Embed Size (px)

DESCRIPTION

Central and Eastern European countries (CEE) had emerged as new players on theworld market, opening its economies to international trade, FDI and internationalisation ofproducts. This paper (i) refers to classical Vernon theory of Product Cycle (PCT), thenanalyses its evolution and following tests by other authors and by Vernon himself, (ii) studiesPCT’s application on Chinese case, in particular on Central office switches industry’s successduring last few years; and CEE countries’ case (CEE is seen as new global location inelectronic industry), and (iii) makes an attempt to analyse Ukrainian economy’s case in termsof PCT, analyses which lessons Ukraine should learn on its way to internationalisation of itsproduction.

Citation preview

1

The Product Cycle Theory for Developing Countries.

Ukrainian case.

Olena Gurova, PhD Student

University of Rouen

Abstract: Central and Eastern European countries (CEE) had emerged as new players on the

world market, opening its economies to international trade, FDI and internationalisation of

products. This paper (i) refers to classical Vernon theory of Product Cycle (PCT), then

analyses its evolution and following tests by other authors and by Vernon himself, (ii) studies

PCT’s application on Chinese case, in particular on Central office switches industry’s success

during last few years; and CEE countries’ case (CEE is seen as new global location in

electronic industry), and (iii) makes an attempt to analyse Ukrainian economy’s case in terms

of PCT, analyses which lessons Ukraine should learn on its way to internationalisation of its

production.

Key words: International Trade, Product Cycle Theory, FDI, MNCs, Vernon,

Technological Gap, CEE.

Introduction Central and Eastern Europe (CEE) has just recently opened its economies to

international trade after the decline of Soviet Era. That means not only liberalization of trade

itself and opening its market for international producers, but also its own production’s

internationalisation. We insist here that market integration is necessary but not sufficient

condition for benefiting from global integration. It is often assumed that industrial integration

would automatically follow the market integration. However, most often this is far from being

a case and the failure of Washington consensus in CEE and CIS countries proved it recently.

Countries could be integrated through markets but not necessarily through production and

technology networks. World economy is much more integrated through finance and trade than

through production and much less through technology. Similar levels of market integration do

not necessarily lead to similar levels of production and technology integration.

2

Thus, here is a question arise – what determines whether firms are able to brake into to

foreign markets? Which are the steps the company and the country should take to make its

product competitive at the international market? What determines the positive input of FDI?

To answer these questions, we propose to use Product Cycle Theory’s (PCT) approach

and to analyse which are the chances for developing countries or countries with transitional

economies for accomplishing the task of bringing new competitive product on foreign market

or at least, to move from the “developing countries” status to “follower” or “leader” in terms

of PCT.

In aim of answering these questions for CEE countries, we find it useful to study some

recent cases such as Chinese, where we already can observe some significant success of

accomplishing Product Cycle.

And, to move to more particular case, we take example of Ukraine, the country that

follows its CEE neighbours in its economical transition; and to try to answer some important

questions rising:

1) Which sectors of Ukrainian economy are developed enough to be export-intensive?

Which sectors of economy should and may Ukraine develop to become a serious

competitor on the international market?

2) Which foreign markets are open and which might be open in the future for Ukraine

as exporter?

3) Which conditions should Ukraine meet to participate in competition on the

international market? What are the obstacles at the moment for FDI hosting and

developing pro-export production?

4) Could PCT be useful for programming the development economies in transition and

in particular Ukrainian?

I - Theoretical approach 1. Classic Theory of Product Cycle by Vernon

The Product Cycle Theory is generalization and extension of the technological gap

model, sketched by M.P. POSNER in 1961, a great deal of the trade among industrialized

countries is based on the introduction of new products and new production process.

3

These give the innovating firm and nation a temporary monopoly in the world market.

Such a temporary monopoly is often based on patens and copyrights, which are granted to

stimulate the flow of inventions.

As the most technologically advanced countries, US exports a large number of new

high-technology products. However, as foreign producers acquire the new technology, they

eventually are able to conquer markets abroad, and even US market for the product, because

of their lower labour cost.

In the mean time, American producers may have introduced still newer product and

the productions processes and may be able to export these products based on the new

technological gap established. A shortcoming of this model, however, is that it does not

explain the size of the technological gaps and doesn’t explore the reason that technological

gaps arise or exactly how they are eliminated over time.

The Product Cycle Theory says that FDI starts to work only when traditional export of

goods doesn’t bring enough of profit any more to the company and as a solution the company

chooses the organizing of production abroad.

The PCT is concerned with the life-cycle of a typical « new product » and its impact

on international trade. R. VERNON (1966) developed his theory in response to the failure of

the United States – the main country to do so – to conform empirically to the Heckscher-

Ohlin Model.

R. VERNON emphasizes manufactured goods, and the theory begins with the

developing a new product in the USA. The new product had two principal characteristics:

1) it caters to high-income demands because the US is a high-income country

2) it promises, in its production process, to be labour-saving and capital-using in

nature.

The reason for including the potential labour-saving nature of the production process

is that the US is widely regarded as a labour-scarce country. Thus, technological change will

emphasize production processes with the potential to conserve this scarce factor of

production.

The theory of R. VERNON divides the life cycle of this new product into three stages

(Figure. 1):

1) The new product stage (innovation stage, production inside the country) –

the product is produced and consumed only inside the country (USA by

Vernon).

4

2) Maturing product stage (export of product) – some general standards for the

product and its characteristics begin to emerge, and mass production

techniques start to be adopted.

At this stage the prices competition is increasing and the costs of products plays

more and more important role. But the company continues the export of the product and

avoids direct investments as long as production costs and transportation costs of this

product are lower than the cost of production abroad. If this proportion changes and

production abroad (investments) becomes more efficient, the company shifts production

of this product to the country with the similar structure of demand and lower level of

salary (as example – for USA in 1960s it was Western Europe).

3) Standardized product stage (technology’s export and product’s import)

– by this time in the product’s life cycle, the characteristics of the

product itself and the production process are well known; the product is

familiar to consumers and the production process to producers.

5

Figure 1. Trade pattern for innovating country.

Vernon hypothesizes that production may shift to the developing countries. Labour

cost again plays an important role, and the developed countries are busy introducing other

products.

Figure 2. PCT in application on 3 types of countries.

Expo

rts (X

) “Leaders” countries

Intermediate countries (“followers”)

Developing countries

Time

I II III IV

Impo

rts (M

)

Innovating country’s consumption

Innovating country’s production

imports Exports

Production Consumption of product

t0 New product stage t1 Maturing product t2 Standardized product stage Time stage

