5 54.8 5,500.9 2,546.0

Total portfolio $ 21,623.3 $ 25,852.2 $ 54.8 $ 47,530.3 $ 43,353.6

Debt $ 0 $ 6,793.5 $ 0 $ 6,793.5 $ 5,396.1

App.-A-18

Fair Value

(millions) Level 1 Level 2 Level 3 Total Cost

December 31, 2019

Fixed maturities:

U.S. government obligations $ 13,251.1 $ 0 $ 0 $ 13,251.1 $ 13,100.7

State and local government obligations 0 1,713.3 0 1,713.3 1,686.0

Corporate debt securities 0 7,067.7 0 7,067.7 6,860.3

Subtotal 13,251.1 8,781.0 0 22,032.1 21,647.0

Asset-backed securities:

Residential mortgage-backed 0 627.5 0 627.5 625.0

Commercial mortgage-backed 0 5,076.2 0 5,076.2 5,020.7

Other asset-backed 0 5,179.5 0 5,179.5 5,164.7

Subtotal asset-backed securities 0 10,883.2 0 10,883.2 10,810.4

Redeemable preferred stocks:

Financials 0 51.7 0 51.7 51.5

Utilities 0 11.1 0 11.1 10.0

Industrials 11.1 121.1 0 132.2 124.2

Subtotal redeemable preferred stocks 11.1 183.9 0 195.0 185.7

Total fixed maturities 13,262.2 19,848.1 0 33,110.3 32,643.1

Short-term investments 1,797.4 1.4 0 1,798.8 1,798.8

Total fixed maturities and short-term 15,059.6 19,849.5 0 34,909.1 34,441.9

Equity securities:

Nonredeemable preferred stocks:

Financials 77.4 850.7 27.1 955.2 891.3

Utilities 0 42.3 0 42.3 39.9

Industrials 0 25.4 16.0 41.4 40.1

Subtotal nonredeemable preferredstocks 77.4 918.4 43.1 1,038.9 971.3

Common equities:

Common stocks 3,306.0 0 0 3,306.0 1,125.2

Other risk investments 0 0 0.3 0.3 0.3

Subtotal common equities 3,306.0 0 0.3 3,306.3 1,125.5

Total equity securities 3,383.4 918.4 43.4 4,345.2 2,096.8

Total available-for-sale portfolio $ 18,443.0 $ 20,767.9 $ 43.4 $ 39,254.3 $ 36,538.7

Debt $ 0 $ 5,119.6 $ 0 $ 5,119.6 $ 4,407.1

Our portfolio valuations, excluding short-terminvestments, classified as either Level 1 or Level 2 inthe above tables are priced exclusively by externalsources, including: pricing vendors, dealers/marketmakers, and exchange-quoted prices.

Our short-term investments classified as Level 1 arehighly liquid, actively marketed, and have a very shortduration, primarily 90 days or less to redemption. Thesesecurities are held at their original cost, adjusted for any

accretion of discount, since that value very closelyapproximates what an active market participant would bewilling to pay for such securities. The remainder of ourshort-term investments are classified as Level 2 and arenot priced externally since these securities continuallytrade at par value. These securities are classified asLevel 2 since they are primarily longer-dated securitiesissued by municipalities that contain either liquidityfacilities or mandatory put features within one year.

App.-A-19

At December 31, 2020, vendor-quoted pricesrepresented 76% of our Level 1 classifications (excludingshort-term investments), compared to 80% atDecember 31, 2019. The securities quoted by vendors inLevel 1 primarily represent our holdings in U.S. TreasuryNotes, which are frequently traded and the quotes areconsidered similar to exchange-traded quotes. Thebalance of our Level 1 pricing comes from quotesobtained directly from trades made on active exchanges.

