Embed Size (px)

Citation preview

The Polish Real Estate GuideEdition 2015

Poland The real state of real estate

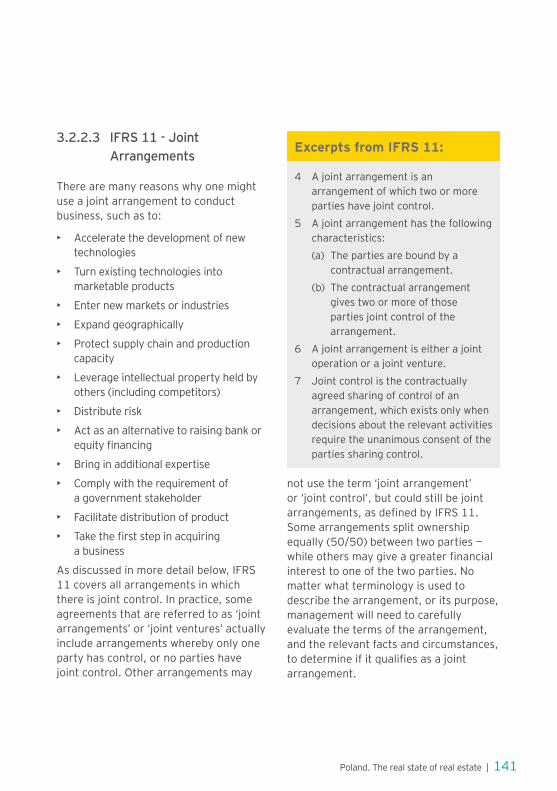

1

2

Preface

page 1

Polish Real Estate Market1.1. Officemarket 3

1.2. Retailmarket 10

1.3. Warehousemarket 15

1.4. Residentialmarket 19

1.5. Investmentmarket 23

1.6. KeycitiesinPoland 30

Legal and tax aspects of investing in real estate2.1. Legalbackground 44

2.2. Investmentvehiclesandstructures 50

2.3. Realestatefinancing 61

2.4. Acquisitionofrealestate–assetdealandsharedeal 74

2.5. Developmentandconstruction 88

2.6. Operationandexploitation 99

2.7. Exitingtheinvestment 107

2.8. Saleandleaseback 108

2.9. Duediligenceaspartoftheacquisitionprocess 110

4

3Accounting aspects of investing in the Real Estate market3.1. Polishaccountingregulations 121

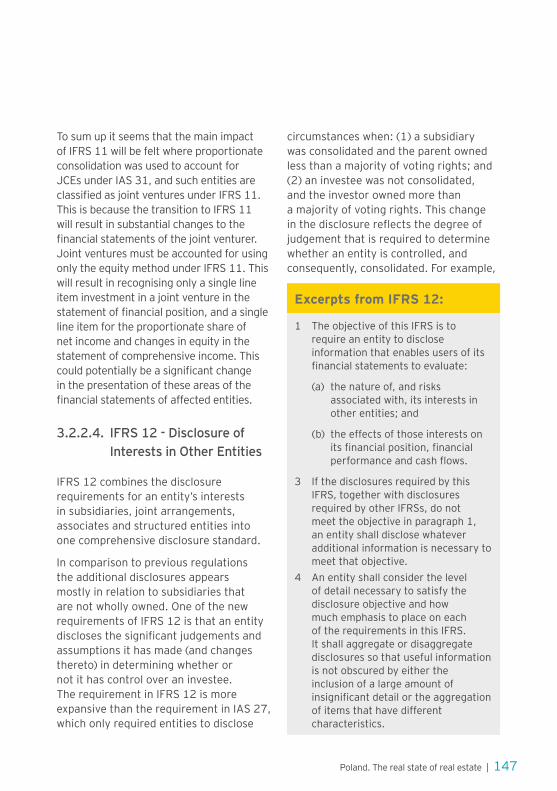

3.2. SelectedAspectsofAccountingforRealEstate underInternationalFinancialReportingStandards(applicableforannualperiodsbeginningon 1January2013) 134

3.3. SelectedIFRSissuesandtheirimplicationsfor realestateentities 152

Contact

page 160

Appendix

page 170

Preface

EY, a globalleaderinassurance,tax,transaction,advisoryandlegalservicespreparedthisguidetothePolishrealestatemarket.Thisguideaimstoprovideitsreaderswitha broadviewofthemarketandthecurrentinvestmentclimate,aswellaslegalandtaxinformation,ina practicalformattohelpyoumakeinformedinvestmentdecisions.OurcombinedexpertiseinthismarkethasenabledustoproducewhatwehopewillbecomeanindispensablereferencetoolonthestateofthePolishrealestatemarket.

Inconjunctionwiththeviewscontainedinthisguide,itisimportanttoseekcurrentanddetailedinformationonthecommercialclimateatthetimeofconsideringyourinvestment,asthiscanchangeatanytime.Thisguidereflectsinformationcurrentasof1January2015unlessstatedotherwise.

Poland.Therealstateofrealestate|1

Polish Real Estate Market

1

2|Poland.Therealstateofrealestate

1.1.OfficemarketPoland–general

Followingmajorreformsin1992,Polandexperiencedaboomineconomicactivityinthe1990s.Likeothermarkets,themodernofficemarketbegantoemergewithaninitialwaveofnewofficeconstructionstartinginthefinancialandpoliticalcapital–Warsaw.

Until1996,annualsupplyremainedbelow50,000m2, whichwassubstantiallylessthantherapidlyincreasingdemand.Becauseofthedifficultlocaldevelopmentandfinancingconditions,supplywasinitiallyslowtorespond.Thesecondhalfofthedecadeshowedarapidincreaseinsupply,asPolanddemonstrateditspoliticalstabilityandsoundeconomicfundamentals.Therapidincreasescontinuedintothefirstpartofthisdecade,initiallyaddressingpent-updemandfromdecadesoflowsupply,butlaterresultinginanofficeoversupplyinmanymajorcitiesandtownsinPoland.Generally,rentswereinsteadydeclinefromthe1990suntil2005.Therunupto2009showedareversalofthistrend,withindicationsofamaturingofficemarketwherenewbuildingscometomarketinamoretimelyresponsetodemand,thusstabilizingrentsandvacancies.Althoughthefinancialcrisistemporarilyaffectedthesituation,WarsawremainsbyfarthelargestofficemarketinPolandandstillattractsmajordevelopmentactivity.Ontheotherhand,otherregionalbusinesscentershaveenteredthepathofstrongeconomicgrowth,increasinginterestinmodernofficeaccommodationeveninsmallercitiesandtowns.OnthemajorityofPolishofficemarkets2011wasoneoftheweakestyearsintermsofnewsupply.Thestrictlendingcriteriaimplementedbybanksafter2008verifiedmostoftheinvestmentprocesses.Currentlyconstructionactivityisrecoveringquickly.Theannuallevelofnewsupplyin2013amountedtonearly670,000m2,whichrepresentedsignificantlyhighergrowthincomparisontopreviousyears.Theleveloftotalcompletionsin2013wasthehighestyearlyvaluerecordedinPolandsince2000.

Poland.Therealstateofrealestate|3

13,0

6,0

11,510,5

13,7

7,5

13,8

15,8

10,4

0

5

10

15

20

25

-

500 000

1 000 000

1 500 000

2 000 000

2 500 000

3 000 000

3 500 000

4 000 000

4 500 000

5 000 000

Warsaw Krakow TriCity Wroclaw Poznan Lodz Katowice Szczecin Lublin

Supply Rents Vacancy rate (%)

Rent

s in

EUR

/m2 /m

onth

Supp

ly in

m2

Source: EY

Office market in Poland

Newsupplyin2014amountedto600,000m2,buttakingpipelineintoconsideration,growingtrendshallcontinueinfollowingyears.Asfarasnewprojectsunderconstructionandproposedareconcerned,in2014thebiggestconstructionactivitywasobservedinWarsaw,Kraków,Tri–CityandKatowice.

Focus on Warsaw

ThemodernofficemarketinWarsawstartedtodeveloprapidlyatthebeginningofthe1990sinresponsetothePolishpoliticaltransitionandeconomicreforms,followedbyagrowthperiodduringrecentyears,inwhichtheWarsawareaplayedamajorrole.

Becauseofitscentralfunctionsandconvenientlocation,thePolishcapitalcityhasreceivedasignificantshareoftheinflowofforeigncapital.Largeforeigncompanies,includingvariousfinancialinstitutions,consultingcompanies,aswellasinternationalfirms,usuallychooseWarsawasalocationoftheirheadquartersinPoland.Inaddition,Warsawhastraditionallybeenthemostimportantadministrativeandbusinesscenterfordomesticcompanies.Thisledtorapid

growthofdemandformodernofficespaceinthecity,whichintheperiodfrom1990untilthefirsthalfof1998resultedin98%to100%occupancyratesaswellasoneofthehighestrentallevelsforofficespaceamongEuropeancities.

Supply

Theendof1998markedthefirstdramaticdateformodernofficespace,whenoverthecourseofoneyearthemodernofficesupplydoubledfromthe300,000m2completedbetween1989and1997to680,000m2.Twoyearslater,stockrosetoapproximately1,360,000m2andalthough54%ofthiswasinthecitycenter,2001markedtheendofthecentrallocation’sdominanceinnewannualsupply.Withtheexceptionof2003,annualdeliveryofmodernofficespaceinnon-centrallocationsexceededcentral,andthetrendcontinuedthrough2013.Attheendoffirsthalfof2013,thetotalmodernofficespaceinWarsawhasexceeded4millionm2,withnon-centrallocationsaccountingforaround70%.WarsawremainsthemostmatureofficemarketinPolandwithatotalofficestockofapproximately4.4millionm2.

4|Poland.Therealstateofrealestate

Source: EY

Annual delivery of modern office space (m2) in Warsaw

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

-

50 000

100 000

150 000

200 000

250 000

300 000

350 000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Vac

ancy

rat

e

Supl

ly in

m2

Non-central City center Vacancy

Asthesupplyofnewspacereachedandsurpasseddemand,themarketsawvacancyratesrisetoveryhighlevels.Startingfrombetween4and6%in1998,thebuildingboomfrom2000to2002helpedvacancyratesriseasfaras20%inthecitycenterand16%intheoutskirts.Asthemarketstabilized,andnon-centrallocationsbecamethenormratherthantheexception,centralandnon-centrallocationsfluctuatedbackandforthbetween15and19%,withnon-centrallocationsfallingbelowthe10%mark(7%onaverage)in2004.

Regardlessoftheproportionofcentraltonon–centrallocations,theoverallvacancylevelinWarsawhassystematicallydecreasedfrom2002until2007,whencentralandnon-centralvacancyratesstoodatthe3.4%and2.9%respectively.Withthecrisescameareversalofthistrend,in2008and2009vacanciesdoubledtoover7%overall.In2010,vacancyrateremainedstableatthelevelof8%.Duetogrowingdemandforofficeaccommodationandlimitedcompletionsin2011,thevacancyrateinWarsawfellandreached6.7%.Howeverattheendof2012,approximately8.8%wasunoccupied.Duetothesignificantvolume

ofnewprojectscompletedin2014,thevacancyrateexceeded13%.Itisexpectedthatthevacancylevelwillrisewithinthenextfewyears.

Onthebasisoflocation,themodernofficestockinWarsawcanbedividedintotwogroups:centralandnon–central.Thecitycenterisboundbyul.Towarowa,ul.Grójecka,ul.Wawelska,al.ArmiiLudowej,theVistulaRiverandal.Solidarności.Themostsignificantofficebuildingslocatedwithinthisareainclude:Rondo1,Lumen,Skylight,Metropolitan,WarsawFinancialCenter,FocusFiltrowa,WarsawTradeTower,SpektrumTower,PlacUniiandAtrium1.Non–centralofficelocationsincludeMokotów,Ochota,Wola,WłochyandPragadistrict.Intheselocations,WiśniowyBusinessPark,BusinessGarden,TrinityPark,MarynarskaBusinessPark,PlatiniumBusinessPark,PoleczkiBusinessPark,CristalPark,JerozolimskieBusinessParkandLipowyOfficeParkwarrantcloserattention.

Yearlynewstockpeakedin2000when360,000m2wasaddedtosupplyandtherehasbeenyear-on-yeargrowthsince2005,when120,000m2ofnewsupplywasadded.

Poland.Therealstateofrealestate|5

Major office developments completed in 2014

Name Location Area (m2) Developer

GdańskiBusinessCentreNon-central InflanckaSt.

46,000 HBReavis

EurocentrumOfficeComplexI

Non-centralJerozolimskieAve.

38,700 CapitalPark

WarsawSpireBCentralGrzybowska/TowarowaSt.

20,000 Ghelamco

NimbusOfficeNon-centralJerozolimskieAve.

19,500 Immofinanz

Atrium1Central JanaPawłaIIAve.

16,500 Skanska

ParkRozwojuINon-centralKonstruktorskaSt.

16,000 EchoInvestment

Source: EY

Accordingtoprojectannouncements,morethan300,000m2ofmodernofficespacewillentertheWarsawmarketin2015.However,thatpredictionissubjecttoanumberofvariables,asdevelopers(andtheirlenders)takeamorecautious

approachtospeculativeprojects.Itisexpectedthatsomeoftheseprojectswillbedelayeduntilsuchtimewhenreasonablelevelofpre-leasinghasbeenachieved.

Theyear2010sawthecompletionofover200,000m2ofnewstock,thoughthiswasplannedwellbeforethecrisisandtheseprojectshadsecuredfinancinginadvanceofnowstricterlendingcriteria.In2011approximately120,000m2weredeliveredtothemarket.Themajorityofspaceisinofficebuildingslocatedoutsideofthecitycenter.In2012themarketwitnessedahighergrowthinnewofficesupply,whichamountedto270,000m2.

In2013arecordamountofnewofficespacedeliveredtothemarketwasobservedexceeding300,000m2.Year2014broughtslightslowdowninnewsupplywithnearly280,000m2ofnewspace.Similarlytopreviousyears,mostofthenewofficebuildingsweresituatedinnon-centrallocations.ThereisexpectedthatWarsawwillstrengthenitspositionintermsofnewofficesupplyoverthenextfewyears.

6|Poland.Therealstateofrealestate

Demand

Thedemandformodernofficespacecomesmainlyfrom:

• PolishandforeigncompanieswhoarebasedinPolandandhaveparticipatedintherapideconomicgrowth;

• newentrantsintothePolishmarket,particularlyevidentin2004,justafteraccessiontotheEuropeanUnionandagainduring2007and2008;

• thenew“ServicesandInformationEconomy”acceleratingtheneedforup–to–dateofficespace.PolandinparticularhasbenefitedfromBusinessProcessOffshoring(BPO);

• stateentitieswhicharemoreandmoreinterestedinleasingofficespaceratherthanoccupyingself-owned,oldandlowqualitybuildings.