6

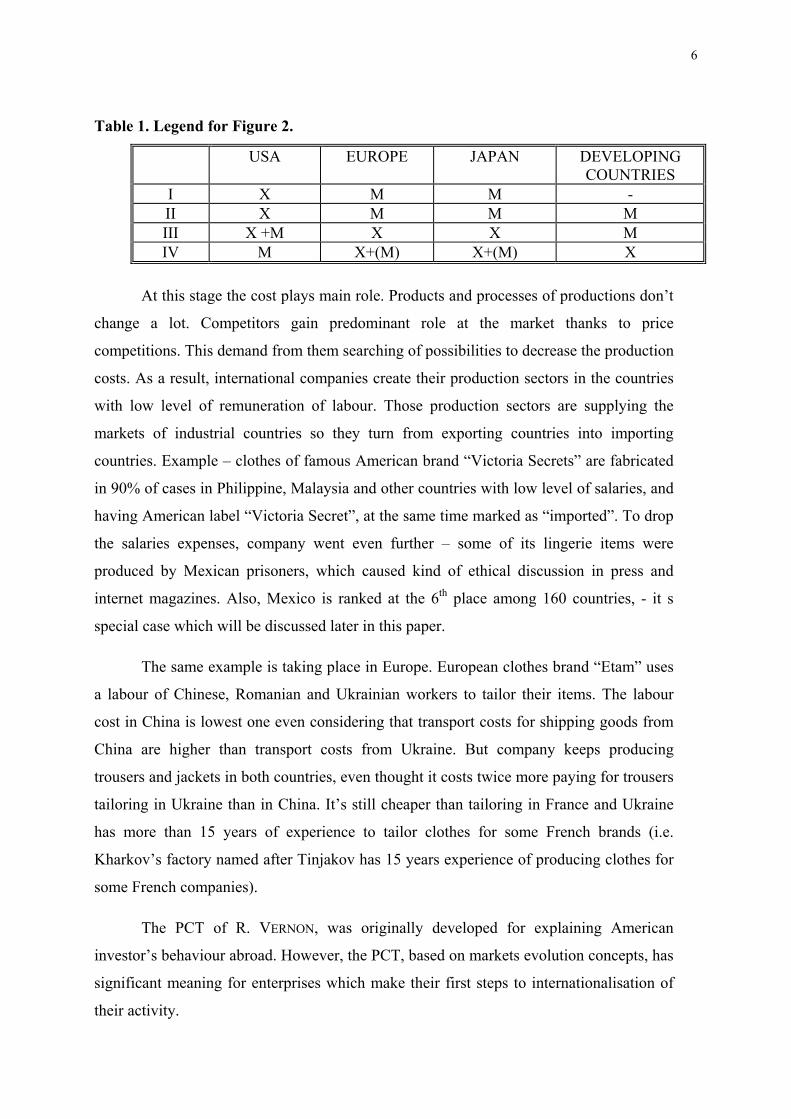

Table 1. Legend for Figure 2.

USA

EUROPE JAPAN DEVELOPING COUNTRIES

I X M M - II X M M M III X +M X X M IV M X+(M) X+(M) X

At this stage the cost plays main role. Products and processes of productions don’t

change a lot. Competitors gain predominant role at the market thanks to price

competitions. This demand from them searching of possibilities to decrease the production

costs. As a result, international companies create their production sectors in the countries

with low level of remuneration of labour. Those production sectors are supplying the

markets of industrial countries so they turn from exporting countries into importing

countries. Example – clothes of famous American brand “Victoria Secrets” are fabricated

in 90% of cases in Philippine, Malaysia and other countries with low level of salaries, and

having American label “Victoria Secret”, at the same time marked as “imported”. To drop

the salaries expenses, company went even further – some of its lingerie items were

produced by Mexican prisoners, which caused kind of ethical discussion in press and

internet magazines. Also, Mexico is ranked at the 6th place among 160 countries, - it s

special case which will be discussed later in this paper.

The same example is taking place in Europe. European clothes brand “Etam” uses

a labour of Chinese, Romanian and Ukrainian workers to tailor their items. The labour

cost in China is lowest one even considering that transport costs for shipping goods from

China are higher than transport costs from Ukraine. But company keeps producing

trousers and jackets in both countries, even thought it costs twice more paying for trousers

tailoring in Ukraine than in China. It’s still cheaper than tailoring in France and Ukraine

has more than 15 years of experience to tailor clothes for some French brands (i.e.

Kharkov’s factory named after Tinjakov has 15 years experience of producing clothes for

some French companies).

The PCT of R. VERNON, was originally developed for explaining American

investor’s behaviour abroad. However, the PCT, based on markets evolution concepts, has

significant meaning for enterprises which make their first steps to internationalisation of

their activity.

7

What is the evidence on the PCT? The product cycle hypothesis suggests two

orderings:

1) more advanced countries are able to begin exporting earlier than developing

countries;

2) less advanced products are developed and exported earlier.

In general, advanced countries are expected to begin exporting more advanced

products earlier than less advanced countries.

However this model can’t describe sufficiently the process of division of markets

by international companies in different countries, it doesn’t explain their specific

advantages.

2. Developing and testing Vernon’s Theory

There is no single all-encompassing test (such as W. LEONTIEF test of Heckscher-

Ohlin) to verify empirically the product cycle theory.

Instead, researches have examined particular features of the PCT to see if they are

consistent with real-world experience. For example, new product development is critical to

the PCT, and it is often the result of research and development (R&D) expeditures.

Therefore, economists hypothesize that, in the USA manufacturing sector, there

should be a positive correlation between R&D expeditures and successful export performance

by industry.

A number of tests indicated this result, including those by D. KEESING (1967) and W.

GRUBER, D. MEHTA, R. VERNON (1967).

I. KRAVIS and R. LIPSAY (1982) found that high R&D intensity was positively

associated with large shares of export by US multinational companies (MNCs).

Furthermore, over the last 25 years, greater shares of US MNCs’ exports have come

from overseas production, which is consistent with the direct-investment and export-

displacement features of the PCT.

In addition, in 1969, L. WELLS examined the income elasticity of demand of the

fastest-growing US exports and found – again, an occurrence consistent with the PCT. It was

Wells, who summarized the product life cycle in tabular form (see table 2).

8

Table 2. PCT by L. Wells (1969).

CYCLE PHASE Early Growth Mature

Demand Structure Low price elasticity for aggregate demand and for individual firm. Nature of demand not well understood by firm

Growing price elasticity for firm. Price competition begins.

Basis of competition is price or product differentiation through marketing techniques.

Production Short runs, rapidly changing techniques dependent on skilled labor. Low capital intensity.

Mass production methods.

Long runs with stable techniques. Labor skills unimportant. Capital intensive.

Industry Structure Small number of firms.

Large number of firms, but many casualties and mergers.

Number of firms declining.

Source: Louis T. Wells, Jr., “The Product Life Cycle Approach”. Among the many other empirical works is G. HUFBAUER’s (1966) study on trade in

synthetic materials. Hufbauer found that the US and other developed countries tended to

export new products while developing countries tended to export older products.

W. GRUBER, D. MEHTA, and R. VERNON (1967) also discovered that research-

intensive US industries have a high propensity to invest abroad.

This is consistent with the maturing product stage of theory.

In 1979 R. VERNON modified his original PCT with respect to the role of

multinationals. Because of the changes that occurred in production conditions in the USA –

mostly because of the convergence of labour costs with other technological leaders such as

Japan, but also the convergence of the level income – it seems likely that the actual

production of new products could take place somewhere else other that in the country in

which the research laboratory is.

For example, while R&D activities will take place in the MNC’s headquarters, usually

in one of the more highly DC’s, the initial production could easily tale place in one of the

MNC’s subsidiary companies located in a developing country. However, this modification

does not bring the product-cycle and the HO trade models any closer together.

In 1972, J. MORRALL found that US industries that were successful exporters also

tended to have relatively high expenditures on non-payroll costs such as advertising, sales

promotions, and so forth.

9

Taking into account all the difficulties in measuring technological advantage, the

empirical evidence is as favorable toward the product-cycle theory as it could be. A number

of studies have incorporated some type of technology-related variables as determinants of the

pattern of trade. A comprehensive survey of the many avenues taken in empirical testing is

presented by A. DEARDORFF (1984). He stresses that all the variables used to explain trade in

these technology-based models are related to two things:

1) the “newness” of the products or process

2) the special knowledge possessed by individuals, firms, and countries that enables

them to develop and exploit available technologies.

This leads A. DEARDORFF to conclude that it is difficult to distinguish the evidence

supporting technology from the evidence supporting human capital and skills as determinants

of trade.