At both December 31, 2020 and 2019, vendor-quotedprices comprised 99% of our Level 2 classifications(excluding short-term investments), while dealer-quotedprices represented 1%. In our process for selecting asource (e.g., dealer or pricing service) to provide pricingfor securities in our portfolio, we revieweddocumentation from the sources that detailed thepricing techniques and methodologies used by thesesources and determined if their policies adequatelyconsidered market activity, either based on specifictransactions for the particular security type or based onmodeling of securities with similar credit quality,duration, yield, and structure that were recentlytransacted. Once a source is chosen, we continue tomonitor any changes or modifications to their processesby reviewing their documentation on internal controls forpricing and market reviews. We review quality controlmeasures of our sources as they become available todetermine if any significant changes have occurred fromperiod to period that might indicate issues or concernsregarding their evaluation or market coverage.

As part of our pricing procedures, we obtain quotes frommore than one source to help us fully evaluate themarket price of securities. However, our internal pricingpolicy is to use a consistent source for individualsecurities in order to maintain the integrity of ourvaluation process. Quotes obtained from the sources arenot considered binding offers to transact. Under ourpolicy, when a review of the valuation received from ourselected source appears to be outside of what isconsidered market level activity (which is defined astrading at spreads or yields significantly different thanthose of comparable securities or outside the generalsector level movement without a reasonableexplanation), we may use an alternate source’s price. Tothe extent we determine that it may be prudent tosubstitute one source’s price for another, we will contactthe initial source to obtain an understanding of the factorsthat may be contributing to the significant price variance.

To allow us to determine if our initial source is providinga price that is outside of a reasonable range, we review

our portfolio pricing on a weekly basis. Whennecessary, we challenge prices from our sources whena price provided does not match our expectations basedon our evaluation of market trends and activity. Initially,we perform a review of our portfolio by sector to identifysecurities whose prices appear outside of a reasonablerange. We then perform a more detailed review of fairvalues for securities disclosed as Level 2. We reviewdealer bids and quotes for these and/or similarsecurities to determine the market level context for ourvaluations. We then evaluate inputs relevant for eachclass of securities disclosed in the preceding hierarchytables.

For our structured debt securities, including commercial,residential, and other asset-backed securities, weevaluate available market-related data for these andsimilar securities related to collateral, delinquencies,and defaults for historical trends and reasonablyestimable projections, as well as historical prepaymentrates and current prepayment assumptions and cashflow estimates. We further stratify each class of ourstructured debt securities into more finite sectors (e.g.,planned amortization class, first pay, second pay,senior, subordinated, etc.) and use duration, creditquality, and coupon to determine if the fair value isappropriate.

For our corporate debt and preferred stock (redeemableand nonredeemable) portfolios, as well as the notesissued by The Progressive Corporation (see Note 4 –Debt), we review securities by duration, coupon, andcredit quality, as well as changes in interest rate andcredit spread movements within that stratification. Thereview also includes recent trades, including: volumetraded at various levels that establish a market; issuerspecific fundamentals; and industry specific economicnews as it comes to light.

For our municipal securities (e.g., general obligations,revenue, and housing), we stratify the portfolio toevaluate securities by type, coupon, credit quality, andduration to review price changes relative to creditspread and interest rate changes. Additionally, we lookto economic data as it relates to geographic location asan indication of price-to-call or maturity predictors. Formunicipal housing securities, we look to changes incash flow projections, both historical and reasonablyestimable projections, to understand yield changes andtheir effect on valuation.

Lastly, for our short-term securities, we look atacquisition price relative to the coupon or yield. Since

App.-A-20

our short-term securities are typically 90 days or less tomaturity, with the majority listed in Level 2 being 30days or less to redemption, we believe that acquisitionprice is the best estimate of fair value.

We also review data assumptions as supplied by oursources to determine if that data is relevant to currentmarket conditions. In addition, we independently revieweach sector for transaction volumes, new issuances,and changes in spreads, as well as the overallmovement of interest rates along the yield curve todetermine if sufficient activity and liquidity exists toprovide a credible source for our market valuations.