Growthsurgedin2007,withtake–upreachingalmost500,000m2.Take-upmoderatedto525,000m2in2008and

Major office developments under construction

Name Location Total office area (m2) Developer

WarsawSpireC&A Central Grzybowska/TowarowaSt. 95,000 Ghelamco

GenerationPark Central Wronia 84,000 Skanska

Q22 Central JanaPawłaIIAve. 55,000 EchoInvestment

GdańskiBusinessCenterII

Non-central InflanckaSt. 45,000 HBReavis

Postępu14 Non-central PostępuSt. 33,700 HBReavis

AstrumBusinessPark

Non-central ŁopuszańskaSt. 30,000 Prochem

RoyalWilanów Non-central Klimczak/PrzyczółkowaSt. 28,000 CapitalPark

DomaniewskaOfficeHub

Non-central DomaniewskaSt. 27,000 PHN

EurocentrumOfficeComplexII

Non-central JerozolimskieAve. 25,000 CapitalPark

Wołoska24 Non-central Wołoska 21,000 Ghelamco

Atrium2 Central Rondo ONZ 20,000 Skanska

PrimeCorporateCenter

Central GrzybowskaSt. 20,000 GolubGetHouse

Source: EY

Poland.Therealstateofrealestate|7

bytheendofthatyearsymptomsofadecliningmarkethademerged,particularlyforofficespaceintheWarsawcitycenter.In2009thetotalvolumeofleasingtransactionsamountedto210,000m2,orapproximately40%ofthepreviousyear’svolume,withamarketrelegatedtomainlysmallleasetransactions.

Currently,demandismuchlessdrivenbybusinessexpansionandratherincreasinglybytenantsrelocatingeithertoimprovetheiraccommodationortoreducecostbyoptimizingspace.Duetothecrisisin2008/2009manytenantsreducedtheirspaceandwereseekingtosublettheexcess.Thissituationchangedin2010,when,duetoamorepositiveeconomicenvironmentandoptimisticforecasts,demandhasrecovered.In2013recordofamountofofficespace(633,000m2)wereleased.In2014demanddroppedby3%to612,000m2,butaccordingtoforecastsdemandwilcontinuetoincreaseinthenearfuture.

Rents

Alongtheclassicsupplyanddemandmodel,rentsinthelate1980sandearly

1990sescalatedasPolandopeneditsborderstoforeigninvestment,andsupplyofmodernofficespacewasextremelylimited.Demandforofficespacepushedrentstotheirpeakin1991ofUSD50/m2/monthforofficespaceofrelativelypoorquality.

Withsuchlimitedsupplyavailable,therewaslittlesegmentationintheWarsawofficemarket,resultinginbothcentralandnon-centrallocationshavingsimilarrentrates.

Thefirstbuildingboomofthelate1990spushedoverallrentsdown,butitwastheintroductionofout-of-townofficeparksaround1996,thathelpeddifferentiatepricesbetweencentralandnon-centrallocations.Thelate1990snoticedrentsformoderncitycenterofficestypically25%to30%higherthanfornewofficesinout–of–townlocations.However,notallofthedifferencecanbeaccountedforbylocationalone,asnon-centrallocationswerebuiltformoreprice–conscioustenantsreadytoacceptalowerstandard.

Thesecondpartoftheboomintheearly21stcenturybroughtwithitadditionalincreasesinsupplyandafurtherdropinoverallrentlevels.Thistemporarilypushedthegapbetweenlocationscloser,butmore

Prime office rents & cumulative office supply

Source: EY

Rent

s in

EUR

/m2 /m

onth

Supp

ly in

m2

0

5

10

15

20

25

30

35

40

45

0

500 000

1 000 000

1 500 000

2 000 000

2 500 000

3 000 000

3 500 000

4 000 000

4 500 000

5 000 000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Supply

8|Poland.Therealstateofrealestate

demandingclientshelpedraisethestandardofcentrallocationsandtwoaltogetherseparatemarketsemerged.

Currencieshavealsoplayedaroleintheleasingmarket.IntheearlyyearslowstandardpropertieswerepricedinPLN,withhigherstandardpropertiesgearedforinternationalclientelebeingdenominatedinDMorUSD.SinceaccessionintotheEU,theEurohasbecomePoland’sstandardreferencecurrencyforleases.Today,rentsforcentrallylocated,highqualityofficebuildingsarebetweenEUR20and24/m2/month.

CurrentrentsforprimeofficespacelocatedoutsideofthecitycenterrangefromEUR11to15/m2/month.Asexpectedinatoughmarket,newrentalcontractsarebeingsignedwellbelowaskingrates.Oursourcessuggesttypicaleffectiverentsareroughly15-25%lowerthanaskingrents.Askingrentsdependmainlyonlocation,buildingstandard,sizeandlengthofleaseterm.

Duetothegrowingdevelopmentactivityandnumberofnewprojectsscheduledforcompletionin2015,itisexpectedthattherentalratesmaydecrease,especiallyinthecentrallocations.Asaresultofintensecompetitionamonglandlords,thedifferencebetweenaskingandeffectiverentsmayincrease.

Standard lease terms

Thefollowingtermsformodernofficebuildingsareregardedascommonfeatureswithinatypicalleaseagreement:

• sincetheintroductionoftheEUR,mostnewleaseshavebeendenominatedinEUR,butpaidinPLNasregulatedby

Polishlawuntil2009(seesectiononlegalandtaxaspects);

• rentsaresubjecttoannualindexationonthebasisoftheconsumerpriceindexintheEurozone(MUICP,HICP);

• servicechargesincludingwater,electricity,heating,air–conditioning,service,cleaning,etc.areaddedtonetrentsandcalculatedaccordingtothearealeased.TheseratesgenerallyvaryfromEUR3.5to5.5/m2/month;

• achargeforcommonspaceisusuallyaddedtothenetofficespace.Thischargecalculationisbasedontheproratashareofcommonspaceused(lift,lobby,reception).Such“add–onfactors”generallyvaryfrom5%to10%oftheleasedarea;

• inadditiontorentandservicecharges,tenantsareobligedtopay23%ValueAddedTax(VAT);

• landlordsusuallyrequiretenantstoprovidearentaldepositorbankguaranteeequalto3-6monthrent;

• leasesrangefrom3to10years;typicalcontractsare5years,withatrendtowardlongerleasesforlargertenantsandnewdevelopments;

• Incentivesfortenantsarecurrentlyacommonpracticeandtheirrangeissubjecttoindividualnegotiations,whichdependmostlyonthesizeoftheoccupiedpremisesandthetermoftheleaseagreement.Typicalleaseincentivesinclude:

• rent–freeperiodofapprox.1monthper1yearofleaseormore;

• fit-outallowanceofapprox.EUR150–200perm2ofnetofficespace.

Poland.Therealstateofrealestate|9

1.2.Retailmarket

Poland – General

Polishretailmarkethasundergonesubstantialchangesinrecentyears,particularlyinlargerurbanareas.Fromjustalimitednumberofstate–ownedandsmallprivateenterprisesatthebeginningofthe1990s,thesupplyhasgrowntoencompassanincreasingnumberofinternationalretailchainsandgoodqualitylocaloutlets.

Foreignshoppingcenteroperators,investorsanddevelopershavemovedacrossnationalbordersinordertoaccessneworlesscompetitivemarketsortoexploitmarketniches.Inthiscontexttheownershipofshoppingcenters,aswellasthemixofretailtenants,isbecomingincreasinglyinternational.

Intheearly1990sPolishretailsupplygrewtosatisfythedemandforfood.ThisledtothearrivalofinternationalbrandsupermarketsincludingBilla,Hit,Rema1000andGlobi.From1996on,PolandhasseenarapidexpansionofmajorhypermarketchainssuchasTesco,Hypernova,Carrefour,Auchan,Géant,E.LeclercandReal.Simultaneously,somesupermarketchainsretreated(e.g.Billa),someweresold(e.g.Hit,Géant,LeaderPrice,Hypernova,Real)andafewnewstrongbrandsappeared(Aldi,Alma,PiotriPaweł,Simply).Moreover,anexpansionofdiscountstoresrepresentedbyLidl,PlusDiscount,NettoandBiedronkahasbeenobserved.

Currently,thetotalmodernretailsupplyaccountsfor12.4millionm2.AlthoughthelargestshareintheretailmarketisheldbyWarsawfollowedbyothermaincitiessuchasTri–City,Poznań,Wrocław,Kraków,ŁódźandKatowice,investorshavebeenseekingopportunitiesinsmallercities,

10|Poland.Therealstateofrealestate

thusmoreandmoreprojectsarebeingopenedandbuiltintownssuchas:Leszno(GaleriaGoplana),Lublin(AtriumFelicity,TarasyZamkowe),JeleniaGóra(GaleriaSudecka,NowyRynek),StarogardGdański(GaleriaNeptun),Olsztyn(GaleriaWarmińska),Kalisz(GaleriaAmber),Ełk(BramaMazur)andPiła(GaleriaVIVO!).

Modernretailspacecompletedin2014amountedtoaround450,000m2. Majornewopeningswithspaceabove40,000m2includedAtriumFelicity(Lublin)andGaleriaWarmińska(Olsztyn).Majorprojectsinthepiplinewithopeningplannedinyears2015-2016areGaleriaPosnania(Poznań),ZieloneArkady(Bydgoszcz),TarasyZamkowe(Lublin)andSukcesja(Łódź).

Developer’sactivityinsmallandmediumcitieshasbeenobservedforafewyears.Theactualamountofspacethatwillbedeliveredtothemarketin2015willdependuponavailabilityoffinancingandtenantdemandforretailspace.Apartfromthemedium-sizeretailprojectsthemarketistendingtowardstheopeningof“stripmalls”(conveniencecenters)-smallretailparkswithanareanotexceeding5,000m2,oftenlocatedintheregionalcitiesandconstitutingcompetitionforregularshoppingcenters.

Asinpreviousyearsin2014trendconsistingmodernizationand/orextensionofexistingshoppingmallshasbeenobservedonthemarket.Themainextensionscompletedin2014wereextensionsofGeminiPark(BielskoBiała)andCHRywal(BiałaPodlaska).Expansionsbeingunderconstructionare

AtriumPromenada(Warsaw),WolaPark(Warsaw)FactoryUrsus(Warsaw),Ogrody(Elbląg),AtriumCopernicus(Toruń),GaleriaSudecka(ex.CHEchoinJeleniaGóra),MagnoliaPark(Wrocław)andGaleriaPomorska(Bydgoszcz).

Supermarketsorhypermarketsarestillthepreferredformulaforanchortenancy,althoughanincreasingnumberofprojectsarelookingtowardsentertainmentfunctionstodecreasegroceryretailingasthebasicdemanddriver.Standardcomplementaryfunctionsstillincludegalleryshops,servicepoints,andafoodcourt.

Overthelastfewyears,newretailformattypeshavealsoemerged,includingshoppingcenterswithachoiceofinteriordecorationbrands(e.g.DomotekainWarsaw),DYIstores(Jula,Castorama,OBI,Praktiker,LeroyMerlin)andretailparks.Themarketforretailoutletcentershasbeendevelopingrapidlyoverthelastfewyears.Twelvecentersarecurrentlyinoperationinthesurroundingareasoflargercities.Theyareoperatedmainlybythreechains-FactoryOutlet,FashionHouseOutletCentreandOutletCenter.Themainschemesdeliveredtothemarketin2014wereOutletCentersinLublinandBiałystok.ThemostsignificantoutletcenterunderconstructionisextensionofFactoryUrsusinWarsaw.

Moreover,someofthelargesthypermarketoperatorslikeTescoorCarrefourhavebeenintroducingnewformatssuchasmini-hypermarketsandsupermarkets(e.g.CarrefourExpressandCarrefourMarket).

Poland.Therealstateofrealestate|11

Inresponsetotherapiddevelopmentofsupermarketanddiscountchainsacrossthecountry.Astothegeographicaldistribution,developmentsfeaturingahypermarketaretypicallybuiltoutsideofthecitycenterwhiledowntownmallsusuallyofferonlyasupermarket.

Themajorhyperandsupermarketchainsintermsofsalesrevenuesinclude:MetroAG(MakroCash&Carry,MediaMarkt,Saturn),JeronimoMartins(Biedronka,Hebe),Tesco,Carrefour,AuchanGroup(Auchan,Real,Simply),SchwarzGroup(Lidl,Kaufland),EmperiaHolding(Stokrotka,Milea),ITM(Intermarche,Bricomarche),E.Leclerc.

Focus on Warsaw

TotalmodernretailsupplyinWarsawexceeds2.1millionm2, but only approximately1.6millionm2ofitcould

beconsidered“modern”retailspacesuitableforinternationaloccupiers.Thisequatestoaround1m2oftotalretailspaceperperson,whicheventakingintoconsiderationthedisposableincomeofWarsaw’sinhabitants,ismuchlowerthaninmajorWesternEuropecities,wheretheratioisonaverage2m2perperson.Modernretailspaceincludesshoppingmallsandhypermarkets,mostofwhicharelocatedoutsidethecitycenter.

Theremainingretailersoccupymostlyretailunitssituatedonthegroundfloorsofresidentialbuildingsordepartmentstoresbuiltbeforethe1990s.

LimitednewretaildevelopmentswererecordedinWarsawin2013and2014.Apartfromthe5,000m2extensionofGaleriaMokotówandopeningofPlacUniiShoppingCenter(15,500m2)(bothin2013),therewasnootherkeydevelopments.

Major shopping centers in Warsaw

Name Location Area (m2) Owner Completion

Arkadia Śródmieście JanaPawłaIIAve. 110,000 Unibail-Rodamco 2004

BlueCity OchotaJerozolimskieAve. 82,000 Singspiel PhaseI–2004

PhaseII-planned

WolaPark Wola GórczewskaSt. 73,000 InterIkeaCenter

PolandPhaseI–2002PhaseII-planned

AtriumPromenada

PragaPołudnieOstrobramskaSt. 66,000 AtriumEuropean

Real Estate

PhaseI–1996PhaseII–1999PhaseIII–2005PhaseIV-planned

12|Poland.Therealstateofrealestate

Name Location Area (m2) Owner Completion

ZłoteTarasy Śródmieście ZłotaSt. 65,000

AXAREIMJVCBREGlobalInvestors

2007

GaleriaMokotów

Mokotów WołoskaSt. 62,500 Unibail-Rodamco

PhaseI–1999PhaseII–2002PhaseIII-2013

SadybaBestMall

Sadyba PowsińskaSt. 27,000 KlepierreGroup 2000

Klif Wola OkopowaSt. 17,800 AEWEurope 1999

PlacUniiShoppingCenter

Mokotów PuławskaSt. 15,500 InvescoReal

Estate 2013

Source: EY

IntherecentyearsWarsaw’shighstreetlandscapehasrecoveredandgainedimportance,althoughincomparisontootherEuropeancapitalsthereisstillmuchtobedone.Highstreetsarelocatedacrossthecentralquadrantofthecity.TworetailcategoriesdominatethehighstreetsprofileinWarsaw:gastronomyandclothing.Anotherwellrepresentedcategoryishealth&beauty.AlsopresenceofluxuryretailersisnoticeableinsomehighstreetsinWarsaw.NowyŚwiatStreetishistoricalaxisofthecitylinkingPlacTrzechKrzyżytotheOldTownandimportanttouristdestination.Therearenumerousrestaurantsandcafeslocatedonthestreet.PlacTrzechKrzyży,ontheotherhand,isdominatedbyprimeandluxurybrands,stylishrestaurantsandcafes.AnotherimportanthighstreetinWarsawisMarszałkowska.ChmielnaStreetispedestrianwalkwayconnecting

NowyŚwiatandMarszałkowskawhichoverflowwithcafesandrestaurants.TheopeningofthesecondmetrolineisexpectedtoenhancetheattractivenessofNowyŚwiatandŚwiętokrzyska.Primehighstreetrentsforunitsofca.100m2 oscillateinrangeEUR70-100month/ m2. UnitsincentralWarsawvaryheavilyintermsofstandardandaccessibility.ForeignanddomesticretailershavealsoestablishedastrongpresenceonthegroundfloorofbuildingsfacingJerozolimskieAvenueandMarszałkowskaStreet.ThesectionofJanaPawłaIIAvenuetothenorthoftheAtriumBusinessCenterhastraditionallybeenknownasashoppingdestinationandtodaystillfeaturesamixofmoderatelypricedstores.Smallclustersofexpensiveshopsarealsofoundinhotelarcadesandonthegroundfloorsofthemajorofficebuildings.