R. FEENSTRA and A. ROSE (2000) use intuitions of Vernon’s Theory to produce a

ranking of products and a ranking of country sophistications. The product and country

ranking are based on the product cycle notion that all goods are not exported by most

countries and that countries tend to export goods to the United States in a sequential order.

First, the ranking of unobserved product sophistication is constructed according to the first

year of exportation. A product is deemed less advanced if it begins to be exported earlier

to the United States. Second, the ranking of country sophistication is constructed

according to the first year in which a country exported each commodity to the United

States.

Empirical analysis shows that countries ranked as more advanced, in the sense that

they tend to export sooner to the United States, tend to grow faster and to display higher

levels of economic activity and of total factor productivity than countries ranked as less

advanced.

The top more sophisticated countries, according to a ranking based on the exports

of manufacturing goods, are Japan, Germany, Canada, the United Kingdom, France, Italy,

Switzerland, the Netherlands, and Mexico. Notice, that the ranking is affected by trade

relations with the United States, which explains why Mexico is number nine among 160

countries as we stated before.

One of the most important questions rising for our further analysis is what

determines whether firms are able to break into foreign markets?

10

A. BERNARD and J. JENSEN (2001) undertake a dynamic econometric analysis

benefiting from the availability of data at the plant level. The study uses a panel of 13 550

US manufacturing plants that operated continuously during the export growth period

1984-92. the plants in the sample were a small percentage of the almost 200 000 plants

surveyed in the Census of Manufactures in 1987 but accounted for 41 percent of total

manufacturing employment and 70 percent of total manufacturing exports in that year.

About 48 percent of the plants in the sample exported in 1984 and 54 percent in 1992.

The econometric analysis tests for the effects of entry costs, exchange rates, plant

characteristics, state export promotion, and other factors, on the probability of exporting.

Entry costs discourage exporting, a finding that is also reported by M. ROBERTS

and J. TYBOUT (1997) for Colombia. Favourable exchange rate shocks and plants

characteristics indicative of past successes are found to significantly increase the

probability of exporting. Export promotion by the states is found to have positive but

statistically insignificant effects on exporting probabilities.

However, the authors indicate that the evidence is subject to the caveat that the

study focuses on the sample of large firms but state export promotion – which mounted to

USD 96 million in 1992 – often targets small and medium enterprises.

II - Application of PCT

1. China’s case

Before we start to analyse the possibility of PCT application on Ukrainian case, we

find it very useful to make some research about other economically developing countries who

have already achieved some significant success in technological gap cut. Which lessons we

can learn from China? What might be useful as patterns for Ukraine in its aspiration for

world’s market?

The research of Z. THAN (2001) is analysing application of PCT on Chinese case, in

particular for Telecom Manufacturing Industry as a case.

China has recently emerged as a significant player in the global telecommunication

industry, in late 1980s. The wireless phone network in Chine has experienced an even higher

growth rate than telephone lines. China’s mobile telephone users reached 120,6 million

persons in 2001, which made Chine the largest mobile communication market in the world,

surpassing the 120,1 million users in the US. A late starter on Internet, China is trying to catch

11

up, with 200-300% annual growth rate. Its enormous market size has attracted almost all the

significant manufactures in the world to engage in various trade and production activities

(AT&T, Motorola, CISCO, Nortel, Ericsson, Nokia, Alcatel, Siemens, NEC, Fujitsu,

Samsung etc.). Direct imports from post-industrial countries continue to support most of

China high-end market. Local subsidiaries and joint ventures of multinational telecom

manufactures have grown to supply a large percentage of the medium-end of Chinese market.

Government policy of China. China has recognized that involving MNCs is a part of

the solution to national economic and social development (UNITCAD, 1999). But China

apparently also realized that “Development of the host countries is a fortuitous side effect at

best, which will only come about if the host government maintains enough autonomy and

control to guarantee that the benefits of foreign direct investments are shared between

providers and recipients of foreign capital” (STALLINGS, 1990). Regulations and policy have

been actively formulated to promote the production localization of MNCs’ subsidiaries and

joint ventures and to nurture indigenous manufacturers in China’s telecom industry. Chinese

government issues and updated regularly “Government Guidelines for Foreign Investment in

Telecommunications”, dividing foreign entries into three categories: encouraged, restricted,

and prohibited.

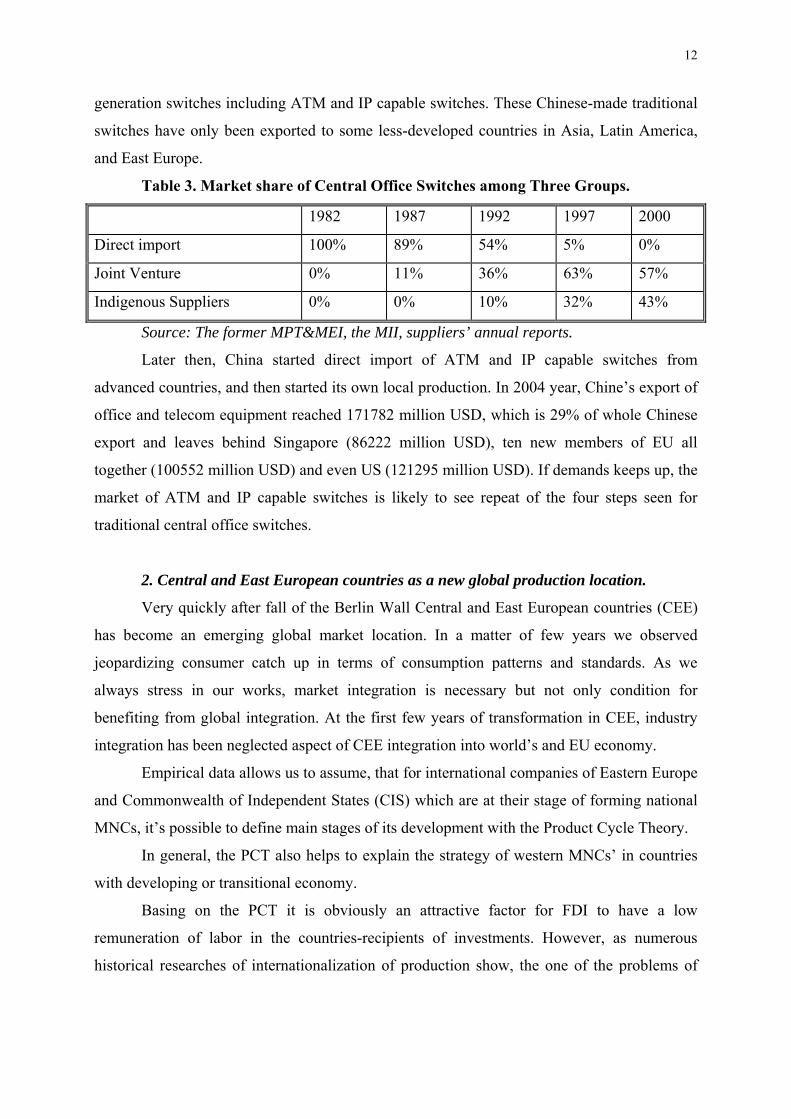

Central office Switches is a good example of PCT application on China’s case.

Traditional Central Office Switch market is an instance where competition among many

MNCs’ is fierce, technology is mature, demand is strong (more than 10 million lines

annually) and China’s government industrial policy can be effectively implemented.

The technology of traditional central office switches is based on the principle of stored

programming control, which originated in the 1960s and became mature in the late 1980s and

1990s. These switches have been deployed on a large-scale in Western countries since 1970s.