During each valuation period, we create internalestimations of portfolio valuation (performance returns),based on current market-related activity (i.e., interestrate and credit spread movements and other credit-related factors) within each major sector of our portfolio.We compare our internally generated portfolio resultswith those generated based on quotes we receiveexternally and research material valuation differences.We compare our results to index returns for each majorsector adjusting for duration and credit qualitydifferences to better understand our portfolio’s results.Additionally, we review on a monthly basis our externalsales transactions and compare the actual final marketsales prices to previous market valuation prices. Thisreview provides us further validation that our pricingsources are providing market level prices, since we areable to explain significant price changes (i.e., greaterthan 2%) as known events occur in the marketplace andaffect a particular security’s price at sale.

This analysis provides us with additional comfortregarding the source’s process, the quality of its review,and its willingness to improve its analysis based onfeedback from clients. We believe this effort helpsensure that we are reporting the most representativefair values for our securities.

Except as described below, our Level 3 securities arealso priced externally; however, due to several factors(e.g., nature of the securities, level of activity, and lackof similar securities trading to obtain observable marketlevel inputs), these valuations are more subjective innature. Certain private equity investments included inthe Level 3 category are valued using external pricingsupplemented by internal review and analysis.

After all the valuations are received and our review iscomplete, if the inputs used by vendors are determined tonot contain sufficient observable market information, wewill reclassify the affected security valuations to Level 3. AtDecember 31, 2020 and 2019, we did not have anysecurities in our fixed-maturity portfolio listed as Level 3.

At December 31, 2020, we owned four privatenonredeemable preferred securities that were pricedinternally or by a pricing firm, and we held three privatenonredeemable preferred securities at December 31,2019. At December 31, 2020, we held two Level 3 otherrisk investments that were priced using the costmethod, compared to one Level 3 other risk investmentat December 31, 2019.

To the extent we receive prices from external sourcesfor the Level 3 securities, we would review those pricesfor reasonableness using internally developedassumptions and then compare our derived prices tothe prices we received. During 2020 or 2019, there wereno material assets or liabilities measured at fair value ona nonrecurring basis.

Based on our review, all prices received from externalsources remained unadjusted. Due to the relative sizeof the Level 3 securities’ fair values compared to thetotal portfolio’s fair value, any changes in pricingmethodology would not have a significant change invaluation that would materially impact net orcomprehensive income.

The following tables provide a summary of changes in fair value associated with Level 3 assets for the years endedDecember 31, 2020 and 2019:

Level 3 Fair Value

(millions)

Fair Valueat Dec. 31,

2019

Calls/Maturities/Paydowns Purchases Sales

Net Realized(Gain)/Loss

on SalesChange inValuation

NetTransfers

In (Out)

Fair Valueat Dec. 31,

2020

Equity securities:

Nonredeemable preferredstocks:

Financials $ 27.1 $ (27.1) $ 35.0 $ 0 $ 0 $ 0 $ 0 $ 35.0

Industrials 16.0 0 0 0 0 0.7 0 16.7

Common equities:

Other riskinvestments 0.3 0 2.8 0 0 0 0 3.1

Total Level 3securities $ 43.4 $ (27.1) $ 37.8 $ 0 $ 0 $ 0.7 $ 0 $ 54.8

App.-A-21

Level 3 Fair Value

(millions)

Fair Valueat Dec. 31,

2018

Calls/Maturities/Paydowns Purchases Sales

Net Realized(Gain)/Loss

on SalesChange inValuation

NetTransfers

In (Out)

Fair Valueat Dec. 31,

2019

Equity securities:

Nonredeemable preferredstocks:

Financials $ 25.1 $ 0 $ 2.0 $ 0 $ 0 $ 0 $ 0 $ 27.1

Industrials 5.0 0 10.0 0 0 1.0 0 16.0

Common equities:

Other riskinvestments 0.3 0 0 0 0 0 0 0.3

Total Level 3securities $ 30.4 $ 0 $ 12.0 $ 0 $ 0 $ 1.0 $ 0 $ 43.4

The following tables provide a summary of the quantitative information about Level 3 fair value measurements for ourapplicable securities at December 31:

Quantitative Information about Level 3 Fair Value Measurements

($ in millions)Fair Value at

Dec. 31, 2020 Valuation Technique Unobservable Input

UnobservableInput

Assumption

Equity securities:

Nonredeemable preferred stocks:

Financials1 $ 25.0 Internal priceUnadjusted purchase price

per share 3.7

Financials2 10.0 Internal priceUnadjusted purchase price

per share 16.9

Industrials 6.9 Pricing firm

Market Approach(Guideline Public Company

Method) 5.4

Industrials 9.8 Pricing firm

Market Approach(Guideline Public Company

Method) 4.8

Subtotal Level 3 securities 51.7

Pricing exemption securities 3.1

Total Level 3 securities $ 54.8

1This security was purchased in May 2020.2This security was purchased in November 2020.

Quantitative Information about Level 3 Fair Value Measurements

($ in millions)Fair Value at

Dec. 31, 2019 Valuation Technique Unobservable Input

UnobservableInput

Assumption

Equity securities:

Nonredeemable preferred stocks:

Financials $ 27.1 Pricing firmRecent transaction price per

share 9.0

Industrials 6.0 Pricing firm

Performance-basedtransaction price adjustment

per share 4.8

Industrials1 10.0 Internal priceUnadjusted purchase price

per share 4.9

Subtotal Level 3 securities 43.1

Pricing exemption securities 0.3

Total Level 3 securities $ 43.4

1The security was purchased in November 2019.

App.-A-22

4. DEBT

Debt at December 31, consisted of:

2020 2019

(millions)Carrying

ValueFair

ValueCarrying

ValueFair

Value

3.75% Senior Notes due 2021 (issued: $500.0, August 2011) $ 499.8 $ 510.9 $ 499.4 $ 515.6

2.45% Senior Notes due 2027 (issued: $500.0, August 2016) 497.3 541.1 496.9 501.5

6 5/8% Senior Notes due 2029 (issued: $300.0, March 1999) 296.9 409.4 296.6 392.5

4.00% Senior Notes due 2029 (issued: $550.0, October 2018) 545.5 660.4 545.0 614.3

3.20% Senior Notes due 2030 (issued: $500.0, March 2020) 496.1 575.5 0 0

6.25% Senior Notes due 2032 (issued: $400.0, November 2002) 396.0 582.0 395.7 552.6

4.35% Senior Notes due 2044 (issued: $350.0, April 2014) 346.7 459.7 346.7 417.0

3.70% Senior Notes due 2045 (issued: $400.0, January 2015) 395.5 481.0 395.4 434.2

4.125% Senior Notes due 2047 (issued: $850.0, April 2017) 841.7 1,113.1 841.6 986.1

4.20% Senior Notes due 2048 (issued: $600.0, March 2018) 590.0 806.7 589.8 705.8

3.95% Senior Notes due 2050 (issued: $500.0, March 2020) 490.6 653.7 0 0

Total $5,396.1 $ 6,793.5 $4,407.1 $5,119.6

All of the outstanding debt was issued by TheProgressive Corporation and includes amounts thatwere borrowed and contributed to the capital of itsinsurance subsidiaries or used, or made available foruse, for other business purposes. Fair values for thesedebt instruments are obtained from external sources.There are no restrictive financial covenants or creditrating triggers on the outstanding debt.

Interest on all debt is payable semiannually at the statedrates. All principal is due at the stated maturity. Each noteis redeemable, in whole or in part, at any time; however,the redemption price will equal the greater of the principalamount of the note or a “make whole” amount calculatedby reference to the present values of remaining scheduledprincipal and interest payments under the note.