Poland.Therealstateofrealestate|13

Currently,asaresultoflowsaturationwithretailspaceinWarsawandlowvacancyrate(approximately1,6%),highstreetlocationsaregaininginpopularity.

SeveralmoresmallshoppingcentersarecurrentlyunderconstructionwithintheagglomerationofWarsaw:FerioWawer(12,500m2),FabrykaWołomin(31,000m2)andGaleriaLegionowo(10,500m2).Additionaly,threeexistingschemesareduringextensionworks(AtriumPromenada,WolaParkandFactoryUrsus)andoneisbeingrefurbished(HalaKoszyki).

Amongshoppingcentersintheplanningphase,thereareGaleriaPółnocna(64,000m2),GaleriaWilanów(61,000m2)andNowaStacjaPruszków(25,000m2).

Retailrentratesvarywidelyanddependmainlyonthetypeofafacility,locationandquality.Over2014therentallevelwasstablewithminorupwardtrendinWarsaw’sprimelocations.Theratesforretailunitsinprimelocations,reachlevelsashighasEUR110/m2/month.

AveragerentsforsmallunitsinmodernshoppingcentersinWarsawrangefromEUR40to50/m2/monthdependingonlocation,unit–sizeandtypeofmerchandise.Primeunitsof100–150m2areletatEUR65to90/m2/month(includingrentsinZłoteTarasyandArkadia,whichrepresentthehighestretailrentsinPoland).LargerunitsleaseforapproximatelyEUR15to30/m2/month.Usuallyanchorstoreoperators

occupyingunitsofmorethan1,000m2 paymuchlessthanothers,withaveragerentsfromEUR9to12/m2/monthandevenlower,aroundEUR5to8/m2/monthforhypermarkets.ServicechargesforsmallerspacevaryfromEUR5to9/m2/month.MajortenantsarechargedEUR2to3.5/m2/month.

Standard lease terms

Standardleasetermsforretailspacearesimilartothoseintheofficemarket.However,thetypicalleaselengthforretailspaceinmodernshoppingcentersrangesfrom5to10years.Anchortenantsusuallyprefer10-yearleaseagreementswithextensionoptions,typicallyforanadditional10-yearperiod.

Withtheincreasingsupplyofretailspace,tenantshavebecomemoredemandinganddevelopersseekingattractivetenantsfrequentlyoffernotonlylowerrentalratesbutalsoincentivessuchas:

• rentfreeperiodrangingfrom1–2monthsforsmallershopsandupto6monthsforlargerunits;

• fit-outallowanceatthelevelof EUR50–200/m2forlargeunitsanduptoEUR600/m2foranchortenants(i.e.withminimum10-yearleaseagreements).

14|Poland.Therealstateofrealestate

1.3.Warehousemarket

Poland – General

ThemodernwarehousemarketinPolandbeganitsdevelopmentintheearly1990s,andcurrentlyincludesover8.8millionm2ofwarehousespace.AlthoughinitiallycentralizedwithintheWarsawmetropolitanarea,themodernmarketcannowbesubdividedintosevenregions,eachofwhichhasawelldevelopedwarehousespace.Theseinclude:Warsaw,Poznań,UpperandLowerSilesia,CentralPoland(Łódź,PiotrkówTrybunalski),Tri-City,andKraków.Logisticscentersarelocatedoutsidecitylimitsandofferinggoodaccesstomajorexistingandplannedhighways.

Oneactivitythathascontinuedeventhroughthecrisishasbeenroadandinfrastructureconstruction.ThiscontinuestoboostinvestorinterestinalternativeregionsincludingSzczecin,ZielonaGóra,Lublin,Toruń,BydgoszczandRzeszów,butthesearenowmostlybuilt-to-suitprojects.Intherecentyearssituationinthefinancialmarketshasdampenedaccessibilitytofinancingwhileraisingthecostofcapital,renderingsomeinvestmentsnolongerfeasible.Thiswasevidentinthe“tightening”bywarehousedevelopers,whowerereducingspeculativeprojectsinordertofocusonmanagingcurrentstock.

Afterafewstableyears,2014broughtastrongupturntothemarket.Newsupplyin2014amountedto1.1Mm2whichismorethan14%growthoftotalmodernwarehousestockandalmost3timesmorethaninyear2013.Despitethelargenewsupply,vacancyratesdecreasedsignificantly–fromc.a.10%in2013to5,5%in2014.Rentsremainonstablelevel.

PositivetrendshouldcontinueinfollowingyearsandwillprobablyaffectalsoregionalmarketssuchasRzeszów,Lublin,BydgoszczandOpole.

Poland.Therealstateofrealestate|15

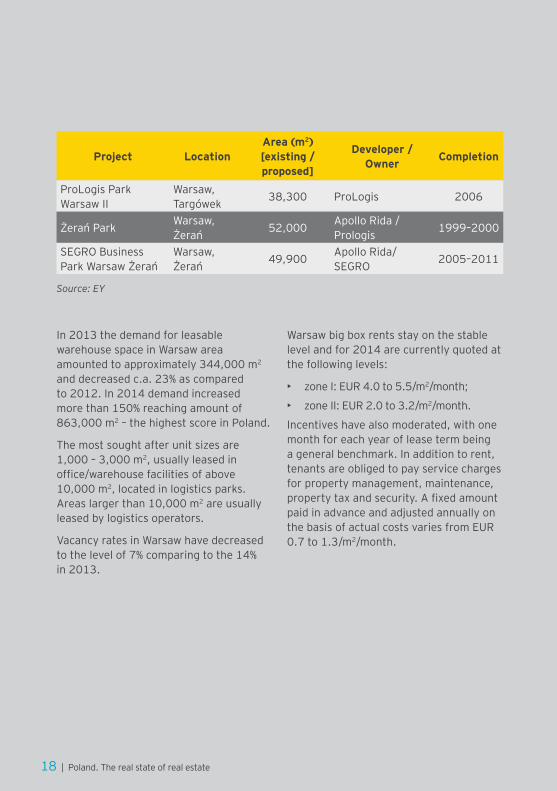

The most active warehouse developers in Poland

Company Country of origin

Major locations (existing and proposed)

AIG/Lincoln USA Gliwice,Łódź,Piaseczno,Stryków,WarsawBiuroInwestycjiKapitałowych Poland Kraków,OżarówMazowiecki,PruszczGdański,

Sosnowiec

Goodman Australia Gdańsk,Gliwice,Kraków,Łódź,Poznań,Toruń,Sosnowiec(underconstruction),Warsaw,Wrocław

MenardDoswell&Company USA Błonie,Czeladź

MetropolGroup Poland Błonie,Warsaw

MLPGroup IsraelBieruń,Lublin(underconstruction),Łódź(underconstruction),Poznań,Pruszków,Tychy,Wrocław(underconstruction)

Panattoni USA

Bielsko-Biała,Błonie,Bydgoszcz,Czeladź,Garwolin,Gdańsk,Gliwice,Kraków,Łódź,Mysłowice,OżarówMazowiecki,Poznań,Pruszków,Robakowo,Rzeszów,Stryków,Święcice,Teresin,Toruń,Warsaw,Wrocław

PointParkProperties UK Mszczonów,Poznań

ProLogis USA

Błonie,Chorzów,DąbrowaGórnicza,Gdańsk,Katowice,Nadarzyn,PiotrkówTrybunalski,Poznań,RawaMazowiecka,RudaŚląska,Sochaczew,Stryków,Szczecin,Teresin,Ujazd,Urzut,Warsaw,Wrocław

SEGRO UK Gdańsk,Gliwice,Łódź,Poznań,Stryków,Tychy,Warsaw,Wrocław

Source: EY

Focus on Warsaw

TheWarsawmodernwarehousestockisdefinedaspropertieswithinapproximately50kmofthecitycenterandissplitintotwozones:

• zoneI:approximately630,000m2 in propertieslocatedwithina15kmradius(Okęcie,Służewiec,Targówek,Żerań),warehousefacilitiesinthiszonehost

mostlypharmaceuticals,cosmeticsandelectronics;

• zoneII:approximately2,150,000m2 inpropertieslocated15to50kmfromthecitycenter(e.g.Piaseczno,OżarówMazowiecki,Błonie,Teresin,Nadarzyn,Pruszków).

AlthoughtheWarsawmetropolitanareacontinuestoaccountforthelargestsingleshareinthePolishmarket(40%

16|Poland.Therealstateofrealestate

oftotalspaceinPoland),thisdominancehasbeensteadilyerodingasdeveloperspushforapresencealongtheemergingmotorwaysoutsidethemajorcities.

ThetotalmodernwarehousespaceintheWarsawMetropolitanArea(ZonesIandII)isestimatedatalmost2.8millionm2 of modernspace.

In2013,around78,000m2ofwarehousespacewascompleted,whichwasover20%decreaseincomparisonto2012.IncontrarytothewholePolishmarket,newsupplyinWarsawin2014was

significantlylowerthaninpreviousyearandamountedto38,000m2.Currentlyabout51,000m2ofwarehousespaceisunderconstructioninWarsawarea.Futuresupplyishardtopinasdevelopersmovetoclientfocusedbuilt-to-suitprojects.

Themajorityofspaceleasedinmoderndistributioncentersislettologisticscompanies,whichsub–letspaceandprovidetheirtenantswithfullservice,includingpackaging,loading,customsclearanceandtransportation.

Examples of class A modern warehouse developments in Warsaw area

Project LocationArea (m2) [existing / proposed]

Developer / Owner Completion

DiamondBusinessPark Piaseczno 57,000 AIGLincoln 2001-2007

EuropolisParkBłonie Błonie 178,000 MenardDoswell/

CAImmo 2006–2012

MilleniumLogisticParkPruszkówII Brwinów 80,000

/302,000 MLPGroup 2007-2014

PanattoniParkOżarów Ożarów 67,800 Panattoni 2009

PanattoniParkPruszków Pruszków 85,300 Panattoni 2007-2009

PlatanPark Warsaw,Ursynów 53,000 PlatanGroup 1998–2001

ProLogisParkBłonie Błonie 153,000 ProLogis 1999–2008

ProLogisParkTeresin Teresin 159,000 ProLogis 2000–2005

ProLogisParkWarsawI

Warsaw,Okęcie 39,000 MenardDoswell/

ProLogis 1995–1997

Poland.Therealstateofrealestate|17

Project LocationArea (m2) [existing / proposed]

Developer / Owner Completion

ProLogisParkWarsawII

Warsaw,Targówek 38,300 ProLogis 2006

ŻerańPark Warsaw,Żerań 52,000 ApolloRida/

Prologis 1999–2000

SEGROBusinessParkWarsawŻerań

Warsaw,Żerań 49,900 ApolloRida/

SEGRO 2005–2011

Source: EY

In2013thedemandforleasablewarehousespaceinWarsawareaamountedtoapproximately344,000m2 anddecreasedc.a.23%ascomparedto2012.In2014demandincreasedmorethan150%reachingamountof863,000m2–thehighestscoreinPoland.

Themostsoughtafterunitsizesare1,000–3,000m2, usually leased in office/warehousefacilitiesofabove10,000m2,locatedinlogisticsparks.Areaslargerthan10,000m2areusuallyleasedbylogisticsoperators.

VacancyratesinWarsawhavedecreasedtothelevelof7%comparingtothe14%in2013.

Warsawbigboxrentsstayonthestablelevelandfor2014arecurrentlyquotedatthefollowinglevels:

• zoneI:EUR4.0to5.5/m2/month;

• zoneII:EUR2.0to3.2/m2/month.

Incentiveshavealsomoderated,withonemonthforeachyearofleasetermbeingageneralbenchmark.Inadditiontorent,tenantsareobligedtopayservicechargesforpropertymanagement,maintenance,propertytaxandsecurity.AfixedamountpaidinadvanceandadjustedannuallyonthebasisofactualcostsvariesfromEUR0.7to1.3/m2/month.

18|Poland.Therealstateofrealestate

1.4.Residentialmarket

Poland – current picture

Year2014wasthebestyearforresidentialmarketsincethefinancialcrisisof2008.Recordlevelofsaleswasobserved.Themarketwasdrivenbymanyfactorswhichcumulateinthatyear,especiallylowinterestrates,newgovernmentprogram“MieszkaniedlaMłodych”andannouncementofnewrestrictionsformortgagegrantingtobeimplementedin2015aswellasstableprices.

ThestockofunitsforsaleonthePolishprimaryresidentialmarkethasbeenrisingseveralyearsinarowuntilthebeginningof2012.AsforQ42012,aggregatedstockofunitsforsaleinsixmainagglomerations(Warsaw,Kraków,Poznań,Wrocław,TricityandŁódź)accountsforapprox.41,000dwellings,whichmeans27%dropincomparisontothesameperiodin2011.Itisaconsequenceofthe“DeveloperAct”enteredintoforceinApril2012.Afterevenworseyear2013(approx.35,000dwellingsattheendoftheyear),2014broughtupturnreaching45,000dwellings.

Onthedemandside,mortgagefinancinghasbeenhamperedbyregulationsbythePolishFinancialSupervisionAuthority(KNF),restrictinggenerallendingtermssuchascreditworthinessandforeigncurrenciesloans,leadingtotheascendanceofPLN-denominatedloans.Ontheotherhand,thedemandisdrivenbyexceptionallylowinterestratesandthenewmortgage-assistancescheme“MieszkaniedlaMłodych”.Howevertheprogramwasintroducedinthebeginningof2014itwillhavemajorimpactinfollowingyears.AlthoughspecifictypeofapartmentsfulfillingMdMprogramparametersareavailableonthemarketthereishugedisproportionregardingpricelimitswithinthecities.