Scale of economy limits the production of central office switches to a few large corporations.

In China, switches were mostly purchased by single monopoly buyer, then China Telecom. A

single monopoly buyer leads to a better organized decision-making process, which makes it

more effective for China to implement its industrial policy through procurement and joint

venture negotiation. These market features have determined an evolution with four distinct

stages for central office switches in China (see table 3).

This development is very close to a typical PC except for the last step. Theoretically,

China should start to export these lower cost switches back to Western countries since the

production is localized to a large extent. However, technologically advances have eliminated

the export opportunities because Western markets have moved to more advanced next

12

generation switches including ATM and IP capable switches. These Chinese-made traditional

switches have only been exported to some less-developed countries in Asia, Latin America,

and East Europe.

Table 3. Market share of Central Office Switches among Three Groups.

1982 1987 1992 1997 2000

Direct import 100% 89% 54% 5% 0%

Joint Venture 0% 11% 36% 63% 57%

Indigenous Suppliers 0% 0% 10% 32% 43%

Source: The former MPT&MEI, the MII, suppliers’ annual reports.

Later then, China started direct import of ATM and IP capable switches from

advanced countries, and then started its own local production. In 2004 year, Chine’s export of

office and telecom equipment reached 171782 million USD, which is 29% of whole Chinese

export and leaves behind Singapore (86222 million USD), ten new members of EU all

together (100552 million USD) and even US (121295 million USD). If demands keeps up, the

market of ATM and IP capable switches is likely to see repeat of the four steps seen for

traditional central office switches.

2. Central and East European countries as a new global production location.

Very quickly after fall of the Berlin Wall Central and East European countries (CEE)

has become an emerging global market location. In a matter of few years we observed

jeopardizing consumer catch up in terms of consumption patterns and standards. As we

always stress in our works, market integration is necessary but not only condition for

benefiting from global integration. At the first few years of transformation in CEE, industry

integration has been neglected aspect of CEE integration into world’s and EU economy.

Empirical data allows us to assume, that for international companies of Eastern Europe

and Commonwealth of Independent States (CIS) which are at their stage of forming national

MNCs, it’s possible to define main stages of its development with the Product Cycle Theory.

In general, the PCT also helps to explain the strategy of western MNCs’ in countries

with developing or transitional economy.

Basing on the PCT it is obviously an attractive factor for FDI to have a low

remuneration of labor in the countries-recipients of investments. However, as numerous

historical researches of internationalization of production show, the one of the problems of

13

using a “cheap” labor by international companies is inevitability of constantly growing level

of salaries. L. KLIMOVICH (1999) sees two reasons why it may happen:

1) self-appraisal of East-European workers which is slightly raised too high because

of their traditionally high social guarantees ;

2) inflation expectations.

Dominating factor in resource's sector is a search for cheapest resources. The bench-

mark of this search is investments in other countries, which will help to form trade flows. To

get access to the resources in foreign country, the company invests there (FDI) and starts to

export this resources from this particular country, which is acceptor of FDI.

Hence, the bench-mark of this process is FDI and international trade flows are its

derivative.

Service's sector. Mechanism of PCT in service’s sector is a bit different. In this sector,

it is necessary to establish company’s subsidiaries in all the beginning. They will demonstrate

the services offered by the company to the clients. The necessity of such presence at the

foreign markets caused some fundamental shifts in the structure of FDI in favour of service

sector.

But there are some serious shifts going on in the service sectors itself too – due to

telecommunication’s sector’s development. The speed of information’s transmission has

increased remarkably during last years. As a result of this process, the demand for FDI in this

sector decreases. At the same time, new opportunities for international business in service

industry arrive – such as information processing, accounting etc.

In other words, we are talking about the activities which were accomplished by each

company themselves; and now are accomplishing by special companies working on

transnational base. In this way company minimize its stuff of accountants and other high-paid

specialists, so it minimize the salary’s payments.

We find not so many examples of such shifting at the Eastern European countries

nowadays. It is probably because there is no necessary level of development of technical base

and specially trained personnel. But we should not exclude the possibility of creation the

international companies’ subsidiaries using the local specialists in the nearest future.

CEEC's electronic industry as a case. Socialist economies of CEE were uncompetitive

in computer production, relying on foreign technology for design and components. Obviously,

their contribution to technology development in electronics was relatively strong only until

the mid-1970s, and dependence later then on foreign technology meant that, in fact, in the

early 1990s, CEECs were still using 1970s electronic technology. It was determined also by

14

poor supply of components and COMECON restrictions. Production was undertaken by

several large electronics companies, which by mid-1990s all but one (Hungarian Videoton)

have been either broken up or slowly deteriorating. The only domestically controlled

successful part of electronics during the 1990s was local PC assembly, especially in Poland.

After the mid-1990s, some of CEECs, like Hungary, the Czech Republic and Poland,

gradually became accepted into the supply base of large electronic companies. The dynamic

of electronics export shown in the table 4.

Table 4. Electronics export of the CEECs, millions current USD 1996 1997 1998 1999 2000 2001 Average

annual rate,%

Hungary 932 3329 4737 6093 7802 7729 42.3 Czech 989 1176 1633 1572 2224 3340 22.5 Poland 612 849 1142 1140 1290 1607 17.5 Russia 784 965 746 929 947 1138 6.4 Romania 36 31 58 176 510 497 54.9 Slovakia 161 246 309 363 382 433 17.9 Slovenia 298 284 276 228 330 350 2.7 Ukraine 57 77 85 94 220 251 28.0 Croatia 123 160 164 124 152 204 8.8 Total 3992 7117 9150 10719 13857 155549 25.4 Source: Reed Electronics Research, The Yearbook of World Electronic Data. 2001/2, 1999/2000 and 2003/4, volume 4, East Europe and World Summary.

In 2003, total electronics production reached 30 milliards USD, which is little above

the production of Mexico (28,5 milliards USD), the bulk of this growth was achieved in the

1997-2000 period. However, this level is still low compared to East Asian economies and

China. For example, Taiwanese electronics production is 5 times larger that Hungarian.

In summary, among emerging markets CEE electronics has become an important

second tier global location i. e. after East Asia with leader producer Hungary, which

electronic production raised from 1,7 milliards USD (1996) to 8,5 milliards USD (2003) –

leaving behind Spain with 6,5 milliards USD (2003).

III. Ukrainian case 1. Economy of Ukraine after collapse of USSR

Ukraine is an Easter European country with a considerable economic potential.

Ukraine produces 5% world’s mineral raw materials and products of its processing. Explored

sources of fossils in Ukraine cost approximately 7 trillions USD. Share of Ukraine in world’s

production of manganese ore is 32%, production of cast iron – 52 million tons, in production

15

of steel – 54 million tons (Ukraine remains on of the largest steel and iron producers in the

world, see appendix 1), production of rolled metal 41,5 million tons. Ukraine holds fifth

place in the world by these indexes.

Detailed analysis of economics potential of Ukraine is done in our previous work (G.

DUTHIL, O. GUROVA, 2005). Here we would mention only some most important points in aim

for possible application of PCT on Ukrainian case.

We should stress that at the moment of USSR’s collapse Ukraine was considered by

specialists of Deutsche Bank as one of the most developed its republics with the best

integration indexes (see appendix 2). In general there were three groups of the country

specified in this work:

1) High level of economic development (Ukraine, Baltic countries, Russia, Georgia)

2) Medium level of economic development (Byelorussia, Kazakhstan, Moldova,

Armenia, Azerbaijan)

3) Low level of economic development (Uzbekistan, Turkmenistan, Kyrgyz,

Tadjikistan).