We issued $500 million of 3.20% Senior Notes due 2030and $500 million of 3.95% Senior Notes due 2050 inMarch 2020, in an underwritten public offering. The netproceeds from these issuances, after deductingunderwriters’ discounts, commissions, and other issuancecosts, were approximately $986.3 million in aggregate.

Aggregate required principal payments on debtoutstanding at December 31, 2020, were as follows:

(millions)Year Payments

2021 $ 500

2022 0

2023 0

2024 0

2025 0

Thereafter 4,950

Total $ 5,450

Prior to certain issuances of our debt securities, weentered into forecasted transactions to hedge againstpossible rises in interest rates. When the contracts wereclosed upon the issuance of the applicable debtsecurities, we recognized the unrealized gains (losses)on these contracts as part of accumulated othercomprehensive income (see Note 1 – Reporting andAccounting Policies for further discussion). Theseunrealized gains (losses) are being amortized as

App.-A-23

adjustments to interest expense over the life of therelated notes. The following table shows the originalgain (loss) recognized at debt issuance and theunamortized balance at December 31, 2020, on apretax basis:

(millions)

UnrealizedGain (Loss)

at Debt Issuance

UnamortizedBalance at

December 31, 2020

3.75% Senior Notes $ (5.1) $ (0.4)

6 5/8% SeniorNotes (4.2) (2.2)

6.25% Senior Notes 5.1 3.2

4.35% Senior Notes (1.6) (1.4)

3.70% Senior Notes (12.9) (11.4)

4.125% SeniorNotes (8.0) (7.5)

We reclassified $1.1 million in 2020, and $1.0 million in2019 and 2018, of net unrealized losses fromaccumulated other comprehensive income to interestexpense on our closed debt issuance cash flow hedges.

During 2020, we renewed the line of credit with PNCBank, National Association (PNC), in the maximumprincipal amount of $250 million. Subject to the termsand conditions of the line of credit documents, advancesunder the line of credit (if any) will bear interest at avariable rate equal to the higher of PNC’s Prime Rate orthe sum of the Federal Funds Open Rate plus 175 basispoints. Each advance must be repaid on the 30th dayafter the advance or, if earlier, on April 30, 2021, theexpiration date of the line of credit. Prepayments arepermitted without penalty. The line of credit isuncommitted and, as such, all advances are subject toPNC’s discretion. We had no borrowings under eitherline of credit in 2020 or 2019.

5. INCOME TAXES

The components of our income tax provision for the years ended December 31, were as follows:

(millions) 2020 2019 2018

Current tax provision

Federal $ 1,395.7 $ 1,133.2 $ 673.1

State 35.6 27.3 21.5

Deferred tax expense (benefit)

Federal 35.8 16.8 (145.9)

State 1.5 3.0 (6.1)

Total income tax provision $ 1,468.6 $ 1,180.3 $ 542.6

The provision for income taxes in the accompanying consolidated statements of comprehensive income differed fromthe statutory rate for the years ended December 31, as follows:

(millions) 2020 2019 2018

Income before income taxes $7,173.2 $5,160.3 $3,163.6

Tax at statutory federal rate $1,506.4 21% $1,083.7 21% $ 664.4 21%

Tax effect of:

Reversal of prior year tax credits 0 0 163.2 3 0 0

Tax credits1 (5.4) 0 (43.9) (1) (76.3) (2)

Stock-based compensation (22.7) (1) (25.9) (1) (25.1) (1)

Tax-deductible dividends (25.1) (1) (14.6) 0 (14.6) 0

Tax-preferenced investment income (15.2) 0 (14.0) 0 (15.6) (1)

Nondeductible compensation expense 6.4 0 8.1 0 (0.2) 0

State income taxes, net of federal taxes 29.3 1 24.0 1 12.2 0

Other items, net (5.1) 0 (0.3) 0 (2.2) 0

Total income tax provision $1,468.6 20% $1,180.3 23% $ 542.6 17%