Poland.Therealstateofrealestate|19

Poland - fundamentalsInthelasttwodecadesPolishresidentialmarketgrowthhasbeendrivenbytheoverallgrowthofthecountry’seconomy,mortgagefinancingdevelopmentaswellaspositivedemographictrends.

Oneoftheturningpointsdeterminingthemarketshapewastheboomperiodof2004-2007,triggeredbytheEUaccessionandresultinginflowofinvestors,mortgagefinancingreleaseandhistoricallylowinterestrates.Theboomreshapedthestateoftheresidentialmarket,pumpingupthepricesofhousingandofresidentialland.

Despitethecontinuingneedforadequatehousing,demandstillreliesonaffordability,andtocapoffafewgoodyearsofstrongpricegrowth,2007markedanotherturningpoint.Moderationinlate2007ledtostagnationin2008,whichultimatelygavewaytopricedecreasesin2009.

AccordingtodatapublishedbytheCentralStatisticalOffice,over143thousandunitshavebeendeliveredin2014(1.2%lesscomparedtothesameperiodof2013),outofwhich58,8thousand(41%)wereconstructedbydevelopers,and76,6thousand(53%)byindividuals.Theremainingsupplywasdeliveredbyhousingcooperativesandmunicipalities,whoseshareremainsmarginal.Althoughnumberofdelivereddwellingsin2014wasabitlowerthaninpreviousyear,therewasasignificantincreaseinbuildingsstarted(16%)andissuedbuildingpermissions(13%).

ThePolishresidentialmarketispresentlythelargestinCentralandEasternEurope,however,itstilllagsbehindwesternEUmembersintermsofquality,ageofstockandlevelofmarketsaturation.

Moreover,statisticalindicators,suchasnumberofresidentialunitsper1,000inhabitants,usablefloorareaperoneinhabitantandperaverageresidentialunit,arebelowtheEuropeanaverage.

AmajorobstacleconstraininghousingsupplyinPolandismainlyadministration-drivenandconsistsofthelimitednumberofzoningplans,coveringbelow30%ofcountry’sarea.Ineachsinglecase,lackofzoningplanresultsinatime-consumingadministrativeprocedure,whichtakesfromafewmonthsuptoevenayear.Itisnecessarytoobtainzoningdecision(WarunkiZabudowy),beforethebuildingpermitcanbeappliedfor.

Focus on Warsaw

Warsaw’sresidentialmarketremainsthemostdevelopedinPoland:demandisdrivenmainlybyin-migration,thehighestincomelevelinPolandandthelowestunemploymentrate.EmploymentandeducationpossibilitiesinWarsawareamagnetforyoungpeoplefromotherregionsofPoland,resultinginthedominanceofmultifamilydevelopmentsintheWarsawresidentialmarket.Morethan10%ofPolishresidentialsupplyisprovidedonWarsawmarket.Theshareofnewhousingunitsinsingle-familydevelopmentsbuiltinWarsawremainsunder1%.Currentlythemarketisdeterminedbyrisingvolume

20|Poland.Therealstateofrealestate

oftransactions,resultingmainlyfromlowinterestrates,savingswithdrawalandreinvestmentaswellasfinancingrestrictionswhichstartedfrom2014andwillbetightenedinfollowingyears(sincethebeginningof2015owncontributionshallbeatleast10%anditwillbeincreasedby5percentagepointsin2016and2017).

Aftertherecordyearof2001,completedunitsinWarsawfluctuatedbetween10,000and15,000p.a.forseveralyears.Followingtheboomperiod,unitcompletionsincreasedto19,049andto19,482,for2008and2009,respectively.However,in2009unitstartswerestarklycurtailed,resultinginthedeliveryofonly12,462dwellingsin2010and9,408in2011.Inthebeginningof2012thesituationontheresidentialmarketwasmainlyinfluencedbyaveryhighsupplyofdwellingsreleasedinJanuary-Aprilperiod.Thiswasmainlydrivenbyintroductionof“DeveloperAct”intheendofApril.Theyear2013showedamoderatedeveloper’soutput:accordingtothedataprovidedbytheCentralStatisticalOffice,nearly13,200apartmentswerecompleted.

Accordingtomarketdata,theprimarymarketinWarsawinQ42014offeredover18,000unitsforsale,outofwhich3,500havebeenalreadydelivered.Warsawremainedthemostexpensiveresidentialmarketwithanaverageapartments’transactionpriceofapprox.7,300PLN/m2.

Buyerspayonaverage7.5%lessthaninitialprice.Thismainlyconcernsthesecondarymarketandisalsoduetobetteralignmentofdemandandsupply,aswellaslargenumberofcompletednewresidentialinvestments.AccordingtoNationalBankofPolandtheaverageaskingpriceofapartmentsontheprimarymarketinWarsawiscurrentlyatthelevelof7,900PLN/m2,whilethehighestaveragepriceswereobservedinŚródmieście(PLN11,400/m2)andthelowestinBiałołękadistrict(belowPLN6,000/m2).ApartfromŚródmieście,themostexpensivedistrictsinWarsawremainMokotów,Ochota,Bielany,UrsynówandŻoliborz.

Similartotherestofthecountry,demandonWarsawmarketisontheupturnduetolowinterestratesandgovernmentsupportbutthereisathreatofaslowdownaftermortgagefinancingregulationsthatwillbetightenedgraduallyinfollowingyears.

Poland.Therealstateofrealestate|21

1.5.InvestmentmarketInitially,developmentofPolishcommercialinvestmentmarkettrailedbehindtherestoftherealestatemarket.Investorswerefewandyieldswereinthedoubledigits.Itwasnotuntil2004andtheadventofEUmembershipthatthesituationimproved.ThatyearmarkedthebeginningofanintensivefouryearperiodofforeigninvestmentinthePolishmarket.Overthisperiod,thevolumeoftransactionsaveragedjustunderEUR4billionayear;afarcryfrom2001whenforeigninvestmentsweremoreorlesslimitedtotheWarsawofficemarket.Furthermore,theearlyyearssawthecommercialinvestmentmarketplaguedwithalackofavailableinvestmentschemes,ormismanagedandoverrentedpropertieswithhighvacancyrates.Theincreasingnumberoftransactionshasnotonlystabilizedinvestments,butcompletelychangedthestructureofyields(downward)andprices(upward).

Thequestionforinvestorsgoingforwardis,whetherPolandwillbouncebackfromthe2008and2009droporwhetherthefundamentalsofpricinghavechangedforever.Earlyindicationssuggestsustainedcomeback.

WarsawremainsanimportanttransactionmarketinPolandperceivedbymanyinvestorsascore,butsmallerscalepropertiesinsecondarytownscontinuetogainground.In2014thetotalvolumeofinvestmenttransactionsinPolandamountedtoapproximatelyEUR3.1billion.Itis6%lessthanin2013butitisstillthesecondbestvaluesince2006whenhighestvolumeeverwereachieved.Themajorinvestmentactivitywasobservedinwarehouseandofficesectors.

Transactionvolumeslooksettorise,supportedinlargepartbyinternationalinvestment,butalsoPolishcapitalseemstocatchup.In2014aPolish

22|Poland.Therealstateofrealestate

closed-endinvestmentfundacquiredaEUR140mlnwarehouseportfolio.ThetransactionwasoneofthebiggestmadebyPolishinvestor.

Major investors

Themainplayersontherealestateinvestmentmarketareforeigninvestmentfunds,andtoalimitedextentinsurancecompanies,banksandwealthyforeignindividuals.

ThePolishActonInvestmentFundsallowsPolishoperatedandregisteredfundstoinvestinrealestateorincompaniesholdingrealestateassetswithoutanyspecificlimitations;asinthecaseofArka(BZWBK),BPH,KBCandSkarbiec.

ThemajorityofrealestateinvestmentfundsoperatinginPolandareforeignfundstreatingtheirpropertiesasinvestmentsinaccordancewiththelegal

regulationsoftheircountriesoforigin.TheirsubsidiariesinPolandworkunderthestandardregulationsoftheCodeofCommercialCompaniesandthusinvestmentsinrealestatearesubjectonlytotheActonPurchaseofRealEstatebyForeigners.Priorto2005theinvestmentmarketwasdominatedbyGerman,American,andAustrianplayers.AfterEUaccessionPolandwitnessedaninitialinfluxofIrishinvestors,lateraccompaniedbySpanishandBritishinvestors.By2009thetrendseemedtohavereversed;GermanfundshaveemergedwellintactwhiletheIrish,andevenmoresotheSpanishinvestors,appeartobehamperedbytheirownmarketsbackhome.

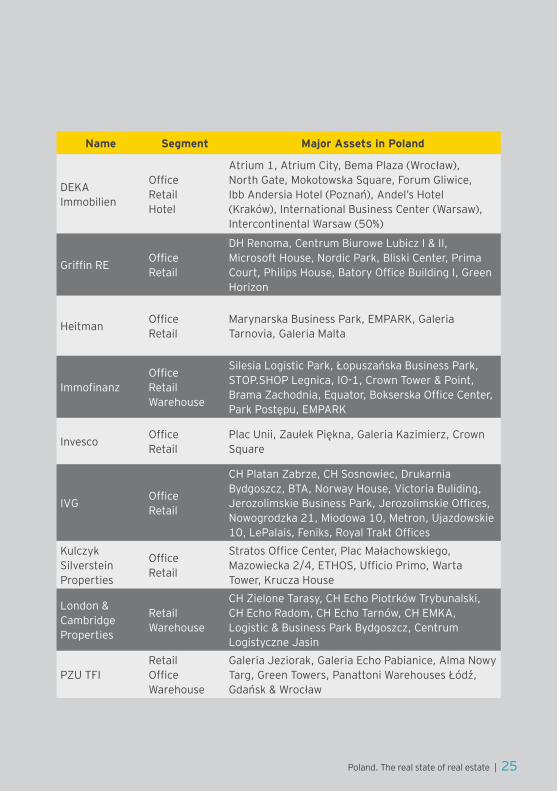

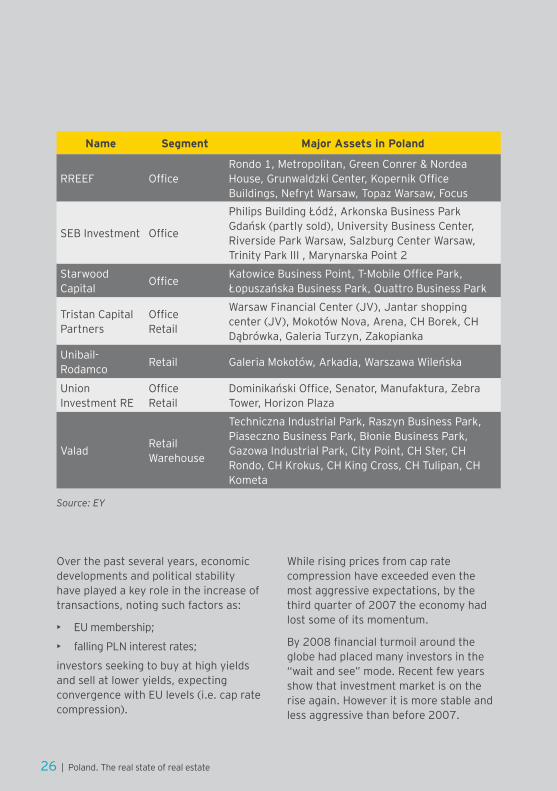

ThelargestrealestatefundsactiveinPolandincludeBlackstone,CAImmo,IVG,DEKA,CBREGlobalInvestors,GriffinandRREEF.

0

1000

2000

3000

4000

5000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

in m

ln E

UR

Total investment volume in all sectors (office, retail, warehouse) 2000–2014

Poland.Therealstateofrealestate|23

Major real estate funds investing in Poland

Name Segment Major Assets in Poland

AEWCapitalOfficeWarehouseRetail

GoodPointPuławska,WarehousesinGliwice,KlifWarsaw,KlifTri-City,AtriumTowerinWarsaw

AIBPoloniaPropertyFund/PeaksideCapital

Office Retail Warehouse

AtriumPlazaWarsaw,AtriumCentrum,WiśniowyBusinessPark,FashionHouseOutletsinSosnowiec,GdańskandWarsaw,DiamondBusinessPark,WarsawDistributionCentre

Allianz RE Office Retail

SilesiaCityCenter,WarsawFinancialCenter,PlatiniumBusinessPark

AtriumEuropeanRealEstate

RetailRedutaShoppingCenter,PromenadaShoppingCenter,GaleriaDominikańska,FocusParkinBydgoszcz,LublinFelicity

AvivaCentralEuropeanPropertyFund

Office Retail

Irydionofficebuilding,Shoppingmalls(FocusMall)inPiotrkówTrybunalski,ZielonaGóra,Rybnik

AxaGroup Retail ZłoteTarasyShoppingCenter-partialinterest

Azora Office

AquariusBusinessHouseinWroclaw,CristalPark,MokotówPlaza,HarmonyOfficeCenterComplexinWarsaw,GreenOfficeComplexandAvatarinKraków(JV)

BlackRock Retail CHKarolinkainOpole,PogoriainDąbrowaGórnicza

Blackstone Retail Warehouse

Shoppingmalls:TwierdzaKłodzko,GaleriaLeszno,MagnoliaPark(Wrocław),TwierdzaZamość(Zamość),WzorcowniaWłocławek,GaleriaPestka(Poznań),GaleriaTęcza(Kalisz),warehouseportfolioinŁódź,Łazy,Błonie,Czeladź,Gliwice,Kraków,Piaseczno

CAImmo OfficeWarehouse

PoleczkiBusinessPark,SaskiPoint,SaskiCrescent,SiennaCenter,EuropolisParkPolandCentral,EuropolisParkBłonie

CBREGlobalInvestors

OfficeWarehouseRetail

WarsawDistributionCentre,ManhattanBusiness&DistributionCentre,IdeaIdea,CHSarniStok,CHOgrody,ZłoteTarasy-partialinterest,GaleriaMazovia,WarsSawaJunior,KingCrossPraga,ProstaOfficeCenter,TrinityOfficePark

24|Poland.Therealstateofrealestate

Name Segment Major Assets in Poland

DEKA Immobilien

Office Retail Hotel

Atrium1,AtriumCity,BemaPlaza(Wrocław),NorthGate,MokotowskaSquare,ForumGliwice,IbbAndersiaHotel(Poznań),Andel’sHotel(Kraków),InternationalBusinessCenter(Warsaw),IntercontinentalWarsaw(50%)

GriffinRE Office Retail

DHRenoma,CentrumBiuroweLubiczI&II,MicrosoftHouse,NordicPark,BliskiCenter,PrimaCourt,PhilipsHouse,BatoryOfficeBuildingI,GreenHorizon