Ukraine also is a country which has legged in the transition stakes (see EBRD, 1997;

World Bank, 1996).

From the moment of its independence Ukraine started to host foreign investments. By

some optimistic expectations, from the moment of USSR’s collapse, Ukraine had good

chances to receive foreign investments, due to some positive factors: its large market with (at

that moment) 51-million population; high level of education of local working population; low

level of salaries; presence of raw materials’ sources; presence of scientific and technical

creations of world’s level; high qualification of workers; relatively developed infrastructure;

good geographical position. However, these estimations didn’t come true, and investment

activity seriously slowed down during 1990-1996 years (investment decreased for 78.5% and

the share of investments in GDP decreased from 22.7% to 13%).

Then, during 2000-2004 years the situation with FDI improved (see Appendix 2). For

last year investments (gross fixed) remained at the level of 20.9% of GDP, which is half less

than the same index in China in the same period of time, although a bit higher than in

Macedonia (with 18,3%) and even Poland (18.2%).

2. International trade evolution

16

Since its independence and fall of certain export restrictions, Ukraine achieved certain

progress in its international trade. The Balance of Ukrainian international trade is shown in

the table 4.

Table 4. Balance of Ukrainian International Trade during, 1996-2006 (million US

dollars)

Years External trade

turnover

Export Import Balance

1997 37516,6 18970,3 -18546,3 424

1998 32563,7 16457,2 -16106, 5 350,7

1999 32295 17058 -15237 1821

2000 37638 19522 -18116 1406

2001 41570 21068 -20502 566

2002 44845 23351 -21494 1857

2003 56618 28953 -27665 1288

2004 73590 39415 -34175 5240

2005 85336 38220 -37180 1040

2006* 95080 51748 -43332 8416

*- forecast by CASE Ukraine, [12]

Source: NBU, CASE Ukrainian Estimations.

It should be mentioned that in spite of very optimistic forecast of some economists

(CASE, 2004), influenced my Orange Revolution Inspiration, the exports level didn’t achieve

expected 45979 million USD in 2005 year, while import was a bit lower than expected 39357

million USD. It still left trade balance positive, but it is one of the worst balance data since

1998 for Ukraine. Instead of programmed 6622 million USD, Ukraine has achieved the

balance of 1040 million USD.

While the trade balance of Ukraine recently remained positive, its structure has had

some negative changes. The main index of export for Ukraine was always iron and steel and

its share in total volume of export constantly growing. Ukraine remains always among few

leading exporters of iron and steel and its share in world’s iron and steel export was 4.2%

which is 6th place among world’s leaders iron and steel exporters.

Table 5 Detailed trade balance of Ukraine by industries, 2000-2005.

INDEX VALUE, MILLION USD SHARE IN ECONOMY’S TOTAL MERCHANDISE EXPORT OR IMPORT, %

IF NOT MENTIONED

17

OTHERWISE 2000 2001 2002 2003 2004 2000 2004 or

nearest year

Imports of agricultural products 1092 n\a 1308 2467 2235 7.8 7.7

Import of fuels and mining

products

5997 6439 6652 7856 10160 43.0 395.0

Exports of manufactures 9,77 10,44 11,86 15.23 22.68 67.1 69.4

Imports of manufactures 5.74 7,01 8,21 11.61 15.19 52.4 15.19

Exports of automotive products 145 167 154 126 214 0.1 0,7

Imports of automotive products 446 617 921 1730 2144 3.2 7,4

Textile exports 127 n\a 158 205 225 0.9 0.7

Textile imports 450 493 516 643 741 3.2 2.6

Clothing exports 417 498 503 568 671 2.9 2,1

Clothing imports 60 82 94 128 124 0.4 0,4

WTO. Statistics: International trade statistic 2005, trade by sector.

At the moment, there are some important structural tendencies of Ukrainian export-

import worth mentioning:

- export of row materials predominant (about 70%), mainly consisting of

ferrous metallurgy’s products – 32%, chemical production – 12%, food

industry – 10%, machine-building – 10%.

- Import, oriented on “vitally important” production – petroleum, gas (52%),

products of machine-building (13%), close burning coal, medical supplies,

food products;

- Extreme irregular allocation of export potential of Ukraine, which means that

4 regions from 25 supply more than 50% of whole export (Dnepropetrovsk,

Donetsk, Lougansk, Odessa regions);

- High orientation of Ukrainian trade on republics of ex-USSR (up to 70% of

external trade turnover in some sectors) predominated during few first years

of independence;

- Domination of raw material intensive equipment in export of products of

machine-building.

One of the most significant changes in Ukrainian international trade is change of its

main trade partners or regional structure of trade.

18

If we look through statistics of few first years of independence, for example 1995year

(see appendix 2), we would notice that 59% of Ukrainian external trade was realized with

CIS countries and only 24% with European countries, which is logical. Ten years later, the

most important export partners for Ukraine are Russia 19.3%, Turkey 7%, Italy 6.1% (2005)

and the most important importers are Russia 33.9%, Germany 11.3%, Poland 6.7%, China

6.5%, and Turkmenistan 5.5% (2005).

3. PCT and chances for Ukraine. Classification of economical sectors

Considering internationalization of Ukrainian companies, it is probably possible (there

are no exact application of the model done yet), to apply the classic Vernon’s model. In this

case we can only hypothesize a second stage of the model – initiation of exporting of selected

goods.

In his later works, R. VERNON (1972) moves forward with his theory and makes very

important remarks about disposition of a country to develop a new product, which means to

become a “leader” in some fields. He says that in order for substantial industrial innovation to

take place in the country, a body of trained engineers and interested businessmen must exist.

But this is not enough. The new products that engineers and businessmen are likely to develop

are those which seem most wanted in the country, that is, those which seem to have the most

ready local market. But there are no two countries in which local market conditions are quite

alike.

In industrial field, to be sure, all countries welcome new products or processes that

will cut costs, Vernon underline (1972). But in the country where skilled labor is exceedingly

scarce and dear while capital is abundant and cheap, the innovations that will cut costs tend to

be labor saving and capital-using. And the countries where raw materials are scarce and dear

while labor is abundant and cheap, the innovations that will capture the imagination of

businessmen and engineers tend to be material-saving and labor saving.

Some authors (L. KLIMOVICH and others) suppose, taking into consideration positive

examples of China, Poland, Czech Republic, Hungary (as analyzed above), that it is possible

for the ex-USSR countries to gain a part of European market. Of course, for the moments it is

only assumption.

For example, Byelorussian metallurgical plant (BMP), after applying certain

innovations, started to produce high tech metal production and became a monopolist on

19

internal market and at the Russian market. Geographical expansion of the sales allowed this

company to occupy 14 % of world market of metal cord. It’s also contributed to effective

export policy of the enterprise. There are some joint ventures founded with partners of this

company. They are located in Western Europe. At the moment there is creation of joint

venture with US partners going on. Unfortunately, there are always some obstacles for

export’s growth in Byelorussia remaining which is beyond the scope of this paper to discuss.

According classification of Pavitt (1984) there are two main sectors of economy exist:

Traditional sectors: in developing countries and countries with transitional economy

this sector hosts up to 44% of FDI in particular in Poland and Ukraine. As an example it is

food production, mineral sources, raw material sectors in Ukraine which attract FDI at the

moment.

Innovation sectors: are not always popular among foreign investors. In whole Central

and Eastern Europe it is Hungary, Czech Republic and Poland who host 82% of all FDI in

innovation sectors.

As competitive high-technological (or innovative) sectors of Ukrainian economy we

have mentioned the aerospace technologies, and aircrafts production. Here might be the key to

the question of possible leading at the international markets for Ukraine. Let’s see the

situation in details in those branches of the economy.

As for aerospace technologies, according to E. KUZNETCOV (2005), vice-president of

National Aerospace Agency of Ukraine, Ukraine just finished to prepare the project of

agreement with EU considering the programme of global civil satellite system EGNOS

Galileo: “We just worked out the project of agreement between Ukraine and EU considering

integration of Ukraine into “Galileo” system. Ukraine will give its on-earth stations of

observation, which will treat telemetric data of European satellites”. The Global European

system of navigation will be expanding in 2007-2008 years. It’s planned to send to the orbit

up to 30 spacecrafts for telecommunication and Earth’s sounding. The total cost of the project

is over 3 milliards euros. “Thanks to Galileo System, the owners of vehicles may always have

the exact information about its location” – E. KUZNETCOV also stressed: “We would like also

to participate in development, production and launching of space technical equipment for

Galileo system, but we faced some refuse because European countries are interested in

promoting their equipment and services, they see Ukraine as serious competitor in this

sphere”. The main competitor for Ukraine in this sphere is France, but French carrier rocket

“Arian” has fewer contracts for space transporting services than Ukrainian carrier rockets

“Cyclone” and “Zenith”.

20

Agreement between Ukraine and EU should lead to their collaboration in civil satellite

navigation. Besides this, the agreement should become a base for following projects and

programmes considering participating of Ukraine in management of Galileo project and help

to approaching between Ukraine and European space agency (ESA).

Galileo is the first common programme of EU and ESA. This new navigation satellite

system is supposed to provide by 2008 year the same level of service as American system

Global Position System (GPS). It’s preview to product and launch to the orbit 38 satellites.

It’s supposed that participation in EGNOS Galileo would provide high-effectiveness

of international transporting corridors going through Ukraine, and will access to high-

frequency navigation information of very vary application, including national economy,

science, national security system etc.

Another product, giving an economic perspective to Ukraine is its aircrafts creation

and construction.

Well-known Ukrainian transporting aircraft AN-225 “Mria” keeps the record on

shipping of large dimension cargo and even mentioned in Guinness Record book (information

by press-service of АНТК named after Antonov with the reference to International Aerospace

Federation - FAI). Furthermore, Antonov’s company has another six international records

achieved at 16, 18, and 19 of June, 2004 by the plane AN-225 “Mrija” after establishing of

commercial flights Prague-Tashkent (transportation of big-volume goods). There are also

some speed records in two classes of turbo-reactive planes C1 and C1t (with the takeoff

weight more than 300 tons) on the approved by FAI routes Prague-Kiiv, Kiiv-Ulianovsk,

Tashkent-Kiiv. The plane AN-225 “Mrija” achieved the speed of 684,67; 662; 693,2 km per

hour. Thus, the plane AN-225 “Mrija” has 240 international records, as a plane which took off

with the maximal weight 640860 kilograms and which has maximum of records, AN-225

“Mrija” was included in Guiness Records book at November,9 2004.

Service's sector in Ukraine is one of developing at the moment.

Summing up, there are some sectors of Ukrainian economy which have certain

potential to become export-intensive. Unfortunately, hosting of FDI in Ukraine is still pretty

chaotic, innovative and service sectors have luck of investment while traditional sectors which

are better to protect, remaining the main destination of FDI.

What are the obstacles which delay the braking into international market for those

potentially successful products for Ukraine? Let’s see in the next part of the paper.

21

4. Obstacles for PCT application on Ukrainian case. Perspectives of further

industrial upgrading.

Considering all said above we can assume, that the country has no chances to

transform its economy into post-industrial only with trade liberalisation (complete fail of

Washington consensus is studied more detailed in our paper O. GUROVA “Globalization and

the process of transition in Eastern-European countries. The case of Ukraine”). It is

impossible, stresses PAKHOMOV Y., and other Ukrainian economists, without developing

science intensive technologies. But even considerably developed technologies can not

guarantee success on the world market without certification and respect of common world’s

standards. In process of developing this paper we arrived to conclusion, however, that there

are some important determinants for becoming a trade leader at the world market for

Ukrainian “strong” sectors of economics:

1) Developing of technological clusters

2) realization of common certification for perspective range of products

3) well-balanced governmental policy towards developing exports, hosting FDI,

developing high tech production (example of China is very useful).

Both, M. PORTER (1990) and S. SOKOLENKO (2003) consider that when we talk about

competitiveness of the country, we should talk about competitiveness of its clusters, not

simply particular firms and companies. The main idea of the cluster theory here is the ability

of the cluster to use whole the range of its internal sources on its maximum. M. PORTER,

within his theory of clusters, developed the system of determinants of counties’

competitiveness, which is called “Diamond Model”.

According to M. PORTER’s theory (1990), cluster is a group of geographically close,

interconnected companies (producers, suppliers etc.) and other establishments connected to

them (universities, authorities, infrastructure’s firms), acting in the same field and

supplementing each others. It means that traditional country advantages (land, location,

natural resources, labor, local population size) which are hardly influenced, should not

determine completely national economy’s opportunity, so, to influence country’s economy’s

development, there clusters’ strategy proposed.

M. PORTER says clusters can influence competition in three ways:

- they can increase the productivity of the companies in the cluster;

- they can drive innovation in the field;

- they can stimulate new business in the field.

22

Well-known examples of clusters are USA/Silicon Valley (computers),

Netherlands/Rotterdam (logistics), India/Bangalore (software outsourcing), USA/Hollywood

(movies), France/Paris (fashion).

St. SOKOLENKO (2003) proposes to use the example of France in cluster’s strategy. In

France, there are few important clusters exist at the moment:

1) healthcare cluster(Lyon, Rhone-Alps)

2) Aerospace technologies cluster (Bordeaux, Toulouse)

3) Transportation and navigation integrated system (Île de France)

4) Telecommunications’ systems’ security (Province, Alps, Cote d’Azûr)

5) Nanotechnologies and microelectronics systems (near Grenoble)

6) Biotechnologies cluster (Midi Tech Santé)

Ukrainian scientists already have some potential for leadership in fields as following:

aerospace technologies; science of materials; electrometallurgy; electric welding; mechanics

of interaction of solids with ionized medium and E-field radiation; mechanics of composition

and heterogeneous medium; methods of nano-processes control; radio-physics; functions’

theory; cryobiology and cryological medicine; neurophysiology; marine radio- and

hemoecology. From our point of view, there some of mentioned field of science may become

the basis for future economic clusters in Ukraine.

Detailed examination of M. PORTER’s theory and its application on Ukrainian case is

beyond the scope of this paper, but the aim of our next paper.

Second obstacle mentioned is certification issue. During Soviet time, Ukrainian

industry as well as industry of other 14 Soviet republics, worked under internal common

standards and certification system. That enabled USSR economy to have commonly

respected, high quality certification within the country and COMECON, but disabled to

export majority of them as well as services. This lead CEE and CIS countries to another

significant gap between them and their potential trade partners. Even thought some of

Ukrainian goods have higher quality than Chinese, for example, we can not offer them, at

European market, because of luck of ISO certificates and different standards. Obviously, there

are only one way to resolve this problem – to let Ukrainian goods get ISO certificates and to

enable Ukrainian producers to be equal players at the world market. This is also one of the

major obstacles for the trade liberalization idea: without world’s common certification,

23

Ukraine became just a good market for international companies, exporter of raw materials, but

not an equal trader.

Conclusion:

It is obvious that PCT developed originally only USA and other developed countries

might be applied for others, even developing economies (China as recent evidence).

It is too early to correlate Ukrainian trade and PCT.