Heitman Office Retail

MarynarskaBusinessPark,EMPARK,GaleriaTarnovia,GaleriaMalta

ImmofinanzOffice Retail Warehouse

SilesiaLogisticPark,ŁopuszańskaBusinessPark,STOP.SHOPLegnica,IO-1,CrownTower&Point,BramaZachodnia,Equator,BokserskaOfficeCenter,ParkPostępu,EMPARK

Invesco Office Retail

PlacUnii,ZaułekPiękna,GaleriaKazimierz,CrownSquare

IVG Office Retail

CHPlatanZabrze,CHSosnowiec,DrukarniaBydgoszcz,BTA,NorwayHouse,VictoriaBuliding,JerozolimskieBusinessPark,JerozolimskieOffices,Nowogrodzka21,Miodowa10,Metron,Ujazdowskie10,LePalais,Feniks,RoyalTraktOffices

KulczykSilversteinProperties

Office Retail

StratosOfficeCenter,PlacMałachowskiego,Mazowiecka2/4,ETHOS,UfficioPrimo,WartaTower,KruczaHouse

London&CambridgeProperties

Retail Warehouse

CHZieloneTarasy,CHEchoPiotrkówTrybunalski,CHEchoRadom,CHEchoTarnów,CHEMKA,Logistic&BusinessParkBydgoszcz,CentrumLogistyczneJasin

PZUTFIRetail OfficeWarehouse

GaleriaJeziorak,GaleriaEchoPabianice,AlmaNowyTarg,GreenTowers,PanattoniWarehousesŁódź,Gdańsk&Wrocław

Poland.Therealstateofrealestate|25

Name Segment Major Assets in Poland

RREEF OfficeRondo1,Metropolitan,GreenConrer&NordeaHouse,GrunwaldzkiCenter,KopernikOfficeBuildings,NefrytWarsaw,TopazWarsaw,Focus

SEBInvestment Office

PhilipsBuildingŁódź,ArkonskaBusinessParkGdańsk(partlysold),UniversityBusinessCenter,RiversideParkWarsaw,SalzburgCenterWarsaw,TrinityParkIII,MarynarskaPoint2

StarwoodCapital Office KatowiceBusinessPoint,T-MobileOfficePark,

ŁopuszańskaBusinessPark,QuattroBusinessPark

TristanCapitalPartners

Office Retail

WarsawFinancialCenter(JV),Jantarshoppingcenter(JV),MokotówNova,Arena,CHBorek,CHDąbrówka,GaleriaTurzyn,Zakopianka

Unibail-Rodamco Retail GaleriaMokotów,Arkadia,WarszawaWileńska

Union InvestmentRE

Office Retail

DominikańskiOffice,Senator,Manufaktura,ZebraTower,HorizonPlaza

Valad Retail Warehouse

TechnicznaIndustrialPark,RaszynBusinessPark,PiasecznoBusinessPark,BłonieBusinessPark,GazowaIndustrialPark,CityPoint,CHSter,CHRondo,CHKrokus,CHKingCross,CHTulipan,CHKometa

Source: EY

Overthepastseveralyears,economicdevelopmentsandpoliticalstabilityhaveplayedakeyroleintheincreaseoftransactions,notingsuchfactorsas:

• EUmembership;

• fallingPLNinterestrates;

investorsseekingtobuyathighyieldsandsellatloweryields,expectingconvergencewithEUlevels(i.e.capratecompression).

Whilerisingpricesfromcapratecompressionhaveexceededeventhemostaggressiveexpectations,bythethirdquarterof2007theeconomyhadlostsomeofitsmomentum.

By2008financialturmoilaroundtheglobehadplacedmanyinvestorsinthe“waitandsee”mode.Recentfewyearsshowthatinvestmentmarketisontheriseagain.Howeveritismorestableandlessaggressivethanbefore2007.

26|Poland.Therealstateofrealestate

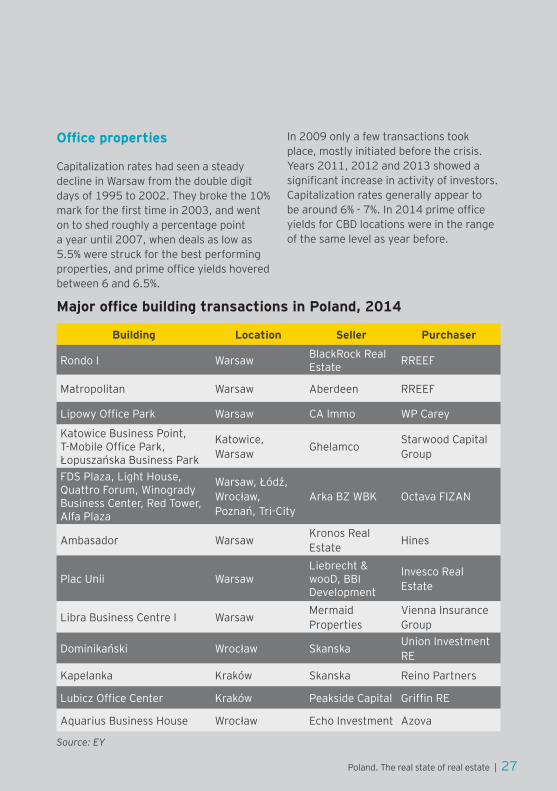

Office properties

CapitalizationrateshadseenasteadydeclineinWarsawfromthedoubledigitdaysof1995to2002.Theybrokethe10%markforthefirsttimein2003,andwentontoshedroughlyapercentagepointayearuntil2007,whendealsaslowas5.5%werestruckforthebestperformingproperties,andprimeofficeyieldshoveredbetween6and6.5%.

In2009onlyafewtransactionstookplace,mostlyinitiatedbeforethecrisis.Years2011,2012and2013showedasignificantincreaseinactivityofinvestors.Capitalizationratesgenerallyappeartobearound6%-7%.In2014primeofficeyieldsforCBDlocationswereintherangeofthesamelevelasyearbefore.

Major office building transactions in Poland, 2014

Building Location Seller Purchaser

Rondo I Warsaw BlackRockRealEstate RREEF

Matropolitan Warsaw Aberdeen RREEF

LipowyOfficePark Warsaw CAImmo WPCarey

KatowiceBusinessPoint,T-MobileOfficePark,ŁopuszańskaBusinessPark

Katowice,Warsaw Ghelamco StarwoodCapital

Group

FDSPlaza,LightHouse,QuattroForum,WinogradyBusinessCenter,RedTower,Alfa Plaza

Warsaw,Łódź,Wrocław,Poznań,Tri-City

ArkaBZWBK OctavaFIZAN

Ambasador Warsaw KronosRealEstate Hines

PlacUnii WarsawLiebrecht&wooD,BBIDevelopment

InvescoRealEstate

LibraBusinessCentreI Warsaw MermaidProperties

ViennaInsuranceGroup

Dominikański Wrocław Skanska UnionInvestmentRE

Kapelanka Kraków Skanska ReinoPartners

LubiczOfficeCenter Kraków PeaksideCapital GriffinRE

AquariusBusinessHouse Wrocław EchoInvestment Azova

Source: EY

Poland.Therealstateofrealestate|27

Intermsofregionalcities,investorsaremorecautiousandprefertobuyA-classproperties,wellleasedandcentrallylocatedinlargecities.Whilein2011noinvestmenttransactiontookplace,in2012and2013severaltransactionsintheregionalcitiesweremade.Year2014broughtsignificantincrease,officeinvestmentvolumeinregionalcitieswasdoubledcomparingto2013,reachingEUR400million.

Retail properties

Significantinvestmentsintheretailmarketdidnotstartuntil2001.ThefirstmajortransactionswereinvestmentsbyRodamcoinGaleriaMokotówandinZłoteTarasythattookplacein2003,withcapitalizationratesatthelevelof9–10.5%.

SincethattimenearlyeverysignificantpropertyinWarsawandotherPolishcities

hasbeenthesubjectofatransaction.By2005capitalizationrateswerepusheddownwardtoroughly8%andcontinuedthisdownwardtrendthroughQ3,2008whentheyrangedbetween5.7%and6.5%.Duetothecrisis,thecapitalizationrateshasincreasedbyapproximately1–1.5%.

Afterveryintensiveyear2013,year2014appearstobepullbackforthemarket.Volumein2014was2.5timeslessthaninpreviousyear,butprognosisarethatthisisonlytemporaryslowdownandyear2015shallbecomparableto2013.In2014thelargestretaildealsincludedPoznańCityCenter,FocusMallBydgoszczandGaleriaMazoviainPłock.Themajormodernretailtransactionsarepresentedinthetablebelow.Capitalizationratesgenerallyappeartobearound7.5-8%.In2014primeretailyieldsinPolandwereintherangeof5.75-7%.

Major modern retail transactions, 2014

Building Seller Purchaser

PoznańCityCenter Trigranit,EuropaCapital,PolskieKolejePaństwoweS.A. ResolutionProperty,ECE

GaleriaMazovia Lewandpol CBREEuropeanShoppingCentreFund

FocusMallBydgoszcz AvivaInvestors AtriumEuropeanRealEstate

PlacUnii Liebrecht&wood,BBIDevelopment InvescoRealEstate

GaleriaPiła RankProgress ImmofinanzGroup

GaleriaOstrowiec USS FirstPropertyGroupNovaPark(50%) CaelumDevelopment Futureal

Source: EY

28|Poland.Therealstateofrealestate

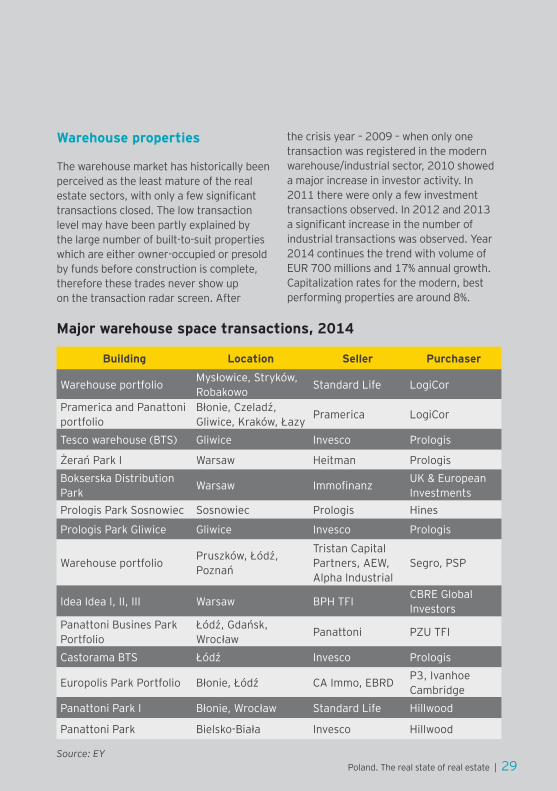

Warehouse properties

Thewarehousemarkethashistoricallybeenperceivedastheleastmatureoftherealestatesectors,withonlyafewsignificanttransactionsclosed.Thelowtransactionlevelmayhavebeenpartlyexplainedbythelargenumberofbuilt-to-suitpropertieswhichareeitherowner-occupiedorpresoldbyfundsbeforeconstructioniscomplete,thereforethesetradesnevershowuponthetransactionradarscreen.After

thecrisisyear–2009–whenonlyonetransactionwasregisteredinthemodernwarehouse/industrialsector,2010showedamajorincreaseininvestoractivity.In2011therewereonlyafewinvestmenttransactionsobserved.In2012and2013asignificantincreaseinthenumberofindustrialtransactionswasobserved.Year2014continuesthetrendwithvolumeofEUR700millionsand17%annualgrowth.Capitalizationratesforthemodern,bestperformingpropertiesarearound8%.

Major warehouse space transactions, 2014

Building Location Seller Purchaser

Warehouseportfolio Mysłowice,Stryków,Robakowo StandardLife LogiCor

PramericaandPanattoniportfolio

Błonie,Czeladź,Gliwice,Kraków,Łazy Pramerica LogiCor

Tescowarehouse(BTS) Gliwice Invesco Prologis

ŻerańParkI Warsaw Heitman PrologisBokserskaDistributionPark Warsaw Immofinanz UK&European

InvestmentsPrologisParkSosnowiec Sosnowiec Prologis Hines

PrologisParkGliwice Gliwice Invesco Prologis

Warehouseportfolio Pruszków,Łódź,Poznań

TristanCapitalPartners,AEW,AlphaIndustrial

Segro,PSP

Idea Idea I, II, III Warsaw BPHTFI CBREGlobalInvestors

PanattoniBusinesParkPortfolio

Łódź,Gdańsk,Wrocław Panattoni PZUTFI

CastoramaBTS Łódź Invesco Prologis

EuropolisParkPortfolio Błonie,Łódź CAImmo,EBRD P3,IvanhoeCambridge

PanattoniParkI Błonie,Wrocław StandardLife Hillwood

PanattoniPark Bielsko-Biała Invesco Hillwood

Source: EYPoland.Therealstateofrealestate|29

1.6.KeycitiesinPoland

WARSAWPopulation 1,729,000

Unemployment 4.3%

Majorindustries Tradeandservices

Majorcompanies Accenture,BankPekao,BGŻ,mBank,BritishAmericanTobacco,Budimex,Bumar,Citibank,Coca-Cola,ColgatePalmolive,Deloitte,EY,FranceTelecom,GeneralMotors,GrupaŻywiec,GTC,HutaArcelorWarszawa,IBM,ING,KompaniaPiwowarska,KPMG,KraftFoodsPolska,MostostalExport,Nestle,PGNiG,PKO,BP,PLLLOT,Polkomtel,Procter&Gamble,PwC,PZU,RBS,RWE,SamsungElectronicsPolska,Shell,Skanska,Strabag,Unilever

Office sector

Rental level (m2/month) EUR21–24(class–Aspace)EUR11–13(class–Bspace)

TotalofficeStock 4,4millionm2ofmodernspace

Currentsupply(selectedbuildings)

AdgarPlaza,Ambassador,Atrium1,AtriumComplex,BusinessGarden,CatalinaOfficeCenter,CristalPark,DeloitteHouse,EMPARK,Equator,Eurocentrum,Focus,GdańskiBusinessCentre,HarmonyOfficeCenter,HorizonPlaza,FeniksOfficeBuilding,Focus,IO-1,JerozolimskieBusinessPark,KonstruktorskaBusinessCenter,KopernikOfficeBuidlings,LipowyOfficePark,Lumen,MarynarskaBusinessPark,MarynarskaPoint,Metropolitan,MilenniumPlaza,MokotówBusinessPark,MokotówNova,MokotówPlaza,Nefryt,NorthGate,OkęcieBusinessPark,ParkPostępu,PlatiniumBusinessPark,PoleczkiBusinessPark,PlacUnii,Rondo1,SaskiCrescent,SaskiPoint,Senator,Skylight,TrinityPark,TulipanHouse,WarsawFinancialCenter,WarsawTradeTower,WilanówOfficePark,WiśniowyBusinessPark,WolfMarszałkowska,ZebraTower

30|Poland.Therealstateofrealestate

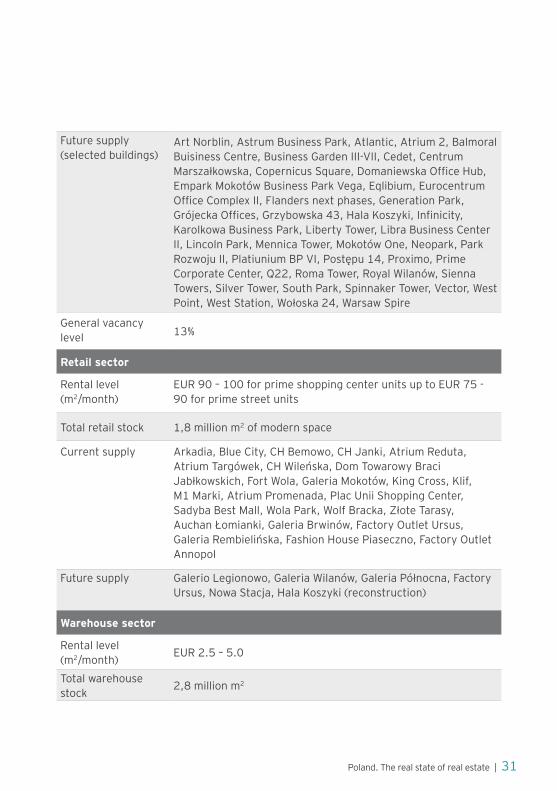

Futuresupply(selectedbuildings)

ArtNorblin,AstrumBusinessPark,Atlantic,Atrium2,BalmoralBuisinessCentre,BusinessGardenIII-VII,Cedet,CentrumMarszałkowska,CopernicusSquare,DomaniewskaOfficeHub,EmparkMokotówBusinessParkVega,Eqlibium,EurocentrumOfficeComplexII,Flandersnextphases,GenerationPark,GrójeckaOffices,Grzybowska43,HalaKoszyki,Infinicity,KarolkowaBusinessPark,LibertyTower,LibraBusinessCenterII,LincolnPark,MennicaTower,MokotówOne,Neopark,ParkRozwojuII,PlatiuniumBPVI,Postępu14,Proximo,PrimeCorporateCenter,Q22,RomaTower,RoyalWilanów,SiennaTowers,SilverTower,SouthPark,SpinnakerTower,Vector,WestPoint,WestStation,Wołoska24,WarsawSpire

Generalvacancylevel 13%

Retail sector

Rental level (m2/month)

EUR90–100forprimeshoppingcenterunitsuptoEUR75-90forprimestreetunits

Totalretailstock 1,8millionm2ofmodernspace

Currentsupply Arkadia,BlueCity,CHBemowo,CHJanki,AtriumReduta,AtriumTargówek,CHWileńska,DomTowarowyBraciJabłkowskich,FortWola,GaleriaMokotów,KingCross,Klif,M1Marki,AtriumPromenada,PlacUniiShoppingCenter,SadybaBestMall,WolaPark,WolfBracka,ZłoteTarasy,AuchanŁomianki,GaleriaBrwinów,FactoryOutletUrsus,GaleriaRembielińska,FashionHousePiaseczno,FactoryOutletAnnopol

Futuresupply GalerioLegionowo,GaleriaWilanów,GaleriaPółnocna,FactoryUrsus,NowaStacja,HalaKoszyki(reconstruction)

Warehouse sector

Rental level (m2/month) EUR2.5–5.0

Totalwarehousestock 2,8millionm2

Poland.Therealstateofrealestate|31

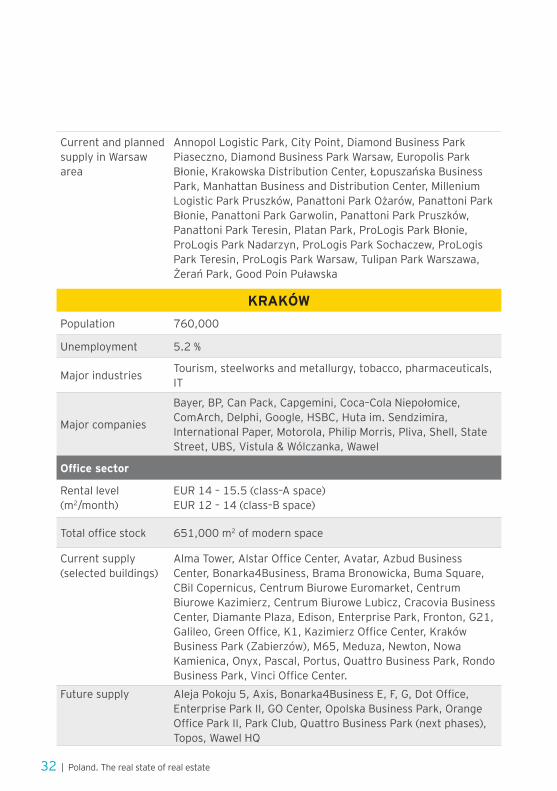

CurrentandplannedsupplyinWarsawarea

AnnopolLogisticPark,CityPoint,DiamondBusinessParkPiaseczno,DiamondBusinessParkWarsaw,EuropolisParkBłonie,KrakowskaDistributionCenter,ŁopuszańskaBusinessPark,ManhattanBusinessandDistributionCenter,MilleniumLogisticParkPruszków,PanattoniParkOżarów,PanattoniParkBłonie,PanattoniParkGarwolin,PanattoniParkPruszków,PanattoniParkTeresin,PlatanPark,ProLogisParkBłonie,ProLogisParkNadarzyn,ProLogisParkSochaczew,ProLogisParkTeresin,ProLogisParkWarsaw,TulipanParkWarszawa,ŻerańPark,GoodPoinPuławska

KRAKÓWPopulation 760,000

Unemployment 5.2%

Majorindustries Tourism,steelworksandmetallurgy,tobacco,pharmaceuticals,IT

Majorcompanies

Bayer,BP,CanPack,Capgemini,Coca–ColaNiepołomice,ComArch,Delphi,Google,HSBC,Hutaim.Sendzimira,InternationalPaper,Motorola,PhilipMorris,Pliva,Shell,StateStreet,UBS,Vistula&Wólczanka,Wawel

Office sector

Rental level (m2/month)

EUR14–15.5(class–Aspace) EUR12–14(class–Bspace)

Totalofficestock 651,000m2ofmodernspace

Currentsupply(selectedbuildings)

AlmaTower,AlstarOfficeCenter,Avatar,AzbudBusinessCenter,Bonarka4Business,BramaBronowicka,BumaSquare,CBiICopernicus,CentrumBiuroweEuromarket,CentrumBiuroweKazimierz,CentrumBiuroweLubicz,CracoviaBusinessCenter,DiamantePlaza,Edison,EnterprisePark,Fronton,G21,Galileo,GreenOffice,K1,KazimierzOfficeCenter,KrakówBusinessPark(Zabierzów),M65,Meduza,Newton,NowaKamienica,Onyx,Pascal,Portus,QuattroBusinessPark,RondoBusinessPark,VinciOfficeCenter.

Futuresupply AlejaPokoju5,Axis,Bonarka4BusinessE,F,G,DotOffice,EnterpriseParkII,GOCenter,OpolskaBusinessPark,OrangeOfficeParkII,ParkClub,QuattroBusinessPark(nextphases),Topos,WawelHQ

32|Poland.Therealstateofrealestate

Generalvacancylevel 6%

Retail sector

Rental level (m2/month)

EUR65-75forprimeshoppingcenterunits EUR50–80forprimestreetunits

Totalretailstock 750,000m2ofmodernspace

Currentsupply GaleriaKrakowska,GaleriaKazimierz,CHKrokus,CHZakopianka,M1Kraków,IKEA,KrakówPlaza,CHCzyżyny,SolvayPark,FuturaPark,CHDekadaPark,Castorama,CHWielicka,Bonarka,GaleriaBronowice

Futuresupply SerenadaShoppingCenter

Warehouse sector

Rental level (m2/month) EUR3.75-4.50

Totalwarehousestock 189,000m2

Currentandplannedsupply

LogisticCenterKrakówI,II,III,KrakówAirportLogisticsCentre,MARRBusinessPark,MKLogisticsPark,PanattoniParkKraków

POZNAŃPopulation 547,000

Unemployment 3.2%

Majorindustries Foodprocessing,electrotechnical,chemical,automotive,retail,services(includingfinanceandbanking),constructionindustry,locationofmajortradefairsinPoland

Majorcompanies AluplastAustria,Beiersdorf,Bridgestone,Carlsberg,CPCInternational,Enea,FranklinTempletonInvestments,GlaxoSmithKline,IKEA,KompaniaPiwowarska,LorensBahlsen,MAN,MiędzynarodoweTargiPoznańskie,Nestle,Volkswagen,Wrigley,Wyborowa

Poland.Therealstateofrealestate|33

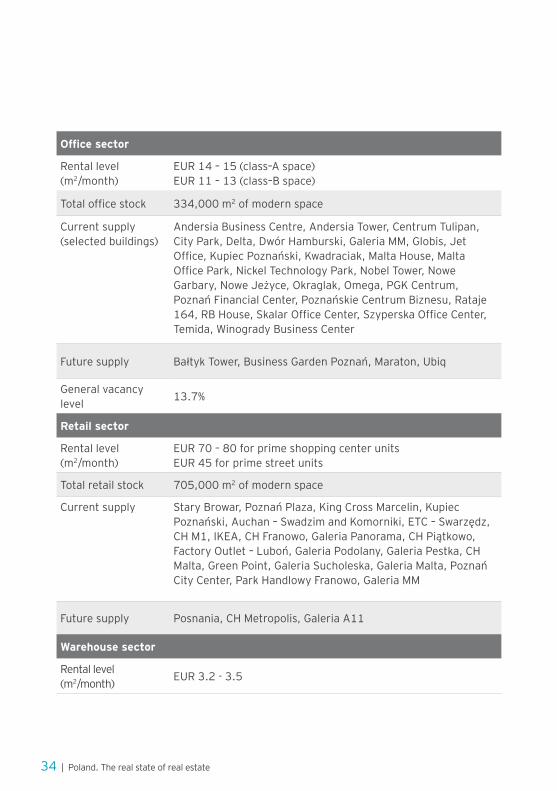

Office sector

Rental level (m2/month)

EUR14–15(class–Aspace) EUR11–13(class–Bspace)

Totalofficestock 334,000m2ofmodernspace

Currentsupply(selectedbuildings)

AndersiaBusinessCentre,AndersiaTower,CentrumTulipan,CityPark,Delta,DwórHamburski,GaleriaMM,Globis,JetOffice,KupiecPoznański,Kwadraciak,MaltaHouse,MaltaOfficePark,NickelTechnologyPark,NobelTower,NoweGarbary,NoweJeżyce,Okraglak,Omega,PGKCentrum,PoznańFinancialCenter,PoznańskieCentrumBiznesu,Rataje164,RBHouse,SkalarOfficeCenter,SzyperskaOfficeCenter,Temida,WinogradyBusinessCenter

Futuresupply BałtykTower,BusinessGardenPoznań,Maraton,Ubiq

Generalvacancylevel 13.7%

Retail sector

Rental level (m2/month)

EUR70–80forprimeshoppingcenterunits EUR45forprimestreetunits

Totalretailstock 705,000m2ofmodernspace

Currentsupply StaryBrowar,PoznańPlaza,KingCrossMarcelin,KupiecPoznański,Auchan–SwadzimandKomorniki,ETC–Swarzędz,CHM1,IKEA,CHFranowo,GaleriaPanorama,CHPiątkowo,FactoryOutlet–Luboń,GaleriaPodolany,GaleriaPestka,CHMalta,GreenPoint,GaleriaSucholeska,GaleriaMalta,PoznańCityCenter,ParkHandlowyFranowo,GaleriaMM

Futuresupply Posnania,CHMetropolis,GaleriaA11

Warehouse sector

Rental level (m2/month) EUR3.2-3.5

34|Poland.Therealstateofrealestate

Totalwarehousestock 1,023,000m2

Currentandplannedsupply

CLIPPoznań,DoxlerBusinessPark,MillenniumLogisticParkPoznań,PanattoniPoznańI,II,III,PanattoniRobakowo,ParkMagazynowyLogit,PointParkPoznań,ProLogisParkPoznańI,II,III,ProLogisParkWrześnia,TulipanParkPoznańI,II,SegroLogisticParkPoznań,AmazonWarehouse

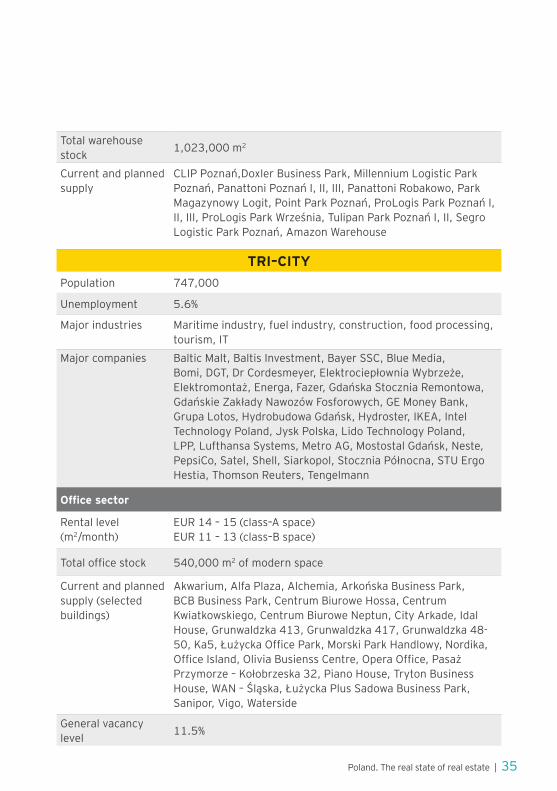

TRI–CITYPopulation 747,000

Unemployment 5.6%

Majorindustries Maritimeindustry,fuelindustry,construction,foodprocessing,tourism,IT

Majorcompanies BalticMalt,BaltisInvestment,BayerSSC,BlueMedia,Bomi,DGT,DrCordesmeyer,ElektrociepłowniaWybrzeże,Elektromontaż,Energa,Fazer,GdańskaStoczniaRemontowa,GdańskieZakładyNawozówFosforowych,GEMoneyBank,GrupaLotos,HydrobudowaGdańsk,Hydroster,IKEA,IntelTechnologyPoland,JyskPolska,LidoTechnologyPoland,LPP,LufthansaSystems,MetroAG,MostostalGdańsk,Neste,PepsiCo,Satel,Shell,Siarkopol,StoczniaPółnocna,STUErgoHestia,ThomsonReuters,Tengelmann

Office sector

Rental level (m2/month)

EUR14–15(class–Aspace) EUR11–13(class–Bspace)