Ukraine economy has range of fields where leading might be possible forced by its

scientific potential and/or its relatively cheap and abundant sources.

There are some valuable experience that Ukraine can learn from its CEE neighbours,

especially Poland and Hungary (in electronics production sector), and China with its

governmental control of FDI and production development.

However, there some serious obstacles as luck of certification, lack of support on

governmental level in such important issues as creation of common programme of export

development and FDI hosting, battling corruption (as an important obstacle to FDI hosting)

etc.

In our opinion, Porter’s “Diamond Model” and clusters’ creation might be a solution

for some perspective sectors of Ukrainian economy.

There are some examples of cluster’s creation in Ukraine which development and

efficiency are worth to observe before making conclusion.

24

Literature AHARONI, Yari, (1969)“The Foreign Direct Investment Decision Process”. Boston:

Harvard University, Division of Research, Graduate School of Business Administration

AZHAR T.M. AND LEUNG L.C., (1993) "A Multi-Attribute Product Life-Cycle

Approach To Replacement Decisions: An Application Of Saaty's System-With-Feedback

Method," Engineering Economist, Summer , pp. 321-344.

BAYUS, B.L. (1994) "Are Product Life Cycles Really Getting Shorter?" Journal Of

Product Innovation Management, September, pp. 300-308.

BENNETT R.C. and. COOPER R.G, (October 1984) "The Product Life Cycle Trap,"

Business Horizons, , pp. 7-16.

BELDERBOS R., SLEWAEGEN L., “ Foreign Investment and International Plant

Configuration: Whither the product Cycle?” NIBOR Reseatch Memorandum RM/00/03.

BELL, J. “The internationalization of small computer softwear firms, A further

challenge to “stage” theotires”, European Journal of Marketing, 29 (8), 60-75.

BENNETT R.C. and COOPER R.G., (1984) "The Product Life Cycle Trap," Business

Horizons, October 1984, pp. 7-16.

BERNARD A. B., JENSEN J. B. (2001) Why Some Firms Export. MIT Dept. of

Economics Working Paper # 97-26.

BUCKLEY, P.J. and CASSON M. (1976). The future of Multinational Enterprise. New

York: Holmes&Meier.

BUCKLEY, P.J. and CASSON M (1981). “The optimal timing of foreign direct

investment” Economic Journal, 91, pp.75-87.

CAMPA, J., DONNENFELD S. and WEBER S. (1998) “Market Structure and Foreign

Direct Investment”, Review of International Economics, 6, pp. 361-380.

CASE Ukraine: Ukrainian Economic Outlook. Tendencies, Estimates, Forecasts.

CATWELL, J. (1995). “The globalisation of technology: what remains of the product

cycle model”, Cambridge Journal of Economics, 19, pp. 155-174.

25

CHUN Zhu Susan. Trade, product cycles, and inequality within and between countries.

Canadian Journal of Economics/ Revue canadienne d’Economique, Vol. 37, No.4.

DANIELS, John D. and RADEBAUGH, Lee, ( ) “International Business Environments

and Operations”.

DAVIDSON W.H. (1980) The Location of Foreign Direct Investment Activity: Country

Characteristics and Experience Effects, Journal of International Business Studies, 11, pp. 9-

22.

DEARDORFF, A. V. (1984) An Exposition and Exploration of Krueger’s Trade Model,

Canadian Journal of Economics 36, pp. 167-175.

DICKEN, P. (1998) Global Shift: transforming the world economy, third edition. Paul

Chapman Publishing ltd., London.

DUNNING, John, (1988) “The Eclectic Paradigm of International Production: A

Restatement and Some Possible Extensions”, Journal of International Business Studies, #19.

DUTHIL G., GUROVA O. (2005) « Ukraine: état économique et perspectives dans

l’Europe », 54 Congres of International Association of Economists, Aix-en-Provence, May,

23-25, 2005.

DUTHIL Gerard. (2006) Progrès technique et marché du travail, L’harmattan.

FEENSTRA, R.C., ROSE A. K. (2000) “Putting Things In Order: Trade Dynamics And

Product Cycles”, The Review Of Economics and Statistics, MIT Press, vol. 82(3), pp. 369-

382.

FOMISHIN S.V. (2002) International Economic Relations on the Edge of Millennia/

Kherson: Oldi-plus,.- 560p

GROSSMAN, GENE and E. HELPMAN, (1991), Endogenous Product Cycles, Economic

Journal, 101, 1214-1229.

HIRSCH, S., (1967), Location of Industry and International Competitiveness, Oxford

University Press, Oxford.

International Economics. Appleyard Field. 3rd ed. (p 176-180).

International Trade. Theory, strategies, and evidence. RIVERA-BATIZ A. LUIS, OLIVA

MARIA-ANGELS. Oxford University Press.

KARLSSON, C., (1988), Innovation Adoption and The Product Life Cycle, Umea

Economic Studies No. 185, Umea University.

26

KIRICHENKO A. (1999) “Foreign Trade of Ukraine on the threshold of III millennium”

Foreign Trade Review.- №1-2.

KLEPPER, S., (1996), “Entry, Exit, Growth, and Innovation over the Product Life

Cycle”, American Economic Review, Vol. 86, 3: 562-84.

KLIMOVICH L., (1999) «Тенденции развития транснациональных компаний в

совсременных условиях». Белорусский журнал международного права и

международных отношенийб № 3.

KRAVIS, I. B. and LIPSAY, R. E. (1982) Location of Overseas Production and

Production for Exports by U. S. Multinational Firms. Journal of International Economics. 12:

201-33.

KUZNETS, S., (1929), “Retardation in Economic Growth”, Journal of Economic and

Business History, 1: 534-60.

E. KUZNETCOV (2005), “Delovoj Myr” programme, UT-1.

MADURA, Jeff, (1998) “International Financial Management”, West Publishing, 653p.

MAGEE, S.P, (1977) “Multinational Corporations, the Industry Technology Cycle and

Development”, Journal of World Trade Low, 2:297-321.

MIKIC M. (1998) International Trade. St. Martin’s Press, New York,.

MYSHKO S. « Ukrainian Export's Potential », Business inform 1998.-#11.

NGUYEN Quoc Hung. Jan. (2004), Product Cycle Mechanism with Foreign Direct

Investment, and the technology Transfer.

PARRY, Thomas, (1981) “The Multinational Enterprise: International Investment and

Host Country Impacts”. Journal of International Business Studies, Vol. 12, No. 1, Tenth

Anniversary Special Issue , pp. 156-158.

PAVITT, K., and ROTHWELL R., (1976), « A comment on « A dynamic model of

process and product innovation », Omega, 4 :375-77.

PORTER M. E., (1990) The Competitive advantage of the nation. New York.

POSNER, M. V. (1961) International Trade and Technical Change, Oxford Economic

Papers 13, pp. 323-341.

POTTS G.W., (1988) "Exploit Your Product's Service Life Cycle," Harvard Business

Review, September-October, pp. 32-34.

Review of Ukraine’s Foreign Trade in 2004 http://www3.sympatico.ca

SALVATORE Dominick. International Economics. 7th ed. (185-188)

27

SHAPIRO, Alan, (2004) “Foundations of Multinational Financial Management”, 5th

ed., John Wiley & Sons.

J. SHEWCHUCK, (1992) "Life Cycle Thinking," CMA Magazine, May, pp. 34-36.

UTTERBACK J. M. and ABERNATHY W. J. (1975) “ A dynamic Model of Process and

Product Innovation”, Omega, Vol. 3, 639-56.

VERNON, R. (1973) Economic and political consequences of multinational enterprise.

VERNON, R. (1972) Economic environment of international business.

VERNON, R. (1973) Entreprises multinationals.

VERNON, R. (1985) Exploring the global economy.

VERNON, R. (1966) "International Investment and International Trade in the Product

Cycle," Quarterly Journal of Economics 80(2):190-207.

VERNON, R. (1977) Storm over the multinationals.

VERNON, R. (1970) Technology factor in international trade.

VERNON, R. (1979) “The Product Cycle Hypothesis in a New International

Environment”. Oxford Bulletin of Economics and Statistics, 41, 225-267.

World Bank statistics: http://wbln0018.worldbank.org

www.ukrstat.gov.ua

28

Appendixes Appendix 1 Rating of world’s largest steel’s producers (by beginning of 2004)

Place in the rating

Name of the company Production (million tons)

1 Arcelor 42,8 2 LNM Group 35,3 3 Nippon Steel 31,3 4 JFE 30,2 5 Posco 28,9 6 Shanghai Baosteel 19,9 7 Corus Group 19,1 8 US Steel 17,9 9 ThyssenKrupp 16,1 10 Nuccor 15,8 13 ISG 10,3 28 « Kryvorozhstal »

(« Криворожсталь ») (became a part of Mital Group in 2006)

7,1

31 ММC names after Illich (ММК им Ильича)

6,5

40 Azovstal (“Азовсталь”) 5,3 55 Zaporozhstal

(“Запорожсталь”) 4,4

67 Alchevsk metal combinat (Алчевский меткомбинат)

3,5

73 DMP named after Petrovsky (ДМЗ им.Петровского)

3,2

Data by International Institute of cast iron and steel, compiled by author.

Appendix 2. Direct Foreign Investments into Ukrainian economy 1999-2005yy. Addition (growth) Year

$ mln Times or %

Per habitant, $ Total, milliards $

1999 50 3.1

2001 80 3,923

2002 1074.82 8,4% 111 5,339

2003 1319,9 16-17% 140 6,6576

2004 1559,5 23% 177 8.3539

Data by The State Statistics committee of Ukraine

29

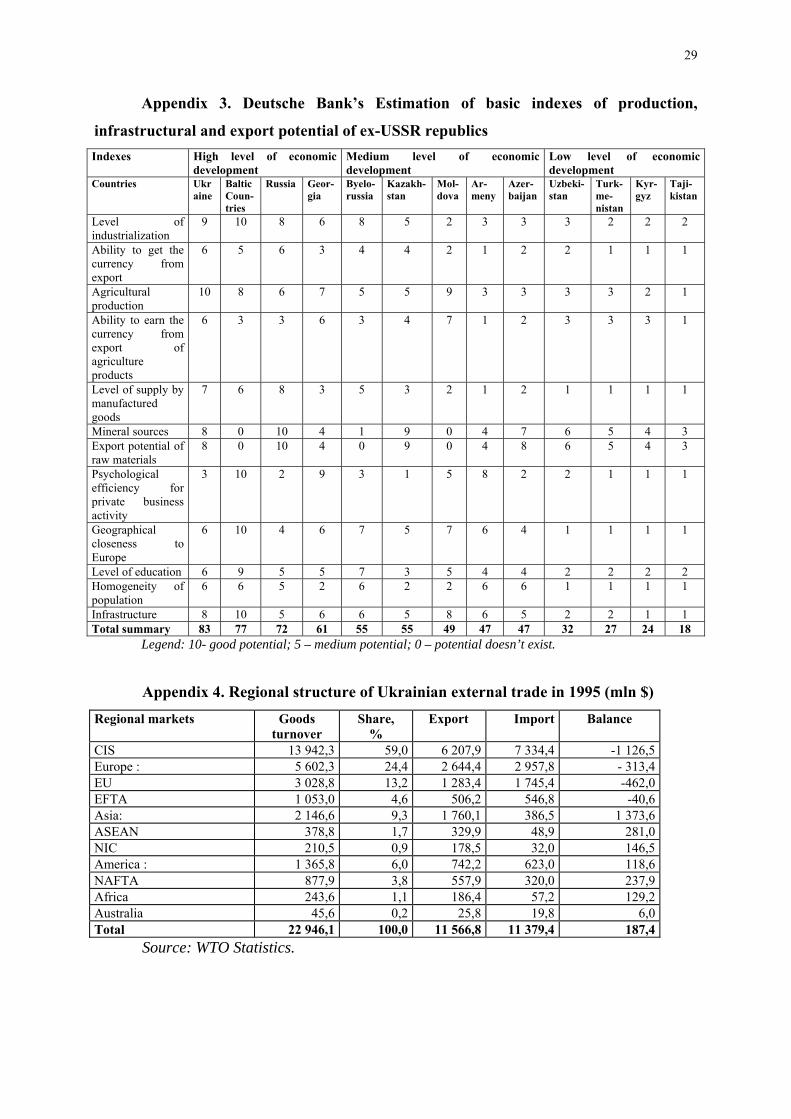

Appendix 3. Deutsche Bank’s Estimation of basic indexes of production,

infrastructural and export potential of ex-USSR republics Indexes High level of economic

development Medium level of economic development

Low level of economic development

Countries Ukraine

Baltic Coun-tries

Russia Geor-gia

Byelo-russia

Kazakh-stan

Mol-dova

Ar-meny

Azer-baijan

Uzbeki-stan

Turk-me-nistan

Kyr-gyz

Taji-kistan

Level of industrialization

9 10 8 6 8 5 2 3 3 3 2 2 2

Ability to get the currency from export

6 5 6 3 4 4 2 1 2 2 1 1 1

Agricultural production

10 8 6 7 5 5 9 3 3 3 3 2 1

Ability to earn the currency from export of agriculture products

6 3 3 6 3 4 7 1 2 3 3 3 1

Level of supply by manufactured goods

7 6 8 3 5 3 2 1 2 1 1 1 1

Mineral sources 8 0 10 4 1 9 0 4 7 6 5 4 3 Export potential of raw materials

8 0 10 4 0 9 0 4 8 6 5 4 3

Psychological efficiency for private business activity

3 10 2 9 3 1 5 8 2 2 1 1 1

Geographical closeness to Europe

6 10 4 6 7 5 7 6 4 1 1 1 1

Level of education 6 9 5 5 7 3 5 4 4 2 2 2 2 Homogeneity of population

6 6 5 2 6 2 2 6 6 1 1 1 1

Infrastructure 8 10 5 6 6 5 8 6 5 2 2 1 1 Total summary 83 77 72 61 55 55 49 47 47 32 27 24 18

Legend: 10- good potential; 5 – medium potential; 0 – potential doesn’t exist.

Appendix 4. Regional structure of Ukrainian external trade in 1995 (mln $) Regional markets Goods

turnover Share,

% Export Import Balance

CIS 13 942,3 59,0 6 207,9 7 334,4 -1 126,5Europe : 5 602,3 24,4 2 644,4 2 957,8 - 313,4ЕU 3 028,8 13,2 1 283,4 1 745,4 -462,0ЕFТA 1 053,0 4,6 506,2 546,8 -40,6Asia: 2 146,6 9,3 1 760,1 386,5 1 373,6АSEAN 378,8 1,7 329,9 48,9 281,0NIC 210,5 0,9 178,5 32,0 146,5America : 1 365,8 6,0 742,2 623,0 118,6NAFTA 877,9 3,8 557,9 320,0 237,9Africa 243,6 1,1 186,4 57,2 129,2Аustralia 45,6 0,2 25,8 19,8 6,0Total 22 946,1 100,0 11 566,8 11 379,4 187,4

Source: WTO Statistics.