Totalofficestock 540,000m2ofmodernspace

Currentandplannedsupply(selectedbuildings)

Akwarium,AlfaPlaza,Alchemia,ArkońskaBusinessPark,BCBBusinessPark,CentrumBiuroweHossa,CentrumKwiatkowskiego,CentrumBiuroweNeptun,CityArkade,IdalHouse,Grunwaldzka413,Grunwaldzka417,Grunwaldzka48-50,Ka5,ŁużyckaOfficePark,MorskiParkHandlowy,Nordika,OfficeIsland,OliviaBusienssCentre,OperaOffice,PasażPrzymorze–Kołobrzeska32,PianoHouse,TrytonBusinessHouse,WAN–Śląska,ŁużyckaPlusSadowaBusinessPark,Sanipor,Vigo,Waterside

Generalvacancylevel 11.5%

Poland.Therealstateofrealestate|35

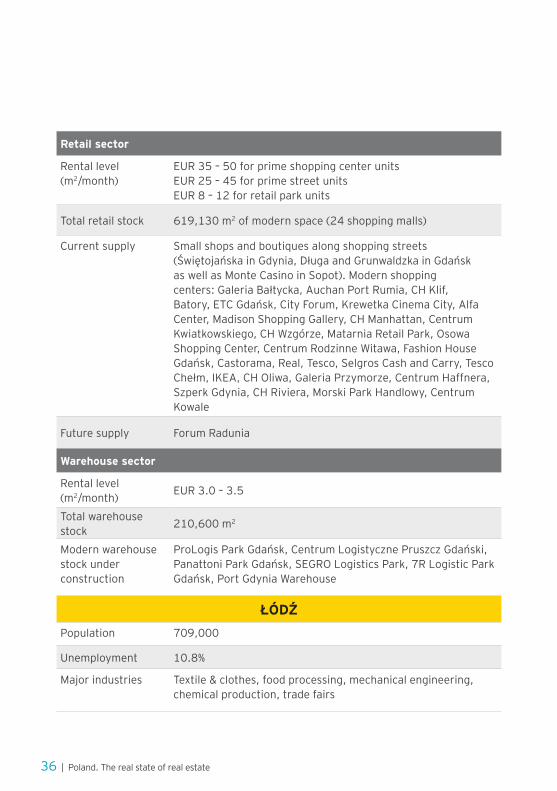

Retail sector

Rental level (m2/month)

EUR35–50forprimeshoppingcenterunits EUR25–45forprimestreetunits EUR8–12forretailparkunits

Totalretailstock 619,130m2ofmodernspace(24shoppingmalls)

Currentsupply Smallshopsandboutiquesalongshoppingstreets(ŚwiętojańskainGdynia,DługaandGrunwaldzkainGdańskaswellasMonteCasinoinSopot).Modernshoppingcenters:GaleriaBałtycka,AuchanPortRumia,CHKlif,Batory,ETCGdańsk,CityForum,KrewetkaCinemaCity,AlfaCenter,MadisonShoppingGallery,CHManhattan,CentrumKwiatkowskiego,CHWzgórze,MatarniaRetailPark,OsowaShoppingCenter,CentrumRodzinneWitawa,FashionHouseGdańsk,Castorama,Real,Tesco,SelgrosCashandCarry,TescoChełm,IKEA,CHOliwa,GaleriaPrzymorze,CentrumHaffnera,SzperkGdynia,CHRiviera,MorskiParkHandlowy,CentrumKowale

Futuresupply ForumRadunia

Warehouse sector

Rental level (m2/month) EUR3.0–3.5

Totalwarehousestock 210,600m2

Modernwarehousestockunderconstruction

ProLogisParkGdańsk,CentrumLogistycznePruszczGdański,PanattoniParkGdańsk,SEGROLogisticsPark,7RLogisticParkGdańsk,PortGdyniaWarehouse

ŁÓDŹPopulation 709,000

Unemployment 10.8%

Majorindustries Textile&clothes,foodprocessing,mechanicalengineering,chemicalproduction,tradefairs

36|Poland.Therealstateofrealestate

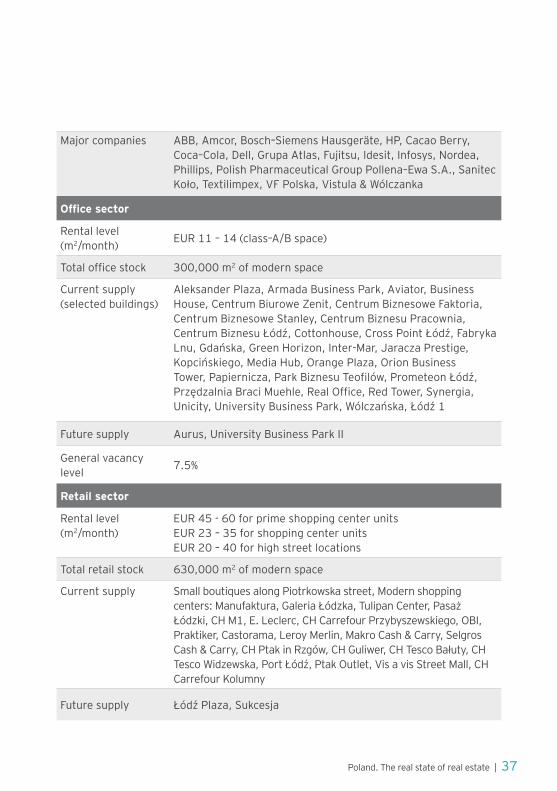

Majorcompanies ABB,Amcor,Bosch–SiemensHausgeräte,HP,CacaoBerry,Coca–Cola,Dell,GrupaAtlas,Fujitsu,Idesit,Infosys,Nordea,Phillips,PolishPharmaceuticalGroupPollena–EwaS.A.,SanitecKoło,Textilimpex,VFPolska,Vistula&Wólczanka

Office sector

Rental level (m2/month) EUR11–14(class–A/Bspace)

Totalofficestock 300,000m2ofmodernspace

Currentsupply(selectedbuildings)

AleksanderPlaza,ArmadaBusinessPark,Aviator,BusinessHouse,CentrumBiuroweZenit,CentrumBiznesoweFaktoria,CentrumBiznesoweStanley,CentrumBiznesuPracownia,CentrumBiznesuŁódź,Cottonhouse,CrossPointŁódź,FabrykaLnu,Gdańska,GreenHorizon,Inter-Mar,JaraczaPrestige,Kopcińskiego,MediaHub,OrangePlaza,OrionBusinessTower,Papiernicza,ParkBiznesuTeofilów,PrometeonŁódź,PrzędzalniaBraciMuehle,RealOffice,RedTower,Synergia,Unicity,UniversityBusinessPark,Wólczańska,Łódź1

Futuresupply Aurus,UniversityBusinessParkII

Generalvacancylevel 7.5%

Retail sector

Rental level (m2/month)

EUR45-60forprimeshoppingcenterunits EUR23–35forshoppingcenterunits EUR20–40forhighstreetlocations

Totalretailstock 630,000m2ofmodernspace

Currentsupply SmallboutiquesalongPiotrkowskastreet,Modernshoppingcenters:Manufaktura,GaleriaŁódzka,TulipanCenter,PasażŁódzki,CHM1,E.Leclerc,CHCarrefourPrzybyszewskiego,OBI,Praktiker,Castorama,LeroyMerlin,MakroCash&Carry,SelgrosCash&Carry,CHPtakinRzgów,CHGuliwer,CHTescoBałuty,CHTescoWidzewska,PortŁódź,PtakOutlet,VisavisStreetMall,CHCarrefourKolumny

Futuresupply ŁódźPlaza,Sukcesja

Poland.Therealstateofrealestate|37

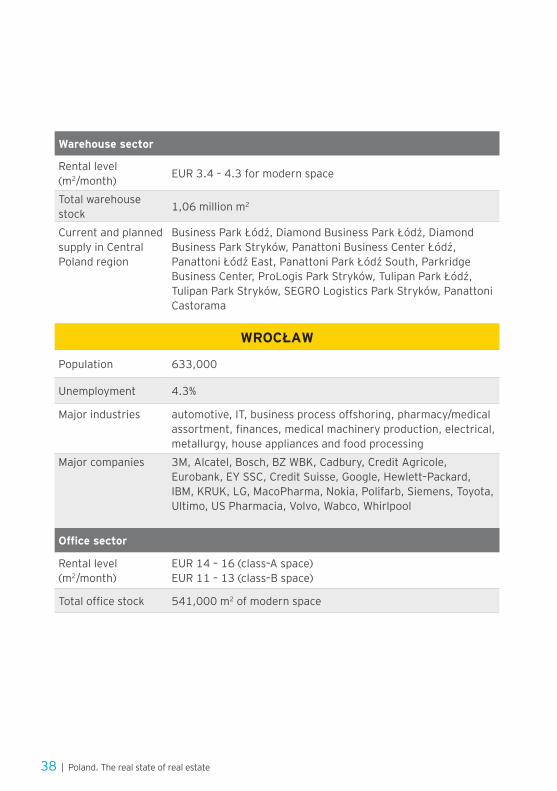

Warehouse sector

Rental level (m2/month) EUR3.4–4.3formodernspace

Totalwarehousestock 1,06millionm2

CurrentandplannedsupplyinCentralPolandregion

BusinessParkŁódź,DiamondBusinessParkŁódź,DiamondBusinessParkStryków,PanattoniBusinessCenterŁódź,PanattoniŁódźEast,PanattoniParkŁódźSouth,ParkridgeBusinessCenter,ProLogisParkStryków,TulipanParkŁódź,TulipanParkStryków,SEGROLogisticsParkStryków,PanattoniCastorama

WROCŁAW

Population 633,000

Unemployment 4.3%

Majorindustries automotive,IT,businessprocessoffshoring,pharmacy/medicalassortment,finances,medicalmachineryproduction,electrical,metallurgy,houseappliancesandfoodprocessing

Majorcompanies 3M,Alcatel,Bosch,BZWBK,Cadbury,CreditAgricole,Eurobank,EYSSC,CreditSuisse,Google,Hewlett–Packard,IBM,KRUK,LG,MacoPharma,Nokia,Polifarb,Siemens,Toyota,Ultimo,USPharmacia,Volvo,Wabco,Whirlpool

Office sector

Rental level (m2/month)

EUR14–16(class–Aspace) EUR11–13(class–Bspace)

Totalofficestock 541,000m2ofmodernspace

38|Poland.Therealstateofrealestate

Currentsupply(selectedbuildings)

AquariusBusinessHouse,ArkadyWrocławskie,AscoBusinessCentre,BemaPlaza,BetaCentre,CuprumNovum,DługoszaBusienssPark,FocusPlaza,GlobisWrocław,GreenTowers,GrunwaldzkiCenter,HeritageGates,HubskaOfficeCenter,LegnickaPark,MillenniumTower,NewPointOffices,Oniro,OławskaPrestige,PasażPkoyhof,Platon,PromenadyEpsilon,QuattroForum,RacławickaCenter,RenaissanceBusinessCentre,SilverForum,SilverTower,SkyTower,SzwedzkaCentrum,WratislaviaTower,WrocławskiParkBiznesu,WestHouse

Futuresupply BusinessGarden,Dominikański,Dubois41,GammaOffice,NorthOffice,Nobilis,WestGate

Generalvacancylevel

10.4%

Retail sector

Rental level (m2/month)

EUR65–75forprimeshoppingcenterunits EUR40–60forprimestreetunits EUR8–12forretailparkunits

Totalretailstock 670,000m2ofmodernspace

Currentsupply PasażGrunwaldzki,ArkadyWrocławskie,MagnoliaPark,FactoryOutlet,CHKorona,BielanyRetailPark(IKEA),AuchanRetailParkBielany,GaleriaDominikańska,SzewskaCenter,Kaufland,CHBorek,TGG,Tesco,E.Leclerc,IKEA,CHMarino,Renoma(aftermodernization,SkyTower,FerioGaj,RetailParkMłyn,FamilyPoint,RetailParkBielany

Futuresupply GaleriaIdylla

Warehouse sector

Rental level (m2/month) EUR2.9-3.5

Totalwarehousestock 895,000m2ofmodernspace

Poland.Therealstateofrealestate|39

Currentsupply ProLogisParkWrocław(I&II)–BielanyWrocławskie,ParkridgeBusinessCenter,TinerLogisticCenter–Pietrzykowice,PanattoniParkWrocław–BielanyWrocławskie,PrologisParkWrocławV,PanattoniBTSforLear,PanattoniforAmazon,GoodmanforAmazon

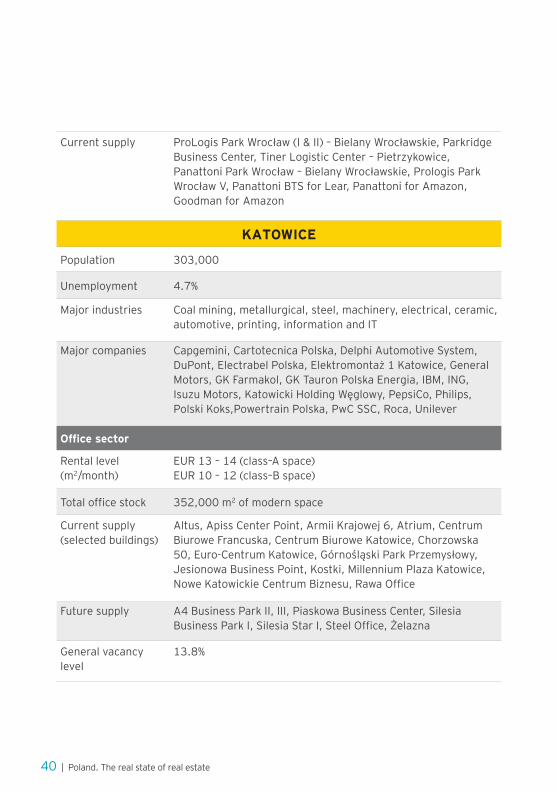

KATOWICE

Population 303,000

Unemployment 4.7%

Majorindustries Coalmining,metallurgical,steel,machinery,electrical,ceramic,automotive,printing,informationandIT

Majorcompanies Capgemini,CartotecnicaPolska,DelphiAutomotiveSystem,DuPont,ElectrabelPolska,Elektromontaż1Katowice,GeneralMotors,GKFarmakol,GKTauronPolskaEnergia,IBM,ING,IsuzuMotors,KatowickiHoldingWęglowy,PepsiCo,Philips,PolskiKoks,PowertrainPolska,PwCSSC,Roca,Unilever

Office sector

Rental level (m2/month)

EUR13–14(class–Aspace) EUR10–12(class–Bspace)

Totalofficestock 352,000m2ofmodernspace

Currentsupply(selectedbuildings)

Altus,ApissCenterPoint,ArmiiKrajowej6,Atrium,CentrumBiuroweFrancuska,CentrumBiuroweKatowice,Chorzowska50,Euro-CentrumKatowice,GórnośląskiParkPrzemysłowy,JesionowaBusinessPoint,Kostki,MillenniumPlazaKatowice,NoweKatowickieCentrumBiznesu,RawaOffice

Futuresupply A4BusinessParkII,III,PiaskowaBusinessCenter,SilesiaBusinessParkI,SilesiaStarI,SteelOffice,Żelazna

Generalvacancylevel

13.8%

40|Poland.Therealstateofrealestate

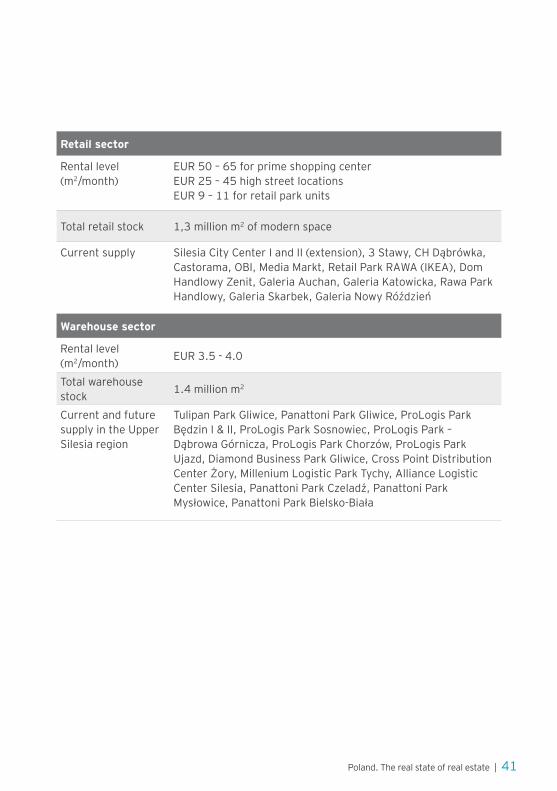

Retail sector

Rental level (m2/month)

EUR50–65forprimeshoppingcenter EUR25–45highstreetlocations EUR9–11forretailparkunits

Totalretailstock 1,3millionm2ofmodernspace

Currentsupply SilesiaCityCenterIandII(extension),3Stawy,CHDąbrówka,Castorama,OBI,MediaMarkt,RetailParkRAWA(IKEA),DomHandlowyZenit,GaleriaAuchan,GaleriaKatowicka,RawaParkHandlowy,GaleriaSkarbek,GaleriaNowyRóździeń

Warehouse sector

Rental level (m2/month) EUR3.5-4.0

Totalwarehousestock 1.4millionm2

CurrentandfuturesupplyintheUpperSilesiaregion

TulipanParkGliwice,PanattoniParkGliwice,ProLogisParkBędzinI&II,ProLogisParkSosnowiec,ProLogisPark–DąbrowaGórnicza,ProLogisParkChorzów,ProLogisParkUjazd,DiamondBusinessParkGliwice,CrossPointDistributionCenterŻory,MilleniumLogisticParkTychy,AllianceLogisticCenterSilesia,PanattoniParkCzeladź,PanattoniParkMysłowice,PanattoniParkBielsko-Biała

Poland.Therealstateofrealestate|41

Legal and tax aspects of investing in real estate

2

42|Poland.Therealstateofrealestate

ThisChapterconsidersthemostimportantlegalandtaxissuesarisingduringeachofthefollowingfivestagesofarealestateinvestment:

• Financing

• Acquisition

• Developmentandconstruction

• Operationandexploitation

• Sale

TheChapterisarrangedsothateachoftheaboveaspectsisdealtwithinaseparatesection(2.3.–2.8.),consideringlegalimplicationsfirst,followedbyanassessmentofrelatedimportanttaxconsequences.

Thesection2.1.onthelegalbackground(below)willintroducethereadertocertainconceptsandtermsthatmaynotbecommonplaceintransactionselsewhereinEurope.ThisshouldbereadasageneralintroductiontothelegalenvironmentinPoland.Thechapteralsocontainssection2.2.oninvestmentvehiclesandstructurespresentinginformationonthemostcommonstructuresusedinrealestateinvestmentsinPoland.Takentogether,theyformthebasisforunderstandingthemostrelevantlegalandtaximplicationsofinvestinginrealestate in Poland.

Legal,financialandtaxduediligencearealsofundamentaltoanyinvestmentcycleandgiventheimportanceofduediligencetoanytransaction,wediscusstherelevantproceduresandkeyconsiderationsindetailinsection2.9.

Poland.Therealstateofrealestate|43

Ingeneral,Polishrealestatelawprovidesquiteclearandstableruleswhichallowpotentialinvestorstomakewell-foundeddecisionsaboutenteringintorealestatetransactions.Additionally,therearemeasuresandinstitutionswhichenableinvestorstosafelyconcludetransactionsadaptedtotheirneedsandexpectations.Inparticular,mostrealpropertydeeds(sale,othertransfers,establishingofamortgage)mustbeexecutedbeforeanotarypublic.Apubliccredibilitywarrantyofthelandandmortgageregisterisanadditionalinstrumentwhichprotectsthepurchaseragainstthirdpartyclaimsandguaranteesthevalidityofthetitleacquired(aslongasthepurchaseractedingoodfaith).

BelowwepresentsomekeyinformationonrealestatelawinPolandwhichshouldbethebaseforothercommentsinthischapter.

2.1.2. Legaltitlestorealestate

ThebasicsourceofrealpropertylawinPolandistheCivilCodeof23April1964(withmanyamendmentssince;hereinafterreferredtoastheCivilCode).Althoughitdoesnotregulatethisbranchoflawexhaustively,itconstitutesabasisforotherregulationsregardinglegaltitlestorealestateandtheirlimitationsormodifications.

ThemostcommonlegaltitlestorealestateinPolandaretheownershipright,theperpetualusufructright,andobligationrights,suchaslease,tenancyorleasing.Polishlawalsoprovidesseverallimitedpropertyrightssuchaseasementsandusufruct.

2.1.Legalbackground

2.1.1. Generalremarks

44|Poland.Therealstateofrealestate

Ownership right

Ownership(prawowłasności)isthebroadestrighttorealestateinPoland,equivalenttoafreehold.Asarule,ownershipconveystherighttopossessanduserealestateforanunlimitedperiodoftime(withtheexceptionofownershipofanybuildingsconnectedwiththeperpetualusufructright;seeourcommentsbelow)andtransferorencumbertherealestate.Theownershiprightmaybelimitedbystatutorylaw,principlesofcommunitylifeandthesocioeconomicpurposeoftheright.Themostcommonlimitationsresultfromconstructionlawandzoningmasterplansadoptedbylocalauthorities(municipalities).

Right of perpetual usufruct

Perpetualusufruct(użytkowaniewieczyste)isarightofusetherealestatewhichmaybegrantedbytheStateinrelationtotheState-ownedlandorbyalocalauthorityinrelationtotheauthority-ownedland.Ineithercasetherespectiveentity(theStateorthelocalauthority)remainstheowneroftheland.

Theperpetualusufructrightissimilartotheownership,however,thereareseveralcrucialdifferences:

• Theperpetualusufructrightiscreatedforadefinedpurpose(developingaprojectorconductingaspecificactivity)setoutinthecontract.Iftheperpetualusufructuaryisinbreachoftheseprovisions,thismayleadtoanincreaseintheannualfeesoreventermination

ofthecontractbythecommoncourt.

• Theperpetualusufructrightiscreatedforaspecificterm,inprincipleforaperiodof99years.

However,whentheeconomicpurposeoftheperpetualusufructofpropertydoesnotrequirelettingthelandforalongerperiod,ashorterperiodofnolessthan40yearsisallowed.Theholderoftherightmayapplyforextendingthetermoftheperpetualusufructforafurtherperiodof40to99yearsfollowingthelapseoftheinitialperiod.Refusaltoprolongthetimelimitisadmissibleonlyonaccountofimportantsocialinterest.

Oncecreated,theperpetualusufructrightcanbeinherited,transferredtothirdpartiesorencumbered(i.e.mortgage,easements).Theholderoftheperpetualusufructrightenjoystherighttousetherealpropertyandtodrawbenefitsfromit,e.g.rentalincome.

Currently,theperpetualusufructrightmaybecreatedbycontract,whichgenerallyrequiresputtingthelandupforatender(thereareseveralexceptionsprovided).Thewinningbiddersignsanotarialdeedwiththeowneroftherealestateestablishingtherightofperpetualusufruct.Theright,however,doesnotcomeintoexistenceuntilitisregisteredinthelandandmortgageregister.Otherissuesinvolvingtheestablishmentandtransferoftheperpetualusufructareaccordinglygovernedbytheregulationsregardingthetransferofownershipofrealestate.

Thecontractunderwhichthelandistransferredforperpetualusufructmay

Poland.Therealstateofrealestate|45

laydownpotentiallimitationsontheuseanddisposalofrealpropertyandindicatethemannerinwhichtherealestateistobe used.

Iftherealestatetransferredforperpetualusufructisapieceofdevelopedland,thebuildingsandotherconstructionserectedthereonaresoldtotheperpetualusufructuaryinadditiontotheestablishmentoftheperpetualusufructright.Ifthebuildingsareerectedaftertheperpetualusufructrightisestablished,theyalsobecometheperpetualusufructuary’sproperty.Separateownershipofthebuildingsduetotheperpetualusufructuaryisarightstrictlyconnectedwiththerightofperpetualusufructand,inconsequence,thebuildingssharethelegal“lot”oftheland.Inparticular,theownershipofbuildingsmaybetransferredonlywiththerightofperpetualusufruct.Oncetheperpetualusufructrightexpires,theholderoftherightisentitledtoareimbursementcorrespondingtothecurrentmarketvalueofthebuildingsandotherimprovementslegallyimplementedonthelandthatisthesubjectoftheperpetualusufructright.

Theperpetualusufructuaryisobligedtopaytotheowneraone-offinitialfeewhichamountsfrom15%to25%ofthetotalmarketvalueoftherealpropertyandthenanannualfeeofupto3%ofthetotalmarketvalueoftheland.Therateof3%isthebasicrateprovidedbythelaw;however,therecanbeotherrates(0.3%,1%,2%)appliedtotherealestateassignedforspecificpurposes,strictly

listedinthelegalprovisions.Thevalueofthelandasestablishedforthepurposeofcalculatingtheannualfeeissubjecttoindexation(notmorethanonceforthreeyears).Theperpetualusufructuaryhastherighttoquestionanewvaluationbeforethelocalappealcommitteeand,ifunsuccessful,beforeacommoncourt.

Subjecttocertainconditions,theperpetualusufructuaryorhislegalsuccessorsmaydemandthattheperpetualusufructrightbeconvertedintoownership.Thelegalprovisionsdonotspecifywhethertheterm“legalsuccessor”referstogeneralsuccessiononly,orwhetheritmaybeapplicabletoentitiesacquiringrealpropertythroughasaleagreement.Thecourtsmoreoftentaketheviewthattheentitiesacquiringrealpropertythroughasaleagreementareentitledtodemandtheconversionintoownership.Thebasicconditionofacquiringtheownershipofrealestateisthepossessionoftherightofperpetualusufructasof13October2005.Theconversiontakesplaceunderanadministrativedecisionofarelevantlocalauthorityandisvalidasatthedatewhenthedecisionbecomesfinal.Suchadecisionalsoconstitutesabasisformakinganentryinthelandandmortgageregister.

Theconversionoftheperpetualusufructrightintoownershiprightissubjecttoafeewhichisequaltothedifferencebetweenthevalueofownershipandthevalueoftheperpetualusufructrighttothe land.

46|Poland.Therealstateofrealestate

Leases and Tenancies

Polishlawdistinguishesbetweentwotypesofleases:lease(najem)andtenancy(dzierżawa).Leasesareusedmainlyforcommercialandresidentialpremises.Tenanciesareusedespeciallyforindustrialandagriculturalproperty.Underaleaseagreement,thelessorundertakestohandovertherealpropertyforthelessee’suseforafixedornon-fixedterm,andthelesseeundertakestopaythelessoranagreedrent.Thetenancycontract,however,providesforthelesseeadditionalrighttocollectprofitsfromtherealestate.

Leasing

Byaleasingcontract,thefinancingparty,whoisanentrepreneur,undertakestoacquiretherealestatefromaspecifiedtransferoronthetermsandconditionssetforthinthatcontractandtogiveitovertotheuserforuseorforuseandcollectionofprofitsforaspecifiedperiod.Theuser,however,undertakestopaythefinancingparty,byinstallments,amonetaryremunerationequaltoatleasttheremunerationorthepriceatwhichthefinancingpartyacquiredtherealestate.

TherearetwotypesofleasingthatcanbeexecutedinPoland:

• operatingleasing,inwhichcasetheleaseholdisanassetofthelessorwhomakesdepreciationwrite-offsandthelesseehasanoptiontopurchasethepropertyattheendoftheleasingterm;

• financialleasing,inwhichcasetheleaseholdisanassetofthelesseewhomakesdepreciationwrite-offsandthe

transferoftheownershipofarealestateattheendoftheleasingtermmaybestipulateddirectlyintheleasingagreement.

Thelesseeshouldchoosethetypeofleasingaccordingtohisrequirementsandneedswithrespecttotaxsettlementsandtheperiodofusingtheleasehold.

Easements

Easements(służebności)overlandarelimitedpropertyrightswhichmaybegrantedoverapieceofrealestate(encumberedproperty)forthebenefitofanotherpieceofrealestate(masterproperty).Dependingonthecontentofaneasementdeed,theholderofthemasterpropertymaybeentitledtoalimiteduseoftheencumberedproperty(activeeasement),ortheholderoftheencumberedpropertymayberestrictedintheexerciseofhisownrightsforthebenefitofthemasterproperty(passiveeasement).

Polishlawdistinguishesbetweentwotypesofeasements:

• groundeasements,whichareestablishedforthebenefitoftheownerorperpetualusufructuaryofthelandandaretransferredtogetherwiththeproperty(whetherthatencumberedorthemasterproperty);

• personaleasements,whichareestablishedforthebenefitofanaturalpersonandarenon-transferrable(norcantherighttoexercisethembetransferred).

TheCivilCodealsolistsaseparatecategoryofeasement,i.e.utilityeasementwhich

Poland.Therealstateofrealestate|47

maybeestablishedforthebenefitofentrepreneursbeingutilityproviders.Autilityprovidermayaskthelandownertoestablishaneasementoverhislandinordertoinstall(andthenoperateandmaintain)e.g.electricitycables,installationsservingtosupplyandtochannelliquids,gas,steamorotherfacilities.Iftherealestateownerrefuses,theutilityprovidermaydemandthataneasementbeestablishedinreturnforanappropriateremuneration.

Inpractice,realestatemaybeencumberedwithmorethanoneeasementorotherlimitedpropertyright.Insuchacase,asarule,arightthataroselatercannotbeexercisedtothedetrimentoftheearlierright;however,therearealsoregulationswhichspecifypriorityinadifferentmanner.